Embed Size (px)

Citation preview

Journal of Housing Research • Volume 9, Issue 1 5q Fannie Mae Foundation 1998. All Rights Reserved.

A Primer on Geographic Information Systems inMortgage Finance

Eric Belsky, Ayse Can, and Isaac Megbolugbe*

Abstract

This article provides an overview of Geographic Information Systems (GIS) and the issues surroundingtheir use in mortgage finance and related industries. After a brief introduction to GIS and geographicdata, the application of GIS technology to mortgage finance is explored. The article also examinesorganizational challenges in developing in-house GIS capability.

GIS’s greatest potential contribution is to credit, property, and agency risk management; marketing;regulatory compliance; and research and development. It is less useful in managing prepayment riskand less still in managing interest rate risk. Most existing applications draw heavily on spatial da-tabase management and map support functions of a GIS, with little emphasis on its spatial analyticalcapabilities. Prototype applications and research and development applications, however, draw onmore powerful spatial analytical methods such as spatial statistics, spatial econometric modeling, andoptimization methods. Spatial research is critical in building next-generation mortgage finance busi-ness applications.

Keywords: GIS; Mortgage finance; Application development; Systems integration

Introduction

The effective and efficient use of information is essential for business success in mortgagefinance. As a result, appraisers, originators, lenders, insurers, real estate agents, and sec-ondary mortgage market participants are all taking a longer and harder look at how theycan use information technology to their advantage.

One of the frontiers in this quest for more intelligent use of information is Geographic In-formation Systems (GIS)—specialized computer information systems for processing geo-graphic data. Because geographic location is key to many residential real estate practices,businesses are increasingly realizing the contribution GIS can make to organizing and man-aging information as well as to management decision making and service delivery. GIStechnology has already been used to evaluate and demonstrate compliance with the Com-munity Reinvestment Act (CRA), target market areas and automate direct mail campaigns,display homes for sale on maps, set property insurance rates, and evaluate variations inlocal market share (Castle 1993; Graham 1992; King 1993). In the near future, GIS willprobably also be usedto automate appraisals,model creditrisk, trackdefaults,andmarkmort-

* Eric Belsky is Executive Director of the Joint Center for Housing Studies at Harvard University. Ayse Can isSenior Director, Program Development at the Fannie Mae Foundation. Isaac Megbolugbe is Management Consul-tant at Pricewaterhouse Coopers LLP. The authors would like to thank Gil Castle for his extremely useful commentsthat helped improve the quality of this article.

6 Eric Belsky, Ayse Can, and Isaac Megbolugbe

gage portfolios to market (Aalberts and Bible 1992; Can and Megbolugbe 1997; Nadler etal. 1993).

Although GIS has great potential to contribute to many of the business functions involvedin mortgage finance, the diffusion of GIS technology within mortgage finance is still in itsinfancy. The rate of diffusion has begun to accelerate, however, as a result of technologicaladvances, regulatory pressures, and market forces. On the regulatory side, the recent pro-liferation of GIS software aimed at helping depository institutions comply with geographicinvestment, lending, and service requirements under CRA promises to expose a growingshare of mortgage lenders to GIS technology. The regulators themselves, in addition to manycommercial vendors, are now selling the data and software needed to automate compliancemonitoring efforts. Moreover, the diffusion of GIS technology is likely to ride the automationwave that is building momentum within the mortgage finance industry, from automatedunderwriting and mortgage delivery to secondary market purchasers and automated ap-praisal systems (Kling 1995; Lebowitz 1995; Malone 1994; Nixon 1995; Portner 1995; Schnei-der 1994; Stetenfeld 1995). All of these developments are fueled by rapid advances in hard-ware and software that support GIS and by an explosion in the commercial availability ofdigital data down to the ZIP Code, census tract, block, and address levels (Bryan and Young1993; Cooke 1993; Stoecker 1993; Thrall and Thrall 1993a, 1993b). As more firms in themortgage finance business begin to use GIS, demonstration effects and competitive pres-sures will speed diffusion.

Most firms that have taken advantage of GIS technology have done so by purchasing GISservices or special purpose GIS desktop systems from external vendors. Much of what hasbeen accomplished thus far with GIS technology in mortgage finance has been done withsystems that have relatively limited analytic functionality. Most software applications sup-port map displays and some simple spatial queries but do not allow their users to performmore complex spatial modeling and analysis. Many in the industry prefer to call these desk-top mapping systems rather than GIS because they lack many basic functions of spatialdatabase management and spatial analysis. Few if any mortgage finance institutions havedeveloped true in-house GIS capability in the sense that spatial data, spatial database man-agement, spatial analysis, and spatial display functions have been fully integrated with theirin-house information system architecture. This stands in contrast to many public planningdepartments and utility companies that have developed full in-house GIS capabilities (Bor-rego 1993).

In the following section, we briefly introduce GIS technology and geographic data and em-phasize the importance of thinking in spatial terms for analyzing problems, opportunities,and challenges within the mortgage finance industry. The third section of the article takesa closer look at the role GIS technology has played and could play in the mortgage financeindustry. In the fourth section, we focus on the development and delivery of GIS businessapplications. We discuss major issues that organizations must deal with, such as building aspatial database, deciding on the functionality the GIS will provide, and integrating GISinfrastructure with existing information systems. We conclude by discussing next-generation GIS applications in mortgage finance and offering some lessons learned fromorganizations that have tried to develop in-house GIS capabilities.

A Primer on Geographic Information Systems in Mortgage Finance 7

GIS and Geographic Data

GIS has been defined and conceptualized in a number of different but related ways. Carter(1989), de Man (1988), Goodchild (1987), and Burrough (1986) argue that GIS is a specialtype of information system that handles spatial data. Dickinson and Calkins (1988) take acomponent view of GIS, arguing that a GIS has three elements: technology (hardware andsoftware), a database, and infrastructure (staff, facilities, etc.). Maguire (1991, 10), in re-viewing these and other definitions of GIS, finds common agreement that ‘‘GIS are systemswhich deal with geographical information.’’ Maguire’s broad definition serves as a usefulstarting point for discussing the properties, functions, workings, and benefits of GIS.

Spatial Data and Spatial Relationships

Maguire’s definition of GIS begs the question, ‘‘What is geographic information?’’ Geographic(or spatial) information is any measurement that is geographically referenced (i.e., that canbe tied to a specific location on the earth’s surface, such as a street address or census tract).All residential real estate information is inherently spatial because housing is fixed in geo-graphic space. Geographic data can be separated into two components: (1) the locational (i.e.,positional or cartographic) information necessary for the map representation of entities and(2) measurements on the selected attributes of map elements. For digital representation,locational information is represented in terms of points (e.g., houses), lines (e.g., streets),and areas (e.g., census tracts). Cartographic representation involves the assignment of co-ordinates to geographic entities that define their positions on the surface of the earth usinga reference coordinate system, such as spherical coordinates of latitude and longitude.

Raster and vector are the two primary data models for representing geographic data indigital form. In the raster data model, geographic space is partitioned into grid cells (pixels)of regular size and shape. Each pixel is assigned a value that represents a measurementvalue for an attribute of a spatial entity. This representation of space, although appropriatefor representation of spatially continuous variables, such as forest cover and other naturalresource information, is not suitable for the representation of residential real estate infor-mation because of the discrete nature of socioeconomic space. Information on households isusually recorded for political or administrative units whose boundaries are arbitrarily de-fined and change over time. In the vector model, locational description of geographic entitiesis represented as a set of coordinates to define their shapes.

One of the most important factors differentiating GIS technology from other data manage-ment technologies is topology (i.e., formal representation of spatial relationships). Peoplecan easily recognize spatial relationships (such as left/west, right/east, above/north, below/south, beside, near, far, touching, between) among geographic entities through visual in-spection of maps (Frank and Mark 1991). It is a challenging task for computers to embedthese spatial cognitive concepts into the digital form of a data structure. There now existseveral GIS software products that formally represent spatial relationships using a topolog-ical vector data model. This is typically done using distance, directional orientation, andconnectivity as the basic spatial elements (see Maguire and Dangermond 1991 for a re-

8 Eric Belsky, Ayse Can, and Isaac Megbolugbe

view).1 Topology is important for a wide range of spatial analysis and query functions, suchas overlay operations, spatial comparisons, networking and routing applications, and prox-imity operations. Explicit representation of topology facilitates the construction of spatialcontiguity matrices and spatial weight matrices, which are essential for capturing and an-alyzing spatial effects (Anselin 1988).

GIS Functionality

Although there are a number of different classifications of GIS functionality (e.g., Anselinand Getis 1992; Maguire and Dangermond 1991; Openshaw 1991), Maguire’s (1991) simplerclassification is appealing because it accords well with how many users—business as wellas academic—view GIS technology. Maguire (1991) categorizes GIS functionality into threeoverlapping groups: map support, spatial database management, and spatial analysis. Mapsupport, especially for presentation purposes, is still the main reason real estate organiza-tions initially acquire GIS technology. Decision makers like this capability because it allowsthem to visualize spatial patterns. The often-heard adage that ‘‘a picture speaks a thousandwords’’ perhaps explains why a function as simple as mapping is so sought after and em-braced. Software can support map displays while having very limited capabilities to performother GIS functions.

