Embed Size (px)

Citation preview

Dave CollyerPresident, Canadian Association of Petroleum Producers

A Perspective on Canada’s Upstream Oil & Gas Sector

2010 Edmonton Real Estate Forum – May 4, 2010

Presentation Outline

• Current business environment

• Industry activity overview

• Natural gas business outlook

• Crude oil business outlook

• CAPP Priorities

• Summary

Business Environment

Global Energy Outlook

• Significant energy demand growth:

Population, standards of living

• Need all forms of energy:Increasing role for renewablesContinuing reliance on hydrocarbons (predominant energy supply source)Increasing role for non-conventional crude oil & natural gas

• Environmental challenges• Technology is a key lever

for sustainable growth

World Energy Demand 1990 - 2030EIA – International Energy Outlook 2009

0

100

200

300

400

500

600

700

800

1990 2005 2006 2010 2015 2020 2025 2030

Other Nuclear Coal Natural Gas Liquids

Quadrillion BTU

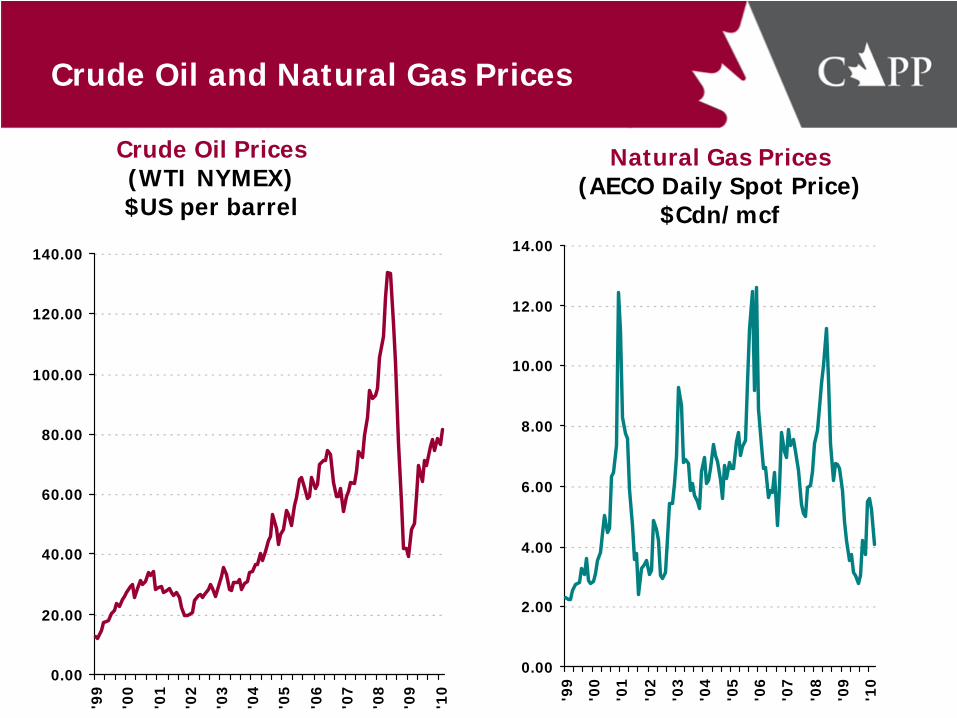

Crude Oil and Natural Gas Prices

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

'99

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

'99

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

Crude Oil Prices (WTI NYMEX)$US per barrel

Natural Gas Prices (AECO Daily Spot Price)

$Cdn/mcf

Payments to Governments by Upstream Oil and Gas Sector

0

5

10

15

20

25

30

35

2005 2006 2007 2008 2009E

Billi

on d

olla

rs

Municipal TaxesBonus & RentalsProvincial Income TaxesFederal Income TaxesCrown Royalties

Industry Activity Overview

Western Canadian Land Sales: Year-to-Date Bonus Bids

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Alberta British Columbia Saskatchewan

