Embed Size (px)

Citation preview

A solution for sustainable economic development

of the Gulf Cooperation Council countries

Katarzyna Czupa

ISLAMIC FINANCE

Islamic finance. A solution for sustainable economic

development of the Gulf Cooperation Council countries

Katarzyna Czupa

Islamic finance. A solution for sustainable economic

development of the Gulf Cooperation Council countries

Centre for International Initiatives Warsaw 2015

The publication was issued within the project ‘Let’s talk about Islamic finance’.

Partners

Edition Katarzyna Czupa Cover project Katarzyna Czupa Language correction Aleksandra Radziwoń ISBN: 978-‐83-‐935548-‐0-‐5 Publisher Centre for International Initiatives Al. Waszyngtona 120/12, 04-‐074 Warszawa e-‐mail: [email protected] www.centruminicjatyw.org

About the author Katarzyna Czupa, Vice-‐President of the Centre for International Initiatives’ Management Board. She holds Master’s degree in international relations from University of Warsaw. She also studies Finance and Accounting (Master’s studies) at the Warsaw School of Economics. Between 2012 and 2014 she was a deputy of editor-‐in-‐chief of the student international affairs review Notabene. Her research interests include finance, Islamic finance, economic policy of the Gulf Co-‐operation Council’s member states as well as internal and foreign policy of the United Kingdom

Abstract The aim of this publication is to analyse the problem of sustainable economic development of the Gulf Cooperation Council (GCC) countries. The analysis focuses on the small and medium enterprises (SMEs), their development and use of financial instruments, especially Islamic financial instruments. It also discusses differences between Islamic and conventional theories of development. As it is proved, the GCC economies should not be perceived as truly and sustainably developed because they are based mainly on profits coming from oil and gas industry, which then are channelled through elaborated network of state-‐owned companies (SOEs). SMEs face many obstacles preventing development of their operations, e.g. financial exclusion. Taking into account the fact that religion plays a significant role in life of the Gulf inhabitants, Islamic finance, which is based on the prohibition on interest rate, may be used as a solution.

1

Table of contents

Abbreviations .............................................................................................................................................................................. 4

Introduction ................................................................................................................................................................................. 5

1. Economic development in the GCC countries .......................................................................................................... 7

1.1. Introductory remarks. Defining development .............................................................................................. 71.2. Macroeconomic performance and development in the GCC countries ............................................. 11

2. Business environment in the GCC ............................................................................................................................... 19

2.1. The role of small and medium enterprises in the Gulf economies ...................................................... 23

2.2. Constraints for the Gulf SMEs’ operations .................................................................................................... 23

3. Financial inclusion as a precondition for development .................................................................................... 29

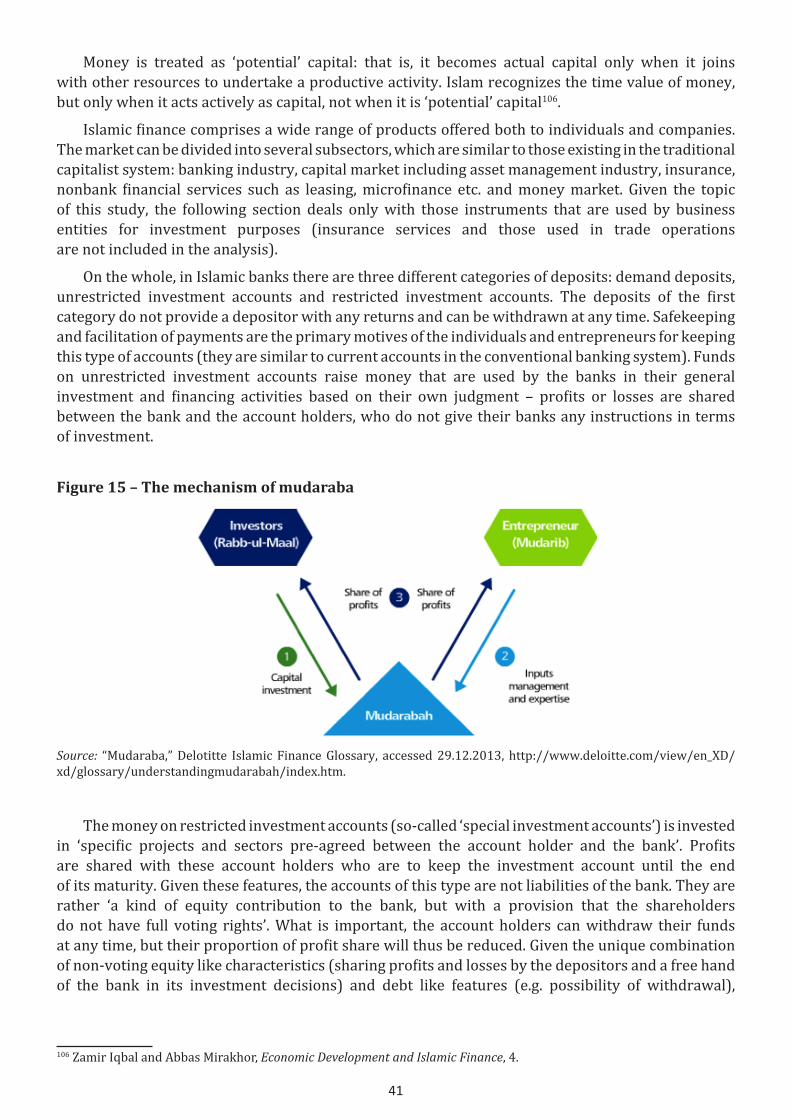

3.1. The role of finance in economy .......................................................................................................................... 293.2. Financial inclusion among the GCC SMEs ...................................................................................................... 31

4. Evolution and characteristics of Islamic finance .................................................................................................. 39

4.1. Main principles .......................................................................................................................................................... 394.2. Towards the Islamic banking .............................................................................................................................. 47

5. Islamic finance as a solution for development of the Gulf SMEs ................................................................... 53

Concluding remarks ............................................................................................................................................................... 61

References .................................................................................................................................................................................. 65

Appendix .................................................................................................................................................................................... 69

2

List of figures

Figure 1 – GDP growth in the GCC member states and leading world economies, 2000-2012 (annual) ..................................................................................................................................................................................... 11

Figure 2 – Share of oil rents in the real GDP, 2000-2010 (percentage) ......................................................... 12

Figure 3 – GDP by economic sectors, 2011 ................................................................................................................. 13

Figure 4 – Share of state spending in non-oil GDP in the GCC and selected international cases, 2000 and 2008 .................................................................................................................................................................................... 14

Figure 5 – The GCC governments’ hydrocarbon revenues and total expenditure, 1980-2010 (real US dollars billions) ....................................................................................................................................................................... 16

Figure 6 – Private investment as a share of GDP, 1995 and 2006 (percentage) ........................................ 21

Figure 7 – The GCC employment in private and public sector, 2011 .............................................................. 22

Figure 8 – Distance to the frontier by region, 2013 ................................................................................................ 26

Figure 9 – Use of and access to financial services .................................................................................................... 30

Figure 10 – Credit growth, year over year, 2006-2011 ......................................................................................... 34

Figure 11 – SMEs loans as a percentage of total loans in selected economies in the MENA, 2009 .... 34

Figure 12 – Sources of working capital and investment finance, by firm size and country group, 2010 ............................................................................................................................................................................. 35

Figure 13 – Leasing volumes as a percentage of GDP in selected world regions, 2008 ......................... 36

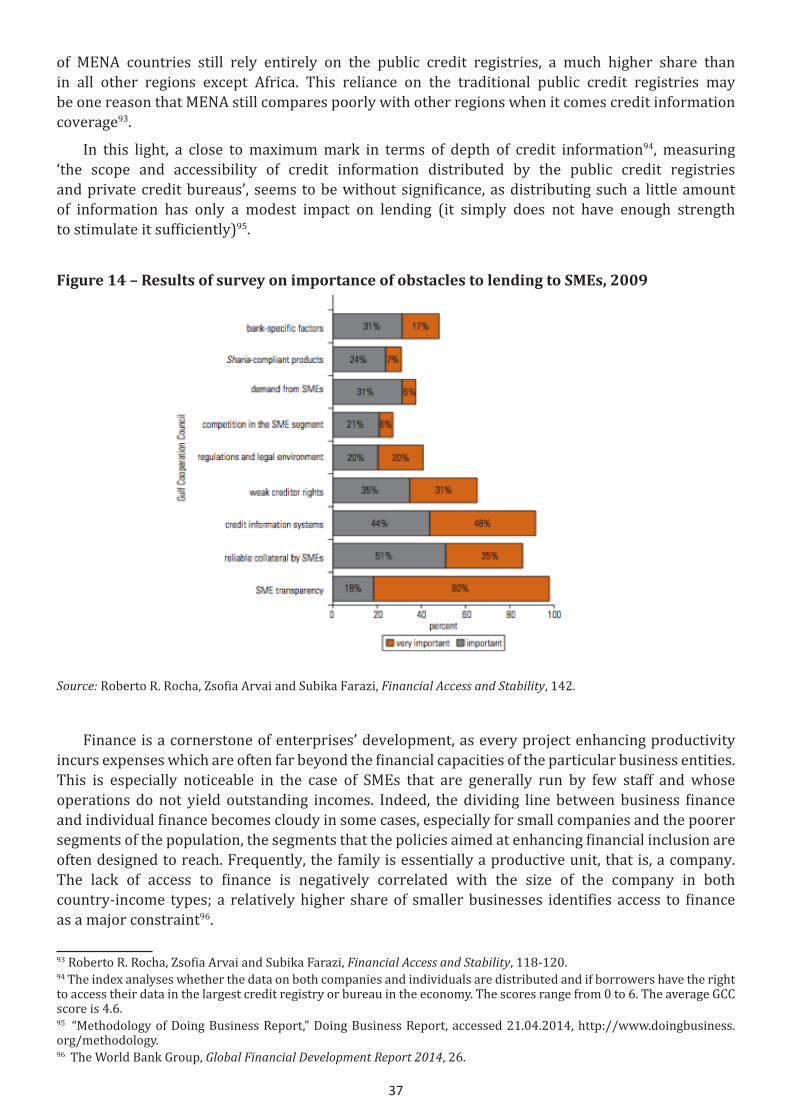

Figure 14 – Results of survey on importance of obstacles to lending to SMEs, 2009 ............................... 37

Figure 15 – The mechanism of mudaraba ................................................................................................................... 41

Figure 16 – The mechanism of musharaka ................................................................................................................. 42

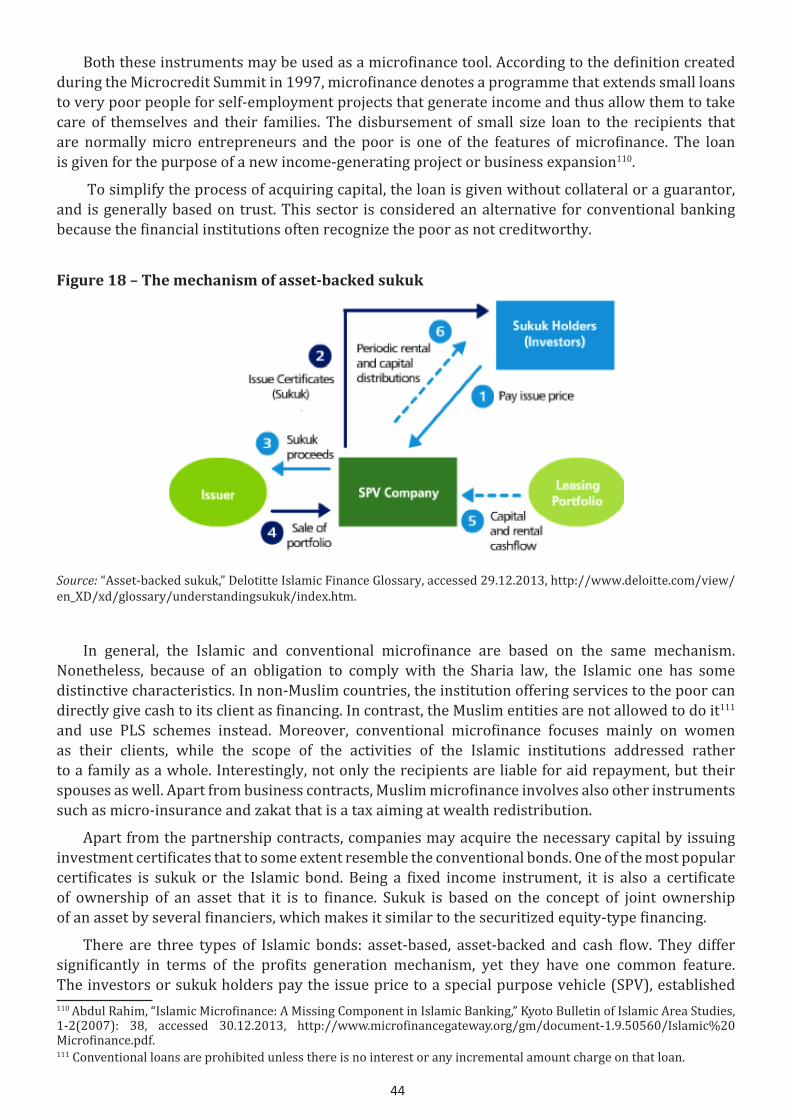

Figure 17 – The mechanism of asset-based sukuk .................................................................................................. 43

