Embed Size (px)

Citation preview

Asian Journal

of Research in

Banking

and

Finance Asian Journal of Research in Banking and Finance Vol. 6, No. 2, February 2016, pp. 1-16.

ISSN 2249-7323 A Journal Indexed in Indian Citation Index

1

www.aijsh.org

Asian Research Consortium

Impact of Gold and Crude Oil on Stock Market Volatility

in India

Dr. Balwinder Singh*; Ms. Kriti Chitkara**

*Professor,

Department of Commerce,

Guru Nanak Dev University,

Amritsar, India.

**Junior Research Fellow,

Department of Commerce,

Guru Nanak Dev University,

Amritsar, India.

DOI NUMBER: 10.5958/2249-7323.2016.00001.8

Abstract

India is the fourth largest importer of Crude oil and the largest importer of Gold in the world.

Trading in Crude Oil, Gold, Crude Futures and Gold Futures on Organized exchanges began in

2005 in India. Since, India is a price-taker, the escalating price of these commodities and their

Futures flares up uncertainty in the economy, as reflected in the Volatility in the Stock Market. The

purpose of the study is to highlight the effect of returns of Crude Oil, Gold, Crude Futures and Gold

Futures on the Volatility in the Indian Stock Market. The study reveals that Crude Oil, Gold and

Crude Futures have a significant impact on the stock Market Volatility in India. The study is useful

for the policy makers and the government to take measures to reduce reliance on imported goods

and harness alternative sources for sustainable economic growth.

Keywords: Crude Futures, Crude Oil, GARCH, Gold, Gold Futures, Stock Market, Volatility.

________________________________________________________________________________

1. Introduction

Stock Markets are the barometer of economic health of an economy. During the last decade, the

Stock Markets and economies have witnessed massive upheavals and tremors. The unpredictable

fluctuations or volatility in the stock market are followed by reduced growth rates in the economy,

Singh & Chitkara (2016). Asian Journal of Research in Banking and Finance,

Vol. 6, No.2, pp. 1-16.

2

as highlighted by Bhowmik (2013). Engle and Patton (2001) are of the view that financial asset

prices do not evolve independently of the market around them. So it is likely that other variables

may contain vital information for the Volatility of a series. Once we know which variables affect

the volatility in the Stock Market, we can formulate strategies or policies to control these variables.

Crude Oil and Gold are the commodities of strategic importance. Crude Oil constitutes above 30%

of the total value of imports in India every year. Gold too has a share of above 10% in total value of

imports in India*. The last decade has witnessed a spike in commodity prices, led by the flare up in

Crude Oil prices. Gold Prices too have shown unprecedented upward movements during the last

decade. And the demand for Crude Oil and Gold in India is rising every year, which is a matter of

concern to the policy makers. With the starting of organised trading in commodities in India, there

has been a spur in the trading of commodities and commodities futures on commodity exchanges.

Having started operations in November 2003, today, MCX holds a market share of over 80% of the

Indian commodity futures market†.

Crude Oil is an input to production and a major energy resource. India imports most of its

requirement of Crude Oil. The value of Crude Oil traded at Multi Commodity Exchange. India was

Rs 13770885.61 lakhs in 2005. The figure stood at Rs. 150743390.24 lakhs in 2010‡. The spot price

of crude oil being traded at MCX stood at Rs. 2967 on March 31, 2006 which rose to Rs. 3768 on

March 31, 2010. As on January 31, 2011, black gold, i.e. crude oil stood at Rs. 4086§. Due to its

escalating prices, Crude Oil has become popular as „Black Gold‟.

The shiny yellow precious metal `gold' has fascinated the common man, the researchers, the

investors, women and kings and so on from time immemorial. It has been described as a

`multifaceted metal' possessing characteristics similar to money, a currency without borders and an

inflation hedge (Tully and Lucey, 2005), a commodity as well as a financial asset (Callaghan, 1991)

and a global store of value (Faugere et al., 2005). It has also been addressed as a safe haven in times

of economic crisis (Baur and Lucey, 2010). India, crowned as the Golden Sparrow, is the world's

largest consumer of gold, purchasing around 700-750 tons of gold every year. Gold hoarding

tendency is well ingrained in the Indian society and unofficial stocks held by Indians is estimated to

be well above 15,000 tonnes, which is around 9% of the total global gold stocks**

. India imported

gold valuing Rs.2237.6 crores in 1994-95, when the total imports stood at Rs. 89970.7 crores. The

value of gold imports in India has risen to Rs. 95323.8 crores in 2008-09 when the total imports are

Rs 1374435.6 crores††

. Since India is a price taker when it comes to Crude Oil and Gold, the

soaring prices of these scarce resources have always been under scrutiny of the

economists.Following is an overview of the economic relationship between Crude Oil and Stock

Market.

* http://siteresources.worldbank.org/INTOGMC/Resources/10-govt_response-hyperlinked.pdf

† http://www.mcxindia.com/aboutus/aboutus.htm

‡ http://www.mcxindia.com/Sitepages/HistoricalDataForVolume.aspx

§ http://www.mcxindia.com/sitepages/SpotMarketHistory.aspx?sLinkPage=Y

** http://www.mcxindia.com/SitePages/ContractSpecification.aspx?ProductCode=GOLD

††http://www.rbi.org.in/scripts/AnnuaIPublications.aspx?head=Handbook%20of%2OStatistics

%20on%20Indian%20Economy

Singh & Chitkara (2016). Asian Journal of Research in Banking and Finance,

Vol. 6, No.2, pp. 1-16.

3

1.1Oil Prices and Stock Market

Oil prices play a unique and pivotal role in the economy as one of the most important input in

production. Therefore the existence of a correlation between Oil Prices and the Stock Market

cannot be ruled out (Morales and Andresso, 2014). It has been stated that Oil prices must always be

considered as one of the factors influencing the stock market returns (Chen, Roll and Ross, 1986).

This is because of the reason that Stock Markets react to oil price shocks (Nandha and Faff, 2007).

Also, the recent upsurge in prices of fossil fuels has led to a downturn in the global share markets

(Shafie and Topal, 2009). The transmission of effect of Oil price hike on Stock Market can be

studied by dividing the entire globe into:

(a) Net Oil Importing countries

(b) Net Oil Exporting countries.

The economies of Net Oil Importing countries are highly dependent upon Crude Oil since it is the

most important source of energy.

The major importers include Canada, European countries, China, Japan and India. The impact of oil

price hike can enter into the stock market through channels at macroeconomic level as well as

microeconomic level (Odusami, 2009). Pandey (2005) explains the phenomenon as follows:

1. Transmission at Macroeconomic Level

The phenomena of transmission of impact of Oil price hike on Stock Market at the macroeconomic

level can be seen in the following ways:

A rise in the Oil prices leads to a high cost of production in the Net Oil Importing

Countries which causes a decline in the real output. This results in a fall in expected

earnings, which negatively impacts the Stock Market returns.

