Embed Size (px)

Citation preview

9

Receivables

Learning Objective 13-1

Describe the nature of the adjusting process.

9-3

Insert Chapter Objectives

Receivables

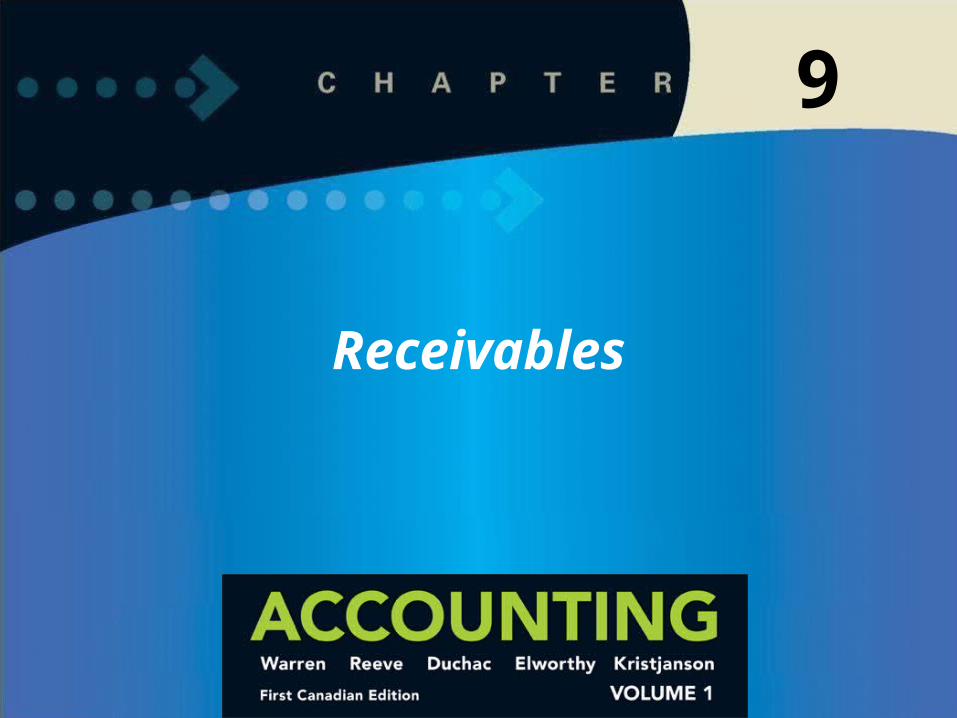

1 Describe the common classes of receivables.

2 Describe the accounting for uncollectible receivables.

3 Describe the direct write-off method of accounting for uncollectible receivables.

After studying this chapter, you should be able to:

9-3

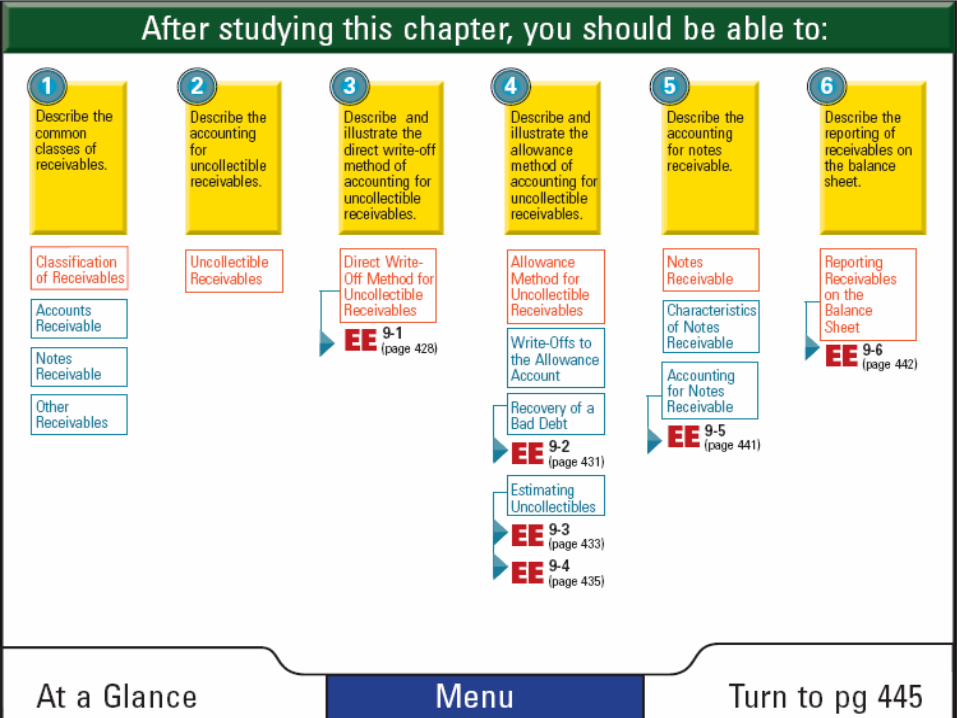

Receivables (continued)

5 Describe the accounting for notes receivable.

6 Describe the reporting of receivables on the balance sheet.

4 Describe the allowance method of accounting for uncollectible receivables.

9-4

9-5

Describe the common classes of receivables.