Spatial database management is the next level up in GIS functionality. We prefer to includeunder this rubric functions that any good database management system (DBMS) wouldperform, but in this case, GIS performs them on both locational and attribute information.Although GIS organizes and manages attribute information just as a traditional relationalDBMS, the management of locational data requires specialized analytical routines to sup-port simple spatial queries, spatial overlays, spatial comparisons, and buffering, which arefar more complex than queries in attribute data. We therefore would include, under spatialdatabase management, GIS functions for storage and structuring of geographic data as wellas analytical functions that support the simple querying and analysis of real estate data.

Analytical functions offered in commercially available GIS software provide limited supportfor the more specialized analysis and modeling of geographic data (Anselin and Getis 1992;Griffith 1993; Haining and Wise 1991). The emphasis in most current commercial GIS soft-ware is on database management and mapping. In this article, we refer to software thatperforms spatial database management functions and mapping as a ‘‘standard GIS toolbox.’’We use this term to differentiate from an ‘‘extended’’ toolbox that contains tools to supportthe unique spatial analysis needs of real estate data. The extended GIS toolbox contains thespatial statistical/econometric tools required to perform what Anselin and Getis (1992) callexploratory and confirmatory research and analysis. The spatial analytical functionalityrequired to conduct spatial research will drive advances in GIS applications in mortgagefinance in the years ahead. Tools for exploratory and confirmatory analysis include

1 The typical format used by desktop mapping systems is a nontopological representation of vector data (also called‘‘unlinked’’ or ‘‘spaghetti’’) in which each map entity is represented as a sequence of coordinates that make up itsboundaries. In this representation, spatial relationships are not encoded. Although it is possible to extract topolog-ical information, the task requires considerable programming effort.

A Primer on Geographic Information Systems in Mortgage Finance 9

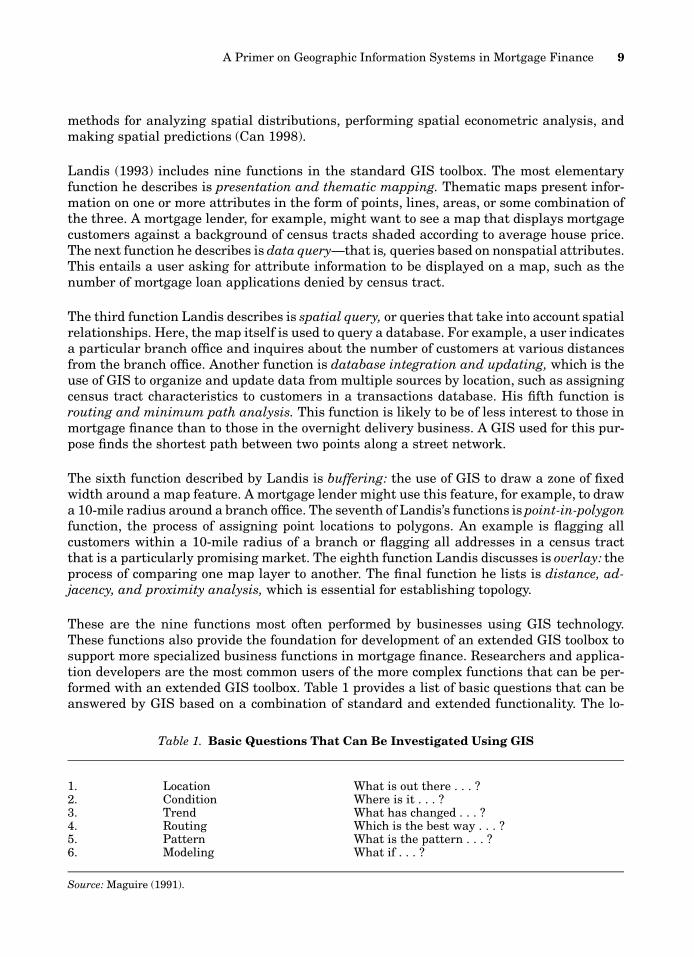

Table 1. Basic Questions That Can Be Investigated Using GIS

1. Location What is out there . . . ?2. Condition Where is it . . . ?3. Trend What has changed . . . ?4. Routing Which is the best way . . . ?5. Pattern What is the pattern . . . ?6. Modeling What if . . . ?

Source: Maguire (1991).

methods for analyzing spatial distributions, performing spatial econometric analysis, andmaking spatial predictions (Can 1998).

Landis (1993) includes nine functions in the standard GIS toolbox. The most elementaryfunction he describes is presentation and thematic mapping. Thematic maps present infor-mation on one or more attributes in the form of points, lines, areas, or some combination ofthe three. A mortgage lender, for example, might want to see a map that displays mortgagecustomers against a background of census tracts shaded according to average house price.The next function he describes is data query—that is, queries based on nonspatial attributes.This entails a user asking for attribute information to be displayed on a map, such as thenumber of mortgage loan applications denied by census tract.

The third function Landis describes is spatial query, or queries that take into account spatialrelationships. Here, the map itself is used to query a database. For example, a user indicatesa particular branch office and inquires about the number of customers at various distancesfrom the branch office. Another function is database integration and updating, which is theuse of GIS to organize and update data from multiple sources by location, such as assigningcensus tract characteristics to customers in a transactions database. His fifth function isrouting and minimum path analysis. This function is likely to be of less interest to those inmortgage finance than to those in the overnight delivery business. A GIS used for this pur-pose finds the shortest path between two points along a street network.

The sixth function described by Landis is buffering: the use of GIS to draw a zone of fixedwidth around a map feature. A mortgage lender might use this feature, for example, to drawa 10-mile radius around a branch office. The seventh of Landis’s functions is point-in-polygonfunction, the process of assigning point locations to polygons. An example is flagging allcustomers within a 10-mile radius of a branch or flagging all addresses in a census tractthat is a particularly promising market. The eighth function Landis discusses is overlay: theprocess of comparing one map layer to another. The final function he lists is distance, ad-jacency, and proximity analysis, which is essential for establishing topology.

These are the nine functions most often performed by businesses using GIS technology.These functions also provide the foundation for development of an extended GIS toolbox tosupport more specialized business functions in mortgage finance. Researchers and applica-tion developers are the most common users of the more complex functions that can be per-formed with an extended GIS toolbox. Table 1 provides a list of basic questions that can beanswered by GIS based on a combination of standard and extended functionality. The lo-

10 Eric Belsky, Ayse Can, and Isaac Megbolugbe

cation question involves queries about the characteristics of given locations (e.g., What isthe number of mortgage originations in a given census tract?). The condition question isconcerned with finding sites that meet certain criteria (e.g., census tracts with the highestconcentration of poverty). The trend question addresses how given phenomena have changedover time. The routing question aims to find the best route between places given certaincriteria. The pattern question is concerned with the geographic distribution of given phe-nomena as well as the processes that give rise to such patterns. Finally, the modeling ques-tion is used to predict and evaluate outcomes under different modeling frameworks. Al-though basic functionality offered in commercially available GIS software would be sufficientto undertake simple data queries in mortgage finance, such as the location and conditionquestions, an extended GIS toolbox is necessary to address more complex analytical ques-tions such as trend, pattern, and modeling.

Mortgage Finance and GIS

GIS technology has a great deal to offer the mortgage finance industry because geographiclocation and spatial relationships have a central role in housing and mortgage market out-comes. Housing is fixed in its location and is durable. As a result, a home’s location relativeto employment opportunities, mortgage finance and housing market intermediaries, publicservices, and amenities exerts a strong influence on its price. The location of a home alsoinfluences the choices and opportunities of its residents and of those seeking to own or rentit. Neighborhood characteristics also influence house prices and choices. These character-istics include the types of homes available, quality of the housing stock, quality and extentof the community infrastructure, quality of public services, and social and economic condi-tions in the neighborhood. Decisions ranging from where to live to what to pay for a hometo whether to maintain or improve a home are all tied to location.

Location also influences mortgage markets. The location of mortgage suppliers defines theavailability of mortgage credit. The segregation of residential space into discrete geographicsubmarkets influences the pattern and nature of mortgage product demand. Neighborhoodconditions influence credit risk because of their effect on the direction of house prices. Prox-imity to employment influences the long-term capacity of borrowers to repay loans, andtherefore influences both prepayment and default behavior. These are just some of the wayslocation plays a role in both housing and mortgage markets (Can 1998).

