Embed Size (px)

Citation preview

9M2013 RESULTS PRESENTATION DECEMBER 23, 2013

DISCLAIMER

This presentation does not constitute or form part of and should not be construed as,

an offer to sell or issue or the solicitation of an offer to buy or acquire securities of

Mechel OAO (Mechel) or any of its subsidiaries in any jurisdiction or an inducement to

enter into investment activity. No part of this presentation, nor the fact of its

distribution, should form the basis of, or be relied on in connection with, any contract

or commitment or investment decision whatsoever. Any purchase of securities should

be made solely on the basis of information Mechel files from time to time with the U.S.

Securities and Exchange Commission. No representation, warranty or undertaking,

express or implied, is made as to, and no reliance should be placed on, the fairness,

accuracy, completeness or correctness of the information or the opinions contained

herein. None of the Mechel or any of its affiliates, advisors or representatives shall

have any liability whatsoever (in negligence or otherwise) for any loss howsoever

arising from any use of this presentation or its contents or otherwise arising in

connection with the presentation.

This presentation may contain projections or other forward-looking statements

regarding future events or the future financial performance of Mechel, as defined in

the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995.

We wish to caution you that these statements are only predictions and that actual

events or results may differ materially. We do not intend to update these statements.

We refer you to the documents Mechel files from time to time with the U.S. Securities

and Exchange Commission, including our Form 20-F. These documents contain and

identify important factors, including those contained in the section captioned “Risk

Factors” and “Cautionary Note Regarding Forward-Looking Statements” in our Form

20-F, that could cause the actual results to differ materially from those contained in

our projections or forward-looking statements, including, among others, the

achievement of anticipated levels of profitability, growth, cost and synergy of our

recent acquisitions, the impact of competitive pricing, the ability to obtain necessary

regulatory approvals and licenses, the impact of developments in the Russian

economic, political and legal environment, volatility in stock markets or in the price of

our shares or ADRs, financial risk management and the impact of general business

and global economic conditions.

The information and opinions contained in this document are provided as at the date

of this presentation and are subject to change without notice

2

FINANCIAL HIGHLIGHTS

61% 59% 60% 59%

31% 33% 33% 32%

1% 1% 1% 1%7% 7% 6% 8%

2Q13 3Q13 9M12 9M13

Steel Mining Ferroalloys Power

SEGMENTS OVERVIEW

REVENUE FROM THIRD PARTIES EBITDA BY SEGMENTS

$ Mln

$ Mln

(1) Adjusted EBITDA represents EBTIDA adjusted by forex gain/loss, interest income, net income on the disposal of non-current assets, amount attributable to non-controlling interests gain/loss from remeasurement of

contingent liabilities at fair value, impairment of long-lived assets and goodwill, result of disposed companies (incl.the result from their disposal) provision for amounts due from related parties and losses from discontinued

