Embed Size (px)

Citation preview

A market leader in retail logistics

Logistics evolved: Agility and Ability

2016 Interim Results Presentation 3 December 2015

2

Disclaimer

This presentation includes statements that are, or may be deemed to be, “forward-looking statements”. These forward-looking statements can be identified by the use of forward-looking terminology, including the terms “believe”, “estimates”, “plans”, “projects”, “anticipates”, “expects”, “intends”, “may”, “will”, or “should” or, in each case, their negative or other variations or comparable terminology. These forward-looking statements include matters that are not historical facts and include statements regarding the Company’s intentions, beliefs or current expectations.

Any forward-looking statements in this presentation reflect the Company’s current expectations and projections about future events. By their nature, forward-looking statements involve a number of risks, uncertainties and assumptions that could cause actual results or events to differ materially from those expressed or implied by the forward-looking statements. These risks, uncertainties and assumptions could adversely affect the outcome and financial effects of the plans and events described herein. Forward-looking statements contained in this presentation regarding past trends or activities should not be taken as a representation that such trends or activities will continue in the future. You should not place undue reliance on forward-looking statements, which speak only as of the date of this presentation. No representations or warranties are made as to the accuracy of such statements, estimates or projections.

Please note that the Directors of the Company are, in making this presentation, not seeking to encourage shareholders to either buy or sell shares in the Company. Shareholders in any doubt about what action to take are recommended to seek financial advice from an independent financial advisor authorised by the Financial Services and Markets Act 2000.

3

Agenda

Highlights – Steve Parkin 1

Financial review – David Hodkin 2

Operational review – Tony Mannix 3

Summary and Q&A – Steve Parkin 4

Highlights 1

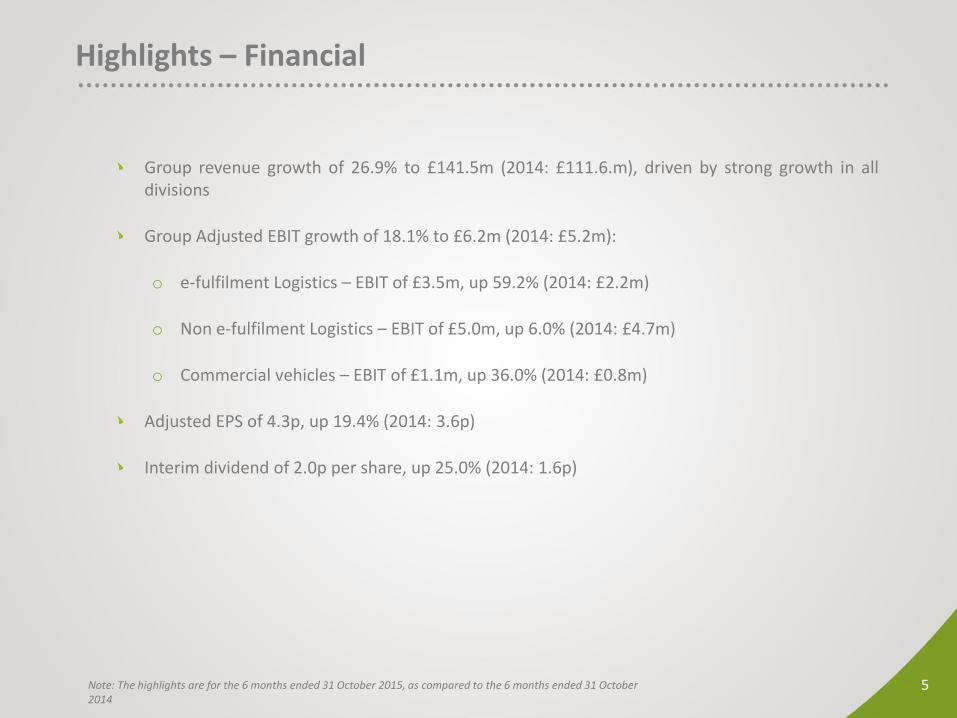

Highlights – Financial

Group revenue growth of 26.9% to £141.5m (2014: £111.6.m), driven by strong growth in all divisions

Group Adjusted EBIT growth of 18.1% to £6.2m (2014: £5.2m):

o e-fulfilment Logistics – EBIT of £3.5m, up 59.2% (2014: £2.2m)

o Non e-fulfilment Logistics – EBIT of £5.0m, up 6.0% (2014: £4.7m)

o Commercial vehicles – EBIT of £1.1m, up 36.0% (2014: £0.8m)