Figure 18 – The mechanism of asset-backed sukuk ................................................................................................ 44

Figure 19 – The mechanism of cash flow sukuk ....................................................................................................... 45

Figure 20 – The mechanism of ijarah ............................................................................................................................ 46

Figure 21 – Global Islamic banking assets growth trend, 2004-2012 ............................................................ 49

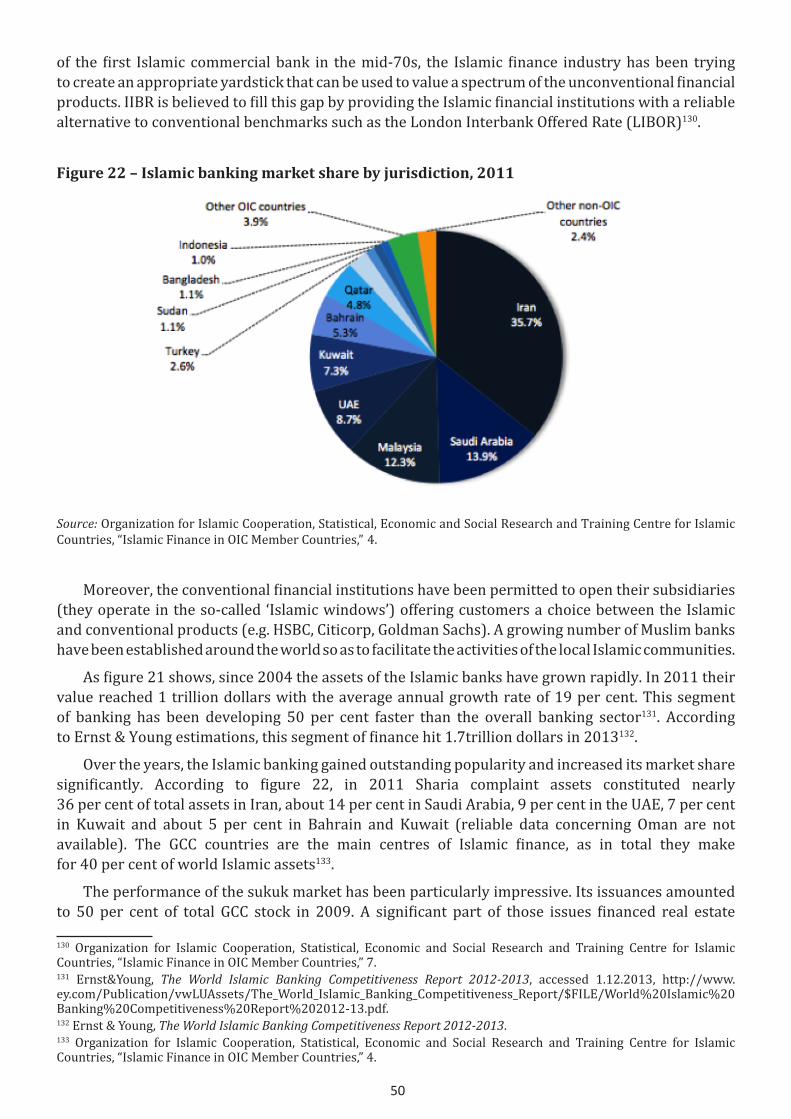

Figure 22 – Islamic banking market share by jurisdiction, 2011 ..................................................................... 50

Figure 23 – Average return on equity and return on assets for Islamic banks, 2008-2011 ................. 54

Figure 24 – Capitalization of Islamic and conventional banks, 2007 and 2011 .......................................... 55

Figure 25 – Issuance of Sukuk in the Gulf Cooperation Council, 2003-2009 ............................................... 56

3

Figure 26 – Islamic Banking, religiosity, and Access of Firms to Financial Services ................................. 57

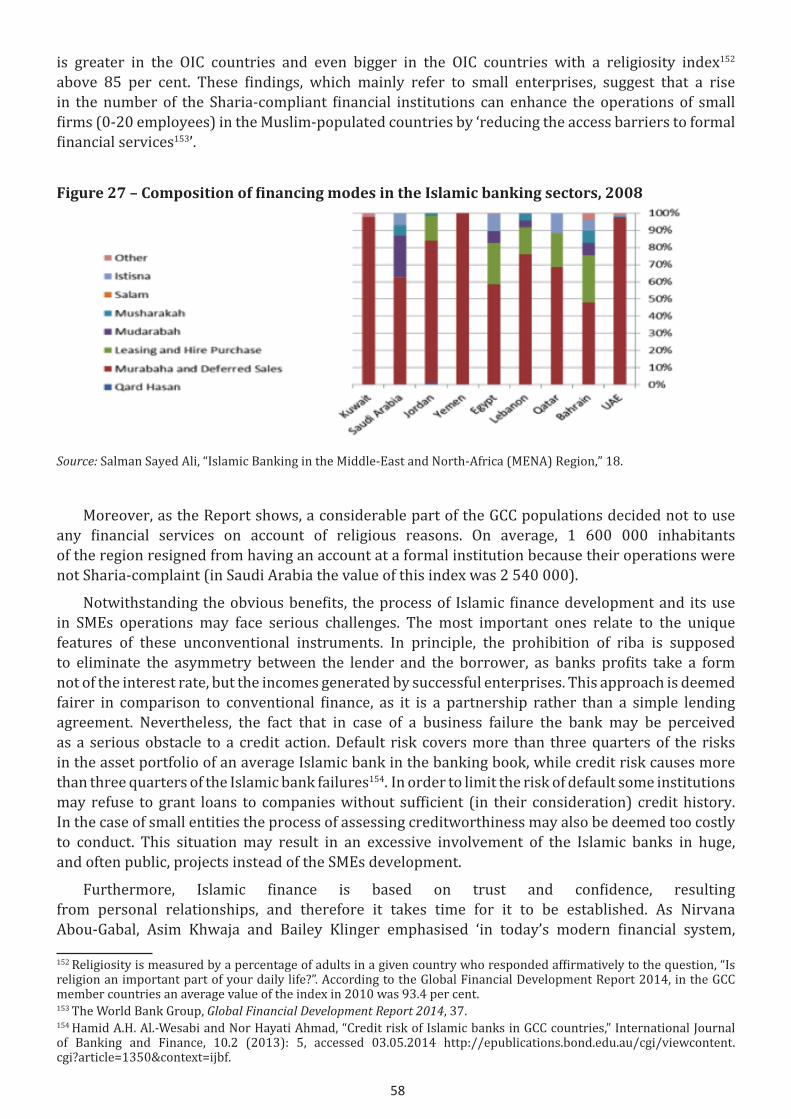

Figure 27 – Composition of financing modes in the Islamic banking sectors, 2008 ................................. 58

Figure 28 – Banking penetration and Islamic banking share, 2012 ................................................................. 59

List of tables

Table 1 – Financial inclusion indicators, 2011 ........................................................................................................... 33

4

Abbreviations

E&Y Ernst and Young

HDI Human Development Index

GCC Gulf Cooperation Council

GDP Gross Domestic Product

IIBT International Islamic Benchmark Rate

MENA Middle East and North Africa

OECD Organisation for Economic Co-operation and Development

R&D Research and Development

ROA Return on assets

ROE Return on equity

SME Small and medium enterprise

SPV Special purpose vehicle

SOE State-owned enterprises

UAE United Arab Emirates

UK United Kingdom

US United States

5

Introduction

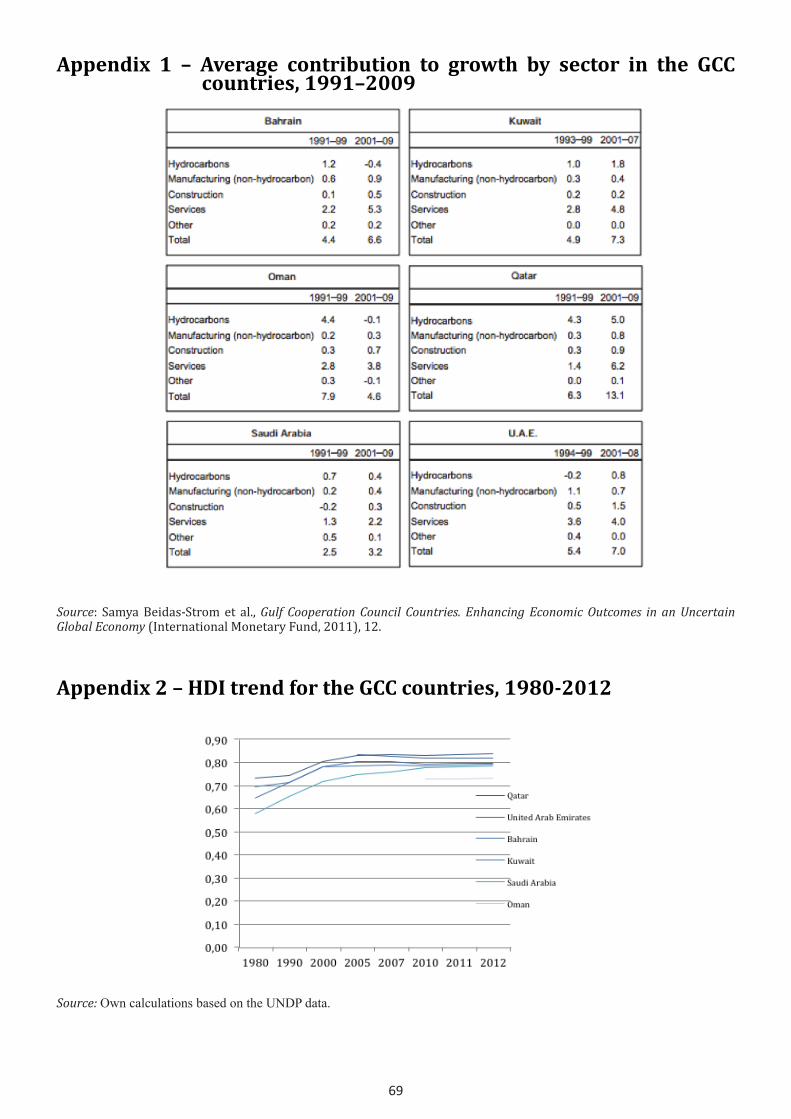

On the surface, the Gulf Cooperation Council member states are one of the most developed countries in the world. They rank at the very top in terms of the gross domestic product (GDP) per capita – in 2012 the average value of the indicator in the region amounted to nearly 44,000 US dollars and was akin to those noted in Japan, Australia and Canada, which are the Organization for Economic Co-operation and Development members1. They are also in the group of countries with a high Human Development Index (HDI). As chart from the appendix 1 shows, since 1980 the indicator increased considerably among all the Gulf states and now its value is similar to these noted in the Central European countries2.

Recently, the Gulf has also become one of the main targets of global investors. Magnificent construction projects such as Burj Khalifa, the tallest building in the world, the 2022 FIFA World Cup in Qatar and numerous artificial private islands (the World archipelago is probably one of the most famous), attracted both international companies and individuals anxious for high profits’ rates. In 2007, before the outbreak of the financial crisis, the average market capitalization of listed companies measured as percentage of GDP in the region was nearly 87 per cent, compared to 63 per cent in Germany and 49 per cent in Poland. The indicator reached the higher values in Kuwait and Bahrain – 164 and 130 per cent respectively against 137 and 135 per cent noted in the United States (US) and the United Kingdom (UK). Although now market capitalization is far from this peak (in 2012 it was around 56 per cent), it is still relatively high and resembles patterns observed in the most dynamic economies in the world.

Given the fact that the GCC countries’ vast reserves of oil and gas3 generate a bulk of national income, those achievements should not come as a surprise. Most of the infrastructure projects as well as investments within the healthcare and education sectors are financed by profits coming from the extraction sector. This model cannot last forever, though, as natural resources are limited.

The aim of this study is to analyse the structure of the GCC companies’ ownership, their performance and contribution to GDP so as to examine patterns shaping particular economies. It describes the business environment in the region paying special attention to small and medium enterprises (SMEs), which in the West are deemed to be the cornerstone of a truly sustainable economy. It points out main obstacles towards enterprises development and discusses economic policies of the Gulf States in order to propose the best solutions facilitating SMEs’ operations, especially in the field of finance. Presenting characteristic features of Islamic finance, the main purpose of the analysis is to verify the hypothesis recommending this instrument as a tool that may help to satisfy financial needs of the small and medium business entities on the Gulf.

The first chapter discusses the issue of development. It shows evolution of the notion, points differences between conventional and Islamic approaches and introduces the concept of sustainable development. In the second part it describes the GCC economies from macroeconomic perspective as well as their performance in terms of human development.

The second chapter addresses the issue of business environment. By presenting contribution

1 Own calculation based on the World Bank data.2 In 2012 the average HDI in the region was 0.791 while in Belarus, Montenegro, Romania and Bulgaria it was 0.793, 0.791, 0.789 and 0.782 respectively. 3 According to BP Statistical Review of World Energy. June 2014, at the end of 2013, share of Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates reserves of total global reserves was 6, 0.3, 1.5, 15.8 and 5.8 per cent respectively. As for gas, shares were as follows 1, 0.5, 13.4, 4.4, 3.3 per cent and 0.1 per cent in Bahrain, which does not possess any oil reserves.

6

of both SMEs and state-owned enterprises to employment, investment and GDP, it explains their role in the Gulf economies. It also analyses constraints for the Gulf SMEs’ operations and compares the operative solutions to those adopted in the most developed countries.

