Embed Size (px)

Citation preview

A Review of Charitable Spending

By UK Charities

December 2015

Contents

Executive Summary 1

Introduction 3

The Research 3

The Findings 4

To be or not to be a charity, that is the question - Case Studies 7

Lloyd’s Register Foundation 7

SheffieldCityTrust 8

Royal National Lifeboat Institution 9

Marie Curie 10

Cancer Research UK 11

Age UK 13

Sue Ryder 14

British Heart Foundation 15

The Charity Commission Websites 15

Conclusions 16

EXECUTIVE SUMMARY

The True and Fair Foundation, founded by the philanthropist and transparency campaigner, Gina Miller, is a strong advocate of accountability, transparency and smarter giving. The aim of this research projectwastoestablishhoweasyordifficultitisfordonorstoassessthepercentageofacharity’sincome that is spent on their end charitable activities.

The research analysed 5,543 charities with over £0.5m in their latest reported accounts, and a total combined income of £40.7bn, and calculated their latest reported spending on charitable activities (according to the Charity Commission’s own websites) as a percentage of their income. During the research the team discovered numerous instances where data on the Charity Commission’s websites were either not up to date or incorrectly listed, or both. The True and Fair Foundation thereforealsouseddatafromthecharity’sownReportandAccountsfiledatCompaniesHouse.

Findings• A staggering 292 charities, with a combined income of £2.4bn in their latest reported accounts on the

Charity Commission’s website, spent 10% or less on their charitable activities• 1,020 charities, with a combined income of £6bn in their latest reported accounts on the Charity

Commission’s website, spent 50% or less on their charitable activities.

Wealsoconductedspecificresearchintocharitieswith£50m+ofincomeintheirlatestreportedaccounts. This analysis found 17 charities with a combined income of £3.5bn, who spent 65% or less on theircharitableactivitiesoverthelastthreefinancialyears:

Charity Name

Lloyd’s Register Foundation

The Racing Foundation

The Motability Tenth Anniversary Trust

Consumers’ Association

SheffieldCityTrust

The Grace Trust

British Heart Foundation

Sue Ryder

Age UK

Oasis Charitable Trust

The Royal Horticultural Society

Dogs Trust

Cancer Research UK

The Guide Dogs For The Blind Association

Shelter, National Campaign For Homeless People Limited

The Royal National Lifeboat Institution

Marie Curie

Average Spending on Charitable Activities As % Income Over Last Three Financial Years

1%

3%

8%

24%

25%

33%

46%

46%

48%

57%

60%

63%

64%

64%

64%

64%

65%

1Source:TrueandFairFoundationbasedondatafromtheCharityCommissionandCompaniesHouse,asat23.11.15

On average, amongst these 17 charities, there was a startlingly low 43% of each £1 spent on charitable activities over the last three financial years.

Other findings include:

• A notable number of data errors on both the Charity Commission’s websites when compared to the charities’ own Report and Accounts

•Noevidenceofeconomiesofscaleleadingtoanyefficienciesthatbenefitedthedonorsoflargercharities

•Theformatofmanyofthecharities’ReportandAccountswerefoundtobeextremelydifficulttounderstand, even by the research team who possess accounting and investment research and analysis expertise.

The True and Fair Foundation findings pose serious questions for the charity sector:

1. Should there be an urgent review of the rules that allow organisations to be granted charitable status?Especiallyasthisstatusmeanscharitiesoftenpaylesstaxintothepublicpurse,benefitfromtax reliefs such as rent and rates, and often receive gift aid, which is essentially the public’s money.

2. Is it now time for a voluntary or mandatory minimum annual dispersal rate set for charities? It is the view of the True and Fair Foundation that a minimum annual dispersal rate of 65% should be debated.

3. Is there a need for a simpler accounting methodology to enable greater understanding by donors aboutcharities’finances?

4.Doesthesectorrequiremorefinancialoversightandaccountability?

5. Why are donors - private, corporate and government - not asking more questions about the charitable work being delivered by charities?

6. Is it time to impose a ‘Give & Good label’ across the charity sector which would clearly allow donors to see how much of annual income is being spent on the end charitable activities?

