Embed Size (px)

Citation preview

A Perspective on Deals in 2014

26th Annual Tulane Corporate Law Institute

Goldman, Sachs & Co.

March 2014

2

This presentation has been prepared by the Investment Banking Division of Goldman Sachs and is not a product of Goldman Sachs Global Investment Research. It should not be used as a basis for trading in the securities or loans of any companies named herein or for any other investment decision. This presentation does not constitute an offer to sell the securities or loans of any companies named herein or a solicitation of proxies or votes and should not be construed as consisting of investment advice.

This presentation has been prepared and is based on information obtained by us from publicly available sources. In preparing this presentation, we have applied certain assumptions, have performed no due diligence, and have relied upon and assumed, without assuming any responsibility for independent verification, the accuracy and completeness of all financial, legal, regulatory, tax, accounting and other information provided to, discussed with or reviewed by us. We assume no liability for any such information. This presentation is necessarily based on economic, monetary, market and other conditions as in effect on, and the information made available to us as of, the dates indicated herein and we assume no responsibility for updating or revising this presentation. Goldman Sachs does not provide accounting, tax, or legal advice.

3

Agenda

I. The Backdrop

II. Is the Market Getting Better?

III. Okay, But We’ve Seen This Before…

IV. Why? What Has Changed?

V. Is the Recovery Durable?

The Backdrop

5

$1,999

$2,432$2,519 $2,549

$2,409

2009 2010 2011 2012 2013

Glo

bal

M&

A V

olu

me

($b

n)

Global M&A Volumes Have Not Grown Since the Financial Crisis…

Source: Thomson Reuters

CAGR (2010-2013)

= (0.3)%

CAGR(2009-2013)

= 4.8%

6

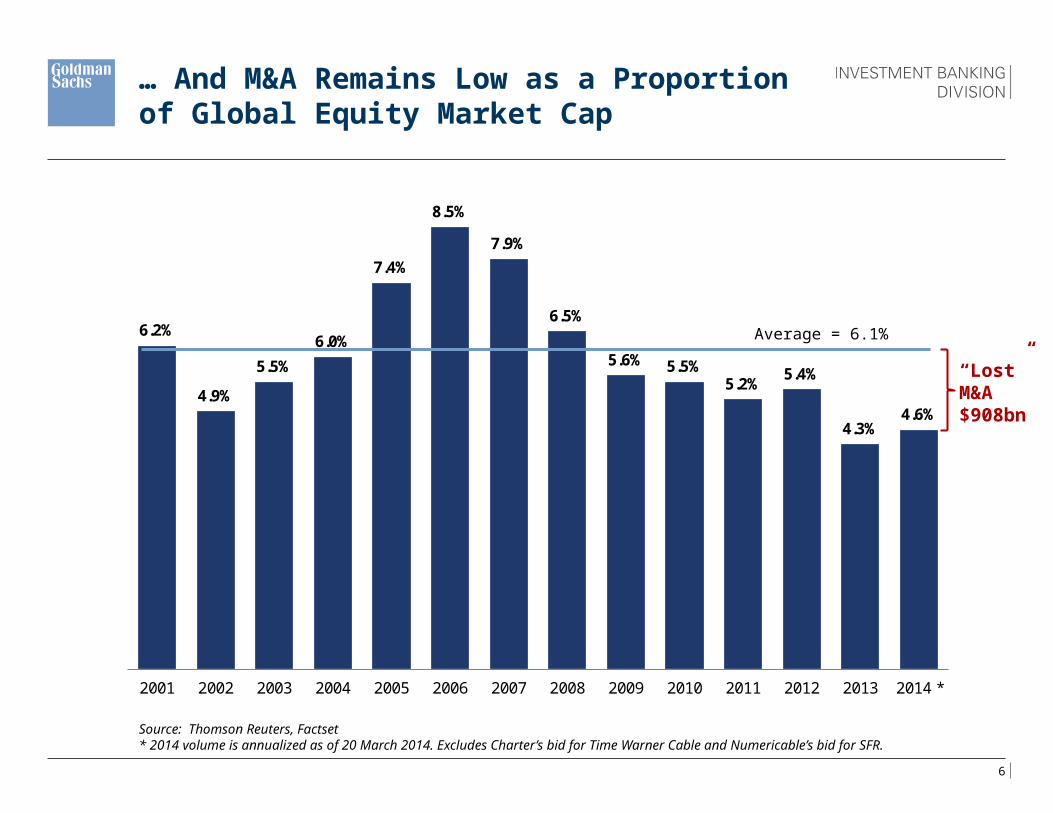

6.2%

4.9%

5.5%

6.0%

7.4%

8.5%

7.9%

6.5%

5.6% 5.5%5.2%

5.4%

4.3%4.6%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 *

… And M&A Remains Low as a Proportion of Global Equity Market Cap

Source: Thomson Reuters, Factset* 2014 volume is annualized as of 20 March 2014. Excludes Charter’s bid for Time Warner Cable and Numericable’s bid for SFR.