operations, net of income tax. 4

Steel Mining Ferroalloys Power

EBITDA(1) BY SEGMENTS

2,243 2,089 8,222 6,692

331

88

421

305

88

397

29

96

147124

62

211

127

64

202

148

49

196

Mining Steel Ferroalloys Power Consolidated*

2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

3Q2013

1%

25%

76%

-2%

2Q2013

2%

2%

32%

64%

Declining prices put pressure on consolidated revenue

which is down to $2.1 bn q-o-q

Bad debt provisions and write-offs due to assets disposals

result in a Net Loss of $2.2 bn for 9M2013

Due to lower cash costs and higher volumes Mining

segment EBITDA grew by 17% q-o-q dominating the

consolidated EBITDA with a share of 76% -3

64

-6-0.6

15

0.6

23

533

-4

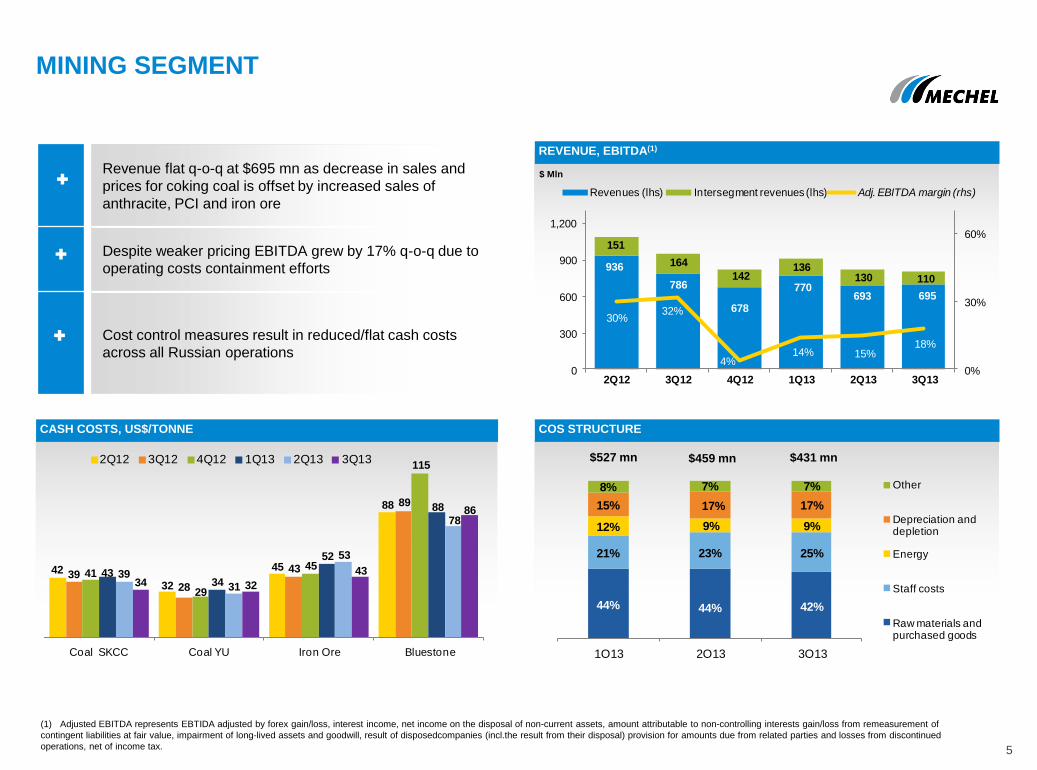

MINING SEGMENT

$ Mln

CASH COSTS, US$/TONNE COS STRUCTURE

$527 mn $431 mn

5

REVENUE, EBITDA(1)

936

786

678

770693 695

151

164

142136

130 110

30%32%

4%14% 15%

18%

0%

30%

60%

0

300

600

900

1,200

2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

Revenues (lhs) Intersegment revenues (lhs) Adj. EBITDA margin (rhs)

42

32

45

88

3928

43

89

41

29

45

115

4334

52

88

3931

53

78

34 32

43

86

Coal SKCC Coal YU Iron Ore Bluestone

2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

44% 44% 42%

21% 23% 25%

12% 9% 9%

15% 17% 17%

8% 7% 7%

1Q13 2Q13 3Q13

Other

Depreciation and depletion

Energy

Staff costs

Raw materials and purchased goods

(1) Adjusted EBITDA represents EBTIDA adjusted by forex gain/loss, interest income, net income on the disposal of non-current assets, amount attributable to non-controlling interests gain/loss from remeasurement of

contingent liabilities at fair value, impairment of long-lived assets and goodwill, result of disposedcompanies (incl.the result from their disposal) provision for amounts due from related parties and losses from discontinued

operations, net of income tax.

