Embed Size (px)

Citation preview

PROOF

vii

Preface ix

List of Figures and Tables xi

List of Abbreviations xii

Acknowledgements xiii

About the Author xv

1 Excise Taxation in Context 1 English Excise Taxation 8 Fiscal Sociology and Economic Thought 11 State Formation or State Building? 14 Notes on Sources and Methodology 16 Chapter Organisation 21

2 The Introduction of the Excises 25 A Matter of ‘Necessity?’ Introduction and Response 28 Administration by Legislation 31 The Origins of the Committee for Regulating the Excise 43 The Limits of ‘Popular Politics’ 49

3 The Excises under the Long Parliament, 1647–1648 55 The Smithfield Riot in a Wider Context 55 The Advent of Excise-Backed Paper 58 The Financial Data: Gross and Net Receipts 62 The Financial Data: Advances, Loans and Anticipations 72 Conclusions 77

4 The Commonwealth Excise, 1649–1653 79 Remodelling the Excise 80 The Introduction of Farming 84 Regulating the Excise 89 Judicial Powers 95 Financial Data 98 Conclusions 106

Contents

PROOF

PROOF

viii Contents

5 The Case of the Soap Boilers 109 The Immediate Context 110 The Caroline Soap Patents 114 The Soap Excise 119 Conclusions 124

6 The Protectorate Excise, 1654–1659 129 The Petition of 1658: An Ex-Post Judgement 129 The New Regime: The Problem Ex-Ante 134 The Struggle for Control 140 Financial Data 149 Conclusions 155

7 The Restoration Excise, 1660–1663 157 The Restoration Financial Settlement 158 The Lord Treasurer and the Excise 165 Excise Establishment, 1652–1662 173 Conclusions 181

8 The Political Economy of Taxation 183 Standards of Equality 183 Alternative Proposals for Fiscal Reform 189 Pro-Excise Pamphlets 196

9 Looking Forward 201

Notes 213

Biblography 223

Index 237

PROOF

PROOF

1

Conventional accounts of the origins of the British fiscal state have an aversion to exploring in detail the advent of markets for debt securities. Most historians agree that in the British Isles the transition from a late medieval demesne-state to a tax state occurred in the seventeenth cen-tury, culminating in the Financial Revolution of the 1690s (Schumpeter, 1918; Braddick, 1994, pp. 1–21).1 Yet no major work of scholarship has looked closely at the link between the two. For most scholars what began during the Civil Wars and Interregnum reached fruition only after the Revolution of 1688/1689. Some authors may acknowledge that post-1688 finance was built on pre-1688 practices, but few have attempted to reconstruct these practices in any detail, much less to link them to the Financial Revolution and the new species of public borrowing which financed the eighteenth-century state. Those who have done so at all have tended to locate structural change within the Restoration period (Brewer, 1988, p. 95). By overcoming the significant archival challenges of reconstructing Interregnum experiments in public finance, this book illuminates the origins of the durable institutions, structures and practices that formed the foundations of the fiscal state in the British Isles. More importantly, however, especially in the second decade of the twenty-first century, this study firmly locates the origins of the public debt in Interregnum experiments with excise taxation. Failure to adopt forms of long-term debt associated with post-1688 finance arose not from a lack of familiarity with these instruments, but rather political instability and the spectre of regime change foreclosed the possibility at key moments. This finding has significant implications for historians of early modern Britain and for macroeconomic policymakers looking to prescribe the means of reassuring markets and citizens alike of a state’s ‘credible commitment’ to honouring its public debts.

1Excise Taxation in Context

PROOF

PROOF

2 Excise Taxation and the Origins of Public Debt

As Davenant’s reflections in Discourses on the Public Revenues of 1698 should remind modern readers, advising governments about how to best manage their debts is not a distinctly modern preoccupation. The advent of the Washington Consensus, however, has made institution building a priority for nation-states and for supranational and global governance structures. Almost twenty-five years after North and Weingast’s first publication in 1989 of their famous ‘Constitutions and Commitments’ article, historians and economists alike have identified four key elements of ‘credible commitment’. Yet each of these factors—parliamentary con-trol over the public finances, transparency in public accounts, account-ability via creditor action and surprisingly deep secondary markets, as well as a stated commitment to maintaining the ‘publike faith’ and the use of common law procedure to adjudicate disputes between taxpay-ers and the regime—were, in fact, in place during the Civil Wars and Interregnum under the Long Parliament and Commonwealth regimes. But they did not, in themselves, produce credible commitment mecha-nisms for generating support for long-term public debt. Rather what the first twenty years of the British experiment with excise taxation teaches modern students of its history is that these are ‘necessary but not suf-ficient’ conditions. Instead there is strong evidence that the most impor-tant ingredient in the durability of commitment mechanisms is also the most elusive and contingent: the perception of the stability and perma-nence of a given regime, whether it be representative and deliberative or monarchical and autocratic.

Four years of archival research for this project uncovered new manu-script material and made possible the re-visitation of known sources that had not been seriously studied for over half a century. Both have yielded a wealth of new information about institutional practices and resistance to them. By drawing together methodological tools employed by historians of public finance, political culture and economic thought, this study assesses what contemporaries learned from successive regimes’ experiments with commodity taxation and elaborates the mechanisms by which the unintended consequences of their actions produced perma-nent structural and even constitutional change. The Financial Revolution emerges as a product of indigenous institutions and practices, not of pre-sumptive English tutelage to ‘Dutch Finance’.

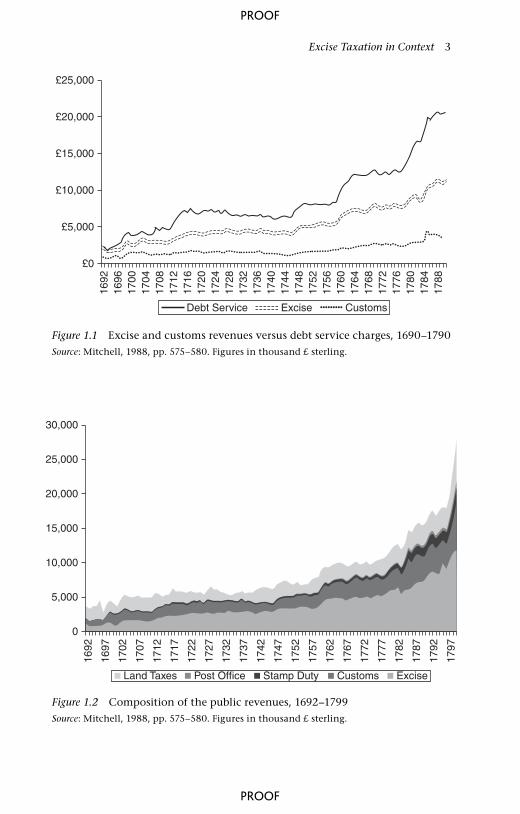

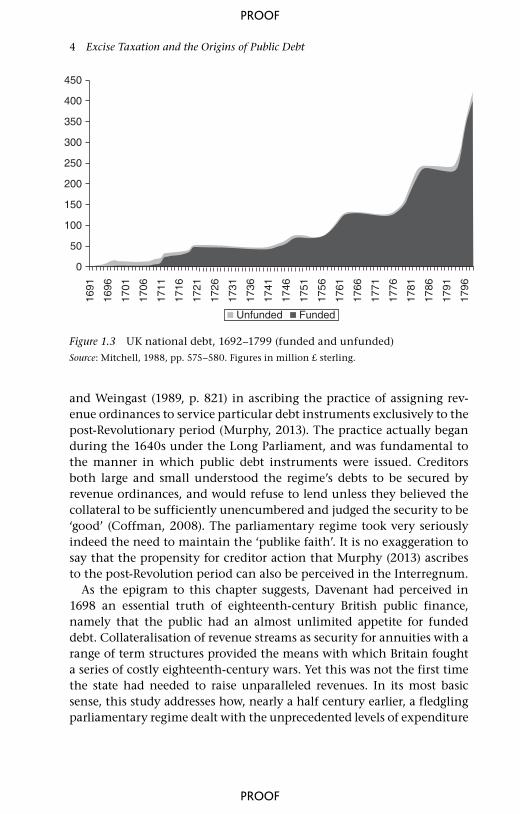

The close connection between excise revenue and government debt service (Figures 1.1–1.3) observable over the course of the eighteenth century arose from the Long Parliament and Commonwealth regimes’ practice of assigning specific revenues to service particular debts (Brewer, 1990; Coffman, 2008). Unfortunately current scholarship follows North

PROOF

PROOF

Excise Taxation in Context 3

Figure 1.1 Excise and customs revenues versus debt service charges, 1690–1790

Source: Mitchell, 1988, pp. 575–580. Figures in thousand £ sterling.

