Embed Size (px)

Citation preview

A STUDY OF FINANCIAL LITERACY LEVEL AMONG COLLEGE

STUDENTS

*Dr. BHAVNA SHARMA ** REENU KUMARI

*Assistant Professor, BPS Mahila Vishwavidyalaya, Khanpur Kalan, Sonipat.

**Research Scholar, BPS Mahila Vishwavidyalaya, Khanpur Kalan, Sonipat.

ABSTRACT

Purpose – The purpose of this paper is to assess the level of financial literacy among college students

and impact of various demographic variables on financial literacy level.

Design/methodology/approach – The proposed models in this paper use fisher exact test to examine

the relationship between financial literacy and demographic variables. Financial literacy level has

been measured by means of a questionnaire comprising several items, including basic financial

literacy, advanced financial literacy and demographic variables. The sample consists of 150 college

students.

Findings – The paper reveals that financial literacy among college students appears to be low. The

results suggest that college student‟s gender, education level and majors have a significant impact on

the financial literacy level.

Research limitations/implications – The main limitation of the empirical study is the small size of

the sample. A larger sample would have given more reliable results and could have enabled a wider

range of analyzes.

Originality/value – The current study is the first to examine the level of financial literacy and

focusing on the link between financial literacy level and demographic variables within the specific

context of Haryana.

Paper type - Research paper

Keywords: Financial Literacy, Demographic factors, Cross tabulation, Fisher‟s exact test

1. INTRODUCTION

Consumers must confront complicated financial decisions at a young age in today‟s demanding

financial environment, and financial mistakes made early in life can be costly (Lusardi et. al, 2009).

The importance of financial literacy has been arising with the deregulation of the financial markets

and the easier access to credit as various financial institutions create cut throat competition in

financial markets for holding greater market share, introduction of various advanced financial

products, and the government‟s initiatives for people to take more responsibility towards financial

decisions and for their retirement incomes (Beal & Delpachitra, 2003; Abraham & Marcolin, 2006).

Financial literacy has been defined as the competence to undertake rational and informed judgments

pertaining to money management (Worthington, 2006). Financial literacy includes general

understanding on saving, investment, spending, budgeting and money management skills and not only

understanding of these concepts but to take rational and informed decisions relating to money matters.

Emmanuel, K., O. (2010) identify some of the key elements of financial literacy skills and knowledge

is:

Mathematical literacy and standard literacy such as basic numeracy and comprehension skills.

Financial knowledge about the nature and main features of basic financial products and the risk

associated with these financial products.

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:4.236VOLUME 5, ISSUE 7, JULY 2017 UGC APPROVED JOURNAL -UGC JOURNAL SERIAL NO: 48817

An Open Access, Peer Reviewed, Refereed, Online and Print International Research Journalwww.icmrr.org 111 [email protected]

Financial competence such as the understanding of the main features of basic financial services,

appreciating the importance of reading and maintaining them, and an appreciation of the

relationship between risk and return.

Financial ability to make pertinent personal life choices about financial issues, and confidence to

seek assistance and support when things go wrong.

So it is very difficult for a common man to deal in complex financial markets and to understand the

risk associated with financial products. Financial literacy affects financial decision making; ignorance

about basic financial concepts can be linked to the lack of retirement planning, lack of participation in

the stock market, and poor borrowing behaviour (Lusardi, A. (2008). Improving individual financial

skills has increasingly been paid attention among various groups including governments, bankers,

employers, policymakers, practioners, researchers and academics both in developed and the

developing countries. In India the Reserve Bank of India (RBI) has undertaken a project titled

“project financial literacy” (2007) the main purpose of the project is to render information regarding

the central bank and general banking concepts such as financial products awareness (credit cards,

insurance, unit trust funds and employees provident fund etc) to various targeted groups, including

school and college going children, women rural and urban poor, defence personal and senior citizens.

The RBI released draft for national strategy on financial education and after that RBI came out with

the concept of financial literacy and credit counseling centers in 2009.

Previous studies have shown that large groups of population are financially illiterate; these

people were unable to manage their finance efficiently, and to plan adequately for their retirement.

This paper added to the existing literature by exploring what college students know and do not know

as determined by a set of simple questions that assessed their financial literacy level.

