Embed Size (px)

Citation preview

NEW ISSUE – BOOK-ENTRY NOT RATED

(See “CONCLUDING INFORMATION - No Rating on the Bonds; Secondary Market” herein)

In the opinion of Jones Hall, A Professional Law Corporation, San Francisco, California, Bond Counsel, subject, however to certain qualifications described herein, under existing law, the interest on the Bonds is excluded from gross income for federal income tax purposes and such interest is not an item of tax preference for purposes of the federal alternative minimum tax imposed on individuals and corporations, although for the purpose of computing the alternative minimum tax imposed on certain corporations, such interest is taken into account in determining certain income and earnings. In the further opinion of Bond Counsel, such interest is exempt from California personal income taxes. See “LEGAL MATTERS - Tax Matters” herein.

SANTA CRUZ COUNTY STATE OF CALIFORNIA

$815,000 COUNTY OF SANTA CRUZ

LIMITED OBLIGATION IMPROVEMENT BONDS ASSESSMENT DISTRICT NO. 15-01

(ORCHARD DRIVE SEWER EXTENSION PROJECT)

Dated: Date of Delivery Due: September 2 as Shown on the Inside Front Cover.

The cover page contains certain information for quick reference only. It is not a summary of the issue. Investors must read the entire Official Statement to obtain information essential to the making of an informed investment decision. Investment in the Bonds involves risks. See “RISK FACTORS” herein for a discussion of special risk factors that should be considered in evaluating the investment quality of the Bonds.

The County of Santa Cruz Limited Obligation Improvement Bonds, Assessment District No. 15-01 (Orchard Drive Sewer Extension Project) (the “Bonds”) are being issued by the County of Santa Cruz (the “County”) pursuant to a Fiscal Agent Agreement, dated as of February 1, 2016 (the “Fiscal Agent Agreement”), by and between the County and The Bank of New York Mellon Trust Company, N.A., as fiscal agent (the “Fiscal Agent”) to: (i) finance the construction of sewer improvements, (ii) pay costs related to the issuance of the Bonds, (iii) capitalize interest on the Bonds through September 2, 2016 and (iv) make a deposit to a Reserve Fund for the Bonds.

The Bonds are being issued pursuant to provisions of the Improvement Bond Act of 1915, being Division 10 of the California Streets and Highways Code (the “Bond Law”). The Bonds are payable from assessments levied pursuant to the Municipal Improvement Act of 1913 (Division 12 of the California Streets and Highways Code) (the “1913 Act”). See “SOURCES OF PAYMENT FOR THE BONDS” and “RISK FACTORS” herein.

Interest on the Bonds is payable semiannually on September 2 and March 2 each year, commencing September 2, 2016 (each, an “Interest Payment Date”), until maturity. The Bonds are subject to optional, sinking fund and extraordinary redemption as described herein. See “THE BONDS - Redemption” herein.

The Bonds are offered when, as and if issued subject to the approval as to their legality by Jones Hall, A Professional Law Corporation, San Francisco, California, Bond Counsel and certain other conditions. Certain legal matters will be passed on for the County by the County Counsel and by Jones Hall, A Professional Law Corporation, San Francisco, California, Disclosure Counsel. It is anticipated that the Bonds in book-entry form will be available for delivery through the facilities of The Depository Trust Company, on or about February 23, 2016.

The date of this Official Statement is February 10, 2016.

2016-0082

$815,000 COUNTY OF SANTA CRUZ

LIMITED OBLIGATION IMPROVEMENT BONDS ASSESSMENT DISTRICT NO. 15-01

(ORCHARD DRIVE SEWER EXTENSION PROJECT)

MATURITY SCHEDULE

(Base CUSIP®† 80182L)

$280,000 Serial Bonds

Maturity Date Principal Interest Reoffering Reoffering

September 2 Amount Rate Yield Price CUSIP®†

2017 $20,000 2.00% 1.04% 101.448 ED3

2020 20,000 2.00 1.66 101.476 EG6

2021 20,000 2.00 1.76 101.258 EH4

2022 20,000 2.00 1.95 100.304 EJ0

2023 20,000 2.00 2.16 98.893 EK7

2024 20,000 2.375 2.38 99.961 EL5

2025 20,000 2.50 2.52 99.831 EM3

2026 20,000 2.625 2.68 99.498 EN1

2027 20,000 2.75 2.81 99.412 EP6

2028 25,000 2.875 2.95 99.218 EQ4

2029 25,000 3.00 3.02 99.778 ER2

2030 25,000 3.00 3.09 98.952 ES0

2031 25,000 3.125 3.18 99.329 ET8

$40,000 2.00% Term Bond maturing September 2, 2019, Yield 1.40%, Price 102.056 CUSIP®† EF8

$140,000 3.25% Term Bond maturing September 2, 2036, Yield 3.47%, Price 96.788 CUSIP®† EY7

$165,000 3.60% Term Bond maturing September 2, 2041, Yield 3.73%, Price 97.870 CUSIP®† FD2

$190,000 3.625% Term Bond maturing September 2, 2046, Yield 3.78%, Price 97.206 CUSIP®† FJ9

