Embed Size (px)

Citation preview

Brazil

A new window of opportunity

José FirmoPresident of Brazilian Petroleum,

Gas and Biofuels Institute

The content of this presentation is merelyinformative and uses data from third parties. IBPdisclaims any responsibility for the completeness,accuracy and timeliness of the presentedinformation, as well as for any effects arising fromits use and interpretation. All intellectual propertyrights in any way related to the presentedinformation, as well as any responsibility for itscontent, lies with its respective authors and/orproprietors.

Disclaimer

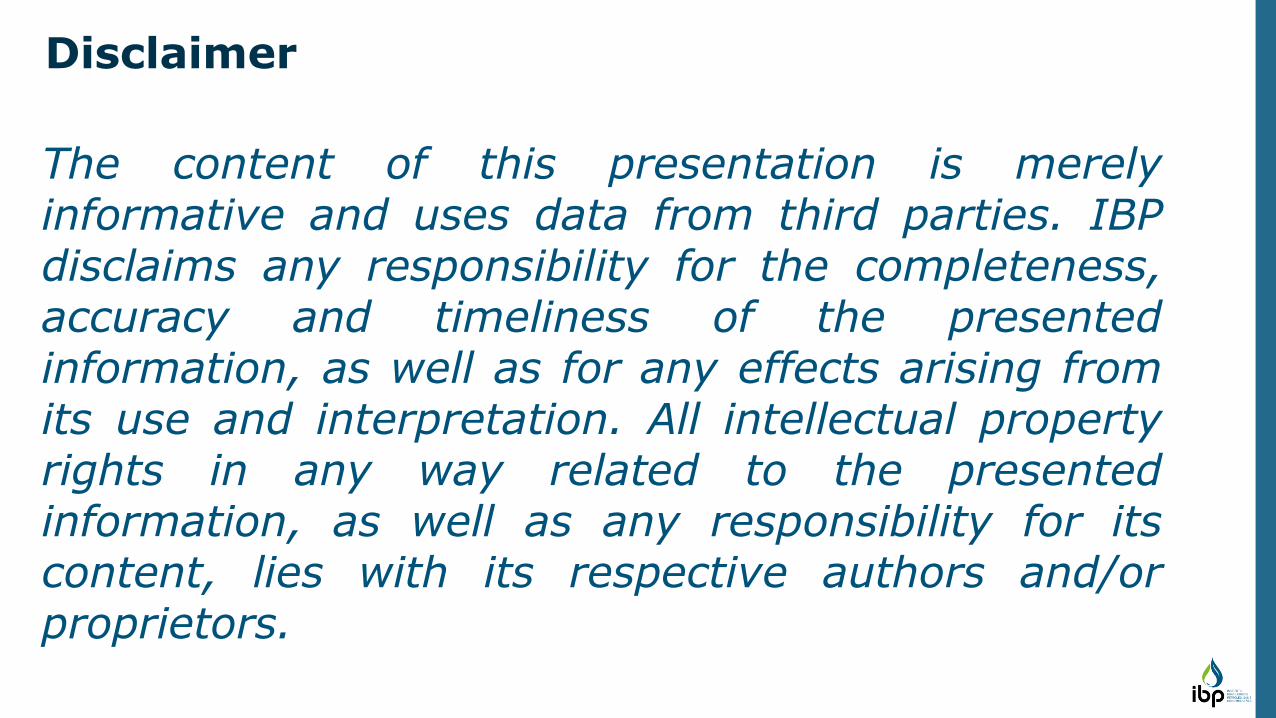

55

38

46

15

22

37

8

13

37

2

15

20

1stRound

2ndRound

3rdRound

4thRound

5thRound

6thRound

7thRound

9thRound

11th &Libra

Round

13thRound

14thRound& PSC

15thRound& PSC

Petrobras Others

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Bidding Rounds | Offshore Operators

Last update April/2018Note: 8th Bidding Round canceled and there were no offshore areas offered in 10th and 12th Bidding Rounds. Source: IBP with data retrieved from ANP

Area by operatorThousand km²

Back to competition!

