Embed Size (px)

Citation preview

A Lot of Hot Air or Coming Disaster: Insurance Coverage for Global Warming Claims

2

Up in Smoke: Insurance Coverage for Global Warming Issues

Presented by:Collin J. Hite

Firmwide Practice Leader, Insurance Coverage Counseling & Litigation GroupMcGuireWoods LLP

Copyright 2009-2010 Collin J. Hite. All Rights Reserved.

3

The Big Four- Cases that Is

• Massachusetts v. EPA• State of Connecticut v. American Electric Power

Company, Inc.• Native Village of Kivalina v. Exxonmobil Corp.• Comer v. Murphy Oil USA

4

Massachusetts v. EPA

• Legally recognized the danger of global warming• Recognized the EPA has authority to regulate

greenhouse gases• Establishes standing threshold for plaintiffs

– Plaintiffs possessed “quasi-sovereign interests” in safeguarding its real property and population from harmful effects of global warming

5

The ocean is rising- let’s sue

6

• Government- standing as large land owner– Coastal property– Sea rising as example of

harm

• Creates standing for any large landowner????

• Signaled a sure sign of litigation to come

7

8

State of Connecticut v. American Electric Power Company, Inc.• 139 page decision reversing trial court• Rejected application of political question doctrine• Found that Plaintiffs did have standing• Found that Plaintiffs did state viable claims under

federal common law of nuisance• Found that Plaintiffs’ claims were not displaced or

preempted at this time

9

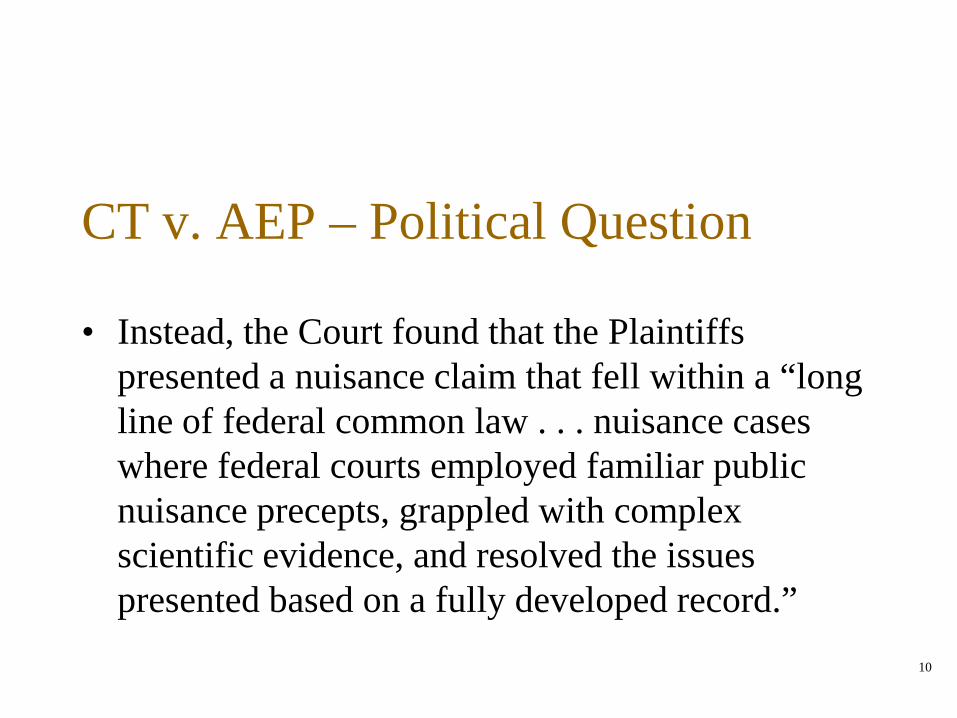

CT v. AEP – Political Question

• Court set a very high bar for application of political question doctrine

• Court concluded that “the Plaintiffs do not ask the court to fashion a comprehensive and far-reaching solution to global climate change, a task that arguably falls within the purview of the political branches.”

10

CT v. AEP – Political Question

• Instead, the Court found that the Plaintiffs presented a nuisance claim that fell within a “long line of federal common law . . . nuisance cases where federal courts employed familiar public nuisance precepts, grappled with complex scientific evidence, and resolved the issues presented based on a fully developed record.”

11

CT v. AEP – Political Question

• The fact that “Plaintiffs’ injuries are part of a worldwide problem does not mean Defendants’ contribution to that problem cannot be addressed through principled adjudication.”

