Embed Size (px)

Citation preview

A discussion on Inbound structuring –

Taxation, Foreign Direct Investments and

Exchange Control Regulations

24 January 2010

CA Rachana Kapadia

CA Janhavi Sharma

2

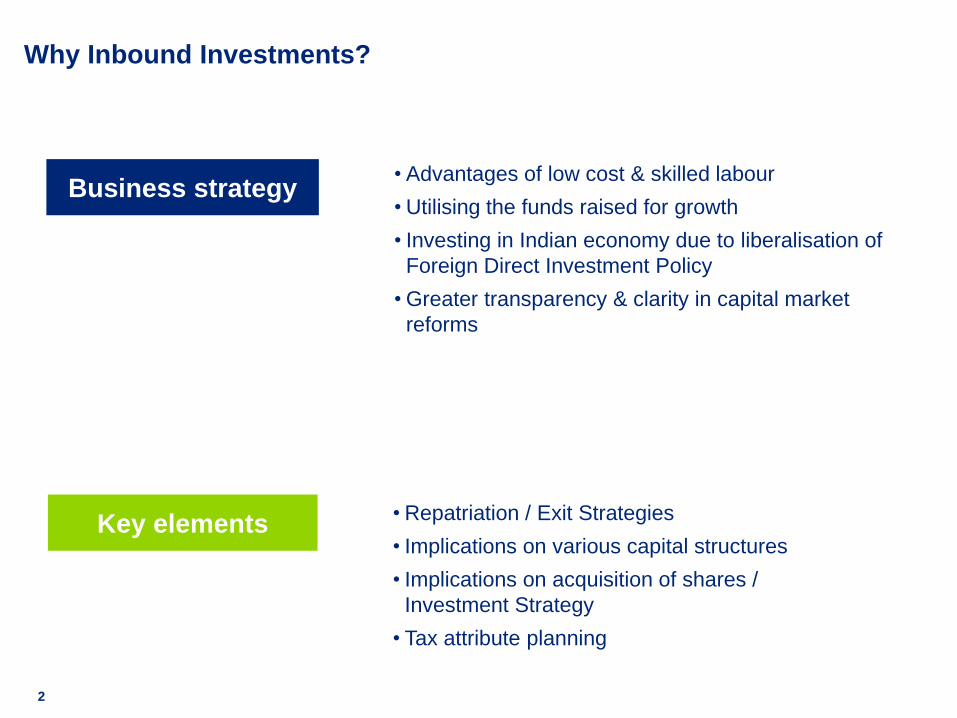

Why Inbound Investments?

• Advantages of low cost & skilled labour

• Utilising the funds raised for growth

• Investing in Indian economy due to liberalisation of

Foreign Direct Investment Policy

• Greater transparency & clarity in capital market

reforms

• Repatriation / Exit Strategies

• Implications on various capital structures

• Implications on acquisition of shares /

Investment Strategy

• Tax attribute planning

Key elements

Business strategy

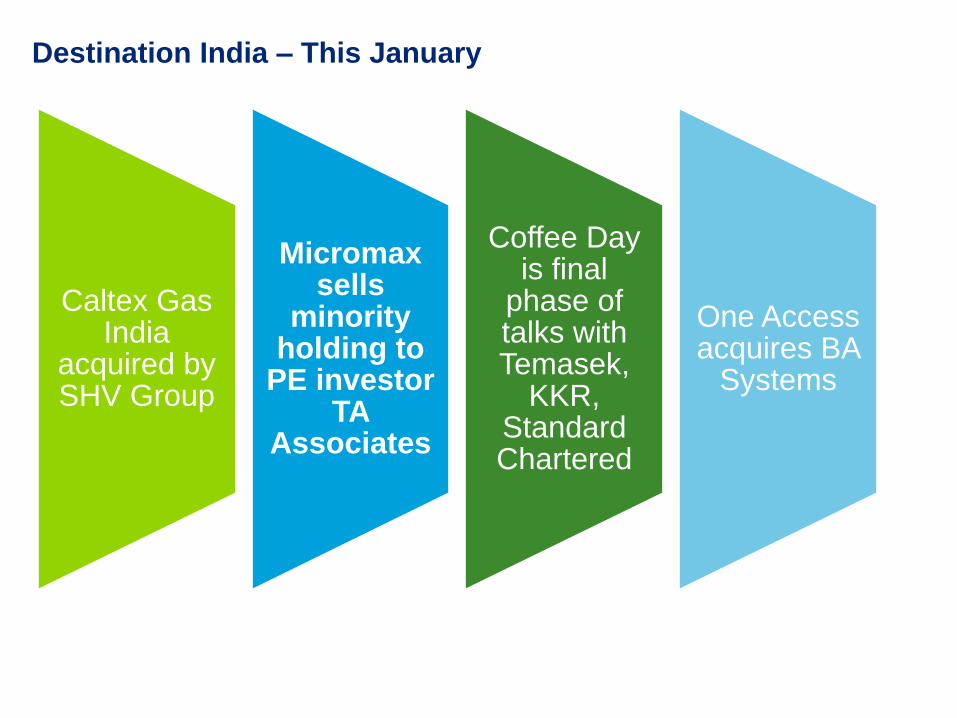

Caltex Gas India

acquired by SHV Group

Micromaxsells

minority holding to

PE investor TA

Associates

Coffee Day is final

phase of talks with Temasek,

KKR, Standard Chartered

One Access acquires BA

Systems

Destination India – This January

Contents

4

FEMA and exchange control

regulations

Recent cases

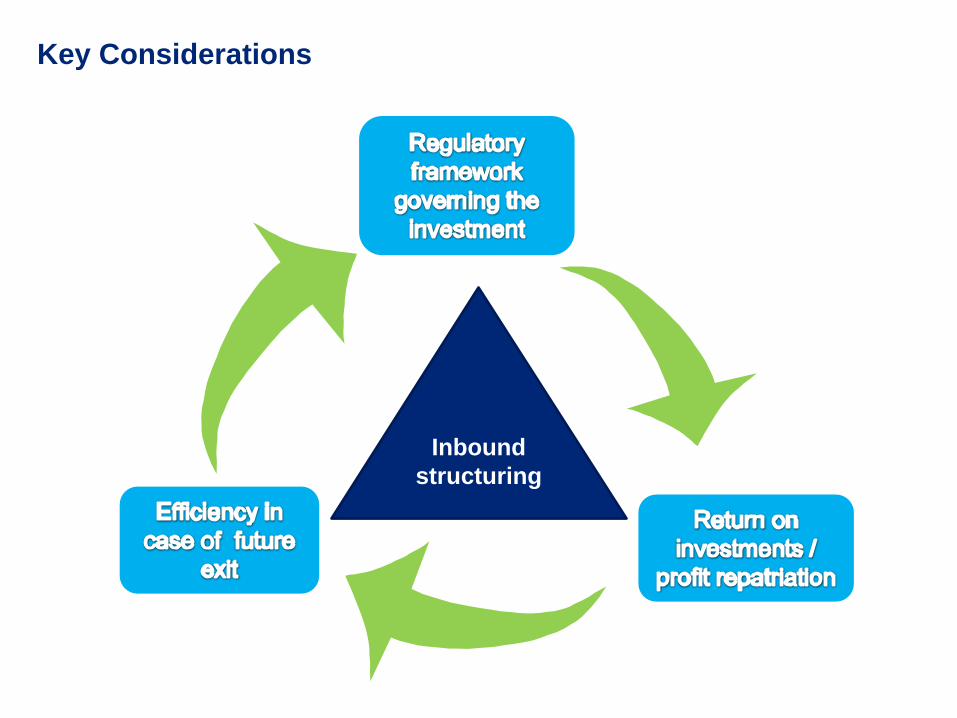

Key Considerations

Inbound

structuring

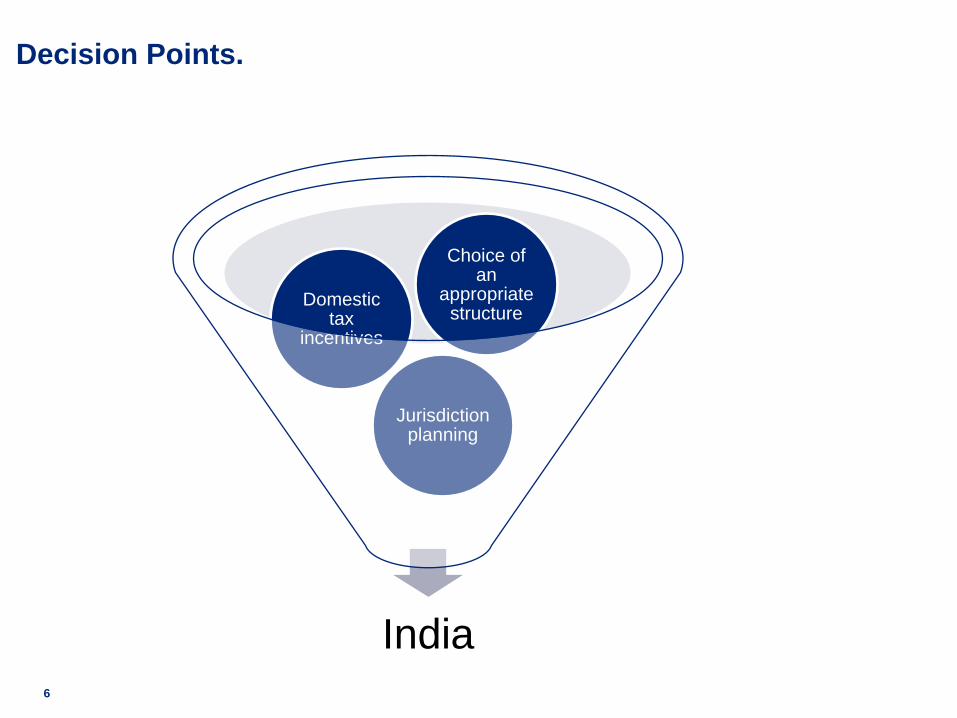

Decision Points.

