Embed Size (px)

Citation preview

A. GoldklangB CPA, MBA Donald E. Harris, CPA Anne M. Sheehan, CPA S. Gail Moore, CPA

1801 Robert Fulton Drive, Suite 200 Reston, VA 20191

Information Included with the Audit

Jeremy W. Powell, Renee L. Watson, CPA

Allison A. Day, CPA MatthewT. Stiefvater, CPA

Cover Letter - The audit report is issued in draft for the Association to review. The cover letter explains what information must be returned to our office before the audit report (and other letters) can be finalized.

Independent Auditor's Report - This is our report on the Association's financial statements. Once finalized, the Association may distribute this document, along with the audited financial statements, notes to financial statements and any supplementary information in its entirety to members, potential members, etc.

Management Letter - The management letter is not a required communication under auditing standards, but is a by-product of the audit. We generally issue a management letter to communicate our comments and recommendations. Use of this letter is restricted to the board of directors and management.

Communication with Those Charged with Governance under SAS No. 114 - Under Statement of Auditing Standards (SAS) No. 114, we are required to communicate audit matters that, in our professional judgment, may be significant and relevant to those charged with governance of the Association. Use of this letter is restricted to the board of directors and management.

Communication of Significant Deficiencies and/or Material Weaknesses under SAS No. 115 - Under Statement of Auditing Standards (SAS) No. 115, we are required to communicate in writing any significant deficiencies and/or material weaknesses in the Association's internal controls. Use of this letter is restricted to the board of directors and management. If we did not note any significant deficiencies or material weaknesses, no letter will be issued.

Representation Letter - The representation letter is a letter from the Association to us confirming that to the best of your knowledge and belief all information was provided or disclosed to us. This letter needs to be signed by the President or Treasurer of the Association and the management agent representative. The letter needs to be returned to our office before the audit can be finalized.

Adjusted Trial Balance and Adjusting Journal Entries - These are the proposed audit adjustments for the period under audit.

phone 703 3919003 fax 703 3919004 www.GGroupCPAs.com

1801 Robert Fulton Suite 200 A. Gold MBA Reston 1 VA 20191

Donald E. CPA Renee L. Anne M. Sheehan1 CPA S. Gail CPA

May 6, 2014

Board of Directors Colonial Village (Village II), A Condominium

Dear Board Members:

Enclosed, please find the draft audit for Colonial Village (Village II), A Condominium for the years ended December 31, 2013 and 2012.

• Please date and sign the enclosed representation letter. The letter needs to be signed by either the President or Treasurer of the Association and the management agent representative. This letter needs to be returned to our office before the audit can be finalized.

• Please send the Association's most recent financial statements (which should include the balance sheet and income statement) to our office with the signed representation letter. We are requesting this information to comply with auditing standards.

• Please return the signed letter and most recent financial statements to our office within 60 days from the date of this letter. This information can be mailed, faxed or emailed to our office. Our email address is [email protected].

If we do not receive the above information within 60 days from the date of this letter, we may need to perform additional audit procedures to satisfy ourselves that no material events have occurred from the date that we completed our audit fieldwork through the date that we receive the signed representation letter. These additional procedures would include examining the bank statements, minutes, financial statements, general ledger and would also include inquiries of management and the board of directors. We will bill the Association for these additional audit procedures at our hourly rates.

Please do not hesitate to contact us if there are any questions regarding the draft audit.

Sincerely,

GOLDKLANG GROUP CPAs, P.C.

phone 703 3919003 fax 703 391 9004 www.GGroupCPAs.com

Principals Howard A. Goldklang1 CPA1 MBA Donald E. Harris1 CPA Anne M. Sheehan, CPA S. Gail Moore, CPA

To the Board of Directors of

1801 Robert Fulton Drive, Suite 200 Reston1 VA 20191

Independent Auditor's Report

Colonial Village (Village II), A Condominium

Report on the Financial Statements

Associate Principals Jeremy W. Powell, CPA Renee L. Watson, CPA

Managers Allison A. Day, CPA

Matthew T. Stiefvater, CPA

We have audited the accompanying financial statements of Colonial Village (Village II), A Condominium, which comprise the balance sheets as of December 31, 2013 and 2012, and the related statements of income and comprehensive income, members' equity and cash flows for the years then ended, and the related notes to the financial statements.

the Financial Statements ./

Management is aJi;rl 1'/rif;RSen\'Lticiil.!of statements in accordance with a,ccounting principles;) generally St,a_tes.· of America; this includes the design, and coptro! releyant ;.to the preparation and fair presentatiqm of;fimtµcia.!,.Btatemtnts,that due to fraud or error. · - ·· . . · · · · ·"''"' ,.,," · · · -

Auditor's Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures' that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our qualified audit opinion.

phone 703 3919003 fax 703 391 9004 www.GGroupCPAs.com

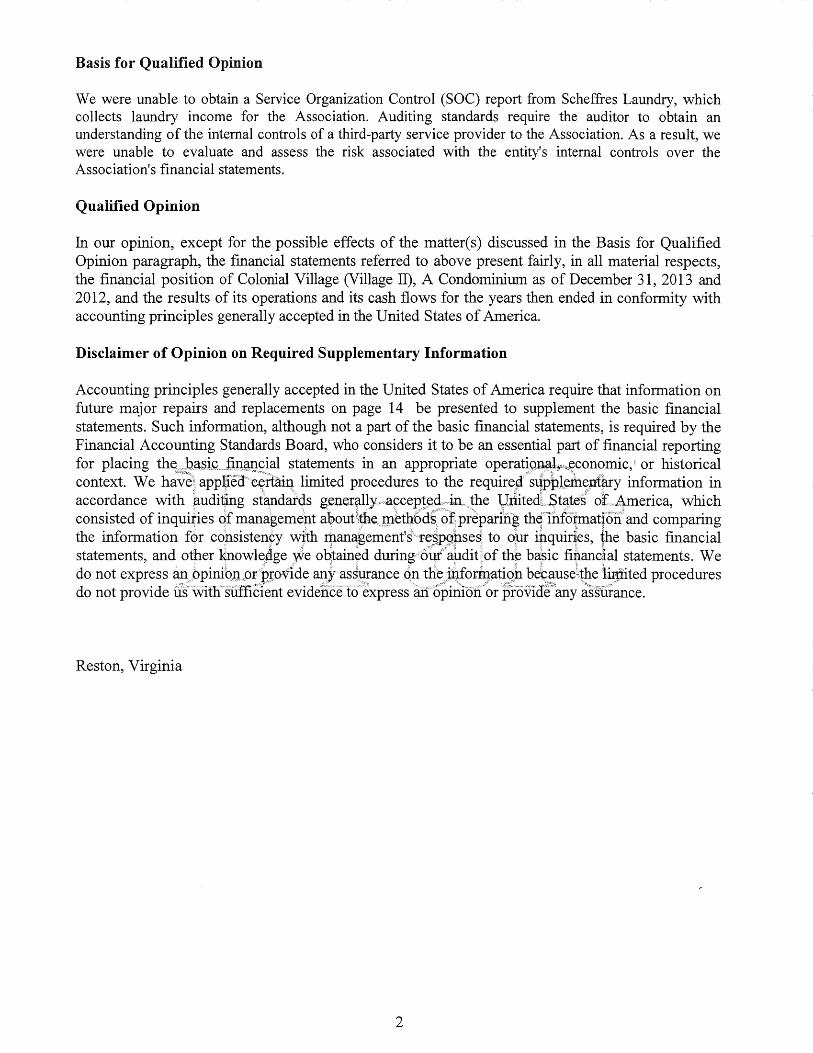

Basis for Qualified Opinion

We were unable to obtain a Service Organization Control (SOC) report from Scheffres Laundry, which collects laundry income for the Association. Auditing standards require the auditor to obtain an understanding of the internal controls of a third-party service provider to the Association. As a result, we were unable to evaluate and assess the risk associated with the entity's internal controls over the Association's financial statements.

Qualified Opinion

In our opinion, except for the possible effects of the matter( s) discussed in the Basis for Qualified Opinion paragraph, the financial statements referred to above present fairly, in all material respects, the financial position of Colonial Village (Village II), A Condominium as of December 31, 2013 and 2012, and the results of its operations and its cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America.

Disclaimer of Opinion on Required Supplementary Information

Accounting principles generally accepted in the United States of America require that information on future major repairs and replacements on page 14 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Financial Accounting Standards Board, who considers it to be an essential part of financial reporting for placing __ statements in an· appropriate 1 or historical context. We have\, limited procedures to the information in accordance with standarcis which consisted of inquiries of manapemeµt otj thfinf ci1111at!Oii' and comparing the information f9r consistenyy w!th to opr the basic financial statements, and otper 1<.nowl5dge yve 09tained thf fi\lancial __ statements. We do not express on procedures do not provide l1swith'suffident evidencefo'express·a.n o'piriiorior provioe"any asshrance.

Reston, Virginia

2

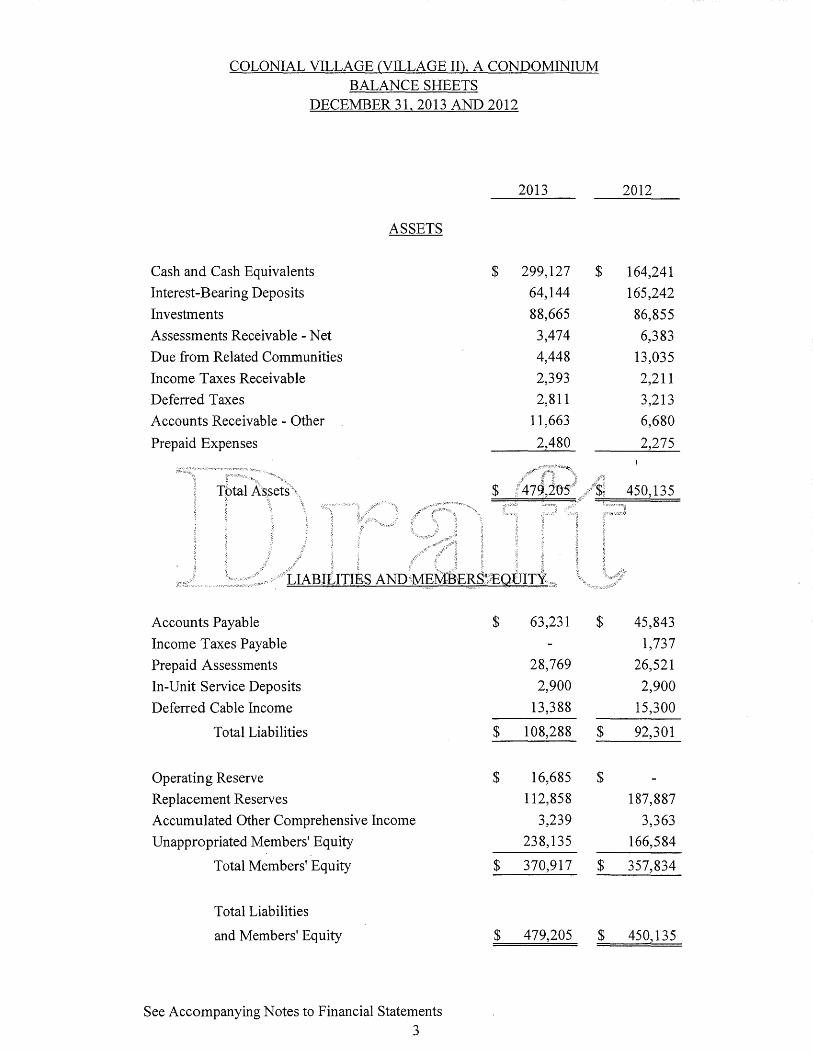

COLONIAL VILLAGE (VILLAGE II), A CONDOMINIUM BALANCE SHEETS

DECEMBER 31, 2013 AND 2012

Cash and Cash Equivalents Interest-Bearing Deposits Investments Assessments Receivable - Net Due from Related Communities Income Taxes Receivable Deferred Taxes Accounts Receivable - Other Prepaid Expenses

ASSETS

$

2013

299,127 64,144 88,665 3,474 4,448 2,393 2,81 1

1 1,663 2,480

$ /479,2ll5'

Accounts Payable Income Taxes Payable Prepaid Assessments In-Unit Service Deposits Deferred Cable Income

Total Liabilities

Operating Reserve Replacement Reserves Accumulated Other Comprehensive Income Unappropriated Members' Equity

