Embed Size (px)

Citation preview

Glasgow Housing Association www.gha.org.uk

A role for the social rented sector in market rental housing Paper for Facing Scotland's Housing Challenges, Part 2 Fanchea Kelly, Executive Director of Housing and Support Services St Andrews University Friday 12 October 2012

1

Contents Introduction………………………………………………………………...p2 1. The Scottish Housing Market and the Glasgow and Clyde Valley

Housing Need Demand Analysis………………………………..p3 2. Housing and Young People……………………………………...p6 3. Housing and Families…………………………………………….p8 4. The Current Private Market Rental Sector……………………..p9 5. Customer Experience and the Need for Change…..………..p10 6. Registered Social Landlords:

Landlord of Choice for ‘Generation Rent’?..............................p12 7. Commercial Lending and the RSL Sector……………………..p14 8. Key Challenges for Social Housing Providers

and Conclusions………………………………………………….p17

Appendix 1……………………………………………………….............p18

2

Introduction GHA greatly welcomes the opportunity to produce this paper which aims to examine the new role of Registered Social Landlords (RSLs) in market rental housing. There are a number of drivers which point to the growing importance of the Private Rented Sector (PRS) playing an increasingly important role in meeting housing demand. A key example of such a driver is the current economic climate, and its effect on the ability of potential house buyers, particularly younger people, to attain mortgage credit. This contraction of availability, coupled with high house prices and increased demand in the social sector are all discussed in the paper below, with a focus on the Glasgow and Clyde Valley market area.

In this context, other drivers to which social housing providers traditionally respond also require new responses. For example, communities are not mono-tenure and do not aspire to be. Social landlords are well placed to explore new solutions on behalf of communities, including moving into some of the current private rental market. This paper examines the changing patterns of demand for affordable, mid and full market rental properties. Provision of the latter tenures has not been the traditional role of RSLs.

This paper also briefly discusses the Scottish Government’s response to these issues and offers some discussion of tenants’ experiences in the PRS and some of the issues that face social landlords in moving into market rental activities.

This paper contends that the housing system in Scotland faces unprecedented challenges and that RSLs need to seek new pathways to create and support a sustainable, high-quality, multi-tenure housing system for future generations. Stepping beyond the provision and management of social housing stock is an integral part of this.

RSLs must have the self confidence to rise to these challenges and use their assets, knowledge of communities, skills and abilities to seek opportunities and seek solutions to the challenges that customers face.

Appendix 1 shows some examples of GHA’s recent activity in the wider rental market.

3

1. The Scottish Housing Market and the Glasgow and Clyde Valley Housing Need Demand Analysis

RSLs are likely to become increasingly involved in the provision of market rental housing as a method of meeting housing demand, along with efficient use of social housing assets. The Scottish Government has made it clear that innovative, radically different ways of meeting housing need across all tenures is required in Scotland. “Homes Fit for the 21st Century”, the Scottish Government’s housing strategy document for the next decade, states: “We need more homes in each of the established tenures: owner occupation, private rent and social rent. But there are growing numbers of people whose needs aren't met by any of these established tenures - people who can't access home ownership and are struggling to afford private rents, yet are unlikely to get a social let. To provide new options for this group, we will require a substantial expansion of mid-range housing products. We will continue to support shared equity, and in particular will expand provision of homes for intermediate rent”1

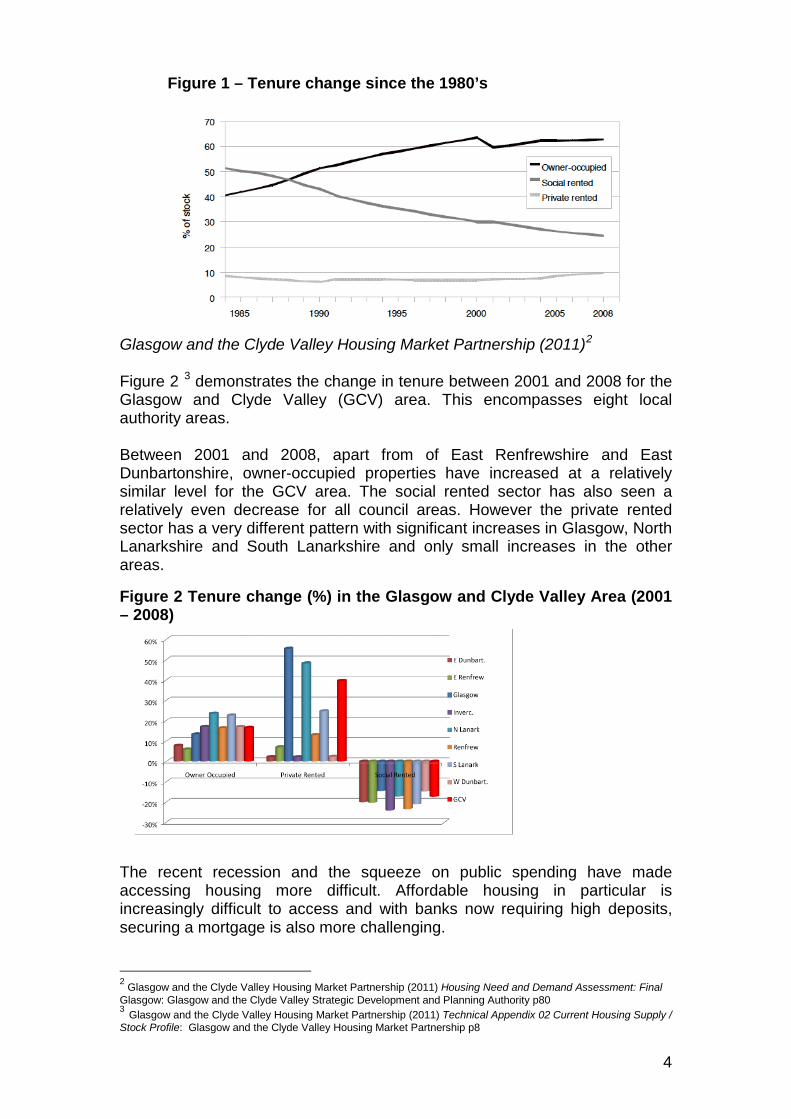

Figure 1

.