GapConcentrationCompetition

Note: TBN means To Be NamedSource: IBP with data retrieved from E&P Brasil and ANP

Installed Bidding in progress

Pending final investment decisions

Final investment decisions

Under construction

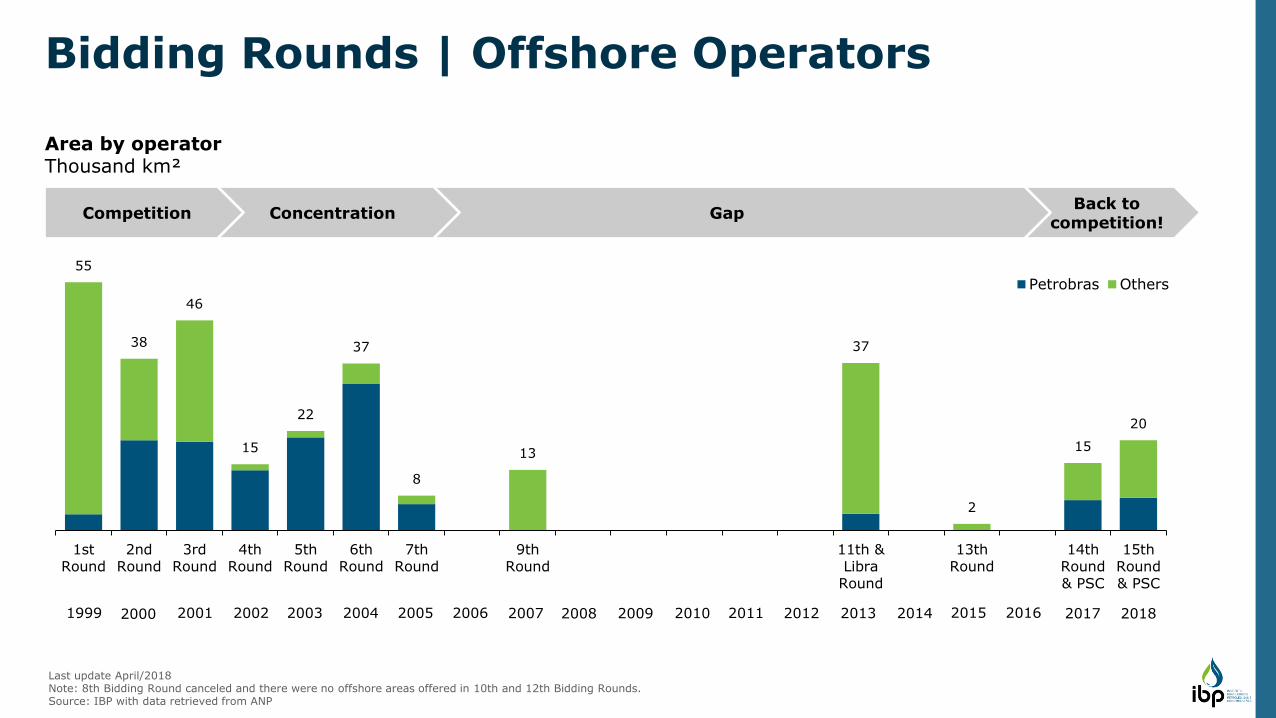

2027’s Forecast

2016 2019 2020 2021 2022

Committed demand (FPSO)

Future investment demand

C. de Caraguatatuba

Lapa

C. de SaquaremaLula Central

C. de MaricáLula Alto

2017 2018

Pioneiro de Libra

LDT Libra

P-76Búzios III

P-75Búzios II

P-68Berbigão

P-67Lula Norte

Campos de GoytacazesTartaruga V.

