Embed Size (px)

Citation preview

RESPARESPAA Guide toComplying withthe Real EstateSettlementProcedures Act

For a complete listing of the business solutions offeredfrom the NATIONAL ASSOCIATION OF REALTORS®, visit us online at www.REALTOR.org/Store.

To receive NAR product updates and specials, send youremail address to: [email protected]

RESPAA Guide toComplying withthe Real EstateSettlementProcedures Act

© 2005 NATIONAL ASSOCIATION OF REALTORS®

All rights reserved.

REGULATORY AND INDUSTRY RELATIONS

The NAR Regulatory and Industry Relations Department isthe vehicle for representing REALTORS® and the real estateindustry in today’s changing regulatory businessenvironment. The Department’s focus includes: Housing,Financial, Business, Commercial and EnvironmentalAffairs; Industry Relations; and Housing Opportunities.The group’s mission is to enhance NAR’s regulatory policypresence in Washington D.C., establish and coordinateformal relations with pertinent industry organizations andgroups, and conduct long-term policy analysis, with specialemphasis on how the real estate industry will be affectedby federal regulations. This mission elevates theAssociation’s regulatory and industry relations efforts tounprecedented levels.

3

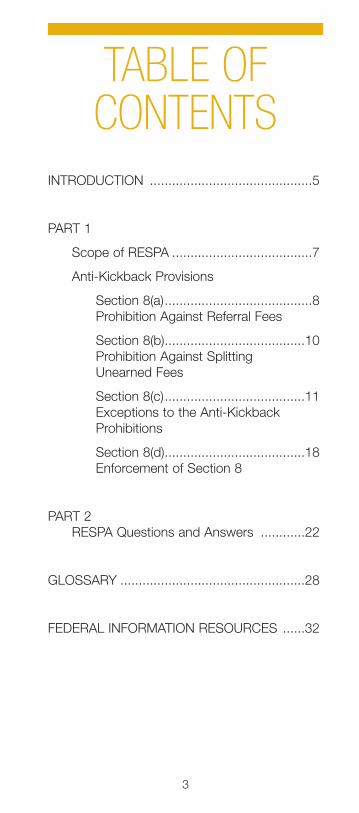

TABLE OFCONTENTS

INTRODUCTION ............................................5

PART 1

Scope of RESPA ......................................7

Anti-Kickback Provisions

Section 8(a)........................................8 Prohibition Against Referral Fees

Section 8(b)......................................10Prohibition Against Splitting Unearned Fees

Section 8(c)......................................11Exceptions to the Anti-Kickback Prohibitions

Section 8(d)......................................18Enforcement of Section 8

PART 2 RESPA Questions and Answers ............22

GLOSSARY ..................................................28

FEDERAL INFORMATION RESOURCES ......32

5

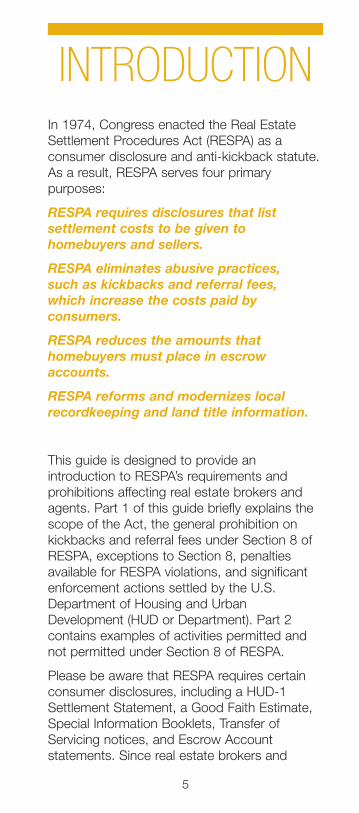

INTRODUCTIONIn 1974, Congress enacted the Real EstateSettlement Procedures Act (RESPA) as aconsumer disclosure and anti-kickback statute.As a result, RESPA serves four primarypurposes:

RESPA requires disclosures that listsettlement costs to be given tohomebuyers and sellers.

RESPA eliminates abusive practices, such as kickbacks and referral fees, which increase the costs paid byconsumers.

RESPA reduces the amounts thathomebuyers must place in escrowaccounts.

RESPA reforms and modernizes localrecordkeeping and land title information.