2. LITERATURE REVIEW

2.1 Financial Literacy

The literature on financial literacy has not expanded substantially in most countries; financial literacy

initiatives are jointly efforts of governments, central bank, regulatory authority‟s financial institutions

and non-governmental organization (NGOs) in addition to international agencies such as OECD and

World Bank. Financial literacy has been studied from different aspects government entities and

private organistaions in developing and developed countries have conducted surveys to measure the

financial literacy of their population. A study conducted by the OECD (2005) analysed the financial

literacy in 12 countries including the USA, the UK, Australia and Japan etc. and the study found that

the financial literacy level is very low for most of the respondents in these countries.

Carolynne, & Richard, (2000) in the article „Conceptualising Financial Literacy‟ examined the nature

of the term financial literacy. The study points out the importance of financial literacy which is to be

encouraged in those who are not financially literate. The authors argued that financial awareness and

financial literacy are not synonymous and financial literacy is a complex phenomenon in need of an

adequate conceptualisation. These perceptions are exemplified by the existence of centers or bodies

dedicated to financial literacy all over the world. The authors search the current literature on financial

literacy and also the usance of the term „literacy‟. They state that the available definitions were found

to be lacking in giving a correct meaning.

ANZ Bank Study (2003) conducted a study with the title „ANZ Survey of Adult Financial Literacy in

Australia‟ it was Australia‟s first national survey on financial literacy was conducted on behalf of the

ANZ Bank by Ray Morgan Research. The study used a telephone survey of 3548 adults and an in-

depth survey of 202 adults and an interview for the study. The objective of the study was to test the

knowledge of respondents against an individual‟s needs and circumstances. The results of the survey

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:4.236VOLUME 5, ISSUE 7, JULY 2017 UGC APPROVED JOURNAL -UGC JOURNAL SERIAL NO: 48817

An Open Access, Peer Reviewed, Refereed, Online and Print International Research Journalwww.icmrr.org 112 [email protected]

indicated that whereas Australians overall were financially literate, only certain groups such as lower

income people, not working or in a unskilled work , people with lower saving levels were identified

financially illiterate. A strong correlation was found between financial literacy levels and socio

demographic factors.

Lusardi, M. (2006) study highlighted that the author developed a module on retirement planning and

financial literacy by using the data of health and retirement study conducted in 2004 in United States.

The module objective was to explore the hypothesis that poor planning may be a primary result of

financial illiteracy. For this purpose the module measured how workers make their saving decisions

and how they collect information for making these decisions. A sample of 1269 adults aged over 50

year was used for the study. And the finding indicated that there is a strong relationship between

financial knowledge and planning; in that those with financial knowledge were more likely to plan

and succeed in their retirement planning. The result also showed that overall financial literacy level is

low among older Americans and some particular groups are at risk. In addition to this the study also

found that the least literate are also the least likely to plan and save for retirement.

Lusardi, M. (2009) the study is developed to identify the link between financial literacy and

retirement planning by exploiting information about respondents financial knowledge acquired in

school before entering the labour market and certainly before starting to plan for retirement. The study

attempted to measure the financial literacy in two forms basic financial literacy and sophisticated

financial literacy. The study found that women showed much lower level of financial literacy than

men, where gender differences were statistically significant. The respondents were found to be

knowledgeable about the functioning of the stock market and risk diversification. The author used

multivariate analysis to link financial literacy with retirement planning holding other socioeconomic

factors constant. The result showed that financial knowledge is influential in retirement planning. The

overall finding of the study indicated that the impact of financial literacy index in the retirement

planning is positive and strongly influences retirement planning.

Seth, et. al. (2010) the study analysed the relationship between financial literacy and demographic

factors of respondents. The study indicated that the financial literacy of investors in Delhi and NCR

was different for different financial instruments. Around 96% of respondents have saving account in

the banks and only 30% had knowledge about National Savings Certificates Public Provident Fund. It

has also found that most of the people relied on the telecast in the TV channels. 98% of respondents

knew about life insurance but only 45% respondent‟s preferred life insurance as the most effective

financial instrument.

Navin, et, al. (2010) conducted a study entitled „Financial Inclusion in the Slums of Mumbai‟ the

study found that only one-third of the respondents had a savings bank account. Significantly, none of

the respondents had an account with any private sector bank. This poor percentage in the heart of the

financial capital of the nation and in areas surrounded by bank branches speaks of the poor state of

financial inclusion. It highlights the pressing need to step up efforts towards including the excluded.

