Embed Size (px)

Citation preview

www.theinternationaljournal.org > RJSSM : Volume: 07, Number: 05, September 2017 Page 122

A Study on Qualitative Research on Level of Attitude, Satisfaction , Perception of

Customer’s on Service Quality Towards Commercial Bank of Ethiopia (WITH SPECIAL REFERENCE TO ASSOSA, ETHIOPIA)

Dr. A Gajendran Shanthi

& Dambush Negasi Hadush

Associate Professor , Assosa University , Assosa University , Ethiopia ABSTRACT

Measuring customer’slevel of satisfaction is too difficult since it is related to the psychological state of mind. An attempt is made to understand the customer’sattitude and their level of satisfaction on services provided by CBE at Assosa. In addition to this, a brief report is made about the existing services, delivery of services, how far the customers using those services and the reasons if any for their preference towards the particular service provider.The main aim of this study is to analyses the demographical factors,level of attitude and relationship between the customer’sattitude, mind set and level of satisfaction. So that we can improve the mindset of the existing customers and existing services of service providers based on the opinion given by CBE Customers towards the quality and types of services provided the service providers to the reasonable extent or not. The researcher also expects that this article persuade many researchers to do further research in the related area and believes that the identified facts expressed by the researchers through this research article will be more helpful to the CBE and its authorities concerned who govern the service provider to provide good quality service to the customers at Assosa. Key words:Commercial Bank of Ethiopia, Attitude, Level of Satisfaction, Bank CustomersAttitude, Level of Satisfaction, Service Quality. INTRODUCTION

Service quality always create a brand image and it will increase the level of satisfaction among customers , reputation of the business , sales, profitability of any organization in any sector. So it is mandatory to analyze the level of service and its quality. On the other hand, Level of satisfaction depends or it is created because the attitude of the customers. Positive attitude of the customers will be generated based on how far the service provider fulfills the level of expectation of the customer at what extent. More than that how far the people who are working in the institution of service provider responding towards the customers, the way they treat customers, speed in doing work at the work spot, their level of commitment also matters. All these criteria’s from customer as well as service provider point of view will be considered to judge the level of satisfaction. Due to time constraints we are preferring to consider only from customer’s point of view to assess their level of attitude towards the service provider and their service , variables related with service quality , how the customers feel towards the services of service provider, . All those are trying to be assessed by the researchers in this research papers. Framing research questionnaires, collection of data , pilot study , revamping the questionnaire , main data collection , usage of Appropriate statistical tools , results were found and its properly analyzed and suggestion’s and recommendations were given for improvement of the service quality of the service provider called Commercial bank of Ethiopia at Assosa, Ethiopia .

LITERATURE REVIEW

Jinea Akhtar (2011)has briefing that “service quality is one of the success factorswhich always influence the competitiveness of an organization. This study examines the relationship between service quality, satisfaction, and loyalty in the private commercial banks in Bangladesh. The determinants of service quality were categorized into product features, physical aspects, customer

www.theinternationaljournal.org > RJSSM : Volume: 07, Number: 05, September 2017 Page 123

services, and technology and security aspects. It has been proved service quality, satisfaction, and loyalty is strongly and positively related to each other”.

Dr. NarinderKaur (2013)has clear“ TRUST as an implicit or explicit pledge of relational continuity between exchange partners. One of the difficulties here is that “Trust” is closely related to the concept of loyalty and commitment and such, as might be considered to be the desired outcome of relationship building in customer market. The study has shown that the “trust” was very strong in Foreign Sector Banks”.

Rajesh Nair, Ranjith P V, Sumana Bose and CharuShri (2010)tried to find out the Service quality of Banks in Navi Mumbai. It tries to look whether there is gap between customer expectations and perceptions of service offered. One of the most popular models, SERVQUAL was used. It was observed that there were five important factors for service quality analysis which are Tangibles, Reliability, Responsiveness, Assurance and Empathy.

VandanaPareek (2014)has concluded that banking industry had sufficiently undergone rapid changes. The study showed that product attributes, employee Characteristics, customer convenience, bank tangibles, cost of transaction and customer communication were the main factors contributing to customer satisfaction in banks.