$459 mn

Revenue flat q-o-q at $695 mn as decrease in sales and

prices for coking coal is offset by increased sales of

anthracite, PCI and iron ore

Despite weaker pricing EBITDA grew by 17% q-o-q due to

operating costs containment efforts

Cost control measures result in reduced/flat cash costs

across all Russian operations

42% 37%45%

39%

23%26%

21%24%

8% 7%11%

8%3% 3%

2%2%

8% 9%8%

8%

15% 17%12%

16%

1% 1% 1% 3%

2Q13 3Q13 9M12 9M13

Coking coal Anthracites and PCI Coke Coking products Steam coal Iron ore Other

MINING SEGMENT

6

REVENUE BREAKDOWN BY REGION AVERAGE SALES PRICES FCA, US$/TONNE

*Restated to include middlings

EXTERNAL SALES STRUCTURE

239

129

94

49

84

229

122

80

49

65

214

93

69

5159

207

95

63

52

92

199

83

66

52

77

178

71

5749

78

Coke Coking coal Anthracite and PCI Steam coal* Iron ore

2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

28% 26% 26% 28%

15%14% 14% 14%

1%1%

10%2%

42%42%

29% 39%

8% 10%13%

10%

1% 2% 4% 3%5% 5% 4% 4%

2Q13 3Q13 9M12 9M13

Russia Europe CIS China Asia w/o China Middle East Other

Coking coal sales down 13% q-o-q due to decrease in domestic

demand

Sales of anthracite and PCI grew by 17% q-o-q due to better

demand from Turkey, UK and China

Prices for coal products fall across the board with iron ore

showing better price resilience

Share of coking coal exports to China in 9M13 grows by 49% y-

o-y offsetting lower shipments to CIS due to dwindling solvent

demand

China starts to dominate in sales outstripping domestic

shipments with overall sales share of 39% for 9M2013

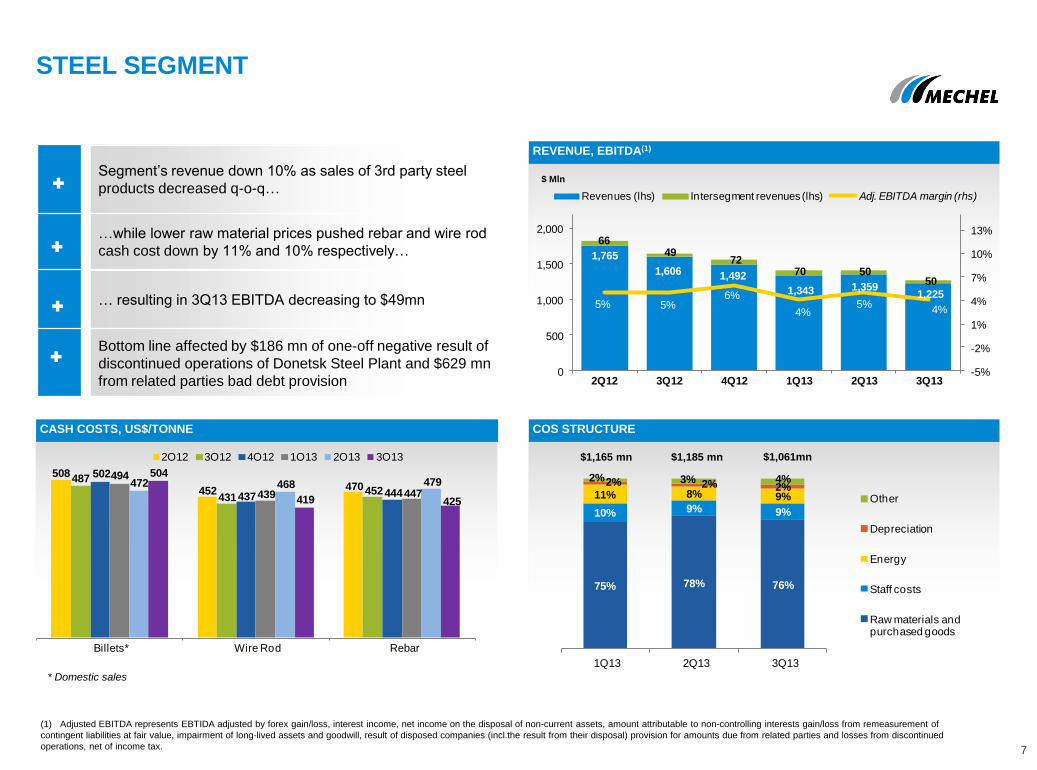

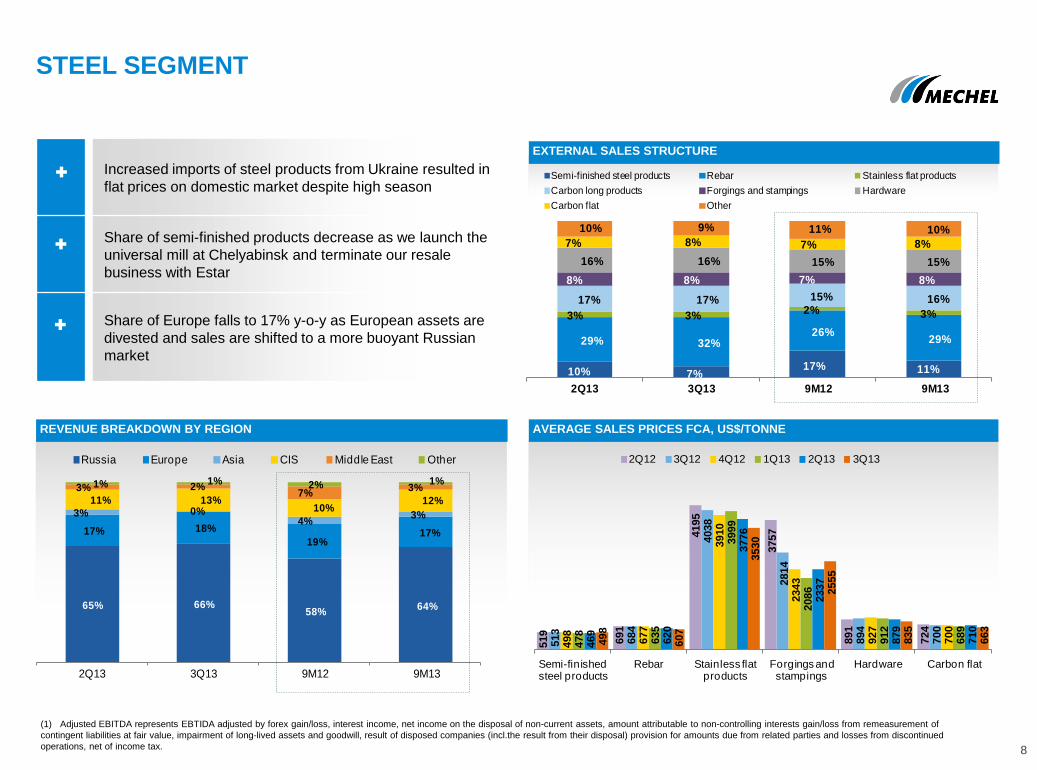

STEEL SEGMENT

7

CASH COSTS, US$/TONNE COS STRUCTURE

REVENUE, EBITDA(1)

$1,165 mn $1,061mn

$ Mln

1,765

1,606 1,492

1,343 1,3591,225

6649

7270 50

50

5% 5%6%

4%5%

4%

-5%

-2%

1%

4%

7%

10%

13%

0

500

1,000

1,500

2,000

2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

Revenues (lhs) Intersegment revenues (lhs) Adj. EBITDA margin (rhs)

508

452 470487

431452

502

437 444

494

439 447472 468 479

504

419 425

Billets* Wire Rod Rebar

2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

75% 78% 76%

10% 9% 9%

11% 8% 9%

2% 2% 2%2% 3% 4%

1Q13 2Q13 3Q13

Other

Depreciation

Energy