India

Jurisdiction planning

Domestic tax

incentives

Choice of an

appropriate structure

6

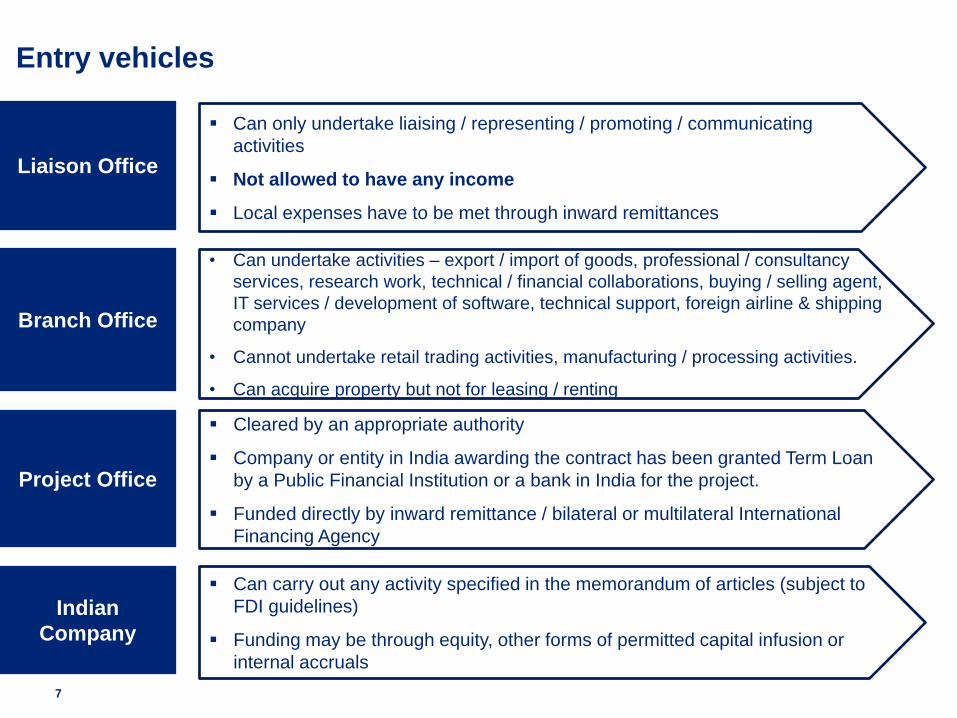

Entry vehicles

7

Liaison Office

Can only undertake liaising / representing / promoting / communicating

activities

Not allowed to have any income

Local expenses have to be met through inward remittances

Branch Office

• Can undertake activities – export / import of goods, professional / consultancy

services, research work, technical / financial collaborations, buying / selling agent,

IT services / development of software, technical support, foreign airline & shipping

company

• Cannot undertake retail trading activities, manufacturing / processing activities.

• Can acquire property but not for leasing / renting

Project Office

Cleared by an appropriate authority

Company or entity in India awarding the contract has been granted Term Loan

by a Public Financial Institution or a bank in India for the project.

Funded directly by inward remittance / bilateral or multilateral International

Financing Agency

Indian

Company

Can carry out any activity specified in the memorandum of articles (subject to

FDI guidelines)

Funding may be through equity, other forms of permitted capital infusion or

internal accruals

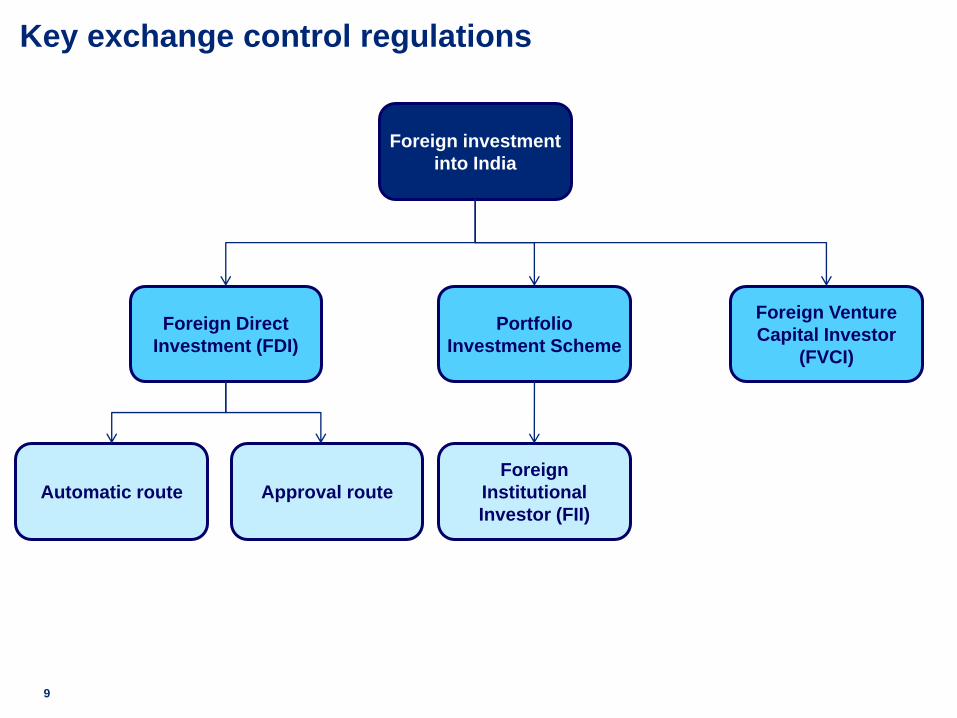

Foreign Direct Investments

9

Foreign investment

into India

Foreign Direct

Investment (FDI)

Foreign Venture

Capital Investor

(FVCI)

Foreign

Institutional

Investor (FII)

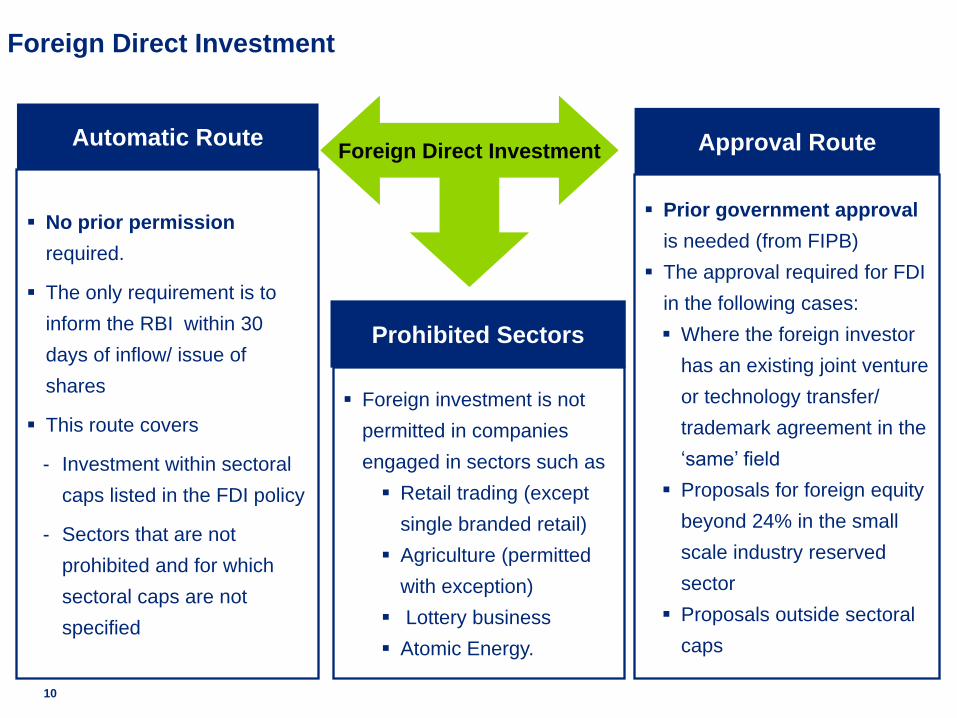

Automatic route Approval route

Key exchange control regulations

Portfolio

Investment Scheme

10

Foreign Direct Investment

Foreign Direct Investment

No prior permission

required.