Adjusted EPS of 4.3p, up 19.4% (2014: 3.6p)

Interim dividend of 2.0p per share, up 25.0% (2014: 1.6p)

5 Note: The highlights are for the 6 months ended 31 October 2015, as compared to the 6 months ended 31 October 2014

6

Highlights – Operational

Continued transition of retail activity to online driving growth with new and existing customers

Click and Collect collaboration with John Lewis Partnership commenced – KPIs consistently attained

o Rollout across estate and into third parties, calendar 2016

Commenced several new operations in the period:

o E-fulfilment for a major international retailer

o Warehousing and returns for Pep&Co

o Implemented new contract with Philip Morris

o Click and Collect services for John Lewis

Continuing strong pipeline of new business opportunities

Servicecare acquired December 2014, delivering results in line with expectations

Strong performance from commercial vehicles business

Financial review 2

8

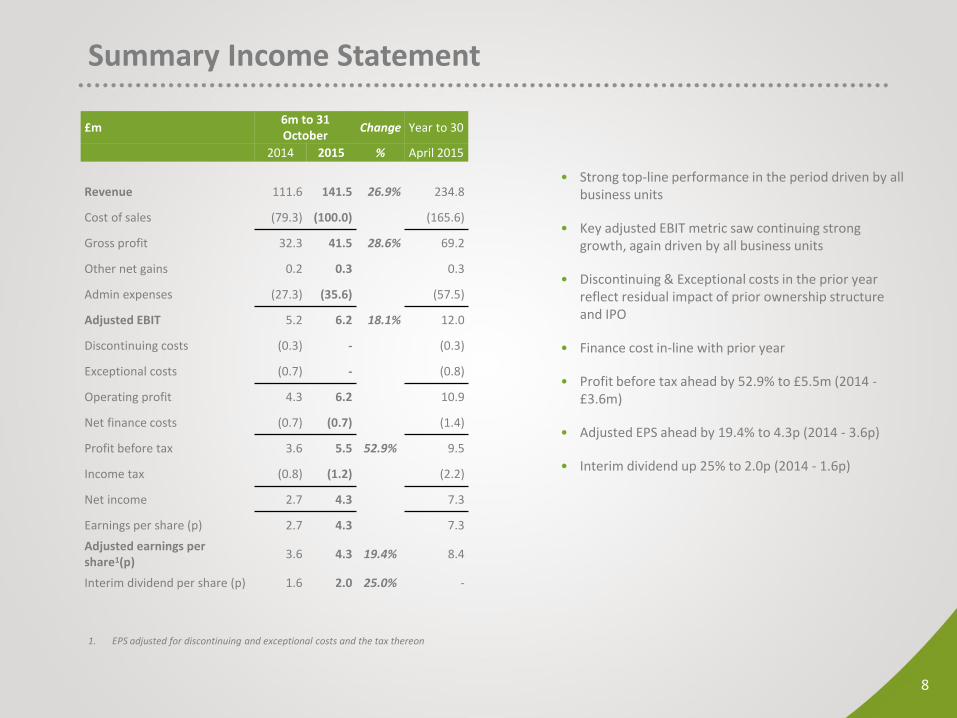

Summary Income Statement

• Strong top-line performance in the period driven by all business units

• Key adjusted EBIT metric saw continuing strong growth, again driven by all business units

• Discontinuing & Exceptional costs in the prior year reflect residual impact of prior ownership structure and IPO

• Finance cost in-line with prior year

• Profit before tax ahead by 52.9% to £5.5m (2014 - £3.6m)

• Adjusted EPS ahead by 19.4% to 4.3p (2014 - 3.6p)

• Interim dividend up 25% to 2.0p (2014 - 1.6p)

1. EPS adjusted for discontinuing and exceptional costs and the tax thereon

£m 6m to 31 October

Change Year to 30

2014 2015 % April 2015

Revenue 111.6 141.5 26.9% 234.8

Cost of sales (79.3) (100.0) (165.6)

Gross profit 32.3 41.5 28.6% 69.2

Other net gains 0.2 0.3 0.3

Admin expenses (27.3) (35.6) (57.5)

Adjusted EBIT 5.2 6.2 18.1% 12.0

Discontinuing costs (0.3) - (0.3)

Exceptional costs (0.7) - (0.8)

Operating profit 4.3 6.2 10.9

Net finance costs (0.7) (0.7) (1.4)

