-

A Cash Conversion Cycle Approach to Liquidity AnalysisAuthor(s):

Verlyn D. Richards and Eugene J. LaughlinSource: Financial

Management, Vol. 9, No. 1 (Spring, 1980), pp. 32-38Published by:

Wiley on behalf of the Financial Management Association

InternationalStable URL: http://www.jstor.org/stable/3665310

.Accessed: 26/01/2015 05:42

Your use of the JSTOR archive indicates your acceptance of the

Terms & Conditions of Use, available at

.http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars,

researchers, and students discover, use, and build upon a wide

range ofcontent in a trusted digital archive. We use information

technology and tools to increase productivity and facilitate new

formsof scholarship. For more information about JSTOR, please

contact [email protected].

.

Wiley and Financial Management Association International are

collaborating with JSTOR to digitize, preserveand extend access to

Financial Management.

http://www.jstor.org

This content downloaded from 111.68.100.252 on Mon, 26 Jan 2015

05:42:16 AMAll use subject to JSTOR Terms and Conditions

http://www.jstor.org/action/showPublisher?publisherCode=blackhttp://www.jstor.org/action/showPublisher?publisherCode=fmahttp://www.jstor.org/stable/3665310?origin=JSTOR-pdfhttp://www.jstor.org/page/info/about/policies/terms.jsphttp://www.jstor.org/page/info/about/policies/terms.jsp

-

A Cash Conversion Cycle Approach to Liquidity Analysis

Verlyn D. Richards and Eugene J. Laughlin

The authors both teach at the College of Business Administration

at Kansas State University, where Verlyn Richards is Professor of

Finance and Eugene Laughlin is Professor of Accounting.

Introduction

Although working capital management receives less attention in

the literature than longer-term investment and financing decisions,

it occupies the major portion of a financial manager's time and

attention [9, p. 173]. In part, this simply reflects the repetitive

nature of in- vestment commitments with relatively short life ex-

pectancy and rapid transformation from one invest- ment form to

another [6, pp. 1-2]. The time devoted to working capital

management, however, also reflects the crucial liquidity - or

repayment capability - im- plications of a firm's short-term

investment and financing policies. Inattention to the liquidity

manage- ment process may cause severe difficulties and losses due

to adverse short-run developments even for the firm with favorable

long-run prospects. Incorrect evaluation of the liquidity

implications of a firm's working capital needs may, in turn,

subject creditors and investors to an unanticipated risk of

default.

Financial managers and their external financial analyst

counterparts recognize, at least intuitively, that all working

capital investments do not enjoy the same life expectancy, nor are

they transformed into

usable liquidity flows at the same speed. It is not clear,

however, that they recognize explicitly the crucial role of these

differences in evaluating a firm's liquidity position. A cash

conversion cycle approach to working capital management illustrates

the potential danger of an intuitive approach to liquidity

analysis.

The Static View

Financial analysts traditionally have viewed the current ratio

as a key indicator of a firm's liquidity position. Logue and

Merville, in an empirical study of the capital asset pricing model,

state this traditional view when they observe that:

As our liquidity variable, the current ratio (CR) - current

assets divided by current liabilities - was chosen. Even a cursory

review of most investment texts suggests this variable's

importance: it is widely understood by investors; has more

intuitive appeal than other measures, such as short-term assets

divided by total assets; and was found in the study by Beaver,

Kettler and Scholes [2] to be highly correlated with Beta [5, p.

40].

32

This content downloaded from 111.68.100.252 on Mon, 26 Jan 2015

05:42:16 AMAll use subject to JSTOR Terms and Conditions

http://www.jstor.org/page/info/about/policies/terms.jsp

-

RICHARDS AND LAUGHLIN/LIQUIDITY ANALYSIS

Generalizations such as these must be viewed with caution. They

fail to recognize that the basic liquidity protection against

unanticipated discrepancies in the amount and timing of operating

cash inflows and out- flows is provided by a firm's cash reserve

investments in combination with its unused borrowing capacity

rather than by total current asset coverage of out- standing

current liabilities.

