Embed Size (px)

Citation preview

A Study on

INDIAN AIRLINE INDUSTRY

Management Research Project -I

Submitted

In the partial fulfillment of the Degree of

Master of Business Administration

Semester-III

By

Patel Dixit K. (12044311084) (F)

Patel Vimal V. (12044311117) (F)

Patel Vipul J. (12044311118) (F)

Parmar Jayesh V. (12044311060) (M)

Sandeep Paul (12044311145) (M)

Zaloriya Kalpesh S. (12044311163) (M)

Under the Guidance of:

Prof. (Dr.) Mahendra Sharma

Prof. & Head,

V. M. Patel Institute of Management.

&

Prof. Harsha Jariwala, Asst. Professor

Prof. Abhishek Parikh, Asst. Professor

V. M. Patel Institute of Management.

Submitted To:

V. M. Patel Institute of Management,

Ganpat University,

Kherva.

(November-2013)

CERTIFICATE BY THE GUIDE

This is to certify that the contents of this report entitled “A STUDY OF INDIAN AIRLINE

INDUSTRY by Patel Dixit K.(084), Patel Vimal V. (117), Patel Vipul J. (118), Parmar Jayesh V.

(060), Sandeep Paul (145), Zaloriya Kalpesh S. (163) submitted to V. M. Patel Institute of

Management for the Award of Master of Business Administration (MBA Semester -III) is original

research work carried out by them under my supervision.

This report has not been submitted either partly or fully to any other University or Institute for award

of any degree or diploma.

Date:

Place: Prof. (Dr.) Mahendra Sharma,

Professor & Head,

V. M. Patel Institute of Management,

Ganpat University.

Kherva.

CANDIDATE’S STATEMENT

We hereby declare that the work incorporated in this report entitled “A STUDY OF INDIAN

AIRLINE INDUSTRY” in partial fulfillment of the requirements for the award of Master of Business

Administration (Semester - III) is the outcome of original study undertaken by us and it has not been

submitted earlier to any other University or Institution for the award of any Degree or Diploma.

Date :

Place :

Patel Dixit K. (12044311084)

Patel Vimal V. (12044311117)

Patel Vipul J. (12044311118)

Parmar Jayesh V. (12044311060)

Sandeep Paul (12044311145)

Zaloriya Kalpesh S. (12044311163)

i

PREFACE

Industrial activity plays an important role in economic development of our country. The knowledge

of present market scenario is very much essential and keeping that in view, our college gave us a

very good opportunity of industrial interaction in terms of Management Research Project-I.

As a part of Our Academic requirement of MBA program, we have selected INDIAN AIRLINE

INDUSTRY as the industry to be analyzed under the subject named MRP-1. The reason to choose

Airline Industry is very obvious. One, that industry has very interesting history and background. It is

concerned with basic Infrastructure development as well as continuous changing advanced

technology. Secondly, it has opportunistic future and directly impact on economy. Industry has a

very rich area of analyzing. Through this kind of Industry Analysis we can have good exercise of

learning and also help us to understand current trend of industry with its all-possible dimensions.

The report covers all the landmark changes in Airline industry and competitive markets being driven

by globalization and Internet technology. It would also provide you the idea of analyzing, crafting,

formulating, evaluating, implementing and executing business strategies related to the Airline

Industry in today’s volatile markets.

ii

ACKNOWLEDGEMENT

We the students of Management at V.M.Patel Institute of Management, Ganpat University are very

much benefited from the help of many people during the evolution of this project.

We would like express our special gratitude to our respected Dr. Mahendra Sharma and Miss. Harsha

Jariwala and all concern persons who have provided us help through their information, guidance and

all kinds of support, which was required for preparation of this report. Without their help it would have

been difficult for us to complete our Management Research Project –I.

As always, we value your recommendations and thoughts about the report. Your comments regarding

coverage and contents will be most welcome, as will your calling our attention to specific errors,

deficiencies and oversights.

By:-

Patel Dixit K. (12044311084)

Patel Vimal V. (12044311117)

Patel Vipul J. (12044311118)

Parmar Jayesh V. (12044311060)

Sandeep Paul (12044311145)

Zaloriya Kalpesh S. (12044311163)

iii

EXECUTIVE SUMMARY

This report analyses the Indian Airline industry with specific regard to the area of passenger travel.

This analysis is performed with the aid of strategic management tools in order to analyse and then

draw up useful perceptions of the industry with the aim of identifying pertinent issues associated with

the current business situation in the sector for example, identifying the specific drivers for change in

the industry and the building possible future scenarios. An in depth overview of the situation of the

industry is first given. This is necessary in order to put the Indian aviation industry into perspective

and to enable the formulation of the factors associated with tools such as PESTEL, SWOT and even

Five Forces analysis. This in turn helps in formulating an accurate picture of key drivers and future

scenarios. In a nutshell, it emerges from the discussion that the market is growing and with vast

potential, thereby presenting conditions conducive to investment in such a market. However, it also

emerges that competition will be fierce and that ironically, even with such a large market, some

players in the industry will not survive unless they adopt strategies that will enable them compete in

both the short and long term. As well as financial analysis and forecasting of the industry.

INDEX

Preface………………………………………………………………………..………… I

Acknowledgement …………………………………………………………...………… II

Executive Summary …………………………………………………………………... III

Particular Page No.

Chapter 1 INTRODUCTION OF THE INDUSTRY 1-5

1.1 Introduction To Airline Industry 1

1.2 Airline Market Share On International Routes 2

1.3 Indian Domestic Airline Market Share 2

1.4 Average Passenger Load Factors On Domestic Routes 5

Chapter 2 MAJOR PLAYERS OF THE INDUSTRY 6-13

2.1 Top 3 Airline Companies In India 7

2.2 Jet Airways 8

2.3 Spice Jet 10

2.4 Kingfisher Airlines 12

Chapter 3 STRATEGIC ANALYSIS 14-42

3.1 Industry Dominant Economic Feature 15

3.2 Key Factor For Future Competitive Success 18

3.3 Porter's Five Forces Model 20

3.4 PEST Analysis 31

3.5 SWOT Analysis 35

3.6 Strategic Groups Mapping 41

Chapter 4 FINANCIAL ANALYSIS 45-64

4.1 Ratio Analysis 45

4.2 Trend Analysis 57

4.4 Common Size Balance Sheet 63

Chapter 5

Chapter 6

Chapter 7

Chapter 8

Chapter 9

BUSSINESS PLAN

FINDING AND RECOMMENDATION

CONCLUSION

BIBLIOGRAPHY

ANNEXURE

65-79

80-81

82-83

84-85

86-90

LIST OF TABLE

No. Particulars Page no.

2.1 Market Share 7

4.1 Current Ratio 47

4.2 Debt Equity Ratio 49

4.3 Debtors Turnover Ratio 51

4.4 Inventory Turnover Ratio 53

4.5 Interest Coverage Ratio 55

4.6 Net sales Trend 57

4.7 PAT Trend 59

4.8 Net Worth Trend 61

4.9 Balance Sheet 63

4.10 Profit & Loss A/C 64

LIST OF FIGURE

No. Particulars Page no.

1.1 Airline Market Share 3

1.2 Domestic Market Share 4

1.3 Passenger Load Factor 5

3.1 Strategic Group mapping 43

4.1 Current Ratio 47

4.2 Debt Equity Ratio 49

4.3 Debtors Turnover Ratio 51

4.4 Inventory Turnover Ratio 53

4.5 Interest Coverage Ratio 55

4.6 Net sales Trend 57

4.7 PAT Trend 59

4.8 Net Worth Trend 61

1 | P a g e

CHAPTER 1

INTRODUCTION

2 | P a g e

Introduction to Airline Industry

1.1 History

The airline was set up under the Air Corporations Act, 1953 with an initial capital of 32

million and started operations on 1 August 1953. It was established after legislation came into

force to nationalize the entire airline industry in India. Two new national airlines were to be

formed along the same lines as happened in the United Kingdom with British Overseas

Airways Corporation (BOAC) and British European Airways (BEA). Air India took over

international routes and Indian Airlines Corporation (IAC) took over the domestic and

regional routes. Eight pre-Independence domestic airlines, Deccan Airways, Airways India,

Bharat Airways, Himalayan Aviation, Kalinga Airlines, Indian National Airways and Air

Services of India and the Domestic wing of Air India, were merged to form the new domestic

national carrier Indian Airlines Corporation. International operations of Air India Ltd. was

taken over by the newly formed Air India International. Indian Airlines Corporation inherited

a fleet of 99 aircraft including 74 Douglas DC-3 Dakotas, 12 Vickers Vikings, 3 Douglas DC-

4s and various smaller types from the seven airlines that made it up.

