Embed Size (px)

Citation preview

A SUMMER PROJECT

ON

SUBMITTED BY:

MEGHA JAIN

PROJECT GUIDE:

Mr. HIREN RAO

SUBMITTED TO:

ARVIND LIMITED

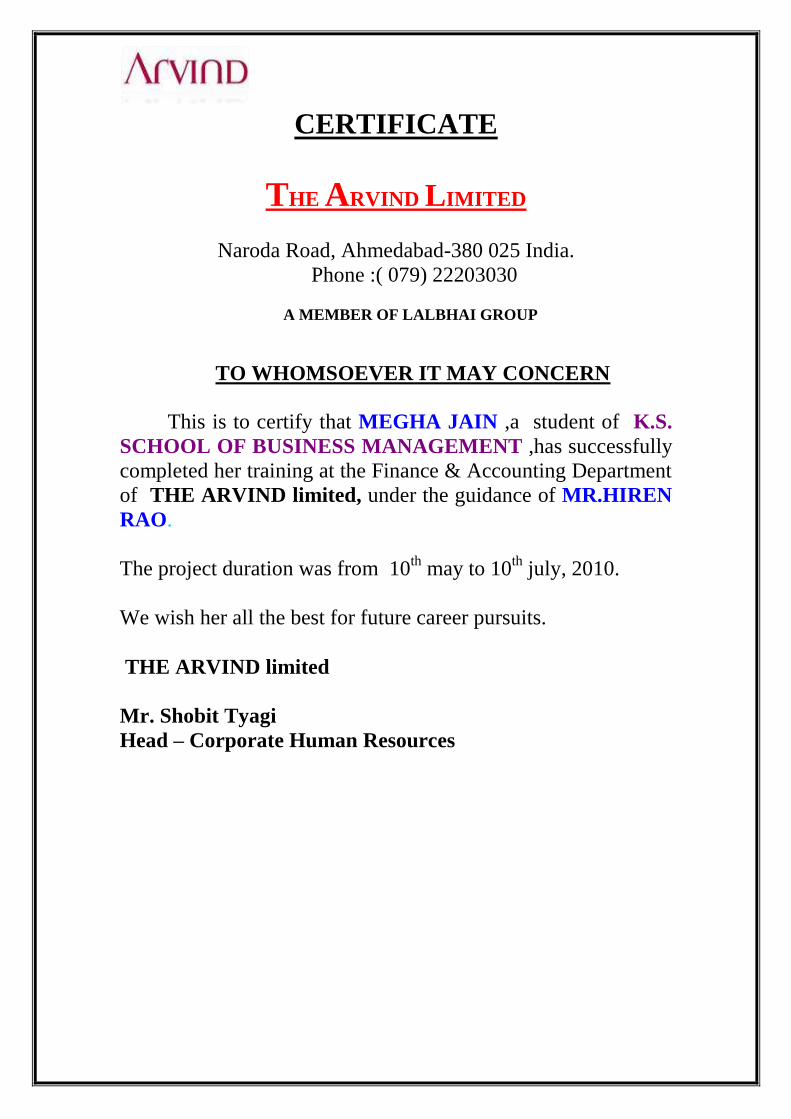

CERTIFICATE

THE ARVIND LIMITED

Naroda Road, Ahmedabad-380 025 India.

Phone :( 079) 22203030

A MEMBER OF LALBHAI GROUP

TO WHOMSOEVER IT MAY CONCERN

This is to certify that MEGHA JAIN ,a student of K.S.

SCHOOL OF BUSINESS MANAGEMENT ,has successfully

completed her training at the Finance & Accounting Department

of THE ARVIND limited, under the guidance of MR.HIREN

RAO.

The project duration was from 10th

may to 10th

july, 2010.

We wish her all the best for future career pursuits.

THE ARVIND limited

Mr. Shobit Tyagi

Head – Corporate Human Resources

PREFACE

For a long time, there is a wind of recession blowing

all over the business world and wealth liberalization policy

in the Indian Economy. So, nowadays market is

becoming more and more competitive.Company demands

more and more professional and accomplished employees.

Students have to get practical training along with

the theoretical knowledge of the business condition. There

are many advantage of making these kinds of reports.

Reading gives only the theoretical knowledge but training

gives an apportunity to learn and apply the concepts in the

real corporate world.

It is true that technical studies can not be perfect

without practical training and perfection is basic necessity

of management student.

ACKNOWLEDGEMENT

Feelings of gratefulness to anyone‘s help directly arise from

bottom of the heart. The small but an important act can prove to be a

milestone in one‘s life. We have achieved an important milestone in our

life by the completion of this project.

The project is dedicated to all the people whom we met and took

guidance from.I take this opportunity to thank the individuals who made

this report a success.

First of all,I am very fortunate that I got training in ARVIND

limited.I sincerely thank MISS MILLI DAS (Head –HR Department).

It is through her continuous guidance and support that the project has

become reality.

I would like to thank Mr. HIREN RAO (Head –Finance

Department) our Project guide, not only for giving me the opportunity

to work on this project, but also for providing me with sound guidance

and the necessary facilities to carry out the project. He constantly insisted

and helped me in learning new things. He provided me a lot of learning

opportunities.

Sincere appreciation is extended to Mr.VINEET SHAH for his

immense help during the course of this work. I would like to thank Mr.

DHARMESH PANDYA, for enabling me to learn and work on SAP for

fixed assets module.

Iwould like to thank MS. INGITA JAIN,our Project faculty

guide, who continuously monitored my work and provided guidance as

and when I needed.

MEGHA JAIN

K.S.SCHOOL OF BUSINESS MANAGEMENT

.

No. Name of content Pg no 1. Introduction to textile industries 1

1.1 Evolution & evaluation of the textile industries 3 1.2 Indian textile Industries 4 1.3 Gujrat textile Industries 5 1.4 Textile Industries Key Facts 6 1.5 Major Players in the textile Ind. In India 7

2. Introduction to Arvind Mills Limited 9 2.1 Company Profile 10 2.2 Fabric Production 11 2.3 Organization Structure 12 2.4 Subsidiaries 13 2.5 Board Of Directors 14 2.6 Group Overview 15 2.7 Company’s Vision 16 2.8 Company’s Mission 17 2.9 Company’s Philosophy 18 2.10 Functioning of the Organization 19 2.11 Denim Manufacturing Process 21 2.12 Market Network of Arvind 24 2.13 Portfolio of Arvind limited 29 2.14 Milestone Achieved 30 2.15 Financial Scenario 32

2.16 Shareholding Pattern of Arvind Limited 33 3. Working Capital Management 36 3.1 Concept of Working Capital 37 3.2 Form of Working Capital 38 3.3 Sources of Working Capital 42 3.4 Objective of Working Capital 45 3.5 Determinates of Working Capital 46 3.6 Significance of adequate Working Capital 48 3.7 Effects of excessive Working Capital 49 3.8 Balance sheet of Arvind Limited 50 3.9 Profit & Loss Account of Arvind Limited 51 3.10 Working Capital on Arvind Limited 52 3.11 Operating and Cash Conversion Cycle 63 3.12 Period of Operating Cycle 69 3.13 Working Capital policy 70 3.14 S W O T Analysis 72 3.15 Future Requirements 73 3.16 Interpretation of Working Capital 74

4. Recommendations 76 5. Conclusion 77 6. Bibliography 78

INTRODUCTION

The Indian textile industry has a significant presence in

the economy as well as in the international textile economy. Its contribution to the

Indian economy is manifested in terms of its contribution to the industrial production,

employment generation and foreign exchange earnings. It contributes 20 % of

industrial production, 9 % of excise collections, 18 % of employment in the industrial

sector, nearly 20 % to the country‘s total export earning and 4 % to the GDP.

CONTRIBUTIONS OF TEXTILE INDUSTRY IN ECONOMY

In human history, past and present can never ignore the importance of textile in a

civilization decisively affecting its destinies, effectively changing its social scenario.

Segments in textile industry:

Readymade Garments- denims, made-ups, shirts, etc.

Cotton Textiles including Handlooms (Mill made / Power loom/ Handloom)

Man-made Textiles

Silk Textiles

Woolen Textiles

Handicrafts including Carpets

Series1, Industrial

Production, 20%, 28%

Series1, Excise Collections, 9%,

13%

Series1, Employment in the Industrial Sector, 18%,

25%

Series1, Country’s total Export Earning,

20%, 28%

Series1, GDP, 4%, 6%

Chart Title

Coir

Jute

Evolution of Textile Industry

The ‗RAG TRADE‘, as it is referred to in the UK and

Australia is the manufacture, trade and distribution of textiles.There were various

stages – from a historical perspective – where the textile industry evolved from being

a domestic small-scale industry, to the status of supremacy it currently holds.

The ‗cottage stage‘ was the first stage in its history where

textiles were produced on a domestic basis. During this period cloth was made from

materials including wool, flax and cotton. The material depended on the area where

the cloth was being produced, and the time they were being made.

In the later half of the medieval period in the northern parts of Europe, cotton came to

be regarded as an imported fiber. During the later phases of the 16th century cotton

was grown in the warmer climates of America and Asia.

A number of new innovations led to the industrialization of the

textile industry. In the initial phases, textile mills were located in and around the

rivers since they were powered by water wheels. After the steam engine was invented,

the dependence on the rivers ceased to a great extent. In the later phases of the 20th

century, shuttles that were used in the textile industry were developed and became

faster and thus more efficient.

Today, modern techniques, electronics and innovation have led

to a competitive, low-priced textile industry offering almost any type of cloth or

design a person could desire. With its low cost labor base, China has come to

dominate the global textile industry.

Indian Textile Industry

Until the economic liberalization of Indian economy, the India

Textile Industry was predominantly unorganized industry. The opening up of Indian

economy post 1990s led to a stupendous growth of this industry.