Increase in Oil prices is followed by a transfer of wealth from Net Oil Importing

Countries to Net Oil Exporting countries, thus forcing a postponement of investment by

the industry in Net Oil Importing Countries. The process is followed by falling Stock

Market returns.

Oil price hike causes inflation and to combat it the policy makers raise the discount rate to

curb money supply. This culminates into the ebbing of Stock Market returns.

2. Transmission at Microeconomic Level

(a) Net Oil Importing Countries (NIC)

At microeconomic level, when Oil prices creep upwards, the economy of Net Oil Importing

Countries is at interface with inflation. The households postpone consumption and go for

Singh & Chitkara (2016). Asian Journal of Research in Banking and Finance,

Vol. 6, No.2, pp. 1-16.

4

precautionary savings followed by a low market sentiment. Hence Net Oil Importing Countries

have to face a situation of decreasing Stock Market returns.

(b) Net Oil Exporting Countries

These countries include the gulf countries, the OPEC countries and other countries such as

Malaysia which are the major exporters of Oil. These countries govern the supply and price levels

of Crude Oil. A rise in Oil prices leads to increased Stock Market returns in the Net Oil Exporting

country. At the same time it spells an inflationary pressure in Net Oil Importing Countries. This

leads to fall in money supply, low purchasing power, falling industry returns, followed by

decreasing Stock Market returns in the Net Oil Importing Countries. The phenomenon causes a fall

in demand for Crude Oil in Net Oil Importing Countries resulting in shallow exports by Net Oil

Exporting countries. Ultimately, Crude Oil led Stock Market falls in the Net Oil Exporting

countries.

Theoretical relationship between Gold and Stock Market is given below.

1.2. Gold and the Stock Market

The relationship between Gold and the Stock Markets as investment avenues has been a matter of

interest, with the coming up of organized commodity exchanges all over the world. Traditionally,

Gold has been viewed as the best hedge against inflation. It is due to the attractive correlation

properties with financial assets that Gold is said to be the best hedge and a safe haven during

economic crisis and market crashes. This was also highlighted by Baur and McDermott (2010),

Tully and Lucey (2005), Baur and Lucey (2010), Jaffe (1989), McCown and Zimmerman (2006),

Draper, Faff and Hillier (2006) in their respective studies. The Indian investor attaches utmost

importance with Gold, as it is ingrained in their psyche. Gold imports constitute above 10% of the

value of total imports in India. Gold and Stock Market compete for investors‟ funds. And therefore,

India being a price taker, the innovations in Gold Prices are likely to impact the Indian Stock

Market. Along with this, Crude Oil Futures and Gold Futures compete with the Stock Market for

investors‟ funds. The present study is an attempt to study the impact of innovations in Crude Oil,

Gold, Crude Futures and Gold Futures on the volatility in Indian Stock Market. The study will be of

benefit to the Indian policy makers in devising the policies related to Crude Oil, Gold and their

Futures so as to help reduce the uncertainty in the Indian Stock Market.

2. Review of Literature

The literature devoted to studying the impact of Crude Oil, Gold, Crude Futures and Gold Futures

is scarce. A brief review of the studies is presented here. Cochrane (1991) and Huang et al. (1996)

showed that the returns on Oil Futures and the Stock Market were connected by a common

stochastic discount factor in a way that the movements in Oil price not only affected expected cash

flow, but also the discount rate via inflation. Further, Jones and Kaul (1996) found a significant

impact of oil price shocks on the Stock Markets of US, Canada, UK and Japan. They revealed that

the Volatility was transmitted to the Stock Market either from the channel of real cash flows or the

expected returns or both. Also, Hayo and Kutan (2004) studied the influence of Oil prices on

Russian Stock Market using GARCH. They found that Crude Oil Volatility does not have a

Singh & Chitkara (2016). Asian Journal of Research in Banking and Finance,

Vol. 6, No.2, pp. 1-16.

5

significant impact on Russian equity index. Draper et al. (2006) also explored the investment role

of precious metals in financial markets in the USA. They showed that precious metals including

Gold showed hedging property during periods of abnormal stock market volatility. Further, Sawyer

and Nandha (2006) investigated the impact of Oil price movements on the Stock prices in Australia,

Japan and Malaysia. It was observed that the Japanese equities responded significantly to Oil

prices, since Japan was a Net Oil Importer. Odusami (2009) revealed that excess Stock Market

return is significantly affected by lagged variation in Crude Oil price. Nandha and Faff (2008) also

examined whether Oil price shocks affected the Stock Market in 35 global industry indices based

on FTSE Global Classification. They found that Oil price changes had an impact on equity returns

of all industry indices except mining, oil and gas. Similarly, Lake, et al. (2009) studied the

influence of Oil price returns and its volatility on Stock Market returns. They observed that Greek

and the US Stock Markets were sensitive to Oil price movements. Sharif, et al. (2005) also explored

the impact of Volatility in Crude Oil on Stock prices in UK. They highlighted that the Volatility in

Oil sector directly impacted the Stocks of Oil and gas sector. Further, Do et al. (2009) investigated

the impact of Gold returns on the Stock Market Volatility in ASEAN countries. The findings

revealed a significant impact of Gold returns on the Stock Market Volatility of all the countries

under study. Arouri et al. (2010) studied the impact of Oil price shocks on equity markets in GCC

countries. They found that GCC equity markets were affected significantly by Volatility in Oil

prices except Bahrain and Kuwait. Similarly, Baur and McDermott (2010) tested whether Gold was

a safe haven against stocks of 53 emerging and developing countries including India. They showed

that Gold was a hedge and a safe haven for European markets and the US but not for Australia,

Canada, Japan and BRIC countries. Further, Bhar and Nikolova (2010) explored the relationship

between world Oil prices and Russian Equity market using GARCH. They highlighted that Russian

Stock Market was affected by past innovations in WTI. Sariannidis et al. (2010) also explored the

impact of macroeconomic variables including Crude Oil on US Stock Market using GARCH. They

showed that Crude oil returns negatively affected US Stock returns. Chang (2011) investigated

volatility spillover between Crude Oil spot and Futures and Stock Market in USA. However, little

evidence of volatility spillover between Crude Oil and Stock Market could be observed. Also,

Sumner, Johnson and Soenen (2010) examined the volatility spillovers among Stocks, bonds and

Gold returns. However, no spillover was found between Gold returns and Stock returns over the

period as a whole. In addition to this, Arouri et al. (2011) discovered Volatility spillover from Oil

Futures to Stock returns in Europe. Elyasiani et al. (2011) studied the impact of movements in Oil

return and Oil return Volatility on Stock returns and Stock return Volatilities for thirteen industries

in US economy. They also found a significant impact of Oil Future returns on sector returns in nine

of the thirteen sectors. According to Basu and Gavin (2011), a huge rise in trading in commodity

derivatives over the past decade can be attributed to the need to hedge risk by commercial

producers and users of commodities. Commodities Futures offer high yields and have now become

a popular means of hedging against Stock Market risk. Narayan and Sharma (2011) have shown

that the Stock Market Volatility in the last decade was impacted by commodity price fluctuations.