Vickers Viscounts were introduced in 1957 with Fokker F27 Friendships being delivered from

1961. The 1960s also saw Hawker Snidely HS 748s, manufactured in India by Hindustan

Aeronautics Limited, join the fleet. The jet age began for IAC with the introduction of the

pure-jet Sud Aviation Caravels airliner in 1964, followed by Boeing 737-200s in the early

1970s. April 1976 saw the first three Airbus A300wide-body jets being introduced. The

regional airline, Vayudoot, which had been established in 1981, was later reintegrated. By

1990,Airbus A320-200s were introduced. The economic liberalization process initiated by the

Government of India in the early 1990s ended Indian Airlines' dominance of India's domestic

air transport industry. Indian Airlines faced tough competition from Jet Airways, Air

Sahara (now Jet Lite), East-West Airlines, Skyline NEPC, and ModiLuft. As of 2005, Indian

Airlines was the second largest airline in India after Jet Airways while Air Sahara controlled

17% of the Indian aviation industry.

3 | P a g e

1.2 Airline Market Share On International Routes To/From India: 2013

On the international front an important development was the fact that in FY2013 for the first

time a foreign carrier, Emirates, claimed the highest market share for traffic to/from India. Air

India, historically the market leader on international routes was impacted by the grounding of

its 787s for most of the last quarter.

Figure 1.1 Airline Market Share on International Routes

While India‟s second largest international carrier, Jet Airways, saw only a marginal increase in

traffic as it consolidated its network and dropped services to points such as New York JFK,

Milan, Johannesburg and Kuala Lumpur.

1.3 Indian Domestic Airline Market Share: FY2013 Vs FY2012

India‟s airlines posted a combined loss of USD1.65 billion in FY2013 (USD1.15 billion if

Kingfisher is excluded), down from approximately USD2.28 billion the previous year. More

than 40% of the loss was incurred in the last quarter alone, squandering the improved

performance posted during the first nine months of the year.

Kingfisher‟s exit from the Indian aviation sector was one of the most significant developments

for the market in FY2013. It highlighted the fragility of the sector when an airline that was the

largest in the country less than two years earlier and with an excellent reputation amongst

passengers, could fall from grace so swiftly.

4 | P a g e

But with it came a silver lining for the remaining carriers. As a result of the removal of

Kingfisher‟s seats, combined with modest capacity induction by other carriers, the

demand/supply dynamics in the market started to favor airlines for the first time since 2004.

This was reflected positively in the average fares which increased by 15-20% year-on-year.

India‟s airlines were showing signs of a steady recovery in financial performance during the

first three quarters of FY2013; however the fourth quarter spoilt the party. Aggressive

discounting during the traditionally weak period between January and March resulted in losses

of USD700 million during this quarter alone (close to USD500 million if Kingfisher is

excluded).

Figure 1.2 Indian Domestic Airline Market Share

The cost environment remained hostile throughout the year with the weakness of the Indian

rupee and continued high oil prices being the key challenges. Even though Brent Crude levels

softened towards the end of the year, the depreciation of the rupee meant that carriers did not

see any benefit from this.

Over the 12 months to 31-Mar-2013, with carriers moving to fill the space vacated by

Kingfisher, all airlines except Jet Konnect saw an increase in their domestic market share over

the previous year, but none more so than IndiGo which saw a 7ppt improvement.

5 | P a g e

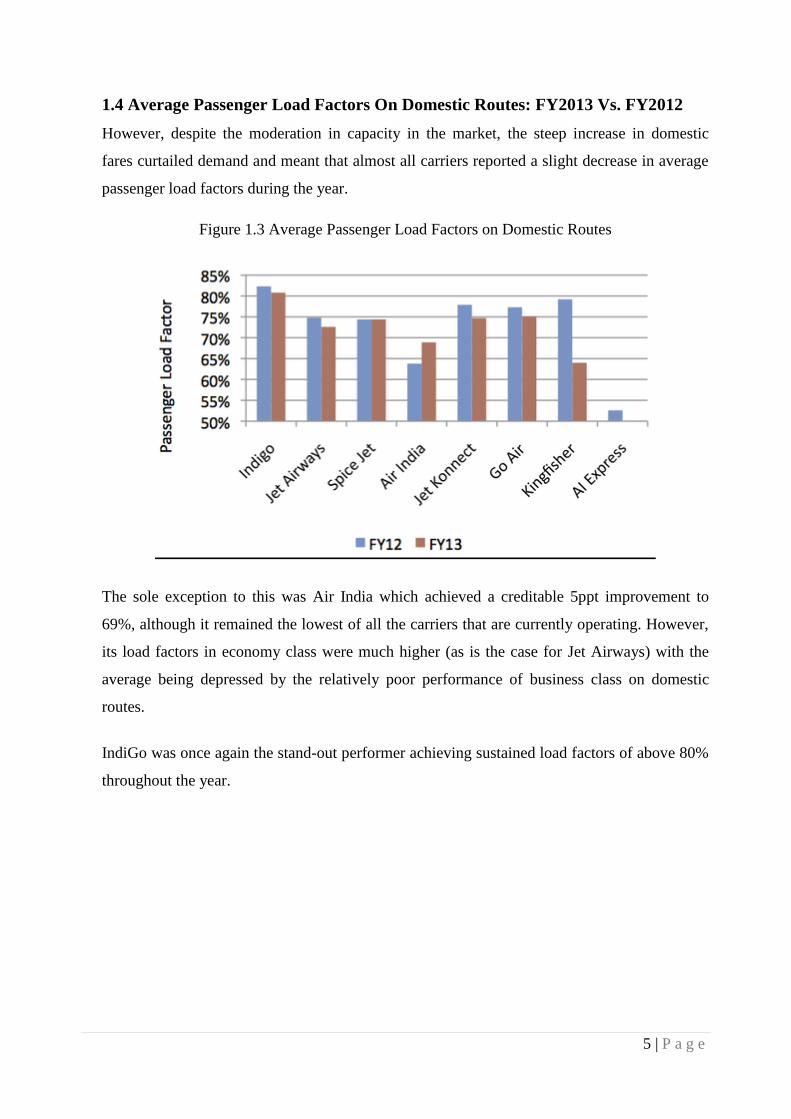

1.4 Average Passenger Load Factors On Domestic Routes: FY2013 Vs. FY2012

However, despite the moderation in capacity in the market, the steep increase in domestic

fares curtailed demand and meant that almost all carriers reported a slight decrease in average

passenger load factors during the year.

Figure 1.3 Average Passenger Load Factors on Domestic Routes

The sole exception to this was Air India which achieved a creditable 5ppt improvement to

69%, although it remained the lowest of all the carriers that are currently operating. However,

its load factors in economy class were much higher (as is the case for Jet Airways) with the

average being depressed by the relatively poor performance of business class on domestic

routes.

IndiGo was once again the stand-out performer achieving sustained load factors of above 80%

throughout the year.