Inter-firm and inter-period comparisons of current ratio

statistics are of questionable value to the finan- cial analyst

because of qualitative differences in the liquidity attributes of

current asset investments. A concentration of current assets in the

less liquid receivables and inventory forms may create an in-

creasing current ratio reflecting a deteriorating ability by the

firm to cover its current liabilities rather than an improved

liquidity position for the firm. Analysts responded to this problem

by supplementing the current ratio with the more restrictive

acid-test ratio, a ratio of the "degree to which a company's

current liabilities are covered by the most liquid current assets"

[1, p. 7]. By eliminating the relatively illiquid inventories and

prepaid operating expenses, the acid- test ratio relates a firm's

current liabilities to its remaining current asset commitments to

cash, near- cash, and receivables. "Thus, the quick or acid-test

ratio is a much more severe test of current liquidity than is the

working capital ratio" [8, p. 645].

The so-called quick assets in this ratio are presumed to be

convertible into cash at approximately their stated balance sheet

amounts. Firms may, however, experience distinct differences in the

speed with which they can convert receivables, as well as

inventories, to usable cash flows. Thus, the acid-test ratio

reflects a different, although not necessarily more reliable, test

of potential solvency than the current ratio does. The usefulness

of both static liquidity indicators is limited by their failure to

provide adequate information about cash flow attributes of the

transformation process within a firm's working capital

position.

Static liquidity indicators emphasize essentially a liquidation,

rather than a going-concern, approach to liquidity analysis. The

ability to meet a firm's obligations through asset liquidation in

the event of default should be viewed as strictly a second line of

defense. Investors should focus their concern on avoiding default

situations by emphasizing 1) a firm's ability to cover its

obligations with cash flows from an employment of inventory and

receivable investments within the normal course of the firm's

operations, and 2) the sensitivity of these operating cash flows

to

declining sales and earnings during periods of economic

adversity. Operating cash flow coverage, rather than asset

liquidation value, is the crucial ele- ment in liquidity

analysis.

The Operating Cycle Concept The flow concept of liquidity can be

developed by

extending the static balance sheet analysis of potential liq-

uidation value coverage to include income statement measures of a

firm's operating activity. In particular, in- corporating accounts

receivable and inventory turnover measures into an operating cycle

concept provides a more appropriate view of liquidity management

than does reliance on the current and acid-test ratio indicators of

solvency. These additional liquidity measures explicitly recognize

that the life expectancies of some working capital components

depend "upon the extent to which three basic activities -

production, distribution (sales), and collection - are

noninstantaneous and un- synchronized" [6, p. 3].

Accounts receivable turnover is an indicator of the frequency

with which a firm's average receivables invest- ment is converted

into cash. Changes in credit and collec- tion policy have a direct

impact on the average outstan- ding accounts receivable balance

maintained relative to a firm's annual sales. Granting more liberal

terms to a firm's customers creates a larger, and potentially less

li- quid, current investment in receivables. Unless sales in-

crease at least proportionately to the increase in receivables,

this potential deterioration in liquidity will be reflected in a

lower receivables turnover and a more ex- tended receivables

collection period. Decisions that com- mit a firm to maintaining

larger average receivables in- vestments over a longer time period

will inevitably result in higher current and acid-test ratios.

Inventory turnovers depict the frequency with which firms

convert their cumulative stock of raw material, work-in-process,

and finished goods into product sales. Adopting purchasing,

production scheduling, and dis- tribution strategies that require

more extensive inventory commitments per dollar of anticipated

sales produces a lower turnover ratio. This, in turn, reflects a

longer and potentially less liquid inventory holding period. If

firms cannot modify either the payment practices established with

trade creditors or their access to short-term debt financing

provided by non-trade creditors, decisions that create longer and

less liquid holding periods will again be accompanied by a higher

current ratio indicator of solvency.