£25,000

£10,000

£5,000

£0

£15,000

£20,00016

9216

9617

0017

0417

0817

1217

1617

2017

2417

2817

3217

3617

4017

4417

4817

5217

5617

6017

6417

6817

7217

7617

8017

8417

88

Debt Service CustomsExcise

30,000

10,000

5,000

0

15,000

20,000

25,000

1692

1697

1702

1707

1712

1717

1722

1727

1732

1737

1742

1747

1752

1757

1762

1767

1772

1777

1782

1787

1792

1797

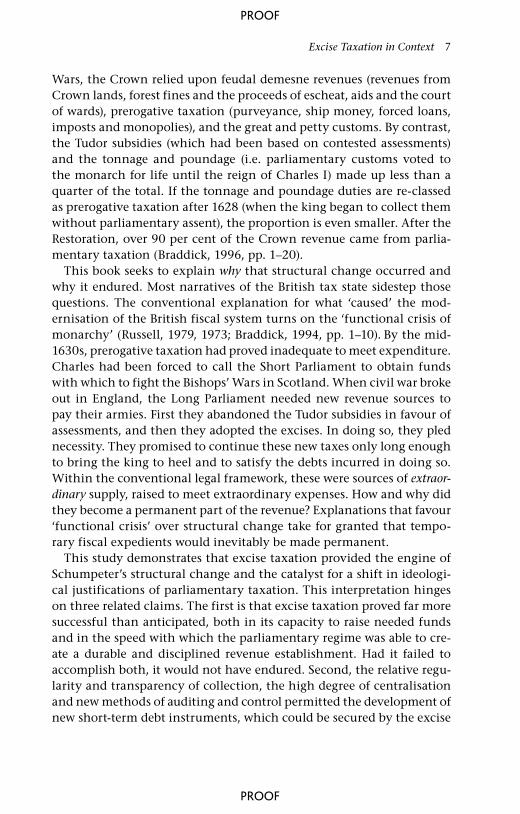

Land Taxes Post Office Stamp Duty Customs Excise

Figure 1.2 Composition of the public revenues, 1692–1799

Source: Mitchell, 1988, pp. 575–580. Figures in thousand £ sterling.

PROOF

PROOF

4 Excise Taxation and the Origins of Public Debt

and Weingast (1989, p. 821) in ascribing the practice of assigning rev-enue ordinances to service particular debt instruments exclusively to the post-Revolutionary period (Murphy, 2013). The practice actually began during the 1640s under the Long Parliament, and was fundamental to the manner in which public debt instruments were issued. Creditors both large and small understood the regime’s debts to be secured by revenue ordinances, and would refuse to lend unless they believed the collateral to be sufficiently unencumbered and judged the security to be ‘good’ (Coffman, 2008). The parliamentary regime took very seriously indeed the need to maintain the ‘publike faith’. It is no exaggeration to say that the propensity for creditor action that Murphy (2013) ascribes to the post-Revolution period can also be perceived in the Interregnum.

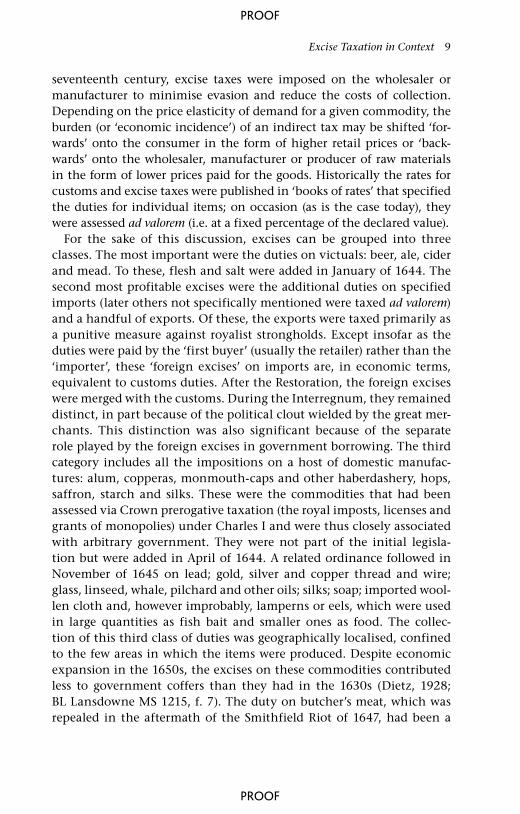

As the epigram to this chapter suggests, Davenant had perceived in 1698 an essential truth of eighteenth-century British public finance, namely that the public had an almost unlimited appetite for funded debt. Collateralisation of revenue streams as security for annuities with a range of term structures provided the means with which Britain fought a series of costly eighteenth-century wars. Yet this was not the first time the state had needed to raise unparalleled revenues. In its most basic sense, this study addresses how, nearly a half century earlier, a fledgling parliamentary regime dealt with the unprecedented levels of expenditure

Figure 1.3 UK national debt, 1692–1799 (funded and unfunded)

Source: Mitchell, 1988, pp. 575–580. Figures in million £ sterling.

450

150

100

50

0

200

250

300

400

350

1691

1696

1701

1706

1711

1716

1721

1726

1731

1736

1741

1746

1751

1756

1761

1766

1771

1776

1781

1786

1791

1796

Unfunded Funded

PROOF

PROOF

Excise Taxation in Context 5

necessary to fight the Civil Wars and then to secure the Commonwealth and Protectorate’s stature on the international stage. Parliament’s success at imposing on a deeply divided kingdom an extra-legal species of indi-rect taxation, which hitherto had been constitutionally anathema and politically unpalatable, remains one of the most striking features of the period. The excise and the levels of government borrowing it supported became permanent parts of the Restoration financial settlement, yet that was far from a foregone conclusion. Understanding how and why excise taxation achieved legitimacy, while preserving a sense for the contingent nature of that process of negotiation, speaks directly to broader questions of the possible rhetorics of legitimation available to any regime.

The settlement of excise taxation was contingent. There were power-ful forces working against it. Opponents of the excise questioned its legality, offered penetrating critiques of its incidence and proposed ingenious alternatives. Domestic commodity taxation appeared to vio-late the Tudor conception of the kingdom as the ‘manor of England’, in which the landed voted impositions on themselves to supply their king. For those who wanted to restore a financial regime that can be termed ‘fiscal feudalism’, excise taxation was particularly loathsome. When it did not bear the taint of Dutch republicanism, the excise smacked of continental absolutism. Proponents thought it the ‘most insensible imposition’, but as disaffected royalists, radicals and independents alike pointed out, the taxation of domestic commodities fell heaviest on the poor. Many Englishmen thought the poor should not pay taxes at all. In the mercantile community, the approval of the excise was far from universal. Special interests argued specific excises hurt trade, destroyed fledgling industries and rewarded professional tax collectors at the expense of more productive members of society.

From the perspective of the state, excise taxation proved nicely suited to the evolving English economy and its new commercial society. Under the Commonwealth regime, officials recognised that the excise could be used to expand the fiscal frontier. Historically, the Home Counties and London contributed disproportionately to the king’s revenue. Extending the geographical reach of the state also offered non-fiscal benefits too. Proponents and opponents alike saw the potential for using excise offic-ers to gather intelligence and monitor dissent. Others cited non-fiscal benefits: the excise discouraged consumption of luxuries, promoted social cohesion (by making the poor stakeholders), encouraged the pro-tection and consolidation of domestic industries, enforced a positive balance of trade and gave the regime the capacity to reduce or expand the quantity of coin in circulation.

PROOF

PROOF

6 Excise Taxation and the Origins of Public Debt

The excise was adopted in a moment of crisis. Precisely because it was so controversial, the excise required new justifications and created new possibilities. The excise created a contemporary discussion about the principles of taxation that shifted the terms of the debate away from constitutional analogies to domestic realities. During the Civil Wars, this was possible in part because the legality of the excise impo-sition rested on the ‘necessity’ argument, but also that the ‘ancient constitution’ had been sundered by the regicide. If the ‘manor of England’ was to be reconciled with the Commonwealth regime, then it had to be re-thought. Under the Protectorate, those who wanted to resurrect the ‘fiscal feudal’ model had to contend with the excise in their analysis, if only to discredit it. In the process of that re-thinking and re-negotiation, other models occurred to contemporaries. Most were continuations of older strands in economic thought. Others were novel. Some, such as Thomas Hobbes’ (1991) Leviathan, employed the language of an abstract state. Some reasoned from fundamental prin-ciples, others from experience.

Conflicts over the excise reveal the contradictions in Protectorate political culture, but these debates also had long-term consequences. To understand the Restoration financial settlement, historians must appre-ciate both the importance of retaining the excise and the significance of the constitutional fiction created to do so. How far did the Convention Parliament ‘restore’ the status quo antebellum? If the language of the Restoration Settlement preserved the ‘medieval doctrines of supply’, the reality was quite different. The fiscal innovations of the Interregnum had altered what might be called ‘state structure’. William Petty’s A Treatise of Taxes and Contributions (1662) saw four pirated printings and dozens of references in contemporary economic thought. Excise taxa-tion facilitated a ‘Fiscal Revolution’ in two senses. It catalysed struc-tural change, but furnished a political compromise, which preserved pre-revolutionary discourses of legitimation even as new ones evolved to describe the new underlying realities. Precisely because of that para-dox, the fate of the excise was paradigmatic of the Stuart Restoration. At the same time the experiments in public borrowing under the Long Parliament offered a blueprint for what was possible after the accession of William and Mary.

Ninety years after Joseph Schumpeter coined the concept, standard narratives of early modern European state formation remain anchored to his notion of the transition from a feudal demesne-state to the begin-nings of the modern tax state. In a very narrow sense, claims for a fis-cal Revolution of the Interregnum are uncontroversial. Before the Civil

PROOF

PROOF

Excise Taxation in Context 7

Wars, the Crown relied upon feudal demesne revenues (revenues from Crown lands, forest fines and the proceeds of escheat, aids and the court of wards), prerogative taxation (purveyance, ship money, forced loans, imposts and monopolies), and the great and petty customs. By contrast, the Tudor subsidies (which had been based on contested assessments) and the tonnage and poundage (i.e. parliamentary customs voted to the monarch for life until the reign of Charles I) made up less than a quarter of the total. If the tonnage and poundage duties are re-classed as prerogative taxation after 1628 (when the king began to collect them without parliamentary assent), the proportion is even smaller. After the Restoration, over 90 per cent of the Crown revenue came from parlia-mentary taxation (Braddick, 1996, pp. 1–20).

