Embed Size (px)

Citation preview

A Visual Tour of Colorado’s

Regional Economies

BOOT CAMP SESSION Wednesday, October 5, 2016

Presented by

Today’s Panelists Elizabeth Garner

State Demographer

Colorado Department of Local Affairs, State Demography Office

James Conner Economic and Market Analysis Division Field Director

HUD Region VIII – Rocky Mountain Region

Ryan McMaken Editor, Mises Wire and The Austrian

The Mises Institute

Today’s Moderator

Alison O’Kelly CDBG-DR and NSP Programs Manager

Colorado Department of Local Affairs, Division of Housing

Workshop Overview

Colorado is maturing economically and

demographically.

With desirable living/working conditions, the

Front Range has landed at the top of many

lists for net migrants within the US.

Demographic factors are pushing Colorado

into a “demographic transition” – are we

ready for how global and national trends may

affect Colorado’s economies?

Learning Objectives Learning Objective #1

Current population, household, and economic estimates

and forecasts for the state/region and the key trends

impacting the State.

Learning Objective #2

Data and trends on housing vacancy rates, foreclosures,

home sales, rents, household formation, housing permits,

and employment.

Learning Objective #3

IMAGE: Incomes, Migration, Age, Growth and

Ethnicity/race and their related factors pushing Colorado

into a “demographic transition.”