Textile industry in India is the second largest employment

generator after agriculture. It holds significant status in India as it provides one of the

most fundamental necessities of the people. Textile industry was one of the earliest

industries to come into existence in India and it accounts for more than 30% of the

total exports. In fact Indian textile industry is the second largest in the world, second

only to china.

Till the year 1985, development of textile sector in India took place

in terms of general policies. In 1985, for the first time the importance of textile sector

was recognized and a separate policy statement was announced with regard to

development of textile sector. In the year 2000, national textile policy was announced.

its main objective was: to provide cloth of acceptable quality at reasonable prices for

the vast majority of the population of the country, to increasingly contribute to the

provision of sustainable employment and the economic growth of the nation; and to

compete with confidence for an increasing share of the global market. The policy also

aimed at achieving the target of textile and apparel exports of us $ 50 billion by 2010

of which the share of garments will be us $ 25 billion.

TEXTILE INDUSTRY KEY FACTS

Indian Textile Industry is one of the largest and oldest industries in India.

Indian Textile Industry is highly fragmented industry; at the same time it is an

independent and self-reliant industry that has shown sustainable growth over

the years.

Indian Textile Industry is second largest industry in terms of providing vast

employment opportunities and employs around 35 million people in country

after agriculture sector...

The Indian Textile Industry plays vital role in economic development and

contributes 14% to industrial production in the country.

Textile Industry contributes around 4% of GDP, 9% of excise collections,

18% of employment in industrial sector, and has 16 % share in country‘s

export

Industry has direct and strong linkage with rural and agriculture sector,

therefore it is estimated that, one of every six households in country is directly

or indirectly dependent on this industry.

Industry contributes around 25% share in the world trade of cotton yarn.

India is evolved as a major contributor in world‘s cotton sector. Indian is the

world‘s third-largest producer of cotton and second-largest producer of cotton

yarns and textiles.

India is the largest exporter of yarn in the international market and has a share

of 25% in world cotton yarn export market.

India contributes for 12% of the world‘s production of textile fibers and yarn.

Indian textile industry is second largest after China, in terms of spindle age,

and has share of 23% of the world‘s spindle capacity.

India has around 6% of global rotor capacity.

The country has the highest loom capacity, including handlooms, and has

share of 61% in world loom age.

Including textiles and garments, 30% of India's export comes from this sector.

Indian Textile Industry is one of the largest industries that provide high

exports and foreign revenue.

Large and potential domestic & international market, large pool of skilled and

cheap labor, well-established industry, promising export potential etc. are few

strengths of Indian Textile Industry.

Highly Fragmented, High dependence on cotton sector, Lower productivity,

Unfavorable Labor Laws is few drawbacks of the industry from which it has

to overcome.

After the elimination of quota restrictions and implementation of National

Textile Policy 2000, it is estimated that the industry will grow with rapid rate

and help to strengthen the Indian economy

STRENGHTS OF TEXTILE INDUSTRY

India has rich resources of raw materials of textile industry. It is one of the

largest producers of cotton in the world and is also rich in resources of fibers

like polyester, silk, viscose etc.

India is rich in highly trained manpower. The country has a huge advantage

due to lower wage rates. Because of low labor rates the manufacturing cost in

textile automatically comes down to very reasonable rates.

India is highly competitive in spinning sector and has presence in almost all

processes of the value chain.

Indian garment industry is very diverse in size, manufacturing facility, type of

apparel produced, quantity and quality of output, cost, requirement for fabric

etc. It comprises suppliers of ready-made garments for both, domestic or

export markets.

WEAKNESS OF TEXTILE INDUSTRY

Indian textile industry is highly fragmented in industry structure, and is led by

small scale companies. The reservation of production for very small

companies that was imposed with the intention to help out small scale

companies across the country, led substantial fragmentation that distorted the

competitiveness of industry. Smaller companies do not have the fiscal

resources to enhance technology or invest in the high-end engineering of

processes. Hence they lose in productivity.

Indian labor laws are relatively unfavorable to the trades and there is an urgent

need for labor reforms in India.

India seriously lacks in trade pact memberships, which leads to restricted

access to the other major markets.

INDIAS MAJOR COMPETITIORS IN THE

WORLD

Gujarat Textile Industry

Gujarat is one the leading industrial states in India and textile

industry in India in particular had contributed in big way to the industrialization of the

state. In fact, development of the many industries like dyestuff, chemicals

Engineering/foundry and cotton farming is solely dependent on these sectors. The

state is well known for development of hybrid cotton, ginning, power looms,

composites mills, spinning units and independent processing houses.

In Gujarat, textile manufacturers use cotton based fabrics in

mill sector, major reason being the availability of the basic raw materials in the state,

i.e. cotton. Similarly many spinning units producing more conservative yarns were

established in the state. The state happened to be more conservative with cotton textile

products mainly in the organized sector, weaving and synthetic textile in decentralized

sector. Surat art silk manufacturers are only exception. Similarly, independent

processing units process synthetic blended and cotton fabrics. Clusters of processing

units are located in Surat, Ahmedabad and Jetpur, though these production units have

good capacity of processing wide range of fabric.

Ready-made Garment manufacturing and hosiery knitwear

unit also exists in SSI categories. In early 1990‘s Gujarat saw dramatic change in its

textile industry scenario where quite a few textile mills started manufacturing Denim.

The Arvind mills, Ashima Textiles, Soma Textiles, Modern Denim, and Arvee denim

started manufacturing denim. So many mills at a time fetched a new name for

Ahmedabad ―Denim city of India‖ whereas city of Surat became ―Silk city of India‖.

MAJOR PLAYERS IN THE TEXTILE INDUSTRY IN INDIA

Arvind limited.

Arvind Mills is one of the major and fully vertically integrated composite

mills players in India. It has large production in denim, shirting and knitted

garments. It is now adding value by manufacturing denim apparel. Its sales are

around US$ 300 million.

Raymond‟s

Raymond‘s has the large, diversified integrated business model, which is

spread across the value chain from yarn to retail. It is specialized in

Diversified woolen textiles. It already supplies to some US retailers.

Reliance Textiles:

Reliance Textiles is one of the major Textile Company that is in business of

fully integrated manmade fiber. It has capacity of more than 6 million tones

per year. It has joint venture partners like, DuPont, Stone & Webster, Since

(Italy) etc.

Vardhaman Spinning vardhman deals in spinning, weaving and processing

segment of the industry. It is planning to double its fabric processing capacity

to 50 million meters. It is an approved supplier to global retailers like Gap,

Target and Tommy Hilfiger. Its sales are little over US$ 120 millions

Welspun India (Manufactures terry towels)

Century Textiles (Composite mill, cotton & Man-made)

Morarjee Mills (Fully integrated Composite Mill)

Indo Rama (Cotton and Man-made)

GTN Textiles (Cotton Yarn and Knit Fabrics)

Ginni Filamentslimited. (Yarn and Fabric)

LNJ Bhilwara Group (Diversified and vertically integrated denim producer

with spinning and weaving capacity)

Mafatlal Textiles (Fully integrated Composite Mill)

Modern Group (Diversified, producer of denim, syntax and thread)

Ashima Syntax (Man-made Fiber)

KG Denim (Fabrics)

Sanghi Polyesterslimited. (Manmade Fiber)

Nova Petrochemicals (Man-made Fiber)

S. Kumar Synfabslimited. (Home furnishing and Suit Fabrics)

Bombay Dyeinglimited. (Composite and fully integrated)

Rajasthan Petro synthetics (Diversified)

BSLlimited. (Textiles)

Garware Polyester (Diversified)

Banswara Syntex (Composite)

National Rayon Corp. (Man-made fiber)

GSL Indialimited. (Threads)

Indian Rayon (Man-Made Fiber)

Alok Textiles (Cotton and Man-made Fiber Textiles)

Sharda Textile Mills (Man-made Fiber)

Birla Group Dormeuil Birla VXLlimited. (Fully integrated woolen textiles)

Gokuldas Images (Diversified)

Hanil Era Textiles (Yarn, Cotton & Man-made Fiber)

Oswal Knit India (Woolen Wear)

Niryat Sam Apparels (Apparel)

MAP SHOWING LOCATION OF TEXTILES CENTRES

IN INDIA

Company Profile

The aim was to indigenously produce fine and superfine cotton fabric as well as

traditional material for vast potential

Indian market.

At this juncture, Arvind Mills was set

up with the pioneering effort of three

brothers, Kasturbhai, Narrotambhai

and Chimanbhai Lalbhai becoming

World‘s largest exporter and Asia‘s

largest producer of denims. During 1980s several mills in Ahmedabad closed down as

a result of competition from cheaper cloth produced by small power loom enterprises.

Militancy spurred by textile labour unions prevented the shutdown of several loss-

making mills, and in the mid 1980s Ahmedabad was a city of industrial strives.

ARVIND MILLS has risen like a phoenix from the ashes of Ahmedabad textile mills.

In just eight years it has successfully implemented a turnaround strategy.

Established in 1930, Arvind Limited is the flagship company

of $ 498 million. Lalbhai Group has now focused its attention on few selected core

product groups. Arvind today is a one-stop shop for all cotton fabric requirements,

where product range spans the entire gamut of cotton fabric. It is also a rapidly

expanding manufacturer of garments such as jeans and shirts. With the best

technology and business acumen Arvind Mills became the true multinational

producing the finest fabric available in the country that rivaled imported fabric. Since

then, there has been no looking back. Having established itself as India‘s largest

denim manufacturer, Arvind Mills is confident that in the near future it will become

the fifth largest denim producer in the world.

FABRIC PRODUCTION

In the 1980s the growing threat from small

power loom operators forced Ahmedabad‘s

composite mills to shift their focus to product

areas in which they could compete. In order to

better address newer and wider business

opportunities, the company shifted perspective

from domestic to international markets. At a

time when the local textile industry was

declining, Arvind‘s management devised a

turnaround strategy called ―Reno vision‖. It

represented an open-minded approach that

would seek out new opportunities.