The cumulative days per turnover for accounts

33

This content downloaded from 111.68.100.252 on Mon, 26 Jan 2015

05:42:16 AMAll use subject to JSTOR Terms and Conditions

http://www.jstor.org/page/info/about/policies/terms.jsp

-

FINANCIAL MANAGEMENT/SPRING 1980

receivable and inventory investments approximates the length of

a firm's operating cycle. Incorporating these asset turnovers into

an operating cycle concept of the current asset conversion period

thereby provides a more realistic, although incomplete, indicator

of a firm's li- quidity position. The operating cycle concept is

deficient as a cash flow measure in that it fails to consider the

li- quidity requirements imposed on a firm by the time dimension of

its current liability commitments. Integrating the time pattern of

cash outflow requirements imposed by a firm's current liabilities

is as important for liquidity analysis as evaluating the associated

time pattern of cash inflows generated by the transformation of its

ci rrent asset investments.

The Cash Conversion Cycle The cash conversion cycle, by

reflecting the net time

interval between actual cash expenditures on a firm's purchase

of productive resources and the ultimate recovery of cash receipts

from product sales, es- tablishes the period of time required to

convert a dollar of cash disbursements back into a dollar of cash

inflow from a firm's regular course of operations. Evaluating the

interrelated cash inflow-outflow pattern underlying a more complete

approach to li- quidity analysis requires an additional flow

indicator for current liabilities, however. This flow concept can

be derived from a payables turnover ratio relating operating costs

requiring current cash expenditures to the accounts payable and

accrued payable liabilities created by the short-term deferral of

these operating expenditures. The relevant payables turnover ratio

will be defined as a firm's annual cash operating ex- penditures

(total operating costs minus depreciation, depletion, amortization,

and related charges that do not require current cash outlays)

divided by the current trade accounts and notes payable plus other

spontaneous liabilities directly associated with deferred payment

of these current operating costs.

As in the case of the inventory and receivables turn- over

concepts, the liquidity implications of a firm's payables turnover

experience can be established more clearly by a time interval

statement reflecting the firm's average payment period.

Specifically, the average payment period - 360 days divided by the

an- nual payables turnover - reflects the average time over which a

firm defers payment on the costs in- curred to support its

operating activities. While declin- ing inventory and receivable

turnover ratios reflect a larger current asset investment that must

be financed over a longer operating cycle interval, a declining

payables turnover ratio indicates a larger accumula- tion over a

longer period of spontaneous working capital financing provided by

trade creditors. The more extended operating cycle associated with

a declining inventory and receivables turnover increases a firm's

potential liquidity management problem. Conversely, the longer

payment period associated with a declining payables turnover tends

to moderate the liquidity management problem for a firm.

Introduction of a payables turnover concept points out that

liquidity analysis requires explicit recognition of the extent to

which four basic activities - purchasing/production, sales,

collection, and payment - create flows within the working capital

accounts that are noninstantaneous and unsynchronized. The cash

conversion cycle concept portrays these flows by integrating

respective time intervals derived from a firm's typical

receivables, inventory, and payables turnover experience. The

concept thereby depicts the residual time interval over which

additional, nonspon- taneous financing must be negotiated to

compensate for the noninstantaneous and unsynchronized nature of a

firm's working capital investment flows.

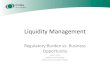

Exhibit 1 illustrates the relationship between a cash conversion

cycle indicator of the firm's additional, nonspontaneous working

capital financing re- quirements and the more traditional operating

cycle concept of its asset conversion period. The diagram points

out that a residual cash flow financing period depicted by the cash

conversion cycle will be in- fluenced by either expansion or

contraction in any of the three liquidity flow measures: the

inventory con- version period, receivables conversion period, or

payables deferral period. An increase in the length of the

operating cycle without a concomitant lengthening of the payables

deferral period creates additional li- quidity management problems

associated with the need to acquire additional nonspontaneous

financing over a longer, and potentially less certain, cash

conversion period.