6 | P a g e

CHAPTER 2

MAJOR PLAYERS

7 | P a g e

2.1 Top 3 Airline Companies In India

Table 2.1 Market Share of Airline Industry

Rank Company Name Company Logo Market Share

1 Jet Airways

20%

2 Spice Jet

18%

3 Kingfisher

3%

8 | P a g e

JET AIRWAYS

Jet Airways (India) Limited (JAIL) was incorporated in 1st April of the year 1992 as a private

company with limited liability and it commenced operations as an Air Taxi Operator in 5th

May of the year 1993 with a fleet of four leased Boeing 737 aircraft and also having ISO 9001

certification for its in-flight services. The Company became the first airline in India to operate

the Boeing 737-400 Aircraft in April of the year 1994 and it operates one of the youngest

aircraft fleets in the world today. The Company was granted the scheduled airline status in

14th January of the year 1995. Jet Airways became a deemed public company in 1st July of

the year 1996.

TYPE Public

PREDECESSOR Jet Airways(India) Limited

FOUNDED 1992

HEADQUARTERS Mumbai, India

KEY PEOPLE Naresh Goyal (CEO & MD)

NET INCOME Rs.17,724.65 Cr (2012-13)

EMPLOYEES 13.16 K(2012)

PARENT Tailwinds Limited

WEBSITE www.jetairways.com

9 | P a g e

Jet Airways was reconverted into a private company as at 19th January 2001. The Company

bagged the prestigious Air Transport World Award 2001 for Market Development and the

TTG Travel Award 2002 for Best Domestic Airline. In the year 2004, the company made tie

up with the South African Airways. During the year 2005, Jet Airways Limited has filed its

draft Red Herring Prospectus with the Securities and Exchange Board of India (SEBI) to enter

the capital market with its initial public offering for used to fund its international expansion

plans. Jet Airways became a public company in 28the December of the year 2004.

The Company launched its first inter-continental flight by linking Mumbai with London

Heathrow by a non-stop day flight in the month of May during the year 2005. Jet Airways

executed its purchase agreement with The Boeing Company, USA in the year 2005, also in the

identical period introduced an In-flight Safety Manual in Braille, signed a pact with Gulf Air

and the company won the Avaya Global Connect Customer Responsiveness Award. During

2005-2006, the company completed the construction of hangar complex with workshop and

allied facilities in Mumbai.

Jet Airways and Etihad Airways, the national carrier of the United Arab Emirates, had inked a

code share agreement in June of the year 2008 and reciprocal frequent flier partnership on the

New Delhi-Mumbai-Abu Dhabi sectors. In same June 2008, launched its daily Mumbai-

Shanghai-San Francisco flight, becoming the first Indian private carrier to operate to China.

The Company enhanced its network connectivity from Pune with the launch of its new direct

services to Hyderabad, Nagpur & Ahmedabad effective from July 15th 2008. During the same

month, Jet Airways got permission for fly to Dubai from Delhi and Mumbai.

10 | P a g e

SPICE JET

TYPE Public

PREDECESSOR Spice Jet Limited

FOUNDED 2005

HEADQUARTERS Gurgaon, India

KEY PEOPLE Kalanithi Maran (CEO & MD)

NET INCOME Rs.5805.14 Cr (2012-13)

EMPLOYEES 5.25 K (2012)

PARENT Sun Group

WEBSITE www.spicejet.com

SpiceJet Ltd is India's best low cost airline, delivering the lowest air fares with the highest

consumer value. The company operates 119 flights daily to 18 cities, namely Ahmedabad,

Bangalore, Bagdogra, Chennai, Coimbatore, Delhi, Guwahati, Goa, Hyderabad, Jammu,

Jaipur, Kochi, Kolkata, Mumbai, Pune, Srinagar, Varanasi and Visakhapatnam. Spicejet Ltd

was incorporated in the year 1984 with the name Genius Leasing Finance and Investment

Company Ltd. In the year 1993, the company ventured into domestic aviation operations under

technical partnership with Deutsche Lufthansa AG.

11 | P a g e

In the year 1994, the name of the company was changed from MG Express to ModiLuft Ltd.

In June 1994, the company entered into a management agreement with Lufthansa to manage

their entire Airline operations. The company suspended their Airline operations in the year

1996 after dissensions grew between Lufthansa and the company. During the year 2000-01,

the name of the company was changed from ModiLuft Ltd to Royal Airways Ltd.

The company started their commercial operations of domestic flight services on May 23, 2005

with three leased Boeing 737-800 aircraft. During the year 2004-05, they signed an agreement

with Boeing for acquiring 20 (737-800) aircrafts and in May 4, 2005, the company changed

the name of the company from Royal Airways Ltd to SpiceJet Ltd. In May 5, 2005, they

entered into a strategic tie up with Indian Oil Corporation Ltd. In November 2005, the

company launched their daily direct flights between Delhi and Kolkata. They also launched

their services to two new spice cities namely, Jammu and Srinagar.

In March 27, 2006, the company launched their first co-branded credit card with State Bank of

India in association with MasterCard International. During the year 2006-07, the company

inducted five new aircraft to their fleet taking the total fleet strength to eleven aircraft. They

started sale of food on board during the year. In August 17, 2006, the company launched

Spicejet Hotels, with the aim of providing a dedicated online Web hotel reservation services to

their customers. In October 2006, they launched new flights between Kolkata and Guwahati.

In January 2007, they introduced two new additional daily flights on the Bangalore - Mumbai

- Hyderabad routes.

12 | P a g e

KINGFISHER AIRLINES

Kingfisher Airlines Limited was an airline group based in India. Its head office is in Andheri

(East), Mumbai and Registered Office in UB City, Bangalore. Kingfisher Airlines, through its

parent company United Breweries Group, has a 50% stake in low-cost carrier Kingfisher Red.

The airline had been facing financial issues for many years. Until December 2011, Kingfisher

Airlines had the second largest share in India's domestic air travel market. However due to a

severe financial crisis faced by the airline at the beginning of 2012, it has the lowest market

share since April 2012.Kingfisher Airlines Ltd is the largest charter aviation company in India.

TYPE Public

PREDECESSOR Kingfisher Airlines Limited

FOUNDED 2004

HEADQUARTERS Mumbai, India

KEY PEOPLE Dr.Vijay Malaya (CEO & MD)

NET INCOME Rs 682.48 Cr (2012-13)

EMPLOYEES 2.85 K (2012)

PARENT Ub Group

WEBSITE www.flykingfisher.com

13 | P a g e

Their principal activity is to provide commercial passenger airline and private helicopter and

airplane chartering services in India. Their business unit Air Deccan, is India's low cost carrier.

Kingfisher Airlines Ltd was incorporated in June 15, 1995 as a private limited company with

the name Deccan Aviation. The company was promoted by G R Gobinath, K J Samuel and

Vishnu Singh Rawal. In January 2005, the company was converted into a public limited

company. In September 1997, the company opened their first base at Jakkur and launched

their first Helicopter. In June 1998, they opened their second base in Hyderabad and in

December 1998, they commenced offshore flying operations. In June 2001, the company

introduced first fixed wing aircraft and in November, they introduced the second fixed wing

aircraft. In August 2003, first Air Deccan flights take place on Bangalore to Hubli and

Bangalore to Mangalore. In December 2003, the company incorporated Deccan Aviation

(Lanka) Pvt Ltd, which is a joint venture company.

The company was established as a 52% subsidiary company to undertake helicopter services

and airline operations in Sri Lanka. In August 2004, they introduced first Airbus A 320. In

March 2005, Air Deccan, entered into tie up arrangement with Club HP. In June 27, 2005,

Deccan Aviation (Lanka) Pvt Ltd ceased to be a subsidiary consequent to the transfer of 4% of

their share to Srilanka nationals. In March 2007, they forayed into Air Cargo Business through

a wholly owned subsidiary. The company hived off Charter Services into a separate entity and

also transfers the Maintenance and Repair Facility into a separate entity.

