Embed Size (px)

Citation preview

ACloser Look

By Brian Hays and Kris Kesling -Hays

Lic Real Estate Broker Lic Mortgage Broker

Lic Mortgage Broker

Talking points Who are Brian & Kris Hays?

• Loan origination in Today’s Market• What differentiates a Mortgage Broker from

other types of “lenders”? • What training is required as a mortgage broker?• What do Mortgage Brokers do?• How do mortgage brokers earn their income?• Different Loan Programs• Scenario workshop

• www.Prefhomes.netwww.preferredpropertiesofsarasota.com

• FOR BUYERS· • Our Listings · • MLS Search ·

• Dream Home

• Loan Application (en) · • Loan Application (sp) ·

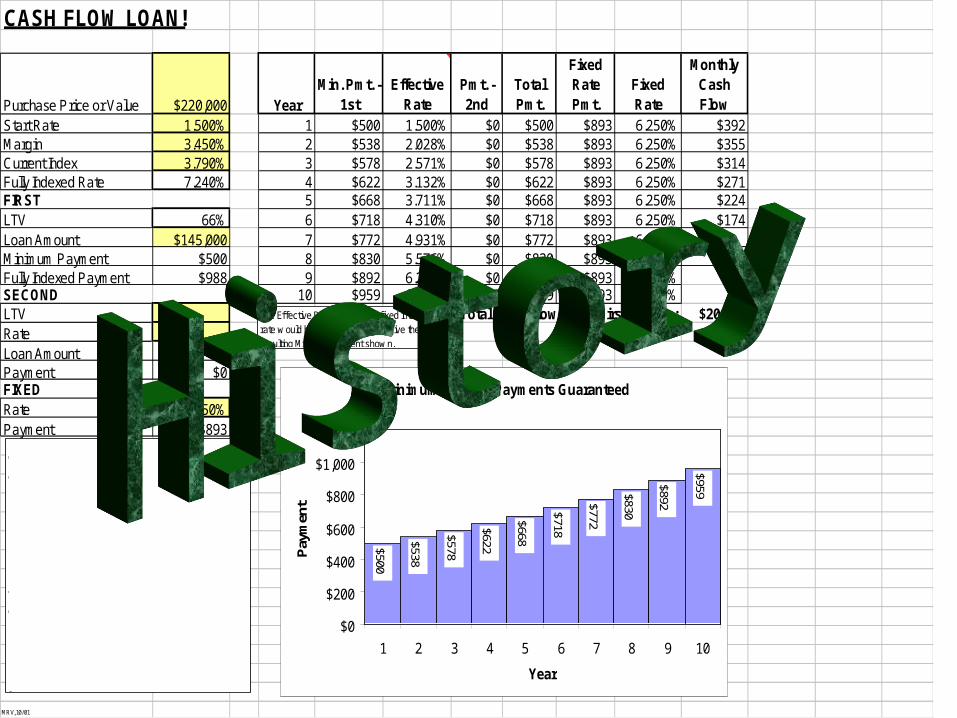

CASH FLOW LOAN!

Purchase Price or Value $220,000 YearMin. Pmt. -

1stEffective

RatePmt. - 2nd

Total Pmt.

Fixed Rate Pmt.

Fixed Rate

Monthly Cash Flow

Start Rate 1.500% 1 $500 1.500% $0 $500 $893 6.250% $392Margin 3.450% 2 $538 2.028% $0 $538 $893 6.250% $355Current Index 3.790% 3 $578 2.571% $0 $578 $893 6.250% $314Fully Indexed Rate 7.240% 4 $622 3.132% $0 $622 $893 6.250% $271FIRST 5 $668 3.711% $0 $668 $893 6.250% $224LTV 66% 6 $718 4.310% $0 $718 $893 6.250% $174Loan Amount $145,000 7 $772 4.931% $0 $772 $893 6.250%Minimum Payment $500 8 $830 5.576% $0 $830 $893 6.250%Fully Indexed Payment $988 9 $892 6.247% $0 $892 $893 6.250%SECOND 10 $959 6.946% $0 $959 $893 6.250%LTV Total Cash Flow in the First 8 Years: $20,780RateLoan Amount $0Payment $0FIXEDRate 6.250%Payment $893

MRV, 10/01

The Effective Rate is w hat the fixed interest rate w ould have to be in order to give the resulting Minimum Payment show n.

