Embed Size (px)

Citation preview

International Journal of Management, IT & Engineering Vol. 8 Issue 8, August 2018, ISSN: 2249-0558 Impact Factor: 7.119 Journal Homepage: http://www.ijmra.us, Email: [email protected] Double-Blind Peer Reviewed Refereed Open Access International Journal - Included in the International Serial Directories Indexed & Listed at: Ulrich's Periodicals Directory ©, U.S.A., Open J-Gage as well as in Cabell’s Directories of Publishing Opportunities, U.S.A

257 International journal of Management, IT and Engineering http://www.ijmra.us, Email: [email protected]

A CAMEL Model Analysis of Selected Public and Private Sector

Banks in India

Kajal Kiran1

Abstract

Banking is one of the fastest growing sectors in India. Banking sector helps in boosting capital formation,

innovation and monetization along with facilitation of monetary policy. Not only the depositors treat sound

financial health of a bank as the guarantee but it is equally significant for the shareholders, employees and whole

economy of a country as well. The present study measures the financial health of top public sector and private

sector banks operating in India using CAMEL Analysis. In the study, seven public sector bank namely State

Bank of India, Bank of Baroda, Bank of India, PNB Bank, Union Bank of India, Canara Bank and IDBI Bank

and four private sector Banks namely ICICI Bank, HDFC Bank, AXIS Bank and Indusind Bank have been

selected as a sample. Data used for the study pertains from 2013-14 to 2016-17 and has been collected from the

annual reports of respective banks. To study every major variable use of various ratios have been made which

helps to analyze the variable in better way.

Keywords: Banks, CAMEL approach, Capital adequacy, Liquidity, asset quality, Management efficiency,

Earning Quality, Liquidity

1. Introduction

A strong, sustainable and viable banking system plays an important role in the overall development of an

economy. Banking sector has contributed in bringing a revolutionary change in reforming sector on the path of

economic growth. In fact, it is the backbone of the economy and one of the key indicators to assess the level of

development of any country. Performance of the banking sector is an effective measure and indicator to check

the performance of any economy to a large extent. The banking sector reforms were started in India as a follow

up measure of financial sector reforms and economic liberalization in the country. The banking sector being the

life line of the economy has been given due weightage in the financial sector reforms. More competitiveness,

productivity and efficiency and adherence to international accounting standards were the basic intentions behind

the initiation of reforms in Indian banking industry.

1 Assistant Professor in Commerce, JC DAV College, Dasuya, [email protected]

ISSN: 2249-0558 Impact Factor: 7.119

258 International journal of Management, IT and Engineering http://www.ijmra.us, Email: [email protected]

Indian banking industry initiated in the early 1990s have been continued till now. As a result of these reforms, there have been

substantial changes in the bye laws, organization, scope and activity level of Indian Banking sector. Thus, Indian banking

industry has shown tremendous growth in the post liberalization era.

Banking performance is assessed by implementing a regulatory banking supervision framework. One of such measures of

supervisory regulation is the CAMEL rating system. In 1980s, US supervisory authorities introduced CAMEL rating system

as a system of rating the banks for on-site examinations of banking institutions. It proved to be a beneficial and efficient tool in

response to the financial crunch in 2008 by the U.S. government.

Camel approach is an effective tool to determine the relative financial strength of a bank and to suggest relevant measures to

improve shortcomings of a bank. In India, on the recommendations of Padmanabham Working Group (1995) committee, RBI

adopted this approach in 1996. At present, two Supervisory Rating Models CAMELS (capital adequacy, asset quality,

management quality, earnings, liquidity and sensitivity to market risk or systems & control) and CACS (capital, asset quality,

compliance and systems & control) are being used in India for rating of the Indian Commercial Banks and Foreign Banks

operating in India respectively.

2. Review of Literature

It has now been well recognized that that financial soundness of a bank depends on the different aspects and not only on the

profitability. A number of studies have been conducted to measure the operational and financial soundness of banks.

Misra and Aspal (2013) evaluate the performance and financial well being of State bank group encompassing State bank of

India, State bank of Hyderabad, State bank of Patiala, State bank of Mysore, State bank of Bikaner and Jaipur and State bank

of Travancore for a period of three years i.e. from 2009-2011.One way ANOVA is applied to determine whether significant

difference exists between the means of CAMEL ratio. They bring out that State bank of India needs to focus on Capital

adequacy and asset quality while State bank of Bikaner and Jaipur and state bank of Patiala have to work on improvement of

management efficiency and earning quality respectively. Gupta (2014) evaluates the performance of public sector banks in

India using CAMEL approach for a period of five years from 2009 to 2013 and brings out that Andhra Bank stood at first

position followed by Bank of Baroda and state bank of Hyderabad while United bank of India secured the least position. Singh

(2015) analyses the overall profitability of four private sector banks i.e. AXIS Bank, ICICI bank, Karur Vysya Bank and Yes

Bank. He measures the performance of the banks on the basis of profitability ratios like interest spread, return on long term

funds, net profit margin, adjusted cash margin, return on assets and return on net worth. ANOVA is also applied to find out the

significant relationship between interest spread, return on long term funds, net profit margin, adjusted cash margin, return on

assets and return on net worth among selected private sector banks. Garg and Kumari(2015) examine the different perspectives

of profitability of five major private banks for ten years from 2004 to 2014 using ratio analysis and ANOVA technique. They

conclude that HDFC Bank has been the excellent performer over the last decade. Meena (2016) assesses the performance of

different public sector and private sector banks by using CAMEL model. In his study, he also investigates the factors that

affect the financial performance of the selected public sector and private sector banks and finds that the management of NPAs

is the weakest area of private sector and public sector banks. Srinivasan and Saminathan (2016) apply CAMEL model to rank

the public sector, private sector and foreign banks on the basis of financial performance from 2012 to 2014.They also find out

that significant difference lies between the mean values of Camel ratios of public sector, private sector and foreign banks

during the period of study. Purohit and Bothra (2018) compare the performance of SBI and ICICI Bank using CAMEL

parameters. They conclude that ICICI bank needs to improve its position with regard to capital adequacy and asset quality

while SBI need to improve its position with regard to management efficiency, earning quality and liquidity.