$ bi

llion

s

2007 2008 2009 2010

Total Wells Drilled in Western Canada

0

4,000

8,000

12,000

16,000

20,000

24,000

28,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009E 2010F

Dry/Susp.GasOil

Source – CAPP. Based on Rig Release

2007 = 18,000

2008 = 16,100

2009F = 8,000

2010F= 10,500

2008 2009F 2010F

Alberta 11,150 5,570 7,300

British Columbia

800 625 750

Saskatchewan 3,870 1,580 2,175

Manitoba 300 225 275

• Oil wells ~40% of total completions

• Previous high in last ten years was 2001 @ 30%

Industry Capital Spending Cdn $billions

Northern Canada

‘08 `09E ‘10F

$0.4 $0.5 $0.5

Oil Sands

‘08 `09E ‘10F

$18 $11 $13

WCSB

‘08 `09E ‘10F $34 $22 $26

East Coast Offshore

`08 `09E ‘10F

$1.3 $1.5 $2.5

Note: Spending in Canada excludes spending associated with mergers & acquisitions

Oil & Gas Investment Spending:2008: $54 billion2009: $35 billion (estimate)2010: $42 billion (forecast)

AB $21 $13 $15 BC $7.9 $6 $7SK $4.8 $3 $4

`08 `09E ‘10F

Capital Investment in Alberta

0

10

20

30

40

50

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009est.

2010frcst.

Oil SandsConventional

$ bi

llion

s

Opportunities in Alberta

• Crude Oil“Unconventional” oil - tight oil resourcesEnhanced oil recovery in mature fields - CO2, polymer

• Oil SandsGlobal scale and global focusMining and drillable

• Natural GasConventional natural gas remains important“Unconventional” natural gas - shale gas, coal bed methane

Why is it Important?

• Benefits to Albertans of investment by the oil and gas industry:

