Embed Size (px)

Citation preview

A Lesson of International Accounting from Railroad Regulationin the United States in the Nineteenth Century

Hidetoshi YamajiResearch Institute for Economics & Business Admin.

Kobe University

Content

Chapter One American Railroad Regulation in the Nineteenth Century and Emergence of

Modern Accounting Information Disclosure

I Preface

II Railroad Regulation in the State of Illinois in relation to the Granger Movement

II-1. Introduction

II-2. Conditions of the States in the Mid-West

II-3. Analysis of Railroad Regulation in the State of Illinois

III Railroad Regulation in the State of Massachusetts

III-1. Introduction

III-2. Conditions of the State of Massachusetts

III-3. Analysis of Railroad Regulation in the State of Massachusetts

IV Conclusion

Commission System and Accounting Information Disclosure

Chapter Two Accounting Information Disclosure of Multinational Enterprises in Contemporary

Times —in relation to Earlier Reports of the United Nation—

I Introduction

II Emergence of Accounting Information Disclosure of Multinational Enterprises

III Development of Accounting Information Disclosure of Multinational Enterprises

IV Turn of Accounting Information Disclosure of Multinational Enterprises

V Some Emerging Issues Conclusion

Chapter Three General Conclusion

I Adaptation of Accounting Information Disclosure to Problem of Multinational Corporations

II Adoption of Commission System by the United Nations

Chapter OneAmerican Railroad Regulation in the Nineteenth Century

and Emergence of Modern Accounting Information Disclosure

I Preface

I-1. IntroductionThe purpose of this paper is to provide an analysis of the relation between the railroad regulations

in the 19th century in the Unites States and the emergence of modern accounting information

disclosure. This analysis would be the base for searching the social foundations of modern accounting

information disclosure conducted in mass democratic society by the big enterprises. Concretely the

two ways of railroad regulation will be recognized in the variety of states' railroad regulations. The

one is the way in which the accounting information disclosure was adopted and the other is the way in

which it was invalid and the direct railroad business regulation by the state was employed. Moreover

the reason why there emerged such differences in railroad regulation is attributed to the differences in

the social and economic structure among states.

The railroad appeared in the 1830s was a catalyst for the social and economic development of the

United States in the nineteenth century. The many securities issued by the railroad corporations

established modern securities markets and communication and transportation systems were developed

along with railroads. As R. W. Fogel pointed out(1), it might have been followed at least a different

course of development of the steel industry, if there was no demand for the steel rails by the railroads.

With regard to the agriculture treated in the section II, this was also the case. The existence of the

railroads enabled to bring together agricultural products, in particular, wheat harvested in the inland

areas to the ports of the Pacific Ocean and to export them to Europe. In other words, the development

of railroads to the west in the United States was accompanied by the advancement to the west of

agricultural frontier so that the mid-western states became progressively the granary not only of the

United States but also of Europe.

The American railroad corporations in the 19th century adopted some kinds of business strategies

in the above-mentioned socio-economic conditions for accumulating their own capitals. On the other

hand, however, the bases of living for the farmers, merchants and mediate and small producers were

considerably influenced by business strategies selected by the relatively large railroad corporations.

This excessive influence caused the necessity of railroad regulations(2). In addition, the accounting

information disclosure was necessitated in certain conditions. Particularly it was adopted and became

important policy only in some states of the earlier period.

Section II will offer the case study in which the accounting information disclosure was adopted as a

means of regulating railroad corporations in failure and direct business regulation by state was

employed instead. Section III will provide the case study in which the accounting information

disclosure was a valid means. The former study was on the case of the state of Illinois and of some

Mid-Western states. The latter analysis was conducted on the state of Massachusetts and some Eastern

states. Section IV points out the elements of socio-economic foundations for emerging accounting

information disclosure.

II Railroad Regulation in the State of Illinois in relation to the Granger Movement

II-1. Introduction(3)

The United States in the nineteenth century was an agricultural country and was in reality

characterized as a granary of Europe which was, in turn, the center of the world economy. For the

inclusion of the American agriculture into the world economy, the establishment of the world-wide

transportation system which brought together farmers' products from inland areas to the shipping

ports of the East Coast which sent them off to Europe, was a physical precondition. That is, the

demand for gathering the grains to the East Coast stimulated the development of the transportation

system within America.

Steam boats running on rivers were the first means of inland transportation. Many canals were

constructed which connected one river to another river or rivers, and to the Great Lakes. Most famous

was the Erie Canal constructed in 1825. This was a kind of main artery which connected inland Mid-

Western areas to the East Coast. For the South, active transportation on the Mississippi River made

New Orleans prosperous.

After a while, railroad transportation came to play an important role as a substitute of the river

transportation for transporting grains. Railroad transportation originally functioned as a

supplementary system to the river and lake transportation, for example, in the case that the Great

Lakes froze in winter. But railroads progressively substituted for steam boats because of their speed

and were the first step for connecting it agriculture to railroads.

Although, earlier we emphasized the relationship between the railroads and agriculture, railroads

were at least in the early years, constructed by the capital contributed not by farmers but by capitalists

and merchants of the east coast area. The merchants of the east coast intended to earn profits from

connecting canals to their own cities, that is, the inland Mid-Western states to the east coast by

constructing railroads. But the direct and indirect aid from farmers became indispensable for

constructing the railroad in the Mid-Western states, only since the latter half of the nineteenth century.

In this area, railroads had the double function of bringing the industrial products and necessities of life

produced in the east cities to the Mid-Western area, and of sending the grains harvested in the latter

area to the former area. In the American domestic economy, the extension of railroads to western

states corresponds to the penetration into the farmers dotted in some frontiers of capitalistic

production system.

Fundamentally and economically the railroads were indispensable for the living of the farmers who

lived in the inland Mid-Western areas. But actually the relationship between railroad corporations and

farmers was not cooperative. It would be better to say that the history of the relationship between

these two organizations in the latter half of the nineteenth century was one of conflict. For railroad

corporations needed to accumulate the capital for the purpose of winning in the capitalistic

competition among railroad corporations. In consequence, they decided naturally to adopt the

management strategies which pressed the insufficiently organized and weak farmers, and small

producers and merchants. Reacting to the immoderate management of railroad corporations, farmers

began to organize themselves in broader areas and to develop an anti-railroad movement beginning in

the 1870s. In the following, we mainly analyze the living and economic conditions of the Mid-

Western farmers and take their relation with railroad corporations into consideration. This analysis is

helpful in finding the social and economic changes among farmers, local governments and railroad

corporations. Moreover, it should contribute to the comparative analysis of the case of the east coast

and its socio-economic foundation for the emerging modern accounting information disclosure in the

middle and the latter half of the 19th century in the United States.

II-2. Conditions of the States in the Mid-West

The most important and the broadest factor which stimulated the farmers to organize themselves

was the countermeasure against the pressure of large railroad corporations. But in this subsection we

should describe their living conditions in detail, in particular, their discontentment and dissatisfaction

in referring to the paper written by E.W.Bemis(4) at the end of the nineteenth century.

First we should point out that the farmers were unsatisfied with the low prices of agricultural

products in two aspects. One aspect was that the seasonal fluctuations in the prices of farm products

unfavorably affected the farmers. The other aspect was that the prices of grains decreased in the long

run. For judging whether the discontent of the farmers were the case or not, some data should be

offered in this context. Table I(5) shows the fluctuation in the price of spring wheat at the Chicago

Grain Exchange, which did not completely correspond to the proper period but may indicate the price

tendency. Figure I(6) provides the data which indicates the decreasing trends in the prices of farm

products. (The long term average price of ten staples in American wholesale markets were added as a

reference).

-------------------------------

Table I and Figure I about here

--------------------------------

From the data of Table I, we can say that the seasonal price of grain was considerably stable. This

was also the case for Corn and Oats in the same period. Bemis also concluded that the dissatisfaction

of the farmers in the period might be groundless by saying that ;

The figures tell their own story. They not only show at there is no fall in prices at harvest

when we should most expect it, but they reveal a remarkable evenness of price between all

the months over a series of years(7).

Therefore, It can not be proven that farmers sold at an unreasonably low price fixed by the pressure of

speculation in the harvest season.

Figure I shows clearly the long term decreasing trends of prices of agricultural products. Bemis was

not, however, in sympathy with farmers in the decreasing price tendencies of their produced goods

because there was no relative change in prices. The long term average prices of industrially produced

goods (iron, wool, oil, salt etc.) were also falling. Bemis thought that the economic conditions facing

farmers did not relatively change.

