Embed Size (px)

Citation preview

A SPECS-TACULAR INDUSTRY:

EYEWEAR

Meg CheeSteph HendartaBrian RodriguezEric Rodriguez

Agenda

Industry Introduction

Industry Overview

Pricing Strategies

Survey Data

Recommendations

Introduction

Introduction // Industry // Pricing // Survey Data // Recommendations

•Determine how Luxottica affects industry prices •Determine how other firms try to competeIndustry Leader

•Does Luxottica exert true monopoly power?•What lines of business does it own and operate?Monopoly?

•Potential impact of Essilor’s merger with Luxottica•Possibilities for better prices in the futureFuture

Introduction // Industry // Pricing // Survey Data // Recommendations

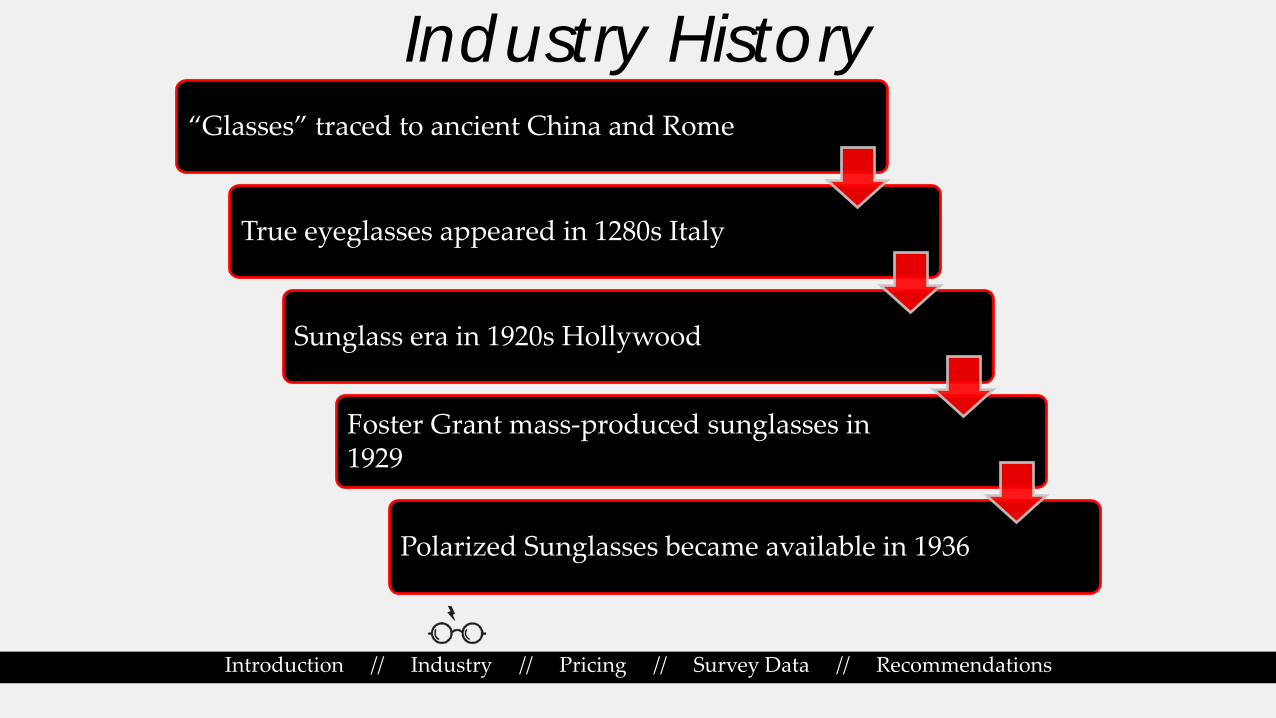

Industry History“Glasses” traced to ancient China and Rome

True eyeglasses appeared in 1280s Italy

Sunglass era in 1920s Hollywood

Foster Grant mass-produced sunglasses in 1929

Polarized Sunglasses became available in 1936

Dominant Player

Introduction // Industry // Pricing // Survey Data // Recommendations

Luxottica – Founded in 1961 • Founded by Leonardo Del Vecchio in Agordo, Italy• Now headquartered in Milan, Italy

Began Vertical Integration through M&A in 1974• Luxottica acquired the wholesale distributor Scarrone• Presence in manufacturing, wholesale, retail, and insurance

Building an Unmatched Brand Portfolio• In-house brands include Ray-Ban, Oakley, and many more• Licenses with many of the world’s most recognized brands

Sunglasses Retail

Introduction // Industry // Pricing // Survey Data // Recommendations

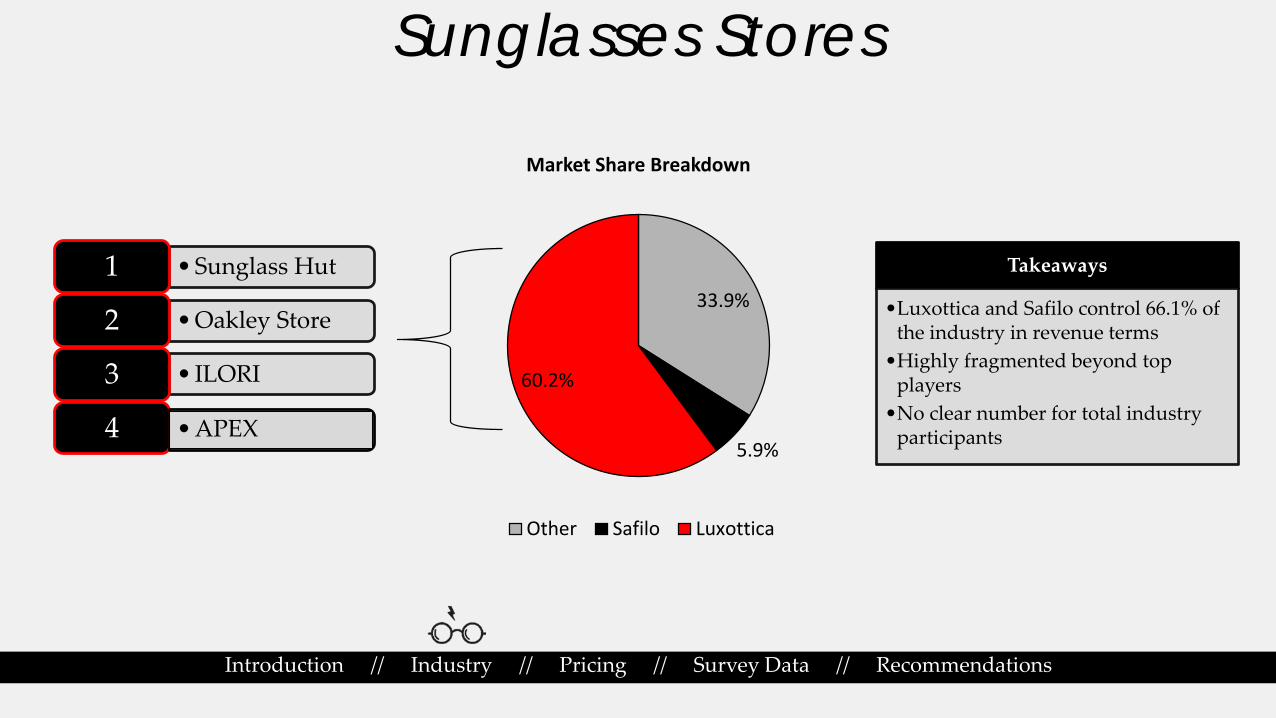

Sunglass Hut

Oakley

ILORI

APEX by Sunglass Hut

Solstice

Sunglasses Stores

Introduction // Industry // Pricing // Survey Data // Recommendations

•Sunglass Hut1

•Oakley Store2

• ILORI3

4

Takeaways

•Luxottica and Safilo control 66.1% of the industry in revenue terms •Highly fragmented beyond top