Dr. T. Vanniarajan, K. SubbashBabu (2011)initiatesthat the important internal service quality factors are their employees' and customers' orientation, team orientation and employee orientation, learning environment and outcome orientation. The important discriminant service quality factors of banks are customers' orientation and team orientation. They identified that these two factors are significantly and positively influencing the customers' satisfaction and the behavioral intention. Their study conveys the need of conversion of “high tech” strategy to “high-touch” strategy to create customer loyalty in the banking industry. STATEMENT OF THE PROBLEM

At present it is well known fact that almost all the business transactions, even payment system also done through online with the help of internet. Based on present technological development and to fulfill the gap between human needs and their expectations in business, banking services are very much important for the same. Even banking sectors trying to satisfy the obligations of the customers , the banks are not able to satisfy the customers that much. Even it’s too difficult to make customers to get hundred percent satisfactions. Many researchers they already made several attempt in the similar area of research but not about CBE that also especially in Assosa. In addition, still there is a need for us to diagnose the service quality and intensive banking services of CBE in Assosa. That is why the researchers they made a different style of approach and an attempt to find the service quality and attitude of various customers and their level of satisfaction towards CBE. The earlier point is the primary focus on the researcher’s point of view to identify and to reveal the facts to upgrade the service quality standards to excel CBE’s Customer related services. OBJECTIVES OF THE STUDY § To highlight the attitude, level of satisfaction, service quality attributes connects with CBE and its

Service Quality. § To examine the relationship between demographical factors and customer satisfaction

HYPOTHESIS

§ There is no significant difference between Age and attitude related factors § There is no significant difference between various types of customers and their level of

satisfaction toward the services provided by Commercial bank of Ethiopia

www.theinternationaljournal.org > RJSSM : Volume: 07, Number: 05, September 2017 Page 124

§ There is no significant difference between service quality variables and customers level of satisfaction

RESEARCH METHODOLOGY

The data required for this study collected from primary and secondary sources. The primary data are collected by distributing questionnaires to customers of Commercial bank of Ethiopia at Assosa.Questionnaire includes both dependent and independent variables. 5 point Likert’s scale which ranges from strongly agrees to strongly disagree and the same is used to identify the attitude of customer’s who are using the service of Commercial bank of Ethiopia, level of satisfaction of the customers and service quality of Commercial Bank of Ethiopia. The researchers framed and segmented the questionnaires in four different levels such as demographical factors of the customers; attitude of customers which influence them to choose CBE, variables connects with level of satisfaction and service quality. The researcher hopes that it is the first attempt at Assosa to carry this research in banking sector towards CBE. Customers of Commercial bank of Ethiopia were interviewed by the researchers andby his trained interviewers at different CBE branches at Assosa.After the collection of research questionnaire , the questionnaires properly ordered , scrutinized , entered in excel sheet then SPSS software Version 20 used and results were obtained then based on the results it was analyses and interpreted , conclusions were made.

DATA COLLECTION, SURVEY AND SAMPLE SIZE

Customer Satisfaction Survey has been conducted to identify the perceptions of CBE which includes only CBE at various branches of CBE, Assosa from October 2016 to January 2017. The data are also collected from different categories of customer’s at different levels.Frequency distribution analysis, Cross tabulation, paired t-test, one sample test were used to find out the factors related to the customer’sattitude service quality of CBE at Assosa.

Samples selected for the present study covers only the Assosa. Totally, 88 customers of CBE were interviewed and their responses too recoded through structured questionnairesby using simple random sampling and convenience sampling method.

LIMITATIONS OF THE STUDY § The present research study includes only commercial bank of Ethiopia ,Assosa. It excludes other private banks in the same region. § This study includes both literate and illiterate § The research questionnaire distributed and data collected in English and not in vernacular language. If the respondents are illiterate, then the interviewer orally translated the questionnaire in local language and responses were recorded by the interviewer himself by hearing their response. § The time taken to collect data is nearly 4 months and those data collected only in Assosa and not in

other cities. RESULTS, DISCUSSIONS AND FINDINGS

The pilot study were conducted and it was checked the reliability of data collection. One fourth of the samples nearly 22 samples were collected and tested and it was resulted from Crown Batch Alfa value shows 91.9 percent. After the pilot study, the necessary modifications were made in the questionnaire and it was finalized. Finally,with the help SPSS software Version 20, the collected data scrutinized, tabulated and the following results were found and the same was given for understanding of the readers. Primarily the demographical factors of the passengers are given as follows:

www.theinternationaljournal.org > RJSSM : Volume: 07, Number: 05, September 2017 Page 125