In 1987 Arvind Mills made a conscious strategic

decision to change its production emphasis from

a portfolio of traditional domestic textiles to

high quality cotton fabrics. This required a level

of technological expertise, which small power

loom operators could not compete with. Arvind

identified denim as a key fabric. International

consultants McKinsey & Co. helped to frame company‘s business strategy, formulate

its organizational restructuring and establishing international alliances.

Today the company is engaged primarily in the manufacturing of indigo-dyed denim

fabrics, fine and superfine cotton shirting and bottom weights, and conventional

domestic fabrics such as sarees and voiles. In 1995 Arvind Mills held an 80% share of

India's domestic market for denim.

Organizational structure

Arvind defines its operations in terms of Strategic Business Units

(SBUs). Each product line – such as denim, shirting, knits, voiles, etc – is designated

as an SBU. Each unit is headed by a president who is able to make independent

decisions on finance and marketing. The president is assisted by vice-presidents who

look after functional divisions.

SUBSIDIARIES

Arvind Mills has 11 subsidiaries, of

which seven are in textile and related

businesses. They are:

Arvind Clothinglimited.

Arvind Fashionlimited.

Arvind Worldwide Inc, USA

Arvind Clothinglimited (ACL), situated in Bangalore, began commercial

production in April 1994. ACL is the exclusive licensee in India of CluettPeabody &

Co of the USA, which owns the Arrow brand name. It has the capacity for making 1

million shirts per annum, and has received ISO 9002 certification.

Arvind Fashionlimited (AFL) is a licensed user of the brand names belonging

to the US Company VF Corporation, which owns the well-known international trade

mark ―Lee‖. The company has a letter of intent from the Indian government (pending

the issue of a license) permitting it to manufacture up to 960,000 garments per annum,

provided it exports 50% of the garments produced.

AFL has invested Rs.160 million in establishing a jeans manufacturing unit at

Bangalore. The state-of-the-art factory, which has a production capacity, of 500,000

pairs of jeans per annum, is equipped with machines made in the USA, Japan and

Europe.

Spring 1995 saw a launch of a wide range of products-including jeans, jackets, denim

shirts, twill shirts, T-shirts and accessories such as belts and bags –under the ―Lee‖

trade mark. These are sold through exclusive showrooms located in major cities

throughout India.

Although its current turnover is small, AFL is in good position to capture a significant

share of the growing domestic market.

Board of Directors

The top management of the company consists of following members:

Company‟s Vision

Name Designation

Mr. Sanjay S. Lalbhai

S/O Mr. Shrenikbhai Lalbhai

Executive Chairman & Managing Director (Promoter)

Mr. Jayesh k. Shah

S/O Mr. Kantilal Shah

Executive Director & Chief Financial Officer

Mr. G.M. Yadwadkar

S/O Mr. M.A Yadwadkar

Non-Executive, Independent – Nominee Director IDBI

Banklimited.

Mr. S.R. Rao

S/O Raghunatha Rao

Non-Executive, Independent – Nominee Director

EXIM Bank of India

Mr. K.M. Jayarao Non-Executive, Independent – Nominee Director

ICICI Banklimited.

Mr. Sudhir Mehta

S/O Uttamlal Nathalal Mehta

Non-Executive, Independent – Director

Mr. Tarun Sheth

S/O Natwarlal Gordhandas Sheth

Non-Executive, Independent – Director

Mr. Munesh Khanna

S/O Narindra Khanna

Non-Executive, Independent – Director

"To achieve global dominance over various businesses built around our core

competencies, through continuous product and technical innovation, customer

orientation and a focus on cost effectiveness".

All along Lalbhai Group has maintained a responsive yet levelheaded attitude towards

the society and its training individuals to create a corporate culture that fosters

excellence. Working in this direction the company has created a learning environment

that nurtures individual talent and intellect. It provides a platform that challenges the

individual capabilities urging them to constantly strive forward towards greater

heights using development as the fundamental tool.

It infuses in individuals a spirit of entrepreneurship which gives courage and

conviction to pursue set goals towards logical achievement and a global mindset that

transcends geographical and cultural boundaries evolving as a world leader. All this is

manifest in an environment fostering innovation and leadership.

Drawing from the Team based structure to encourage individuals to mesh up into

cross-cultural teams in all operational processes. This process provides opportunities

for individuals to match their capabilities with organizational expectations creating a

mechanism for updating the system. A strong sense of ownership and commitment

towards the organization and the business as a whole is the basic premise of all the

company actions.

Company‟s Mission

Arvindlimited. has laid down certain aims and objectives to be achieved while

pursuing its corporate activities. These are:

To provide a favorable work environment to the employees to direct their working

towards achievement of corporate goals.

To provide opportunities creating a mechanism for updating the system

To manage the institution as a trust, as empowered leaders and do all that needs to

be done ethically for the purpose of the institution.

To create a vibrant institution for the future of this nation and the world at large

To be a world leader in an environment fostering innovation and leadership.

To reinforce connections, and catalyze the chemistry that allows connections to be

translated into action which is beneficial for both the organization and the

individual.

Company‟s Philosophy

"It is my responsibility as a leader to create an environment where excellent

people would like to come and give their best, to create a vision, to give freedom

for excellence."

- Sanjay Lalbhai (Managing Dir.)

―We believe in potential of every human being. Our Human Resource Development

policy reflects this belief.

We recruit the best talent wherever we do business, offer competitive compensation,

provide a dynamic work environment, make people accountable for results, and chart

their growth through systematic career planning. Our structures are well defined

which allows us to be more flexible and respond to the customers promptly.

We encourage innovation and entrepreneurship and motivate our people to take on

leadership roles through job re-assignments. This helps us create a learning

organization with a workforce that has multi-dimensional experiences and skills.

Our campus recruitment program and on-going involvement with educational

institution ensures access to highly trained managers, engineers and workers to

support our aggressive global plans. And our training centers – FOUNTAINHEAD

(the hub of all training activities at Arvind), INDRADHANUSH (for operatives),

ORCHID (for behavioral training), and CALCULUS (for computer training) –

ensures they continue to learn and grow.

Functioning of the Organization

Each ‗Strategic Business Unit‘ is headed by a Business Head. There are also small

garment units at Asoka and Retail outlets at Naroda. The organization has adopted a

Hybrid Structure to be more responsive to the changing markets in which the

Functional and the Divisional structures are combined together. As the organization

grew larger with several products and markets, it typically organized into self-

contained divisions. Functions like marketing, which is important to each product or

market are decentralized to the self-contained units. However, some functions like

Finance, MIS, Legal and Secretarial, Taxation and Services that are stable and require

economies of scale and in-depth specialization are centralized at Naroda Corporate

headquarters. Each of these departments provides services for the entire

organization.

The main product divisions are Denim, Shirting, Knits and Central Utility that are

created to serve a different market. Individually, they all require a different strategy

and management style. Each product Line Head is in charge of all functions of that

product such as marketing, planning, supply and distribution, and manufacturing.

There is no Matrix reporting, which means that they follow one-to-one reporting. The

Supervisors will report to the Functional Heads or Managers and the managers in turn

will report to the Managing Director who is the apex of the organization.

EMPLOYEES

The company in all is operating on strength of nearly 3000 managerial cadder

employees and approximately 15000 first line managers. Employees are all qualified

and technically efficient to serve its clients. Employees are given training of all the

products and services so that they can serve its clients better. Company has a healthy

incentive structure for its employees.

TURNOVER

The approximate turnover of the company was Rs. 2344.99 crores (as per current

financial year 2008-2009).

GEOGRAPHICAL SPREAD

Arvind‘s worldwide network facilitates Global account management for the leading

brands and local customers. With offices in New York, London, Bangladesh, Delhi,

Ahmedabad, Mumbai, and Bangalore, Arvind has made itself ready to attend to its

customers anywhere on the Globe. Besides their global offices, they have independent

and devoted sales force for all locations and dedicated resources for key accounts.

Denim Manufacturing Process

The term "Denim" has originated from the city of Nimes in France where "serge de

Nimes" was manufactured. Denim is made from a vat dye, the Indigo dye, which is

applied to cotton fabric in loosely held form in layers. As far as manufacturing

process of denim is concerned, it is similar to that of Grey fabric up to the process of

weaving with the only difference that in case of Denim Fabric, it is dyed at the stage

of sizing where as in case of Grey Fabric, the decision regarding dyeing stage depends

upon the finished product.

SPINNING

The initial processes of denim manufacturing consist of the regular activities of

opening and blending of cotton fibers. Carding is done to

remove any foreign matter and the short fibers so that cotton

takes the form of a web which is then converted into a rope-

like form, the sliver. Then drawing process produces a

single, uniform sliver from a number of carded slivers. Yarn

is then spun through Open-End Spinning or Ring Spinning.

Roving is also carried on, if the spinning has to be done through Ring Spinning.

Generally, denim fabric are 3/1 warp-faced twill fabric made from a yarn dyed warp

and an un-dyed weft yarn. Normally dyed and Grey ring or open- end yarns are used

in warp and weft respectively. The warp yarn is indigo dyed.

WARP preparation – Dyeing and Sizing process

Warp yarns are indigo dyed and sized with the help of two

methods:

(i) Threads from several back beams are combined to form a

warp sheet and dyed and sized on the same machine.

(ii) Threads, about 350-400 in number are formed into ropes.

12-14 ropes run adjacent to each other through the continuous

dyeing unit. After dyeing, the ropes are dried on drying cylinders and then collected in

a can.

After that, a worker's beam is prepared. Sizing is then done in the conventional

manner.