1

9-5

9-6

The term ? includes all money claims against other entities, including people, companies, and other organizations.

1

9-7

? are normally expected to be collected within a relatively short period, such as 30 or 60 days.

1

9-8

? are amounts that customers owe for which a formal, written instrument of credit has been issued.

1

9-9

Other receivables include ?.

If expected to be collected within ?, they are classified as current assets.

If collection is expected beyond one year, they are classified as noncurrent assets.

1

9-10

Describe the accounting for uncollectible receivables.

2

9-9

9-11

Regardless of how careful a company is in granting credit, some credit sales will be uncollectible.

The operating expense account is called ?, uncollectible accounts expense, or doubtful accounts expense.

2

9-12

The direct write off method records bad debt expense only when an account is judged to be worthless.

The allowance method records bad debt expense by estimating uncollectible accounts at the end of the accounting period.

2

9-13

The direct write off method is sometimes used by ? and companies with ? receivables.

Generally accepted accounting principles, however, require companies with a large amount of receivables to use the ? method.

2

9-14

Describe the direct write-off method of accounting for uncollectible receivables.

3

9-15

9-15

Under the direct write-off method, Bad Debt Expense is not recorded ?

At that time, the customer’s account receivable is written off.

3

9-16

On May 10, a $4,200 accounts receivable from D. L. Ross has been determined to be uncollectible.

3

?

9-17

The direct write-off method is used by businesses where receivables are a small part of the current assets and any bad debt expense is small or ?.

An amount is considered immaterial when it doesn’t affect the users of the financial statements or change their decisions regarding the company.

3

9-18

Example Exercise 9-13

Direct Write-off MethodJournalize the following transaction using the direct write-off method of accounting for uncollectible receivables.

Jul. 9 Received $1,200 from Jay Burke and wrote off the remainder owed of $3,900 as uncollectible.

9-19

Jul. 9 ?………………………………………….. ?

?………………………..... ?

?… ?

For Practice: PE 9-1

Follow My Example 9-1

9-19

Describe the allowance method of accounting for uncollectible receivables.

4

9-20

9-20

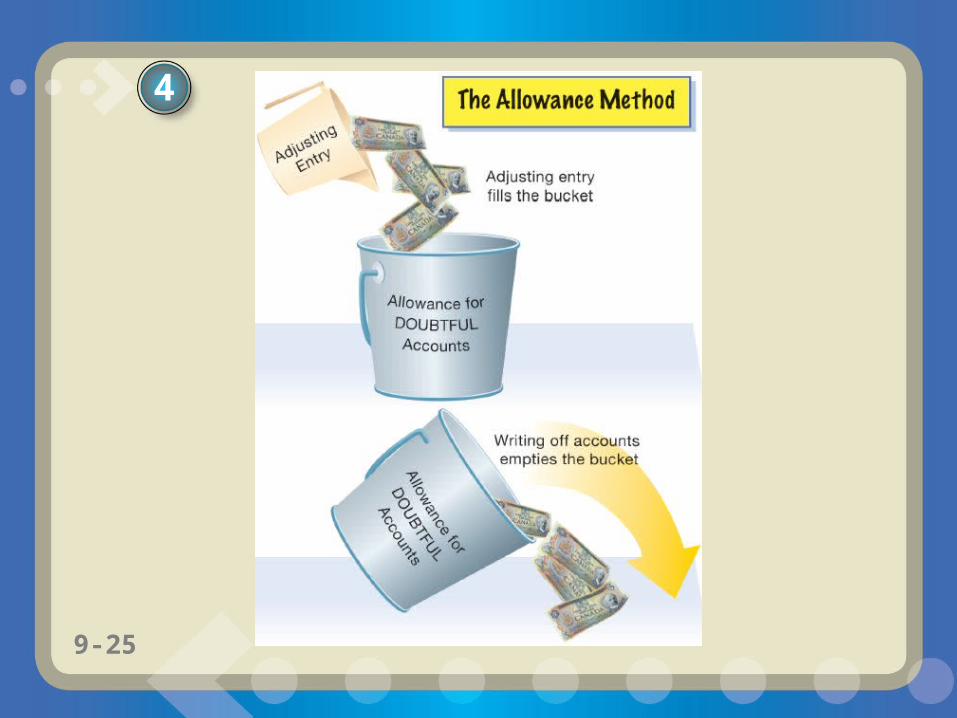

The allowance method estimates the uncollectible accounts receivable at the end of the accounting period.

Based on this estimate, Bad Debt Expense is recorded by an adjusting entry.

4

9-21

Because it is not known which specific customer accounts will become uncollectible, a contra asset account, ?, is credited for the estimated bad debts.

4

9-22

On December 31, ExTone Company estimates that a total of $30,000 of the $200,000 balance of their Accounts Receivable will eventually be uncollectible.

4

?