Agenda

Panelist Presentations • Feel free to raise your hand and ask questions

during the presentations

• Panelists may answer later in presentation, or

• We may add issues to “Parking Lot” to discuss or

answer during discussion sessions later in the

workshop

Panelist Discussion

Audience Discussion and Q&A

Elizabeth Garner

State Demography Office

Colorado Department of Local Affairs

October 2016

Demography.dola.colorado.gov

Growing Forward

Population and Economic

Transitions for Colorado

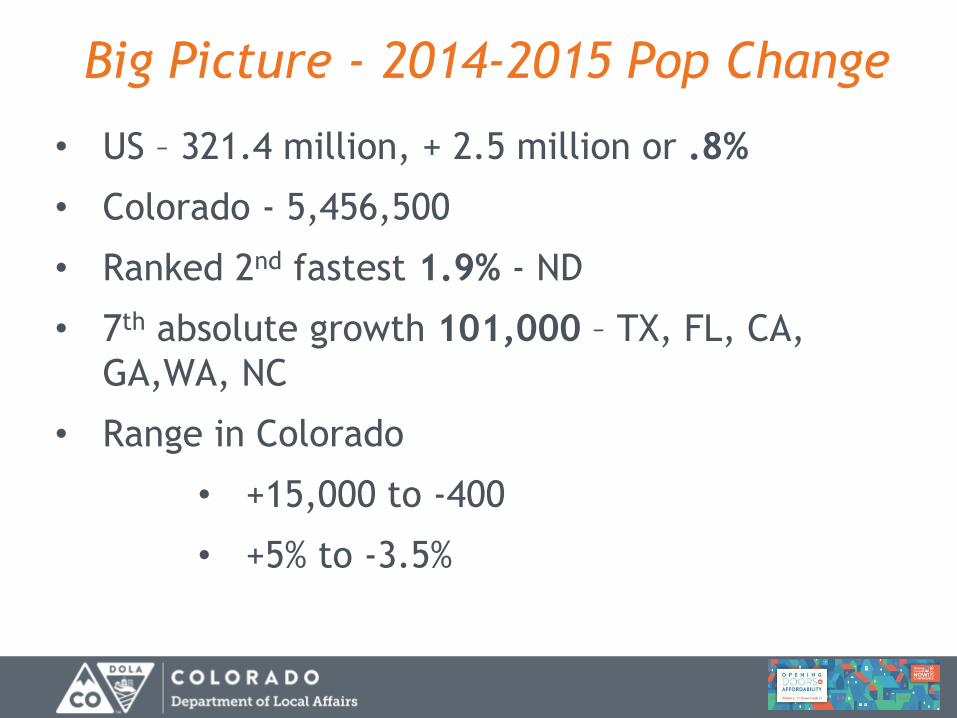

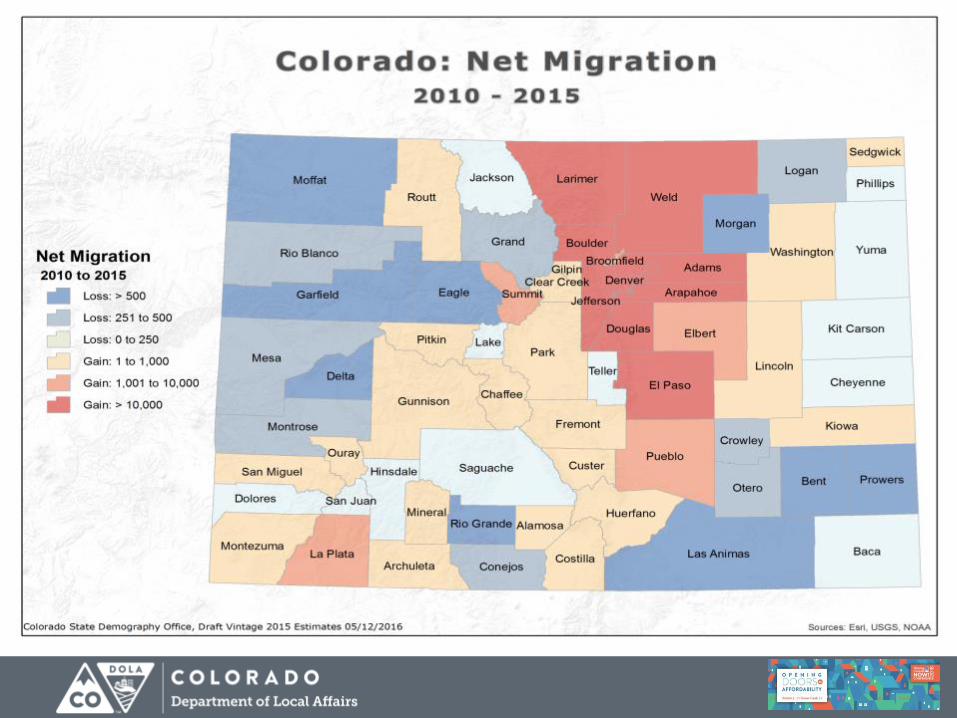

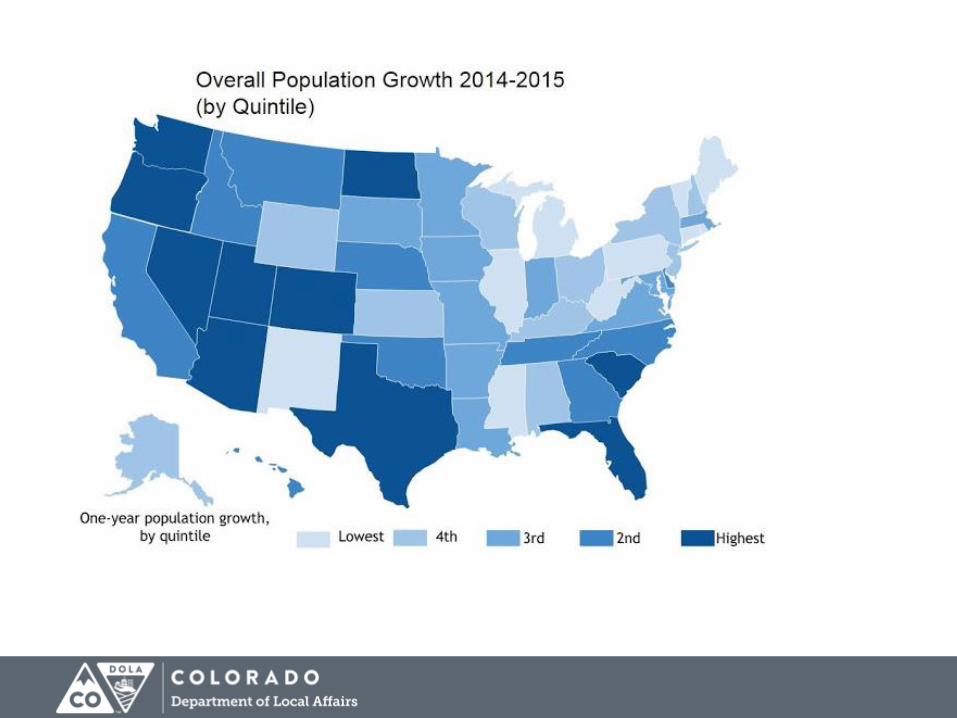

Big Picture - 2014-2015 Pop Change

• US – 321.4 million, + 2.5 million or .8%

• Colorado - 5,456,500

• Ranked 2nd fastest 1.9% - ND

• 7th absolute growth 101,000 – TX, FL, CA,

GA,WA, NC

• Range in Colorado

• +15,000 to -400

• +5% to -3.5%

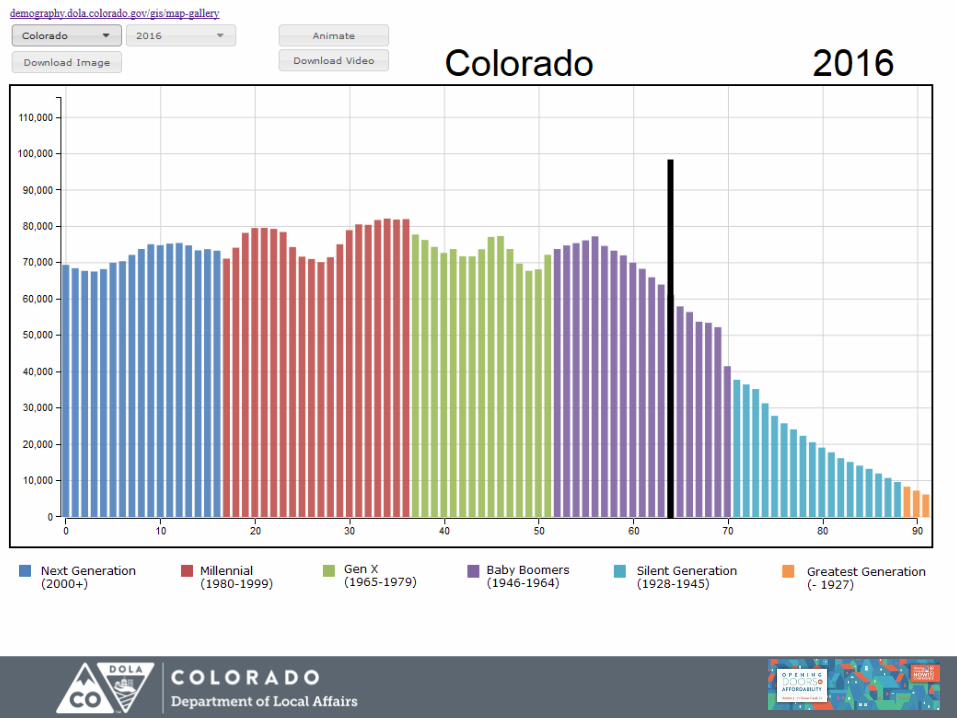

Age

State Demography Office v2014

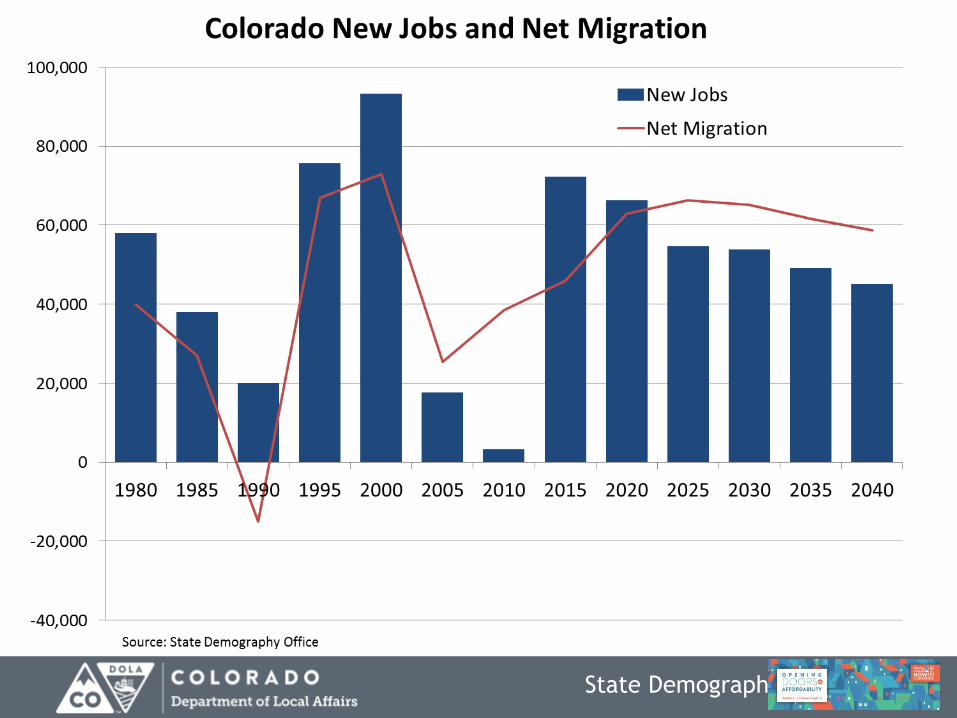

Forecast

2010-40

State 2.8M

Front Range 2.4M

Denver Metro 1.5 M

North Front Range 500K

South Front Range 400K

Rest of State 400K

AGE

Age Summary

• Fastest growth in households in the 65+ (2.5 as

fast as the Millennials)

• 1991 peak year born for Millennials. Currently

25 years old.

• 43% of 25-34 year olds are home-owners.

• 25-29 year olds move on average every 2.5

years.

• Millennials 25-34 have a lower Real median

household income compared to Boomers and

