Embed Size (px)

Citation preview

ARTICLE IN PRESS

Volume 88, Issue 1, April 2008ISSN 0304-405X

Managing Editor:Contents lists available at ScienceDirect

JOURNAL OFFinancialECONOMICSG. WILLIAM SCHWERT

Founding Editor:MICHAEL C. JENSEN

Advisory Editors:EUGENE F. FAMA

KENNETH FRENCHWAYNE MIKKELSON

JAY SHANKENANDREI SHLEIFER

CLIFFORD W. SMITH, JR.RENÉ M. STULZ

Associate Editors:HENDRIK BESSEMBINDER

JOHN CAMPBELLHARRY DeANGELO

DARRELL DUFFIEBENJAMIN ESTY

RICHARD GREENJARRAD HARFORD

PAUL HEALYCHRISTOPHER JAMES

SIMON JOHNSONSTEVEN KAPLANTIM LOUGHRAN

MICHELLE LOWRYKEVIN MURPHYMICAH OFFICERLUBOS PASTORNEIL PEARSON

JAY RITTERRICHARD GREENRICHARD SLOANJEREMY C. STEIN

JERRY WARNERMICHAEL WEISBACH

KAREN WRUCK

Journal of Financial Economics

Journal of Financial Economics 91 (2009) 102–117

0304-40

doi:10.1

$ Thi

Welfare

Post-Do

am grat

Parlour,

work, a

HEC Pa

2005).

Confere

for acc

Markets

Econom

support

Social R

E-m

Published by ELSEVIERin collaboration with theWILLIAM E. SIMON GRADUATE SCHOOL OF BUSINESS ADMINISTRATION, UNIVERSITY OF ROCHESTER

Available online at www.sciencedirect.com

journal homepage: www.elsevier.com/locate/jfec

A market-clearing role for inefficiency on a limit order book$

Jeremy Large

Oxford-Man Institute of Quantitative Finance, and AHL, Man Investments, Blue Boar Court, Alfred Street, Oxford OX1 4EH, UK

a r t i c l e i n f o

Article history:

Received 5 July 2007

Received in revised form

15 October 2007

Accepted 4 December 2007Available online 8 October 2008

JEL classification:

C73

G14

G24

Keywords:

Stochastic sequential game

Stationary equilibrium

Limit order book

Market depths

Bid–ask spread

5X/$ - see front matter & 2008 Published by

016/j.jfineco.2007.12.004

s paper previously appeared under the na

when Assets Trade on a Penny. It was mainly w

ctoral Research Fellow of All Souls College, Un

eful to Thierry Foucault, Albert Menkveld, M

Hyun Shin, and Gunther Wuyts for insightful

s well as to anonymous referees. I thank sem

ris (December 2005) and Warwick Business

I also thank participants at the Dauphine/

nce, Paris (June 2006). I thank the Bendheim

ommodating me at Princeton University,

Group for accommodating me at the

ics, during part of the writing. I gratefully ack

from the US-UK Fulbright Commission and

esearch Council, UK.

ail address: [email protected]

a b s t r a c t

Limit order markets with stationary dynamics attract equal volumes of market orders

and uncanceled limit orders, equalizing the supply and demand for liquidity and

immediacy. To maintain this balance, market orders must share any benefit obtained by

limit order traders from more efficient trading conditions, such as better order queuing

policies. Therefore an efficient market places a low price on immediacy, producing small

bid–ask spreads. Furthermore, when price-discreteness leads to a mainly constant

spread, cutting the price tick raises surplus. This is modeled with a stochastic sequential

game, using stationarity considerations to bypass direct analysis of traders’ intricate

market forecasts.

& 2008 Published by Elsevier B.V.

1. Introduction

Electronic limit order books have become a dominantmode of exchange on liquid financial markets. Where thetrading day is sufficiently long and uninterrupted, theorder book microstructure has time to evolve into astationary distribution. This paper explores the constraints

Elsevier B.V.

me: Price Tick and

ritten while I was a

iversity of Oxford. I

eg Meyer, Christine

discussions of this

inar participants at

School (November

Banque de France

Center for Finance

and the Financial

London School of

nowledge financial

the Economic and

stationarity imposes. Stationarity is useful because itimplies that depths rise as often as they fall. Therefore,over time traders choose to submit equally many marketorders as limit orders (leaving canceled orders aside).Following Foucault, Kadan, and Kandel (2005), one maythink of limit orders as the supply of liquidity orimmediacy, and market orders as the demand; andunderstand this as a ‘liquidity market-clearing’ condition.This paper models a dynamic setting where, by concen-trating on this condition, traders’ equilibrium strategiescan be characterized. This leads to results about welfare,market inefficiency, and average depths, as functions of thetick size and other institutional features.

This setting has two important features: first, followingthe literature of Foucault, Kadan, and Kandel (2005),Goettler, Parlour, and Rajan (2005), Parlour (1998), Ohta(2006), and Rosu (2006), it contains only liquidity trading.This means that traders’ idiosyncratic impulses to tradethe asset are insensitive to its fundamental value.However, as in Foucault (1999) and Parlour (1998), tradersare strategic, dynamically choosing between limit ordersand market orders by trading-off delay against slippage.

ARTICLE IN PRESS

best ask, At

best bid, Bt

140.5

141.0

141.5

142.0

142.5

143.0

143.5

144.0

144.5

8:00

Time on 5 January 2004

Pric

e (p

ence

)

k = 0.25 pence

9:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00

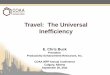

Fig. 1. The prices of the best bid and best ask for Vodafone shares on the London stock exchange, 5 January 2004. The number of transactions on this day

was 14 times higher than the number of changes in the bid (ask). The bid–ask spread was wider than 0.25 pence, only 3.5% of the time. The notation,

k, indicates the price tick size.

J. Large / Journal of Financial Economics 91 (2009) 102–117 103

Second, the market exhibits tight bid–ask spreadsbecause of a large price tick size, so that the spread ispractically always constant and equal to the price tick size.This feature, first modeled in Parlour (1998), is found inField and Large (2008) in fixed-income limit ordermarkets, including 10-, five- and two-year US TreasuryBond futures, as well as short-term interest rate futuressuch as Euribor, Short Sterling, and Eurodollar. Until early2007, Vodafone on the London stock exchange (LSE)(depicted in Fig. 1) was another example.

In the model, the tick size fixes market efficiency at asingle level consistent with stationarity. Consequently,without changing the tick size, adaptations to the tradingenvironment intended to improve welfare fail. Forexample, Field and Large (2008) note that some of theabove futures markets use a price-time matching rule forlimit orders, while others prefer a pro-rata rule. Recently,exchanges have experimented with a third, hybrid, order-matching rule for Euribor and Short Sterling.1 How shouldthe order-matching rule be chosen? Underlying equili-brium responses vary with the choice of order-matchingrule; nevertheless, I show that because market dynamicsare in any case stationary, market efficiency is invariant.I also prove similar invariances with respect to the qualityof trader information, and the rate of trader arrival.2

A useful intuition for the invariance results is asfollows. As a benchmark, consider a stationary equili-brium satisfying the liquidity market-clearing condition.Suppose that changing a primitive of the model, such asthe queuing rules, resulted in another stationary equili-brium with greater surplus per agent but the samebid–ask spread. As market orders’ slippage would notthereby change, nor, in the current setting, would theirpayoff. Thus the supposed gains in surplus would beenjoyed only by limit order-submitters. So, the marketwould be oversupplied with agents who prefer to submit

1 See www.euronext.com/fic/000/022/595/225955.pdf (28 June

2007). Section 6.2 explains the pro-rata order-matching rule.2 Section 7 proves a similar invariance with respect to average

depths, under conditions.

limit orders, which in turn would accrue indefinitely,violating the stationarity of offered depths in equilibrium.This is a contradiction. So, the new equilibrium offers nogreater surplus. A converse argument shows that it alsooffers no less.

Since the market only contains liquidity traders,their surplus equals those gains from trade that arenot wasted (1) as limit orders await their counterpartiesor (2) in matching failures when the asset is bought (sold)by a trader with an excessively low (high) willingness topay. The waste is the market’s inefficiency, which isidentified, via this analysis, by the ‘liquidity market-clearing’ condition. Inefficiency adjusts to a market-clearing level when the market microstructure is sta-tionary.

On markets like the one in Fig. 1, where the bid–askspread is normally equal to the price tick size, theexchange can directly alter the bid–ask spread byadjusting the price tick. In fact, in February 2007, theLSE cut Vodafone’s tick size by 60%. My results supportsuch a policy: in the model, the price tick size has a strongpositive effect on market inefficiency and should be cut, atleast so far as the bid–ask spread continues to approx-imate the price tick size. The mechanism for this works asfollows: being equal to the bid–ask spread, the tick size isthe penalty paid for the advantage of immediate execu-tion. Hence, cutting it encourages too many market ordersto sustain stationarity, unless at the margin limit ordersalso become ex ante more attractive—in aggregate,increasing ex ante surplus.