4 Payment Options from Month to Month: * Minimum Payment* Interest Only Payment* 30 Year Payment* 15 Year Payment

Equity Builder Bi-weekly Payment Option:* Auto. Draft 1/2 the minimum monthly payment every 2 weeks.* Reduces the life of the loan by 7 to 11 years.

Minimum Monthly Payments Guaranteed

$500

$538

$578

$622

$668

$718

$772

$830

$892

$959

$0

$200

$400

$600

$800

$1,000

$1,200

1 2 3 4 5 6 7 8 9 10

Year

Pay

men

t

CASH FLOW LOAN!

Purchase Price or Value $220,000 YearMin. Pmt. -

1stEffective

RatePmt. - 2nd

Total Pmt.

Fixed Rate Pmt.

Fixed Rate

Monthly Cash Flow

Start Rate 1.500% 1 $500 1.500% $0 $500 $893 6.250% $392Margin 3.450% 2 $538 2.028% $0 $538 $893 6.250% $355Current Index 3.790% 3 $578 2.571% $0 $578 $893 6.250% $314Fully Indexed Rate 7.240% 4 $622 3.132% $0 $622 $893 6.250% $271FIRST 5 $668 3.711% $0 $668 $893 6.250% $224LTV 66% 6 $718 4.310% $0 $718 $893 6.250% $174Loan Amount $145,000 7 $772 4.931% $0 $772 $893 6.250%Minimum Payment $500 8 $830 5.576% $0 $830 $893 6.250%Fully Indexed Payment $988 9 $892 6.247% $0 $892 $893 6.250%SECOND 10 $959 6.946% $0 $959 $893 6.250%LTV Total Cash Flow in the First 8 Years: $20,780RateLoan Amount $0Payment $0FIXEDRate 6.250%Payment $893

MRV, 10/01

The Effective Rate is w hat the fixed interest rate w ould have to be in order to give the resulting Minimum Payment show n.

4 Payment Options from Month to Month: * Minimum Payment* Interest Only Payment* 30 Year Payment* 15 Year Payment

Equity Builder Bi-weekly Payment Option:* Auto. Draft 1/2 the minimum monthly payment every 2 weeks.* Reduces the life of the loan by 7 to 11 years.

Minimum Monthly Payments Guaranteed

$500

$538

$578

$622

$668

$718

$772

$830

$892

$959

$0

$200

$400

$600

$800

$1,000

$1,200

1 2 3 4 5 6 7 8 9 10

Year

Pay

men

t

FundemAll Bank NICHES • Low rates on non-conforming products• No M.I…….Escrows Optional• 100% Purchases, + 6% seller CCs (incl ppds)• 100% C/O Refis• 100% w/575 score• 100% w/one active trade, OR, RENT• 100% Limited doc• 100% Stated Income• 100% Condos (Hi Rise, too)• 100% 2-4 units, O/O….STATED• 100% 1st Time Home Buyer• 100% 1 Day out of BK or FC• 100% REHABBED FLIP Properties• 100% 18 month S/E• CONFORMING FALLOUT• 12 month personal or BUSINESS BANK STATEMENTS w/525• 6 month STATEMENTS w/650 = Limited Doc• Mtg lates OK, if incl in score (or, will be graded)• No VOR programs• No payment shock, reserves or VODs (on most programs)• Debt ratios to 55%• Collections/Chg offs remain open (Child Supp must be in repymt)• Judgements < $1,000 remain open• Interest Only option, 90K min, 2,3 or 5 yr.• Reasonable closing costs…$620, 1st….$200, 2nd (Fla.)• Loan amounts to $750K, 1st• $900K, combos• Cash in hand to $150K, after debt consol & CCs