As far as we are depending upon the data offered by Bemis, farmers were not always unfavorably

influenced by the changes both in relative and in absolute prices of agricultural products. If so, the

dissatisfactions held by the farmers in the Mid-Western areas, were they at least partially a kind of

illusion ? We must pay attention to the fact that the price data inserted by Bamis was the one collected

at the Chicago Exchange although we can not concretely present the contra-data against Bemis's data.

The prices shown in Table I and Figure I were not prices at which the farmers sold their harvested

grains to brokers and were not the ones which the farmers entirely accepted. This fact has two

meanings. The one is that there were some differences between the prices at which farmers sold their

grains to brokers and the prices at which brokers sold them at the Exchange. The other is that these

prices should be related to the railroad and warehouse fees. Then we must refer to Table II (8)which

indicates that the fees at which farmers in the Mid-Western and the Southern areas sent their grains to

Chicago by train were relatively higher than the fees which dominated in the east coast areas. The

reason why the fees of transportation were relatively high should in reality be attributed not to

physical conditions but to the economically monopolistic positions held by the mid-western

railroad corporations and warehouse lenders. Naturally they charged high fees to the insufficiently

organized farmers(9). Consequently we must consider it unreasonably costly for farmers to send their

grains to the large exchanges located in big cities. Then there emerged a second and particularly

discontentment among farmers. That is, farmers were dissatisfied with the rapid accumulation of

properties by the railroad managers and warehouse lenders by using unfair rates systems which had

harmful effects on them. In considering both the changes in grain prices and the rate policies adopted

by the railroad and warehouse managers, we must conclude that the dissatisfaction held by the

farmers in the Mid-Western and the Southern areas became real ones by the strengthened influence of

two factors even if the prices of industrial products were falling along with the agricultural ones in the

long term.

-------------------

Table II about here

-------------------

The third factor was related to the insufficiency of the social capital in the rural areas compared

with urban areas. In particular, the incomplete facilities of schools delayed the spread and

improvement of agricultural technology for increasing productivity. This was the case especially in

the South(10).

The fourth factor was relatively high interests at which farmers borrowed(11). There was also the

taxation system which imposed unfair taxes on farmers. For example, the securities held by urban

people could be concealed more easily than the cattle held by farmers when assessing the tax values(12).

Moreover farmers had more serious damages than residents in cities when encountering natural and

unexpected accidents since they had few savings(13).

Judging from earlier surveys with regard to discontentment among farmers, it becomes clear that

there was one common characteristic among them. It is the fact that all discontentment factors were

related to the urbanization and to becoming more capitalistic. Farmers in that period felt that they did

not enjoy the benefits accrued from the capitalistic production system which benefited urban residents.

They had also the feeling that they were exploited by banks and railroad corporation main offices

which were located in urban cities and which were centers of capitalistic and commercialized

economy. It seems that these feelings fostered discontent among farmers. Surprisingly enough they

looked enviously even at the labor class which began to develop a labor movement and to throw

discontent into the capitalistic production system. Farmers were dissatisfied with the situation in

which capitalists and labor were respectively organized in cities for seeking their own purposes while

they were organized too insufficiently to show off their existence(14).

The discontent of farmers stimulated and prompted American farmers' movements since the 1870s.

Needless to say, the discontentment factors provided the content of farmers' movements ; concretely:

the spread of agricultural education to improve productivity, the direct purchasing of necessities of

living and farming implements by themselves to avoid their exploitation by urban merchants, the

requirement by local governments of railroad regulations, and the establishment of farmers'

organizations for pursuing their purposes. These discontents gave birth to the Granger Movement. The

living conditions and farmers' movements in the mid-western areas would have provided after all the

method of railroad regulation which was helpful for explaining the emergence and validity in modern

mass-democratic society for accounting information disclosure.

II-3. Analysis of Railroad Regulation in the State of Illinois(15)

Although it was usually said that the Granger Movement was the first large scale farmers'

movement in American history, it was not the first American farmers' movement. From the viewpoint

of farmers' organizations, the earliest farmers' organization was established after the War of

Independence. After that, some organizations appeared and disappeared both at the state level and at

the federal level. In the early years, influential farmers convened to discuss the problem of

improving agricultural technologies for raising productivity. Such endeavors helped established the

Federal Bureau of Agriculture in 1862. Also, all early farmers' organizations were not voluntarily

organized and were not organized from the bottom by individual farmers.

There emerged a voluntary and early organization in the 1830s in which farmers participated and

which intended to defend members' economic interests in watching contemporary economic

conditions. That was the New England Association of Farmers, Mechanics and Other Workingmen.

According to the comment of J.R.Commons,(16)

This association, though at first rather an industrial than a political organization, eventually

advocated a mechanics' lien law, reform in the militia system, simplification of the laws,

extension of the suffrage, reform in the land tenure laws, in the system of taxation, and in

banks and other incorporated monopolies, abolition of imprisonment for debt, protection of

labour instead of capital, factory legislation, especially in the interest of women and children,

a better system of education, in particular, provision for the education of children in factory

districts, and shorter hours of labour.

The high ideals suggested the high consciousness of the members. The main constituent of the

organization was, however, not farmers but labor. Substantially farmers were not active members and

were taken advantage of by labor(17)(18). This organization of which assertion enables us to recognize

the serious critical mind was not a pioneer of farmers organization. Nonetheless it suggests the

extension of the darkness produced by capitalistic production system.

The true pioneers must be small farmers' societies and clubs which were independently dotted

throughout at least twenty states. They extended throughout New York, Vermont, Oregon, Washington,

California and so on from the 1850s to the 1860s. In the meetings of these societies, the regulation of

railroad corporations did not yet come out to the surface for discussion. The main theme was

exclusively concerned with the federal congress or state assembly. After that, the theme gradually

changed to the railroads which developed degressively only in the period of the Civil War but

continued to press farmers to accept unreasonable rates.

When he was aware of the living conditions and wanted to improve them, O.H.Kelley organized in

1867 at the state of Minnesota a farmer organization named the Patron of Husbandry which

consisted of suborganizations, that is, Granges. The membership of the Grange was limited to men

more than eighteen years old and women more than sixteen years old who were engaged in

agriculture. Each group, which was composed of at least nine men and four women, was authorized as

a Grange. According to the saying of Kelley the original purpose for this organization was the social

and cultural progress of farmers' living similar to the one for above-mentioned societies and clubs(19).

It intended to promote the spread and propagation of progressive agricultural technology(20). For

clarifying the earlier characteristic of the Granger Movement, some words of Kelley should be cited

as follows:(21)

Among the objects in view may be mentioned a cordial and social fraternity of the farmers all

over the country. Encourage them to read and think; to plant fruit and flowers, ---- beautify their

homes; evaluate them; make them progressive.

These purposes were petit-bourgeois and consequently suggested only a closed and self-sufficient

orientation among farmers although the objectives largely appealed to farmers all over the states.

But at this earlier time, from the Granger Movement we can not recognize the attention that farmers

paid to general economic conditions and to other social classes and organizations.

The earlier Granger Movement did not pretend to revolutionize the social structure producing the

discontent of farmers. They were discontent only with being differentiated and being ignored by other

social classes after first affirming their basic socio-economic foundations --- or it would be better to

say --- without considering their basic socio-economic foundations. Then the means of improvement

suggested in the earlier Movement was reciprocal, calming the feelings of farmers. Although these

peculiarities were continuously held among farmers, the farmers' movement became more aggressive

after the 1870s(22).

Farmers came to be discontent with the earlier movement so that the policy and principle of the

movement was forced to be revised. Then the Granges turned their attention to the outside social

classes. They started collecting and communicating rapidly the information concerning prices,

volumes of demand and supply, market conditions and transportation of grains in addition to setting

the facilities and extending co-operative purchasing. Thus, farmers began to take advantage of the

information which was produced by the interactions of the outside social classes other than farmers.

In consequence, this also meant that farmers began to take part in or to have something to do with the

outside social classes.