Firms in the mortgage finance industry must concern themselves with space not only be-cause locational influences are so strong in the market they serve but also because theygenerally have to formulate location-specific marketing strategies. The highly segregatednature of residential space demands that mortgage lenders target their products, services,and marketing efforts to the specific character of different demographic groups that occupydifferent market areas. Also, because the nature of the competition faced by participants inthe mortgage finance process varies across different areas, they must develop different com-petitive strategies to suit the character of their competition in different areas.

GIS technology has the potential to support a wide range of business applications in mort-gage finance. At the most elemental level, it can provide mapping capabilities to help deci-sion makers visualize the spatial distribution of variables that affect their business

A Primer on Geographic Information Systems in Mortgage Finance 11

performance, such as the location of borrowers, competitors, and branches. At a higher level,it can be used to combine multiple variables such as the racial and income composition ofneighborhoods with the location of recent mortgage originations. In addition, businesses canuse GIS for map-driven information management that allows them to examine businessdata at any level of geography (from states or metropolitan areas on a national map, to ZIPCodes or census tracts, to individual observations like homes and branch offices) and gen-erate attribute information on that level. Businesses can also use GIS to support queriesrelating to distance, such as how many mortgage originations within one mile of a branchoffice went to another lender. At still higher levels of functionality, GIS is capable of advancedpredictive and optimization modeling. It can be used, for example, to select the optimalnumber, location, and size of branch offices to service a market area given some decisionrules about how far any share of potential borrowers can be from a branch office (Birkin andClarke 1998).

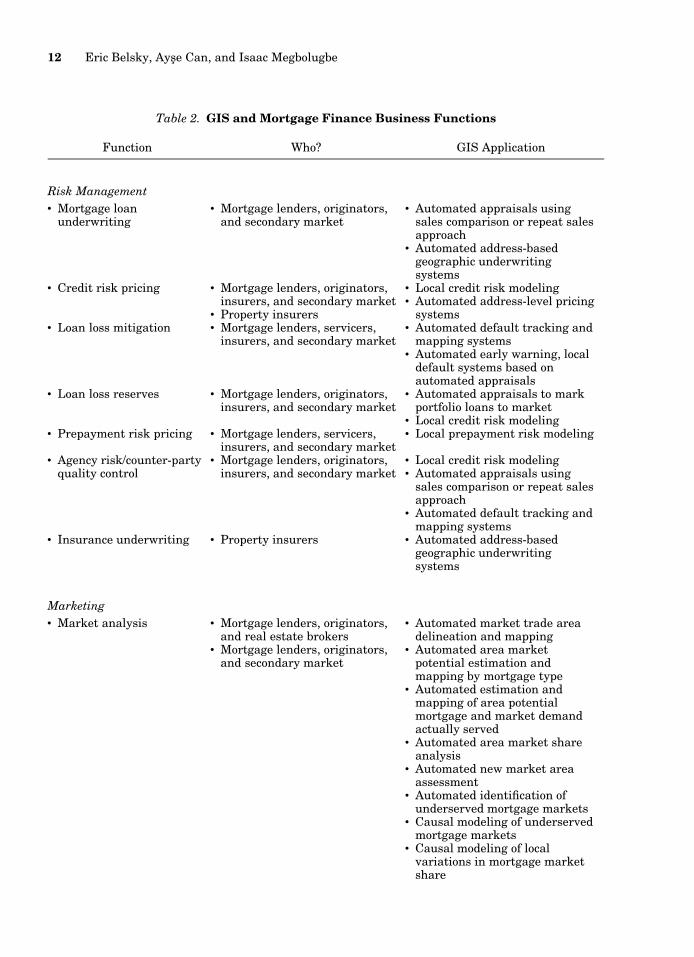

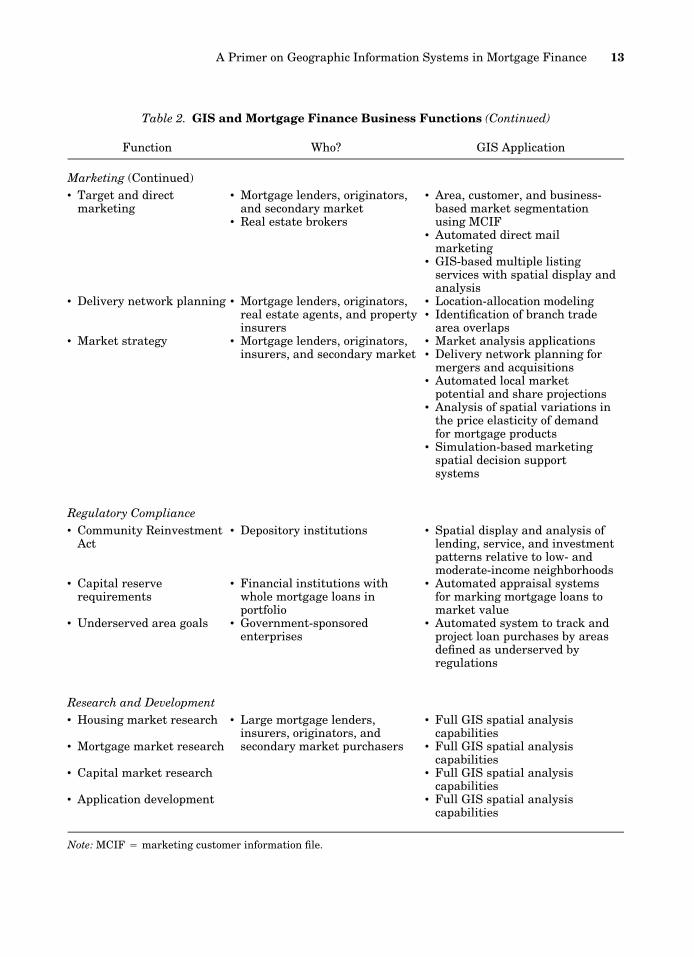

To bring some order to the wide range of possible GIS applications, we have grouped themunder four major business functions: risk management, marketing, regulatory compliance,and research and development (table 2). Some GIS applications may serve more than onebusiness function. In addition to existing applications, we discuss a range of potential ap-plications, several of which are already in the prototype stage of development. GIS technol-ogy is still relatively new to mortgage finance, but as greater experience is gained with it,many of these applications will also end up in commercial use. The primary constraints ontaking applications from the prototype stage to commercial use are the need for furtherresearch and testing and the quality, cost, and availability of data.

Risk Management

Property insurers, mortgage insurers, and mortgage lenders all must manage risks. Mort-gage lenders and insurers manage risks related to the mortgage loan itself, whereas propertyinsurers manage risks of loss of property because of theft, fire, and natural disasters. Allcan and increasingly do use GIS to help them manage these risks.

The three risks related to the mortgage itself that lenders or other investors must manageare interest rate, prepayment, and credit risk (Diamond and Lea 1995). Interest rate risk isthe risk that the interest rate on long-term fixed-rate mortgage assets already originatedwill at some point fall below the interest rate on the short-term liabilities that are used tofund them. Prepayment risk is the risk that borrowers will return principal at a time whenlenders must reinvest the funds at a lower interest rate than when the mortgage was orig-inated. Credit risk is the risk that some portion of the principal will not be recovered as aresult of borrower default.

Of these three risks, credit risk is the only one that is strongly influenced by local factors.Both prepayment risk and interest rate risk are driven mostly by changes in interest ratesat the national level. Falling rates increase the probability that borrowers will refinancetheir mortgages and that lenders will be hurt by mismatches in the duration of their assetsand liabilities. Because all areas of the country are exposed to the same changes in interestrates at about the same time, local factors do not play much of a role in determining a

12 Eric Belsky, Ayse Can, and Isaac Megbolugbe

Table 2. GIS and Mortgage Finance Business Functions

Function Who? GIS Application

Risk Management• Mortgage loan

underwriting• Mortgage lenders, originators,

and secondary market• Automated appraisals using

sales comparison or repeat salesapproach

• Automated address-basedgeographic underwritingsystems

• Credit risk pricing • Mortgage lenders, originators,insurers, and secondary market

• Property insurers

• Local credit risk modeling• Automated address-level pricing

systems• Loan loss mitigation • Mortgage lenders, servicers,

insurers, and secondary market• Automated default tracking and

mapping systems• Automated early warning, local

default systems based onautomated appraisals

• Loan loss reserves • Mortgage lenders, originators,insurers, and secondary market

• Automated appraisals to markportfolio loans to market

• Local credit risk modeling• Prepayment risk pricing • Mortgage lenders, servicers,

insurers, and secondary market• Local prepayment risk modeling

• Agency risk/counter-partyquality control

• Mortgage lenders, originators,insurers, and secondary market

• Local credit risk modeling• Automated appraisals using

sales comparison or repeat salesapproach

• Automated default tracking andmapping systems

• Insurance underwriting • Property insurers • Automated address-basedgeographic underwritingsystems

Marketing• Market analysis • Mortgage lenders, originators,

and real estate brokers• Mortgage lenders, originators,

and secondary market

• Automated market trade areadelineation and mapping

• Automated area marketpotential estimation andmapping by mortgage type

• Automated estimation andmapping of area potentialmortgage and market demandactually served