players•No clear number for total industry

participants

33.9%

5.9%

60.2%

Market Share Breakdown

Other Safilo Luxottica

•APEX

Eyeglasses Retail

Introduction // Industry // Pricing // Survey Data // Recommendations

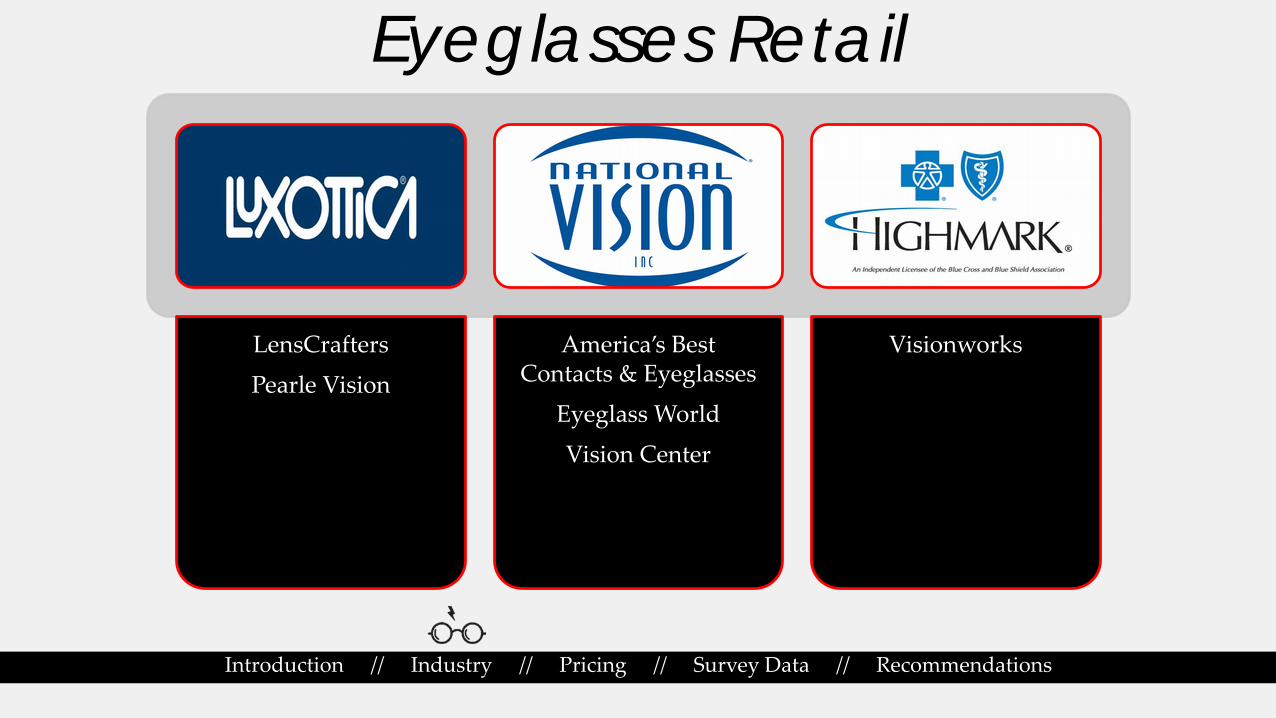

LensCrafters

Pearle Vision

America’s Best Contacts & Eyeglasses

Eyeglass World

Vision Center

Visionworks

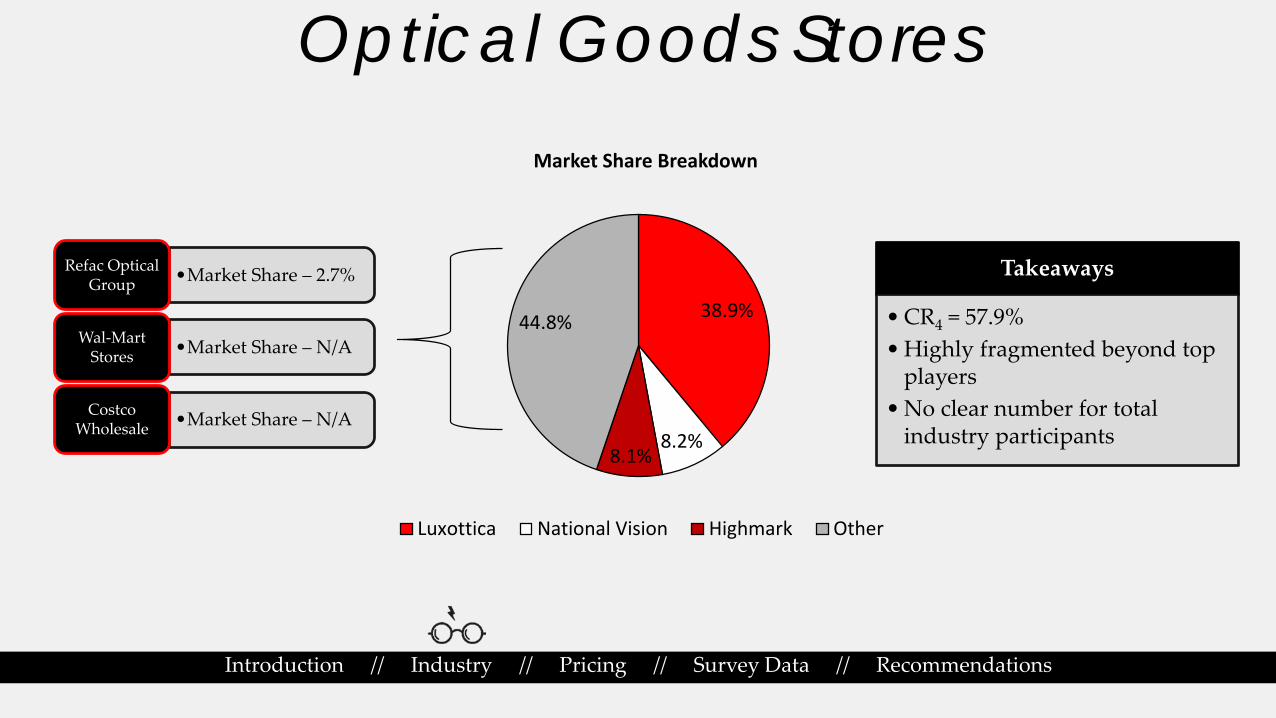

Optical Goods Stores

Introduction // Industry // Pricing // Survey Data // Recommendations

•Market Share – 2.7% Refac Optical Group

•Market Share – N/A Wal-Mart Stores

•Market Share – N/A Costco Wholesale

Takeaways

•CR4 = 57.9% •Highly fragmented beyond top

players•No clear number for total

industry participants

38.9%

8.2%8.1%

44.8%

Market Share Breakdown

Luxottica National Vision Highmark Other

Introduction // Industry // Pricing // Survey Data // Recommendations

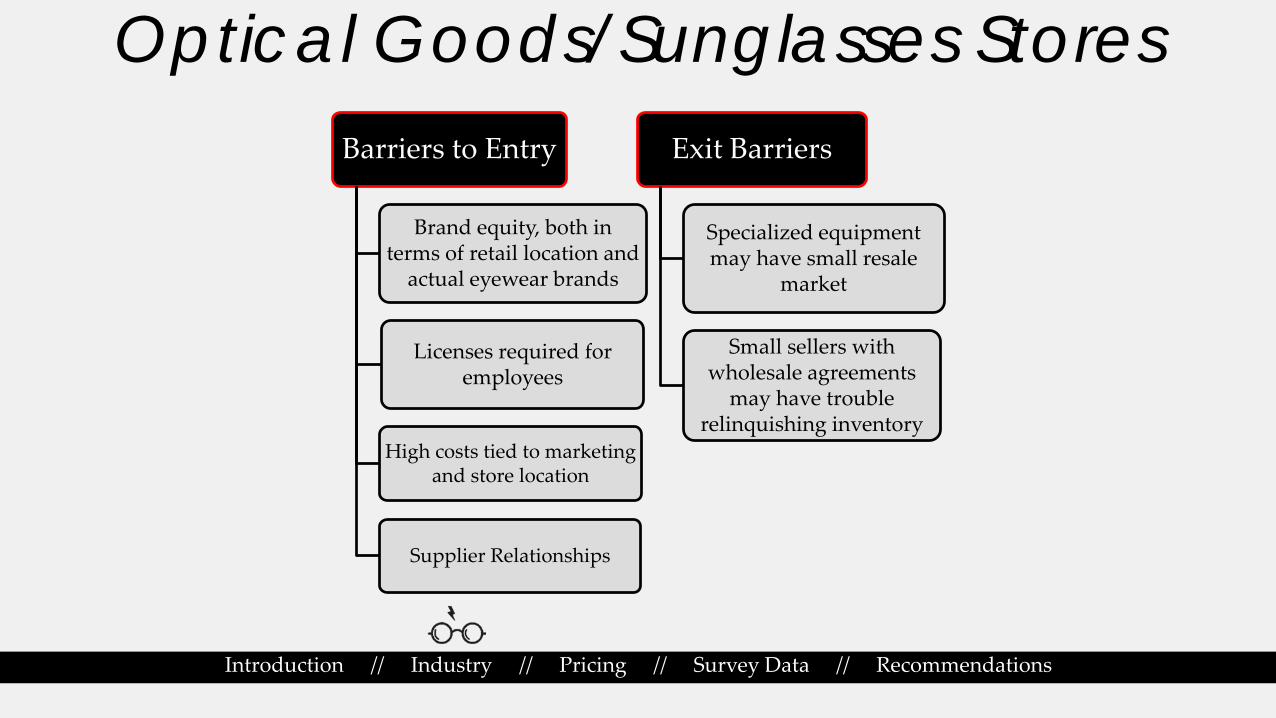

Optical Goods/Sunglasses Stores Barriers to Entry

Brand equity, both in terms of retail location and

actual eyewear brands

Licenses required for employees

High costs tied to marketing and store location

Supplier Relationships

Exit Barriers

Specialized equipment may have small resale

market

Small sellers with wholesale agreements

may have trouble relinquishing inventory

Introduction // Industry // Pricing // Survey Data // Recommendations

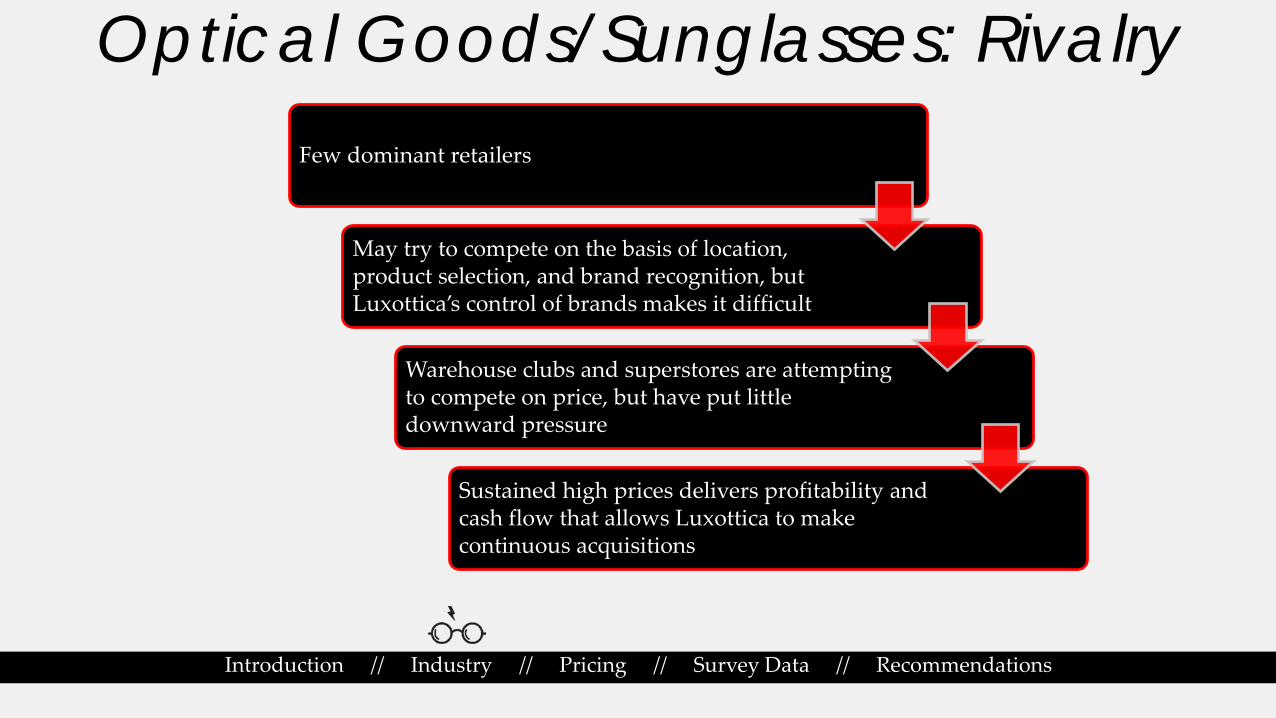

Optical Goods/Sunglasses: Rivalry Few dominant retailers

May try to compete on the basis of location, product selection, and brand recognition, but Luxottica’s control of brands makes it difficult

Warehouse clubs and superstores are attempting to compete on price, but have put little downward pressure

Sustained high prices delivers profitability and cash flow that allows Luxottica to make continuous acquisitions

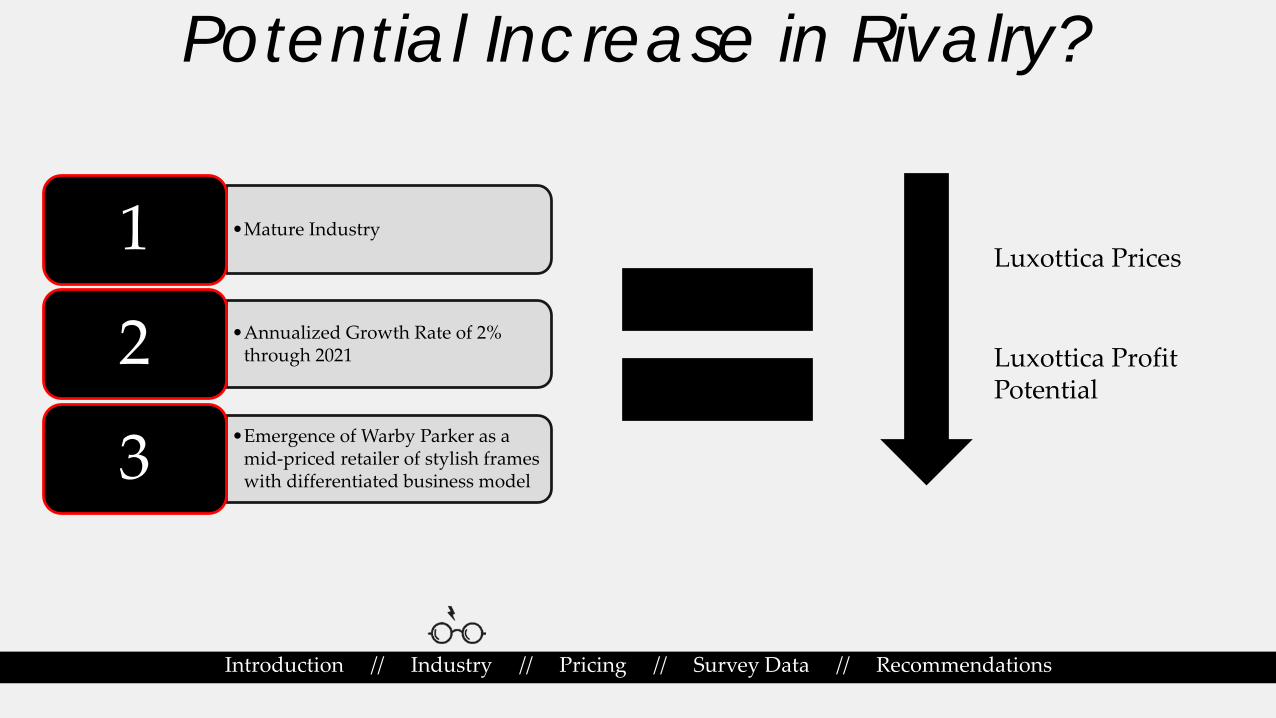

Potential Increase in Rivalry?

Introduction // Industry // Pricing // Survey Data // Recommendations

•Mature Industry1•Annualized Growth Rate of 2%

through 20212•Emergence of Warby Parker as a

mid-priced retailer of stylish frames with differentiated business model3

Luxottica Prices

Luxottica Profit Potential

Introduction // Industry // Pricing // Survey Data // Recommendations

Characteristic Differentiated Slightly Differentiated

Undifferentiated Comments

Design Frame and lens shape, frame size

Function Some differentiation may stem from lenses

Appearance/Brand Varied brand loyalties

Geo. Market Offerings regionally uniform

Price Wholesalers, superstores, Warby Parker

Age Group Discounted offerings to kids

Customer Service Warby Parker

Eyeglass/Sunglass Differentiation Matrix

Government Regulation

Introduction // Industry // Pricing // Survey Data // Recommendations

FDA Regulation• Eyeglasses and sunglasses considered Class 1 medical devices•Must follow status-quo FDA guidelines such as those related to flammable materials,

and the “Drop Ball” test

Employee Qualifications/State Rules• Various license requirements for optometrists and opticians• 4 states, including New York, have special laws governing over the counter eyeglasses

The FTC’s “Eyeglass Rule”• Requires that optometrists and ophthalmologists provide patients with a copy of their

prescription without extra costs or conditionality• Sen. Charles Schumer has pushed for revisions of the rule

Industry Organization

Introduction // Industry // Pricing // Survey Data // Recommendations

Follows a model of extreme vertical integration

•Full control over the supply chain•Design•Manufacturing •Distribution•Retail

•No outsourcing – everything is produced in-house•Most companies invest intensely on internal R&D•Large number of different models being designed and

manufactured, all with different seasonalities, life cycles and marketing strategies