3. Need of the study

The present study is undertaken to highlight the comparative analysis on financial performance of selected top public sector

and private sector banks in India through CAMEL Analysis Model. Through the study we would came to know the financial

position of the selected 11 top banks operating in India.

ISSN: 2249-0558 Impact Factor: 7.119

259 International journal of Management, IT and Engineering http://www.ijmra.us, Email: [email protected]

4. Objectives of the Study

The objectives of the study are:

To analyze the financial performance of selected Public sector and Private Sector banks in India on different

parameters of camel model.

To examine the overall relative financial position of selected Public sector and Private Sector banks in India .

To give recommendations for improvement in performance of public and private sector banks of India.

5. Research Methodology

5.1 Data Collection

The present study is based on Secondary data. The relevant data has been collected from the annual reports of selected banks.

In addition to the records of the bank, data were also collected from banking bulletin, websites, newspapers, magazines and

various journals.

5.2 Selected Banks for the study:

Seven public sector banks namely (State Bank of India, Bank of India, Bank of Baroda, Union Bank of India, PNB Bank,

IDBI Bank and Canara bank) and four Private sector banks (ICICI bank, HDFC Bank, AXIS Bank, Indusind Bank) have been

taken as sample

5.3 Time Period of the study:

The study covers a period of four financial years i.e. from 2013-14 to 2016-17.

5.4 Analytical Tools:

To look at the financial soundness of the selected Public and Private sector banks in India, internationally accepted CAMEL

rating parameters have been applied. CAMEL is an acronym for five parameters (capital adequacy, assets quality,

management soundness, earnings and liquidity). CAMEL rating is a subjective model which assesses financial strength of a

bank, whereas CAMEL ranking indicates the banks comparative position with reference to other banks.

Ratios and averages have been used for analysis. Averages are calculated using MS-Excel.

6. Empirical Results and Discussion

6.1 Financial performance of Selected public and private sector banks in India on different

parameters of CAMEL model

(1) CAPITAL ADEQUACY

Capital Adequacy is a key indicator of financial well being of a bank. It describes whether the bank has adequate capital to

meet unexpected losses. It gives the indication of overall financial position of the banks and also the ability of the management

to meet the need for additional capital and also to maintain depositor’s confidence and preventing the bank from going

bankrupt. Capital adequacy of a bank can be measured by using following ratios:

ISSN: 2249-0558 Impact Factor: 7.119

260 International journal of Management, IT and Engineering http://www.ijmra.us, Email: [email protected]

Capital adequacy ratio (Tier 1 Capital + Tier 2 Capital)

Risk weighted Assets

a measure of the amount of a bank's core capital

expressed as a percentage of its risk weighted Assets.

Higher the ratio better it is

Advance to assets ratio Total advances/ Total assets Aggressiveness of a bank in lending, thus resulting in

better profitability. Higher the ratio better it is

Debt equity ratio Outside liabilities /Net worth Higher ratio indicates less protection for the creditors

and depositors in the banking system.

Government securities to

total investment

Govt.Securities/Total investment The higher the Government securities to investment

ratio, the lower the risk involved in bank's investments.

A minimum Capital to risk-weighted Assets Ratio (CRAR) prescribed by Reserve Bank of India for banks with regard to

credit risk, market risk and operational risk on an ongoing basis is 9 % as against Basel norms of 8 %. Ranking of the Banks

under study on the basis of CAR as per Table-1(annex.) indicates that ICICI bank ranks on the top position with highest CAR

of 17.19, followed by HDFC, AXIS, INDUSIND and SBI having CAR of 15.74, 15.35, 14.18 and 12.67. Advance to assets

ratio as per Table-2 (annex.) indicates that Union Bank of India bags the top position with highest advance to assets ratio of

0.65, followed by HDFC, INDUSIND, having values of 0.64, 0.63. ICICI bank secures the top position with respect to Debt

equity ratio with lowest Debt Equity ratio of 6.98, followed by INDUSIND, HDFC and AXIS having values of 8.12, 9.06 and

9.26 [Table 3 (annex.)]. Ranking of the Banks under study on the basis of Govt Securities to total investment [Table-

4(annex.)] indicates that BOI stands on the top position with highest Govt Securities to total investment value of 0.89,

followed by CANARA, BOB and PNB having values of 0.88, 0.85 and 0.80.

Result of the group averages of four ratios of capital adequacy is expressed in Table-5(annex.) which indicates that HDFC

bank and INDUSIND bank are jointly at Top in this category with group average of 3.50 followed by ICICI bank and AXIS

Bank with average of 4.0 and 4.75 due to better performance of these private sector banks in Debt Equity, Advances to Assets

ratio, and capital adequacy ratio.

(2) ASSET QUALITY

Asset quality assesses the soundness of financial institutions against loss of value in the assets .Asset impairment adversely

affects the solvency of the financial institutions. The level and severity of non-performing assets, adequacy of provisions,

distribution of assets etc impacts the asset quality. The ratios used to assess asset quality are:

Net NPAs to Net advances Lower ratio is a sign of credit efficiency of bank

Total Investment to total assets Higher ratio adversely affects the profitability of banks

Net NPAs to total assets Lower the ratio, better is the performance of bank

Ranking of the Banks under study on the basis of Net NPA to Net advances as per Table-6(annex.) demonstrates that HDFC

bank ranked on the top position with lowest Net NPA to Net Advances ratio of 0.28, followed by INDUSIND, AXIS and

ICICI having values of 0.35, 0.98 and 2.75. Total investment to total assets ratio [ Table-7(annex.)] indicates that BOB bank

is on the top position with lowest Total investment to total assets ratio of 0.18, followed by BOI, INDUSIND and UBI having

values of 0.20, 0.23 and 0.25. Net NPA to Total Assets as per Table-8(annex.) provides that HDFC bank and INDUSIND

Bank are jointly ranked on the top position with lowest Net NPA to Total assets ratio of 0.002, followed by AXIS, ICICI and

SBI having values of 0.006, 0.017 and 0.019.