Financial Management Implications of the Cash Conversion

Cycle

Working capital provided by vendors in the normal course of a

firm's operations is spontaneous financing in the sense that it

will automatically increase and decrease over time. The

availability of such financing is tied directly to the typical

trade credit terms offered by vendors to their customers and the

volume of goods and services acquired under these terms. A dis-

tinguishing feature of this spontaneous financing is the

34

This content downloaded from 111.68.100.252 on Mon, 26 Jan 2015

05:42:16 AMAll use subject to JSTOR Terms and Conditions

http://www.jstor.org/page/info/about/policies/terms.jsp

-

RICHARDS AND LAUGHLIN/LIQUIDITY ANALYSIS

Exhibit 1. Cash Conversion Cycle Product

Sales Inventory Receivables

Conversion Period Conversion Period

~~o -~ ~ Operating Cycle c _ _ Payables _LCash

Deferral Period h Conversion Cycle Cash Outlay

I x 0 : :r

CD

absence of explicit financing charges as long as purchasers pay

within the stipulated credit period or within the discount period

when a cash discount is offered for early payment. In addition to

the spon- taneity and nonexplicit cost attributes, trade credit

also provides flexibility to working capital manage- ment because

"experience shows that it is possible to achieve continuity in the

supply of trade credit even in adversity when the credit

relationship is well managed" [9, p. 231].

Some instances are found where "manufacturers quite literally

supplied all the financing for new firms by selling on credit terms

substantially longer than those of the new company" [9, p. 230].

The more typical firm will find, however, that reliance on trade

credit can be economically justified for financing only a portion

of its working capital investments. The remaining working capital

investment requirements must be supported by negotiating explicit

nonspon- taneous financing arrangements with the firm's creditors

and owners. It is the need for, and the li- quidity management

problems created by, this ad- ditional working capital financing

requirement that provides the basic rationale for adapting the

operating cycle concept to a cash conversion cycle concept of

liquidity analysis.

Cash management constraints imposed by the more uncertain cash

flows typically associated with a longer cash conversion cycle

force firms to modify both the investment and financing aspects of

their working capital management policies. From a financial struc-

ture standpoint, operating cash flow constraints restrict a firm's

ability to support additional working capital financing

requirements by supplementing spontaneous trade credit with

nontrade sources of short-term credit. Short-term creditors are

less in- clined to finance additional working capital in- vestments

on which there is a greater risk of default and a greater potential

loss in liquidation value in the event of default. Therefore, firms

will have to rely more extensively on longer-term financing

arrange- ments to support desired extensions of their non-cash

current asset commitments to less liquid inventory and

receivable investments.

From the investment side, firms will be required to maintain

additional liquidity reserves in compensating and precautionary

balances in order to compete for the additional nonspontaneous

financing desired to support a longer and less certain cash

conversion cy- cle. These additional commitments to precautionary

balance investments will be required to protect providers of

long-term, as well as short-term, financ- ing against unpredictable

variations in a firm's pattern of future operating cash flows.

In general, the movement toward a longer cash con- version cycle

will produce a larger required commit- ment to cash, as well as

non-cash, current asset in- vestments and a less extensive relative

ability to finance these investments with current liabilities.

Therefore, working capital management policies that create a longer

cash conversion cycle can be expected to produce a higher current

and acid-test ratio posi- tion for the firm. In contrast to the

conventional view that higher current and acid-test ratios reflect

a more liquid working capital investment position, this analysis

suggests that these higher ratio values may simply be the

by-product of a more extensive commit- ment to less liquid forms of

current asset investments.

Negotiating nonspontaneous financing to support both inventory

and receivables investments held beyond the payables deferral

period would not be a significant management problem if firms could

predict with a high degree 9f certainty the future pattern of their

operating cash flows. In an uncertain economic environment,

however, the general availability of additional credit financing,

and a firm's additional short-term borrowing capability in

particular, may be inversely related to the length of its cash

conversion cycle. This inverse relationship exists because longer

cash conversion cycles reduce the flexibility available to firms in

managing their cash flows in the face of economic adversity. The

greater potential for being locked into excessive inventory and

uncollectible receivables investments reduces a firm's ability to

rely on funds derived from operating cash flows for a timely

repayment of maturing obligations.