Total Members' Equity

Total Liabilities

. ·:1

$

$

$

$

-·-····

63,231

28,769 2,900

13,388 108,288

16,685 112,858

3,239 238,135 370,917

$

..... '-""-•

$

$

$

$

2012

164,241 165,242 86,855 6,383

13,035 2,21 1 3,213 6,680 2,275

450,135

45,843 1,737

26,521 2,900

15,300

92,301

187,887 3,363

166,584 357,834

and Members' Equity $ 479,205 $ 450,135

See Accompanying Notes to Financial Statements 3

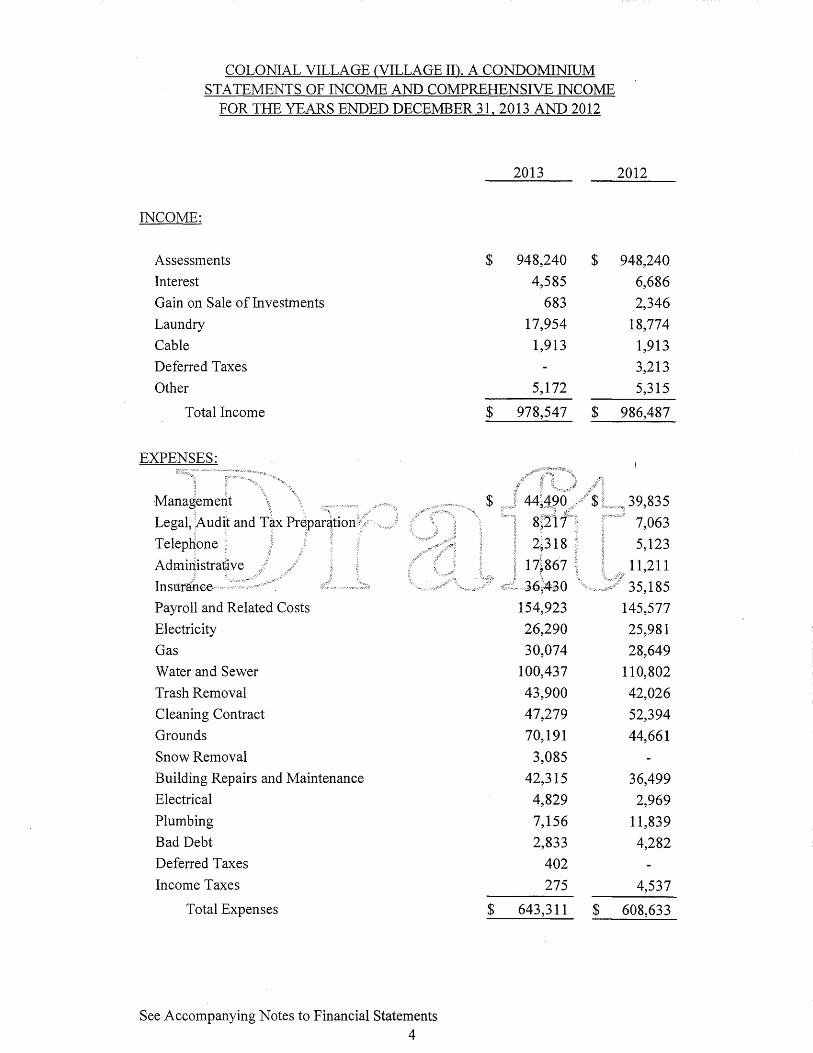

COLONIAL VILLAGE (VILLAGE II), A CONDOMINIUM STATEMENTS OF INCOME AND COMPREHENSIVE INCOME

FOR THE YEARS ENDED DECEMBER31, 2013 AND 2012

INCOME:

Assessments Interest Gain on Sale of Investments Laundry Cable Deferred Taxes Other

Total Income

EXPENSES: ;.; .... , ....... ,, .... ,.,., .... ... , .... , ...

·Managemeqt "\. '\\ >;;<:······-..,;'· .. ·.·· Legal, Audh and · ·

' Administrative .. : :; ... , .. Insurarice·.':: ·:: .-::•· ......

Payroll and Related Costs Electricity Gas Water and Sewer Trash Removal Cleaning Contract Grounds Snow Removal Building Repairs and Maintenance Electrical Plumbing Bad Debt Deferred Taxes Income Taxes

Total Expenses

See Accompanying Notes to Financial Statements 4

2013

$ 948,240 $ 4,585

683 17,954

1,913

5,172

$ 978,547 $

154,923 26,290 30,074

100,437 43,900 47,279 70,191

3,085 42,315

4,829 7,156 2,833

402 275

$ 643,311 $

2012

948,240 6,686 2,346

18,774 1,913 3,213 5,315

986,487

39,835 7,063 5,123

11,211 35,185

145,577 25,981 28,649

110,802 42,026 52,394 44,661

36,499 2,969

11,839 4,282

4,537

608,633

COLONIAL VILLAGE (VILLAGE II), A CONDOMINIUM ST A TEMENTS OF INCOME AND COMPREHENSIVE INCOME

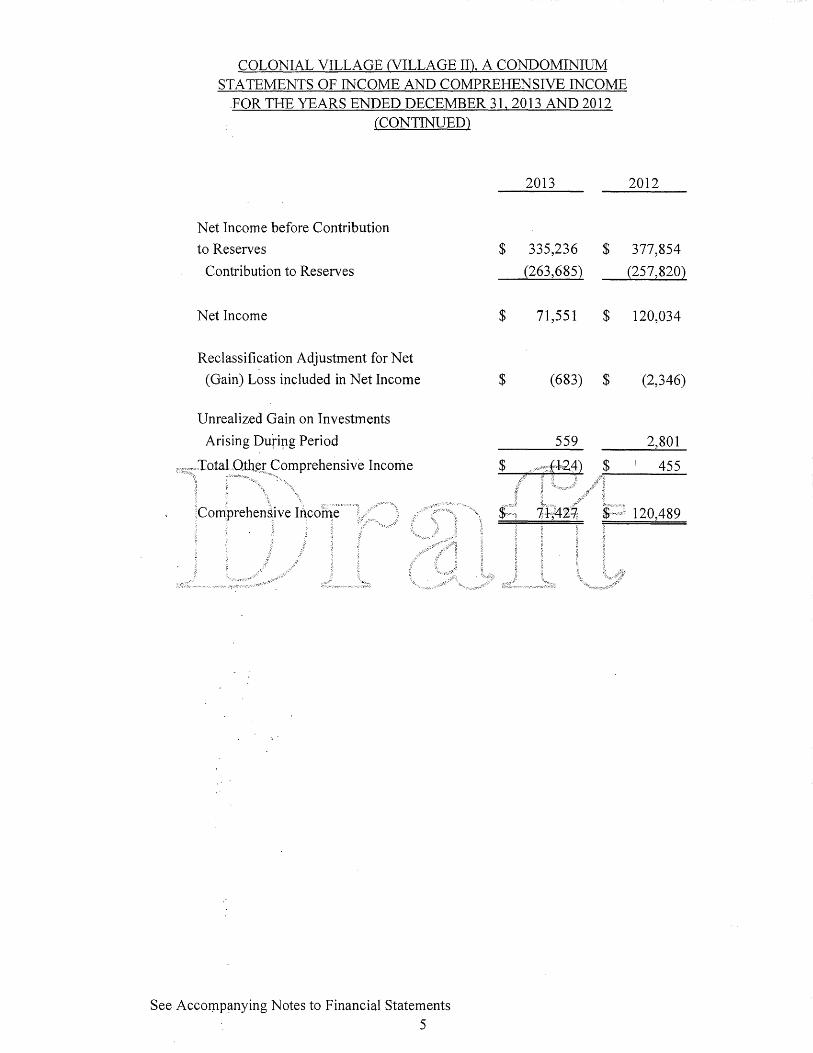

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012 (CONTINUED)

Net Income before Contribution to Reserves

Contribution to Reserves

Net Income

Reclassification Adjustment for Net (Gain) Loss included in Net Income

Unrealized Gain on Investments Arising Duriµg Period

See Accompanying Notes to Financial Statements 5

$

$

$

$

$

2013

335,236 $ (263,685)

71,551 $

(683) $

559 ,,,fl,,2,4) $

;{!} ·-

,:/;:j;:'

$·-·i•";<;''""g

2012

377,854 (257,820)

120,034

(2,346)

2,801

455

120,489

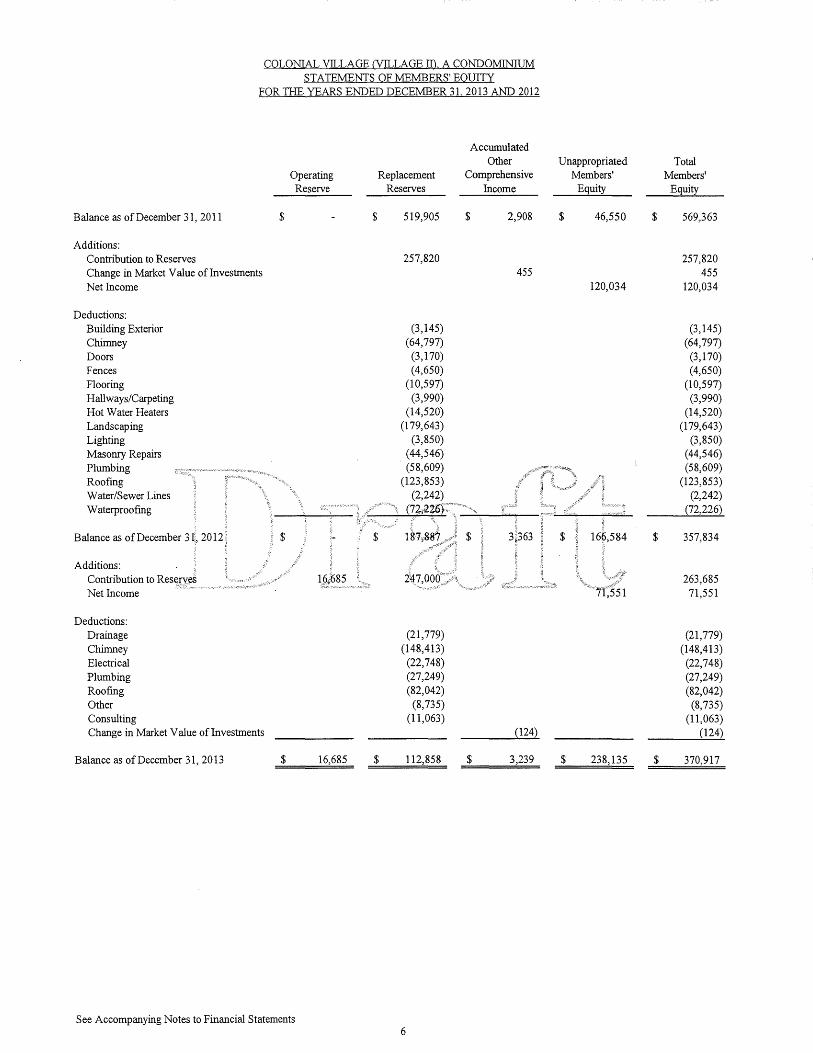

COLONIAL VILLAGE CVILLAGE ID A CONDOMINIUM STATEMENTS OF MEMBERS' EOUITY

FOR THE YEARS ENDED DECEMBER 31 2013 AND 2012

Accumulated Other

Operating Replacement Comprehensive Reserve Reserves Income

Balance as of December 31, 2011 $ $ 519,905 $ 2,908

Additions: Contribution to Reserves 257,820 Change in Market Value of Investments 455 Net Income

Deductions: Building Exterior (3,145) Chimney (64,797) Doors (3, 170) Fences (4,650) Flooring (10,597) Hallways/Carpeting (3,990) Hot Water Heaters (14,520) Landscaping (179,643) Lighting (3,850) Masonry Repairs (44,546) Plumbing (58,609) Roofing (123,853) Water/Sewer Lines Waterproofing

Balance as of December

Additions: Contribution to Net Income

Deductions: Drainage (21,779) Chimney (148,413) Electrical (22,748) Plumbing (27,249) Roofing (82,042) Other (8,735) Consulting (11,063) Change in Market Value of Investments (124)

Balance as of December 31, 2013 $ 16,685 $ 112,858 $ 3,239

See Accompanying Notes to Financial Statements 6

Unappropriated Total Members' Members'

Equity Equity

$ 46,550 $ 569,363

257,820 455

120,034 120,034

(3,145) (64,797)

(3, 170) (4,650)

(10,597) (3,990)

(14,520) (179,643)

(3,850) (44,546) (58,609)

(123,853) (2,242)

(72,226)

$ 357,834

263,685 71,551

(21,779) (148,413)

(22,748) (27,249) (82,042)

(8, 735) (11,063)

(124)

$ 238,135 $ 370,917

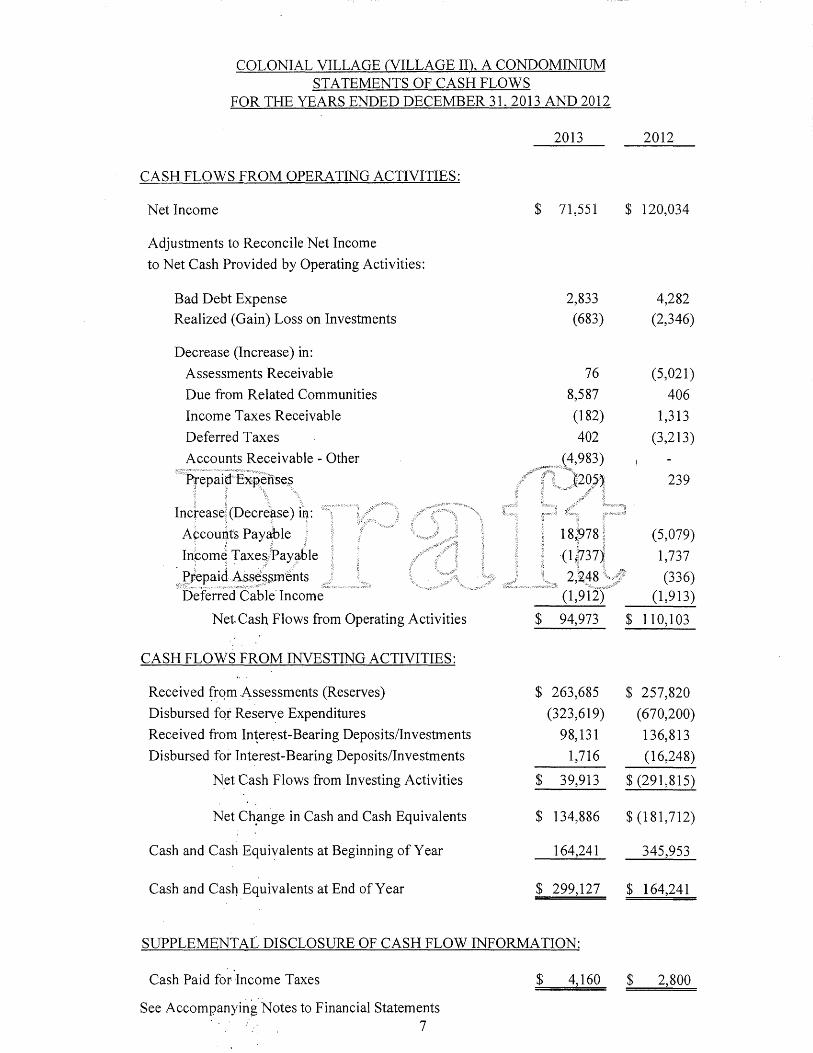

COLONIAL VILLAGE CVILLAGE II), A CONDOMINIUM STATEMENTS OF CASH FLOWS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

2013 2012

CASH FLOWS FROM OPERATING ACTIVITIES:

Net Income

Adjustments to Reconcile Net Income to Net Cash Provided by Operating Activities:

Bad Debt Expense Realized (Gain) Loss on Investments

Decrease (Increase) in: Assessments Receivable Due from Related Communities Income Taxes Receivable Deferred Taxes Accounts Receivable - Other

:.: . \•

InJease!l •fo: Accouri,t's Payable Inbome

....... .. Deferred Income

Net Cash, Flows from Operating Activities

CASH FLOWS FROM INVESTING ACTIVITIES:

Received frqm .Assessments (Reserves) Disbursed for Reserve Expenditures Received from Deposits/Investments Disbursed for Interest-Bearing Deposits/Investments

N_et Cash Flows from Investing Activities

Net Chf!nge in Cash and Cash Equivalents

Cash and Cash Equivalents at Beginning of Year

Cash and Cash Equivalents at End of Year

$ 71,551

2,833 (683)

76 8,587 (182) 402

( 4,983)

::·;,.,;,-.• ,,,

$ 120,034

4,282 (2,346)

(5,021) 406

1,313 (3,213)

239

(5,079) 1,737 (336)

(1,913)

or31).