This book seeks to explain why that structural change occurred and why it endured. Most narratives of the British tax state sidestep those questions. The conventional explanation for what ‘caused’ the mod-ernisation of the British fiscal system turns on the ‘functional crisis of monarchy’ (Russell, 1979, 1973; Braddick, 1994, pp. 1–10). By the mid-1630s, prerogative taxation had proved inadequate to meet expenditure. Charles had been forced to call the Short Parliament to obtain funds with which to fight the Bishops’ Wars in Scotland. When civil war broke out in England, the Long Parliament needed new revenue sources to pay their armies. First they abandoned the Tudor subsidies in favour of assessments, and then they adopted the excises. In doing so, they pled necessity. They promised to continue these new taxes only long enough to bring the king to heel and to satisfy the debts incurred in doing so. Within the conventional legal framework, these were sources of extraor-dinary supply, raised to meet extraordinary expenses. How and why did they become a permanent part of the revenue? Explanations that favour ‘functional crisis’ over structural change take for granted that tempo-rary fiscal expedients would inevitably be made permanent.

This study demonstrates that excise taxation provided the engine of Schumpeter’s structural change and the catalyst for a shift in ideologi-cal justifications of parliamentary taxation. This interpretation hinges on three related claims. The first is that excise taxation proved far more successful than anticipated, both in its capacity to raise needed funds and in the speed with which the parliamentary regime was able to cre-ate a durable and disciplined revenue establishment. Had it failed to accomplish both, it would not have endured. Second, the relative regu-larity and transparency of collection, the high degree of centralisation and new methods of auditing and control permitted the development of new short-term debt instruments, which could be secured by the excise

PROOF

PROOF

8 Excise Taxation and the Origins of Public Debt

ordinances and priced by the market. The market pricing of short-term debt broadened and deepened credit markets. Third, the excises had no legal precedent (or dubious ones at best) and thus required new justifi-cations. By voting to retain the excise in exchange for the permanent abolition of the court of wards, the Cavalier Parliaments maintained a constitutional fiction based on medieval doctrines of supply. In effect, the excise offered a solution, acceptable both to adherents of an older model of fiscal feudalism and to those who pressed for reform.

English Excise Taxation

In July 1643, the English Parliament passed the first excise acts in order to raise money to finance the army.2 The king followed suit in December and the Scottish Convention of Estates in February (Engberg, 1966). Very few records of the royalist excise impositions remain, but those that do hint at the desperate state of Charles I’s finances. The royalist schedule of commodities was more extensive than those of Parliament’s original ordinance, and their rates were higher. The royalists desper-ately needed new sources of funds. John Wandesford, collector for the excise, won his post through his willingness to make loans to the king. The duties themselves were eventually collected by the clerks of the markets or, alternatively, by royalist commanders.3 Although they may well have inspired a proposal in the 1660s for the clerks of markets to collect the excise, no reference to these royalist imposts has been found in contemporary discussions of the excise after the Restoration (BL Add MS 28078, f. 452). Elias Ashmole, king’s commissioner for the excise at Lichfield, was the sole known royalist excise officer to have a career in the excise after the Restoration. Ashmole served Charles II as excise comptroller and auditor. The Parliamentary excise, by contrast, devel-oped into a permanent part of the Protectorate’s ordinary revenue by 1655 and was retained by the Cavalier Parliaments in 1660/1661. Despite a tendency among modern historians to see these duties as a parliamen-tary innovation, they had been proposed earlier in the century under the same name. Duties on domestic commodities in a broader sense had some recent legal precedent in Crown prerogative taxation through imposts, monopolies, patents and grants, which Charles had imposed in the 1630s under Personal Rule.

In economic terms, taxes are classified as ‘direct’ and ‘indirect’. Direct taxes are assessed upon individuals (or legal entities) while indirect taxes are levied upon expenditures. Indirect taxes are levied on the production or consumption of commodities or on commercial transactions. In the

PROOF

PROOF

Excise Taxation in Context 9

seventeenth century, excise taxes were imposed on the wholesaler or manufacturer to minimise evasion and reduce the costs of collection. Depending on the price elasticity of demand for a given commodity, the burden (or ‘economic incidence’) of an indirect tax may be shifted ‘for-wards’ onto the consumer in the form of higher retail prices or ‘back-wards’ onto the wholesaler, manufacturer or producer of raw materials in the form of lower prices paid for the goods. Historically the rates for customs and excise taxes were published in ‘books of rates’ that specified the duties for individual items; on occasion (as is the case today), they were assessed ad valorem (i.e. at a fixed percentage of the declared value).

For the sake of this discussion, excises can be grouped into three classes. The most important were the duties on victuals: beer, ale, cider and mead. To these, flesh and salt were added in January of 1644. The second most profitable excises were the additional duties on specified imports (later others not specifically mentioned were taxed ad valorem) and a handful of exports. Of these, the exports were taxed primarily as a punitive measure against royalist strongholds. Except insofar as the duties were paid by the ‘first buyer’ (usually the retailer) rather than the ‘importer’, these ‘foreign excises’ on imports are, in economic terms, equivalent to customs duties. After the Restoration, the foreign excises were merged with the customs. During the Interregnum, they remained distinct, in part because of the political clout wielded by the great mer-chants. This distinction was also significant because of the separate role played by the foreign excises in government borrowing. The third category includes all the impositions on a host of domestic manufac-tures: alum, copperas, monmouth-caps and other haberdashery, hops, saffron, starch and silks. These were the commodities that had been assessed via Crown prerogative taxation (the royal imposts, licenses and grants of monopolies) under Charles I and were thus closely associated with arbitrary government. They were not part of the initial legisla-tion but were added in April of 1644. A related ordinance followed in November of 1645 on lead; gold, silver and copper thread and wire; glass, linseed, whale, pilchard and other oils; silks; soap; imported wool-len cloth and, however improbably, lamperns or eels, which were used in large quantities as fish bait and smaller ones as food. The collec-tion of this third class of duties was geographically localised, confined to the few areas in which the items were produced. Despite economic expansion in the 1650s, the excises on these commodities contributed less to government coffers than they had in the 1630s (Dietz, 1928; BL Lansdowne MS 1215, f. 7). The duty on butcher’s meat, which was repealed in the aftermath of the Smithfield Riot of 1647, had been a

PROOF

PROOF

10 Excise Taxation and the Origins of Public Debt

particularly contentious tax. Otherwise these industrial excises gener-ated the most popular hostility and elite resistance. In spite of attempts to make these duties profitable by leasing them as kingdom-wide farms, their collection had all but lapsed by the late 1650s.

The Restoration Excise Acts, in omitting the last class of commod-ity, both confirmed the existing practice and reflected a wider trend towards the modernisation of the fiscal system made possible by suc-cessive regime changes (O’Brien and Hunt, 1997). The excise on beer, ale and cider (along with perry, mead, spirits or ‘strong waters’, vinegar, coffee, chocolate and tobacco) became the mainstay of the Restoration excise revenue stream. In 1661, after the ‘foreign excises’ were merged with customs; the remaining minor excises (spirits, vinegar, coffee, chocolate and tobacco) were collected by ‘composition’ (where the pro-ducers or wholesalers negotiated a fixed charge in lieu of measuring the actual quantities) by the sub-commissioners. By the mid-1660s, the farming contracts frequently mentioned only the ‘excise on beer, ale, cider, perry and mead’.

Although the details differed by commodity, the basic principles of excise collection changed very little over time. Unless the liable parties had ‘compounded’ with the local excise office, the excise officer would visit their places of business at intervals prescribed by the statutes. After ascertaining the quantity of goods for sale, he would issue a voucher for the excise due. Vouchers could be paid to the county collector or at the local excise office, which had operating hours prescribed by statute. Upon payment, the office issued receipts, which were required to move or sell the excisable commodity. Violators were subject to seizure. Failure to pay the duty timely could result in seizure (or ‘distraint’) of mer-chandise or the tools of the trade. In rare cases, offenders faced impris-onment. ‘Gauging’ referred to the practice of measuring the expected production of beer or ale from the various steps in the brewing process and reconciling them with the quantity of finished product in order to detect frauds and evasion. ‘Tasting’ denoted a variety of practices designed to detect frauds perpetrated by vinters, distillers and the pro-ducers of cider, perry and mead. Under ordinary circumstances, excise collectors were indemnified against liability in suits at common law challenging arrests, seizures or property damage. For the minor excises, composition was the usual method of collection. Recent accounts of the excise have privileged this practice in an effort to highlight the degree of negotiation, cooperation and even ‘brokerage’ of the duty by elites in the localities (Braddick, 1994; Ashworth, 2003).

PROOF

PROOF

Excise Taxation in Context 11

Fiscal Sociology and Economic Thought

The symptomatic as well as causal significance of seismic shifts in state finance—what Joseph Schumpeter called ‘fiscal sociology’—should not be ignored (1918, pp. 4–7). Shorn of its polemical value in Cold War debates about the growth or putative crisis of the ‘tax state’ (the original German article was, after all, only translated into English in 1954), Schumpeter’s methodological orientation suggests a means of bridging several com-peting historiographies. One of Schumpeter’s modern disciples offers a cogent definition of fiscal sociology as:

the ramifications of the fiscal activities of the state into areas which are not their primary target. These effects may occur in sectors not directly affected such as related markets, but they may also occur outside the economic sphere proper, such as in politics, culture, reli-gion, or society at large

(Backhaus, 2004, p. 1)

This approach offers a place to both description and narrative and hence suggests the organisation of this work.

