Embed Size (px)

Citation preview

A Discussion of "The Transmission of MonetaryPolicy through Banks’Balance Sheets"

Anthony Brassil, Jon Cheshire, Joseph Muscatello

Discussant: Aarti Singh (USyd)

April 12, 2018

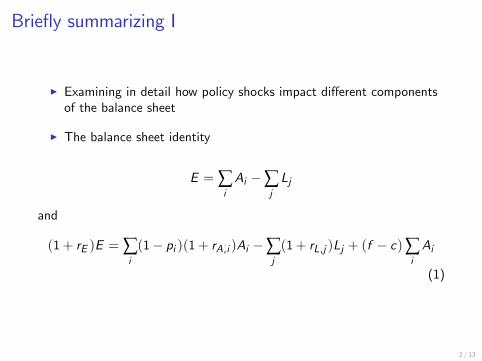

Briefly summarizing I

I Examining in detail how policy shocks impact different componentsof the balance sheet

I The balance sheet identity

E = ∑iAi −∑

jLj

and

(1+ rE )E = ∑i(1− pi )(1+ rA,i )Ai −∑

j(1+ rL,j )Lj + (f − c)∑

iAi

(1)

2 / 13

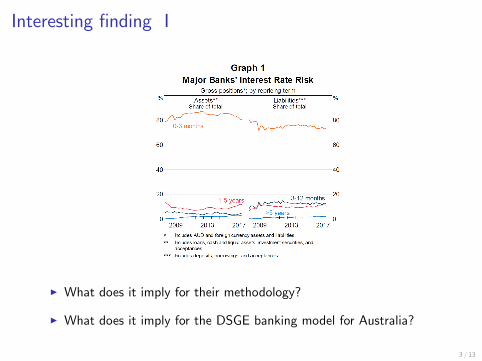

Interesting finding I

I What does it imply for their methodology?

I What does it imply for the DSGE banking model for Australia?

3 / 13

Interesting finding II

I imperfect competition in the banking sector; no re-pricing friction (asmaturity mismatch doesn’t matter for Australia)

I policy shocks are not attenuated by the banking sector

I are we back in the Gertler and Karadi (2011) world where monetarypolicy shocks are amplified by the banking sector?

4 / 13

Non-discretionary items on the balance sheet I

I Provisions: incomplete pass through, 100 basis put cut in the cashrate reduces annual provision rates by 7 basis points

I Wholesale debt markets: complete pass through

I No/low interest rate deposits: spreads change one-for-one

I Non-loan assets: full pass through

I Conclusion: almost complete pass-though of cash rate changes todiscretionary components

5 / 13

Lending rates and deposit rates: incomplete pass-through I

I ROE: not changed much in spite of falling cash rates

I Balance sheet identity implies even incomplete pass through todiscretionary components of the balance sheet

I Main finding: deviation of 7 basis point from full pass through whenoffset by both lending and deposit rate; 11 when offset by lendingrate alone....

I Welfare implication; loss in savings?

I Suggestion: time series analysis

6 / 13

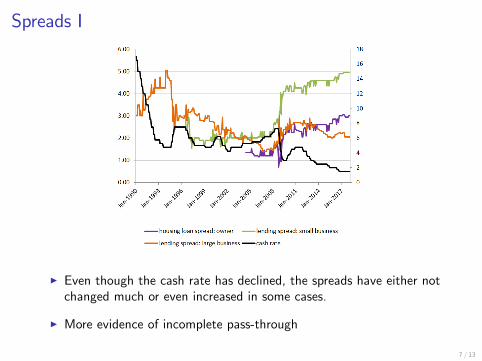

Spreads I

I Even though the cash rate has declined, the spreads have either notchanged much or even increased in some cases.

I More evidence of incomplete pass-through

7 / 13

Mark-ups and mark-downs I

I Imperfect competition in the banking sector implies that banks willcharge interest rates that are a mark-up over their marginal cost

rL = µLRL = µLrc

rA = µARA = µA [(1− λ)RL + λrτ ]

I For the 2007-2016 period, µL = 0.92.

I And assuming λ = 0.25, rτ = 8%, µA = 1.47

8 / 13

Competition in the banking sector I

I "What Drives Bank Competition? Some International Evidence"Claessens, S. and L. Laeven. (2004) Journal of Money, Credit, andBanking

I 50 countries, 1994-2001

I PR H-statistic: H<0 indicates monopoly, H=1 indicates perfectcompetition and 0<H<1indicates monopolistic competition

9 / 13

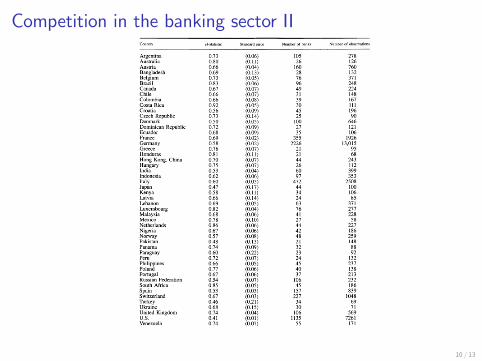

Competition in the banking sector II

10 / 13

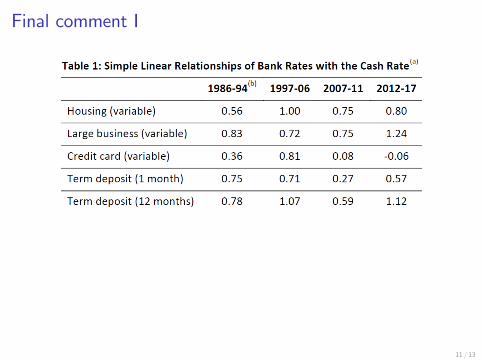

Final comment I

11 / 13

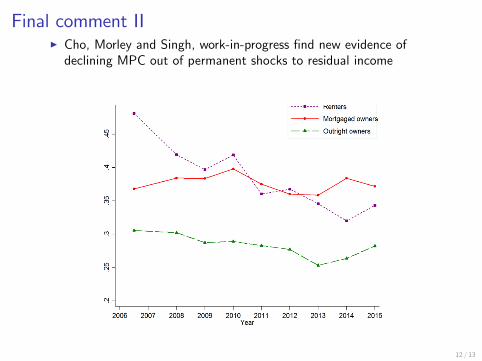

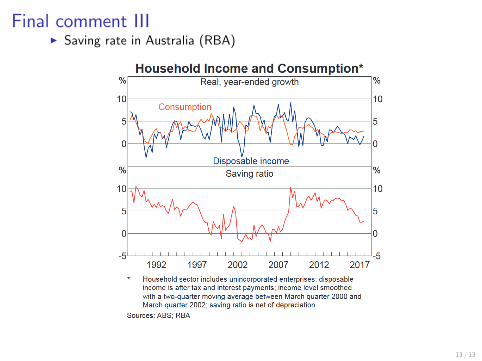

Final comment III Cho, Morley and Singh, work-in-progress find new evidence ofdeclining MPC out of permanent shocks to residual income

12 / 13

Final comment IIII Saving rate in Australia (RBA)

13 / 13