The Airline business of Kingfisher Airlines Ltd merged with the company with effect from

April 1, 2008 and the name of the company was changed to Kingfisher Airlines Ltd. The

airline had shut down its operations when on 20 October 2012 the DGCA suspended its flying

license. The suspension had been due to failure to give an effective response to the show-cause

notice issued by DGCA. However, the airline had locked out its employees for several days

before this suspension. On 25 October 2012, the employees agreed to return to work. In

February 2013 the Indian government announced the withdrawal of both domestic and

international flight entitlements allocated to the airline.

14 | P a g e

CHAPTER 3

STRATEGIC ANALYSIS

15 | P a g e

3.1 INDUSTRY’S DOMINANT ECONOMIC FEATURES

Market Size:

The global airline industry consists of over 2000 airlines operating more than 23,000aircraft,

providing services to over 3700 airports. In the year 2009, the industry‟s revenue was

estimated to be $483 billion. Major services of this industry include domestic passenger flights

which accounts for about 30 percent of industry revenue, international passenger flights

contributing 25%, domestic cargo flights contributing 20%, international cargo flights which

account for about 10% and domestic commuter passenger flights contributing 10% of the

industry revenue. The U.S constitutes the largest airlines industry in the world, accounting for

about 49.8% of the global revenue. US airlines reported over $160 billion in total revenues,

with approximately 545,000 employees and operate over 11 million flight departures per year,

and carry one third of the world‟s total air traffic.

Growth Rate:

The global airlines industry grew by 6.3% in 2008 to reach a value of $467.4 billion. In2013,

the global airlines industry is forecast to have a value of $609.3 billion, an increase of

30.4%since 2008. The growth of world air travel has averaged approximately 5% per year

over the past 30 years, with substantial yearly variations due to changing economic conditions

and differences in economic growth in different regions of the world. The domestic segment

dominated in the global airline industry and accounted for 1.4 billion passengers in 2007,

equivalent to 66.5% of the industry's overall volume.

Number of Rivals:

The airline industry is characterized by the high competition that exists among the rival

airlines due to its low cost nature. Since the carriers are involved in a constant struggle to take

away the market share from each other, the rivalry is increased, as it is easy for buyers to

switch between the airlines companies, depending on price. The airlines are continually

competing against each other in terms of prices, technology, in-flight entertainment, customer

services and many more areas. The industry is fragmented into many small companies. The

key competitors in the industry include: American airlines, Delta, southwest, United airlines

etc. As in many mature industries, consolidation is a trend. Airline groupings may consist of

limited bilateral partnerships, long-term alliances, mergers, or takeovers. Due to the large

16 | P a g e

number of airline companies the industry is not going through a period of consolidation to a

smaller number of companies.

Scope of Competitive Rivalry:

Services of the industry can be segregated as domestic, regional, within the continent or travel

between continents. Large companies compete with other major companies on a national or

global scale. However, Small airlines can compete by serving local or regional routes.

Competitive rivalry is high and hence, the demand for air travel is inelastic because there are

many different airlines to choose from. Example: Southwest VS American airlines.

Number of Buyers:

The market demand is fragmented among many buyers. The important customer segments in

the industry include corporations, SME‟S and leisure travellers. The various airlines are

competing for the same customer, which also results in strengthening the buyer power.

Individuals wishing to travel have various options to choose from when selecting an airline but

price is usually the most important factor. Hence, the bargaining power of customers in the

airline industry is very high since they are price sensitive and search for the best deals

available.

The Degree of Product Differentiation:

The products and services of the rivals in the industry are less differentiated. The airline

companies mostly fly similar aircrafts and hence, have identical or near identical seating

configurations. Frequencies and timings are very similar with only a few airlines prepared to

allow their competitors with frequency advantage. The onboard products are also mostly

comparable, and do not have much change. In order to attract more customers there is severe

price competition within the industry, with airlines ruthlessly undercutting each other with fare

promotions. Hence the look alike products of rivals cause heightened price competition.

Product Innovation:

Innovation plays a major role in airlines‟ strategy, which focuses on Internet Protocol

technologies, end-to-end services to the desktop and airport integration. The airline industry is

characterized by having rapid product innovation and depending on the market conditions and

buyer demands certain products may have short life cycles in this industry. For example some

flights may have innovation in their in-flight products, and thus if it is unpopular with

17 | P a g e

passengers it has to be quickly withdrawn. Hence, there are opportunities to overtake key

rivals by being the first to market with next generation products.

Pace of Technological Change:

The airline industry is growing leaps and bounds because of the revolutionary advancement in

the techno world. It has completely changed the structure, form, and future of the industry in

all ways. Internet has given a huge thrust to the industry by heightening the comfort level

provided by art transport in various ways. The benefits offered include the availability of

cheap airfares through online booking; Travelers can also compare prices of different airlines

and then choose the best offered price. Carriers have been able to add more functionality,

especially in customer service areas ranging from check-in desks upwards. Furthermore, they

have also been able to integrate internal systems. Internet Technology has become recognized

as a major enabler for aviation to work effectively and safely, while achieving substantial cost

savings. Hence, industry members cannot operate without technological capabilities and thus

they need technology to compete and survive within the industry.

Supply/ Demand Conditions:

Intense competition within the industry leads to surplus of capacity in several markets. As a

result of surplus of capacity many airline companies get into the price war in order to attract

more customer demand. Hence, surplus of capacity may push prices down however; this

usually doesn‟t affect the profit margins. This is because the prices are lowered as a result of a

cut in the costs. The airline companies in the case of excess capacity, cut back on the cost in

the form of entertainment, meals etc

Vertical Integration:

Vertical integration maybe found in some of the companies in the airline industry. By

performing the traditional role of travel agents airlines achieve forward integration. Likewise

by performing the role of suppliers such as aircraft maintenance and in flight catering airlines

have backward integration. In this industry, some competitors operate in multiple stages

18 | P a g e

3.2 KEY SUCCESS FACTORS

Key success factors describe main parts of performance that are important for the firm to

achieve its objectives and mission. Top level management absolutely considers these factors

daring the setting overall goals. These key success factors give a widespread knowledge for

the entire company. Therefore, any action that the firm commences must make sure constantly

greater performance in these key parts if not the firm may not be competent to accomplish its

goals and theses may full to achieve its mission. In the service/ airline industry, predominantly

the capital-intensive, the key success factors are described below.

Strong Management:-

There must be strong management of everything that is advantages for the organization. The

airline has at all the time evaded, disdained and vogue everything that may increase costs and

makes difficult the basis travels plan. Management ranks are inclined, healthy compensated

and significantly productive.

Capable Workforce:-

Highly qualified and competence workforce is very essential in this industry or service

oriented industry. They must possess strong communication skills and soft spoken with

customers. There must be training programs focusing to enhance their abilities and skills and

these campiness must be customer focused and they cannot leave the organization and create

difference.

Service Promotion And In-Flight Service:-

The promotion in this industry is mainly targeted to enhance the based of loyal customers and

also focused to the regular high-revenue customer. The in-house service such as booking ease,

air crack type, aircraft seating space, class of service offerings must be at least industry coach

cabin that is slightly more specials. There are no assigned seats, no meals, just beverages and

Jencks. Therefore, simple service is a major critical success factor.

Non-Stop Flying:-

Destination from one point to anthers point should be nonstop. This activity minimizes the

time that planes take while reaching the destination and it allows airline more to be in the air,

it results in good image and increases passengers credibility.

19 | P a g e

Financial Management:-

Thriving management of this factor facilitates airline to regulate investment for growth. There

is accountability of the unit revenue to compute the profitability. Which is calculated by

revenues minus all the expenses divided by the total seats flown.

Efficient Management of Cost:-

Maximizing revenues by implying creative and competitive, pricing structure to attract all the

profitable segments and sustaining frequent and profitable customer base is most important

key success factor for this industry. Efficient management cost by focusing on the price

hedging during volatile periods and maintaining fuel procurement is an important factor.

Route System:-

An airline route organization is the most reliable factor. Where to fly and how frequently are

the success factors that must be harmonized to demand and simultaneously planned to increase

the aircraft utilization.