Staff costs

Raw materials and purchased goods

(1) Adjusted EBITDA represents EBTIDA adjusted by forex gain/loss, interest income, net income on the disposal of non-current assets, amount attributable to non-controlling interests gain/loss from remeasurement of

contingent liabilities at fair value, impairment of long-lived assets and goodwill, result of disposed companies (incl.the result from their disposal) provision for amounts due from related parties and losses from discontinued

operations, net of income tax.

$1,185 mn

Segment‟s revenue down 10% as sales of 3rd party steel

products decreased q-o-q…

…while lower raw material prices pushed rebar and wire rod

cash cost down by 11% and 10% respectively…

… resulting in 3Q13 EBITDA decreasing to $49mn

Bottom line affected by $186 mn of one-off negative result of

discontinued operations of Donetsk Steel Plant and $629 mn

from related parties bad debt provision

* Domestic sales

65% 66%58%

64%

17% 18%

19%17%

3% 0%4%

3%

11% 13%10%

12%

3% 2%7%

3%1% 1% 2% 1%

2Q13 3Q13 9M12 9M13

Russia Europe Asia CIS Middle East Other

STEEL SEGMENT

8

REVENUE BREAKDOWN BY REGION AVERAGE SALES PRICES FCA, US$/TONNE

EXTERNAL SALES STRUCTURE

10% 7%17% 11%

29% 32%26%

29%

3% 3%2% 3%

17% 17% 15% 16%

8% 8% 7% 8%

16% 16% 15% 15%

7% 8% 7% 8%

10% 9% 11% 10%

2Q13 3Q13 9M12 9M13

Semi-finished steel products Rebar Stainless flat products

Carbon long products Forgings and stampings Hardware

Carbon flat Other

519

691

4195

3757

891

724

513

684

4038

2814

894

700

498

677

3910

2343

927

700

478

635

3999

2086

912

689

469

620

3776

2337

879

710

498

607

3530

2555

835

663

Semi-finished steel products

Rebar Stainless flat products

Forgings and stampings

Hardware Carbon flat

2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

(1) Adjusted EBITDA represents EBTIDA adjusted by forex gain/loss, interest income, net income on the disposal of non-current assets, amount attributable to non-controlling interests gain/loss from remeasurement of

contingent liabilities at fair value, impairment of long-lived assets and goodwill, result of disposed companies (incl.the result from their disposal) provision for amounts due from related parties and losses from discontinued

operations, net of income tax.