“Lost” M&A $908bn

Average = 6.1%

7

2009 2010 2011 2012 2013

$754 $787 $964 $933 $1,042

$618 $716

$751 $846 $641

$626

$929 $805 $770

$726 $1,999

$2,432 $2,519 $2,549

$2,409

US M&A Volume EMEA Rest of World

An

no

un

ce

d M

&A

Vo

lum

e (

$b

n)

U.S. M&A Has Been the Biggest Contributor to Volume and Growth…

Source: Thomson Reuters

2009-2013 CAGR

3.7%

0.9%

8.4%

8

… Driven By a Faster Recovery of U.S. GDP and Strong Fixed Investment…

% Change in GDP (YoY)

% Change in Fixed Investment (YoY)

Source: GS Research; Region Aggregate Nominal GDP (PPP) Weighted

2009 2010 2011 2012 2013 2014 2015E(5.0)%(4.0)%(3.0)%(2.0)%(1.0)%0.0 %1.0 %2.0 %3.0 %4.0 %

(2.8)%

2.5 %1.8 %

2.8 %1.9 %

2.8 %3.2 %

(4.2)%

2.0 %1.7 %

(0.3)%

0.1 %

1.6 % 1.8 %

2009 2010 2011 2012 2013 2014 2015E(20.0)%

(15.0)%

(10.0)%

(5.0)%

0.0 %

5.0 %

10.0 %

(16.7)%

1.5 %

6.2 %8.3 %

4.3 %6.4 % 7.9 %

(12.5)%

0.1 % 1.6 %

(2.7)% (2.3)%

2.7 % 2.9 %

USA Europe

9

European Corporates Still Rely Heavily on Bank Funding

France Portugal Germany Italy Greece Spain US0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

90 %

100 %

Bond-Market Funding Bank Loans

10

… And European Banks Are Still in Recovery Mode

Source: Bloomberg

Nov-2009 Jul-2010 Apr-2011 Jan-2012 Oct-2012 Jun-2013 Mar-201440%

60%

80%

100%

120%

140%

160%

180% S&P 500 Banks Index Stoxx Europe 600 Banks

Daily from 02-Nov-2009 to 24-Mar-2014

Ind

exed

Pri

ce

79.1%

(2.5)%

11

Cross-Border M&A Has Been a Remarkably Stable Contributor to M&A Activity

Strategic Cross-Border M&A Cross-Border M&A by Industry – 2009-2014 YTD

Cross-Border M&A by Industry – 2013-2014 YTD

Source: Thomson Reuters. 2014 YTD as of 20 March 2014. Total volume excludes Charter’s bid for Time Warner Cable and Numericable’s bid for SFR. Analysis is for deals >$250 million.

* 2014 volume is annualized as of run rate on 20 March 2014.

Natural Resources

32%

Technology, Media & Telecom

17%

Industrial14%

Consumer Retail13%

Financial Institutions10%

Healthcare9%

Real Estate5%

Technology, Media & Telecom

22%

Natural Resources

21%

Industrial15%

Consumer Retail12%

Healthcare12%

Financial Institutions

9%

Real Estate8%

53%

60% 64%66%

64%

84%47%

40%36%

34%

36%

16%

25%

35%

31% 33%

28%

33%

2009 2010 2011 2012 2013 2014*

% o

f T

ota

l M&

A

An

no

un

ced

M&

A V

olu

me

($b

n)