The only requirement is to

inform the RBI within 30

days of inflow/ issue of

shares

This route covers

- Investment within sectoral

caps listed in the FDI policy

- Sectors that are not

prohibited and for which

sectoral caps are not

specified

Automatic Route

Prior government approval

is needed (from FIPB)

The approval required for FDI

in the following cases:

Where the foreign investor

has an existing joint venture

or technology transfer/

trademark agreement in the

‘same’ field

Proposals for foreign equity

beyond 24% in the small

scale industry reserved

sector

Proposals outside sectoral

caps

Approval Route

Foreign investment is not

permitted in companies

engaged in sectors such as

Retail trading (except

single branded retail)

Agriculture (permitted

with exception)

Lottery business

Atomic Energy.

Prohibited Sectors

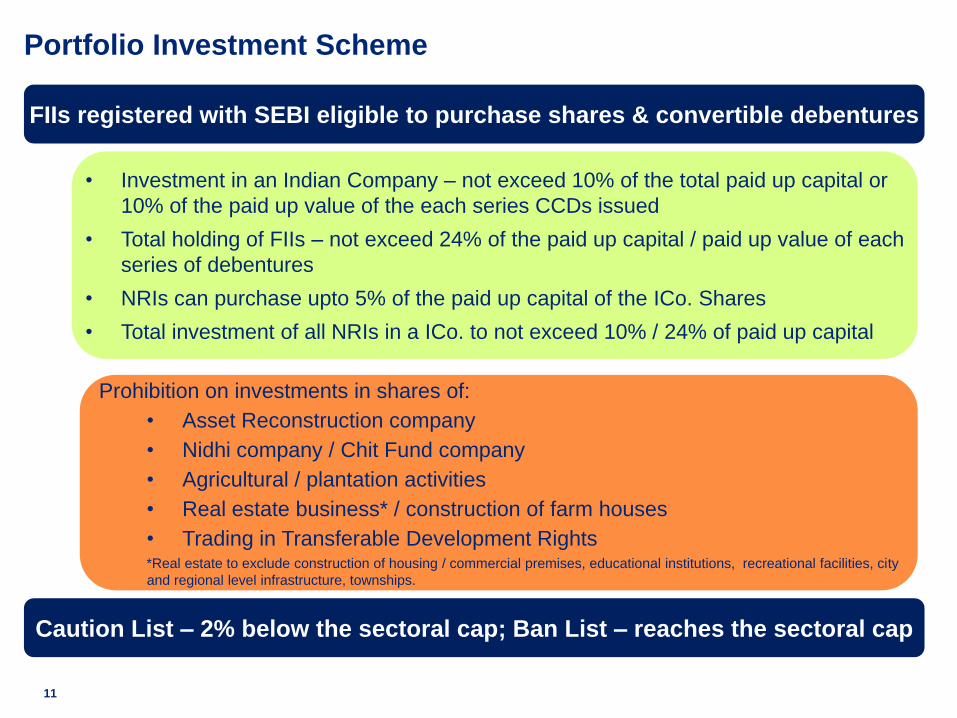

Portfolio Investment Scheme

FIIs registered with SEBI eligible to purchase shares & convertible debentures

11

• Investment in an Indian Company – not exceed 10% of the total paid up capital or

10% of the paid up value of the each series CCDs issued

• Total holding of FIIs – not exceed 24% of the paid up capital / paid up value of each

series of debentures

• NRIs can purchase upto 5% of the paid up capital of the ICo. Shares

• Total investment of all NRIs in a ICo. to not exceed 10% / 24% of paid up capital

Prohibition on investments in shares of:

• Asset Reconstruction company

• Nidhi company / Chit Fund company

• Agricultural / plantation activities

• Real estate business* / construction of farm houses

• Trading in Transferable Development Rights*Real estate to exclude construction of housing / commercial premises, educational institutions, recreational facilities, city

and regional level infrastructure, townships.

Caution List – 2% below the sectoral cap; Ban List – reaches the sectoral cap

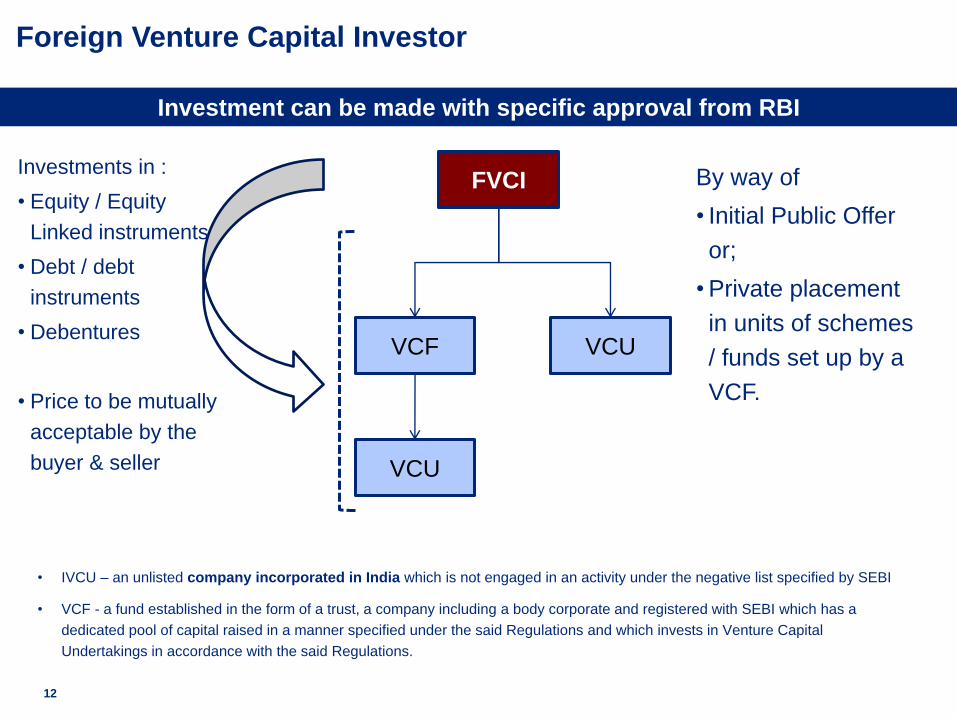

Foreign Venture Capital Investor

• IVCU – an unlisted company incorporated in India which is not engaged in an activity under the negative list specified by SEBI

• VCF - a fund established in the form of a trust, a company including a body corporate and registered with SEBI which has a

dedicated pool of capital raised in a manner specified under the said Regulations and which invests in Venture Capital

Undertakings in accordance with the said Regulations.

12

FVCI

VCU

VCF VCU

Investments in :

• Equity / Equity

Linked instruments

• Debt / debt

instruments

• Debentures

• Price to be mutually

acceptable by the

buyer & seller

Investment can be made with specific approval from RBI

By way of

• Initial Public Offer

or;

• Private placement

in units of schemes

/ funds set up by a

VCF.

13

Fema and Exchange Control Regulations

Funding for the investment

14

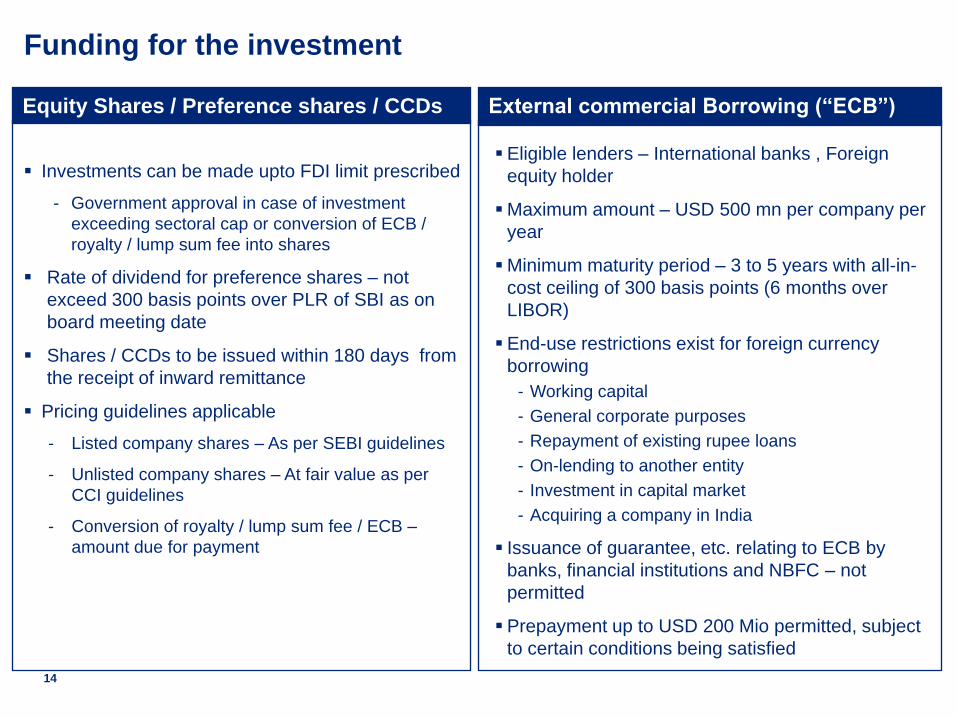

Equity Shares / Preference shares / CCDs

Investments can be made upto FDI limit prescribed

- Government approval in case of investment

exceeding sectoral cap or conversion of ECB /

royalty / lump sum fee into shares

Rate of dividend for preference shares – not

exceed 300 basis points over PLR of SBI as on

board meeting date

Shares / CCDs to be issued within 180 days from

the receipt of inward remittance

Pricing guidelines applicable

- Listed company shares – As per SEBI guidelines

- Unlisted company shares – At fair value as per

CCI guidelines

- Conversion of royalty / lump sum fee / ECB –

amount due for payment

External commercial Borrowing (“ECB”)