The principle of the movement was developed to result in two watch words which reflected the new

purposes of the movement; " cooperation " and " down with monopolies ". After that, the movement

was developed along the new principle which was authorized in 1871 at a general meeting. How

strongly this new principle captured the hearts of farmers than the old one did can be verified by the

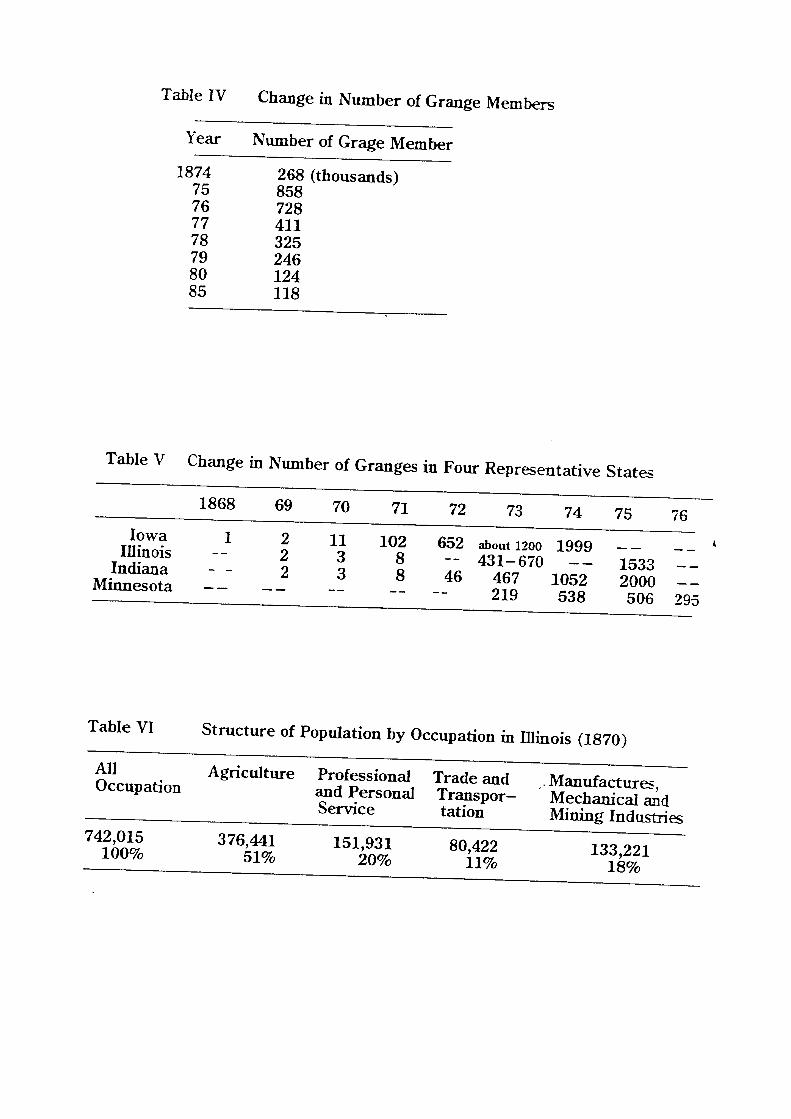

increase in the number of Granges. Table III, IV and V provide the evidence for proof. These tables

tell us that the peak in which the Granges increased in number and accordingly in aggressiveness and

activeness can be recognized in the first half of the 1870s. The movement extended from Minnesota,

Iowa, Illinois and Indiana through Missouri and Ohio to New York, Tennessee, Massachusetts, Kansas,

Kentucky, Vermont, Georgia and South Carolina(23).

--------------------------------------

Table III, IV and V about here

-------------------------------------

Next, we should analyze some concrete effects brought about by the Granger Movement. First of

all, we must look at the Granger legislation in some states. Strictly speaking, the Grange itself was

only a reciprocal organization prohibited to attend to political activities. But we can not deny that it

functioned as a substantial base for farmers' political and legislative activities. In the process of the

movement, farmers pressed their local governments to legislate some laws to protect their own

interests. This was " the Granger Legislation ". Some laws by the Granger Legislation were brought to

court for trial by railroad corporations and states. These were afterwards called " the Granger Cases ."

The state of Illinois was identified with the Granger Cases. But they spread over some states, in

particular, over the states in the Mid-Western areas.

The Constitution of the state of Illinois was amended in 1870(24). It was not only the power of the

Granger Movement but also another power of farmers' association that forced the Illinois state

government to amend the Constitution which newly contained the railroad and warehouse

regulations(25). Since the beginning of the 1860s, laws regulating railroads were many times presented

to the state assembly of the state of Illinois. In these attempts the Act concerning Railroad Rates was

passed through the Assembly in 1869. This Act prohibited rate setting based on the notorious pro rate

principle. But the prohibition was invalid because the Act presented no concrete alternative principle.

On the other hand, it grew the demand for regulating railroads of farmers organized as society and

club. Before long the fourth constitutional convention was held at Springfield in December, 1869.

This convention was adjourned for a while. In this adjournment, the public opinion demanding the

railroad regulation rose in tension. For example, the informal talk of a farmer, H.C.Wheeler was

referred to in an article of the Prairie Farmer, a journal which was popular among farmers of Illinois:

....the farmers of the great North-west concentrate their efforts, power, and means, as the

great transportation companies have done theirs.... And, to this end, I suggest a convention

of those opposed to the present tendency to monopoly and extortionate charges by our

transportation companies, to meet at Bloomington, Illinois, on the 20th day of April

next. ....Farmers, now is the time for action(26).

Such a trend was supported by newspapers and extended to farmers in the north and mid-western

areas.

In the beginning of the conventional session the representatives, however, opposed regulating the

railroad companies, in particular, regulating the transportation rates by the state in spite of the farmers'

aggressive opinions. For example, R.P.Hanna who was a representative said as follows:(27)

Build competing lines, hold out liberal inducements for capitalists to come from every

portion of the country and invest their capital and compete with them. When you have done

this, the problem is solved and the true and only relief furnished.

Judging from the mention of R.P.Hanna, representatives were distressed about unreasonable

rates of transportation but they generally thought that there was no means for regulating railroads

practicable for the state government. At last, farmers' opinion supported by the farmers' movement,

however, pressed a representative of Bloomington, R.Benjamin, who was also a famous researcher of

Constitution, to make a expression that the state government was able to have a right to regulate the

railroad fees. Since railroad corporations had been established for the public good, and had been given

the power of public domain, they were under the control of the legislature. R.Benjamin asserted

that;(28)

there are and can be no vested rights of governmental power in any individual or

corporation, except those conferred by the constitution,

This opinion was agreed to spontaneously by many representatives to add to the new Constitution the

sections ( from Section 9 to Section 15 ) concerning the railroad rate regulations. The following two

sections were cited as a reference ;(29)

Section 12. Railways...are hereby declared public highways, and shall be free to all persons

for the transportation of their persons and property thereon, under such regulations as may

be prescribed by law. And the General Assembly shall, from time to time, pass laws

establishing reasonable maximum rates of charges for the transportation of passengers and

freight on the different railroads in this state.

Section 15. The general Assembly shall pass laws to correct abuses and to prevent unjust

discrimination and extortion in the rates of freight and passenger tariffs on the different

railroads in this state, and enforce such laws by adequAte penalties, to the extent, if

necessary for that purpose, of forfeiture of their property and franchises.

The amendment to the Constitution in 1870 was decided by direct voting of the electorate. The

Constitution as a whole was approved by 134,227 against 35,443. The Sections with regard to railroad

regulation were voted independently and passed by 144,750 against 23,525. The Sections concerning

the warehouse regulation were also passed by 143,532 against 22,702. In this connection Table VI(30)

shows the contemporary population structure by occupation in the state of Illinois. Cook County, in

which was located Chicago, was by far the area of Illinois first in industrial production output and

consequently a leader in modernization. In other words, only Cook County had progressed in

featuring railroad industry while the other counties had a production structure mainly characterized by

agriculture. In 1870 the industrial output of Cook County totaled 92 million dollars, contrasted to the

output of 8 million dollars recorded in the secondly industrialized Peoria County. These polarizations

both in population structure by occupation and production structure surely contributed to the passage

of the new Constitution in Illinois(31).

-------------------------

Table VI about here

-------------------------

In 1871 some laws regulating railroads and warehouses were enacted based on the new

Constitution in the state assembly by members of the assembly who were elected by the Grange

farmers. At this time the Board of Railroad and Warehouse Commissioners was established.

Subsequently we analyze the content and its development of railroad regulations in the state of Illinois

by referring to the earlier annual reports issued by the Board(32).

