Embed Size (px)

Citation preview

..

, this report is restricted to use within the Bank. --_._--. , ..

No. E 85 RESTRICTED

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

SUMMAR Y OF ECONOMIC AND FINANCIAL

DEVELOPMENTS IN INDIA IN THE LAST HALF

OF 1949

March 17,1950

Economic Department

Prepared by: William N. Gilmartin

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Summary of Economic and Financial Developments in India in the Last Half

of 1949

Summary

The purpose of the present study is to review briefly tl~ economio

and financial developments in India in the latter half of 1949 as indi-

cated in information available here. A more detailed analysis of the

situation is deferred until the return of the Bank Mission which is now

conducting a survey of Indian economic and financial conditions.

The most striking of recent economic developments in India has been

the substantial improvement in the external trade position. The heavy

trade deficit, incurred in the first half of 1949 was sharply reduced in

the second half of the year and India's sterling balances~ which fell by

about Rs. 2,000 million during January-June, remained approximately

constant between June and December. On hard-currency accounts there was

a small surplus in the last half of the year as compared with a large

deficit in the first half.

Devaluation of the rupee by )0% in September was followed by an

increase in Indian export volu."ne, as well as value in terms of rupees,

"while imports were sharply curbed in the latter months of 1949 by severe

administrative restrictions. Since devaluation, India also appears to

have enjoyed some improvement in its over-all terms of trade. However,

no significant impact of devaluation on internal cost/price relationships

was noticeable up to the end of the year.

- 2 -

In spite of the reduction in the trade deficit, relative stability

was maintained in the internal money supply and in the price level. This

may be attributed in part to the 8 point economic program, adopted by the

Government in October to cope with problems arising from devaluation and

from the lethargy in the long-term money market. Among other measures,

the program included economies in Government spending, an intensified

savings drive, increased export duties, and tighter ceilings on key com

modity prices_ The recent budget statement indicates a smaller gap be

tween ordinary receipts and total expenditures during the current fiscal

year than was originally forecast.

It would appear, however, that temporary factors have played a sub

stantial role in the improved trade position and in the stable internal

financial situation. A conplete suspension in the licensing of private

hard-currency imports between June and September, and subsequent delays

in processing applications for such licenses have undoubtedly left a back

log of hard-currency import demand which will be carried over to become

effective in 1950. Soft-currency im~orts were also subject in the last

half of 1949 to severe licensing restrictions which have now been some

what relaxed. These influences indicate an increase in the rate of im

ports in 1950, but may be counteracted to some extent by the announced

decision of the Government to reduce grain imports this year to less tnan

half the 1949 level. Formidable difficulties, arising out of the problems

-3-

of rationing and nrocurement, are likely to be encountered, however, in

carrying out this decision. Other uncertainties also exist in India's

current export position, notably in the ability of certain export lines

to sustain the momentum which was built up following devaluation.

In the internal financial field, seasonal factors appear to have been

important in the maintenance of a stable money supply at the same time that

the trade deficit was reduced. The normal slack season in the demand for

short-term financing was probably accentuated and prolonged in the last

half of 1949 by reduced activity in the jute and textile industries and

by the suspension of trade with Pakistan after September_ As a result,

substantial short-term Government borrowing was resumed during July-September

and in early December for the first time since November 1948, while there

was a cont~a~ private bank financing by almost Rs. 1,000 million in

the last/~ of the year. The long-term money market continued to languish

throughout 1949, however, and recently a contraction in available short-term

credit has been reported. An upward tendency in money supply and prices has

been apparent in early 1950.

Perhaps, the most disturbing aspect of recent developments in India,

has been the virtually complete stalemate in trade relations with Pakistan.

This followed Pakistan's decision not to devalue and the subsequent refusal

of India to recognize the Pakistan rupee at a premium of 44% over the Indian

rupee. The continuation of this deadlock injects serious uncertainties into

the Indian economic picture. This applies not only to India1s jute industry,

-4-

which has been heavily dependent on raw jute from Pakistan, but t:hrough

out a wide range of other economic activities. In addition to the loss

of the Pakistan market for Indian coal, textiles, steel, and numerous other

commodities, India will have to draw on other sources to an increased extent

for raw cotton imports" part of which vn.ll require dollar payments. The

ability of the jute industry to maintain present levels of production is

uncertain, little can be expected in the way of raw' jute and raw cotton

exports, and export earnings fro~ hides and skins are likely to be curtailed.