7. Should there be a periodic three year review of organisations’ charitable status?

8.Shouldtherebelimitsonseniorexecutiveremuneration,includingpensionprovision?

It is the view of the True and Fair Foundation that as the State continues to shrink, the charity sector will become even more important to society. But this does not excuse many of the excesses and inefficienciesthatappearprevalentwithinthissector.

Some commentators express concern that the charity sector faces being over-regulated and becoming another arm of the state. The True and Fair Foundation totally disagrees with this view, as the charity sector, with an estimated income £64bn (in England and Wales), £13bn of which comes from government and is public money, should be open to scrutiny and accountability.

2

INTRODUCTION

Organisations within the charity sector have been increasingly the focus of public scrutiny. Scandals withinhighprofilecharitableinstitutionsexplodingacrossthemediahaveresultedinpublicoutrageand political knee jerk reactions to the apparent or implied misuse of public and private donor funds.

The True and Fair Foundation believes that the bad apples within the charitable sector are often characterised by a lack of proper governance and ethical conduct, transparency and accountability as well as low conversion of income into charitable expenditure.

Whilst many dynamic charities undertake invaluable work with the most disadvantaged in society, they need to be accountable to their donors and funders, as well as to those they serve.

Recent well publicised examples have made it easy to criticise the sector, but there are serious questions that need to confronted and debated. The sector needs to embrace change and scrutiny to restore the public’s waning trust.

Corporategovernanceiscriticalandplaysapivitolroleinfinancialinvestmentsandperformance,butthisalsoappliestothemoneytheBritishpublicgenerouslygivestocharitiestheybelievecanfilltheincreasing social care and social justice gaps.

Few people outside the charity sector understand how charities are structured. In addition, given the substantial amounts of public and government money handed over to organisations with charitable status, it is our view that high levels of transparency and accountability should be mandatory rather than optional.

THE RESEARCH

New research from the True and Fair Foundation analysed 5,543 charities with a total income of £40.7bn in their latest reported accounts with the simple aim of identifying the proportion of their income spent on their end charitable works.

During the analysis, the team uncovered a number of disturbing issues, such as the reliability of data on the Charity Commission’s websites, why certain organisations have charitable status, how low a proportion of income is spent on charitable activities and how so many charities’ Report and Accounts are incomprehensible, confusing and misleading for donors.

All the data used in this report is publicly available either via the Charity Commission or Companies House. The key data points of ‘income’ and ‘charitable activities’ are the same data points used by the Charity Commission.

To aid donors, the Charity Commission launched a new charity search tool on the 20th March 2015, which highlights the proportion of charities’ ‘total incoming resource’ as recorded in their Statement of Financial Activities (SOFA) that was spent on ‘charitable activities’.