$ 94,973 $ 110,103

$ 263,685 $ 257,820 (323,619) (670,200)

98, 131 136,813 1,716 (16,248)

$ 39,913 $ (291,815)

$ 134,886 $ (181,712)

164,241 345,953

$ 299,127 $ 164,241

SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION:

Cash Paid for Income Taxes $ 4,160 $ 2,800

See Accompanying Notes to Financial Statements . 7

COLONIAL VILLAGE (VILLAGE II), A CONDOMINIUM NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2013 AND 2012

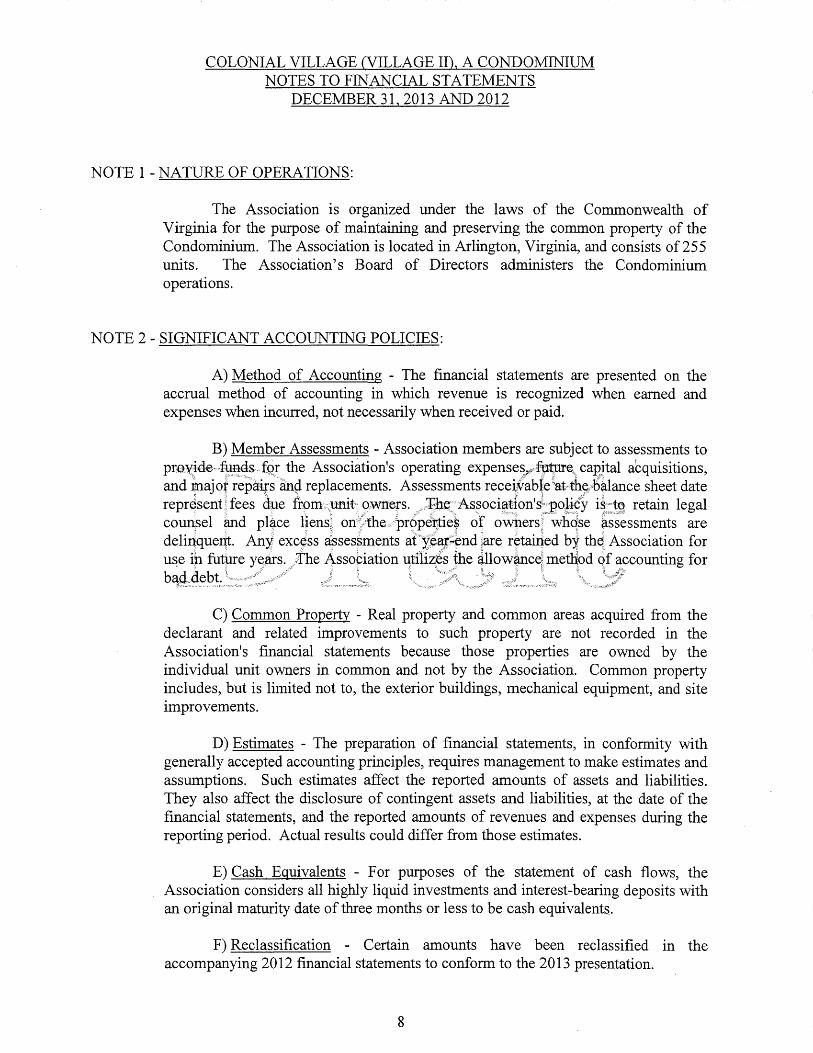

NOTE 1 - NATURE OF OPERATIONS:

The Association is organized under the laws of the Commonwealth of Virginia for the purpose of maintaining and preserving the common property of the Condominium. The Association is located in Arlington, Virginia, and consists of 255 units. The Association's Board of Directors administers the Condominium operations.

NOTE 2 - SIGNIFICANT ACCOUNTING POLICIES:

A) Method of Accounting - The financial statements are presented on the accrual method of accounting in which revenue is recognized when earned and expenses when incurred, not necessarily when received or paid.

B) Member Assessments - Association members are subject to assessments to the Association's operating caBjtal abquisitions,

and 1najo£ repaip· replacements. Assessments sheet date represent;; fees due ftpm;::;init19wners. retain legal coilll;sel liens') of owpers,' wh9se assessments are delinquent. Ani assessments at \are b4 the; Association for

iµ futpre _,The 4ssopiation l\tilizes !he met}ibd qf for ba.,gdebt<,, ...... ,.· .· · · · · · '.,..... .., .. · .h'

C) Common Property - Real property and common areas acquired from the declarant and related improvements to such property are not recorded in the Association's financial statements because those properties are owned by the individual unit owners in common and not by the Association. Common property includes, but is limited not to, the exterior buildings, mechanical equipment, and site improvements.

D) Estimates - The preparation of financial statements, in conformity with generally accepted accounting principles, requires management to make estimates and assumptions. Such estimates affect the reported amounts of assets and liabilities. They also affect the disclosure of contingent assets and liabilities, at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

E) Cash Equivalents - For purposes of the statement of cash flows, the Association considers all highly liquid investments and interest-bearing deposits with an original maturity date of three months or less to be cash equivalents.

F) Reclassification - Certain amounts have been reclassified m the accompanying 2012 financial statements to conform to the 2013 presentation.

8

COLONIAL VILLAGE CVILLAGE II), A CONDOMINIUM NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2013 AND 2012 (CONTINUED)

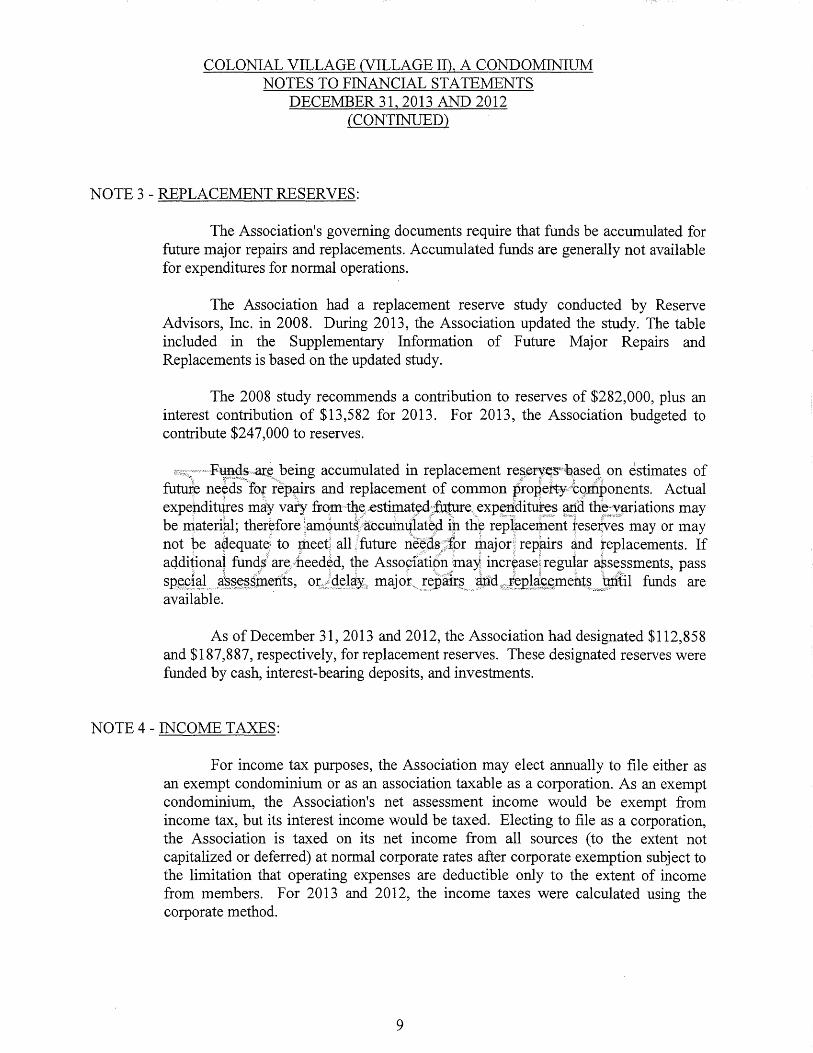

NOTE 3 - REPLACEMENT RESERVES:

The Association's governing documents require that funds be accumulated for future major repairs and replacements. Accumulated funds are generally not available for expenditures for normal operations.

The Association had a replacement reserve study conducted by Reserve Advisors, Inc. in 2008. During 2013, the Association updated the study. The table included in the Supplementary Information of Future Major Repairs and Replacements is based on the updated study.

The 2008 study recommends a contribution to reserves of $282,000, plus an interest contribution of $13,582 for 2013. For 2013, the Association budgeted to contribute $247,000 to reserves.

accumulated in replacement on estimates of futufr nef ds 'fot and replacement of common Actual expeµdi11.lres maf. vary may be m_aterial; theryfore replaceipent rese1f'eS may or may not pe adequat5\ to all ;future zj:iajor;' replacements. If

tpe regular pass .. ..• major.,,_ :::!nd funds are available. - -. .· . . - . - --

As of December 31, 2013 and 2012, the Association had designated $112,858 and $187,887, respectively, for replacement reserves. These designated reserves were funded by cash, interest-bearing deposits, and investments.

NOTE 4 - INCOME TAXES:

For income tax purposes, the Association may elect annually to file either as an exempt condominium or as an association taxable as a corporation. As an exempt condominium, the Association's net assessment income would be exempt from income tax, but its interest income would be taxed. Electing to file as a corporation, the Association is taxed on its net income from all sources (to the extent not capitalized or deferred) at normal corporate rates after corporate exemption subject to the limitation that operating expenses are deductible only to the extent of income from members. For 2013 and 2012, the income taxes were calculated using the corporate method.

9

COLONIAL VILLAGE (VILLAGE II), A CONDOMINIUM NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2012 AND 2011 (CONTINUED)

NOTE 4 - INCOME TAXES (CONTINUED):

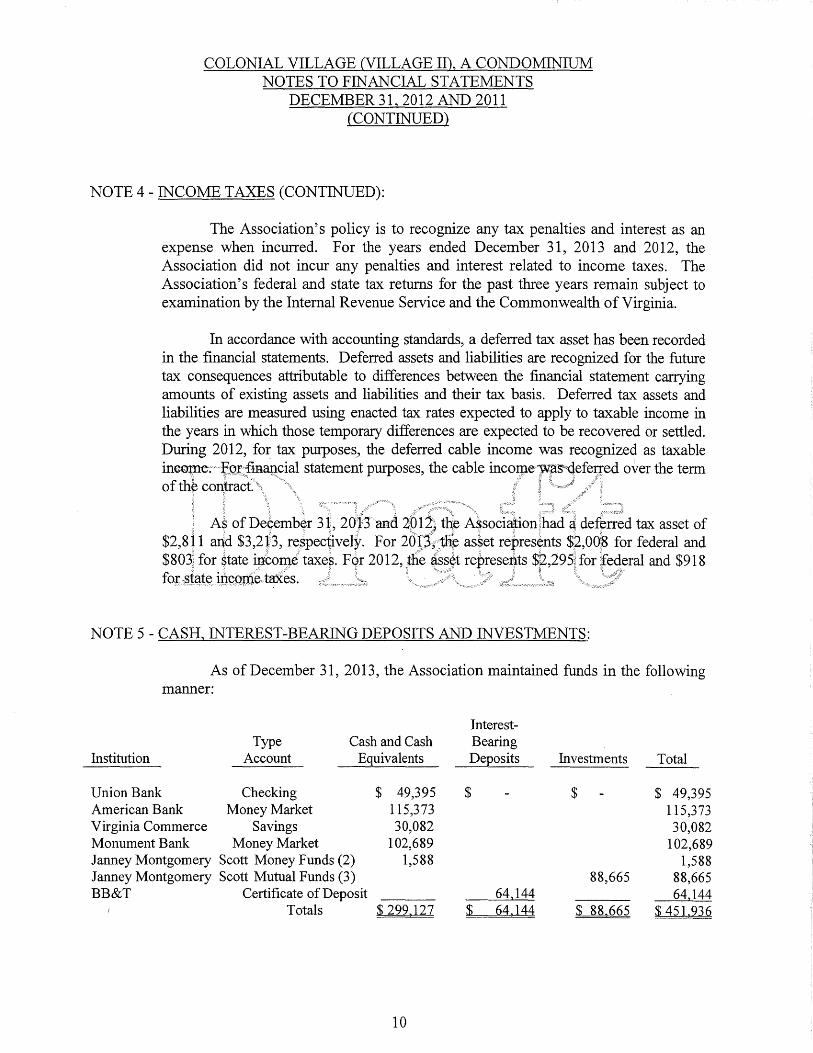

The Association's policy is to recognize any tax penalties and interest as an expense when incurred. For the years ended December 31, 2013 and 2012, the Association did not incur any penalties and interest related to income taxes. The Association's federal and state tax returns for the past three years remain subject to examination by the Internal Revenue Service and the Commonwealth of Virginia.