P-74Búzios I

Petrojar IAtlanta

P-77Búzios IV

P-79Atapú I

P-69Ext. Sul Lula

TBNKangaroo &

Echidna

GuanabaraMero Pilot

CariocaSépia

TBNRev. Marlim

II

TBNRev. Marlim I

TBNParque das

Baleias

TBNBúzios V

TBNSergipe

TBNItapu

TBNMero II

7

4

6

33

Recoverable volume

New investments

Offshore wells

Production units

Drilling rigs simultaneously

Flowlines

Gas pipelines

Oil production increase

+10 bi bbl

US$230 bi

300

39

20

1,100 km

600 km

+2 MMbpd

P-66Lula Sul

2

120

100

80

60

40

20

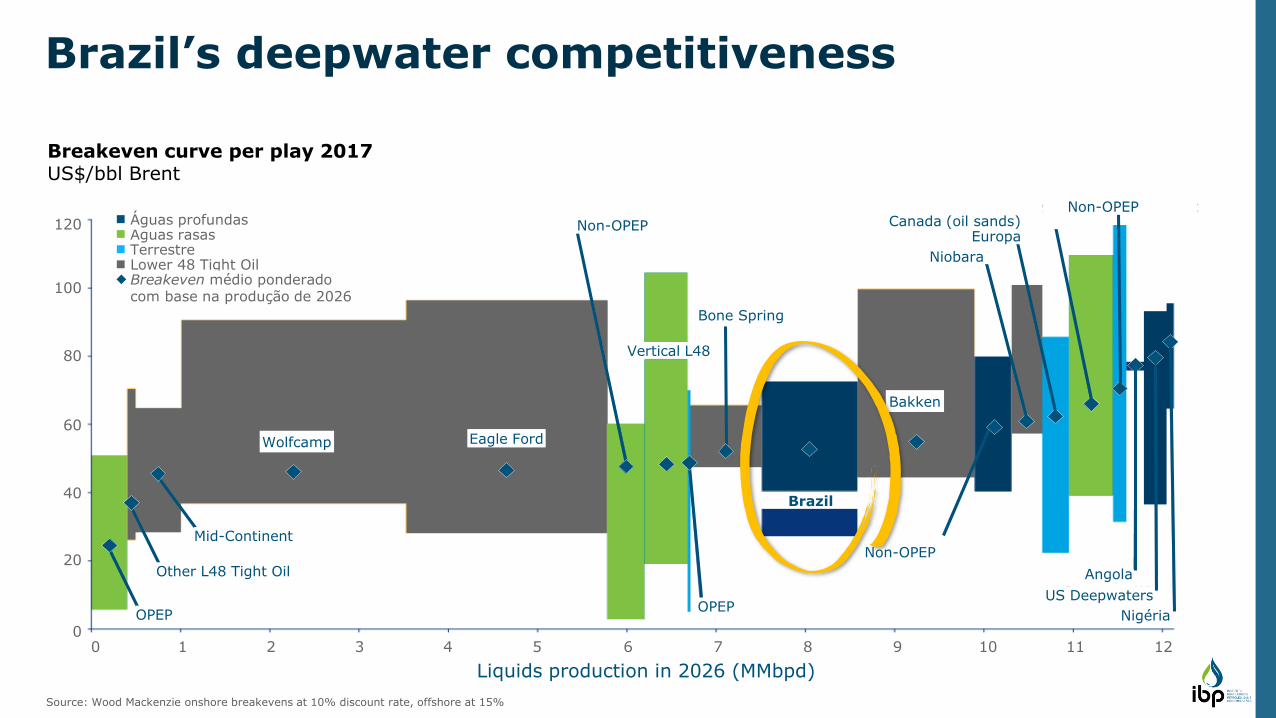

00 1 2 3 4 5 6 7 8 9 10 11 12

TerrestreLower 48 Tight OilBreakeven médio ponderado com base na produção de 2026

OPEP

Other L48 Tight Oil

Mid-Continent

Wolfcamp Eagle Ford

OPEP

Non-OPEP

Angola

US Deepwaters

Vertical L48

Bakken

Bone Spring

Non-OPEP

Niobara

EuropaCanada (oil sands)

Nigéria

Brazil

Águas rasasÁguas profundas

Non-OPEP

Liquids production in 2026 (MMbpd)