Profit before tax 3.6 5.5 52.9% 9.5

Income tax (0.8) (1.2) (2.2)

Net income 2.7 4.3 7.3

Earnings per share (p) 2.7 4.3 7.3

Adjusted earnings per share1(p)

3.6 4.3 19.4% 8.4

Interim dividend per share (p) 1.6 2.0 25.0% -

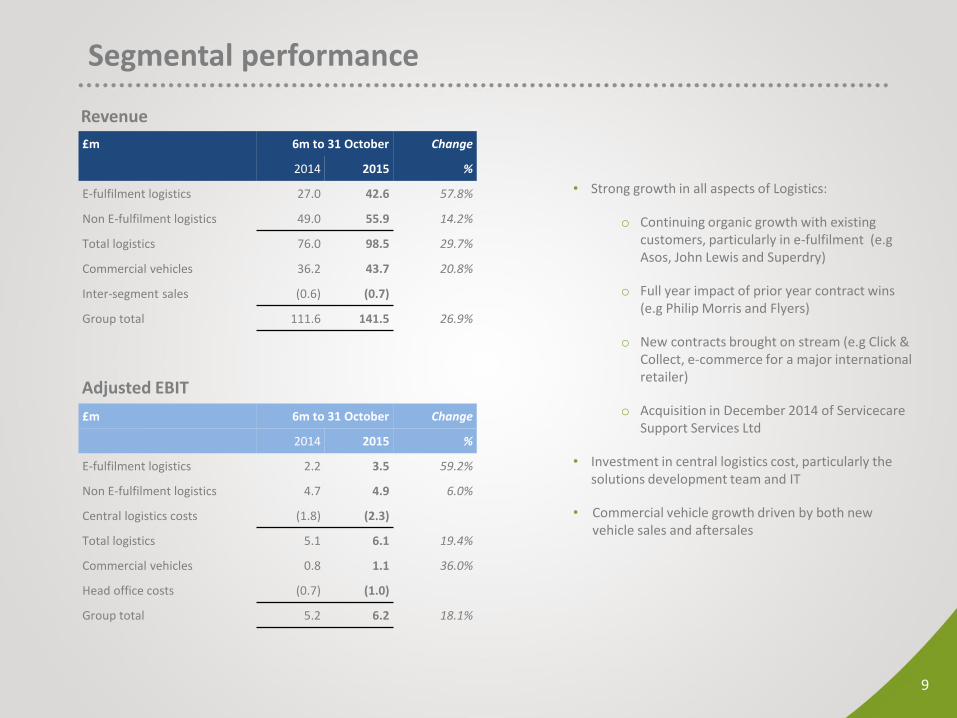

Segmental performance

• Strong growth in all aspects of Logistics:

o Continuing organic growth with existing customers, particularly in e-fulfilment (e.g Asos, John Lewis and Superdry)

o Full year impact of prior year contract wins (e.g Philip Morris and Flyers)

o New contracts brought on stream (e.g Click & Collect, e-commerce for a major international retailer)

o Acquisition in December 2014 of Servicecare Support Services Ltd

• Investment in central logistics cost, particularly the solutions development team and IT

• Commercial vehicle growth driven by both new vehicle sales and aftersales

9

£m 6m to 31 October Change

2014 2015 %

E-fulfilment logistics 27.0 42.6 57.8%

Non E-fulfilment logistics 49.0 55.9 14.2%

Total logistics 76.0 98.5 29.7%

Commercial vehicles 36.2 43.7 20.8%

Inter-segment sales (0.6) (0.7)

Group total 111.6 141.5 26.9%

£m 6m to 31 October Change

2014 2015 %

E-fulfilment logistics 2.2 3.5 59.2%

Non E-fulfilment logistics 4.7 4.9 6.0%

Central logistics costs (1.8) (2.3)

Total logistics 5.1 6.1 19.4%

Commercial vehicles 0.8 1.1 36.0%

Head office costs (0.7) (1.0)