Similarly, Choo, et al. (2012) examined the behaviour of Japanese Stock Market with respect to

volatility in macroeconomic variables including Crude Oil and Gold in Japan using GARCH. It was

found that Gold and Crude Oil Volatility had no impact on Japanese Stock Market. They found the

evidence of Volatility spillover from Gold Market to Stock Market and vice versa. Mensi et al.

(2013) further explored the Volatility transmission among Gold, Stocks and energy markets,

including Crude Oil. They observed that the Volatility in Stock Market affects the Gold and Crude

Singh & Chitkara (2016). Asian Journal of Research in Banking and Finance,

Vol. 6, No.2, pp. 1-16.

6

markets and vice versa. Hamma et al. (2014) too found the evidence of Volatility spillover from

Crude Oil market to the Tunisian Stock Market. Dhaoui and Khareif (2014) discovered a significant

effect of Oil price shocks on Stock Market returns of seven countries. This was due to the fact that

Oil constitutes a major input for many industries. Arouri et al. (2015) showed that past Gold returns

are significant in explaining the dynamics of conditional return and Volatility of Chinese Stock

Market. However, research literature that focuses on the impact of Crude Oil, Gold, Crude futures

and Gold Futures on the uncertainty in the Indian Stock Market is neglibile. It is vital to study these

variables in this perspective since India is Net Oil Importing country and Net Gold Importing

country. High values of the import of these mineral resources have implications for the economy.

Along with this, the organised trading in commodities and commodity futures in India has affected

the Indian Stock Market and economy at large. The present study attempts to fill these gaps in

existing literature. The findings shall be useful to the Indian policy makers in formulating resource

policies that would help to check Stock Market fluctuations led by Crude Oil and Gold.

3. Database and Methodology

The Stock Market is the indicator of the overall economic health of an economy. Bombay stock

exchange (BSE) is the largest Stock Exchange in India. BSE Sensex has been used as a proxy of

Indian Stock Market, being the oldest Stock Market Index. The strategic resources, namely, Gold

and Crude Oil constitute more than 40% of the value total‡‡

imports in India every year. So it will

be useful to understand their impact on the Indian Stock Market. With the beginning of organised

trading on Commodity Exchanges in India, Crude Futures and Gold Futures compete for investors‟

funds. Thus it was imperative to introduce these variables to understand the impact on Indian

Equity Market. The daily closing Sensex values have been obtained from the official website of

Bombay Stock Exchange, India§§

. The daily closing Crude Oil spot prices, Gold spot prices, 3-

months Crude Oil Futures and 3-months Gold Futures data have been taken from the official

website of Multi Commodity Exchange (MCX), India***

. The study spans from 2nd

May, 2005 to

31st March, 2011. The starting date of the period is taken as 2

nd May, 2005, as the trading in Gold,

Crude Oil, Gold Futures and Crude Oil Futures was introduced on MCX on this date. The period

covers major economic innovations like the inception of organised trading in Crude Oil, Gold,

Crude Futures and Gold Futures. The period also accounts for the global economic recession due to

US Sub-prime mortgage crisis. Along with this, it was during the chosen period that there was a

flare up in commodity prices, led by the Oil Bubble. Therefore, understanding the impact of

strategic resources like Crude Oil and Gold on the Stock Market, especially during this period,

would be of special interest to the economists and policy makers.

Engle (1982) and Bollerslev (1986) observed that there is significant non constancy in the variances

of equity returns. To capture this non constant variance they designed GARCH (1, 1) model using

stationary log of equity returns. The model considers the variance of the current error term to be a

function of previous period‟s error terms. The study utilises the log transformation of return series

of the variables. Logarithmic transformation has distinct merits. Using logarithms, one may transfer

‡‡ http://siteresources.worldbank.org/INTOGMC/Resources/10-govt_response-hyperlinked.pdf

§§ http://www.bseindia.com/indices/IndexArchiveData.aspx

*** http://www.mcxindia.com/sitepages/bhavcopy.aspx

Singh & Chitkara (2016). Asian Journal of Research in Banking and Finance,

Vol. 6, No.2, pp. 1-16.

7

non linear relationship into a linear one. In addition to this, when using logarithmic series, the

estimated coefficients have an immediate interpretation as elasticities. Also, when applying log

transformation to the data, the series becomes compact, often resulting in constant variance for the

transformed series (Camilleri, 2006).

Forecasting the Financial Markets is prone to errors of inconstant magnitude (Engle, 2007). This

behaviour is known as heteroskedasticity. The unpredictable market fluctuations may be large for

some periods and smaller for other periods. In econometric terms, this uncertainty or risk is

synonymous to Volatility. Stock Market is the mirror of buoyancy or dullness in the economy.

Knowing about risk or Volatility in the Stock Market is useful to make informed decisions.

According to Engle and Patton (2001), financial asset prices do not evolve independently of the

market around them. So it is likely that other variables may contain vital information for the

Volatility of a series. Bollerslev and Chou (1992) were of the view that many questions in finance

can only be meaningfully handled within a multivariate framework. He also observed that

multivariate model for estimating Volatility was superior to univariate models. In this context we

attempt to study the Volatility in returns of Sensex as affected by Crude Oil, Gold, Crude Futures

and Gold Futures. The time varying Volatility in Sensex returns shall be modelled using

Generalised Autoregressive Conditional Heteroskedasticity (GARCH) model given by Engle

(2007).

The estimation of Volatility requires the times series to be stationary. The stationarity of return

series is tested using Augmented Dickey Fuller (ADF) Test at 5% level of significance. In order to

study the transmission of shocks from these variables to the Indian Stock Market, the return series

of Crude Oil, Gold, Crude futures and Gold Futures are added to the variance equation of GARCH

model. Finally, the residual heteroskedasticity in GARCH model of Sensex Volatility is tested

using ARCH (Autoregressive Conditional Heteroskedasticity) test.