† Copyright 2016, American Bankers Association. CUSIP® is a registered trademark of the American Bankers Association. CUSIP data herein is provided by CUSIP Global Services Bureau, operated by Standard & Poor’s. This data is not intended to create a database and does not serve in any way as a substitute for CUSIP Global Services. CUSIP numbers have been assigned by an independent company not affiliated with the County and are included solely for the convenience of the holders of the Bonds. None of the County, the Municipal Advisor or the Underwriter takes any responsibility for the selection or uses of these CUSIP numbers, and no representation is made as to their correctness on the Bonds or as included herein. The CUSIP number for a specific maturity is subject to being changed after the issuance of the Bonds as a result of various subsequent actions including, but not limited to, a refunding in whole or in part or as a result of the procurement of secondary market portfolio insurance or other similar enhancement by investors that is applicable to all or a portion of certain maturities of the Bonds.

GENERAL INFORMATION ABOUT THIS OFFICIAL STATEMENT

Use of Official Statement. This Official Statement is submitted in connection with the offer and sale of the Bonds referred to herein and may not be reproduced or used, in whole or in part, for any other purpose. This Official Statement is not to be construed as a contract with the purchasers of the Bonds.

Effective Date. This Official Statement speaks only as of its date, and the information and expressions of opinion contained in this Official Statement are subject to change without notice. Neither the delivery of this Official Statement nor any sale of the Bonds will, under any circumstances, create any implication that there has been no change in the affairs of the County or any other parties described in this Official Statement.

Estimates and Forecasts. When used in this Official Statement and in any continuing disclosure by the County, any press release and any oral statement made with the approval of an authorized officer of the County or any other entity described or referenced herein, the words or phrases “will likely result,” “are expected to,” “will continue,” “is anticipated,” “estimate,” “project,” “forecast,” “expect,” “intend” and similar expressions identify “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements are subject to risks and uncertainties that could cause actual results to differ materially from those contemplated in such forward-looking statements. Any forecast is subject to such uncertainties. Inevitably, some assumptions used to develop the forecasts will not be realized and unanticipated events and circumstances may occur. Therefore, there are likely to be differences between forecasts and actual results, and those differences may be material.

Limit of Offering. No dealer, broker, salesperson or other person has been authorized by the County to give any information or to make any representations in connection with the offer or sale of the Bonds other than those contained herein and if given or made, such other information or representation must not be relied upon as having been authorized by the County, the Municipal Advisor or the Underwriter. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Bonds by a person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale.

Preparation of this Official Statement. The information contained in this Official Statement has been obtained from sources that are believed to be reliable, but this information is not guaranteed as to accuracy or completeness. The information and expressions of opinions herein are subject to change without notice and neither the delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the County since the date hereof. This Official Statement is submitted in connection with the sale of the Bonds referred to herein and may not be reproduced or used, in whole or in part, for any other purpose, unless authorized in writing by the County. All summaries of the Bonds, the Fiscal Agent Agreement or other documents, are made subject to the provisions of such documents and do not purport to be complete statements of any or all of such provisions. Reference is hereby made to such documents on file with the Auditor-Controller-Treasurer-Tax Collector for further information. See “INTRODUCTION - Summary Not Definitive.”

The Underwriter has provided the following sentence for inclusion in this Official Statement: The Underwriter has reviewed the information in this Official Statement in accordance with, and as part of, its responsibilities to investors under the federal securities laws as applied to the facts and circumstances of this transaction, but the Underwriter does not guarantee the accuracy or completeness of such information.

Bonds are Exempt from Securities Laws Registration. The issuance, sale and delivery of the Bonds has not been registered under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended, in reliance upon exemptions for the execution, sale and delivery of municipal securities provided under Section 3(a)(2) of the Securities Act of 1933 and Section 3(a)(l2) of the Securities Exchange Act of 1934.

Stabilization of Prices. In connection with this offering, the Underwriter may overallot or effect transactions which stabilize or maintain the market price of the Bonds at a level above that which might otherwise prevail in the open market. Such stabilizing, if commenced, may be discontinued at any time. The Underwriter may offer and sell the Bonds to certain dealers and others at prices lower than the public offering prices set forth on the inside cover page hereof and said public offering prices may be changed from time to time by the Underwriter.

County Website. The County maintains a website. The information on such website is not part of this Official Statement and is not intended to be relied on by investors with respect to the Bonds unless specifically set forth or incorporated herein.

COUNTY OF SANTA CRUZ, CALIFORNIA

BOARD OF SUPERVISORS

John Leopold, Supervisor, 1st District Zach Friend, Supervisor, 2nd District

Ryan Coonerty, Supervisor, 3rd District Greg Caput, Supervisor, 4th District

Bruce McPherson, Supervisor, 5th District ________________________________________

COUNTY STAFF

Susan A. Mauriello, County Administrative Officer Edith Driscoll, Auditor-Controller-Treasurer-Tax Collector

Carlos Palacios, Assistant County Administrative Officer John Presleigh, Director of Public Works

Dana McRae, County Counsel ________________________________________

PROFESSIONAL SERVICES

Bond Counsel and Disclosure Counsel Jones Hall

A Professional Law Corporation San Francisco, California

Municipal Advisor Harrell & Company Advisors, LLC

Orange, California

Assessment Engineer Bowman & Williams Santa Cruz, California

Fiscal Agent The Bank of New York Mellon Trust Company, N.A.