……..$1 in investment generates $3 in value creation for Albertans

AttractCapital

Jobs

InvestmentNew Businesses

Taxes andRoyalties

IncreasesStandardof Living

Natural Gas

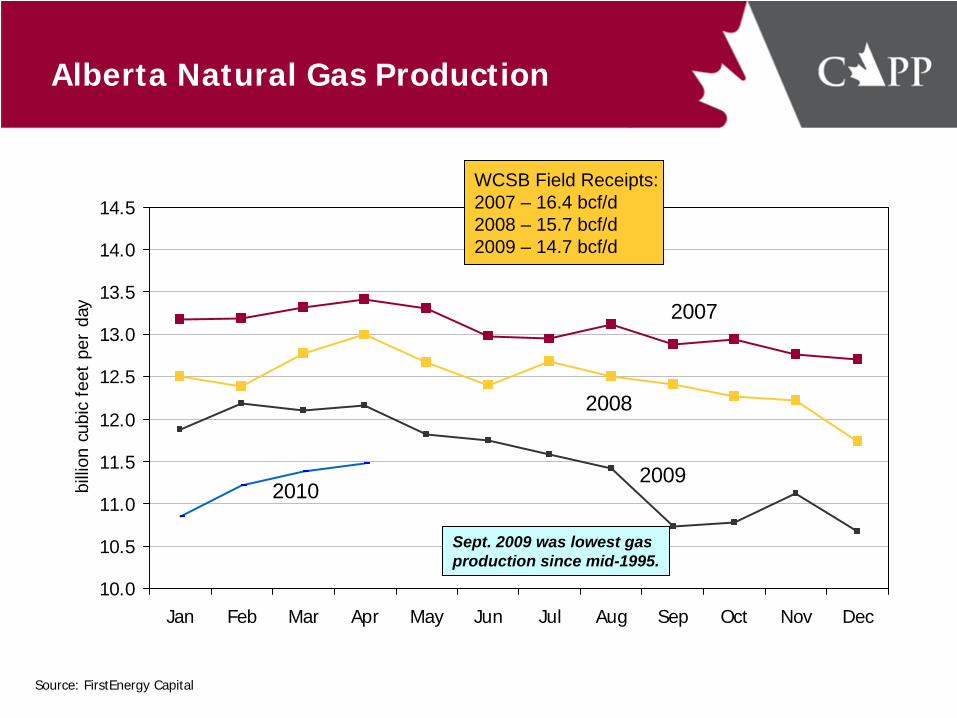

Alberta Natural Gas Production

10.0

10.5

11.0

11.5

12.0

12.5

13.0

13.5

14.0

14.5

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

billi

on c

ubic

fee

t pe

r da

y

Source: FirstEnergy Capital

2008

2007

20092010

WCSB Field Receipts: 2007 – 16.4 bcf/d2008 – 15.7 bcf/d2009 – 14.7 bcf/d

Sept. 2009 was lowest gas production since mid-1995.

N.A. Natural Gas Supply Outlook

• Shale gas supply a game- changer

• Technology breakthroughs

• New producing regions

• Emerging stakeholder environmental concerns (footprint, water)