Group total 5.2 6.2 18.1%

Revenue

Adjusted EBIT

10

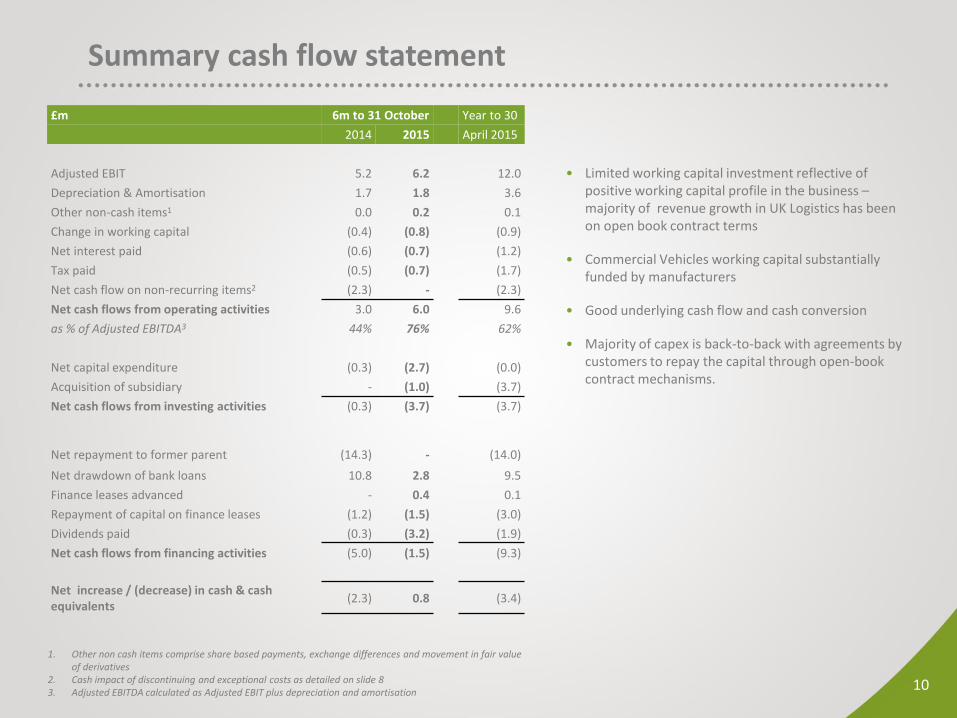

Summary cash flow statement

• Limited working capital investment reflective of positive working capital profile in the business – majority of revenue growth in UK Logistics has been on open book contract terms

• Commercial Vehicles working capital substantially funded by manufacturers

• Good underlying cash flow and cash conversion

• Majority of capex is back-to-back with agreements by customers to repay the capital through open-book contract mechanisms.

£m 6m to 31 October Year to 30

2014 2015 April 2015

Adjusted EBIT 5.2 6.2 12.0

Depreciation & Amortisation 1.7 1.8 3.6

Other non-cash items1 0.0 0.2 0.1

Change in working capital (0.4) (0.8) (0.9)

Net interest paid (0.6) (0.7) (1.2)

Tax paid (0.5) (0.7) (1.7)

Net cash flow on non-recurring items2 (2.3) - (2.3)

Net cash flows from operating activities 3.0 6.0 9.6

as % of Adjusted EBITDA3 44% 76% 62%

Net capital expenditure (0.3) (2.7) (0.0)

Acquisition of subsidiary - (1.0) (3.7)

Net cash flows from investing activities (0.3) (3.7) (3.7)

Net repayment to former parent (14.3) - (14.0)

Net drawdown of bank loans 10.8 2.8 9.5

Finance leases advanced - 0.4 0.1

Repayment of capital on finance leases (1.2) (1.5) (3.0)

Dividends paid (0.3) (3.2) (1.9)

Net cash flows from financing activities (5.0) (1.5) (9.3)

Net increase / (decrease) in cash & cash equivalents

(2.3) 0.8 (3.4)

1. Other non cash items comprise share based payments, exchange differences and movement in fair value of derivatives

2. Cash impact of discontinuing and exceptional costs as detailed on slide 8 3. Adjusted EBITDA calculated as Adjusted EBIT plus depreciation and amortisation