12

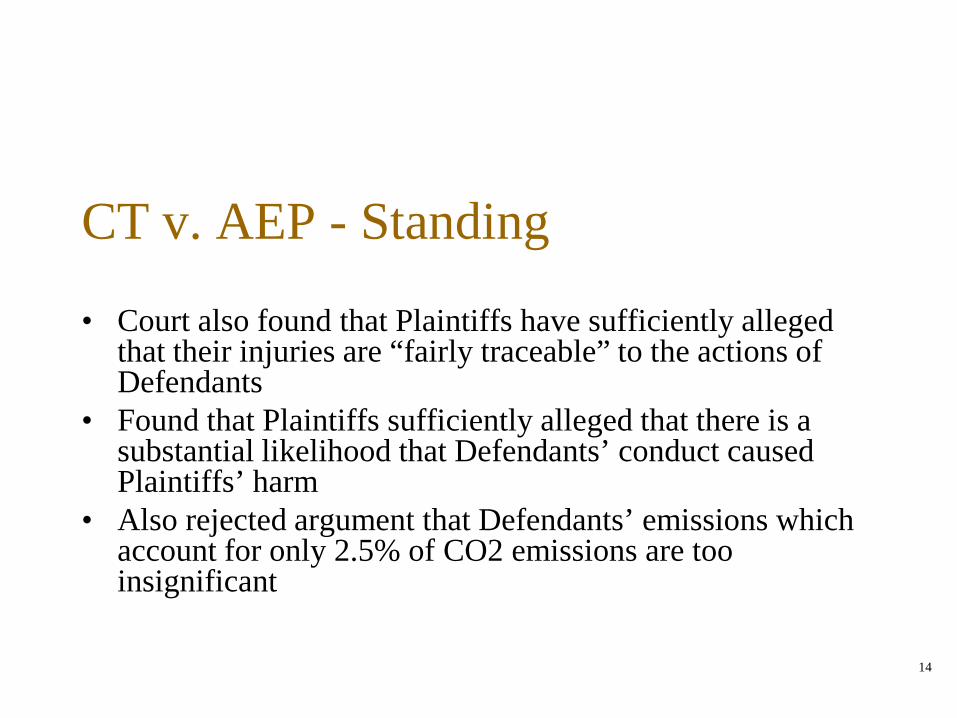

CT v. AEP - Standing

• Court also found that Plaintiffs had standing• Found that Plaintiffs did allege current injury• Piggybacked on Mass. v. EPA which held that coastal

erosion caused by global warming was a current injury• Found that the reduced size of the California snowpack

which has resulted in declining water supplies and flooding was a concrete injury that far exceeds a trifle

13

CT v. AEP - Standing

• Also found that future injury allegations such as rising sea levels causing flooding made by Plaintiffs are proper because they are “imminent” threats

• Court agreed that effects alleged by Plaintiffs are “certain to occur” and are “certainly impending”

• Relied again on Mass. v. EPA to find that incremental injury suffices for injury in fact: “The risk of catastrophic harm though remote is nevertheless real.”

14

CT v. AEP - Standing

• Court also found that Plaintiffs have sufficiently alleged that their injuries are “fairly traceable” to the actions of Defendants

• Found that Plaintiffs sufficiently alleged that there is a substantial likelihood that Defendants’ conduct caused Plaintiffs’ harm

• Also rejected argument that Defendants’ emissions which account for only 2.5% of CO2 emissions are too insignificant

15

CT v. AEP - Displacement

• Court also held that Plaintiffs’ claims are not displaced at this time by existing federal statutory law.

• “It may happen that new federal laws and new federal regulations may in time pre-empt the field of federal common law of nuisance. But until that comes to pass, federal courts will be empowered to appraise the equities of the suits alleging creation of a public nuisance by greenhouse gases.

• Court did address the proposed EPA Endangerment finding and said that this finding would not be enough to result in displacement even if made final

1616

Kivalina, Alaska Sued 20 U.S. Oil, Power and Coal Companies for $400MM Due to Global Warming

1717

Kivalina v. ExxonMobil Corp.