Eligible lenders – International banks , Foreign

equity holder

Maximum amount – USD 500 mn per company per

year

Minimum maturity period – 3 to 5 years with all-in-

cost ceiling of 300 basis points (6 months over

LIBOR)

End-use restrictions exist for foreign currency

borrowing

- Working capital

- General corporate purposes

- Repayment of existing rupee loans

- On-lending to another entity

- Investment in capital market

- Acquiring a company in India

Issuance of guarantee, etc. relating to ECB by

banks, financial institutions and NBFC – not

permitted

Prepayment up to USD 200 Mio permitted, subject

to certain conditions being satisfied

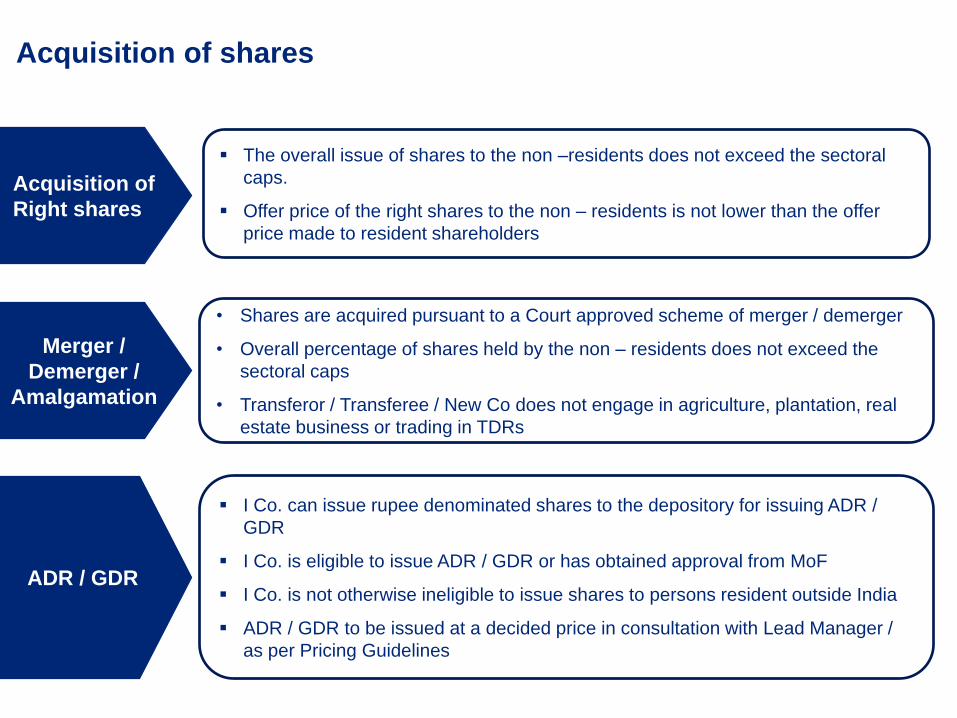

Acquisition of shares

Acquisition of

Right shares

The overall issue of shares to the non –residents does not exceed the sectoral

caps.

Offer price of the right shares to the non – residents is not lower than the offer

price made to resident shareholders

Merger /

Demerger /

Amalgamation

• Shares are acquired pursuant to a Court approved scheme of merger / demerger

• Overall percentage of shares held by the non – residents does not exceed the

sectoral caps

• Transferor / Transferee / New Co does not engage in agriculture, plantation, real

estate business or trading in TDRs

ADR / GDR

I Co. can issue rupee denominated shares to the depository for issuing ADR /

GDR

I Co. is eligible to issue ADR / GDR or has obtained approval from MoF

I Co. is not otherwise ineligible to issue shares to persons resident outside India

ADR / GDR to be issued at a decided price in consultation with Lead Manager /

as per Pricing Guidelines

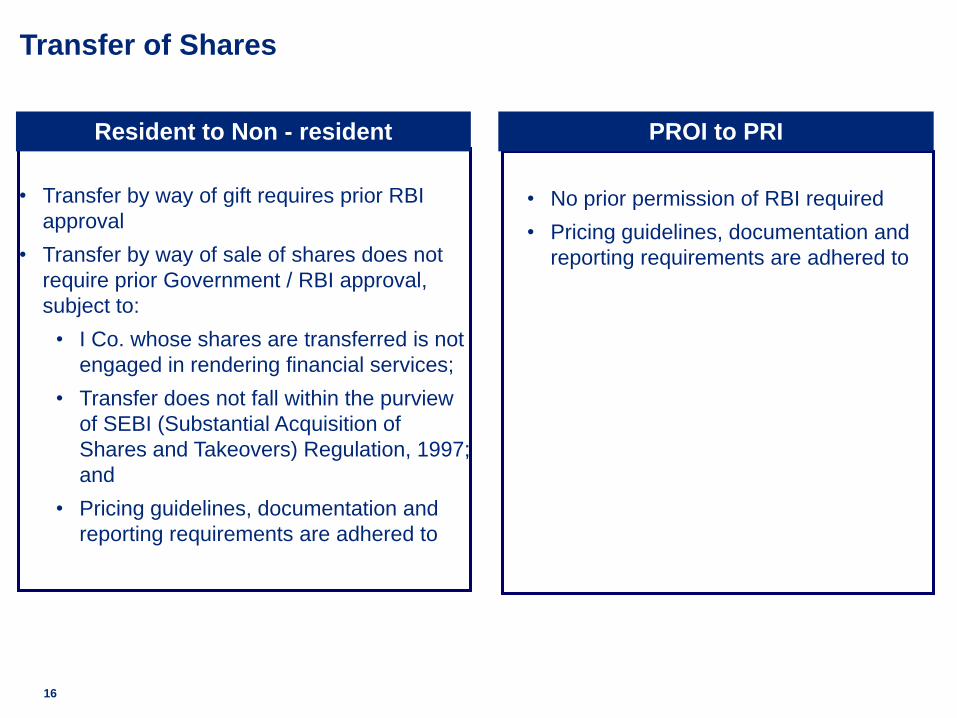

Transfer of Shares

• Transfer by way of gift requires prior RBI

approval

• Transfer by way of sale of shares does not

require prior Government / RBI approval,

subject to:

• I Co. whose shares are transferred is not

engaged in rendering financial services;

• Transfer does not fall within the purview

of SEBI (Substantial Acquisition of

Shares and Takeovers) Regulation, 1997;

and

• Pricing guidelines, documentation and

reporting requirements are adhered to

16

• No prior permission of RBI required

• Pricing guidelines, documentation and

reporting requirements are adhered to

Resident to Non - resident PROI to PRI

17

Press Notes 2, 3 & 4 (2009 series)

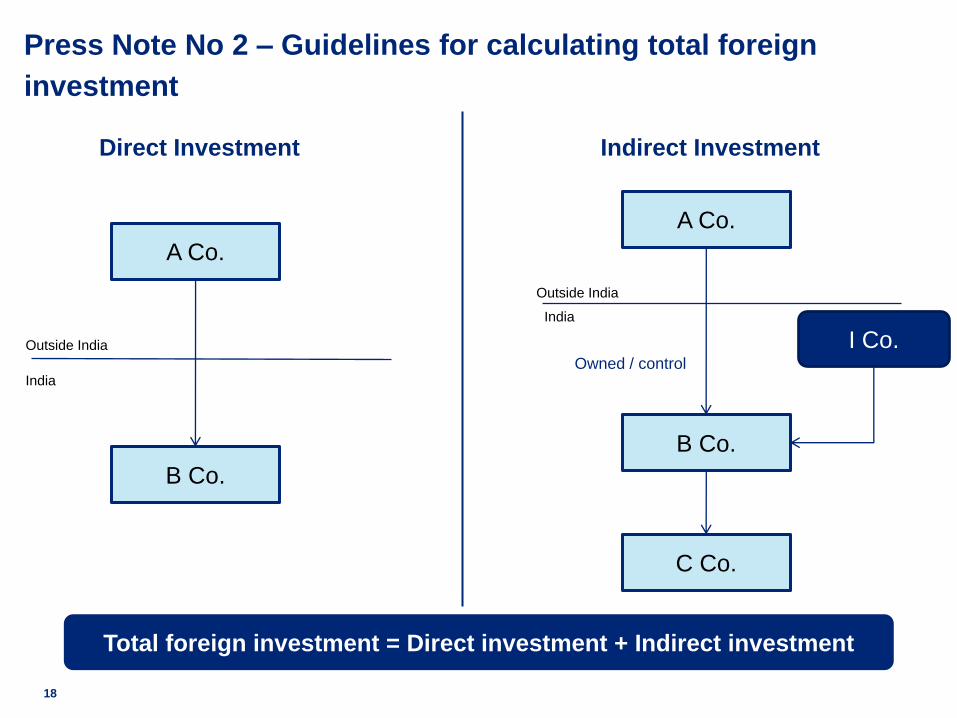

Press Note No 2 – Guidelines for calculating total foreign

investment

18

A Co.