4. Analysis and Discussion

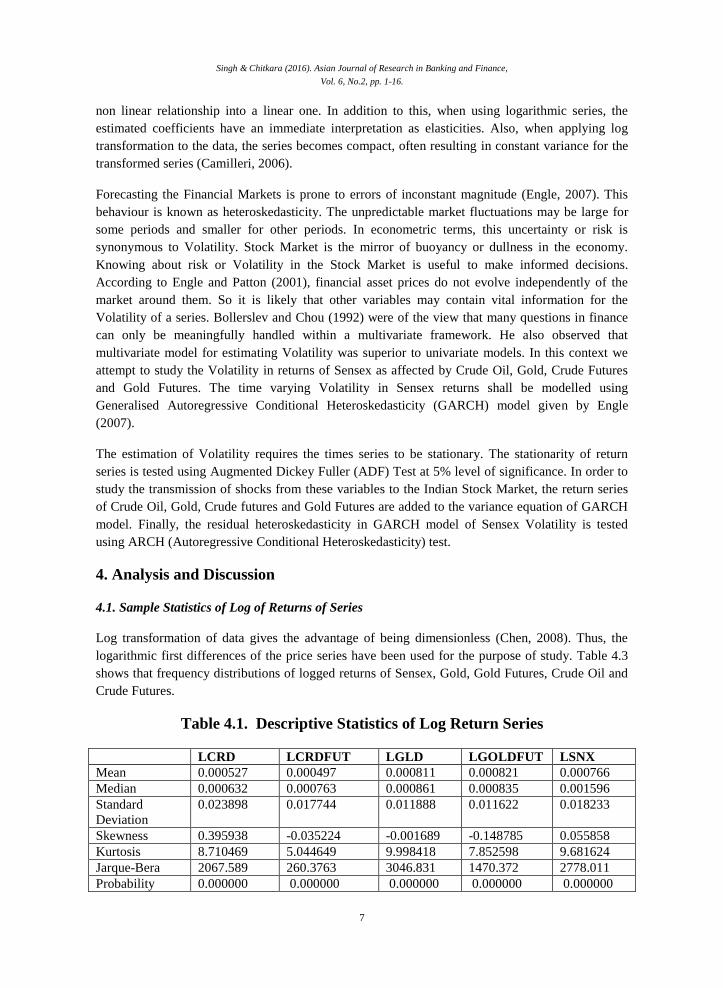

4.1. Sample Statistics of Log of Returns of Series

Log transformation of data gives the advantage of being dimensionless (Chen, 2008). Thus, the

logarithmic first differences of the price series have been used for the purpose of study. Table 4.3

shows that frequency distributions of logged returns of Sensex, Gold, Gold Futures, Crude Oil and

Crude Futures.

Table 4.1. Descriptive Statistics of Log Return Series

LCRD LCRDFUT LGLD LGOLDFUT LSNX

Mean 0.000527 0.000497 0.000811 0.000821 0.000766

Median 0.000632 0.000763 0.000861 0.000835 0.001596

Standard

Deviation

0.023898 0.017744 0.011888 0.011622 0.018233

Skewness 0.395938 -0.035224 -0.001689 -0.148785 0.055858

Kurtosis 8.710469 5.044649 9.998418 7.852598 9.681624

Jarque-Bera 2067.589 260.3763 3046.831 1470.372 2778.011

Probability 0.000000 0.000000 0.000000 0.000000 0.000000

Singh & Chitkara (2016). Asian Journal of Research in Banking and Finance,

Vol. 6, No.2, pp. 1-16.

8

The means of return series indicate that Gold Futures and Gold gave the highest daily mean returns

to the investors closely followed by Sensex. This was also observed in a study by Sumner et al.

(2010) and Mensi et al. (2013). Crude oil series showed mean returns much less than Gold, Gold

Futures and Sensex. Crude Futures gave the lowest mean return of all. Table 4.1 shows that highest

volatility was observed in the returns of Crude Oil, as given by standard deviation. This indicates

the riskiness of Crude Oil during 2005-2011. Sensex appeared to have a lower dispersion from

mean and thereby lower riskiness than Crude Futures, as also noted in a study by Anoruo and

Mustafa (2007). Crude Oil was also more volatile than Gold as was observed by Hammoudeh and

Yuan (2008) in his study. Gold and Gold Futures were seemingly the safest bet during the period

under study due to lower standard deviations compared to returns of other variables under

consideration. Gold exhibited the least volatility. They attributed this to the reason that a good

portion of Gold supply comes from recycling which may reduce Volatility. All of the displayed

financial variables had asymmetric frequency distributions. The distributions of mean returns of

Crude Futures, Gold and Gold Futures are negatively skewed. This means that decreases in returns

occurred more often than increases during 2005 to 2011. Morales and Andresso (2014) had also

found Gold returns to be negatively skewed in their study. A negative skewness means that the

investor could expect unpleasant surprises more than pleasant ones on a daily basis while investing

in Crude Futures, Gold and Gold Futures during 2005 to 2011.

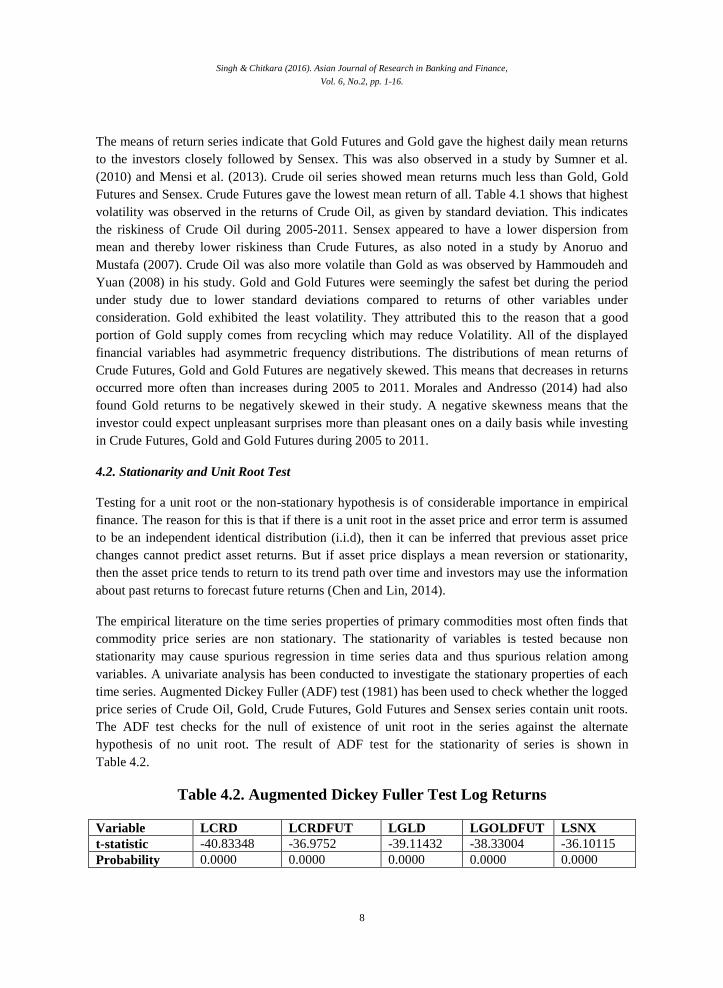

4.2. Stationarity and Unit Root Test

Testing for a unit root or the non-stationary hypothesis is of considerable importance in empirical

finance. The reason for this is that if there is a unit root in the asset price and error term is assumed

to be an independent identical distribution (i.i.d), then it can be inferred that previous asset price

changes cannot predict asset returns. But if asset price displays a mean reversion or stationarity,

then the asset price tends to return to its trend path over time and investors may use the information

about past returns to forecast future returns (Chen and Lin, 2014).