Cross-Region Intra-Region % of Total M&A

$404

$693

$638

$686

$551

$765

12

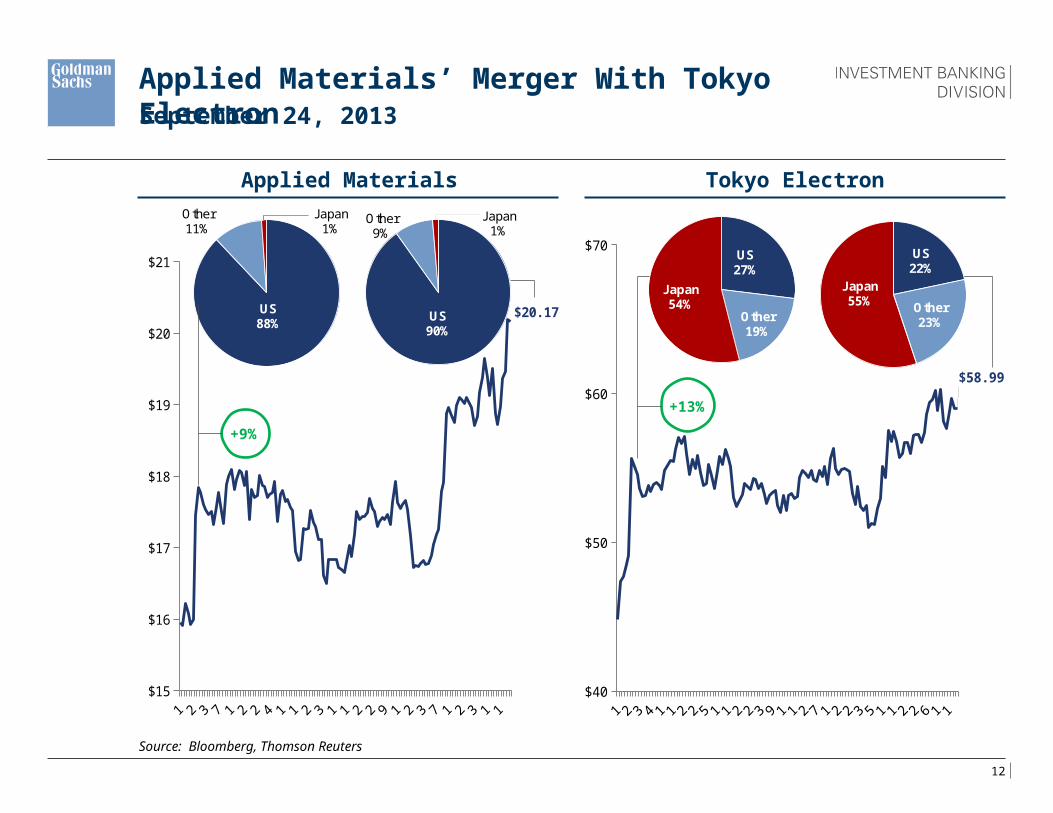

US27%

Other19%

Japan54%

Sep-2013 Dec-2013 Mar-2014$40

$50

$60

$70

$58.99

US22%

Other23%

Japan55%

Sep-2013 Dec-2013 Mar-2014$15

$16

$17

$18

$19

$20

$21

$20.17

Applied Materials’ Merger With Tokyo Electron

Applied Materials Tokyo Electron

Source: Bloomberg, Thomson Reuters

+9%

+13%

US90%

Other9%

Japan1%

US88%

Other11%

Japan1%

September 24, 2013

13

M&A Mix by Industry

2009-2012 2013-2014 YTD

Source: Thomson Reuters. 2014 YTD as of 20 March 2014. Volume excludes Charter’s bid for Time Warner Cable and Numericable’s bid for SFR.

Natural Resources29%

Financial Institutions16%

Technology, Media & Telecom

16%

Industrial11%

Consumer Retail10%

Real Estate9%

Healthcare9%

Technology, Media & Telecom

26%

Natural Resources20%

Real Estate15%

Consumer Retail12%

Industrial10%

Financial Institutions

9%

Healthcare9%

TMT and Natural Resources Are Going Through Significant Structural Changes

14

While Broad Financial Sponsor Activity is Growing, “Pure” LBO Activity Remains at 5% of Volume

Financial Sponsors Activity (ex IPOs) LBO Activity

Source: Thomson Reuters. 2014 YTD as of 20 March 2014. Total volume excludes Charter’s bid for Time Warner Cable and Numericable’s bid for SFR.

34%

45%32%

21%

43%

36%

66%

55%68%

79%

57%

64%

2%

6% 6% 5%

7%

6%

2009 2010 2011 2012 2013 2014YTD

% o

f T

ota

l M&

A

An

no

un

ced

M&

A V

olu

me

($b

n)

Public Company Target Other % of Total M&A

$45

$134$140 $138

$176

$38

42%

35%

42%34%

48%

47%

14%

17%

15% 22%

16%

25%

44%

49%

43%44%

36%

28%

12%

20%

23%24%

25%26%

2009 2010 2011 2012 2013 2014YTD

% o

f T

ota

l M&

A

An

no

un

ced

M&

A V

olu

me

($b

n)

Sponsor as Seller Secondary Sponsor Sales

Sponsor as Buyer % of Total M&A

$231

$491

$576$604 $606

$170

15

Divestitures and Spin-Offs Are Almost Half of M&A Activity, Largely Driven by Activist Pressure…

Annual Divestiture Activity

Source: Thomson Reuters. 2014 YTD as of 20 March 2014. Total volume excludes Charter’s bid for Time Warner Cable and Numericable’s bid for SFR. * 2014 volume is annualized as of run rate on 20 March 2014.

Recent Significant Divestitures / Spin-offs

$683

$1,045

$913

$1,177

$1,063

$967

34%

43%

36%

46%44%

35%

2009 2010 2011 2012 2013 2014*

Div

est

itu

res

as

% o

f To

tal M

&A

Div

est

itu

re V

olu

me

($

bn

)

Divestitures % of Total M&A

16

… Which Has Intensified as Their Funding Has Grown

Source: HFR Global Hedge Fund Industry Report

$36.2

$46.8

$50.9

$65.5

$93.1

2009 2010 2011 2012 2013

AU

M (

$b

illi

on

)

17

Activism May Be the New Form of Hostile M&A

Source: Thomson Reuters, Factset. 2014 is annualized based on totals as of 20 March 2014.

2009 2010 2011 2012 2013 2014 Annualized-100%

0%

100%

200%

300%

400%

500%

600%

0%

163%

0%

565%

Global Hostile Volume ($bn) Activism Situations (#)

Ind

exed

Val

ue

18

… Although Deal Jump Activity Has Been Active

Source: Thomson Reuters

Year Target Initial Topping Jurisdiction IndustryAmt ($bn)

Winning Bidder

2014 Time Warner Cable Charter Communications Comcast Corp US Media $70.7 Pending

2012 Sprint Nextel Softbank DISH Network US Telecom 37.8 Initial

2013 DellSilver Lake, Management

Blackstone / Carl Icahn

US Technology 22.9 Initial

2014 SFR (Vivendi) Bouygues Telecom Numericable Gp Europe Telecom 18.1 Pending

2012 Clearwire Sprint Nextel DISH Network US Telecom 9.9 Initial

2013 Tele2 Russia Holding VTBA1 Investment / Investor Group

Europe Telecom 4.2 Initial

2013Commonwealth Ppty Office Fund

GPT DEXUS Ppty, CPPIB Australia Real Estate 3.5 Topping

2013 Rede Energia COPEL, Energisa Energisa Latin America Nat Res 2.0 Initial

2014 Amcol International Imerys Minerals Technologies US Nat Res 1.7 Topping

2013Block BC-10, Parque das Conchas

Sinochem BC-10 Petroleo Ltda Latin America Nat Res 1.5 Topping

2013 The Men’s Wearhouse Jos A Bank Clothiers N/A US Retail 1.5Pac-Man

Successful

Total $173.8

Bidders

Is the Market Getting Better?