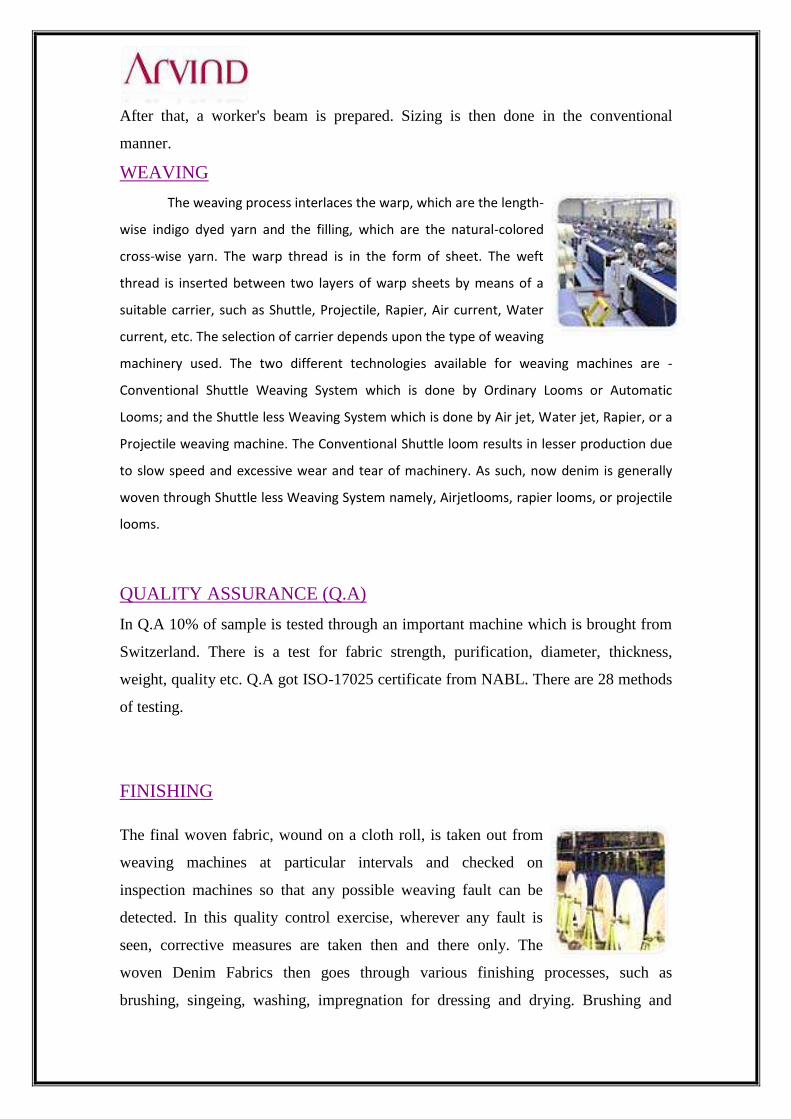

WEAVING

The weaving process interlaces the warp, which are the length-

wise indigo dyed yarn and the filling, which are the natural-colored

cross-wise yarn. The warp thread is in the form of sheet. The weft

thread is inserted between two layers of warp sheets by means of a

suitable carrier, such as Shuttle, Projectile, Rapier, Air current, Water

current, etc. The selection of carrier depends upon the type of weaving

machinery used. The two different technologies available for weaving machines are -

Conventional Shuttle Weaving System which is done by Ordinary Looms or Automatic

Looms; and the Shuttle less Weaving System which is done by Air jet, Water jet, Rapier, or a

Projectile weaving machine. The Conventional Shuttle loom results in lesser production due

to slow speed and excessive wear and tear of machinery. As such, now denim is generally

woven through Shuttle less Weaving System namely, Airjetlooms, rapier looms, or projectile

looms.

QUALITY ASSURANCE (Q.A)

In Q.A 10% of sample is tested through an important machine which is brought from

Switzerland. There is a test for fabric strength, purification, diameter, thickness,

weight, quality etc. Q.A got ISO-17025 certificate from NABL. There are 28 methods

of testing.

FINISHING

The final woven fabric, wound on a cloth roll, is taken out from

weaving machines at particular intervals and checked on

inspection machines so that any possible weaving fault can be

detected. In this quality control exercise, wherever any fault is

seen, corrective measures are taken then and there only. The

woven Denim Fabrics then goes through various finishing processes, such as

brushing, singeing, washing, impregnation for dressing and drying. Brushing and

singeing eliminate impurities and help to even the surface of denim fabric. Dressing

regulates the hand and rigidity of the fabric while compressive shrinking manages

its dimensional stability. The standard width denim fabrics are then sent for making

up. In this process, the fabric is cut into the desired width according to the size

required. The made- up denim fabric is then thoroughly checked for defects such as

weaving defects, uneven dyeing, bleaching and dyeing defects, oil stains, or patches.

After inspection, the final product is categorized quality-wise. The faultless fabrics

are sent to the packaging department while the defective ones are sent for further

correction.

INSPECTION

There are four rating system. It inspects physical parameter like width, square & linkej.

Complete material inspection is done as per the quality requirement of the customer & from

their product is delivered in the market. There are 13 inspection machines and each machine

has two operators.

Market Network of Arvind

Only two ingredients go into the making of Arvind denim – world-class quality and

complete customer orientation. A strong team of industry‘s best-qualified talents

forms the founding dimensions.

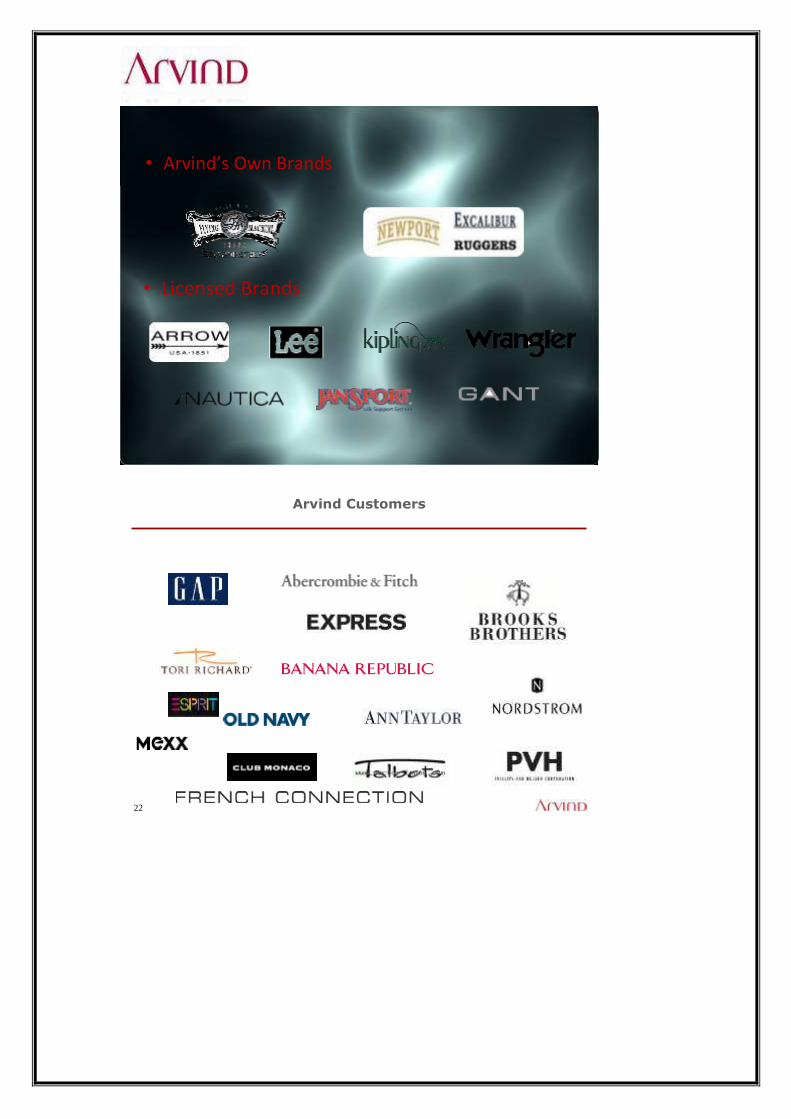

Arvind Limited today is reinforcing its marketing efforts by focusing on brand

development. They expect to strengthen its existing relationship with global brands

such as Marks & Spencer, V.F. Corporation, Calvin Klein, GAP, Benetton, Polo,

Espirit, Tommy Hilfiger, Hugo Boss and Liz Clairborne to list a few by developing

value added products and providing superior level of service. The complexity has

enhanced Arvind's product range and made it more responsive to the changing

requirements of some of the leading garment brands.

Arvind has single handily developed a multi-billion denim market in India. The

BRANDS fostered by Arvind include:

Lee & Arrow for the super premium segment

Flying Machine & Excalibur for the premium segment

Newport for the economy and

Innovative „Ruf & Tuf‟ for the mass market

The company has recently made a foray into children segment by introducing Lee

Youth, Ruggers Kids & Newport Kids. Similarly in tie-up with Cluett Peabody, USA,

to manufacture and market their world famous Arrow shirts, it launched what is

today‘s India‘s most inspirational brand of dress shirts.

In a world without boundaries, Arvind FABRICS are equally universal in their appeal.

Arvind aims to enrich lifestyles globally, inspiring diverse customers with the beauty

of their fabric.

Arvind was already making shirting for the Indian market. In 1990,

it decided to focus on high value shirting, so as to expand their

markets beyond India's borders. As a part of their commitment to

being a value-adding partner to each of the customers, Arvind

Shirting‘s have invested US $ 100 million in Santej. This plant has an annual capacity

of 34 million meters of 100% cotton woven. Arvind's philosophy in manufacturing is

'Excellence in Quality and Flexibility in Production'. In the entire process of

operations, eco-friendliness is critically monitored and ensured. The plant is also

configured to handle small order sizes as well as very long order lengths with

consistent quality.

Arvind has recently set up a dedicated bottom weights plant as part

of Arvind Polycot Limited. This new addition to the Arvind Textile

Complex brings the total investment in the complex up to Rs.12000

million. The plant is an integrated facility that sources yarn from

Arvind at Ahmedabad. It has both weaving and processing infrastructure, captive

power supply, steam generation and a wastewater treatment plant. The latter makes it

a zero discharge complex i.e. one that recycles all its wastewater.