The empirical literature on the time series properties of primary commodities most often finds that

commodity price series are non stationary. The stationarity of variables is tested because non

stationarity may cause spurious regression in time series data and thus spurious relation among

variables. A univariate analysis has been conducted to investigate the stationary properties of each

time series. Augmented Dickey Fuller (ADF) test (1981) has been used to check whether the logged

price series of Crude Oil, Gold, Crude Futures, Gold Futures and Sensex series contain unit roots.

The ADF test checks for the null of existence of unit root in the series against the alternate

hypothesis of no unit root. The result of ADF test for the stationarity of series is shown in

Table 4.2.

Table 4.2. Augmented Dickey Fuller Test Log Returns

Variable LCRD LCRDFUT LGLD LGOLDFUT LSNX

t-statistic -40.83348 -36.9752 -39.11432 -38.33004 -36.10115

Probability 0.0000 0.0000 0.0000 0.0000 0.0000

Singh & Chitkara (2016). Asian Journal of Research in Banking and Finance,

Vol. 6, No.2, pp. 1-16.

9

ADF test for the first difference of all logged series shows that the probability values of t-statistic is

not significant at 5%. Hence the null of unit root can be rejected for all logged variables after first

differencing at 5% level of significance. Therefore our return series are stationary. In other words,

logged price series of Crude Oil, Gold, Crude Futures, Gold Futures and Sensex are I (1).

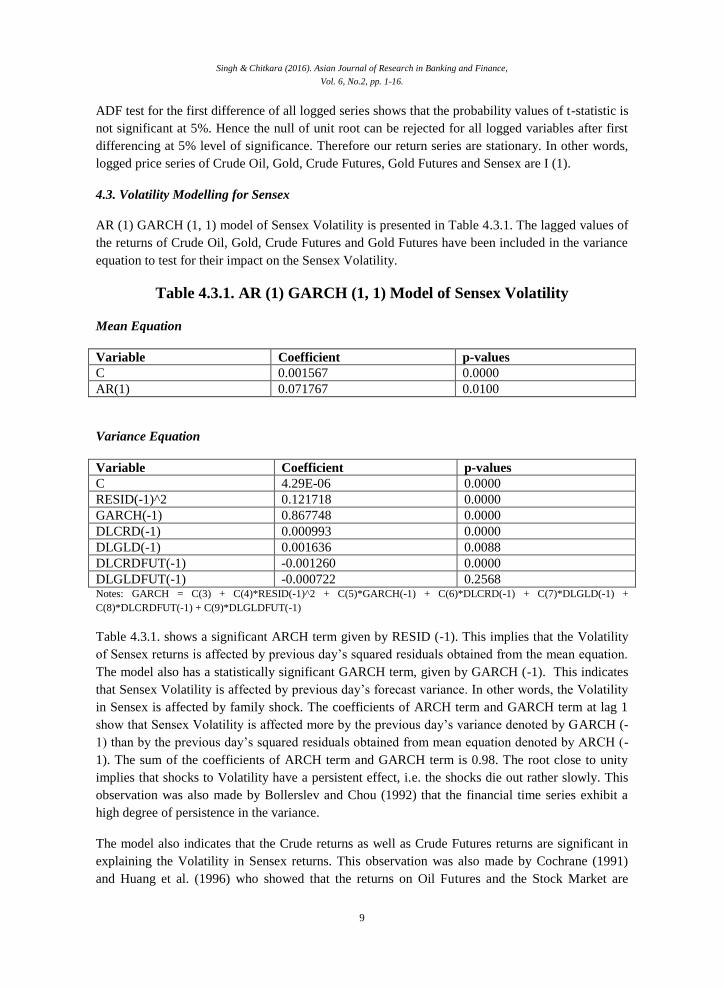

4.3. Volatility Modelling for Sensex

AR (1) GARCH (1, 1) model of Sensex Volatility is presented in Table 4.3.1. The lagged values of

the returns of Crude Oil, Gold, Crude Futures and Gold Futures have been included in the variance

equation to test for their impact on the Sensex Volatility.

Table 4.3.1. AR (1) GARCH (1, 1) Model of Sensex Volatility

Mean Equation

Variable Coefficient p-values

C 0.001567 0.0000

AR(1) 0.071767 0.0100

Variance Equation

Variable Coefficient p-values

C 4.29E-06 0.0000

RESID(-1)^2 0.121718 0.0000

GARCH(-1) 0.867748 0.0000

DLCRD(-1) 0.000993 0.0000

DLGLD(-1) 0.001636 0.0088

DLCRDFUT(-1) -0.001260 0.0000

DLGLDFUT(-1) -0.000722 0.2568 Notes: GARCH = C(3) + C(4)*RESID(-1)^2 + C(5)*GARCH(-1) + C(6)*DLCRD(-1) + C(7)*DLGLD(-1) +

C(8)*DLCRDFUT(-1) + C(9)*DLGLDFUT(-1)

Table 4.3.1. shows a significant ARCH term given by RESID (-1). This implies that the Volatility

of Sensex returns is affected by previous day‟s squared residuals obtained from the mean equation.

The model also has a statistically significant GARCH term, given by GARCH (-1). This indicates

that Sensex Volatility is affected by previous day‟s forecast variance. In other words, the Volatility

in Sensex is affected by family shock. The coefficients of ARCH term and GARCH term at lag 1

show that Sensex Volatility is affected more by the previous day‟s variance denoted by GARCH (-

1) than by the previous day‟s squared residuals obtained from mean equation denoted by ARCH (-

1). The sum of the coefficients of ARCH term and GARCH term is 0.98. The root close to unity

implies that shocks to Volatility have a persistent effect, i.e. the shocks die out rather slowly. This

observation was also made by Bollerslev and Chou (1992) that the financial time series exhibit a

high degree of persistence in the variance.

The model also indicates that the Crude returns as well as Crude Futures returns are significant in

explaining the Volatility in Sensex returns. This observation was also made by Cochrane (1991)

and Huang et al. (1996) who showed that the returns on Oil Futures and the Stock Market are

Singh & Chitkara (2016). Asian Journal of Research in Banking and Finance,

Vol. 6, No.2, pp. 1-16.

10

connected by a common stochastic discount factor. Jones and Kaul (1996) had also highlighted the

impact of Oil price shocks on the Stock Markets of US, Canada, UK and Japan from the channel of

real cash flows or the expected returns or both. The result of present study is also supported by

Odusami (2009) who showed that excess Stock Market return is significantly affected by lagged

variation in Crude Oil price. Also, Arouri et al. (2011) had found the evidence of Volatility

spillover from Oil Futures to stock returns in Europe. Likewise, Narayan and Sharma (2011) had

shown that innovations in commodity markets affect equity markets and vice versa. Elyasiani et al.