This approach becomes increasingly applicable as firms

experience greater volatility in their sales revenue and,

therefore, greater uncertainty in predict- ing the amount and

timing of their cash receipts in response to changing economic

conditions. The im- portance of this increased unpredictability is

magnified, or mitigated, by three additional, in- terrelated

factors: the relative amounts of variable and

35

This content downloaded from 111.68.100.252 on Mon, 26 Jan 2015

05:42:16 AMAll use subject to JSTOR Terms and Conditions

http://www.jstor.org/page/info/about/policies/terms.jsp

-

FINANCIAL MANAGEMENT/SPRING 1980

fixed cash operating expense, the extent of built-in rigidities

in the current asset turnovers, and the availability of borrowing

capacity to support discon- tinuities in the firm's cash flow

pattern. Larger amounts of fixed cash expenses, lower current asset

turnovers, and reduced availability of borrowing capacity

significantly increase liquidity management problems created by an

underlying volatility in revenue. The effect of these three factors

is incor- porated in the cash conversion cycle approach to li-

quidity management.

A Cash Conversion Cycle Illustration Cash conversion cycle

analysis can be implemented

for most firms with conventional income statement and balance

sheet data. For publicly held firms, this information is generally

available in their annual reports to stockholders and their SEC

10-K reports. Exhibit 2 depicts the data required for cash

conversion cycle analysis as reported in the financial statements

for Martin Marietta Corporation. Exhibit 3 illustrates the firm's

liquidity indicators computed from these data. This firm was

selected because it reflects the logic of cash conversion cycle

analysis reasonably well in an actual rather than a theoretical

context.

The primary point, as illustrated by the Martin Marietta

experience, is that static liquidity analysis in the form of

current and acid-test ratios may not provide meaningful indicators

of the liquidity position with respect to the more appropriate cash

flow stand- point. The decline in the cash conversion cycle and in

the associated need for nonspontaneous financing over the 1975-1978

period is indicative of a moderating li- quidity management

problem. This contrasts with an implied increase in the liquidity

management problem from the declining current ratio viewpoint or an

in- determinate change in the firm's liquidity position relative to

the mixed behavior pattern in the acid-test ratio. The current

ratio, as traditionally interpreted, would appear to give the wrong

indicator of change in liquidity position while the acid-test ratio

simply fails to indicate clearly a pronounced change in the firm's

operating cash flows.

The cash conversion cycle should be evaluated in relation to a

firm's maintenance of liquidity reserve in- vestments, its

availability of unused borrowing capacity, and potential volatility

in the firm's cash flows. Exhibit 3 points out that a supplementary

test of liquidity reserve position can be constructed by comparing

the firm's cash assets - working cash balances plus temporary cash

investments - to its total current assets. The data for Martin

Marietta

show that a more rapid recovery of operating cash ex- penditures

has been accompanied by an increasing proportion of current assets

held in the most liquid form. In the previous section, we noted

that additional liquidity reserves will be required to support a

longer and less certain cash conversion cycle. By contrast, an

increasing liquidity reserve investment coincident with a shorter

and more certain cash conversion cycle would contribute to an

improving liquidity position. This observed relationship for Martin

Marietta again suggests an improving liquidity position despite a

declining current ratio and an indeterminant trend in the acid-test

ratio.

Illustrating the interrelationship among the cash conversion

cycle, the availability of unused borrowing capacity, and the

associated problem of cash flow volatility is beyond the scope of

this paper. Procedures for stipulating a firm's borrowing capacity

in relation to uncertainty about its future cash flows are not yet

well-developed in the literature. Recently, articles by Kim [3],

Scott [7], and Kraus and Litzenberger [4] appear to provide useful

insights into the problem of evaluating corporate debt capacity.

Continued research along the lines they have suggested may allow a

more explicit extension of the cash conversion cycle concept to

consider the liquidity management effects of debt capacity

constraints.