In 1986, we looked for textiles that had global demand, high

margins, and high entry level barriers (either of technology,

expertise or set-up costs), and very importantly, low "fashion

volatility". We wanted to focus on fabric that would never go out of

style. Our analysis of potential products threw up denim as the answer. With a

production capacity of 120 million meter per annum, Arvind is currently India‘s

largest and world‘s third largest denim manufacturer.

It sells under the brand names ―ARVIND DENIM‖ and ―BIG MILL DENIM‖ (in

Europe). In India Arvind commands a market share of approximately 64% which is

five times that of the next largest player. Our denim is used to make India‘s leading

jeans brands – Flying Machine, Killer, Levi‘s, Numero Uno, Pepe, Texas jeans, UFO

and Wrangler. All the leading local denim manufacturers use ―Made from original

Arvind denim‖ as an indicator of high quality and consistency.

Arvind also exports denim to over sixty-six countries worldwide. Denim exports

constitute of approximately 50% of the turnover.

Today Arvind is making yet another foray in the manufacture of the

finest quality Cotton Knits in the world. This new venture features a

technical collaboration with Alamac Knits Inc, USA to manufacture

high value and high-fashion knits. With an investment of US $50

million, the plant will produce fabric in both tubular and open widths. The product

range aims to offer widest choice in both tubular and open widths in single (Jersey,

Pique, Textures, Pointless, Fleece, French Terry, Jacquards in solids, feeds and

automatics) and double (Interlocks, Needle-outs, ottomans, Pointless, Textures,

Reversible, jacquards, Ribs in solids, feeds and automatics, Collars: Plains and

Jacquards) knits. It will manufacture a knits range from casuals to formal, active wear

to sleepwear, for diverse use in men's, women's and children's clothing. Arvind‘s large

color and fabric library, stocking samples and a well equipped fabric resource centre

facilitates customers to access fabric that will enhance their lifestyles.

• Arvind’s Own Brands

• Licensed Brands

22

Arvind Customers

Portfolio of Arvindlimited.

Portfolio Percentage%

Denim 26%

Shirting 11%

Garment 16%

Brand/Retail 21%

Others 26%

Percentage% Denim

26% 26%

Percentage% Shirting

11% 11%

Percentage% Garment

16% 16%

Percentage% Brand/Retail

21% 21%

Percentage% Others

26% 26%

Arvind Portfolio

Milestones Achieved

1931

Arvind Limited was set up by Lalbhai Brothers in the “Manchester of East”.

1934

With sales reaching Rs. 45.76 lakhs and a profit of almost Rs. 3 lakhs, Arvind

establishes itself amongst the foremost textile units in the country.

1985

First Meter of Denim churned out.

1986

An uninterrupted record of not missing out on paying dividend to its

shareholders.

An established leader in fine & superfine cotton fabrics for Indian market.

Renovation: First company to bring globally accepted fabrics Denim, yarn dyed

shirting fabrics & wrinkle free gabardines to India.

1987

The largest zero discharge green effluent treatment plant in India.

Commitment to greener world.

First company to bring International shirt brand ―Arrow‖ to India

First company to start dedicated ―retail‖ outlets for Arrow brand

Awarded various awards for Highest exports and ISO.

1989

Largest denim & shirting in South Asia.

3rd Largest denim capacity in the world.

1990

Introduction of Premium Shirting‘s Division.

1993

Office set up in New York, London & Hong Kong.

1994

Arvind ventures into Brands—Flying Machine acquired…..

BEGINNING OF AN ERA

1995

LEE commenced production. Introduction of Ruf & Tuf, ready to stitch denim.

1997

Commission of State-of-the-art manufacturing unit at Santej (Ahmadabad).

First Indian company to detribalize the cotton textile business from cotton fields

to apparel retailing.

1997-

1998

First company to introduce ERP SAP business solutions.

2002

Arvind` does a unique financial restructuring.

2004

Relocation of Mauritius Plant at the end of quota regime.

2008

Company launches 'Mega mart', now India's largest value apparel-retail chain

Largest portfolio of International brands: Lee, Wrangler, Nautical, Jan sport,

Kipling, Tommy, Arrow, US Polo, Izard, Pierre Cardin, Palm Beach, Cherokee,

hart Schaffer Marx.

Financial Scenario

Arvindlimited is acclaimed in the Indian corporate field for its financial skills. Being

the phase of rapid growth or downturn the company has demonstrated swift, sharp and

robust financial acumen to navigate the company through different phases of

economic cycles. Arvind Mills was the first Textile Company from India to issue

GDRS in the year 1992-93. Highly complex financial restructuring exercise involving

more than 80 domestic and international tenders, who the company implemented

following the major downturn in the business cycle during year 2000-2002, is

considered to be the benchmark for the Indian corporate. Arvindlimited has been

making judicious choice of fund leasing avenues in the domestic as well as

international markets so as to utilis very efficient capital structure, which is in the tune

with operating risks and enhances the shareholder‘s value.

The company has laid down the risk management policy to manage the financial risks

emerging out of currency and interest rate. It runs an active treasury desk so as to

make use of modern hedging tools available to manage financial risks.

Arvind Mills was the first Textile Company in India to implement ERP, SAP as back

as in the year 1997-98. The company follows best accounting practices to prepare its

financial statements as envisaged in the Indian and international accounting standards.

SHAREHODING PATTERN OF ARVINDlimited.

Particulars NO.OF SHARES % OF TOTAL

Promoters 76908767 35.24%

Institution 42340700 19.40%

General public 98980382 45.36%

Grand total 218229849 100%

Graph

From old to New

Arvindlimited is the flagship company of the Lalbhai Group and one of India‘s largest

integrated textile manufacturers and branded apparel retailers. The re-branding

exercise comes in the wake of Arvindlimited transforming itself from a pure fabric

company to a diversified business group focusing on branded apparel and retail.

Initially, when the company was set up as Arvind Millslimited, it was simply about

fabric. But gradually, it has spread its tentacles into retail and branded apparel, which

today contributes the maximum to the company‘s growth. Seven years ago, with

everything else constant, the logo was changed. In all, since Arvind Mills was set up

in 1931, this is the first extensive re-branding exercise it has taken up.

Sharp, but well rounded, the forms of the logotype

represent an organization that is integrated and works

across the value chain from stylish fabrics to iconic brands.

With an element of classicism, the logo symbolizes an

organization that has a rich heritage, while remaining

contemporary through changing times. The burgundy red

denotes maturity, its rich tones carrying a sense of depth

and more than a hint of passion.

No particular font has been used for the logo – it is hand drawn and, therefore, an

exclusively crafted logo.

Highlighting the significance of the change in identity, Sanjay Lalbhai, chairman and

managing director, Arvindlimited, says, ―Over eight decades, we have changed the

face of fashion by evolving constantly. As we get ready to address wider opportunities

to create wealth for our stakeholders, we have evolved new ways of thinking and a

new direction. The new identity reflects the shift in the corporate identity from a large

integrated textile player to a lifestyle solutions company and the name of the company

reflects the same trust but new opportunities.‖

Arvind Mills - old logo

Arvindlimited - new logo

Arvindlimited has licensing relationships with international brands such as Arrow,

Gant, Cherokee, USPA, Hart Schaffner Marx, Sansabelt, Pierre Cardin and a joint

venture with VF Corporation, which covers Lee, Wrangler, Jansport, Nautica, Kipling

and Tommy Hilfiger. In addition, Arvind owns a number of successful Indian brands

such as Flying Machine, Newport, Excalibur and Ruf and Tuf. It also owns the retail

chain, Mega mart, which has 83 outlets in 30 towns. Recently, Arvindlimited opened

a 40,000 square foot Mega mart outlet in Chennai.

Arvind Mills changes name, focus, strategy

Textile major Arvind Mills which has been recently going through a bad patch owing

to rising rupee, reducing exports and falling margins is undertaking a business

transformation in a bid to become a billion dollar company.

The company has firstly changed its name from ‗Arvind Millslimited‘ to

‗Arvindlimited‘ with a new logo and identity to reflect a company which is diversified

with focus on branded apparel and retail. The promoters will increase their stake from

34% to 47% and infuse Rs.188 crore capital into the company.

Also, half of the Rs.1400 crore debts which Arvindlimited has would be repaid by

selling off land at Ahmedabad and Bangalore thus positively affecting the company‘s

profitability.

Arvind is now giving more focus to brands and retail which until now contributes

19% of total revenue. It will also move to become an integrated textile player by

producing fabric as well as retailing it. With a combination of its own as well as

licensed brands, Arvind aims to become the largest apparel brand in India with focus

on Tier II and III cities.

Major emphasis would be on the value store format ‗Megamart‘ which is targeted to

achieve Rs.1000 crore sales in 3 years. Other than that Arvind plans to setup 250

small format and 30 large format stores by 2012.The strategy may work out to be

rewarding for the company as it has a good portfolio of domestic and international,

and has been an established national player. The move would also help it to ward off

any risk it faces from the recession in export markets.

Concept of Working Capital

A company invests its funds for long term purposes and short term operations. That

portion of a company‘s capital, which is required for minimum stock of raw material

to maintain continuity in production, minimum stock of finished goods to fulfill future

demand, payment of wages and salaries of labourers and employees is called Working

Capital. In other words, working capital is that part of the firm‘s capital which is

required for financing short term or current assets such as debtors, inventories,

marketable securities and cash.

The word working capital comprises of two words ‗working‘ and ‗capital‘. In trade

and industry, the word ‗working‘ with reference to capital means circulation of

capital from one form to another during day-to-day operations of the business whereas

the word ‗capital‘ refers to the monetary values of all the assets (tangible and

intangible) of the business.