The role of private banks in this area needs to be examined. Second, among those who did not have a

bank account, only 8% had ever tried opening a bank account but were unsuccessful. The remaining

had never approached a bank. Third, out of the respondents who did not have a bank account, only

one-fifth were saving privately. These are the persons who could be tapped by banks and brought

within the fold of the formal financial institutions. The vast number of the remaining (four-fifths)

respondents had either no savings or the desire to save.

Lusardi, A. (2011) conducted a study by using survey data from eight countries to document the level

of financial literacy around the world. The author used compound interest, inflation and risk

diversification questions in their survey for measuring financial literacy level of respondents. The

study found that financial literacy is very low around the world no matter of the financial markets

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:4.236VOLUME 5, ISSUE 7, JULY 2017 UGC APPROVED JOURNAL -UGC JOURNAL SERIAL NO: 48817

An Open Access, Peer Reviewed, Refereed, Online and Print International Research Journalwww.icmrr.org 113 [email protected]

development and type of financial services & products provided. The older population considers itself

well informed, but in reality they are less informed than average. Gender and education plays very

significant role in financial literacy level women are less financially literate than men and educated

people are more informed about financial matters. The author argued that financial literacy level

affects the retirement planning, saving and investment decisions.

Joseph, J. (2012) highlighted that a sample of 300 families of economically marginalized households

was taken for the study and descriptive statistics and regression analysis were used for data analysis.

The study found that overall financial literacy rate is excellent and 95.3 percent of population is

financial included. It is observed that financial literacy increases as there is increase in the general

level of literacy rate. Borrowing literacy is lower than other parameters of financial literacy. The

lower level of borrowing literacy makes the people to borrow makes them to have unproductive loans

or it may be at higher interest rate.

Mahdzan, & Tabiani, (2013) in their paper, tried to examine the influence of financial literacy on

individuals saving in the context of emerging market, Malaysia. The researcher conducted the survey

of 148 individuals by using convenience sampling technique in Malaysia. Using individual saving as

independent variable and financial literacy, saving regularity, gender, age, children, and experience as

dependent variables the study found that financial literacy is an important factor of individual saving.

And the study also found that there was a positive relationship between gender and the probability of

positive saving indicating that men have a higher probability of positive saving as opposed to women,

ceteris paribus, so it is important for policy makers to increase financial literacy of households by

implementing various financial education programs.

Bhushan, P. (2014) examined the awareness level and investment behavior of salaried individuals of

Himachal Pradesh towards financial products and also the relationship between financial literacy and

investment preferences for financial products. The author found that only 24.6% respondents had

invested in pension funds, which means most of the people do not plan for retirement which is not a

very healthy sign. Also 77.7% people had invested in life insurance which means that people are

aware about the importance of life insurance. Only 39.1% respondents invest in public provident fund.

Narula, S. (2015) in their study focused to identify and evaluate the financial literacy level of retail

investors of Delhi and analysed the impact of different demographic factors on financial literacy. And

also to understand the variation between personal investment decision of the investors of different

financial literacy level with respect to short, medium and long term. Through statistical measures such

as ANOVA, t-test and Friedman test, it was found that the investors had a medium level of knowledge

and skills in financial literacy. Significant difference was observed between financial literacy among

various age groups. The study also indicated that investment decisions were related to time period as

the preference of investors of same level of financial literacy was different in different time period.

2.2 Demographic variables

Demographic factors such as age, gender, education level, income levels and majors have been found

to influence the financial literacy level (Shaari, et al. 2013; Nga, H. et al. 2010; Chen & Volpe, 1998;

Aggarwal, M. & Gupta, M. 2014; Al- Tamimi et al. 2009). This study investigates the relationship

between gender, education level, education major (business/ non business) on financial literacy.

On the basis of review following hypothesis framed which is further tested in the form of sub

hypotheses:

H0: There is no significant impact of demographic variables on financial literacy level.

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:4.236VOLUME 5, ISSUE 7, JULY 2017 UGC APPROVED JOURNAL -UGC JOURNAL SERIAL NO: 48817

An Open Access, Peer Reviewed, Refereed, Online and Print International Research Journalwww.icmrr.org 114 [email protected]

Gender

Females have often been found to possess less financial literacy and awareness level compared to

males (Chen, & Volpe, 1998; Nga, H. et al. 2010; Bhushan, P. & Medury, Y. 2013). Chen, & Volpe,

(2002) found that men scores high on general concepts of finance, savings & borrowing, insurance

and investment compared to women. Females have more difficulty to cope up with economic and

financial market and product development than do males (Lusardi, A. 2011).