9-23

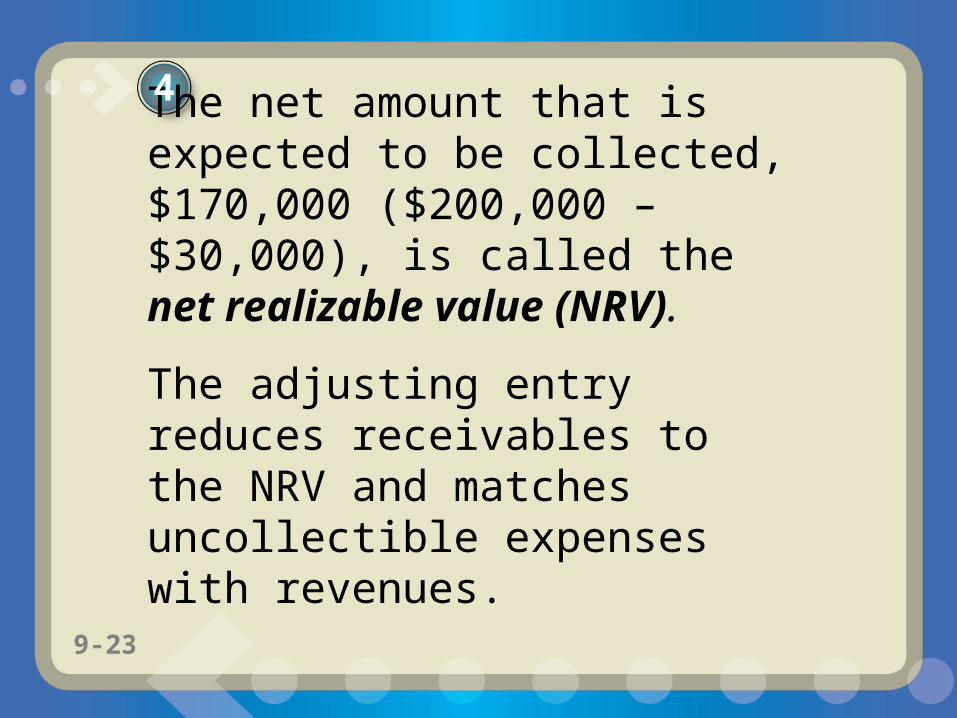

The net amount that is expected to be collected, $170,000 ($200,000 – $30,000), is called the net realizable value (NRV).

The adjusting entry reduces receivables to the NRV and matches uncollectible expenses with revenues.

4

9-24

Write-Offs to the Allowance Account

On January 21, John Parker’s account totaling $6,000 is written off because it is uncollectible.

4

?