This guide is designed to provide anintroduction to RESPA’s requirements andprohibitions affecting real estate brokers andagents. Part 1 of this guide briefly explains thescope of the Act, the general prohibition onkickbacks and referral fees under Section 8 ofRESPA, exceptions to Section 8, penaltiesavailable for RESPA violations, and significantenforcement actions settled by the U.S.Department of Housing and UrbanDevelopment (HUD or Department). Part 2contains examples of activities permitted andnot permitted under Section 8 of RESPA.

Please be aware that RESPA requires certainconsumer disclosures, including a HUD-1Settlement Statement, a Good Faith Estimate,Special Information Booklets, Transfer ofServicing notices, and Escrow Accountstatements. Since real estate brokers and

6

agents are not responsible for providing thesedisclosures, this guide does not review thedisclosure requirements under RESPA.

Moreover, please be aware that many stateshave enacted laws with similar prohibitions andconsumer protections as provided underRESPA. This guide discusses only the federalrequirements of RESPA and does not take intoconsideration any additional regulations thatmay have been imposed on the state level. It ispossible that state laws may prohibit activitiesthat are permissible under RESPA, and werecommend that you consult with a RESPAattorney to ensure that you comply with allapplicable laws. This guide is not intended toprovide you with legal advice as to the mattersdiscussed herein.

The NATIONAL ASSOCIATION OF REALTORS®

acknowledges the contribution made to thisguide by:

Phillip L. Schulman, Esq.Kirkpatrick & Lockhart Nicholson Graham LLP1800 Massachusetts Avenue, NW, Suite 200Washington, DC 20036(202) 778-9000 / www.klng.com

7

PART 1SCOPE OF RESPA

RESPA applies to settlement services.*Settlement services are provided by settlementservice providers. Settlement services arethings associated with the purchase of a homethat occur at or before settlement. If the serviceoccurs after settlement, it is generally notconsidered a settlement service. Settlementservices include the following:

Real estate broker or agent services

Services related to the issuance of a title insurance policy

Origination of a mortgage loan

Services rendered by a mortgage broker

Services related to origination, processing, or funding of a mortgage loan

Services rendered by an attorney

Document preparation, including notarization, delivery, and recordation

Rendering credit reports and appraisals

Rendering inspections

Settlement or closing

Services involving hazard, flood, or other casualty insurance or homeowners’ warranties

Services involving real property taxes or other assessments or charges on real property

Any other services that a settlement service provider requires a borrower to pay for before or at closing

*Terms appearing in italics are further defined in the Glossaryto this guide.

8

RESPA, therefore, governs the activities of aperson or entity that provides any of theservices listed above, including real estatebrokers and agents.

RESPA does not apply to:

• Transactions that are primarily for business,commercial, or agricultural purposes

• Government or governmental agencies orinstrumentalities

• Temporary financings

• Secondary market transactions

ANTI-KICKBACKPROVISIONS

Section 8 of RESPA prohibits referral fees andkickbacks to settlement service providersbecause these fees raise the cost of services toconsumers. Section 8 is divided into four parts:

• Section 8(a) prohibits referral fees

• Section 8(b) prohibits the splitting ofunearned fees

• Section 8(c) lists exceptions to theprohibitions in Sections 8(a) and (b)

• Section 8(d) governs the enforcement ofRESPA

Section 8(a) – Prohibition AgainstReferral FeesSection 8(a) prohibits a person from giving orreceiving any fee, kickback, or thing of valuepursuant to any written or oral agreement orunderstanding that business involving a realestate settlement service and a federally relatedmortgage loan will be referred to any person.

9

Four elements are required for a Section 8(a)violation:

1. A settlement service involving a federallyrelated mortgage loan. RESPA defines afederally related mortgage loan as a loansecured by a first or subordinate lien on aone-to-four family residential dwelling(including manufactured homes) that meetscertain other criteria. A federally relatedmortgage loan means any loan that placesa lien on a one-to-four family property andincludes both government-insured andconventional mortgage loans.

2. A referral of business incident to or part ofa settlement service pursuant to an agreement or understanding

Please be aware that the agreement orunderstanding does not have to be writtenor verbalized, but may be established bypractice, pattern, or course of conduct.

3. Payment or receipt of a fee or thing ofvalue

HUD’s regulations provide that a fee orthing of value is virtually anything onereceives in consideration for referring asettlement service, including, but notlimited to:

• Money or fees• Discounts• Duplicate payments of a charge• Stock, dividends, distribution of profits• Credits representing money that may be

paid at a future date• Opportunity to participate in a money-

making program• Retained or increased earnings• Increased equity in a parent or subsidiary

entity• Special bank deposits or accounts, or

special or unusual banking terms• Services of all types at special or free rates

10

• Lease or rental payments based in wholeor in part on the amount of business referred

• Trips and payment of another person’s expenses

• Reduction in credit against an existing obligation

4. For the referral of settlement servicebusiness

Section 8(b) – Prohibition AgainstSplitting Unearned FeesIn addition to the prohibition on kickbacks andreferral fees, RESPA prohibits a person fromgiving and receiving any portion, split, orpercentage of any fee charged or received for areal estate settlement service in connectionwith a federally related mortgage loan, unlessthe portion of the fee is for services actuallyperformed.