B Co.

India

Outside India

Direct Investment

A Co.

B Co.

India

Outside India

Indirect Investment

C Co.

I Co.

Total foreign investment = Direct investment + Indirect investment

Owned & control

Owned / control

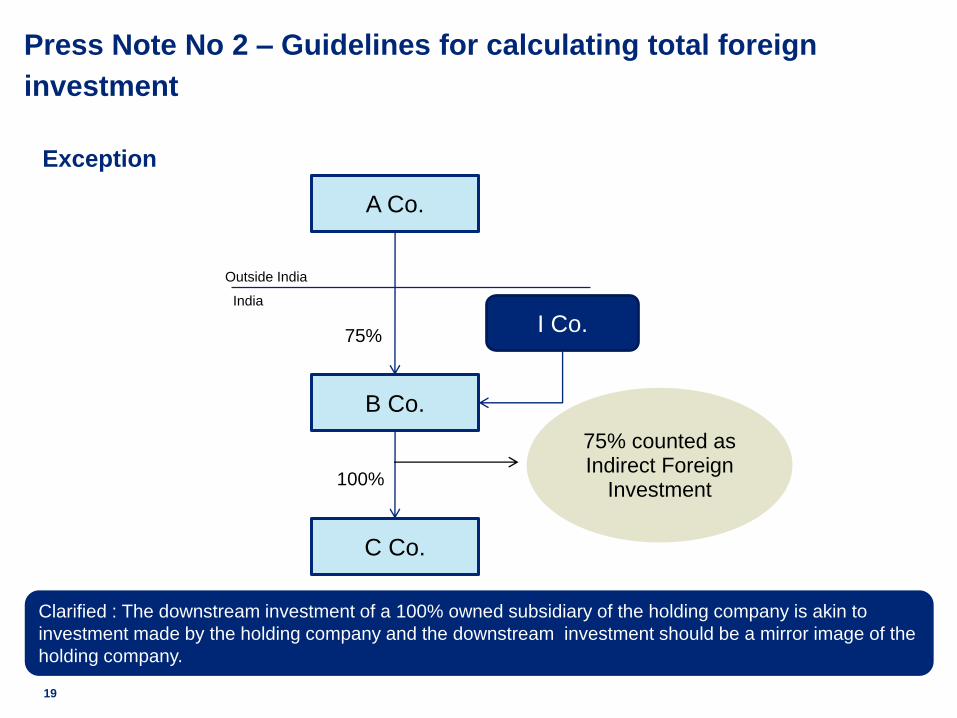

Press Note No 2 – Guidelines for calculating total foreign

investment

Exception

19

A Co.

B Co.

India

Outside India

C Co.

I Co.75%

100%

75% counted as Indirect Foreign

Investment

Clarified : The downstream investment of a 100% owned subsidiary of the holding company is akin to

investment made by the holding company and the downstream investment should be a mirror image of the

holding company.

Press Note No 2 – Guidelines for calculating total foreign

investment

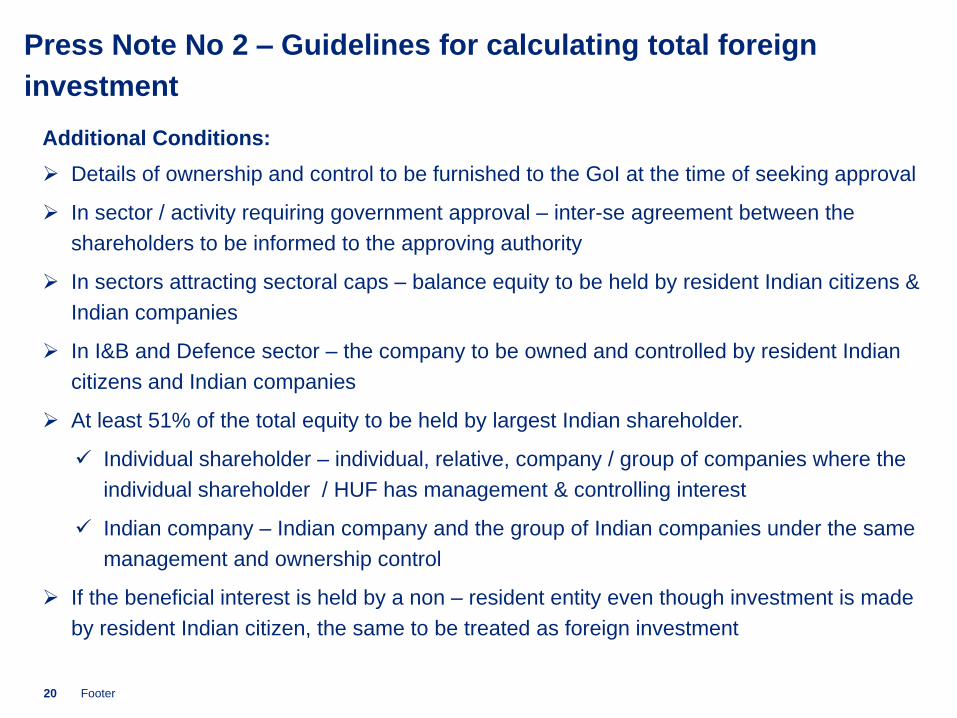

Additional Conditions:

Details of ownership and control to be furnished to the GoI at the time of seeking approval

In sector / activity requiring government approval – inter-se agreement between the

shareholders to be informed to the approving authority

In sectors attracting sectoral caps – balance equity to be held by resident Indian citizens &

Indian companies

In I&B and Defence sector – the company to be owned and controlled by resident Indian

citizens and Indian companies

At least 51% of the total equity to be held by largest Indian shareholder.

Individual shareholder – individual, relative, company / group of companies where the

individual shareholder / HUF has management & controlling interest

Indian company – Indian company and the group of Indian companies under the same

management and ownership control

If the beneficial interest is held by a non – resident entity even though investment is made