The third part of the study concerns financial inclusion and the role of finance in human and economic development. It discusses these issues from both conventional and Islamic perspective and provides various data in terms of individuals and business access to and use of finance.

The fourth chapter is thoroughly devoted to Islamic finance. The first section contains plentiful information on main principles of this unconventional finance and instruments used by SMEs. The second section shows evolution of this segment of finance both from the regional and global perspective.

The aim of the last part of the analysis is to establish whether Islamic finance is a plausible solution for the development of the Gulf SMEs. It presents current patterns in the use of this unconventional finance and points what risks and opportunities the prohibition of the interest involves. The final section describes actions that have been taken by the GCC incumbents in the past years and gives some recommendations in terms of policies relating to SMEs, finance and economy in general.

The research is based on reports published by global institutions and companies dealing with collecting data in the field of development, finance (both conventional and Islamic), entrepreneurship and macroeconomics, namely the World Bank, International Monetary Fund, United Nations, Organisation for Economic Co-operation and Development, Ernst&Young, Deloitte, British Petroleum, Islamic Service Board etc. Some statistics and figures come also from publications issued by renowned Western and Gulf universities, think tanks and governmental organizations (e.g. London School of Economics, Harvard University, Islamic Research and Development Institute, QFinance and Gulf Lead Consultants). All analyses were conducted with use of a variety of modern indicators measuring the GCC countries’ performance in the given fields and comparing results with those achieved by the most developed states. When it was possible, original documents were used. Given the fact that the author of this thesis does not speak Arabic, information was obtained only from the English and Polish references. So as to ensure high quality of the research the most up-to-date data was collected. Nonetheless, in some cases the author was not able to attain required sources, as in the GCC system of data collection is not sufficiently developed.

7

1. Economic development in the GCC countries

1.1. Introductory remarks. Defining development

Defining development is considered as one of the most demanding tasks in the academic field. Scholars find establishing one and accurate definition particularly challenging due to the multidimensional nature of the phenomenon. Nonetheless, bearing in mind the scope of this study, it is necessary to describe the issue thoroughly lest cause any misinterpretations.

As of yet the most comprehensive definition of development has been presented in the Human Development Report 1990, according to which human development is ‘a process of enlarging people’s choices. The most critical of these wide-ranging choices are to live a long and healthy life, to be educated and to have access to resources needed for a decent standard of living. Additional choices include political freedom, guaranteed human rights and personal self-respect. (…) Human development thus concerns more than the formation of human capabilities, such as improved health or knowledge. It also concerns the use of these capabilities, be it for work, leisure or political and cultural activities. And if the scale of human development fails to balance the formation and use of human capabilities, much of the human potential will be frustrated’4.

The wealth of nations and its causes have been analysed for centuries. They were examined by such famous scholars as Adam Smith, David Ricardo and John Stuart Mill, representatives of so-called classical economics. Although while explaining disparities in particular countries’ development they focused on different aspects, they all pointed an unequal distribution of factors of productions (land, labour and capital), their values and thus different costs of production as primary causes of the problem5. Marxian model of economic growth put greater emphasis on the relations of production, referring to mode-specific ways of production in which human beings are joined in the production process, that is, the relations of production are concerned with class relations amongst members of society. In his view, development is a linear process and communism is its final stage6. Neoclassical school of thought tended to be resolutely micro-oriented. Its leading representatives, namely Alfred Marshall, Karl Menger and William Stanley Jevons, were concerned with conditions required for equilibrium in individual markets (e.g. the utility-maximizing behaviour of individuals and the profit-maximizing actions of the perfectly competitive firms)7.

Explanations and prescriptions were provided also by John Maynard Keynes, a strong advocate for state interventionism, Robert Solow, who proved that due to diminishing returns output growth is generated by technology changes rather than an increase in capital, and Walt Rostow, and author of stagesof growth theory8. Joseph Stiglitz and Gerald Meier, often pointed that issues such as macrostability, trade liberalization, property rights and poverty reduction are of utmost importance for economic development9.

4 UNDP, Human Development Report 1990 (New York: Oxford University Press, 1990), 1. 5 Ingrid Rima, Development of Economic Analysys (United Kingdom: Routledge, 2009), 196-197. 6 Danuta Drabińska, Miniwykłady z historii myśli ekonomicznej. Od merkantylizmu do monetaryzmu (Warszawa: Szkoła Główna Handlowa, 2007), 55. 7 Ingrid Rima, Development of Economic Analysys, 54, 283-285, 318. 8 Walt W. Rostow, Theorists of Economic Growth from David Hume to the Present. With a Perspective on the Next Century (New York: Oxford University Press, 1990), 281, 342, 374-380. 9 Gerald M. Meier and Joseph F. Stiglitz, Frontiers of Development Economics. The Future in Perspective, (New York: The World Bank and Oxford University Press, 2001), accessed 31.08.2014, http://www-wds.worldbank.org/external/default/WDSContentServer/WDSP/IB/2001/03/28/000094946_01032805420961/Rendered/PDF/multi0page.pdf.

8

Until the publication of the Human Development Report it was generally assumed that the level of income is the best possible measure of welfare, since access to money provides a great deal of opportunities and permits the exercise of almost every option. However, it is true only up to a point. Income is a means, not an end. It may be used for many different purposes such as purchasing essential medicines or drugs. The well-being of a society depends on the uses to which its income is put, not on the level of income itself10. Human problems occur in many developed countries and no automatic link has been observed between the growth of income and human progress. Hence, it is essential to emphasize that income levels, by themselves, are no guarantee for prosperity and progress.

Due to the shift in the academic field towards a more complex approach focusing on the quality of human life11, for more than two decades human development has been measured not only by the yardstick of income, but also by a more comprehensive index known as the human development index (HDI) serving as a frame of reference for both social and economic development. This indicator consists of three main components: health, education and living standards, which are measured with the use of adequate indices. The first component is based on life expectancy at birth. The second one comprises the years of schooling for adults aged 25 years and expected years of schooling for children of school entering age. The decent standard of living component is measured by GNI per capita (PPP$) instead of GDP per capita (PPP$)12.

The significance of other factors does not mean that economic growth is irrelevant. A lack or at least shortage of necessary resources seriously impedes the realization of any development programs. Yet it must be also gauged whether people can lead long and healthy lives, whether they have the opportunity to be educated and whether they are free to use their knowledge and talents to shape their own destinies13. Taking all of that into account, the development analysis should discover how a link between growth and progress can be created and reinforced. In other words, it should focus on the issue known as sustainable development.

This concept was defined for the first time in the report entitled Our Common Future (also known as the Brundtland report), prepared by the United Nations’ Commission on Environment and Development. According to the document, sustainable development is ‘the development that meets the needs of the present without compromising the ability of future generations to meet their own needs. It encompasses two key concepts: the concept of ‘needs’, in particular the essential needs of the world’s poor, to which overriding priority should be given; and the idea of limitations imposed by the state of technology and social organization on the environment’s ability to meet the present and future needs’. As it was emphasized, development involves a progressive transformation of the economy and society. Physical sustainability cannot be secured unless development policies pay attention to such considerations as changes in access to resources and in the distribution of costs and benefits. Even the narrow notion of physical sustainability implies a concern for social equity between generations, a concern that must logically be extended to equity within each generation14.

According to Agenda 21, a roadmap to sustainable development containing ‘a comprehensive plan of action to be taken globally, nationally and locally, all countries should develop policies that improve efficiency in the allocation of resources and take full advantage of the opportunities offered by the changing global economic environment. In particular, wherever appropriate, countries should:

10 Gerald M. Meier and Joseph F. Stiglitz, Frontiers of Development Economics, 10.11 This change in approach is generaly ascribed to Amartya Sen, winner of the 1998 Nobel Prize in Ecnomics and co-creator of Human Development Reports and Mahbub-ul-Haq, game theorist and profesor at the University of Karachi.12 “Definition of Human Development Index,” UNDP, accessed 02.01.2014, http://hdr.und org/en/statistics/hdi.13 UNDP, Human Development Report 2010. 20th Anniversary Edition. The Real Wealth of Nations: Pathways to Human Development (New York: Palgrave Macmillan, 2010) IV. 14 “Report of the World Commission on Environment and Development. Our Common Future,” United Nations, accessed 25.04.2014, http://www.un-documents.net/our-common-future.pdf.

9

(i) encourage the private sector and foster entrepreneurship by improving institutional facilities for enterprise creation and market entry; (ii) promote and support the investment and infrastructure required for sustainable economic growth and diversification on an environmentally sound and sustainable basis; (iii) provide scope for appropriate economic instruments, including market mechanisms, in harmony with the objectives of sustainable development and fulfilment of basic needs; (iv) promote the operation of effective tax systems and financial sectors; and (v) provide opportunities for small-scale enterprises, both farm and non-farm, and for the indigenous population and local communities to contribute fully to the attainment of sustainable development’15.

It has often been said that poor performance of developing countries in both social and economic field derives from the past institutional infrastructure, reflecting a belief system of beliefs that is difficult to change either because the needed changes, which are to enhance the economic performance of the country, conflict with the religion itself or pose a threat to the existing political or business leaders. The so-called developed world, also known as the North, envisaged an ideal political-economic institutional structure that has a potential for achieving a good economic performance and societal well-being as a framework of (i) an institutional matrix that defines and establishes a set of rights and privileges; (ii) a stable structure of exchange relationships in economic and political markets; (iii) a government that is credibly committed to a set of political rules and enforcement to protect individuals, organizations, and exchange relationships; (iv) rule compliance as a result of internalization of norms as well as coercive enforcement; (v) a set of economic institutions that create incentives for members of society and organizations to engage in productive activities; (vi) a set of property rights and an effective price system that lead to low transaction costs in production, exchange, and distribution16.

Stressing the importance of well-being rather than affluence, this approach is akin to the Islamic concept of development. The difference is that the Muslims care about social and economic justice, morality, compassion, generosity and charity even more than their Christian counterparts.

The essential framework for individual and collective human progress is presented in the Qur’an, and is, in turn, made operational by the traditions of the Prophet Mohammad. (…) The Qur’an provides the framework and specifies the rules (institutions) that are, to a degree, abstract, while the traditions of the Prophet articulate the operational form of these rules17. According to the Islamic school, prosperity is based on three pillars: individual self-development, physical development of the earth and the development of the community. Development is described as a sustainable process of human growth toward perfection with the use of natural resources, which leads to full integration and unity of society. These dimensions are connected to the point where balanced progress in all three areas is needed to achieve development.

Moral behaviour is the core of the Muslim tradition. It is also noticeable when it comes to organization of the economy. The underlying principles of Islamic economy are respecting property rights, commitment to contracts and market orientation, which are all to reduce uncertainty.

The Islamic doctrine recognizes property as a gift from Allah, which was given to humans to serve equal wealth creation. At the very beginning, property rights belonged to Allah, who in his graciousness transferred them to all of mankind upon the condition that the natural resources would be shared evenly and combined with the people’s labour would be used to produce goods and services. Individuals can gain legitimate property rights only through two ways: by their creative labour, and/or by transfers-exchange, contracts, grants, or inheritance – from those who have acquired the property rights title to an asset as a result of their own labour. Hence, work is perceived

15 “Agenda 21, United Nations Conference on Environment & Development,” United Nations, Sustainable Development Knowledge Platform, accessed 25.04.2014, http://sustainabledevelopment.un.org/content/documents/Agenda21.pdf.16 Zamir Iqbal and Abbas Mirakhor, Economic Development and Islamic Finance (Washington D.C.: International Bank for Reconstruction and Development, 2013), 156. 17 Zamir Iqbal and Abbas Mirakhor, Economic Development and Islamic Finance, 158.

10

as the foundation of the property rights acquisition mechanism. It is prohibited to obtain property rights through gambling, theft, earning interest on money lent, bribery, or generally from any sources considered unlawful18.

The significance of property rights is strongly correlated with the commitment to contracts. The human fulfilment is contingent on patient and tolerant interaction and cooperation with other humans. Entrepreneurs of all kinds are subject to the rules of economic behaviour that forbid cheating, wasting (itlaf), overusing (israf), and causing harm to any trading partner. They must not do so both with respect to the Creator and other humans.

A contract is to be written and witnessed since there is a strong interdependence between contract and trust. Without trust, contracts become difficult to negotiate and conclude, as well as costly to monitor and implement. When and where trust is weak, complex and expensive administrative devices are needed to enforce contracts. Moreover, it is generally recognized that unambiguous contracts – the ones that foresee all contingencies – do not exist, as not all contingencies can be foreseen19.

It must be noted that markets play a crucial role in the Islam economy, but Muslim economic transactions differ considerably from the conventional ones. In the traditional capitalism the market norms are shaped by the notion of self-interest, which implies ’rational’ behaviour as maximizing the satisfaction that is utility or profit. In this concept individuals matter more. The community benefits chiefly thanks to self-realization of particular individuals and it is not itself a priority.

In Islam, by contrast, the market is only an instrument used in order to enhance extensive development. The principles shaping the pattern of preferences of entrepreneurs are constructed outside the market and they must learn them before engaging in any economic activity. The behaviour of consumers, producers, and traders, informed by their preferences, is subject to rules determined outside the market. In a market where there is full rule-compliance, the price that prevails for goods, services, and factors of production is considered just. The resulting incomes are considered justly earned. Therefore, the resulting distribution is just20.