Group averages of three ratios of Asset Quality [Table-9(annex.)] makes it clear that HDFC bank and INDUSIND bank are

jointly at Top in this category with group average of 2.0 followed by AXIS bank and BOB Bank with average of 3.33 and

3.67 due to better performance of these private sector banks in all three ratios of Asset Quality. Amongst Public sector banks

only Bank of Baroda has shown good asset quality management.

ISSN: 2249-0558 Impact Factor: 7.119

261 International journal of Management, IT and Engineering http://www.ijmra.us, Email: [email protected]

(3) MANAGEMENT EFFICIENCY

The management efficiency signifies the ability of banks top management to take right decisions. It enables the evaluation of

better management quality and discounting poorly managed ones and helps a bank to achieve sustainable growth. It sets vision

and goals for the business and checks out that it achieves them. The ratios in this element encompass subjective analysis to

determine the efficiency and effectiveness of management. The ratios used to evaluate management efficiency are:-

Total advances to total deposits Indicates the ability of the bank to convert deposits into high earning advances.

Higher ratio is better

Business per Employee Efficiency of the employees to generate business (total advances and total

deposits). The higher the ratio ,better it is.

Profit per Employee Efficiency of the employees to generate profit for the bank. Higher ratio is

better.

Return on Equity Profits available for shareholders. Higher ratio signifies efficiency of the bank.

Total Advances to Total Deposits ratio [Table-10(annex.)] indicates that ICICI bank is ranked on the top position with highest

Total Advances to Total Deposits ratio of 1.02, followed by INDUSIND, AXIS and HDFC having values of 0.92, 0.90 and

0.84. As per table11 (annex.) business per employee of IDBI bank is the maximum. Thus IDBI bags the top position with

highest Business per employee ratio of 248.73, followed by BOI, BOB and UBI having values of 194.20, 179.58 and

150.40.Profit per employee as shown in Table-12(annex.) brings out that AXIS bank secures the highest position with highest

Profit per employee ratio of 1.43, followed by ICICI, HDFC and INDUSIND having values of 1.40, 1.33 and 0.99. Table-

13(annex.) shows that HDFC bank gets the first rank with highest ROE ratio of 19.22, followed by INDUSIND , AXIS and

ICICI having values of 16.55, 14.69 and 12.58. The result of the group averages of four ratios of Management Efficiency is

expressed in Table-14(annex.), which indicates that AXIS bank is ranked at Top with group average of 3.25 followed by ICICI

Bank and HDFC Bank jointly second with average of 4.25 and INDUSIND Bank on third position with value 4.75 due to

better performance of these private sector banks in Total advances to total deposits, profit per employee and ROE. Public

sector banks have shown better performance only in Business per employee category under management efficiency

parameters.

(4) EARNING QUALITY

The sustainability in income and growth of future earnings indicates the quality of earnings. Interest rate policies and

sufficiency of provisioning help to evaluate the earnings and profitability. The ratios that are used to evaluate earning quality

are:-

Interest income to total income Represent the share of interest income in total income. Higher ratio is better

Operating profits to total assets Indicates operating income of the bank per rupee invested in total assets. Higher

ratio is better.

Net interest margin to total assets Excess of interest earned over interest expended relative to total assets

Return on assets Efficiency with which bank uses its assets to generate net income.

Interest income to total income shown in Table 15 (annex.) indicates that UBI and BOI are jointly on the top position with

highest interest income to total income ratio of 0.90, followed by CANARA , BOB and IDBI (jointly second) and PNB having

values of 0.89 and 0.88 respectively. Operating profit to total assets as per Table-16(annex.) brings out that ICICI Bank

secures the top position with highest operating profit to total asset ratio of 3.29, followed by INDUSIND, HDFC and AXIS

having values of 3.25, 3.22 and 3.16 respectively. Table 17 (annex.) provides that Net interest margin to total assets ratio of

HDFC Bank is the highest i.e. 4.14 followed by INDUSIND, AXIS and ICICI having values of 3.59, 3.30 and 3.00

respectively. Ranking of the Banks under study on the basis of ROA shown in Table-18(annex.) indicates that HDFC bank is

ranked on the top position with highest ROA ratio of 1.95, followed by INDUSIND , ICICI and AXIS having values of 1.87,

1.62 and 1.50 respectively. Results of the group averages of three ratios of Earning Quality is expressed in Table-19(annex.),

which indicates that HDFC bank is ranked at Top in this category with group average of 2.25 followed by INDUSIND bank

ISSN: 2249-0558 Impact Factor: 7.119

262 International journal of Management, IT and Engineering http://www.ijmra.us, Email: [email protected]

and ICICI bank with average of 3.00 and 3.75 due to better performance of these private sector banks in Operating profit to

total assets and NIM to Total Assets and ROA. Public sector banks have shown better performance only in Interest income to

total income category under earning quality parameters.

(5) LIQUIDITY:

Liquidity is the capability of banks to meet its financial obligations. Too low liquidity hampers the capacity of banks to meet

its current financial liabilities. On other hand, too high liquidity indicates that banks are not making the proper use of their

cash and hence blocking the way of profitability. Thus a proper equilibrium is necessary in liquidity to balance high profit as

well as liquidity. The ratios suggested to measure liquidity under CAMEL Model are:-

Liquid assets to total assets Higher ratio is better .