by resident Indian citizen, the same to be treated as foreign investment

20 Footer

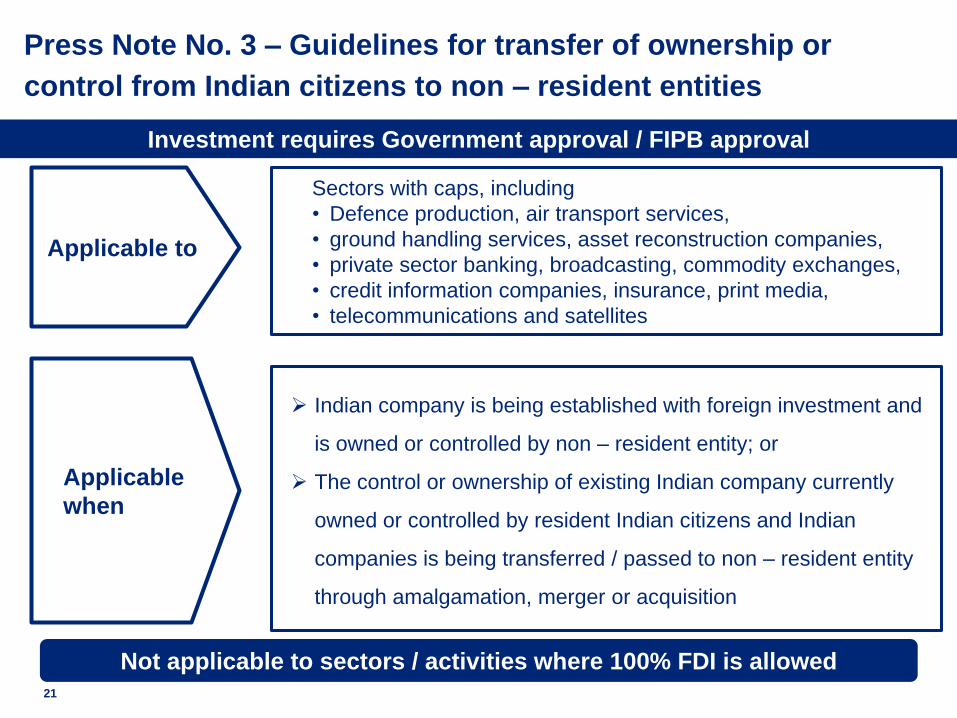

Press Note No. 3 – Guidelines for transfer of ownership or

control from Indian citizens to non – resident entities

21

Applicable to

Applicable

when

Sectors with caps, including

• Defence production, air transport services,

• ground handling services, asset reconstruction companies,

• private sector banking, broadcasting, commodity exchanges,

• credit information companies, insurance, print media,

• telecommunications and satellites

Indian company is being established with foreign investment and

is owned or controlled by non – resident entity; or

The control or ownership of existing Indian company currently

owned or controlled by resident Indian citizens and Indian

companies is being transferred / passed to non – resident entity

through amalgamation, merger or acquisition

Investment requires Government approval / FIPB approval

Not applicable to sectors / activities where 100% FDI is allowed

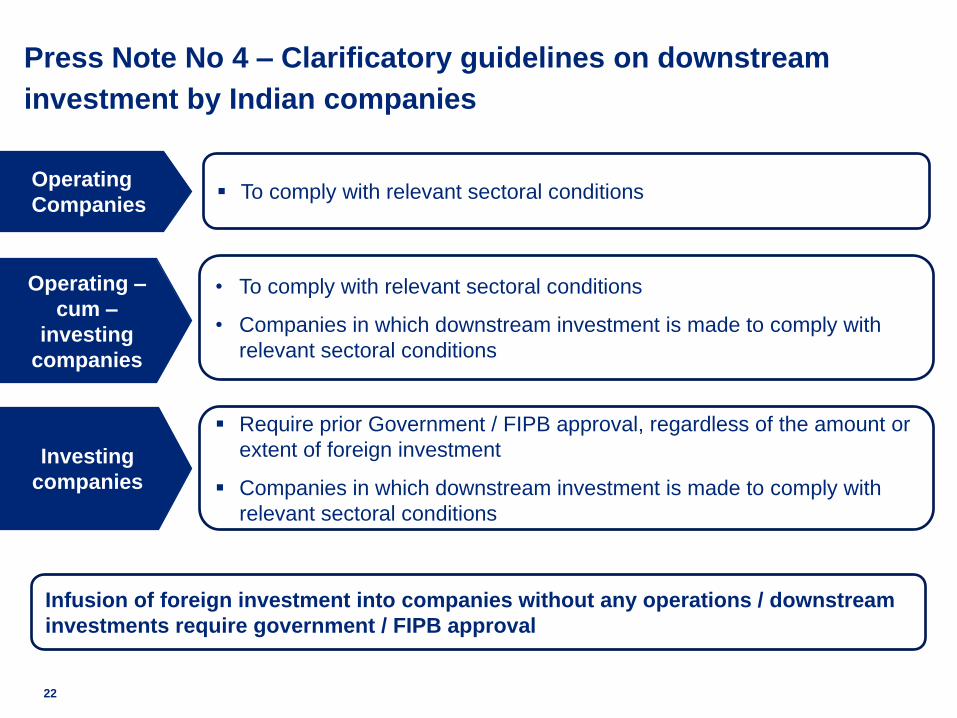

Press Note No 4 – Clarificatory guidelines on downstream

investment by Indian companies

22

Operating

Companies To comply with relevant sectoral conditions

Operating –

cum –

investing

companies

• To comply with relevant sectoral conditions

• Companies in which downstream investment is made to comply with

relevant sectoral conditions

Investing

companies

Require prior Government / FIPB approval, regardless of the amount or

extent of foreign investment

Companies in which downstream investment is made to comply with

relevant sectoral conditions

Infusion of foreign investment into companies without any operations / downstream

investments require government / FIPB approval

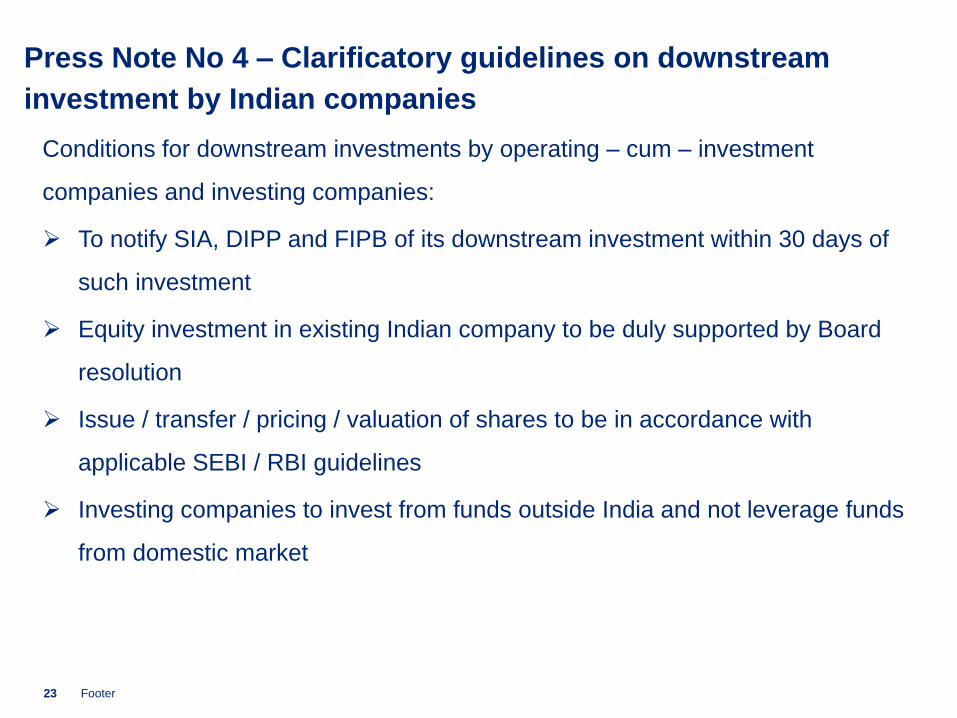

Press Note No 4 – Clarificatory guidelines on downstream

investment by Indian companies

Conditions for downstream investments by operating – cum – investment

companies and investing companies:

To notify SIA, DIPP and FIPB of its downstream investment within 30 days of

such investment

Equity investment in existing Indian company to be duly supported by Board

resolution

Issue / transfer / pricing / valuation of shares to be in accordance with

applicable SEBI / RBI guidelines

Investing companies to invest from funds outside India and not leverage funds

from domestic market

23 Footer

24

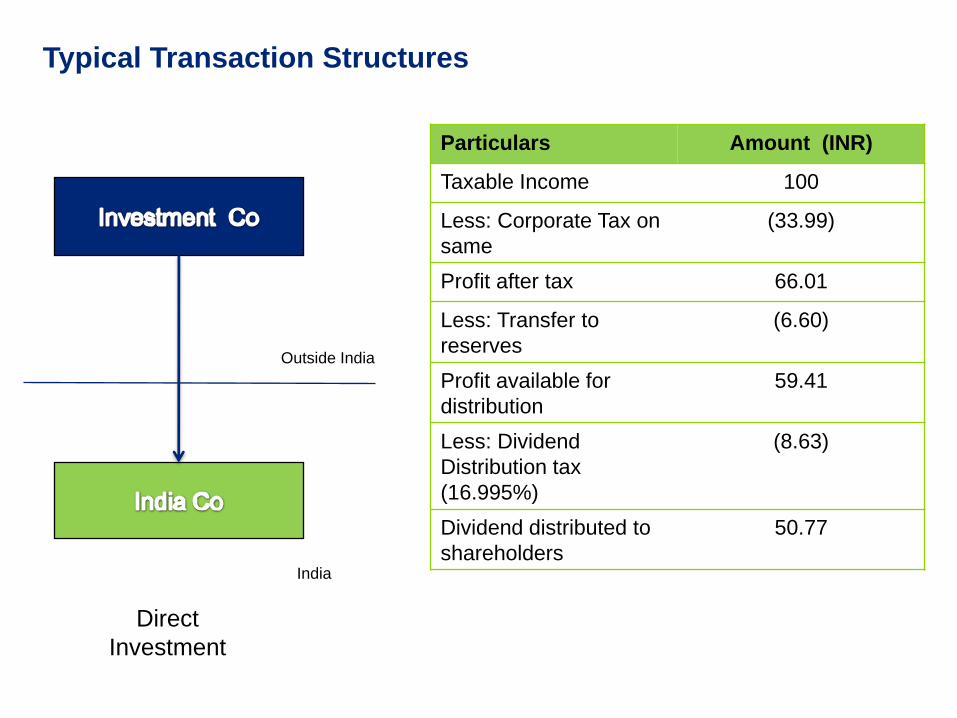

Direct Tax Implications

Typical Transaction Structures

Particulars Amount (INR)

Taxable Income 100

Less: Corporate Tax on

same

(33.99)

Profit after tax 66.01

Less: Transfer to

reserves

(6.60)

Profit available for

distribution

59.41

Less: Dividend

Distribution tax

(16.995%)

(8.63)