In accordance with accounting standards, a deferred tax asset has been recorded in the financial statements. Deferred assets and liabilities are recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their tax basis. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. During 2012, for tax purposes, the deferred cable income was recognized as taxable

statement purposes, the cable incol]le'}'V'fl'.S"'<.lefe11ed o\rer the term of the contracf"·- " - :c ·' · -

_.·.:·.<::·;'

•• of December 3 i', 2df3'and defF;;d tax asset of $2,811 at{d $3,2f·3, For 20J.'3f;::tlie represynts $f,00)8 for federal and $803i for Fqr 2012, ;the represe11ts fegeral and $918

.. taxes. · · · · · · '' . - · · ··· ·-...... _

NOTE 5 - CASH, INTEREST-BEARING DEPOSITS AND INVESTMENTS.:

As of December 31, 2013, the Association maintained funds in the following manner:

Institution Type

Account Cash and Cash

Equivalents

Union Bank Checking American Bank Money Market Virginia Commerce Savings Monument Bank Money Market Janney Montgomery Scott Money Funds (2) Janney Montgomery Scott Mutual Funds (3) BB&T Certificate of Deposit

Totals

$ 49,395 115,373 30,082

102,689 1,588

$ 299.127

10

Interest-Bearing Deposits

$

$ 64 144 64.144

Investments

$

88,665

$ 88.665

Total

$ 49,395 115,373 30,082

102,689 1,588

88,665 64.144

$ 451.936

COLONIAL VILLAGE (VILLAGE II), A CONDOMINIUM NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2013 AND 2012 (CONTINUED)

NOTE 5 - CASH, INTEREST-BEARING DEPOSITS AND INVESTMENTS: (CONTINUED)

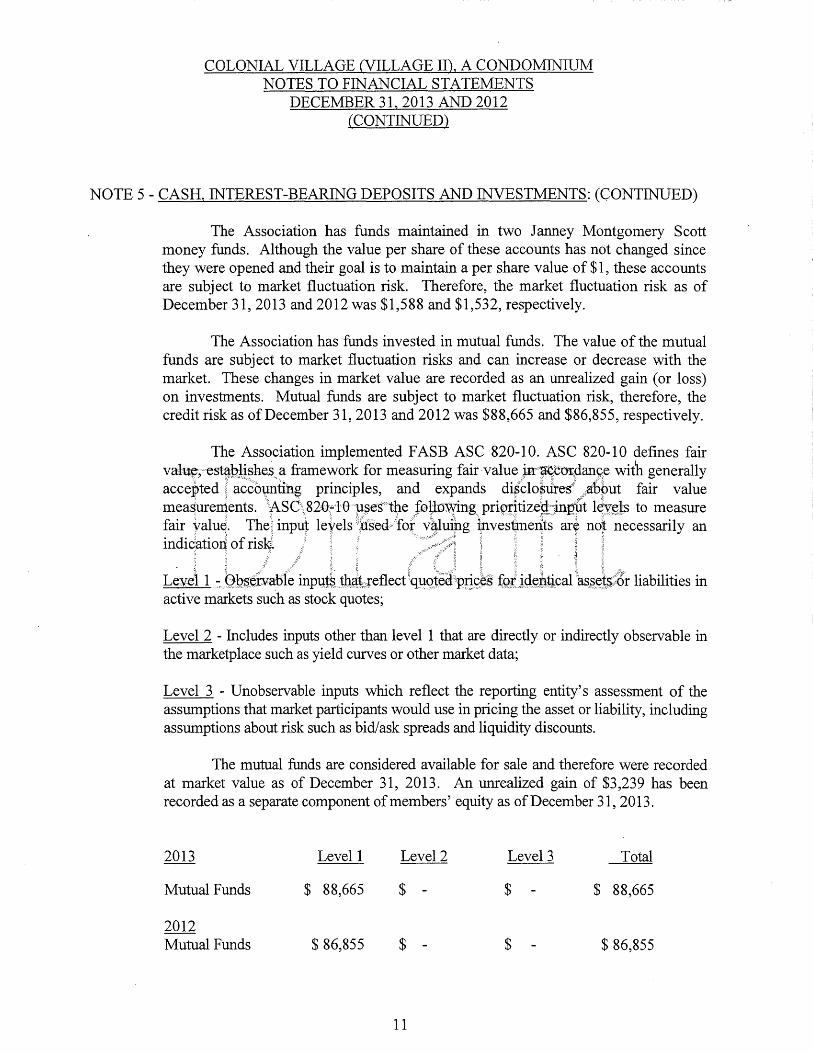

The Association has funds maintained in two Janney Montgomery Scott money funds. Although the value per share of these accounts has not changed since they were opened and their goal is to maintain a per share value of $1, these accounts are subject to market fluctuation risk. Therefore, the market fluctuation risk as of December 31, 2013 and 2012 was $1,588 and $1,532, respectively.

The Association has funds invested in mutual funds. The value of the mutual funds are subject to market fluctuation risks and can increase or decrease with the market. These changes in market value are recorded as an unrealized gain (or loss) on investments. Mutual funds are subject to market fluctuation risk, therefore, the credit risk as of December 31, 2013 and 2012 was $88,665 and $86,855, respectively.

The Association implemented F ASB ASC 820-10. ASC 820-10 defines fair .. aframework for measuring fair with generally

accepted .! principles, and ,,;trbput fair value to measure

fair yalue. The·: input leyels }iS'ed,Tof ipves1P1e11ts ary noi necessarily an indication of risl<l · - - - -- - -

1 liabilities in active markets such as stock quotes;

Level 2 - Includes inputs other than level 1 that are directly or indirectly observable in the marketplace such as yield curves or other market data;

Level 3 - Unobservable inputs which reflect the reporting entity's assessment of the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk such as bid/ask spreads and liquidity discounts.

The mutual funds are considered available for sale and therefore were recorded at market value as of December 31, 2013. An unrealized gain of $3,239 has been recorded as a separate component of members' equity as of December 31, 2013.

Level 1 Level2 Level3 Total

Mutual Funds $ 88,665 $ - $ $ 88,665

2012 Mutual Funds $ 86,855 $ - $ $ 86,855

11

COLONIAL VILLAGE (VILLAGE II), A CONDOMINIUM NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2013 AND 2012 (CONTINUED)

NOTE 6 - ASSESSMENTS RECEIVABLE - NET:

The Association utilizes the allowance method of accounting for bad debt. Individual receivables are written off as a loss when a determination is made that they are non-collectible. Under the allowance method, collection efforts may continue and recoveries of amounts previously written off are recognized as income in the year of collection.

Assessments Receivable Less: Allowance for Doubtful Assessments Assessments Receivable - Net

NOTE 7 - DEFERRED CABLE INCOME:

2013 2012

$ 9,504 (6,030)

$ 3.474

$ 10,664 (4,281)

$ 6.383

; ... signed a 10-year cable agreerenf January 2011 and ending granted the

corppany ins7an; .. qn the fsso9iation's received a fee of

$75 per unit f?r.a;9tal !s a prorated <?.!:.!h!§ ... feemust over

the life of the agreement and was recorded as deferred cable income. During 2013 and 2012, $1,913 per year was recognized as income to the Association. As of December 31, 2013 and 2012, the balance in deferred cable income was $13,388 and $15,300, respectively.

NOTE 8 - PAYROLL AND RELATED COSTS:

The Association's management agent utilizes a central management payroll system, whereby payroll returns were filed under the management agent's name and federal identification number. In addition to the payment of management fees, the Association reimbursed management for wages, payroll taxes, workers' compensation and health insurance for employees that performed work for the Association.

NOTE 9 - OPERATING RESERVE:

During 2013, the Association established an operating reserve for unexpected contingencies. During 2013, the Association elected to contribute $16,685 to this fund. As of December 31, 2013 the balance in the operating reserve was $16,685. This fund was funded by cash, interest-bearing deposits, and investments.

12

COLONIAL VILLAGE (VILLAGE II), A CONDOMINIUM NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2013 AND 2012 (CONTINUED)

NOTE 10 - SUBSEQUENT EVENTS:

In preparing these financial statements, the Association has evaluated events and transactions for potential recognition or disclosure through [date to be inserted upon finalization], the date the financial statements were available to be issued.

13

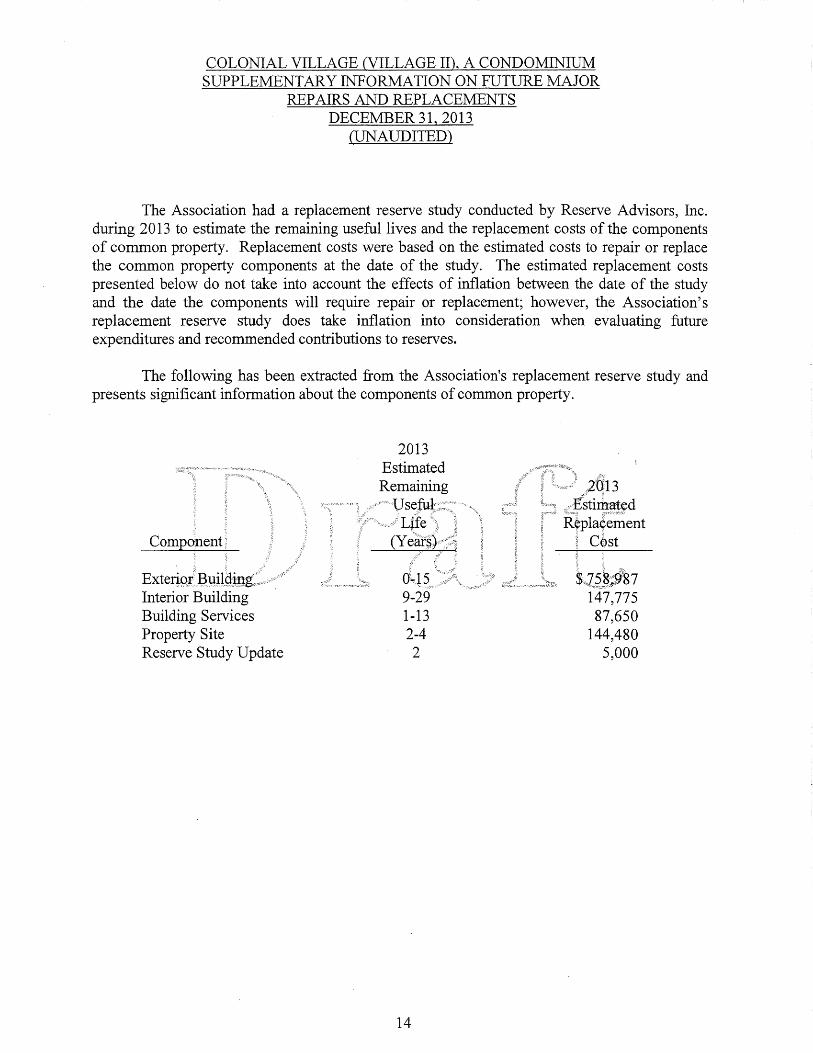

COLONIAL VILLAGE (VILLAGE II), A CONDOMINIUM SUPPLEMENTARY INFORMATION ON FUTURE MAJOR

REP AIRS AND REPLACEMENTS DECEMBER31, 2013

(UNAUDITED)

The Association had a replacement reserve study conducted by Reserve Advisors, Inc. during 2013 to estimate the remaining useful lives and the replacement costs of the components of common property. Replacement costs were based on the estimated costs to repair or replace the common property components at the date of the study. The estimated replacement costs presented below do not take into account the effects of inflation between the date of the study and the date the components will require repair or replacement; however, the Association's replacement reserve study does take inflation into consideration when evaluating future expenditures and recommended contributions to reserves.

The following has been extracted from the Association's replacement reserve study and presents significant information about the components of common property.

,. .

Component:

·' > .·.

Interior Building Building Services Property Site Reserve Study Update

2013 Estimated Remaining

9-29 1-13 2-4 2

14

Cost

$,}·,',',·, 5. 'g··· ···'£187 147,775 87,650

144,480 5,000

Principals Howard A. Goldklang1 CPA, MBA Donald E. Harris, CPA Anne M. Sheehan, CPA S. Gail Moore, CPA

1801 Robert Fulton Drive, Suite 200 Reston, VA 20191

Management Letter

Associate Principals Jeremy W. Powell1 CPA Renee L. Watson, CPA

Managers Allison A. Day1 CPA

MatthewT. Stiefvater1 CPA

This communication is intended solely for the information and use of management and the board of directors and is not intended to be and should not be used by anyone other than these specified parties.

May 6, 2014

Board of Directors Colonial Village (Village II), A Condominium

Dear Board Members:. __ ,,,., ... ,,,, \: .,t

We have audited the 4nanciAf for the year ended December; 31, 2oi13. During Sf verrl"'inatters that are opportunities for controls and a rysult, we make the following cormpe1pts aJ.1d . .. , , . . · .

Financial Analysis ·· ·. '. .*, ... , ..

As of December 31, 2013, the Association had a surplus of $254,820 in excess operating funds (operating reserve and unappropriated members' equity). This represents approximately 27% of annual assessments. We recommend the Association maintain excess operating funds at a level of 10% to 20% of annual assessments. Any funds in excess of 20% may be transferred to replacement reserves.

The Association's level of delinquencies remains well below our recommended maximum level of 3 % of annual assessments. As of December 31, 2013, the assessments receivable balance represents approximately 1 %, which is excellent.

The designated replacement reserves of $112,858 were funded by cash, interest-bearing deposits, and investments as of December 31, 2013.