Summary An examination of conventional, static balance

sheet liquidity ratios indicates the inherent potential for

misinterpreting a firm's relative liquidity position. The extension

of this traditional analysis to include flows embodied in the

operating cycle concept through receivable and inventory turnover

measures directs attention only to the timing of a firm's cash

inflows and excludes from consideration the time element of its

cash outflow requirements. Since cash outflows are not synchronized

with inflows for the typical firm, such an omission is a serious

deficiency in liquidity analysis. Adopting a payables turnover

concept ex- tends the operating cycle analysis to incorporate both

the relevant outflow and inflow components. The resulting cash

conversion cycle analysis provides more explicit insights for

managing a firm's working capital position in a manner that will

assure the proper amount and timing of funds available to meet a

firm's liquidity needs.

References 1. Annual Statement Studies, Philadelphia, Robert

Morris

Associates, 1977.

36

This content downloaded from 111.68.100.252 on Mon, 26 Jan 2015

05:42:16 AMAll use subject to JSTOR Terms and Conditions

http://www.jstor.org/page/info/about/policies/terms.jsp

-

RICHARDS AND LAUGHLIN/LIQUIDITY ANALYSIS

Exhibit 2. Selected Financial Data for Martin Marietta

Corporation (000,000 omitted)*

Year Ended December 31 1978 1977 1976 1975

Net sales $1,758 $1,440 $1,213 $1,053

Cost of goods sold $1,269 $1,030 $ 876 $ 774 Selling, general

and

administrative expense 192 161 142 132 Depreciation,

depletion,

and amortization 72 66 63 60

Total operating expense $1,533 $1,257 $1,081 $ 966

Net operating income $ 225 $ 183 $ 132 $ 87

Cash and short-term investments $ 204 $ 158 $ 107 $ 46

Notes and accounts receivable 283 227 178 147

Inventories 199 209 199 186 Prepayments and other

current assets 16 11 11 14

Total current assets $ 702 $ 605 $ 495 $ 393

Accounts payable $ 133 $ 106 $ 86 $ 78 Salaries, benefits,

and

payroll tax 72 48 37 33 Income taxes 210 151 88 36 Current

maturities of

long-term debt 14 16 16 14

Total current liabilities $ 429 $ 321 $ 227 $ 161

*Source: Years 1977 and 1978, Martin Marietta Corporation Annual

Report to Stock- holders, 1978. Years 1975 and 1976, Martin

Marietta Corporation 10-K reports to the SEC.

Exhibit 3. Liquidity Ratios and Cash Conversion Cycle for Martin

Marietta Corporation

1978 1977 1976 1975

Static Ratios: Current Ratio 1.64 1.88 2.18 2.44 Acid-Test Ratio

1.14 1.20 1.26 1.20

Turnover Ratios: Receivables Turnover 6.21 6.34 6.81 7.16

Inventory Turnover 6.38 4.93 4.40 4.16 Payables Turnover* 7.13 7.73

8.28 8.16

Cash Conversion Cycle: Receivables Conversion Period 58 days 57

days 53 days 50 days Inventory Conversion Period 56 days 73 days 82

days 87 days Operating Cycle 114 days 130 days 135 days 137 days

Less: Payment Deferral Period 50 days 47 days 43 days 44 days Cash

Conversion Cycle 64 days 83 days 92 days 93 days

Supplementary Static Ratio: Cash Assets/Current Assets 0.29 0.26

0.22 0.12

*Cost of goods sold plus selling and general and administrative

expense divided by accounts payable plus salaries, benefits, and

payroll tax.

37

This content downloaded from 111.68.100.252 on Mon, 26 Jan 2015

05:42:16 AMAll use subject to JSTOR Terms and Conditions

http://www.jstor.org/page/info/about/policies/terms.jsp

-

FINANCIAL MANAGEMENT/SPRING 1980

2. W. Beaver, P. Kettler, and M. Scholes, "The Association

Between Market Determined and Accounting Deter- mined Risk

Measures," The Accounting Review (Oc- tober 1970), pp. 654-682.