“Homes Fit for the 21st Century” also opens the way, through further consultation on a range of tenancy regimes, to give RSLs greater flexibility and “responsibility to determine their own approach to meeting need”. This means that the building blocks are being put in place to make it easier for RSLs to expand their activity in the wider rental market. The Housing Need and Demand Analysis carried out in 2011 for the Glasgow and Clyde Valley area, demonstrated that there is a strong demand for affordable housing in the City. Further work carried out with customers shows that people are waiting longer for social housing in Glasgow than they did in the past. This shortage of affordable housing has only occurred relatively recently in Glasgow, given that previous work between 2004 and 2007 identified a surplus of social rented stock.

Flexibility of rented tenures over time will be vital for housing providers to meet housing demand. Examples of such flexibility are potentially moving from full market rental to social rental or from social rented sector to the mid-market rented sector. There are emerging models, particularly in England, of how social housings providers are managing their assets in flexible ways. The key to this is in devising pricing and funding structures that enable RSLs to manage their portfolios effectively to meet specific local housing demands.

shows there has been a noticeable change in the tenure pattern

across Scotland as a whole in recent decades. Owner occupation has increased from around 40% to just over 60% from the early 1980’s, with the social rental sector falling from just over 50% to around 25%. The trend in private sector rented accommodation has remained reasonably steady until around 2004, when it increased.

1 Homes Fit for the 21st Century: The Scottish Government's Strategy and Action Plan for Housing in the Next Decade: 2011-2020 http://www.scotland.gov.uk/Publications/2011/02/03132933/3

4

Figure 1 – Tenure change since the 1980’s

Glasgow and the Clyde Valley Housing Market Partnership (2011)2

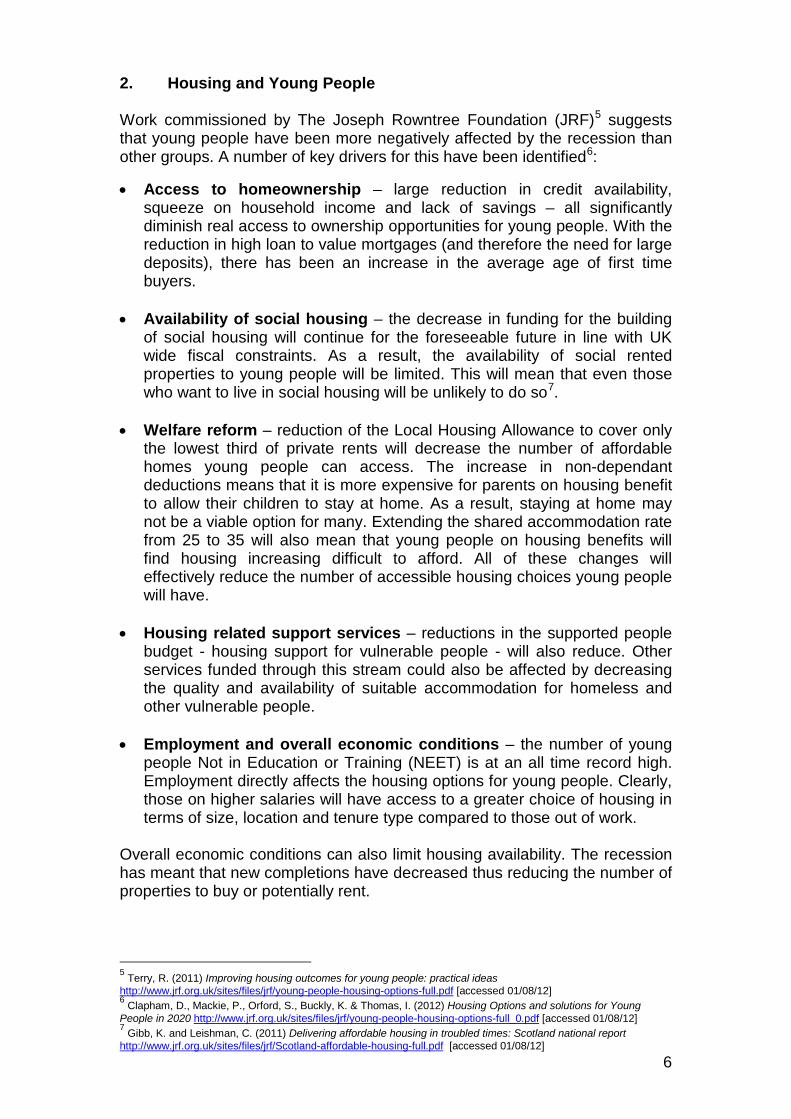

Figure 2

3

Figure 2 Tenure change (%) in the Glasgow and Clyde Valley Area (2001 – 2008)

demonstrates the change in tenure between 2001 and 2008 for the Glasgow and Clyde Valley (GCV) area. This encompasses eight local authority areas.

Between 2001 and 2008, apart from of East Renfrewshire and East Dunbartonshire, owner-occupied properties have increased at a relatively similar level for the GCV area. The social rented sector has also seen a relatively even decrease for all council areas. However the private rented sector has a very different pattern with significant increases in Glasgow, North Lanarkshire and South Lanarkshire and only small increases in the other areas.

The recent recession and the squeeze on public spending have made accessing housing more difficult. Affordable housing in particular is increasingly difficult to access and with banks now requiring high deposits, securing a mortgage is also more challenging.