20

$490

$647

$566

$847

$502 $525

$711$671

$599

Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14

Glo

bal

M&

A V

olu

me

($b

n)

$684*

M&A Volumes Have Improved over the Last Three Quarters…

* Estimated quarterly total for Q1 2014 based on volumes as of 20 March 2014.Source: Thomson Reuters. Global volume excludes Charter’s bid for Time Warner Cable and Numericable’s bid for SFR. 2014 YTD as of 20 March 2014.

21

…With 2014 M&A Volumes Outpacing the Same Period In the Prior Two Years…

Source: Thomson Reuters. 2014 as of March 20, 2014. Excludes Charter’s bid for Time Warner Cable and Numericable’s bid for SFR.

$429$457

$641

$420$439

$599

2009 YTD 2010 YTD 2011 YTD 2012 YTD 2013 YTD 2014 YTD

Glo

ba

l M&

A V

olu

me

($

bn

)

22

Global U.S. Only

Source: Thomson Reuters, as of March 25.* 2014 YTD volume excludes Charter’s bid for Time Warner Cable ($62.6 billion)** 2014 YTD volume excludes Numericable’s bid for SFR ($16.3 billion)

Significant Year on Year Gains 2013-2014

YTD

($ in billions) 2014 2013 % change y-o-y

Total M&A Volume *,** $623 $458 36 %

Strategic Cross-Border 223 107 108

Divestitures & Spinoffs ** 218 201 8

Hostile M&A 73 36 101

LBO 43 73 (41)

YTD

Number of Deals over: 2014 2013 % change y-o-y

$500mm *,** 208 155 34 %

$1bn *,** 111 82 35

$5bn *,** 16 7 129

$10bn *,** 8 4 100

YTD

($ in billions) 2014 2013 % change y-o-y

Total M&A Volume * $295 $223 32 %

Strategic Cross-Border 74 19 280

Divestitures & Spinoffs 75 81 (8)

Hostile M&A 69 28 148

LBO 30 60 (50)

YTD

Number of Deals over: 2014 2013 % change y-o-y

$500mm * 83 67 24 %

$1bn * 47 38 24

$5bn * 6 6 0

$10bn * 4 4 0

23

A Shift from Tactical M&A to Strategic M&A…

Source: Thomson Reuters

Technology, Media & Telecom

Consumer / Retail

Healthcare

Industrials

Acquiror Target Size ($bn)

Investor Group Dell $19.3

Verizon Communications

Verizon Wireless 130.3

Comcast NBC Universal 14.7

Investor Group HJ Heinz $27.3

Investor Group Neiman Marcus 6.0

Thermo Fisher Scientific

Life Technologies

$15.4

Valeant Pharmaceuticals

Bausch + Lomb 11.6

Fiat Chrysler $4.4

Koch Industries Molex 6.7

2013Financing / "Clean-Up" Transaction

Acquiror Target Size ($bn)

ComcastTime Warner Cable

$70.7

Facebook WhatsApp 19.5

Suntory Beam $15.7

AB Acquisitions Safeway 9.2

Actavis plc Forest Labs $23.3

McKesson Celesio 7.0

AMEC Foster Wheeler $2.8

Verso Paper NewPage 4.3

2014Strategic Transaction

24

52% 54% 59%

42% 42%

74%

27%29%

11%

24%

39%

10%1%

3%

2% 8%

2%5%

1%

8%

6% 2%

9% 5%

2%

5%

10%23%

5% 3%17% 13%

2% 2% 2%

2009 2010 2011 2012 2013 2014

% o

f $

Vo

lum

e o

f $1

bn

+ D

eals

Corporate / Corporate Divestiture - Corporate Buyer Divestiture - LBO BuyerPublic to Private Spinoff Other

… Which is A Marked Shift in Tone

Source: Thomson Reuters. U.S. targeted deals >$1 billion. Other includes negotiated share repurchases and rescues. Analysis for 2014 as of 20 March 2014.

25

Corporate Leaders are More Confident…

Source: Factset

Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 201340

45

50

55

60

65

CEO Confid...

Above 50 = Positive

Below 50 = Negative

26

…The Impact of Share Buybacks is Less Pronounced…

Note: Buyback yield is defined as shares repurchased divided by shares outstanding at the beginning of the period.Source: GS Research

2.2%

2.8%

0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

S&

P 5

00

Tra

ilin

g 1

2-m

on

th Y

ield

Dividend Yield

Buyback Yield

27

As Interest Rates Rise, Companies Are Accelerating M&A Projects

Source: Bloomberg and Thomson Reuters

Jan-1983 Jan-1987 Jan-1991 Jan-1995 Jan-1999 Jan-2003 Jan-2007 Jan-20110%

2%

4%

6%

8%

10%

12%

14%

16%

$0

$50

$100

$150

$200

$250

10Y US Treasury Rate US M&A Volume ($bn 3mo Moving Avg.)