3. E. Han Kim, "A Mean-Variance Theory of Optimal Capital

Structure and Corporate Debt Capacity," Jour- nal of Finance (March

1978), pp. 45-63.

4. A. Kraus and R. Litzenberger, "A State-Preference Model of

Optimal Financial Leverage," Journal of Finance (September 1973),

pp. 911-922.

5. Dennis E. Logue and Larry J. Merville, "Financial Policy and

Market Expectations," Financial Manage-

ment (Summer 1972), pp. 37-44. 6. Dileep R. Mehta, Working

Capital Management,

Englewood Cliffs, N.J., Prentice-Hall, Inc., 1974. 7. James H.

Scott, Jr., "A Theory of Optimal Capital

Structure," The Bell Journal of Economics (Spring 1976), pp.

33-54.

8. G. A. Welsch and R. N. Anthony, Fundamentals of Financial

Accounting, revised ed., Homewood, Ill., Richard D. Irwin,

1977.

9. J. Fred Weston and Eugene F. Brigham, Essentials of

Managerial Finance, 5th ed., Hinsdale, Ill., The Dryden Press,

1979.

FINANCIAL MANAGEMENT ASSOCIATION TENTH ANNUAL MEETING

The Financial Management Association brings together practicing

financial managers from industry, financial institutions, and

nonprofit and governmental organizations, and members of the

academic community with interests in financial and investment

decision-making. The tenth annual program, October 23-25, 1980, at

the Marriott Hotel in New Orleans, Louisiana, will stress the in-

terrelationships between theory and practice in financial and

investment management.

1980 Annual Meetings

Dates: October 23-25, 1980

Place: Marriott Hotel New Orleans, Louisiana

Program Participation:

Meeting Arrangements:

Placement Information:

Professor Frank K. Reilly College of Commerce and Business

Administration University of Illinois Urbana, Illinois 61801 Tel:

(217) 333-6391

Professor Donald Woodland Louisiana State University College of

Business Administration Baton Rouge, Louisiana 70803

Professor John Boquist Graduate School of Business Indiana

University Bloomington, Indiana 47401 Tel: (812) 337-8568

38

This content downloaded from 111.68.100.252 on Mon, 26 Jan 2015

05:42:16 AMAll use subject to JSTOR Terms and Conditions

http://www.jstor.org/page/info/about/policies/terms.jsp

Article Contentsp. 32p. 33p. 34p. 35p. 36p. 37p. 38

Issue Table of ContentsFinancial Management, Vol. 9, No. 1

(Spring, 1980), pp. 1-89Front Matter [pp. 1-6]Capital Budgeting:

Problems and PracticesCapital Budgeting Methods and Risk: A Further

Analysis [pp. 7-11]A Note on Capital Budgeting and the Three Rs

[pp. 12-13]An Application of the Capital Asset Pricing Model to

Divisional Required Returns [pp. 14-19]Debt Capacity and the

Capital Budgeting Decision: A Comment [pp. 20-22]Debt Capacity and

the Capital Budgeting Decision: A Revisitation [pp. 23-26]

Paper Selected from the 1979 MeetingsAn Empirical Investigation

of Small Bank Stock Valuation and Divided Policy [pp. 27-31]

A Cash Conversion Cycle Approach to Liquidity Analysis [pp.

32-38]The Effect of Forced Conversions on Common Stock Prices [pp.

39-45]The Financial Planning and Management of Real Estate

Developments [pp. 46-52]The Use of Financial Ratios in Credit

Downgrade Decisions [pp. 53-56]Some Portfolio IssuesOptimal

Selection of Passive Portfolios [pp. 57-66]Portfolio Revision: A

Turnover-Constrained Approach [pp. 67-75]

The Evaluation of Leveraged Leases [pp. 76-80]Incentive

Compensation and REIT Financial Leverage and Asset Risk [pp.

81-87]The Effect of Financial Leverage on Air Carrier Earnings: A

Breakeven Analysis: Comment [pp. 88-89]Back Matter