A serious burden is imposed on India's internal finances by heavy military

outlays (currently amounting to half of ordinary Government expenditures)

vvhich are associated ln large part with the deterioration in Indo-Pakistan

relations.

In view of the imnortance of temporary factors and in the light of

certain unfavorable developments, particularly in Indo-Pakistan relations,

the recent lmprovement in the general economic and financial situation

should not be interpreted too optimistically. Inflationary pressures seem

likely to continue as a problem and there will probably be a somewhat larger

trade deficit in the first half of 1950 than in the preceding six months.

Cabinet officials state only that the payments deficit for the year ending

in June 1950 will be kept within the amount of the releases from India's

sterling balances during this period. This, however, will represent a sub

stantial improvement over the extrem.e imbalance in India's external accounts

which developed during the last half of 1948 and the first six months of 1949.

Summary of Economic and Financial Developments in India in the Last Half

of }949

The Position in January-June 1949

The review of economic and financial developments in India during 1/

the first half of 1949, prepared by the Economic Department last August~

stressed the seriousness of the increasing imbalance in India's external

trade and payments position. It was pointed out that the relative stability

in the internal financial situation and the degree of progress achieved in

domestic production were overshadowed by, and partly the result of, a trade

deficit which reached record proportions during the first six months of the

year. The degree of imbalance in India's current external accounts which

developed in early 1949 apparent in the following comparisons of the

balance of payments by six month periods between January 1948 and July 1949:

~~ India's Balance of Payments on Current Account

January 1948 - June 1949 (in millions of rupees)

Jan .... June 1948 Jan.-June 1949 Rec. Pay. Net

July-Dec, 1948 Rec. Pay. Net. I Eec;----pay. Net

Trade 2469 2246 .J. 223 1868 2~99 - 731 '1928 3519 - 1591 Services, Donations,

1216-lH~ _ 686 etc. 554 586 - 32 530 I 636 820 - 184 - - ,-Total 3023 2832 f 191 2398 3815 -1417 12564 1~339 - 1775

~~

.----...--- . ---Excluding transactions with Pakistan. On trade accounts India had an estimated deficit with Pakistan of about Rs. 300 million during July-Dec, 1948, and of about Rs. 50 million during Jan ... June 1949.

';} .• H"

" Includes Rs. 600 million paid to U.K. for defense stores and other wartime installations in India.

±/Recent Economic Developments in India (No. E-6oA) August 12, 1949. I

- 2 -

The Trade Situation in July-December, 1949

The last six months of 1949 witnessed a marked reversal of the earlier

trend in India's external financial position. The deficit on seaborne trade

was cut from about Rs. 1,500 million in the first half of 1949 to less than

Hs. 400 million in the period July-December through an increase in exports

and a decrease in imports, amounting to about 20% in each case (See Annex I).

In the closing quarter of the year, following the devaluation of the rupee

by 30% in September, Indian seaborne trade sbo1Tfed an eX:90rt surulus for the

first time since the last quarter of 1947. The post-devaluation rise in

exports applied to most major eX?ol~ commodities, except raw jute and raw

cotton, and reflected increased volume as well as a higher rupee value.

Imports fell as a result of a temporary General suspension in the licensing

of hard-currency imports and a restriction of soft-currency im:9orts to high

priority items. It also appears that there was an improvement in India's

terms of trade following devaluation. The weighted average unit value of

major exports in December was about 20% higher than in August whereas indexes

of export prices in the U.K. and the U.S. indicate an increase in the average 1/

rupee value of Indian imports by something under 10%7

While balance of payments data for the last half of 1949 are not yet

---------------------------. --------------------~-- ------------~-------~ Y Devaluation does not a'''oear to have had any sirnificant inpact on

domestic cost-price rel~tionships up to the end of the year. As noted below the price level was stabilized in the last quarter of 19)./.9 and in December the index of workE,rs f cost of livinf in Bombay 'v'ias less than 1% above the pre-devaluation level.