11

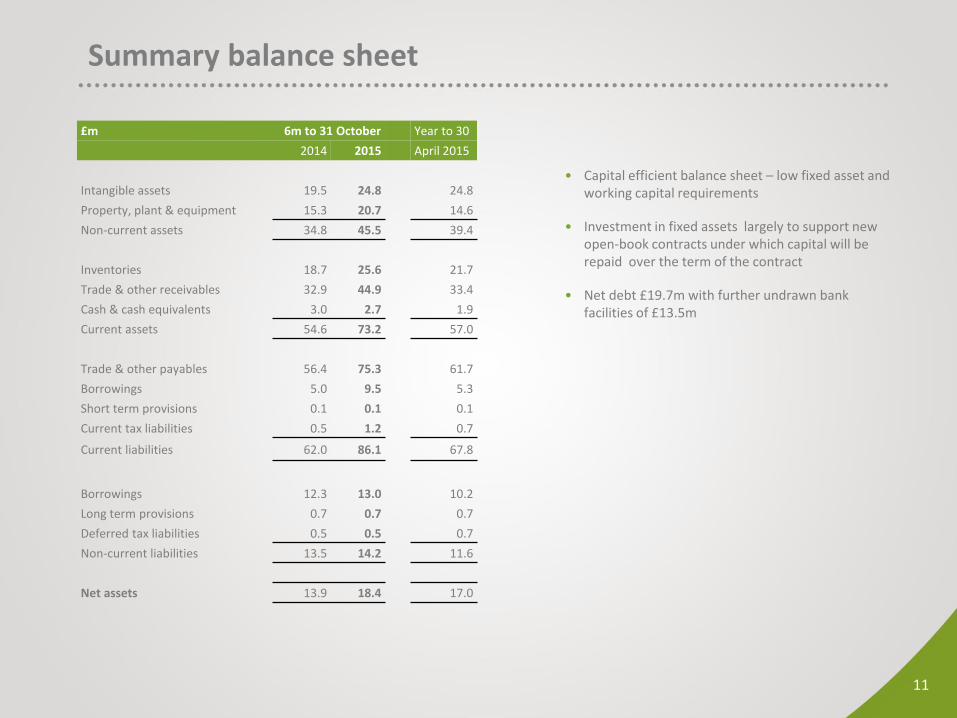

Summary balance sheet

• Capital efficient balance sheet – low fixed asset and working capital requirements

• Investment in fixed assets largely to support new open-book contracts under which capital will be repaid over the term of the contract

• Net debt £19.7m with further undrawn bank facilities of £13.5m

£m 6m to 31 October Year to 30

2014 2015 April 2015

Intangible assets 19.5 24.8 24.8

Property, plant & equipment 15.3 20.7 14.6

Non-current assets 34.8 45.5 39.4

Inventories 18.7 25.6 21.7

Trade & other receivables 32.9 44.9 33.4

Cash & cash equivalents 3.0 2.7 1.9

Current assets 54.6 73.2 57.0

Trade & other payables 56.4 75.3 61.7

Borrowings 5.0 9.5 5.3

Short term provisions 0.1 0.1 0.1

Current tax liabilities 0.5 1.2 0.7

Current liabilities 62.0 86.1 67.8

Borrowings 12.3 13.0 10.2

Long term provisions 0.7 0.7 0.7

Deferred tax liabilities 0.5 0.5 0.7

Non-current liabilities 13.5 14.2 11.6

Net assets 13.9 18.4 17.0

Operational review 3

13

Overview

The Group’s strategy is set around four key principles – all of which have seen positive developments over the period under review:

Build on Clipper’s market leading customer proposition and continue to expand the customer base

Continue European expansion through our profitable German platform

Develop new, complementary products and services

Consider complementary acquisition opportunities

E-fulfilment

Another significant period of development for our offering in this space, with expansion delivered across the board, as structural changes taking place in the retail sector have continued apace:

New contracts taken operational in the period, including: o FarFetch o Lavitta o BAT Vype e-cigarettes o A major international retailer o Fashion operation for a Dublin based department store business.

Additional enhanced processing services developed for ASOS to support the Boomerang returns operation

Fulfilment support for M&S e-comm – awkward products – Christmas trees, gift wrap Existing e-comm customers still experiencing volume shift into on-line driving continued Clipper growth – further enhanced by the associated returns activity

14

Non E-fulfilment

A strong performance in the period, which again illustrates that Clipper’s consultancy-led approach allows the Group to deliver significant levels of growth and profitability in the more traditional logistics space:

Contract extensions with a number of clients during the period, including Build a Bear (5 year) & Liberty (10 year) Secured a number of new contracts including: • Haddad – children’s branded fashion – DC operation • M&Co – full outsourced transport to store operation • Pep & Co – DC & transport operation • M&S returns support

15

In addition, we relocated the Liberty operation to our Swadlincote site (and agreed a 10 year contract extension) and relocated Joerns Healthcare to Rotherham – both to cater for growth

Created a George Home furniture sample showroom & photo studio for Asda within the Wynyard import facility

Servicecare

16

Amazon – processing and sortation of Amazon returns across a variety of product categories AO.com – product refurbishment trial underway