3

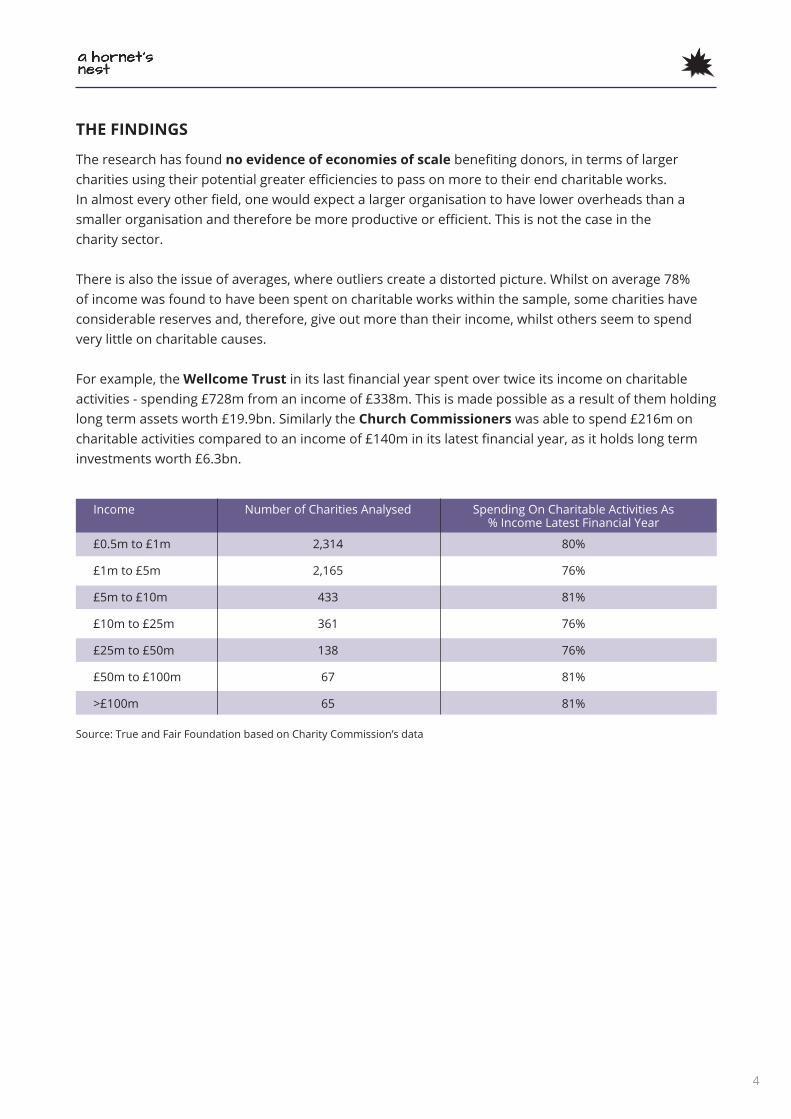

THE FINDINGS

The research has found no evidence of economies of scalebenefitingdonors,intermsoflargercharitiesusingtheirpotentialgreaterefficienciestopassonmoretotheirendcharitableworks. Inalmosteveryotherfield,onewouldexpectalargerorganisationtohaveloweroverheadsthanasmallerorganisationandthereforebemoreproductiveorefficient.Thisisnotthecaseinthecharity sector.

Thereisalsotheissueofaverages,whereoutlierscreateadistortedpicture.Whilstonaverage78%of income was found to have been spent on charitable works within the sample, some charities have considerable reserves and, therefore, give out more than their income, whilst others seem to spend very little on charitable causes.

For example, the Wellcome Trustinitslastfinancialyearspentovertwiceitsincomeoncharitableactivities-spending£728mfromanincomeof£338m.Thisismadepossibleasaresultofthemholdinglong term assets worth £19.9bn. Similarly the Church Commissioners was able to spend £216m on charitableactivitiescomparedtoanincomeof£140minitslatestfinancialyear,asitholdslongterminvestments worth £6.3bn.

Income

£0.5m to £1m

£1m to £5m

£5m to £10m

£10m to £25m

£25m to £50m

£50m to £100m

>£100m

Number of Charities Analysed

2,314

2,165

433

361

138

67

65

Spending On Charitable Activities As % Income Latest Financial Year

80%

76%

81%

76%

76%

81%

81%

Source:TrueandFairFoundationbasedonCharityCommission’sdata

4

Large Charities Spending Less Than 65% Of Income On Charitable Activities

Thefirststepoftheresearchwastoanalysecharitieswithover£50mofannualincome,whichspentless than 70% on charitable activities, according to the Charity Commission’s website. We then looked at the resulting sample’s latest Companies House accounts, as during our research we discovered that in many cases the Charity Commission’s data was over a year old or erroneously listed, or both. We then averaged the proportion of their overall income spent on charitable activities over their last threefinancialyearsinordertosmoothoutyeartoyearfluctuationsinincomeorcharitablespending.

The following 17 charities were all found to have spent an average of 65% or less of their overall income on charitable activities over their last three financial years. The total income of these 17 charities was £3.5bn in their last financial year.

5

Source:TrueandFairFoundationbasedondatafromtheCharityCommissionandCompaniesHouse,asat23.11.15SomedatapointshavebeenchangedtoreflecttheactualnumbersrevealedinCompaniesHousefiledaccountswherethesehavedifferedfromtheCharityCommission’sdataoraremorerecentthantheCharityCommission’sdata.