2 Glasgow and the Clyde Valley Housing Market Partnership (2011) Housing Need and Demand Assessment: Final Glasgow: Glasgow and the Clyde Valley Strategic Development and Planning Authority p80 3 Glasgow and the Clyde Valley Housing Market Partnership (2011) Technical Appendix 02 Current Housing Supply / Stock Profile: Glasgow and the Clyde Valley Housing Market Partnership p8

5

If the British economy remains stagnant, just over one in four people – 27% – will be in "mortgaged homeownership" by 2025, compared with 43% in 1993-94 and 35% now4

4“Housing in Transition: Understanding the dynamics of tenure change” commissioned by Shelter and the Resolution Foundation and published by the Cambridge Centre for Housing and Planning Research, June 2012.

. The signals therefore are that there will be a strong demand for rental homes.

6

2. Housing and Young People

Work commissioned by The Joseph Rowntree Foundation (JRF)5 suggests that young people have been more negatively affected by the recession than other groups. A number of key drivers for this have been identified6

• Access to homeownership – large reduction in credit availability, squeeze on household income and lack of savings – all significantly diminish real access to ownership opportunities for young people. With the reduction in high loan to value mortgages (and therefore the need for large deposits), there has been an increase in the average age of first time buyers.

:

• Availability of social housing – the decrease in funding for the building

of social housing will continue for the foreseeable future in line with UK wide fiscal constraints. As a result, the availability of social rented properties to young people will be limited. This will mean that even those who want to live in social housing will be unlikely to do so7

.

• Welfare reform – reduction of the Local Housing Allowance to cover only the lowest third of private rents will decrease the number of affordable homes young people can access. The increase in non-dependant deductions means that it is more expensive for parents on housing benefit to allow their children to stay at home. As a result, staying at home may not be a viable option for many. Extending the shared accommodation rate from 25 to 35 will also mean that young people on housing benefits will find housing increasing difficult to afford. All of these changes will effectively reduce the number of accessible housing choices young people will have.

• Housing related support services – reductions in the supported people

budget - housing support for vulnerable people - will also reduce. Other services funded through this stream could also be affected by decreasing the quality and availability of suitable accommodation for homeless and other vulnerable people.

• Employment and overall economic conditions – the number of young

people Not in Education or Training (NEET) is at an all time record high. Employment directly affects the housing options for young people. Clearly, those on higher salaries will have access to a greater choice of housing in terms of size, location and tenure type compared to those out of work.

Overall economic conditions can also limit housing availability. The recession has meant that new completions have decreased thus reducing the number of properties to buy or potentially rent.

5 Terry, R. (2011) Improving housing outcomes for young people: practical ideas http://www.jrf.org.uk/sites/files/jrf/young-people-housing-options-full.pdf [accessed 01/08/12] 6 Clapham, D., Mackie, P., Orford, S., Buckly, K. & Thomas, I. (2012) Housing Options and solutions for Young People in 2020 http://www.jrf.org.uk/sites/files/jrf/young-people-housing-options-full_0.pdf [accessed 01/08/12] 7 Gibb, K. and Leishman, C. (2011) Delivering affordable housing in troubled times: Scotland national report http://www.jrf.org.uk/sites/files/jrf/Scotland-affordable-housing-full.pdf [accessed 01/08/12]

7

Whilst the private rented sector remains attractive for many young people given the flexibility of the tenure, research suggests that moving to the owner-occupied sector is still the long-term aim for most. There is, however, growing momentum for the idea that private renting represents a sensible and affordable long term housing tenure, due to the greater affordability offered in not requiring a large deposit8

8 From The Citylets Report, Issue 22, Quarter 2, 2012 - The Scottish Private Rented Sector

.

8

3. Housing and Families

It is not just young, single people who are locked out of the property market and forced into an under-regulated rental sector due to rising house prices, falling real wages and banks that are unwilling to lend. The same difficulties are now besetting families with children, many of whom are paying half or more of their income in rent and, as a result, have little or nothing left at the end of the month to save for a deposit.

Over the past five years, the JRF analysis also shows that the number of families with children having to rent private accommodation has soared by 86% – more than double the increase across all households (41%).

The increase in the proportion of families with children who are renting privately is expected to be most stark in London, rising from 25% now to 33% by 2025. Overall, the analysis predicts that more than a third (36%) of British households will be renting by 2025.

According to a report by Shelter9

9 Shelter (2012) Consultation response: A strategy for the private rented sector

, one in five 31 to 44 year olds who do not have children delay starting a family because of the lack of affordable housing.

JRF research predicts that 1.5 million people aged 18-30 will be pushed into private rent by 2020, unable to access either home ownership or a social tenancy. In some cases, this is likely to leave young families vulnerable to the whims of landlords in an insecure tenure.

http://scotland.shelter.org.uk/__data/assets/pdf_file/0010/577522/Shelter_Scotland_PRS_Strategy_Consultation_Response_July_2012_FINAL.pdf [accessed 27/08/12]

9

4. The Current Private Market Rental Sector Evidence from Shelter, among others, suggests that the quality of PRS housing in Scotland is varied:

• 31% of people who called Shelter Scotland’s helpline in 2011/12 to seek help in dealing with a housing problem were private renters, whereas they comprise only 11% of all households in Scotland.

• 16% of homeless applicants come from the PRS, as opposed to 12% of applicants from the social rented sector.

• 67% of private rented homes failed the Scottish Housing Quality Standard and 8% of private rented homes have a “poor” National Home Energy Rating compared to 3% of owner occupied and 1% of social rented properties. According to Shelter’s research, 21% of private renters who were surveyed in the Shelter research were looking for help in dealing with dampness or disrepair.