• Village must relocate due to erosion / flooding caused by GW

• Defendants emit millions of tons of greenhouse gases

• Defendants responsible for impact of GW

• Defendants created public nuisance and engaged in conspiracy

• “Long campaign by power, coal and oil companies to mislead the public about the science of global warming”

• $400MM Damages– past and ongoing contributions

to GW – furthering conspiracy to

suppress link between emissions and GW

18

Native Village of Kivalina v. Exxonmobil Corp.• Trial court dismissed case• Found that the case poised political questions• Court had issues with standing• Took an opposite view from the Second Circuit

19

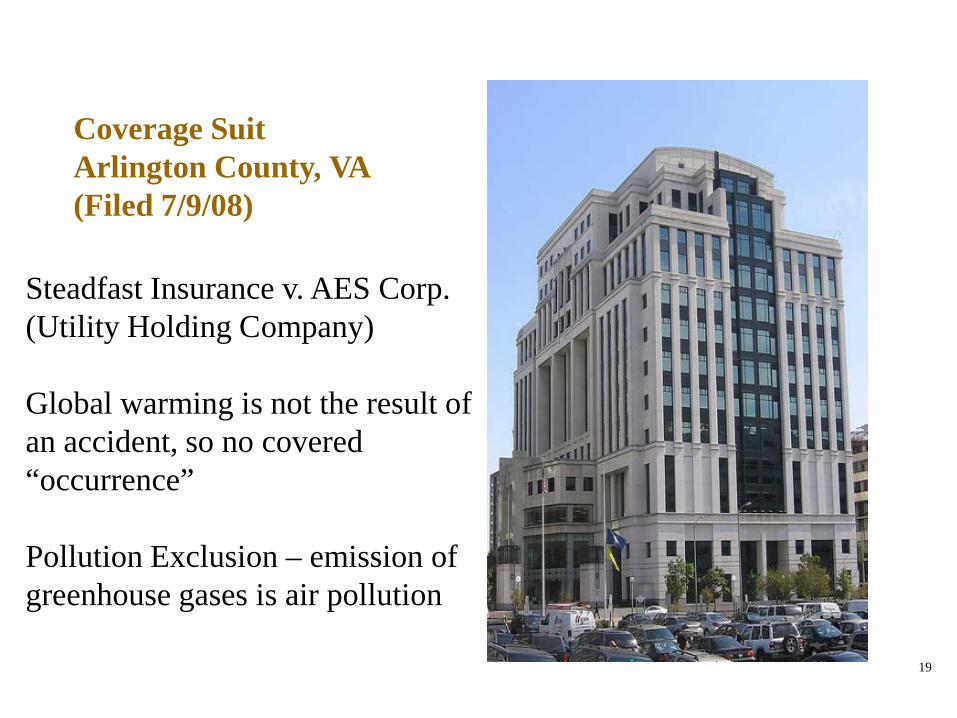

Coverage Suit Arlington County, VA(Filed 7/9/08)

Steadfast Insurance v. AES Corp. (Utility Holding Company)

Global warming is not the result of an accident, so no covered “occurrence”

Pollution Exclusion – emission of greenhouse gases is air pollution

20

Comer v. Murphy Oil USA

• 5th Circuit allows case by private citizens

• Claims are nuisance, negligence and trespass

• Had been dismissed for lack of standing and political question jurisdiction

• Follows the 2nd Cir.’s logic in Connecticut v. AEP

• BEWARE- nuisance is where the plaintiffs’ trial bar is headed

21

Insurer’s Response

• Withdraw from risky markets- coastal areas• Reduce writing of new risk in these areas or raise

premiums• Encourage govt. to adopt stronger building codes

22

Insurer’s Proactive Efforts

• Breaks for hybrid autos• Encourage construction with green technology

23

Insurance Coverage & Climate Change

• Property claim- will rise– Coastal– Droughts and fires– Business interruption

• Third party liability– Looks backwards– Regulatory action– D&O and Professional

Liability– Green tech services= E&O

24

Is There Coverage for Global Warming?

• Fortuity Requirement– Expected or intended exclusion

• Purposefulness of act vs. expectation of harm• Insurers more likely to have success that insured intentionally

emitted climate changing greenhouse gases• This intentional act means- no accident• Insurers can argue that as of a certain date insured expected it

was causing harm

25

Loss in Progress Rule

• Precludes coverage for damage beginning prior to inception of policy

• “Montrose endorsement”• Some courts limit application• Trend is a broader application against

policyholders

26

The Pollution Exclusion

• pollution exclusionA provision in either first-party or third-party insurance policies that excludes coverage for losses caused by "pollution," a term usually defined to mean an irritant or contaminant, whether in solid, liquid, or gaseous form, including—when they can be regarded as an irritant or contaminant—smoke, vapor, soot, fumes, acids, alkalis, chemicals, and waste.