Service Organization Control (SOC) Report

Professional standards require that we evaluate the effect of the internal controls at service organizations on the Association's financial statements. During 2013, the Association contracted with Scheffres Laundry to collect laundry income and, accordingly these activities were not processed through the Association's account and internal control systems. As a result, the control process of Scheffres Laundry is relevant to the Association's ability to prevent, detect and correct errors that may occur through the service organizations billing and collection activities. To assist user auditors

phone 703 3919003 fax 703 391 9004 www.GGroupCPAs.com

(and the user entity) in evaluating these processes, certain service organizations are required to engage firms to complete an internal control audit and produce Service Organization Control (SOC) reports. Based on discussions with Scheffres Laundry, they have not obtained a SOC report and, accordingly, we cannot evaluate the effect of their internal controls on the Association's financial statements. The audit opinion was qualified for this reason.

Account Receivable - Other

As of December 31, 2013, the Association's financial statements still reflect a receivable of $6,680 from Tru Green Landscape for a duplicate payment in 2008. We continue to recommend the Association pursue a refund or consider writing off this amount; write-offs should be documented in the meeting minutes.

Duplicate Payments

During our examination of the Association's expenses, we noticed the Association paid its garbage vendor twice for the February 2013 garbage collection. We recommend the Association contact the vendor to obtain a refund.

Additionally, the Association paid for 6 applications for Integrated Plant Management services, including a duplicate charge for service on July 25, 2013. The Integrated Plant Management contract calls for 5 applications. We recommend the Association contact the vendor and obtain a refund.

- I

Tax Refund __ , _____ ,_, ,,",,,,, .. ,8-'"

.l

As of December! 31,12013,\ the r[ir;di $'408 due from the Commonwealth of Virginia/ for/:'20Ll. ; We 'protj-iptly contact the Commonwealth Vir,ginia/to qollect ithe -remaini11g 4D 1 J refund before statute of limitations expires.

..... > c: ·:.. ,::• \ •.. .:. :: \.

. ...... .

Due to Related Communities

The Association is owed a net of $4,125 from Colonial Village III (CVIII) for services in 2012 and 2013 that were paid on behalf of the Association by CVII. The breakdown is as follows:

Water bills paid in 2012 by CVII for CVIII 2013 Administrative Salary paid by CVII for CVIII CVIII's November 2013 Laundry Commission Received by CVII

Net Due From CVIII

$ 3,840 1,367

(l,082) $ 4.125

Additionally, the Association is owed $324 from Colonial Village I (CVI) for 2012 salaries and related payroll expenses.

We recommend the Association pursue collection of these amounts from CVI and CVIII.

Payroll Chargebacks

As of December 31, 2013, there is a remaining balance due to management of $385 for 2012 and 2013 net payroll activity.

2

Contribution to Reserves

According to the 2013 reserve study's recommendations, the Association's replacement reserve balance does not appear to be sufficient. The study recommends a balance at year-end of $382,736. As of December 31, 2013, the Association had $112,858 designated for replacement reserves. The Association needs to accumulate sufficient funds for replacement reserves or, when repairs or replacements are necessary the funds will not be available. We recommend the Association consider whether an additional contribution is necessary.

Late Fees on Expenses

During 2013, the Association incurred penalties for late payments of certain utility bills. Because of the steepness of these penalties and to avoid having to pay deposits, the Association should make every effort to pay invoices in a timely manner.

Insurance

We recommend the Association meet with its insurance agent at least annually to discuss insurance coverage. The Association should make sure the insurance policies provide the necessary and appropriate protection. In addition to all of the standard coverage that is usually recommended, the Association should maintain appropriate crime and directors & officers (D&O) coverage. At a minimum, the Association should maintain crime coverage that equals or exceeds the total of its funds or as It should be structured to include a mis1appropriation committed by a Boardf employee of the Association, the management company, includiqg principals>.

.. . ·1 '.; i; '}

Federal Deposit Irtsurabce Corlooratlon fFDIC)

The FDIC monitor its accounts and lnllnediately transfer :fuilds in excess of the FDIC limff to-- other instifutions or Treasury instruments so all Association funds will be insured. The Association should also periodically check the ratings for all financial institutions used by the Association.

Income Taxes

For 2013, we recommend the Association file using the corporate method.

We shall be pleased to discuss our comments and recommendations in greater detail and we are always available to give advice on any financial matter. Please do not hesitate to contact us if there are any questions regarding proper accounting procedures or the implementation of our suggested changes.

Very truly yours,

GOLDKLANG GROUP CPAs, P.C.

3

Principals Howard A. Goldklang1 CPA1 MBA Donald E. Harris, CPA Anne M. Sheehan, CPA S. Gail Moore, CPA

1801 Robert Fulton Drive, Suite 200 Reston1 VA 20191

Associate Principals Jeremy W. Powell 1 CPA Renee L. Watson, CPA

Managers Allison A. Day, CPA

Matthew T. Stiefvater1 CPA

Communication with Those Charged with Governance under SAS No. 114 This communication is intended solely for the information and use of management and the board of directors and is not intended to be and should not be used by anyone other than these specified parties.

May 6,2014

Board of Directors Colonial Village (Village II), A Condominium

Dear Board Members:

We have audited'hhe of Colonial Village (ViV'ag9 FI),)1?:,/Cpndominium as of December 31, 2013 an,d for ·t.he Professional standards require that ;we provide Jbout ourj: tinder generally accepted auditing .stanqards, we1J as 9erteyin elaied to;i the 2plantjed srope and timing of our audit. We such: inf Pref es .. sional standards also require thatjve commuTii.cate. to the.Jollowii1:g ilifori.nati,pn IelateqJo ow au<jit

• ·.:::···.· ... ···: ••..••.•• ,.. •. '·.·, .. ··:.·.-,:·::·.:»···:;·-·:·=· .• •• . ...-.•. •• ,., •.... :· •. -·· • . • .-.. :·>·. '':.. . . .. ··. '· :· C'. : •••. •;,. ••• , ••• _. .•.••• .,.,-, • . ···\':·····. •• • •••

Our Responsibility under U.S. Generally Accepted Auditing Standards

As stated in our engagement letter, our responsibility, as described by professional standards, is to express an opinion about whether the financial statements prepared by management with your oversight are fairly presented, in all material respects, in conformity with U.S. generally accepted accounting principles. Our audit of the financial statements does not relieve you or management of your responsibilities.

Our responsibility for the supplementary information required by the Financial Accounting Standards Board, as described by professional standards, is to apply certain limited procedures to the information about management's methods of preparing the information; however, we will not express an opinion or any assurance on the information.

Planned Scope and Timing of the Audit

An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements; therefore, our audit will involve judgment about the number of transactions to be examined and the areas to be tested.

Our audit will include obtaining an understanding of the CIRA and its environment, including internal control, sufficient to assess the risks of material misstatement of the financial statements and

phone 703 3919003 fax 703 3919004 www.GGroupCPAs.com

to design the nature, timing, and extent of further audit procedures. Material misstatements may result from (1) errors, (2) fraudulent financial reporting, (3) misappropriation of assets, or (4) violations of laws or governmental regulations that are attributable to the Association or to acts by management or employees acting on behalf of the Association. We will generally communicate our significant findings at the conclusion of the audit. However, some matters could be communicated sooner, particularly if significant difficulties are encountered during the audit where assistance is needed to overcome the difficulties or if the difficulties may lead to a modified opinion. We will also communicate any internal control related matters that are required to be communicated under professional standards.

Significant Audit Findings

Qualitative Aspects of Accounting Practices

Management is responsible for the selection and use of appropriate accounting policies. The significant accounting policies used by the Association are described in Note 2 to the financial statements. No new accounting policies were adopted and the application of existing policies was not changed during the year. We noted no transactions entered into by the Association during the year for which there is a lack of authoritative guidance or consensus. All significant transactions have been recognized in the financial statements in the proper period.

Accounting estimates are an integral part of the financial statements prepared by management and are based on and experience about past and and assumptions about future events. estimates are particulaf1y because of their significance to the affecting them may differ tho$e no acpounting estimates for the year under audit. , ,

Certain .. .. e 011 .. to

financial statement users. There were no significant discloslires to the financiaf statements for the year under audit.

The financial statement disclosures are neutral, consistent, and clear.

Difficulties Encountered in Performing the Audit

We encountered no significant difficulties in dealing with management in performing and completing our audit. However, we were unable to obtain a Service Organization Control (SOC) report from the Association's laundry service provider as required by auditing standards.

Corrected and Uncorrected Misstatements

Professional standards require us to accumulate all misstatements identified during the audit, other than those that are clearly trivial, and communicate them to the appropriate level of management. The adjusting journal entries have been provided to the Association. The journal entries are material, either individually or in the aggregate, to the financial statements.

Disagreements with Management

For purposes of this letter, a disagreement with management is a financial accounting, reporting, or auditing matter, whether or not resolved to our satisfaction, that could be significant to the financial

2

statements or the auditor's report. We are pleased to report that no such disagreements arose during the course of our audit.

Management Representations

We have requested certain representations from management that are included in the management representation letter.

Management Consultations with Other Independent Accountants

In some cases, management may decide to consult with other accountants about auditing and accounting matters, similar to obtaining a "second opinion" on certain situations. If a consultation involves application of an accounting principle to the Association's financial statements or a determination of the type of auditor's opinion that may be expressed on those statements, our professional standards require the consulting accountant to check with us to determine that the consultant has all the relevant facts. To our knowledge, there were no such consultations with other accountants.

Other Audit Findings or Issues

We generally discuss a variety of matters, including the application of accounting principles and auditing standards, with management each year prior to retention as the Association's auditors. However, in the normal course of our and our responses were not a cql1dfriqn-fo"'pur retention. - , -,, _____ f_,,,=,_,,;:"r __ -,

Required Suppl emf ntar.y Infotmatid.n

With respect to ie by Standards Board, we management about their methods of preparing the information; comparing the information for consistency with management's responses to the foregoing inquiries, the basic financial statements, and other knowledge obtained during the audit of the basic financial statements; and obtaining certain representations from management, including about whether the required supplementary information is measured and presented in accordance with prescribed guidelines.

Very truly yours,

GOLDKLANG GROUP CPAs, P.C.

3

Principals Howard A. Goldklang, CPA, MBA Donald E. Harris, CPA Anne M. Sheehan, CPA S. Gail Moore, CPA

1801 Robert Fu !ton Drive1 Suite 200 Reston, VA 20191

Associate Principals Jeremy W. Powell, CPA Renee L. Watson, CPA

Managers Allison A. Day, CPA

Matthew T. Stiefvater1 CPA

Communication of Significant Deficiencies and/or Material Weaknesses under SAS No. 115 This communication is intended solely for the information and use of management and the board of directors and is not intended to be and should not be used by anyone other than these specified parties.

May 6, 2014

Board of Directors Colonial Village (Village II), A Condominium

Dear Board Members: ·.;-;.-:;:•:\O:":·.·,········.-·.· .... ,.. ..

In planning and of the financial statements of (Village II), A Condominium as of 31\ 20l3 .. with auditing standards generally acc;epted in the S"tatesof w-,e coiisidere<l internal control over financial cqntrol) as f9r des1gnip.g aupit Rrocedures that are appropriate in_ thf for s the. purpos7,·· OUf 0)1 the financial statements, but .. <?!'·;the Association's internal control. Accord111gly, we do not express an op1nion' ori the-'diect!veness"o:f the Association's internal control.

Our consideration of internal control was for the limited purpose described in the preceding paragraph and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies and, therefore, material weaknesses or significant deficiencies may exist that were not identified. However, as discussed below, we identified certain deficiencies in internal control that we consider to be material weaknesses or other deficiencies that we consider to be significant deficiencies.

A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the Association's financial statements will not be prevented, or detected and corrected, on a timely basis. We consider the following to be material weaknesses or significant deficiencies in internal control:

phone 703 391 9003 fax 703 391 9004 www .GGroupCPAs.com

Report Qualification - Scheffres Laundry SOC Report

Professional standards require that we evaluate the effect of the internal controls at service organizations on the Association's financial statements. During 2013, the Association contracted with Scheffres Laundry to collect laundry income and, accordingly, these activities were not processed through the Association's accounting and internal control systems. As a result, the internal controls of Scheffres Laundry are relevant to the Association's ability to prevent, detect and correct errors that may occur through the service organizations billing and collection activities. To assist user auditors (and the user entity) in evaluating these processes, certain service organizations are required to engage firms to complete an internal control audit and produce Service Organization Control (SOC) reports. Based on discussions with Scheffres Laundry, they have not obtained a SOC report and, accordingly, we cannot evaluate the effect of their controls on the Association's financial statements. The audit opinion was qualified for this reason.

Very truly yours,

GOLDKLANG GROUP CPAs, P.C.

2

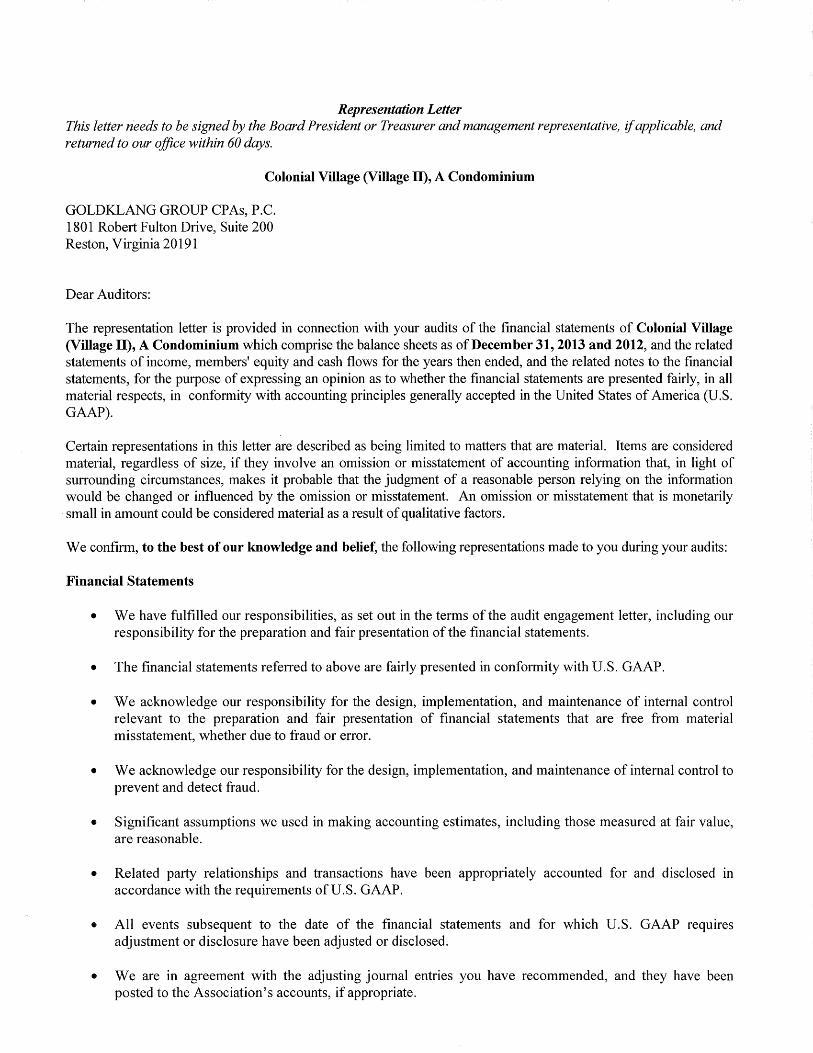

Representation Letter This letter needs to be signed by the Board President or Treasurer and management representative, if applicable, and returned to our office within 60 days.