• Automated area market shareanalysis

• Automated new market areaassessment

• Automated identification ofunderserved mortgage markets

• Causal modeling of underservedmortgage markets

• Causal modeling of localvariations in mortgage marketshare

A Primer on Geographic Information Systems in Mortgage Finance 13

Table 2. GIS and Mortgage Finance Business Functions (Continued)

Function Who? GIS Application

Marketing (Continued)• Target and direct

marketing• Mortgage lenders, originators,

and secondary market• Real estate brokers

• Area, customer, and business-based market segmentationusing MCIF

• Automated direct mailmarketing

• GIS-based multiple listingservices with spatial display andanalysis

• Delivery network planning • Mortgage lenders, originators,real estate agents, and propertyinsurers

• Location-allocation modeling• Identification of branch trade

area overlaps• Market strategy • Mortgage lenders, originators,

insurers, and secondary market• Market analysis applications• Delivery network planning for

mergers and acquisitions• Automated local market

potential and share projections• Analysis of spatial variations in

the price elasticity of demandfor mortgage products

• Simulation-based marketingspatial decision supportsystems

Regulatory Compliance• Community Reinvestment

Act• Depository institutions • Spatial display and analysis of

lending, service, and investmentpatterns relative to low- andmoderate-income neighborhoods

• Capital reserverequirements

• Financial institutions withwhole mortgage loans inportfolio

• Automated appraisal systemsfor marking mortgage loans tomarket value

• Underserved area goals • Government-sponsoredenterprises

• Automated system to track andproject loan purchases by areasdefined as underserved byregulations

Research and Development• Housing market research

• Mortgage market research

• Capital market research

• Application development

• Large mortgage lenders,insurers, originators, andsecondary market purchasers

• Full GIS spatial analysiscapabilities

• Full GIS spatial analysiscapabilities

• Full GIS spatial analysiscapabilities

• Full GIS spatial analysiscapabilities

Note: MCIF 4 marketing customer information file.

14 Eric Belsky, Ayse Can, and Isaac Megbolugbe

mortgage lender’s exposure to risk resulting from falling rates.2 Nevertheless, at least asmall part of prepayment risk is influenced by local factors when prepayment results fromhome sales. Home sales, unlike significant changes in interest rates, are often driven by localfactors, such as the rate of job creation and the age structure of the population. As a result,GIS technology can play a role in modeling prepayment risk, but its contribution is at themargin because prepayment risk is driven mostly by national interest rate changes. GIStechnology therefore has little to offer for the active management of interest rate and pre-payment risk, but has a great deal to offer for managing credit risk.

Mortgage lenders and mortgage insurers manage credit risk by four primary means: under-writing, loss mitigation, loan loss reserves, and pricing. Lenders and mortgage insurers useunderwriting to manage risk by granting mortgage credit to only those borrowers and trans-actions that meet standards intended to screen out bad risk. Lenders and insurers use pric-ing to manage risk by setting interest rates or a guaranty fee high enough to cover expectedlosses on accepted loans plus some rate of return. They use loan loss mitigation strategiesto manage credit risk by acting swiftly to minimize potential losses when signs of a paymentproblem, such as delinquent payments, are first recognized. And finally, they use loan lossreserves as a cushion against expected losses in light of changes in the risk characteristicsof the portfolio over time. GIS can contribute to all four of these methods for controllingcredit risk.

GIS Technology and Underwriting. GIS can help in underwriting mortgages by using spatialdata to estimate the fair market value of individual properties. Estimating the real value iscentral to managing credit risk because it determines the value of the collateral that securesa loan. One of the most important factors in managing credit risk is controlling the size ofa mortgage loan relative to the value of its collateral (Lekkas, Quigley, and Van Order 1993;Quercia and Stegman 1992). The lower the loan-to-value ratio, the smaller the chance thata borrower will end up with negative net equity in the home and the greater the lender’sprotection against house price declines. Negative net equity is considered a necessary, evenif not a sufficient, condition for default. Accurate assessments of property value thereforelie at the heart of credit risk management.

Most appraisals are conducted by sending appraisers out to the field to estimate value usingthe cost, sales comparison, and income approaches (American Institute of Real Estate Ap-praisers 1987). The income approach is used only to assess the value of rental properties.Both the cost and sales comparison approaches to estimating value involve making estimatesbased on local market factors. The sales comparison approach typically involves basing anestimate of value on three recent, nearby comparable sales, adjusted for slight differencesin the physical characteristics of the property and site (sometimes also adjusted for thelength of time on the market and the size of the supply of homes for sale in the local market).

2 Even though all areas of the country are affected by changes in interest rates at about the same time, localreactions to these changes may vary as a result of systematic spatial variations in the characteristics of mortgageborrowers and lenders. Evidence suggests, for example, that low-income borrowers prepay at lower rates than high-income borrowers in falling interest rate environments. Because neighborhoods are often segregated along incomelines, prepayments triggered by falling rates may therefore vary systematically by neighborhood. Similarly, lendersin some areas may be more strongly affected by falling interest rates than in others because some lenders did apoorer job than others of matching the duration of their assets with their liabilities. However, the chances thatlenders’ strategies will vary systematically across space are not nearly as great as the chances that conditions thatfavor turnover of for-sale homes will.

A Primer on Geographic Information Systems in Mortgage Finance 15

The cost approach involves estimating the replacement cost of the home, which depends onthe local cost of land, materials, and labor. Many of the processes involved in making thesejudgments can be enhanced by a GIS with the appropriate data and analytical tools. At leastone vendor, Marshall & Swift, sells a package for cost-estimating commercial properties thattakes into account locational variations in material and labor. Weber (1990) reports on aprototype for a system to estimate commercial property values based on gravity models ofpotential property demand.

A much more powerful application of GIS technology to appraisal, however, and one thatdraws on its full analytical powers, is its use to make sales comparisons. Data on the physicalcharacteristics and selling prices of homes are increasingly available at the address levelfrom commercial vendors (such as TRW-Redi, Transamerica, and Data Quick). Researchershave already begun developing advanced spatial analytical tools that come very close toreplicating a manual sales comparison approach in the automated environment of GIS (Canand Megbolugbe 1997; Pace and Gilley 1995; Rodriguez, Sirmans, and Marks 1995). Thesetools combine information on housing attributes with spatial information on nearby com-parable repeat sales in a hedonic equation to make a point estimate of a subject property’svalue.3

Automated appraisal systems using GIS capabilities can be used either to select a bestestimate of value automatically or to support the individual judgment of an appraiser. Ap-praisers can use automated systems to enter a property address and have automaticallygenerated such information as the rate of house price change on repeat sales in the neigh-borhood (defined by ZIP Code, census tract, or area defined as having a homogeneous rateof house price change based on GIS analysis) for the past one, three, and five years; recentsales prices of comparable homes by distance from the subject property; house price changein the metropolitan area; forecasted unemployment rates in the metropolitan areas; andhouse price volatility. Used this way, automated appraisal systems are best thought of asspatial decision support systems because they support a decision about a semistructuredproblem. In a fully automated system, the estimate produced by the GIS model is acceptedas the estimate of fair market value without manual review.

Although it may be a few more years before GIS tools are used to automate appraisals forunderwriting, there is a strong likelihood that some form of automated appraisal systemsbased on GIS technology will soon be developed for commercial use. Use of GIS-driven au-tomated appraisal systems will reduce costs and the time it takes to underwrite mortgages.

GIS Technology and Loan Loss Mitigation. GIS technology can also be used to improve loanloss mitigation efforts. Early signs of heavily concentrated defaults are easily picked up ina GIS, and a GIS can be used to identify places where house prices appear to be on thedecline (Aalberts and Bible 1992). The value of identifying geographic areas that are devel-

3 A GIS-based approach to automated appraisals differs from computerized automated mass assessment (CAMA)systems that are now widely used for tax assessment and portfolio management purposes. There are two types ofCAMA systems. One constructs a repeat sales index for an area and adjusts values for all homes in that area thathave not sold using that index (Case, Pollakowski, and Wachter 1991; Crone and Voith 1992). The other estimatesa hedonic equation for an area using recent sales and uses it to assess current values for homes there that havenot sold (Atkinson and Crocker 1987; Eckert and O’Connor 1992). Although both approaches could, and likely inthe future will, be enhanced by the incorporation of information on the absolute and relative location of repeat andrecent sales, neither now does. Nevertheless, some lenders are already using CAMA systems based on repeat salesto streamline underwriting for applications from areas with consistently stable or rising prices.

16 Eric Belsky, Ayse Can, and Isaac Megbolugbe

oping problems is significant. It can help lenders (in the primary and secondary markets)work with servicers to take actions to help stem the tide by concentrating their efforts earlyon in the areas that need it the most. Data availability is not a problem for primary andsecondary mortgage market institutions because information on delinquent loans by addressis kept in-house by these institutions and house price data, as noted above, are widely avail-able from outside vendors.