Three elements are required for a Section 8(b)violation:

• A settlement service involving a federallyrelated mortgage loan

• A split of an unearned fee between two ormore parties or a mark-up of an unearned fee

• A payment for the referral of business, ratherthan for services actually performed

Some federal circuit courts have interpretedSection 8(b) differently from HUD. The Seventh,Fourth, and Eighth Circuits have concluded thatSection 8(b) requires an actual split of theunearned portion of a fee between two or moreparties in order for a Section 8(b) violation tooccur. For example, a lender orders a creditreport, which costs $15. The lender chargesthe consumer $25 for the credit report, paysthe credit bureau $15 for the cost of the reportand retains the $10 excess. The lender thenpays the real estate agent who referred theconsumer $5 from the $10 excess. In this

11

example, the $10 represents the unearnedportion of a credit report fee, and the $5payment to the agent qualifies as an actual splitin violation of RESPA.

HUD, however, does not require a split of a feeto find a Section 8(b) violation, and theEleventh, Second, and Third Circuits haveagreed with HUD. HUD issued a policystatement, which describes three scenarioswhere a Section 8(b) violation would occur:

• Two or more persons split a fee and oneperson did not perform any services toreceive a share of the fee

• One person marks up the cost of a third-party service and keeps the differencewithout providing any goods or services tojustify the additional charge

• One person charges a fee for no, nominal orduplicative work, or a fee that exceeds thevalue of the goods or services provided

Using the example above, HUD would take theposition that the lender’s mark up of a $15credit report fee to $25, and retention of the$10 extra, is all that is required to constitute aviolation of Section 8(b).

Section 8(c) – Exceptions to theAnti-Kickback ProhibitionsDespite the prohibitions in Section 8 of RESPA,Congress understood that a number ofbusiness referrals that occur in the settlementservice industry do not harm consumers. As aresult, Congress permitted certain conduct tobe exempt from RESPA and HUD’s scrutiny. If afee or thing of value is paid under one of theseexceptions, the person or entity does notviolate RESPA. These exceptions are listed onthe next page.

12

1. Cooperative agreements betweenlisting and selling real estate brokers

This exception refers only to fee divisionswithin real estate brokerage arrangementswhen all parties are acting in a real estatebrokerage capacity. Please be aware thatthis exception has no applicability to feearrangements between real estate brokersand mortgage brokers, or betweenmortgage brokers.

2. Payments to an attorney for servicesactually rendered

3. Payments by a title company to its dulyappointed title agent for servicesperformed in the issuance of a titlepolicy

To qualify for this exception and receivecompensation as a title agent, an entitymust perform “core title services” and beliable to its insurer for any negligence inconnection with the issuance of a defectivetitle policy. Core title services include:

• Examination and evaluation of the title evidence to determine insurability

• Preparation and issuance of the title commitment

• Clearance of underwriting objections• Preparation and issuance of the title

policy• Handling of closing or settlement where

the closing is part of an all-inclusive title insurance rate

4. Payments by a lender to its dulyappointed agent for servicesperformed in the making of a loan

This exception is unclear and there is littleexplanation provided in the statute,regulations, or legislative history regardingthe meaning of the exception.

13

5. Payments by an employer to itsemployee

Under this exception, an employer may payits own employees for any referral activities.The referred party, however, may not paythe employee or reimburse the employerfor the employee’s referral.

HUD has not articulated a position on whoconstitutes an “employee” under RESPA.Nevertheless, if a person satisfies allInternal Revenue Service requirements foremployment, a reasonable basis exists toconclude that he or she will be consideredan employee under RESPA. Theseemployment requirements include, to namea few:

• Employee is subject to employer’s supervision and control

• Employee maintains a physical presence at the employer’s office

• Employee uses employer’s office suppliesand equipment

• Employee works a set number of hours for employer

• Employee receives paychecks and W-2 forms from employer

It is important to emphasize that real estateagents are typically consideredindependent contractors and notemployees, and, therefore, are not eligiblefor this exception.