10 Y

ear

US

Tre

asu

ry R

ate

(Co

nst

ant

Mat

uri

ty)

US

An

no

un

ced M

&A

Vo

lum

e ($bn

)

Okay, But We’ve Seen This Before…

… How Is the Market Different Today?

29

Series1

(1.3)%(1.9)%

0.3 % 0.3 %

1.8 %

3.1 %3.6 %

5.2 %

Ind

exed

Sto

ck

Pri

ce R

eacti

on

There Has Been A Demonstrable Shift Toward Shareholder Support of M&A…

One-Day Indexed Stock Price Reaction for Buyers

One-Week Indexed Stock Price Reaction for Buyers

Note: Stock Price reaction relative to the S&P 500. Deals with transaction value greater than $1,000mm with a US public acquiror.Source: Bloomberg, Thomson Reuters, Capital IQ

2008 2009 2010 2011 2012 2013 1H 2013 2H 2014 YTD

Series1

(1.7)% (1.7)%

(0.1)%

0.0 %

2.0 %

3.6 %4.1 %

4.7 %

Ind

exed

Sto

ck

Pri

ce R

eacti

on

2008 2009 2010 2011 2012 2013 1H 2013 2H 2014 YTD

30

…Which Started to Accelerate in Q3 2013…

Source: Bloomberg, Thomson Reuters, Capital IQ. Deals with transaction value greater than $1,000mm with a US public acquiror.

Proportion of Deals with Positive Acquiror One Day Stock Price Reactions

Series1

50.0 %

54.2 %

69.6 %

75.0 %73.3 %

Pro

po

rtio

n o

f D

ea

ls w

ith

Po

sit

ive

On

e D

ay

Sto

ck

Pri

ce

Re

ac

tio

ns

Q1 2013 Q2 2013 Q3 2013 Q4 2013 2014 YTD

31

…Driven by Investor Sentiment Regarding EPS Impact…

Source: Thomson Reuters, Company disclosure. Deals with transaction value greater than $1,000mm with a US public acquiror.¹ Includes deals announced as dilutive or accretive in years after FY1.² Deals that are announced as immediately accretive or accretive in FY1.

Dilutive Transactions1

2009-2010 2013-2014 YTD

Accretive Transactions2

2009-2010 2013-2014 YTD

Series1(6.0)%

(4.0)%

(2.0)%

0.0 %

2.0 %

4.0 %

6.0 %

-3.9

0.70.2 %

5.4 %

Ac

qu

iro

r S

toc

k P

ric

e R

ea

cti

on

On

e D

ay

P

os

t-A

nn

ou

nc

em

en

t

32

(40)% (30)% (20)% (10)% 0% 10% 20%

(15)%

(10)%

(5)%

0%

5%

10%

15%

Acquiror One Day Post Announcement Share Price Reaction

FY

2 A

cc

reti

on

…And Clear Evidence That Investors Believe in the Value of EPS Accretion Again…

2009-2010 2013-2014 YTD

Source: Thomson Reuters, IBES, Company’s disclosures. Deals with transaction value greater than $1,000mm with a US public acquiror.Notes: (1) FY2 accretion represents FY2 expected accretion disclosed by the acquiror when available, or is otherwise FY2 EPS IBES estimate immediately post close (or 6 months post announcement when close has not yet occurred) relative to FY2 EPS IBES estimate immediately pre-announcement.

R² = 0.1015

(30)% (20)% (10)% 0% 10% 20% 30% 40%

(10)%

(5)%

0%

5%

10%

15%

20%

25%

30%

Acquiror One Day Post Announcement Share Price Reaction

FY

2 A

cc

reti

on

R² = 0.428

33

Devon /GeoSouthern

Advance AutoParts

PackagingCorp / Boise

Actavis /Warner Chilcott

SalixPharmaceuticals

/ Santarus

Scientific GameCorp / WMSIndustries

0.0% 17.5% 35.0% 52.5% 70.0%

5.0%

16.6%

10.8%

1.3%

15.0%

5.5%

20.0%

20.0%

23.2%

30.0%

31.1%

108.3%

FY2 Accretion Acquiror Stock Price Reaction at Announcement

… Strong Projected Earnings Are Driving Stock Prices Higher…

Significant cost and tax synergies (96% of target’s EBITDA)

Strong strategic rationale, significant revenue synergies

Operational synergies and tax benefits totally more than $400mm (~30% of target’s EBITDA)

Strong consolidation rationale and significant synergies (~35% of target’s EBITDA)

Strategic rationale and significant synergies (~70% of target’s EBITDA)

Use of leverage to finance growth, market focus on execution of forward growth plans

Notes: (1) FY2 accretion represents FY2 expected accretion disclosed by the acquiror when available, or is otherwise FY2 EPS IBES estimate immediately post close (or 6 months post announcement when close has not yet occurred) relative to FY2 EPS IBES estimate immediately pre-announcement.