20 | P a g e

3.3 PORTER'S FIVE FORCES MODEL

One important component of industry and competitive analysis involves delving into the

industry‟s competitive process to discover what the main sources of competitive pressure are

and how strong each competitive force is. This analytical step is essential because managers

cannot devise a successful strategy without in-depth understanding of the industry‟s

competitive character.

Even though competitive pressures in various industries are never precisely the same, the

competitive process works similarly enough to use a common analytical framework in gauging

the nature and intensity of competitive forces.

Two things determine your company‟s profitability- the industry in which it competes and its

strategies position in the industry. Some industries have inherently low profit potential while

others are highly profitable. The most profitable companies have a strongest competitive

position in a profitable industry. The poorest companies have weak positions in weak

industries.

The following write-up is a view of the Indian airline industry from these five angles leading

to the expected changes in the coming years in the underlying structure of the Indian airline

industry.

21 | P a g e

Porters five force model

22 | P a g e

3.3.1. THREAT OF NEW ENTRANTS

Threat of new entrants is another major aspect of the five forces. This aspect has a low threat

for the airline industry. There are two aspects that do however raise the threat level. First, there

are extremely low switching costs. Second, there are no proprietary products or services

involved.

Even with these two aspects the industry still has a very low threat overall. Existing firms have

a large cost advantage. This industry requires a large amount of capital and without a strong

customer base there will be little to no profit in the first few years. Existing firms can and will

use their high capital to retaliate against newer firms with whatever means necessary such as

lowering prices and taking a loss.

Although there are low switching costs between brands, consumers tend to only chose well-

known names. Airline tickets are expensive so people don‟t want to give that money to firms

they don‟t trust. There is also a huge safety aspect involved and most consumers feel safer

with firms that have been around for a long period of time. This industry requires plane and

flying experience which also lowers the threat of entry. When firms decide to enter the market

they first have to become licensed which can take about a year. After that they are constantly

being regulated by several organizations such as the Federal Aviation Administration and the

Department of Transportation. The time and money spend to solely open an airline company is

enough to prevent most people from entering the industry.

Airport Slot Availability

The limited access to airport slots93 has long been a barrier to the European airline industry as

national airlines had access to the best slots in the major airport hubs94 and new entrants to the

market would only have little success as they would be given none or off-peak slot allocations

at the airports. In order to liberalise this market the European Commission introduced

legislation regulating the allocation of airport slots in the EU95. The reasons for this

legislation was the significant and consistent growth in air traffic in the EU and the delays and

other difficulties experienced in this increase of airport capacity. Creating more competition

was also an explicit objective for this regulation and two key aims were “to facilitate

competition and encouraging entrance into the EU market and to ensure that slots at congested

airports are allocated on the basis of neutral, transparent and non-discriminatory rules”

23 | P a g e

Predatory Pricing as a Barrier To Entry

The concept of predatory behaviour is based on incumbents in an industry squeeze out new

entrants by temporarily lowering their prices to match the new competitor or even introduce

prices below the levels of these new entrants, who often do not have enough capital to survive

such a price war, until they have been driven out of the market. After the new entrant has lost

this price war, the incumbent then increases its prices back to pre-competition levels. Within

the context of the airline industry allegations of predatory pricing is most often made when a

low fare carrier enters a market or specific route serviced by a full-service carrier prior to its

entry. The latter will then lower its prices attempting to cause the former to exit this market or

route.

Frequent-Flyer Programs

Frequent-flyer programs are marketing schemes by airlines giving customers a gift, usually

free travel, when they have conducted a certain amount of business with the airline. These

programs have made many customers, especially business travellers, prefer a certain airline or

airline alliance as they would receive bonus flights, free hotel accommodation or other free

gifts the scheme provides, although they may be able to buy a cheaper flight at another airline.

The reason has often been that the company pays for the flights but the individual employee

receives the bonus points. It has also been widely stated that purpose of the programs is to

offer commission on business purchases in the form of a gift to the agent, who does the buying

for the business. When the buyer places an unusually high value on the bonus relative to the

value he/she places on the marginal payments for the purchased travel, as results from this

principal/agent problem, the effectiveness of the frequent-flyer program increases.

Economies of Scale

Classic industrial studies109 have concluded that there are no significant economies of scale

with regards to the airline industry, when looking at the whole system. Even when looking at

the city-pair market economies of scale it was concluded that in a liberalised market it is

impossible to use the economies of scale that exists in theory. This would be to use larger

aircraft as studies have shown that the average cost per passenger is lower in a large aircraft

such as the Boeing 747-400 than in a smaller Boeing 737-400110 and it would therefore be

preferable to have larger aircraft serve a city-pair but with less frequency in order to increase

the load factor, but this is of course impossible as travellers on high passenger-volume city

pairs like London-Dublin demand high frequency, which in turn means that economies of

24 | P a g e

scale is no substantial barrier to entry. However, LFA´s like Ryan air has countered traditional

theory and have achieved economies of scale. Not by using larger aircraft, but through their

low cost structure they are able to sell tickets at lower prices, thereby stimulating demand and

increase their load factors, hence lowering their unit cost per passenger. This will be explored

further in the Ryan air case study later in this thesis.

Empirical Study On Barriers To Entry

Australia/New Zealand, Canada, USA and Europe on their perception on the effectiveness of

barriers to entry in the airline market. The study showed that managers of low fare airlines

perceived strategic barriers such as code sharing, superior service and hub-and-spoke systems

as significantly smaller barriers than other airlines, but found airport fees as a significantly

higher barrier to entry than other airlines. This is easy to understand as the airport fees amount

to a higher percentage of the total ticket price with low fare airlines as their prices are

generally lower and the airport fees are most often fixed, meaning the fee remain the same

regardless of whether the ticket price is €100 or €1000. Moreover, a strong cash position

and/or large firm size is also seen to weaken the effectiveness of strategic barriers such as

predatory pricing, code-sharing, brand name, customer segmentation and advertising. A recent

study was performed by doing a survey, where data was collected by airline managers

3.3.2. THREAT FROM SUBSTITUTES

This industry has a medium substitute risk level. There are substitutes in the airline industry.

Consumers can choose other form of transportation such as a car, bus, train, or boat to get to

their destination. There is however a cost to switch. Some means of transportation can be more

costly than a plane ticket. The main cost is time. Planes are by far the fastest form of

transportation available. Airlines surpass all other forms of transportation when it comes to

cost, convenience, and sometimes service. Consumers do sometimes choose other methods for

various reasons such as cost if they are not traveling very far which raises the risk.

Government policies affecting the attractiveness of alternative modes of travel or

communication affect the impact of substitutes on airlines. Cumbersome security procedures

on airports make air travel less attractive.

25 | P a g e

Alternative Modes of Transportation

Very little research has been done on the impact of automobiles, buses and business/corporate

aviation as an alternative mode of transport vis-à-vis scheduled air transport. Therefore I will

only make a few general comments with regards to them.

Bus Service

There is basically only one major bus service operator on a pan-European level that has

scheduled routes in a European network and that is Euro lines. It is not one entity though, as it

is comprised of 30 independent bus companies operating a network together.128 Pan-

European coach service is in my opinion only a substitute for air travel, when you travel short

distances and have little concern as to the time consumption or when purchasing a pass and

making many stops (travel a short distance numerous times). Senior management at leading

European low fare airlines such as Ryan air have argued that airlines cannot compete with

other modes of transport for journeys of less than approximately 400 km.129 The product

would target groups from the lower echelon of society such as students and shoestring

travellers. The advantage is that one may choose to travel on the same day as ticket prices are

usually flat through as season, unlike air travel where one may pay dearly for same day

travel130.