Housing issues noted included poor housing conditions, neighbourhood management problems, some unsatisfactory private landlords and issues relating to new migrants. The Scottish Government introduced the Private Rented Sector (Scotland) Act 2011 to:

• Sharpen up existing local authority powers in respect of registration, for both landlords and Houses in Multiple Occupation

• Implement new regulations on overcrowding • Introduce pre-tenancy information packs • Introduce a Tenancy Deposit Scheme protecting tenants’ deposits

by placing them with an independent third party. In July 2012, the Government-sponsored PRS Strategy Group set out proposals10

A key challenge in improving standards is the fragmented nature of the PRS. According to the Scottish Government, PRS landlords tend to own a small number of properties. Recent evidence found that just over 4 in 5 (84%) PRS dwellings were owned by 'individuals, a couple or a family', while 14% were 'owned by a company, partnership or property trust', and 2% were owned by an institution.

, for a more strategic approach for managing the private rented sector in Scotland. These proposals aim to driving up the somewhat poor standards currently in PRS sector.

10 The Scottish Government, Consultation on a Strategy for the Private Rented Sector, April 2012ategy for the http://www.scotland.gov.uk/Publications/2012/04/5779/3

10

5. Customer Experience and the Need for Change

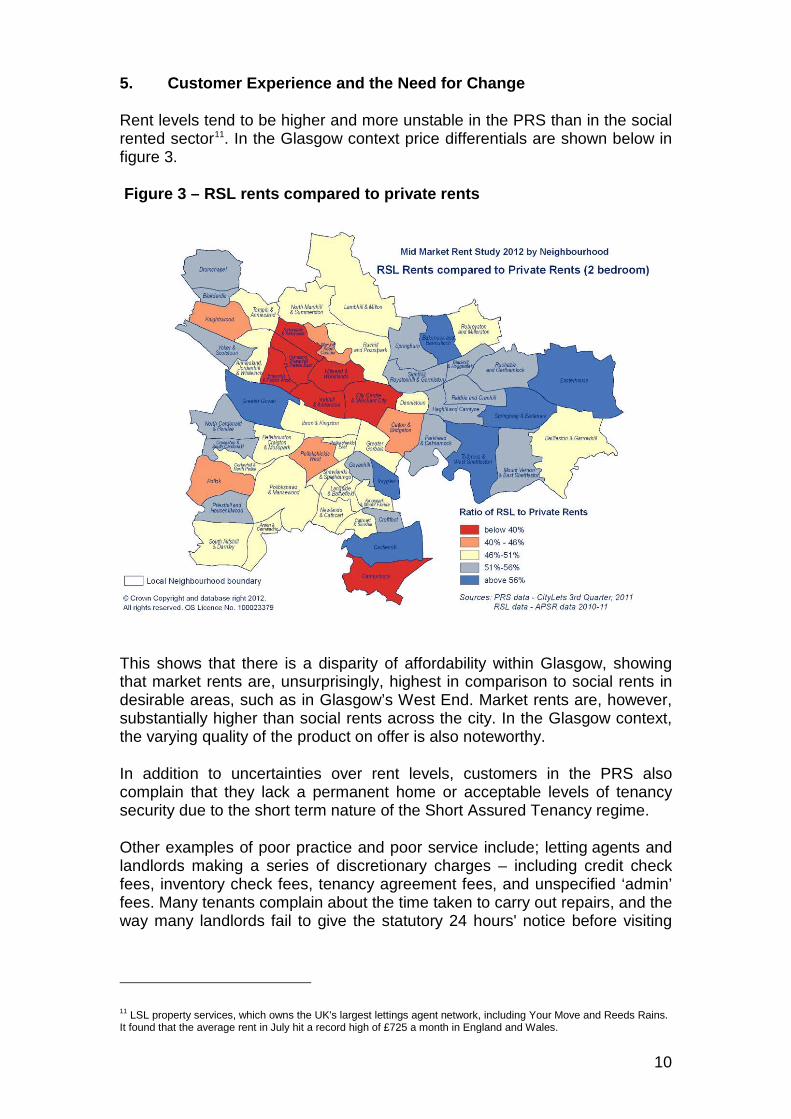

Rent levels tend to be higher and more unstable in the PRS than in the social rented sector11. In the Glasgow context price differentials are shown below in figure 3.

Figure 3 – RSL rents compared to private rents

This shows that there is a disparity of affordability within Glasgow, showing that market rents are, unsurprisingly, highest in comparison to social rents in desirable areas, such as in Glasgow’s West End. Market rents are, however, substantially higher than social rents across the city. In the Glasgow context, the varying quality of the product on offer is also noteworthy.

In addition to uncertainties over rent levels, customers in the PRS also complain that they lack a permanent home or acceptable levels of tenancy security due to the short term nature of the Short Assured Tenancy regime.

Other examples of poor practice and poor service include; letting agents and landlords making a series of discretionary charges – including credit check fees, inventory check fees, tenancy agreement fees, and unspecified ‘admin’ fees. Many tenants complain about the time taken to carry out repairs, and the way many landlords fail to give the statutory 24 hours' notice before visiting

11 LSL property services, which owns the UK's largest lettings agent network, including Your Move and Reeds Rains. It found that the average rent in July hit a record high of £725 a month in England and Wales.

11

the property. Many tenants also report problems recovering their deposit in full when they move on.12

• Market expansion to cope with growing pressure on the PRS and social rented housing

The customer experience, combined with changing housing market context, increased demand and government policy direction show that the PRS requires change. Examples of the changes required, which social landlords could respond to, are:

• Greater choice and value for money – much better service levels are needed

• Security and accountability in a regulated market • Fit for purpose, quality, sustainable and suitable options -

addressing the issues of affordability, stability and quality that so many renters face

• Affordable and stable rents - rents demanded by landlords are hitting record levels

12 http://www.guardian.co.uk/money/2010/mar/13/letting-agents-hidden-charges

12

6. Registered Social Landlords: Landlord of Choice for ‘Generation Rent’?

Social housing is facing fundamental questions about its present and its future role. Public funding cuts and a reform of the welfare state could see housing benefit, its primary source of regular income, greatly reduced and restricted. This is in addition to major reductions in supply subsidy.