Colonial Village (Village II), A Condominium

GOLDKLANG GROUP CPAs, P.C. 1801 Robert Fulton Drive, Suite 200 Reston, Virginia 20191

Dear Auditors:

The representation letter is provided in connection with your audits of the financial statements of Colonial Village (Village II}, A Condominium which comprise the balance sheets as of December 31, 2013 and 2012, and the related statements of income, members' equity and cash flows for the years then ended, and the related notes to the financial statements, for the purpose of expressing an opinion as to whether the financial statements are presented fairly, in all material respects, in conformity with accounting principles generally accepted in the United States of America (U.S. GAAP).

Certain representations in this letter are described as being limited to matters that are material. Items are considered material, regardless of size, if they involve an omission or misstatement of accounting information that, in light of surrounding circumstances, makes it probable that the judgment of a reasonable person relying on the information would be changed or influenced by the omission or misstatement. An omission or misstatement that is monetarily small in amount could be considered material as a result of qualitative factors.

We confirm, to the best of our knowledge and belief, the following representations made to you during your audits:

Financial Statements

• We have fulfilled our responsibilities, as set out in the terms of the audit engagement letter, including our responsibility for the preparation and fair presentation of the financial statements.

• The financial statements referred to above are fairly presented in conformity with U.S. GAAP.

• We acknowledge our responsibility for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

• We acknowledge our responsibility for the design, implementation, and maintenance of internal control to prevent and detect fraud.

• Significant assumptions we used in making accounting estimates, including those measured at fair value, are reasonable.

• Related party relationships and transactions have been appropriately accounted for and disclosed in accordance with the requirements of U.S. GAAP.

• All events subsequent to the date of the financial statements and for which U.S. GAAP requires adjustment or disclosure have been adjusted or disclosed.

• We are in agreement with the adjusting journal entries you have recommended, and they have been posted to the Association's accounts, if appropriate.

• We are not aware of any pending or threatened litigation, claims, or assessments or unasserted claims or assessments that are required to be accrued or disclosed in the financial statements in accordance with U.S. GAAP, and we have not consulted a lawyer concerning pending litigation, claims, or assessments.

• Material concentrations have been properly disclosed in accordance with U.S. GAAP.

• Guarantees, whether written or oral, under which the Association is contingently liable, have been properly recorded or disclosed in accordance with U.S. GAAP.

• Transfers or designations of equity balance or inter-equity borrowings have been properly authorized and approved and have been properly recorded or disclosed in accordance with U.S. GAAP.

• Uncollectible inter-equity loans have been properly accounted for and disclosed in accordance with U.S. GAAP.

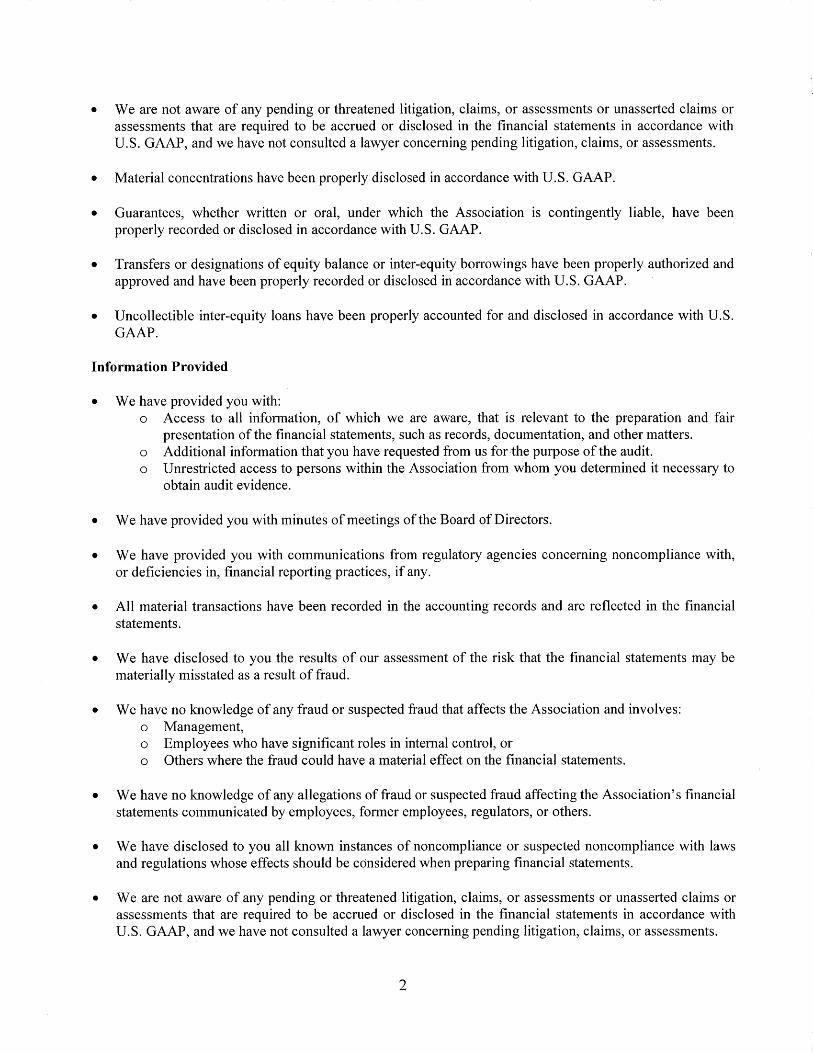

Information Provided

• We have provided you with: o Access to all information, of which we are aware, that is relevant to the preparation and fair

presentation of the financial statements, such as records, documentation, and other matters. o Additional information that you have requested from us for the purpose of the audit. o Unrestricted access to persons within the Association from whom you determined it necessary to

obtain audit evidence.

• We have provided you with minutes of meetings of the Board of Directors.

• We have provided you with communications from regulatory agencies concerning noncompliance with, or deficiencies in, financial reporting practices, if any.

• All material transactions have been recorded in the accounting records and are reflected in the financial statements.

• We have disclosed to you the results of our assessment of the risk that the financial statements may be materially misstated as a result of fraud.

• We have no knowledge of any fraud or suspected fraud that affects the Association and involves: o Management, o Employees who have significant roles in internal control, or o Others where the fraud could have a material effect on the financial statements.

• We have no knowledge of any allegations of fraud or suspected fraud affecting the Association's financial statements communicated by employees, former employees, regulators, or others.

• We have disclosed to you all known instances of noncompliance or suspected noncompliance with laws and regulations whose effects should be considered when preparing financial statements.

• We are not aware of any pending or threatened litigation, claims, or assessments or unasserted claims or assessments that are required to be accrued or disclosed in the financial statements in accordance with U.S. GAAP, and we have not consulted a lawyer concerning pending litigation, claims, or assessments.

2

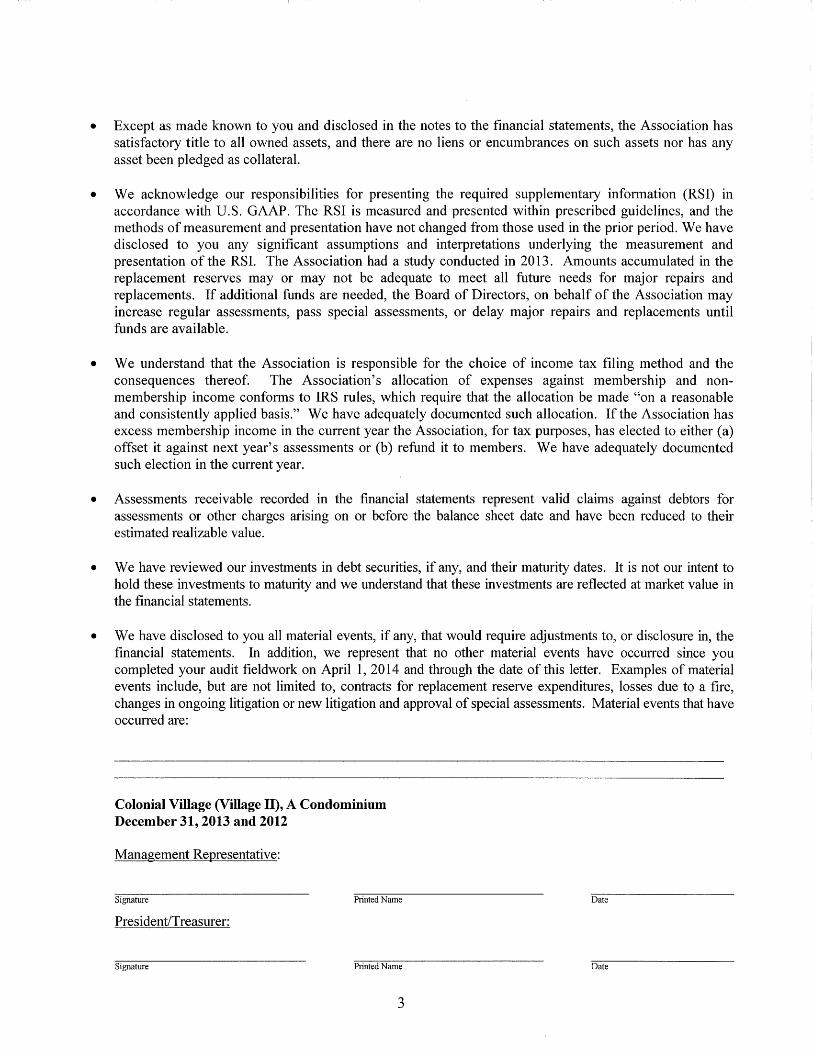

• Except as made known to you and disclosed in the notes to the financial statements, the Association has satisfactory title to all owned assets, and there are no liens or encumbrances on such assets nor has any asset been pledged as collateral.

• We acknowledge our responsibilities for presenting the required supplementary information (RSI) in accordance with U.S. GAAP. The RSI is measured and presented within prescribed guidelines, and the methods of measurement and presentation have not changed from those used in the prior period. We have disclosed to you any significant assumptions and interpretations underlying the measurement and presentation of the RSI. The Association had a study conducted in 2013. Amounts accumulated in the replacement reserves may or may not be adequate to meet all future needs for major repairs and replacements. If additional funds are needed, the Board of Directors, on behalf of the Association may increase regular assessments, pass special assessments, or delay major repairs and replacements until funds are available.

• We understand that the Association is responsible for the choice of income tax filing method and the consequences thereof. The Association's allocation of expenses against membership and non-membership income conforms to IRS rules, which require that the allocation be made "on a reasonable and consistently applied basis." We have adequately documented such allocation. If the Association has excess membership income in the current year the Association, for tax purposes, has elected to either (a) offset it against next year's assessments or (b) refund it to members. We have adequately documented such election in the current year.

• Assessments receivable recorded in the financial statements represent valid claims against debtors for assessments or other charges arising on or before the balance sheet date and have been reduced to their estimated realizable value.

• We have reviewed our investments in debt securities, if any, and their maturity dates. It is not our intent to hold these investments to maturity and we understand that these investments are reflected at market value in the financial statements.