Asda – electrical returns, trial commenced on refurbishment and secondary market sales on a profit share basis Collect, repair and return concept – working with Domestic and General and Argos Creation of a direct to consumer channel through eBay for Highcrest

17

E-fulfilment – Developments

• Click & Collect – “Project Dice”

Solution developed for the John Lewis Partnership - next day click & collect solution for the John Lewis and Waitrose businesses. Fully integrated with the JLP carrier selection systems providing a seamless customer experience. If the customer selects “click & collect” for an on-line JLP order the Clipper delivery label is produced & we provide the end to end solution - trunking, sortation (at the Clipper Swadlincote site) and the final delivery transport to the store. The development provides all customer updates via text/e-mail and all processes are via handheld devices in real time. The initial solution has been in place since September and handles volume to 115 Waitrose stores – peak day to date 24,000 parcels. Post Christmas this will increase to all JLP and Waitrose stores. The additional sorter planned for the JLP Ancillary project will allow for the introduction of other retail customers. For information over 60% of all JLP online activity is now ordered on the basis of click & collect

18

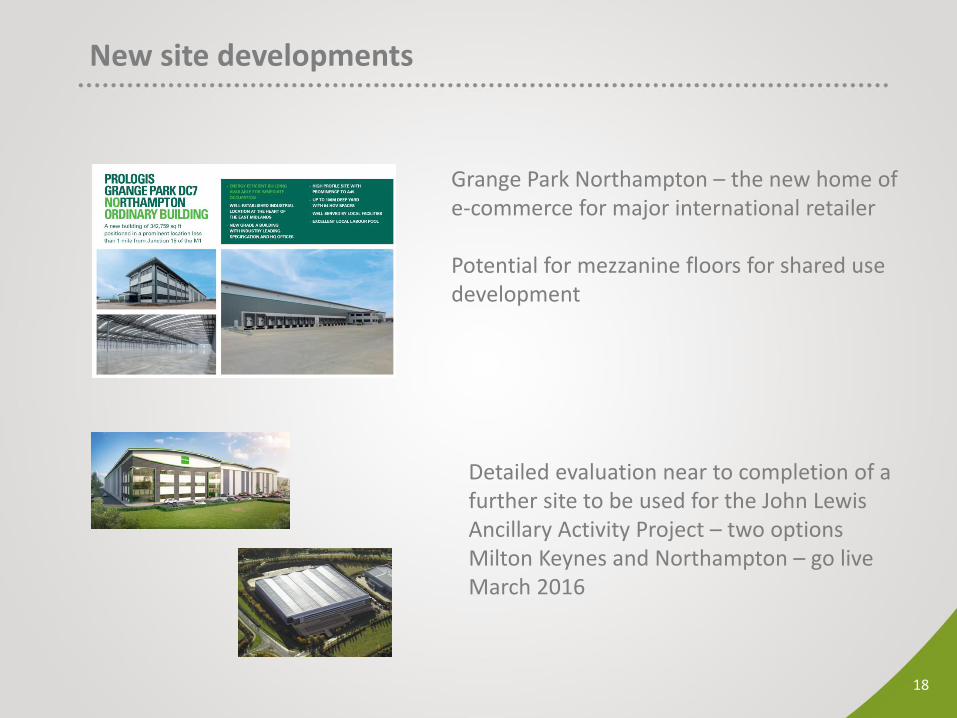

New site developments

Grange Park Northampton – the new home of e-commerce for major international retailer Potential for mezzanine floors for shared use development

Detailed evaluation near to completion of a further site to be used for the John Lewis Ancillary Activity Project – two options Milton Keynes and Northampton – go live March 2016