(2011) had made a similar observation for thirteen industries in US economy and found a

significant impact of Oil Future returns on sector returns in nine of the thirteen sectors. The result

was supported by Chang (2011), who found the evidence of transmission of shocks from the returns

of Crude Oil Futures market to the Stock Markets in USA. Hamma et al. (2014) also showed the

evidence of Volatility spillover from Crude Oil market to the Tunisian Stock Market. Likewise,

Dhaoui and Khraief (2014) found significant effect of Oil price shocks on Stock Market returns of

seven countries. He attributed this to the fact that Oil constitutes a major input for many industries.

The model of Sensex Volatility shows that Gold price shocks are transmitted to the Stock return

Volatility. The result is supported by Basu and Gavin (2011), who stated that a huge rise in trading

in commodity derivatives over the past decade could be attributed to the need to hedge risk by

commercial producers and users of commodities. They added that Commodities Futures offer high

yields and have now become a popular means of hedging against Stock Market risk. Narayan and

Sharma (2011) too, had found that the Stock Market Volatility in the last decade was impacted by

commodity price fluctuations. Similarly, Clark (1973), Tauchen and Pitts (1983) and Ross (1989)

had highlighted that the Volatility of asset prices is can be attributed to the information flow among

the markets. Following this, it can be inferred that the prices and Volatility of the Gold, Oil and

Stocks are linked through the information flow among markets. Likewise, Do et al. (2009) had

revealed a significant impact of Gold returns on the Stock Market Volatility of ASEAN. The result

of present study is also supported by Arouri et al. (2015) who found that past Gold returns are

significant in explaining the Volatility of Chinese Stock Market.

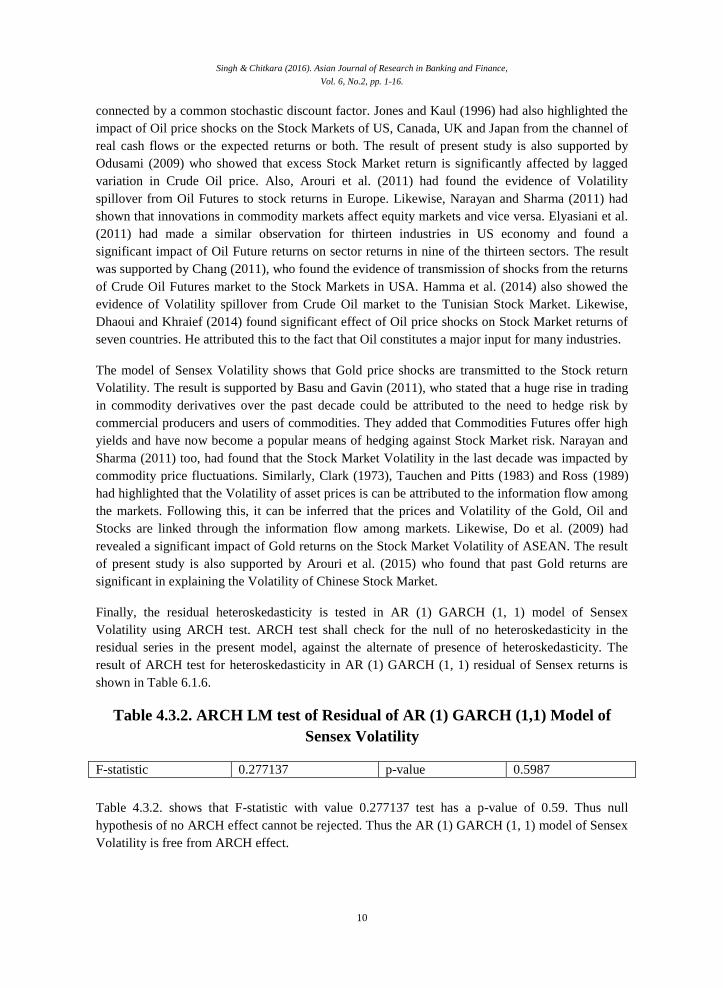

Finally, the residual heteroskedasticity is tested in AR (1) GARCH (1, 1) model of Sensex

Volatility using ARCH test. ARCH test shall check for the null of no heteroskedasticity in the

residual series in the present model, against the alternate of presence of heteroskedasticity. The

result of ARCH test for heteroskedasticity in AR (1) GARCH (1, 1) residual of Sensex returns is

shown in Table 6.1.6.

Table 4.3.2. ARCH LM test of Residual of AR (1) GARCH (1,1) Model of

Sensex Volatility

F-statistic 0.277137 p-value 0.5987

Table 4.3.2. shows that F-statistic with value 0.277137 test has a p-value of 0.59. Thus null

hypothesis of no ARCH effect cannot be rejected. Thus the AR (1) GARCH (1, 1) model of Sensex

Volatility is free from ARCH effect.

Singh & Chitkara (2016). Asian Journal of Research in Banking and Finance,

Vol. 6, No.2, pp. 1-16.

11

4.4. Conclusion and Implications

Volatility in the Indian Stock Market is affected by the innovations in Gold, Crude Oil as well as

Crude Futures. This implies that the investors and the fund managers need to keep a close watch on

Gold and Crude Oil markets while investing in the Indian Stock Market. This also gives rise to the

hedging opportunities for the risk-averse investors. The returns in Crude Futures have an impact on

the Volatility in the Indian Stock Market. The onset of organized trading on Commodity bourses in

India has brought with it the travails of speculation as well. Suitable taxes need to be imposed on

the transactions in Crude Oil Futures to check speculative activity on commodity bourses in India.

According to Bhowmick (2013), high Volatility in the Stock Market indicates uncertainty and

instability in the economy. Oil is an input to production and changes in Oil price make the Indian

financial market vulnerable. Crude Oil and Gold are commodities of strategic importance

throughout the world. India is one of the largest importer of Crude Oil†††

and the largest importer of

Gold‡‡‡

. The demand for these commodities is massively growing every year. Thus, Indian

economy is substantially affected by the price fluctuations in Oil and Gold. The present study

shows that Crude Oil, Gold as well as Crude Futures are significant in explaining the Volatility in

the Indian Stock Market from 2005 to 2011. Indian economy is a price taker and has to bear the

brunt of the fluctuations in the international Crude Oil and Gold markets, as reflected in the Stock

Market.

In order to minimize the effect of Crude Oil shocks, India needs to adopt double-edged policies that

reduce the demand as well as the import of Crude Oil. On the supply side, it is imperative to

maintain strategic oil reserves to counterbalance the impact of oil led Volatility on Indian economy

and Stock Markets. There is a dire need to pump up the energy conservation practices in India, so

as to reduce dependence on Crude Oil. The government of India has been providing Oil subsidies

of about $6–$7 billion. Despite this, the losses suffered by Oil companies amounted to $22 billion

in the year ending March 2009. Such price Volatility can produce unexpected large losses from

hedging and increase the costs of price control. Major policy initiatives should also be put in place

to curb the demand for Crude Oil by deregulating the Crude Oil in India and executing stringent

energy tax reforms. The introduction of Compressed Natural Gas in Delhi and a major government

intervention in making Delhi a green and clean capital has been a successful move. It included the

compulsory use of CNG by the public transport. The same model, if replicated across India can

drastically check the demand for Oil imports and Oil-led Volatility in the Indian economy.