The fact that interest rate based debt contracts of any type are deemed unlawful and as such are excluded from Islamic economy may provide an explanation of the specific shape of the Islamic economy. These contracts are replaced by the exchange ones, which, unlike the interest-based agreements21, entail a property claim on the principal and a portion of profits of the borrower before and after profits or losses are realized. In turn, parties willing to enter a contract must have the title to what they are going to exchange. They also need a place or a forum necessary for consummation of the exchange – that is a market – with rules ensuring its efficient operation (such as freedom of choice, freedom of contract, no restrictions on trade both international or interregional); free and transparent information concerning the price, quality, and quantity of goods; the specification of the exact date for the completion of transaction when it is to take place over time; the specification of the property and other rights of all parties in every contract.

In a nutshell, development means enhancing the quality of human lives understood as their capabilities. Both conventional and Islamic approaches focus on human empowerment understood as the ability to make their own and truly independent choices. The western countries accentuate the importance of education, health and decent level of income, while for the Muslim world justice, morality and the minimization of uncertainty are considerably more important. Notwithstanding differences, these concepts point to the necessity of providing people with even access to various 18 Any enterprises involving gambling, alcohol distribution, prostitution or pornography are banned in Islam. 19 Zamir Iqbal and Abbas Mirakhor, Economic Development and Islamic Finance, 172. 20 Zamir Iqbal and Abbas Mirakhor, Economic Development and Islamic Finance, 174. 21 According to Zamir Iqbal and Abbas Mirakhor, interest rate–based debt contracts do not result in exchange of full property claims. They only create a property claim for the lender on the property claims of the borrower in the amount of principal and interest, whether or not repayable ex post.

11

resources, as it is the only proper means of improving their opportunities and thus ensuring sustainable development.

1.2. Macroeconomic performance and development in the GCC countries

The Gulf Cooperation Council is a political and economic organization comprising six countries located in the Middle East, namely Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates (UAE). It was established in 1981 in Riyadh, Saudi Arabia.

According to the Article 4 of the Charter, the GCC was created so as to effect co-ordination, integration and inter-connection between member states in all fields in order to achieve unity between them; to deepen and strengthen relations, links and areas of cooperation now prevailing between their peoples and to formulate similar regulations in various fields such as economic and financial affairs, education, culture, social and health affairs. The preamble of the Charter emphasizes the special relations, common qualities and systems founded on the creed of Islam, faith in a common destiny that bring these nations together22.

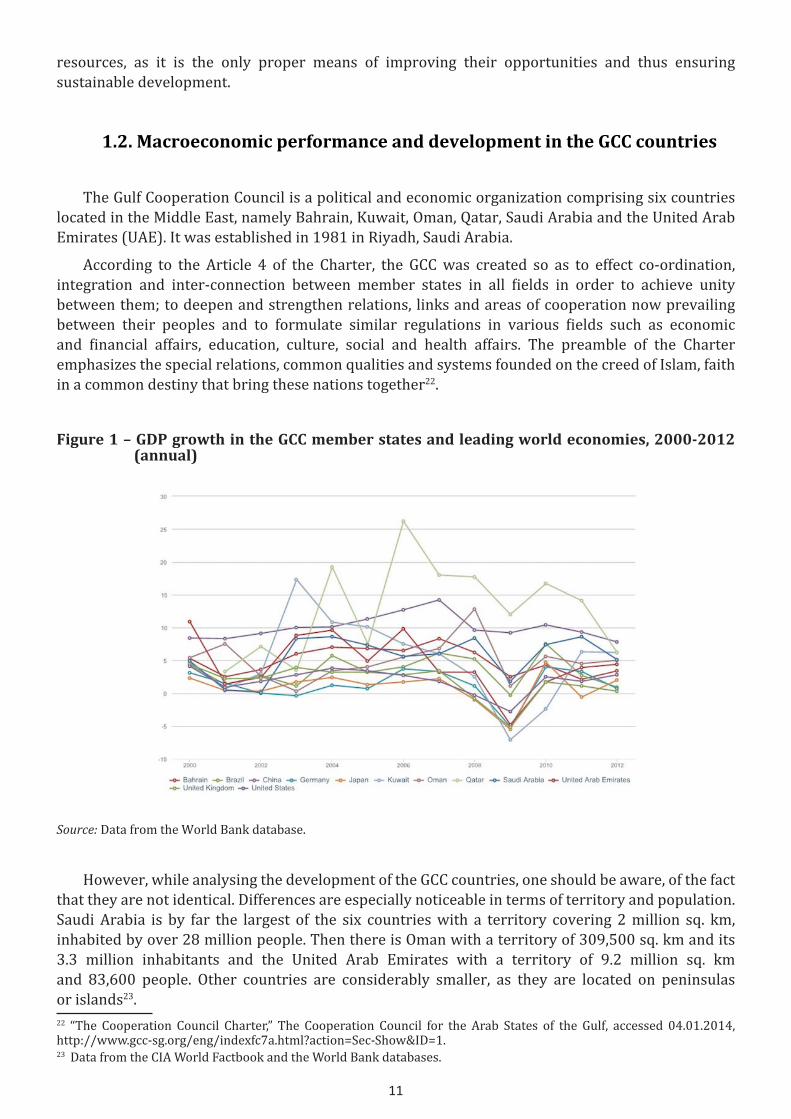

Figure 1 – GDP growth in the GCC member states and leading world economies, 2000-2012 (annual)

Source: Data from the World Bank database.

However, while analysing the development of the GCC countries, one should be aware, of the fact that they are not identical. Differences are especially noticeable in terms of territory and population. Saudi Arabia is by far the largest of the six countries with a territory covering 2 million sq. km, inhabited by over 28 million people. Then there is Oman with a territory of 309,500 sq. km and its 3.3 million inhabitants and the United Arab Emirates with a territory of 9.2 million sq. km and 83,600 people. Other countries are considerably smaller, as they are located on peninsulas or islands23. 22 “The Cooperation Council Charter,” The Cooperation Council for the Arab States of the Gulf, accessed 04.01.2014, http://www.gcc-sg.org/eng/indexfc7a.html?action=Sec-Show&ID=1.23 Data from the CIA World Factbook and the World Bank databases.

12

Furthermore, although in all the GCC countries power is concentrated in the hands of the members of royal families, who are appointed to the most important state offices, particular political systems in the region have some specific features that make each of them unique. For instance, all states but Bahrain have legislative bodies, playing mostly an advisory role, whose deputies are chosen in general elections or are nominated by local communities. The Sharia law is the cornerstone of the GCC countries’ legal systems, yet the scope of citizens’ rights and freedoms is not identical24.

Notwithstanding some differences in the geographical and political field, the Gulf states resemble each other significantly in terms of economy. In 2012 the total value of the GCC’s GDP reached nearly 15,490bn US dollars25. For obvious reasons, the sizes of their economies vary considerably. Saudi Arabia, the biggest country in terms of both territory and population, produced the most (711bn US dollars, which is about 45 per cent of the total regional output). Yet the performance of its smaller neighbours was no less impressive. Total GDP of Qatar and Kuwait was 192 and 183bn US dollars respectively, accounting for 12 and 11.6 per cent of the regional production26.

Figure 2 – Share of oil rents in the real GDP, 2000-2010 (percentage)

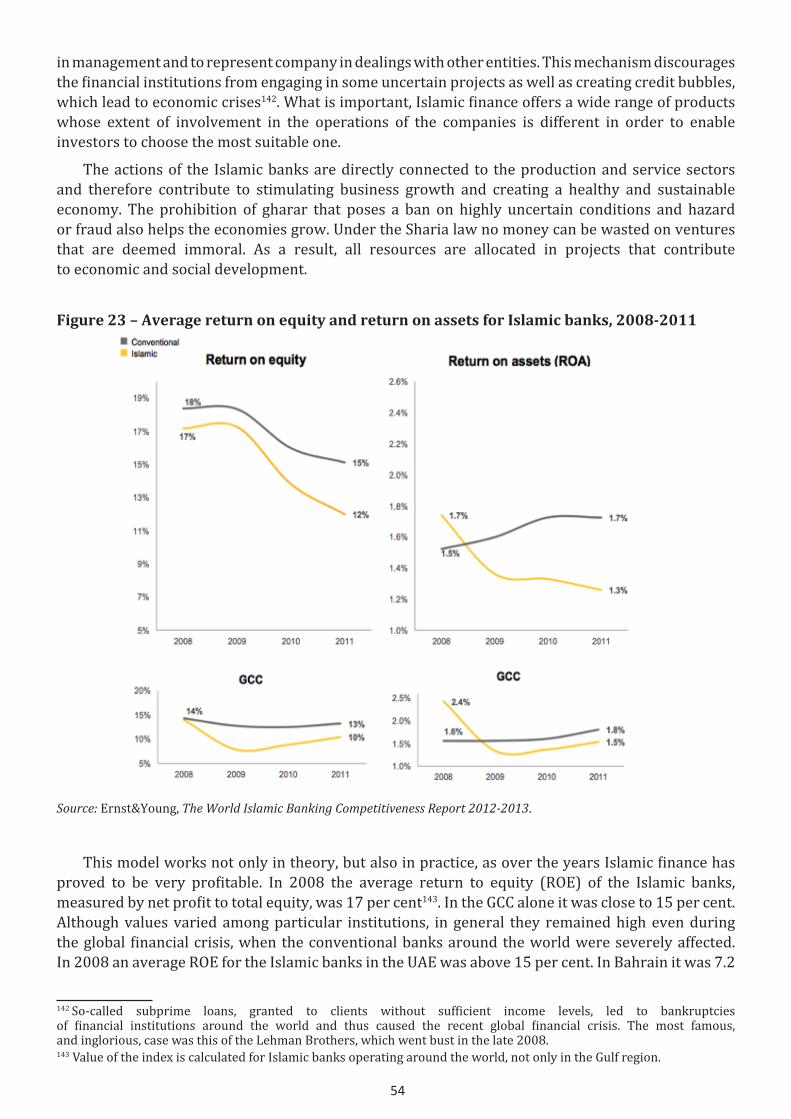

Source: Data from the World Bank database.

Moreover, as figure1 shows, since the very beginning of the 21st century the yearly GDP growth among all the GCC members was almost constantly positive (on the account of the outbreak of the global financial crisis a drop was noted in 2008). In 2012 the average growth rate in this region exceeded 5 per cent, which compared to the US’s 2.8 per cent, Germany’s 0.7 per cent the UK’s 0.3 per cent is undoubtedly a remarkable feat. Only China’s GDP growth was higher (in the same period its GDP increased by nearly 8 per cent).

The GCC societies benefited from this outstanding economic performance. In 2012 an average GDP per capita in the region was nearly 44,000 US dollars (in Qatar it was 93,825 US dollars). This value is akin to those noted in the most developed countries. In the same period the US GDP per

24 Saudi Arabia is deemed to be the most conservative among the GCC members. 25 Data from the World Bank database.26 Own calculations based on The World Bank data.

13

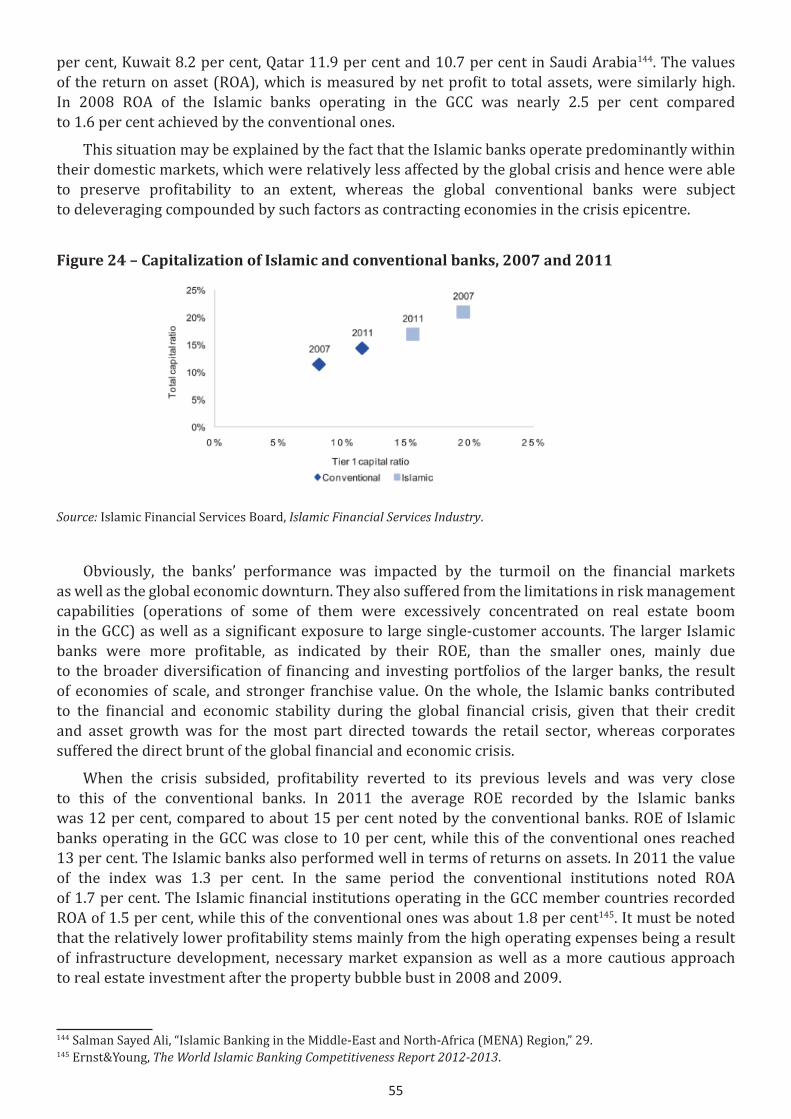

capita was 51,748 US dollars, while in Germany it was 42,624 US dollars27. A considerable improvement has also been noted in terms of quality of life. All the Council members are in high positions in the Human Development Report’s ranking. Qatar and the United Arab Emirates, placed in the group of countries with a very high HDI, are in the 36 and 41 places respectively. Bahrain, Kuwait, Saudi Arabia and Oman, which are in 48, 54, 57 and 84 places respectively, are marked as countries with a high HDI28.