- 3 -

available, the striking improvement in the external payments position

since June is reflected in the fact that India's sterling balances have

remained constant for the period July-December whereas they fell by al

most Rs. 2,000 million in the first half of the year (See Annex IV).

On hard-currency accounts, Government officials have stated that there

was a surplus of about 1~13 Billion in the last half of 1949" as compared

vrith a hard-currency trade deficit duri.ns: January-June of about '5145

million. (See Annex ) • This marked improvement is also reflected in

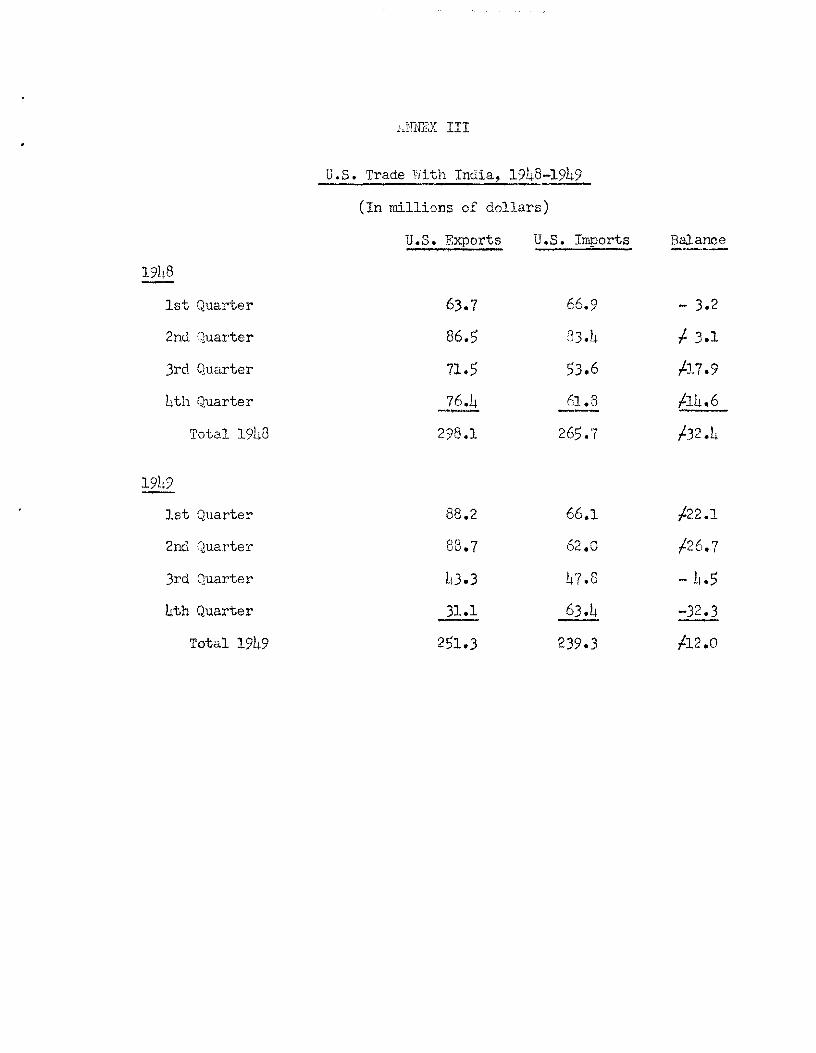

u. s. trade statistics during 1949 (See Annex III).