• We have disclosed to you all material events, if any, that would require adjustments to, or disclosure in, the financial statements. In addition, we represent that no other material events have occurred since you completed your audit fieldwork on April 1, 2014 and through the date of this letter. Examples of material events include, but are not limited to, contracts for replacement reserve expenditures, losses due to a fire, changes in ongoing litigation or new litigation and approval of special assessments. Material events that have occurred are:

Colonial Village (Village II), A Condominium December 31, 2013 and 2012

Management Representative:

Signature Printed Name

President/Treasurer:

Signature Printed Name

3

Date

Date

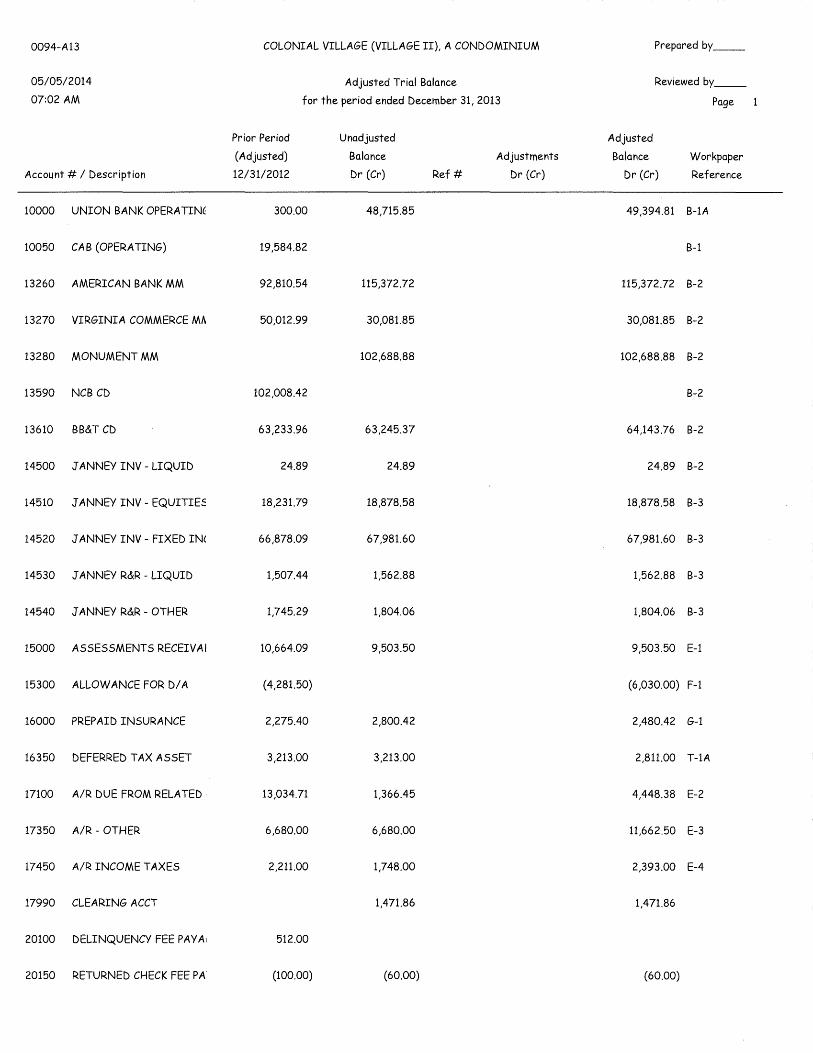

0094-A13 COLONIAL VILLAGE (VILLAGE II), A CONDOMINIUM Prepared by __

05/05/2014 Adjusted Trial Balance Reviewed by __ 07:02 AM for the period ended December 31, 2013 Page

Prior Period Unadjusted Adjusted (Adjusted) Balance Adjustments Balance Workpaper

Account # I Description 12/31/2012 Dr (Cr) Ref# Dr (Cr) Dr (Cr) Reference

10000 UNION BANK OPERA 300.00 48,715.85 49,394.81 B-1A

10050 CAB (OPERATING) 19,584.82 B-1

13260 AMERICAN BANK MM 92,810.54 115,372.72 115,372.72 B-2

13270 VIRGINIA COMMERCE MA 50,012.99 30,081.85 30,081.85 B-2

13280 MONUMENT MM 102,688.88 102,688.88 B-2

13590 NCB CD 102,008.42 B-2

13610 BB&T CD 63,233.96 63,245.37 64,143.76 B-2

14500 JANNEY INV - LIQUID 24.89 24.89 24.89 B-2

14510 JANNEY INV - EQUITIE.: 18,231.79 18,878.58 18,878.58 B-3

14520 JANNEY INV - FIXED IN( 66,878.09 67,981.60 67,981.60 B-3

14530 JANNEY R&R - LIQUID 1,507.44 1,562.88 1,562.88 B-3

14540 JANNEY R&R - OTHER 1,745.29 1,804.06 1,804.06 B-3

15000 ASSESSMENTS RECEIVAI 10,664.09 9,503.50 9,503.50 E-1

15300 ALLOWANCE FORD/A (4,281.50) (6,030.00) F-1

16000 PREPAID INSURANCE 2,275.40 2,800.42 2,480.42 G-1

16350 DEFERRED TAX ASSET 3,213.00 3,213.00 2,811.00 T-lA

17100 AIR DUE FROM RELATED · 13,034.71 1,366.45 4,448.38 E-2

17350 AIR- OTHER 6,680.00 6,680.00 11,662.50 E-3

17450 A/R INCOME TAXES 2,211.00 1,748.00 2,393.00 E-4

17990 CLEARING ACCT 1,471.86 1,471.86

20100 DELINQUENCY FEE PAYA1 512.00

20150 RETURNED CHECK FEE PA (100.00) (60.00) (60.00)

0094-Al3 COLONIAL VILLAGE (VILLAGE II), A CONDOMINIUM Prepared by __

05/05/2014 Adjusted Trial Balance Reviewed by __ 07:02 AM for the period ended December 31, 2013 Page 2

Prior Period Unadjusted Adjusted (Adjusted) Balance Adjustments Balance Workpaper

Account# I Description 12/31/2012 Dr (Cr) Ref# Dr (Cr) Dr (Cr) Reference

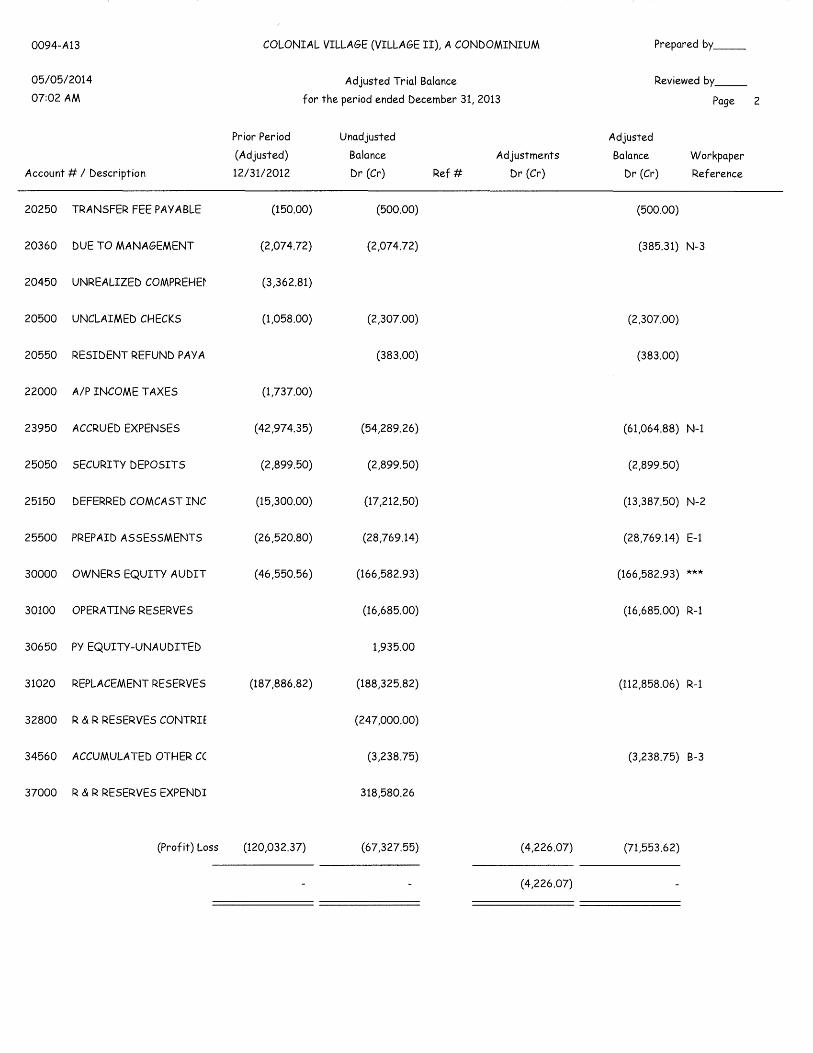

20250 TRANSFER FEE PAYABLE (150.00) (500.00) (500.00)

20360 DUE TO MANAGEMENT (2,074.72) (2,074.72) (385.31) N-3

20450 UNREALIZED COMPREHEt (3,362.81)

20500 UNCLAIMED CHECKS (1,058.00) (2,307.00) (2,307.00)

20550 RESIDENT REFUND PAYA (383.00) (383.00)

22000 A/P INCOME TAXES (1,737.00)

23950 ACCRUED EXPENSES (42,974.35) (54,289.26) (61,064.88) N-1

25050 SECURITY DEPOSITS (2,899.50) (2,899.50) (2,899.50)

25150 DEFERRED COMCAST INC (15,300.00) (17,212.50) (13 ,387.50) N-2

25500 PREPAID ASSESSMENTS (26 ,520.80) (28,769.14) (28,769.14) E-1

30000 OWNERS EQUITY AUDIT (46,550.56) (166,582.93) (166,582.93) ***

30100 OPERA TING RESERVES (16,685.00) (16,685.00) R-1

30650 PY EQUITY-UNAUDITED 1,935.00

31020 REPLACEMENT RESERVES (187,886.82) (188,325.82) (112,858.06) R-1

32800 R & R RESERVES CONTRIE (247,000.00)

34560 ACCUMULATED OTHER CC (3,238.75) (3,238.75) B-3

37000 R & R RESERVES EXPENDI 318,580.26

(Profit) Loss (120,032.37) (6 7,327.55) (4,226.07) (71,553.62)

(4,226.07)

0094-A13 COLONIAL VILLAGE (VILLAGE II), A CONDOMINIUM Prepared by __

05/05/2014 Adjusted Trial Balance Reviewed by __ 07:02 AM for the period ended December 31, 2013 Page 3

Prior Period Unadjusted Adjusted (Adjusted) Balance Adjustments Balance Workpaper

Account # I Description 12/31/2012 Dr (Cr) Ref# Dr (Cr) Dr (Cr) Reference

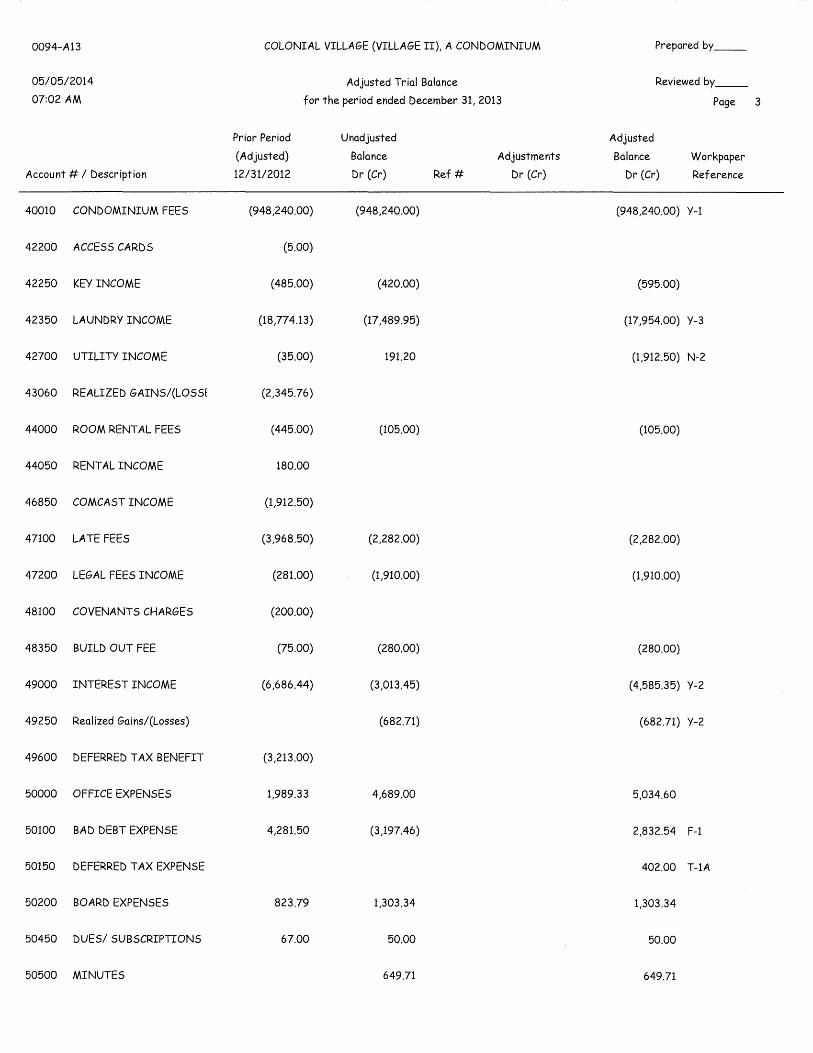

40010 CONDOMINIUM FEES (948,240.00) (948,240.00) (948,240.00) Y-1

42200 ACCESS CARDS (5.00)

42250 KEY INCOME (485.00) (420.00) (595.00)

42350 LAUNDRY INCOME (18,774.13) (17,489.95) (17,954.00) Y-3

42700 UTILITY INCOME (35.00) 191.20 (1,912.50) N-2

43060 REALIZED GAINS/(LOSSI (2,345.76)

44000 ROOM RENT AL FEES (445.00) (105.00) (105.00)

44050 RENT AL INCOME 180.00

46850 COMCAST INCOME (1,912.50)

47100 LATE FEES (3,968.50) (2,282.00) (2,282.00)

47200 LEGAL FEES INCOME (281.00) (1,910.00) (1,910.00)

48100 COVENANTS CHARGES (200.00)

48350 BUILD OUT FEE (75.00) (280.00) (280.00)

49000 INTEREST INCOME (6,686.44) (3,013.45) (4,585.35) Y-2

49250 Realized Gains/(Losses) (682.71) (682.71) Y-2

49600 DEFERRED TAX BENEFIT (3,213.00)

50000 OFFICE EXPENSES 1,989.33 4,689.00 5,034.60

50100 BAD DEBT EXPENSE 4,281.50 (3,197.46) 2,832.54 F-1

50150 DEFERRED TAX EXPENSE 402.00 T-lA

50200 BOARD EXPENSES 823.79 1,303.34 1,303.34

50450 DUES/ SUBSCRIPTIONS 67.00 50.00 50.00

50500 MINUTES 649.71 649.71

0094-A13 COLONIAL VILLAGE (VILLAGE II), A CONDOMINIUM Prepared by __

05/05/2014 Adjusted Trial Balance Reviewed by __ 07:02 AM for the period ended December 31, 2013 Page 4

Prior Period Unadjusted Adjusted (Adjusted) Balance Adjustments Balance Workpaper