27

• “Sudden and Accidental” Pollution Exclusion• Absolute Pollution Exclusion• Pollution Exclusion with 72-hour Clause

28

Wrap Up Coverage Issues

• Trigger of Coverage• Allocation• Punitive Damages• Anti-Stacking• D&O Issues

29

THANK YOU

Collin J. HiteMcGuireWoods LLP

901 East Cary Street, Richmond VA 23219Direct Telephone: 804.775.7791

Facsimile: [email protected]

Business DepartmentCapital Markets | Energy & Utilities | Health Care | International | Land Use & Environmental

Mergers & Acquisitions, Securities & Corporate Services | Real Estate Transactions | Tax & Employee Benefits | Technology & Business

Litigation DepartmentAntitrust & Trade Regulation | Business & Securities Litigation | Complex Commercial Litigation | Financial Services Litigation | Government Investigations

IP Litigation/Patents | Labor & Employment | Product & Consumer Litigation | Restructuring & Insolvency | Toxic Torts & Environmental Litigation

ATLANTA • BALTIMORE • CHARLOTTE • CHARLOTTESVILLE • CHICAGO • JACKSONVILLE • LOS ANGELESNEW YORK • NORFOLK • PITTSBURGH • RALEIGH • RICHMOND • TYSONS CORNER • WASHINGTON, D.C. • WILMINGTON

ALMATY, KAZAKHSTAN | BRUSSELS, BELGIUM | LONDON, UNITED KINGDOM

www.mcguirewoods.com

2009 McGuireWoods LLP

www.marsh.com

Climate ChangeIs it a GL or an Environmental Issue?

May 18, 2010

Peter MavraganisSenior Vice PresidentMarsh Global Energy Practice [email protected]

Carbon Capture andStorage

32Marsh

Carbon Capture and StorageMajor Global Regulatory and Risk Issues

Is C02 a waste product or pollutant?

How will CO2 Emissions be Managed and Reduced– Carbon Capture and Storage (CCS) Who will be liable for long term storage? Make CCS mandatory or optional? How to make CCS economically attractive? What is the value of each unit of sequestered C02? How will underground reservoir ownership be determined? How to deal with multiple levels of regulations? How to relate CCS to Emissions Managed and Reduced Through

- Enhanced Oil Recovery- Enhanced Methane Recovery?

More Efficient Scrubber Technology

Carbon Capture and Storage – Project Risks

34Marsh

Carbon Capture and StorageProject Risks

Carbon Capture– Contingent processing risks Syngas explosions Air separation Units/ Oxygen High temperature gasification CO2 removal / Refrigeration Integrated Gasification Combined Cycle (IGCC) machinery

breakdown– CO2 specific risks Supercritical state post compression – pressure/temperature Personnel hazards Pipelines Carbon credit revenue (Business Interruption)

35Marsh

Carbon Capture and StorageProject Risks

Carbon Storage projects– Well blowout injection wells– Short term liabilities– Long tail pollution liabilities (Environmental risks)– Loss of carbon credits

Contingent risks between Capture and Sequestration projects– Most of the projects have interdependency risks with CO2 sales

agreement – title changing at the capture plant– Both parties are therefore exposed from a revenue point of view to

each others risks– Insurance solution – Suppliers and Customers extension to traditional

Business Interruption coverage (BUT – there has to be damage!)– Need for coverage flexibility - Traditional property damage processing

risks (Capture projects) linked to reservoir integrity risks (CCS)

36Marsh

Carbon Capture and StorageCO2 Specific Catastrophic Financial Risks

Remediation costs associated with ground water contamination….deep formations can be very costly to remediate– Carbonic acid – Mobilization of contaminants such as Lead and Arsenic– Displacement and migration of brines

Third party liabilities resulting from major release of CO2 from storage system

Financial impact to business if foreseen CO2 credits are not traded or banked– Replace first party credits Reputational risk if not replaced Inflation in carbon trading market results in replacement costs

higher than expected– Over the counter trading: Contractually bound to replace carbon credits? Cost to replace credits (either direct cost or unanticipated inflation)

37Marsh

Carbon Capture and StorageInsurance Role

Construction All Risk– Fire and explosion– Natural perils e.g. earthquake, water inundation– Accidental impact– Defective workmanship or materials

Construction All Risk – Advance loss of profits– To include CO2 sales and carbon credit revenue– Contingent risks

Project cargo insurance– Loss or damage to processing equipment

Professional Indemnity – for CCS advisors and engineers

Third party liability – for project phase including commissioning and maintenance periods

Contractors pollution liability – may be relevant for sophisticated CCS implementation projects

Well control – for drilling CO2 injection wells into existing reservoirs

Carbon credit delivery guarantee – for technology performance risk

Construction phase

38Marsh

Carbon Capture and StorageInsurance Role

Operational phase

Property All Risks / Business interruption– Carbon capture processing and CCS surface facilities focus– Business interruption to include carbon credit consideration, EOR

revenue and contingent capture / storage risks– C02 inventory loss – compensation needed?