Liquid assets to demand deposits Higher ratio is better

Liquid assets to total deposits Higher ratio is better

Approved securities to total assets Higher ratio is better

Ranking of the Banks under study on the basis of Liquid assets to total assets is shown in Table-20, which indicates that BOB

Bank is ranked on the top position with highest Liquid Assets to total asset ratio of 0.21, followed by BOI, PNB and

CANARA(Jointly third) having values of 0.14 and0.10 (both PNB and CANARA). Ranking of the Banks under study on the

basis of Liquid Assets to Demand Deposits is shown in Table-21, which indicates that BOI Bank is ranked on the top position

with highest Liquid Assets to Demand Deposit ratio of 3.50, followed by BOB, CANARA and PNB having values of 3.21,

2.61 and 1.77. Ranking of the Banks under study on the basis of Liquid Assets to Total Deposits is shown in Table-22, which

indicates that BOB Bank is ranked on the top position with highest Liquid Assets to Total Deposit ratio of 0.24, followed by

BOI, ICICI and INDUSIND (jointly third) having values of 0.16 and 0.13 (both ICICI and INDUSIND). Ranking of the

Banks under study on the basis of Approved Securities to Total Assets is shown in Table-23, which indicates that IDBI Bank

and CANARA Bank are jointly ranked on the top position with highest Approved Securities to Total Assets ratio of 0.23,

followed by PNB and SBI(Jointly second) and HDFC and UBI (jointly third) having values of 0.20 (both PNB and SBI) and

0.19 (both HDFC and UBI).

Result of the group averages of four ratios of Liquidity is expressed in Table-24, which indicates that BOI bank is ranked at

Top in this category with group average of 2.25 followed by BOB bank, CANARA bank and PNB with average of 2.75, 3.00

and 3.25 due to better performance of these public sector banks in all the four parameters of Liquidity. Private sector banks

have to make more efforts in terms of Liquidity parameter to get better results in future.

6.2 Composite Ranking (Overall Performance) of Selected Public and Private sector Banks

Composite Ranking of the all the 11 Banks under study on the basis of CAMEL Analysis is shown in Table-25(annex.) on the

basis of performance in last four Financial years 2014-2017, the Table depicts that on the basis of this analysis INDUSIND

Bank is at First Position followed by HDFC Bank , ICICI Bank and AXIS Bank. SBI is at fifth position and top among the

public sector banks.

6.3 Findings and Suggestions

The paper brings out that Indusind bank, HDFC bank, ICICI bank, AXIS bank and SBI bank are occupying the top five

positions while BOB, BOI, PNB, UBI , Canara bank and IDBI are on bottom six positions. In top five positions, only one

public sector bank i.e. SBI has managed to secure the position and the other four are all selected private sector banks. All the

bottom six banks are public sector banks. The minute analysis of the present study puts the light on the fact that all private

sector banks have shown sound performance on capital adequacy, asset quality, management efficiency and earning quality

parameter. However, on the basis of liquidity, public sector banks have shown better performance as compared to private

sector banks. Amongst public sector banks, only SBI has shown consistent performance on all the parameters and has fitted

itself among top five banks on the yardstick of CAMEL model. All the other public sector banks have to work to improve

capital adequacy, asset quality, management efficiency and earning quality.

ISSN: 2249-0558 Impact Factor: 7.119

263 International journal of Management, IT and Engineering http://www.ijmra.us, Email: [email protected]

7. Conclusion

Banking system of a country influences its economy significantly. Reserve bank of India adopted CAMEL rating system in

1996 along with other existing techniques and procedures in order to evaluate the performance of the banks. The present study

analyses the performance of eleven banks (4 private sector and 7 public sector ) on the basis of CAMEL model. The results

show that private sector banks outperform public sector banks and first four ranks go to the credit of all the selected private

sector banks. The private sector banks have to improve performance on liquidity aspect and public sector banks have to focus

on capital adequacy, asset quality, management efficiency and earning quality.

References

Articles a) A Purohit, P. B. (2018). A Camel model analysis of selected public and private sector banks in India. ASAR International

Conference.

b) Garg, K. (2015). An empirical analysis of profitability position of selected private sector banks in India. Journal of Management

Sciences and Technology , 2 (3), 22-28.

c) Meena. (2016). Financial Analysis of Select Banks using Camel approach a study with reference to Indian Banking

Industry. International Journal of reseach and scientific innovation , 3 (10), 30-35.

d) Misra, A. (2013). A Camel Model analysis of State Bank Group. World Journal of Social Sciences , 3 (4), 36-55.

e) R, G. (2014). An analysis of Indian Public sector Banks using Camel approach. IOSR Journal of Business and

Management , 16 (1), 94-102.

f) Singh, A. K. (2015). An analysis of profitability position of private banks in India. International Journal of Scientific

and Research Publications , 5 (5), 1-11.

g) Srinivasan, S. (2016). A Camel model analysis of Public,Private and Foreign Sector Banks in India. Pacific Business

Review International , 8 (9), 45-57.

Websites 1) www.moneycontrol.com/financials/ 2) https://www.sbi.co.in/ 3) https://www.pnbindia.in/ 4) www.bankofbaroda.co.in/ 5) www.hdfcbank.com/ 6) www.icicibank.com/ 7) www.axisbank.com/ 8) https://www.rbi.org.in/scripts/AnnualReportMainDisplay.aspx