This mechanism is well illustrated by a comparison inGoettler, Parlour, and Rajan (2005) of two simulatedlimit order markets, which are identical except thatthe tick size is halved in the second simulation (seetheir Tables XIII and XIV). The cut in the tick diminishesthe average quoted spread (although it need not: seeSeppi, 1997 on non-monotonicities). This benefits marketorders. Equally, limit orders trade at worse prices; butare compensated for this in stationary equilibriumwith lower execution risk, and a shorter wait to trade.As execution risk is lower, the aggregate effects of the

ARTICLE IN PRESS

J. Large / Journal of Financial Economics 91 (2009) 102–117104

smaller price tick are greater welfare and less ineffi-ciency.3

The adjustment of inefficiency to market-clearinglevels can be understood partly as an adjustment inaverage depths, since (all other things being equal—inparticular the order arrival rate) high depths are symp-toms of inefficient congestion as limit orders queue totrade. This paper analyzes depths’ role and providesempirical predictions: average depths at the best bidand ask (‘inside depths’) increase with

�

in a

des

quo

(see

order arrival rate (in the sense of Foucault, Kadan, andKandel, 2005: i.e., limit orders plus market orders perunit time), which proxies for trading volume and

� the price tick size.Depths’ positive dependence on trading volume isobserved on the stock exchange of Hong Kong in Brock-man and Chung (1996). On the other hand, Lee, Mucklow,and Ready (1993) find that at times of high traded volume,NYSE specialists reduce their choice of quoted insidedepths. Kavajecz (1999) also focuses on the NYSE.Foucault, Kadan, and Kandel (2005) and Rosu (2006) alsopredict more aggressive limit orders when the orderarrival rate rises (or impatience falls). However, this showsup in a narrower bid–ask spread rather than in higherdepths.

Depths’ positive dependence on the price tick size wasestimated for NYSE stocks in Harris (1994), and wascorroborated in a suite of contemporary and subsequentpapers on recent cuts in price tick size; see the survey inGoldstein and Kavajecz (2000). Among others, importantpapers in this area are Ahn, Cao, and Choe (1996, 1998),Bessembinder (2000), Jones and Lipson (2001), Porter andWeaver (1997), Ronen and Weaver (2001), and Van Ness,Van Ness, and Pruitt (2000). Field and Large (2008) findthat when a market’s pricing grid is very coarse, itsaverage inside depths can exceed the average trade size bya large multiple. My prediction holds when the tick size islarge; and in this respect complements Seppi (1997),which predicts that depths are increasing in the tick sizewhen the tick size is small.

Kadan (2006) also predicts a decline in liquiditysupply, coupled with an increase in welfare, when thetick size falls: a decreasing tick size (in a competitivemarket) shifts rents from liquidity suppliers to a separatepopulation of liquidity demanders, who consequentlytrade greater volumes, boosting welfare. By contrast, inthe current model, welfare per (unit) trade improveswhen the tick size falls, whether or not volumes rise.Empirically, the effect of cuts in tick size on volumes hasvaried depending on the case: the literature on thissubject is well surveyed in Goldstein and Kavajecz (2000).

Cordella and Foucault (1999) and Foucault, Kadan, andKandel (2005) describe a countervailing advantage of a

3 In Goettler, Parlour, and Rajan (2005), as here, welfare is decreasing

verage depth. This runs counter to the intuition that high depths are

irable since unusually large market orders can trade at or near the

tes, which nonetheless is an important consideration in some cases

Jones and Lipson, 2001).

large tick size, namely that it helps to make the marketmore resilient. Rosu (2006) also treats market resiliency,in cases of a small or absent price tick. Questions ofmarket resiliency, which are outlined in empirical work inBiais, Hillion, and Spatt (1995), Coppejans, Domowitz, andMadhavan (2004), and Large (2007), are not raised by thecurrent model, because it describes a highly resilient‘tight’ market, where the spread equals its minimum ticksize most of the time. Likewise, issues in Seppi (1997)regarding variation in trader size offer a complementaryinsight into the effects of changing the tick size.

Specifically, the model is a stationary equilibrium in astochastic sequential game, where, as in Foucault, Kadan,and Kandel (2005), Goettler, Parlour, and Rajan (2004,2005), Hollifield, Miller, and Sandas (2004), Parlour(1998), and Rosu (2006), traders arrive at a limit orderbook sequentially and may alter its state. Prevailing prices,spreads, and depths fluctuate stochastically with thesequence of market orders, limit bids, and limit asks.Agents trade one unit, and then leave. They face a simpletrade-off between (1) a market order and (2) a limit orderat a better price which must wait for execution. Otheraspects of this trade-off are analyzed in Cohen, Maier,Schwartz, and Whitcomb (1981), Chakravarty and Holden(1995), Foucault (1999), and Handa and Schwartz (1996).A number of simplifications are made to the action space:hidden or iceberg orders are not available; and orders maynot be canceled or submitted speculatively behind thebest quotes.

Modeling a sequence of traders who share a stationarydecision problem can yield clean analytic solutions aboutcomplex limit order book dynamics. This approach isdeveloped in Foucault (1999), Foucault, Kadan, and Kandel(2005), and Rosu (2006); Parlour (1998) by contrast isrobust to non-stationarity. For example, Foucault (1999)ensures stationarity by introducing a random end-dateinto the model. However, a stationary decision problemcan be consistent with a non-stationary—even explosive—

market state. This is the case in Foucault (1999), where theunderlying price is an unbounded random walk. Goettler,Parlour, and Rajan (2004, 2005) go a different way,exploiting the ergodicity and (near) stationarity of themarket state around the asset’s consensus value, in orderto design market games for simulation, where unlimitedinformation about optimal strategies can be gathered intime.4

This paper uses the stationarity of the market state toderive equilibrium best responses analytically, withoutneeding to tackle the intricate market forecasting pro-blems solved by traders in equilibrium. To do this, itintroduces a subset of ‘uninformed’ traders who do notobserve the market state, because they have not invested(at a cost of x40) in the necessary technology. Informedtraders’ behavior has complicated contingencies, whichwe cannot derive. However, the best response of unin-formed traders can be identified: as they give ergodicweights to the various market states that they might

4 Because of its fixed initial value, the market state is not strictly

stationary in Goettler, Parlour, and Rajan (2005).

ARTICLE IN PRESS

J. Large / Journal of Financial Economics 91 (2009) 102–117 105

encounter, they rationally adopt the average traderbehavior. But average trader behavior is pinned-down bythe market-clearing condition.

Viewed ex post, the liquidity market-clearing conditionis a necessary accounting identity: that for every marketorder there is an executed limit order, and vice versa.Consequently, it exists in earlier dynamic models. But itseffects differ, depending on the treatment of cancelation.In Foucault (1999) limit orders cancel automatically ifthey do not execute in one period; in Ohta (2006) theyhave two periods to execute. This guarantees market-clearing trivially. On the other hand, in Foucault, Kadan,and Kandel (2005) cancelation is not permitted. Therefore,ex ante, traders choose to submit equal volumes of marketand limit orders, and my model’s key driving mechanismis clearly present. Their paper finds that, as here, widespreads are a source of inefficiency,5 but it focuses oncases where wide spreads are strategically posted.Goettler, Parlour, and Rajan (2004, 2005), and Rosu(2006), are intermediate cases with some cancelation.

Other important theoretical antecedents to this workare in Anshuman and Kalay (1998), Bernhardt andHughson (1996), and Portniaguina, Bernhardt, and Hugh-son (2006), which study tick size, inside depths, andwelfare in markets with dealers. A good overview of thisliterature is available in Kadan (2006). In the prominentworks of Kyle (1985) and Glosten and Milgrom (1985),market dynamics are studied when some agents obtainelsewhere superior information about the underlyingasset’s future cash flows. This introduces a set ofimportant economic issues about the winner’s curse, orpicking-off risk in limit order execution, in the sensedeveloped inter alia in Foucault (1999) and Handa andSchwartz (1996). These issues are somewhat orthogonalto this paper’s interest in the matching properties of themarket.6 In the current setting, by contrast, some tradersdo have superior information, but only about future orderflow, which they infer rationally from the current marketstate.

The paper proceeds as follows. Section 2 details themodel and equilibrium, and previews the paper’s mainresults. Section 3 proves the main theorems aboutstrategies and surplus (detailed derivations are left tothe Appendix). Section 4 interprets these results. Section 5proves that equilibrium exists. Section 6 investigatesadaptations to the model, including the effect of introdu-cing order cancelation. With empirical consequences inmind, Section 7 derives average inside depths in asimplified model and draws out some comparative statics.Section 8 concludes.

5 And they find another source: when impatient traders submit limit

orders. See their Section 2.2.3.6 Arguably, in this setting moderate asymmetric information about

fundamentals enhances trading surplus. It deters limit orders because of

the winner’s curse (see Foucault, 1999; Handa and Schwartz, 1996). But it

leaves expected market order slippage unchanged. So stationarity

requires that this deterrent to limit orders be offset: and the offsetting

effects may enhance efficiency. This may help in thinking about why

inside information is scarcely detrimental to welfare in the comparative

simulations of similar models in Goettler, Parlour, and Rajan (2004).

2. The model

One agent (or player, or trader) arrives at each timet 2 N. The duration between successive times t and ðt þ 1Þis the constant D40.7 The agent makes two actions, thenleaves the game. First she chooses whether to acquireinformation about the market, and second she submits anorder. The player has a type, bt , which I introduce later.I first describe the market state, which she can learn if shewishes.

Let k40 be the price tick size. All admissible prices aremultiples of k. Prices B and A are lower and upperinclusive bounds on prices, respectively. They are multi-ples of k. Mathematically, they close the model in animportant way. However, since they may be arbitrarilyfar apart, their economic importance is comparativelylimited.