The domestic excise offers a compelling case study into the insti-tutional mechanics of state formation in the British Isles and a lens through which to re-assess the political culture and economic thought of the Civil Wars and Interregnum. The excise was adopted in a moment of crisis. Opponents of the excise questioned its legality, critiqued its incidence and proposed alternatives. But as David Hume realised, excise taxation (especially on the production of native liquors) proved nicely suited to the evolving English economy and its new commercial soci-ety:

In every nation, there are always some methods of levying money more easy than others, agreeably to the way of living of the people, and the commodities they make use of. In Britain, the excises upon malt and beer afford a large revenue; because the operations of malt-ing and brewing are tedious, and are impossible to be concealed; and at the same time, these commodities are not so absolutely necessary to life, as that the raising their price would very much affect poorer sort. These taxes being all mortgaged, what difficulty to find new ones! What vexation and ruin of the poor!

(David Hume, ‘Of Public Credit’, 1753, p. 171)

PROOF

PROOF

12 Excise Taxation and the Origins of Public Debt

William Petty’s Treatise on Taxes (1662) can be read as a statement of the Restoration synthesis. Much of his analysis came from observations about the effects of two decades of commodity taxation. His formulation of ‘value’, his implicit arguments about the economic incidence of vari-ous forms of taxation, his insights into the circulation of money and the probable effects of various taxes on the balance of trade, and his descrip-tion of the social consequences of taxation rested on the excise. Although no one offered as systematic an articulation as Petty, his contemporaries presented similar analyses. By offering the state a ‘cut’, the excise had made plain that trade created value. This argument no longer required ‘set piece’ references to the Dutch Republic. Petty reconciled the com-mercial and landed economies by arguing (as Quesnay would a century later) that in a closed system (modelled after the body), labour and land values were equivalent, and could be expressed in terms of each other. For him, this meant the Hearth Tax was the best ‘accumulative excise’, but for others it meant that land and commodity taxes could and should co-exist. The Long Parliament’s experiment with excise taxation helped create an indigenous discourse in defence of the tax state with which to answer advocates of a return to older models.

The excise not only democratised government credit markets, but also complicated the factional struggles in the House of Commons and the relationship between Parliament and the executive. An elaborate gov-ernment bureaucracy was the accomplishment of the Commonwealth regime. Yet ironically, a highly disciplined excise establishment could be used to extend the reach of executive power. The Commonwealth regime’s adoption of revenue farming, far from an abandonment of direct collection, was one strategy among many for ensuring that the state could borrow. Under the Protectorate, justifications for the practice changed. Tax farming (insofar as it offered the analogy to cultivating the ‘manor of England’) fitted with the regime’s ‘Elizabethan turn’ in state finance (Ashley, 1962, pp. 1–6). Cromwell was no friend to the merchant-financiers, who had been willing to lend before. In 1656, the foreign excise duties on wine became the flash point for Parliament’s suspicions of the regime’s financial incompetence. The ensuing debate did nothing to quell the growing arbitrariness of Protectorate govern-ment. This re-played in a minor key the conflict that had brought England to civil war in 1641. The resulting changes to the excise laws momentarily crippled collection.

Conflicts over the excise reveal the contradictions in Protectorate political culture, but these debates also had long-term consequences. To understand the Restoration financial settlement, historians must

PROOF

PROOF

Excise Taxation in Context 13

appreciate both the importance of retaining the excise and the signifi-cance of the constitutional fiction created to do so. Parliament granted half the duty on excisable liquors to the Crown in perpetuity to replace the income from the Court of Wards and the revenues associated with the rights of purveyance. The Commons had intended that the other half, voted to the monarch for life, would ensure that the Crown’s ordinary revenues were sufficient for this king to ‘live on his own’ (Chandaman, 1975, pp. 38–44). As one scholar noticed, this settlement very nearly achieved the aims of Salisbury’s Great Contract of 1610 (Roseveare, 1969, p. 55). Parliament may have ignored Fortescue’s pref-erences for re-endowing the Crown via subsidies and the skilful applica-tion of the rights primer seisin or escheat, but the Commons laboured to retain the underlying assumptions of a demesne-state (Fortescue, 1997, pp. 106–108). Domestic commodity taxation held new challenges in financial forecasting for perspective lenders and for the regime. The collapse of the Protectorate excise farms in 1658 led to widely different valuations. It fell to Thomas Wriothesley, fourth earl of Southampton and lord treasurer from September 1660 until his death in May 1667, to investigate. Understanding Southampton’s efforts furnishes an exam-ple of how a moderate royalist, who spent the Interregnum in internal exile only to emerge as a leading figure after the Restoration, grappled with the evidence of its financial experiments. To a surprising degree, Southampton was able both to diagnose and to avert the structural problems with the Protectorate excise farms and to protect the interests of loyal cavaliers in the counties.

Those who remain unconvinced of the usefulness of ‘fiscal sociology’ might try this thought experiment. Imagine twentieth-century America without a federal income tax. There would have been no Internal Revenue Service, no 1044 or W-9 or W-4 forms, no tax preparation services, no audits, no withholding (and no threats of back-up with-holding), no exemptions, no mortgage deductions and no tax shelters. Americans might have seen no distinction between earned income and capital gains. The taxpayers could not have expected refunds or welcomed election-year rebates. There would be no debates about an alternative minimum tax. The Treasury Department might still have an Internal Revenue Service, but in the absence of an alternative revenue source its gross collections would have been half of their present levels. Collecting the other half would have required a fraction of the cur-rent personnel. Consider how much of twenty-first century American political debate (and economic thought) turns around raising or lower-ing federal income tax rates. Bear in mind how much consumer and

PROOF

PROOF

14 Excise Taxation and the Origins of Public Debt

investor behaviour is structured around avoiding tax liability. Just as income taxes define the modern American state, the excise defined the mid-seventeenth and eighteenth-century British one.

State Formation or State Building?

This book argues that a critical period in state formation in the British Isles was a product of unintended consequences. Excise taxation was born of one political crisis and offered a solution to another. It both required and subsequently furnished new means of legitimisation of ‘state ideas’ and delivered ambivalent long-term and short-term gains for both the institutions and the political elites who together governed what was to become Great Britain. It was first proposed as a solution to highly contingent challenges (financing of royalist and parliamen-tary armies during the English Civil Wars), but in twenty years it had changed the parameters of state power in abiding and important ways. This framing, which highlights the structural processes, complements current functionalist accounts.

In his synthetic account of State Formation in Early Modern England, Braddick proposes a very useful operational definition of ‘state’ that per-mits scholars of the early modern British Isles to move away from those cumbersome notions of ‘state-systems’ and ‘ensembles of institutional-ized political power’ (Poulantzas, 1973, p. 92). Braddick uses ‘state’ as a ‘term of art’, as shorthand for a ‘coordinated and territorially bounded network of agents exercising political power’ (2000, p. 6). Braddick opts for this functional definition, specifying that ‘the state is a network of agencies distinguished by the kind of power they exercise, rather than the precise form of these agencies (there is no insistence that they be bureaucratic, for example) or the ends to which they were employed’ (2000, p. 6). This formulation frees the historian of the early modern British (or English) state from the strictures of Weberian or Marxist soci-ology: ‘looking at the whole range of institutions embodying political power, it is clear that no single will, or group interest, lay behind all the uses made of these offices’ (Braddick, 2000, p. 7). In his account, Braddick distinguishes amongst four distinct states (the patriarchal state, the fiscal-military state, the confessional state and the dynastic state), ‘all contained within the overall network of political agencies’ (2000, p. 94). As he acknowledged, the activities of one can enlarge the power of one or come at the expense (or neglect) of another. This book is concerned principally with what his typology classifies as the ‘fiscal state’, but less with its functions than with the structures and

PROOF

PROOF

Excise Taxation in Context 15

institutions through which power was exercised and the ideas used to justify them.

If early modern British historians have tended to accept the use of ‘state’ more readily than their continental counterparts, they have been careful to distinguish between ‘state building’ and ‘state forma-tion’, characterising the first as a deliberate strategy and the second as a long-term, structural process (Braddick, 2000, pp. 1–8). Preoccupied primarily with debating the ‘functional crisis of monarchy’ as a cause of the Civil Wars or explaining the Financial Revolution of the early eighteenth century, monographic studies of state formation often cover hundred-year sweeps (Brewer, 1988). In contrast, the case studies in state building frequently emerge from the investigation of individual politi-cal careers (Scott, 2003). Braddick distinguished them accordingly: ‘the emphasis of [this] analysis is on the impersonal forces which shape the uses of political power rather than the purposeful actions of individuals or groups—it is, in short, a study of state formation rather than of state building’ (Braddick, 2000, p. 1).

In this book, these two terms receive a different gloss. State building is still the history of individual intentions or group projects, but state formation is foremost the history of consequences. State formation rep-resents more than the product of impersonal forces; in aggregate, it must be seen as a gradual accretion of (largely) unintended consequences of tactical manoeuvres of elites within these networks. Braddick makes a similar observation, when he stated:

different groups, responding to a variety of different challenges and opportunities, sought to make use of the resources at their disposal. They attempted to redefine the scope of existing offices, or invent new ones, and in doing so they appealed to the legitimating ideas current in society at large

(Braddick, 2000, p. 7)

Networks of players improvise expedient solutions to crises or chal-lenges. Whether they succeed or fail constrains the options of future players, shapes the terms in which they can legitimise their choices and may even re-define the network. These decisions may or may not lead to long-term gains in the power of the ‘state system’ and subsequent re-framings of ‘state ideas’. When they do, the trend that emerges can be understood as ‘state formation’.

What role then do individuals play in this scheme? Here again Braddick suggests a useful heuristic. He suggests, ‘the process of legitimation [of

PROOF

PROOF

16 Excise Taxation and the Origins of Public Debt

state ideas] acted as a constraint on officeholders and limited their free-dom to pursue their own interests, narrowly conceived. In order for legitimating ideas to have this force, it is not necessary that they be genuine motives for action, of course.’ Ideas do more than simply cloak the activities of the state system. In short, as Braddick finished: ‘they may not explain why a person is acting in a particular way, but they are none the less among the things that constrain those actions’ (Braddick, 2000, p. 70). This book supports the truth of that formulation.