The law passed in 1871 was the Act Establishing a Reasonable Maximum of Charge for the

Transportation of Passengers. The law obliged railroad corporations to file to the Board the annual

report which disclosed their annual revenues. The Board adopted the policy to recommend a

maximum rate respectively to each railroad which was classified to four (A,B,C and D) ranks

according to the revenue information. The filing system of annual report to the Board was a main

means of railroad regulation in the state of Illinois from the earliest period. From the following

sentence cited from the first annual report of the Board, we can imagine how strongly the Board

expected the success of regulation by the filing system ;(33)

If this Board should succeed in nothing else than in furnishing the public with accurate

and reliable information as to the operation of the large moneyed power embodied in the

railroad interests, so as to indicate reasonable means of protection against its encroachments,

it will have performed a very important and useful function of a considerate government.

On August 1, 1871 railroad corporations filed to the Board their first annual reports which were

incomplete and were forced to be modified, although the Board required only a very simple format of

an annual report. The incompleteness could be explained by some factors. Railroad corporations

adopted different accounting systems each other. They did not record any information concerning

original subscribers of stock, original contributors of capital and amounts of cash contributed because

of their many time transmutations.

When implementing the filing system for railroad regulation, the most important issue was a fact

that there was no accounting information regarding the income earned within the state of Illinois

because railroad corporations usually conducted business with an interstate charter. On the other hand,

this information was indispensable for the Board to decide the rate ranking. The Board was confident

that it could considerably collect the necessary information by continuous suggestion and education to

railroads. According to the filed accounting information, it became clear that railroad corporations in

Illinois almost had charged unreasonably high rates to passengers and had continued adopting

differentiating rates. We must our attention to the fact that the Board disclosed gathered information

and rate ranking of each railroad in newspapers. Based on the information, private individuals who

were discontent over the rates charged could sue the railroads concerned for refunding of rates. Such a

system and the procedures surrounded railroad regulation in Illinois in the earliest period.

As you have already recognized, there was a big issue in the 1871 law. According to the law,

......the action to enforce penalties for its violation is given to the party aggrieved,

exclusively, and this Board does not seem to possess any authority to institute actions to

recover penalties for the violation of that law nor has it any control over actions

instituted by private individuals(34).

Needless to say, the issue was a conceptual limitation of "party aggrieved" to private individuals.

Naturally each private individual had less power than large railroad corporations so that an individual

could not easily sue them for recovering penalties. Thus, the early filing system was in reality invalid

for establishing a maximum fair rate.

Learning a lesson from this failure of regulation, a new and more rigid law for railroad regulation

was passed in 1873. According to the new law, the Board had a right to fix rates and to become a

party aggrieved. Some suit cases were reported in the fourth annual report of the Board issued in

1874(35). That is, the Board came to have a right to directly control railroad businesses. Of course, the

filing system was continuously used in combination with the direct control of business.

After that, railroad regulation in Illinois entered a new stage. The decisions whether laws regulating

railroads and warehouses were constitutional or not in referring to the American Federal

Constitution were brought to court by the railroad corporations and warehouse companies. As we

have already mentioned, a series of such cases were called the Granger Cases. The typical case was

Mann vs. Illinois in 1876(36). The issue of the case was whether the law passed in 1873 was

constitutional or not in referring to the American Federal Constitution. The Supreme Court approved

its constitutionality(37).

It would be very difficult for us to decide whether railroad regulation in the state of Illinois was

successful or not. But we must add that a historian evaluated the strong railroad regulation in Illinois

as a limited success. An another researcher affirmatively evaluated the results of regulation in Illinois.

At any rate, by the 1880s railroad regulation was well under way in the state of Illinois(38).

Turning our attention to the aspect of business conditions of railroad corporations in Illinois, we

analyze particularly the Illinois Central Railroad. Why they did not accept an indirect regulation, a

filing system or information disclosure system ? As a consequence, why did they ultimately go to the

point of accepting direct control of business ?

The Illinois Central Railroad was chartered in 1850 and was expanded by the donation of lands

from the government to become the largest railroad corporation in Illinois. Sometimes this

corporation had the rumor that it could be misapprehended as a real estate company. It was financed

not, by issuing stocks, but by issuing bonds on mortgage of endowed lands. It was told that the

corporation's stock was used to be delivered only as premiums on subscribers of bond. The total

amount of the bond issued was 9 million dollars in contrast to three hundred thousand dollars in the

amount of outstanding stock. In addition, the considerable part of the stock of this railroad was issued

in the English capital market.

Turning our interests to the aspect of management of the Illinois Central Railroad, the proper

development as a corporation of this railroad was disturbed by economic depression, poor harvest and

the Civil War from 1857 to 1870. In addition, the managers of this corporation continued to be

annoyed by foreign intervention -- as we have already mentioned, the stock was almost issued in

England -- so that they could not help adopting more conservative management policies than the ones

adopted if the capital had been contributed by the people living along the railroad line or at least

American people. In consequence, it did not implement the active management strategies adopted by

other competitive railroad corporations so that it often lost passengers and customers. It obtained only

temporary success which in turn, visited it as a loss afterwards(39). Moreover, it could not afford to

accept the requirements presented by the public, in particular, farmers.

We have analyzed the socio-economic conditions at the end of the 1860s and in the first half of the

1870s in which railroad regulation appeared, the changes in means of regulation and the management

conditions of railroad corporations in the state of Illinois. The state had double polarizations both in

population structure by occupation and in industrial production structure and consequently had a

temporary but considerably aggressive farmers' movement requiring anti-railroad and anti-

monopolistic policies. Under such circumstances, the discontent of farmers directly resulted in the

direct control of railroad business in which were fixed railroad rates by the government. In regard to

the indirect regulation method of accounting information disclosure, it was invalid because the

railroad corporations being regulated were forced to adopt unstable and profit oriented management

policies ignoring farmers' demand by foreign intervention and competitive pressure.

The trend of railroad regulations like Illinois expanded over Iowa, Wisconsin, Minnesota and the

states in the Mid-Western areas. Subsequently we should look at the development of direct fixation of

ratea by government in the state of Wisconsin. The assembly of Wisconsin passed the Potter Law

which was evaluated at that time as one of the strongest laws in Granger legislation. The analysis of

the development of railroad regulation in Wisconsin would be helpful as a supplementary analysis to

the state of Illinois.

According to the first annual report of the railroad Commissioners of the State of Wisconsin(40), the

Potter Law was the result of the efforts made by the producing population who were awakened to the

realities of unfair behaviors and of unreasonable rates taken for a long time by railroad corporations in

Wisconsin. This resulted in the Potter Law regulation for rate setting as a reaction to railroad's unfair

behaviors. For example, the legislature had rights to establish reasonable rates by setting maximum

total incomes or maximum earnings and to establish the maximum amount of investment in new

railroad lines. As a result, this law was particularly burdensome for the new railroad lines.

Furthermore, the regulation was not flexibly adapted so there emerged some bad influences. The

annual report of the Commissioners in 1874 had already suggested that investments in new lines were

little by little decreasing in length(41). Such a tendency increased in tension and afterwards railroad

corporations in Wisconsin stopped paying dividends. What was worse, general investment behavior in

Wisconsin became inactive, which led to the depression in the Wisconsin economy. The strong

railroad regulation in Wisconsin reflected in the Potter Law was unsuccessful, in provoking the

economic depression in the whole state. The Eighth Annual Report of the Commission of Wisconsin

issued in 1881 indicated that only five railroad corporations among at least thirty corporations