There are numerous concepts of working capital as given by various accountants,

financial experts, entrepreneurs and economists. Important among them are –

Balance Sheet or Traditional Concept

Operating Cycle Concept

Forms of Working Capital

Working capital is the amount of funds required to cover the cost of operating the

enterprise. In other words, working capital may be defined as excess of current assets

over current liabilities. It may be classified in two ways i.e. (i) on the basis of balance

sheet concept and (ii) on the basis of time. These are illustrated by the following chart.

Types of working capital

On the basis of B/S concept

Gross Working Capital

Net Working Capital

On the basis of time

Permanent or Regular

Working Capital

Variable or Temporary

Working Capital

Seasonal Working Capital

Specific Working Capital

On the basis of B/S concept

According to this concept, working capital is calculated on the basis of the balance

sheet prepared at a specific date. It is further classified it two forms- gross and net

working capital.

o Gross Working Capital – The gross working capital refers to the firm‘s investment

in current assets. The sum of current assets is a quantitative aspect of working

capital which emphasizes more on quantity than its qualities.

o Net Working Capital - Net working capital is the difference between the current

assets and the current liabilities or the excess of total current assets over total

current liabilities.

Net working capital may also be defined as, that part of a firm’s current assets

which is financed with long term funds. The net working capital may either be

positive or negative. When current assets exceed current liabilities, working capital

is positive and negative when current liabilities exceed current assets.

On the basis of Time

Working capital is the amount required in different forms at successive stages of

operation during the net operating cycle period of an enterprise. The duration or time

required to complete the sequence of events right from purchase of raw materials/goods

for cash to the realization of sales in cash is called the operating cycle or working

capital cycle. On the basis of time working capital may be classified as (i) Permanent or

regular working capital; and (ii) Variable or temporary working capital.

o Permanent or regular working capital – It represents the irreducible minimum

amount that is permanently blocked in the business and cannot be converted into

cash in the normal course of business. It has following characteristics :

a. It keeps on changing its form from one current asset to another

b. The size of working capital grows with the growth of the business

c. As long as the firm is a going concern, this part of working capital

cannot substantially be reduced.

o Variable or temporary working capital – Any amount over and above the

permanent working capital is variable or temporary working capital. It fluctuates

as per the change in the production and sale activities. It can further be classified

in following two forms:

a. Seasonal working capital – The capital required to meet the seasonal

demands of the enterprise is called seasonal working capital. It is of

short-term nature and thus has to be financed from short-term sources

like bank loan etc.

b.Specific working capital – Specific working capital is that part of the

working capital which is required to meet unforeseen contingencies like

slump, strike, flood, war etc.

Components of Working Capital

Working capital refers to the metric valuation of the current assets and the current

liabilities. These two are the basic components of working capital.

CURRENT ASSETS ARE:

(1) Inventories

(2) Sundry Debtors

(3) Bills Receivables

(4) Cash & Bank Balances

(5) Short term investment

(6) Advances such as advances for purchase of raw materials,

component and consumable stores, prepaid expenses etc.

CURRENT LIABILITIES ARE:

(1) Sundry Creditors

(2) Bills Payable

(3) Creditors for outstanding expenses

(4) Provision for tax

(5) Other provision against the liabilities payable within a period

of 12 months

Sources of Working Capital

Funds available for a period of one year or less are called short-term finance. In India

short-term funds are used to finance working capital. Two most significant forms of

working capital are: trade credit, bank borrowing.

The use of trade credit has been increasing over the years in India. Trade credit as a

ratio of current assets is about 40 percent. It is indicated by the Reserve Bank of India

that trade credit has grown faster than the growth in sales.

Bank borrowing is the next important source of working capital finance. Before

seventies, bank credit was liberally available to firms. It became a resource after

eighties because of the change in the government policy.

Another form of short-term working capital finance which has recently developed in

India is Commercial Paper.

Trade credit

Trade credit refers to the credit that a customer gets from supplier of goods in the

normal course of business. In practice, the buying firms do not have to pay cash

immediately for the purchase made. It is a major source of financing for firms. In

India, it contributes to about one-third of the short-term financing.

Trade credit is mostly an informal arrangement, and is granted on an open account

basis. Once the trade links have been established between the buyer and seller, they

have each other‘s mutual confidence and trade credit becomes a routine activity. Open

account trade credit appears as sundry creditors on the buyer‘s balance sheet. Trade

credit may also take the form of bills payable. A bill is formal acknowledgement of an

obligation to repay the outstanding amount.

It also involves some credit terms. These credit terms refer t the conditions under

which the supplier sells on credit to the buyer, and the buyer is required to repay the

credit. These conditions include the due date and the cash discount (if any) given for

prompt payment.

Bank Finance

Banks are the main institutional sources of working capital finance in India. A bank

considers a firm‘s sales and production plans and the desirable levels of current assets

in determining its working capital requirements. The amount approved by the bank for

the firm‘s working capital is called credit limit. Credit limit is the maximum funds

which a firm can obtain from the banking system. In the case of firms with seasonal

businesses, banks may fix separate limits for the peak level credit requirement and

normal non-peak level credit requirement indicating the periods during which the

separate limits will be utilized by the borrower.

A firm can draw funds from its bank within the maximum credit limit sanctioned. It can

draw funds in the following forms: (a) overdraft, (b) cash credit, (c) bills discounting,

and (d) working capital loan.

Overdraft Under the overdraft facility the borrower is allowed to withdraw funds in

excess of the balance in his current account upto a certain specified limit during a

stipulated period. Interest is charged on daily balances on the amount actually

withdrawn subject to some minimum charges.

Cash Credit Under the cash credit facility, a borrower is allowed to withdraw funds

from the bank upto the sanctioned credit limit against the security of current assets. He

is not required to borrow the entire sanctioned credit at once, rather, he can draw

periodically to the extent of his requirements and repay by depositing surplus funds in

his cash credit account. Interest is payable on the amount actually utilized. It is more

flexible from borrower‘s point of view.

Bills Discounting Under the purchase or discounting of bills, a borrower can obtain

credit from the bank against its bills. The bank purchases or discounts the bill and

provides the amount within the overdraft limit. Before purchasing or discounting, bank

satisfies itself as to the creditworthiness of the borrower. When a bill is discounted, the

borrower is paid the discounted amount of bill viz. full amount of bill minus discount

charged by the bank. The bank collects the full amount on maturity.

Letter of Credit Suppliers, particularly foreign suppliers, insist that the buyer should

ensure that his bank will make the payment if he fails to meet its obligation. This is

ensured through a letter of credit (L/C) arrangement. A bank opens an L/C in favour of

a customer to facilitate his purchase of goods. This arrangement passes the risk of the

supplier to the bank. Bank will make payment to the supplier on behalf of the customer

only when he fails to meet the obligation.

Working Capital Loan a borrower may sometimes require ad hoc or temporary

accommodation in excess of sanctioned credit limit to meet unforeseen contingencies.

Banks provide such accommodation through a demand loan account or a separate non-

operable cash credit account. The borrower is required to pay a higher rate of interest on

such additional credit.

Commercial paper

Commercial paper (CP) is an important money market instrument in advanced countries

like USA to raise short-term funds. In India, the Reserve Bank of India (RBI)

introduced the commercial paper scheme in the Indian money market in 1989.

Commercial paper is a form of unsecured promissory note issued by firms to raise

short-term funds. The buyers of commercial paper include banks, insurance companies,

unit trusts and firms with surplus funds to invest or a short period with minimum of

risk. Given this investment objective of the investors in the commercial paper market,

there would exist demand for commercial papers of highly creditworthy companies.

In India, the issue of commercial paper is being regulated by RBI. Those companies are

allowed to issue commercial papers which have a net worth of Rs.10 crore, maximum

permissible bank finance of not less than Rs.25 crore, and are listed on the stock

exchange. A company can issue CPs amounting to 75percent of the permitted bank

credit.In addition to the above mentioned sources, accrued expenses and deferred

income are other spontaneous sources of short-term financing. Accrued Expenses

represent a liability that a firm has to pay for the services which it has already received.

Deferred Income represents funds received by the firm for goods and services which it

has agreed to supply in future.

Objective of Working Capital Management

a. To minimize the amount of capital employed in financing the current assets.

This will also lead to improvement in the ―Return on Capital Employed‖.

b. To manage the current assets in such a way that the marginal return on

investment in these assets is not less then the cost of capital acquired to finance

them. This will ensures the maximization of the value of the business units.

c. To maintain the proper balance between the amount current assets and liabilities

in such a way that the firm is always able to meet its financial obligation

whenever due.

d. To ensure the smooth working of the units without any production held-ups due

to paucity of funds.

e. To ensure easy and cheapest availability of resources at the time of growth and

expansion activities.

Determinants of Working Capital

The following factors should be considered carefully while determining the amount of

working capital required:

1. Nature of business – The amount of working capital is basically related to the nature

and the volume of the business. Firms engaged in public utility services require

moderate amount of working capital whereas firms producing luxury goods require

large amount of working capital.

2. Size of business – Size is also a determining factor in estimating working capital

requirements. The size may be measured either in terms of scale of operations or in terms

of assets or sales.

3. Changes in technology – Changes in technology may lead to improvement in

processing of raw material, saving in wastage, higher productivity and more speedy

production. All these improvements enable the firm to reduce the working capital

requirements.

4. Length of operating cycle – The amount of working capital depends upon the length

or duration of operating cycle. The speed with which the operating cycle is completed,

determines the amount of working capital. The larger is the period, the more is the

investment in inventories and wage bills.

5. Terms of purchase and sale – A firm buying raw materials and other services on

credit and selling on cash basis will require less investment in current assets as compared

to a firm which purchases on cash basis and sells on credit. The period of credit and the

efficiency in collection of debts also influence the amount of working capital required.

The terms and conditions of purchase and sale are generally governed by the prevailing

trade practices and by changing economic condition.