19

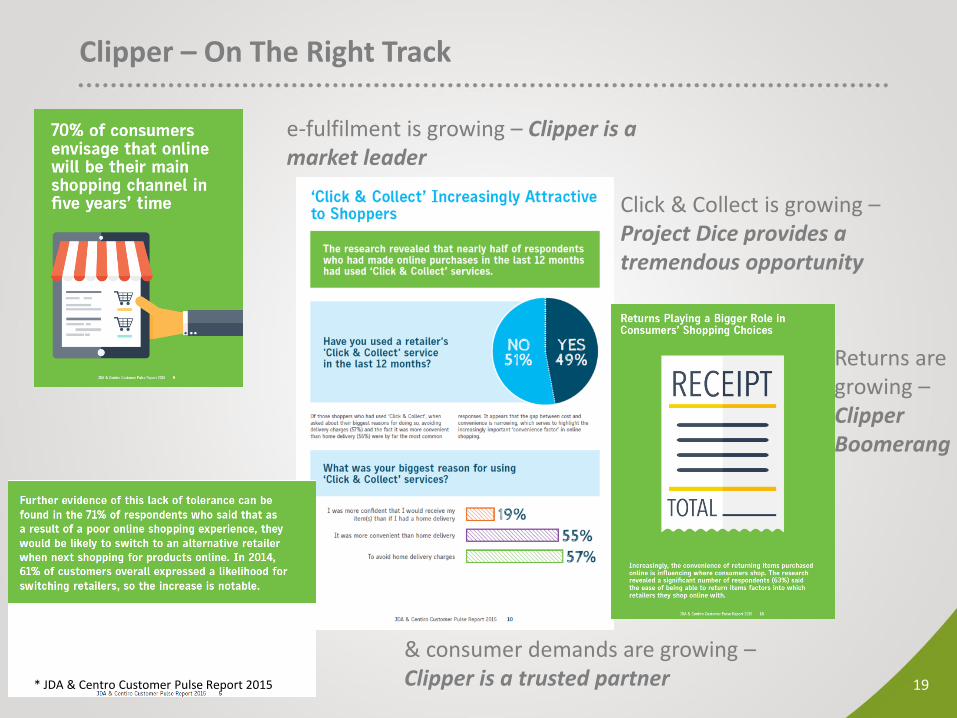

Clipper – On The Right Track

e-fulfilment is growing – Clipper is a market leader

Click & Collect is growing – Project Dice provides a tremendous opportunity

Returns are growing – Clipper Boomerang

& consumer demands are growing – Clipper is a trusted partner * JDA & Centro Customer Pulse Report 2015

Summary and Q&A 4

21

Outlook

Positive momentum into H2 and FY17:

o Contract wins achieving full run-rate

o Click & Collect

o Servicecare

o Strong new business pipeline

Confident of delivering strong financial performance for full year FY16 and into FY17

22

Appendix

23

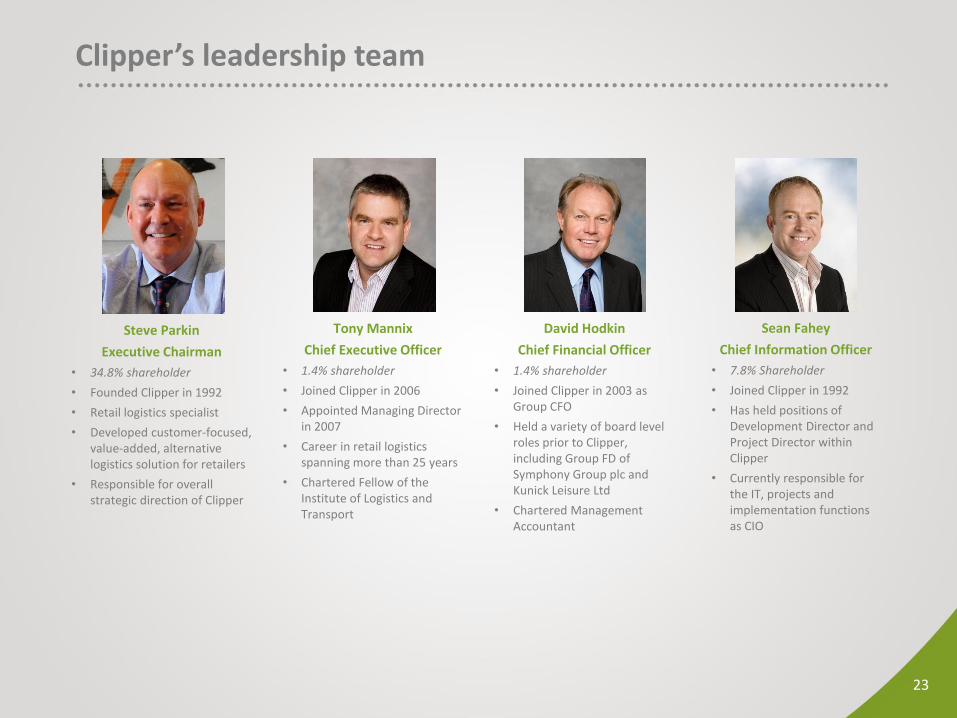

David Hodkin

Chief Financial Officer

• 1.4% shareholder

• Joined Clipper in 2003 as Group CFO

• Held a variety of board level roles prior to Clipper, including Group FD of Symphony Group plc and Kunick Leisure Ltd