6. Payments for services actuallyrendered or goods actually provided

To qualify for this exception, a real estatebroker or agent must satisfy a two-parttest:

1. Actual, necessary, and distinct goods or services must be provided

2. The compensation must be reasonably related to the goods and services provided.

14

With regard to actual goods and services:

• A title agency must perform core title services.

• A mortgage broker must take a loan application and perform at least 5 of the following 13 additional items:

– Analyze the borrower’s income and debt, and pre-qualify the borrower to determine the maximum allowable mortgage.

– Educate the borrower in the home buying and financing process, advise him or her about different types of available loan products, and demonstrate how closing costs and monthly payments differ for different products.

– Collect financial information (tax returns, bank statements) and other related documents.

– Initiate and order Verifications of Employment and Deposit.

– Initiate and order requests for mortgage and other loan verifications.

– Initiate and order appraisals.

– Initiate and order inspections or engineering reports.

– Provide disclosures to the borrower.

– Assist the borrower in understanding and clearing credit problems.

– Maintain regular contact with the borrower, real estate agents, and lender between the time of application and closing, and gather any additional information as needed.

– Order legal documents.

15

– Determine whether the property was located in a flood zone or order such service.

– Participate in the loan closing.

If a mortgage broker takes a loanapplication and performs counseling-typeservices, HUD will consider the followingadditional factors to ensure that meaningfulcounseling is performed and that a brokeris not compensated for steering acustomer to a particular lender:

– The entity furnishes the borrower an opportunity to consider products from at least 3 different lenders

– The entity receives the same compensation regardless of which lender’s products are ultimately selected

– Any payment for the counseling services is reasonably related to the services performed and not based on the amount of loan business referred toa particular lender

• HUD does not define core services for other types of settlement services providers. Nevertheless, numerous othergoods, such as rental of a desk in a real estate broker’s office, services performedby a real estate broker or agent for other settlement service providers, or goods provided, such as software technical support, can qualify for the exception, as long as the services are actual, necessary, and distinct from services already being provided by the real estate broker or agent.

With regard to the compensation paid, itmust be reasonably related to the value ofthe goods or services provided.

16

HUD has not offered meaningful guidance as tohow to determine the reasonableness of aparticular fee. The Department, however, hasindicated that it may be appropriate to considerfees generally charged in the marketplace forthe service provided or the internal cost ofproviding the service. Determining fair marketvalue is a business decision that a real estatebroker or agent must be able to defend shouldHUD or a court question its reasonableness.

Please be aware, however, that RESPA is not arate-setting statute and does not prescribe howmuch a real estate broker or agent may charge.As noted above, RESPA requires that a fee becommensurate with the value of the servicesprovided.

7. Payments among affiliated businessarrangements (AfBAs)

In 1993, RESPA was amended to permittwo settlement service providers to ownother settlement service providers or enterinto a joint venture operation, so long asthe AfBA adheres strictly to RESPArequirements and guidelines. Thus, if a realestate broker refers customers to a titleinsurance agency in which the real estatebroker owns a 50% interest, thisarrangement qualifies as an AfBA.Generally, this exception permits the AfBAowners to receive a return on theirownership interest in the AfBA, and thesepayments are not considered to be referralfees.

To comply with RESPA, an AfBA mustmeet the following requirements of a safeharbor test:

• The AfBA owner who refers business to the AfBA must provide a written disclosure on a separate sheet of paper of the existence of the arrangement along with a written estimate of the charge or range or charges imposed by

17

the AfBA no later than the time of the referral.

• The customer being referred must not berequired to use any particular provider of settlement services.

• No payments, other than a return on ownership interest or payments otherwise permitted under the statute may be received under the arrangement.

In addition to meeting the three-part safeharbor test, an AfBA must be a bona fideprovider of settlement services, rather thana “sham” business used to disguise referralfees. HUD issued a Statement of Policythat lists several factors to be used todetermine if an AfBA is a bona fide providerof settlement services. Please note that anAfBA does not have to meet all factors tobe lawful, and no one particular factor willdetermine whether an AfBA is legitimate.These factors are summarized below:

• An AfBA must have sufficient initial capital, typical in the industry, to conduct the settlement service business for whichit was created.

• The AfBA must have its own employees.

• The AfBA must either manage its own affairs or, if one of its owners provides management services, pay such owner the fair market value of its services.

• The AfBA must have its own office spaceso that the public can clearly identify the entity with which it is doing business. If an AfBA rents space from an owner, it must pay fair market rent to the owner for the space and facilities used.