Indraprastha Gas Ltd. was incorporated solely for the purpose of distributing CNG in the National

Capital Territory (NCT). It distributes CNG through CNG stations for transportation and also

distributes Piped Natural Gas to domestic, commercial and industrial users. It has replaced the

demand for diesel and Liquefied Petroleum Gas (LPG) to some extent. It is also vital for the

government to work constructively to reduce the dependence on Crude Oil as a major energy

source. There is a need to focus on harnessing renewable sources of energy like geothermal energy,

solar energy and wind energy, which are abundant in India, for building a sustainable future.

††† http://www.mcxindia.com/Uploads/Products/89/Crudeoil.pdf

‡‡‡ http://www.mcxindia.com/SitePages/ContractSpecification.aspx?ProductCode=GOLD

Singh & Chitkara (2016). Asian Journal of Research in Banking and Finance,

Vol. 6, No.2, pp. 1-16.

12

The Indian government needs to develop relevant import policies and taxation policies to reduce the

demand for Gold and Crude oil. Also, the authorities need to pace up energy conservation

mechanisms as well as harnessing of alternative sources of energy in order to safeguard the Stock

Market and the economy from jolts in global Crude Oil and Gold Markets. Policies well framed and

executed in this direction would help to cushion the Indian Stock market and the economy from the

developments in Gold, Crude Oil and Crude Futures.

References

Anoruo, Emmanuel and Mustafa, Muhammad (2007),"An Empirical Investigation into the Relation

of Oil to Stock Market Prices", North American Journal of Finance and Banking Research,

Vol 1, No. 1.

Arouri, Mohamed El Hedi and Rault, Christopher (2010),"Oil Prices and Stock Markets: What

Drives What in the Gulf Corporation Council Countries?", Available at

http://ssrn.com/abstract=1549536

Arouri, M.E.H., Jouini, J., & Nguyen, D.K. (2011), “Volatility Spillovers between Oil Prices and

Stock Sector Returns: Implications for Portfolio Management”, Journal of International

Money and Finance, Vol 30, pp 1387-1405.

Arouri , Mohamed El Hedi; Lahiani, Amine and Nguyen, Duc Khuong (2015), “ World Gold Prices

and Stock Returns in China: Insights for Hedging and Diversification Strategies”,

Economic Modeling, Volume 44, pp 273–282.

Basu, Parantap and Gavin, William T.(2011),” What Explains the Growth in Commodity

Derivatives?”, Federal Reserve Bank of St. Louis Review, Vol. 93, No. 1, pp. 37-48.

Baur, Dirk G., Lucey, Brian M. (2010). "Is Gold a Hedge or a Safe Haven? An Analysis of Stocks,

Bonds and, Gold", The Financial Review, Vol. 45, Issue 2, pp, 217-229.

Baur, Dirk G., and McDermott, Thomas K. (2010), “Is Gold a Safe Haven? International

Evidence”, Journal of Banking and Finance, Volume 34, Issue 8, pp 1886-1898.

Bhar, Ramaprasad and Nikolova, Biljana (2010), "Global oil Prices, Oil Industry and Equity

Returns: Russian Experience", Scottish Journal of Political Economy, Volume 57, Issue 2,

pp. 169-186.

Bhowmik, D. (2013), “Stock Market Volatility: An Evaluation”, International Journal of Scientific

and Research Publications, Volume 3, Issue 10.

Bollerslev, T. (1986), “Generalized Autoregressive Conditional Heteroskedasticity”, Journal of

Econometrics, Vol 31, pp 307-327.

Bollerslev, Tim and Chou, Ray Y. and Kroner, Kenneth F (1992), “ARCH Modeling in Finance: A

Review of Theory and Empirical Evidence”, Journal of Econometrics, Vol 52, pp 5-59.

Singh & Chitkara (2016). Asian Journal of Research in Banking and Finance,

Vol. 6, No.2, pp. 1-16.

13

Callaghan, Gary O‟ (1991), “The Structure and Operation of the World Gold Market”, Available at

http://ssrn.com/abstract=885158

Camilleri (2006), “An Analysis of Stock Index Distributions of Selected Emerging Markets”, Bank

of Valetta Review, Vol 33, pp 33-49.

Chang, Chia-Lin; McAleer, Michael and Tansuchat Roengchai (2011), “Crude Oil Hedging

Strategies Using Dynamic Multivariate GARCH”, Energy Economics, Vol 33, Issue 5.

Chen, Mei-Hsiu (2008), “Understanding World Commodity Prices: Returns, Volatility and

Diversification” Available at http://ssrn.com/abstract=1253202.

Chen, Nai-Fu; Roll, Richard and Ross, Stephen A. (1986), "Economic Forces and the Stock

Market", Journal of Business, Vol. 59, Issue 3, pp. 383-403.

Chen, S. W. and Lin, Shih-Mo (2014), “Non-linear Dynamics in International Resource Markets:

Evidence from Regime Switching Approach”, Research in International Business and

Finance, Vol 30, pp. 233-247.

Choo, Wei-Chong; Lee, See-Nie and Ung, Sze-Nie. (2012),“Macroeconomics Uncertainty and

Performance of GARCH Models in Forecasting Japan Stock Market Volatility”,

International Journal of Business and social Science, Vol 2, No 1.

Clark, P.K. (1973), A Subordinated Stochastic Process Model with Finite Variance for Speculative

Prices, Econometrica, Vol 41, No 1, pp 135-155.

Cochrane, John H. (1991), Asset Pricing, Princeton, New Jersey: Princeton University Press.

Dhaoui, Abderrazak and Khraief , Naceur (2014), “ Empirical Linkage between Oil Price and Stock

Market Returns and Volatility: Evidence from International Developed Markets”.

Economics Discussion Papers, No 2014-12, Kiel Institute for the World Economy.

Dickey, D. and W.A, Fuller, 1981, “Likelihood Ratio Statistics for Autoregressive Time Series with

a Unit Root” Econometrica, Vol 49, pp. 1057-1038.

Do, Giam Quang; Mcaleer, Michael and Sriboonchitta, Songsak (2009), “Effects of International

Gold Market on Stock Exchange Volatility: Evidence from ASEAN Emerging Stock

Markets”, Economics Bulletin, Volume 29, Issue 2, Pages: 599-610.

Draper, Paul; Faff, Robert and Hillier, David (2006), "Do Precious Metals Shine? An Investment

Perspective", Financial Analysts Journal, Vol. 62, No. 2, pp. 98-106.

Elyasiani, E., Mansur, I., Babatunde, O. (2011), “Oil Price Shocks and Industry Stock Returns”,

Energy Economics, Vol 33, No 5, pp 33-52.