• Chartered Management Accountant

Tony Mannix

Chief Executive Officer

• 1.4% shareholder

• Joined Clipper in 2006

• Appointed Managing Director in 2007

• Career in retail logistics spanning more than 25 years

• Chartered Fellow of the Institute of Logistics and Transport

Steve Parkin

Executive Chairman

• 34.8% shareholder

• Founded Clipper in 1992

• Retail logistics specialist

• Developed customer-focused, value-added, alternative logistics solution for retailers

• Responsible for overall strategic direction of Clipper

Clipper’s leadership team

Sean Fahey

Chief Information Officer

• 7.8% Shareholder

• Joined Clipper in 1992

• Has held positions of Development Director and Project Director within Clipper

• Currently responsible for the IT, projects and implementation functions as CIO

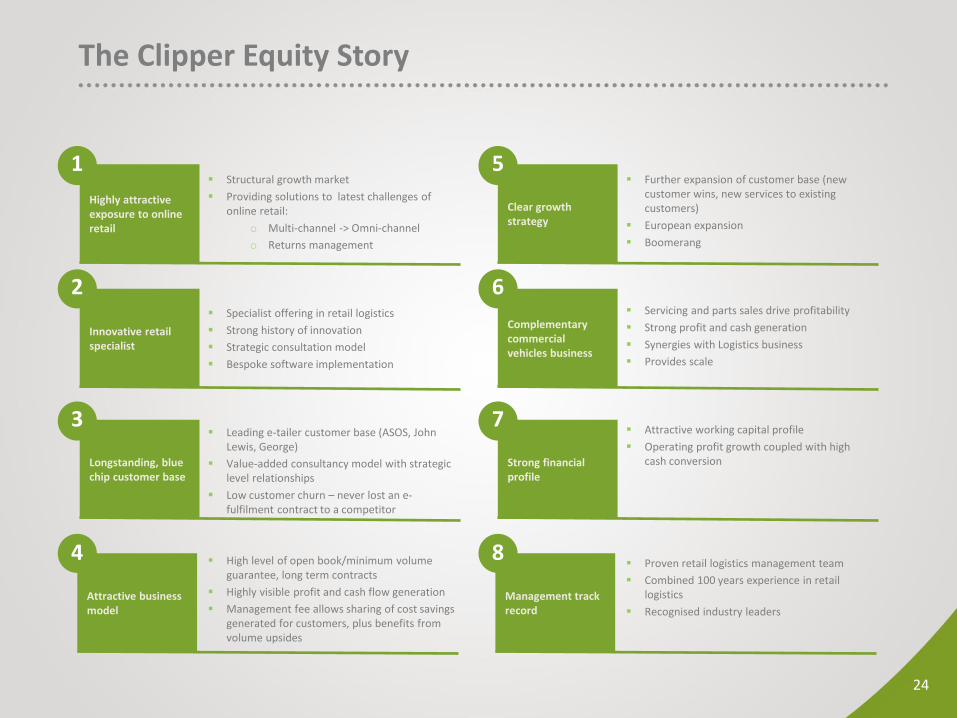

Highly attractive exposure to online retail

24

Structural growth market

Providing solutions to latest challenges of online retail:

o Multi-channel -> Omni-channel

o Returns management

Specialist offering in retail logistics

Strong history of innovation

Strategic consultation model

Bespoke software implementation

Leading e-tailer customer base (ASOS, John Lewis, George)

Value-added consultancy model with strategic level relationships

Low customer churn – never lost an e-fulfilment contract to a competitor

High level of open book/minimum volume guarantee, long term contracts

Highly visible profit and cash flow generation

Management fee allows sharing of cost savings generated for customers, plus benefits from volume upsides

The Clipper Equity Story

Innovative retail specialist

Longstanding, blue chip customer base

Attractive business model

Clear growth strategy

Further expansion of customer base (new customer wins, new services to existing customers)

European expansion

Boomerang

Servicing and parts sales drive profitability

Strong profit and cash generation

Synergies with Logistics business

Provides scale

Attractive working capital profile

Operating profit growth coupled with high cash conversion

Proven retail logistics management team

Combined 100 years experience in retail logistics

Recognised industry leaders

Complementary commercial vehicles business

Strong financial profile

Management track record

1

2

3

4

5

6

7

8