Los Angeles, California

TABLE OF CONTENTS

INTRODUCTION ...................................................... 1 The County ................................................................ 1 The District ................................................................ 1 Security and Sources of Repayment for the

Bonds ...................................................................... 1 Purpose ...................................................................... 2 Property Values .......................................................... 2 Summary Not Definitive ............................................ 2

THE FINANCING PLAN .......................................... 3 Estimated Uses of Funds............................................ 3 Estimated Improvement Costs ................................... 3

THE BONDS ............................................................... 4 Authority for Issuance ............................................... 4 General Provisions ..................................................... 4 Book-Entry System .................................................... 5 Redemption ................................................................ 5 Scheduled Debt Service on the Bonds ....................... 8

THE DISTRICT ....................................................... 11 General ..................................................................... 11 Assessed Values ....................................................... 11 Assessment Parcels .................................................. 13 Assessed Value to Assessment Lien Ratios .............. 15 Delinquencies .......................................................... 16 Effective Tax Rates .................................................. 16 Direct and Overlapping Debt ................................... 17

SOURCES OF PAYMENT FOR THE BONDS ................................................................... 19 Repayment of the Bonds .......................................... 19 Reserve Fund ........................................................... 22

RISK FACTORS ....................................................... 23 General ..................................................................... 23 Payment of the Assessment Not a Personal

Obligation ............................................................. 23 No County Obligation to Pay Debt Service ............. 23 Risks of Real Estate Secured Investments

Generally ............................................................... 23 Risks Related to Declines in Home Values .............. 24 Valuation of Property in the District ........................ 24 Factors Affecting Parcel Value and Aggregate

Values .................................................................... 26

Other Possible Claims Upon the Value of an Assessment Parcel ................................................. 27

Risks Related to Availability of Mortgage Loans ..................................................................... 27

Foreclosure and Sale Proceedings ........................... 28 Depletion of Reserve Fund ...................................... 28 Prepayment of Assessments ..................................... 29 Bankruptcy ............................................................... 29 FDIC/Federal Government Interests in

Properties .............................................................. 29 Loss of Tax Exemption ............................................ 31 IRS Audit of Tax-Exempt Bond Issues .................... 31 No Acceleration Provision ....................................... 31 Proposition 218 ........................................................ 31 Ballot Initiatives and Legislative Measures ............. 32 Limited Secondary Market ...................................... 33 Limitations on Remedies ......................................... 33

LEGAL MATTERS .................................................. 34 Enforceability of Remedies ..................................... 34 Approval of Legal Proceedings ............................... 34 Tax Matters .............................................................. 34 Absence of Litigation .............................................. 35

CONCLUDING INFORMATION .......................... 36 No Rating on the Bonds; Secondary Market ........... 36 Underwriting ............................................................ 36 The Municipal Advisor ............................................ 36 Continuing Disclosure ............................................. 36 Execution ................................................................. 37

APPENDIX A - COUNTY OF SANTA CRUZ INFORMATION STATEMENT

APPENDIX B - SUMMARY OF THE FISCAL AGENT AGREEMENT

APPENDIX C - FORM OF CONTINUING DISCLOSURE CERTIFICATE

APPENDIX D - PROPOSED FORM OF OPINION OF BOND COUNSEL

APPENDIX E - THE BOOK-ENTRY SYSTEM

San Francisco

Sacramento

Santa Cruz

San Diego

Los Angeles

San Jose

Bakersfield

Fresno

SANTA CRUZ COUNTY LOCATION MAP

1

OFFICIAL STATEMENT $815,000

COUNTY OF SANTA CRUZ LIMITED OBLIGATION IMPROVEMENT BONDS

ASSESSMENT DISTRICT NO. 15-01 (ORCHARD DRIVE SEWER EXTENSION PROJECT)

This Official Statement which includes the cover page and appendices (the “Official Statement”) is provided to furnish certain information concerning the sale of the County of Santa Cruz Limited Obligation Improvement Bonds, Assessment District No. 15-01 (Orchard Drive Sewer Extension Project) (the “Bonds”).

INTRODUCTION The description and summaries of various documents hereinafter set forth do not purport to be comprehensive or definitive, and reference is made to each document for the complete details of all terms and conditions. All statements herein are qualified in their entirety by reference to each document. All capitalized terms used in this Official Statement and not otherwise defined herein have the same meaning as in the Fiscal Agent Agreement (defined below).

The County

The County was incorporated in 1850. It has a general law form of government. It is located on the coast of California, between the San Francisco Bay area and the Monterey Bay Peninsula, 74 miles south of San Francisco.

For further information concerning the County, see “APPENDIX A - COUNTY OF SANTA CRUZ INFORMATION STATEMENT” herein.