Source: Wood Mackenzie onshore breakevens at 10% discount rate, offshore at 15%

Brazil’s deepwater competitiveness

Breakeven curve per play 2017US$/bbl Brent

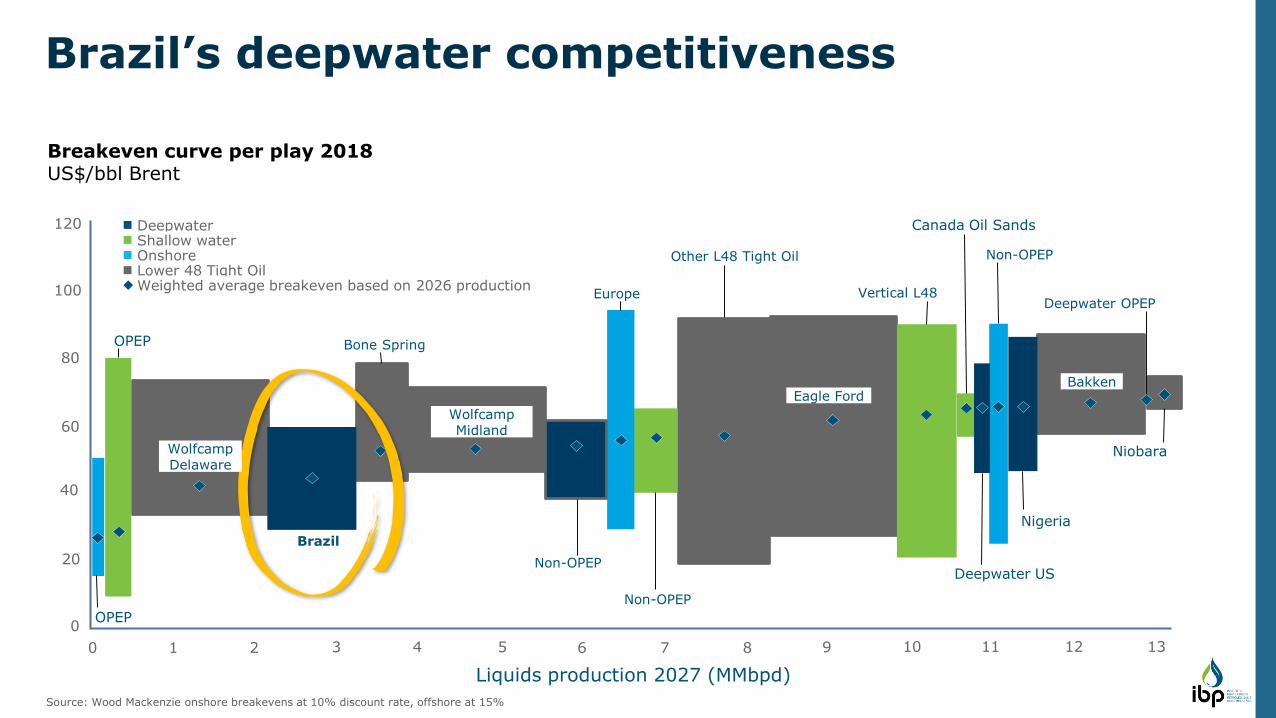

Deepwater OPEP

Brazil

120

100

80

60

40

20

0

0 1 2 3 4 5 6 7 8 9 10 11 12 13

Niobara

OPEP

OPEP

WolfcampDelaware

Bone Spring

WolfcampMidland

Non-OPEP

Europe

Other L48 Tight Oil

Eagle Ford

Vertical L48

Non-OPEP

Nigeria

Breakeven curve per play 2018US$/bbl Brent

Liquids production 2027 (MMbpd)

Canada Oil Sands

Non-OPEP

Deepwater US

Bakken

DeepwaterShallow waterOnshoreLower 48 Tight OilWeighted average breakeven based on 2026 production