H0a. There is no significant difference between male and female financial literacy level.

Education level

More educated people are more informed, yet education is far from a perfect proxy for literacy

(Lusardi, A. 2011). Financial literacy level is positively related with the level of education and

participants with a highest educational degree have a higher level of personal financial literacy level

(Shaari, et al. 2013; Al- Tamimi et al. 2009; Bhushan, P. & Medury, Y. 2013).

H0b. There is no significant difference between financial literacy levels on the basis of education

level.

Majors (Business and non-business)

Chen & Volpe (1998, 2002) identified that business college students have higher personal financial

literacy compared to non business college students. Commerce students are better in comparison to

non commerce students with regard to financial literacy level (Aggarwal, M. & Gupta, M. 2014).

Accounting and finance majors youths have higher general financial awareness compared to

marketing and general majors (Nga, H. et al. 2010).

H0c. There is no significant difference between financial literacy level on the basis of

major/discipline.

3. PROBLEM STATEMENT AND CONCEPTUAL FRAMEWORK FOR THE STUDY

Indian economy is entering into second phase of financial sector reforms; as a result it will be

incorporated with world economy at a greater rapidity and will face increasing risk of adverse impact

of world economic crisis. This requires knowledge about the financial markets, advanced financial

products & services and also proper attitude as well as behavioral skills. These activities need

budgeting, planning and involve savings and investments, in this situation adequate level of financial

literacy is requisite for financial safety and security required for the individuals. It effects day to day

money management as well as long term requirement like buying home, children education, and

secure retirement. Lower level of financial literacy and ineffective money management skills can also

result in behavior that makes consumers more susceptible to a financial emergency. India is having

the largest young population in the world (UN report, 2014). For the economic development of a

country adequate level of financial literacy should be possessed by youth population. Keeping this in

view, the present study measures the financial literacy level of college students.

Following conceptual framework is adopted for the study on the basis of “How ordinary consumers

make complex economic decisions: Financial literacy and Retirement readiness” by Lurardi, &

Mitchell (2009).

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:4.236VOLUME 5, ISSUE 7, JULY 2017 UGC APPROVED JOURNAL -UGC JOURNAL SERIAL NO: 48817

An Open Access, Peer Reviewed, Refereed, Online and Print International Research Journalwww.icmrr.org 115 [email protected]

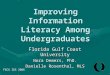

Basic financial literacy

Figure. 1

4. RESEARCH METHODOLOGY

4.1 Objectives of the study

i. To measure the financial literacy level of college students.

ii. To identify the impact of various demographic factors like gender, education level and majors

on the financial literacy level.

iii. To give suggestions for improving financial literacy.

4.2 Research Design: This study is descriptive in nature and survey method is employed.

4.3 Source of Data: Data required for the study is obtained from both secondary and primary sources.

Questionnaire was prepared for measuring financial literacy level by a series of questions based on

“How ordinary consumers make complex economic decisions: Financial literacy and Retirement

readiness” by Lurardi, & Mitchell (2009). A total of 13 questions were asked to test basic and

advanced financial literacy level.

4.4 Sample Description: The sampling unit is 150 students in the age group of 18 to 25 belonging to

different faculties of Science, Arts and Commerce students of a private and government higher

education institution in Haryana. Hypothesis testing was conducted through Fisher‟s Exact test.

5. RESULTS AND DISCUSSION

5.1 The profile of the study’s respondents

Table: 1

Characteristics Frequencies Percentage (%)

Gender

Male 67 44.7

Female 83 55.3

Education level

Graduation 74 49.3

Post graduation 76 50.7

Majors / Discipline

Business 86 57.3

Non business 64 42.7

Source: compiled from primary data

Basic financial

literacy:-

a) Simple interest

b) Compound

interest

c) Inflation

d) Time value of

money

e) Purchasing

power of money

Advanced financial

literacy:-

a) Stock market

functioning

b) Knowledge of mutual

funds

c) Interest rate and bond

price link

d) Safer: company stock

and Mutual fund

e) Riskier: stocks and

bonds

f) Long period returns

g) Highest fluctuation

security

h) Risk diversification

Overall

Financial

Literacy

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:4.236VOLUME 5, ISSUE 7, JULY 2017 UGC APPROVED JOURNAL -UGC JOURNAL SERIAL NO: 48817

An Open Access, Peer Reviewed, Refereed, Online and Print International Research Journalwww.icmrr.org 116 [email protected]

Table 1 gives the summary of the demographic characteristics of the respondents. From a total of 150

respondents, 44.7% of them were male and 55.3% of female. In terms of education level 49.3% were

graduates and 50.7% of them were post graduates. Majority of the respondents i.e. 57.3% in our

sample were from business discipline followed by 42.7% from non business discipline.