There is a stochastic process w ¼ fwt : t 2Ng, where wt

is a state variable describing the shape of the limit orderbook. It is a vector of integers, each indicating the depth atsome price between B and A. The first element in wt is thedepth at B, the second is the depth at ðBþkÞ, and so oninductively until A. Therefore wt has length ð1þ ðA� BÞ=kÞ.If an element of wt is positive there are unfilled bids at thatprice. If it is negative, there are unfilled asks. An exampleto work through is shown in Fig. 2.

Definition 1. For all prices p such that BopoA, define

Lpt ¼ jw

ð1þðp�BÞ=kÞt j, (1)

using wit to mean the ith element of wt .

Say that Lpt is the market depth at price p at time t.

Definition 2. Let the best ask, At , be the lowest price withan unfilled ask, or A if there are no asks. Let the best bid, Bt ,be the highest price with an unfilled bid, or B if there areno bids.

Only states with At4Bt arise. We may call LAtt the ‘depth

at the best ask,’ and LBtt the ‘depth at the best bid’: they are

the inside depths. I will operationalize the concept ofstationary microstructure, which was heavily leant uponin the Introduction, by finding a game where w is

stationary.

2.1. Competitive fringe of traders

As in Foucault, Kadan, and Kandel (2005) and Rosu(2006) there is a competitive fringe of traders standingready to sell and buy when prices rise above, or fall below,the range ðA;BÞ. By transacting with them, agents canalways sell immediately at at least B, and buy immediatelyat at most A, even if the limit order book is empty (whenwt ¼ 0).8 So fringe traders periodically hold a positive

7 In an earlier version of this paper, the duration between successive

times t and ðt þ 1Þ was an exponentially distributed random variable

independent of Ft . This assumption leaves all results of the paper

unchanged, except for the existence result in Proposition 5.1. A problem

arises in the proof of existence because the assumption implies an

uncountable state space.8 A vector of zeros will be denoted by 0, in bold.

ARTICLE IN PRESS

Bt At

280

bestbid best

ask

B A

depth at the best ask

depth at the best bid

mid-quote

PriceD

epth

0

30

-40282 284 286 288 290 292 294 296 298

Fig. 2. An example of a market state at time t is given. Columns indicate depths at various prices. The price tick size, k, is 2. The state variable, wt , is

wt ¼ ð6;0;15;30;�40;�10;�15;0;0;�2Þ: these 10 values are the heights of the columns. Positive elements of wt indicate unfilled bids in the order book;

while negative entries (with a light shade) are unfilled asks. The fixed lower price limit, B, is 280; and the fixed upper price limit, A is 298. The best bid, Bt ,

is 286; and At ¼ 288. So the bid–ask spread, ðAt � Bt Þ, is 2, which equals k. The depth at the best bid, LBtt , is 30; and LAt

t ¼ 40. Slippage is calculated relative

to the mid-quote of 287.

J. Large / Journal of Financial Economics 91 (2009) 102–117106

inventory in the asset. Even if this eventuality is extremelyinfrequent, the detailed analysis of the game keeps trackof this inventory, and checks it reverts to zero in finiteexpected time.

To model this without more notation, I formally defineL

Bt ¼ w1

t and LAt ¼ �w

ð1þðA�BÞ=kÞt . In principle this implies that

depths at the two extreme prices B and A can go negative.‘Negative depth’ will have the natural interpretation thatthe fringe traders hold positive inventory in the asset.

2.2. Acquiring order book information

The first of player t’s two actions is taken before shegoes to the market. She decides whether to invest in acostly technology permitting her to condition her beha-vior on up-to-date prices and depths, as summarizedby wt. The investment has a cost of x40, representing thecomputing and physical effort of arranging to gather,organize, interpret, and act on timely information.

In fact, player t can mix over this choice. So she choosesa probability pt from the interval ½0;1�. With probability pt

she observes wt , but she pays a cost x40 to do so.Otherwise she does not observe wt and pays no cost.

Notice that the choice whether to invest in thetechnology is made ex ante, even before the trader learnsanything about her trading objective and preferences. Thisis realistic whenever, as is usually the case on financialmarkets, traders cannot develop exchange-specific tech-nology and skills only for the purpose of a single trade.

2.3. Choice of order

On arriving at the market, the trader knows wt if shepaid x for order book information. She now performs thesecond of her two actions, which is to select one of fourorders of unit quantity: a bid, ask, buy, or sell. Buy and sell

are market orders which execute immediately, while bid

and ask are limit orders, which execute sequentiallyaccording to a price-then-time matching rule.

Assumption 1. Bids and asks cannot be submitted behindthe best quotes.

So, bids cannot be submitted at prices below Bt, and asks

cannot be priced above At . This helpfully reduces thenumber of order types to only four. Even though an ask orbid is initially submitted at the most aggressive priceavailable, it may become stale, as before execution itsprice may come to differ substantially from either At or Bt

as they change.The assumption is most plausible for those assets

where the bid–ask spread is normally equal to the pricetick size, with high offered depths at Bt and At . Then,empirically, the most aggressive price possible (as limitedby the large price tick size) is chosen by a wide range oftrader types. An analysis of limit order submission outsidethe quotes is given in Cordella and Foucault (1999) in amodel of a limit order book with bid–ask spreadsroutinely wider than the price tick.

2.4. Payoffs

In choosing her order, player t trades off slippageagainst delay. Slippage is the amount by which her pricefalls short of the mid-quote, mt , which is the average of At

and Bt . So her slippage is

direction� ðp�mtÞ,

where direction is þ1 if she buys, and �1 if she sells, and p

is her trade price. Evidently, slippage can be negative. Italso fluctuates with the bid–ask spread, ðAt � BtÞ. How-ever, a benefit of the current setting is that, whilestochastic, the bid–ask spread is predominantly constantand equal to the price tick size, k. So given Assumption 1,we have that predominantly

slippage ¼

k

2order is a buy or sell;

�k

2order is a bid or ask:

8>><>>:

(2)

Just when the bid–ask spread is momentarily wider than k,(2) is incorrect. However, to simplify the problem, in theformulation of payoffs I adopt (2) as the definition ofslippage at all times.

Player t’s trade-off between slippage and delay de-pends on her type, bt , which is drawn randomly from a

ARTICLE IN PRESS

J. Large / Journal of Financial Economics 91 (2009) 102–117 107

symmetric distribution on the interval ½�bþ;bþ�, inde-pendently of all other random variables known at time t.The cumulative distribution function (CDF) of this dis-tribution is called F.

The agent’s payoff from trading is

direction� bt � slippage. (3)

Thus bt40 gives player t a motive to buy, while bto0gives a motive to sell. The trade’s payoff is penalizedadditively by the slippage. The benefit of trading with alimit order, rather than a market order, is to enjoy negativeslippage. However, a player waits to trade if she uses alimit order, and the payoff in (3) is discounted at rater40. The rate is the same for all traders; but a player withlarge jbtj, who will gain more from a trade, finds waitingmore costly. So, a large jbtj should indicate a preferencefor market orders.

In reality, limit orders typically wait at most a fewminutes to execute, not long enough for impatience, asusually understood, to become important. So I do notinclude impatience here. Rather, the rate r capturesopportunity and capital costs outside the model that theagent incurs in waiting to trade. One way of introducing ris to endow each player with an imminent, unobserved,idiosyncratic liquidity event or deadline.9

The payoff to player t is summarized in PtðbtÞ:

Definition 3. Let PtðbtÞ be the value of (3) whendiscounted at rate r until execution, minus x, the cost ofthe trading technology, if she invested in it.

Observe that we may exclude a fifth action of no order,which would result in zero payoff. Since limit orders havenegative slippage, for any player type at least one out ofbid or ask has positive expected payoff.10

2.5. Order submission: via a trading algorithm

To formalize order submission I introduce a tradingalgorithm. This establishes the notation for cutoffs, ct ,which will be central to the solution (and it simplifies theproof that equilibrium exists). Analytically it impliesnothing new: Section 3.2 will show that changing theinformation set can yield an observationally identicalgame without a trading algorithm.

Instead of submitting the order herself, playert programs the algorithm up-front, before she learns

bt . Conditional on the signal wt iff she observes it, sheselects a cutoff vector ct.

11 Let R be R [ f�1;1g, the

9 On this interpretation the deadline arrives exogenously as the first

event of a Poisson process with parameter r. Execution after the deadline

results in a zero payoff. It is possible to formulate an adapted version of

the model with the same qualitative properties, where, as in Foucault,

Kadan, and Kandel (2005), rather than having a discount rate, traders

undergo a constant waiting cost per unit time that their limit order

remains in the market before trading.10 Although somewhat specific to the current payoff structure, this

reflects a general property of limit order markets: that trading with a

limit order ‘wins the spread.’11 At some notational expense, I could have it that in advance she

programs the algorithm with a suitable ct for every state of the market

that it might encounter.

closure of R. Then

ct is a vector of three weakly increasing elements in R3,

and each element of ct is a cutoff determining the order.The algorithm is fast enough to act upon bt . It compares ct

to bt , and submits an order on that basis. Without yetknowing bt , the trader can use ct to determine whichorder will be made for each possible value of bt .