Pros and Cons of Vertical Integration

Introduction // Industry // Pricing // Survey Data // Recommendations

Pros Cons

• Reduced transaction costs• Allows more efficient collaboration

between different units• No need to coordinate between different

organizations to outsource tasks • High degree of control over quality of

the products, which means a higher competitive advantage for luxury brands

• Less flexibility in the market• Less access to different methods and

technologies• Less variety in production

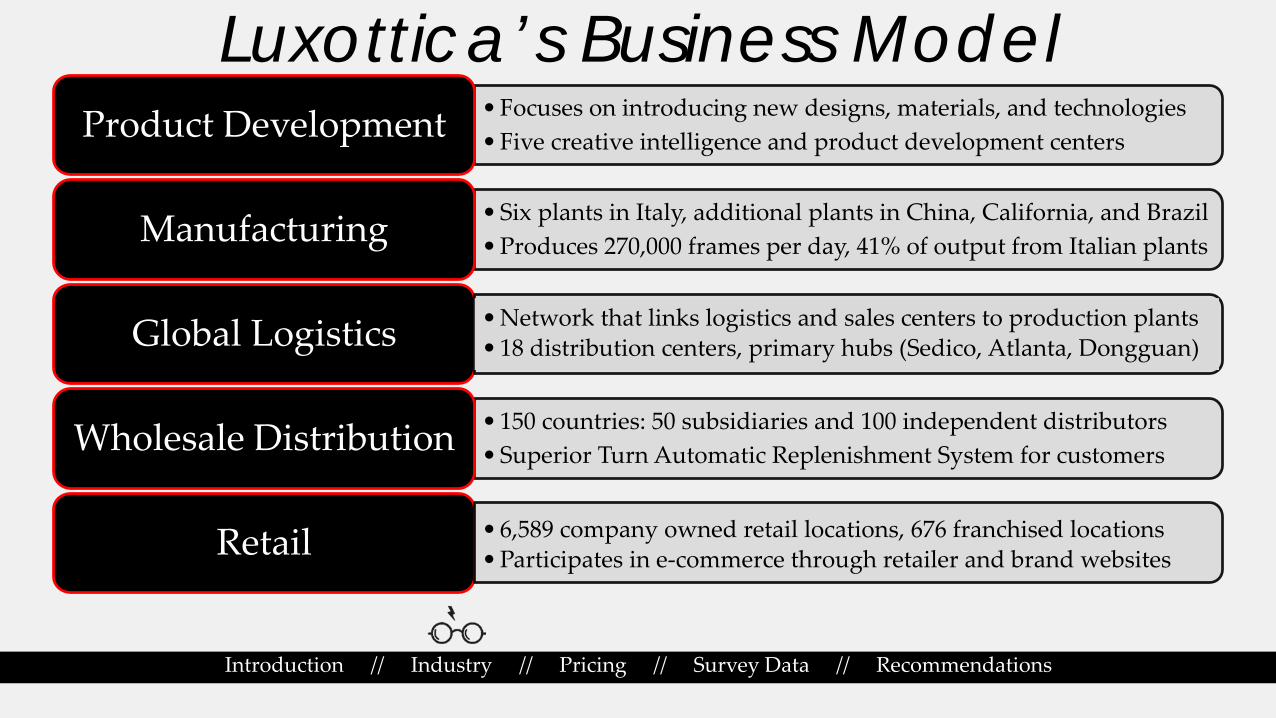

Luxottica’s Business Model

Introduction // Industry // Pricing // Survey Data // Recommendations

•Focuses on introducing new designs, materials, and technologies•Five creative intelligence and product development centersProduct Development

•Six plants in Italy, additional plants in China, California, and Brazil •Produces 270,000 frames per day, 41% of output from Italian plantsManufacturing

Global Logistics

•150 countries: 50 subsidiaries and 100 independent distributors•Superior Turn Automatic Replenishment System for customersWholesale Distribution

Retail

•Network that links logistics and sales centers to production plants•18 distribution centers, primary hubs (Sedico, Atlanta, Dongguan)

•6,589 company owned retail locations, 676 franchised locations•Participates in e-commerce through retailer and brand websites

Luxottica’s Brands

Introduction // Industry // Pricing // Survey Data // Recommendations

In-House Brands Licensed Brands

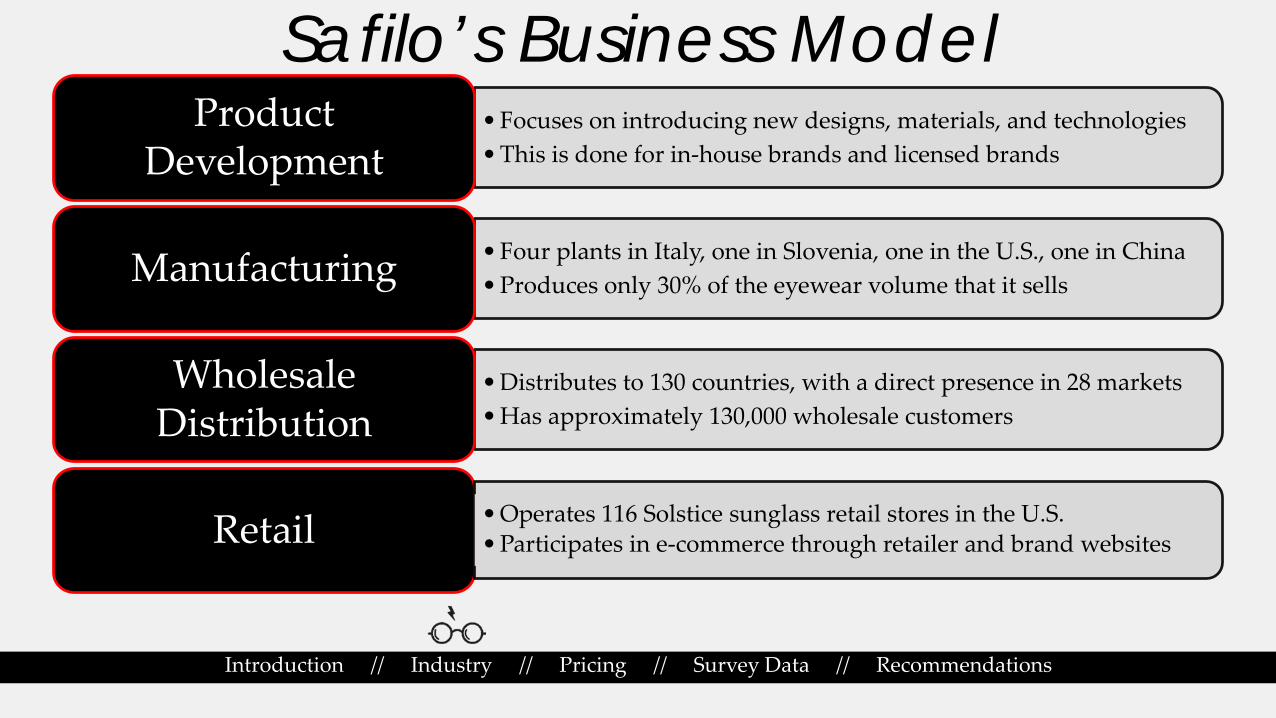

Safilo’s Business Model

Introduction // Industry // Pricing // Survey Data // Recommendations

•Focuses on introducing new designs, materials, and technologies•This is done for in-house brands and licensed brands

Product Development

•Four plants in Italy, one in Slovenia, one in the U.S., one in China•Produces only 30% of the eyewear volume that it sellsManufacturing

•Distributes to 130 countries, with a direct presence in 28 markets•Has approximately 130,000 wholesale customers

Wholesale Distribution

Retail •Operates 116 Solstice sunglass retail stores in the U.S.•Participates in e-commerce through retailer and brand websites

Safilo’s Brands

Introduction // Industry // Pricing // Survey Data // Recommendations

In-House Brands Licensed Brands

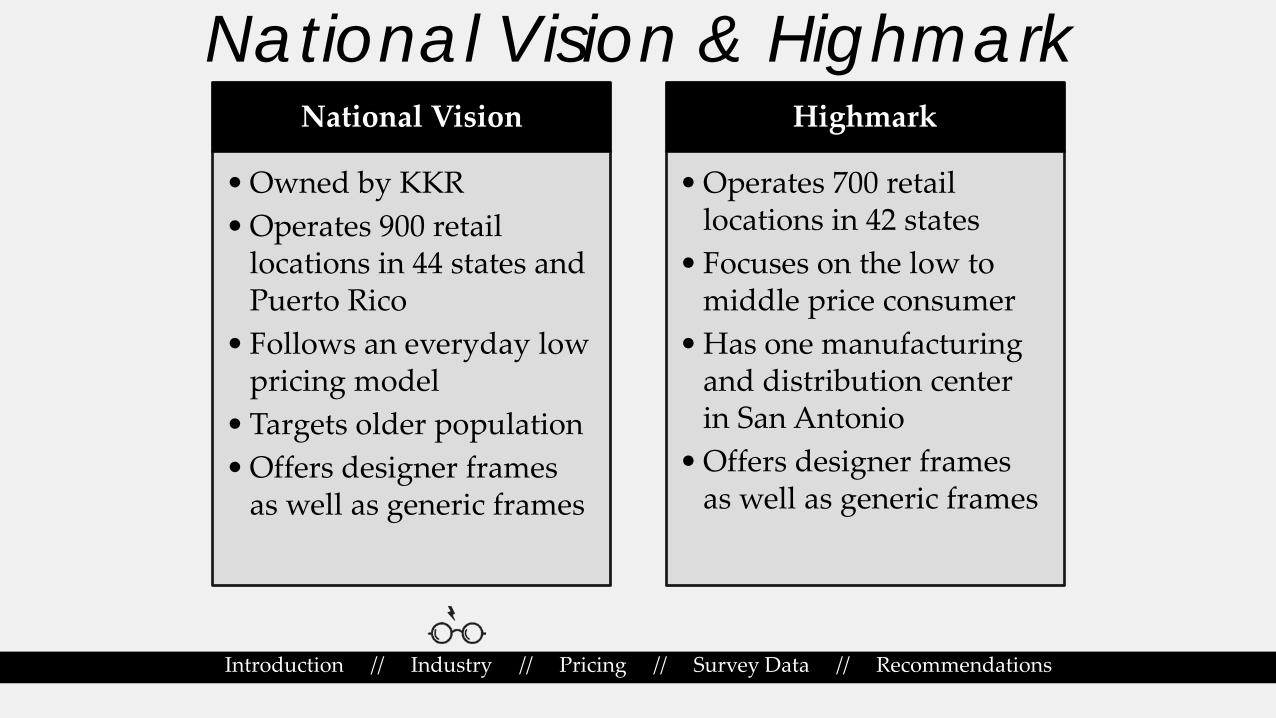

National Vision & Highmark

Introduction // Industry // Pricing // Survey Data // Recommendations

National Vision

•Owned by KKR•Operates 900 retail

locations in 44 states and Puerto Rico

• Follows an everyday low pricing model

•Targets older population•Offers designer frames

as well as generic frames

Highmark

•Operates 700 retail locations in 42 states

• Focuses on the low to middle price consumer

•Has one manufacturing and distribution center in San Antonio

•Offers designer frames as well as generic frames

Luxottica and Essilor Merger

Introduction // Industry // Pricing // Survey Data // Recommendations

$24 Billion Dollar Purchase Price• Combined firm to be called EssilorLuxottica• Deal follows four years of negotiations

Maximum Vertical Integration• Luxottica will now produce prescription lenses• Significant cost and revenue synergies

True Monopoly Power• Some analysts believe that the deal will pass• Lack of overlap in current business models

The End of Safilo?

Introduction // Industry // Pricing // Survey Data // Recommendations

Losing Licensing Agreements• Saint Laurent, Gucci, Armani, Alexander McQueen• Will most likely lose the Dior license

Diminishing Retail Presence• 300 Solstice stores in 2009, 116 remaining in 2016• May look to sell off remaining retail assets

Weak In-House Brands• Only 25% of revenue comes from in-house brands• Very difficult to compete with Ray-Ban and Oakley

Pricing Strategies

Introduction // Industry // Pricing // Survey Data // Recommendations

Extremely High Markup• Demonstrates Luxottica’s market power• Luxottica can be viewed as a price maker