The District

Assessment District No. 15-01 (the “District”) was created by the County pursuant to proceedings taken under the Municipal Improvement Act of 1913 (Division 12 of the Streets and Highways Code) (the “1913 Act”). The District includes a total of 27 parcels, of which 23 parcels are subject to the Assessments (as defined below) securing the Bonds. See “THE DISTRICT” herein. As of the Closing Date, the Assessments total $816,500, $1,500 more than the par amount of the Bonds.

Security and Sources of Repayment for the Bonds

The Bonds will be issued under the Fiscal Agent Agreement, dated as of February 1, 2016 (the “Fiscal Agent Agreement”), between the County and The Bank of New York Mellon Trust Company, N.A., Los Angeles, California, as fiscal agent (the “Fiscal Agent”) (see “APPENDIX B - SUMMARY OF THE FISCAL AGENT AGREEMENT” herein) and pursuant to the Act.

The Bonds are limited obligations of the County secured by a first lien on the unpaid assessments (the “Assessments”) levied by the County on the parcels in the District with unpaid assessments (the “Assessment Parcels”) pursuant to the 1913 Act and the funds pledged therefor under the Fiscal Agent Agreement. Assessments levied on the property in the District are estimated to be sufficient, if paid

2

timely, to pay the aggregate amount of the principal and interest on the Bonds. See “SOURCES OF PAYMENT FOR THE BONDS” and “RISK FACTORS” herein.

The County has covenanted to cause foreclosure proceedings to be commenced and prosecuted against Assessment Parcels with delinquent installments of Assessments under certain circumstances. For a more detailed description of the foreclosure covenant see “SOURCES OF PAYMENT FOR THE BONDS - Repayment of the Bonds - Foreclosure Covenant.”

The Bonds are special obligations of the County payable solely from the unpaid Assessments and other assets pledged therefor under the Fiscal Agent Agreement. The Bonds do not constitute a debt or liability of the County, the State of California or of any political subdivision thereof, other than the County to the limited extent described herein. The County shall only be obligated to pay the principal of the Bonds, and the interest thereon, from the funds described herein, and neither the faith and credit nor the taxing power of the County or the State of California or any political subdivision thereof is pledged to the payment of the principal of or the interest on the Bonds, except to the limited extent described herein. See “SOURCES OF PAYMENT FOR THE BONDS” and “RISK FACTORS” herein.

Purpose

Proceeds from the Bonds will be used to (i) finance the construction of public improvements of benefit to property within the District, (ii) pay costs related to the issuance of the Bonds, (iii) capitalize interest on the Bonds through September 2, 2016 and (iv) make a deposit to a Reserve Fund for the Bonds (see “THE FINANCING PLAN - Estimated Uses of Funds” herein).

Property Values

The County has relied on the assessed valuations of the County Assessor for the valuations for the 23 Assessment Parcels presented in this Official Statement. See “RISK FACTORS” and “THE DISTRICT - Assessed Values.”

Summary Not Definitive

The summaries and references contained herein with respect to the Fiscal Agent Agreement and other statutes or documents do not purport to be comprehensive or definitive and are qualified by reference to each such document or statute, and references to the Bonds are qualified in their entirety by reference to the form thereof included in the Fiscal Agent Agreement. Capitalized terms used herein and not defined shall have the meaning set forth in the Fiscal Agent Agreement. Copies of the documents described herein are available for inspection during the period of initial offering of the Bonds at the offices of the Municipal Advisor, Harrell & Company Advisors, LLC, 333 City Boulevard West, Suite 1430, Orange, California 92868, telephone (714) 939-1464. Copies of these documents may be obtained after delivery of the Bonds from the Auditor-Controller-Treasurer-Tax Collector, County of Santa Cruz, 701 Ocean Street, Santa Cruz, California 95060.

3

THE FINANCING PLAN

Estimated Uses of Funds

The net proceeds from the sale of the Bonds, equal to $785,937.95 (par amount of $815,000.00, less net original issue discount of $12,762.05 and less Underwriter’s discount of $16,300.00), will be applied as follows:

Improvement Fund $651,741.01 Reserve Fund (1) 45,752.50Capitalized Interest Account (2) 13,244.44Costs of Issuance Fund (3) 75,200.00 Total Uses $785,937.95 __________________________________________

(1) Equal to the Reserve Requirement for the Bonds as of the closing date. See “SOURCES OF PAYMENT FOR THEBONDS - Reserve Fund.”

(2) Interest on the Bonds is capitalized through September 2, 2016.

(3) Costs of Issuance includes Bond Counsel fee, Disclosure Counsel fee, Fiscal Agent fee, Municipal Advisor fee,Assessment Engineer fee, printing costs and other miscellaneous costs of issuance.

Estimated Improvement Costs

The data shown below is the estimated costs of the public sewer facilities (the “Facilities”) contained in the Engineer’s Report prepared by Bowman & Williams, Consulting Civil Engineers and construction bids received December 10, 2015. The Facilities consist of an extension of the sanitary sewer pipeline, necessary to connect homes in the District to the existing sewer system.