Automobiles

Regarding automobiles one must intuitively argue that the price of fuel is an important

determinant of its role as a valid substitute for air travel. The lower the fuel price is for your

automobile, the more likely you are to use it more, both for short- and long-distance travel. As

one knows from the US the use of the automobile for long journeys across states if fairly

common, but the price of fuel is also approximately 1/3 of the price in Europe, mainly due to

higher taxes in the latter. A recent paper discussing the automobile as a substitute for rail or air

travel also conclude that there is a group of potential passengers, that consider their

automobile as an alternative mode of transport and make their decision considering the

variable costs like fuel etc. of using the automobile.131 Given the high fuel prices in Europe,

although higher fuel prices in the airline industry has also led to a surcharge there, is putting a

limit on the automobile as a viable alternative for air transport in long-distance travel (more

than 400 km as was mentioned earlier as the lower limit for feasible competition between

airlines and alternative modes of transportation) combined with the longer time consumption

of using the latter mode of transport. Only when car-pooling can it be viable on a cost basis.

26 | P a g e

Rail service

More research has been conducted with respect to rail service as a substitute mode of

transportation with the introduction of the high-speed trains in Europe such as the TGV and

Euros tar. It can be argued132 that shorter average travel distances and competition from the

high-speed train services will mean that air route density in Europe will not reach US levels,

where the rail network is much less developed and has no high-speed trains apart from The

Acela Express that runs between Boston and Washington D.C. in the densely populated

Northeast Corridor. This service shares the problem of the Euro star in the UK part of its

network that the rail tracks.

3.3.3. RIVALRY AMONG COMPETITORS

The last area of the five forces is the rivalry among existing players. The rivalry in the airline

industry is very intense for many reasons. The industry is currently very stagnant. It seems to

be in the mature stage of the business cycle. The number of competitors stays the same in the

long run and it doesn‟t seem to be under or over capacitated. The fixed costs are extremely

high in this industry. This makes it hard to leave the industry because they are probably in

long term loan agreements in order to stay in business. The products involved or the planes are

highly complex which also heightens the competition.

Competition among major players is extremely intense in many aspects. Switching costs are

generally low, even though companies have tried to increase switching costs with the use of

"frequent yer" programs. Highly competitive industries generally earn low returns because the

cost of competition is high. This can spell disaster when times get tough in the economy.

Rivalry among existing firms in this industry has increased over the last 15 years as market

liberalisation has led to increased competition. The low fare airlines have been able to lower

the prices of airfares through their business models focusing on price leadership forcing full

service airlines to also lower their prices to avoid losing more market share.

Competitive rivalry in the Indian airline low industry can be can be split up in two parts:

Rivalry between low fare airlines and full service airlines creating subsidiaries or other

methods to compete with the prices offered by the former.

Internal rivalry between low fare airlines.

The issue of competition will not be explored more in-depth in this section as it will be

analysed more comprehensively in the competition analysis later in this thesis.

27 | P a g e

3.3.4. BARGAINING POWER OF SUPPLIER

Next we look at the bargaining power of the suppliers. In this case the major suppliers are the

airplane manufacturers. The top two manufacturers in the world currently are Boeing and

Airbus(Odell, Mark). In this industry the inputs are extremely standardized. Airline companies

only seem to differentiate with amenities. The planes are very similar. Currently some

manufacturers are trying to make their plans more eco-friendly.

Airline companies cannot easily switch suppliers. Most firms have long term contracts with

their suppliers. Planes are such high capital products that firms probably make long term loan

agreements and have more favourable credit terms when they don‟t switch companies. It is

difficult to enter into the plane manufacturing industry because of the capital needed to enter.

The amount of money and expertise needed to make even one plane is around 200 million

dollars. For this reason there are very few suppliers in the airline industry. Airline firms are the

only source of income for these manufacturers so their business is extremely important. Based

on these things the bargaining power of suppliers has a low threat as well.

Aircraft Manufacturers

Suppliers have a strong bargaining position if they are concentrated. This is, in particular, the

case for the aircraft manufacturers because only a few companies are producing aircraft. There

are effectively only two major global players in the aircraft business with regards to larger

aircraft and that is Boeing of the US and Airbus, which is a European consortium. Other

companies such as Bombardier of Canada are focusing on smaller regional aircraft and a

company such as Gulfstream focuses mainly on business jet aircraft.

Airlines cannot substitute aircraft by any other products and these are therefore an important

factor for the airlines, which strengthens the position of the aircraft manufacturers. However,

in the light of the recent downturn in air travel over the past few years demand for aircraft has

fallen dramatically making the bargaining position of the aircraft manufacturers in this

contract, suggestions that Boeing had been forced to give a 30% discount from the official list

price was not denied.

Labour

Airlines are dependent on their skilled employees, especially pilots and technical personnel.

Network airlines are particularly vulnerable to disruptions at their hubs, which increases the

28 | P a g e

power of unions at these locations. For other services, like station/ground services, general

administration, and marketing/distribution, outsourcing is an alternative that has been widely

used.

Unions tend to be local monopolies. In airlines there are usually different unions for different

types of staff, with each of them having the ability to disrupt operations. Union power and

regulation have led to a significant lack of downward flexibility in staffing levels and wages,

especially for legacy airlines. There are significant cost differences between new entrants,

companies in bankruptcy protection, and unionized incumbents, where high wages continue to

be paid relative to other industries, especially for employees with specialized skills like pilots.

Employees have traditionally been one of the groups most successful in capturing the value

created by the airline industry. They remain powerful where labor regulations and the hub-

spoke system given them critical leverage. Because union power often rises as companies

mature, the nature of labour relations also erodes industry structure by encouraging entry (and

bankruptcy) to avoid union-related costs, even if there is no other productivity advantage.

Airports

Many airports are local monopolies with limited competition from nearby secondary airports.

There is little entry by new airports, so the main check of the exploitation of market power is

through economic regulation or, to a lesser extent, competition policy (or potentially the licensing

policy if airport operations are put out on temporary license). The pricing power that the local

monopoly gives to an airport depends significantly on the potential traffic flows to which it

provides access.

Many airports have become more aggressive in their fee structures following privatization. But

many airports, especially in the US, continue to be used by local government to foster economic

development through subsidizing airlines‟ operations. On average airports do not earn their cost

of capital, but in Europe and the Asia-Pacific region they generally do.

Airport switching costs are high, especially for network airlines that are focused on providing

connections. It is easier for point-to-point airlines, especially LCCs flying to larger metropolitan

areas with a number of airports or regional airports not served by network airlines. Cargo airlines,

too, might have a stronger position, especially where the logistical service includes different

modes of transportation.

Airports only marginally better profitability compared to airlines indicates that their effective

bargaining power has been limited. Their main impact on airline industry structure has been

29 | P a g e

through infrastructure capacity constraints and other operational practices that have limited

effective airline capacity adjustments in serving particular connections.

Ground Handling Services/Catering

Ground handling suppliers tend to operate as local monopolies or oligopolies. Airlines are

often the dominant or only buyers of the services provided by ground handling companies.

Their services are technically homogenous and there are many potential entrants outside the

industry with the necessary skills. Switching costs within the existing set of providers are

small. The main barrier to entry is regulation that gives service providers local monopoly

rights.

Most airlines still provide ground handling services themselves (estimated 60% of the market

in 2005) but the degree of outsourcing to independent handlers (24%) and airports (16%) is

expected to rise significantly. Some of the independent handlers belong to larger international

groups but the global market is still highly fragmented. The market for ground handling

services has been liberalized in the US and Europe; here the market share of independent

handlers is already the highest. Elsewhere, there is little competition and airlines usually

provide these services themselves. Many of the independent handlers are profitable, at levels

comparable to companies providing similar services in other parts of the economy.

Ground handling/catering providers have limited bargaining power, largely because airlines

have the option of providing the service in-house. More liberalization in this market will lead

to more outsourcing but limit the market power of these service providers by reducing entry

barriers.

Providers of debt financing have many alternatives for investment, and can demand financing

terms that create solid returns taking into account the risks of the airline industry.

Providers of equity capital, often critical to survival in times of distress, are able to push for

attractive conditions. Given the low overall market capitalization of the airline industry,

investors view equity positions in airlines as high risk but high-return opportunities.