(2) Stock price reaction one day post announcement is relative to the undisturbed date.Source: Thomson Reuters, Capital IQ

Key Drivers

100.0% 120.0%

34

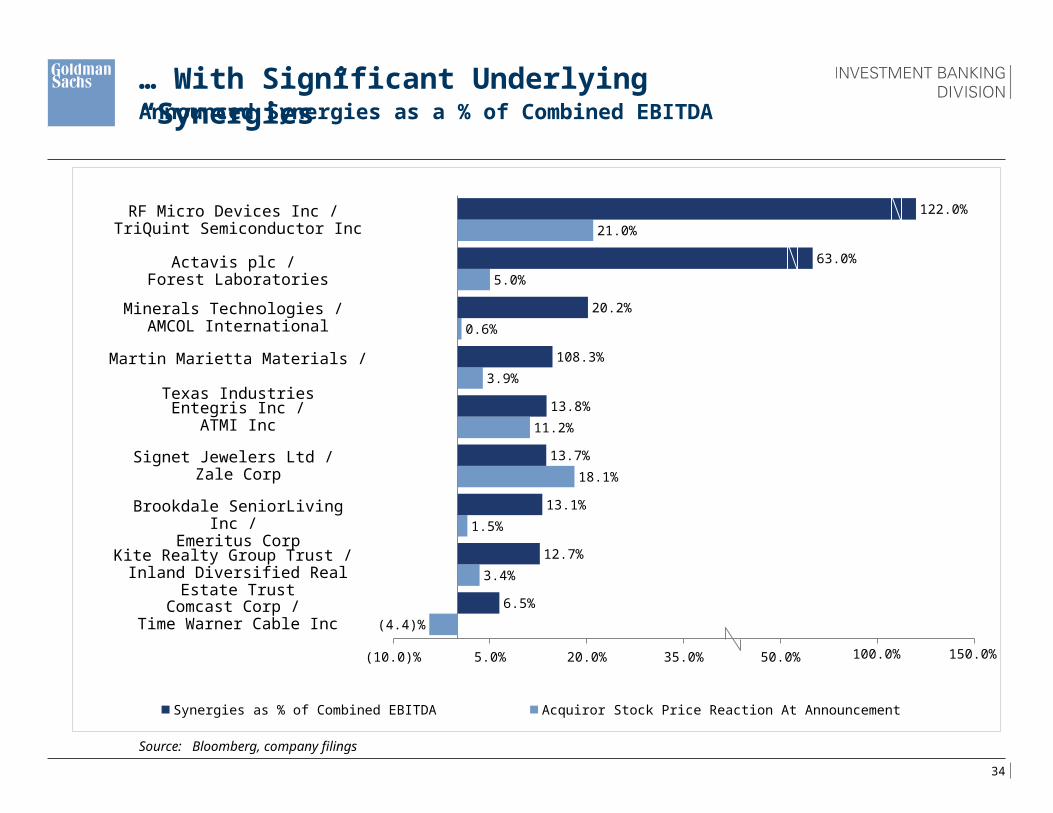

… With Significant Underlying “Synergies”Announced Synergies as a % of Combined EBITDA

Source: Bloomberg, company filings

(10.0)% 5.0% 20.0% 35.0% 50.0% 65.0% 80.0%

(4.4)%

3.4%

1.5%

18.1%

11.2%

3.9%

0.6%

5.0%

21.0%

6.5%

12.7%

13.1%

13.7%

13.8%

108.3%

20.2%

63.0%

122.0%

Synergies as % of Combined EBITDA Acquiror Stock Price Reaction At Announcement

100.0% 150.0%

RF Micro Devices Inc / TriQuint Semiconductor Inc

Actavis plc / Forest Laboratories

Minerals Technologies / AMCOL International

Martin Marietta Materials / Texas Industries

Entegris Inc /ATMI Inc

Signet Jewelers Ltd / Zale Corp

Brookdale SeniorLiving Inc / Emeritus Corp

Kite Realty Group Trust / Inland Diversified Real Estate Trust

Comcast Corp / Time Warner Cable Inc

35

18-Feb-2014 25-Feb-2014 4-Mar-2014$75

$80

$85

$90

$95

$100$99.04

Clo

sin

g P

ric

e (

US

D)

… Illustrated by Signet’s Acquisition of Zale…

Source: Bloomberg, company filings

41% premium Investors expect deal to be dilutive due to

the high premium Announces synergies of $100mm,

representing 143% of the target’s EBITDA

+18%

+25%

February 19, 2014

36

However, Reaction Has Varied by Sector…

Note: Includes deals from 2013 and 2014 YTD with a transaction value of $1,000mm or greater and a US public acquiror.Source: Capital IQ, Thomson Reuters

6.5% 6.3%

7.3%

6.4%

7.6%

9.3%

3.9%

5.1%5.4%

3.0% 3.0%

5.6%

2.0%

1.1%

2.7%

0.5% 0.7%

2.4%

(1.6)% (1.5)%

(2.3)%

(4.0)%

(2.0)%

-

2.0%

4.0%

6.0%

8.0%

10.0%

One Day One Week One Month

Acq

uir

or

Sto

ck P

ric

e R

eact

ion

Consumer Retail Industrials Healthcare TMT Real Estate Energy and Power Financials

37

10-Mar-2014 12-Mar-2014 14-Mar-2014 16-Mar-2014$21.1

$21.5

$22.0

$22.4

$22.8

$23.2

$23.6

$22.42

Ac

qu

iro

r C

los

ing

Pri

ce

(U

SD

)

And Investors Can Still Be CautiousEnergy XXI’s Acquisition of EPL Oil & Gas March 12, 2014

Source: Bloomberg, company filings

-7%

Energy XXI announces the acquisition of EPL Oil & Gas for $2.2 bn

Transaction was announced as additive to EPS Investors were expecting share repurchases

Why? What Has Changed?