Xers at the same age.

Income

Household Income….its future is

demographically challenged

• Age distributions – End of “demographic

dividend”. Slow growth in the 45-64 year olds.

• Occupational Mix – high and low service

• More race/ethnicity diverse especially at young

end but achievement gap is growing as well –

impacts income

• Household type and size – single and smaller

• Youth un- and under employment - Long term

permanent impacts on earnings

State Demography Office

To Ponder in State • Disparate Growth and Migration – how much,

where, and can we compete for the best and the

brightest?

• Aging – we are getting old fast, is the state ready for

the changes to the labor force, income, industrial mix,

housing, etc.

• Income Challenges – how could downward pressure

impact our state?

• Housing –Right amount, right place, right price, right

type.

Thank you

State Demography Office

Department of Local Affairs

Elizabeth Garner

303-864-7750

Demography.dola.colorado.gov

October 2016

James Conner

EMAD Field Director

HUD Region VIII – Rocky Mountain Region

Economic and Market Analysis Division

(EMAD) Overview

Regional Economic and

Housing Market Conditions

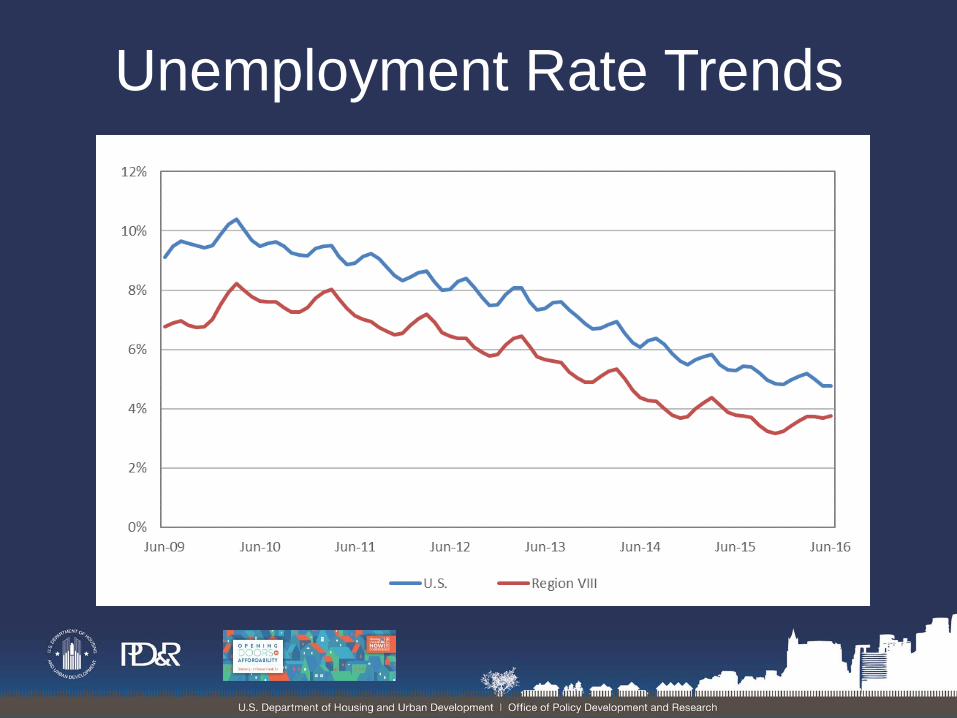

• The region’s economy continued to grow in second

quarter 2016, but at a slower pace than previously.

• The rate of nonfarm payroll growth in the Rocky

Mountain region now lags that of the nation.