A very important fact is that the GCC economies are driven by oil industry production. As figure 2 shows, oil rents contribute significantly to their real GDP. In 2010 profits coming from this sector accounted for nearly 50 per cent of Saudis and Kuwaiti revenues. Although the values noted in rest of the Council members were lower, they still exceeded the world average, which is well below 10 per cent. The yearly variations in the particular countries’ oil dependency stem from the volatility of oil prices that directly affect incomes.

Recently, each country has adopted a development strategy aiming at the economic diversification and creation of employment for nationals. Diversification may be defined in different ways depending on the field of application, yet on the whole it refers to ‘exports, and specifically to policies aiming to reduce the dependence on a limited number of export commodities that may be subject to price and volume fluctuations or secular declines’. (…) It also involves a shift from one sector or industry to another, and generally from the primary to the secondary and tertiary sectors’29.

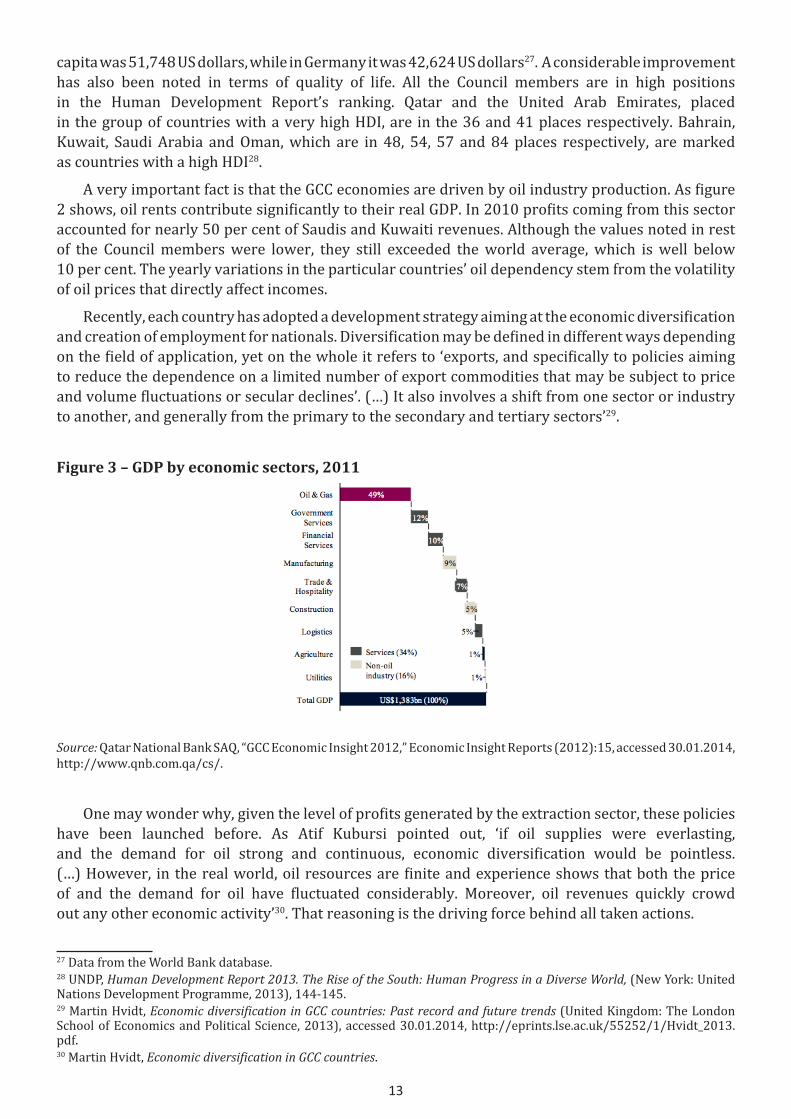

Figure 3 – GDP by economic sectors, 2011

Source: Qatar National Bank SAQ, “GCC Economic Insight 2012,” Economic Insight Reports (2012):15, accessed 30.01.2014, http://www.qnb.com.qa/cs/.

One may wonder why, given the level of profits generated by the extraction sector, these policies have been launched before. As Atif Kubursi pointed out, ‘if oil supplies were everlasting, and the demand for oil strong and continuous, economic diversification would be pointless. (…) However, in the real world, oil resources are finite and experience shows that both the price of and the demand for oil have fluctuated considerably. Moreover, oil revenues quickly crowd out any other economic activity’30. That reasoning is the driving force behind all taken actions.

27 Data from the World Bank database. 28 UNDP, Human Development Report 2013. The Rise of the South: Human Progress in a Diverse World, (New York: United Nations Development Programme, 2013), 144-145. 29 Martin Hvidt, Economic diversification in GCC countries: Past record and future trends (United Kingdom: The London School of Economics and Political Science, 2013), accessed 30.01.2014, http://eprints.lse.ac.uk/55252/1/Hvidt_2013.pdf.30 Martin Hvidt, Economic diversification in GCC countries.

14

The efforts aiming at creating a modern and fully sustainable economy date back to the wake of the so-called oil shocks that occurred in the 1970s. This goal has proven especially challenging, however, and a wide range of measures has been adopted since then.

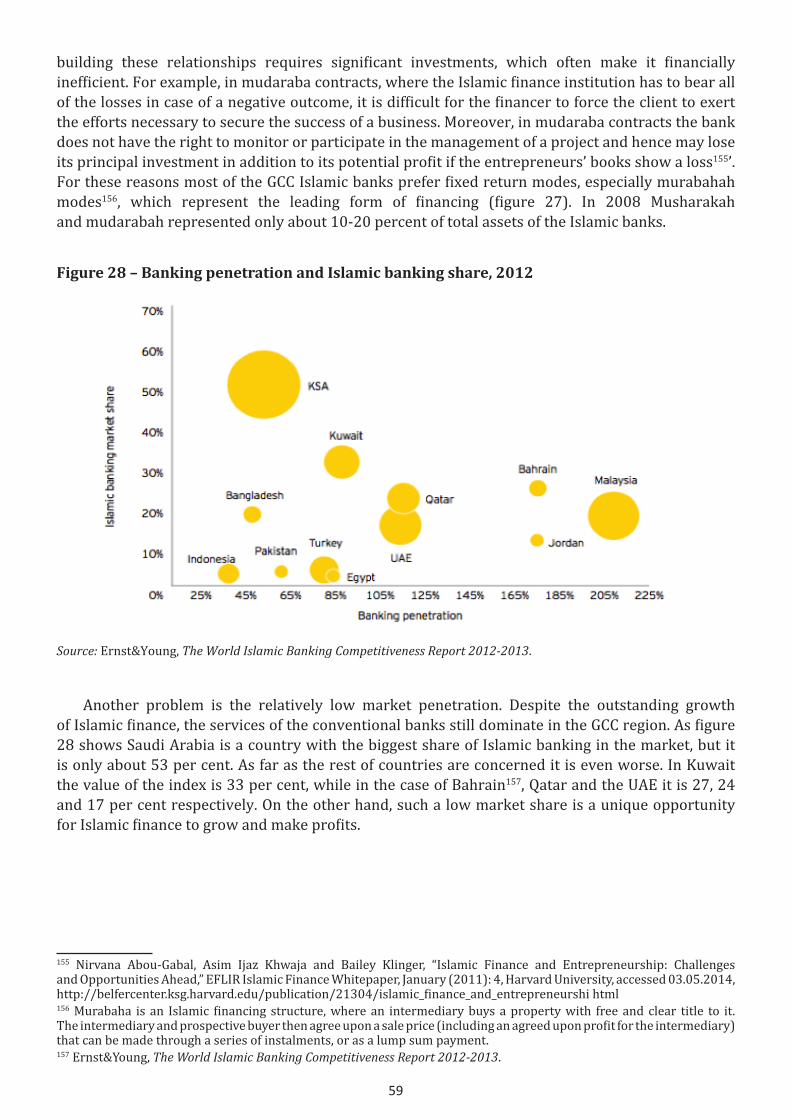

Figure 4 – Share of state spending in non-oil GDP in the GCC and selected international cases, 2000 and 2008

Source: Steffen Hertog, The private sector and reform in the Gulf Cooperation Council (United Kingdom: London School of Economics and Political Science, 2013), accessed 01.02.2014, http://www.lse.ac.uk/IDEAS/programmes/kuwait/documents/The-private-sector-and-reform-in-the-GCC.pdf.

Saudi Arabia has the longest and most developed tradition of planning among the GCC member states, institutionalized in the Ministry of Economy and Planning. Since 1970, nine development plans have been implemented. The latest, the Ninth Development Plan, applies to the 2010-2014 period. In 2004 a Long-Term Strategy, which covers the years 2005-2024, was published31. In July 2008, Qatar published a long-term plan called Qatar National Vision 203032, which was followed by the Qatar National Development Strategy 2011-201633 in March 2011. In October 2008, Bahrain adopted the Economic Vision 2030 plan34, and a year later the National Economic Strategy35, which is a detailed and short-term spending plan (its implementation is to help to achieve the Vision 2030 goals). Similarly, in 2010 the National Assembly of Kuwait accepted the State Vision Kuwait 2035 and a five-year development plan, concerning the years 2010 to 2014, which were accompanied by the adoption of a detailed expenditure budget36. In February 2010, the UAE launched its Vision 202137 followed by the UAE Government Strategy (2011-2013)38. Oman’s the Eighth Five-Year Development Plan (2011-2015) was announced in January 201139.

31 Martin Hvidt, Economic diversification in GCC countries. 32 General Secretariat for Development Planning, Qatar National Vision (Doha: General Secretariat for Development Planning, 2008), accessed 30.01.2014, http://www.gsd gov.qa/portal/page/portal/gsdp_en/qatar_national_vision/qnv_2030_document/QNV2030_English_v2.pdf.33 General Secretariat for Development Planning, Qatar National Development Strategy 2011-2016, (Doha: General Secretariat for Development Planning, 2011), accessed 30.01.2014, http://www.gsd gov.qa/gsdp_vision/docs/NDS_EN.pdf.34 “Economic Vision 2030 for Bahrain,” Bahrain News Agency, accessed 30.01.2014. http://bna.bh/portal/en/news/428203. 35 “New Budget Process,” Ministry of Finance of Kingdom of Bahrain, accessed 30.01.2014, https://www.mof.gov.bh/topiclist.asp?ctype=budget&id=870.36 Tariq A. Aldowaisan, A Reconciliated Country Vision, September (2010), accessed 30.01.2014. http://glc-im.com/wp-content/uploads/2012/12/Reconciled.Kuwait.Vision.E.pdf.37 “UAE Vision.” Vision 2021, accessed 30.01.2014, http://www.vision2021.ae/.38 “UAE Strategy 2011-2013” The Cabinet of United Arab Emirates, accessed 30.01.2014, http://uaecabinet.ae/en/Strategies/Pages/20112013-Strategy.aspx#.UuqB8nd5M1g.39 “Sultanate of Oman Major Business Sectors,” Embassy of Switzerland, accessed 30.01.2014, http://www.s-ge.com/de/filefield-private/files/784/field_blog_public_files/4852.

15

The purpose of these strategies is to enhance the competitiveness of the national economies in the global arena. All of them stress the need to boost productivity and competitiveness, and include promotion of a business environment conducive to growth. Targeted areas also include integrating the countries’ economies with the global knowledge economy, encouraging entrepreneurship, attracting foreign investment, fostering innovation and ensuring access to financing for small and medium-sized enterprises (SMEs). Other themes focus on recognition of the need to improve education and health outcomes, and the desirability of improving the efficiency of the public sector40. In short, the underlying goal of all these reforms is ‘to shift from an economy built on oil wealth to a productive, globally competitive economy, shaped by the government and driven by a pioneering private sector – an economy that raises a broad middle class that enjoy good living standards through increased productivity and high-wage jobs’41.

In the first decade of 21st century, all the GCC countries experienced an increase in the non-oil sectors’ contribution to the GDP growth. As set out in appendix 1, the services sector has played the central role in the diversification. Nonetheless, differences in shares of particular segments of the sector among the GCC countries can be observed. In the period 2000-2009, financial services grew rapidly in Bahrain, Kuwait, Qatar and the UAE, while the real estate services sector developed mostly in the UAE. Government services grew throughout the region, most markedly in Bahrain and the UAE. The construction boom was most pronounced in the UAE, with a significant growth in Qatar and Oman. Tourism is a rapidly growing sector in several countries, with Saudi Arabia – based on religious tourism – among the top 20 destinations in the world by the number of tourists42.