• The AfBA must provide “substantial services,” or the essential functions and types of services generally performed by the type of entity at issue. For example, in the case of a joint venture title

18

insurance agency, these substantial services are termed “core title services.”

• The AfBA must perform all “substantial services” itself and may not subcontract out such functions. Non-substantial services may be subcontracted out, which include, for example, those relatedto management, accounting, and human resources.

• The AfBA must actively compete in the marketplace for business and attempt to market its services to others besides its joint venture partners.

An entity that meets both the safe harbortest and performs the functions of a bonafide business will satisfy the AfBArequirements. As a result, such an entitymay refer business to and receivedividends from an affiliated settlementservice provider without risk of violatingSection 8.

Please refer to Affiliated BusinessArrangements, A Guide to Complyingwith the Real Estate SettlementProcedures Act (item #126-120) for moreinformation on RESPA’s requirements.

Section 8(d) – Enforcement ofSection 8Real estate brokers and agents should beaware that RESPA authorizes harsh penaltiesfor those in violation of Section 8. Specifically,to enforce the prohibitions against kickbacksand the splitting of fees, Section 8(d) givesHUD the authority to impose the followingpenalties:

• Civil and criminal penalties

• Imprisonment for up to one year

• A fine of up of $10,000

19

• Both imprisonment and a fine

• Treble damages, which means a person whoviolates Section 8 of RESPA must pay threetimes the amount of the charge for thesettlement service involved in the violation

RESPA also authorizes the following entities orpersons to sanction violators:

• State attorney generals and state insurancecommissioners

• HUD, in the case of FHA-insured or VA-guaranteed loans

• Consumers

If a person or entity violates the anti-kickbackprovisions of RESPA, a consumer has one yearto bring an action in court in connection withthe violation. The government, however, maybring an action within three years of theviolation. Business competitors have nostanding to bring a law suit to enforce RESPA.

Over the past couple of years, HUD hasincreased its enforcement staff and stepped upits pursuit of RESPA violators. From theseefforts, note that HUD often has focused itsenforcement efforts on real estate brokers andaffiliated business arrangements. For example,in a July 28, 2003 press release, HUDannounced a settlement agreement with asavings bank, which allegedly paid up to $100to real estate agents for filling out andsubmitting on-line applications for prospectiveborrowers. Under the settlement, the bankagreed to discontinue the practice and paid afine to the U.S. Treasury. The Departmentstated that “HUD has long considered that areal estate agent may not be compensated formerely filling out a loan application” and thatsuch “compensation may even be considered afee for the referral of business in violation ofSection 8(a) of RESPA.” A few months later,HUD announced a similar settlement for allegedpayments to real estate agents for allegedly

20

taking loan applications. This lender agreed topay the government $15,000 as a settlement.

HUD also has pursued real estate brokers andagents for accepting website “virtual tours” ofbroker properties paid for by various titlecompanies. In two separate settlementagreements, real estate brokers agreed to pay$5,200 and $14,000 respectively to settleHUD’s allegations and to discontinue all suchpractices. In addition, HUD has pursued realestate brokers for accepting conference roomrental fees in excess of fair market value.According to the Department, any portion ofthe rental fee received above fair market valueconstituted an alleged fee for the referral ofbusiness. Two real estate brokers agreed topay HUD $45,000 and $15,000.

Moreover, as real estate brokers and agentsoften maintain ownership interests in jointventures, HUD’s recent enforcement effortsinvolving affiliated business arrangements are ofparticular concern. For example, on March 21,2005, HUD announced a settlement withseveral entities that owned a joint venturesettlement company. One such entity wascomprised of real estate agents and distributedits profits from the joint venture based on theagents’ volume of referrals. HUD alleged thatthese payments constituted referral fees, ratherthan returns on an ownership interest, and theparties agreed to pay $325,000 and to modifycertain business practices. Most recently, HUDentered into a settlement agreement with anAtlanta-based real estate broker for allegedpayments to real estate agents. Specifically,HUD alleged that the broker provided agentswith relocation services, paid commissionsimmediately at closing, offered incentives, suchas trips and baseball tickets, and paid highercommissions in exchange for referrals to thebroker’s affiliated business. The real estatebroker agreed to pay a $250,000 fine.

21

Based on these actions, if you encounter anissue in your day-to-day operations that raisesa question under RESPA, it is important thatyou seek additional resources and legal advice,if necessary. As you have read, RESPAviolations can carry serious consequences, andit is imperative that you be aware of possibleRESPA issues at all times.