GIS Technology and Loan Loss Reserve. On the loan loss reserve side, GIS technology canplay a role by improving credit loss forecasts and by marking a portfolio of loans to marketusing automated appraisals to update loan-to-value ratios and hence the risk profile of theportfolio. The demand for accuracy in marking a portfolio to market for the purposes of earlyloss mitigation and establishing loan loss provisions is generally lower than the demand foraccuracy at the underwriting stage. In fact, and partly for this reason, automated repeatsales indexes are already widely used by the industry to mark mortgage portfolios to market(Pollakowski 1995; Stephens et al. 1995). These systems calculate a repeat sales index usingdigital data to determine the direction and magnitude of average price changes at the county,ZIP Code, or census tract levels.4 These systems do not yet, however, take advantage of thepower of GIS technology. GIS can be used to identify areas of homogeneous house pricechange by using spatial association measures to discern spatial patterns in repeat sales.This capability would free automated repeat sales systems from having to rely arbitrarilyon census, ZIP Code, and political geography to construct indexes and mark loans to market.Eventually, GIS will probably be used to improve mark-to-market systems by combining aGIS-based repeat sales method with point value estimates based on the weighted distancesof recent sales from each property being marked to market.

GIS Technology and Credit Risk Pricing. At some point, GIS technology may also play a rolein pricing mortgages. Although pricing decisions involve marketing and finance as well ascredit risk management, expected credit losses form an important capstone for these deci-sions. Credit losses are a function not only of borrower characteristics and loan terms butalso of the location of the collateral. Expected credit losses are highest in areas that arevulnerable to price declines or labor dislocations in the early years of a mortgage. Lenderstherefore have a strong interest in being able to predict which areas will experience pricedeclines or rising unemployment within the first several years after a mortgage is originated.Modeling determinants of house price declines and labor dislocations at the local level canbe conducted in a GIS environment. Nadler et al. (1993), for example, report on an effort topredict mortgage defaults and loan losses at the metropolitan level conducted by Fitch In-vestor Services. With this kind of interest already expressed on Wall Street for local-levelloss forecasting, GIS may soon be used to predict the incidence of default and loan lossseverity at the appropriate level of geographic detail. Armed with local default and loan lossprediction capability, mortgage lenders can do a better job of pricing and diversifying risk.Local estimates of credit risk are useful whether lenders use them to charge different inter-est rates in different areas to reflect underlying credit risk or to establish a more realisticaverage price for all areas based on the expected geographic mix of loans. These kinds ofGIS applications for pricing, however, are not yet available.

4 Automated appraisal systems based on repeat sales throw out much potentially valuable information on recentsales. This makes it difficult to construct a reliable index for places where there are few identifiable paired repeatsales. As a result, coverage of nonmetropolitan areas by these systems is often weak.

A Primer on Geographic Information Systems in Mortgage Finance 17

GIS Technology and Insurance Underwriting. GIS technology can also help property insurersunderwrite and price their policies. This is an important aspect of the credit risk borne bymortgage insurers and lenders because borrowers who lack adequate property insurancecoverage are more apt to default after a disaster than those with adequate coverage. GISapplications have already been developed that allow insurers to determine whether a prop-erty falls within an area prone to a natural disaster such as a flood or earthquake. An evenmore powerful application enables property insurers to set rates on a property based on anautomated assessment of the crime rate in its neighborhood and how far it is from thenearest fire hydrant, fire station, and police station (Francica 1993; Kochera 1994). Theseapplications are highly data intensive, yet have already been used commercially. An exampleis the Geographic Underwriting System (GUS)5 (Sharp 1996).

GIS Technology and Agency Risk. One final risk that virtually all parties to a mortgagetransaction must manage is agency risk: the risk that a counterparty will behave in a fashionthat exposes the primary party to some risk. In mortgage markets, the most common sourcesof agency risk are fraud and malfeasance. Risk could take the form of an intentional decisionto sell mortgages that the seller knows are likely to perform poorly to another party. Thistype of agency risk is called adverse selection. GIS technology can help manage agency riskin several ways. Mortgage lenders and insurers can use a GIS-driven automated appraisalsystem as a quality control device to monitor the accuracy of manual underwriting. Propertyinsurance companies can use automated assessment of hazard zones and other componentsof shared risk to perform quality control assessments of their agents. Mortgage lenders andinvestors can use GIS to identify areas where the performance of seasoned loans is likely tobe poorer than average as a way to guard against adverse selection in the sale of seasonedloans.

Marketing

Like risk management applications, marketing applications can range from simple mapvisualizations to more complex GIS-based modeling. Marketing variables such as the sizeof the potential market, the market served, market share, neighborhood demographic char-acteristics, branch locations, trade areas, customer addresses, and product profitability canall be captured or created, stored, manipulated, combined, analyzed, and displayed. Mar-keting customer information file (MCIF) applications using GIS technology have been de-veloped to perform these functions (Graham 1992). With geocoding capabilities often builtin so that customer address information can easily be imported and used to create a spatialdatabase, these packages offer mortgage lenders and originators a convenient way to seg-ment markets, target direct mail to them, and assess their profitability.

Increasingly, all or most of the data needed to perform these functions are available at lowcost in digital form. Most depositories and many mortgage bankers operating in metropolitanareas must, under the Home Mortgage Disclosure Act (HMDA), annually report on theirmortgage originations, mortgage applications, select characteristics of applicants, and mort-

5 GUS is a registered trademark of Datamap, Inc.

18 Eric Belsky, Ayse Can, and Isaac Megbolugbe

gage sales to the secondary market (Canner and Smith 1992). The Federal Reserve compilesthe data and offers them for sale to the public in a variety of formats and at reasonablecosts. The HMDA data can be supplemented with census and other data on demographicand housing stock characteristics down to the census tract level, and for some variables, theblock level. Mortgage lenders and originators can combine low-cost external databases withinformation on their customers to form powerful MCIFs.

Some mortgage lenders, originators, and consultants are applying GIS technology to at leasteight marketing challenges (Beaumont 1991a; Clark 1993; Hall 1993; King 1993; Pittmanand Thrall 1992). First, GIS is being used to delineate the trade areas of individual branchesbased on the addresses of their customers or mortgage applicants. Second, lenders are usingGIS to estimate area market potential for particular mortgage products by combining sec-ondary source demographic information with primary information on mortgage customersby product to estimate the number of potential customers by area. Potential market demandcan be compared to actual originations by using HMDA data. Third, GIS technology is beingused to measure market penetration by area. Competition in both the primary and secondarymarkets can be assessed in this way because HMDA data contain information on both mort-gage originations and mortgage sales to the secondary market. Fourth, mortgage originatorsare using GIS to segment markets based on geodemographics. As Graham (1992) points out,GIS-based marketing systems accommodate both customer-based segmentation and bank-based segmentation. Customer-based segmentation defines markets based on the needs andwants of different customer groups. Bank-based segmentation defines markets based on theprofiles of current bank customers, the products they purchase, and their profitability. Be-cause residential space is often segregated by race, ethnicity, income, age, or nationality,different customer segments often concentrate in different neighborhoods. Knowing the lo-cation of residents that fit a target market profile lets companies target them through geo-graphic marketing strategies. A related marketing use for GIS technology is therefore tar-geted marketing. Once the locations of the target markets have been identified, GIS can beused to generate mailing labels for direct mail campaigns. Mortgage lenders and originatorsinterested in expanding can assess market potential, market penetration, and competitionin these places. GIS technology is also used to plan the delivery network for mortgages andother loan products: A lender can assess where branch trade areas may overlap and wherelocating an additional branch might cut into a competitor’s market share. The technologyalso supports location-allocation modeling, which identifies the optimal number and/or con-figuration of branch locations using user-defined measures of optimality (Birkin and Clarke1998; King and Willer 1993). Such models have the potential to save companies a great dealof money while improving their delivery systems.