6. Inventory - Some concerns are force to hold large inventories in terms of raw

materials or finished goods due to the reason of seasonal nature of availability,

long distances, scarcity etc, in such case the working capital requires is more.

7. Business cycles – Business cycle refers to the alternate expansion and contraction

in general business activities. In a period of boom when the business is

prosperous, there is need for larger amount of working capital due to increase in

sales and rise in prices of raw materials. The contrary happens in the period of

depression.

8. Profit margin – A high rate of profit margin due to quality products or good

marketing management or monopoly power in the market, reduces the working

capital requirements of the firm, as profit earned in cash is a source of working

capital. On the contrary, firms earning low margin of profits due to competition or

mismanagement need larger amount of working capital.

9. Credit policy – A firm following liberal credit policy and thus granting credit

facilities to all customers without evaluating the credit worthiness will require

more working capital to carry book debts. On the contrary, a firm that adopts strict

credit policy and grants facilities to customers with high credit standing will

require less amount of working capital as funds tied-up in receivables will be

released promptly for further uses.

Significance of adequate Working Capital

Adequate working capital is a source of energy to any business organization. It provides

the following advantages to a business enterprise:

1. Adequate working capital enables a firm to make prompt payments to the suppliers

and thus it can also avail the advantage of cash discount by paying cash for the

purchase of raw material.

2. If a firm has adequate working capital, it can declare and distribute enough dividends

when there are sufficient profits. This creates satisfaction among the shareholders.

3. In business, promptness to third parties creates goodwill and increases the debt

capacity of the concerned firm. This in turn ensures uninterrupted flow of production.

4. A firm having adequate working capital and liquid assets can arrange loans from the

banks on easy and favourable terms, as it provides a good security for the unsecured

loans.

5. Adequate working capital has psychological effect on the directors and executives of

the firm as it motivates them to work vigorously. It creates an environment of

security, confidence, high morale and increases overall efficiency in the business.

6. Adequate working capital increases the productivity or efficiency of fixed assets in the

business.

Effects of excessive Working Capital

Excess or redundant working capital refers to the idle funds which do not earn any profits

for the firm. ―Inadequate working capital is disastrous; whereas redundant working

capital is a criminal waste‖. A firm may suffer following disadvantages from excess

working capital:

1. It may lead to unnecessary purchasing and accumulation of inventories causing more

chances of mishandling of inventories, theft, waste, losses, etc.

2.Excessive working capital implies excessive debtors and defective credit policies

causing higher incidence of bad debts that ultimately affects profits of the firm.

3.It indicates inefficient management of the firm. It shows that the management is not

interested in effectively utilizing the resources and encouraging economy.

4.Excessive working capital remains idle and earns no profits for the firm, even though

interest has to be paid on it. This reduces the amount of profits.

5.It is an indicator of inefficient management. Hence, shareholders believe that they are

not getting proper return on their investments. This results in lowering the value of

shares causing discontentment among shareholders.

6.It promotes profits of speculative nature by stock-piling. It results in liberal dividend

policy, but the management has to face difficulties in future when there are no

speculative profits.

( Rs. in Crore )

Particulers As at

31.03.09

As at

31.03.08

As at

31.03.07

As at

31.03.06

SOURCES OF FUND

Share holder fund

Share capital 260.10 273.30 255.58 265.48

Reserves & surplus 940.47 1197.05 1113.45 1266.47

Total 1200.57 1470.35 1369.03 1531.95

Secured Loans 1920.90 1774.94 1772.74 1688.38

Unsecured Loans 103.04 97.52 161.57 152.99

Deferred Tax Liability 12.82 12.82 12.82 12.82

TOTAL 3237.33 3355.63 3334.16 3386.14

APPLICATION OF FUND

Fixed Assets

Gross Block 3056.80 2942.99 2817.21 2192.24

Less- Depreciation (1014.51) (906.78) (772.32) (882.64)

Net Block 2042.29 2036.21 2044.89 1309.60

Capital Work in Progress 81.58 116.14 71.45 79.59

Investment 100.06 104.99 48.05 348.10 FOREIGN CURRENCY MONETARY ITEM

TRANSLATION

DIFFERENCE ACCOUNT

6.77 0.00 0.00

0.00

Current assets, Loan & Advance

Inventories 581.47 575.34 645.01 479.26

Sundry Debtors 350.84 261.77 204.85 368.28

Cash & Bank Balance 26.83 16.32 22.31 9.59

Other Current Assets 54.90 73.26 54.95 38.68

Loan & Advance 578.47 544.45 663.79 1041.44

Total 1592.51 1471.14 1590.91 1937.25

Less-Current Liability & Provision

Liabilities 463.29 360.54 408.99 243.31

Provisions 132.66 21.81 12.15 45.09

Total 595.95 382.35 421.14 288.40

Net Working Capital 996.56 1088.80

1169.77 1648.85

Miscellaneous Expenditure (to the

extent not written off)

10.07 9.50 0.0 0.00

TOTAL 3237.33 3355.63 3334.16 3386.14

( Rs. in Crore )

Particular 2008-09 2007-08 2006-07 2005-06 2004-05

INCOME

Sales & Operating Income 2344.99 2290.33 1847.99 1592.00 1654.91

Other Income 51.91 15.91 13.17 22.52 4.99

Total 2396.90 2306.24 1861.16 1614.52 1659.90

EXPENSES

Raw Materials Consumed 695.83 611.26 571.93 500.24 612.24

Purchase of Finished Goods 257.90 305.54 36.97 4.45 7.63

Employee Emoluments 244.80 230.39 204.33 135.74 123.09

Others 924.47 861.04 780.24 534.14 542.92

Interest & finance cost 222.13 131.40 150.26 138.64 108.92

Depreciation 122.05 136.64 143.36 155.10 149.07

Exceptional items (net) 11.53 9.31 0.00 0.00 0.00

Decrease/(Increase) in Stocks (34.86) (9.49) (53.64) 9.82 (12.76)

Total 2443.86 2276.09 1833.45 1478.14 1530.60

Profit before tax for the year (46.96) 30.15 27.71 136.38 129.30

Less- Current tax 0.00 3.10 0.00 11.40 1.95

Less-Deferred Tax 0.00 0.00 0.00 8.27 0.00

Less –Fringe benefit tax 1.86 2.25 11.62 0.95 0.00

Add: MAT Credit Entitlement 0.00 (3.10) (11.61) (11.40) 0.00

Profit For the year (48.82) 27.90 0.00 127.16 127.35

Less- Prior Period Income/(Expense) 0.95 (0.54) 0.00 0.00 0.00

Profit before (47.87) 27.36 25.27 0.00 0.00

Extra ordinary items (net) 0.00 0.00 94.29 0.00 0.00

Profit after Extra ordinary items (47.87) 27.36 119.56 0.00 0.00

Balance as per last year‟s balance sheet 434.92 425.00 321.17 232.74 127.77

Interim Dividend on Preference Shares (1.68) (2.48) (3.14) (3.80) (4.09)

Tax on Interim Dividend (0.29) (0.42) (0.44) (0.53) (0.53)

Proposed dividend on Equity Shares 0.00 0.00 0.00 (20.94) (19.54)

Tax proposed dividend 0.00 0.00 0.00 (2.94) (2.74)

Additional dividend on equity share 0.00 0.00 0.00 (1.40) 0.00

Tax on additional dividend (80.10) 0.00 0.00 (0.20) 0.00

Provision for leave encashment (9.58) (1.34) 0.00 0.00 0.00

Transferred to capital redemption reserves (13.20) (13.20) (9.90) (9.92) (3.48)

Transferred to debenture redemption

reserve

0.15 0.00 (2.25) 1.00 8.00

Balance Carried to Balance Sheet 282.34 434.92 425.00 321.17 232.74

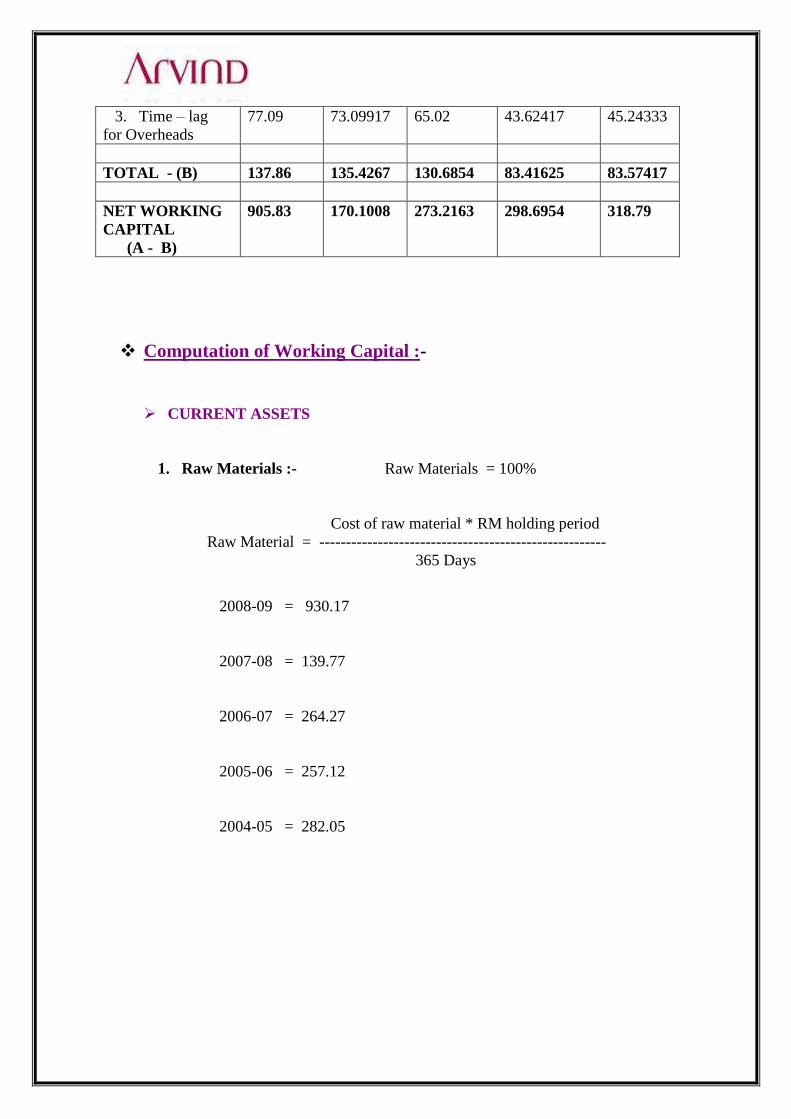

( Rs. in Crore ) (Actual working capital)