Please contact NAR, or visit our website atwww.REALTOR.org/RESPA for moreinformational materials on RESPA compliance.

22

PART 2RESPA QUESTIONSAND ANSWERS

1. QUESTION: A real estate agent issponsoring an open house for otheragents. A local title agency reimburses thereal estate agent for the cost of a luncheonand the title agency does not market itstitle services at the open house. Is this aviolation of Section 8 of RESPA?

ANSWER: Yes, this is a violation ofRESPA. By reimbursing the real estateagent for the cost of the luncheon, thetitle agency has given the real estateagent a thing of value in considerationfor the referral of business. Both thetitle agency and the real estate agentcould be held responsible for theRESPA violation. If, however, the realestate agent attends the open house tomake a presentation or to otherwisemarket its services, such paymentsmay be lawful under RESPA.

2. QUESTION: A real estate broker and amortgage lender agree to jointly place afull-page advertisement in a localnewspaper. Each company gets exactlyone-half of the page to advertise itsservices. Each company pays one-half ofthe cost of the advertisement. Is this aviolation of Section 8 of RESPA?

ANSWER: No, this appears to complywith RESPA. As long as theadvertising costs paid by each partyare reasonably related to the value ofthe goods or services received inreturn (i.e., the amount of advertising),no violation exists. HUD has

23

recognized that “[n]othing in RESPAprevents joint advertising[,]” but theDepartment takes the position that “ifone party is paying less than a pro ratashare for the brochure oradvertisement, there could be a RESPAviolation.” *

3. QUESTION: The owner of a title agencymeets the owner of a real estate brokeragefirm for dinner at a local restaurant. Thepurpose of the dinner is for the twoindividuals to discuss future marketingopportunities. After the discussion hasended, the owner of the title agency paysfor the real estate broker’s dinner. Is this aviolation of Section 8 of RESPA?

ANSWER: No, this appears to complywith RESPA. The owner of the titleagency can pay for dinner and notviolate RESPA because the purpose ofthe dinner was business related andwas not a payment for the referral ofbusiness.

4. QUESTION: A buyer’s real estate agentcouriers a purchase agreement to a seller’sreal estate agent and pays a $15 courierfee. The real estate broker charges thebuyer $25 for the courier service and keepsthe remaining $10 for its own use. Is this aviolation of Section 8 of RESPA?

ANSWER: Yes, this could be aviolation of RESPA. According to HUD,marking up the $15 fee and keepingthe extra $10 is a violation of RESPA ifthe real estate broker did not performadditional services to justify the $10mark up.

* HUD Website, Frequently Asked Questions About RESPA ForIndustry, http://www.hud.gov/offices/hsg/sfh/res/resindus.cfm.

24

5. QUESTION: A mortgage lender devises acontest among local real estate agentswhere the real estate agent that refers themost customers to the lender will receive avacation cruise to Alaska. Is this a violationof Section 8 of RESPA?

ANSWER: Yes, this is a violation ofRESPA. The vacation cruise is a thingof value in exchange for the referral ofbusiness and violates Section 8’s anti-kickback provisions. Both themortgage lender and the real estateagents can be held responsible for theviolation under RESPA.

6. QUESTION: “A” is a real estate brokerwho refers business to its affiliate titlecompany “B.” “A” provides its customerswith an affiliated business disclosure thatlists the range of charges that “B” willcharge for title services, states that “A” hasa financial interest in “B,” and notifies thecustomer that he or she is not required touse “B” for title services. Does this violateSection 8 of RESPA?

ANSWER: No, this complies withRESPA. The referrer of business to anaffiliated entity is required to provide awritten disclosure to each consumerthat identifies the affiliatedrelationship, provides the charges orrange of charges that the joint venturegenerally charges, and notifies theconsumer that he or she is notrequired to use the affiliated business.

7. QUESTION: Real estate broker “A” andtitle insurance company “B” create anaffiliated title agency “C.” “C” pays annualdividends to “A” and “B” in proportion tothe amount of business that each refers to“C” during the year. Is this a violation ofSection 8 of RESPA?

25

ANSWER: Yes, this is a violation ofRESPA. An affiliated business mayonly pay its partners in annualdividends that are based on theamount of stock held by the partners.RESPA prohibits the payment ofdividends based on the amount ofbusiness referred or expected to bereferred to an affiliated business.

8. QUESTION: A title company places a faxmachine in the office of a real estate brokerto expedite the process of placing titleorders with the title company. The titlecompany expects that the real estatebroker will refer business to the titlecompany if the broker can quickly sendinformation to the title company. The faxmachine is used only for communicationbetween the real estate broker and the titlecompany. The real estate broker has aseparate fax machine for general business.Is this a violation of Section 8 of RESPA?