Source: Wood Mackenzie onshore breakevens at 10% discount rate, offshore at 15%

Brazil’s deepwater competitiveness

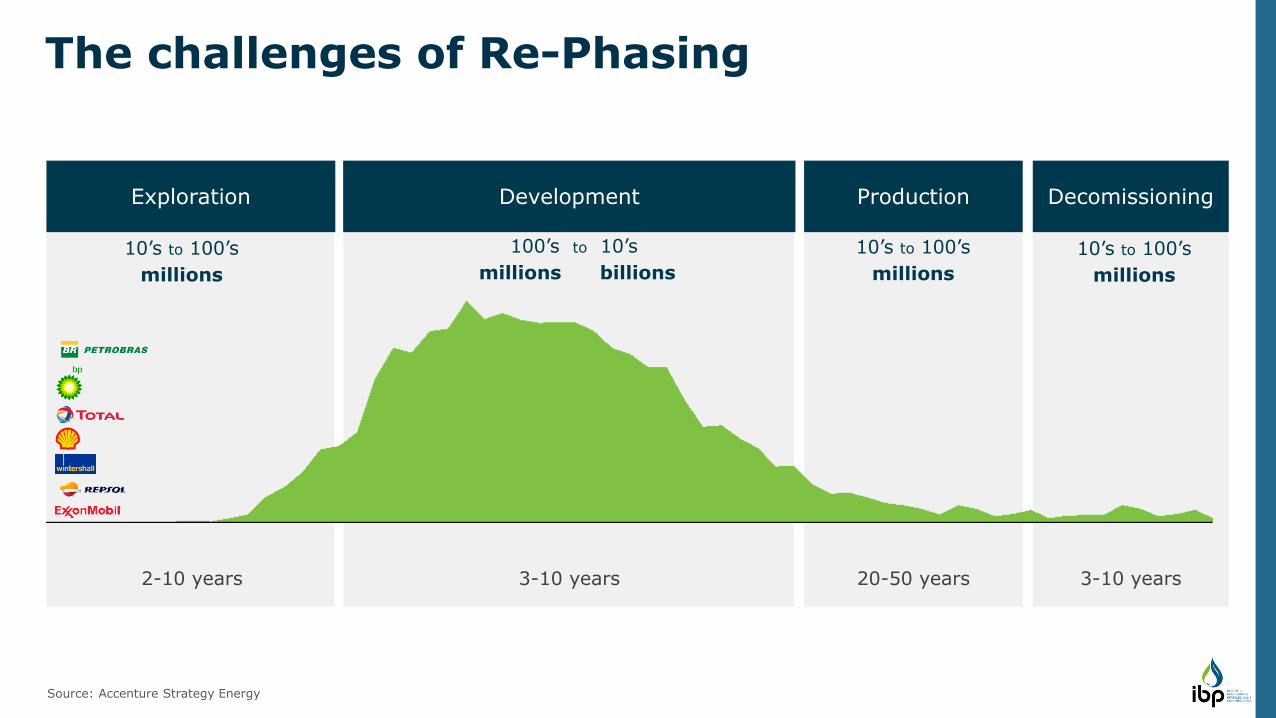

Source: Accenture Strategy Energy

Exploration Development Production Decomissioning

2-10 years 3-10 years 20-50 years 3-10 years

10’s to 100’s

millions

The challenges of Re-Phasing

100’s to 10’s

millions billions

10’s to 100’s

millions

10’s to 100’s

millions

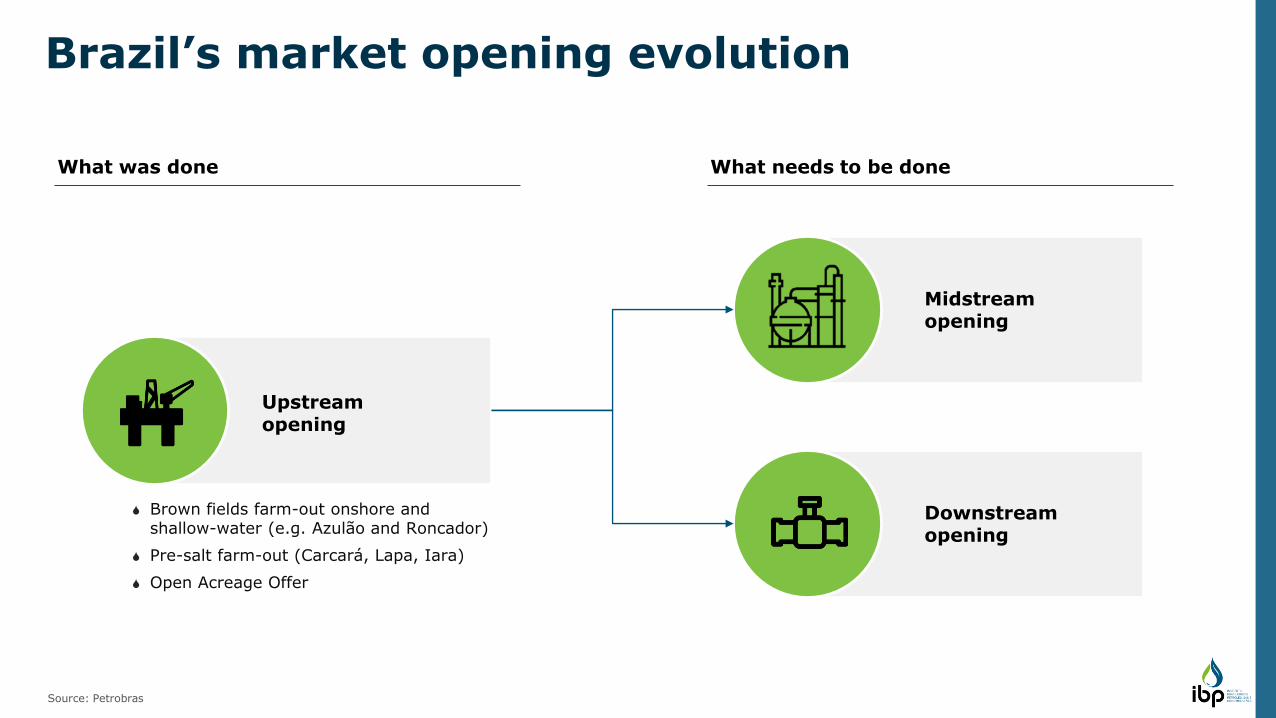

What was done What needs to be done

Upstreamopening

Midstreamopening

Downstreamopening

Brazil’s market opening evolution

Brown fields farm-out onshore and shallow-water (e.g. Azulão and Roncador)

Pre-salt farm-out (Carcará, Lapa, Iara)