Increased imports of steel products from Ukraine resulted in

flat prices on domestic market despite high season

Share of semi-finished products decrease as we launch the

universal mill at Chelyabinsk and terminate our resale

business with Estar

Share of Europe falls to 17% y-o-y as European assets are

divested and sales are shifted to a more buoyant Russian

market

AVERAGE FERROSILICON SALES PRICES AND CASH COSTS, US$/TONNE

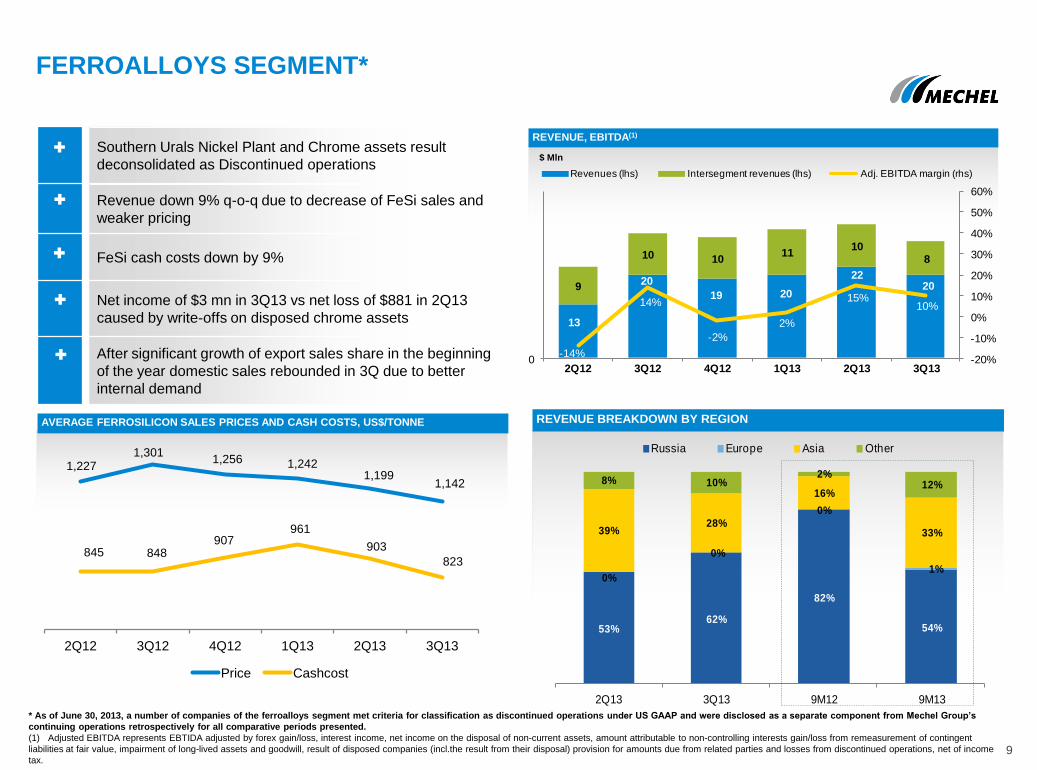

FERROALLOYS SEGMENT*

REVENUE, EBITDA(1)

9

$ Mln

13

20

19 20

22209

10 1011

108

-14%

14%

-2%

2%

15%10%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

02Q12 3Q12 4Q12 1Q13 2Q13 3Q13

Revenues (lhs) Intersegment revenues (lhs) Adj. EBITDA margin (rhs)

* As of June 30, 2013, a number of companies of the ferroalloys segment met criteria for classification as discontinued operations under US GAAP and were disclosed as a separate component from Mechel Group’s

continuing operations retrospectively for all comparative periods presented.

(1) Adjusted EBITDA represents EBTIDA adjusted by forex gain/loss, interest income, net income on the disposal of non-current assets, amount attributable to non-controlling interests gain/loss from remeasurement of contingent

liabilities at fair value, impairment of long-lived assets and goodwill, result of disposed companies (incl.the result from their disposal) provision for amounts due from related parties and losses from discontinued operations, net of income

tax.