Several additional uses of GIS technology for marketing by mortgage lenders and secondarymarket purchasers may be possible. It could be used to identify underserved mortgage mar-kets. Essentially, this would involve modeling the determinants of mortgage demand andsupply at the local level (Megbolugbe and Cho 1993; Perle, Lynch, and Horner 1993). Areaswith fewer originations or applications than predicted by such a model would then warrantfurther investigation to determine what is holding back market demand. GIS also could beused to evaluate the reasons for geographic variations in a company’s market share. Thosevariations can be systematic or random. If the variations are systematic, GIS can facilitateinvestigation of possible causes. Differences in the amount of money spent by differentbranches on marketing, the mix of products offered at different branch locations, the average

A Primer on Geographic Information Systems in Mortgage Finance 19

characteristics of the population in different areas, and spatial variations in the nature ofthe competition (such as the number and type of competitors) might lead to systematicvariations at the primary market level. At the secondary market level, the characteristicsof the population in different areas and the types of lenders most active in specific areasmight be the sources of geographic variation in market share. Insights into the causes ofunderperformance relative to the competition in different markets could help improve per-formance and gain market share. GIS technology could also be used to project market vol-umes by area. This would involve making local-level projections of market growth and mar-ket share. Although such a capability would benefit all lenders, it would be particularlyuseful to the secondary mortgage market enterprises, Fannie Mae and Freddie Mac, becausethey are required to meet numerical goals for purchases from areas defined by the federalgovernment as underserved.6 Finally, it could be used to evaluate spatial variations in theprice elasticity of demand for different mortgage products. At present, however, the datanecessary to estimate separately these elasticities are not available at low cost. Firms wouldhave to collect detailed time-series data on changes in volume in different interest rateenvironments, controlling for local economic conditions such as unemployment and income.This data may become available as organizations see the benefits of changing their databasestructure to track volume changes.

GIS applications can be used at both the middle-management and upper-management levelsto inform marketing decisions. At the executive level, the information generated from GIScan be used to develop geographically targeted market, competitive, and pricing strategies.Applications have not yet been developed that simulate outcomes under varying strategicplans and marketing assumptions. Nevertheless, GIS technology has the potential to deliversuch executive spatial decision support system (SDSS) applications in the future.

Regulatory Compliance

GIS has become an important tool for evaluating and demonstrating compliance with theCommunity Reinvestment Act (CRA), which imposes an affirmative obligation on all depos-itory institutions to meet the credit needs of their entire community, including low- andmoderate-income neighborhoods, consistent with safe and sound operations. Lenders mustdemonstrate to their regulators that they are making an effort to meet, and are succeedingat meeting, the needs of low- and moderate-income neighborhoods. Several software pack-ages have been developed to help banks and thrifts evaluate their CRA performance. Thesepackages rely heavily on HMDA and 1990 census data. They vary in functionality, ease ofuse, and report formats (Thrall 1998). At a minimum, these packages can define marketareas based on the observed pattern of mortgage loan applications, approvals, and denialsand then provide map overlays of census tracts by income so the patterns of service andunderservice can be evaluated. Some provide more sophisticated functions, such as rankingareas for CRA potential and estimating market shares of mortgage loan applications, ap-

6 Underserved areas are defined for the purposes of meeting regulatory requirements in metropolitan areas ashouseholds located in tracts that have either (1) at least 30 percent minority residents and a tract median incomeat or below 120 percent of adjusted median income (AMI) or (2) a median income less than or equal to 90 percentof AMI. Underserved nonmetropolitan areas are defined as counties that have either (1) at least 30 percent minorityresidents and a county median income at or below 120 percent of the statewide nonmetropolitan median incomeor (2) a median income less than or equal to 95 percent of the greater of statewide nonmetropolitan median incomeor nationwide nonmetropolitan median income.

20 Eric Belsky, Ayse Can, and Isaac Megbolugbe

provals, and denial by census tract. Clearly, the use of GIS technology for CRA compliancehas much in common with its uses for marketing. As more financial institutions that useGIS for CRA compliance begin to recognize its potential for marketing, more of them willlikely pursue MCIFs to target low- and moderate-income markets and markets segmentedalong other lines.

GIS technology will probably also be used in the future to support compliance with capitalreserve requirements. Recent regulations require financial institutions to assess their re-serve requirements based on the market rather than the book value of their portfolio. In thecase of mortgages, this means estimating the current value of a mortgage based on its cur-rent loan-to-value ratio, its coupon compared with current mortgage interest rates, and itsremaining term. GIS can be used to improve estimates of current market value using al-gorithms that emulate a manual sales comparison method.

Research and Development

GIS can play an important role in corporate research and development. Many opportunitiesto gain an edge over the competition can be developed by exploiting information on spatialvariations in market competition, market potential, and credit risks. Many of the potentialapplications described previously will demand further research before they go beyond theprototype stage. For example, the use of GIS technology to simulate the sales comparisonand cost approaches to appraisal awaits further testing of the accuracy of using digital dataand computer algorithms for that purpose. Also, the more sophisticated and powerful usesof GIS technology for risk management, pricing, and marketing depend on progress in de-veloping models that can forecast local housing supply and demand conditions, project mar-ket demand by product and local area, evaluate local-level credit risk, and identify areaswhere mortgage demand is not being adequately met by suppliers.

Indeed, real estate researchers are increasingly turning to GIS applications to improve theirunderstanding of how real estate and mortgage markets operate. Much of this work hasfocused on understanding land use change (Thrall, McClanahan, and Thrall 1995), neighbor-hood housing market change (Thrall et al. 1993), and house price determination (Can andMegbolugbe 1997). Basic research will provide the models and algorithms that will drivetomorrow’s GIS applications.

Capturing the Benefits of GIS Technology: Developing In-HouseGIS Applications

Given the wide variety of potential uses for spatial data and analysis in mortgage financeand related industries, many organizations want GIS capabilities. Organizations can cap-ture the benefits of GIS technology either by relying on external vendors or by developingan in-house GIS capability. The simplest and the fastest way for organizations to capturethe benefits of GIS technology is by contracting with external GIS service providers to pro-duce standardized reports using GIS. The principal disadvantage of this approach is that itlimits the use of GIS technology to a narrowly defined set of uses and report formats thatare available from commercial vendors. The utility of this approach is limited in the long

A Primer on Geographic Information Systems in Mortgage Finance 21

term because almost all the applications outlined in the previous section rely on the use ofproprietary business data and in-house knowledge about highly specialized business func-tions. Therefore, most large organizations in mortgage finance would be better off with aninternal GIS capability to develop GIS applications. Nevertheless, many organizations con-tinue to rely on external GIS service providers as their first step into the world of GIS.Outside vendors are commonly called on to geocode data and monitor regulatory compliance.

A more complex way of working with GIS providers is to commission vendors or consultantsto develop special-purpose GIS systems to meet certain business needs. An increasing num-ber of vendors have begun offering customized GIS systems for CRA compliance, site selec-tion, and marketing, among other special needs (see Business Geographics 1997 for a list ofGIS services that are commercially available). These customized applications typically comewith basic spatial database management functions, such as importing, retrieving, manipu-lating, and displaying spatial data. They usually support spatial queries and map overlays.Often they come complete with nonproprietary geocoded data such as map files and censusdemographics that can be manipulated alone or in concert with proprietary business data.

The chief advantage of purchasing such systems is that they help organizations become morefamiliar with the broad array of potential uses of GIS without forcing them to make costlyup-front changes to their existing information systems architecture. These systems alsoprovide greater control over report generation and stronger interactive capabilities. Theycan be introduced without significant changes to the organizational structure. The chiefdrawbacks are that these systems deprive organizations of the opportunity to develop in-house capacity to build proprietary applications and bring the benefits of GIS technology toa broader range of their business functions. Although organizations can work with vendorsto custom-tailor multiple applications, economies of scale in application development endup being captured by the vendors rather than their customers.

Relying strictly on external GIS service providers is most attractive to those who are alreadyconvinced of the benefits of GIS technology for a particular application but do not anticipateusing it for many applications. It is also attractive to those who can foresee wanting GIS tohelp them meet other business needs in the future but want to take a slow and cautiousapproach now. As these organizations gain familiarity with the technology, some may thendecide to engage with it in a more profound way.

A smaller number of organizations may want to develop in-house capacity to build GISapplications to meet specialized business needs, especially industry leaders that want todevelop proprietary applications that place them out in front of their competition. Devel-oping in-house GIS capability to process and use automated spatial data in business appli-cations involves a greater level of institutional commitment and degree of organizationalchange than relying on external vendors for predeveloped applications. Of course, somecomponents of internal GIS application development may still require contracting for exter-nal GIS services, such as programming and developing Web-based applications.