9-25

4

9-26

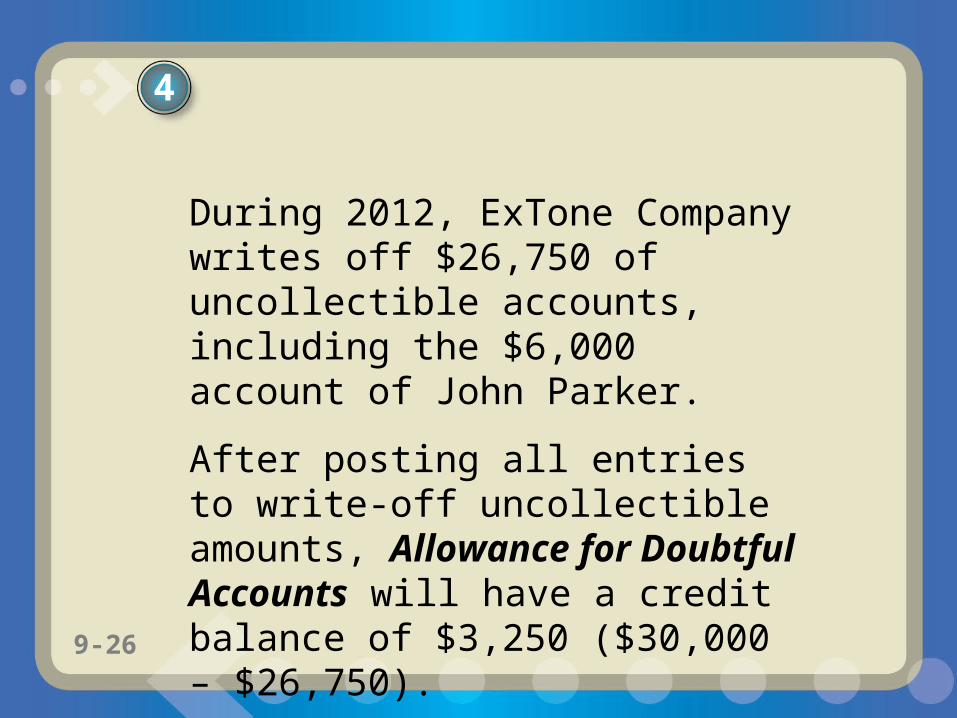

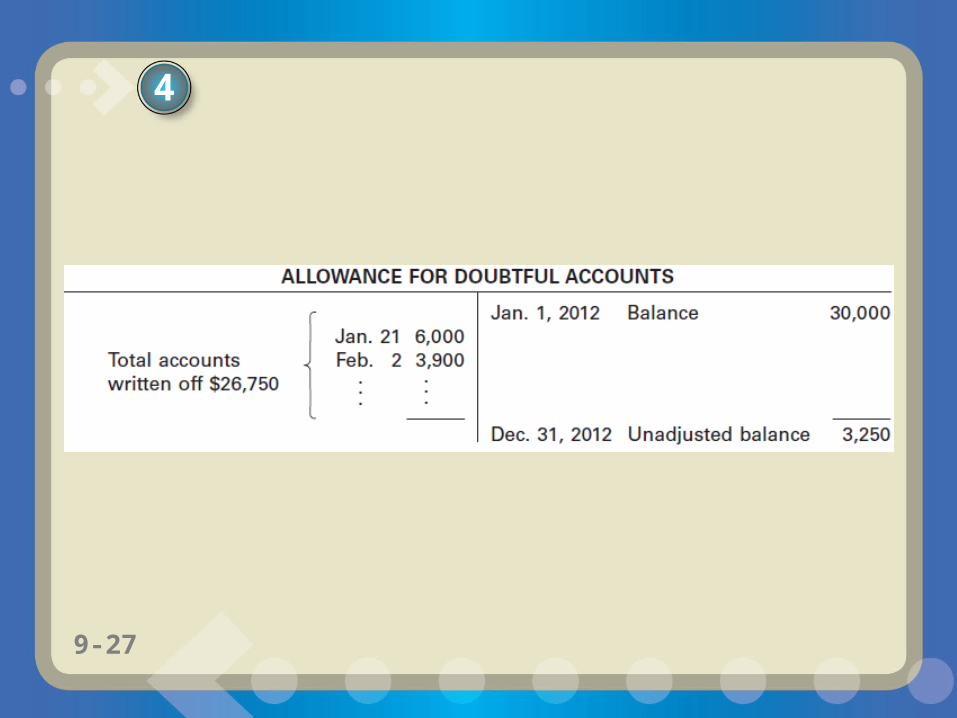

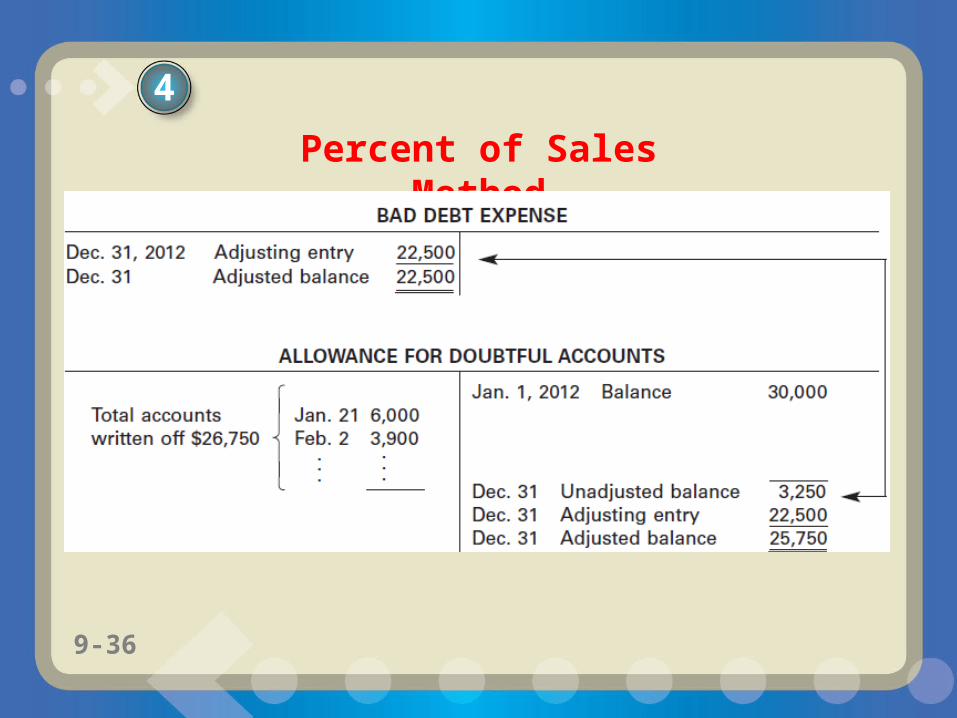

During 2012, ExTone Company writes off $26,750 of uncollectible accounts, including the $6,000 account of John Parker.

After posting all entries to write-off uncollectible amounts, Allowance for Doubtful Accounts will have a credit balance of $3,250 ($30,000 – $26,750).

4

9-27

4

9-28

An account receivable that has been written off against the allowance account may be collected later.

The account is reinstated by an entry that ? the write-off entry.

The cash received in payment is then recorded as a receipt on account.