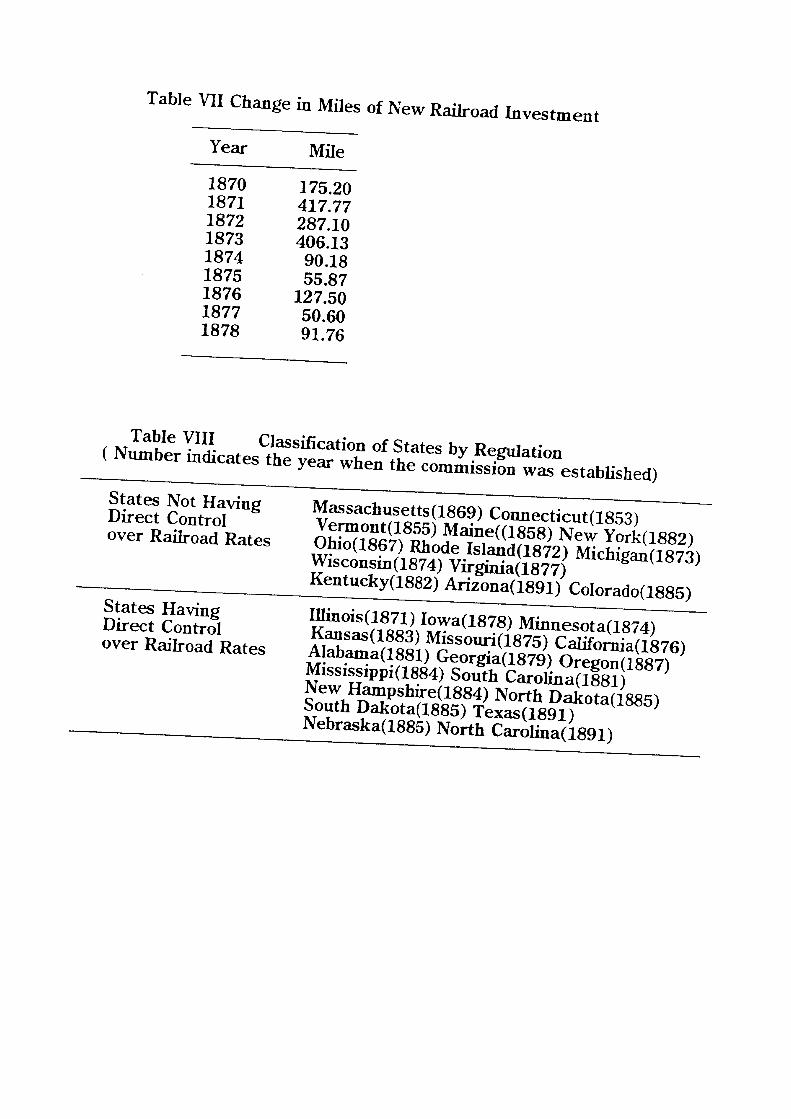

reported their dividends(42). The changes in miles of new railroads in Wisconsin were shown as Table

VII which was cited from the Fifth Annual Report of the Commission of Wisconsin issued in 1878(43).

--------------------------

Table VII about here

-------------------------

In this section, we analyze railroad regulation in the Mid-Western areas, in particular, in the state of

Illinois which was instigated by the Granger Movement. In the development of regulation, the means

of regulation using accounting information disclosure was invalid and the direct control of business

establishing reasonable rates was adopted in some states. Such a type of regulation obtained limited

success in Illinois but failed in many Mid-Western states typically exemplified by the development in

Wisconsin(44). Many states abolished the Granger legislations and some states relaxed their railroad

regulations. The state of Wisconsin changed its means of regulation from the direct control of

business to indirect regulation using accounting information disclosure(45).

On the other hand, the Granger Movement itself became inactive since the latter half of the 1870s

as it had achieved good results of passing Granger legislation in many states in the first half of the

1870s. The discontent and demand of farmers were changing in appearance from the Granger

Movement, the Greenback Movement to the Populist Movement(46). Finally we should add that the

Granger itself continued to function as a reciprocal organization for farmers.

III Railroad Regulation in the State of Massachusetts

III-1. Introduction There seems to be two types of railroad regulation in the Unites States occurring in the latter half of

the nineteenth century. Regulatory subject was uniquely the state which established railroad

commission or board of railroad commissioners. The data concerning the year when railroad

commissions were established in each state were offered in Table VIII(47). Although there were time

differences among states, each had a commission for regulating railroads.

We can classify two types of means employed by states in railroad regulation. The one was, as we

have already seen, direct control of business through establishing fixed rates. And the other was

indirectly by requiring only accounting information disclosure. The ratio of direct regulation to

indirect regulation could be informed from Table IX(48). We selected the state of Illinois as a typical

example of the former and the state of Massachusetts as typical of the latter. In the previous studies,

however, these two types of railroad regulation were not equally evaluated. Many historians attached

more importance to the direct control of business than to information disclosure. Previously it was

understood that the regulation of large corporations first required by farmers was conducted by the

state using the direct control of business which was succeeded by the Interstate Commerce

Commission and step by step strengthened by the Sherman Antitrust Act and the Hepburn Antitrust

Act. It means that the direct control of business continues to be dominant in the area of corporate

regulation in general. In reflecting such a general understanding, for example, R.V.Fletcher did not

evaluate the indirect regulation(49). H.U.Faulkner also said that (50);

(commissions of experts) were of two kinds: the strong commission, as in Illinois, with

power to regulate rates and enforce the law; and the weaker commission, as in

Massachusetts, with powers merely advisory and the duty to make reports to the

legislature.

These two researchers have a common characteristic of treating the function of information disclosure

lightly although Faulkner used such wording as " it may be said that the latter type in the long run

often proved to be the most successful"(50). But we want to re-evaluate properly the regulating function

of information disclosure in a mass democratic society to evaluate the accounting information

disclosure from the new socio-economic viewpoint. Then we can recognize the utilization of

accounting information disclosure by regulatory agencies of local and federal governments in the

development of regulating large organizations from the latter half of the nineteenth century to the

beginning of the twentieth century in addition to employing direct control of business. The ultimate

purpose of this chapter is to clarify the socio-economic foundations of modern accounting information

disclosure by studying the concrete reasons why two different types of regulation appeared in

different states having different social structures and different industrial structures. In this section

we try to analyze the socio-economic conditions and the development of railroad regulation in the

state of Massachusetts in contrast to the ones in the state of Illinois. Before this analysis the survey on

the development of the railroad and its surrounding interests in Massachusetts will be offered in the

next subsection (III-2.).

III-2. Conditions of the State of Massachusetts(51)

First of all, we must evaluate the significance of railroad construction in the state of Massachusetts

of the nineteenth century in the light of the development of railroads in the United States. Generally,

the early period of constructing railroads in the United States was divided into four stages. In the first

stage, short line railroads were constructed as supplementary transportation to river transportation

mainly in the East Coast states. This stage would correspond to the period extending from 1827 in

which was chartered the Baltimore and Ohio Railroad to the 1830s. Since then, railroad construction

began in Massachusetts. The second stage corresponded to the period extending from the 1840s to the

1850s, in which railroad industry was established as the center of economy and in which it was

completed the construction of four trunk line railroads. A large amount of capital also began to flow

from England in this period(52). The third stage included the period in which large railroad

corporations wove the mesh of railroad transportation all over the states. This period falls from the

1860s to the first half of the 1870s. The fourth stage comes under the period beginning from the latter

half of the 1870s when investment bankers entered into railroad industry by reorganizing stagnant

railroad corporations. It was a sign of monopolization which would blow up in and affect all

industries at the turn of the century.

The first stage was the stage in which railroads were employed as supplementary to steam boats

and were unanimously built and financed by the merchants and the bankers of large cities in the east

coast or by the aid of local governments in an attempt to join their own cities and trunk canals. The

ultimate end was to join them to the Mid-Western granaries. The Mohauk and Hudson Railroad and

some railroads in Massachusetts were constructed under such intention. How some large cities in the

east coast were eager to obtain the leading and central position in the mesh of railroad transportation

would be exemplified by the competition between the Mohauk and Hudson Railroad and the one in

Troy(53).

The second stage was the one of completion of trunk lines which extended from the east coast

through the Appalachians to Lake Erie, that is, to the Mid-West. The New York Central Railroad had

the first trunk line. It was established in 1853 by merger but its antecedents were jointly connected to

each other to become a trunk line. In the 1850s, the Pennsylvania Railroad, the Erie Railroad and the

Baltimore and Ohio Railroad in succession completed trunk lines. In this period, capital came from

England to be invested in the expansion of trunk lines. For example, the Pennsylvania Railroad

promptly decided to introducecapital from England for expanding its lines(54).

The 1860s was the third stage. Railroad construction was stimulated by the famous executives with

which the railroad corporations were identified after years. For example, C.Vanderbilt of the New

York Central and J.Gould of the Erie have even now stable positions in American business history.

They accumulated their properties commonly by manipulating the stock of their corporations

and they deserved being criticized by the public. The managements and promoters in this period,

however, had such common characteristics. In fact this period is even now called the " Gilded Age."

Thus farmers became discontent at watching exactly the behavior of these managements.

The management style and the competition of constructing railroads in the third stage had relatively

shorter lives. In the fourth stage, investment bankers including J.P.Morgan showed off their financial

power by reorganizing railroad corporations that had gone bankrupt in the 1870s' depression. After

that, they began to play an important role in the merger movement at the turn of the century on the

base of financial powers accumulated in the process of railroad reorganizations.