Dividend distributed to

shareholders

50.77

Direct

Investment

Outside India

India

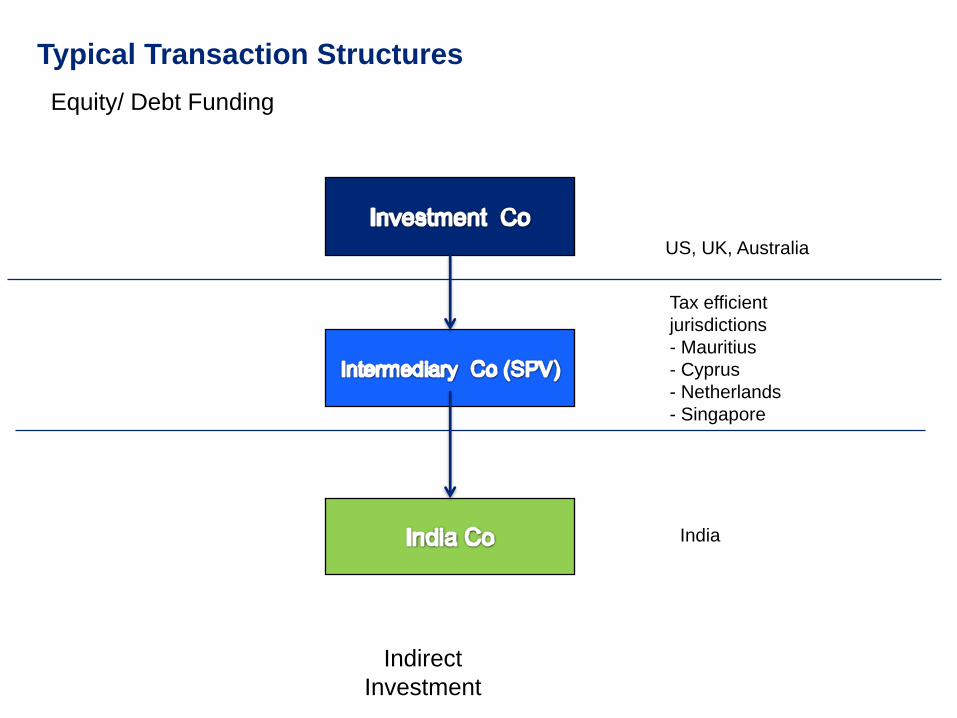

Typical Transaction Structures

Tax efficient

jurisdictions

- Mauritius

- Cyprus

- Netherlands

- Singapore

US, UK, Australia

India

Equity/ Debt Funding

Indirect

Investment

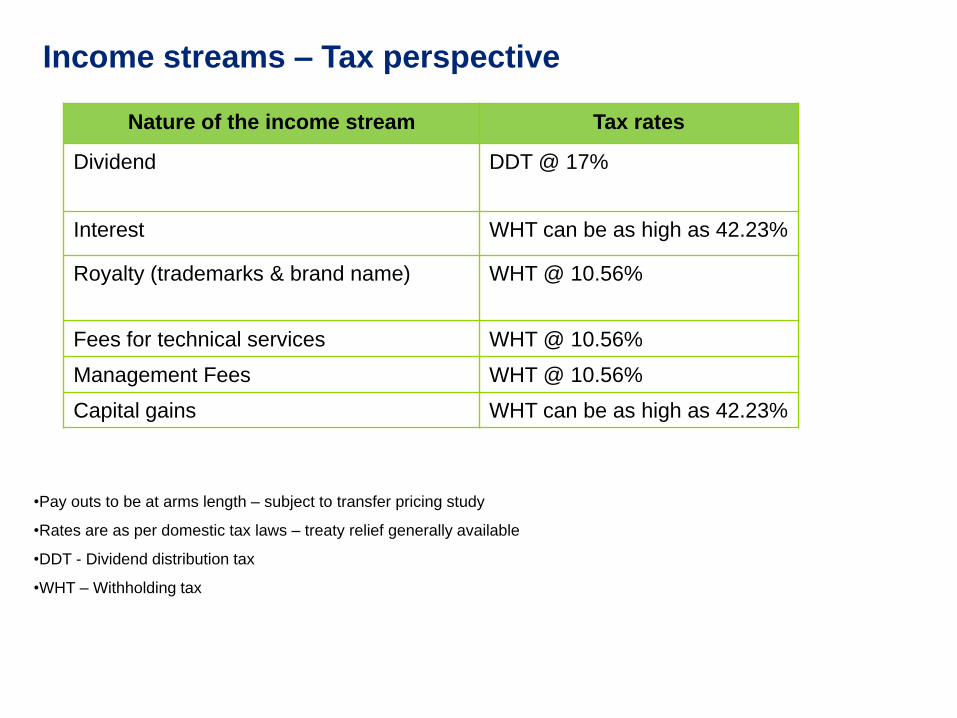

Nature of the income stream Tax rates

Dividend DDT @ 17%

Interest WHT can be as high as 42.23%

Royalty (trademarks & brand name) WHT @ 10.56%

Fees for technical services WHT @ 10.56%

Management Fees WHT @ 10.56%

Capital gains WHT can be as high as 42.23%

Income streams – Tax perspective

•Pay outs to be at arms length – subject to transfer pricing study

•Rates are as per domestic tax laws – treaty relief generally available

•DDT - Dividend distribution tax

•WHT – Withholding tax

Tax Treaty Provisions

• Indian Government has entered into agreement (Double Taxation

Avoidance Agreement/ Treaty Agreements) with Governments of

various other countries/contracting state

• Treaties often provide lower tax rates and exemptions in addition

to those available under the domestic tax provisions

• A non-resident may choose to be governed by the domestic tax

provisions or provisions under the treaty whichever are more

beneficial

• A person is entitled to claim application of treaty provisions only if

he is a tax resident of either of the country/contracting state.

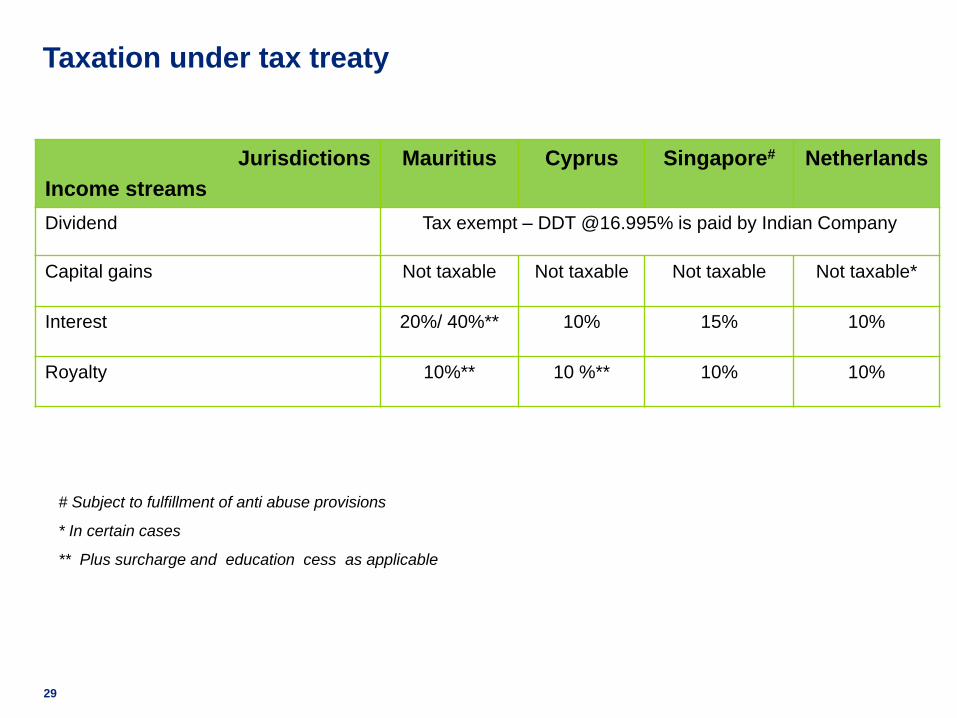

29

Jurisdictions

Income streams

Mauritius Cyprus Singapore# Netherlands

Dividend Tax exempt – DDT @16.995% is paid by Indian Company

Capital gains Not taxable Not taxable Not taxable Not taxable*

Interest 20%/ 40%** 10% 15% 10%

Royalty 10%** 10 %** 10% 10%

# Subject to fulfillment of anti abuse provisions

* In certain cases

** Plus surcharge and education cess as applicable

Taxation under tax treaty

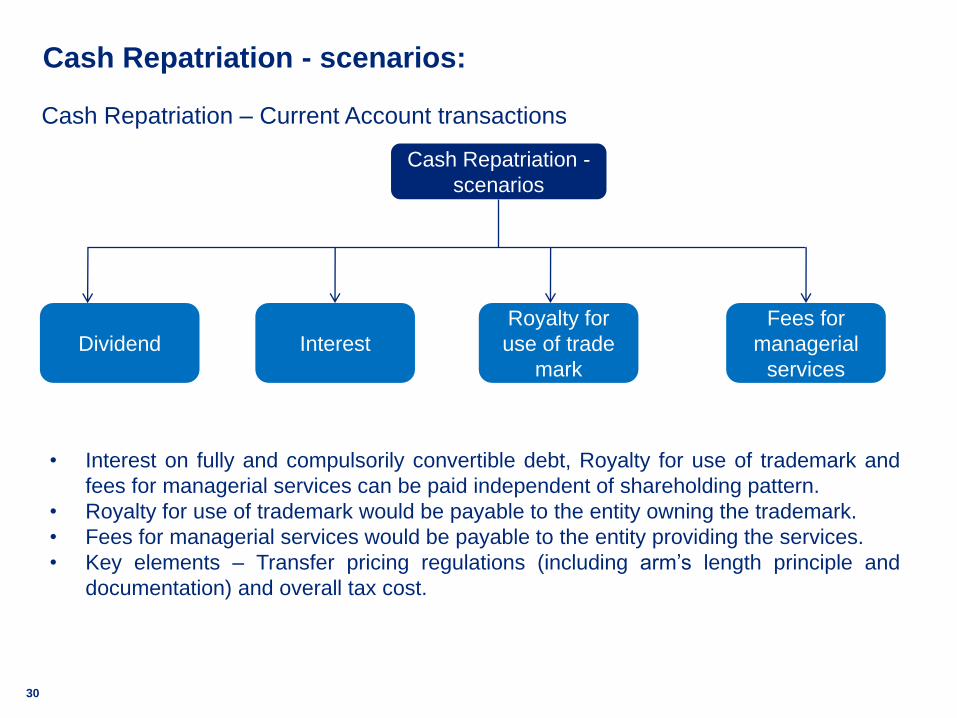

Cash Repatriation - scenarios:

30

Cash Repatriation -

scenarios

Dividend Interest

Royalty for

use of trade

mark

Fees for

managerial

services

• Interest on fully and compulsorily convertible debt, Royalty for use of trademark and

fees for managerial services can be paid independent of shareholding pattern.