On average a startlingly low 43% of each £1 of income was spent on charitable activity.

Charity Name

Lloyd’s Register Foundation

The Racing Foundation

The Motability Tenth Anniversary Trust

Consumers’ Association

SheffieldCityTrust

The Grace Trust

British Heart Foundation

Sue Ryder

Age UK

Oasis Charitable Trust

The Royal Horticultural Society

Dogs Trust

Cancer Research UK

The Guide Dogs For The Blind Association

Shelter, National Campaign For Homeless

People Limited

The Royal National Lifeboat Institution

Marie Curie

Spending on Charitable Activities As % Income

Last Three Financial Years

1%

3%

8%

24%

25%

33%

46%

46%

48%

57%

60%

63%

64%

64%

64%

64%

65%

Average 43%

Last Financial Year Income

£1,062,537,000

£50,932,901

£54,376,000

£102,831,000

£48,186,000

£91,678,745

£288,200,000

£95,431,000

£174,575,000

£271,709,000

£73,157,000

£84,743,000

£634,900,000

£101,100,000

£69,565,000

£190,100,000

£154,805,000

£3,548,826,646

Last Financial Year Spending On Charitable

Activities

£14,490,000

£1,146,153

£4,093,000

£22,796,000

£17,021,000

£29,874,716

£113,700,000

£42,585,000

£83,956,000

£151,935,000

£47,641,000

£57,185,000

£422,700,000

£56,400,000

£39,541,000

£122,200,000

£105,585,000

£1,332,848,869

Charities Spending Less Than 50% Of Income On Charitable Activities

The research analysis found 1,020 charities, with a combined income of £6bn in their latest reported accounts, all of whom received an income of £0.5m or more, that spent 50% or less of their income on charitable activities.

Charities Spending Less Than 10% Of Income On Charitable Activities

The team were staggered to find 292 charities, with a combined income of £2.4bn in their latest reported accounts, that spent 10% or less on their charitable activities.

The True and Fair Foundation suggests this situation has occurred as there are no legally binding rules on charities annual dispersal rates or overhead costs, Chief Executives’ salaries or bonuses.

The research also found that the quality and transparency of reporting within charity report and accounts is poor. The resulting standard makes it almost impossible for any donor to work out how efficientaparticularcharityis,oreasilygaugewheretheir£1isbeingspent.

The fact that any charity is allowed to spend less than 50%, let alone less than 10%, on their charitable activities is a scandal. When you also consider that the public purse may receive less taxes from these organisations as a result of various charitable allowances, it is a travesty that they are not required to spendasignificantpercentageoftheirincomeontheircharitableendeavourstokeepthesevarioustaxadvantages.

6

To be or not to be a charity, that is the question

Lloyd’s Register Foundation

Another pressing issue for the charitable sector and the Commission is to review which organisations are allowed to hold charitable status.

The trading company Lloyd’s Register Group Limited is part of the registered charity, the Lloyd’s Register Foundation.Lloyd’sRegisterprovidesqualityassuranceandcertificationforships,offshorestructures and shore-based installations, such as power stations and railway infrastructure. Whilst the charity sets out to ‘support the advancement of public education particularly focused on engineering and science, and which will fund research and development into issues which promotes safety of life at sea, on land and in the air’ from ‘total incoming resources of £1,062.5 million’, the amount spent on charitable activitieswas£14.5m,just1.3%ofthisamountinitslatestfinancialyear.

It could be said this analysis is unfair as most of the income relates to commercial trading activities – but that is the point. Why should this organisation have charitable status and any taxable advantages pertaining from this status? Interestingly, even though the charity accounting standards (SORP) recommends salaries to be disclosed by charities, our research discovered that the Lloyd’s Register escapesanypaytransparency:‘Due to the high number of qualified and skilled staff the SORP’s requirement to disclose the number of all Group employees who received emoluments over £60,000 is commercially sensitive to the operations of that Group and is not made here with the agreement of the Foundation’s trustees.’