Table –1: Demographical factors of the Customers of Commercial Bank of Ethiopia

Segmentation Category Frequency % Valid %

Cumulative %

Age

Below 20 9 10.2 10.2 10.2 21-41 64 72.7* 72.7 83.0 41-60 14 15.9 15.9 98.9 Above 60 1 1.1 1.1 100.0 Total 88 100.0 100.0

Sex Male 65 73.9* 73.9 73.9 Female 23 26.1 26.1 100.0 Total 88 100.0 100.0

Marital Status

Married 42 47.7* 47.7 47.7 Single 41 46.6 46.6 94.3 Others 5 5.7 5.7 100.0 Total 88 100.0 100.0

Customer Status

Student 11 12.5 12.5 12.5 Business person 25 28.4 28.4 40.9 Service personnel 44 50.0* 50.0 90.9 Retired person 2 2.3 2.3 93.2 Self employed 6 6.8 6.8 100.0 Total 88 100.0 100.0

Total Annual Household Income

Less than 100,000 Birr 60 68.2* 68.2 68.2 Less than 200,000 Birr 24 27.3 27.3 95.5 Less than 300,000 Birr 4 4.5 4.5 100.0 Total 88 100.0 100.0

Usage Pattern ( in Years)

Less than 1 year 7 8.0 8.0 8.0 Less than 2 years 7 8.0 8.0 15.9 Less than 3 years 18 20.5 20.5 36.4 More than 3 years 56 63.6* 63.6 100.0 Total 88 100.0 100.0

Source: Primary data - Computed From the above table , it is observed that out of total collected samples , the majority of the respondents i.e. 72.7 % lies between the age group of 21- 41. When we considered the gender, it was found that 73.9 % of respondents are using CBE banking services. 47.7% of married customers, 50% of salaried people, 68.2% of the customers who belongs to the category of income of less than 100,000 Birr, 63.6% of the customers who are using banking services more than 3 years were using CBE’s services more.

Table –2 :Cross tab between Type of customers and their Satisfaction towards the Services

Provided by CBE

Respondents Opinion Types of CBE’s Customers Total

Student Business person

Service personnel

Retired person

Self employed

Satisfaction towards the services provided by CBE, Assosa.

Very poor 0 0 2 0 0 2 Poor 2 2 3 0 1 8 Satisfactory 1 4 6 0 0 11 Good 5 9 16 1 0 31* Very Good 0 9 13 1 4 27 Excellent 3 1 4 0 1 9

Total 11 25 44 2 6 88

www.theinternationaljournal.org > RJSSM : Volume: 07, Number: 05, September 2017 Page 126

Source: Primary data – Computed The above table shows the cross tabulation between the various type of customers and the services offered by CBE at Assosa , from the above table it is found that the majority of the customers of CBE are satisfied with the provided services of CBE (Good – 31%, Very good – 27%, Excellent – 9%). It was proved that majority of the samples taken it for the present study felt that the services provided by CBE is satisfied , good, very good and excellent.

Table –3 :Cross tab between Various Customers of CBE and Level of Supervision by officers at

CBE

Respondents Opinion Types of CBE’s Customers

Total Student Business person

Service personnel

Retired person

Self employed

Level of supervision by officers at CBE, Assosa.

HDS 0 0 2 0 0 2 DS 1 3 6 0 0 10 N 2 6 16 1 5 30 S 5 10 19 1 0 35*

HS 3 6 1 0 1 11* Total 11 25 44 2 6 88

Source: Primary data – Computed HDS – Highly Dis satisfied, DS-Dissatisfied, N- Neutral, S- Satisfied, HS- Highly Satisfied

The above table is the cross tab between the various customers and their opinion towards the

level of supervision by the officers of CBE at Assosa city and it shows customers in which extent they are satisfied with the level of supervision from officers that means the people who are assigned the task of managing customers and who are authorized to manage the branch and their transactions, customer related service. Regarding the same it is observed from the computed results through primary data is 35% of customers are satisfied, 11% of people are highly satisfied with the level of supervision from officers of CBE at Assosa.