ANSWER: No, this appears to complywith RESPA. The title companyprovides the fax machine in exchangefor actual services from the real estate broker and the fax machine isdedicated to business conducted onlywith the real estate broker. If, however,the real estate broker uses the faxmachine both for business with thetitle company and its general realestate business, this may constitute aviolation of RESPA.

9. QUESTION: A settlement agentconducts real estate closings in theconference room of the real estate brokerwith the expectation that the real estatebroker will refer closing business to thesettlement agent. The settlement agent

26

pays fair market value to rent theconference room for each closing. Is this aviolation of Section 8 of RESPA?

ANSWER: No, this appears to complywith RESPA. HUD has determined thata settlement service provider may renta conference room or other officespace from another settlement serviceprovider, as long as it pays fair marketvalue to rent the space. HUD also hasstated that fair market value should bebased on what a non-settlementservice provider would pay for thesame amount of space and services inthe same or a comparable building.

10. QUESTION: A real estate broker pays itsreal estate agents $20 for each referral theagents make to the real estate broker’saffiliated mortgage company. Is this aviolation of Section 8 of RESPA?

ANSWER: Yes, this is a violation ofRESPA. Although RESPA provides anexception for payments made from anemployer to its employees, paymentsbetween a real estate broker and itsreal estate agents do not qualify forthis exception. Real estate agents areconsidered independent contractors,rather than employees of the realestate broker. As a result, the $20payments described above constitutepayments in return for the referral ofbusiness in violation of RESPA.

11. QUESTION: A homeowner’s insurancecompany gives a real estate brokermarketing materials, such as deskcalendars, pens, and notepads, all of whichpromote the homeowner’s insurancecompany’s name. Is this a violation ofSection 8 of RESPA?

27

ANSWER: No, this appears to complywith RESPA. HUD’s RESPA regulationsprovide an exception to Section 8 fornormal promotional and educationalactivities that are not conditioned onthe referral of business and that do notdefray expenses that otherwise wouldbe incurred by persons in a position torefer settlement service business.

12. QUESTION: A mortgage lender occupiesan office in a real estate broker’s businessin order to pre-qualify customers formortgage financing. Occasionally, realestate agents take loan applications fromtheir customers and receive $40 in returnfor each application. Is this a violation ofSection 8 of RESPA?

ANSWER: Yes, this may be a violationof RESPA, according to HUD. HUD hastaken the position that to becompensated as a mortgage broker, aperson must take a loan applicationand perform at least five additionalservices in order to receive payment.Thus, if a real estate agent takes theloan application, but does not performany other functions, he or she cannotreceive payment under RESPA.

28

GLOSSARY Affiliated Business ArrangementAn arrangement in which:

• A person who is in a position to referbusiness incident to or a part of a real estatesettlement service involving a federally relatedmortgage loan, or an associate of suchperson, has either an affiliate relationship withor a direct or beneficial ownership interest ofmore than one percent in a provider ofsettlement services

• Either of such persons directly or indirectlyrefers such business to that provider oraffirmatively influences the selection of thatprovider.

12 U.S.C. § 2602(7).

Affiliate RelationshipThe relationship among business entities whereone entity has effective control over the otherby virtue of a partnership or other agreement oris under common control with the other by athird entity or where an entity is a corporationrelated to another corporation as parent tosubsidiary by an identity of stock ownership. 24 C.F.R. § 3500.15(c)(2).

Agreement or UnderstandingAn agreement or understanding for the referralof business incident to or part of a settlementservice need not be written or verbalized butmay be established by practice, pattern, orcourse of conduct. When a thing of value isreceived repeatedly and is connected in anyway with the volume or value of the businessreferred, the receipt of the thing of value isevidence that it is made pursuant to anagreement or understanding for the referral ofbusiness. 24 C.F.R. § 3500.14(e).

29

AssociateOne who has one or more of the followingrelationships with a person in a position to refersettlement business:

• A spouse, parent, or child of such person

• A corporation or business entity that controls,is controlled by, or is under common controlwith such person

• An employer, officer, director, partner,franchisor, or franchisee of such person

• Anyone who has an agreement,arrangement, or understanding, with suchperson, the purpose or substantial effect ofwhich is to enable the person in a position torefer settlement business to benefit financiallyfrom the referrals of such business.