Notes on Sources and Methodology

Thirty-five of the fifty-three printed treatises, pamphlets, broadsides and ballads analysed in this book can be found among the Thomason Tracts.4 All but a handful of the rest are available in the other British Library collections or in the Goldsmith-Kress Collection of Economic Literature at the Senate House Library of the University of London. During the Civil Wars and Interregnum, the distinction between popu-lar and elite discourses was not hard and fast. Internal evidence dem-onstrates that many of the longer treatises (which might otherwise be classified as ‘elite discourses’) were written, at least in part, in response to ‘popular’ (or ‘cheap print’) polemics. The size and richness of this material makes it possible to trace the evolution of attitudes towards the excise within key strands of contemporary constitutional and economic thought.

The surviving manuscript evidence for the excise collection under the Long Parliament is confined to a very limited number of sources, especially compared to the available material for the Commonwealth, Protectorate and Restoration excises. The surviving Audit Office rolls are in very poor condition. Although produced in 1662, they claim to be copies of the originals. There are no surviving Audit Office rolls from the earliest period (1643–1647), though there is substantial circumstantial evidence to suggest that these figures were kept.5 In 1662, Southampton’s Treasury completed their reconstruction of the Interregnum Exchequer rolls, which have strangely been described by the National Archives as ‘Accounts the Commissioners of the excise’. These are in better condi-tion, but it is less clear what they capture. In the decade before the re-es-tablishment of the Exchequer under the Protectorate in 1654, the public revenue was administered by funds. The earliest roll, which covers the period from 29 September 1647 to 29 September 1650, gives the total revenue (and that for London and each of the counties) for the three years broken down by the original ordinance (September 1643, January

PROOF

PROOF

Excise Taxation in Context 17

1644, July 1644, November 1645).6 This artefact of Parliamentary man-agement has the advantage of establishing numerically that the first of these ordinances, the so-called Grand excise (initially issued in July and re-issued in September) represented the overwhelming majority of the revenue collected as excises. Between 1647 and 1650, it yielded over 90 per cent of the total.7 Because the Long Parliament had no functioning Exchequer, every time they passed a new ordinance to raise revenue they established treasurers who presided over a corresponding fund into which the monies were paid. These accounts represent the actual monies paid into the separate funds in the London Office for each of the excise ordinances (rather than the value of the receipts or vouch-ers issued for excise). The numbers should be read with caution as they may underestimate the total revenues collected since some monies were collected and spent in the localities without ever reaching the London Office.8

A single manuscript leaf in the Bodleian Library offers an abstract of the excise office’s annual accounts from September 1643 to June of 1650. As with Southampton’s reconstructions of the official accounts, this abstract’s accounting assumptions are not clear. Insofar as the two sources differ by about 10 per cent in the period from 1647 to 1650, this discrepancy deserves closer scrutiny. There are a handful of scattered state papers from the period before the regicide and two receipt books from October 1644.9 The most useful sources for the administrative his-tory of excise under the Long Parliament are the Journals of the House of Commons and of Lords. Surprisingly few scholars have examined either source in detail. Excise business was an ever-present item on the Commons’ agenda. Between 1643 and 1649, the Commons dispensed with some 800 separate pieces of excise business. Scarcely a session went by without Parliament confronting some aspect of the excise. Careful reading of this material, coupled with the corresponding entries in the Lords journals, reveals a great deal about the routine administration of the new tax.

Compared to the records for the excise under the Long Parliament, considerable archival evidence survives for the Commonwealth and Protectorate excises. None of the secondary literature on the Interregnum excise examines this material in any detail. Not only do the Declared Accounts and Audit Office scrolls offer valuable financial data, but also these same records provide detailed information about the administrative structures of the excise establishment. Although these parchment rolls were also compiled in the early 1660s, the pre-ambles state that they were based upon earlier accounts. There is ample

PROOF

PROOF

18 Excise Taxation and the Origins of Public Debt

evidence from the parliamentary record and the records of the Committee for Regulating the excise that the commissioners’ accounts were submitted routinely, reviewed by the auditors and comptrollers, and were approved, thereby discharging the commissioners from fur-ther liability.10 On the other hand, the poor material condition of the scrolls presents technical challenges. For 1650–1653, only the Exchequer roll survives; the Audit Office’s copy has been lost.11 Although support-ing documents conventionally employ Arabic numbers for computation, the Protectorate and Restoration Exchequers still used Roman numer-als in official documents. Occasional discrepancies emerge, especially where the paper is torn or the notation lends itself to scribal errors. The accounts contain lists of sub-commissioners and revenue by counties and ports, beer farms by counties and cities (where the farms were let separately), arrears and defalcations (including carry-forwards from pre-vious accounting periods), salaries in the London Office, orders paid and to whom, plus those still outstanding, as well as interest paid on secured debt and to whom. While several scholars have used the material selec-tively, only one has examined the records of the farms and none have systematically analysed the financial data. Close reading of this material reveals the aggressiveness of the Commonwealth’s attempts to regulate and extend the excise.

If the financial records of the Commonwealth have been under- examined, even less has been written about the administration. A hardbound book, containing a redaction of both committee minutes and copies of orders, for the Committee for Regulating the Excise is preserved in the Bodleian Library as Rawlinson C386.12 This redac-tion, which dates from the 1660s, covers the period between November 1649 and June 1652. Although a second volume did not survive, other material does.13 A letter book in the National Archives of correspond-ence between the excise commissioners and excise committee includes correspondence from 1652.14 A handful of miscellaneous orders and warrants are bound with other collections of state papers.15 Another hardbound volume, similar in construction to the others, includes cop-ies of excise patents, warrants, orders and leases from 1647 to 1667.16 This is one of three such volumes, which together cover the period from 1647 to 1687. These compilations are most likely the result of the Earl of Rochester’s investigations in the 1680s. For the 1660s, this material overlaps with that preserved in Southampton’s books.17 In the National Archives, there is one surviving lease for Leicester in March of 1651.18 An excise officer’s logbook from 1653–1654 and a petition from 1651 from a ‘stranger merchant’ offer a glimpse into the little explored

PROOF

PROOF

Excise Taxation in Context 19

foreign excise.19 Occasional letters from the commissioners to offi-cials in the localities offer insight into those relationships.20 All told, there are over 500 separate entries in the committee’s minute and order book and associated papers. The total volume of material for the Commonwealth excise administration stretches to over 300 manuscript pages without including the information that can be gained from the Audit Office and Exchequer rolls. This new material does not include the indemnity court records analysed by Braddick (1994, pp. 168–230). Of Braddick’s eighty-eight indemnity cases, only a third date from the Commonwealth period. This material can be supplemented by printed references in the Calendar of State Papers Domestic series, in the House of Commons Journal and in Acts and Ordinances.

Changes in the administration of the excise under the Protectorate had a corresponding effect on the nature of the surviving evidence of its operations. The Exchequer’s Declared Accounts and the Audit Office rolls together provide an accounting of the contracted value of the beer farms and the revenue collected by the sub-commissioners. They also detail arrears and give the specifics of debts serviced. Because the excise ordinances were consolidated into one ordinance in March 1654, little effort was made to distinguish the share of the revenue arising from the foreign excises versus the native commodities exempted from the farms of excisable liquors. Except for London and the bills of mortal-ity, the Declared Accounts give gross receipts for sub-commissioners by county without specifying the nature of the commodity excised. On the other hand, these accounts provide detailed information on the nature of arrearages, which gives a basis for assessing the relative success of farming arrangements. Although there are no surviving Declared Accounts from March 1654 to March 1658 in the Exchequer-series, the Audit Office has copies from March 1655 through to the Restoration.21 Net receipts pose a more difficult problem. Because the May ordi-nance ordered that the excise revenues be paid directly into the newly re-established Protectorate Exchequer, two scholars have seen these entries as a means to reconstructing the net revenue (Ashley, 1934, pp. 68–69; Wheeler, 1999, pp. 164–165). This method understates net receipts. The Declared Accounts show that the excise commissioners directly disbursed funds not only for salaries, but also for debt service (including interest owed and principal repayments), pensions, grants and rebates (or drawbacks) on re-exports. Those monies never reached the Exchequer. The Exchequer and Audit Office, by listing the farm-ers and sub-commissioners, permit detailed tracking of the farmers and sub-commissioners who provided the middle management of the

PROOF

PROOF

20 Excise Taxation and the Origins of Public Debt

excise. They also allow attribution of arrearages and some assessment of the declining value of the imposts on native commodities other than excisable liquors.

While the records of the Commission for Appeals and Regulating the Excise (the replacement of the Committee for Regulating the Excise) are comparatively scant, a surviving warrant book suggests some measure of continuity within a more limited remit.22 Ten leases, in varying con-dition, survive. Together they provide the details of the farming con-tracts.23 From at least May 1656, the London Excise Office was required to make weekly reports of the cash it held. Evidence exists that the auditors complied.24 Like its predecessor, the Commission for Appeals had the responsibility for dealing with foreign ambassadors and their allowances.25 Two receipt books for salaries and payments by the com-missioners for the excise from either side of the Restoration divide allow an assessment of the continuity of personnel at the lower lev-els.26 Thomas Birch’s Collection of the State Papers of John Thurloe includes correspondence with Lord Broghill (Roger Boyle) over the Irish and Scottish customs and excises revenues and with General Monck over Scottish finances and offers insight into the use of the excise establish-ment to collect domestic intelligence. Thomas Burton’s Parliamentary Diary supplements the Journals of the House of Commons in provid-ing records of the key Protectorate excise debates. The evidence for the Protectorate excise administration was not as systematically preserved as that of the Commonwealth, but there is more variety in the sources.