• Shifting S/D dynamic

Western Canada – Resource Plays

Source: TransCanada

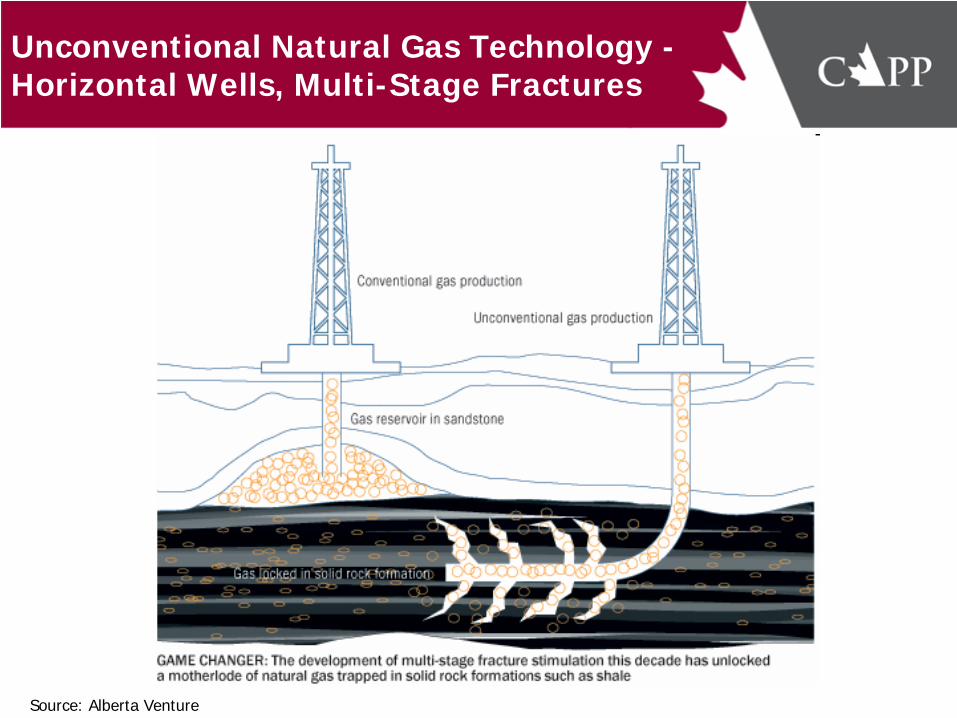

Unconventional Natural Gas Technology - Horizontal Wells, Multi-Stage Fractures

Source: Alberta Venture

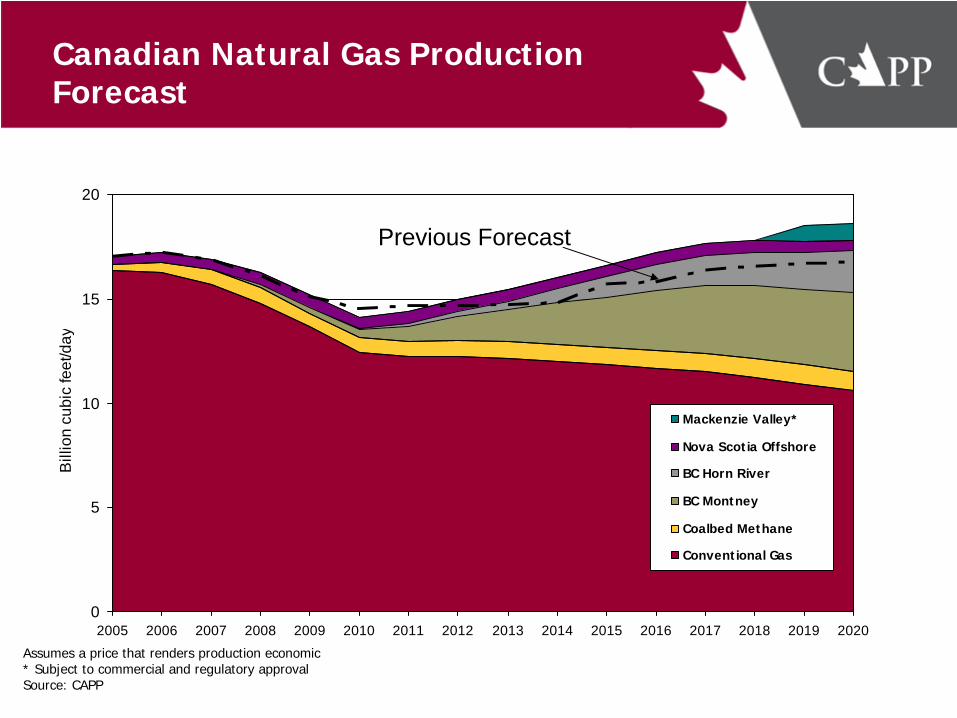

Canadian Natural Gas Production Forecast

0

5

10

15

20

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Bill

ion

cubi

c fe

et/d

ay

Mackenzie Valley*

Nova Scotia Offshore

BC Horn River

BC Montney

Coalbed Methane

Conventional Gas

Assumes a price that renders production economic* Subject to commercial and regulatory approvalSource: CAPP

Previous Forecast

Implications & CAPP Response

• ImplicationsEmerging supply and demand imbalance in North AmericaPressure on competitiveness and basin economics in Western CanadaPipeline utilization issues: lower volume = higher tollAvailability of new infrastructure: right place, right timeIncreasing focus on offshore exports

• CAPP ResponseA key driver in the Alberta Competitiveness ReviewProactive efforts on pipeline settlements and ratesOngoing focus on alignment of supply and pipeline capacity….increasing focus on offshore markets Canadian Natural Gas Initiative

Crude Oil

Global Crude Oil Reserves by Country

Source: Oil & Gas Journal Dec. 2008

21303644

60

9299102

115

136

175

264

0

50

100

150

200

250

300

Saudi Arabia Canada Iran Iraq Kuwait VenezuelaAbu Dhabi Russia Libya Nigeria Kazhakhstan UnitedStates