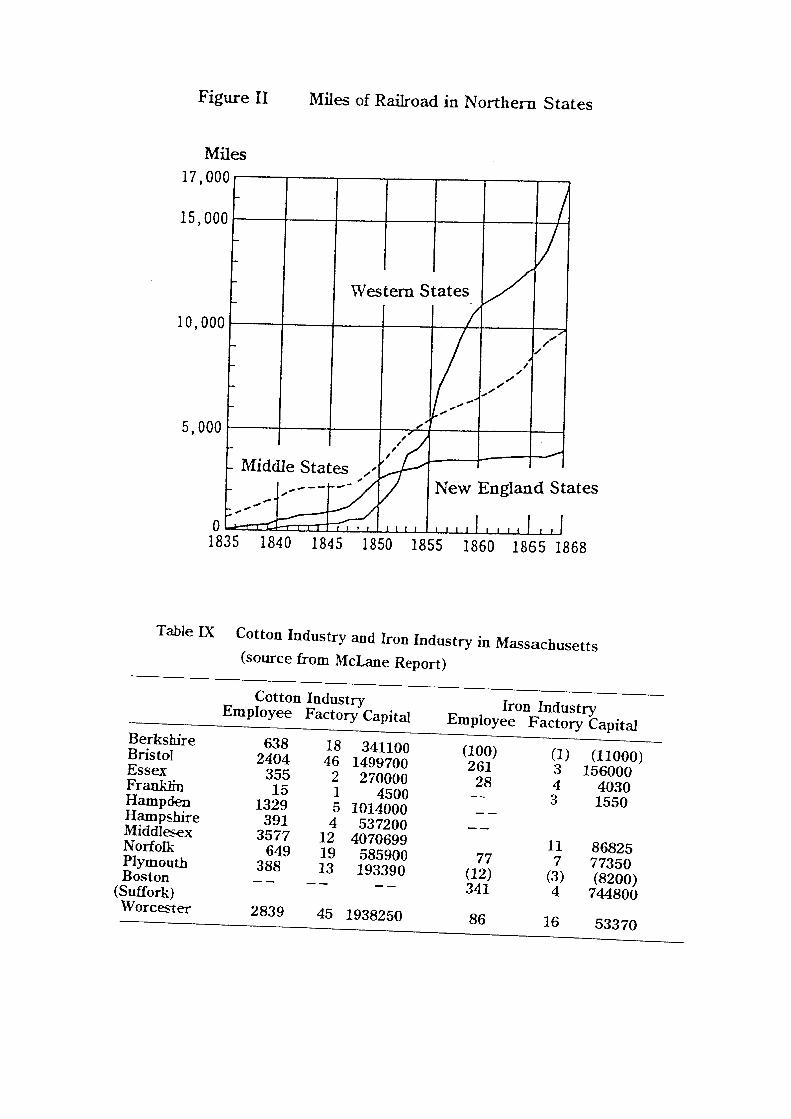

The first three stages of railroad development is the subject of my analysis concerning railroad

development in Massachusetts. At this point it seems proper to offer the data with regard to railroad

miles constructed in the northern areas of the United States (see Figure II(55)).

-------------------------

Figure II about here

-------------------------

Judging from Figure II, the miles of railroad in the New England states remained on a stable level at

least since the 1860s. It means the cease of intensive railroad construction in the New England. The

New England states include Main, New Hampshire, Vermont, Massachusetts, Rhode Island and

Connecticut

Now we turn our attention to the trend of interest groups surrounding railroad industry in

Massachusetts(56). They had a leading position among the East Thirteen states after Independence.

Although since the first issue of the Census statistics in 1790 the total population of the United States

increased in percent to 150% by 1820, the one in the Massachusetts increased only 30%. It seems that

the states to the west of the East Thirteen states including Kentucky, Tennessee, Ohio, Louisiana,

Indiana, Missouri, Illinois, Alabama and so on, made progress rapidly while Massachusetts remained

stable in progress.

Boston which is the most populous city in Massachusetts prospered as a center of domestic and

international trade. It gathered products from New England, India, China, and the East and the West

islands of India, and shipped them not only to American domestic markets but also to remote

European markets. This was the case for some another cities in Massachusetts so that they could

accumulated considerable capital to contribute to the subsequent industrial revolution and

economic development in this area.

This prosperity from international trade enjoyed by some cities in Massachusetts was attributed to

their geographic superiority. Entering into the nineteenth century, New York became a menace to

Boston because the former, facing the Hudson River, was superior to the latter in geographic position

for connecting domestic trade to international trade. Additionally the state of New York completed the

Erie Canal in 1825 under the direction of D.W.Clinton. By this canal New York held an unshakable

position in connecting the Pacific Ocean and Lake Erie, that is, between international trade and

domestic trade. In considering the economic affairs surrounding Massachusetts, we can easily imagine

that social and local economic-interest groups commonly recognized the importance of improving

inner-state transportation and of expanding it to the West(57).

Turning to the economic and industrial conditions within Massachusetts, merchants were

gradually missing their opportunities of investments in competing with the ones in New York. The

accrued extra capital, however, fostered the cotton industry in this area. For example, the Boston

M.Company established in 1813 in the East of Massachusetts succeeded in the cotton industry and

recorded a seventeen percent dividend in 1817. Thus Boston was enlivened again by the development

of the cotton industry.

Agriculture in Massachusetts at this time was also prosperous in Worcester and the Worcester

Agricultural Society was organized in 1825. This area became active in the cotton industry, beginning

in the 1830s.

The coexistence of the cotton industry, of the agriculture and of the demand for farming

implements brought birth to the steel industry in Massachusetts. As a reference we should cite from

the McLane Report the data concerning the cotton and the steel industries in Massachusetts in this

period(58) .

-----------------------

Table X about here

-----------------------

Massachusetts was at last re-established as one of the biggest industrial districts in the United States

when it changed its economic structure from the international commercial trade to the production

industry. Consequently, Massachusetts was characterized as one of the foremost states in regard to the

American Industrial Revolution and continues to be analyzed until now by many researchers. As a

researcher gave importance to the cotton industry(59), so another researcher paid attention to the steel

industry(60). But the existence of agriculture should never be neglected. With their economic power the

merchants and bankers in Boston still had a large influence. It should be taken into consideration the

distribution of industry by the region shown in Table X. We should confirm here one important

characteristic concerning the economic structure of Massachusetts. Massachusetts had first an

experience of modern industrialization in the United States and had also first an experience of having

the socio-economic structure typically recognized in the highly developed capitalistic economic

society. There emerged many organized interest groups which included not only the traditional

farmers and merchants but also the professional people who accrued from the capitalistic production

system. The regional conflict had already been recognized since the 1830s. Then we must conclude

that the state of Massachusetts had already produced the prototype of the modernized socio-economic

structure which would become dominant by the industrial monopolization movement in the United

States as a whole at the turn of the century and in which the managements of relatively large

corporations actively adopted management policies in considering into accounts and reacting to the

demands and requirements proposed by many different organized interest groups.

III-3. Analysis of Railroad Regulation in the State of Massachusetts

The analysis concerning the development of railroad regulation in the state of Massachusetts will

be offered in this subsection. Since the 1820s, the railroad construction from Boston to Albany in the

state of New York was earnestly studied in Massachusetts. The main issue of railroad construction

was a financial problem. That is, which should contribute the funds, the state government or the

private sector ? If the state government would finance the railroad construction, it meant that the state

people as taxpayers substantially had to pay the costs which were involved in the construction. Thus,

the necessity of the railroad was discussed in terms of the interests surrounding the railroad. We must

pay attention to the fact that the discussion was conducted in the form of town meetings which were,

of course, the democratic tradition of Massachusetts(61). As a result, the Boston and Worcester

Railroad was chartered for constructing a railroad from Boston to Worcester located in the middle of

the way to Albany(62). But many local governments in the state of Massachusetts did not financially

support the railroad construction including the Boston and Worcester Railroad(63), even though

state governments in the United States generally and substantially financed the large social

infrastructures in this period. This fact meant that the general public in Massachusetts had not yet

evaluated the usefulness of railroads(64). Although refusing to finance railroad construction, the state

government had a right to charter it because the establishment of the corporation was based on the

charter system(65). Then the real issue was what kind of power the state should give in the charter to

corporations which would undertake railroad construction. The wording of the charter saved face for

the regulators and anti-monopolists who feared the monopolization of railroads , but the substance

gave to the private investors, that is, stockholders, nearly everything they desired(66). S.Salsbury

said that;

The legislature, however, insisted that the railroad should keep no secrets. To this end the

directors were to report annually to the General Court the company's receipts, expenditures,

and operations. As if this were not enough, the charter added that the corporation's books "

shall at all times be open to the inspection of any Communities of the Legislature." Stiff

penalties would result from failure to so comply(67).