Table –4 :Cross tab between Age and Level of Satisfaction towards the Services provided by

CBE

Respondents opinion Age

Total Below 20

21-41

41-60

Above 60

Level of satisfaction towards services provided by CBE

Very poor 0 2 0 0 2 Poor 0 8 0 0 8

Satisfactory 1 6 4 0 11 Good 4 20 7 0 31*

Very Good 3 20 3 1 27 Excellent 1 8 0 0 9

Total 9 64 14 1 88 Source: Primary data - Computed

The cross tab reveals that 31% of customers felt that their level of satisfaction towards the services provided at CBE is good. On the other hand 27% customers feels the level of satisfaction is very good about the services of CBE. And 9% customers felt that the services provided by CBE and at the same time their level of satisfaction is Excellent.

www.theinternationaljournal.org > RJSSM : Volume: 07, Number: 05, September 2017 Page 127

Table –5 :Cross tab between Installation of ATM Machines at near to CBE and Various Customers

Respondents Opinion

Criteria to Measure Level of Satisfaction

Types of CBE’s Customers Total Student Business

person service

personnel Retired person

Self employed

Installation of ATM Machines at near to CBE

HDS 0 0 3 0 0 3 DS 1 5 6 0 3 15 N 0 4 5 2 0 11 S 7 13 22 0 1 43*

HS 3 3 8 0 2 16 Total 11 25 44 2 6 88

Source: Primary data – Computed HDS – Highly Dis satisfied, DS-Dissatisfied, N- Neutral, S- Satisfied, HS- Highly Satisfied

The above table shows that 43% of respondents are satisfied and 16 % of the respondents are highly satisfied with the installation of ATM Machines which are established near to CBE. The advantage of this facility will lead to reduce too much crowd in CBE.It will make the CBE customers to have consistent usage towards ATM services ifthey have it near to bank.

Table –6:Cross tab between Age and Respondents opinion towards Safety measures, fire

extinguishers, security persons at CBE

Respondents Opinion Criteria to Measure Level of Satisfaction

Age Total Below

20 21-41

41-60

Above 60

Safety measures at bank, fire extinguishers, security persons

HDS 1 7 0 0 8 DS 2 6 2 0 10 N 0 19 3 0 22 S 6 21 9 1 37*

HS 0 11 0 0 11 Total 9 64 14 1 88

Source: Primary data - Computed HDS – Highly Dis satisfied , DS-Dissatisfied , N- Neutral , S- Satisfied , HS- Highly Satisfied

In addition to the opinion of customers, the above table which represents the views of

customers and it disclose the fact that 37% and 11% of CBE customers are satisfied and highly satisfied with the performance of safety measures, fire extinguisher installation and security persons of CBE.

Table – 7 : Cross Tab between Commercial Bank of Ethiopia’s Service Charge for Providing

Service and Various customers’ opinion

Respondents Opinion

Criteria to Measure Level of Satisfaction

Types of CBE’s Customers Total Student Business

person Service

personnel Retired person

Self employed

CBE’s Service Charge for Providing its Customer Service

HDS 2 1 0 0 0 3 DS 4 10 12 0 3 29 N 0 4 9 0 0 13 S 2 9 17 2 1 31*

HS 3 1 6 0 2 12 Total 11 25 44 2 6 88

Source: Primary data - Computed

www.theinternationaljournal.org > RJSSM : Volume: 07, Number: 05, September 2017 Page 128