9) www.canarabank.in

10) www.unionbankofindia.co.in

11) www.bankofindia.co.in

12) www.idbi.com

13) www.indusind.com

ISSN: 2249-0558 Impact Factor: 7.119

264 International journal of Management, IT and Engineering http://www.ijmra.us, Email: [email protected]

Annexure

Table 1: Capital Adequacy Ratio Table 2: Advance To Assets Ratio

BANK 2014 2015 2016 2017 AVG RANK

SBI 0.66 0.63 0.63 0.55 0.62 4

HDFC 0.62 0.62 0.66 0.64 0.64 2

ICICI 0.6 0.6 0.6 0.6 0.60 5

PNB 0.64 0.64 0.63 0.58 0.62 4

AXIS 0.6 0.61 0.64 0.62 0.62 4

Canara 0.61 0.6 0.59 0.59 0.60 5

BOB 0.6 0.6 0.57 0.55 0.58 6

UBI 0.65 0.67 0.66 0.63 0.65 1

IDBI 0.6 0.59 0.58 0.53 0.58 6

BOI 0.65 0.65 0.59 0.59 0.62 4

Indusind 0.63 0.63 0.63 0.63 0.63 3

Table 3: Debt Equity Ratio Table 4:Govt. Sec. To Total Investment

BANK 2014 2015 2016 2017 AVG RANK

SBI 0.76 0.76 0.77 0.77 0.77 6

HDFC 0.78 0.72 0.77 0.76 0.76 7

ICICI 0.54 0.58 0.7 0.7 0.63 9

PNB 0.78 0.82 0.8 0.79 0.80 4

AXIS 0.61 0.62 0.71 0.72 0.67 8

Canara 0.85 0.86 0.89 0.9 0.88 2

BOB 0.83 0.81 0.86 0.88 0.85 3

UBI 0.74 0.78 0.8 0.79 0.78 5

IDBI 0.65 0.69 0.88 0.9 0.78 5

BOI 0.88 0.88 0.9 0.89 0.89 1

Indusind 0.71 0.72 0.81 0.86 0.78 5

BANK 2014 2015 2016 2017 AVG RANK

SBI 12.44 12 13.12 13.11 12.67 5

HDFC 16.07 16.79 15.53 14.55 15.74 2

ICICI 17.7 17.02 16.64 17.39 17.19 1

PNB 11.52 12.21 11.28 11.66 11.67 7

AXIS 16.07 15.09 15.29 14.95 15.35 3

Canara 10.63 10.56 11.08 12.86 11.28 9

BOB 12.28 12.61 13.18 12.24 12.58 6

UBI 10.8 10.22 10.08 11.79 10.72 11

IDBI 11.68 11.76 11.67 10.7 11.45 8

BOI 9.97 10.73 12.01 12.14 11.21 10

Indusind 13.83 12.09 15.5 15.31 14.18 4

BANK 2014 2015 2016 2017 AVG RANK

SBI 14.73 15.18 14.9 14.4 14.80 6

HDFC 10.31 8.52 8.75 8.66 9.06 3

ICICI 7.12 7.03 7.03 6.72 6.98 1

PNB 13.92 13.93 15.76 15.69 14.83 7

AXIS 9.03 9.34 8.88 9.79 9.26 4

Canara 15.61 16.2 16.5 16.32 16.16 8

BOB 17.33 16.95 15.7 16.24 16.56 9

UBI 18.15 18.27 16.67 17.88 17.74 10

IDBI 12.92 13.6 12.34 14.58 13.36 5

BOI 18.16 18.67 18.66 19.36 19.71 11

Indusind 8.64 9.26 6.92 7.66 8.12 2

ISSN: 2249-0558 Impact Factor: 7.119

265 International journal of Management, IT and Engineering http://www.ijmra.us, Email: [email protected]

Table 5: Composite Capital Adequacy

BANK Capital Adequacy

Ratio

Advance to Total

Assets Debt Equity

Govt Securities to Total

Investment Group Rank

Ratio Rank Ratio Rank Ratio Rank Ratio Rank AVG Rank

SBI 12.67 5 0.62 4 14.80 6 0.77 6 5.25 4

HDFC 15.74 2 0.64 2 9.06 3 0.76 7 3.50 1

ICICI 17.19 1 0.60 5 6.98 1 0.63 9 4.00 2

PNB 11.67 7 0.62 4 14.83 7 0.80 4 5.50 5

AXIS 15.35 3 0.62 4 9.26 4 0.67 8 4.75 3

Canara 11.28 9 0.60 5 16.16 8 0.88 2 6.00 6

BOB 12.58 6 0.58 6 16.56 9 0.85 3 6.00 6

UBI 10.72 11 0.65 1 17.74 10 0.78 5 6.75 8

IDBI 11.45 8 0.58 6 13.36 5 0.78 5 6.00 6

BOI 11.21 10 0.62 4 19.71 11 0.89 1 6.50 7

Indusind 14.18 4 0.63 3 8.12 2 0.78 5 3.50 1

Table 6: Net NPAs to net advances Table 7: Total investment to total assets

BANK 2014 2015 2016 2017 AVG RANK

SBI 0.24 0.26 0.24 0.3 0.26 5

HDFC 0.25 0.28 0.23 0.25 0.25 4

ICICI 0.3 0.29 0.22 0.21 0.26 5

PNB 0.26 0.25 0.24 0.26 0.25 4

AXIS 0.3 0.29 0.23 0.21 0.26 5

Canara 0.26 0.27 0.26 0.26 0.26 5

BOB 0.18 0.17 0.18 0.19 0.18 1

UBI 0.26 0.25 0.22 0.25 0.25 4

IDBI 0.31 0.34 0.26 0.26 0.29 6

BOI 0.2 0.19 0.19 0.2 0.20 2

Indusind 0.25 0.23 0.22 0.21 0.23 3

BANK 2014 2015 2016 2017 AVG RANK

SBI 2.57 2.12 3.81 3.71 3.05 5

HDFC 0.27 0.25 0.28 0.33 0.28 1

ICICI 0.97 1.61 2.98 5.43 2.75 4

PNB 2.85 4.06 8.61 7.81 5.83 10

AXIS 0.44 0.46 0.74 2.27 0.98 3

Canara 1.98 2.65 6.42 6.33 4.35 8

BOB 1.52 1.89 5.06 4.72 3.30 6

UBI 2.33 2.71 5.25 6.57 4.22 7

IDBI 2.48 2.88 6.78 13.21 6.34 11

BOI 2 3.36 7.79 6.9 5.01 9

Indusind 0.33 0.31 0.36 0.39 0.35 2

ISSN: 2249-0558 Impact Factor: 7.119

266 International journal of Management, IT and Engineering http://www.ijmra.us, Email: [email protected]

Table 8 : Net NPAs To Total Assets

Table 9 : Composite Asset Quality

BANK Net NPA to Net Advances Total Investment to Total Assets Net NPA to Total Assets Group Rank