Their latest accounts, also shows that no UK corporation tax was paid as ‘the foundation is a UK registered charity, and is exempt from Corporation Tax to the extent that surpluses are applied to its charitable purposes.’

7

Sheffield City Trust

SheffieldCityTrustappearstobelargelyresponsibleforoperatingvariousleisurecentresaroundSheffieldincludingtheMotorpointArena(previouslySheffieldArena).

Their charitable status begs the question, if they are being given local and central government money to provide services for the community, why do they appear to have spent as little as 25%, on average, on their charitable works over the last three years?

8

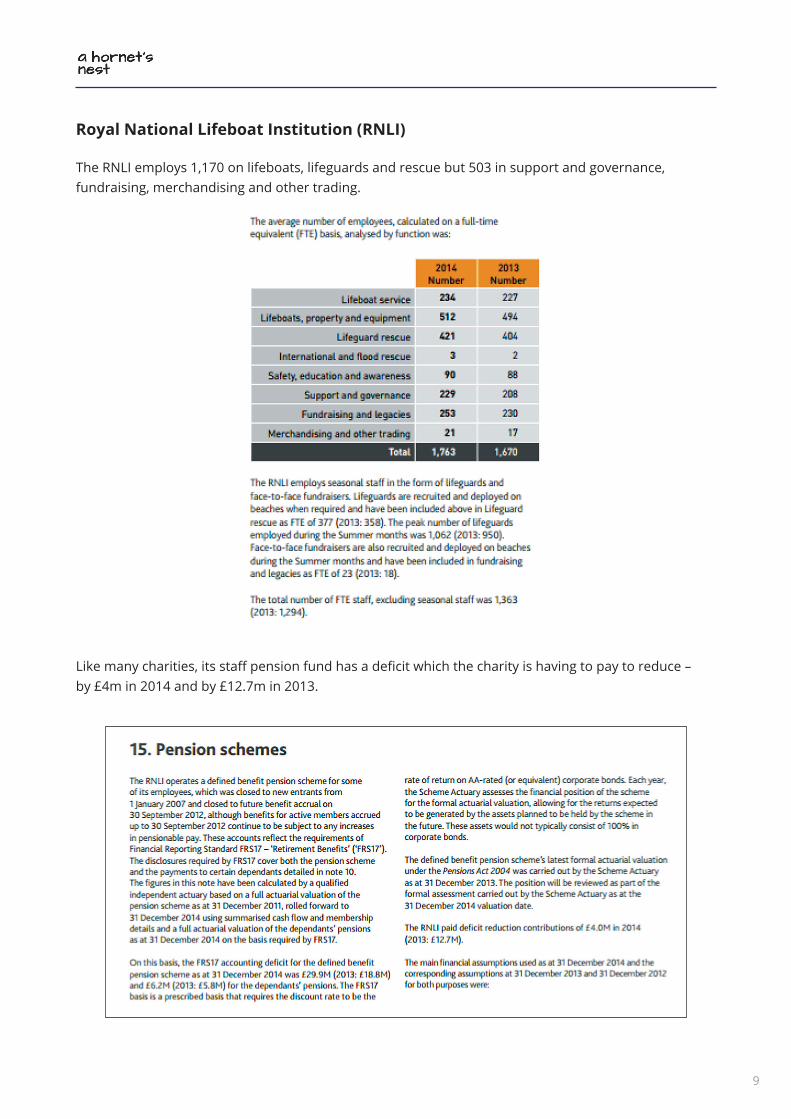

Royal National Lifeboat Institution (RNLI)

The RNLI employs 1,170 on lifeboats, lifeguards and rescue but 503 in support and governance, fundraising, merchandising and other trading.

Likemanycharities,itsstaffpensionfundhasadeficitwhichthecharityishavingtopaytoreduce–by £4m in 2014 and by £12.7m in 2013.

9

Marie Curie

Marie Curie employs 3,164 in hospices and nursing, compared to 1,179 in fundraising, publicity, shops and support. The number in fundraising alone is 441.

10

During our analysis of some of the UK’s largest charities we were surprised by the numbers employed withinfundraising,aswellassomeofthesalarylevels.Forexample:

Cancer Research UK

We also found that within Cancer Research UK they have more than 2,000 employees directly employed in fundraising.