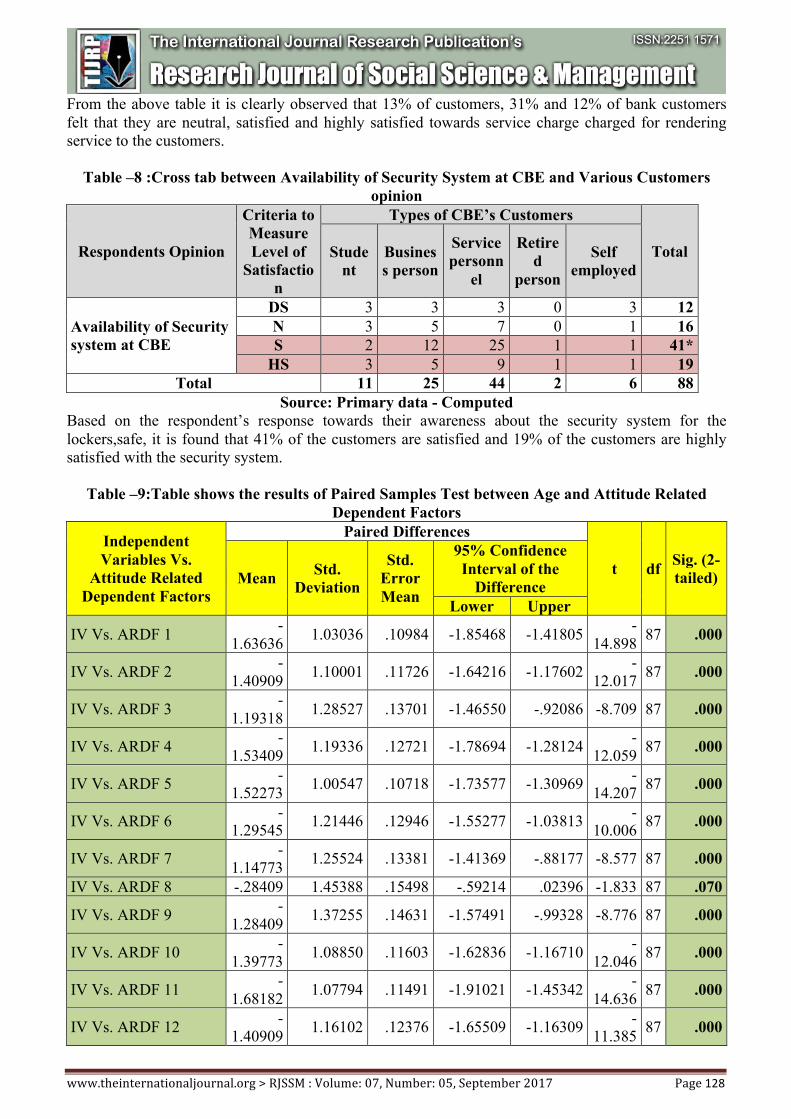

From the above table it is clearly observed that 13% of customers, 31% and 12% of bank customers felt that they are neutral, satisfied and highly satisfied towards service charge charged for rendering service to the customers.

Table –8 :Cross tab between Availability of Security System at CBE and Various Customers

opinion

Respondents Opinion

Criteria to Measure Level of

Satisfaction

Types of CBE’s Customers

Total Student

Business person

Service personn

el

Retired

person

Self employed

Availability of Security system at CBE

DS 3 3 3 0 3 12 N 3 5 7 0 1 16 S 2 12 25 1 1 41*

HS 3 5 9 1 1 19 Total 11 25 44 2 6 88

Source: Primary data - Computed Based on the respondent’s response towards their awareness about the security system for the lockers,safe, it is found that 41% of the customers are satisfied and 19% of the customers are highly satisfied with the security system.

Table –9:Table shows the results of Paired Samples Test between Age and Attitude Related

Dependent Factors

Independent Variables Vs.

Attitude Related Dependent Factors

Paired Differences

t df Sig. (2-tailed) Mean Std.

Deviation

Std. Error Mean

95% Confidence Interval of the

Difference Lower Upper

IV Vs. ARDF 1 -1.63636 1.03036 .10984 -1.85468 -1.41805 -

14.898 87 .000

IV Vs. ARDF 2 -1.40909 1.10001 .11726 -1.64216 -1.17602 -

12.017 87 .000

IV Vs. ARDF 3 -1.19318 1.28527 .13701 -1.46550 -.92086 -8.709 87 .000

IV Vs. ARDF 4 -1.53409 1.19336 .12721 -1.78694 -1.28124 -

12.059 87 .000

IV Vs. ARDF 5 -1.52273 1.00547 .10718 -1.73577 -1.30969 -

14.207 87 .000

IV Vs. ARDF 6 -1.29545 1.21446 .12946 -1.55277 -1.03813 -

10.006 87 .000

IV Vs. ARDF 7 -1.14773 1.25524 .13381 -1.41369 -.88177 -8.577 87 .000

IV Vs. ARDF 8 -.28409 1.45388 .15498 -.59214 .02396 -1.833 87 .070

IV Vs. ARDF 9 -1.28409 1.37255 .14631 -1.57491 -.99328 -8.776 87 .000

IV Vs. ARDF 10 -1.39773 1.08850 .11603 -1.62836 -1.16710 -

12.046 87 .000

IV Vs. ARDF 11 -1.68182 1.07794 .11491 -1.91021 -1.45342 -

14.636 87 .000

IV Vs. ARDF 12 -1.40909 1.16102 .12376 -1.65509 -1.16309 -

11.385 87 .000

www.theinternationaljournal.org > RJSSM : Volume: 07, Number: 05, September 2017 Page 129