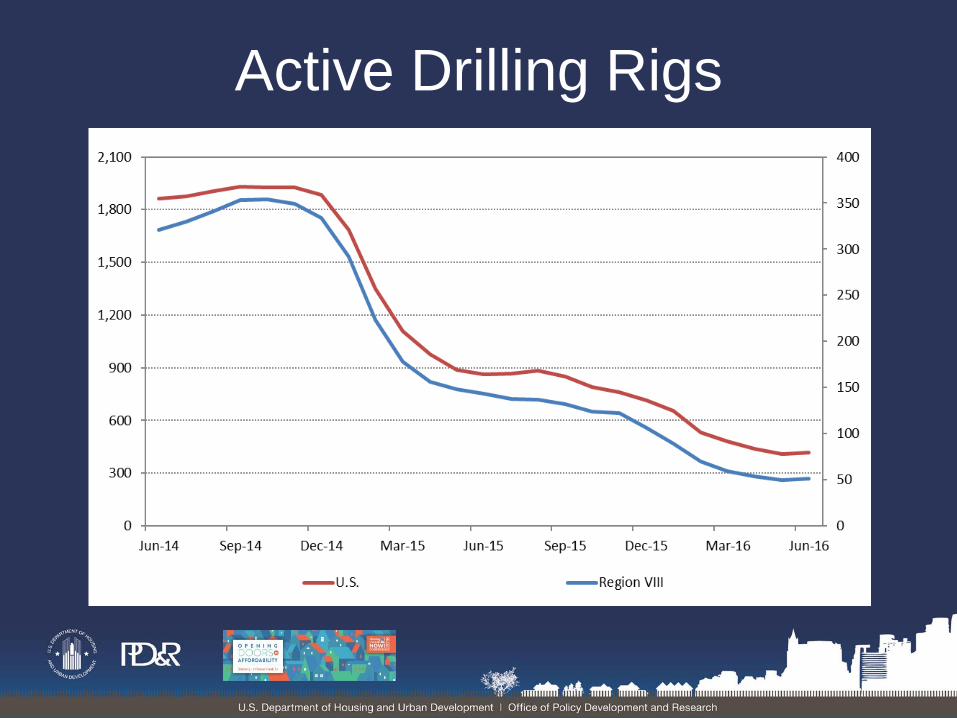

• Declines in the energy industry were offset by

growth in the tourism, healthcare, and construction

industries.

• Job losses in energy producing areas were offset

by strong job growth in Colorado and Utah.

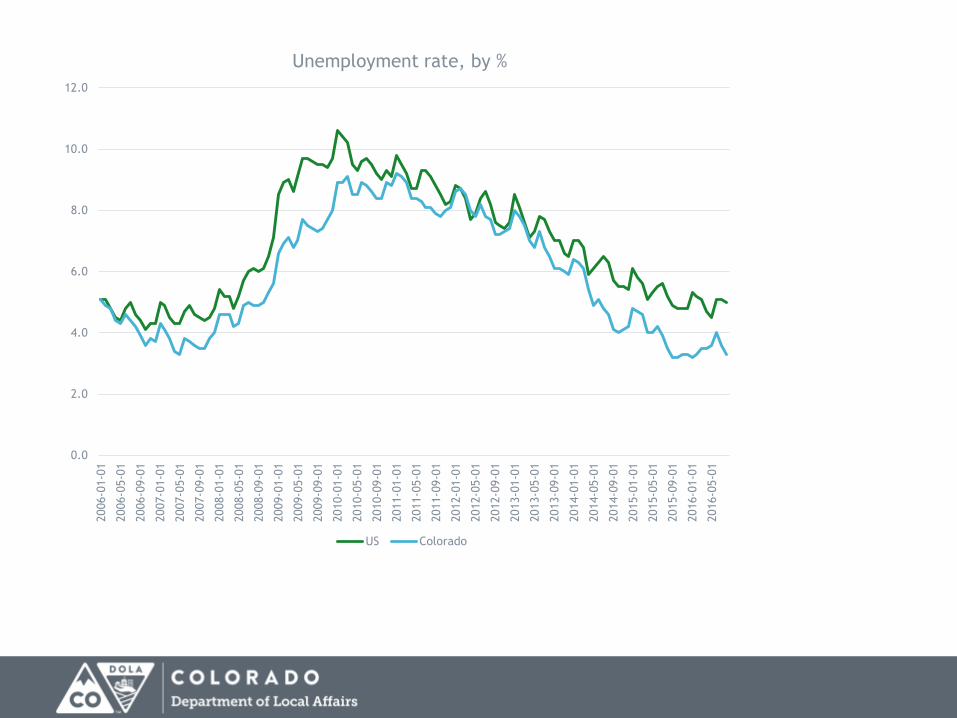

Economic Conditions:

Nonfarm Payroll Growth

Payroll Changes by Sector

Active Drilling Rigs

Unemployment Rate Trends

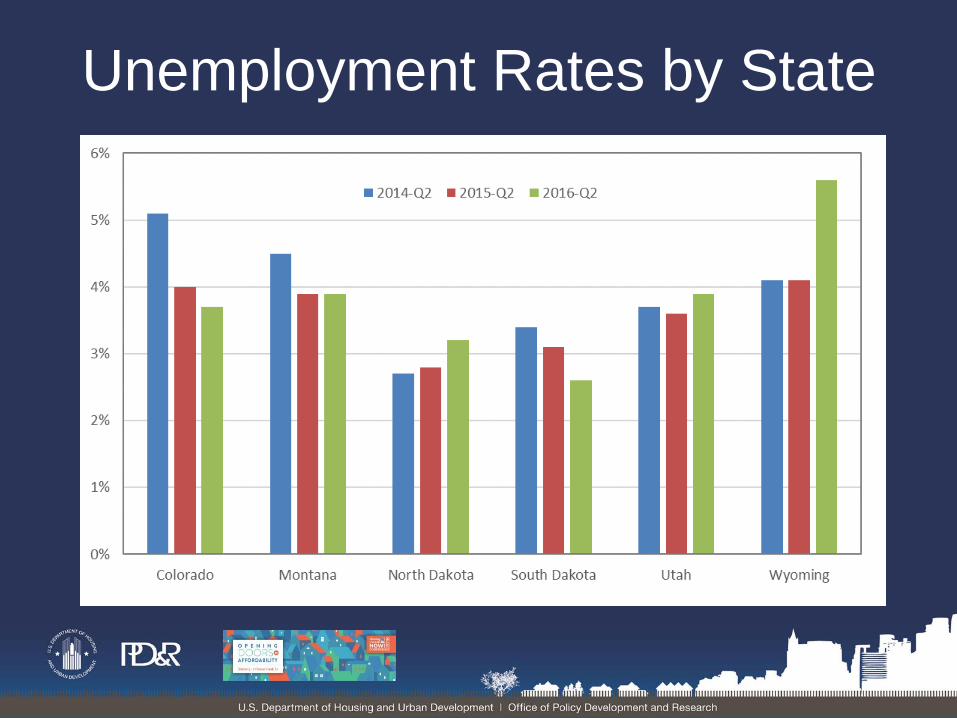

Unemployment Rates by State

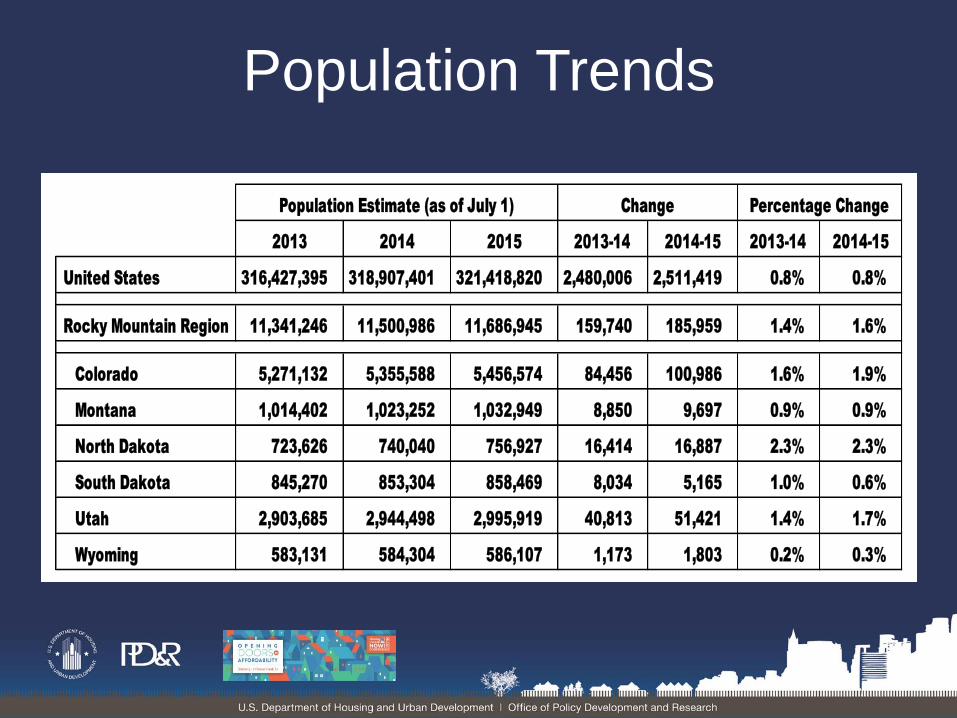

• The population in the region grew at double the

national rate from July 2014 to July 2015.

• Net in-migration to the region was relatively strong,

particularly in Colorado.

• In Utah, strong population growth was driven by

net natural increase (births minus deaths).

• Population growth was comparatively slower in

Montana, South Dakota, and Wyoming.

Population Trends:

Population Trends

2013 2014 2015 2013-14 2014-15 2013-14 2014-15

United States 316,427,395 318,907,401 321,418,820 2,480,006 2,511,419 0.8% 0.8%

Rocky Mountain Region 11,341,246 11,500,986 11,686,945 159,740 185,959 1.4% 1.6%

Colorado 5,271,132 5,355,588 5,456,574 84,456 100,986 1.6% 1.9%

Montana 1,014,402 1,023,252 1,032,949 8,850 9,697 0.9% 0.9%

North Dakota 723,626 740,040 756,927 16,414 16,887 2.3% 2.3%

South Dakota 845,270 853,304 858,469 8,034 5,165 1.0% 0.6%

Utah 2,903,685 2,944,498 2,995,919 40,813 51,421 1.4% 1.7%

Wyoming 583,131 584,304 586,107 1,173 1,803 0.2% 0.3%

Population Estimate (as of July 1) Change Percentage Change

• Home sales demand remains strong.

• Sales market conditions are tight or slightly tight in

much of the region.

• Supply of for-sale home listings very low in many

metropolitan areas.

• Year-over-year home price increases as high as

10% in some metropolitan areas in the region.

Home Sales Market:

Home Sales Market Conditions

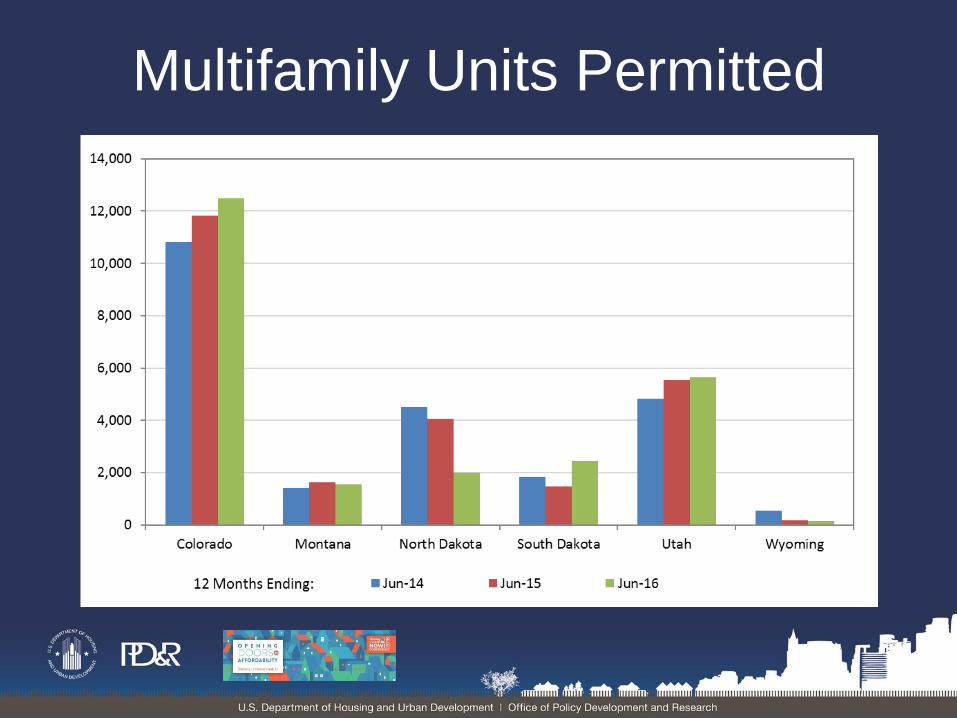

Single-Family Homes Permitted

• Population growth continues to support demand.