Detailed minute books, records of patents, warrants, and leases for Southampton’s Treasury are all preserved in the National Archives as are copies of reports to the Privy Council and the king.27 Compared to the earlier material, they pose no particular methodological difficulties. The closure of HM Customs and Excise Library (at Kings Beam House) in 2003 and the integration of those records into the National Archive’s catalogues brought this material together for the first time.

Chapter Organisation

Chapter 2 investigates the political negotiations that led to the imposi-tion of the excises in July 1643 and considers how far these expedients succeeded. By employing previously under-used sources in the National Archives, the Bodleian Library, and the British Library, it is possible to reconstruct how the parliamentary excise was administered during the First Civil War. To a surprising degree, Parliament was responsive both to petitions from special interests that pled hardship and to complaints

PROOF

PROOF

Excise Taxation in Context 21

from the excise commissioners about the extent of frauds and eva-sion. Many of the practices, which became standard later, were first introduced during this period. As the excise ordinances came to secure increasingly unmanageable levels of short-term public debt, parliamen-tary management of the excise began to break down.

Chapter Three considers the administration of the excise from the Smithfield Riot to the establishment of the Commonwealth. There is a general consensus that the public debts incurred by the Long Parliament cast a long shadow over the financial stability of the Commonwealth and Protectorate regimes, thereby ensuring the retention of fiscal inno-vations like the excise and complicating factional rivalries in the city. This chapter reconstructs the various secondary markets in excise-backed government paper and analyses the decisions to dispose of capital assets (the bishops’ lands, Crown lands, and the dean and chap-ter lands) in the late 1640s. Public faith bills and military debentures were deeply discounted in well-developed secondary markets in the late 1640s and early 1650s. These developments prove to be the most important context for understanding the ‘re-modelling’ of the excise in 1649–1650. Far more than localised resistance, the state’s credit needs shaped the development of the excise establishment. This was the most important force behind the adoption of tax farming in this branch of the revenue.

On the basis of fresh investigations into the institutional culture of the excise commission, Chapter 4 argues that the basic administrative structure was in place by 1650. Detailed minutes of the parliamentary Committee for Regulating and Improving the Excise demonstrate the regime’s commitment to supervising the excise establishment. They show that both tax farmers and sub-commissioners were monitored and that farming represented not so much a policy shift towards pri-vate interests as one strategy among many employed to enhance both revenue collection and access to credit. The body of administrative law around the excise (both in its substance and its procedures) developed out of precedent set down in this period.

Chapter 5 furnishes a case study in how taxpayers contended with the excise. Despite the conceptual similarities between the royal imposts of the 1630s and the industrial excises of the 1640s and 1650s, these fis-cal exactions receive separate treatment in the scholarly literature. The ‘Soap Makers Complaint’ of 1650 offers an opportunity to view disputes about the excise on soap through the lens of the controversies attendant to the earlier soap patents. Rather than offering evidence for general-ised resistance to the excise by humble artisans, the ongoing pamphlet

PROOF

PROOF

22 Excise Taxation and the Origins of Public Debt

war between rival companies of soap boilers involved some of the most powerful men in London. Unpacking these rivalries reveals the highly contingent nature of the Long Parliament’s fiscal experiments, while also underscoring the contribution of parliamentary revenue commit-tees to the development of the procedures and practices that governed the growing excise establishment. It also offers a window into how the Long Parliament and Commonwealth regimes conducted their manage-ment of the public revenue and illustrates their commitment to stand-ards of transparency, accountability and respect for property rights that are generally first ascribed to the Williamite regime.

Chapter 6 resumes the chronological narrative with a study of the Protectorate excise. As many other scholars have noted, Cromwell had an essentially Elizabethan vision of government finance. Cromwell abhorred reliance upon established London financial interests. In re-establishing the ancient Exchequer, he adopted none of the innovations of parlia-mentary finance. His animosity towards groups who had previously lent funds to the Commonwealth narrowed his regime’s financial base, even as the Protectorate regime’s other reformist projects bore fruit. As a conse-quence, Cromwell became dependent instead upon syndicates of farmers, who were willing to make advances to the regime in exchange for direct control of the revenue stream. Meanwhile the Protectorate Parliaments fought Cromwell’s extensions of executive power by disabling the excise officers from imposing punitive measures without the cooperation of the local justices of the peace (JPs). This re-played in a minor key the conflict that had brought England to civil war in 1641. By the end of Cromwell’s reign, most of the Protectorate excise farms had failed. These bankrupt-cies contributed to the financial difficulties faced by Richard Cromwell after his father’s death.

Chapter 7 eschews the temptation to see the Stuart Restoration of 1660 as an end point. Almost all of the surviving records of the Interregnum excise regime come from the investigations of the Lord Treasurer Southampton after the Restoration. Southampton and Elias Ashmole, comptroller of the excise for the city of London and future accountant-general of the whole excise, were able to preserve for the restored regime the lessons of Interregnum finance. As salary books from both sides of the Restoration confirm, much of the excise establishment had survived not only the Protectorate but also regime change. These continuities in the administrative structures and in personnel facilitated the settlement of the excise. Southampton was successful at brokering a compromise with local interests and in rewarding those who had been loyal to the Crown. Through his commitment to the ‘ancient course of the Exchequer’ and

PROOF

PROOF

Excise Taxation in Context 23

to the rule of law, Southampton was able to defuse resistance to the tax and secure continued access to financial markets. Analysis of the role of the excise in supplying government credit elaborates a neglected dimen-sion of the politics of patronage and elite formation.

The outlines of a new political economy of taxation emerge in Chapter 8. When Parliament resorted to excise taxation during the Civil Wars, they had intended it as a temporary expedient for financing what they understood as the extraordinary expenses of funding the war against the king. Permanent settlement of the excise was unthinkable. Yet amidst common law objections to excise taxation, new discourses were available to pro-excise pamphleteers as independent justifications for Parliament’s imposition of the tax. These evolved into the theory of compensatory taxation advocated by William Petty in 1662. Taken together, these print polemics point to a native discourse on the tax state that significantly pre-dates the late eighteenth-century contribu-tions made by Adam Smith. The Interregnum’s experiment with excise taxation provides both the impulse and the context for a significant shift in attitudes towards the public revenue as a whole and in them we can see the genesis of notions of the ‘public debt’.

Chapter 9 looks ahead to the Revolution of 1688/1689. The Restoration financial settlement both consolidated the innovations of Interregnum public finance and preserved the inherent constitutional contradictions and the resulting conflicts of interest. The financial settlement of 1690, by contrast, formally renounced Fortescue’s ideal. Wary of their experi-ences of Crown finance in the 1680s (in which the shift to direct col-lection of the excise in 1683 converted under-supply into over-supply), Parliament intentionally created a financial settlement in 1690, which, by virtue of being ‘temporary, inadequate and encumbered’, safe-guarded the political settlement. This outcome was not inevitable, but rather was the result of bitter political contest and of ‘rent-seeking’ by a new species of financial elites (Clay, 1978). In a different constitutional moment than that of 1647/1648, the advent of widely held long-term debt instruments offered a solution palatable to what Davenant would describe as ‘both parts of the Constitution, Legislative and Ministerial’ (1698, pp. 42–43). In the growth, as in the genesis of the public debt, the excise revenue played a central part, and would continue to do so through the long eighteenth century.

PROOF

PROOF

237

Abercrombie, Captain Jeremiah 59–60

Abercrombie (Denton), Susan 59–60, 75, 202

absolutism 5accountability 2, 22, 77, 109, 127, 231accountants (accomptants) 44, 169,

171, 173, 174,175advances 22, 31–2, 37, 41, 58–59, 61,

72–74, 83, 84, 89, 104, 129–30, 136, 138, 140, 147, 176, 180, 204–7, 217, 219

administration by legislation 31–43aids 7Aldworth, Richard 90, 113Allen, Robert 221Allen, Alderman Thomas 138Allowances 10, 35–38, 93, 172, 196,

221almsmen 85Alum Works, Royal 115ancient constitution 6, 27, 159–160,

189, 191, 198Andrewes, Alderman Thomas 61Angel, Robert 174annuities 4, 59–60, 75, 77, 202apothecaries 39appropriation, principle of 42, 211Archer, John 51army 8, 31, 37, 40–41, 45–49, 52–53,

56–57, 60, 66, 72–77, 80–3, 98, 104, 163, 190, 202, 218,

arrears 18–19, 39, 46–48, 63–66, 68, 70–71, 73, 80–82, 87–88, 100–102, 122, 131, 135, 139, 141, 148, 150, 151, 160, 163–164, 169–171, 173–174, 181, 216, 217, 218, 219, 220, 221

artificers 39, 42–3Ashley, Maurice 129Ashworth, William 53, 110, 219Ashmole, Elias 8, 22, 157, 166, 180

assaults of excisemen 95, 111, 188assessments 7, 41, 46, 50–1, 56, 74,

81–2, 135, 143, 160, 163, 188, 191, 213, 215

Attorney-General 143, 218Audit Office 8, 16–19, 43–4, 63–4, 68,

88, 93, 171, 214, 219, 220Auditor 8, 18, 20, 27, 34, 36–9, 43,

63–4, 76, 87, 93, 98–100, 106, 161, 166–9, 171, 213, 215

Backhaus, Jürgen G. 11Baker, James 116Ball, John 175bankers 32, 58, 59, 133, 206, 207Barber, William 116Barbor, Ralph 175, 221Barebones Parliament 137, 168Barfoot, Robert 116Barnard, Samuel 174–5Barrett, Thomas 221Bartlett, Samuel 166Baynes, Captain Adam 138, 143, 145,