IV Vs. ARDF 13 -1.31818 1.21811 .12985 -1.57628 -1.06009 -

10.151 87 .000

IV Vs. ARDF 14 -1.20455 1.28796 .13730 -1.47744 -.93165 -8.773 87 .000

IV Vs. ARDF 15 -1.31818 1.18947 .12680 -1.57021 -1.06616 -

10.396 87 .000

IV Vs. ARDF 16 -1.12500 1.32884 .14165 -1.40655 -.84345 -7.942 87 .000

IV Vs. ARDF 17 -1.71591 .99364 .10592 -1.92644 -1.50538 -

16.200 87 .000

Source: Primary data - Computed IV – Independent Variable / ARDF I TO ARDF 17 (ARDF – Attitude Related Dependent

Factor) In this research study, the researchers identified customer’s attitude related variable. The

researchersidentifiedthe variable which connects with attitude of customers and how the same make them to choose Commercial Bank of Ethiopia and its services.In addition to these, the researchers used paired sample t-test to find the level of significance between age and attitude related factors and it was found and proved that it is significance. It means there is a significant difference between age and the attitude of the customers towards choosing their service provider Commercial Bank of Ethiopia.

Table –10: Table showing paired sample test between different types of customers and their level

of satisfaction towards the services provided by Commercial Bank of Ethiopia, Assosa. Paired Samples Test

Pair

Independent Variables

Vs. Level of Satisfaction

Paired Differences

t Df Sig. (2-

tailed) Mean Std. Deviation

Std. Error Mean

95% Confidence Interval of the

Difference Lower Upper

1 IV Vs. DF-LOS 1 -1.27273 1.29302 .13784 -1.54669 -.99876 -9.234 87 .000

2 IV Vs. DF-LOS 2 -.63636 1.43984 .15349 -.94144 -.33129 -4.146 87 .000

3 IV Vs. DF-LOS 3 -.72727 1.43621 .15310 -1.03158 -.42297 -4.750 87 .000

4 IV Vs. DF -LOS 4 -.42045 1.45208 .15479 -.72812 -.11279 -2.716 87 .008

5 IV Vs. DF-LOS 5 -1.29545 1.23325 .13146 -1.55675 -1.03415 -9.854 87 .000

6 IV Vs. DF-LOS 6 -1.46591 1.06078 .11308 -1.69067 -1.24115 -

12.963 87 .000

7 IV Vs. DF-LOS 7 -1.03409 1.44992 .15456 -1.34130 -.72688 -6.690 87 .000

8 IV Vs. DF-LOS 8 .47727 1.58279 .16873 .14191 .81263 2.829 87 .006

9 IV Vs. DF-LOS 9 -.53409 1.24059 .13225 -.79695 -.27124 -4.039 87 .000

10 IV Vs. DF-LOS 10 -.61364 1.62192 .17290 -.95729 -.26998 -3.549 87 .001

11 IV Vs. DF-LOS 11 -.81818 1.52787 .16287 -1.14191 -.49446 -5.023 87 .000

Source: Primary data - Computed

www.theinternationaljournal.org > RJSSM : Volume: 07, Number: 05, September 2017 Page 130

*Note: IV – Independent Variable / DF-LOS 1 TO DF-LOS 11 ( DF- Dependent Factor / LOS – Level of Satisfaction )

On the basis of computed results through primary data,the researchers identified the second segment of dependent variables (11 variables) which connects and decides the level of satisfaction.The researchers also used paired sample t-test on level of satisfaction towards provided services of CBE among various customers to find the level of significance. From the above table, it was found that there is significance. It means there is a significant difference between various types of customers and their level of satisfaction towards the services provided by Commercial Bank of Ethiopia.