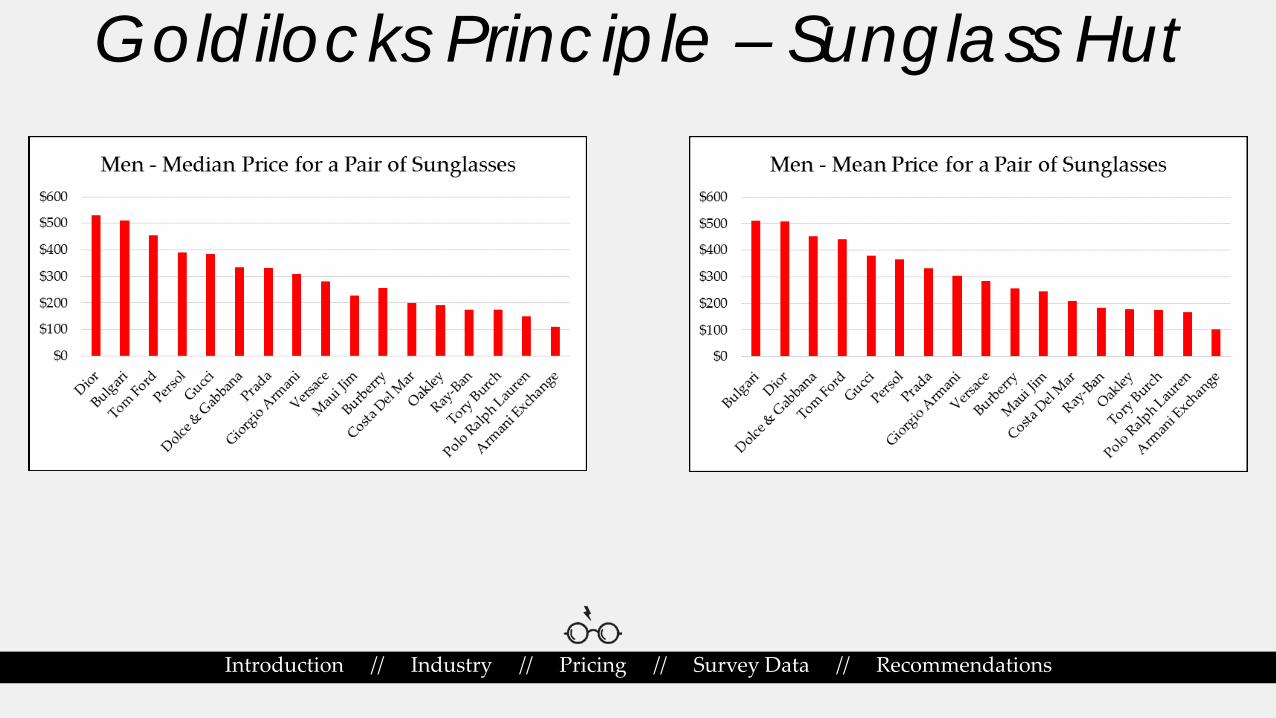

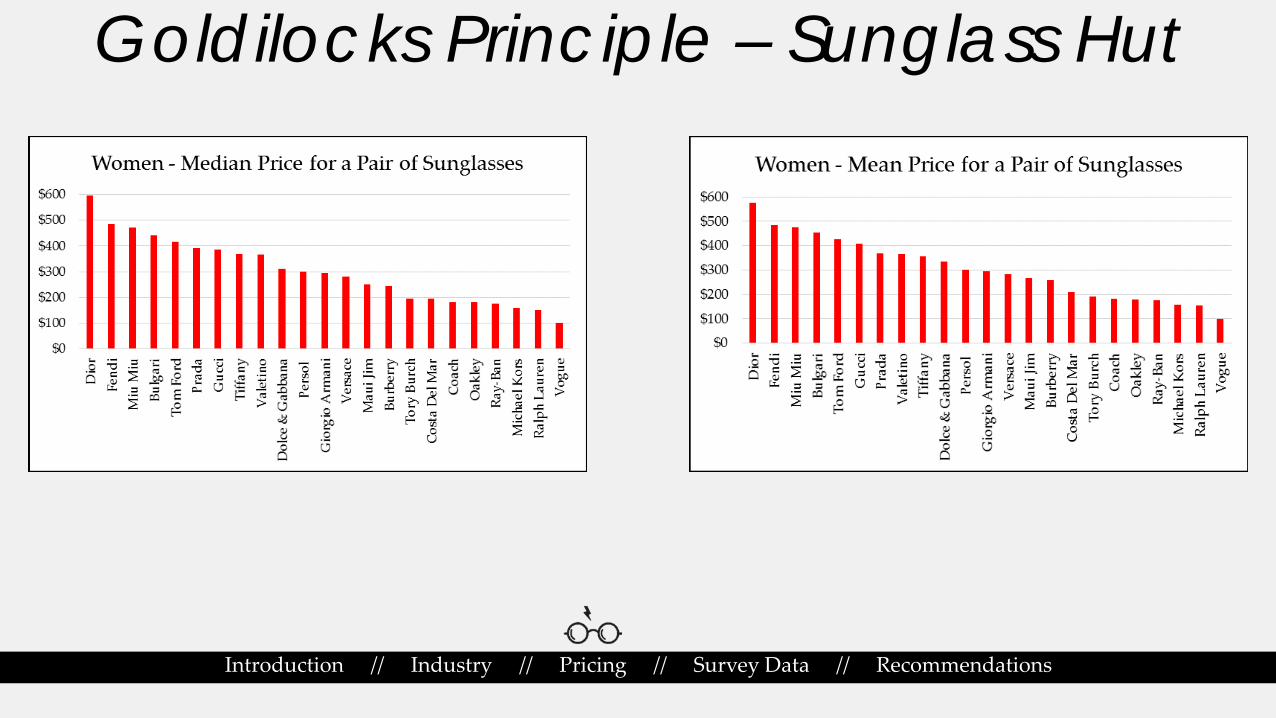

Goldilocks Principle• Pricing of popular in-house brands• Deviation from classic Goldilocks Principle

Tacit Collusion vs. Undercutting• Pricing in Sunglass Hut vs. Solstice• Price competition in prescription frame market

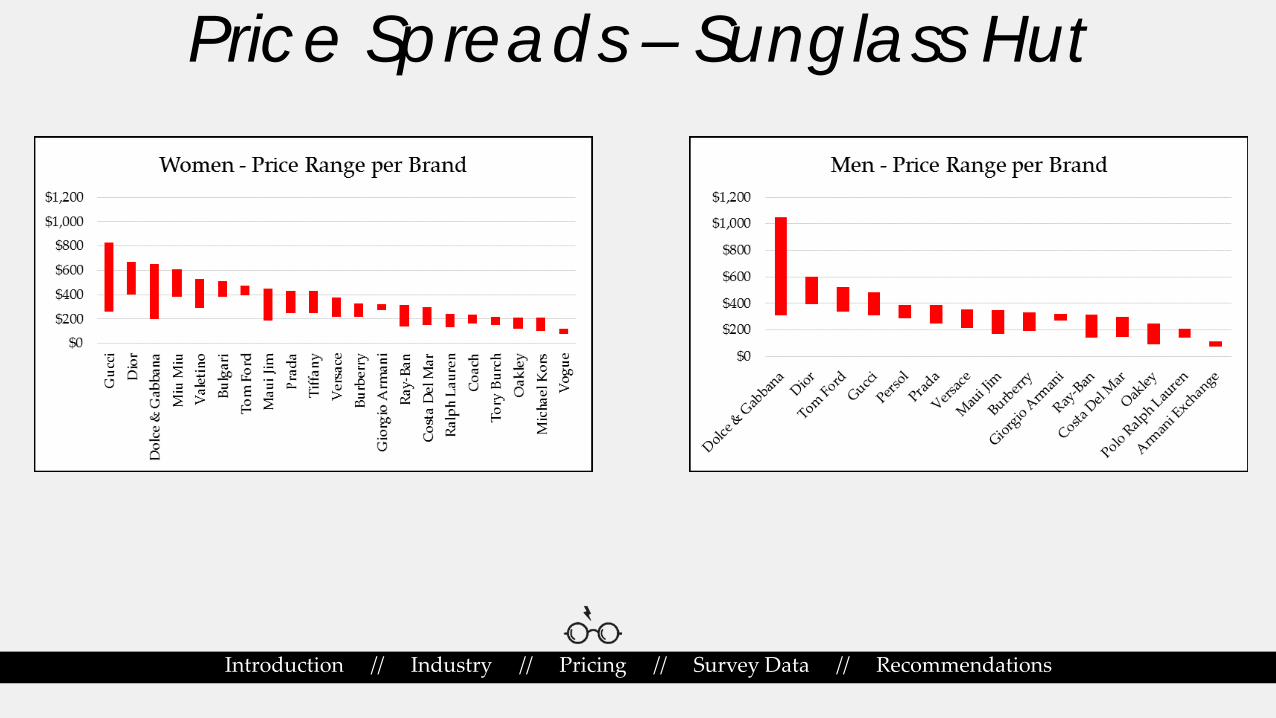

Illusion of Choice in Stores• Appearance of brand competition in retail• Similar price ranges for various brands

How High is the Markup?

Introduction // Industry // Pricing // Survey Data // Recommendations

Self-Selection in Stores

Introduction // Industry // Pricing // Survey Data // Recommendations

Second Degree Price Discrimination Through Brand Isolation!

Goldilocks Principle – Sunglass Hut

Introduction // Industry // Pricing // Survey Data // Recommendations

Goldilocks Principle – Sunglass Hut

Introduction // Industry // Pricing // Survey Data // Recommendations

Price Spreads – Sunglass Hut

Introduction // Industry // Pricing // Survey Data // Recommendations

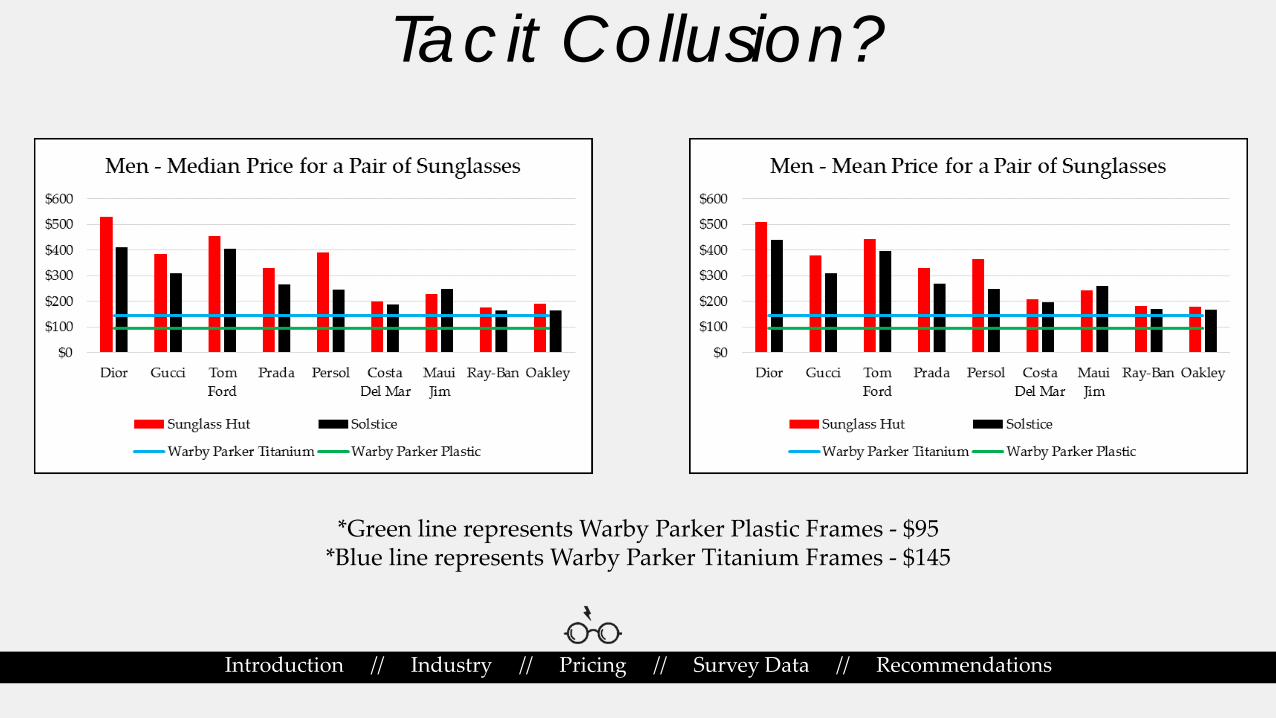

Tacit Collusion?

Introduction // Industry // Pricing // Survey Data // Recommendations

*Green line represents Warby Parker Plastic Frames - $95*Blue line represents Warby Parker Titanium Frames - $145

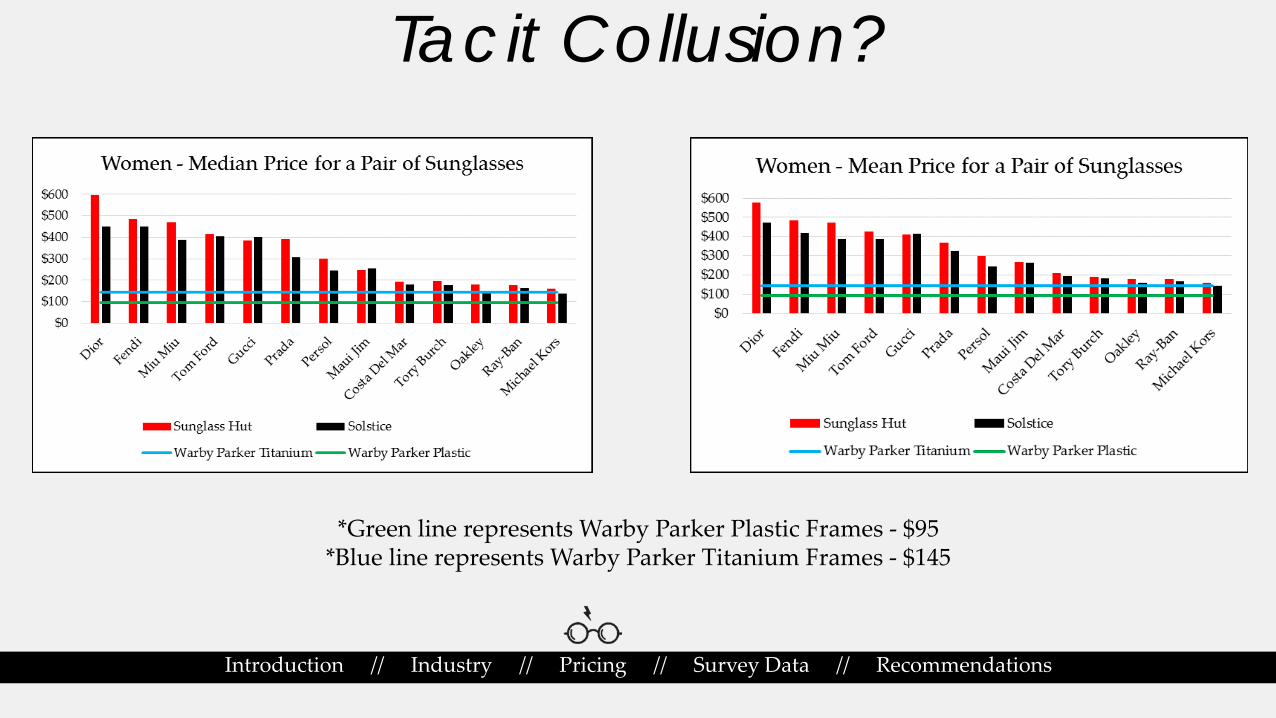

Tacit Collusion?