Internal Financial Developments :;).lring July-December 1949 i "'_ .•.. -

Meanwhile, in spite of the large reduction in the trade and pay

ments deficit in the latter part of 1949, the internal financial situation

continued on an even keel. ~loney supply remained stable and the upward

tendency in the price level in the second and third quarters of the year

was checked in the fourth quarter. This may be explained, in part, by

measures taken by the Government, under the 8 point economic program

announced in October, to cope 1~~h problems arising from devaluation of

the rupee (See Annex VIII). The rate of over-all Government exPenditure 1/

'Ivas reduced; export duties were increased, and cuts were imposed on

'--~--------.-------.----11 In the revised budget estimate for fiscal 1949~SO total Government ex

pendi tures are now forecast at [18. 64 minion less than in the original budget estimate. Ordinary expenditures are expected to exceed previous estimates by Rs. 136 million but this more than offset by an esti-mated reduction in capital outlays of Rs. 200 million. Ordinary revenues are now expected to be Rs. 94 million higher in the current fiscal year than was originally estimated. The orieinal and revised budget estimates

- 4 -

controlled prices of certain key items, such as food grains, textiles,

iron and steel, and coal.

It seems fairly evident, however, that any improvement which may have

occurred in the ratio of Government receipts to expenditures in the last

half of 1949, as compared with the first half, was not of sufficient magnitude

to offset the loss of counter-inflationary inflUences arising from the sharp

reduction in the import surplus. HOi'rever, a further factor appears to have

played a major role, namely a marl{ed contraction in private short-term bank

financing (by Rs. 978 million durine: I,1ay-December) I which '!{as partly a seasonal

for fiscal 1949-50, and the estiraate for fiscal 1950-51 are as follows:

Indian Budget Lstimates for 1949-50 and 1950-51 (in millions of rupee~)

191.~9-50 .. t"--' ....... '. 1950-51 First Budg~t Est. f Revised Budget Est. f FirAt;. Budget Est.

Ordinary Revenues Expenditures Balance

Capital Expenditures

3230 3225

,L 5

1710

Excess of Total Expenditures over Ordinary Revenues 1705

3324 3361 - 37

1510

1547

3392 3379 ,L 13

1050

1037

- 5 -

1/ phenomenon; and partly related to the decline in imports and hence in re-

quirements for import credits. At the same time, sales of Treasury Bills

by the Government, which had been completely suspended in the first half

of 1949, amounted to almost Rs. 400 million in the second half. P.eserve

Bank holdings of 'Treasury Bills increased between July and December by only

Rs. 27 million.

Other Aspects,of Recent Economic Developments

In general, the statistical picture of economic and financial

developments in the latter half of 1949 presents an a~pearance of sub-

stantial improvement. It is not the intention here to attempt a detailed

analysis of these developments in view of the present economic survey

which is being made in India by a Bank Mission. It should be noted, how-

ever, that the picture has not been without its unfavorable aspects; that

at least a part of the improvement in trade, especially in the hard-currency

trade balance, was due to special circumstances; and that there are numerous

uncertainties involved in India 1 s trade prospects in the immediate future.

It has already been noted that seasonal factors were partly responsible for

Y There is normally in India a slack season in the short-term money market running usually from March or April to about October. It arises primarily from the cycle of crop movements. This seasonal pattern was delayed in 1949 because of the heavy demand for import credits in the first half of the year and was prolonged partly by the suspension of trade with Pakistan after September. The slack season was probably also accentuated in 1949 by reduced activity in the jute and textile industries.

- 6 -

recent monetary stability_ Some upvrard tendency in the money supply and

in prices is already apparent in statistics for January and February, 1950

and sales of Treasury Bills have been sus,endecl since late December due to

a contraction in the availability of short-term funds. The long-term money

market has continued to languish and central Government borrowing, other

than short-term, during 1949 was confined to a conversion loan of Rs. 320

million in July.

Some gains in over-all industrial YJroduction probably occurred in

1949 as compared with 1948 but these appear to have modest in snite

of a substantial improvement in railway transportation and the elimination

of priorities for the movement of freir;ht traffic. Among major Indian

industries a larger physical output was recorded in coal (by 4%), steel

(8%), cement (33%), paper (6%) and sugar. But against this, production

was dOYin in the important jute and cotton textile industries. Jute

production fell from the 1948 level by 9% and the output of cotton yarn

and cotton cloth declined b~t about 10~~.