5.2 Financial literacy level

Table: 2 Descriptive Summary

Financial literacy questions Correct

Answers

(%)

Incorrect

Answers

(%)

Q1- Simple Interest 88.0 12.0

Q2- Compound interest 36.0 64.0

Q3- Inflation rate 68.0 32.0

Q4- Time value of money 54.0 46.0

Q5- Purchasing power 70.0 30.0

Q6- Stock market functioning 47.3 52.7

Q7- Knowledge of Mutual Fund 33.3 66.7

Q8- Interest Rate / Bond Prices Link 38.7 61.3

Q9- Safer 44.0 56.0

Q10- Riskier 62.7 37.3

Q11- Long Period Returns 42.7 57.3

Q12- Highest fluctuation 58.7 41.3

Q13- Risk diversification 46.7 53.3

Source: compiled from primary data

As Table 2 summarizes how participants answered financial literacy measurement questions. The

highest score recorded (88%) relates to the question about the simple interest calculation. And lowest

score recorded (33.3%) pertains to the knowledge of mutual funds and followed by (36%) compound

interest and (38.7%) relates to the interest rate and bond prices linkage. More than 50% of the

respondents have no knowledge about stock market and its functions, safety of stocks highest return

security and risk diversification questions. General knowledge of respondents risk diversification

(46.7%), highest return security (42.7%), stock market functioning (47.3%) and safety of stocks (44.0)

topics can be considered as low. Only 4 out of 13 statements have more than 60% correct answers.

This suggests that the respondent‟s financial literacy level is low.

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:4.236VOLUME 5, ISSUE 7, JULY 2017 UGC APPROVED JOURNAL -UGC JOURNAL SERIAL NO: 48817

An Open Access, Peer Reviewed, Refereed, Online and Print International Research Journalwww.icmrr.org 117 [email protected]

5.3 Effect of demographic variables on financial literacy

Table: 3 Fisher’s Exact test and Cross tabulation between the financial literacy level and

Gender

Financial literacy statements Male

(correct

answer %)

Female

(correct

answer

% )

Fisher’s Exact test

Q1- Simple Interest 80.6 94.0 Value

10.220

df

3

Exact Sig.(2-

sided)

.007

Q2- Compound interest 16.4 51.8 46.336 4 .001

Q3- Inflation rate 49.3 83.1 28.996 4 .001

Q4- Time value of money 52.2 55.4 5.277 4 .250

Q5- Purchasing power 71.6 68.7 2.936 4 .620

Q6- Stock market functioning 40.3 53.0 9.771 5 .063

Q7- Knowledge of Mutual Fund 29.9 36.1 8.129 5 .133

Q8- Interest Rate / Bond Prices Link 16.4 56.6 44.710 4 .001

Q9- Safer 28.4 39.8 6.084 3 .075

Q10- Riskier 47.8 74.7 12.645 3 .003

Q11- Long Period Returns 29.9 53.0 21.400 4 .001

Q12- Highest fluctuation 49.3 66.3 5.127 4 .252

Q13- Risk diversification 37.3 54.2 22.641 4 .003

Source: Created by authors

Cross tabulation results (Table: 3) show that 12 out of 13 financial literacy measurement statements

have more percentage of female respondents correct answers in comparison to male respondents. The

results of cross tabulation shows that male‟s financial literacy level is low.

Simple interest – Fisher‟s exact test statistics of 10.220 (Sig. value < 0.05)

Compound interest - Fisher‟s exact test statistics of 46.336 (Sig. value < 0.05)

Inflation – Fisher‟s exact test statistics of 28.996 (Sig. value < 0.05)

Interest rate / bond price linkage - Fisher‟s exact test statistics of 44.710 (Sig. value < 0.05)

Risk associated with securities – Fisher‟s exact test statistics of 12.645 (Sig. value < 0.05)

Long period returns – Fisher‟s exact test statistics of 21.400 (Sig. value < 0.05)

Risk diversification – Fisher‟s exact test statistics of 22.641 (Sig. value < 0.05)

More than half of the statements have Fisher‟s exact test p- value (Sig. value < 0.05) indicated that

there is significant difference in financial literacy level of respondents on the basis of gender.