Ratio Rank Ratio Rank Ratio Rank AVG Rank

SBI 3.05 5 0.26 5 0.019 5 4.67 5

HDFC 0.28 1 0.25 4 0.002 1 2.00 1

ICICI 2.75 4 0.26 5 0.017 4 4.00 4

PNB 5.83 10 0.25 4 0.035 9 7.33 8

AXIS 0.98 3 0.26 5 0.006 3 3.33 2

Canara 4.35 8 0.26 5 0.026 6 6.00 7

BOB 3.30 6 0.18 1 0.019 5 3.67 3

UBI 4.22 7 0.25 4 0.028 7 5.67 6

IDBI 6.34 11 0.29 6 0.035 9 8.33 9

BOI 5.01 9 0.20 2 0.030 8 6.00 7

Indusind 0.35 2 0.23 3 0.002 1 2.00 1

BANK 2014 2015 2016 2017 AVG RANK

SBI 0.013 0.01 0.023 0.028 0.019 4

HDFC 0.002 0.002 0.002 0.002 0.002 1

ICICI 0.006 0.01 0.018 0.033 0.017 3

PNB 0.018 0.024 0.053 0.045 0.035 8

AXIS 0.003 0.003 0.005 0.014 0.006 2

Canara 0.012 0.016 0.038 0.037 0.026 5

BOB 0.009 0.011 0.028 0.026 0.019 4

UBI 0.015 0.018 0.035 0.042 0.028 6

IDBI 0.015 0.017 0.039 0.069 0.035 8

BOI 0.013 0.022 0.046 0.04 0.030 7

Indusind 0.002 0.002 0.002 0.002 0.002 1

ISSN: 2249-0558 Impact Factor: 7.119

267 International journal of Management, IT and Engineering http://www.ijmra.us, Email: [email protected]

Table 10: Total Advances to Total Deposits Table 11: Business Per Employee

BANK 2014 2015 2016 2017 AVG RANK

SBI 106.38 123.4 141.1 162.4 133.32 8

HDFC 89 101 113.9 123.6 106.88 9

ICICI 74.7 83.2 94.3 98.9 87.78 10

PNB 128.3 131.9 135.9 141.7 134.45 7

AXIS 123 137.1 148.4 140 137.13 6

Canara 143.84 143.5 144.46 144.28 144.02 5

BOB 186.5 188.9 168 174.9 179.58 3

UBI 137.6 144.6 155.1 164.3 150.40 4

IDBI 246.53 262.1 251.8 234.5 248.73 1

BOI 196.3 206.9 179.6 194 194.20 2

Indusind 71.71 71.92 76.46 91.63 77.93 11

Table 12:Profit Per Employee Table 13: Return on Equity

BANK 2014 2015 2016 2017 AVG RANK

SBI 10.03 10.62 7.3 6.31 8.57 5

HDFC 21.28 19.37 18.26 17.95 19.22 1

ICICI 14.02 14.55 11.43 10.33 12.58 4

PNB 9.75 8.17 5.81 3.31 6.76 7

AXIS 17.43 17.75 16.81 6.76 14.69 3

Canara 8.95 8.79 -8.86 3.44 3.08 8

BOB 13.36 8.96 -13.48 3.44 3.07 9

UBI 9.48 9.32 6.34 2.37 6.88 6

IDBI 5.00 3.64 -14.08 -20.52 -6.49 11

BOI 10.14 5.57 -19.5 -5.04 -2.21 10

Indusind 16.89 18.22 16.14 14.96 16.55 2

BANK 2014 2015 2016 2017 AVG RANK

SBI 0.86 0.82 0.85 0.77 0.83 5

HDFC 0.82 0.81 0.85 0.86 0.84 4

ICICI 1.02 1.07 1.03 0.95 1.02 1

PNB 0.77 0.76 0.78 0.67 0.75 8

AXIS 0.83 0.88 0.96 0.92 0.90 3

Canara 0.72 0.7 0.68 0.69 0.70 10

BOB 0.7 0.69 0.67 0.64 0.68 11

UBI 0.77 0.81 0.78 0.76 0.78 7

IDBI 0.84 0.8 0.81 0.71 0.79 6

BOI 0.78 0.76 0.7 0.68 0.73 9

Indusind 0.91 0.93 0.95 0.89 0.92 2

BANK 2014 2015 2016 2017 AVG RANK

SBI 0.49 0.6 0.47 0.51 0.52 6

HDFC 1.2 1 1.5 1.6 1.33 3

ICICI 1.4 1.6 1.4 1.2 1.4 2

PNB 0.5 0.5 -0.6 0.2 0.15 9

AXIS 1.5 1.7 1.8 0.7 1.43 1

Canara 0.5 0.5 -0.5 0.2 0.18 8

BOB 1 0.7 -1 2.6 0.83 5

UBI 0.5 0.5 0.4 0.2 0.4 7

IDBI 0.68 0.5 -2.1 -2.8 -0.93 11

BOI 0.63 0.37 -1.22 -0.32 -0.14 10

Indusind 0.9 0.94 0.99 1.13 0.99 4

ISSN: 2249-0558 Impact Factor: 7.119

268 International journal of Management, IT and Engineering http://www.ijmra.us, Email: [email protected]

Table 14: Composite Management Efficiency

BANK Total Advances to Total

Deposits

Business Per

Employee

Profit Per

Employee

Return on Equity

Ratio Group Rank

Ratio Rank Millions Rank Millions Rank Ratio Rank AVG Rank

SBI 0.83 5 133.32 8 0.52 6 8.57 5 6.00 4