12 U.S.C. § 2602(8).

Federally Related Mortgage LoanAny loan (other than temporary financing suchas a construction loan) which:

(A) Is secured by a first or subordinate lien onresidential real property (including individualunits of condominiums and cooperatives)designed principally for the occupancy offrom one to four families, including anysuch secured loan, the proceeds of whichare used to prepay or pay off an existingloan secured by the same property

(B) (i) Is made in whole or in part by any lenderthe deposits or accounts of which areinsured by any agency of the federalgovernment, or is made in whole or in partby any lender which is regulated by anyagency of the federal government

(ii) Is made in whole or in part, or insured,guaranteed, supplemented, or assisted inany way, by the Secretary [of HUD] or anyother officer or agency of the federalgovernment or under or in connection witha housing or urban development program

30

administered by the Secretary [of HUD] or ahousing or related program administered byany other such officer or agency

(iii) Is intended to be sold by the originatinglender to the Federal National MortgageAssociation, the Government NationalMortgage Association, the Federal HomeLoan Mortgage Corporation, or a financialinstitution from which it is to be purchasedby the Federal Home Loan MortgageCorporation

(iv) Is made in whole or in part by any“creditor,” as defined in section 1602(f) oftitle 15 [Truth in Lending Act], who makesor invests in residential real estate loansaggregating more than $1,000,000 peryear, except that for the purpose of thischapter, the term “creditor” does notinclude any agency or instrumentality ofany State.

12 U.S.C. § 2602(1).

ReferralA referral includes any oral or written actiondirected to a person which has the effect ofaffirmatively influencing the selection by anyperson of a provider of a settlement service orbusiness incident to or part of a settlementservice when such person will pay for suchsettlement service or business incident theretoor pay a charge attributable in whole or in partto such settlement service or business. Areferral also occurs whenever a person payingfor a settlement service or business incidentthereto is required to use a particular providerof a settlement service or business incidentthereto. 24 C.F.R. § 3500.14(f).

Required UseA situation in which a person must use aparticular provider of a settlement service inorder to have access to some distinct serviceor property, and the person will pay for the

31

settlement service of the particular provider orwill pay a charge attributable, in whole or inpart, to the settlement service. However, theoffering of a package (or combination ofsettlement services) or the offering of discountsor rebates to consumers for the purchase ofmultiple settlement services does not constitutea required use. Any package or discount mustbe optional to the purchaser. The discountmust be a true discount below the prices thatare otherwise generally available, and must notbe made up by higher costs elsewhere in thesettlement process. 24 C.F.R. § 3500.2(b).

Settlement ServicesAny service provided in connection with a realestate settlement including, but not limited to,the following: title searches title examinations,the provision of title certificates, title insurance,services rendered by an attorney, thepreparation of documents, property surveys,the rendering of credit reports or appraisals,pest and fungus inspections, services renderedby a real estate agent or broker, the originationof a federally related mortgage loan (including,but not limited to, the taking of loanapplications, loan processing, and theunderwriting and funding of loans), and thehandling of the processing, and closing orsettlement. 12 U.S.C. § 2602(3).

Thing of ValueAny payment, advance, funds, loan, service, orother consideration. 12 U.S.C. § 2602(2).

It includes, without limitation, monies, things,discounts, salaries, commissions, fees,duplicate payments of a charge, stock,dividends, distributions of partnership profits,franchise royalties, credits representing moniesthat may be paid at a future date, theopportunity to participate in a money-makingprogram, retained or increased earnings,increased equity in a parent or subsidiary entity,special bank deposits or accounts, special or

32

unusual banking terms, services of all types atspecial or free rates, sales or rentals at specialprices or rates, lease or rental payments basedin whole or in part on the amount of businessreferred, trips and payment of another person’sexpenses, or reduction in credit against anexisting obligation. 24 C.F.R. § 3500.14(d).

FEDERALINFORMATIONRESOURCES

For more information on RESPA and HUD’sregulation of real estate brokers and agents,please visit:

http://www.hud.gov/offices/hsg/sfh/res/respa_hm.cfm

or contact HUD’s RESPA Enforcement Office at:

U.S. Department of Housing and Urban DevelopmentOffice of Consumer and Regulatory AffairsInterstate Land Sales/RESPA DivisionRoom 9146451 Seventh Street, SWWashington, DC 20410

Tel: (202) 708-4560

Fax: (202) 708-4559

Email: [email protected]

© 2005 NATIONAL ASSOCIATION OF REALTORS® 126-110All rights reserved. (10/05)

A REALTOR BenefitsSM Publication.