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:4.236VOLUME 5, ISSUE 7, JULY 2017 UGC APPROVED JOURNAL -UGC JOURNAL SERIAL NO: 48817

An Open Access, Peer Reviewed, Refereed, Online and Print International Research Journalwww.icmrr.org 118 [email protected]

Table: 4 Chi-square test (Fisher’s exact test) and Cross tabulation between the Financial

literacy level and Education level

Financial literacy statements Graduatio

n (correct

answer %)

Post

graduat

ion

(correc

t

answer

% )

Chi-square value

(Fisher’s Exact test)

Q1- Simple Interest 86.5 89.5 Value

2.572

df

3

Exact

Sig.(2-

sided)

.470

Q2- Compound interest 23.0 48.7 12.723 4 .008

Q3- Inflation rate 58.1 77.6 9.412 4 .034

Q4- Time value of money 51.4 55.6 6.518 4 .147

Q5- Purchasing power 74..3 65.8 3.268 4 .542

Q6- Stock market functioning 36.5 57.9 34.441 5 .001

Q7- Knowledge of Mutual Fund 41.9 25.0 16.604 5 .003

Q8- Interest Rate / Bond Prices Link 43.2 34.2 5.719 4 .217

Q9- Safer 43.2 44.7 12.052 3 .004

Q10- Riskier 54.1 71.1 14.949 3 .001

Q11- Long Period Returns 41.9 43.4 10.809 4 .020

Q12- Highest fluctuation 44.6 72.4 15.155 4 .003

Q13- Risk diversification 45.9 47.4 3.117 4 .533

Source: Created by authors

As Table 4 summarize the Cross tabulation and Fisher‟s exact test results for measuring the

association between education level and financial literacy level. Cross tabulation results show that 10

out of 13 financial literacy measurement statements have more percentage of post graduate

respondents correct answers in comparison to graduate respondents. The results indicated that post

graduate college students are more financial literate in comparison to graduate students.

Compound interest - Fisher‟s exact test statistics of 12.723(Sig. value < 0.05)

Inflation – Fisher‟s exact test statistics of 9.412 (Sig. value < 0.05)

Stock market functioning - Fisher‟s exact test statistics of 34.441 (Sig. value < 0.05)

Knowledge of mutual funds- Fisher‟s exact test statistics of 16.604 (Sig. value < 0.05)

Safety of stocks- Fisher‟s exact test statistics of 12.052(Sig. value < 0.05)

Risk associated with securities- Fisher‟s exact test statistics of 14.949 (Sig. value < 0.05)

Long period return security- Fisher‟s exact test statistics of 10.809 (Sig. value < 0.05)

Highest fluctuated security- Fisher‟s exact test statistics of 15.155 (Sig. value < 0.05)

8 out of 13 financial literacy statements have Fisher‟s exact test p- value (Sig. value < 0.05) indicated

that there is significant association between financial literacy level and education level. Our results

prove that null hypothesis is rejected and post graduate students are more financially literate in

comparison to graduate students.

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:4.236VOLUME 5, ISSUE 7, JULY 2017 UGC APPROVED JOURNAL -UGC JOURNAL SERIAL NO: 48817

An Open Access, Peer Reviewed, Refereed, Online and Print International Research Journalwww.icmrr.org 119 [email protected]

Table: 5 Chi-square test (Fisher’s Exact test) and Cross tabulation between the Financial

literacy level and Majors/ Discipline

Financial literacy statements Business

(correct

answer %)

Non

business

(correct

answer %

)

Chi-square value (Fisher’s

Exact test)

Q1- Simple Interest 91.9 82.8 Value

4.175

df

3

Exact

Sig.(2-

sided)