Banding

£60,001 - £70,000

£70,001-£80,000

£80,001-£90,000

£90,001 - £100,000

£100,001 - £110,000

£110,001 - £120,000

£120,001 - £130,000

£130,001 - £140,000

£140,001 - £150,000

£150,001 - £160,000

£160,001 - £170,000

£170,001-£180,000

£180,001-£190,000

£190,001 - £200,000

£230,001 - £240,000

£240,001 - £250,000

Group 2015 No.

86

43

33

18

10

4

3

6

4

2

3

2

1

2

1

1

219

Group 2014 No.

72

42

19

26

7

4

4

7

5

1

1

3

1

2

1

-

195

Thenumberofemployeesduringtheyear,whosegrosspayandbenefits(excludingemployerpensioncontributionsandawardstoinvestors)fellwithinthefollowingbands,was:

Charitable activities

Fundraising

Support services

Group 2014 No.

1,391

1,931

476

3,798

Group 2015 No.

1,411

2,062

491

3,964

Theaverageheadcountofemployees,analysedbyfunction,was:

11

ThetablebelowistakenfromtheCancerResearchUKaccounts:

Thismightsuggesttoareaderthatlastyear80%ofits£621mincomewasspentoncharitableactivities. But it transpires they have excluded ‘trading income and expenditure associated with events, registration fees and the products donated and sold in our shops.’

According to its ‘Consolidated Statement of Financial Activities’ the amount spent on charitable activities was £422.7m rather than the £464m in the table above; and the total incoming resources was £634.9m, rather than the £621m in the table above.

Of course, it is explained by Cancer Research UK how the numbers in the table were calculated. ItissurprisingsuchadifferenceappearsbetweenourownanalysisandthatofCancerResearchUK;especially as the Charity Commission appear to have used the same methodology as ourselves.

It is also notable that The Charity Commission appears to have used the wrong years income - as their calculations show a 57% charitable spend. This error raises questions as to the reliability of data on the Charity Commission’s website, even in terms of very basic reporting.