Construction Costs (with contingency) $476,298 Design and Construction Administration 49,500 Connection Fees 192,978 County Administrative Costs 52,238 Total Improvement Costs 771,014 Less: Prepaid Assessments (119,273) Deposit to Improvement Fund $651,741

4

THE BONDS

Authority for Issuance

The Bonds are issued by the County pursuant to the 1913 Act, the Improvement Bond Act of 1915, as amended, Division 10 of the California Streets and Highways Code (the “Bond Law”) and Resolution No. 28-2016 adopted by the Board of Supervisors on January 26, 2016 (the “Resolution”).

General Provisions

Repayment of the Bonds. The Bonds shall be issued as fully registered Bonds without coupons in the denomination of $5,000 or any integral multiple thereof, except that one Bond may contain any off amount, and shall mature as set forth on the inside front cover page. The Bonds shall bear interest at the rates set forth on the inside front cover page payable on each March 2 and September 2 (the “Interest Payment Dates”) in each year, beginning September 2, 2016. Interest shall be calculated on the basis of a 360-day year composed of twelve 30-day months. Each Bond shall bear interest from the InterestPayment Date next preceding the date of authentication thereof unless (i) it is authenticated and registeredas of an Interest Payment Date, in which event it shall bear interest from such Interest Payment Date, or(ii) it is authenticated prior to the first Interest Payment Date of September 2, 2016, in which event it shallbear interest from the Bond Date, which is the closing date of the Bonds.

Interest on the Bonds (including the final interest payment upon maturity or earlier redemption) is payable in lawful money of the United States of America by check of the Fiscal Agent mailed by first class mail on the applicable Interest Payment Date to the registered Owner thereof at such registered Owner’s address as it appears on the Bond register maintained by the Fiscal Agent at the close of business on the 15th day of the calendar month immediately preceding the applicable Interest Payment Date, whether or not such day is a Business Day (a “Record Date”), or by wire transfer made on such Interest Payment Date upon written instructions of any Owner of $1,000,000 or more in aggregate principal amount of Bonds delivered to the Fiscal Agent prior to the applicable Record Date. The principal of the Bonds and any premium on the Bonds are payable in lawful money of the United States of America upon surrender of the Bonds at the Principal Office of the Fiscal Agent, except as provided in “APPENDIX E - THE BOOK-ENTRY SYSTEM.”

Transfer or Exchange of Bonds. Any Bond may, in accordance with its terms, be transferred, upon the Bond register by the person in whose name it is registered, in person or by such person's duly authorized attorney, upon surrender of such Bond for cancellation, accompanied by delivery of a duly written instrument of transfer in a form approved by the Fiscal Agent. Whenever any Bond or Bonds are surrendered for transfer, the County shall execute and the Fiscal Agent shall authenticate and deliver a new Bond or Bonds, for like aggregate principal amount(s), maturity(ies) and interest rate(s) in the denominations authorized by the Fiscal Agent Agreement. Bonds may be presented for exchange at the Principal Office of the Fiscal Agent for a like aggregate principal amount of Bonds of authorized denominations and of the same maturity. The cost for any services rendered or any expenses incurred by the Fiscal Agent in connection with any such transfer or exchange shall be paid by the County; provided, however, that the Fiscal Agent shall collect from the Owner requesting such transfer or exchange any tax or other governmental charge required to be paid with respect to such transfer, including the costs otherwise payable by the County.

Neither the County nor the Fiscal Agent will be required to make any transfer or exchange of Bonds on or after a Record Date and before the next ensuing Interest Payment Date.

5

The foregoing provisions regarding the transfer and exchange of the Bonds apply only if the book-entry system is discontinued. So long as the Bonds are in the book-entry system of The Depository Trust Company (“DTC”) as described below, the rules of DTC will apply for the transfer and exchange of Bonds.

Book-Entry System

DTC will act as securities depository for the Bonds. The Bonds will be issued as fully registered securities registered in the name of Cede & Co. (DTC’s partnership nominee) or such other name as may be requested by an authorized representative of DTC. One fully registered Bond will be issued for each maturity of the Bonds, each in the aggregate principal amount of such maturity, and will be deposited with DTC. Purchasers of beneficial interests in the Bonds will not receive physical certificates. For information on DTC and its book-entry system, see “APPENDIX E.”

Discontinuance of Book-Entry System. DTC may discontinue providing its services as securities depository with respect to the Bonds at any time by giving reasonable notice to the County or the Fiscal Agent. Under such circumstances, in the event that a successor securities depository is not obtained, Bonds are required to be printed and delivered as described in the Fiscal Agent Agreement. The County may decide to discontinue use of the system of book-entry transfers through DTC (or a successor securities depository). In that event, the Bonds will be printed and delivered as described in the Fiscal Agent Agreement.