.232

Q2- Compound interest 39.5 31.3 4.561 4 .310

Q3- Inflation rate 61.6 76.6 4.339 4 .339

Q4- Time value of money 47.7 62.5 4.274 4 .336

Q5- Purchasing power 66.3 75.0 3.678 4 .441

Q6- Stock market functioning 54.7 37.5 38.102 5 .001

Q7- Knowledge of Mutual Fund 44.2 18.8 39.131 5 .001

Q8- Interest Rate / Bond Prices Link 39.5 37.5 4.549 4 .336

Q9- Safer 52.3 32.8 9.849 3 .012

Q10- Riskier 69.8 53.1 13.885 3 .001

Q11- Long Period Returns 55.8 25.0 23.180 4 .001

Q12- Highest fluctuation 68.6 45.3 13.462 4 .005

Q13- Risk diversification 55.8 34.4 17.318 4 .001

Source: Created by authors

Table 5 depicts the Cross tabulation and Fisher‟s exact test results for measuring the association

between education level and financial literacy level. Cross tabulation results show that 10 out of 13

financial literacy measurement statements have more percentage of business stream respondents

correct answers in comparison to non business stream respondents. The results indicated that business

students have more knowledge about financial concepts in comparison to non business students.

Stock market functioning - Fisher‟s exact test statistics of 38.102 (Sig. value < 0.05)

Knowledge of mutual funds- Fisher‟s exact test statistics of 39.131 (Sig. value < 0.05)

Safety of stocks- Fisher‟s exact test statistics of 9.849 (Sig. value < 0.05)

Risk associated with securities- Fisher‟s exact test statistics of 13.885 (Sig. value < 0.05)

Long period return security- Fisher‟s exact test statistics of 23.180 (Sig. value < 0.05)

Highest fluctuated security- Fisher‟s exact test statistics of 13.462 (Sig. value < 0.05)

Risk diversification- Fisher‟s exact test statistics of 17.318 (Sig. value < 0.05)

It is found that more than half of financial literacy statements have Fisher‟s exact test p- value (Sig.

value < 0.05) indicated that there is significant difference in financial literacy level on the basis of

majors and discipline. Therefore, we can reject our null hypothesis and business students are better in

comparison to non business students with regards to financial literacy level.

6. FINDINGS AND SUGGESTIONS

The results of the study strongly indicated that financial literacy level of college students is

very low. As a subsidiary finding, demographic factors such as gender, education level and

type of majors have positive impact on financial literacy level of the college students [Shaari,

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:4.236VOLUME 5, ISSUE 7, JULY 2017 UGC APPROVED JOURNAL -UGC JOURNAL SERIAL NO: 48817

An Open Access, Peer Reviewed, Refereed, Online and Print International Research Journalwww.icmrr.org 120 [email protected]

et al. 2013; Nga, H. et al. 2010; Chen & Volpe, 1998; Aggarwal, M. & Gupta, M. 2014; Al-

Tamimi et al. 2009].

Consistent to previous studies, business discipline students were found to have higher

financial literacy level. [Aggarwal, M. & Gupta, M. 2014; Nga, H. et al. 2010]

Financial Education should be provided at secondary and senior secondary level of education

and courses for managing personal finance can be offered to students in colleges. And these

courses should be made compulsory for all disciplines.

Campaigns for spreading awareness about financial literacy concepts and banking concepts

need to be intensified. This can be done through innovative dissemination channels including

films, documentaries, pamphlets and road shows.

Parents can also influence the behaviour of their children by developing the habits of savings,

planning, budgeting, consumer awareness etc.

Websites can be launched which offer free financial information to youth and these websites

must be reliable and committed to educate the youth on a wide range of financial and banking

concepts.

Government should support financial literacy programs and schemes in urban as well as rural

areas it was found that government supported projects and programs help common improving

their financial literacy.

Global guidelines and standards for financial literacy initiatives and consumer protection

frameworks in financial markets should be formulated.

In addition, the study implies that there is room for joint efforts of private and public

institutions of higher learning, financial institutions and the ministry of higher education to work

together in developing a comprehensive curriculum which is currently non-exists for improving

financial literacy and awareness level of students. Thus it becomes the need of the hour that

government as well as policy makers take necessary steps to improve the level of financial literacy

among population.

REFERENCES

1. Hussein A Hassan Al- Tamimi, Al Anood Bin Kalli (2009), “Financial literacy and

investment decisions of UAE investors”, The Journal of Risk Finance, Vol. 10, No. 5, pp.

500-516.

2. Beal D J and Delpachitra S (2003), “Financial literacy among Australian university students”,

Economic Papers, Vol. 22, No. 1, pp. 65-78.

3. Bhushan P and Medury Y (2013), “Financial literacy and its determinants”, International

Journal of Engineering, Business and Enterprise Applications, Vol. 4, No. 2, pp. 155-160.