Factors in the Improvement in Hard-C;:~cy Tracie

Even the improvement in the trade position in the last half of 1949

vras not entirely a matter for satisfaction in view of the circumstances

responsible, at least in part, for the approximate balance in h:lrd-currency

trade accounts. Al thougl: there ",as a SUbstantial increase in the dollar

value of hard-currency exports in the last quarter of the year, as compared

with the second and third quarters, this increase was only to about the

- 7 -

level of the first quarter and for the full six months of July-December

the value of hard-currency exports, expre in dollars, was no higher

than in the first half of the year. It is clear, therefore, that the im-

provement in the hard-currency trade position ':yas entirely due to a sharp . 1/ decline in im:;Jorts. - This clecline may be largel~T attributed to the conplete

suspension in the processing of applications for Jrivate hard-currency im-2/

port licenses between June and September -; and the delays to v.rhich the

processing of hard-currency im:;Jort 5.lJplications has been subject since

September. This situation has undoubtedly a considerable backlog

of hard-currency import demand from the July-December licensing period

which will be carried over to raise the level of hard-currency imports on

private account in 1950.

The Indo-Pakistan Trade Deadlock

Perhaps the most disturbing development in the Indian economy and in

India's trade prospects in recent months has been the serious deterioration

in economic relations with Pakistan and the virtual standstill in trade

between the ty.[Q countries following Pakistanis decision not to devalue and

the refusal of India to recognize the Pakistan rupee at a premium of 44%

----~---------------~-,------ ----~-----

Indian statistics on hard-currency in the last half of 1949 are not available but U.S. figures show a decline in eJ-:tlorts to India from ?~177 million in the first half of 1949 to ~~ 74 million in the last half.

This was the result of delays in revlslng the hard-currency import program follo'wing the agreement among the Commom1fealth Countries in mid-19u9 to reduce dollar imports by 25%. As late as November 29, 1949 the Finance Minister stated that as of that date no hard-currency exchange had yet been released against new Drivate import licenses issued under the July-December import propram.

- 8 -

over the Indian rupee. The effects of a continued stalemate in Indo-1/

Pakistan trade will extend. beyond. the mutual loss of the substantial

co:maerce between the two countries. As far as India is concerned, it

';:i11 mean increased imports of rcr,; cotton from other sources (this in-

crease has been estimated at at least 200,000 bales in 1950, a substantial

part of yrhich may have to be purchased with hard-currency), and a con-

siderable loss in export earnings from raw jute, raw cotton, and hides

and skins.

Possibly even more serious is the threat to India's export position

in manufactured jute. There is considerable question as to how long India

can maintain present levels of jute manufacture, and as to how much the

output of jute goods may eventually have to be reduced in the absence of

raw jute supplies from Pakistan. Indian press reports contend that, at

tIle reduced output level prevailing in the latter Dart of 1949, the Indian

mills can maintain production beyond the first half of 1950 on the basis

01 raw jute available from the current domestic crop together with jute

on order in Pakistan prior to devaluation, 7Thich Pakistan has acreed to

release, plus some supplies Nepal ane: such stocl<:s as l'tcre held by the

Indian mills in December. In the latter half of 1950 and thereafter it is

The economic consequences of unfavorable relations '''"ith Pakistan are not confined to the trade 5i tuation~ Heavy military outlays, associated at least in part with Indo-Pakistan differences, account for half of estimated ordinary Indian Government exoenditures in 1949-50 and 1950-51 and represent a continuing burden on the internal financial resources of both countries.

- 9 -

anticipated that domestic production vdll have increased sufficiently to 1/

meet over 80% of India1s normal requirements: These reports may be some-

what optimistic in the extent of their reliance on domestic production and

on the orpanization of efficient facilities for the marketing'of increased

supplies of domestic jute. In any case, in the continued absence of sup-

from Pakistan, they leave little room for Indian exports of raw jute

or for relief to the Indian mills from the high prices and scarcities of

raw jute which have prevailed in the past year.

Other Uncertainties in the Trade Position ! ,

There are other uncertainties in India's foreign trade outlook during

1950 in addition to the probable increase in private hard-currency imports

and the effects of a continued stalemate in Pakistan trade. Some examples

may be noted.