Rule for the trading algorithm: On behalf of the agent,the trading algorithm submits an order to the limit orderbook, denoted ort . It automatically selects ort ¼ orðbt ; ctÞ,where

�

orðbt ; ctÞ is sell if bt is less than all three elements of ct; � orðbt ; ctÞ is ask if bt is less than exactly two elementsof ct;

� orðbt ; ctÞ is bid if bt is less than exactly one elementof ct;

� orðbt ; ctÞ is buy if bt is less than none of the elementsof ct .

It will become apparent why ort is sell when bt is verylow, while ort is buy when bt is very high; and why ask

and bid are at intermediate realizations of bt . The reason-ing for this goes back to the early work of Parlour (1998).

2.6. Discussion previewing the results

To look ahead: I will be interested in an equilibriumwhere all agents choose ct identically given their signalof wt , and where the dynamics of buying and selling arealike. I will identify the choice of ct when player t receivesno signal, and, with this, derive market efficiency.Theorem 3.3 will show that

when player t is uninformed of wt ; ct ¼

F�1ð14Þ

0

F�1ð34Þ

0BB@

1CCA.

(4)

This is illustrated in Fig. 3. Traders with bt below F�1ð14Þ

submit a market sale, and trade immediately; traders withbt 2 ½F

�1ð14Þ;0Þ submit a limit ask; and so on.

I briefly review the intuition for the theorem’s result,and what may be inferred from it. We start from theliquidity market-clearing condition discussed in theIntroduction. For this game, the condition requires thatover time equally many limit orders as market orders aresubmitted to the exchange. Therefore, bids, asks, buys, andsells are, on average, equally likely to be submitted by anytrader of unknown type. When selecting from these fouroptions ‘blindly’, i.e., without knowledge of wt , a trader cando no better than to ascribe ergodic weights to eachpossible state wt that they might encounter. In conse-quence, the uninformed trader faces an average of theproblems faced by better-informed traders. Her responseto this average problem is equal to the average response:and therefore also involves submitted bids, asks, buys, andsells with equal probability. This best response is given in

ARTICLE IN PRESS

-k 02

sell

�t

F’

F-1[¼] F-1 [¾]

ask bid buy

k2

Fig. 3. The distribution of the type, bt , and (dotted lines) the three equilibrium cutoffs for traders who do not observe wt . The sizes of the four delimited

areas under F 0 are equal to one another and equal to 14.

J. Large / Journal of Financial Economics 91 (2009) 102–117108

Fig. 3, and is such as to break the type space into fourquartiles of equal probability.

It is thereby possible to identify the best response to anabsence of limit order book information, while bypassingthe out-of-equilibrium reasoning for that best responsealmost entirely. Such reasoning is intricate and involved,for it reviews each possible market state; and for thatstate, it considers the market’s likely subsequent evolution.Tackling it head-on might be infeasible. Furthermore, thederivation makes scanty use of the details of the market’sdynamics, and is therefore invariant to many features,including D, the rate of trader arrival, r, the discount rate,and the order queuing rules imposed by the exchange.

Fig. 3 implies certain indifference conditions for thetypes F�1

ð14Þ and F�1ð34Þ, which are enough to identify the

inefficiency of the market. As a result, market efficiencyhas the same invariances as those just mentioned of Fig. 3.In fact, the only policy variable that it depends on is theprice tick size, k. The price tick fixes the bid–ask spread,and thereby holds market inefficiency at a liquiditymarket-clearing level.

Intuitions for these results were presented in theIntroduction; and Section 3 provides rigorous proofs,extensions, and conditions.

2.7. Shape of the CDF, F

As Section 6.1 will argue, the above analysis isapproximately correct for reasonable shapes of F. How-ever, it is only precisely right for a certain family of CDFs,F, of bt . Specifically, suppose that for all b 2 S ¼

ð�bþ;�k=2�,

FðbÞ ¼Z

k

2� b

. (5)

The constant Z is chosen to ensure that Fð1Þ ¼ 1. Tosatisfy (5) there are suitable atoms at �bþ and bþ. Thistruncation of F simply ensures that moments exist. Itshould not be too extreme: suppose that bþ4k=ð1� e�rDÞ.However, it should also allow some dispersion: supposeFð�k=2Þ4 1

3. A typical form of F is depicted in Fig. 3.

2.8. State transitions

When an order is submitted to the limit order book,this changes the order book shape. A limit order adds to

the already-assembled offered depth; while a marketorder, by trading with an extant limit order, diminishesthe depth. So there is a sequence of transitions in the statevariable, wt , induced by order submission. Indeed, thestate wtþ1 is measurable with respect to wt and ort .Specifically, wtþ1 is equal to wt , except that

�

if ort ¼ sell, then its depth at Bt is 1 less (so LBttþ1 ¼

LBtt � 1);

�

if ort ¼ buy then its depth at At is 1 less; � if ort ¼ bid then depth at p is 1 more: where p ¼ðAt � kÞ unless LBtt o0, when p ¼ Bt;

�

if ort ¼ ask then depth at p is 1 more: where p ¼ðBt þ kÞ unless LAtt o0, when p ¼ At .

The latter two bullet points implement Assumption 1, thatbids and asks are not submitted outside the quotes. Theyalso include special rules for when the competitive fringeof traders have positive inventory and prices are at upperor lower limits, leading to LAt

t o0 or LBtt o0. On those

occasions, the bid or ask executes immediately.

2.9. Equilibrium

Let the initial condition, w0, be a random variable witha distribution S.

Definition 4. Define player t’s overall action to be at , soat ¼ ðpt ; ctÞ.

Let us say that the (Bernoulli) random variable Zt 2

f0;1g is 1 if player t observes the market state wt , and zerootherwise. Adopt the convention that if Zt ¼ 0, then Ztwt isthe scalar, 0.

Definition 5. Define player t’s signal to be Ztwt .

So if Ztwt ¼ 0 player t may infer that Zt ¼ 0, and that shehas no information about the current limit order book, assummarized by wt. But if Zt ¼ 1 then player t’s signal Ztwt

is just wt .

Definition 6. A strategy is a function which maps signals,Ztwt , into actions, at . It is a pair ðp; cð�ÞÞ, where p 2 ½0;1�and c takes as its argument signals of the form Ztwt .

In a stationary Markov equilibrium all traders have thesame strategy. Equilibrium is a probability space ðO;F; PÞ,together with a strategy and the primitives of the model.

ARTICLE IN PRESS

J. Large / Journal of Financial Economics 91 (2009) 102–117 109

Although formally there is no mixing over strategies, theaction pt parameterizes the distribution of the randomvariable Zt . In this way we may interpret agent t asrandomizing her choice whether to learn wt .

Definition 7. Let Etpy ;cy indicate the expectations operator

when for all sat, as ¼ ðp; cðZswsÞÞ, the equilibrium action;but player t may be different: for at ¼ ðpy; cyÞ.

Equilibrium properties:

1.

Players choose actions at ¼ ðp; cðZtwtÞÞ. (So pt ¼ p andct ¼ cðZtwtÞ.)2.

When pt ¼ p and ct ¼ cðZtwtÞ, player t acts in the waywhich maximizes the conditional expectation ofPtðbtÞ, given other players’ strategies. Precisely,Etpy ;cðZtwt Þ

½PtðbtÞ� (6)

exists and is maximized when py ¼ p. And for allsignals z,

Etp;cy ½PtðbtÞjZtwt ¼ z� (7)

exists and is maximized when cy ¼ cðzÞ.

As mentioned in the Introduction, I will be exclusivelyconcerned with equilibria where the state variableprocess, w, is stationary. Although this stationarityproperty makes equilibrium existence harder to prove,the benefit is substantial: if the state variable were notstationary, then the decision problem of ‘blind’ traderswould not be stationary, and their best response wouldnot be constant (it would depend on t, the time since thegame began). As was previewed in Section 2.6, if theirdecision problem is constant then it is tractable.

I also concentrate on buy–sell symmetric equilibrium,where buyers and sellers behave alike, but symmetricallyto one another. Buy–sell symmetry is precisely defined inthe Appendix. It is a natural constraint in this symmetricenvironment where buyers and sellers face congruentpayoffs and symmetric model primitives. However, it issimply a desirable equilibrium selection, although it maybe that all equilibria in this game are buy–sell symmetric.

3. Equilibrium characterization

The characterization of equilibrium will proceed infour parts. After a section introducing some notation,Section 3.2 establishes that, when ignorant of the limitorder book (i.e., when Zt ¼ 0), traders face a particularaverage problem. In parallel, Section 3.3 deduces fromstationarity the average best response.

After these preliminary steps, Section 3.4 provides themain theorems of the paper. The reader can move directlyto those, if desired. It shows that the best response,namely cð0Þ, to the average problem just mentioned, is thisaverage best response, which depends in fact on thequartiles of F—as depicted in Fig. 3. This identifies cð0Þ andindirectly thereby surplus per agent.

The results of this section are interpreted in Section 4,while the fairly involved proof of equilibrium existence isleft to Section 5.

3.1. Notation and definitions

Definition 8. If player t submits a bid or an ask, then let TBt

and TAt , respectively, be their times to execution.

Then trader t’s payoff, PtðbtÞ is given by

PtðbÞ ¼ �xZt þ

b�k

2ort ¼ buy;

�b�k

2ort ¼ sell;

bþk

2

� �e�rTB

t ort ¼ bid;

�bþk

2

� �e�rTA

t ort ¼ ask:

8>>>>>>>>>>>><>>>>>>>>>>>>:

(8)

An expectation without sub- or superscripts, E, will meanequilibrium expectations. For out-of-equilibrium expecta-tions, it will clarify some expressions to suppress thesymbol p in Et

p;cy , by writing Etcy for Et

p;cy.