12

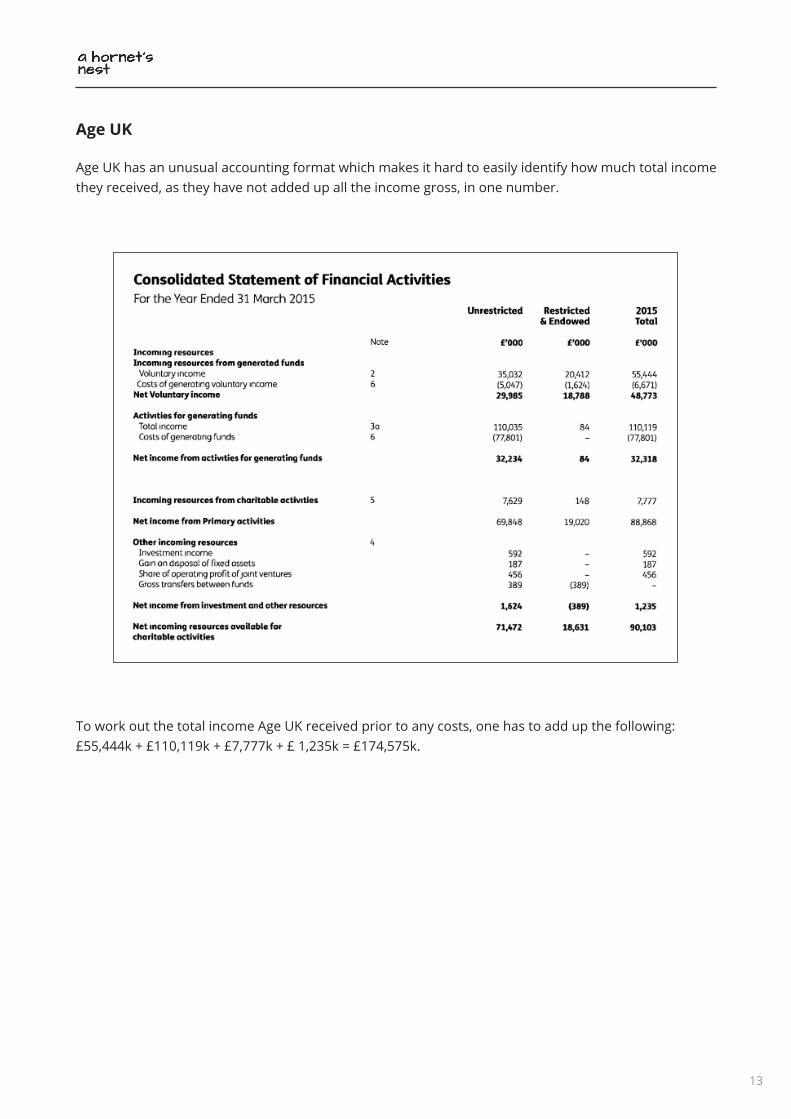

Age UK

Age UK has an unusual accounting format which makes it hard to easily identify how much total income they received, as they have not added up all the income gross, in one number.

ToworkoutthetotalincomeAgeUKreceivedpriortoanycosts,onehastoaddupthefollowing:£55,444k+£110,119k+£7,777k+£1,235k=£174,575k.

13

Sue Ryder

Looking at the Sue Ryder accounts, it appears that the amount it cost to raise their funds was greater thanthecharitableactivitiestheyconducted:

14

British Heart Foundation

There appears to be many examples where the cost of raising funds is greater than the amount spent on charitable activities. Another example is the British Heart Foundation, which, according to their last Report and Accounts, have a total cost of generating funds of £172.4m, compared to a total charitable expenditure of £113.7m.

15

The Charity Commission’s Websites

OurresearchanalysisandfindingsraisesquestionsabouttherigourofthedatadisplayedontheCharity Commission’s websites - both their main site and their newer ‘Beta’ site.

There were numerous occasions when the report and accounts data on the Commission’s websites differedfromtheactualdataintheannualreportandaccounts,orthereportandaccountsontheCharityCommissionisnotthemostuptodatesetofaccountsasfiledatCompaniesHouse.

CONCLUSIONS

The True and Fair Foundation findings pose serious questions for the charity sector:

1. Should there be an urgent review of the rules that allow organisations to be granted charitable status?Especiallyasthisstatusmeanscharitiesoftenpaylesstaxintothepublicpurse,benefitfromtax reliefs such as rent and rates, and often receive gift aid, which is essentially the public’s money.

2. Is it now time for a voluntary or mandatory minimum annual dispersal rate set for charities? It is the view of the True and Fair Foundation that a minimum annual dispersal rate of 65% should be debated.

3. Is there a need for a simpler accounting methodology to enable greater understanding by donors aboutcharities’finances?

4.Doesthesectorrequiremorefinancialoversightandaccountability?

5. Why are donors - private, corporate and government - not asking more questions about the charitable work being delivered by charities?

6. Is it time to impose a ‘Give & Good label’ across the charity sector which would clearly allow donors to see how much of annual income is being spent on the end charitable activities?

7. Should there be a periodic three year review of organisations’ charitable status?

8.Shouldtherebelimitsonseniorexecutiveremuneration,includingpensionprovision?

It is the view of the True and Fair Foundation that as the State continues to shrink, the charity sector will becomeapivotalpartofsociety.Howeverthisdoesnotexcusemanyoftheexcessesandinefficienciesthat appear prevalent within this sector.

Some commentators express concern that the charity sector faces being over-regulated and becoming another arm of the state. The True and Fair Foundation totally disagrees with this view, as the charity sector, with an estimated income of £64bn (in England and Wales), £13bn of which comes from government and is public money, should be open to scrutiny and accountability.

Trust in the sector is being eroded as light is shone on negative practices, and as this necessary inquisition of the sector continues, charities have to embrace this new landscape and adapt, evolve and betransparentsodonorscanbeconfidentthattheyhavearighttobesupported.

16

True and Fair Foundation2 Eaton Gate, Westminster, London SW1W 9BJ

www.trueandfairfoundation.com