4

Recovery of a Bad Debt

9-29

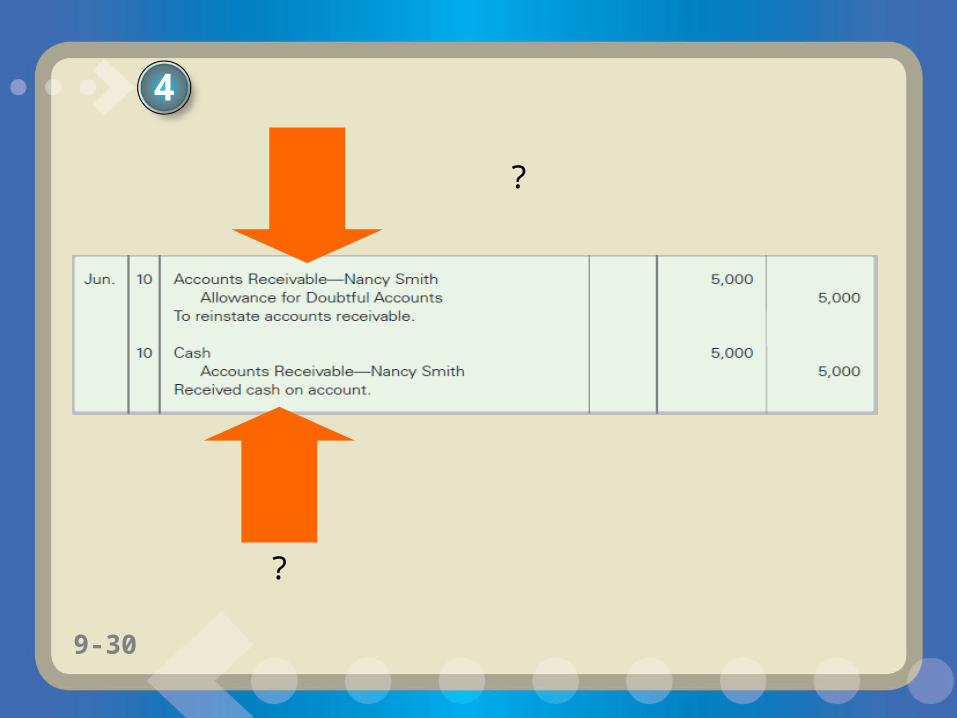

Nancy Smith’s account of $5,000, which was written off on April 2, is later collected on June 10.

Two entries are needed: ?

4

9-30

?

?

4

9-31

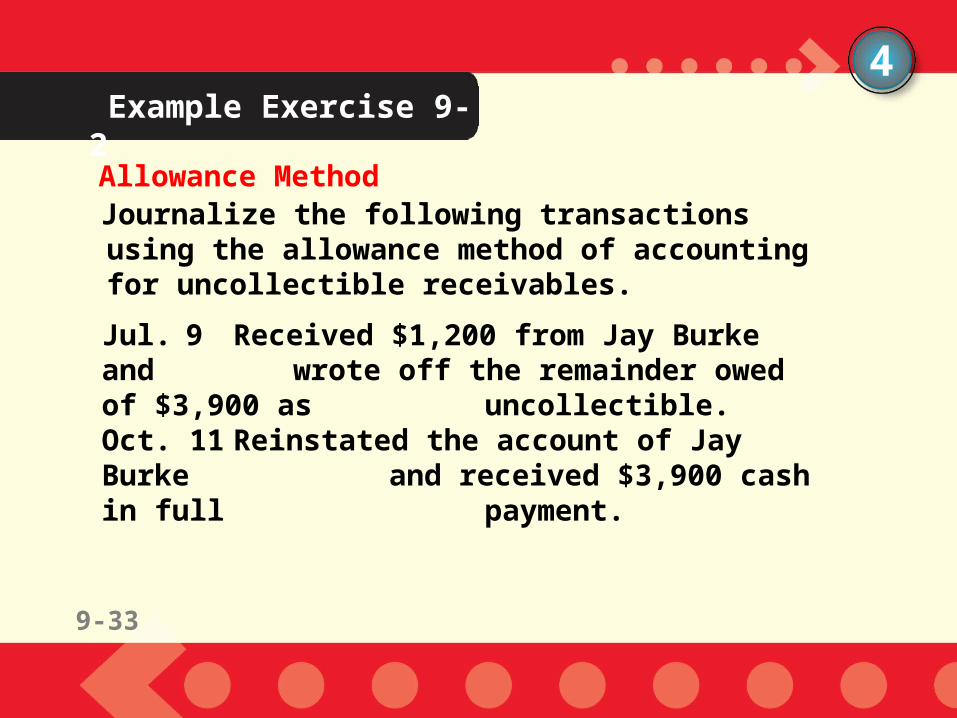

Example Exercise 9-24

Allowance MethodJournalize the following transactions using the allowance method of accounting for uncollectible receivables.

Jul. 9 Received $1,200 from Jay Burke and wrote off the remainder owed of $3,900 as uncollectible.

Oct. 11 Reinstated the account of Jay Burke and received $3,900 cash in full payment.