4. Bhushan P (2014), “Relationship between financial literacy and investment behaviour of

salaried individuals”, Journal of Business Management & Social Science Research, Vol. 3,

No. 5, pp. 82-87.

5. Carolynne L J and Richard M (2000), “Conceptualising financial literacy” Business School

Research Paper Series, Loughborough University.

6. Chen H and Volpe R (1998), “An analysis of personal financial literacy among college

students”, Financial Service Review, Vol. 7, No. 2, pp. 107-128.

7. Chen H and Volpe R (2002), “Gender differences in personal financial literacy among college

students”, Financial Service Review, Vol. 11, pp. 289-307.

8. Emmanuel Kojo Oseifuah (2010), “Financial literacy and youth entrepreneurship in South

Africa”, African Journal of Economic and Management Studies, Vol. 1, Iss. 2, pp. 164 – 182.

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:4.236VOLUME 5, ISSUE 7, JULY 2017 UGC APPROVED JOURNAL -UGC JOURNAL SERIAL NO: 48817

An Open Access, Peer Reviewed, Refereed, Online and Print International Research Journalwww.icmrr.org 121 [email protected]

9. Joseph J (2012), “Financial literacy of economically marginalized people of Kerala”,

Unpublished data, School of Gandhian Thought and Development Studies, Mahatma Gandhi

University Kerala.

10. Lusardi A and Mitchell O S (2011), “Financial literacy around the world: An overview”,

National Bureau of Economic Research, Working paper no. 17107.

11. Lusardi A, Mitchell O S and Curto Vilsa (2009) “Financial literacy among the young:

Evidence and implication for consumer policy”, National Bureau of Economic Research,

Working paper no. 15352.

12. Lusardi A (2008), “Financial literacy: An essential tool for informed consumer choice?”,

National Bureau of Economic Research, Working Paper No. 14084.

13. Lusardi M and Mitchell O S (2006), “Financial literacy and planning: Implications for

retirement wellbeing”, Michigan Retirement Centre, Working paper 2005-108.

14. Lusardi M and Mitchell O S (2009), “How ordinary consumers make complex economic

decisions: Financial literacy and retirement readiness”, National Bureau of Economic

Research, Working paper no. 15350.

15. Mahdzan N S and Tabiani S (2013), “The impact of financial literacy on individual saving:

An exploratory study in Malaysian context”, Transformations in Business and Economics,

Vol. 12, No. 1, pp. 41-55.

16. Navin B and Arnav C (2010), “Financial inclusion in the slums of Mumbai”, Economic and

Political Weekly, October 16, 2010, Vol. 45 No. 42.

17. Joyce K H Nga, Lisa H L Yong and Rathakrishnan D Sellappan (2010), “A study of financial

awareness among youths”, Young Consumers, Vol. 11, No. 4, pp. 277-290.

18. Narula S (2015), “Financial literacy and personal investment decisions of retail investors in

Delhi”, International Journal of Science, Technology & Management, Vol. 4, No. 1, 33-42.

19. Organization for Economic Co-operation and Development (2005), “Improving financial

literacy: Analysis of issues and policies”, Organization for Economic Co-operation and

Development, Paris: OECD Publications, ISBN 92-64-01257.

20. Pallavi S, Patel G and Krishnan K K (2010), “Financial literacy & investment decisions of

Indian investors: A case of Delhi & NCR”, Birla Institute of Management Technology,

Greater Noida, India.

21. Roy Morgan Research (2003), “ANZ Survey of adult financial literacy in Australia”, ANZ

Banking Group, Melbourne, Roy Morgan Research, pp. 1-77.

22. Shaari A N, Hasan A N, Mohamed H M and Sabri J A (2013), “Financial literacy: A study

among the university student”, Interdisciplinary Journal of Contemporary Research Business,

Vol. 5, No. (2), pp. 279-294.

23. Worthington A C (2006), “Predicting financial literacy in Australia”, Financial Services

Review, Vol. 15, No. 1, pp. 59-79.

24. www.google.com

25. www.rbi.org.in

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:4.236VOLUME 5, ISSUE 7, JULY 2017 UGC APPROVED JOURNAL -UGC JOURNAL SERIAL NO: 48817

An Open Access, Peer Reviewed, Refereed, Online and Print International Research Journalwww.icmrr.org 122 [email protected]