Definition 9. Let cask be the cutoff function such that theplayer is sure to submit an ask, so

cask ¼ ð�1;1;1Þ0, (9)

and define csell, cbid, and cbuy similarly.

I will often use the out-of-equilibrium expectationsoperator Et

caskwhich describes what would happen if

player t were forced to submit an ask.

Definition 10. Let the expected discount factor associatedwith limit order execution be

Etcask½e�rTA

t �, (10)

which, in a buy–sell symmetric equilibrium, is equal toEt

cbid½e�rTB

t �.

An important step in the characterization of welfare inthis game, will be to identify the expected discount factorassociated with limit order execution.

3.2. Out-of-equilibrium reasoning when Zt ¼ 0

In equilibrium, we can consider the case of a player, t,who could observe bt and Zt , and on this basis select theorder, ort (bid, ask, etc.), conditioning her selection on hersignal Ztwt . So, she is able to act directly on the exchange,rather than via a trading algorithm. She is not therebyconstrained by buy–sell symmetry (which is definedprecisely in Definition 15 of the Appendix). Note that thestochastic time to execution were she to submit an ask isindependent of her type, bt . So, if bt is very low, sheprefers to act urgently with a sell. Over a suitable regionher payoff is monotonic in bt so at some cutoff sheswitches and prefers an ask. A similar argument applies tobuyers, implying another cutoff. So the player wouldchoose a cutoff strategy, implementable through a choiceof ct . Therefore, the structure in the trading algorithm’suse of the cutoffs in ct described in Section 2.5 is in factnot a constraint to optimal order submission.

Denote the first element of a vector, v, by v1. Theanalysis will be concerned mainly with c1

t and c1ðZtwtÞ.

ARTICLE IN PRESS

J. Large / Journal of Financial Economics 91 (2009) 102–117110

A player t who knows that bt ¼ c1ðZtwtÞ is at a cutoffwhere she is indifferent between submitting an ask and asell, on observing Ztwt . This can be formalized as follows:from (8),

�c1ðZtwtÞ �k

2

� �¼ �c1ðZtwtÞ þ

k

2

� �Et

cask½e�rTA

t jZtwt�. (11)

Proposition 3.1. In a buy–sell symmetric equilibrium where

p 2 ð0;1Þ

Fðc1ð0ÞÞ ¼ E½Fðc1ðZtwtÞÞ�. (12)

Proof. See Appendix.

The proof of Proposition 3.1 follows the reasoning aboutout-of-equilibrium paths, of a marginal cutoff type who isindifferent between submitting an ask, and submitting asell, and who does not observe the state wt . It shows thatshe faces the average of the problems faced by playerswho observe wt , and therefore uses an average cutoff.Because of the form of the indifference condition (11), thisaverage is hyperbolic rather than, more familiarly, arith-metic; and it can be represented in terms of the CDF, F. Theproof makes no reference to the details of the dynamicequilibrium, in particular to the distribution of TA

t .The next part shows how stationarity in fact identifies

E½Fðc1ðZtwtÞÞ�: for, were it higher or lower, depths would benon-stationary.

3.3. The consequences of stationarity

The following lemma states that in equilibrium sells,buys, bids, and asks are equally prevalent to one another inthe order flow. This formalizes one of the paper’s mainintuitions: namely, that if depths are stationary then theaverage number of executed limit orders per unit timeequals the average number of market orders. As discussedin the Introduction, this can be interpreted as a ‘liquiditymarket-clearing’ condition.

Definition 11. Let Dt ¼PQ

p¼M Lpkt . So, Dt is the total market

depth at time t.

Lemma 3.2. In a buy–sell symmetric equilibrium where

p 2 ð0;1Þ, for any t

Pr½ort ¼ sell� ¼ Pr½ort ¼ ask� ¼ Pr½ort ¼ bid�

¼ Pr½ort ¼ buy� ¼ 14. (13)

Proof. Since fwtg is stationary with a first moment, fDtg isalso. Dtþ1 always differs from Dt by exactly 1. So, Dt risesas often as it falls. As it falls exactly when ort 2 fsell; buyg,for all t

Pr½ort 2 fsell; buyg� ¼ 12. (14)

In a buy–sell symmetric equilibrium, w and �revðwÞ havethe same distribution. So, buy and sell are equallyprevalent orders. And, bid and ask are equally prevalentorders. &

Since sells, or market sales, are submitted by thoseplayers who draw bt below c1ðZtwtÞ,

Pr½ort ¼ selljZtwt� ¼ Fðc1ðZtwtÞÞ. (15)

Given Lemma 3.2 this implies (by the Law of IteratedExpectations) that

E½Fðc1ðZtwtÞÞ� ¼14. (16)

This equation is central. Think of F�1ð14Þ as the median

seller. Then (16) shows that the median seller isF�1E½Fðc1ðZtwtÞÞ�. So, because of stationarity, in particularof the stationarity of offered depths, the median seller is(just like c1ð0Þ although for quite different reasons), adeformed average of the set of marginal types, fc1ðZtwtÞg

(it might have been a simple arithmetic average if F had auniform CDF). In the light of this, it is perhaps a naturalthought that the median seller would be roughlyindifferent between a sell and an ask in the average oftheir problems, as faced by traders with Zt ¼ 0. In fact,features of F imply that this deformation is the same asthe one in Proposition 3.1, so that this natural thought isexactly true. This is formalized in Theorem 3.3.

3.4. The main theorems

Theorem 3.3. In a buy–sell symmetric equilibrium where

p 2 ð0;1Þ,

cð0Þ ¼

F�1ð14Þ

0

F�1ð34Þ

0BBBB@

1CCCCA. (17)

Proof. From Proposition 3.1 and (16), c1ð0Þ ¼ F�1ð14Þ. The

theorem then follows from the buy–sell symmetry ofcð0Þ. &

The derived best response is illustrated in Fig. 3.Theorem 3.3 shows that the types who have

bt ¼ �F�1½14�, are, when Zt ¼ 0, indifferent between (1) a

limit order and (2) a market order which incurs k in extraslippage. This actually identifies the expected discount

factor associated with limit order execution, namelyEt

cask½e�rTA

t �, for, from (11),

�F�1 1

4

� ��

k

2

� �¼ �F�1 1

4

� �þ

k

2

� �Et

cask½e�rTA

t �, (18)

so that

Etcask½e�rTA

t � ¼ 1�k

k

2� F�1 1

4

� � . (19)

Furthermore, it leads to a characterization of eachagent’s expected payoff:

Definition 12. Let d be defined by

d ¼E½jbtj : jbtjoF�1

½34��

F�1½34�

, (20)

so that d is a measure of F’s relative dispersion within itsinterquartile range, ½F�1

½14�; F�1½34��.

Theorem 3.4. In a buy–sell symmetric equilibrium

where p 2 ð0;1Þ the ex ante expected payoff, or surplus, of

ARTICLE IN PRESS

J. Large / Journal of Financial Economics 91 (2009) 102–117 111

player t is given by

E½PðbtÞ� ¼ EðjbtjÞ �k

2

k

2þ dF�1 3

4

� �

k

2þ F�1 3

4

� �0BB@

1CCA. (21)

Proof. See Appendix for the full proof. From Theorem 3.3,any player t with Zt ¼ 0 foresees ex ante, that ort 2

fbid; askg iff bt is in the interquartile range of F, and so

Prfort 2 fbid; askgjZt ¼ 0g ¼ 12. (22)

Furthermore, the cases where bt is in the interquartilerange of F are exactly the cases where her payoff to tradingis discounted due to delay. But, the expected discountfactor for these cases is known from (19). Combining theseobservations, her ex ante surplus follows after algebra.

Were it not for the cost x, this would be exceeded by the

surplus of those for whom Zt ¼ 1; but, since players mix

between Zt ¼ 0 and 1, in fact x absorbs exactly this excess.

Ex ante surplus is therefore equal to expected surplus

conditional on Zt ¼ 0. &

4. Interpretation of the result and comparative statics

Theorem 3.4 shows that surplus per agent in thismarket is strictly less than E½jbtj�. This bound, E½jbtj�, hasthe following interpretation. Consider an ideal marketwhere no trader waits to trade, and each trade has theproperty that the buyer, say player t, had btX0 while theseller, say s, had bsp0. Then the trading surplus achievedwith each trade would be

E½ðbt � bsÞjbtX0;bsp0�, (23)

or 2E½jbtj�. Per trader, the surplus would be E½jbtj�.Both of these ideal conditions are violated by the

electronic limit order book in practice. Theorem 3.4quantifies the resulting shortfall in surplus, or inefficiencyper trader; and it shows the shortfall to be a necessarycondition for stationarity. It is

k

2

k

2þ dF�1 3

4

� �

k

2þ F�1 3

4

� �0BB@

1CCA. (24)

Given F and k (so that the bid–ask spread is held fixed)this shortfall or inefficiency is invariant to changes in theother primitives of the model which may freely alter both

�

(Order flow) the duration between trader arrivals, Dand � (Quality of trader information) the endogenous propor-tion of traders, p, who observe wt .