Open Acreage Offer

Source: Petrobras

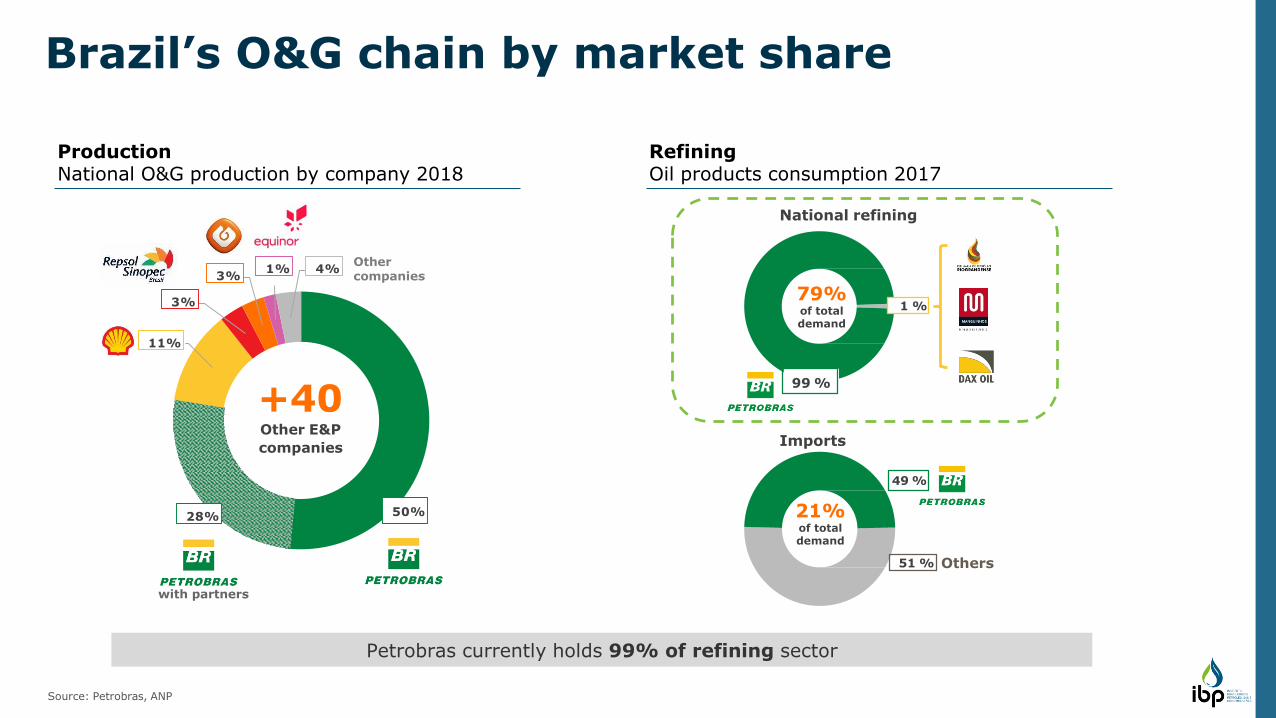

Source: Petrobras, ANP

Brazil’s O&G chain by market share

50%28%

11%

3%

3%1% 4%

+40Other E&P

companies

with partners

Other companies

Imports

51 %

21%of total demand

Others

National refining

99 %

1 %79%of total demand

49 %

Petrobras currently holds 99% of refining sector

ProductionNational O&G production by company 2018

RefiningOil products consumption 2017

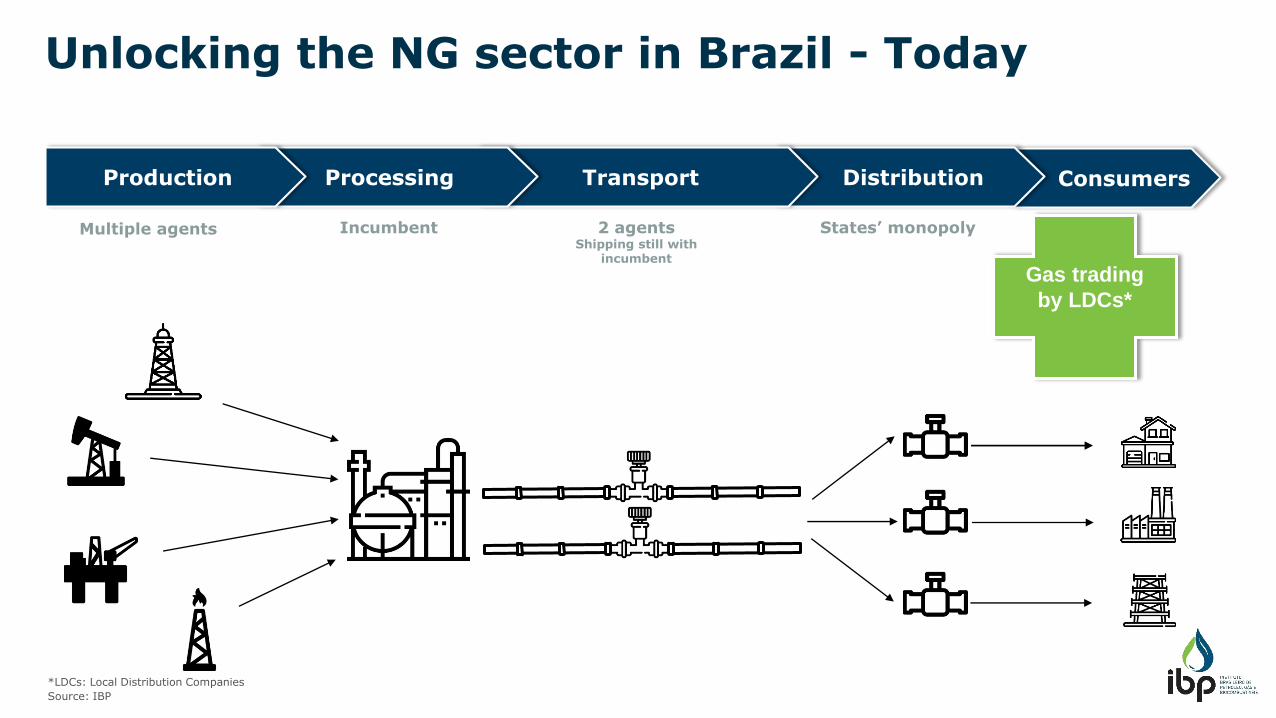

ConsumersDistributionTransportProcessingProduction