Introduction // Industry // Pricing // Survey Data // Recommendations

*Green line represents Warby Parker Plastic Frames - $95*Blue line represents Warby Parker Titanium Frames - $145

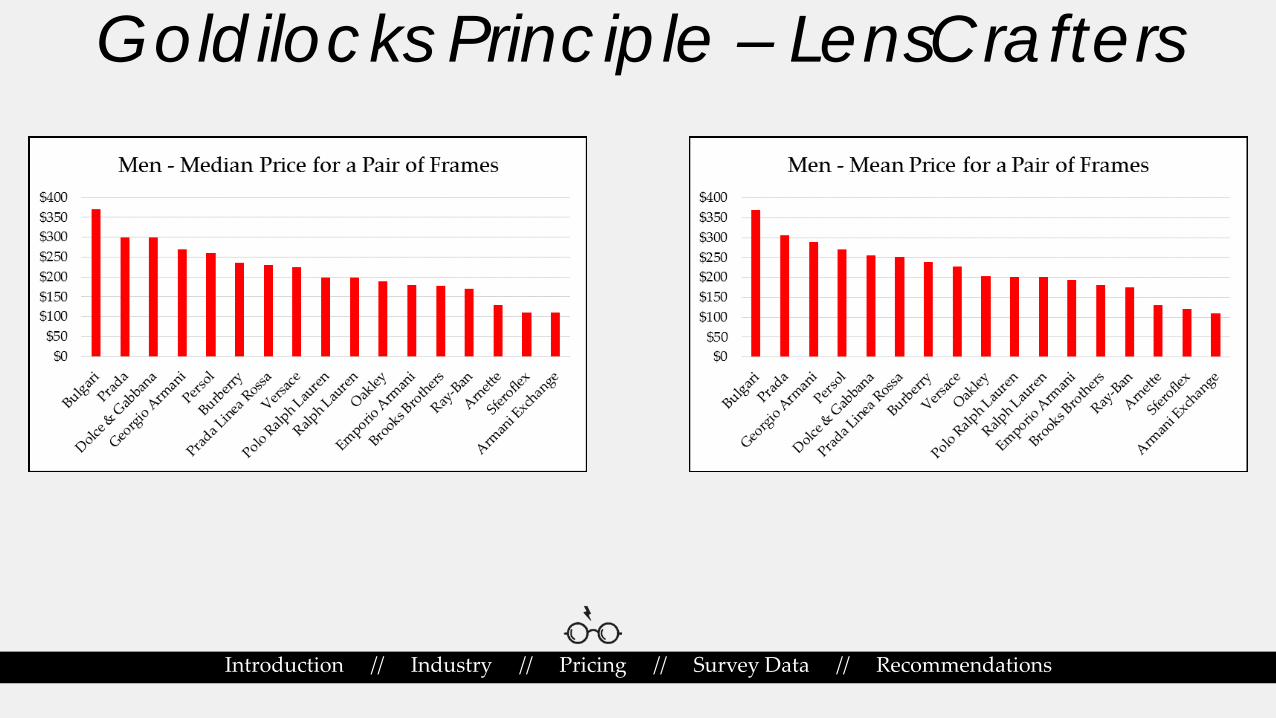

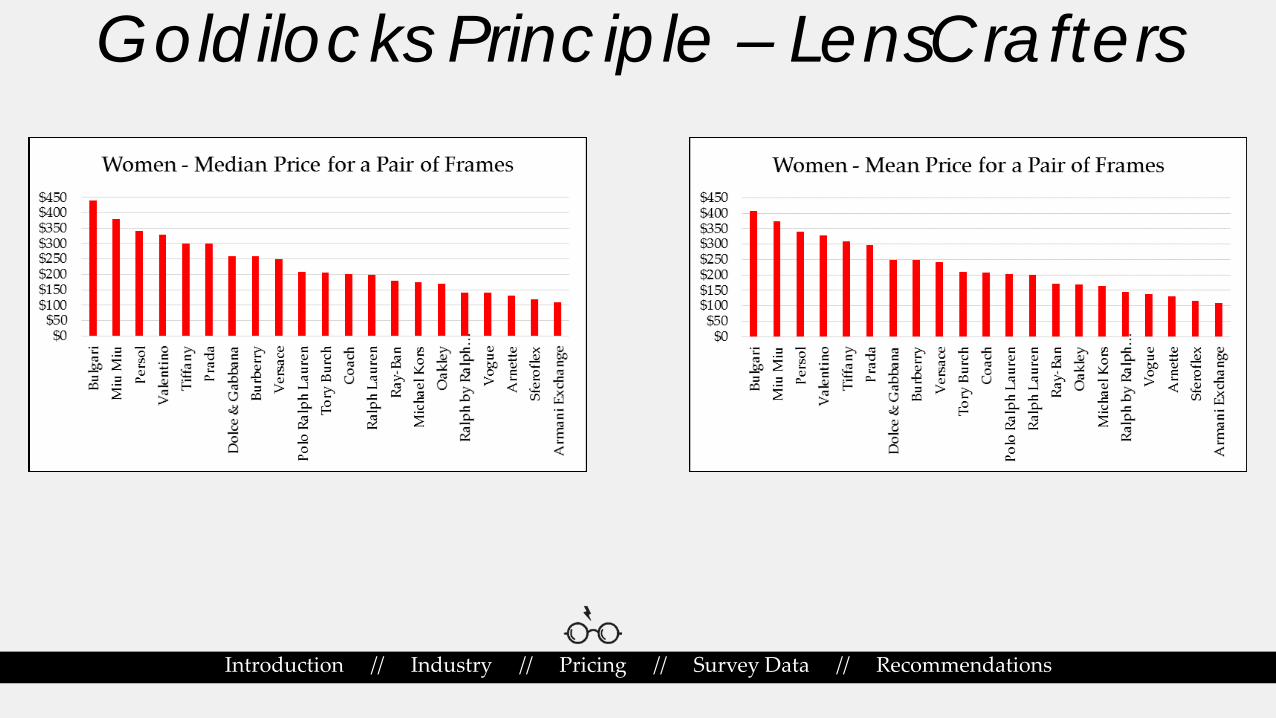

Goldilocks Principle – LensCrafters

Introduction // Industry // Pricing // Survey Data // Recommendations

Goldilocks Principle – LensCrafters

Introduction // Industry // Pricing // Survey Data // Recommendations

Price Spreads – LensCrafters

Introduction // Industry // Pricing // Survey Data // Recommendations

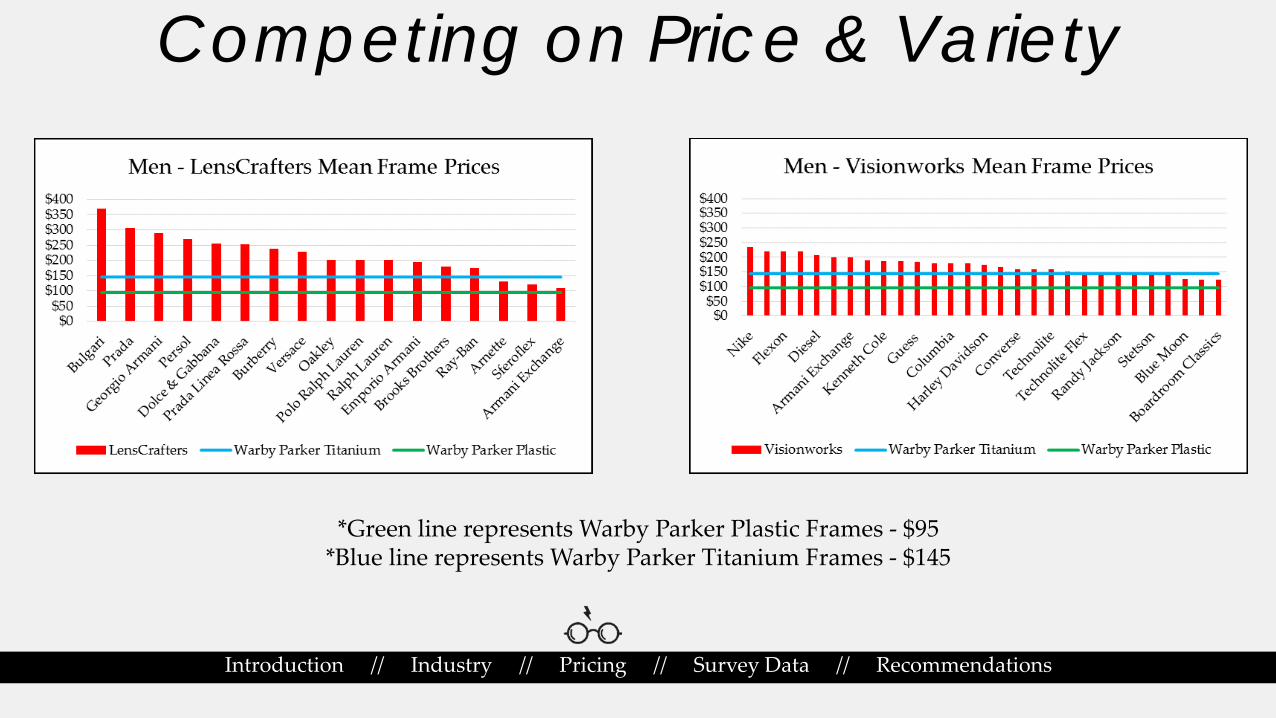

Competing on Price & Variety

Introduction // Industry // Pricing // Survey Data // Recommendations

*Green line represents Warby Parker Plastic Frames - $95*Blue line represents Warby Parker Titanium Frames - $145

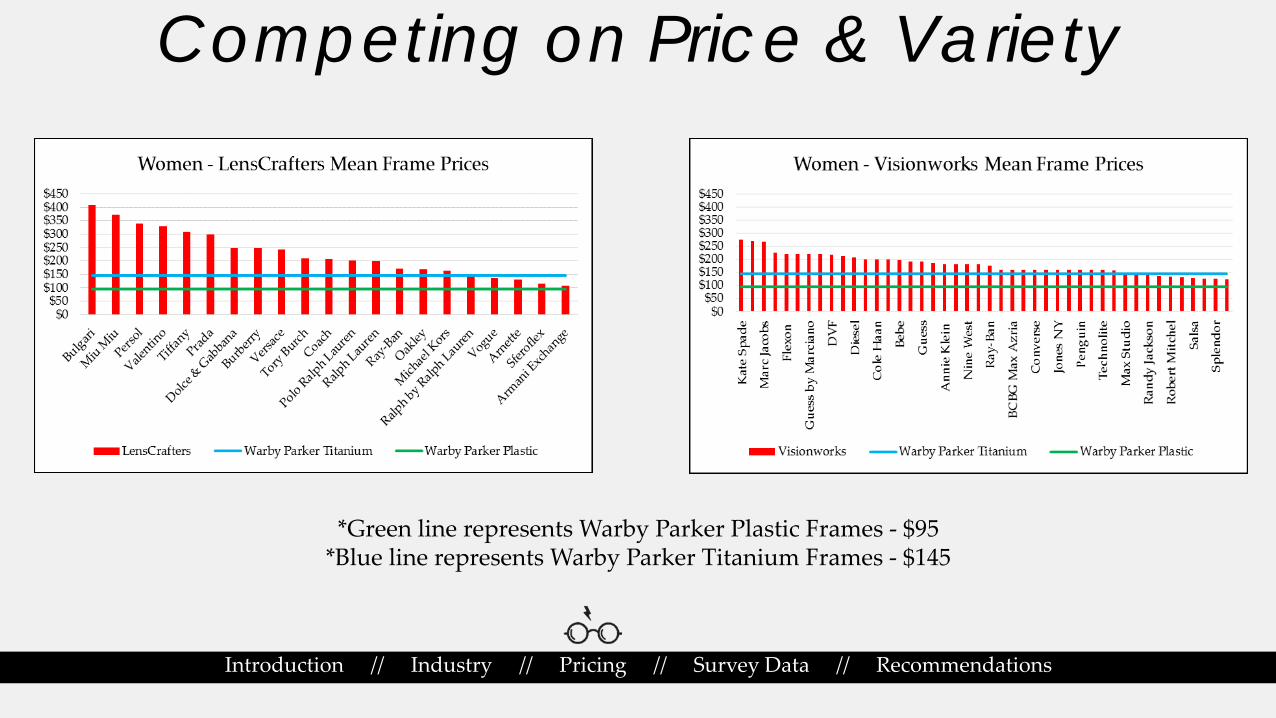

Competing on Price & Variety

Introduction // Industry // Pricing // Survey Data // Recommendations

*Green line represents Warby Parker Plastic Frames - $95*Blue line represents Warby Parker Titanium Frames - $145