Third party liability

Environmental liability (storage focus) – principal and contractor focus for potential sub surface problems

Well control for injection wells – blowout risk and associated liabilities including evacuation costs

39Marsh

Carbon Capture and StorageInsurance Role

Facility Closure and Decommissioning

• Risks comparable to those for energy or chemical plant

• Should consider plugging of injection wells and associated risks

• Should consider any implications for loss of earnings due to delays

Post Closure

• Post-closure liabilities unlikely to be insurable due to very long time scales and uncertainty in predicting geological behaviour

• Proposed fund for long term measurement, monitoring and verification costs provided by operator

• When does owner liability end?

40Marsh

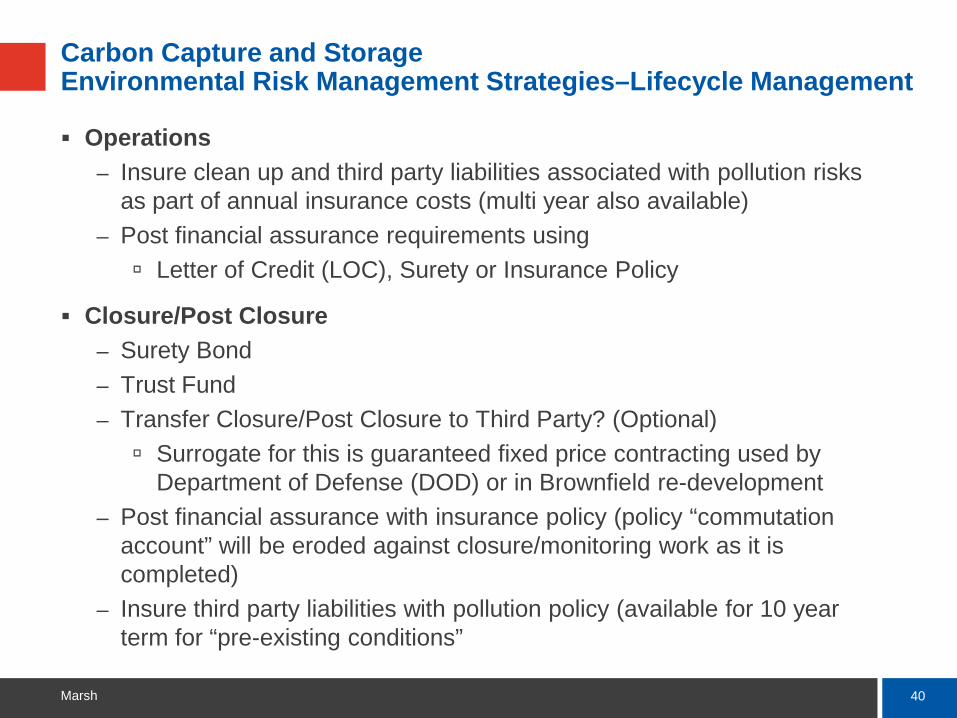

Carbon Capture and StorageEnvironmental Risk Management Strategies–Lifecycle Management

Operations– Insure clean up and third party liabilities associated with pollution risks

as part of annual insurance costs (multi year also available)– Post financial assurance requirements using Letter of Credit (LOC), Surety or Insurance Policy

Closure/Post Closure– Surety Bond– Trust Fund– Transfer Closure/Post Closure to Third Party? (Optional) Surrogate for this is guaranteed fixed price contracting used by

Department of Defense (DOD) or in Brownfield re-development– Post financial assurance with insurance policy (policy “commutation

account” will be eroded against closure/monitoring work as it is completed)

– Insure third party liabilities with pollution policy (available for 10 year term for “pre-existing conditions”

41Marsh

Carbon Capture and StorageInsurance Consideration Summary

“Traditional Risks”

Property Policies readily available – Years of experience with similar operations

Casualty Program Considerations– Is a catastrophic loss sudden and accidental?– Maintain sudden and accidental coverage in casualty program– AEGIS typically used for Power/Energy/Utility clients, but may

exclude “disposal” which could be defined as applying to sequestration

– Traditional Casualty programs will not cover gradual pollution events, will not provide first party clean up coverage, and will not provide coverage for waste disposal

42Marsh

Carbon Capture and StorageInsurance Consideration Summary

Pollution aspects of geologic sequestration are insurable– Traditional environmental insurance markets have forms which lend

themselves to covering these gradual losses– Precedent for writing similar risks through insuring subsurface gas

storage facilities– Market has responded and has underwritten pilot scale programs– Specialty form available which provides sudden and accidental,

transportation, control of well, gradual pollution coverage and nominally financial assurance

Limits of Liability?– Dependent on project (considerations) Depth of sequestration Presence of shallow aquifers High consequence area?