Redemption

Optional Redemption. The Bonds may be redeemed prior to maturity, in whole or in part, at the option of the County beginning on September 2, 2016 and on any Interest Payment Date thereafter, from any source of available funds, at a redemption price (expressed as a percentage of the principal amount of Bonds to be redeemed) together with accrued interest to the date fixed for redemption as follows:

Redemption Dates Redemption PricesSeptember 2, 2016 through and including March 2, 2024 103%September 2, 2024 and March 2, 2025 102%September 2, 2025 and March 2, 2026 101%September 2, 2026 and any Interest Payment Date thereafter 100%

Extraordinary Redemption from Assessment Prepayments. The Bonds are subject to extraordinary redemption prior to their stated maturities, as a whole or in part on a pro-rata basis among maturities, as a result of the prepayment of Assessments, from amounts deposited in the Prepayment Account of the Redemption Fund, on any Interest Payment Date, at a redemption price (expressed as a percentage of the principal amount of the Bonds to be redeemed) plus with accrued interest to the date of redemption, as follows:

Redemption Dates Redemption PricesSeptember 2, 2016 through and including March 2, 2024 103%September 2, 2024 and March 2, 2025 102%September 2, 2025 and March 2, 2026 101%September 2, 2026 and any Interest Payment Date thereafter 100%

6

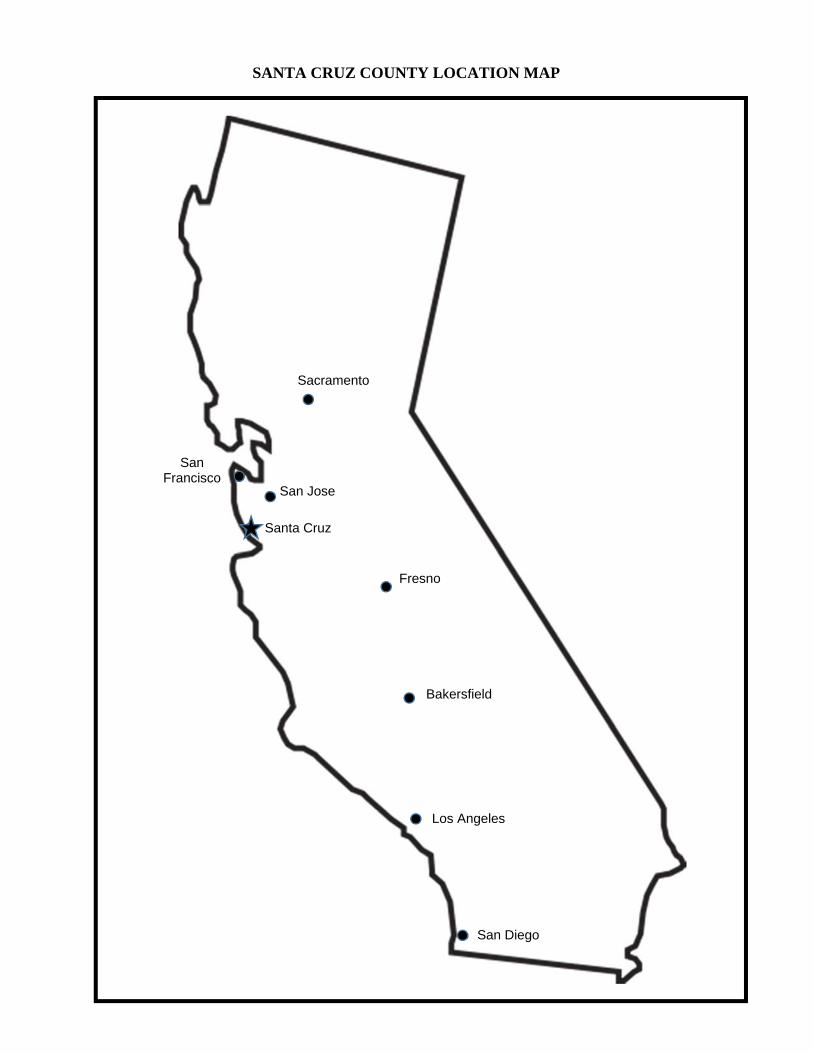

Mandatory Sinking Fund Redemption of Bonds. The Bonds maturing September 2, 2019, September 2036, September 2041 and September 2, 2046, (collectively, the “Term Bonds”) are subject to mandatory redemption in part by lot from Sinking Fund Payments made by the County at a redemption price equal to the principal amount thereof to be redeemed, plus accrued interest to the redemption date, without premium, in the aggregate respective principal amounts and on the dates as set forth in the following schedules; provided, however, if some but not all of the Term Bonds have been redeemed through optional redemption or extraordinary redemption from prepayments, the total amount of all future Sinking Fund Payments shall be reduced by the aggregate principal amount of Term Bonds of such maturity so redeemed, to be allocated among such Sinking Fund Payments on a pro rata basis integral multiples of $5,000 as determined by the Fiscal Agent, notice of which determination shall be given by the Fiscal Agent to the County.