The ‘New Times, New Businesses’ project, an international housing research and knowledge exchange project, led by the Centre for Housing Research at the University of St Andrews, involving non-market housing providers from five countries. New Times, New Businesses asks fundamental questions about social housing and its future. The project, which is nearing completion, contends that social housing providers have to ask themselves what the purpose of the sector is in new times and who it is for, and from there to redefine their role.

The new regulatory environment in Scotland also helps provide a more flexible environment for RSLs who wish to develop into new business areas. The new approach increases focus on risk assessment and management, ensures broader group control of subsidiaries, and looks to RSL Boards to set strong strategic direction for their new businesses.

The housing issues we face across the sectors are not just about how we house the poor. Demographic and economic circumstances mean that when we look at affordability, we must look beyond the poorest in society.

RSLs should, however, be well placed to consider the broader needs of their communities across tenures. This may, in due course, lead them to question the fundamental concepts of the spectrum of tenures and ask whether we need to have some new tenure descriptions which can respond to issues of community sustainability. The contention in this paper is that rather than focus on assets, RSLs are good at focusing on people and local communities first, and that strength should inform their strategic approach to market rental.

Access to affordable housing is in a state of crisis in Scotland. In the case of GHA, more than 25,000 households are on waiting lists. Realistically, many of these applicants have little chance of attaining a social tenancy. While 10,000 households apply under the homelessness legislation each year, there are only around 9,000 social lets in Glasgow from all RSLs each year.

Relatively few RSLs appear to have thought proactively about their potential role in stabilising and improving a share of the current private rented sector as part of a comprehensive ‘housing options’ approach, where applicants can be assisted to attain a suitable home in a tenure that they can realistically attain and sustain.

RSLs, depending on their specific circumstances, may be well placed to purchase and develop new homes specifically for market rent, with the flexibility to use them for other tenures. This can be a financially sensible response to a potential housing crisis, while helping to build future financial capacity within the sector, while taking some pressure off social housing waiting lists now.

13

Mid Market Rental (MMR) is an option already used and explored by a small number of RSLs, but is gaining scale within some organisations. A recent study carried out on behalf of Glasgow City Council and GHA13

• The market for MMR could be substantial ranging from around 24,000 households aged under 45 years currently unable to afford Local Housing Allowance level private rents, to 28,500 unable to afford average private rents.

identified a substantial market for MMR housing within the city. The report has a number of key findings including:

• The estimates based on not being able to afford to own their own property are higher, at around 36,000-37,000.

• The overall estimate of the market is likely to be around 10% of the current Glasgow household population.

• Lack of savings contributes negatively and significantly to access to mortgage finance. The estimated ‘market’ for mortgage-guarantee or savings-orientated solutions is 16,500 based on lowest quartile.

• Almost half of those in the market for MMR, based on current residents, are in the 15% most deprived data zones. This clearly suggests a strong regeneration role for MMR and fits with idea that the key role for RSLs is about communities rather than simply assets and specific tenures.

• The likely income threshold for MMR to be affordable is between £15,000 (above the Housing Benefit threshold) and £30,000, although this may vary for larger households and by local markets.

Findings from focus groups of Glasgow tenants and residents also suggest that RSLs would be the preferred management agent for MMR, bringing the advantage of regulation and public accountability.

By diversifying into the provision of a wider range of rented accommodation, RSLs could meet the needs of some young people and low and middle income families. RSLs have years of experience in delivering good quality housing at an affordable price. These skills could be used to make RSLs prominent players in this market, and use their skills to drive up the quality of rented accommodation in all tenures.

There is however no doubt that new skills are also needed; better marketing skills, sales skills, customer service skills and commercial and financial planning skills, are all required to develop sustainable businesses in a wider rental market.

As anchors in their communities, housing associations can be the landlord of choice for the groups discussed above who are unlikely to attain either a social tenancy or gain access to homeownership.

13 Evans, A. (2012) Research into the Potential Market for Mid-Market Rent In Glasgow p.52 http://www.glasgow.gov.uk/NR/rdonlyres/F727EAE4-F486-4DEF-8A55-E059023F1EBE/0/POTENTIALMMRMARKETGLASGOWRESEARCHSTUDYFINALREPORTAP RIL2012.pdf [accessed 27/08/12]

14

7. Commercial Lending and the RSL Sector So if there is opportunity of demand, can the financial capacity of RSLs deliver the necessary supply? The financial certainties which tended to drive the behaviour of RSLs can no longer be taken for granted in the current economic climate. Shifts in commercial lending patterns in the past 2/3 years mean that RSLs can no longer rely on the financial assumptions of the last few decades. Changing banks rules in relation to capital weighting requirements have meant that long term (i.e. 30 years) financial terms are rare with a strong preference to lend on 5 to 7 year terms. The pricing of loans has also increased from 20 basis points to between 200 and 250 basis points. The traditionally relaxed approach by commercial banks in lending to RSLs has therefore changed and loan and covenant compliance have become even more central to treasury management.