Engle, Robert F.(1982), Autoregressive Conditional Heteroskedasticity with Estimates of the

Variance of United Kingdom Inflation. Econometrica, Vol 50, pp 987-1007.

Singh & Chitkara (2016). Asian Journal of Research in Banking and Finance,

Vol. 6, No.2, pp. 1-16.

14

Engle, Robert F. and Granger, C.W.J. (1987), “Cointegration and Error Correction: Representation,

Estimation and Testing”, Econometrica, Vol 55, No 2, pp. 251-276.

Engle, Robert F and Patton, Andrew J (2001), “What Good is a Volatility Model?”, Quantitative

Finance, Vol 1, pp. 237-245.

Faugere, Christophe, and Erlach, Julian Van (2005), “The Price of Gold: A Global Required Yield

Theory”, The Journal of Investing, Vol. 14, No. 1, pp. 99-111.

Hamma, Wajdi; Jarboui, Anis and Gorbel, Ahmed (2014) , “Effect of Oil Price Volatility on

Tunisian Stock Market at Sector Level and Effectiveness of Hedging Strategy”, Procedia

Economics and Finance, Vol 13, pp. 109-127.

Hammoudeh, Shawkat and Yuan, Yuan (2008), "Metal Volatility in the Presence of Oil and Interest

Rate Shocks", Energy Economics, Vol. 30, Issue 2, pp.606-620.

Hayo, Bernd and Kutan, Ali M. (2004), "The Impact of News, Oil Prices and Global Market

Developments on Russian Financial Markets", Economics of Transition, Volume 13,

No. 2, pp. 373-393.

Jaffe, Jeffrey F. (1989), “Gold and Gold Stocks as Investment for Institutional Portfolios”,

Financial Analyst Journal, Vol. 45, No. 2, pp. 53-59.

Jones, Charles M. and Kaul, Gautam (1996), “Oil and the Stock Markets”, Journal of Finance,

Vol. 51, Issue 2, pp.463-491.

Lake, Andreas Ektor and Katrakilidis, Constantinos (2009) "The Effects of the Increasing Oil Price

Returns and its Volatility on Four Emerged Stock Markets", European Research Studies,

Volume 12, Issue 9, pp. 149-161.

Mensi, Walid; Beljid, Makram; Boubaker, Adel and Managi, Shunsuke (2013), “Correlations and

Volatility Spillovers across Commodity and Stock Markets: Linking Energies, Food, and

Gold”, Economic Modelling, Vol 32, pp 15-22.

Morales, Lucia and Andresso, Bernadette (2014), “Volatility Analysis of Precious Metal Returns

and Oil Returns: An ICSS Approach”, Journal of Economics and Finance,

Volume 38, Issue 3, pp 492-517.

McCown, James Ross and Zimmerman, John R. (2006), "Is Gold a Zero beta Asset? Analysis of

the Investment Potential of Precious Metals”, http://ssrn.com/abstract=920496

Nandha, Mohan and Hammoudeh, Shawkat (2007), “Systematic Risk, Oil Price and Exchange Rate

in Asia-Pacific Stock Markets”, Research in International Business and Finance, Vol. 21,

Issue 2, pp. 326-341.

Nandha, Mohan and Faff, Robert (2008), "Does Oil Move Equity Prices A Global View?", Energy

Economics, Vol. 30, Issue 3, pp. 986-997.

Singh & Chitkara (2016). Asian Journal of Research in Banking and Finance,

Vol. 6, No.2, pp. 1-16.

15

Narayan, P.K., & Sharma, S. (2011),“New Evidence on Oil Price and Firm Returns”, Journal of

Banking and Finance, Vol 35, pp 3253-3262.

Odusami, Babatunde Olatunji (2009), "Crude Oil Shocks and Stock Market Returns", Applied

Financial Economics, Vol. 19, Issue 4, pp. 291-303.

Radhika (2005), "Macroeconomic Implications of Oil Price Hike". Available at

http://ssrn.com/abstract=838784

Ross, S.A. (1989), “Information and Volatility: The No-Arbitrage Martingale Approach to Timing

and Resolution Irrelevancy”, The Journal of Finance, Vol 44, No 1, pp 1-17.

Sariannidis, Nikolaos; Giannarakis, Grigoris; Litinas, Nicolaos and Konteos, George (2010), “Á

GARCH Examination of Macroeconomic Effects on U.S. Stock Market: A Distinction

between the Total Market Index and the Sustainability Index”, European Research Studies

Journal, Vol 13, Issue 1.

Sawyer, Kim R. and Nandha, Mohan (2006), “How Oil Moves Stock Prices”, Available at

http://ssrn.com/abstract=910427

Shafie, Shahriar and Topal, Erkan (2009), "A Long Term View of the Worldwide Fossil Fuel

Prices", Applied Energy, Volume 87, Issue 3, pp. 988-1000.

El-Sharif, Idris; Brown, Dick; Burton, Bruce; Nixon, Bill and Russell, Alex (2005), "Evidence on

the Nature and Extent of the Relationship between Oil Prices and Equity Values in the

UK", Energy Economics, Vol. 27, Issue 6, pp. 819-830.

Sumner, Steven W.; Johnson, Robert and Soenen, Luc, (2010), "Spillover Effects among Gold,

Stocks and Bonds", Journal of' Centrum Cathedra, Volume 3, Issue 2, pp. 106-120.

Tauchen, G.E., Pitts, M. (1983), The Price Variability-Volume Relationship on Speculative

Markets, Econometrica, Vol 51, Issue 2, pp. 485-505.

Tully, Edel and Lucey, Brian M. (2005), "APGARCH Investigation of the Main Influences on the

Gold Price" Available at http://ssrn.com/abstract=792205

Weblinks

http://siteresources.worldbank.org/INTOGMC/Resources/10-govt_response-hyperlinked.pdf

http://www.mcxindia.com/aboutus/aboutus.htm

http://www.mcxindia.com/Sitepages/HistoricalDataForVolume.aspx

http://www.mcxindia.com/sitepages/SpotMarketHistory.aspx?sLinkPage=Y

http://www.mcxindia.com/SitePages/ContractSpecification.aspx?ProductCode=GOLD

Singh & Chitkara (2016). Asian Journal of Research in Banking and Finance,

Vol. 6, No.2, pp. 1-16.

16

http://www.rbi.org.in/scripts/AnnuaIPublications.aspx?head=Handbook%20of%2OStatistics%20on

%20Indian%20Economy

http://siteresources.worldbank.org/INTOGMC/Resources/10-govt_response-hyperlinked.pdf

http://www.bseindia.com/indices/IndexArchiveData.aspx

http://www.mcxindia.com/sitepages/bhavcopy.aspx

http://www.mcxindia.com/Uploads/Products/89/Crudeoil.pdf

http://www.mcxindia.com/SitePages/ContractSpecification.aspx?ProductCode=GOLD