Southern Urals Nickel Plant and Chrome assets result

deconsolidated as Discontinued operations

Revenue down 9% q-o-q due to decrease of FeSi sales and

weaker pricing

FeSi cash costs down by 9%

Net income of $3 mn in 3Q13 vs net loss of $881 in 2Q13

caused by write-offs on disposed chrome assets

After significant growth of export sales share in the beginning

of the year domestic sales rebounded in 3Q due to better

internal demand

53%62%

82%

54%

0%

0%

0%

1%

39%28%

16%

33%

8% 10%2%

12%

2Q13 3Q13 9M12 9M13

Russia Europe Asia Other

REVENUE BREAKDOWN BY REGION

1,227 1,301

1,256 1,242 1,199

1,142

845 848 907

961

903

823

2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

Price Cashcost

POWER SEGMENT

10

AVERAGE ELECTRICITY SALES PRICES AND CASH COSTS (RUSSIA), US$/MWH COS STRUCTURE

REVENUE, EBITDA(1)

$ Mln

53.5 54.7 53.856.2

52.554.4

28.030.1

24.5 26.2

29.0

35.0

2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

Sales price Cash costs

89% 86% 87%

4% 4% 3%5% 8% 7%

1% 1% 1%1% 1%

2%

1Q13 2Q13 3Q13

Other

Depreciation

Energy

Staff costs

Raw materials and purchased goods

$249 mn $197 mn

168140

220227

169149

95 98

118 123

10198

2%-2%

4% 7%1%

-2%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

100

200

300

2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

Revenues (lhs) Intersegment revenues(lhs) Adj. EBITDA margin (rhs)

(1) Adjusted EBITDA represents EBTIDA adjusted by forex gain/loss, interest income, net income on the disposal of non-current assets, amount attributable to non-controlling interests gain/loss from remeasurement of

contingent liabilities at fair value, impairment of long-lived assets and goodwill, result of disposed companies (incl.the result from their disposal) provision for amounts due from related parties and losses from discontinued

operations, net of income tax.

$201 mn

Traditional seasonal decrease in revenues and margins

Lower production volumes and seasonal maintenance works

and repairs resulted in cash costs growth

Consolidated P&L

11

REVENUE DYNAMICS REVENUE, EBITDA(1) AND NET PROFIT

Consolidated EBITDA down 3% q-o-q to $196 mn as improvement in Mining segment profitability is not enough to offset declining margins

in steel, power and ferroalloys segments

9M2013 bottom line affected by write offs of $1,085 mn as a result of discontinued operations, $645 mn of bad debt provisions and FX

loss of $151 mn

3Q2013 FINANCIAL PERFORMANCE Q-O-Q HIGHLIGHTS:

$ Mln $ Mln

2,243 2,089

-78-76

0

1,000

2,000

3,000

2Q2013 Volume Price 3Q2013

2881

25522409 2360 2243

2089

421 397147 211 202 196

-823

55

-1114

-321

-1799

-127

15%16%

6% 9% 9%

9%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

(1,900)

(1,400)

(900)

(400)

100

600

1,100

1,600

2,100

2,600

3,100

3,600

2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

Revenue (lhs) Adj. EBITDA (lhs) Net profit (lhs) Adj. EBITDA

(1) Adjusted EBITDA represents EBTIDA adjusted by forex gain/loss, interest income, net income on the disposal of non-current assets, amount attributable to non-controlling interests gain/loss from remeasurement of

contingent liabilities at fair value, impairment of long-lived assets and goodwill, result of disposed companies (incl.the result from their disposal) provision for amounts due from related parties and losses from discontinued

operations, net of income tax.