1. The Government has announced its intention to reduce grain imports

from 3.7 million tons in 19u9 to 1.5 million tons in 1950. This 'would mean

a large saving on imports estimated at between Rs. 800 to Rs. 1,000 million

~ The 19u9-50 Indian jute crop has been variously estimated at around 2.8 to 3 million bales. The crop target for 1950-51 is 4.5 to 5 million bales. If this target is realized the domestic crop would be only about 1 million bales short of the nonna1 Indian jute l1'j.ll reqUirements. India's requirements of Pakistan jute during 1949-50 were estimated in July 1949 at 4 mi1J.ion bales.

- 10 -

1 / or around 15% of total imports in 1949.- Difficulties may be encountered,

however, in holding grain imports to this level in view of the past de-

~endence of the rationing system on foreign supplies. Increased domestic

[rain procurement and perhaps some reduction in grain rations may be neces-

sary, both of which measures will be difficult and unpopular. It is re-

ported, on the other hand, that large stocks of grains have been carried

over from 1949 which, if correct, will strengthen the :nossibilities of re

maining Yfithin the announced import target for 1950.

2. A more liberal licensing policy for certain soft-currency imports

such as non-ferrous metals, raw silk, silk yarn, tallow, heavy chemicals,

nev1rsprint, drugs, and other commodities has already been adopted and the

restrictions imposed on soft-currency imports in Nay 1949 and especially

in August may be somewhat further relaxed in vie,r of the recent upward trend

jn India's sterling balances.

3. 1::hile exports of most major Indian export conunodities, except raw

cotton and raw jute, increased in volume as well as value in terms of rupees

following devaluation, the prospects in 1950 involve varying degrees of

uncertainty for different commodities. The 8i tuation in jute [:oods, raw

jute and raw cotton has already been mentioned. Of India's other leading

exports - tea, cotton textiles, and vegetable oils and oilseeds .,.. only tea

In addition this would mean substantial savings in hard-currency if India successful in reported plans to obtain 900,000 tons of grain in soft-currency areas or through barter agreements. Assuming that all of the remaining 600,000 tons were to be purchased in hard-currency the cost would be in the order of Rs. 250 million whereas in 1949 hard-currency grain imports have been unofficially reported at Bore than Rs. 780 million.

- 11 -

seems reasonably certain of maintaining or oerhaps improving on the in

creased volume and value of shipments in 1949. The prosnects for textile

exports seem Generally favorable although here the sUbstantial recent im

provement occurred after devaluation at a time when rupee export prices

were under controlled ceilings. These controls have now been removed and

it remains to be seen what price increases will take Dlace and how external

demand will react to higher Indian textile prices. The situation in

vegetable oils and seeds is even more uncertain in view of recent temporary

restrictions on groundnut and linseed exports in an effort to check the

rapid rise in the domestic prices of these commodities which has taken place

during the last weeks of 1949 and the first part of 1950.

The preceding examples of some of the uncertainties in India's present

trade position indicate that the improvement in the trade balance in the

latter part of 1949 does not warrant too optimistic a view regarding trade

prospects this year. An additional over-all trade deficit, larger perhaps

than in the last half of 1949, and some deficit in hard-currency trade may

be expected in the first six months of 1950. Certainly, however, for 191.].9-

50 as a whole the current payment deficit will be far below that of the

previous year which anlounted to over Rs. 2,500 million. Indian Cabinet

officials have stated recently that any excess of current payments over

receipts for the year ending in June would be within the limit of the U.K. -

India agreement for releases from India's sterlinG balances. This could

- 12 -

I.to 1/ mean an over-all deficit up to 111 50 million (:'::s. ~ mil1ion)-plus any

excess, not to exceed an additional 1,50 million, attributable to liabili-

ties arising after July 1, 1949 as a result of import committments entered

into under the liberal open r:eneral license which was cancelled in May 1949.

It could also mean a hard-currency deficit for the year ending in June 1950.