• Development activity has been very strong during

the past 1-2 years in many parts of the region.

• Markets that were previously tight have eased in

many of the major metropolitan areas.

• Pipeline of development activity remains strong in

areas such as Colorado and Utah.

Apartment Market:

Apartment Market Conditions

Multifamily Units Permitted

EMAD Resources at HUD User www.huduser.gov

U.S. Housing Market Conditions—Regional Narratives Quarterly updates on housing markets in each of the ten HUD regions

http://www.huduser.gov/portal/ushmc/home.html#regional_map

Comprehensive Housing Market Analysis Reports Detailed reports with historic trends and forecasts (metropolitan areas)

http://www.huduser.gov/portal/ushmc/chma_archive.html

U.S. Housing Market Conditions—Housing Market Profiles Summarizing recent trends and current conditions (metropolitan areas)

Http://www.huduser.gov/portal/ushmc/profile_archive.html

Market At A Glance (MAAG) Reports Regional, state, county, and metro-level data on economy, population, and housing

http://www.huduser.gov/portal/ushmc/mag.html

EMAD Region VIII

Contact Information

James Conner – Field Director

Sam Young – Field Economist

Katharine Auchter – Field Economist

0.0

2.0

4.0

6.0

8.0

10.0

12.02006-0

1-0

1

2006-0

5-0

1

2006-0

9-0

1

2007-0

1-0

1

2007-0

5-0

1

2007-0

9-0

1

2008-0

1-0

1

2008-0

5-0

1

2008-0

9-0

1

2009-0

1-0

1

2009-0

5-0

1

2009-0

9-0

1

2010-0

1-0

1

2010-0

5-0

1

2010-0

9-0

1

2011-0

1-0

1

2011-0

5-0

1

2011-0

9-0

1

2012-0

1-0

1

2012-0

5-0

1

2012-0

9-0

1

2013-0

1-0

1

2013-0

5-0

1

2013-0

9-0

1

2014-0

1-0

1

2014-0

5-0

1

2014-0

9-0

1

2015-0

1-0

1

2015-0

5-0

1

2015-0

9-0

1

2016-0

1-0

1

2016-0

5-0

1

Unemployment rate, by %

US Colorado

5.3 5 4.9

3.9

3.5 3.3 3.2

2.9

0

1

2

3

4

5

6

Unemployment Rate, by %, August 2016

2.26

2.16

1.76

1.88 1.83

1.50

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

2006-0

1-0

1

2006-0

6-0

1

2006-1

1-0

1

2007-0

4-0

1

2007-0

9-0

1

2008-0

2-0

1

2008-0

7-0

1

2008-1

2-0

1

2009-0

5-0

1

2009-1

0-0

1

2010-0

3-0

1

2010-0

8-0

1

2011-0

1-0

1

2011-0

6-0

1

2011-1

1-0

1

2012-0

4-0

1

2012-0

9-0

1

2013-0

2-0

1

2013-0

7-0

1

2013-1

2-0

1

2014-0

5-0

1

2014-1

0-0

1

2015-0

3-0

1

2015-0

8-0

1

2016-0

1-0

1

2016-0

6-0

1

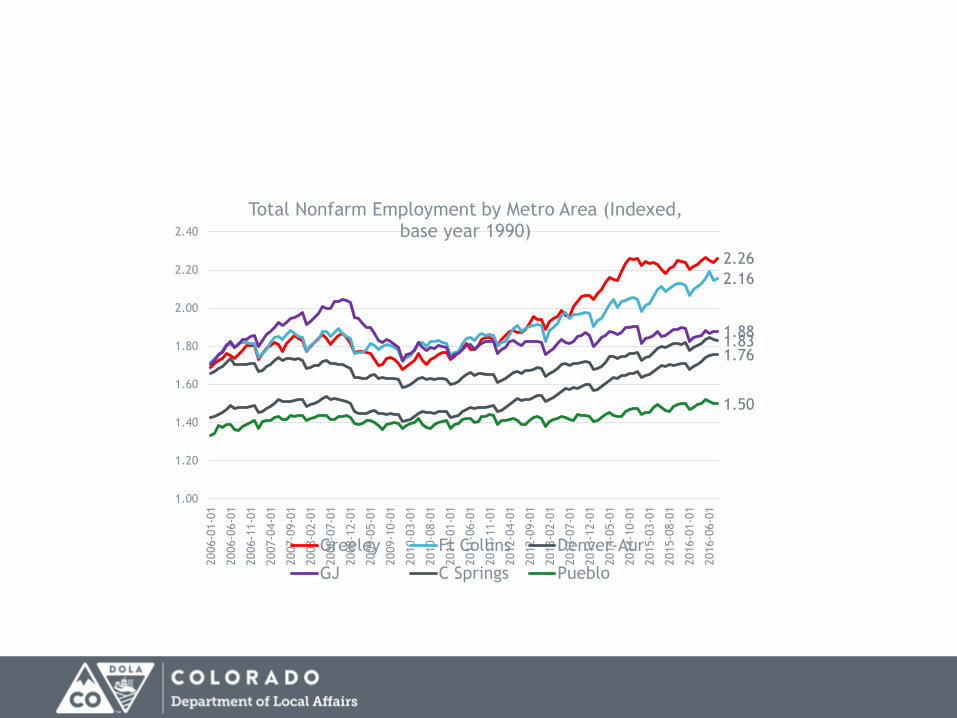

Total Nonfarm Employment by Metro Area (Indexed, base year 1990)