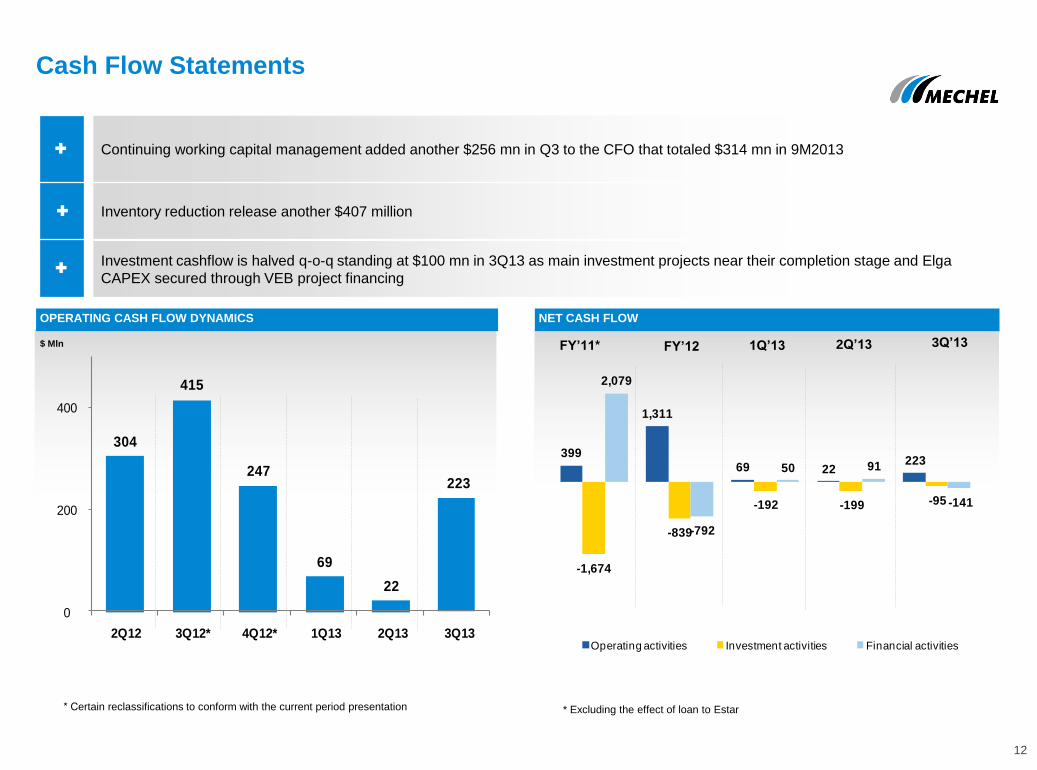

Cash Flow Statements

12

OPERATING CASH FLOW DYNAMICS NET CASH FLOW

Continuing working capital management added another $256 mn in Q3 to the CFO that totaled $314 mn in 9M2013

Inventory reduction release another $407 million

Investment cashflow is halved q-o-q standing at $100 mn in 3Q13 as main investment projects near their completion stage and Elga

CAPEX secured through VEB project financing

$ Mln FY’11* FY’12 1Q’13

* Excluding the effect of loan to Estar

2Q’13 3Q’13

304

415

247

69

22

223

0

200

400

2Q12 3Q12* 4Q12* 1Q13 2Q13 3Q13

399

1,311

69 22223

-1,674

-839

-192 -199 -95

2,079

-792

50 91

-141

Operating activities Investment activities Financial activities

* Сertain reclassifications to conform with the current period presentation

Successful refinancing and improved liquidity to service upcoming maturities

Net debt stable, estimated at $9.4 bln (including financial lease) as

of December 6, 2013

Cash and available credit lines total $0.44 bln as of December 6,

2013

Company succeeded in refinancing of PXF (granting additional

grace period of 12 months and extending the tenor until December

2016), Sberbank (grace period of 15 months, extending the tenor

until December 2018), VTB and GPB. New levels of financial

covenants ratios negotiated (including testing holiday until

December 2014)

DEBT PROFILE AS OF DECEMBER 6, 2013

RUR 58%

USD 35%

EUR 7%

Russian

Banks

69%

14

DEBT MATURITY SCHEDULE AS OF DECEMBER 6, 2013 ** DEBT MATURITY SCHEDULE AS OF JUNE 1, 2013 WITH PRO FORMA*

Foreign

Banks

20%

Bonds

11%

** assuming refinancing of GBP lines of 2009 and changes in schedule of VTB – lease from December 20, 2013

DRAFT

123 84 - - - -

506

1,788 1,866 1,630

1,336

584

81

472 314

472

-

-

156

- - -

-

-

97

139

86 51

37

15

965

2,483

2,267 2,153

1,373

598

0

500

1000

1500

2000

2500

3000

1.6.13 2013 2014 2015 2016 2017 2018 and after

Renewable lines Other term loans

Expiration of put options on bonds Maturity of bonds

Expiration of financial lease

79 131 99

1,306

2,146 2,153

1,447

780

429

198 297

-

-

-

- -

-

-

13

168

118 77

57

24

191

2,034

2,461 2,527

1,504

803

0

500

1000

1500

2000

2500

3000

20.12.13 2013 2014 2015 2016 2017 2018 and after

Renewable lines Other term loans

Expiration of put options on bonds Maturity of bonds

Expiration of financial lease

* assuming refinancing of GBP lines according to the terms of executed committed credit facilities