… Positive Investor Sentiment Has Been the Missing Piece

39

4,401

4,279

4,171

4,102

4,180

3,950

4,000

4,050

4,100

4,150

4,200

4,250

4,300

4,350

4,400

4,450

2009 2010 2011 2012 2013

# o

f D

om

es

tic

Co

mp

an

ies

Lis

ted

on

NY

SE

an

d

Na

sd

aq

Source: World Federation of Exchanges

CAGR = (1.3)%

There Are Fewer Opportunities to Invest in the Public Markets…

40

… And There Are Record Inflows Into Equity Mutual Funds…

Source: Strategic Insight Simfunds

$(40)

$(149)

$ 44

$ 405

$ 462

$(200)

$(100)

$ 0

$ 100

$ 200

$ 300

$ 400

$ 500

2009 2010 2011 2012 2013

Ne

t N

ew

Flo

ws

($

bn

)

41

… Which Is Helping the US and European IPO Markets…

US IPOs Year to Date

US IPOs by Industry (2013-2014 YTD)

European IPOs Year to Date

European IPOs by Industry (2013-2014 YTD)

Source: Dealogic and Thomson Reuters; YTD as of March 19. Industry mix based on dollar volume.

$3.5

$6.8$8.627 25

45

0

10

20

30

40

50

0

2

4

6

8

10

12

14

16

2012 YTD 2013 YTD 2014 YTD

# o

f IP

Os

$ V

ol

($b

n)

Deal Value ($bn) # of Deals

$0.7

$3.1

$13.7

1915

30

0

10

20

30

40

50

0

2

4

6

8

10

12

14

16

2012 YTD 2013 YTD 2014 YTD

# o

f IP

Os

$ V

ol

($b

n)

Deal Value ($bn) # of Deals

CRG, 4 %

FIG, 48 %

HC, 10 %IND, 5 %

NR, 14 %

RE, 8 %

TMT, 11 %

CRG, 7 %

FIG, 32 %

HC, 0 %

IND, 23 %

NR, 11%

RE, 13 %

TMT, 14 %

42

$(197.8)

$(316.9)

$(111.1)

$ 180.0 $ 173.6

$(0.1)

$(350.0)

$(250.0)

$(150.0)

$(50.0)

$ 50.0

$ 150.0

$ 250.0

$ 350.0

2009 2010 2011 2012 2013 2014 YTD

Investors Are Turning to “Active” Funds Again…

Flows to Passive Funds ($bn)

Flows to Active Funds ($bn)

Source: Strategic Insight Simfunds, 2014 YTD as of Feb-14

$ 157.6 $ 168.1 $ 155.2 $ 225.2

$ 288.7

$ 46.5

$(350.0)

$(250.0)

$(150.0)

$(50.0)

$ 50.0

$ 150.0

$ 250.0

$ 350.0

2009 2010 2011 2012 2013 2014 YTD

43

… And “Active” Fund Managers Need to Create Alpha and Generate Superior Returns

Cumulative Average Returns to Passive Funds (%)

Cumulative Average Returns to Active Funds (%)

Note: Returns are net of feesSource: Strategic Insight Simfunds

2009 2010 2011 2012 2013 2014 YTD(5.0)%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0% 28.5%

13.3%

(4.9)%

12.3%

18.5%

1.4%

2009 2010 2011 2012 2013 2014 YTD(5.0)%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0% 26.8%

12.3%

(1.5)%

11.5%15.3%

1.6%

44

Which is Driving Some Investors Into Deal Stocks to Create Alpha…

Source: Thomson Reuters, Bloomberg, Deals with transaction value of $2,000mm or greater, with a US public acquiror.

At Announcement

3.5x

5.4x5.7x

6.4x

2010 2011 2013 2014 YTD

Mu

ltip

le t

o A

cqu

iro

r P

re-A

nn

ou

nce

men

t 3

Mo

nth

A

DT

V

45

… And Some Targets To Trade Through Offer Prices...Acquiror One Week Gross Arbitrage Spread