In fact, inefficiency per trader is a little under half theprice tick size: which is natural, for half of all traders optto wait for a counterparty by submitting a limit order, andthese traders expect the wait to be less costly than payingup the price tick to cross the bid–ask spread, and tradingimmediately.

4.1. Benefits to cutting the price tick size

Theorem 3.4 shows that the inefficiency per trader liesbetween dk=2 and k=2. Holding fixed F�1 3

4

� �and d, it is

increasing in the price tick, k (given the relationship of F tok in (5) it is not strictly possible to hold F fixed in thisthought experiment where k changes).

In (24), the half-spread bounds the inefficiency pertrader above. An explanation for this is that exactly half ofthose traders drawing Zt ¼ 0 wait inefficiently beforetrading; and when a trader does wait, she finds paying thespread ex ante weakly costlier than waiting.

Cutting the tick size affects surplus per player becauseit makes market orders strictly more attractive. All otherthings remaining equal, some types would be induced tosubmit market orders, who previously preferred limitorders. This would violate Theorem 3.3 and imply ashortage of limit orders over time, non-stationary depths,and no equilibrium. In equilibrium, therefore, endogenousfrictions adjust to restore the types in cð0Þ to theirrespective indifference conditions as illustrated in Fig. 3(for example, average depths fall). Hence, perhaps coun-terintuitively, like market orders, limit orders also becomeex ante more attractive when the bid–ask spread falls—

which necessarily involves an increase in ex ante welfareper player.

The Introduction compared this mechanism to asimilar one in Kadan (2006). A countervailing considera-tion, regarding resiliency, is developed in Cordella andFoucault (1999) and Foucault, Kadan, and Kandel (2005).

5. Existence of equilibrium

Goettler, Parlour, and Rajan (2005) point out that aresult of Rieder (1979) can be used to prove the existenceof equilibrium in this context. To apply his result directlyhere, however, initially we must make some restrictions:

1.

Suppose that the initial condition is fixed at, say,w1 ¼ ð1;0;0; . . . ;0;�1Þ.2.

Suppose that p 2 ð0;1Þ is fixed and exogenous. 3. Suppose that traders are restricted to buy–sell sym-metric choices of ct .

4. Suppose that cð0Þ is fixed at its value in Theorem 3.3.Rieder (1979) proves the existence of a stationaryequilibrium with Markov strategies when there are acountable number of players, a countable state space, anda compact action space (as ct inhabits a compact space).His result applies to this restricted game (although bt ,whose space is not countable, requires technicalattention).

While this shows the existence of a stationarysequential equilibrium, it does not guarantee that wt is astationary random variable with a first moment. However,as p40, all orders are with positive probability observedby some traders. This creates negative feedback in depths,because it is unattractive to traders to add their limitorder to a deep book: many therefore submit a marketorder, which clears depths away.

ARTICLE IN PRESS

J. Large / Journal of Financial Economics 91 (2009) 102–117112

More formally, the Appendix lays out the proof thatthere exists some large number L� such that when insidedepths deviate from zero by more than L�, they drifttowards zero; and that this drift can be boundeduniformly away from zero. Thus, a drift condition, asexpressed in Tweedie (1976, 1983), is satisfied. In ageneralized sequential game Large and Norman (2008)use drift condition results in Tweedie (1983) to show thatthis implies that the state variable wt is ergodic and has afirst ergodic moment.

In this equilibrium, the above four restrictions can berelaxed sequentially:

1.

As equilibrium is stationary, the initial condition, w1,can be altered within its recurrent set withoutchanging equilibrium strategies. Large and Norman(2008) show that it can therefore be set to a stochasticvalue drawn from the ergodic distribution of wt; andthat the state process (wt) is then stationary.2.

There exists a value of x which exactly compensates‘blind’ traders for being uninformed of wt . Setting x tothis value implies that traders are willing to mix overZt , so that p is at a (weakly) optimal value.3.

Trader t’s best response to a buy–sell symmetricmarket is to act in a buy–sell symmetric way herself,so it is no restriction to impose that ct is buy–sellsymmetric.4.

Theorem 3.3 applies here, so fixing the value of cð0Þabove was not restrictive.Therefore:

Proposition 5.1. For all p 2 ð0;1Þ, there exists an x, such

that a buy–sell symmetric equilibrium exists where pt ¼ pfor all t.

6. Comments on the model and alternativeformulations

This section provides comments about adaptations tothe model which weaken or change leading assumptions.It addresses the effect of cancelation on the model, theconsequences of a change in the queuing rules enforced bythe exchange, and the robustness of the model to thefunctional form of F.

6.1. The functional form of F

Proposition 3.1 depends importantly on the specifica-tion of the functional form of F in Section 2.7. On thisproposition hangs the main Theorems 3.3 and 3.4. It istherefore important to understand the sensitivity of themodel to this tractability assumption. This subsectionaddress the issue in two ways. First, it considers the casewhere the CDF of bt is a uniform distribution, Fu, andconsiders the modification this brings to the results.Second, it shows that given any symmetric distribution forbt with support ½�bþ;bþ�, Theorems 3.3 and 3.4 are true inthe limit of a sequence of equilibria such that p! 0.

6.1.1. A uniform distribution for bt

Consider a buy–sell symmetric equilibrium wherep 2 ð0;1Þ, and where bt are i.i.d. random variablesdistributed uniformly between �bþ and bþ. Call the CDFof bt , Fu. Let F, not now a primitive of the model, be afunction satisfying the conditions in Section 2.7. Then,tracing through its proof, it can be seen that Proposition3.1 is still true: Fðc1ð0ÞÞ ¼ E½Fðc1ðZtwtÞÞ�. Equally, Lemma3.2 is also still true: the four order types are equallyprevalent in the order flow. However, it follows fromLemma 3.2 now that, in contrast to (16), E½Fuðc1ðZtwtÞÞ� ¼

14.

Rearranging,

c1ð0Þ � F�1u ð

14Þ ¼ F�1

ðE½Fðc1ðZtwtÞÞ�Þ � F�1u ðE½Fuðc

1ðZtwtÞÞ�Þ.

(25)

So c1ð0Þ differs from the median seller, F�1u ð

14Þ, by the

quantity on the right-hand side of (25). This has thefollowing interpretation: F�1

u ðE½Fuðc1ðZtwtÞÞ�Þ is the arith-metic mean of the finite elements of c1ðZtwtÞ

� . On the

other hand, F�1ðE½Fðc1ðZtwtÞÞ�Þ is a distorted, hyperbolic,

mean of them. Therefore, insofar as the hyperbolic meanapproximates the arithmetic mean, Theorem 3.3 isapproximately true.

6.1.2. A limit as p! 0Suppose now that bt are i.i.d. random variables,

distributed symmetrically about zero with support½�bþ;bþ�. Call the CDF of bt simply F. Consider a sequenceof buy–sell symmetric equilibria with p 2 ð0;1Þ of asequence of games where in the limit p! 0, so that asthe sequence progresses fewer and fewer traders observe wt .This is somewhat related to the idea of an exchange ‘goingdark,’ a phenomenon which has occurred, see Hendershottand Jones (2005).

Note that in the limit,

Fðc1ð0ÞÞ � Pr½ort ¼ sell� ! 0, (26)

for in a market where almost all traders observe Ztwt ¼ 0,the events ½ort ¼ sell� and ½btpc1ð0Þ� are almost the same.But Lemma 3.2 is true of every equilibrium in thesequence. Hence

c1ð0Þ ! F�1ð14Þ. (27)

Therefore, in the limit Theorem 3.3 is true. So, in the limitF�1ð14Þ is indifferent between ½ort ¼ ask� and ½ort ¼ sell�.

Therefore, in the limit (19) is true. Finally, the proof of thepaper’s main welfare result, Theorem 3.4 is true as stated,for the limit as p! 0.

6.2. Other queuing rules for limit orders

In the model, as almost universally in reality, limitorders execute in sequence according to price priority.When, however, they are equally priced, price prioritymust be supplemented by a further criterion: in the modelthey execute in the order in which they were submitted.

Field and Large (2008) exhibit an alternative to thistime priority (or FIFO) rule: some markets operate on apro rata system, whereby all limit orders at the same pricetrade simultaneously against each countervailing market

ARTICLE IN PRESS

J. Large / Journal of Financial Economics 91 (2009) 102–117 113

order. The market order is normally too small totrade with them all in their entirety. So, the trade isshared among the limit orders in proportion to their size(the exchange uses rounding rules and a coin-flip todistribute ‘odd lots’ arising due to quantity discreteness).

This can be implemented within the current model asfollows: suppose that an independent, fair coin-flip isused to allocate each sell (buy) to the extant bids at Bt

(asks at At). How would this change the results of themodel?

Since TAt and TB

t are not now measurable with respectto the history of orders, the proof of equilibrium existencedoes not follow as stated in Section 5. However, existenceaside, the characterizations of equilibrium in Theorems3.3 and 3.4 are true. Tracing through the proofs of thesetheorems, it can be seen that no distributional propertiesof TA

t and TBt are invoked. So the proofs remain valid under

the altered distribution.We may conclude, subject to a concern about equili-

brium existence, that trader surplus is unchanged by thealtered queuing rules. An intuition for this was given inthe Introduction.

6.3. Cancelation

This section discusses an adaptation to the modelwhere periodically limit orders are canceled involuntarily.This modeling feature is present in Goettler, Parlour, andRajan (2005) and Hollifield, Miller, and Sandas (2004), butis replaced with an endogenous cancelation decision inthe simulations in Goettler, Parlour, and Rajan (2004).Deliberate, endogenous cancelation of limit orders, whileoften the more realistic case, is harder to analyze in thisframework, and would be an interesting exercise forfuture work.