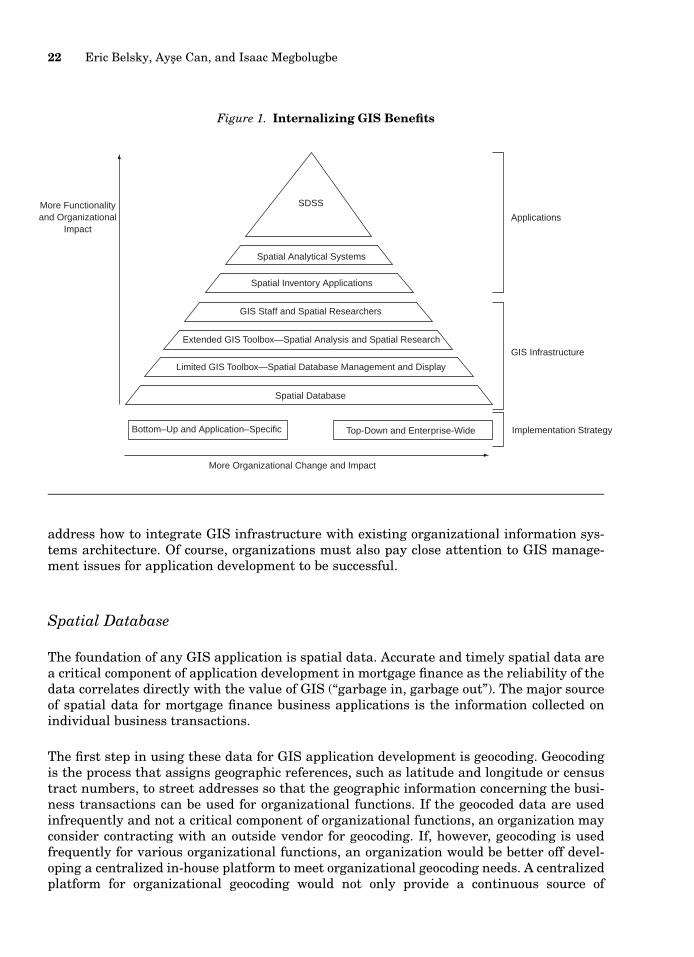

As shown in figure 1, the development of internal GIS business applications requires thatorganizations build an internal GIS infrastructure (i.e., spatial data, a GIS toolbox, GISstaff, and spatial researchers). Application development also requires that organizations

22 Eric Belsky, Ayse Can, and Isaac Megbolugbe

Figure 1. Internalizing GIS Benefits

More Functionalityand Organizational

Impact

SDSS

Spatial Analytical Systems

Spatial Inventory Applications

GIS Staff and Spatial Researchers

Extended GIS Toolbox—Spatial Analysis and Spatial Research

Spatial Database

Limited GIS Toolbox—Spatial Database Management and Display

More Organizational Change and Impact

Bottom–Up and Application–Specific Top-Down and Enterprise-Wide Implementation Strategy

GIS Infrastructure

Applications

address how to integrate GIS infrastructure with existing organizational information sys-tems architecture. Of course, organizations must also pay close attention to GIS manage-ment issues for application development to be successful.

Spatial Database

The foundation of any GIS application is spatial data. Accurate and timely spatial data area critical component of application development in mortgage finance as the reliability of thedata correlates directly with the value of GIS (‘‘garbage in, garbage out’’). The major sourceof spatial data for mortgage finance business applications is the information collected onindividual business transactions.

The first step in using these data for GIS application development is geocoding. Geocodingis the process that assigns geographic references, such as latitude and longitude or censustract numbers, to street addresses so that the geographic information concerning the busi-ness transactions can be used for organizational functions. If the geocoded data are usedinfrequently and not a critical component of organizational functions, an organization mayconsider contracting with an outside vendor for geocoding. If, however, geocoding is usedfrequently for various organizational functions, an organization would be better off devel-oping a centralized in-house platform to meet organizational geocoding needs. A centralizedplatform for organizational geocoding would not only provide a continuous source of

A Primer on Geographic Information Systems in Mortgage Finance 23

geocoded data for in-house GIS applications development but, more important, would ensureconsistency and integrity among various GIS applications (Can 1996).

For spatial data to add value to organizational productivity, the widespread benefits of thosedata must be realized. One emerging approach in the industry is spatial data warehousing.Spatial data warehousing is a product of the ever-increasing efforts by large corporations tointegrate many operational corporate systems into decision support systems to take advan-tage of information that resides in multiple systems. A data warehouse can help corporationsuse spatial data more broadly. Because of the volume and complexity of spatial data, how-ever, it is essential that corporations employ appropriate technologies for spatial data ware-housing (Kilty 1997)

Configuring the GIS Toolbox: Building GIS Functionality

Organizations must configure a GIS toolbox that meets the functional requirements of ap-plications they want to develop. GIS business applications vary in their level of complexityand resulting GIS functionality. Crain and MacDonald (1984) distinguish among inventory,analytical, and management applications. The primary use of GIS in many organizations isspatial inventory applications including assembling, organizing, and displaying spatial dataand undertaking simple spatial and data queries. Simple spatial inventory applications canoften be created easily using the standard GIS toolbox included in commercial GIS software.Some desktop mapping systems may also be a viable option for spatial inventory applica-tions. Recent advances in information technology allow the integration of some GIS func-tionality with low-priced desktop mapping systems that are exploding in the mainstreambusiness market (Thoen 1998).

For some organizations, decisions about the GIS toolbox will end here because they will havefound a software package that meets all their needs. Many, though, will want an extendedGIS toolbox to develop spatial analytical applications to address specific business needs. Themost feasible approach to development of an extended GIS toolbox is to acquire existingcommercial GIS software that offers the analytical functionality for spatial database man-agement and map support. This would also be the most flexible approach because somehighly specialized GIS applications in mortgage finance, especially those for marketing andregulatory compliance, can be built around the standard GIS functionality of commercialGIS software.

Other applications that require augmenting the standard functionality with more sophis-ticated spatial analytical tools can be developed in any combination of the following threeways. The first involves the use of programming tools that are now increasingly availablein commercial packages such as the scripting languages (e.g., Avenue and AML [Arc Macrolanguage] from ESRI and MapBasic from MapInfo). Second, several stand-alone GIS func-tions are offered in Visual Basic (e.g., MapObjects from ESRI). Third, if application devel-opment requires advanced statistical and spatial analytical methods, a statistical/econo-metric package can be used in conjunction with GIS (see Anselin 1998 for a detaileddiscussion). There are a number of good packages for advanced spatial analysis, such asSpaceStat and S-Plus for spatial statistical analysis and modeling.

24 Eric Belsky, Ayse Can, and Isaac Megbolugbe

At the highest level of complexity, organizations may use GIS to support the activities ofdecision makers. This can be achieved by building SDSSs to handle spatial modeling andanalysis (Densham 1991; Peterson 1998). SDSSs use sophisticated spatial analytical andmodeling and allow users interactively to experiment with and evaluate alternative solu-tions to often semistructured problems. To build an SDSS, organizations must go the addi-tional step of bringing a decision-logic structure to business problems. Models must be builtto emulate that structure creating a ‘‘model base’’ composed of models and model buildingblocks, a ‘‘model base management system,’’ and a ‘‘dialogue management system’’ (userinterface) that allows decision makers to interact with spatial data through displays andreports (Sprague 1980).7 Tools such as fourth-generation languages and spreadsheets canbe used with relative ease as ‘‘SDSS generators’’ to develop applications to address manyproblems using a limited set of model building blocks.

All organizations must hire expert staff or consultants to help them select the appropriatelevel of GIS functionality for their needs.

Integrating GIS Infrastructure: Computer Platform and Network Environment

It is important to emphasize the additional demands typical GIS applications place on anenterprise’s computer platform due to the spatial nature of geographic data. A typical GISapplication is interactive (the user interacts with the computing system); multiuser (manyusers must be able to access the geographical database simultaneously); graphic (the systemmust be able to input and output data graphically); and requires storage systems capableof processing large volumes of data quickly to provide immediate answers to users’ queries(Goodchild 1991). Fortunately, steady technological advancements coupled with reductionsin cost for both hardware and software make it possible to meet these demands.

Most GIS software programs run on a standard personal computer (PC) (IBM PC, Mac PC)at the low end and on Unix workstations (SUN, IBM, HP, DEC, etc.) at the high end, witha local area network (LAN) or as a stand-alone environment. Both platforms, especially PCplatforms, are becoming more affordable. Although the PC environment has been importantin providing easy-to-use GIS systems for general users, the availability of Unix workstationswith multitasking operating systems has provided the much needed power and speed forGIS database management and subsequent application development and research.

Today, GIS application development is greatly benefiting from progress in computer networktechnology and services as well as the Internet. The client/server environment is especiallysuited for GIS applications. With a wide range of network software available for LAN en-vironments, it is now possible to develop an enterprise-wide interactive GIS application withboth software and databases served and shared by a LAN. By effectively distributing and

7 Sprague’s (1980) classic decision support system framework has been adapted for SDSSs by Densham (1991).Many others have developed approaches to thinking about the development of SDSSs including Armstrong andDensham (1990), Armstrong, Densham, and Rushton (1986), Beaumont (1991b), M. Clarke (1989), Densham andGoodchild (1989), Fedra and Reitsma (1989), and Peterson (1993).

A Primer on Geographic Information Systems in Mortgage Finance 25

Table 3. Model Organizational Chart for In-House GIS Application Developmentand Delivery

Information SystemsDepartment

Research and DevelopmentDepartment

Users

• Manage and maintaingeocoded database

• Manage and maintain GIShardware

• Manage applicationproduction

• Assist in applicationdevelopment

• Train end users• Support end users’

software

• Conduct spatial research• Assist in application

development• Use research software• Assist in user training

• Assist in applicationdevelopment

• Receive end user training• Use end user software

sharing a wide variety of spatial databases and software access across the network, a systemdesigner can make computer resources easier and more efficient to access. The result islower cost and increased efficiency of GIS application development and delivery.