The U. I:. has agreed to cover Indiafs'hard-currency deficits in return for

India IS :')ledge to hold hard-currency im;:lorts ( exclusive of those financed~

by the IBRD) to 75% of the 1948 level. It is :Jrobable that Y.rithln the

limits of this pledge India can raise the level of hard-currency imports

in the current six months above that during July-December 1949.

Y Excluding the value of imports finanoed by loans frOB the IBRD.

ANNEX.!

!E~1an Seaborne Trade, ~Flv 1948.December 194~

(In millions of rupees)

1948

3rd Quarter 4th Quarter

Tota1-July-Dec.'48

1949

1st Quarter 2nd Quarter

Total-Jan.-June '49

3rd Quarter~ 4th Quarterg,.

Total-July-Deo.t4~

Imports

1,236 1.23S--

1,621 1 2764

1,562

2,470

3,385

... 1.220 .

2,782

V Baaed on customs returns.

Exports !Incl.Reexport§)

1,079 ..... 1.049

1,031 942

1,007 •. 1.400

2,128

1,973

2,407

Surplus (,l) or Defi9it ( ... }

-157 -182

-342

-590 I ,,;826

-1412

-555 _..tlSO

- 375

ZI Import figures for July-December 1949 are preliminary revisions as reported unofficially in the Indian press. Export figures for the same period are from the annual budget message of February 28, 1950.

ANNEX II

Indian Seaborne Trade by Currency Areas. 194~-49l1 ............" t •

(In millions of rupees)

. Hard Currency Ar~e ~ Other Currency Area. _ Imports Exports Balance Imports Exports Balance

January-June 852 839 ... 13 1,394 1,629 ~235

.ML ~ -287 1.749 ; 1.'304 -442 July-December

Total 1948 1,703 1,403 .... )00 3 i 143 2,933 -210

January-June 1,005 516 -489 2,626 1,412 -1,214

.Jl:..El:. 657Y n.e. noe. 1.691Y n.s • -- -....-- ; July-December

Total 1949 1,173 3,103

11 Figures for 1948 and January-June 1949 are based on records of the Exohange Control Department of the Reserve Bank while the export figures for JulyDecember 1949 are preliminary reports based on customs returns as reported in the Indian press. A comparison with Annex I will indicate the su~ stantial differences in trade statistics for the same period as derived from exchange control records ano ss reported in customs returns. No precise exp1a~ation of these differences is available although it is possible that some trade on Government account is not included in oustoms returns and that some oustoms reports represent only approximate valuation.

21 Excluding reexports.

l~NNEX III

U.S. Trade W~th India, 1948-1949

(In millions of dollars)

U.S. Exports U.S. Imports Balance -------1948

1st Quarter 63.7 66.9 - 3.2

2nd Quarter 86.5 33.4 I- 3.1

3rd Quarter 71.5 53.6 1-17.9

4th Quarter 76.4 61.8 /-~4_6 . -Total 1948 298.1 265.7 1-32.4

1949

1st Quarter 88.2 66.1 !-22.1

2nd rJuarter 88.7 62.0 /-26.7

3rd Quarter L~3.3 47.8 -4.5

4th Quarter 31.1 63.4 -32.3 - -Total 1949 251.3 239.3 /-12.0

1945

1946

1947

1948 Y March

June

September

December

1949

lJarch

June

September

December

1950

ANNEX IV

India's Sterling Balances

1945-l950Y

(In millions of rupees)

February 17

16,677

16,227

15,185

11,000

10,253

9,,441

8,281

7,894

8,263

8,458

11 Figures are for last Friday of period. Sterling balances of Pakistan are included through June 1948 but excluded thereaftero

ANNEX V

Central Government Deposits in the Reserve Bank of India, 1945-1950, r./

(In millions 01: rupees)

1945 4,808

1946 4,576

1947 3,460

1948 March 3,200 June 2,859 September 2;297 December 2,145

1949 March 1,839 June 1;252 September 1,456 December 1,520

1950 February 10 1,532

Y Figures are for last Friday of period. Deposits of Pakistan are included through June 1948 but excluded thereafter~