3.3.5. BARGAINING POWER OF BUYERS

The airline industry is made up of two groups of buyers. First, there are individual flyers. They

buy plane tickets for a number of reasons that can be personal or business related. This group

30 | P a g e

is extremely diverse; most people in developed countries have purchased a plane ticket. They

can do this through the specific airline or through the second group of buyers; travel agencies

and online portals. This buyer group works as a middle man between the airlines and the

flyers. They work with multiple airline firms in order to give customers the best flight

possible. Between these two groups there is definitely large amount of buyers compared to the

number of firms.

There are low switching costs between firms because many people choose the flight based on

where they are going and the cost at the time. This is some loyalty to firms but not enough for

high switching costs. Each customer needs a lot of important information. They need to know

the details of what is provided during the flight. Buyers need to understand the timing of the

flight and the safety aspects of flying in general. The service provided is unique. Each airline

has a niche. Some airlines focus on cost, while others focus on having the best amenities, etc.

Overall the bargaining power of buyers has an extremely low threat in this industry.

Business Customers

Frequency is a key differentiator among airlines of a similar type on a given connection.

Airlines have tried to create higher switching costs but these are meaningful mainly for

business travellers. Loyalty programs create switching costs; they have significant effect,

especially for business travellers. Expiration/„inflation‟ of frequent flyer miles creates

incentives to use miles/stay loyal to a given airline/alliance but reduce their value. Operational

coordination in alliances or a large own network is also creating some switching costs for

consumers; there is evidence of a (limited) hub premium for network airlines.

Leisure Customers

The choice of carriers is almost entirely based on price, with low willingness to pay for shorter

travel time or carrier-specific services. In transparent pricing structure due to price

discrimination (time of purchase, overall bundle, flexibility) creates incentives for consumers

to search for “better price”. In transparent additional costs for add-on services (baggage,

priority boarding, credit card use, booking fees, etc.) differentiate between airline types and

classes of services, but not within these groups. Service is highly similar across airlines, at

least within the broad classes of carriers (Network vs. LCC) but also across these groups for

economy class service. For leisure customers there are no inherent costs associated with flying

31 | P a g e

with another airline. Loyalty programs only matter for those passengers that are travelling

extensively on business.

Air Cargo Customers

Freight forwarders control 60% of the global market and wield significant power. Consistent

with this, they earn significant returns on capital relative to airlines.

OVERALL ASSESSMENT

SR. NO. FORCE CONDITION REASONS

1 Existing rivalry High

Limited Product

Differentiation, High Sunk

Cost, Low Marginal Cost,

Multiple Direct and Indirect

Rivals

2 Threat of New Entrance High

Low Switching Cost, High

Capital Requirement,

Demand Side Benefit of

Scale

3 Substitute products Medium

Technology for web-

conferencing if Improving,

No direct substitutes to

industry

4 Bargaining Power of

Supplier High

Aircraft and engine

producers both oligopolies,

Airports are local

monopolies with significant

power

5 Bargaining power of

Buyer High

Buyers are fragmented, Air

travel perceived as

standardized product, Low

switching Cost.

32 | P a g e

3.4 PEST ANALYSIS

PEST analysis is nothing but analysis of external environmental factors. The factors included in

PEST analysis are political/legal, economic, social-cultural, and technological. Each industry is

more or less affected by each of these factors. Every industry has to consider these factors because

these factors can create opportunity or threat at regular period of time. We will now discuss all

these factors in detail.

3.4.1. POLITICAL-LEGAL FACTORS

Many political factors affect and create opportunity or threat for the industry. Due to the

socialist leaning of some of the ministers many multinationals had to move out of India in the

late 70s. A deep-seated fear of multinationals made the political leaders to shut the door on

giant multinational companies for painfully long times. When things turned from bad to worse,

the situation was sought to remedy through a bold liberalization Programme in the early 90s.

Apart from a willingness to bend the rules and get along with the times, political stability is

also essential for economic growth. After liberalization steps taken by P.V. Narasimha Rao

government 1992, they could not make the bold decision on liberalization or could not

implement the planned programs because of the Babri Masjid demolition and subsequent

securities scams. The NDA government also could not go for bold decisions on

disinvestments, power sector reforms, and labor reforms etc. due to the scams of the ministers.

Recent UPA government is also find troubles because of the left parties who are giving

support.

The political party in power decides the legal framework. The government, therefore, may

legislate on matters like wage fixation, managerial remuneration, safety and health at work,

location of plants, entry of multinationals, price controls, import-export policy, licensing

policy etc. During the license-permit-raj that prevailed till the late 80s, licensing policies,

quota restrictions, import duties, FOREX regulations, restrictions on FDI flows, controls on

distribution and pricing of commodities, regulations on all aspects of corporate functioning,

had really put the captains of industry in a spot and pushed them to the wall. The liberalization

measures, macroeconomic reforms, and structural adjustments brought about in the early 90s

have altered the economic scenario quite dramatically. Obviously companies that want to do

business globally must pay attention to the above developments closely and learn to adapt

themselves to the laws of the land. The rules of competition, trademark rights, price controls,

33 | P a g e

product quality lows, and a number of other legal issues in individual countries may be of

special importance to global companies.

• Liberalization of the Sector • Interface form Other Agencies

• Excise Duty and Sales Tax on Aviation Turbine Fuel

• Modernization of Airports • Entry of Low Cost Carriers

3.4.2. ECONOMIC FACTORS

Economic factors throw light on the nature and direction of the economy in which the industry

operates. Interest rates, inflation rates, unemployment rates, gross national product, sectoral

growth rate of agriculture, industry infrastructure, level of disposable income, availability of

credits are some of the economical factors which affect more or less to each industry.

The World Economy

Demand for air travel is characterised by very high income elasticity. Research has shown that

there is a two-to-one relation between demand for air travel and world GDP. Therefore the

airline industry is very dependent on the world economy and its trade cycles. Particularly full

service airlines are susceptible to up- and downturns as they rely heavily on the high-yielding

Business Class/First Class passengers, who can be expected to drop in numbers when

economic activity is low. Another problem with the airline industry in the relation to the trade

cycle is that increasing capacity during upturns can be very difficult, as it often requires the

purchase of new aircraft.

However, the delivery time of an aircraft can be several years and if the airline, eager to prop

up capacity, purchases a large amount of aircraft, the trade cycle may be in a downturn at the

time of delivery, which means that these aircraft must stand idle as the capacity need is no

longer there, or be sold at a significant cost because of the lack of demand.

Therefore long-term planning is important within the airline industry as the investment in

aircraft is a significant financial burden, but of course predicting the development of the trade

cycle is evenly difficult.

Labour Costs

The level of labour costs usually also follow the level of economic activity. A higher level of

economic activity puts upward pressure on the wages as demand increases. However, in countries with

inflexible labour markets and/or strong unions, it is very difficult for airlines to reduce their labour

costs again through lowering wages or reducing the workforce, when theyare hit by downturns,

34 | P a g e

remembering from the research earlier mentioned that airlines generally are hit hard from a downturn

in the economy through the two-to-one correlation between air travel and world GDP.

Fuel Prices

The level of fuel prices has a profound impact on airline economics as the fuel costs constitute

10-14% of an airline‟s operating costs.85 This percentage obviously rises when fuel prices rise

sharply as is presently the case. Several measures can be taken by the airlines in order to lower

these costs.

Fuel-Efficient Aircraft

Through purchasing newer, more fuel-efficient aircraft, airlines can decrease the consumption

of fuel on their flights. Of course, airlines in financial peril often do not have this option as the

purchase of aircraft is very costly, so they cannot enjoy the long-term benefits of these more

fuel-efficient aircraft, as they would not be able to fulfil their short-term financial obligations

associated with such an investment. Additionally airlines specialising in short-haul flights

would benefit the most of more fuel-efficient aircraft as they use up more fuel, in relative

terms, than a long-haul flight as the largest consumption of fuel takes place in the processes of

take-off and landing. At cruising altitude (which is obviously longer on a long-haul flight) the

consumption of fuel is much lower.