FundemAll Bank NICHES • Low rates on non-conforming products• No M.I…….Escrows Optional• 100% Purchases, + 6% seller CCs (incl ppds)• 100% C/O Refis• 100% w/575 score• 100% w/one active trade, OR, RENT• 100% Limited doc• 100% Stated Income• 100% Condos (Hi Rise, too)• 100% 2-4 units, O/O….STATED• 100% 1st Time Home Buyer• 100% 1 Day out of BK or FC• 100% REHABBED FLIP Properties• 100% 18 month S/E• CONFORMING FALLOUT• 12 month personal or BUSINESS BANK STATEMENTS w/525• 6 month STATEMENTS w/650 = Limited Doc• Mtg lates OK, if incl in score (or, will be graded)• No VOR programs• No payment shock, reserves or VODs (on most programs)• Debt ratios to 55%• Collections/Chg offs remain open (Child Supp must be in repymt)• Judgements < $1,000 remain open• Interest Only option, 90K min, 2,3 or 5 yr.• Reasonable closing costs…$620, 1st….$200, 2nd (Fla.)• Loan amounts to $750K, 1st• $900K, combos• Cash in hand to $150K, after debt consol & CCs

A Brief Summary Of The New Mortgage Relief Plan

• Jan. 6-- the American Securitization Forum issued 'Streamlined Foreclosure and Loss Avoidance Framework for Securitized Sub-prime Adjustable Rate Mortgage Loans.' It has been endorsed by The Treasury Department, Department of Housing and Urban Development, and federal bank regulators. It

sets forth a voluntary system for lenders to streamline the evaluation of their securitized sub-prime loan portfolios ...

• At the heart of HAMP is a net present value model that calculates whether a modification is more valuable to the mortgage holder than proceeding to foreclosure. Problem is, the model is not publicly available, which limits everyone’s ability to determine and debate whether certain choices and assumptions built into the model are appropriate.

• HAMP Design – "Pay for Success" Incentive Structure• HAMP offers "pay for success" incentives to servicers,

investors and borrowers for successful modifications. This aligns the incentives of market participants and ensures efficient expenditure of taxpayer dollars.

• Servicers receive an up-front payment of $1,000 for each successful modification after completion of the trial period, and "pay for success" fees of up to $1,000 per year, provided the borrower remains current. Homeowners may earn up to $1,000 towards principal reduction each year for five years if they remain current and pay on time.

• HAMP also matches reductions in monthly payments dollar-for-dollar with the lender/investor from 38 percent to 31 percent DTI. This requires the lender/investor to take the first loss in reducing the borrower payment down to a 38 percent DTI, holding lenders/investors accountable for unaffordable loans they may have extended.

• To encourage the modification of current loans expected to default, HAMP provides additional incentive to servicers and lender/investors when current loans are modified.

• Mortgagee Incentives Under FHA-HAMP, the Mortgagee may receive an incentive fee of up to $1,250. This total includes $500 for the partial claim and $750 for the loan modification. To receive the incentive payments, the Partial Claim and Loan Modification must meet the requirements of Mortgagee Letters 2008-21, 2003-19, 2002-17, 2000-05, and comply with instructions and requirements in this Mortgagee Letter and Attachment. Mortgagees may also claim up to $250 for reimbursement of title search and/or recording fees.

• http://www.treas.gov/press/releases/tg217.htm

Mortgage Chief Resigns; Emergency Rules Instituted

• Aug 13, 2008 - McClatchy Tribune Business News Author(s): Catherine Dolinski • Aug. 13--TALLAHASSEE -- Florida's top regulator of mortgage brokers said

Tuesday that he will leave his post Sept. 30 amid continuing criticism for allowing thousands of ex-convicts to obtain mortgage brokering licenses and, in some cases, commit fraud.