billi

on b

arre

ls

Includes 170 billi

on barrels

of oil s

ands reserves

OtherAccessibleReserves

State ownedor controlled

Accessible

Canada’sOil Sands

World OilReserves

OtherAccessibleReserves

53%

47%

AccessibleOil Reserves

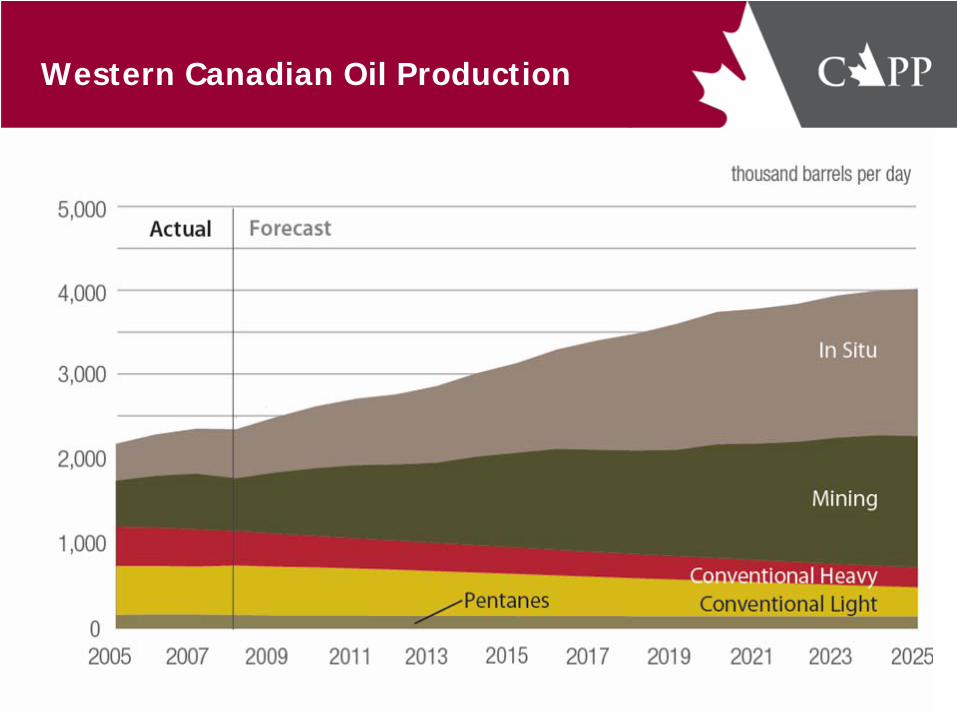

Canadian Crude Oil Production Outlook

Total Canadian Oil Production

Western Canadian Oil Production

Oil Sands GHG Emissions In Context

Oil Sands Communications

• Information/EducationEnglish, French, Norwegian, and GermanInformation on environment, economics and energyReal examples of technology

• Websiteswww.capp.cawww.canadasoilsands.ca

• Social MediaFacebook, Twitter

• Come See For Yourself videosWebsiteYoutube

Short Term Outlook for Crude Oil

• The Opportunity:Improving economy reviving projects - stronger oil prices and lower costsProjects under construction:

• Imperial Kearl Lake• Shell Jackpine and Shell Upgrader (including Quest CCS project)

Projects re-activated:• Suncor Firebag Phases 3 and 4• Devon Jackfish Phase 3 application in 2010• Cenovus Christina Lake – application for phases E, F, G• ConocoPhillips/Total – Surmount phase 2• Husky/BP – Sunrise phase 1

Oil sands attracting foreign investmentEnhanced Oil/Tight Oil opportunities:

• Technology-enabled plays such as the Bakken, Cardium and Viking attracting increasing interest (multi-frac horizontal wells)

• The Challenges:Potential for return of upward cost pressuresEnvironmental performanceOpposition to oil sands development…..the “off hydrocarbons” agendaDeveloping offshore markets

CAPP Priorities

2010 CAPP PRIORITIES – “THE BIG 4”

• Alberta Competitiveness ReviewFiscalRegulatory

• Industry Reputation: (Performance + Communications) x Time

“Alberta is Energy” (also B.C. & Saskatchewan)Canadian Natural GasOil Sands Performance and CommunicationsResponsible Canadian Energy

• Environment Policy & Regulation

• Pipeline Tolls

Summary

Summary – Oil & Gas Sector Outlook

• Near term remains challenging:Emerging from economic downturn….but not out of the woods yetCrude oil outlook more encouraging; natural gas less certain Public expectations of industry/gov’t continue to increaseOngoing opposition from ENGOs, other stakeholders

• Fundamentals sound for medium to longer term:Very large resource base (oil and gas)Canadian industry track record and capabilityReliable supplier with good market access

• Industry leadership:Investing to create jobs & economic growth across Canada Environmental performance supported by strict regulationsDeveloping / deploying technology as a key lever (environment & supply)Addressing public perception of industryConstructive engagement in public policy & regulation

• Require a balanced “3E” approach to public policy