3.4.3. SOCIAL FACTOR

The social factors that affect a firm include the values, attitudes, beliefs, opinions, and

lifestyles of persons in the social environment, as developed from demographic, cultural,

religious, educational, and ethnic conditioning. Like other forces in the external environment,

social factors change continually. As social attitudes, beliefs, and values change, so does the

demand for various types of dresses, books, leisure activities, etc.

• Developments in Airport Cities

• Employment Opportunities

• Ensuring a Level Playing Field

• Safety Regulation

• Increase in disposable income

• Increase in business travel

• Increase in consumer spending

35 | P a g e

Change In The Perception Of Air Travel

While air travel was earlier seen as an expensive cost and was not easily available financially

for lower- and middle class income groups, the low cost revolution that has made air travel

across Europe available to the larger public through lower fares.

3.4.4. TECHNOLOGICAL FACTOR

The Increasing use of the internet has provided money opportunities to airline. for e.g.

introduced a service, through the internet wherein the unoccupied seated are auctioned one

week prior to the departure. The internet also provided many internet based services to

customer such as online ticket booking, updated flight information & handling of customer

complaints.

Trade & development association is funding a feasibility study and workshop for the airports

authority of Indian as part of a long-term efforts to promote Indian aviation infrastructure. The

authority is developing modem communication, navigation, surveillance and air traffic

management systems for Indian aviation sector that will help the country meet the expected

growth and demand for air passenger and cargo service over the next decade.

These technological changes in the environment have an impact on airline industry in india as

well. Better airport infrastructure, means better handling of airplanes, which can help reduce

maintenance cost. It also facilities more flights to such destinations.

• Growth of Electronic Ticketing

• Satellite based Navigation Systems

• Technical Cooperation with EU

The Internet And Videoconferencing

The above mentioned factors are the most influential drivers of change in the airlines´

microenvironment regarding technological issues. However, as they influence the industry, it

is found more relevant to explore these topics more in-depth in the Five Forces industry

analysis in the next chapter under the sections of buyer power and threat from substitutes,

respectively, in order to compare them with others factors influencing the industry.

36 | P a g e

3.5 SWOT ANALYSIS

3.5.1 STRENGTH

Fastest transportation service.

Highly trained staff.

Ticket pricing is on the hand of players.

No substitute for international travellers as efficient as airlines.

Concentration on customer satisfaction.

High entry barriers to new player.

Large Route Network

Their extensive route network, particularly from its bases in London and Dublin but also ever

increasing in Continental Europe, provides it with a resource not available to all its

competitors as its customers can reach an airport close to almost any European destination at a

price below the competition. Although it was established in the previous section that most of

their cost advantage is lost when having to make a transfer on a point-to-point service like

Ryanair, one may still obtain a cheaper ticket than competitors for longer journeys between

smaller such as Aarhus-Palermo via London, where at least one transfer would also be needed

on any other airline increasing costs (at least from more airport fees and taxes) and travel time.

Network Of Business Partners

This network provides Ryanair with substantial ancillary revenue as shown in the financial

analysis through the mainly commission based partnerships with hotels, hostels, car rentals

etc. extending its value chain from just the traditional revenue stream of selling seats in an

aircraft to generating revenue both up and down the value chain from pre-flight revenue (e.g.

commission from airport buses) and post-flight (e.g. commission from car rentals).

Financial Resources

As shown in the example of its price war with Go in 2001 they have the financial resources to

force its competitors to retreat in price wars, which is a huge materialistic resource for an

airline as it enables it to defend its routes – and conquer other promising city-pairs. Its low

break-even load factor is also proof of the fact that Ryanair can sustain a prolonged period of

37 | P a g e

time with lower-than-average load factors and still remain profitable, where many other

airlines will sustain losses.

Non-Scheduled Revenues

Ryanair has achieved to bring in substantial ancillary revenue and profits through low-cost

ventures with various partners based on commission, which limits its risk exposure.

Furthermore they have achieved it solely by offering these services online through their

website, reducing the costs of providing the services to a minimum.

Other airlines are also beginning to offer these services (easyJet even as an integrated part of

their overall holding company as explained earlier), but Ryanair still has a competence here,

which other airlines have not yet been able to imitate with the same success.

Cost Leadership

Ryanair´s obvious competence is its ability to achieve cost leadership via its tireless efforts in

cutting costs throughout the organisation. These efforts conform to Porter‟s theory on

achieving overall cost leadership as analysed in the Ryanair case study, but it also conforms

with other theories.

With regards to its aim to achieve high market share and achieve economies of scale they also

conform with the PIMS (Profit Impact on Market Strategy) findings from where it may be

concluded that high volume and particularly high market share leads to lower overall costs and

is hence, related to higher profitability.221 Classical theory on the economies of scale per

product specification222 and production design and techniques223 as well as more recent

theory on lowering cost of input through bulk purchasing and standardisation224 (e.g.

homogenous fleet) and maximising capacity utilisation (e.g. low turnaround time) supports

Ryanair´s approach to cost leadership

Core Competence

Although Ryanair has created a competence in generating ancillary revenue, which is higher

than the industry in general and has therefore achieved a competitive advantage, I do not

assess this as a sustainable competitive advantage, making it a core competence, as this

competence can be duplicated with relative ease by its competitors as I cannot identify any

significant barriers to entry. Ryanair has a certain first-mover advantage that puts it higher on

the learning curve, but if the competition focuses on generating ancillary revenue as Ryanair

has done, I assess it as very feasible to reach the same competence, although Ryanair has an

38 | P a g e

advantage in its economies of scale and can therefore generate higher volume for its partners

in their network.

3.5.2 WEAKNESS

High maintenance cost.

Labour intensive industry.

Directly dependent on some other industry like tourism and corporate travellers.

High wages paid to the staff.

The Service Factor

As duplication is not an imminent threat or weakness as analysed above, one must consider the

scenario where customers may opt for other LFA´s where the no-frills approach is not as bare

bone as that of Ryanair. As mentioned earlier Southwest provides free soft drinks and snack

boxes on its flights as does Air Berlin and as the market matures passengers may consider

using an airline with a minimum of service. From its strategy of outsourcing customer related

functions such as call centers and check-in desks and the fact that it cannot be contacted by

neither phone (except for bookings) nor e-mail it is obvious that Ryanair puts little emphasis

on customer service and although I realise this is a part of their production design that leads to

lower costs one may consider options, which could create ancillary revenue to the company

but also give customers increased service value. A possibility would be to give customers

access to lounges, where this is possible as many of the airports services by Ryanair are

secondary airports without these facilities. However, at the airports with lounges operated by

e.g. Servisair, like Stansted and Dublin Airport customers could have the option at the time of

booking to buy an optional access to this lounge at a fee. This would generate

commissionbased

ancillary revenue for Ryanair and at the same time help terminate a potential weakness, while

giving passengers wishing to “upgrade” their service level this option. Also, Ryanair prides

itself for being “no. 1 for fewest complaints”228 but this does not necessarily mean they have

the most satisfied customers. The fact is that you cannot contact Ryanair´s customer service by

neither telephone, e-mail or letter correspondence. The only way of contacting them is by fax

and therefore many customers may refrain from contacting the airline as is would be too much

hassle for people not owning a fax and Ryanair also allow themselves 7 working days to

39 | P a g e

respond. They do, however, have contact phone numbers for each airport they serve in case of

lost baggage inquiries on arrival at the airports

Secondary and Provincial Airports

As it is an integral part of Ryanair´s strategy to use these airports as they are cheaper and less

congested it is also a double-edged sword as these airport are sometimes a significant distance

from the destination many passengers aim for. Airports that on Ryanair´s website are named

Brussels/Charleroi, Stockholm/Skavsta and Paris/Beauvais refer to the former being the

terminal destination for most travellers but the former being the airport and passenger can