Nevertheless, as figure 4 shows the oil and gas sector still plays a major role in economy. In 2011 it accounted, on average, for the half of the GCC members’ GDP, while the government services, financial services, manufacturing and construction made for 12 per cent, 10 per cent, 9 per cent and 5 per cent respectively. On the whole, non-oil industry constituted only 16 per cent of the total production.

It must be noted that the share of state spending in the non-oil gross domestic product and of the government consumption in the total final consumption is considerably higher than in other parts of the world. Many of the 2000s booms, and thus a bulk of the diversification projects, were driven by state expenditures, which, as figure 5 shows, are strongly correlated with the hydrocarbon revenues. The GCC’s impressive results in terms of the HDI stem solely from government spending. What is more, an abnormally high share of private household consumption is financed through civil service wages, which dominate the total wage income of the GCC nationals (this issue will be explained more thoroughly in the second chapter).

As far as state spending and consumption patterns are concerned, Bahrain and the UAE seem to be more diversified than their neighbours. In the case of Bahrain, these figures seem to be explained by the fact that this country’s economy is dominatedby private service sector, financed, to a significant extent, by private capital from other GCC countries. Data concerning the UAE might understate the government’s role. It is because outside of Dubai the private sector activity is restricted, which makes unclear whether the United Nation’s figures for government spending and consumption include also ‘the emirate-level and public company activities’43.

Taking into account all presented information, the GCC countries have undoubtedly developed over the last few decades. Thanks to abundant oil and gas resources their economies have been

40 Samya Beidas-Strom et al., Gulf Cooperation Council Countries. Enhancing Economic Outcomes in an Uncertain Global Economy (International Monetary Fund, 2011), 2. 41 “Economic Vision 2030 for Bahrain,” Bahrain News Agency, accessed 30.01.2014. http://bna.bh/portal/en/news/428203.42 Samya Beidas-Strom et al., Gulf Cooperation Council Countries, 3. 43 Steffen Hertog, The private sector and reform in the Gulf Cooperation Council.

16

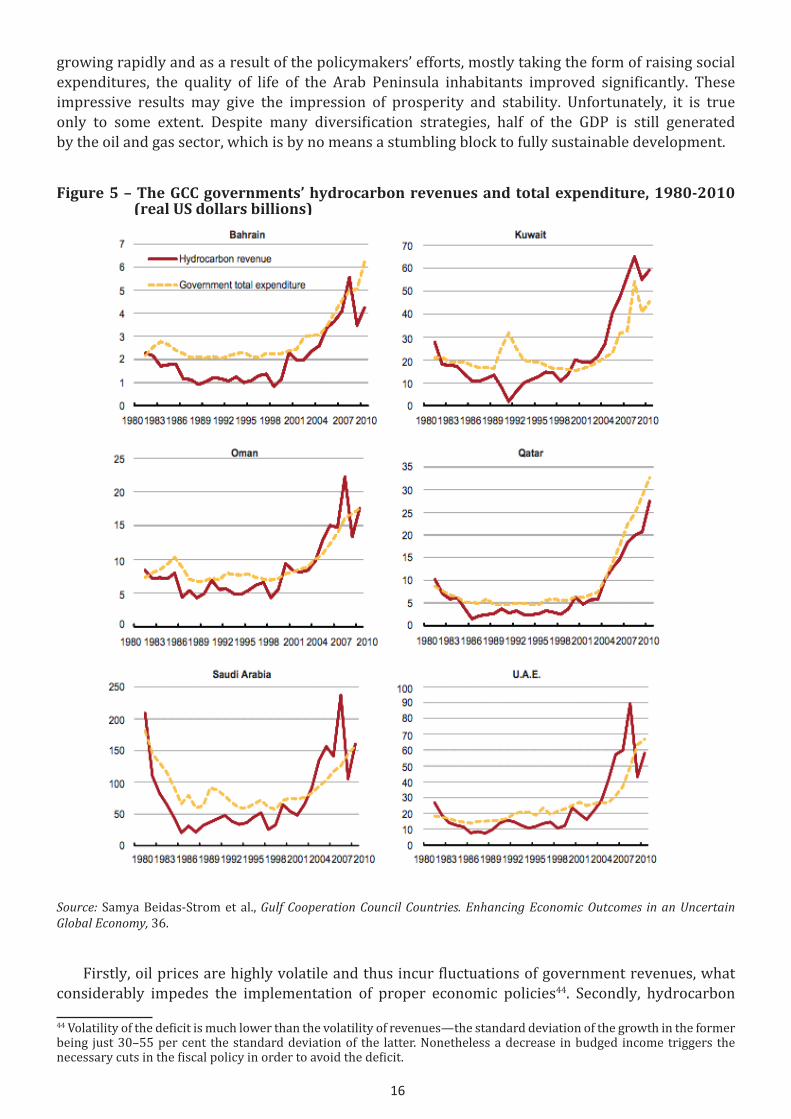

growing rapidly and as a result of the policymakers’ efforts, mostly taking the form of raising social expenditures, the quality of life of the Arab Peninsula inhabitants improved significantly. These impressive results may give the impression of prosperity and stability. Unfortunately, it is true only to some extent. Despite many diversification strategies, half of the GDP is still generated by the oil and gas sector, which is by no means a stumbling block to fully sustainable development.

Figure 5 – The GCC governments’ hydrocarbon revenues and total expenditure, 1980-2010 (real US dollars billions)

Source: Samya Beidas-Strom et al., Gulf Cooperation Council Countries. Enhancing Economic Outcomes in an Uncertain Global Economy, 36.

Firstly, oil prices are highly volatile and thus incur fluctuations of government revenues, what considerably impedes the implementation of proper economic policies44. Secondly, hydrocarbon

44 Volatility of the deficit is much lower than the volatility of revenues—the standard deviation of the growth in the former being just 30–55 per cent the standard deviation of the latter. Nonetheless a decrease in budged income triggers the necessary cuts in the fiscal policy in order to avoid the deficit.

17

resources are not renewable, meaning that someday they will peter out and bring no more profits. Thirdly, the employment creation provided by the oil sector is limited it is assessed that it employs less than 3 per cent of the region’s labour force. This economic model simply cannot work forever and without a doubt will not ensure the development that ‘meets the needs of the present without compromising the ability of future generations to meet their own needs’45.

As Martin Hvid noticed, ‘the Gulf states’ drama is that it [oil extraction] is not simply another economic activity added to other existing productive sources within a viable and modern economy, as it is with the Netherlands or, for that matter, Canada, Australia, and the Scandinavian countries. In the Gulf, the oil sector dominates the economy; it is almost the unique source of wealth’46.

So as to examine the problem of the GCC economies more deeply and understand why the diversification efforts failed, an analysis of the GCC business environment and enterprises performance must be conducted.

45 “Report of the World Commission on Environment and Development. Our Common Future,” United Nations, 37.46 Martin Hvidt, Economic diversification in GCC countries, 4.

18

19

2. Business environment in the GCC

2.1. The role of small and medium enterprises in the Gulf economies

It is a widely known fact that small and medium enterprises are a stepping-stone towards truly sustainable development, as they contribute significantly to job creation, economic growth and diversification. According to the OECD data, at the turn of 21st century SMEs contributed to over 55 per cent of GDP and over 65 per cent of total employment in high-income countries, over 60 per cent of GDP and over 70 per cent of total employment in low-income countries and 95 per cent of total employment and about 70 per cent of GDP in middle-income countries47.

The notion of entrepreneurship development as well as the SME term itself was conceived in the late 1940s along with the introduction of so-called targeted policies (grants, subsidized credits, special tax treatment etc.). Nonetheless, statistical definition of SMEs still considerably varies by country, generally comprising at least one of the following factors: the number of employees, the annual turnover and assets of a company. Given the relative ease of data collection, the most commonly variable used is the number of employees. The EU and a large number of the OECD, transition and developing countries set the upper limit of the number of employees in the SMEs between 200-250. In Japan and the USA the thresholds are 300 and 500 employees respectively48. At the lower end of the SME scale, many countries consider companies as small or the medium ones when they hire less than 10 employees49. It should be noted that irrespectively of the level of economic development, a considerable proportion of micro and (sometimes) small enterprises operate in the informal sector or the shadow economy.

As far as the GCC is concerned, there is also no common definition of SMEs that would be accepted and used by all the Council members. In Bahrain, an enterprise that is considered to be of micro size has up to 10 employees, while small and medium-sized ones have up to 50 and 150 employees respectively. In terms of investment levels the thresholds in each category are 53,000, 1.3 million and 5.3 million dollars. In Saudi Arabia, small businesses hire less than 60 people and their assets are worth up to 1.3 million dollars while the medium ones employ less than 100 and invest no more than 5.3million dollars. The UAE’s micro enterprises have less than 10 workers, while the small and medium ones have less than 25 and 100 employees respectively (in the latter case turnover cannot surpass 100 million Dirham per year, which is equivalent to 27 million dollars). In Oman, companies with up to 5 hired people are treated as micro ones, while small and medium entities employ 20 and 100 people respectively. Kuwaiti institutions use mainly financial criteria defining small and medium enterprises as projects with the capital between 500,000 and 520,000 dollars. Interestingly enough, in Qatar there seems to be no consensual definition pertaining to any of the types of enterprises50.

47 2nd OECD Conference of Ministers Responsible for Small and Medium Sized Enterprises, Promoting Entrepreneurship and Innovative SMEs in a Global Economy: Towards a More Responsible and Inclusive Globalisation (Istanbul: Organisation for Economic Co-Operation and Development, 2004), accessed 17.02.2014, http://www.oecd.org/cfe/smes/31919278.pdf. 48 2nd OECD Conference of Ministers Responsible for Small and Medium Sized Enterprises, Promoting Entrepreneurship and Innovative SMEs in a Global Economy: Towards a More Responsible and Inclusive Globalisation.49 As a result of a serious lack of cooperation between the government institutions the criteria differ also within the particular countries. 50 Steffen Hertog, Benchmarking SME Policies in the GCC: a survey of challenges and opportunities (Brussels: Eurochambres, 2010), accessed 17.02.2014, http://eprints.lse.ac.uk/29870/.

20

On average, SMEs employ between 10 and 50 workers, so their impact on employment across the GCC is above 8.5 million jobs51.

The access to data concerning the SMEs’ share in the Gulf economies has improved over the years, however, specific figures are still scarce and often patchy, what often makes them incomparable across countries. The statistical data used in this paper were prepared by the EU-GCC Chamber Forum and are of the best possible quality accessible to a young researcher.

On the whole, SMEs constitute more than 90 per cent of enterprises in every GCC member country. In 2007 there were about 40,000 SMEs operating in Bahrain, indicating a high density of business – one company per 25 inhabitants of the country. Nearly 50 per cent of entire workforce was hired in micro-enterprises with up to 4 employees. In the same period in Kuwait the estimated number of SMEs amounted to ca. 33,000. According to the data from 2008, in Oman nearly 45,000 companies were considered as small or medium – 42.6 per cent were sole proprietorships while 37.2 per cent employed up to 5 workers. The same year in Saudi Arabia 785,000 enterprises were registered, 764,000 of which had only one employee, meaning that there was one SME per 25 inhabitants of the kingdom. As for Qatar, statistics about its private sector are divided into two groups: concerning entities with less than 10 employees, and those with 10 employees or more. In 2006 the number of companies employing less than 10 people exceeded 10,000, which constituted 75 per cent of all businesses. As far as the United Arab Emirates are concerned, the latest data that proves reliable comes from 1995. Back then, more than 92,000 companies were registered as having less than 100 employees. According to the EU-GCC Chamber Forum, till 2005 their number rose to about 157,00 and in 2007 there were 85,000 SMEs registered in the Dubai Chamber of Commerce and Industry alone52.

While analysing the sectoral breakdown of small and medium business entities, it is noticeable that they are a very heterogonous group. It is so due to the fact that these types of enterprises offer a chance of decent and, even more importantly, independent life to everybody, regardless of their profession. An enterprise of micro or small size may be established and run equally by a merchant, farmer, hairdresser as well as an engineer, artist, architect etc. They may operate both in the city and countryside, selling their products and services on the local, regional and sometimes even on the global market.

According to the Bahraini Ministry of Industry and Commerce, in 2007 more than a third of the SMEs dealt with manufacturing fabricated metal products, 16 per cent produced non-metallic mineral products, 15 per cent operated in chemicals and chemical products segment and 11 per cent dealt with food production53. In Kuwait, small and medium-sized business entities are concentrated in two sectors: in 2007 a third of the SMEs was active in the construction and industry segment and 40 per cent dealt with wholesale/retail trade and hotels and restaurants. As for Saudi Arabia, in 2008 almost a half of the SMEs operated in the commercial and hotel sector, a third dealt with construction and 12 per cent were active in industry. In 2006, about 65 per cent of Qatari small and medium businesses dealt with trade, almost 20 per cent operated in industry and 15 per cent ran hotels and restaurants. Merchants also dominate the United Arab Emirates’ market – 60 per cent of SMEs deal with trade, while 35 per cent of them operate in the services sector54. In the case of Oman, there are no available data in terms of sectoral breakdown. On the whole, in 2010 across the GCC region 47 per cent of SMEs were engaged in commercial, trading

51 Omar Fisher, “Small and Medium-Sized Enterprises and Risk in the Gulf Cooperation Council Countries: Managing Risk and boosting Profit,” QFinance, accessed 10.05.2014, http://www.financepractitioner.com/contentFiles/QF02/gwtb8s2b/10/0/small-and-medium-sized-enterprises-and-risk-in-the-gulf-cooperation-council-countries-managing-risk-and-boosting-profit.pdf. 52 Steffen Hertog, Benchmarking SME Policies in the GCC. 53 Venture Capital Fund Bahrain, Private Placement Memorandum, (Bahrain: Venture Capital Fund Bahrain, 2008), 22, http://www.lf.bh/docs/VCF-Private%20Placement%20Memorandum-En.pdf, accessed: 20.02.2014.54 Steffen Hertog, Benchmarking SME Policies in the GCC.