Account # I Description 12/31/2012 Dr (Cr) Ref# Dr (Cr) Dr (Cr) Reference

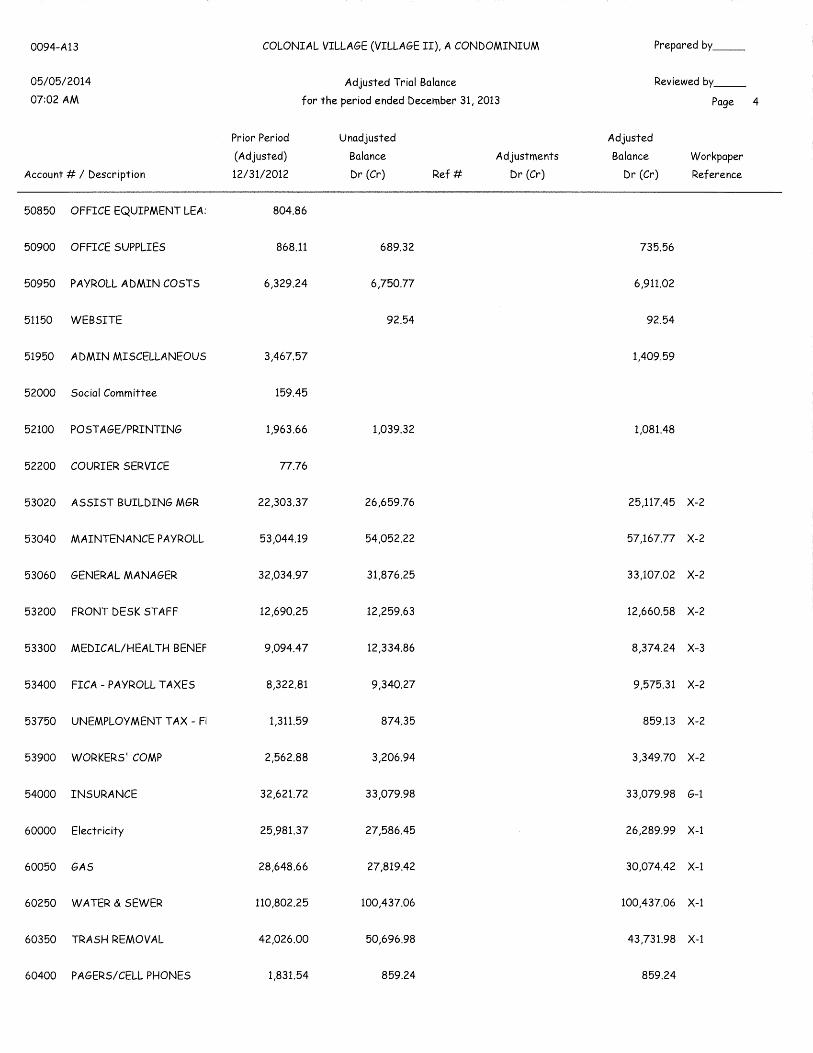

50850 OFFICE EQUIPMENT LEA: 804.86

50900 OFFICE SUPPLIES 868.11 689.32 735.56

50950 PAYROLL ADMIN COSTS 6,329.24 6,750.77 6,911.02

51150 WEBSITE 92.54 92.54

51950 ADMIN MISCELLANEOUS 3,467.57 1,409.59

52000 Social Committee 159.45

52100 POSTAGE/PRINTING 1,963.66 1,039.32 1,081.48

52200 COURIER SERVICE 77.76

53020 ASSIST BUILDING MGR 22,303.37 26,659.76 25,117.45 X-2

53040 MAINTENANCE PAYROLL 53,044.19 54,052.22 57,167.77 X-2

53060 GENERAL MANAGER 32,034.97 31,876.25 33,107.02 X-2

53200 FRONT DESK STAFF 12,690.25 12,259.63 12,660.58 X-2

53300 MEDICAL/HEAL TH BENEF 9,094.47 12,334.86 8,374.24 X-3

53400 FICA - PAYROLL TAXES 8,322.81 9,340.27 9,575.31 X-2

53750 UNEMPLOYMENT TAX - Fl 1,311.59 874.35 859.13 X-2

53900 WORKERS' COMP 2,562.88 3,206.94 3,349.70 X-2

54000 INSURANCE 32,621.72 33,079.98 33,079.98 G-1

60000 Electricity 25,981.37 27,586.45 26,289.99 X-1

60050 GAS 28,648.66 27,819.42 30,074.42 X-1

60250 WATER & SEWER 110,802.25 100,437.06 100,437.06 X-1

60350 TRASH REMOVAL 42,026.00 50,696.98 43,731.98 X-1

60400 PAGERS/CELL PHONES 1,831.54 859.24 859.24

0094-A13 COLONIAL VILLAGE (VILLAGE II), A CONDOMINIUM Prepared by __

05/05/2014 Adjusted Trial Balance Reviewed by __

07:02 AM for the period ended December 31, 2013 Page 5

Prior Period Unadjusted Adjusted (Adjusted) Balance Adjustments Balance Workpaper

Account # I Description 12/31/2012 Dr (Cr) Ref# Dr (Cr) Dr (Cr) Reference

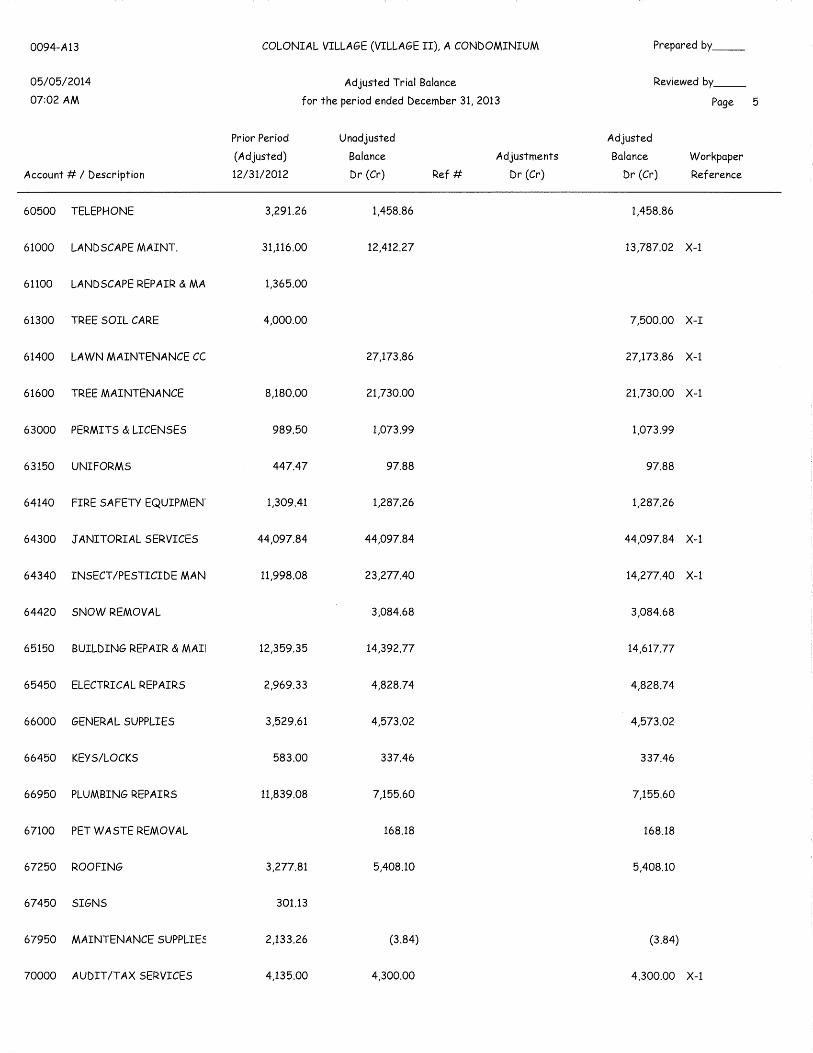

60500 TELEPHONE 3,291.26 1,458.86 1,458.86

61000 LANDSCAPE MAINT. 31,116.00 12,412.27 13,787.02 X-1

61100 LANDSCAPE REPAIR & MA 1,365.00

61300 TREE SOIL CARE 4,000.00 7,500.00 X-I

61400 LAWN MAINTENANCE CC 27,173.86 27,173.86 X-1

61600 TREE MAINTENANCE 8,180.00 21,730.00 21,730.00 X-1

63000 PERMITS & LICENSES 989.50 1,073.99 1,073.99

63150 UNIFORMS 447.47 97.88 97.88

64140 FIRE SAFETY EQUIPMEN' 1,309.41 1,287.26 1,287.26

64300 JANITORIAL SERVICES 44,097.84 44,097.84 44,097.84 X-1

64340 INSECT /PESTICIDE MAN 11,998.08 23,277.40 14,277.40 X-1

64420 SNOW REMOVAL 3,084.68 3,084.68

65150 BUILDING REPAIR & MAii 12,359.35 14,392.77 14,617.77

65450 ELECTRICAL REPAIRS 2,969.33 4,828.74 4,828.74

66000 GENERAL SUPPLIES 3,529.61 4,573.02 4,573.02

66450 KEYS/LOCKS 583.00 337.46 337.46

66950 PLUMBING REPAIRS 11,839.08 7,155.60 7,155.60

67100 PET WASTE REMOVAL 168.18 168.18

67250 ROOFING 3,277.81 5,408.10 5,408.10

67450 SIGNS 301.13

67950 MAINTENANCE 2,133.26 (3.84) (3.84)

70000 AUDIT /TAX SERVICES 4,135.00 4,300.00 4,300.00 X-1

0094-Al3 COLONIAL VILLAGE (VILLAGE II), A CONDOMINIUM Prepared by __

05/05/2014 Adjusted Trial Balance Reviewed by __

07:02 AM for the period ended December 31, 2013 Page 6

Prior Period Unadjusted Adjusted (Adjusted) Balance Adjustments Balance Workpaper

Account # I Description 12/31/2012 Dr (Cr) Ref# Dr (Cr) Dr (Cr) Reference

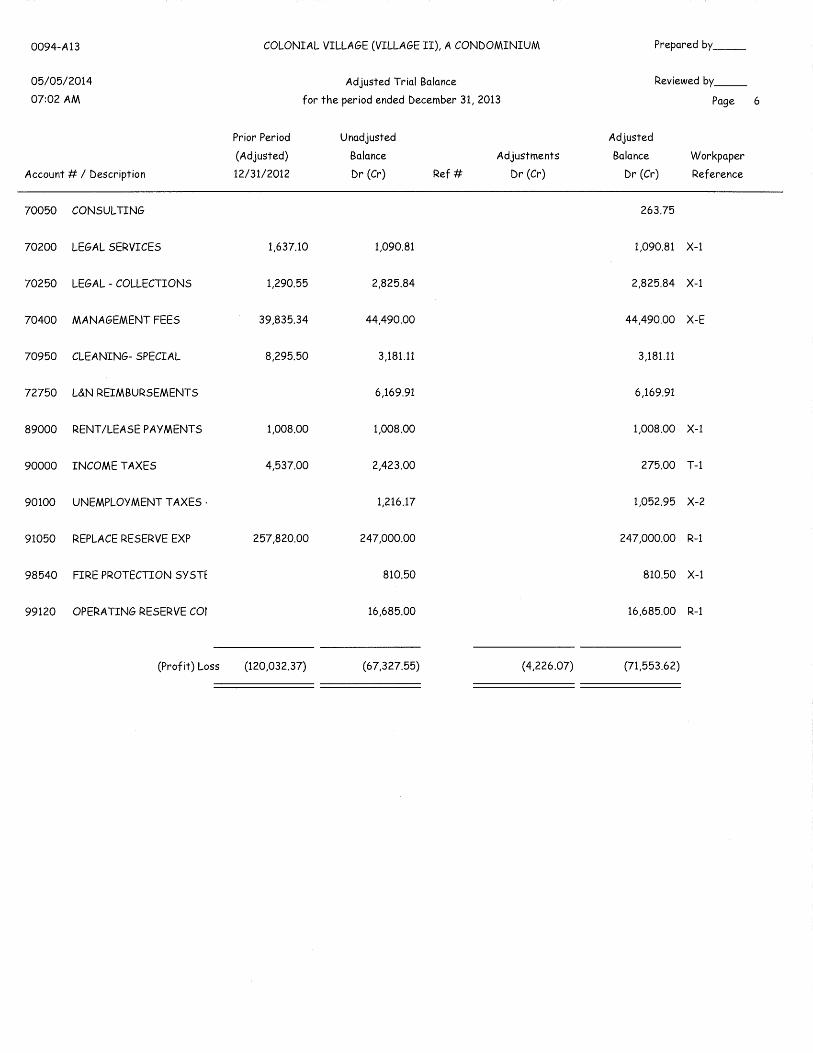

70050 CONSULTING 263.75

70200 LEGAL SERVICES 1,637.10 1,090.81 1,090.81 X-1

70250 LEGAL - COLLECTIONS 1,290.55 2,825.84 2,825.84 X-1

70400 MANAGEMENT FEES 39,835.34 44,490.00 44,490.00 X-E

70950 CLEANING- SPECIAL 8,295.50 3,181.11 3,181.11

72750 L&N REIMBURSEMENTS 6,169.91 6,169.91

89000 RENT/LEASE PAYMENTS 1,008.00 1,008.00 1,008.00 X-1

90000 INCOME TAXES 4,537.00 2,423.00 275.00 T-1

90100 UNEMPLOYMENT TAXES · 1,216.17 1,052.95 X-2

91050 REPLACE RESERVE EXP 257,820.00 247,000.00 247,000.00 R-1

98540 FIRE PROTECTION SY STE 810.50 810.50 X-1

99120 OPERA TING RESERVE cor 16,685.00 16,685.00 R-1

(Prof it) Loss (120,032.37) (67,327.55) (4,226.07) (71,553.62)

0094-A13

05/05/2014 07:02 AM

Account#

COLONIAL VILLAGE (VILLAGE 11), A CONDOMINIUM

Adjusting Journal Entries for the period ended December 31, 2013 Page

Account Name I Description Debits Credits

Totals