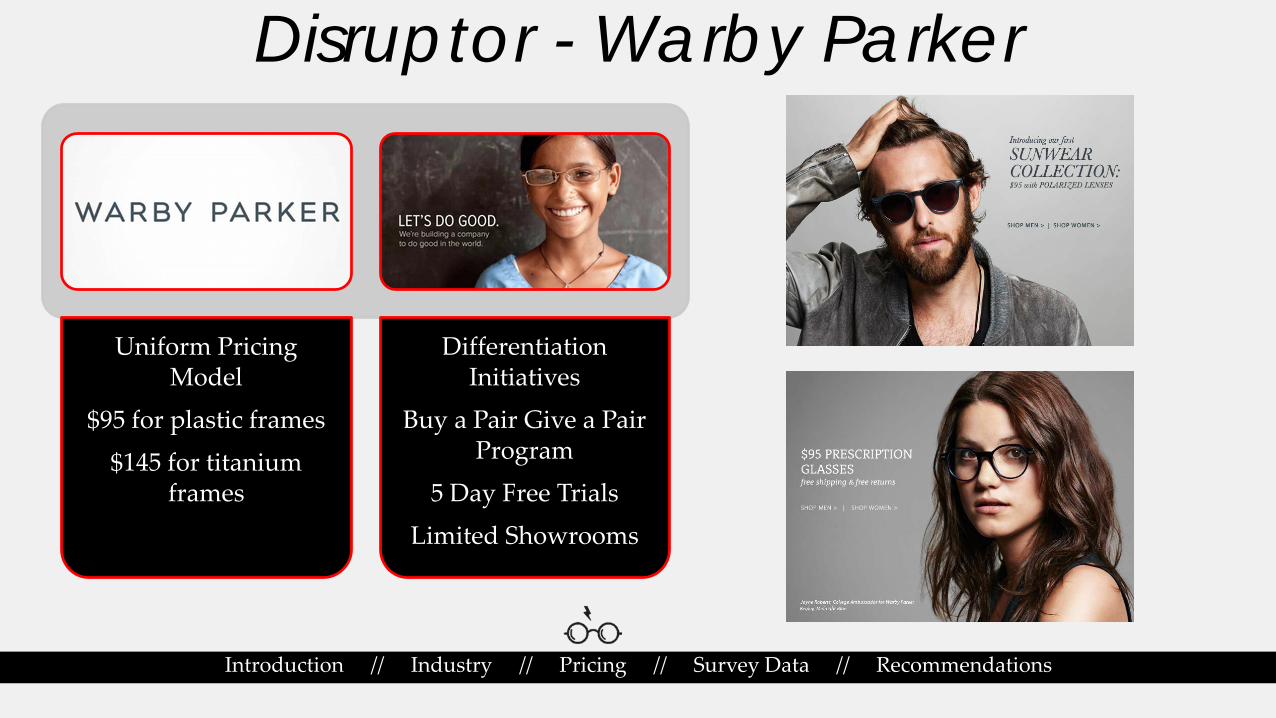

Disruptor - Warby Parker

Introduction // Industry // Pricing // Survey Data // Recommendations

Uniform Pricing Model

$95 for plastic frames

$145 for titanium frames

Differentiation Initiatives

Buy a Pair Give a Pair Program

5 Day Free Trials

Limited Showrooms

Survey

Introduction // Industry // Pricing // Survey Data // Recommendations

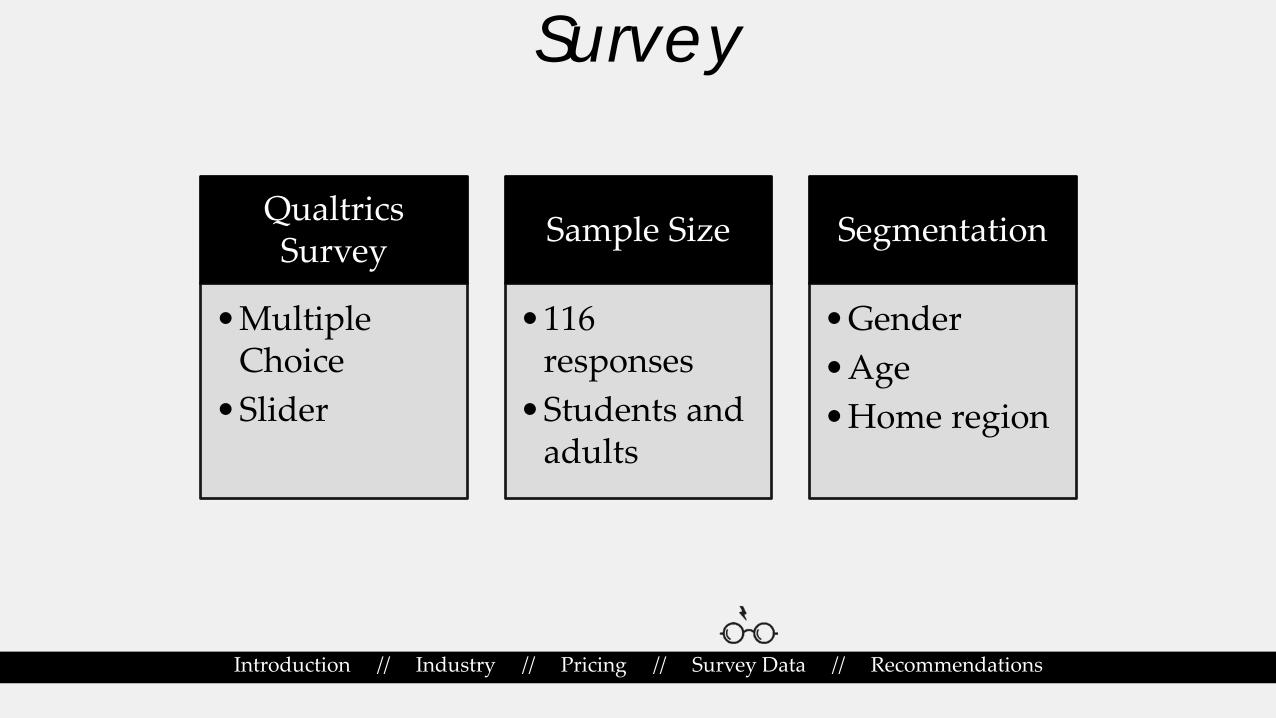

QualtricsSurvey

•Multiple Choice•Slider

Sample Size

•116 responses•Students and

adults

Segmentation

•Gender•Age•Home region

Survey

Introduction // Industry // Pricing // Survey Data // Recommendations

Survey

Introduction // Industry // Pricing // Survey Data // Recommendations

Ray-Ban’s Clubmaster Fleck, $160 Prada, $390

Oakley’s Holbrook Polarized, $170

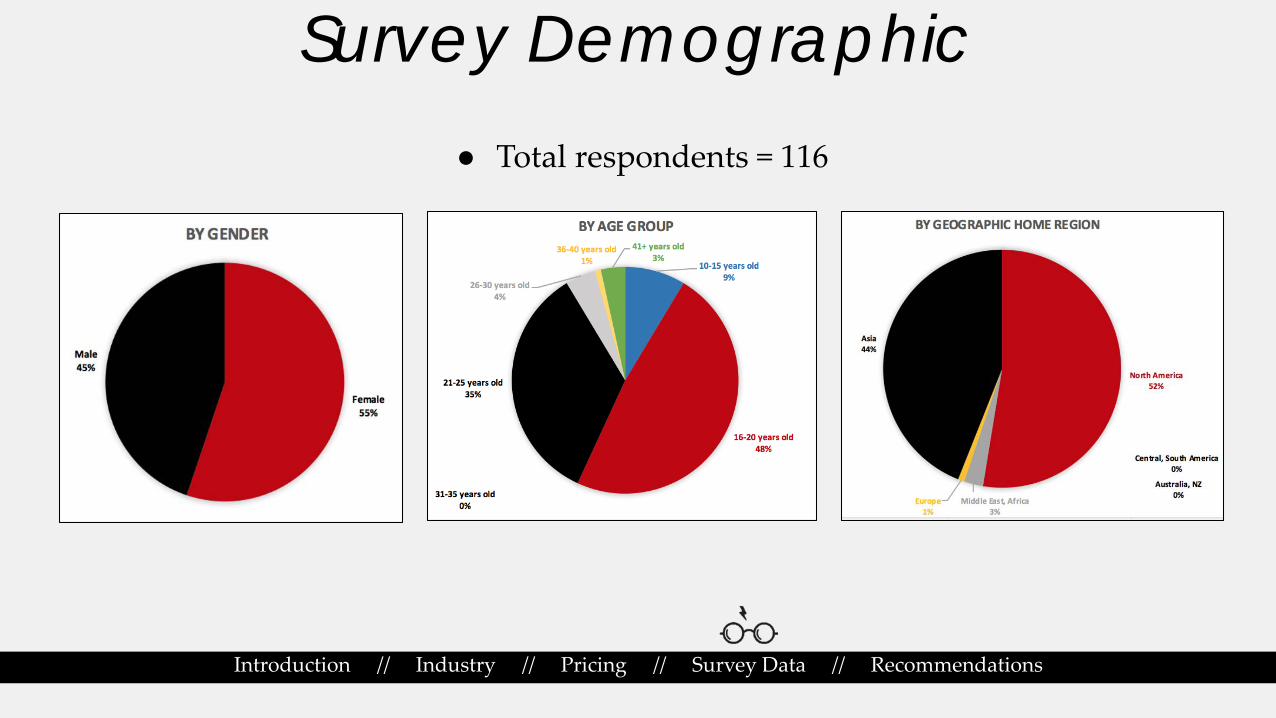

Survey Demographic