69 340 31

440

Cash

Other undrawn credit lines

ECA undrawn amount

283

367

141

790

Cash

Other undrawn credit lines

ECA undrawn amount

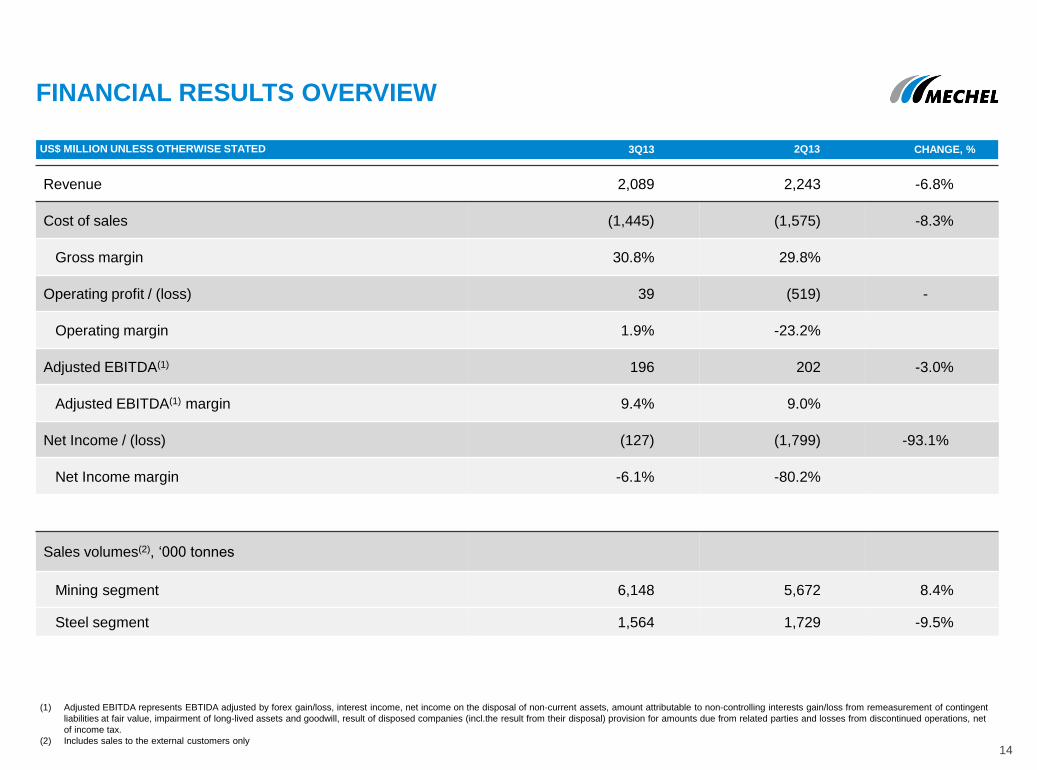

Revenue 2,089 2,243 -6.8%

Cost of sales (1,445) (1,575) -8.3%

Gross margin 30.8% 29.8%

Operating profit / (loss) 39 (519) -

Operating margin 1.9% -23.2%

Adjusted EBITDA(1) 196 202 -3.0%

Adjusted EBITDA(1) margin 9.4% 9.0%

Net Income / (loss) (127) (1,799) -93.1%

Net Income margin -6.1% -80.2%

Sales volumes(2), „000 tonnes

Mining segment 6,148 5,672 8.4%

Steel segment 1,564 1,729 -9.5%

FINANCIAL RESULTS OVERVIEW

(1) Adjusted EBITDA represents EBTIDA adjusted by forex gain/loss, interest income, net income on the disposal of non-current assets, amount attributable to non-controlling interests gain/loss from remeasurement of contingent

liabilities at fair value, impairment of long-lived assets and goodwill, result of disposed companies (incl.the result from their disposal) provision for amounts due from related parties and losses from discontinued operations, net

of income tax.

(2) Includes sales to the external customers only

US$ MILLION UNLESS OTHERWISE STATED 3Q13 2Q13 CHANGE, %

14