Computer platform and network choices are heavily influenced by organizational issuesbecause the location of GIS infrastructure is driven by decisions about who in the organi-zation needs access to GIS infrastructure, what level of access they need, and how GIS-related functions will be placed in the organizational structure.

Operating an in-house GIS application development and migration function demands thatmanagement decide where to locate staff responsible for (1) spatial database creation andmaintenance, (2) GIS hardware support, (3) spatial research, (4) application development,(5) software application support, and (6) training and staff development. These functionscan be concentrated in a single department or distributed among many departments.

In table 3, we offer one application development and delivery model. In this model, spatialdatabase and GIS hardware management functions are centralized in the information ser-vices department; spatial research functions are centralized in the research and develop-ment department; training and staff development is handled by the information services ora human resource development department; and the remaining functions (application de-velopment and software support) are shared between information services, research, andany departments expected to make heavy demands on GIS applications. For a detailed dis-cussion of management and organizational issues, see Somers (1998).

Conclusion

GIS has already made a contribution to several business functions in mortgage finance; ithas proven its worth for risk management, marketing, and regulatory compliance. Research

26 Eric Belsky, Ayse Can, and Isaac Megbolugbe

that will bring even more profound uses for GIS technology to mortgage finance is alsoprogressing.

One particularly important research development is the creation and testing in a GIS en-vironment of algorithms that emulate the sales comparison and cost approaches to appraisal(Can and Megbolugbe 1997). These algorithms and the data they operate on could soonrevolutionize and automate property valuation for underwriting, loan loss mitigation, es-tablishing loan loss reserves, meeting capital reserve requirements, and modeling creditrisk. The next most important frontier that researchers will explore with GIS technology ismodeling default, loan loss, and prepayment probabilities at the local level. At first, thisresearch will likely use local house price change and volatility as simple proxies for theunderlying complexity of local housing and mortgage market dynamics. Future GIS re-search, however, will strengthen credit and prepayment risk models by decomposing thefactors that affect not only local house price change but also turnover in the labor marketand access to employment opportunities. This will help predict the probability of occurrenceof negative net equity among borrowers at the local level and the resulting prepaymentprobability.

Despite the clear benefits of GIS technology, many in the industry have been slow to takeadvantage of it. That is beginning to change, however, as more learn about and see firsthandthe benefits of GIS for their operations. Most organizations that decide to take advantageof GIS will probably continue to rely on external vendors for applications and support. Asmore of them gain experience with GIS, though, more will consider making the management,analysis, and display of geographic information an integral part of their business.

A number of lessons have been learned by organizations in other industries that have de-veloped in-house GIS capability. A. L. Clarke (1991) reviews two studies that examinedcommon pitfalls and key elements to success in internalizing GIS infrastructure (Depart-ment of the Environment 1987; Tomlinson 1987). Those studies found that the major factorsinhibiting success were plans that were overly ambitious from the start, user needs thatwere either poorly defined or poorly understand by systems and application developers,conservatism of users, overly optimistic cost estimates, and insufficient commitment of re-sources to get the job done. The study by the Department of the Environment in the UnitedKingdom also found that the introduction of GIS is most successful when executives, seniormanagement, and GIS team members are committed to it; the organization has experienceworking in a multidisciplinary and cooperative way; geographic information is essential tobusiness operations; management has experience with automated information systems; andthe organization can afford to experiment with different systems before settling on one.Somers (1998) stresses the importance of formulating a clear strategic vision about whatrole GIS will play in the organization and educating and training senior management andusers about GIS and geographic information throughout the process. Landis (1993) empha-sizes the importance of adapting GIS as much as possible to an organization’s corporateinformation culture and demonstrating the business value of GIS technology with a cost-benefit analysis before investment decisions are made. Companies in the mortgage financeindustry that intend to develop an in-house GIS capability can learn from these lessons andbenefit from this advice.

A Primer on Geographic Information Systems in Mortgage Finance 27

References

Aalberts, Robert J., and Douglas S. Bible. 1992. Geographic Information Systems: Applications for theStudy of Real Estate. Appraisal Journal 60(4):483–92.

American Institute of Real Estate Appraisers. 1987. The Appraisal of Real Estate. 9th ed. Chicago.

Anselin, Luc. 1988. Spatial Econometrics, Methods and Models. Dordrecht: Kluwer Academic.

Anselin, Luc. 1998. GIS Research Infrastructure for Spatial Analysis of Real Estate Markets. Journalof Housing Research 9(1):113–33.

Anselin, Luc, and Arthur Getis. 1992. Spatial Statistical Analysis and Geographic Information Sys-tems. Annual of Regional Science 26:19–33.

Armstrong Marc P., and Paul J. Densham. 1990. Database Organization Alternatives for Spatial De-cision Support Systems. International Journal of Geographical Information Systems 4:3–20.

Armstrong, Marc P., Paul J. Densham, and G. Rushton. 1986. Architecture for a Microcomputer-BasedDecision Support System. Proceedings of the 2nd International Symposium of Spatial Data Handling.Williamsville, NY: International Geographical Union.

Atkinson, Scott E., and Thomas D. Crocker. 1987. A Bayesian Approach to Assessing the Robustnessof Hedonic Property Value Studies. Journal of Applied Econometrics 2:27–45.

Beaumont, John R. 1991a. GIS and Market Analysis. In Geographical Information Systems: Principlesand Applications, ed. David J. Maguire, Michael F. Goodchild, and David W. Rhind, 139–51. London:Longman.

Beaumont, John R. 1991b. Spatial Decision Support Systems: Some Comments with Regard to TheirUse in Market Analysis. Environment and Planning A 23:311–17.

Birkin, Mark, and Graham Clarke. 1998. GIS, Geodemographics, and Spatial Modeling in the U.K.Financial Service Industry. Journal of Housing Research 9(1):87–111.

Borrego, Jacqueline. 1993. Beyond AM/FM: Using GIS to Forecast Customer Growth and More. GISin Business ’93 Conference Proceedings. Fort Collins, CO: GIS World.

Bryan, Nora Sherwood. 1993. Government and the Business of Data. In Profiting from a GeographicInformation System, ed. Gilbert H. Castle III, 257–74. Fort Collins, CO: GIS World.

Burrough, Peter A. 1986. Principles of Geographic Information Systems for Land ResourcesAssessment.Oxford, England: Clarendon.

Business Geographics. 1997. 1998 Buyers Guide. Fort Collins, CO: GIS World.

Can, Ayse. 1993. TIGER/Line Files in Teaching GIS. International Journal of Geographical Informa-tion Systems 7(6):561–72.

Can, Ayse. 1996. A Prototype Geocoding System for the Housing and Mortgage Finance Industry. Work-ing Report, Fannie Mae Foundation, Office of Housing Research.

Can, Ayse. 1998. GIS and Spatial Analysis of Housing and Mortgage Markets. Journal of HousingResearch 9(1):61–86.

28 Eric Belsky, Ayse Can, and Isaac Megbolugbe

Can, Ayse, and Isaac Megbolugbe. 1997. Spatial Dependence and House Price Index Construction.Journal of Real Estate Finance and Economics 14:203–22.

Canner, Glenn B., and Dolores S. Smith. 1992. Expanded HMDA Data on Residential Lending: OneYear Later. Federal Reserve Bulletin 78(11):801–24.

Carter, James R. 1989. On Defining the Geographic Information System. In Fundamentals of Geo-graphic Information Systems: A Compendium, ed. William J. Ripple, 3–7. Bethesda, MD: AmericanSociety for Photogrammetry and Remote Sensing and American Congress on Surveying and Mapping.

Case, Bradford, Henry O. Pollakowski, and Susan M. Wachter. 1991. On Choosing among House PriceIndex Methodologies. AREUEA Journal 19(3):286–307.

Castle, Gilbert H., III. 1993. Real Estate. In Profiting from a Geographic Information System, ed.Gilbert H. Castle III, 85–104. Fort Collins, CO: GIS World.

Clark, Rodney E. 1993. Market Area Analysis: Using Geocoded Customer Data and Demographics toDetermine Branch Market Areas. GIS in Business ’93 Conference Proceedings. Fort Collins, CO: GISWorld.

Clarke, A. L. 1991. GIS Specification, Evaluation, and Implementation. Proceedings of GeographicInformation Systems Workshop.

Clarke, M. 1989. Geographical Information Systems and Model Based Analysis: Towards EffectiveDecision Support Systems. Proceedings of the GIS Summer Institute. Amsterdam: Kluwer.

Cooke, Donald F. 1993. Spatial Data for Business. In Profiting from a Geographic Information System,ed. Gilbert H. Castle III, 211–30. Fort Collins, CO: GIS World.

Crain, I. K., and C. L. MacDonald. 1984. From Land Inventory to Land Management. Cartographica21:40–46.