Table –11: Table showing One-Sample Test on Service Quality Variables Connects with

Customers Level of Satisfaction

Service Quality Variabl

e

Service Quality Variables

Test Value = 0 t Df Sig. (2-

tailed) Mean

Difference

95% Confidence Interval of the

Difference Lower Upper

SQV 1 Reliability towards CBE 66.371 87 .000 4.28409 4.1558 4.4124

SQV 2 Purpose fulfilment of given services of CBE 32.957 87 .000 3.62500 3.4064 3.8436

SQV 3 Ability of the working personnel of CBE 41.218 87 .000 3.73864 3.5584 3.9189

SQV 4 Response level of working personnel of CBE

34.723 87 .000 3.54545 3.3425 3.7484

SQV 5 Time consumption towards customer service

25.120 87 .000 3.19318 2.9405 3.4458

SQV 6 Level of safety in remittance 32.085 87 .000 3.43182 3.2192 3.6444

SQV 7 Comfort level of customers 30.726 87 .000 3.51136 3.2842 3.7385

SQV 8 Economy in operation of Accounts 44.687 87 .000 3.78409 3.6158 3.9524

Source: Primary data – Computed *Note: SQV 1 TO SQV 8 (SQV – Service Quality Variables)

The third hypothesis tested with one sample t-test on Service quality variables related with Commercial bank of Ethiopia. From the above table clearly shows that all service quality variables are found significant. It means there is a strong relationship between service quality and the service provider, level of satisfaction towards Commercial bank of Ethiopia. CONCLUSION

Based on the analysis, results and discussions, the researchers concluded that it is important for commercial bank of Ethiopia to give more priority for attracting customers by knowing their basic needs and wants towards banking service. Commercial bank of Ethiopia has to understand the mind set of customers as much as possible,by conducting awareness programs to explain their latest services , advancement and technological improvements like phone banking , fund transfer , easy access through internet banking etc. They should take measures to make customers to know about the recent updates about CBE. If commercial bank of Ethiopia fails to identify the perception, attitude, priority and preferences of the customers then hundred percent they may lose their customers due to shifting customers from their bank to private banks for better service. Then it leads CBE to get failure to achieve their business objectives too. Therefore the success of commercial bank of Ethiopia starts from

www.theinternationaljournal.org > RJSSM : Volume: 07, Number: 05, September 2017 Page 131

identifying the attitude which means identifying the fundamental or basic needs and expectations of the CBE customers. So it is mandatory for CBE to concentrate more and giving high priority for the attitude, perception of customers to get success in banking sector. SUGGESTIONS

§ It is too important all service providers to concentrate on providing quality service , maintaining security system and safety features for public deposit and at the place of customers visit to the bank, reasonable increase in service charge , effective customer management system, ensuring level of comfort, giving attractive features, ensuring accessibility of banking services, trying to improve the level of response of service personnel’s who are direct contact with the customers at branch office to enhance the services and service quality to satisfy existing customer and to attract new customers.

§ It is also important to take measures towards the service quality enhancement by giving intensive training to the service personnel’s who are working in CBE to improve customer satisfaction.

§ Equality should be maintained that means equal priority should be given to the various type of customers irrespective of the category to attract them, to increase the reputation of Commercial of Ethiopia and to improve the level of satisfaction of various customers at CBE.

REFERENCES

§ Biranchi Narayan Swar(2011) A Study of Customer Satisfaction & Service Quality Gaps in Selected Private, Public & Foreign Banks, SIES Journal of Management, March 2011, Vol.7(2): 62-73

§ Dr. Narinder Kaur(2013) Customer Relationship Management in Indian Banking Sector in BVIMR Management Edge, Vol. 6, No. 1 (2013) PP 33-43

§ Jiang, J. J., G. Klein, et al. (2002). "Measuring information system service quality: Servqual from the other side." MIS Quarterly 26(2): 145-166.

§ Jiang, J. J., G. Klein, et al. (2002) investigated that SERVQUAL is indeed a satisfactory instrument for measuring Information System service quality. Other measures of service quality have included the skill, experience, and capabilities of the support staff.

§ JineaAkhtar (2011). Determinants of service quality and their relationship with behavioural outcomes: Empirical study of the private commercial banks in Bangladesh. International Journal of Business and Management, 6(11), 146-156. Retrieved from http://search.proquest.com/docview/906290463?accountid =172684

§ Rajesh Nair, Ranjith P V, Sumana Bose and CharuShri(2010) A Study of Service Quality on Banks with Servqual Model, SIES Journal of Management, April - August 2010, Vol.7(1): 35-45

§ Dr. T. Vanniarajan, K. Subbash Babu(2011) Internal Service Quality And Its Consequences In Commerical Banks: A H R. Perspective Global Management Review | Volume 6 | Issue 1 | November 2011