Greeley Ft Collins Denver-Aur

GJ C Springs Pueblo

12,468

1,872

7,117

883

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2007q1

2007q2

200

7q

3

2007q4

2008q1

2008q2

2008q3

2008q4

2009q1

200

9q

2

2009q3

2009q4

2010q1

2010q2

2010q3

2010q4

2011q1

2011q2

2011q3

2011q4

2012q1

2012q2

2012q3

2012q4

2013q1

2013q2

2013q3

201

3q

4

2014q1

2014q2

2014q3

2014q4

2015q1

2015q2

2015q3

2015q4

2016q1

2016q2

Quarterly Foreclosure Totals in Colorado

Filings Sales

46,394

4,151

25,054

1,744

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016(YTD)

Annual Foreclosure Totals

Filings

Sales

0

2000

4000

6000

8000

10000

12000

14000

1stQ 2ndQ 3rdQ 4thQ

Foreclosure Filings by Quarter

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

10,264

8,874

7,603 7,576

5,473

4,097

2,945 2,525

1,264 703 611

0

2,000

4,000

6,000

8,000

10,000

12,000

Number of Households Per Foreclosure Sale, 2nd Q 2016

0

10000

20000

30000

40000

50000

60000

70000

80000

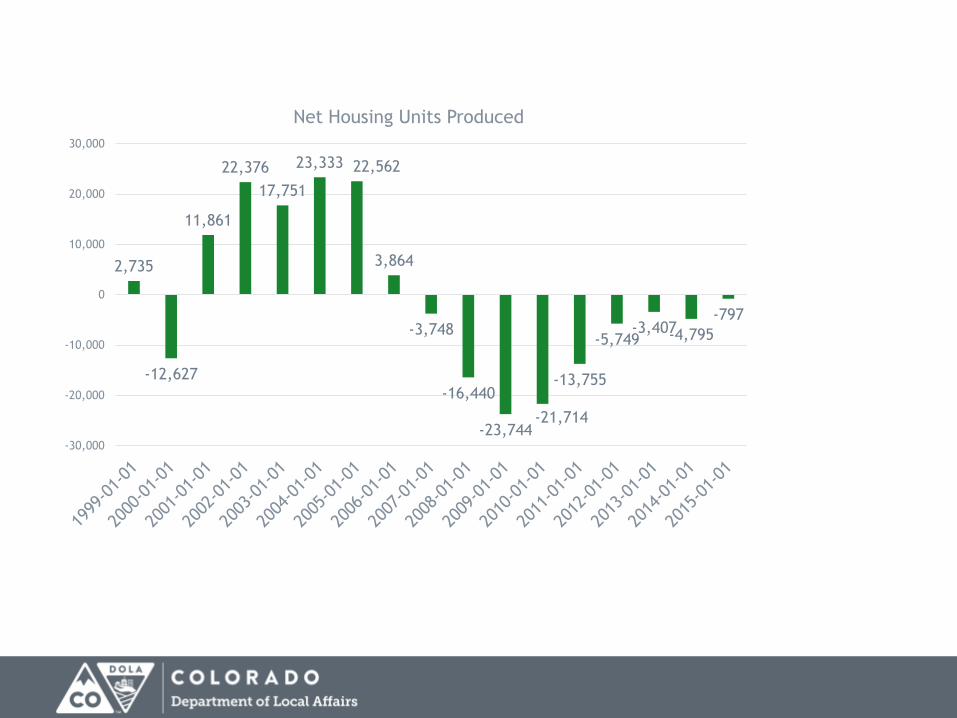

Housing Units vs. Households

New Households Total Housing Units

2,735

-12,627

11,861

22,376

17,751

23,333 22,562

3,864

-3,748

-16,440

-23,744 -21,714

-13,755

-5,749 -3,407 -4,795

-797

-30,000

-20,000

-10,000

0

10,000

20,000

30,000

Net Housing Units Produced

0

2

4

6

8

10

12

14

90

q1

91

q1

92

q1

93

q1

94

q1

95

q1

96

q1

97

q1

98

q1

99

q1

00

q1

01

q1

02

q1

03

q1

04

q1

05

q1

06

q1

07

q1

08

q1

09

q1

10

q1

11

q1

12

q1

13

q1

14

q1

15

q1

16

q1

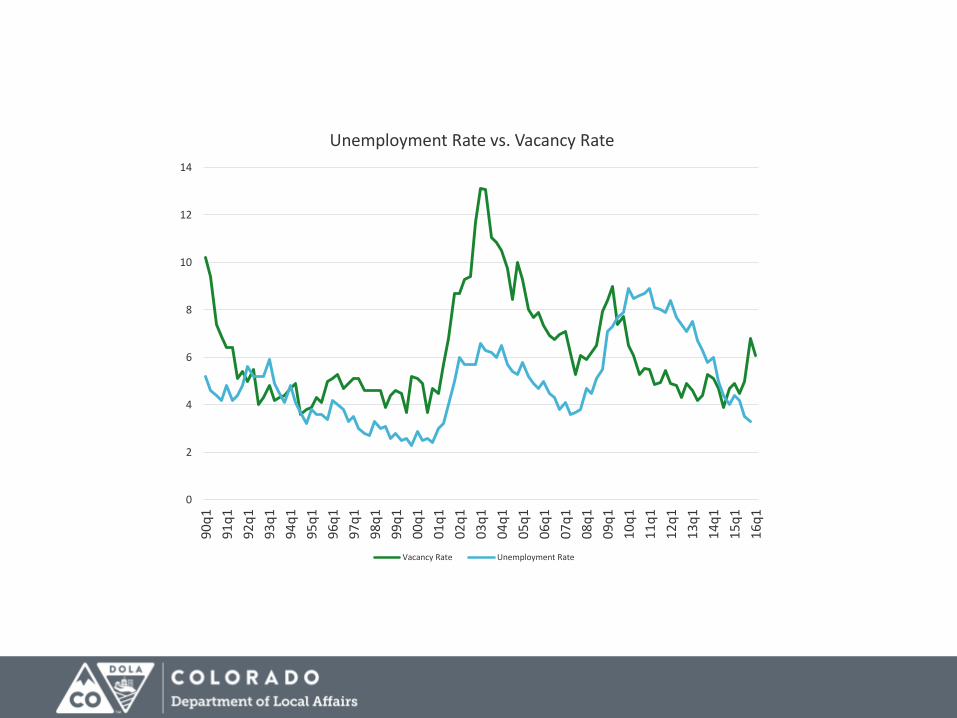

Unemployment Rate vs. Vacancy Rate

Vacancy Rate Unemployment Rate

0

200

400

600

800

1000

1200

1400

1600

81

q3

82

q1

82

q3

83

q1

83

q3

84

q1

84

q3

85

q1

85

q3

86

q1

86

q3

87

q1

87

q3

88

q1

88

q3

89

q1

89

q3

90

q1

90

q3

91

q1

91

q3

92

q1

92

q3

93

q1

93

q3

94

q1

94

q3

95

q1

95

q3

96

q1

96

q3

97

q1

97

q3

98

q1

98

q3

99

q1

99

q3

00

q1

00

q3

01

q1

01

q3

02

q1

02

q3

03

q1

03

q3

04

q1

04

q3

05

q1

05

q3

06

q1

06

q3

07

q1