• Meanwhile, the state is taking new steps to make it harder for ex-felons to get into the mortgage brokering business. But whether the new rules are legal remains unclear, since the state has made restoration of civil rights for felons nearly automatic - including the right to hold professional licenses.

• Cabinet's vote to adopt emergency rules to make it tougher for felons to work as mortgage brokers. Depending on their crime, some will be ineligible for licenses; others will have to wait between five and 15 years after completing their sentences.

• They will last 90 days, giving the state time to initiate the time-consuming process of setting permanent rules,

• All states must eventually comply with tough new federal regulations

Refinancing no longer a sure thing By TARA SIEGEL BERNARD THE NEW YORK TIMESPublished: Saturday, January 24, 2009

• Refinancing is a very difficult proposition right now • the number of homeowners seeking to refinance their

homes has spiked to its highest level in five years. • many have been unable to win approval • lenders have become more cautious about whom they

will lend to • increasingly stringent credit requirements • plunging property values have erased all or most of the

equity in their homes.

US mortgage insurers see claims still risingBy Kathy Shwiff Jan. 20, 2009 http://www.marketwatch.com/news/story/EARNINGS-PREVIEW-US-mortgage-insurers/story.aspx

• Mortgage insurers, which cover potential lender losses on loans to borrowers who can't come up with a 20% down payment, have seen claims skyrocket in the past year as the credit crunch made it difficult for borrowers to refinance and for lenders to resell foreclosed properties at a profit. Currently no MI Co. will insure condominiums in Florida.

Appraisal Code Moves Ahead • Starting May 1,2009, lenders taking loan applications must comply

with the code that applies to all loans sold to Fannie Mae and Freddie Mac

• The new code is designed to take loan officers and mortgage brokers out of the process of selecting and influencing the appraisal process.

• Use appraisal management companies to comply with the GSEs' appraisal standard

PRO• Consumer Mortgage Coalition expects the transition to go smoothly. CMC

represents some of the largest banks and mortgage companies, including First American that owns eAppraiseIT.

CON• The National Association of Mortgage Brokers has tried to get the courts

and Congress to block the implementation of the GSE appraisal code • Model is "flawed," NAMB says, it will produce "poor qualify" appraisals at an

increased cost to consumers. • The Appraisal Institute and other appraiser trade groups warned

Congress that appraisal management companies keep "half the appraisal fee in most cases" and they reply on less experienced and less competent appraisers.

FHA Originations more common now than GSEs

• Originations of Federal Housing Administration single-family loans are catching up with Fannie Mae and Freddie Mac loans, according to the chief executive of a cooperative of 125 regional mortgage banking firms

• In January 2007, FHA lending made up only 1% of Lenders One loan production, and 60% was Fannie/Freddie conventional loans. In the second quarter of 2008, FHA product constituted 41.5% of originations, while conventional originations totaled 53.1%

• FHA is getting a lot of good publicity and that the federal mortgage insurance program has not raised its fees or tightened its underwriting standards, as Fannie and Freddie and the private mortgage insurance companies have

• investors will no longer buy FHA loans with credit scores below 580. "Some won't do it below 600 or 620,"

Traditional Mortgage Brokerage Business

Marketing:– Realtors– Sphere of Influence– General Public (ADV)

Loan Placement: DU/LP (conforming) FHA Alternates (Jumbo, Niche, USDA) Hard Money Non- Institutional (private)

Attend Closing:What do Mortgage Brokers actually do at closings?

All lending Business’s are not created equally

There is a difference between,TITLE XXXVIII

BANKS AND BANKING

And,TITLE XXXIII

REGULATION OF TRADE, COMMERCE,

INVESTMENTS, AND SOLICITATIONS – CHAPTER 494

» MORTGAGE BROKERAGE AND MORTGAGE LENDING

Education & License Requirements

• Compliance News Recap• Mortgage Licensing Registry Launched

• The House recently passed a predatory-lending bill (H.R. 3915) that requires the creation of a nationwide mortgage licensing system and registry

Licensed Mortgage Originators need a Federal Id Number

Loan Pricing

Loan Pricing

↔ Par →

Pricing 1 point yield →spread

Pricing Adjustments

Lock Period

Quo t ed RaTe

Lets go shopping @

5%?