In Massachusetts at this time, it had already become an important issue to adjust the differences of

interests concerning railroad among several varied interest groups which consisted of banking, real

estate holding, wholesale, retail, merchandising, investing, manufacturing and so on(68). We can cite

the following sentences from S.Salsbury again;

(The history of railroads in this period in Massachusetts was) ...the history of how these

powerful groups exerted pressures to force the railway managements to serve particular

interests(69),

and also was the history of adjusting conflicting interests. But after all the Boston and Worcester

Railroad was welcomed at its opening in April of 1834 because the success of the Baltimore and Ohio

Railroad had already been confirmed(70).

We focus on the conflicting interests and its adjustment process of railroads in Massachusetts in the

rest of this subsection.

The managements of the Boston and Worcester Railroad were oriented to local interests so that the

board of directors intensively discussed the rate setting policy. In the 1830s, directors D.Denny and

D.Henshow, insisted that low rates were beneficial both for the public and for the railroad itself in the

long run(71). On the other hand, N.Hale supported by the interests of banks, favored raising the rates.

This conflict ended in a temporary policy of raising rates. But the rates were cut down when the

earnings of the railroad increased in 1839(72). These facts tell us that the management of the railroad

was conducted in consideration of the interest groups involved.

By the way, the Western Railroad was also chartered for extending its railroad to Albany in March

of 1833 after the charter of the Boston and Worcester Railroad. Now we must look at financing of this

new railroad. The board of directors of the railroad needed very badly the financial support from the

state government. Then directors G.Bliss,Jr and J.Willard asserted the establishment of the State Bank

of Massachusetts by the charter which assured the purchase of the stock of the Western Railroad by

the bank. But this assertion was opposed by democrats. Thereafter, the railroad began to obtain the

support of the public and it succeeded to earn the support of two counties, Franklin and Hampshire

because it had succeeded in obtaining the agreement of the journals, Courier and Mercury. After that,

the plan of establishing the state bank itself was revoked by democrats but still the railroad was

successful in obtaining financial support from the state in the sense that the state came to purchase one

third of the stock issued by the Western Railroad(73). On account of this fact, the railroad included the

state as stockholders in its interest groups.

There appeared a conflict among real estate holders because the prices of the real estate fluctuated

depending upon the location of railroad stations. The town of Worcester held mass meetings for

opposing and protesting the one sided decision of stations' location by the Western Railroad and for

communicating the public's demands to the railroad(74). On the other hand, the Western Railroad issued

the bulletin " Address to the People " for appeasing the public(75). This could be considered as a kind

of disclosure policy taken voluntarily by the corporation.

Next we discuss another conflict concerning the rate setting policy among directors of the Western

railroad in the 1840s. When he asserted that the railroad could be managed on the same low rate basis

as the steam boats, E.H.Derby wanted to hold actual control power over the corporation by winning

the support of the public. W.Jackson naturally opposed the opinion of Derby because of its

impossibility. The interesting point was the means by which Derby gradually obtained the support of

the public. He explained to the public that the railroad could conduct business on the same rate basis

as the Erie Canal through some articles in journals and some addresses by using statistical simulations.

The statistical data contained the net income calculated from the total revenue and expenditures of

labor cost, maintenance cost and so on accrued on the condition that the transportation facilities of the

Western Railroad were fully and completely operated(76). This discussion ended up to the compromise

that the low rate was adopted concerning the passenger and the high rate was supported in the case of

freight(77). The discussion regarding rate setting exactly indicates the monopolization of railroad

industry in Massachusetts according to a railroad fee theory(78).

The fact that the information disclosure regarding railroad corporations became worthy of notice,

in other words, the fact that the public always watched the behaviors of railroads, pressed the state

assembly to pass the law regulating the accounting procedures of railroad corporations in 1846 before

the establishment of the Board of Railroad Commissioners. It seems that this law gave influence to the

subsequent accounting information disclosure of railroad corporations in Massachusetts(79).

We tried to describe the circumstances surrounding railroads and the behavior of management in

the first half of the nineteenth century in Massachusetts by referring to the cases of the Boston and

Worcester Railroad and the Western Railroad as historical instances. This analysis should clarify that

it was necessary for the railroad corporations in Massachusetts to conduct management behavior in

consideration of several opposing interest groups -- the public as a whole -- into account. For example,

information disclosures were employed to appease and to persuade the public. This meant that the

railroads began to have monopolistic powers and to allow a margin for adopting modernized

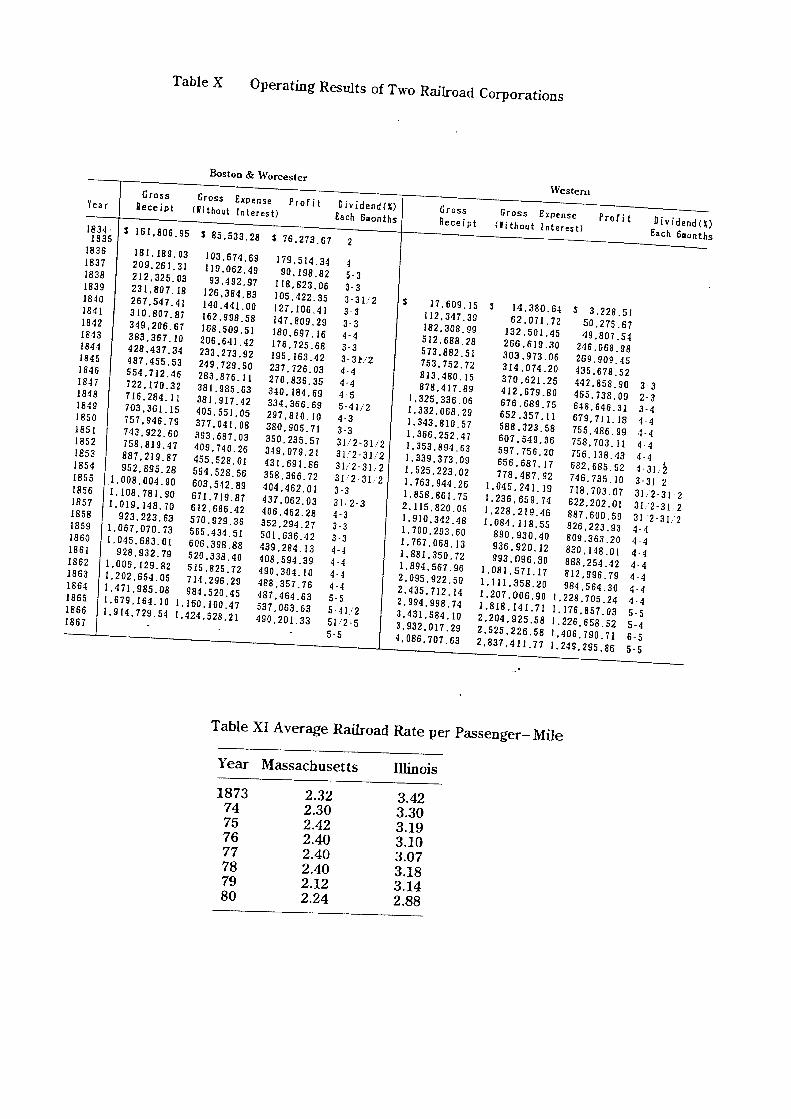

democratic management policy. We can supplement this assertion by showing the stable and

increasing propensity of dividends for the two railroad corporations ( see Table XI(80)). The public of

Massachusetts criticized and watched railroads only after they affirmed the existence of the railroads.

The conservative opposition to railroads in a sense on the side of the public was exactly reflected in

the gradual increase in the number of passengers. Table XI can also offer data with regard to two

railroads' passengers. Thus the situation in Massachusetts contrasts remarkably with the one in

Illinois.

------------------------

Table XI about here

------------------------

In following the way of monopolization, railroads gradually extended(81). The Boston and Worcester

Railroad and the Western Railroad merged into the Boston and Albany Railroad. This merger was

accelerated by competition from the New York Central Railroad(82). And in 1869 the Board of

Railroad Commissioners was established in bringing with only the information disclosure

requirement(83). Then we should analyze, first of all, the content of the requirement by referring to the

First Annual Report issued by the Board(84).