Closure/Post Closure Care– Liability in Perpetuity?– Surety and Trust Funds– Insurance?

43Marsh

The information contained in this publication provides only a general overview of subjects covered, is not intended to be taken as advice regarding any individual situation, and should not be relied upon as such. Insureds should consult their insurance and legal advisors regarding specific coverage issues. All insurance coverage is subject to the terms, conditions, and exclusions of the applicable individual policies. Marsh cannot provide any assurance that insurance can be obtained for any particular client or for any particular risk.

Statements concerning legal matters should be understood to be general observations based solely on our experience as insurance brokers and risk consultants and should not be relied upon as legal advice, which we are not authorized to provide. All such matters should be reviewed with your own qualified legal advisors.

All insurance coverage is subject to the terms, conditions, and exclusions of the applicable individual policies. Marsh cannot provide any assurance that insurance can be obtained for any particular client or for any particular risk.

Marsh is part of the family of MMC companies, including Kroll, Guy Carpenter, Mercer, and the Oliver Wyman Group (including Lippincott and NERA Economic Consulting).

This document or any portion of the information it contains may not be copied or reproduced in any form without the permission of Marsh Inc., except that clients of any of the MMC companies need not obtain such permission when using this report for their internal purposes, as long as this page is included with all such copies or reproductions.

Copyright 2009 Marsh Inc.MA10-10021 All rights reserved

www.marsh.com

Climate Change Litigation in Europe and Insurance Programs

Lex Mundi Webinar onInsurance Coverage for Global Warming Claims

Munich, May 18, 2010

Rechtsanwalt Uwe M. Erling, LL.M.,Rechtsanwalt Dr. Thomas Heitzer

46

Agenda

■ Climate change litigation in Europe

– Challenges under the European Emissions Trading Scheme

– Other Challenges

■ European concepts for environmental liability insurance programs

■ Developments in continental Europe and UK in climate change related insurance programs

Climate Change Litigation in Europe

48

Climate Litigation Overview

Claims under EU ETS vs. Govt.

■ challenges of allocation decision

- allocation rules

- benchmarks

- scope of scheme

■ monitoring and reporting

■ in Germany, more than 600 claims (2005 – 2007)

Claims of Others vs. Govt.

■ Micronesia vs. Czech Republic (2010)

■ Datteln Power Plant (2009)

■ only few cases so far

Claims vs. Industry

■ no cases so far

49

Micronesia vs. Czech Republic

■ Facts:

– Punerov Power Station biggest CO2 emitter in CZ (11.1 Mio. t/a)

– Federated States of Micronesia (107,000 citizens) filed objection with Czech Env. Ministry in January 2010 concerning overhaul permit

■ Legal basis for objection

– Czech Environmental Impact Assessment (EIS) Law

– no limit on which nation can participate in process

■ Reaction to claim

– government postponed decision

– reassessment of carbon output finds BAT of 42 % not met (39 – 40 %)

– EIS did not cover comparison BAT 42 % 39 – 40 %

– final decision pending

50

Datteln (Germany) Power Plant

■ Facts:

– E.ON plans to build coal burning power block 4 (1,100 MW) at city of Datteln

– net efficiency exceeds 45 %

– farmer files claim against zoning plan and argues against location

■ Higher Admin. Court for North-Rhine Westphalia (September 2009) declares zoning plan void, because (among other reasons)

– lack of compliance with state development plan, which requires resources and climate friendly energy usage

■ Federal Admin. Court (March 2010): upholds judgment

■ Outlook: city and state start new procedure to revise zoning plan and state development plan