9-33

9-32

Example Exercise 9-2 (continued)

Jul. 9 ?…………………………………………… ?

?……….. ?

?……. ?

11 ?……………………………………………. ??…….. ?

9-34

For Practice: PE 9-2

Oct. 11 ?………... ?

?…….. ?

4

Follow My Example 9-2

9-33

Estimating Uncollectibles

2. Aging of receivables method.

The allowance method uses two ways to estimate the amount debited to Bad Debt Expense.1. Percent of sales method.

4

9-34

Percent of Sales Method

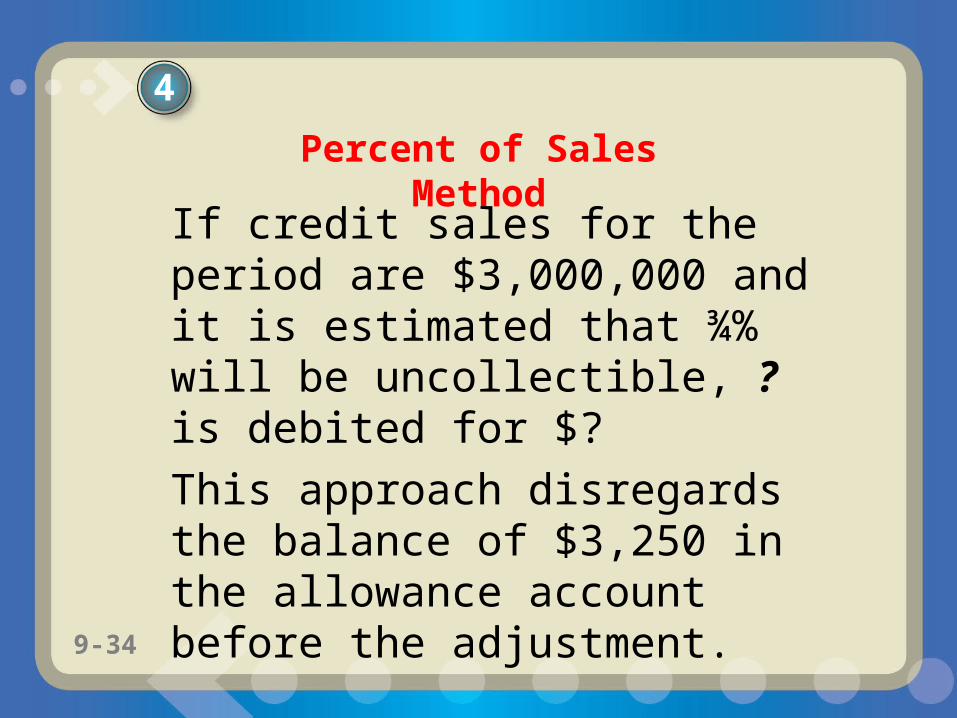

If credit sales for the period are $3,000,000 and it is estimated that ¾% will be uncollectible, ? is debited for $?

This approach disregards the balance of $3,250 in the allowance account before the adjustment.

4

9-35

Percent of Sales Method

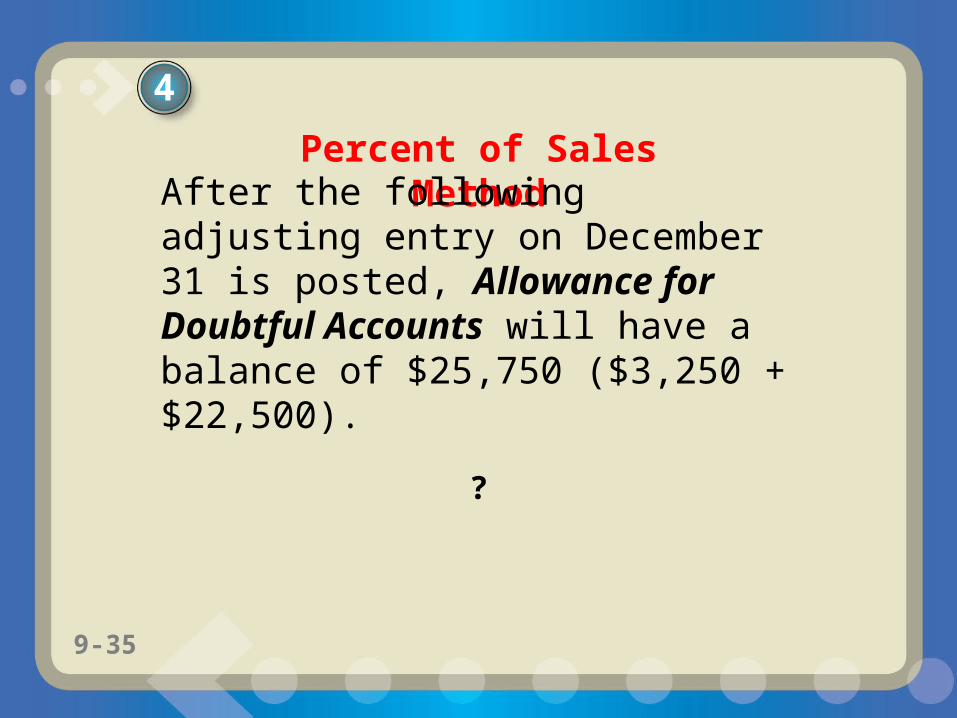

After the following adjusting entry on December 31 is posted, Allowance for Doubtful Accounts will have a balance of $25,750 ($3,250 + $22,500).