21

and hotel businesses, 27 per cent in construction, 12 per cent in manufacturing, 6 per cent in social services and 8 per cent in sundry other sectors55.

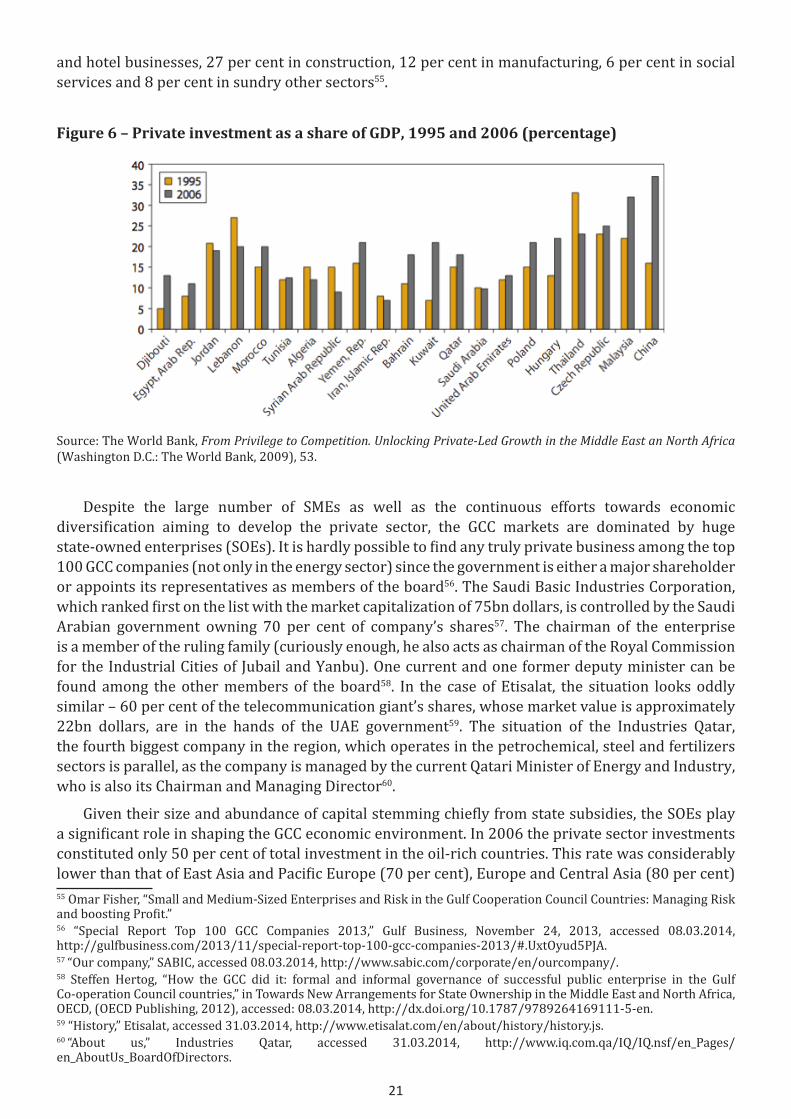

Figure 6 – Private investment as a share of GDP, 1995 and 2006 (percentage)

Source: The World Bank, From Privilege to Competition. Unlocking Private-Led Growth in the Middle East an North Africa (Washington D.C.: The World Bank, 2009), 53.

Despite the large number of SMEs as well as the continuous efforts towards economic diversification aiming to develop the private sector, the GCC markets are dominated by huge state-owned enterprises (SOEs). It is hardly possible to find any truly private business among the top 100 GCC companies (not only in the energy sector) since the government is either a major shareholder or appoints its representatives as members of the board56. The Saudi Basic Industries Corporation, which ranked first on the list with the market capitalization of 75bn dollars, is controlled by the Saudi Arabian government owning 70 per cent of company’s shares57. The chairman of the enterprise is a member of the ruling family (curiously enough, he also acts as chairman of the Royal Commission for the Industrial Cities of Jubail and Yanbu). One current and one former deputy minister can be found among the other members of the board58. In the case of Etisalat, the situation looks oddly similar – 60 per cent of the telecommunication giant’s shares, whose market value is approximately 22bn dollars, are in the hands of the UAE government59. The situation of the Industries Qatar, the fourth biggest company in the region, which operates in the petrochemical, steel and fertilizers sectors is parallel, as the company is managed by the current Qatari Minister of Energy and Industry, who is also its Chairman and Managing Director60.

Given their size and abundance of capital stemming chiefly from state subsidies, the SOEs play a significant role in shaping the GCC economic environment. In 2006 the private sector investments constituted only 50 per cent of total investment in the oil-rich countries. This rate was considerably lower than that of East Asia and Pacific Europe (70 per cent), Europe and Central Asia (80 per cent) 55 Omar Fisher, “Small and Medium-Sized Enterprises and Risk in the Gulf Cooperation Council Countries: Managing Risk and boosting Profit.” 56 “Special Report Top 100 GCC Companies 2013,” Gulf Business, November 24, 2013, accessed 08.03.2014, http://gulfbusiness.com/2013/11/special-report-top-100-gcc-companies-2013/#.UxtOyud5PJA. 57 “Our company,” SABIC, accessed 08.03.2014, http://www.sabic.com/corporate/en/ourcompany/. 58 Steffen Hertog, “How the GCC did it: formal and informal governance of successful public enterprise in the Gulf Co-operation Council countries,” in Towards New Arrangements for State Ownership in the Middle East and North Africa, OECD, (OECD Publishing, 2012), accessed: 08.03.2014, http://dx.doi.org/10.1787/9789264169111-5-en.59 “History,” Etisalat, accessed 31.03.2014, http://www.etisalat.com/en/about/history/history.js. 60 “About us,” Industries Qatar, accessed 31.03.2014, http://www.iq.com.qa/IQ/IQ.nsf/en_Pages/en_AboutUs_BoardOfDirectors.

22

and Latin America and the Caribbean (95 per cent) for 2006. Even in the non-oil-rich MENA economies the level of private investment was higher (62 per cent)61. As a result, the bulk of achievements in terms of diversifications result directly from the SOEs operation, which – being a kind of governmental tool – are commonly used to implement the government’s policies. Thanks to the sovereign backing them they are able to engage in longer-term strategies of research and product development, which are often too risky for private entities and do not yield sufficient profits. The enormous infrastructure investment activities conducted by Etihad (Abu Dhabi), Emirates (Dubai) and Qatar Airways (Qatar) 62, SABIC’s involvement in materials research and national human resource development, or the efforts of the Abu Dhabi’s ATIC to create a local semi-conductor industry thanks to large-scale local recruitment and training are perfect examples63.

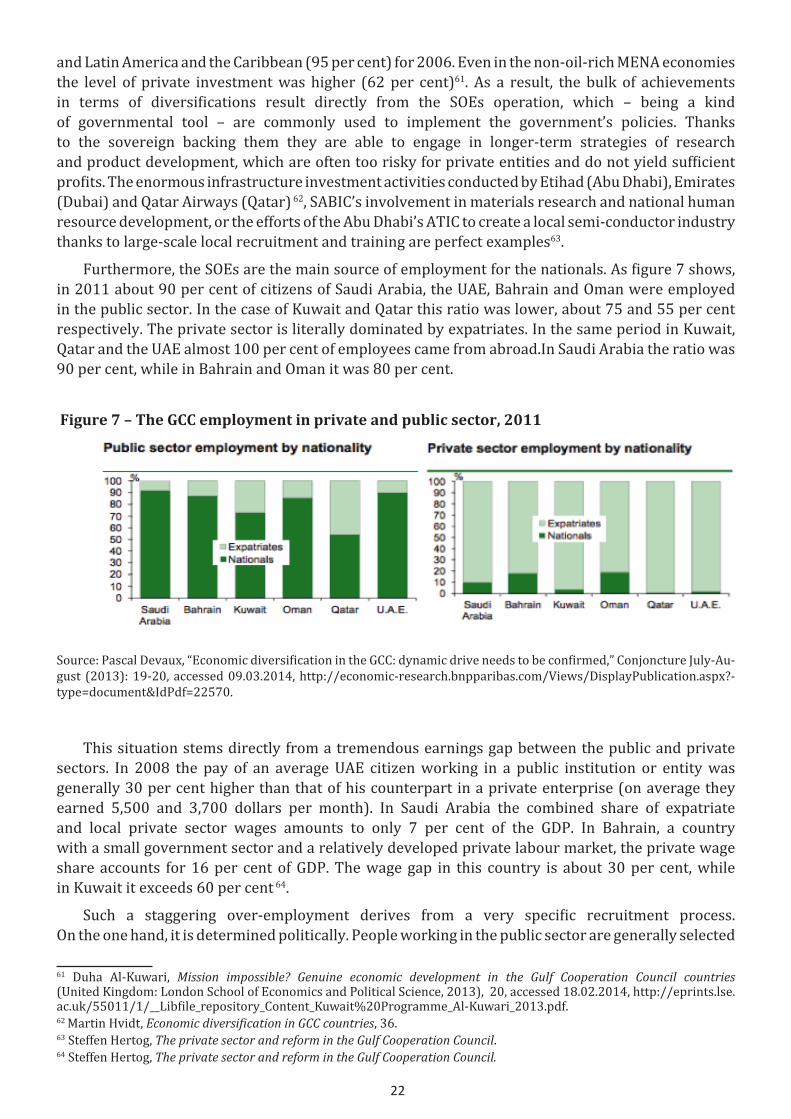

Furthermore, the SOEs are the main source of employment for the nationals. As figure 7 shows, in 2011 about 90 per cent of citizens of Saudi Arabia, the UAE, Bahrain and Oman were employed in the public sector. In the case of Kuwait and Qatar this ratio was lower, about 75 and 55 per cent respectively. The private sector is literally dominated by expatriates. In the same period in Kuwait, Qatar and the UAE almost 100 per cent of employees came from abroad.In Saudi Arabia the ratio was 90 per cent, while in Bahrain and Oman it was 80 per cent.

Figure 7 – The GCC employment in private and public sector, 2011

Source: Pascal Devaux, “Economic diversification in the GCC: dynamic drive needs to be confirmed,” Conjoncture July-Au-gust (2013): 19-20, accessed 09.03.2014, http://economic-research.bnpparibas.com/Views/DisplayPublication.aspx?-type=document&IdPdf=22570.

This situation stems directly from a tremendous earnings gap between the public and private sectors. In 2008 the pay of an average UAE citizen working in a public institution or entity was generally 30 per cent higher than that of his counterpart in a private enterprise (on average they earned 5,500 and 3,700 dollars per month). In Saudi Arabia the combined share of expatriate and local private sector wages amounts to only 7 per cent of the GDP. In Bahrain, a country with a small government sector and a relatively developed private labour market, the private wage share accounts for 16 per cent of GDP. The wage gap in this country is about 30 per cent, while in Kuwait it exceeds 60 per cent 64.

Such a staggering over-employment derives from a very specific recruitment process. On the one hand, it is determined politically. People working in the public sector are generally selected

61 Duha Al-Kuwari, Mission impossible? Genuine economic development in the Gulf Cooperation Council countries (United Kingdom: London School of Economics and Political Science, 2013), 20, accessed 18.02.2014, http://eprints.lse.ac.uk/55011/1/__Libfile_repository_Content_Kuwait%20Programme_Al-Kuwari_2013.pdf. 62 Martin Hvidt, Economic diversification in GCC countries, 36.63 Steffen Hertog, The private sector and reform in the Gulf Cooperation Council. 64 Steffen Hertog, The private sector and reform in the Gulf Cooperation Council.

23

not on the basis of their qualifications but rather thanks to their family connections65. On the other hand, working patterns are shaped by basic market forces. Most of the jobs in private enterprises – which are created mainly during periods of prosperity, meaning high energy sources prices – tend to go to foreign workers, as the price of this type of labour is simply lower. On the whole, the rise in the employment of nationals is noted solely after administrative interventions of forced ‘Saudi-zation’, ‘Kuwait-ization’ or ‘Oman-ization’. ‘Business for the most part has been fighting this nationalization agenda tooth and nail, as it increases costs and saddles them with more demanding employees who are much harder to dismiss66’.

One must be aware that the number of jobs created by the private sector in the GCC is significant. The fact that they are low-paid results from the factor-intensive growth approach that limits private-driven diversification and is politically as well as economically unsustainable in the long term (this issue will be discussed more deeply in the next section of the thesis)67. As a result, in spite of the increasing share of the private sector in GDP, generation of private demand remains quite limited. This means that in most GCC countries an untypically large part of consumer demand is, in fact, financed via state salaries and transfers – in Saudi Arabia, state salaries are twice the size of combined private salaries68.