07

q3

08

q1

08

q3

09

q1

09

q3

10

q1

10

q3

11

q1

11

q3

12

q1

12

q3

13

q1

13

q3

14

q1

14

q3

15

q1

15

q3

16

q1

Average Rent in Metro Denver

0

200

400

600

800

1000

1200

1400

16008

1q

3

82

q3

83

q3

84

q3

85

q3

86

q3

87

q3

88

q3

89

q3

90

q3

91

q3

92

q3

93

q3

94

q3

95

q3

96

q3

97

q3

98

q3

99

q3

00

q3

01

q3

02

q3

03

q3

04

q3

05

q3

06

q3

07

q3

08

q3

09

q3

10

q3

11

q3

12

q3

13

q3

14

q3

15

q3

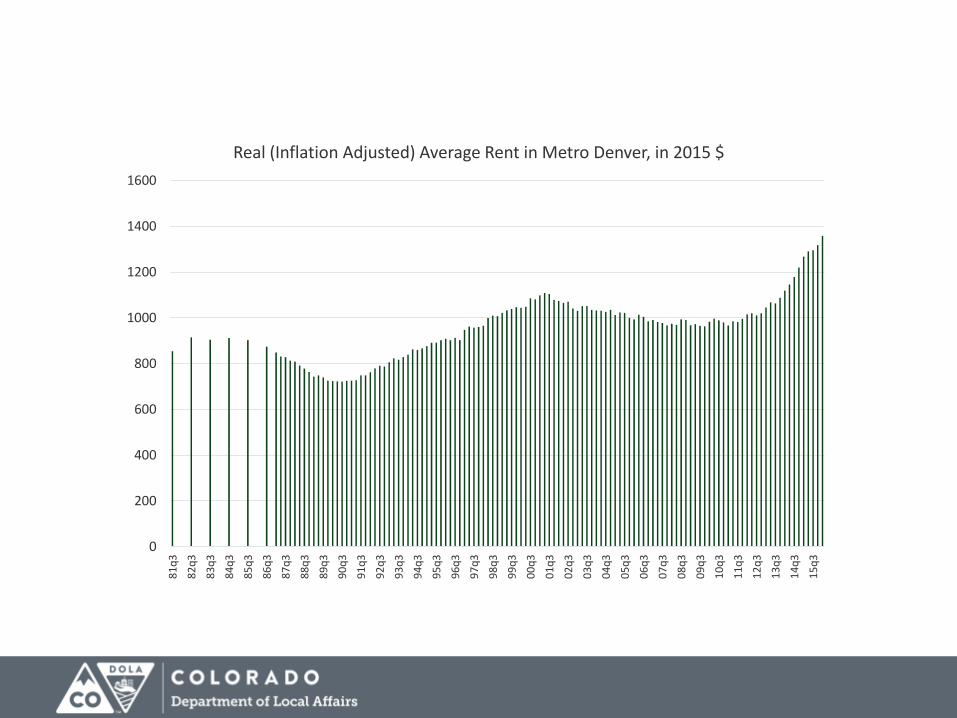

Real (Inflation Adjusted) Average Rent in Metro Denver, in 2015 $

8.9

9.8

8.4

9.1

9.9

4.5 4.2

5.4

11.1

2.2

5.2

10.6

4.5 4.6

5.9

1.6

2.1

3.7

5.4 5

2.1

3.5

2.9 2.6

0

2

4

6

8

10

12

Metro Den C Springs Pueblo Greeley Ft Collins GJ

2nd Q Apt Vacancy Rate, by %

2009 2013 2015 2016

-1.7

1.5 0.9

-0.2 -1.2

0.6

4.3 3.9

-5

7.9

0

-12.5

13.2

4.4

0.16

13.7

17.9

-1.1

8.3

10.2

11.6

4.2

0

-0.5

-15

-10

-5

0

5

10

15

20

Metro Den C Springs Pueblo Greeley Ft Collins GJ

% Growth in Average Rent

2009 2013 2015 2016

2,453,848 2,548,945

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

Colorado: Total Tax Return Filers

$21,825

$20,581

$18,881

$0

$5,000

$10,000

$15,000

$20,000

$25,000

2000200120022003200420052006200720082009201020112012201320142015

Colorado: Real Average Income Tax Collections, in $ per filer

0

100,000

200,000

300,000

400,000

500,000

600,000

Colorado: SNAP Recipients (Individuals Participating)

Panel Discussion Elizabeth Garner

State Demographer

Colorado Department of Local Affairs, State Demography Office

James Conner Economic and Market Analysis Division Field Director

HUD Region VIII – Rocky Mountain Region

Ryan McMaken Editor, Mises Wire and The Austrian

The Mises Institute

Panel Moderator

Alison O’Kelly CDBG-DR and NSP Programs Manager

Colorado Department of Local Affairs, Division of Housing

Open Discussion

and

Q&A

Did we address everything

in the Parking Lot?

A Visual Tour of Colorado’s

Regional Economies

Please fill out the

workshop evaluations.

Thank you for attending

Boot Camp Workshop #3