HDFC 0.84 4 106.88 9 1.33 3 19.22 1 4.25 2

ICICI 1.02 1 87.78 10 1.4 2 12.58 4 4.25 2

PNB 0.75 8 134.45 7 0.15 9 6.76 7 7.75 7

AXIS 0.90 3 137.13 6 1.43 1 14.69 3 3.25 1

Canara 0.70 10 144.02 5 0.18 8 3.08 8 7.75 7

BOB 0.68 11 179.58 3 0.83 5 3.07 9 7.00 5

UBI 0.78 7 150.40 4 0.4 7 6.88 6 6.00 4

IDBI 0.79 6 248.73 1 -0.93 11 -6.49 11 7.25 6

BOI 0.73 9 194.20 2 -0.14 10 -2.21 10 7.75 7

Indusind 0.92 2 77.93 11 0.99 4 16.55 2 4.75 3

Table 15: Interest Income To Total Income Table 16: Operating Profit To Total Assets

BANK 2014 2015 2016 2017 AVG RANK

SBI 1.91 2.1 1.96 2.01 2.00 6

HDFC 3.22 3.22 3.21 3.21 3.22 3

ICICI 2.93 3.18 3.49 3.55 3.29 1

PNB 2.21 2.07 1.78 2.1 2.04 5

AXIS 3.17 3.17 3.22 3.08 3.16 4

Canara 1.5 1.34 1.3 1.57 1.43 10

BOB 1.54 1.44 1.27 1.61 1.47 9

UBI 1.57 1.58 1.44 1.73 1.58 7

IDBI 1.74 1.67 1.47 1.24 1.53 8

BOI 1.64 1.26 0.98 1.57 1.36 11

Indusind 3.24 3.12 3.25 3.39 3.25 2

BANK 2014 2015 2016 2017 AVG RANK

SBI 0.83 0.81 0.81 0.77 0.81 5

HDFC 0.84 0.84 0.85 0.85 0.85 4

ICICI 0.81 0.8 0.77 0.74 0.78 7

PNB 0.9 0.89 0.88 0.84 0.88 3

AXIS 0.81 0.81 0.81 0.79 0.81 5

Canara 0.91 0.91 0.9 0.85 0.89 2

BOB 0.9 0.91 0.9 0.86 0.89 2

UBI 0.91 0.9 0.9 0.87 0.90 1

IDBI 0.9 0.88 0.89 0.88 0.89 2

BOI 0.9 0.91 0.92 0.85 0.90 1

Indusind 0.81 0.8 0.78 0.78 0.79 6

ISSN: 2249-0558 Impact Factor: 7.119

269 International journal of Management, IT and Engineering http://www.ijmra.us, Email: [email protected]

Table 17 :Net Interest Margin To Total Assets Table 18: Return on Assets

BANK 2014 2015 2016 2017 AVG RANK

SBI 0.65 0.68 0.46 0.41 0.55 5

HDFC 2 2.02 1.89 1.88 1.95 1

ICICI 1.78 1.86 1.49 1.35 1.62 3

PNB 0.64 0.53 -0.61 0.19 0.19 7

AXIS 1.78 1.83 1.72 0.65 1.5 4

Canara 0.54 0.55 -0.52 0.2 0.19 7

BOB 0.75 0.49 -0.78 0.2 0.17 8

UBI 0.52 0.49 0.35 0.13 0.37 6

IDBI 0.41 0.29 -1.09 -1.37 -0.44 9

BOI 0.51 0.27 0.94 -0.24 0.37 6

Indusind 1.81 1.9 1.91 1.86 1.87 2

Table 19 :Composite Earning Quality

BANK

Interest Income to

Total Income

Operating Profit to

Total Assets

Net Interest Margin

to Total Assets

Return on Asset

Ratio Group Rank

Ratio Rank Ratio Rank Ratio Rank Ratio Rank AVG Rank

SBI 0.81 5 2.00 6 2.71 5 0.55 5 5.25 5

HDFC 0.85 4 3.22 3 4.14 1 1.95 1 2.25 1

ICICI 0.78 7 3.29 1 3.00 4 1.62 3 3.75 3

PNB 0.88 3 2.04 5 2.65 6 0.19 7 5.25 5

AXIS 0.81 5 3.16 4 3.30 3 1.5 4 4.00 4

Canara 0.89 2 1.43 10 1.84 10 0.19 7 7.25 8

BOB 0.89 2 1.47 9 1.93 9 0.17 8 7.00 7

UBI 0.90 1 1.58 7 2.22 7 0.37 6 5.25 5

IDBI 0.89 2 1.53 8 1.69 11 -0.44 9 7.50 9

BOI 0.90 1 1.36 11 1.96 8 0.37 6 6.50 6

Indusind 0.79 6 3.25 2 3.59 2 1.87 2 3.00 2

BANK 2014 2015 2016 2017 AVG RANK

SBI 2.93 2.86 2.6 2.44 2.71 5

HDFC 4.14 4.14 4.15 4.13 4.14 1

ICICI 2.91 3.07 3.11 2.91 3.00 4

PNB 3.14 2.87 2.41 2.16 2.65 6

AXIS 3.3 3.37 3.36 3.17 3.30 3

Canara 1.98 1.86 1.77 1.74 1.84 10

BOB 1.98 1.92 1.84 1.98 1.93 9

UBI 2.37 2.3 2.11 2.08 2.22 7

IDBI 1.85 1.68 1.66 1.56 1.69 11

BOI 2.11 1.91 1.91 1.91 1.96 8

Indusind 3.61 3.44 3.55 3.77 3.59 2

ISSN: 2249-0558 Impact Factor: 7.119

270 International journal of Management, IT and Engineering http://www.ijmra.us, Email: [email protected]

Table 20: Liquid Assets to Total Assets Table 21 :Liquid Assets to Demand Deposits