NC Says "No" to Yield Spread Premiums

• Wednesday, August 20, 2008 –

• Staff Writer, Originator Times

• RALEIGH, NC - North Carolina Governor Mike Easley signed House Bill 2188 - which eliminates rate or yield spread premiums - into law. North Carolina is the first state to ban yield spread premiums.

1 Month LIBOR Rate 9/8/08 8/8/08 9/8/07

→PAR→

Index + Margin = Actual Rate

Start Rate

2.49 2.46 5.80

1/25/09

Renovation Lending

• A Renovation Loan is a fully disbursed mortgage that adds the costs of repairs or improvements into the mortgage to purchase or refinance a property

Renovations to Consider Additions, alterations, improvements and

structural changes to a home Remodel kitchens and bathrooms Flooring, Carpet or Tile Repair or replacement of plumbing, heating,

air conditioning or electrical systems Exterior siding, Windows and Doors Roofing, Gutters and Downspouts Repair an existing pool

General Specifications

Purchase or No Cash-out Refinance 15, 20, 25 or 30yr Fixed Rate Mortgage 1-4 Family Owner Occupied Property; Must be at least 1yr old & complete An Appraisal based on the future value or

“as completed” value of the property is required on all 203(k) loans

On HUD Repo’s, the “as is” appraisal (the original appraisal from HUD that comes with the contract) will also need to be provided

8/4/09 getting ready to close

• As soon as we receive the final approval of the HUD, I am going to call and set up a closing time with him and let him know how much he needs to bring to closing. The lender is pretty quick to respond so I should have the revised HUD approved shortly.

• And then…………………

• Taylor, Bean & Whitaker Mortgage Corp. is no longer originating, underwriting, or processing loans in any jurisdiction, effective Wednesday, August 5, 2009.

• Taylor, Bean and Whitaker Mortgage Corp. – one of the largest non-bank residential lenders in Florida – has been barred from issuing mortgages in the state by the Florida Office of Financial Regulation.

• The state agency released an emergency cease and desist order Aug. 7 against Ocala-based Taylor Bean, which has 30 offices in Florida. State residents in the middle of the application process should be placed with viable alternate lenders.

• The Wall Street Journal called Taylor Bean the third-largest

underwriter of FHA loans in the country.

Hard Money

• * No Fico Requirement• * No Credit History Required• * No Seasoning• * Foreclosure Bailout- Ok• * BK buyout- Ok• * SISA• * Max LTV 65% • * Pre-pay buyout ok• * Rates from 11 to 12.5%• * Points range from 2 to 3.5%• * Loan modification

How much can be charged legally?

• 494.0042 Brokerage fees.-- • (1) A mortgage brokerage fee earned by a licensee, pursuant to ss.

494.003-494.0043, is not considered interest or a finance charge under chapter 687.

• (2) A person may not charge or exact, directly or indirectly, from the mortgagor a fee or commission in excess of the maximum fee or commission specified in this section. The maximum fees or commissions that may be charged for mortgage loans are as follows:

• (a) On a mortgage loan of $1,000 or less: $250. • (b) On a mortgage loan exceeding $1,000 and not exceeding $2,000: $250

for the first $1,000 of the mortgage loan, plus $10 for each additional $100 of the mortgage loan.

• (c) On a mortgage loan exceeding $2,000 and not exceeding $5,000: $350 for the first $2,000 of the mortgage loan, plus $10 for each additional $100 of the mortgage loan.

• (d) On a mortgage loan exceeding $5,000: $250 plus 10 percent of the entire mortgage loan.