One result has been the emergence of the bond market as a mechanism for RSLs to raise long term finance. The changing external environment for fund managers in terms of their appetite to risk and return has made the RSL sector an attractive investment opportunity. This is because the bond market likes the simplicity of structure and the comfort associated with the regulated nature of the sector. The pricing of bonds reflects the markets’ view of the risk associated with particular structures and organisations. RSL funders’ appetite for lending to the sector has reflected its perception as a traditionally low risk and high regulated environment. However, in general RSL asset strength is good and government backing is implicit, at least for the time being. All of these have meant that pricing and terms compare favourably with more commercial lending. There is an emerging role for pension and insurance funds to directly fund the sector and similar to bond investors their investment is long term in nature and based on a relatively low risk profile. Other commercial structures are being developed for perceived higher risk full market rental properties that may be listed. However t,he consequence is that investors are looking for significantly higher levels of return. The risk and reward equation has become more central to the view of all funders in their approach to lending. Indeed the variation within commercial lenders of appetites for lending for activity outside of perceived ‘traditional’ RSL activities has become more apparent. This is a response to the overall credit position of the individual bank and their exposure to the sector as a whole. The consequence is that RSLs must be more flexible in how they use private finance, playing to the credit appetite of the various funding structures. Scale becomes important too both in relation to the ability of organisations to be able to participate in the variety of structures that are available, but also in their ability to absorb risk across the portfolio of properties they may have.

15

The Scottish Housing Regulator, as mentioned above, now emphasises the need for Boards to be fully aware of, and in control of, the risk and reward equation when they set their strategic direction and manage its implementation. So while it is early days for RSLs in Scotland, and will require new and different commercial and financial planning skills, there are opportunities in relation to the financial markets to broaden the asset base for meeting future housing need and demand.

16

8. Key Challenges for Social Housing Providers and Conclusions This paper contends that there is a clear case for a role for RSLs in the provision of market rental housing. It is, however, dependent on housing organisations being dynamic, high quality service providers, which are adaptable and open to innovation. The role is of course also very dependent on the financial capacity they can maximise from their asset base, and the skills to manage that base. This has important implications for the ways that RSLs perceive, organise and govern themselves and for how the government relates to the sector. RSLs also must also have appropriate appetite for risk, and have management and governance structures that facilitate this within regulatory guidance. Specifically, RSLs might consider actions such as:

• Assets - the RSL sector should ask itself about the housing assets needed in communities and how RSLs can use these assets over time, responding to the demand profile on a more flexible and fluid basis than the large scale housing needs studies commonly used by strategic housing authorities.

• Careful marketing of mixed tenure regeneration sites – housing associations need to strengthen marketing approaches. A more strategic approach to marketing in the next few years may also include ensuring that stakeholders, including elected representatives, understand why RSLs should engage in market rental activity within local communities.

• Planning – ensure rental market developed in areas where it is

most needed - working closely with the strategic housing authorities, and local councils to help provide a product that is currently not or scarcely available in those areas in terms of price and quality.

• Targeted approach – customer profiling: This could include

identifying a percentage of households with incomes that are above the housing benefit eligibility rate and so could afford MMR without housing benefit but below the rate where they could comfortably afford full market prices).

In conclusion, RSLs, as “community anchors” have an important role to play in market rental housing. Social landlords, not only because of assets, but because of their intelligence on what communities are and what they demand and require, are fundamentally placed to use their assets to have a role in all housing tenures, if they have the desire and asset base to do so and if the banks and bond markets are receptive to their plans. If expertise in disciplines such as asset management, customer service and building neighbourhoods is also considered, social landlords are very well placed to help drive up standards in the current private rented sector and

17

meet housing need through offering a wider range of tenures for a wider range of people. There is real opportunity for RSLs to extend their activity into market rental, becoming “more enterprising but no less social” in their purpose.

18

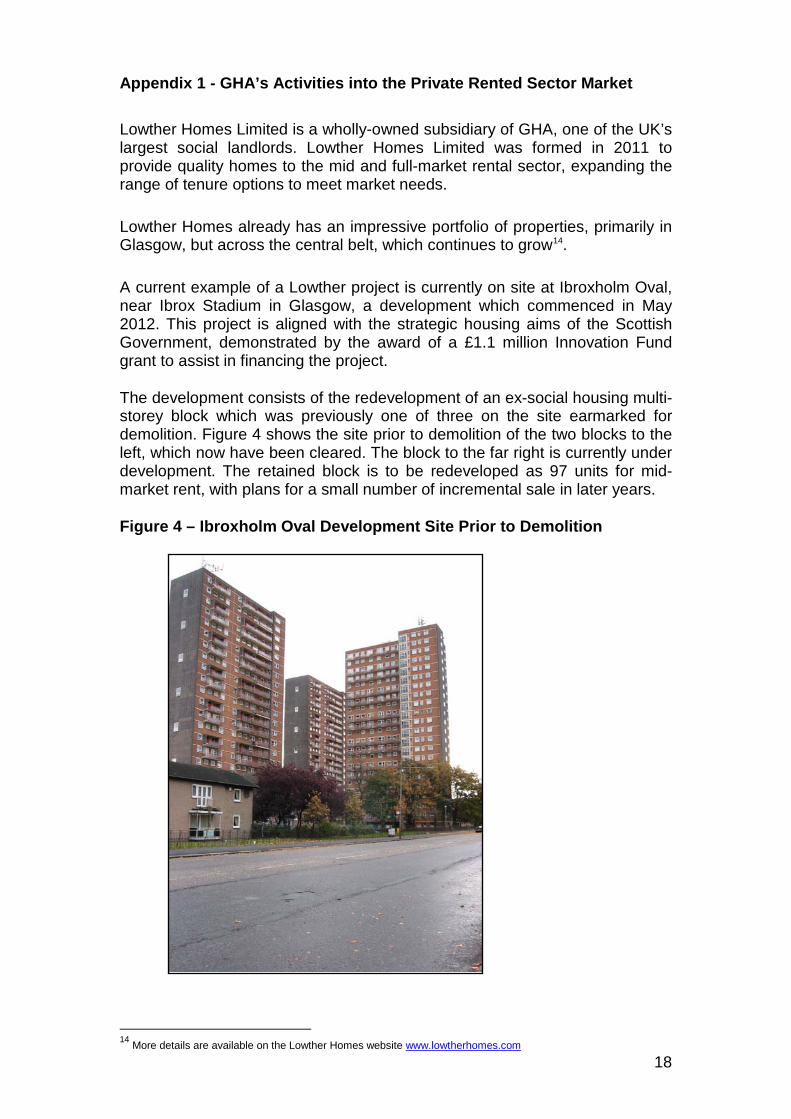

Appendix 1 - GHA’s Activities into the Private Rented Sector Market Lowther Homes Limited is a wholly-owned subsidiary of GHA, one of the UK’s largest social landlords. Lowther Homes Limited was formed in 2011 to provide quality homes to the mid and full-market rental sector, expanding the range of tenure options to meet market needs. Lowther Homes already has an impressive portfolio of properties, primarily in Glasgow, but across the central belt, which continues to grow14