European concepts for environmental liability insurance programs

52

EU Environmental Liability Directive

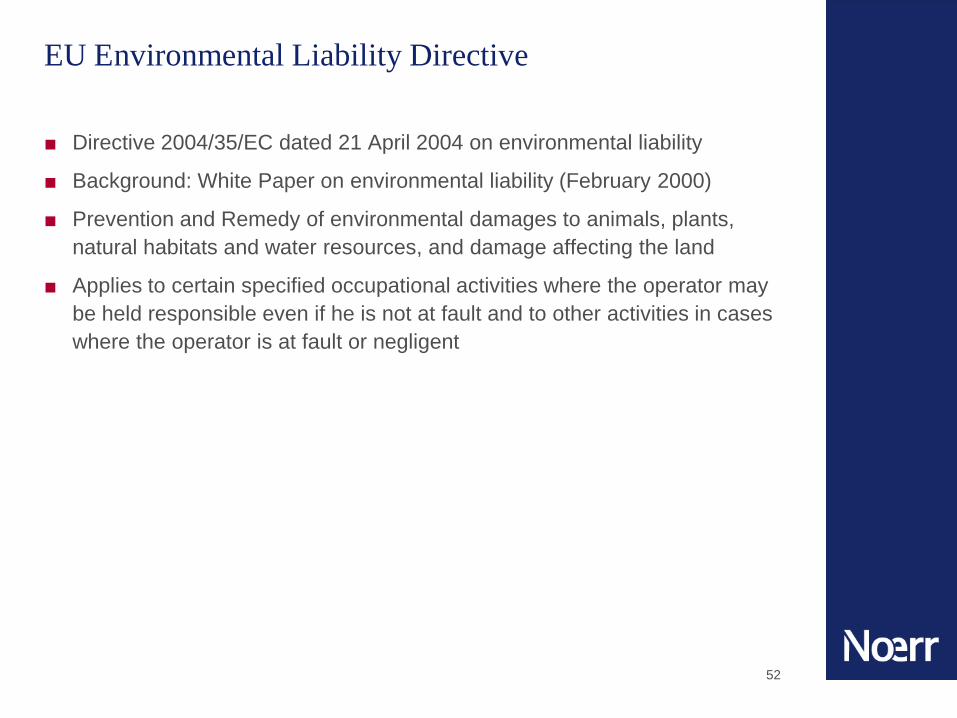

■ Directive 2004/35/EC dated 21 April 2004 on environmental liability

■ Background: White Paper on environmental liability (February 2000)

■ Prevention and Remedy of environmental damages to animals, plants, natural habitats and water resources, and damage affecting the land

■ Applies to certain specified occupational activities where the operator may be held responsible even if he is not at fault and to other activities in cases where the operator is at fault or negligent

53

EU Environmental Liability Directive

■ Is based (as the first EU legislation) on the „polluter pays“ principle, which

– was already set out in the Treaty establishing the European Community

– helps to deter breaches of environmental standards

– contributes to the achievement of objectives and the application of Community policy in this area

■ Includes no obligation for operators to take out a financial security, such as insurance, to cover their potential insolvency, however Member States are required to encourage operators to make use of such mechanisms

■ Transformation of Directive in EU Member States

54

German Environmental Liability Law

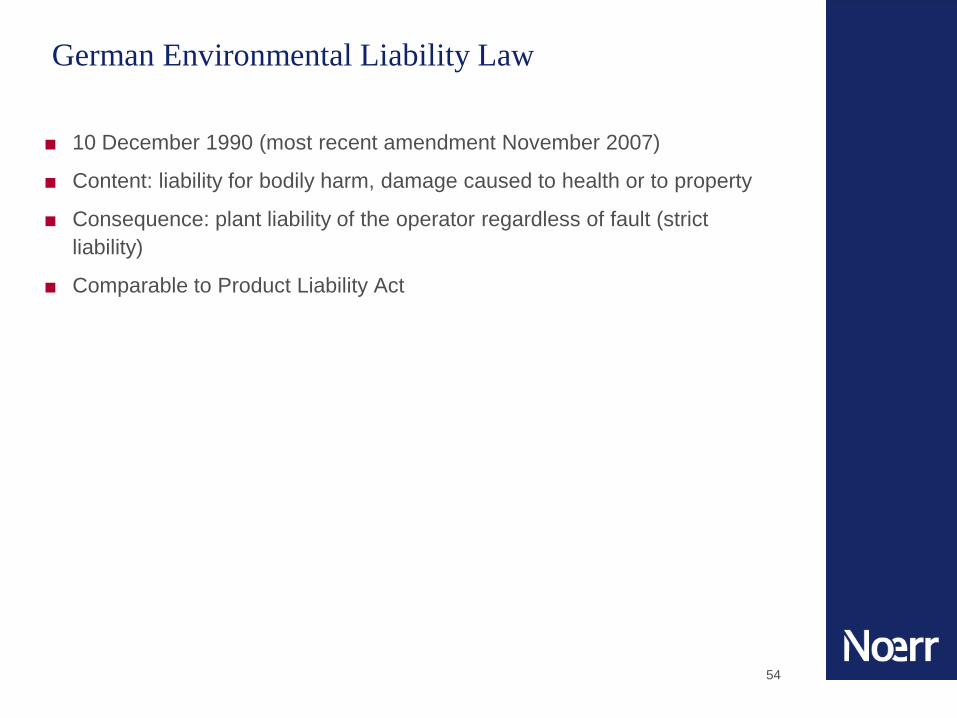

■ 10 December 1990 (most recent amendment November 2007)