The most important function to be conducted by the Board was to inspect both the management

ways and conditions and the obedience to their own charters and to the laws in Massachusetts of

railroad corporations by referring to the annual reports filed by railroads for the purpose of evaluating

railroads within the state in terms of the public's safety and convenience. So the Board had a right to

visit for inspection any railroad within the state when necessary. The duties and rights of the Board

were provided by Section 3 in Chapter 408 of the law passed in 1869. According to the law,(85)

Commissioners shall inform such railroad corporation of the improvements and charges

which they adjudge to be proper and a report of the proceedings shall be included in the

annual report of the commissioners to the legislature.

In other words, the Board was invested only with the duty and right to counsel improvements and

to report them to the legislature when railroads violated their charters or laws. The legislature

disclosed the facts. Naturally the Board itself was at the beginning bewildered by its limited powers.

For example, when the Board was consulted in the case of the Boston and Lowell Railroad's refusal to

offer transportation service to a certain customer, it could not bring the railroad to court by itself

because of its limited rights. With regard to this case, the Board expressed its regret in the First

Annual Report(86).

Then we would like to know whether the way of regulation adopted by the Board in Massachusetts

was successful or not. It is generally understood that the Board was established only to assure the

publicity of the railroads because of holding no power to directly control railroads. So the Board was

treated lightly and was itself annoyed. As we have already pointed out, some historians did not

evaluate the Board and its regulating power. The descriptions drawn by A.T.Hadley and F.C.Clark(87)

is, however, useful for answering this question from another viewpoint. They insisted on its

successfulness. As far as we agree with the opinion of Hadley, we must indicate originally some data

supporting its successfulness. Concretely, the passenger rates both in Illinois and Massachusetts are

offered as Table XII(88). According to Table XII, the decrease in price for passenger rates was

observable in both states.

-------------------------

Table XII about here

-------------------------

If we can say that the railroad regulation system, that is, regulation by (accounting) information

disclosure in Massachusetts was at least partly successful, we must next sum up the reasons. As a

matter of fact, the reasons are expected to suggest also the socio-economic foundations for modern

accounting information disclosure typically observable in a modern capitalistic economy.

The first reason is that the railroad corporations in Massachusetts were sensitive to public opinion.

The persons holding property rights, including the stock reflecting equity and managers managing

them, had to regard for others to protect their property rights because the concept of property right

itself was relatively new one and consequently was not defended by long term conventions. In

particular, the large monopolistic railroad corporations were apt to be criticized and to be watched by

the public because they earned considerable profits and in turn they actively adopted a management

policy for keeping the public in good humor. On the other hand, it can be understood that the Board in

Massachusetts expertly read the tendency of the railroads. The Board, for example, educated public

opinion so that the public voluntarily demanded improvements to railroads. By depending on this

policy the Board could force the railroads to install safety devices and to run the trains beneficially for

local industries in addition to setting reasonable rates which were intended. These functions seem to

be inherent in information disclosure systems. The publicity had substantial power over requiring

respect and obedience from the railroads(89).

The second reason is that the interests both of railroads and the public in the long run came to an

agreement. If the management of large railroad corporations had intended only to make their

dividends as large as possible, it would have been possible by oppressing the local transportation

companies. But if they had done so, they would have lost connection with local transportation services

and would have had to invest huge funds into local services. Needless to say, such a policy was very

dangerous for the railroads themselves. Then for railroads there was a necessity to keep harmony with

the local transportation companies. By forcing the railroads to disclose their management and

accounting information, the Board could prevent the oppression of the public's interests caused by

possible the railroads' short-profit maximizing behavior. On the one hand, the function of information

disclosure allowing the public to watch the management behavior of large corporations and on the

other hand, the existence of monopolization of the railroad industry, both were prerequisites to the

prevention of immoderate management of railroad corporations. Although the Board of Massachusetts

also employed this function of information disclosure, it did not appear to be sufficiently evaluated for

its results(90).

The third reason is that the railroad industry in Massachusetts had a relatively long history and

consequently had entered into stable business conditions. We have repeatedly mentioned, there existed

no active competition and no aggressive management behavior(91). As free competition was valid for

expanding rapidly the railroad mesh at the sacrifice of the public's interests, so the monopolization of

railroad industry was a prerequisite to a high quality transportation system and management system to

railroads. Generally the monopolization or oligopolization seems to be an economic prerequisite to

the social structure in which the public can inspect the management behavior of big businesses by

using management and accounting information disclosure and can also demand their improvements

and big businesses can, in turn, take moderate management policies in reacting to public opinion. Of

course, such a social structure was for the first time realized in smaller size in the state of

Massachusetts, than in the United States as a whole at the turn of the century. We can not also ignore

the coexistence of several organized interest groups, that is, the organized public as a whole.

The fourth reason is that there was an ideal and an institutional tradition with regard to democracy

which was typically reflected in the town (or mass) meeting in Boston. The tradition gave active

influence to the public's function of watching big corporations.

The state of Massachusetts succeeded in railroad regulation by using only information disclosure in

the above mentioned four reasons, which brought about two derivative effects. The one was that there

was no support among the members of the Board for nationalization of railroad. The other was that

some states gradually adopted railroad regulation by information disclosure accompanying

improvements of some accounting techniques and rules, especially after the Granger Movement was

finished about 1878(92). Such states naturally experienced the changes in their socio-economic

structure into a modernized one like Massachusetts. The real case of Wisconsin has been already

offered in the previous section. Before long, the Interstate Commerce Commission would adopt the

accounting information disclosure as a measure of big business regulation at the Federal Government

level.

IV Conclusion

In this chapter, we have analyzed the development of railroad regulations both in the mid-western

states and in the East Coast states for finding the socio-economic foundations of the modern

accounting information disclosure typically conducted by modern big business. Thus we would like to

sum up some analytical results as conclusions, although we should recognize that the limited number

of sample states may result in a limited conclusion. The period treated in Section III was older than

the one in Section II. The peculiarity of the state of Massachusetts determined that the modernized

socio-economic structure in which the several organized interest groups watched the railroads, caused

the railroads, in turn, to adopt moderate management policy for appeasing them. At the beginning, the

people in Massachusetts doubted the necessity of a railroad but after that they began to criticize the

railroad after accepting its existence. The democratic tradition continued to remain in Massachusetts

and such a socio-economic structure enabled the Board of the Railroad Commissioners established in

1869 to succeed in regulating railroads by utilizing only accounting information disclosure. At this

point we must attend to the fact that resolution of the economic problem by accounting information

disclosure could never become the essential resolution to the economic problems in this period

accrued from the capitalistic production system which was gradually penetrating into the United

States as a whole. The resolution of economic problems by accounting information disclosure is only

a temporary resolution on the condition that the capitalistic production system was extending, that is,

monopolization was expanding.

The polarization of the economic interest groups resulted in the strong and direct control of

business of railroad corporations by the state legislatures in mid-western states. In such circumstances

there emerged the polarized conflict between farmers and railroads so that farmers required strong

regulations over railroads. It seems, however, that farmers were essentially conservative in nature.

The strong regulations became invalid after they prevented sound economic development in some

certain states. In Mid-Western states, several interest groups were gradually organized within a state

and after that these organizations extended beyond the boundary of states to become nationa wide.

This was the case even for farmers. All the interest groups, including farmers were incorporated into

the reproduction system of big business enterprises.

We dare to say that the socio-economic structure established in Massachusetts in the middle of the

nineteenth century was in similitude formed at the turn of the century in the United States as a whole

as a result of appearance of modern big business system or modern industrial monopolization. In

regard to the accounting information disclosure, new big businesses, for example U.S.Steel, other than

railroad corporations also began to adopt it to reconcile the anti-monopolistic movement developed

actively at the turn of the century. We can also find in the Progressive Movement the real case of

emerging democratic ideology like a town meeting tradition in Massachusetts. The analysis of these

phenomena will be conducted in the next chapter.

Notes(1) The effects that were brought about by the development of railroad industry in the United States were

differently evaluated among economic historians including W.W.Rostow and R.W.Fogel.

(2) Syoujirou Ishii, Amerika Tetsudou Ron, Cyuoukeizai-sya, 1974, p.67.

(3) The references of this subsection are as follows; A.Fishlow, American Railroad and the Transportation of the