. A current example of a Lowther project is currently on site at Ibroxholm Oval, near Ibrox Stadium in Glasgow, a development which commenced in May 2012. This project is aligned with the strategic housing aims of the Scottish Government, demonstrated by the award of a £1.1 million Innovation Fund grant to assist in financing the project.

The development consists of the redevelopment of an ex-social housing multi-storey block which was previously one of three on the site earmarked for demolition. Figure 4 shows the site prior to demolition of the two blocks to the left, which now have been cleared. The block to the far right is currently under development. The retained block is to be redeveloped as 97 units for mid-market rent, with plans for a small number of incremental sale in later years.

Figure 4 – Ibroxholm Oval Development Site Prior to Demolition

14 More details are available on the Lowther Homes website www.lowtherhomes.com

19

The project is aimed at the mid market rental market. The development is aimed at people, including key workers e.g. at the nearby new South Glasgow Hospitals campus, seeking a quality housing product which, due to current market conditions, they are unlikely to achieve through purchase and who are unlikely to attain a social tenancy.

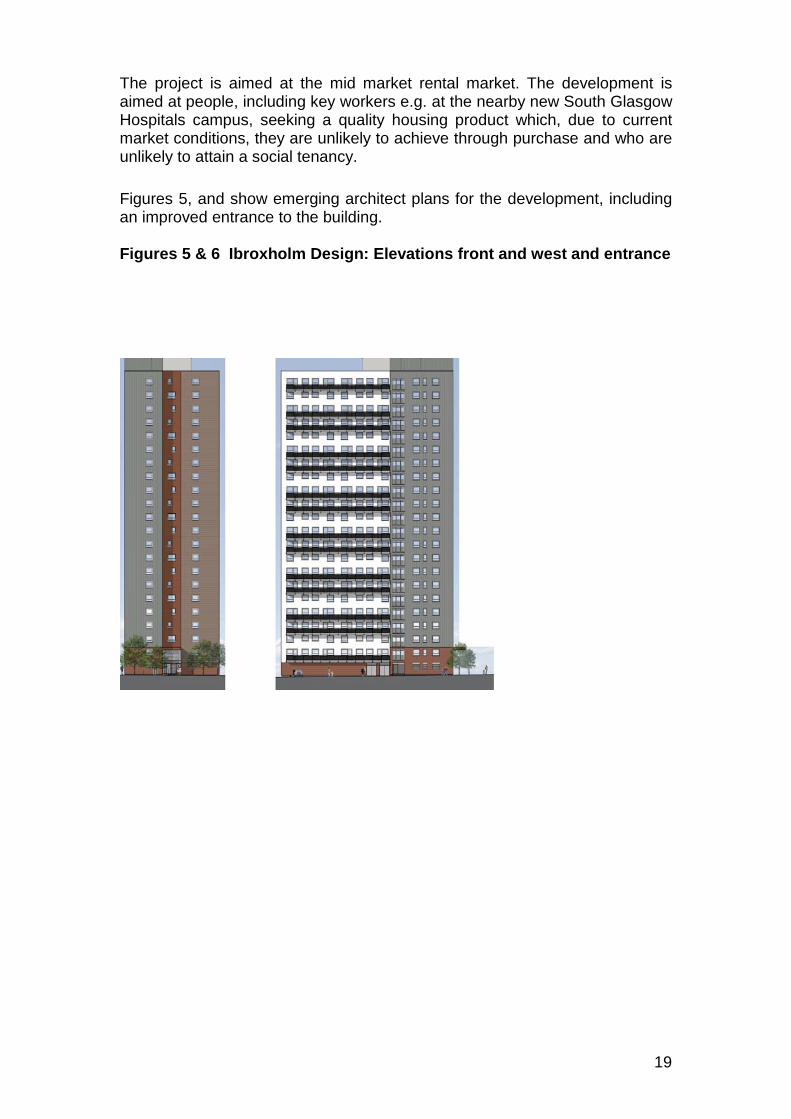

Figures 5, and show emerging architect plans for the development, including an improved entrance to the building.