Despite an undoubtedly significant role of the SOEs, the GCC governments have always pursued a pro-capitalist economic agenda. Unlike most of the republican regimes of the Arab region, local merchants never had to witness the waves of nationalization that crippled business classes in countries like Algeria, Egypt or Syria. One should be aware that the Gulf economies have never been particularly diversified. In the early oil era the actual productive capacities of the GCC entrepreneurs were particularly limited – they often operated as intermediaries and access brokers for international companies providing most of the actual goods and services that the rapidly growing GCC economies demanded. Now private business plays a more significant role in the sectors like education, health, telecoms, heavy industry and air transport, which until the 1990s were partly or completely state-controlled.

Nevertheless, aiming to create truly sustainable production patterns, the GCC incumbents should step up their efforts towards supporting the SMEs development (creating a business-friendly environment is one of the points of the Agenda 21). As it will be proved in the next section of the study, the SMEs’ small contribution to GDP and to job creation is not a result of their defective nature. They just face too many challenges precluding them from thriving.

2.2. Constraints for the Gulf SMEs’ operations

The existence SMEs is not a simple guarantee of growth and prosperity. It is merely a precondition. Undoubtedly, they facilitate economic growth inducing productivity, job creation and consumption. But it is not their quantitative development that ensures truly sustainable development. From the economic point of view, there is no big difference whether one hundred or two hundred merchants operate in a country barely making ends meet and who are thus unable to hire any extra employees. Small and medium entrepreneurs willing to innovate and advance are much more important. It is therefore the increase in the SMEs’ operations quality that truly matters.

65 It is essential to note that they very well educated because being born to affluent families can afford to pay for educations at foreign universities. 66 Steffen Hertog, The private sector and reform in the Gulf Cooperation Council.67 Steffen Hertog, State and private sector in the GCC after the Arab uprisings (United Kingdom: LSE Research Online, 2014), accessed 10.05.2014, http://eprints.lse.ac.uk/54399/1/Hertog_state_private_sector_GCC_after_arab_uprising_final.pdf.68 Steffen Hertog, The private sector and reform in the Gulf Cooperation Council.

24

The Gulf economies combine features of developed and emerging markets in a very peculiar way. The income levels are high, infrastructure is well developed, national populations are well educated and large companies are generally professionally run. Furthermore, small and medium enterprises constitute a majority of business entities in the GCC countries. Yet they do not contribute to GDP and job creation as one may think, since wages offered in this segment are relatively low and employers favour hiring expatriates. It is so because they operate in a highly unfriendly environment constraining their genuine development. These include both universal problems that SMEs around the world struggle with, and numerous issues that are characteristic of the GCC states.

Firstly, there is the issue of modern technology and necessary infrastructure within companies. Technological innovation is undoubtedly a vital tool for enhancing efficiency and competitiveness. Thanks to the cutting edge innovations, it is possible to produce more using the same (or even lower) amount of resources. Such a process is called ‘intensive growth’. In factories, modern production lines streamline production, making it both faster and cheaper. In trade, better cars, well-equipped warehouses (such as cold stores with well-functioning cooling systems) improve merchants’ capabilities. The same happens with services where tools of higher quality help to save time and thus make it possible to serve more consumers.

Nevertheless, as far as the GCC countries are concerned, research and development (R&D) in the region is still a fledgling area. Technology clusters around specific industries and the links between business and the local universities are still very weak. In 2009, R&D expenditure constituted 0.11 per cent of GDP in Kuwait, 0.08 per cent in Saudi Arabia and less than 0.1 per cent in the UAE69.

Secondly, there is a problem with human resources. One does not need specialised knowledge to notice that educated staff facilitates daily operations. Not only are such employees able to use more advanced technology and solve problems quickly and easily, but they may also innovate and propose their own solutions. Well-qualified employees are not simply labour, they are human capital.

Yet again, plenty of problems appear. Companies operating in the Gulf region are considerably short of skilled human resources. Employees in the Arab SMEs are generally weak in terms of their knowledge and skills of market analysis, marketing and product innovation as well as business planning and financial management. Better-qualified people prefer to work in the SOEs where the wages are higher. The private sector is literally dominated by expatriates who often lack basic education. According to a study conducted by the SMEs Center at the Rihyadh Chamber of Commerce and Industry, 44 per cent of the SMEs’ managers see workforce issues as an important obstacle to their development70.

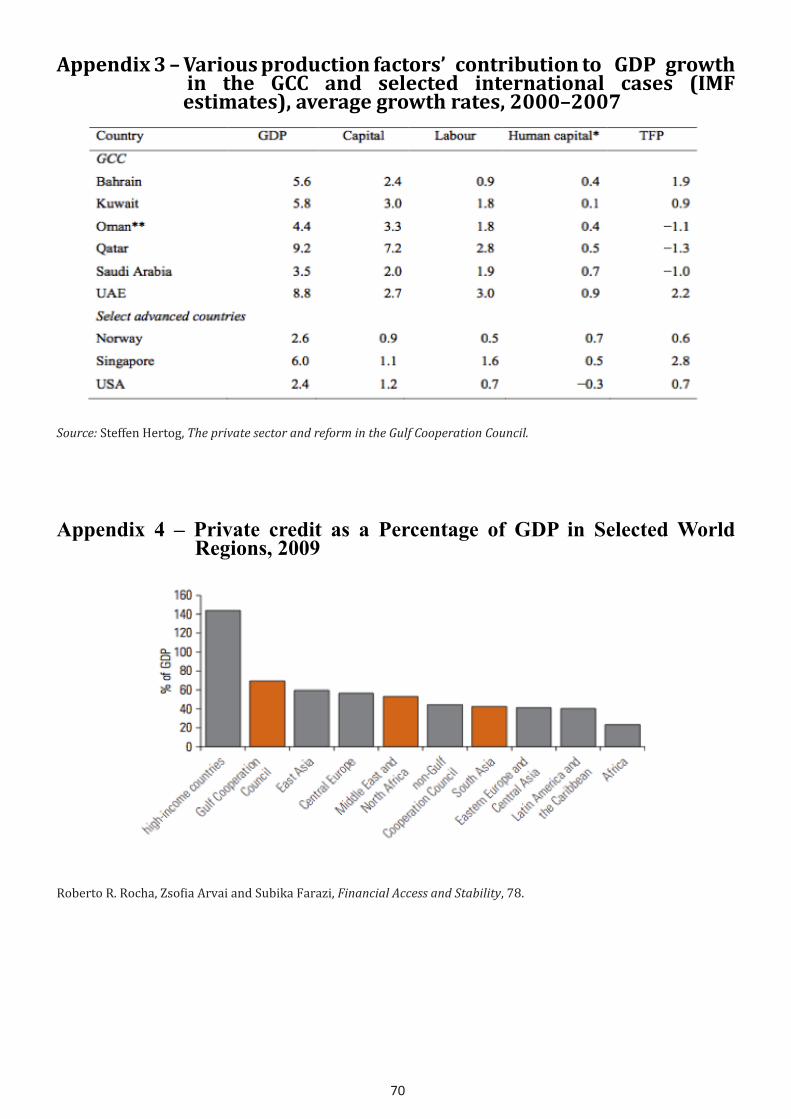

The contribution of production factors to GDP in the GCC varies from the one observed in developed countries. On the whole, economic growth has been significantly based on capital input71 – in the Gulf between 2000 and 2007 the average growth rate was 3.4 per cent, while in the USA it was only 1.2. Similarly, the average growth rate of labour volume used in production processes (2.03 per cent) exceeds the ones noted in the advanced economies (0.7 per cent, 0.5 per cent noted in the USA and Norway respectively). When it comes to human capital, the situation is better – 0.5 per cent in the GCC versus -0.3 in the USA and 0.7 per cent in Norway. We should remember, however, that it is an average growth rate of the contribution of particular factors, not their share in total GDP.

The average growth in total-factor productivity, an index including technological improvements, is less impressive. Its values in Oman, Qatar and Saudi Arabia were negative (about -1 per cent)

69 Steffen Hertog, The private sector and reform in the Gulf Cooperation Council. 70 Steffen Hertog, Benchmarking SME Policies in the GCC: a survey of challenges and opportunities.71 The capital of the private sector has been generally put into housing, land and real estate infrastructure rather than into technology acquisition.

25

and for the whole region it was only 0.43 per cent (in the USA and Norway it was 0.7 and 0.6 per cent respectively). This situation reflects the GCC growth patterns. For decades, development has been based on the extensive use of production factors rather than improvements in their productivity, let alone development of human capital. Apart from almost unlimited access to capital provided by the extraction sector as well as cheap labour, this situation also results from low user energy prices, which are immensely subsidised by the state. In these circumstances, entrepreneurs have simply no incentive to innovate. Instead of investing their money in research and development or organising trainings for their employee, they prefer to remain on a resource-intensive, low-to-mid-tech development path.

Dealing with national administration is not an easy task anywhere. Complicated procedures, concerning not only establishing companies but also their daily operations, sometimes demanding deep knowledge on law, high administrative fees and, most importantly, a great deal of wasted time are without doubt stumbling blocks to entrepreneurship. Doing Business, a report prepared by the World Bank, compares the ease of doing business between different countries. The index is calculated on the basis of the rankings of each economy in 10 fields: starting a business, dealing with construction permits, getting electricity, registering property, getting credit, protecting investors, paying taxes, trading across borders, enforcing contracts and resolving insolvency. In the 2014 edition of the report the UAE, Saudi Arabia, Bahrain, Oman, Qatar and Kuwait ranked 23rd, 26th, 46th, 47th, 48th and 104th respectively. It may seem remarkable, yet we should bear in mind that the United States and Norway, which the GCC members where compared with in terms of productivity of production factors’, ranked 4th and 9th respectively72.

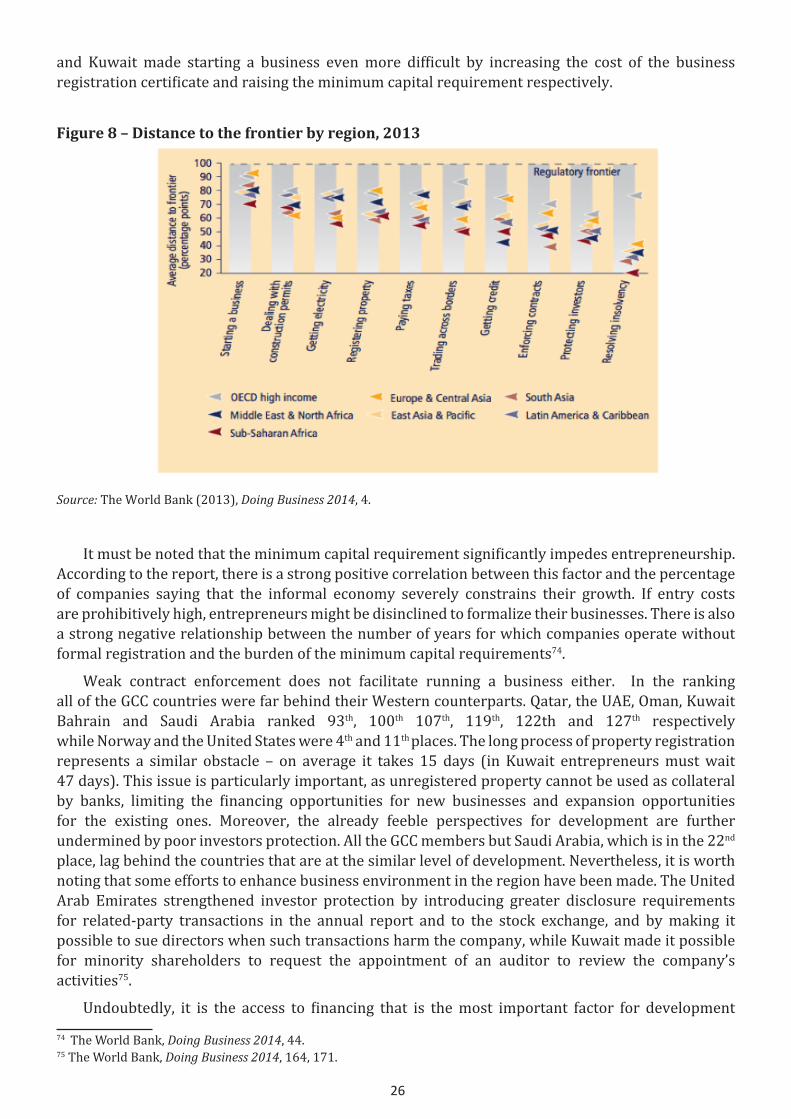

To complement ranking measuring the ease of doing business, in 2012 the report introduced another category – the distance to frontier, an absolute measure of business regulatory efficiency. By showing the distance of each economy to the ‘frontier’ – which represents ‘the best performance observed on each of the Doing Business indicators’ since 2003 or the year in which the data for the indicator were first collected – this measure ‘aids in assessing how much the regulatory environment for local entrepreneurs improves in absolute terms over time’. The measure is normalized in a range between 0 and 100, with 100 representing the frontier. The higher score indicates the more efficient business environment and the stronger legal institutions (for a detailed description of the methodology, see the chapter on the ease of doing business and distance to frontier)73.

As chart 8 shows, despite their high level of economic growth and development, the Middle East countries perform worse than their high-income OECD partners or countries in Europe and Central Asian do. The worst results are noted in terms of protecting investors, enforcing contracts, getting credit and resolving insolvency. An analysis of the particular components of the index helps to understand the roots of this situation.