Introduction // Industry // Pricing // Survey Data // Recommendations

● Total respondents = 116

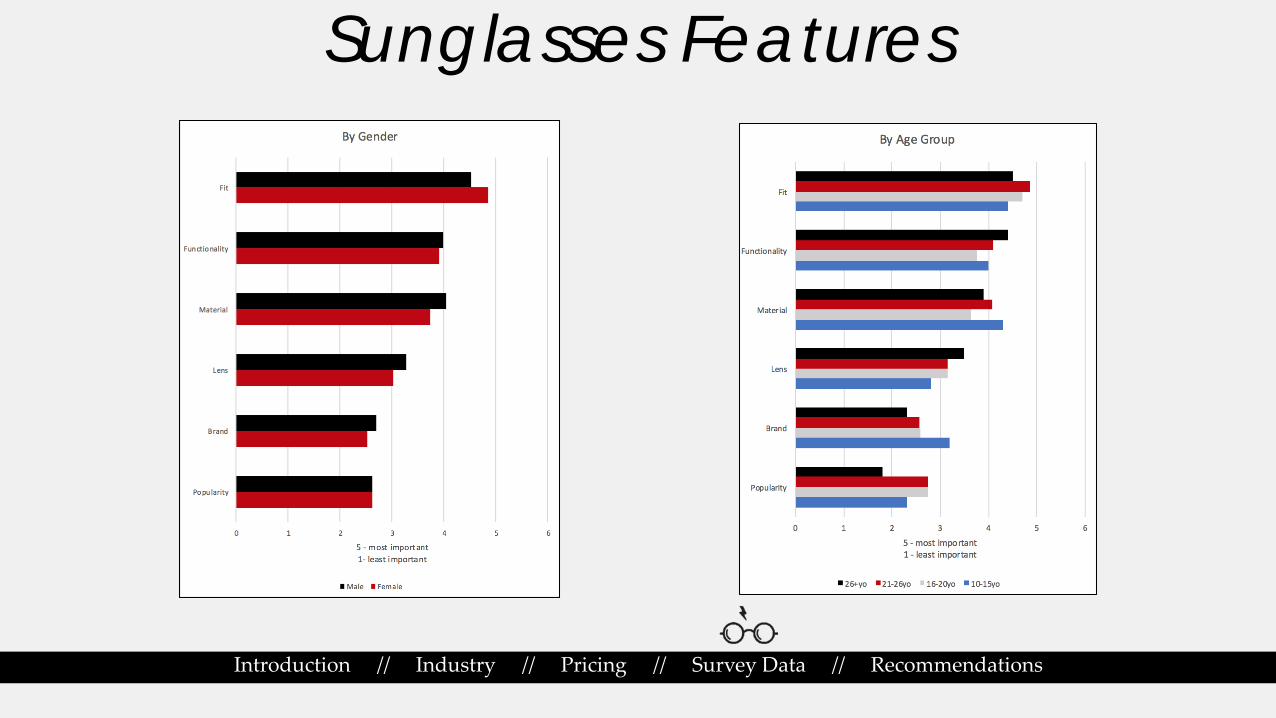

Sunglasses Features

Introduction // Industry // Pricing // Survey Data // Recommendations

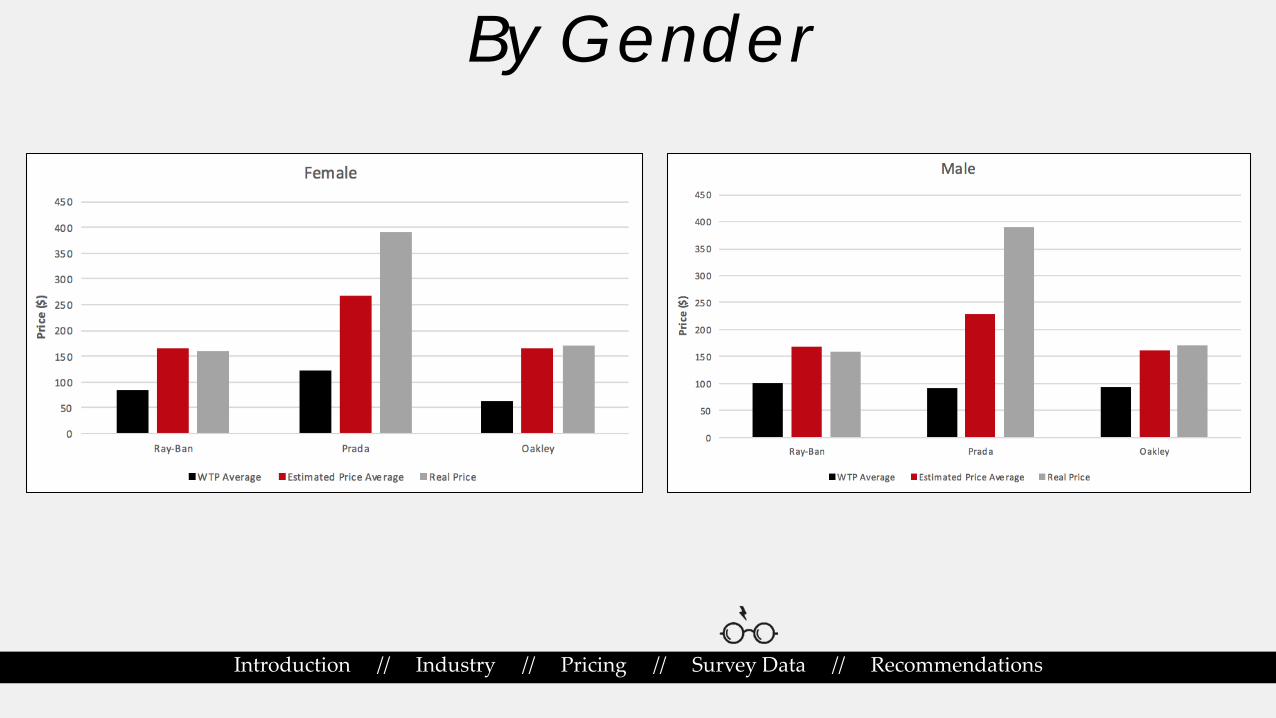

By Gender

Introduction // Industry // Pricing // Survey Data // Recommendations

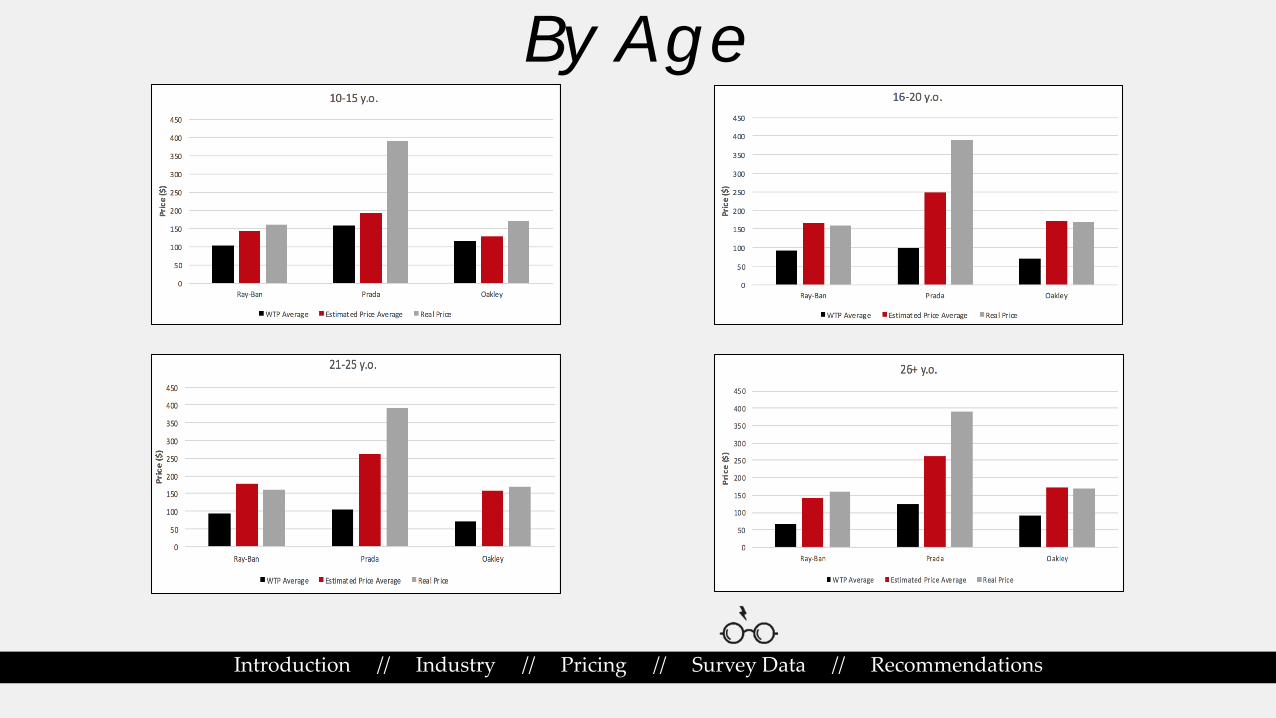

By Age

Introduction // Industry // Pricing // Survey Data // Recommendations

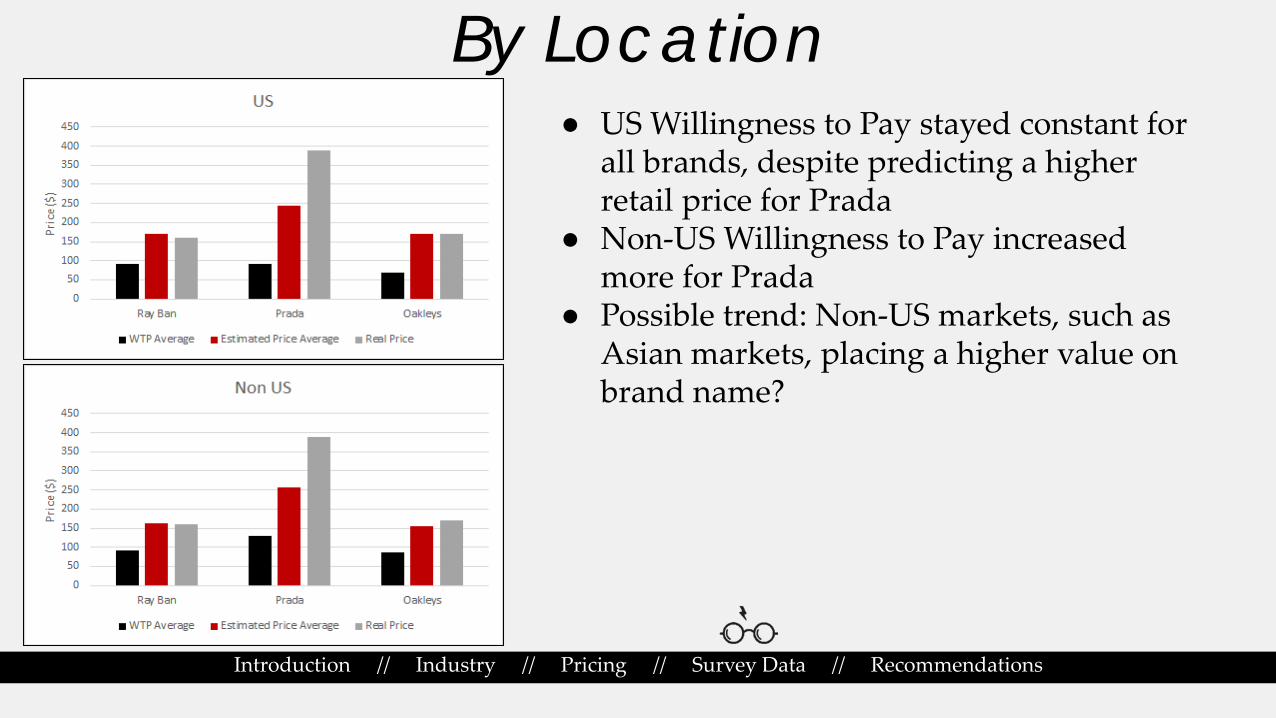

By Location

Introduction // Industry // Pricing // Survey Data // Recommendations

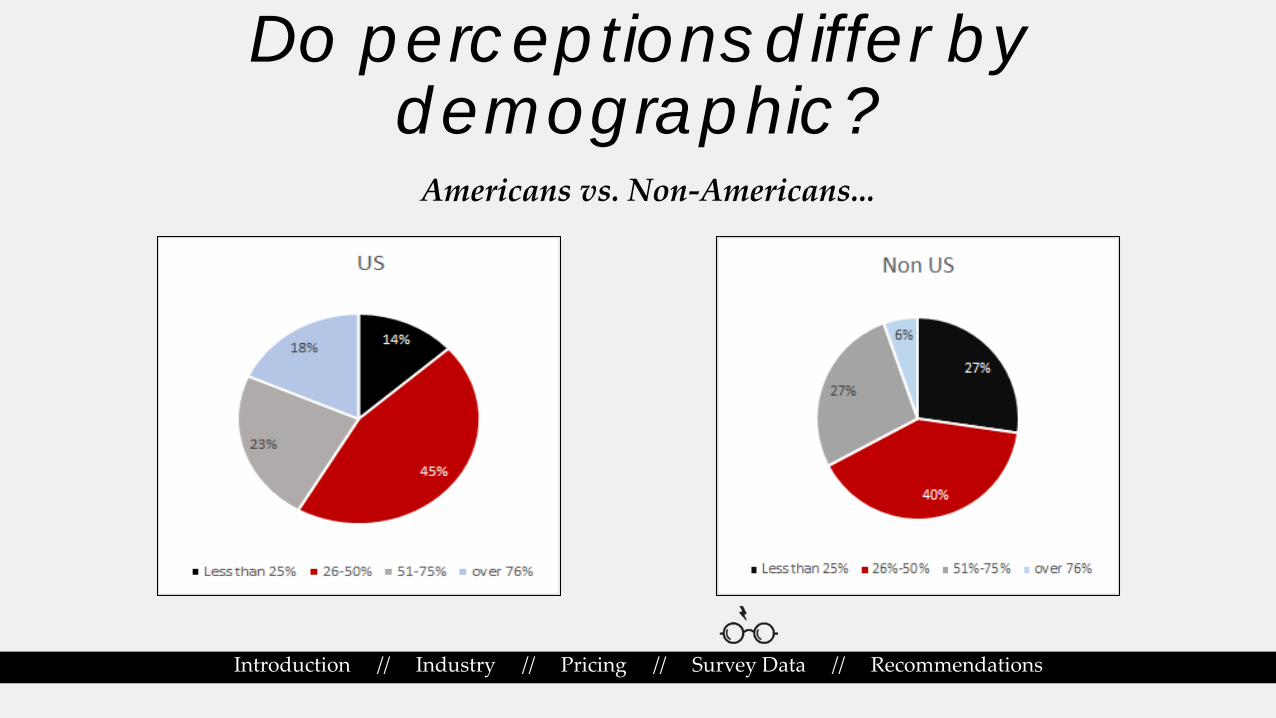

● US Willingness to Pay stayed constant for all brands, despite predicting a higher retail price for Prada

● Non-US Willingness to Pay increased more for Prada

● Possible trend: Non-US markets, such as Asian markets, placing a higher value on brand name?