SINKING PAYMENT SCHEDULE FOR TERM BONDS MATURING SEPTEMBER 2, 2019

Redemption Date September 2 Principal Amount

2018 $20,000 2019 (maturity) 20,000

SINKING PAYMENT SCHEDULE FOR TERM BONDS MATURING SEPTEMBER 2, 2036

Redemption Date September 2 Principal Amount

2032 $25,0002033 25,0002034 30,0002035 30,0002036 (maturity) 30,000

SINKING PAYMENT SCHEDULE FOR TERM BONDS MATURING SEPTEMBER 2, 2041

Redemption Date September 2 Principal Amount

2037 $30,0002038 30,0002039 35,0002040 35,0002041 (maturity) 35,000

SINKING PAYMENT SCHEDULE FOR TERM BONDS MATURING SEPTEMBER 2, 2046

Redemption Date September 2 Principal Amount

2042 $35,0002043 35,0002044 40,0002045 40,0002046 (maturity) 40,000

7

Selection of Bonds for Redemption. Whenever provision is made in the Fiscal Agent Agreement for the redemption of less than all of the Bonds, the County shall select Bonds for redemption in such a way that the ratio of Outstanding Bonds to issued Bonds shall be approximately the same in each annual series insofar as possible (i.e. on a pro rata basis among maturities of the Bonds). Within each annual maturity, the Fiscal Agent shall select Bonds for retirement by lot.

For purposes of such selection, all Bonds will be deemed to be comprised of separate $5,000 denominations and such separate denominations will be treated as separate Bonds which may be separately redeemed. Further, the provisions of Part 11.1 of the Bond Law are applicable to the advance payment of Assessments and to the calling of the Bonds.

Notice of Redemption. The Fiscal Agent shall cause notice of any redemption to be given by registered or certified mail or by personal service to the respective registered Owners of any Bonds designated for redemption, at their addresses appearing on the Bond Register in the Principal Office of the Fiscal Agent at least 30 days before the applicable Interest Payment Date. The Fiscal Agent shall also cause notice of redemption to be sent to the Securities Depositories at least one day earlier than the giving of notice to the Owners as aforesaid; provided, however, such mailing to the Securities Depositories shall not be a condition precedent to such redemption. Failure to so mail any notice of redemption, or of any person or entity to receive any such notice, or any defect in any notice of redemption, shall not affect the validity of the proceeding for the redemption of such Bonds.

Rescission of Redemption. The County may rescind any optional or extraordinary redemption by written notice to the Fiscal Agent on or prior to the date fixed for redemption. Any notice of redemption shall be cancelled and annulled if for any reason inadequate funds are on deposit in the Redemption Fund 5 days prior to the redemption date, and such cancellation shall not constitute an Event of Default. The Fiscal Agent shall mail notice of rescission of redemption in the same manner notice of redemption was originally provided.

Partial Redemption. Upon surrender of Bonds redeemed in part only, the County shall execute and the Fiscal Agent shall authenticate and deliver to the registered Owner, at the expense of the County, a new Bond or Bonds, of the same series and maturity, of authorized denominations in aggregate principal amount equal to the unredeemed portion of the Bond or Bonds.

Effect of Redemption. From and after the date fixed for redemption, if funds available for the payment of the principal of, and interest and any premium on, the Bonds or portion of Bonds so called for redemption have been deposited in the Redemption Fund on the date fixed for redemption, then such Bonds or portion of Bonds so called for redemption shall be defeased and shall cease to be entitled to any benefit under the Fiscal Agent Agreement other than the right to receive payment of the redemption price, and no interest shall accrue thereon on or after the redemption date specified in such notice.