Source: Thomson Reuters, Capital IQ

0.2%

0.3%

0.3%

2.6%

3.2%

5.8%

8.4%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0%

Zale / Signet Jewelers

Santarus / Salix Pharmaceuticals

CEC Entertainment / Apollo Global Management

ArthroCare Corp / Smith & Nephew

Celesio AG / McKesson Corp

Sirius XM / Liberty Media

AMCOL International / Minerals Technologies

Acquiror One Week Gross Arbitrage Spread

46

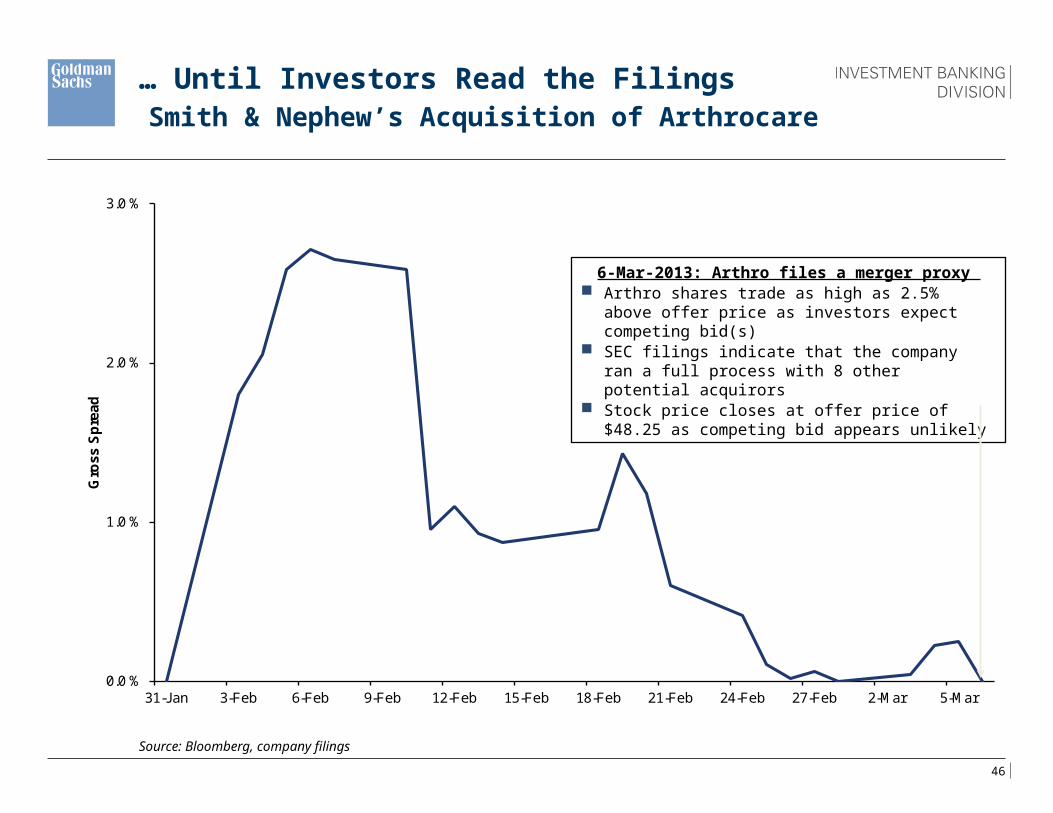

Source: Bloomberg, company filings

0.0 %

1.0 %

2.0 %

3.0 %

31-Jan 3-Feb 6-Feb 9-Feb 12-Feb 15-Feb 18-Feb 21-Feb 24-Feb 27-Feb 2-Mar 5-Mar

Gro

ss S

pre

ad

6-Mar-2013: Arthro files a merger proxy Arthro shares trade as high as 2.5% above offer price

as investors expect competing bid(s) SEC filings indicate that the company ran a full process

with 8 other potential acquirors Stock price closes at offer price of $48.25 as

competing bid appears unlikely

… Until Investors Read the FilingsSmith & Nephew’s Acquisition of Arthrocare

Is the Recovery Durable?

48

Investors Are Strongly Encouraging Companies to Invest and Grow to Fill the Growth Gap

Source: Bloomberg

66%

46%

14%

(10)%

0%

10%

20%

30%

40%

50%

60%

70%

Sep-11 Feb-12 Jun-12 Oct-12 Feb-13 Jun-13 Oct-13 Mar-14

Cu

mu

lati

ve G

row

th S

ince

30-S

ep-2

011

S&P 500 Increase FY1 PE Increase Earnings Increase

PE MultipleExpansion

49

2013 Global M&A Additional M&A Volume if USReturns to 10-year Average of

Market Cap

Additional M&A Volume if Asia &Europe Return to 10-year Average

Proportion to US Volume

2013 + "Return to Normal"

2407

$253

655

$3,315

An

no

un

ce

d M

&A

Vo

lum

e (

$b

n)

What if M&A Activity Approached Historic Levels of Relative Volumes?

Source: Thomson Reuters and FactSet

+11%

+27%

+38%

50

Shuanghui Intl / Smithfield Foods

Glencore Intl / Xstrata

CITIC / AsiaInfo-Linkage

AT&T / T-Mobile

United Parcel Service / TNT Express

Deutsche Borse / NYSE Euronext

Anheuser-Busch InBev / Grupo Modelo

AMR Corp / US Airways

Silver Lake / Dell

McKesson / Celesio

Boise / PCA

Shanghui Intl / Smithfield Foods

Coca-Cola / China Huiyuan Juice

BHP Billiton / Potash Corp

BAE Systems / EADS

Shareholders

GovernmentRegulators

But… There Are Plenty of Headwinds

51

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1985 1989 1993 1997 2001 2005 2009 2013

Glo

ba

l M&

A V

olu

me

($

bn

)

The Long Term View of M&A Market is Volatile… But Upward Trending

Source: Thomson Reuters

CAGR 9%