CURRENT ASSETS

PARTICULAR 2009 2008 2007 2006 2005

Raw Materials 930.17 139.77 264.27 257.12 282.05

Work in progress 202.19 147.36 140.34 112.91 87.73

Finished goods 136.51 243.23 198.42 71.91 103.54

Sundry Debtors 350.84 261.77 204.85 368.28 319.11

Cash &Bank

Balance

26.83 89.58 77.26 48.27 51.10

Total 1646.54 881.71 885.14 858.49 843.53

CURRENT LIABILITIES

PARTICULAR 2009 2008 2007 2006 2005

Sundry Creditors 344.46 360.54 408.99 243.31 238.76

Wages 212.64 207.12 174.50 112.54 101.83

Overheads 925.15 877.19 780.24 534.14 542.92

Total 1482.25

1444.85

1363.73 898.99 883.51

Net WC 164.29 (563.14) (478.59) (40.50) (39.98)

Time period of working capital

Raw Materials = 100%

Work in process = 1 month

Finish goods =1 month

Debtors = 2 month

Creditors = 1.5 month

Wages = 1 month

Overheads = 1 month

NET WORKING CAPITAL:-

Net Working Capital =Total Current Assets – Total Current

Liabilities

2009

= 1646.54-1482.25

= 164.29

2008

= 881.71-1444.85

= (563.14)

2007

= 885.14 - 1363.73

= (478.59)

2006

= 858.49 – 898.99

= (40.50)

2005

= 843.53 – 883.51

= (39.98)

WORKING CAPITAL OF THE ARVIND LTD.

(Actual working capital) (Rs.in crore)

WORKING

CAPITAL

2008-09 20007-08 2006-07 2005-06 2004-05

CURRENT

ASSETS

1. Raw

Materials

930.17 139.77 264.27 257.12 282.05

2. Work in

process

16.84 12.28 11.695 9.409167 7.310833

3. Finished

goods 11.38 20.26916 16.535 5.9325 8.628333

4. Debtors 58.47 43.62833 34.141167 61.38 53.185

5. Cash & Bank

Balance 26.83 89.58 77.26 48.27 51.19

TOTAL - (A) 1043.69 305.5275 403.9017 382.1117 4023642

CURRENT

LIABILITIES

1. Time – lag

for Creditors

43.05 45.0675 51.12375 30.41375 29.845

2. Time – lag

for Wages

17.72 17.26 14.54167 9.378333 8.485833

3. Time – lag

for Overheads

77.09 73.09917 65.02 43.62417 45.24333

TOTAL - (B) 137.86 135.4267 130.6854 83.41625 83.57417

NET WORKING

CAPITAL

(A - B)

905.83 170.1008 273.2163 298.6954 318.79

Computation of Working Capital :-

CURRENT ASSETS

1. Raw Materials :- Raw Materials = 100%

Cost of raw material * RM holding period

Raw Material = ------------------------------------------------------

365 Days

2008-09 = 930.17

2007-08 = 139.77

2006-07 = 264.27

2005-06 = 257.12

2004-05 = 282.05

2. Work in process :- (Work in process = 1 month )

WIP cost * WIP holding period

WIP = --------------------------------------------

365 days/ 12 months

202.19 * 1 months

2008-09 = -----------------------------

12 months

2008-09 = 16.84

147.36 * 1 months

2007-08 = -----------------------------

12 months

007-08 = 12.28

140.34 * 1 months

2006-07 = -----------------------------

12 months

2006-07 = 11.69

112.91 * 1 months

2005-06 = -----------------------------

12 months

2005-06 = 9.41

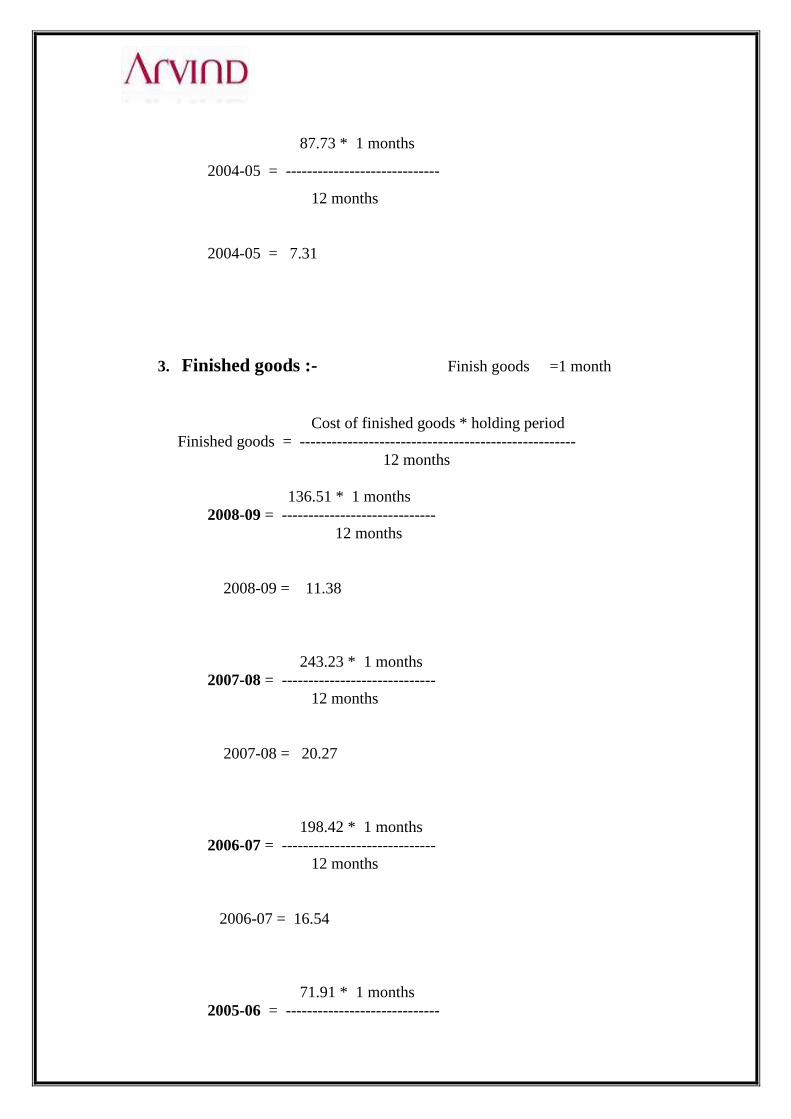

87.73 * 1 months

2004-05 = -----------------------------

12 months

2004-05 = 7.31

3. Finished goods :- Finish goods =1 month

Cost of finished goods * holding period

Finished goods = ----------------------------------------------------

12 months

136.51 * 1 months

2008-09 = -----------------------------

12 months

2008-09 = 11.38

243.23 * 1 months

2007-08 = -----------------------------

12 months

2007-08 = 20.27

198.42 * 1 months

2006-07 = -----------------------------

12 months

2006-07 = 16.54

71.91 * 1 months

2005-06 = -----------------------------

12 months

2005-06 = 5.93

103.54 * 1 months

2004-05 = -----------------------------

12 months

2004-05 = 8.63

4. Sundry Debtors :- Debtors = 2 month

Credit sales * debtors collection period

Sundry Debtors = -----------------------------------------------------

12 months

350.84 * 2 months

2008-09 = -----------------------------

12 months

2008-09 = 58.47

261.77 * 2 months

2007-08 = -----------------------------

12 months

2007-08 = 43.63

204.85 * 2 months

2006-07 = -----------------------------

12 months

2006-07 = 34.14

368.28 * 2 months

2005-06 = -----------------------------

12 months

2005-06 = 61.38

319.11 * 2 months

2004-05 = -----------------------------

12 months

2004-05 = 53.19

Current Liability :-

1. Sundry Creditors :- (Creditors = 1.5 month)

Credit purchase * credit period allowed by creditors

Sundry Creditors = ------------------------------------------------------------------

12 Months

344.46 * 1.5 months

2008-09 = -----------------------------

12 months

2008-09 = 43.05

360.54 * 1.5 months

2007-08 = -----------------------------

12 months

2007-08 = 45.07

408.99 * 1.5 months

2006-07 = -----------------------------

12 months

2006-07 = 51.12

243.31 * 1.5 months

2005-06 = -----------------------------

12 months

2005-06 = 30.41

238.76 * 1.5 months

2004-05 = -----------------------------

12 months

2004-05 = 29.85

2. Direct Wages :- Wages = 1 month

Cost of direct wages * payment period

DW = ----------------------------------------------------

12 months

212.64 * 1 months

2008-09 = -----------------------------

12 months

2008-09 = 17.72

207.12 * 1 months

2007-08 = -----------------------------

12 months

2007-08 = 17.26

174.50 * 1 months

2006-07 = -----------------------------

12 months

2006-07 = 14.54

112.54 * 1 months

2005-06 = -----------------------------

12 months

2005-06 = 9.38

101.83 * 1 months

2004-05 = -----------------------------

12 months

2004-05 = 8.49

3. Overheads :- Overheads = 1 month

Total cost of overheads * avg. time-lag in

payment of overheads

Overheads = ---------------------------------------------------------------

12 Months

925.15 * 1 months

2008-09 = -----------------------------

12 months