Perceptions of the Industry

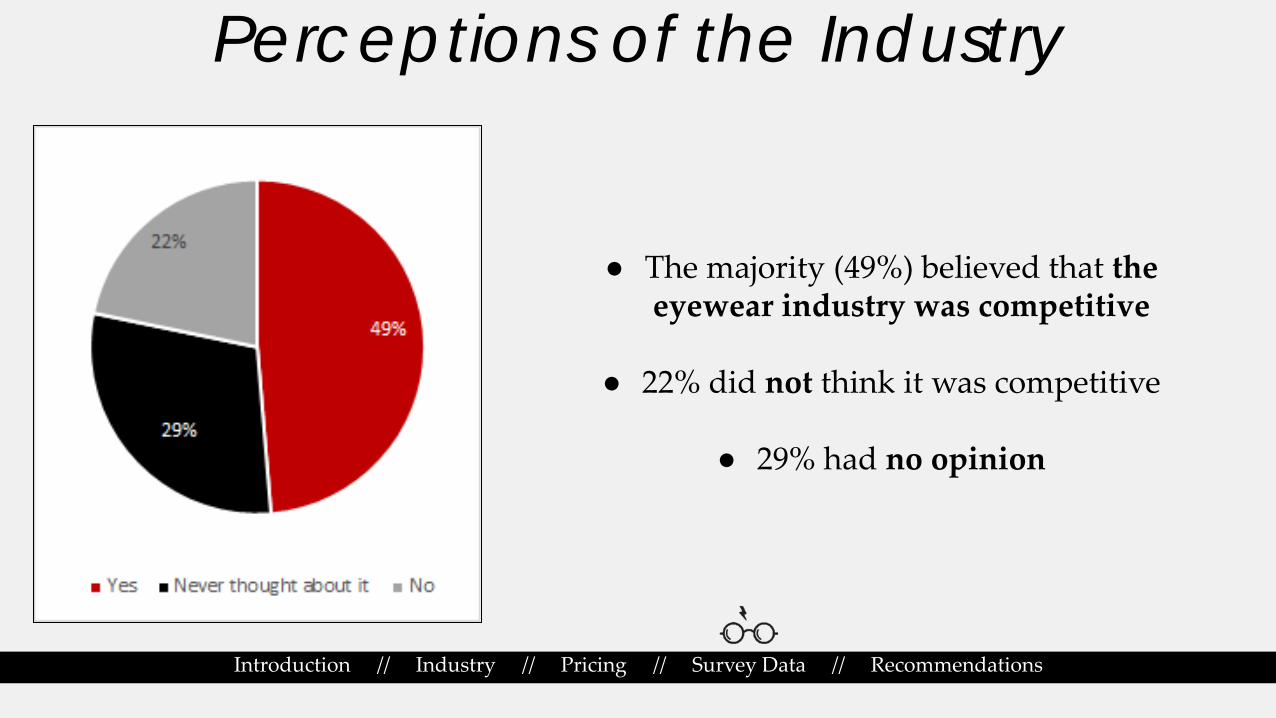

Introduction // Industry // Pricing // Survey Data // Recommendations

● The majority (49%) believed that the eyewear industry was competitive

● 22% did not think it was competitive

● 29% had no opinion

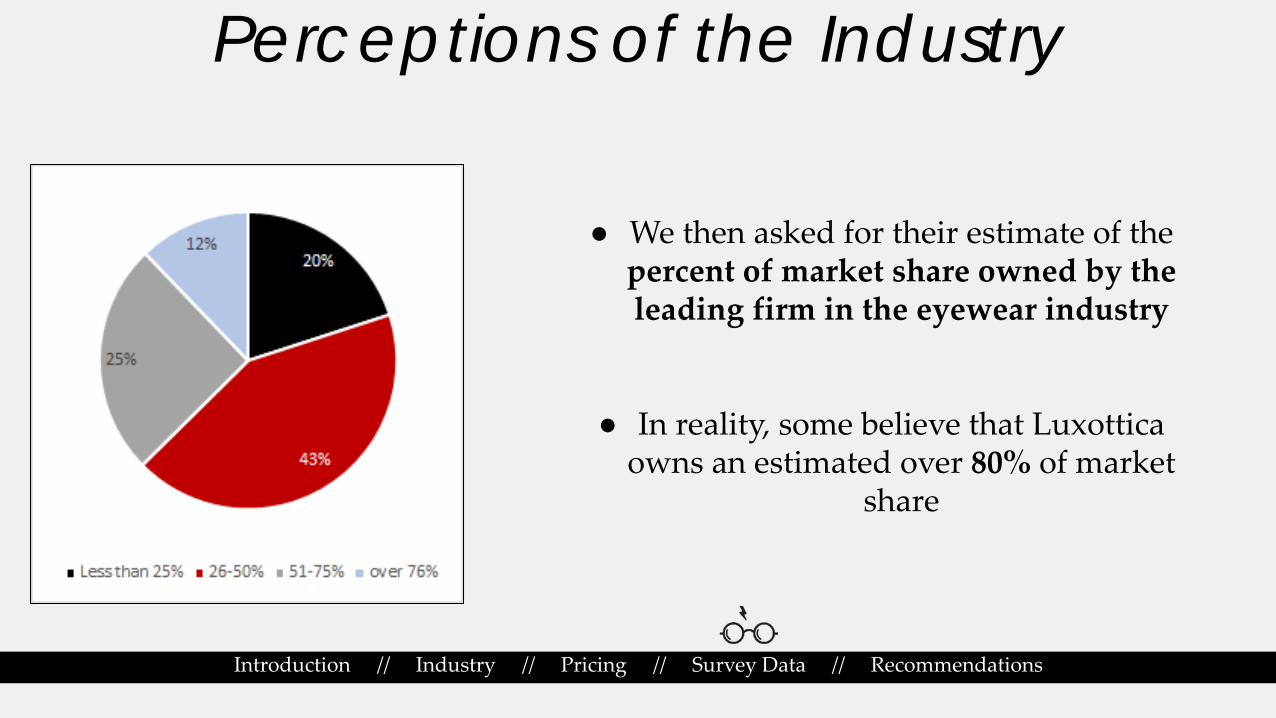

Perceptions of the Industry

Introduction // Industry // Pricing // Survey Data // Recommendations

● We then asked for their estimate of the percent of market share owned by the leading firm in the eyewear industry

● In reality, some believe that Luxottica owns an estimated over 80% of market

share

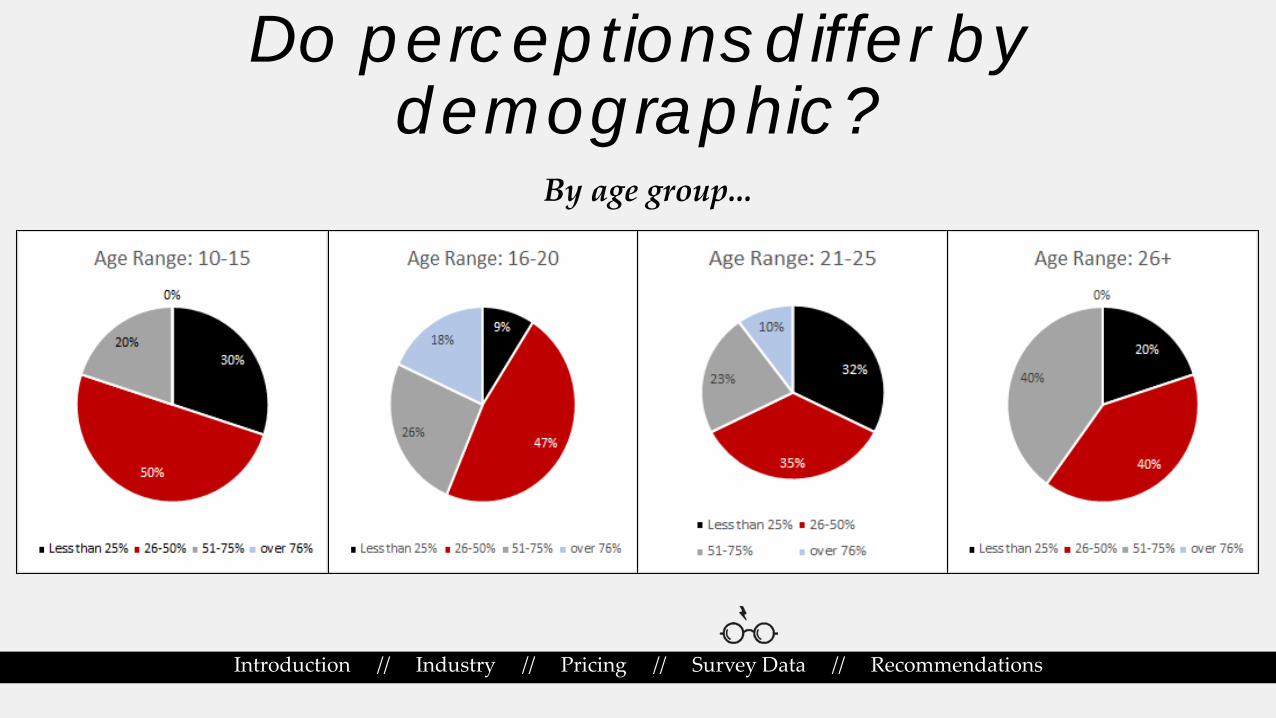

Do perceptions differ by demographic?

Introduction // Industry // Pricing // Survey Data // Recommendations

By age group...

Do perceptions differ by demographic?

Introduction // Industry // Pricing // Survey Data // Recommendations

Americans vs. Non-Americans...

Data Summary

Introduction // Industry // Pricing // Survey Data // Recommendations

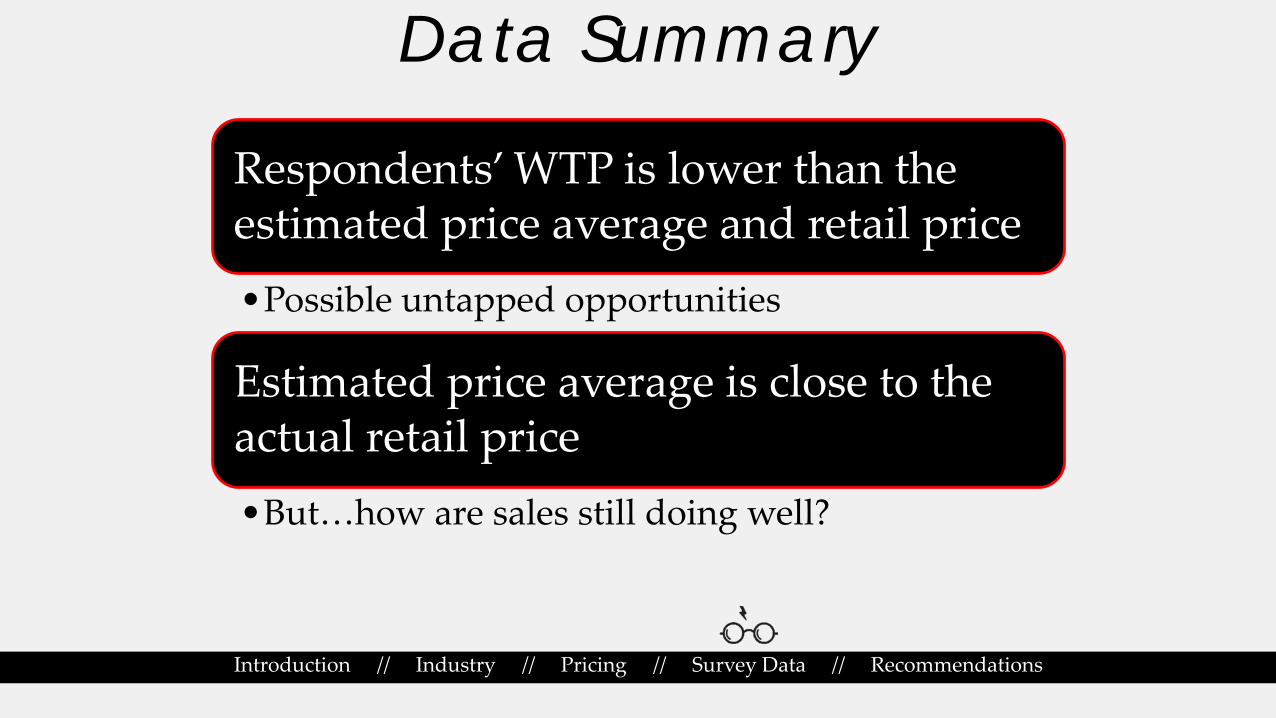

Respondents’ WTP is lower than the estimated price average and retail price•Possible untapped opportunities

Estimated price average is close to the actual retail price•But…how are sales still doing well?

Potential Criticisms

Introduction // Industry // Pricing // Survey Data // Recommendations

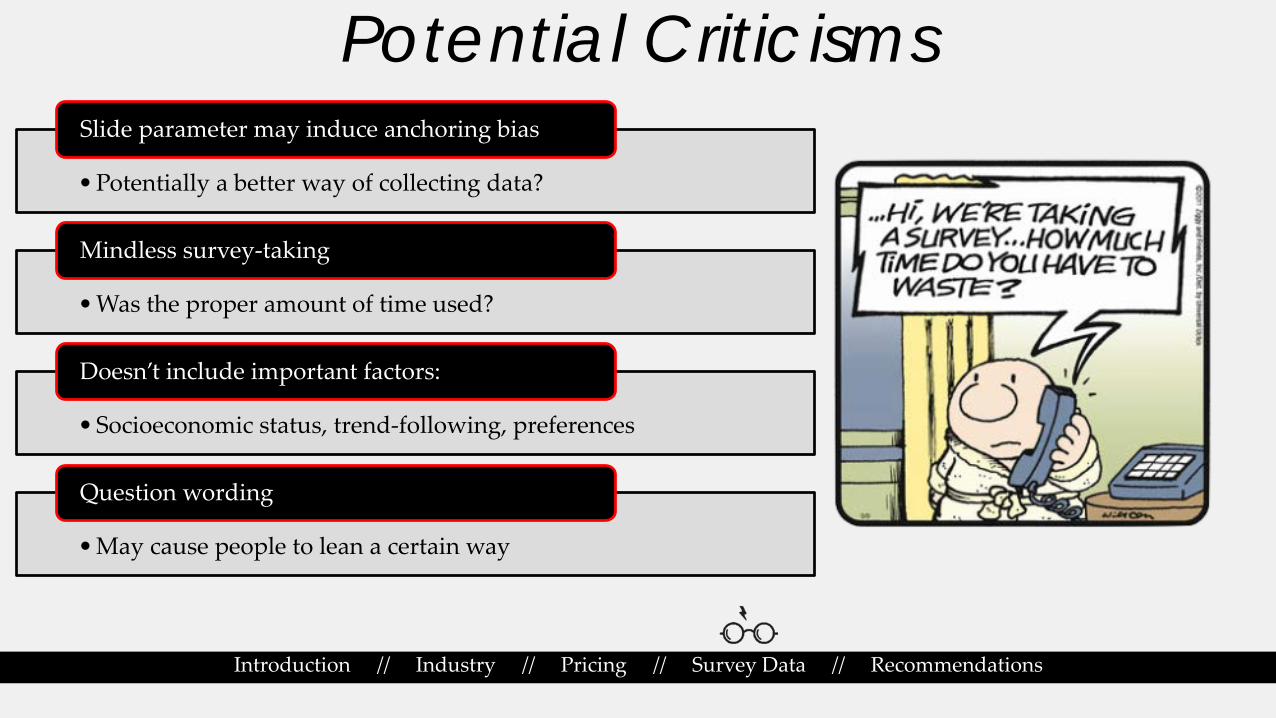

•Potentially a better way of collecting data?

Slide parameter may induce anchoring bias

•Was the proper amount of time used?

Mindless survey-taking

•Socioeconomic status, trend-following, preferences

Doesn’t include important factors:

•May cause people to lean a certain way

Question wording

Recommendations

Introduction // Industry // Pricing // Survey Data // Recommendations

Important trends to jump on:•Millennial price sensitivity•Eye health awareness• Sustainable business practices• Service-centricity•Personalization•New technology

Recommendations

Introduction // Industry // Pricing // Survey Data // Recommendations

•Market lower-end sunglass brands to younger demographics•Late teens/early twenties seem more aware of the lack of

competition •Differentiate products to appeal to millennials

Target different age ranges

•Design products that flaunt the company logo and have a distinctive appearance•Create customer value through prestige•Target the Asian market?

Prestige pricing

Investments

Introduction // Industry // Pricing // Survey Data // Recommendations

High Barriers to Entry

•Difficult to compete with established brands

Competition

• Luxottica has the advantage of economies of scale

Different Perspective

• Sustainable business practice

•Niche market

•Awareness of industry trends

Analyst Perspective

• Expect Luxottica’s stock to perform well

• Short sell Safilo’s stock

• Look into start-up disruptors

Questions?