Figures 5 & 6 Ibroxholm Design: Elevations front and west and entrance

20

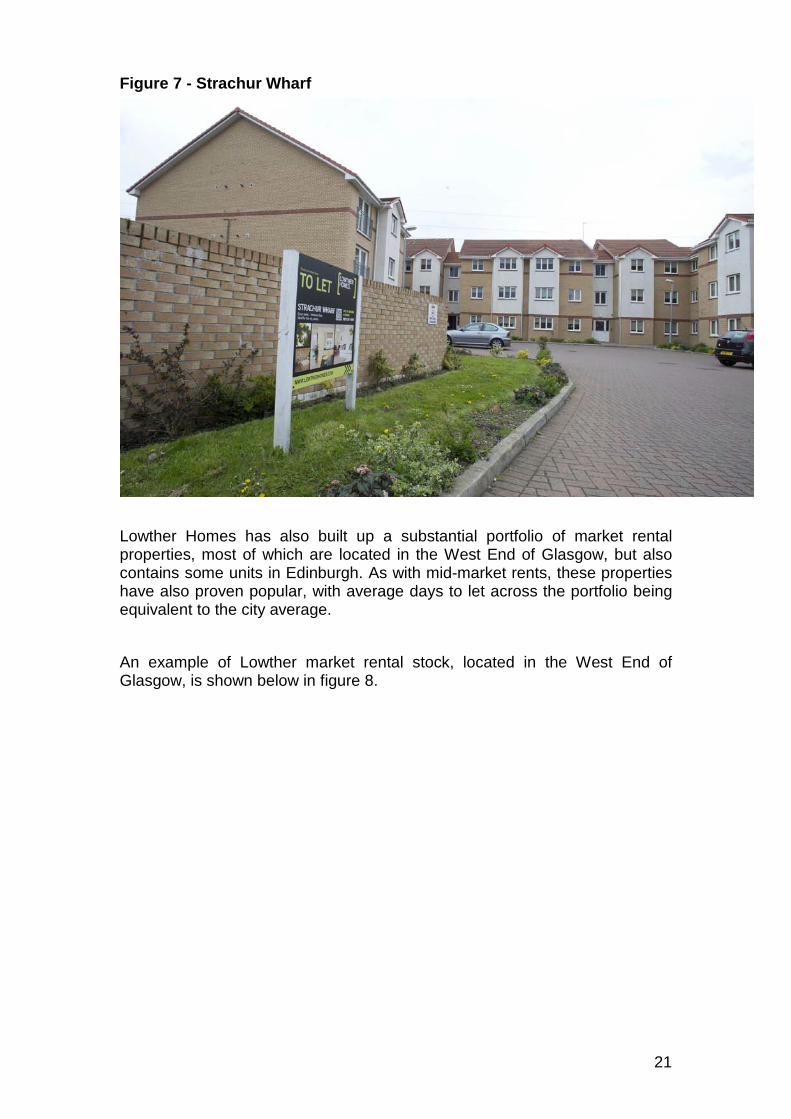

Another example of a mid-market rental development is at Strachur Wharf in Lambhill in the north west of Glasgow. The development was also supported by funding from the Scottish Government’s Innovation and Investment Fund of £360,000. These properties proved very popular and the twenty-four units let very quickly, taking an average of 20 days to let. This compares very favourably to 27 days taken to rent PRS properties in the Jordanhill and Broomhill areas of the city, which have the shortest time to let in Glasgow.15

15 From The Citylets Report, Issue 22, Quarter 2, 2012 - The Scottish Private Rented Sector

This popularity is testament to the quality and affordability of the product. The development is illustrated in figure 7 below.

21

Figure 7 - Strachur Wharf

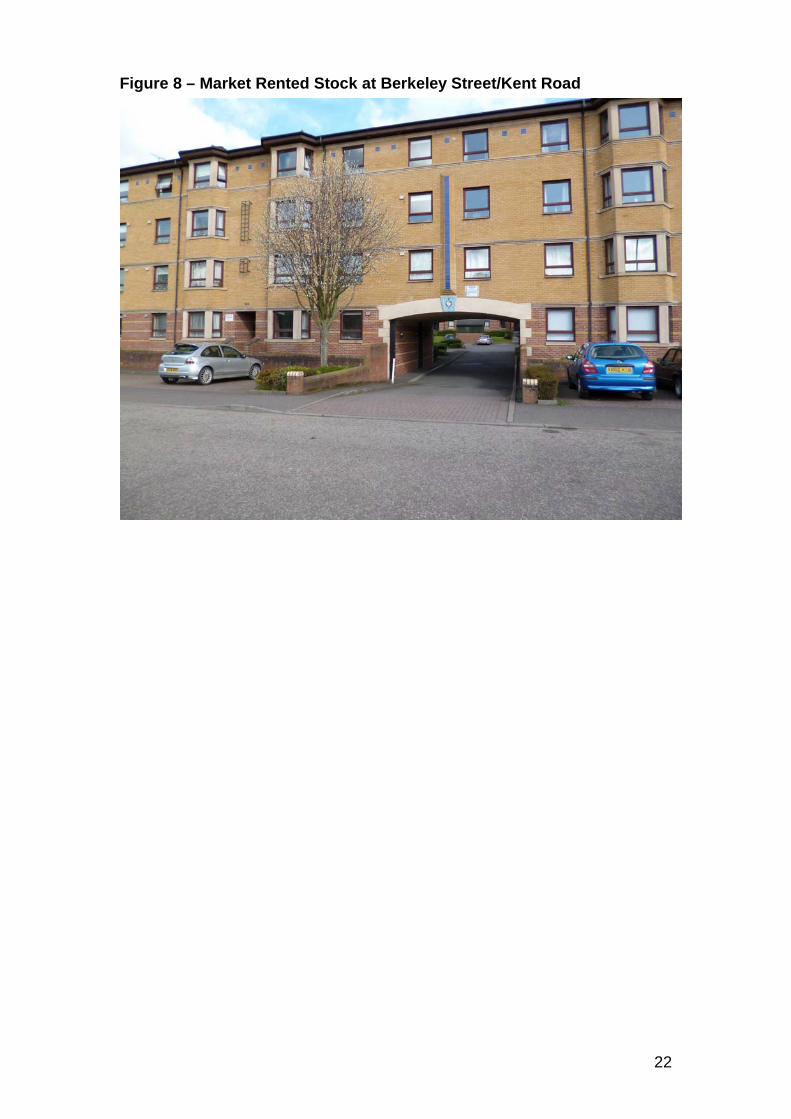

Lowther Homes has also built up a substantial portfolio of market rental properties, most of which are located in the West End of Glasgow, but also contains some units in Edinburgh. As with mid-market rents, these properties have also proven popular, with average days to let across the portfolio being equivalent to the city average.

An example of Lowther market rental stock, located in the West End of Glasgow, is shown below in figure 8.

22

Figure 8 – Market Rented Stock at Berkeley Street/Kent Road