148Beane, Humphrey 176Bedford, earl (later duke) of (William

Russell) 27, 31, 113Bennet, Jervas 138Bertie, Sir Charles 206Best, Richard 130Birch, Colonel John 161, 167, 209Birch, Thomas 20Bishops’ Wars 7Bocket, John 138Bond, Denis 87Bond, William 64, 87Bostock, Edmund 204Braddick, Michael J. 14–16, 19, 47–53,

98, 104, 110, 151–2, 214, 215Brereton, James 221Brereton, Sir William 40Brewer, John 176

Index

PROOF

PROOF

238 Index

brewers 27, 35, 53, 81, 86, 89, 95, 99, 109, 126, 131, 140–142, 147, 151–2, 169–170, 180–1, 194–7

brewing victuallers 81, 86, 126, 152, 170, 185, 196

Brewster, Robert 90Booth, Robert 112–3, 122–7Bourchier, Sir John 115, 124Broghill, Baron (Roger Boyle) 20brokerage 10, 50, 151, 182Brook, Sir Basil 115–118Broomfield, Laurence 215Bucknall, William 180, 203–4, 209Bulstrode, Thomas 83, 90, 138Burgundy 25Burr, Thomas 94Burton, Thomas 20Bury, Richard 138, 148–9,Bury, William 51

Calverd, Peter 204capitulation taxes 196Carter, John 116Cavalier Parliaments 8, 155, 179Cavalier Party 13, 163, 205, 211Cave, Norrice 51certificate 44, 59, 112Chaloner, Thomas 115Chambers, Alderman Richard 61Charles I, king 7–9, 27, 31–2, 86, 114,

138, 158, 162–3, 184Charles II, king 8, 127, 156, 157, 182,

190Chamberlen, Peter 190–1Champante, John 174Cheeks, John 221Chiffinch, Thomas 166Church, William 47Clarendon, earl of (Edward Hyde) 28,

159, 162, 164, 166, 189, 194, 199Clarges, Sir Thomas 208Clark, Thomas 175Clement, Gregory 90, 113Clifford, Baron (Thomas

Clifford) 202–4City Alarum 30civil list 211Coke, Edward 27Cole, William 191–2

collateral, excises as 4, 32, 49, 54, 75–76, 82, 156, 202, 211

Collection of Statutes 179Collins, Francis 221Collins, Richard 175colonies, American 113, 190–1compensatory taxation, theory of 23,

110, 183–5, 189commissioners, customs 41, 57, 61, 97commissioners, excise 18–21, 25,

32–3, 38, 41–47, 60–72, 76, 87, 89, 93, 95, 97–98, 101, 106, 136, 139–142, 147–8, 155, 165, 214, 216, 217

Commission for Appeals and Regulating the Excise 20, 90–1, 107, 131, 136, 138–9, 146–9, 171

committee, local v. national v. regional 32–33, 46

Committee for Accounts (Accompts) 44–45

Committee for Advance of Money 33, 51, 215, 216

Committee for Assessments 46Committee for Compounding 33, 46,

51, 216Committee for Improving the

Excise 33, 34, 41, 42, 44, 45–47, 60, 87, 89, 215

Committee for the Public Revenue 33, 34, 46

Committee for Regulating and Improving the Excise 21, 79

Committee for Regulating the Excise 18, 20, 43, 46–48, 68, 70, 78, 80–83, 89–90, 96, 100, 104, 106–7, 111–5, 124–7, 138, 170, 173, 215

Committee for Safety 46Committee for Sequestrations 33,

46, 51Committee for Taking Accounts 33,

44–45Committee, Indemnity 19, 47–51, 79,

80, 96,Committee, Navy 71, 113, 218Committeeman Curried, The 56–7Committee-man, local 46, 50–1,

56–7, 82

PROOF

PROOF

Index 239

Common Council, London 47, 60, 62, 74, 76, 133, 140, 202

Complete Gauger, The 175composition (mode of collection) 3,

10, 32, 51, 59, 86, 117, 122, 147–8, 165, 169–70, 181–2

Compton, Sir Henry 115, 118Concerning Impositions, Tonnage,

etc. 37, 137–8, 198Considerations Touching Upon the

Excise 196constables 35, 145, 146Cornwall, Edward 204Council of State 33, 63, 66, 76, 82,

90, 104, 113, 127, 130–1, 136–8, 140–1, 145, 181, 217

Convention of Estates, Scottish 8, 29Convention Parliament 6, 157–8,

160, 163Cooke, Henry 174Coote, Sir Charles 61Countrey Gaugers, The 175court of wards 7, 8, 13, 26, 32,

160–162, 194Cox, Richard 116, 123Cradocke, Francis 191, 193Craestor, John 92credible commitment 1–2creditor action 2, 4, 58, 62, 77, 202Crofton, Zachary 191–2, 195–6Cromwell, Oliver 12, 22, 33, 59, 107,

129–140, 144–6, 149–152, 156, 159, 163, 165, 167–8, 189, 191, 219

Cromwell, Richard 22, 129, 139, 149, 151, 163, 189, 191

Crowe, John 48, 98crown lands 7, 21, 55, 77Cruise, Timothy 175Cullum, Thomas 72, 83, 217customs 3, 7, 9, 10. 20. 26, 32, 35,

39, 41, 46, 53, 57, 61, 86, 96, 97, 133, 136, 142, 144, 162, 164, 174, 179, 185, 190, 192–3, 197–8, 204, 206–9, 211, 221, 222

customs, great and petty 7

Danby, earl of (Thomas Osborne) 181, 202–210, 222

D’Anvers, Sir John 183

Darley, Richard 87Darrel, Samson 175Dashwood, George 204, 206, 209,

210Davenant, Charles 2, 4, 23Davies, John 37, 137–8, 198Davies, Matthew 174–5Davies, Richard 48Davis, Mark 148Debt service 2–4, 19, 31, 75–76, 78,

80, 167, 201, 212Decimation Tax 143Declaration and Proclamation of the

Army of God 191Declaration and Protestation 134Declaration in Vindication 57, 185Declared Accounts 17, 19, 60, 64,

68–71, 76, 81, 87, 98–101, 132, 148–9, 155, 171, 173, 218, 222

defalcations 18, 90, 180–1Delinquents 33, 46, 51–2, 70, 117–8,

134, 170demesne revenues 7, 26demesne-state 1, 6, 13, 213Dighton, Daniel 124Dipper, Henry 221Discourses on the Public Revenue 2, 4, 23distraint (seizure) 10, 30, 35, 47, 90,

95–7, 167Divers, John 174Dodson, William 91Dove, John 87Dove, Henry 221Down Survey 198Downes, Richard 83Downing, Sir George 113, 145–6, 159,

162, 166–7, 191, 206Drinkwater, Robert 116Duncombe, Sir Charles 210

Easterly, Francis 221Edmonds, Simon 47–8Edmonds, Barnaby 47–8, 98, 221Edward III, king 25, 27Elsing, Henry 138Entring Book 203episcopacy 76, 157, 192escheat 7, 13, 26Evelyn, John 109–110, 126, 127

PROOF

PROOF

240 Index

Exchequer 16–19, 22, 27, 31–2, 43, 62–9, 73, 99, 129, 132, 149–151, 157, 159, 164–7, 170, 171, 173, 195, 204, 206, 207, 217–220

Exchequer, re-established 17, 19, 22, 99, 129, 159, 173, 220

Excise, Additional 158, 208–9Excise, London Office 17, 18, 20, 35,

40–1, 52, 65, 69, 72, 74, 81–82, 89, 93, 98, 99–101, 126, 142, 151, 168–9, 171, 174–5, 215

excise boll (on imported salt) 26excises, by commodity

aqua vitae 40beer and ale 9–11, 18–19, 34–37, 81,

85–89, 92, 95, 102, 119, 125, 129–32, 135, 143–5, 149, 155, 161, 164, 170–175, 178, 185, 194–197, 219–221

butcher’s meat (flesh) 9, 29, 38–40, 42, 52–3, 56–57, 63, 65, 68, 70, 82, 85–6, 102–3, 185, 213

cider and perry 9–10, 34–37, 86, 92, 102, 129, 132, 169, 174, 220

chocolate 10, 169, 194coffee 10, 56, 164, 169, 194copper wire 9, 42–3, 70, 112, 121,

220copperas (alum) 9, 38 70, 115, 220drapery (linen) 34, 35, 47, 97, 102,

125, 143, 174, 213, 220figs 34flax 38fish (pilchard) oil 9, 42–3, 70, 112,

115–7, 120, 122furs 34glass 9, 35, 42, 70, 220gold thread 9, 42–3, 70, 112, 220grocery 35, 102, 120, 122, 174haberdashery 9, 33, 34, 35, 51hemp 38herring 39, 71home-brewed beer 81, 85, 135hops 9, 38iron 38, 153, 220lamperns (eels) 9, 42–3lead 9, 27, 42–3, 70, 172leather 34, 35, 120malt 11, 27, 141

mead 9–10, 34–37, 86, 92, 102, 129, 132, 169, 174, 220

metheglin 130, 132, 169monmouth-caps 9, 38, 78paper 35, 220pepper 34pitch 38raisins 34resin 38saffron 9, 38, 70salt 9, 226, 35, 38–40, 42, 52–3, 57,

63, 65, 70, 86, 88, 102–4, 109, 120, 172, 185, 218, 220

sherbet 169silks 9, 34–5, 38, 42–3, 70silver thread 9, 42–3, 70, 112, 135,

220skins (hides) 35soap 9, 21, 22, 30, 35, 43, 53, 70,

86, 88, 92, 102, 104, 106, 109–127, 218, 219, 220

spirits 10, 40strong waters 10, 40, 169, 175sugar 34tarch 9, 38, 70tallow 38, 112, 115, 120, 122, 126tar 38tea 169, 194tobacco 10, 34–36, 38, 48, 81, 102,