1945

1946

1947

1948

March June September December

1949

];1arch June September December

1950

January

11 End of period.

ANNEX VI

Money; Supply. in India

1945-1950Y

(In millions of rupees)

curr~nci!l 13,090

13,370

13,370

14,160 14,220 1),120 12,920

12,800 12,6)0 ll,890 12,120

12,340

Deposit Money

7,430

7,980

8,030

8,270 8,700 7,840 7,650

7,420 6,890 7,090 6,690

6,940

Total

21,350

21,400

22,430 22,920 20,960 20,570

20,220 19,520 18,980 18,790

19,280

y Fi:;ures for March and June 1948 include Pakistan notes. Currency in circulation at the end of July 1948, exclusive of Pakist2.n notes, was Rs. 1),440 million. The reduction in the circulating currency during July 1948-June 1949 does not represent a net reduction in India since about Rs. 820 million of the decline was due to the return of Indian notes from Pakistan.

1948

January

March

June

September

December

1949

Barch

June

Septemb~r

December

1950

Al'll'J:SX VII

Index. of YJho1esale Prices in India!! (Year Ending August 1939 = 100)

All Commodities

329.2

340.7

370.2

February 4

y Weekly averages.

Foodstuffs

347.7

347.1

377.0

396.6

397.5

376.5

381.6

403.2

374.0

..,nne?!; VIII

statement of the Finance 'inister on the 8 Point Economic Program of the Indian Government

The entire policy of the Goverr~ent in the economic field came under detailed revie,-, last September when the devaluation of the rupee and the poor response of the market to Government's borrouing operations underlined the need for action to secure that further impetus was not given to the inflationary trends and an eight-point programme for meeting the altered situation was announced early in Octol::er. This programme envisaged:

1.. the formulation of the future pattern of trade to secure economy in the expenditure of foreign exchange with due regard to the ess(311tial needs of the country;

2. the employment of the country's bargaining power as a large-~cale purchaser to get a reduction to reasonable levels of prices of raw materials imported from countries lin th appl'eciated currencies;

3. the prevention of speculative price increases by legislative and administrative measures and the regulation of credit facilities;

4. the imposition of customs duties on articles exported to hard currency areas so as to ensure the maximum runount of foreign exchange and the equitable distribution of the advantage resulting from devaluation among the foreign importer, the Indian manufacturer and the public exchequer;

5. the stimulating of investment by an intensified savings drive by propaganda and, failing this, by compulsion and by provision of mlitable Governmental assistance for the extension of banking facilities in rural areas;

6. the extension of facilities for voluntary settlement of taxes payable in respect of war profits of assessees whose cases had not been referred to the Investigation Commission;

7. the introduction of economy measures to secure substantial savings in the current year l s budget and the budget for the eoming year and, lastly

8. the taking of steps, in consultation ,dth the State Gover~.ments, for bringing ab-out an aggregate reduction of 10 percent in the retail prices of essential commodities, including manufactured goods and food grains.

Among the measures taken under this programme may l::e mentioned the increase in the export duties on raw cotton and hessian, the former from Rs /fJ per bale to H.s 100 per bale and the latter from Rs 80 per ton to Rs 350 per ton, the levY of export duties on I[nlstard oil and certain categories of iron and steel, the reduction in the price of cotton textiles and yarn by a cut in the ex-mill

-1 ....

- 2-

prices and the margin allmfed for distribution, and, more recently by tr..e reduction in the level of excise duties on cloth, the reduction in the price of pig iron and the selling prices of all catee;ories of iron and steel and t:r..e reduction in the price of certain categories of coal and the grant of coal freight concessions to certain industries.

Rs regards food grain prices, the Government have decided to effect a reduction ranging from 3 percent to 15 percent in the issue prices, to be secured partly by a reduction in distribution and other incidental charges and partly by the lot.Jering of procurement prices. The cumulative effect of the measures taken to secure a reduction in the price level v111l take some time to be realised but they have already contributed towards holding the price level in recent months.

SourcE!: Hhite Paper on the Indian Budget, February 28, 1950.