• Royalty for use of trademark would be payable to the entity owning the trademark.

• Fees for managerial services would be payable to the entity providing the services.

• Key elements – Transfer pricing regulations (including arm’s length principle and

documentation) and overall tax cost.

Cash Repatriation – Current Account transactions

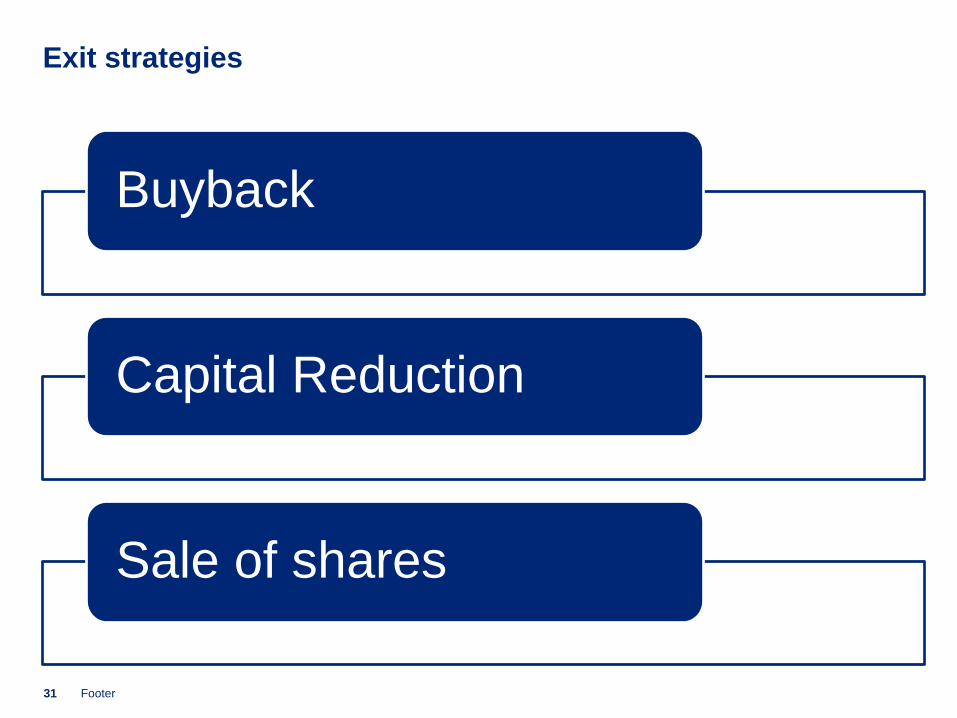

Exit strategies

Buyback

Capital Reduction

Sale of shares

31 Footer

Case study

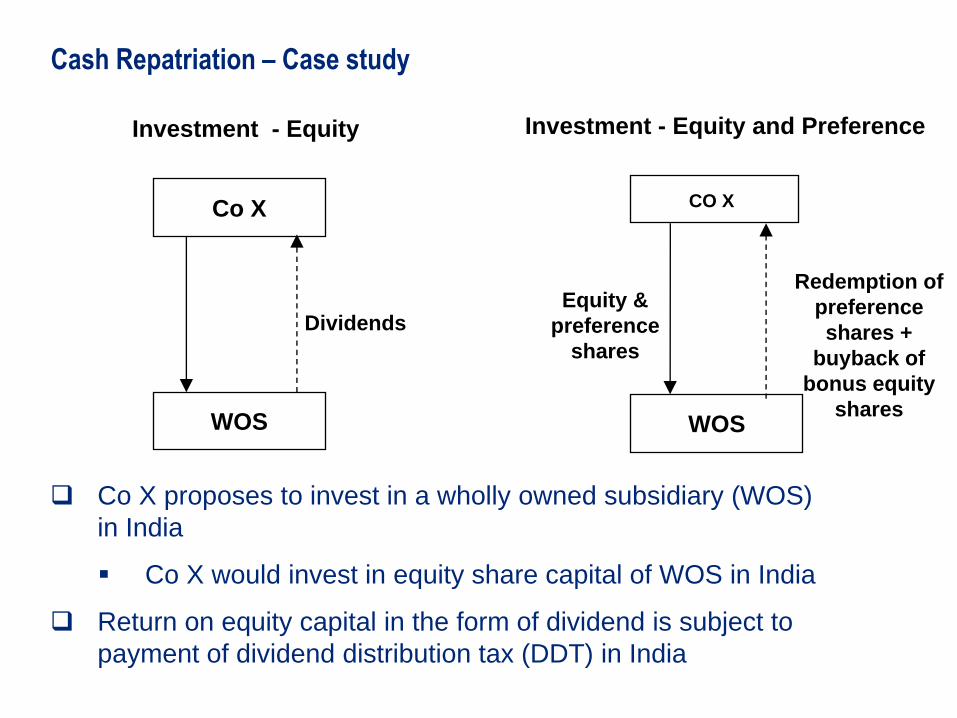

Investment - Equity

Co X

WOSEquity

shares

Dividends

CO X

WOS

Equity &

preference

shares

Redemption of

preference

shares +

buyback of

bonus equity

shares

Investment - Equity and Preference

Cash Repatriation – Case study

Co X proposes to invest in a wholly owned subsidiary (WOS)

in India

Co X would invest in equity share capital of WOS in India

Return on equity capital in the form of dividend is subject to

payment of dividend distribution tax (DDT) in India

02/5/

2010

34

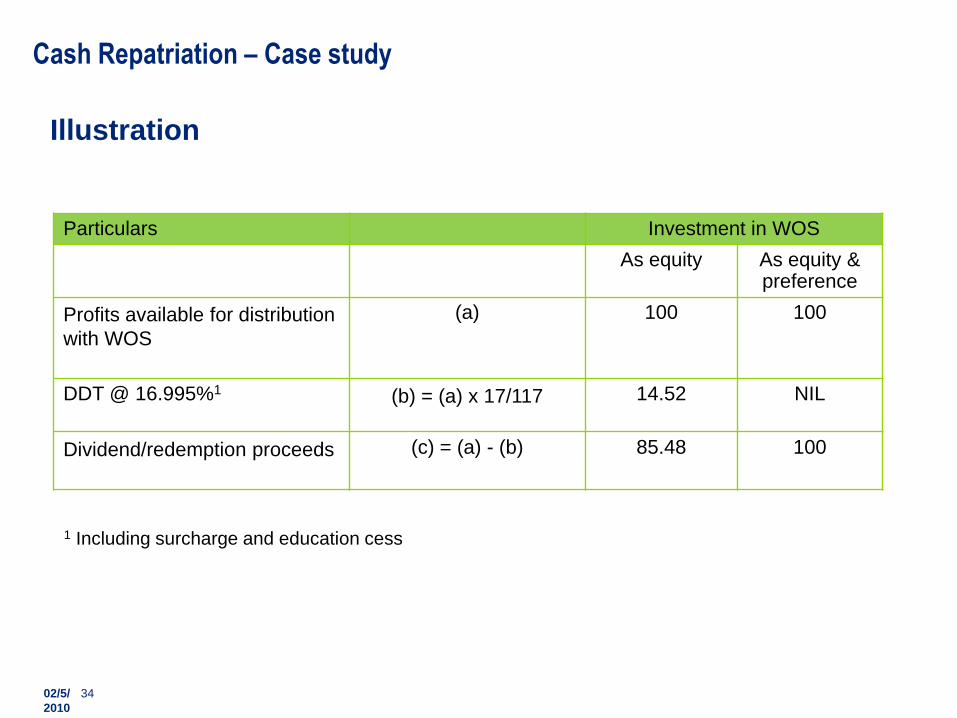

Particulars Investment in WOS

As equity As equity & preference

Profits available for distribution

with WOS

(a) 100 100

DDT @ 16.995%1 (b) = (a) x 17/117 14.52 NIL

Dividend/redemption proceeds (c) = (a) - (b) 85.48 100

Illustration

1 Including surcharge and education cess

Cash Repatriation – Case study

QUESTIONS??

Thank you

![SELLING INBOUND: TRANSFORM YOUR REP'S INBOUND SELLING SKILLS [INBOUND 2014]](https://img.pdfslide.us/doc/110x75/55d54cf8bb61ebdb228b46ca/selling-inbound-transform-your-reps-inbound-selling-skills-inbound.jpg)