135, 139, 141, 174, 193, 216tobacco pipes 38, 42, 88, 92,

103–4, 218upholstery 35vegetable (linseed) oil 9, 42–3, 70,

116–17, 120, 122vinegar 10, 194whale oil 9, 42–3, 70, 116–7, 120,

122wine 12, 34–7, 65, 81, 94, 102, 135,

139, 145–6, 162, 174, 193, 208, 209

woolen cloth 25, 27, 42, 70, 125, 218

excise collectors 5, 10, 34, 44–5, 53, 79, 111, 167, 173, 196

excise comptroller 8, 18, 2, 33, 42–3, 65, 93, 100, 106, 157, 166, 169, 181, 205, 215

excise, double 110–112

PROOF

PROOF

Index 241

excise farming 10, 12, 19–21, 30, 34, 55, 66, 68, 79–80, 84–92, 102, 106, 121–3, 127, 136, 138–141, 165–166, 168, 171, 178–180, 182, 191, 210, 211, 216, 219, 220

excise farms 10, 13, 18, 18, 22, 26, 69, 70, 84, 86, 88–91, 92, 99, 101–4, 129, 130, 132–3, 136, 139–41, 147–55, 158, 160, 162–3, 166, 170–1, 173–4, 176–7, 179, 181, 204–7, 210–11, 216, 218–9

excise farms. County 87, 101, 102, 104, 105, 106, 130, 136, 146, 149, 150–4, 168–170, 172, 173, 177–8, 180, 218, 219, 221

excise farmers 19, 21, 22, 30, 69, 78–9, 83, 86–91, 97–106, 120, 124, 129, 130–3, 136–7, 139, 141, 143–9, 152, 154–6, 161, 165, 167–8, 170, 174, 176, 180–1, 192, 204–7, 209–10, 216, 218–9

excise frauds 10, 21, 25, 30, 33, 41, 90, 93, 96, 99, 131, 142, 168, 180, 192, 197, 213, 216

excise, method and form 170excise, royalist 8, 38, 49excise sub-commissioners 10, 18–19,

21, 41, 49, 64, 67, 69–72, 78–9, 81–3, 85–102, 104, 106, 122, 130–2, 139, 145–7, 149, 151, 155, 164, 167–72, 175–6, 181, 196, 205, 217, 218, 219, 220

excise tickets 35, 39, 47, 124excise versus customs 3excise, women’s resistance to 53Exclusion Crisis 207, 209, 211executive power 12, 22, 129, 140,

136, 139, 141, 201

Falconbridge, Thomas 64Fauntleroy, Thomas 69–71, 98–101,

169, 216fee-farms 26, 86, 162, 218Fielder, John 90Fifth Monarchists 127Financial Revolution 1–2, 15, 77, 127,

202–3financial settlement, Restoration 5–6,

12–13, 23, 134, 155–165, 189, 202–4

financial settlement, Revolution 163, 202–203, 211–212

Finch, Sir Hineage 162Fine, Selma E. 64, 66, 68, 90, 214fines, knighthood 86fines, recusancy 86fines, evading the excise 30, 34–6,

42, 47, 52–3, 95, 130, 146, 150, 155, 169, 170, 196

fiscal feudalism 5–8. 158, 202Fiscal Revolution 6, 77fiscal sociology 11, 13Foot, John 47Foote, Sir Thomas 83, 147, 217forced loans 7foreign excises 9–10, 19, 25, 29, 34,

38, 41, 68, 71, 88, 103, 132, 139, 142, 145–6, 155, 168, 174, 179, 187, 192–3

ad valorem 9, 142ambassadorial allowances 20, 98first buyer, levied on 9, 26, 38,

39–43, 50, 70, 121, 213importer 9, 26, 35, 42, 193Spanish wines 139, 145–6

forest fines 7Fortescue, John 13, 23, 26–7, 29, 189,

191, 194, 203Fortescue, Sir Nicholas 115, 118Foulke, John 61Foxcroft, George 138France 62, 158Freeman Inslaved 194French, Thomas 148

Gage, George 115–6, 118Gape, John 148, 176Gardiner, William 149gaugers 79, 81, 93, 142, 147–8,

173–175, 196gauging 10, 95, 147–8, 151–2, 169–70,

174–5, 181Gerrard, Gilbert 63, 65, 215Gethin, Maurice 60Glyd, Richard 215Goldsmith-Kress Collection 16, 110Goldsmith-bankers 58, 60Goldsmiths’ Hall 33, 51Goodwin, John 60

PROOF

PROOF

242 Index

Grafton, Zachary (see Crofton, Zachary)

Gravenor, John 148Great Contract 13, 26, 31, 161Grene, Giles 57, 185, 215Gresham College 198Gretwyke, Roger 90Griffen, Edwyn 116Griffiths, Richard 48Grossfield, Robert 148Guilford, Sir Henry 115, 118Guy, Henry 209

half-excise 36Halifax, marquis of (George

Savile) 209, 210, 214, 220Halifax, earl of (Charles Montagu) 214Hampden, John 160, 161, 220Hampden’s Case 115Harding, Edward 218Hardres, Sir Thomas 218Hardwick, Colonel John 114, 116,

119, 121, 124, 126–7Harper, William P. 69–73, 86,Hart, Thomas 116Hartlib, Samuel 198Harvey, EdmundHaselrig, Arthur 27Hawkins, JohnHawkins, Mr 193–4Hayes, Alderman John 112, 114, 116,

119, 124, 127, 218Heads of Proposals 31, 53hearth tax 12, 206, 210Heyfield, Theodore 175Heyton, Francis 221Hieron, John 174Hillesden House 59History of Parliament Trust 214Hobbes, Thomas 6, 183Hodges, Luke 90, 138House of Commons 12, 13, 17, 19,

20, 25, 28, 29, 32–38, 40, 41, 43, 51, 57, 60–62, 72, 75–76, 80–81, 83, 85, 87, 89, 98, 106, 118–119, 123, 160–2, 164, 185, 190, 203, 214, 218

House of Lords 17, 37, 59, 85, 89, 119, 160, 190, 213

Howland, John 175Howlett, Thomas 114Hughes, Edward 89, 132, 143, 146,

147, 210, 215Humberston, Thomas 96Hume, David 11, 233Hunt, William 175Huntingdon, Major Robert 204, 210Huntingford, John 176Hutter, Augustine 95Hynd, Richard 116

Ibeson, James 144–5imposition, voluntary (Jacobean) 27imposts, royal 7–9, 21, 27, 33, 86–7,

109, 114, 125Independents 5, 52, 75, 111Industrial excises 10, 21, 30, 86, 103,

104, 109, 126, 168, 174, 179, 182, 221

Ingham, John 174insensible imposition, excise as 5,

50, 189Instrument of Government 134Ireland 20, 27, 43, 59, 60, 61, 77, 136,

138, 190, 198, 210, 215

James, Margaret 236James, Sir John 207, 210James I, king 27, 115James II, king 209Jesuit College in Caen 198Jones, Humphrey 137Jones, Roger 115, 118, 124Judiciall Arraingment 134judicial powers 80, 90, 95–98, 118,

125, 139, 151, 168, 181justices of the peace (JPs) 22, 35,

94, 96, 106, 117, 129–31, 141, 146–7, 155, 167–8, 170, 176, 179

Juxon, William 117

Kay, Richard 94Keeble, John 221Kennedy, William 110–1Kent, Richard 205, 207–8, 210King, Colonel Edward 51–2King William’s War 160

PROOF

PROOF

Index 243

land sales, crown 7, 21, 55, 77, 215episcopal 31, 73–6, 82royalist 77, 82

Lane, Thomas 148Langbridge, Thomas 174Langham, John 64, 72, 83Langham, George 138Lasham, William 174Laud, William 117law, civil 137, 183, 189, 191, 229law, common 2, 10, 23, 27, 47–8, 138,

183, 189, 191, 196, 202, 222lease 18, 20, 86, 130, 132, 152, 165,

176, 181, 204, 209, 210, 214, 218ledger books 167, 169, 171, 221Leviathan 6Levy, Hermann 236Lilburne, John 110, 113–4, 123, 127Lindenbaum, Peter 222liquidity 61, 77, 216Lister, Thomas 51Littlewood, Joseph 175loans 7, 8, 32–3, 27, 40, 48, 55, 58,

59, 61–2, 69, 72–4, 76, 104, 133, 140, 156, 180, 186, 203, 206, 211, 216, 217

Lockley, William 174London’s Account 56London Company of Brewers 35, 89,

95, 99, 140London Company of Soapmakers 117Long Parliament 2, 4, 6–7, 12, 16–7,

21–2, 30–31, 33–34, 36, 40, 43, 45–47, 49, 51, 53, 55, 57, 59, 6–63, 65, 67–78, 80, 84, 98, 101, 104, 109, 114, 118, 121, 124, 134, 138, 162, 216, 217

Looking-Glasse for Sope-Patentees 116, 120–1

Lux in tenebris 69–71, 98–101, 169, 216

malignants 28, 39, 50, 57, 85, 144, 189

manor of England 5–6, 12, 26, 190Manton, Captain Nathaniel 133, 147markets, credit and money 2, 8, 11–2,

21, 23, 48, 55, 59, 75, 77, 80, 204, 207, 210

Marsh, William 175

Mary, Queen 6, 155Master of the Rolls 143Matthews, William 47Maxey, Nathaniel 175Mayhew, Robert 175Mayor, John 175military debentures 21, 55, 58–9, 77Milner, Tempest 60Monck, General George 20, 190monopolies 7–9, 27, 30, 33, 86, 115,