Adapt the model so that there exists g 2 ½0;1Þ, such thatat each time t, each extant bid and ask is independentlyremoved from the limit order book with probability g,without payoff to its submitter.

Although such involuntary cancelation may seemto be detrimental to traders, in fact it is advantageousfor trader surplus. When g ¼ 0 we revert to the originalgame. Consider a buy–sell symmetric equilibriumwhere g40. As some limit orders are now removedbefore they trade, stationarity implies that initially limitorders are voluntarily submitted more frequently thanmarket orders, and therefore more frequently than inequilibrium when g ¼ 0. Since setting g40 does notchange the payoff to a market order, if more limitorders are to be submitted, they must become moreattractive to traders in this equilibrium when g40,than when g ¼ 0. This implies that there is a highersurplus per agent.

So, the dominant effect of involuntary cancelation isthe positive externality for other limit orders when a limitorder is removed, causing them to trade sooner.12

12 A full proof of this (which would unfortunately require an

involved reformulation of the model) proceeds via the intermediate

result that if g40 then c1ð0ÞoF�1ð14Þ.

7. Average depths

As mentioned in the Introduction, surplus per agentmay be thought of as the gains from trade that are not lost(1) in the delay as limit orders await their counterpartiesor (2) in matching failures when the asset is bought (sold)by a trader with an excessively low (high) willingness topay. The first of these, waiting, is closely correlated withmarket depths. Therefore the identification of marketinefficiency in Theorem 3.4 may also be informative aboutaverage depths.

This section studies the stationary distribution ofdepths in a special case to understand better theirsensitivity to parameters in the trading environment. Itconcentrates simply on their first moment, namelyaverage inside depth: and shows that (to a first orderapproximation) this does indeed adjust in ways consistentwith the invariances implied by Theorems 3.3 and 3.4. Thesection is in this way complementary to the study inParlour (1998) of depths’ transitions from one state to thenext. The special case of the model that will be analyzedhas these features:

�

The

cou

thin

The market is a ‘two-tick’ market, where A ¼ Bþk, sothat there are only two admissible prices for trade:B and A.

� In equilibrium, the market is fairly efficient, so thate�rTAt 1.

�

In equilibrium p 0, so that inefficiencies arising dueto mismatched counterparties scarcely arise.13If the market is not two-tick, then limit orders riskbecoming ‘stale’ if At and Bt move far away before theyexecute. Their submitters may be compensated for this bylower inside depths. Where pb0, so that a substantialnumber of traders obtain order book information, averagedepths decline where such traders avoid adding to deeporder books, but rise where traders are drawn to supplyliquidity to order books of low depths. A characterizationof average inside depth under these generalizations isbeyond the current scope.

Definition 13. Define LAtþt for maxfLAt

t þ 1;0g. So LAtþt is a

measure of depth (where the inventory of the competitivefringe of traders outside the model is excluded). DefineLBtþ

t likewise.

Recall (19), which gave the equilibrium expecteddiscount factor associated with a limit order:

1� Etcask½e�rTA

t � ¼k

k

2� F�1 1

4

� � .

Via a Taylor expansion, we have that

1� e�rTAt ¼ rTA

t þ OpððrTAt Þ

2Þ. (28)

13 Theorem 3.3 shows that when Zt ¼ 0, player t sells iff bto0.

refore, when p 0 the inefficiencies arising due to badly matched

nterparties are almost zero. More precisely, as in Section 6 one may

k of a sequence of equilibria such that p! 0.

ARTICLE IN PRESS

J. Large / Journal of Financial Economics 91 (2009) 102–117114

As e�rTAt 1, ðrTA

t Þ2 is small, and

1� Etcask½e�rTA

t � rEtcask½TA

t �. (29)

Etcask½TA

t � is the expected time until LAtþt future buys have

been submitted. The duration between the consecutivearrivals of traders is D. Consider a sequence of equilibriawhere p! 0. In the limit, the probability of each futuretrader submitting a buy is 1

4. Hence in the limit

Etcask½TA

t � ¼ 4DE½LAtþt �. (30)

Combining (19), (28), and (30), when p 0

E½LAtþt �

1

4Drk

k

2� F�1 1

4

� �0BB@

1CCA. (31)

Although this analysis has considered the waiting time ofan ask at At , an equivalent analysis and the sameapproximation hold when At is replaced with Bt .

Comparative statics: On the basis of (31) some com-parative statics can be derived for the equilibrium average(positive) depths at the best ask, as captured by E½LAtþ

t �,which might also be called the average inside depths:

�

freq

for

Average inside depth is increasing in the tick size, k.This is because, as discussed in the Introduction, agreater tick size would cause a shortage of marketorders, unless depths rise to make limit orders lessattractive. This effect was observed in Goldstein andKavajecz (2000) and Harris (1994), and related predic-tions are made in Kadan (2006) and Seppi (1997).

� Average inside depth is increasing in the order arrivalrate, 1=D. An increased order arrival rate, would clear agiven depth faster. All other things being equal, thiswould attract too many limit orders to sustainstationarity. To offset this, equilibrium depths rise.This corresponds to a finding in Brockman and Chung(1996) for the stock exchange of Hong Kong.14

�

But average inside depth is decreasing in traderimpatience, r, since impatient traders avoid limitorders, violating the stationarity of wt , unless inducednot to by low depths.The latter two predictions are consistent with a findingin Foucault (1999), Foucault, Kadan, and Kandel (2005),and Rosu (2006): namely, that spreads narrow whenimpatience, r, falls, or when the time between traders, D,falls. If narrower spreads and higher inside depths areboth observable effects of aggressive limit order submis-sion, then their sensitivities to D and r should be alike.

8. Conclusion

The market-clearing condition is a central means ofanalyzing prices without modeling market microstructuredetails directly. In focusing on these details, this paper

14 See also Danielsson and Payne (2002) which, at a 20-second

uency, gives nuanced evidence on depths and order flow dynamics

Reuters FX markets. It does not fully isolate inside depths.

rediscovers market clearing in a different context: ina minimal stationarity property of microstructuredynamics, meaning that a limit order book induces inexpectation equal numbers of market orders and uncan-celed limit orders over time. To understand the conse-quences of this, a limit order market is modeled where thebid–ask spread is almost always constant. Its stationaritypermits us to derive welfare, and the best response ofparticular traders, while bypassing altogether their diffi-cult problem of forecasting the dynamic order book.Applying this approach to stochastic sequential gameswith binary action, such as queuing, may offer anintriguing opening for future research.

Equilibrium effects lead to striking invariances intrader surplus: with respect to changes in the sophistica-tion of trading (p); in the rate of order flow (D); and inlimit order queuing rules. In every such case, the market’sendogenous inefficiency does not vary, for its anticipatedsensitivity to the change is perfectly offset by endogenousequilibrium adjustments, for example in average depths.

But trader surplus is decreasing in the tick size. Cuttingthe tick size lets the bid–ask spread decline, improving theprospects of a market order, and thereby overcomingtraders’ incentives to add their limit orders to an already-congested limit order book. Trader surplus is therebyenhanced.

This provides an intuition for using the quoted oreffective spread as a measure of market quality: for itshows that a wide bid–ask spread not only penalizesmarket orders but also penalizes limit orders, viaequilibrium effects (although it might, on the face of it,appear to favor limit orders). Extending this insight toother forms of market microstructure institution, whichmight involve introducing a market-clearing role forbid–ask spreads as well as for market inefficiency anddepths, represents another future research avenue ofconsiderable interest.

Appendix A

A.1. Definition of a buy–sell symmetric equilibrium

Definition 14. For any vector v, let revðvÞ be v withits elements reversed. Say a function f is buy–sellsymmetric if for any argument, v, f ð�revðvÞÞ and revðf ðvÞÞ

exist, and

f ð�revðvÞÞ ¼ �revðf ðvÞÞ. (32)

Definition 15. An equilibrium is buy–sell symmetric if c isbuy–sell symmetric.

Note that �revðwtÞ represents a limit order book wherethe unfilled bids and asks in the order book at time t havebeen ‘swapped.’ Put loosely, Definition 15 states that abuyer responds to wt just as a seller would respond to�revðwtÞ. This has the consequence that the (ordered)pair of processes ðw;bÞ has the same distribution asð�revðwÞ;�bÞ.