Multiple agents 2 agentsShipping still with

incumbent

States’ monopolyIncumbent

*LDCs: Local Distribution Companies

Source: IBP

Gas trading

by LDCs*

Unlocking the NG sector in Brazil - Today

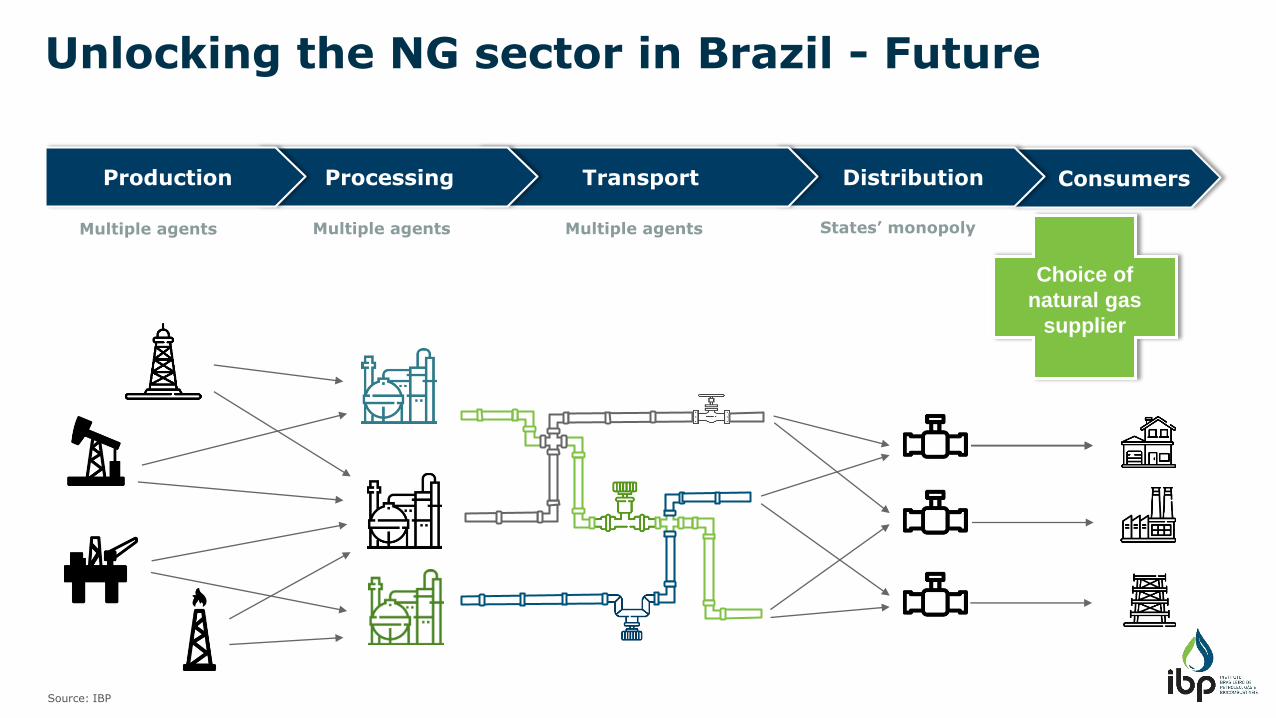

Multiple agentsMultiple agents

Choice of

natural gas

supplier

Source: IBP

ConsumersDistributionTransportProcessingProduction

Multiple agents States’ monopoly

Unlocking the NG sector in Brazil - Future

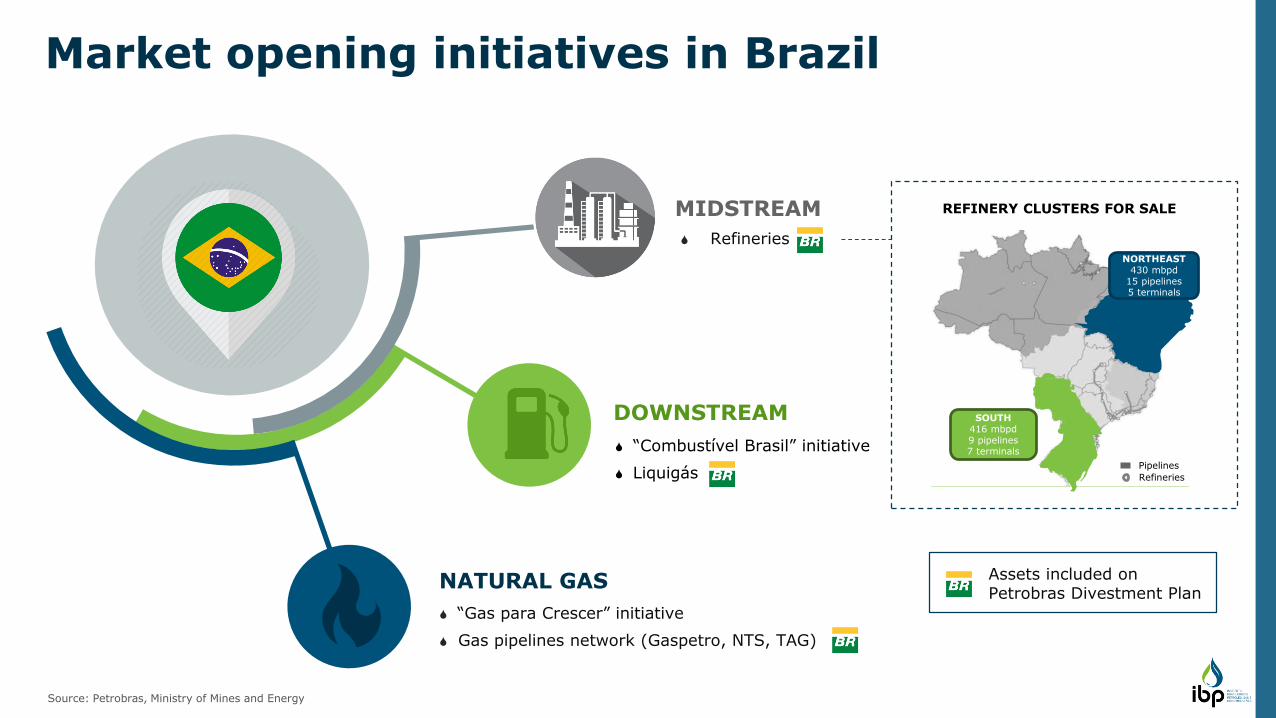

Pipelines

Refineries

NORTHEAST430 mbpd

15 pipelines5 terminals

SOUTH416 mbpd9 pipelines7 terminals

REFINERY CLUSTERS FOR SALE

NATURAL GAS

“Gas para Crescer” initiative

Gas pipelines network (Gaspetro, NTS, TAG)

Refineries

MIDSTREAM

“Combustível Brasil” initiative

Liquigás

DOWNSTREAM

Assets included on Petrobras Divestment Plan

Market opening initiatives in Brazil

Source: Petrobras, Ministry of Mines and Energy

Brazil is back

Enjoy this opportunity to do business and networkin this giant energy market.

25

Thank you!

José Firmo

President of Brazilian Petroleum, Gas and Biofuels Institute

(IBP)