4

?

9-36

Percent of Sales Method

4

9-37

Example Exercise 9-34

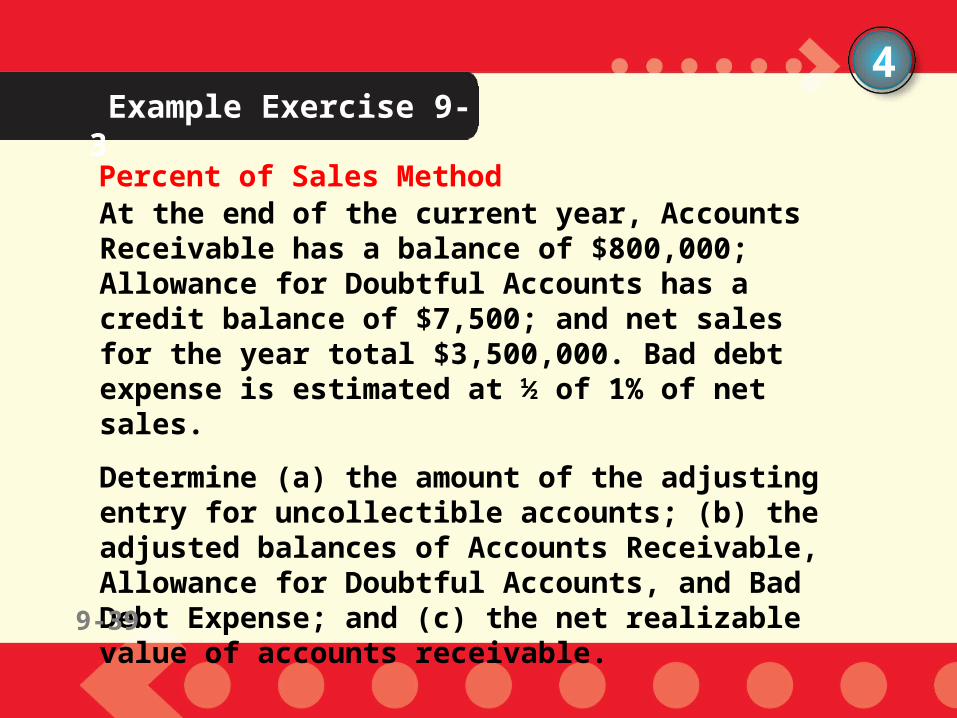

Percent of Sales MethodAt the end of the current year, Accounts Receivable has a balance of $800,000; Allowance for Doubtful Accounts has a credit balance of $7,500; and net sales for the year total $3,500,000. Bad debt expense is estimated at ½ of 1% of net sales.

Determine (a) the amount of the adjusting entry for uncollectible accounts; (b) the adjusted balances of Accounts Receivable, Allowance for Doubtful Accounts, and Bad Debt Expense; and (c) the net realizable value of accounts receivable.

9-39

9-38

4Example Exercise 9-3 (continued)

9-40

For Practice: PE 9-3

Follow My Example 9-3

9-39

Aging of Receivables

The longer an account receivable is outstanding, the less likely it is that it will be collected.

Basing the estimate of uncollectible accounts on how long specific amounts have been outstanding is called aging the receivables.

4

9-40

4Aging of Receivables Schedule December 31, 2012

Exhibit 1

9-41

The estimate based on receivables is compared to the balance in the allowance account to determine the amount of the adjusting entry.