ARTICLE IN PRESS

J. Large / Journal of Financial Economics 91 (2009) 102–117 115

A.2. Proof of Proposition 3.1

Note that in equilibrium

Etcask½e�rTA

t jZtwt ¼ 0� ¼ Etcask½e�rTA

t �, (33)

for the fact that Zt ¼ 0, provides no information about thestate of the process w. The lower bound imposed on bþ inSection 2.7 ensures that all finite cutoffs c1ðZtwtÞ areidentified by (11) and within the support of bt . Rearran-ging (11), using the definition of F,

Fðc1ðZtwtÞÞ ¼Zkð1� Et

cask½e�rTA

t jZtwt�Þ. (34)

Taking expectations in (34),

Etcask½Fðc1ðZtwtÞÞ� ¼

Zkð1� Et

cask½e�rTA

t �Þ. (35)

From (33) and (34), the right-hand side of this is Fðc1ð0ÞÞ.So the proposition follows on observing that since thedistribution of Ztwt is unchanged by a change in ct ,

E½Fðc1ðZtwtÞÞ� ¼ Etcask½Fðc1ðZtwtÞÞ�. (36)

A.3. Proof of Theorem 3.4

The expected payoff ex ante to player t is E½PðbtÞ�. Sincep 2 ð0;1Þ, the player is indifferent to the realization of Zt . SoE½PðbtÞ�¼E½PðbtÞjZt ¼ 0�: The right-hand side of this is, fromTheorem 3.3 and (8), and exploiting the buy–sell symmetry,

1

2E bt �

k

2

Zt ¼ 0; ort ¼ buy

� �, (37)

þ1

2E bt þ

k

2

�e�rTB

t

� Zt ¼ 0; ort ¼ bid

� �. (38)

Rewriting, this is

1

2EðbtjZt ¼ 0; ort ¼ buyÞ �

k

4, (39)

þ1

2Eðbt jZt ¼ 0; ort ¼ bidÞ þ

k

4, (40)

�1

2E bt þ

k

2

� �ð1� e�rTB

t Þ

Zt ¼ 0; ort ¼ bid

� �. (41)

The first two lines of this sum to EðjbtjÞ. So, the wholeexpression is

EðjbtjÞ �1

2dF�1 3

4

� �þ

k

2

� �E½1� e�rTA

t jZt ¼ 0; ort ¼ ask�,

(42)

and, finally, from (19),

E½1� e�rTAt jZt ¼ 0; ort ¼ ask� ¼ 1� Et

cask½e�rTA

t � ¼k

k

2� F�1 1

4

� � .

(43)

A.4. Stationarity of the state, wt

This section discusses how to use drift conditionresults in Large and Norman (2008), which applies results

in Tweedie (1983), in order to prove the stationarity of thestate wt when in stationary Markov equilibrium underrestrictions 1–4 of Section 5.

From Tweedie (1983) we can infer the followingcondition:

Condition A.1. Let Wt , defined for t 2 N, be a Markov

process with state space contained in Z, where for all Wt the

conditional support of ðWtþ1 �WtÞ is f�1;0;1g. Suppose

that there exists a threshold L� 2 N and Z 2 Rþ such that

E½jWtþ1jjWt�pjWtj � Z

whenever jWtj4L�. Then a distribution may be given to W0

so that Wt is stationary.

An intuition for this condition is that the process revertstoward zero outside ½�L�; L��, so that L� and �L� arepositive recurrent. It is now applied in various cases whenWt is a function of the offered depth at time t.

A.4.1. First, let Wt ¼minðw1t ;0Þ

So Wt is non-zero only in the case of a negative depthat Bt , when Bt ¼ B. Then (1) no player, knowing that thebid depth is negative, would submit a buy (since a bid

would have superior slippage and also execute immedi-ately) and (2) if bt ¼ 0 player t would submit a bid. SoPr½ort ¼ bidjZt ¼ 1�4 1

2, while only types below �k=2 canprefer to sell, so Pr½ort ¼ selljZt ¼ 1�pFð�k=2Þ. Players withZt ¼ 0 submit bids and sells with equal probability. Hencein the case of a negative depth at Bt bid pressure strictlyexceeds sell pressure, and there is upward drift to thenegative depth, back towards zero.

A.4.2. Second, let Wt ¼ minðLAtþt ; LBtþ

t Þ

Recall that LAtþt is maxfLAt

t þ 1;0g, and LBtþt is

maxfLBtt þ 1;0g. So Wt is the lesser of the two inside

depths, provided it is positive. For any natural number L,let LAðL; tÞ O be the set fo 2 O : Wt ¼ L; ort ¼ askg andconsider the quantity

supfE½e�rTAt jwt ; ort�ðoÞ : o 2 LAðL; tÞg. (44)

For all t this quantity converges to zero as L!1 sincetime to execution is at most as fast as if all future traderssubmitted buys, a time which becomes arbitrarily distantas L!1. Hence from (11), inffc1ðwtÞ : Wt ¼ Lg convergesto �k=2 (from below) as L!1, and so inffFðc1ðwtÞÞ :Wt ¼ Lg converges to Fð�k=2Þ, which is 4 1

3. Hence thereexist L� and a4 1

3 such that for all L4L�,

Pr½ort ¼ selljZt ¼ 1;Wt ¼ L�4a413. (45)

There is an equivalent argument on the other side of thebook, and that bid, ask, sell, and buy are of course mutuallyexclusive. Hence there also exist L� and Z40 such that forall L4L�,

Pr½ort ¼ selljZt ¼ 1;Wt ¼ L�413þ Z,

Pr½ort ¼ buyjZt ¼ 1;Wt ¼ L�413þ Z,

Pr½ort ¼ bidjZt ¼ 1;Wt ¼ L�o13� Z,

Pr½ort ¼ askjZt ¼ 1;Wt ¼ L�o13� Z.

ARTICLE IN PRESS

J. Large / Journal of Financial Economics 91 (2009) 102–117116

Therefore there exists an Z�40 such that if Wt4L�,

E½Wtþ1jWt ; Zt ¼ 1�oWt � Z�. (46)

But as, when Zt ¼ 0, bid, ask, sell, and buy are played withequal probability,

E½Wtþ1jWt ; Zt ¼ 0� ¼Wt . (47)

Combining the last two equations using the law of iteratedexpectations,

E½Wtþ1jWt ; Zt ¼ 1�oWt � pZ�. (48)

A.4.3. Third, let Wt ¼ jLAtþt � LBtþ

t j

So, disregarding negative depths, Wt is the absolutedifference between the depth at the best bid, and thedepth at the best ask. As the equilibrium is buy–sellsymmetric, consider w.l.o.g. the case where LAtþ

t 4LBtþt . Let

c2ðwtÞ be the second element of cðwtÞ. Then,

k

2� c2ðwtÞ

� �Et

cask½e�rTA

t jwt� ¼k

2þ c2ðwtÞ

� �Et

cbid½e�rTB

t jwt�.

(49)

Now, Etcbid½e�rTB

t jwt � is at most as great as e�rDLBtþt since time

to execution is at most as fast as if all future traderssubmitted sells. And, Et

cask½e�rDTA

t jwt� is larger thane�rL

Atþt Fð�bþÞ, since for all wt there is probability of at least

Fð�bþÞ of a trader arriving who submits a buy. Using theseinequalities,

k

2� c2ðwtÞ

� �e�rDL

Atþt Fð�bþÞ4

k

2þ c2ðwtÞ

� �e�rDL

Btþt (50)

so

e�rDðLAtþt Fð�bþÞ�L

Btþt Þ41þ

2c2ðwtÞ

k

2� c2ðwtÞ

� � . (51)

Under the maintained assumption that LAtþt 4LBtþ

t ,

WtFð�bþÞoLAtþ

t Fð�bþÞ � LBtþt . (52)

So,

sup2c2ðwtÞ

k

2� c2ðwtÞ

� � : Wt ¼ L

8>><>>:

9>>=>>;oe�rDLFð�bþÞ � 1, (53)

and, via an increasing transformation,

supfFðc2ðwtÞÞ : Wt ¼ LgoF

k

2ðe�rDLFð�bþÞ � 1Þ

2þ e�rDLFð�bþÞ � 1

0B@

1CA, (54)

so that

supfFðc2ðwtÞÞ : Wt ¼ Lg ! F �k

2

� �, (55)

as L!1. As inffFðc1ðwtÞÞ : Wt ¼ Lg converges to Fð�k=2Þfrom below,

limL!1

Pr½ort ¼ askjZt ¼ 1;Wt ¼ L� ¼ 0. (56)

But for all wt there is probability of at least Fð�bþÞ of atrader arriving who submits a buy.

Therefore there exists an L� and an Z�40 such that ifWt4L�,

E½Wtþ1jWt�oWt � Z�. (57)

A.4.4. Conclusion

The three previous parts showed that minðLBtt ;0Þ,

minðLAtt ;0Þ, and minðLAtþ

t ; LBtþt Þ are ergodic with first

ergodic moment, and therefore can be given initialdistributions so that they are stationary with firstmoment. Then, minðLBt

t ; LAtt Þ can also; and the third part

showed that jLAtþt � LBtþ

t j can also. Combining theseresults, we have that LBt

t and LAtt can be given initial

distributions so that they are stationary with firstmoment, so that they are positive recurrent at zero.Therefore the support of the random variables At and Bt isfB;Bþk; . . . ; A� k; Ag, implying that wt can be given aninitial distribution so that it is stationary with firstmoment.

References

Ahn, H., Cao, C., Choe, H., 1996. Tick size, spread and volume. Journal ofFinancial Intermediation 5, 2–22.

Ahn, H., Cao, C., Choe, H., 1998. Decimalization and competition amongstock markets: evidence from the Toronto stock exchange cross-listed securities. Journal of Financial Markets 1, 51–87.

Anshuman, V., Kalay, A., 1998. Market making with discrete prices.Review of Financial Studies 11 (1), 81–109.

Bernhardt, D., Hughson, E., 1996. Discrete pricing and the design ofdealership markets. Journal of Economic Theory 71, 148–182.

Bessembinder, H., 2000. Tick size, spreads, and liquidity: an analysis ofNasdaq securities trading near ten dollars. Journal of FinancialIntermediation 9, 213–239.