■ Content: liability for bodily harm, damage caused to health or to property

■ Consequence: plant liability of the operator regardless of fault (strict liability)

■ Comparable to Product Liability Act

Developments in Continental Europe and UK in climate change related insurance programs

56

Climate Litigation Background

■ Cause of risk or damage:

– Increase of temperature, sea level or change in vegetation

– Extreme weather events being more frequent and intensive

– Due to scientific researches up to 90 % anthropogenic reasons

■ Potential plaintiffs:

– Private Individuals (in developing countries)

– Developing countries

– Countries in „trouble regions“, e.g. Small Island States

■ Potential defendants:

– Industry (energy, automobile, oil etc.)

– States

Insurance Coverage: Climate Change Liability Insurance?

57

Climate Litigation Background

■ Liability – Legal Problems:

– Jurisdiction

– Breach of duty by the defendant in regard to the plaintiffs

(negligence, strict liability, nuiscane, products liability, conspiracy)

– Injuries compensable in damages

– Causation

– Various polluters

– Specific damage cannot clearly be attributed to one polluter (multiple gases, billions of sources, worldwide mixing etc.)

– Damages caused by centuries of pollution

– Possibility to impose a generic liability for a group of defendants? How to allocate the liability among them?

– Measuring of damages; problem if damages not occurred yet

58

Climate Litigation Background

■ Today

– Different Types of Liability

– Direct: Damages directly caused by (carbon) emissions

– Indirect: Damages indirectly connected to climate change

– inter alia: D&O Liability, in the case the climate change has not been sufficiently considered

– Defense Coverage?

■ Tomorrow

– Increasing need for insurance due to indirect liability

– Legislation, judiciary and public get used to the idea of liability

– higher standards to mitigate climate change result in reducement of liability?

59

Climate Litigation Background

■ New Types of Coverage for New Types of Liability?

– breach of duty of information

– wrongful behaviour in Emergency Scenarios

– mistakes in the handling of catastrophes

Coverage under Company Liability Insurance / Product Liability Insurance?

60

Your Contact Partners

Uwe Marcus Erling, LL.M.RechtsanwaltT +49-(0)89-286 [email protected]

Dr. Thomas HeitzerRechtsanwaltT +49-(0)211-499 [email protected]

61

Offices

BerlinNoerr LLPCharlottenstraße 5710117 BerlinGermanyT +49-(0)30-20 94-20 00

BratislavaNoerr s.r.o.AC DiplomatPalisády 29/A81106 BratislavaSlovak RepublicT +421-(0)2-59 10 10 10

BucharestS.P.R.L. Menzer & Bachmann -NoerrStr. General ConstantinBudişteanu nr. 28 C, Sector 1010775 BucharestRomaniaT +40-(0)21-312 58 88

BudapestNoerr & Partners Law OfficeFő utca 14-181011 BudapestHungaryT +36-(06)1-224 09 00

DresdenNoerr LLPPaul-Schwarze-Straße 201097 DresdenGermanyT +49-(0)351-816 60-0

DüsseldorfNoerr LLPVictoriaplatz 240477 DüsseldorfGermanyT +49-(0)211-499 86-0

Frankfurt am MainNoerr LLPBörsenstraße 160313 Frankfurt am MainGermanyT +49-(0)69-97 14 77-0

KievNoerr TOVVul. Khreschatyk, 7/1101001 KievUkraineT +380-44-495 30 80

MoscowNoerr OOO1-ya Brestskaya ul. 29125047 MoscowRussian FederationT +7-495-799 56 96

MunichNoerr LLPBrienner Straße 2880333 MunichGermanyT +49-(0)89-286 28-0

New YorkNoerr LLPRepresentative Office885 Third Avenue, Suite 2406New York, NY 10022USAT +1-212-433-13 96

PragueNoerr v.o.s.Na Poříčí 1079/3a110 00 Prague 1Czech RepublicT +420-233 11 21 11

WarsawNoerr Sp. z o.o. Spiering Sp. k.Al. Armii Ludowej 2600-609 WarsawPolandT +48-(0)22-579 30 60

![BERRY ELEMENTARY SCHOOL · on next slide.] Buses will be dismissing in the bus parking lot as car riders are coming through the back of the bus lot---again travel slowly and carefully](https://img.pdfslide.us/doc/110x75/5f6b99f6c29fd2586f763f14/berry-elementary-school-on-next-slide-buses-will-be-dismissing-in-the-bus-parking.jpg)