4

Aging of Receivables Method

9-42

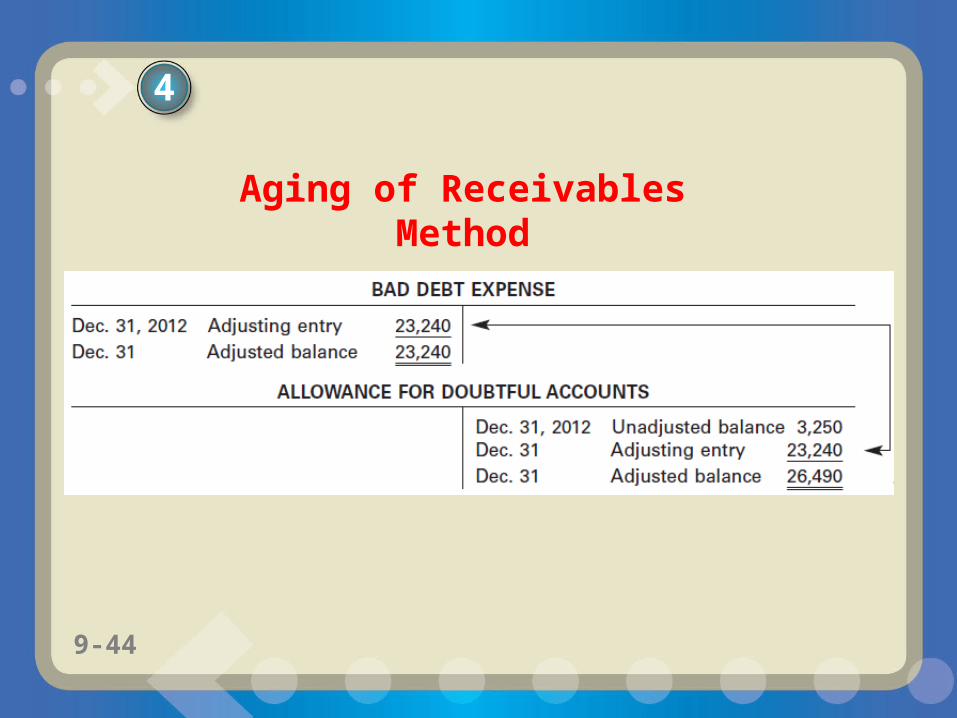

ExTone has an unadjusted credit balance of $3,250 in Allowance for Doubtful Accounts.

In Exhibit 1 the estimated uncollectible accounts totaled $26,490.

4

Aging of Receivables Method

9-43

The amount to be added to the allowance account is $23,240 ($26,490 – $3,250). The adjusting entry is as follows:

4

Aging of Receivables Method

?

9-44

4

Aging of Receivables Method

9-45

If the unadjusted balance of the allowance account had been a debit balance of $2,100, the amount of the adjustment would have been $28,590.

4

Aging of Receivables Method

9-46

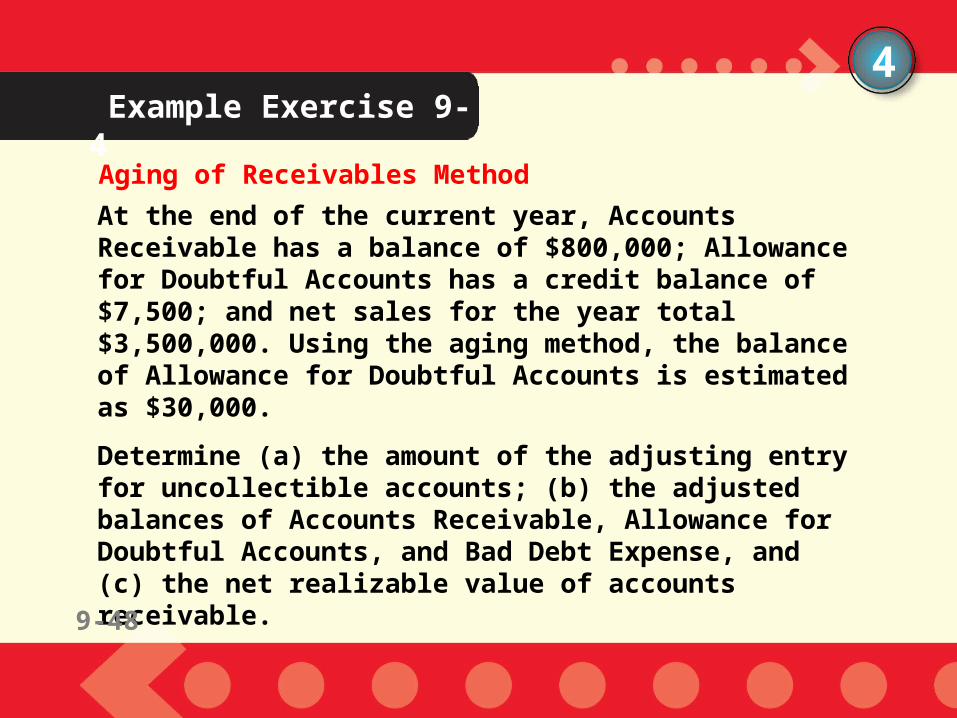

Example Exercise 9-44

Aging of Receivables Method

At the end of the current year, Accounts Receivable has a balance of $800,000; Allowance for Doubtful Accounts has a credit balance of $7,500; and net sales for the year total $3,500,000. Using the aging method, the balance of Allowance for Doubtful Accounts is estimated as $30,000.

Determine (a) the amount of the adjusting entry for uncollectible accounts; (b) the adjusted balances of Accounts Receivable, Allowance for Doubtful Accounts, and Bad Debt Expense, and (c) the net realizable value of accounts receivable.

9-48

9-47

4Example Exercise 9-4 (continued)

(a) ?

(b) ?

(c) ?

9-49

For Practice: PE 9-4

Follow My Example 9-4

9-48

Differences Between Estimation Methods

Compare and contrast:

Percent of Sales Method vs

Aging of Receivables

Describe the focus of each method, financial statement of emphasis, and use the ExTone

Company example to describe/show the financial impact on the Bad Debt Expense Estimate and

Allowance for Doubtful Accounts Estimate.