$0 $10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

Property Managers

Appraisers

Title Examiners

Real Estate Brokers

Real Estate Sales

Loan Officers

1191

4113

-20

2123

-20

9341

-90

2141

-90

2213

-20

72

2008

2007

2006

2005

2004

2003

2002

Employment by Occupation

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

Pro

pert

y

Managers

Appra

isers

Title

Exam

iners

Real

Esta

te

Bro

kers

Real

Esta

te

Sale

s

Loan

Off

icers

11 9141 13-2021 23-2093 41-9021 41-9022 13-2072

Nu

mb

er

em

plo

yed

2002

2003

2004

2005

2006

2007

Lets lend out some $?$?$?$?$

Scenario Workshop • Female age 25, 620 middle credit score - wants to

purchase first home. Currently works in a restaurant as a server, a job she’s had for the past 6 mos. She says she doesn’t claim all her tips so she won’t have to pay taxes on the income. Current paystub shows $1,200 per mos. Prior 2 year history work history shows 3 jobs non continuous and different lines of work. She currently lives with family and has for the past year. She has $500 in the bank.

• How can we help this young lady?Loan Placement???DU/LP (conforming) FHA Alternates (Jumbo, Niche, USDA) Hard Money Non- Institutional (private)

• A forty five year old business man,725 middle score - wants to refinance his purchase combo loan from Aug 2005 into a single loan of 350K (amount borrowed in 05) at a fixed rate – no cash back. This man has a successful business, tax returns show him paying tax on an adjusted gross of $22,000.

• What can we do for this gentleman? Loan Placement?? DU/LP (conforming) FHA Alternates (Jumbo, Niche, USDA) Hard Money Non- Institutional (private)

• 55 year old business man, 450 middle -wants a $50000 first mortgage loan on his primary residence worth about 475000 which he owns free and clear. His business has been established for about 20 years and his debt to income is about 15%.

• What can we do for this man?Loan Placement?? DU/LP (conforming) FHA Alternates (Jumbo, Niche, USDA) Hard Money Non- Institutional (private)

• Individual, 725 middle - wishing to buy primary residence. 3 mos on the current job with previous job in a different line of work, and a 2 mos job gap. Currently pays $800 per mos in rent which will go to approximately $1500 if approved. There is about $37,000 in liquid reserves. Full doc ratio’s are 40/41.

• What can we do to help this person?Loan Placement??

DU/LP (conforming)

FHA

Alternates (Jumbo, Niche, USDA)

Hard Money

Non- Institutional (private)

• 681 middle, with solid credit history • 90% LTV rate and term, owned home for 2.5 years• $200 in a checking,$6000 IRA• Laid off in 2006,worked temp jobs and collected

unemployment for the last 2 years, found new work 1mos ago, still in a temp position, although employer letter said this position was likely to be permanent.

• What can we do to help this person?Loan Placement?? DU/LP (conforming) FHA Alternates (Jumbo, Niche, USDA) Hard Money Non- Institutional (private)

• Man with 780 middle wishes to buy condo in Sarasota as primary for 74K. In his line of work he travels extensively on the US on a work visa. He currently owns a home in the Northeast worth 250K . He has sufficient assets to pay cash for the property if he desired. Income is not a problem for ratio’s

Loan Placement??

DU/LP (conforming)

FHA

Alternates (Jumbo, Niche, USDA)

Hard Money

Non- Institutional (private)

Bonus Bonus Bonus BonusBonus

• 63 year old woman,450 middle, in foreclosure, house in poor condition, owes 115,000, house worth about 250,000

• Give away hint – We have not discussed this type of loan

• “ You must have a plan and actually implement and track for you to be successful. Wishing and praying and hoping are not enough,.. You must do something , You must have a plan and system that produces loans for you everyday regardless of rates , regardless of closed real estate offices , regardless of any other real or imagined excuse that pops up.”

• www.loanofficersuccess.com • PS please feel free to forward this to anyone you

think will benefit from it.