BANK 2014 2015 2016 2017 AVG RANK

SBI 1.19 1.36 1.2 1.45 1.30 5

HDFC 0.64 0.49 0.44 0.42 0.50 11

ICICI 0.96 0.85 1.02 1.01 0.96 7

PNB 1.44 1.69 2.03 1.93 1.77 4

AXIS 0.58 0.64 0.52 0.58 0.58 10

Canara 2.53 2.45 2.86 2.61 2.61 3

BOB 2.61 2.81 3.87 3.54 3.21 2

UBI 1.02 1.06 0.98 1.25 1.08 6

IDBI 0.68 0.48 0.57 0.96 0.67 9

BOI 2.84 3.56 4.22 3.38 3.50 1

Indusind 0.69 0.87 0.65 0.95 0.79 8

Table 22: Liquid Assets to Total Deposits Table 23 :Approved Securities to Total Assets

BANK 2014 2015 2016 2017 AVG RANK

SBI 0.186 0.196 0.185 0.231 0.20 2

HDFC 0.193 0.204 0.177 0.188 0.19 3

ICICI 0.161 0.166 0.157 0.146 0.16 6

PNB 0.204 0.202 0.185 0.205 0.20 2

AXIS 0.182 0.178 0.166 0.155 0.17 5

Canara 0.219 0.229 0.23 0.233 0.23 1

BOB 0.147 0.138 0.154 0.164 0.15 7

UBI 0.197 0.193 0.179 0.197 0.19 3

IDBI 0.204 0.235 0.233 0.232 0.23 1

BOI 0.175 0.17 0.176 0.181 0.18 4

Indusind 0.177 0.164 0.18 0.176 0.17 5

BANK 2014 2015 2016 2017 AVG RANK

SBI 0.07 0.077 0.069 0.079 0.07 6

HDFC 0.081 0.062 0.055 0.057 0.06 7

ICICI 0.07 0.065 0.083 0.098 0.08 5

PNB 0.082 0.092 0.108 0.123 0.10 3

AXIS 0.074 0.078 0.063 0.084 0.07 6

Canara 0.091 0.089 0.103 0.101 0.10 3

BOB 0.198 0.207 0.199 0.217 0.21 1

UBI 0.065 0.059 0.072 0.073 0.07 6

IDBI 0.051 0.041 0.044 0.09 0.06 7

BOI 0.107 0.123 0.163 0.153 0.14 2

Indusind 0.078 0.099 0.072 0.104 0.09 4

BANK 2014 2015 2016 2017 AVG RANK

SBI 0.091 0.102 0.091 0.105 0.10 6

HDFC 0.108 0.081 0.071 0.076 0.08 7

ICICI 0.125 0.117 0.142 0.155 0.13 3

PNB 0.1 0.113 0.135 0.142 0.12 4

AXIS 0.101 0.112 0.093 0.121 0.11 5

Canara 0.107 0.103 0.118 0.119 0.11 5

BOB 0.23 0.24 0.233 0.25 0.24 1

UBI 0.078 0.071 0.085 0.087 0.08 7

IDBI 0.072 0.056 0.061 0.122 0.08 7

BOI 0.129 0.144 0.193 0.178 0.16 2

Indusind 0.112 0.145 0.109 0.147 0.13 3

ISSN: 2249-0558 Impact Factor: 7.119

271 International journal of Management, IT and Engineering http://www.ijmra.us, Email: [email protected]

Table 24 : Composite Liquidity

BANK Liquid Assets to

Total Assets

Liquid Assets to

Demand Deposits

Liquid Assets to

Total Deposits

Approved Securities to

Total Assets Group Rank

Ratio Rank Ratio Rank Ratio Rank Ratio Rank AVG Rank

SBI 0.07 6 1.30 5 0.10 6 0.20 2 4.75 5

HDFC 0.06 7 0.50 11 0.08 7 0.19 3 7.00 11

ICICI 0.08 5 0.96 7 0.13 3 0.16 6 5.25 7

PNB 0.10 3 1.77 4 0.12 4 0.20 2 3.25 4

AXIS 0.07 6 0.58 10 0.11 5 0.17 5 6.50 10

Canara 0.10 3 2.61 3 0.11 5 0.23 1 3.00 3

BOB 0.21 1 3.21 2 0.24 1 0.15 7 2.75 2

UBI 0.07 6 1.08 6 0.08 7 0.19 3 5.50 8

IDBI 0.06 7 0.67 9 0.08 7 0.23 1 6.00 9

BOI 0.14 2 3.50 1 0.16 2 0.18 4 2.25 1

Indusind 0.09 4 0.79 8 0.13 3 0.17 5 5.00 6

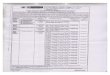

Table 25: Composite Ranking (Overall Performance) of Selected Public and Selected Private Sector

Banks

BANK C A M E L Average Rank

SBI 5.25 4.67 6.00 5.25 4.75 5.18 5

HDFC 3.50 2.00 4.25 2.25 7.00 3.80 2

ICICI 4.00 4.00 4.25 3.75 5.25 4.25 3

PNB 5.50 7.33 7.75 5.25 3.25 5.82 8

AXIS 4.75 3.33 3.25 4.00 6.50 4.37 4

Canara 6.00 6.00 7.75 7.25 3.00 6.00 10

BOB 6.00 3.67 7.00 7.00 2.75 5.28 6

UBI 6.75 5.67 6.00 5.25 5.50 5.83 9

IDBI 6.00 8.33 7.25 7.50 6.00 7.02 11

BOI 6.50 6.00 7.75 6.50 2.25 5.80 7

Indusind 3.50 2.00 4.75 3.00 5.00 3.65 1