8

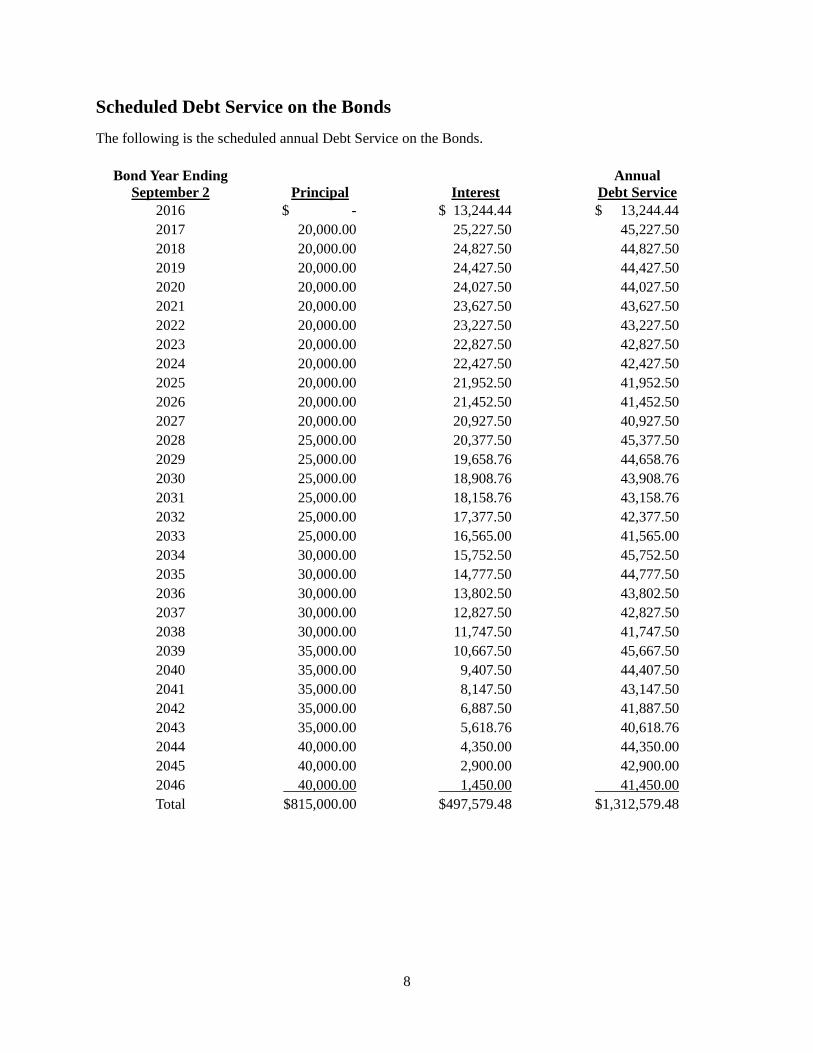

Scheduled Debt Service on the Bonds

The following is the scheduled annual Debt Service on the Bonds.

Bond Year Ending September 2 Principal Interest

Annual Debt Service

2016 $ - $ 13,244.44 $ 13,244.44 2017 20,000.00 25,227.50 45,227.502018 20,000.00 24,827.50 44,827.502019 20,000.00 24,427.50 44,427.502020 20,000.00 24,027.50 44,027.502021 20,000.00 23,627.50 43,627.502022 20,000.00 23,227.50 43,227.502023 20,000.00 22,827.50 42,827.502024 20,000.00 22,427.50 42,427.502025 20,000.00 21,952.50 41,952.502026 20,000.00 21,452.50 41,452.502027 20,000.00 20,927.50 40,927.502028 25,000.00 20,377.50 45,377.502029 25,000.00 19,658.76 44,658.762030 25,000.00 18,908.76 43,908.762031 25,000.00 18,158.76 43,158.762032 25,000.00 17,377.50 42,377.502033 25,000.00 16,565.00 41,565.002034 30,000.00 15,752.50 45,752.502035 30,000.00 14,777.50 44,777.502036 30,000.00 13,802.50 43,802.502037 30,000.00 12,827.50 42,827.502038 30,000.00 11,747.50 41,747.502039 35,000.00 10,667.50 45,667.502040 35,000.00 9,407.50 44,407.502041 35,000.00 8,147.50 43,147.502042 35,000.00 6,887.50 41,887.502043 35,000.00 5,618.76 40,618.762044 40,000.00 4,350.00 44,350.002045 40,000.00 2,900.00 42,900.002046 40,000.00 1,450.00 41,450.00 Total $815,000.00 $497,579.48 $1,312,579.48

DISTRICT LOCATION

COUNTY OF SANTA CRUZ

DISTRICT LOCATION

MONTEREY BAY

LOCATION MAP 9

SANTA CLARA COUNTY

MONTEREY COUNTY

ASSESSMENT DIAGRAM

10

11

THE DISTRICT The information set forth herein regarding ownership of real property in the District and the property owners within the District was obtained through the County and others and has not been independently verified. Neither the County, the Municipal Advisor nor the Underwriter make any representation as to the accuracy or completeness of any such information. This information has been included because it is considered relevant to an informed evaluation of the District. The information should not be construed to suggest that the Bonds or the Assessments that are pledged to pay debt service on the Bonds are personal obligations of the property owners within the District. The owners of property within the District will not be personally liable for payments of the Assessments.

General

The District encompasses approximately 7 net acres in an unincorporated area of the County known as Graham Hill. The District is located 2 ½ miles north of the City of Santa Cruz. At the time of formation, the District contained 27 taxable parcels, 26 of which are developed with single family homes. The assessment on 4 parcels has been prepaid in full. Accordingly, the Bonds will be secured only by the 23 Assessment Parcels (one of which is vacant property) for which the Assessments have not been prepaid.

Assessed Values

For all Assessment Parcels, the County-determined assessed valuation is provided as an estimate for purposes of valuation. The County assessed valuation is derived from the Fiscal Year 2015/16 County Assessor’s assessed valuation of land and improvements. A complete list of Assessment Parcels, Fiscal Year 2015/16 assessed values and Assessment liens is shown below under the caption “Assessment Parcels.” The County’s assessed valuation of land and improvements is based on the base year assessed value (which may or may not be reflective of the fair market value of the land and improvements) increased by a maximum of 2% per year each year thereafter, as allowed under Article XIIIA of the Constitution of the State of California. Values may also be decreased if inflation is negative (for example, the inflation factor for Fiscal Year 2010/11 was -0.237%). Therefore, the assessor’s value typically does not accurately reflect the fair market value of the land and improvements which may be higher or lower than the Assessor’s value. Further, due to timing, the Assessor’s value may not reflect the most recent sale price of a parcel or new construction on a parcel. See “RISK FACTORS - Valuation of Property in the District” herein. The fair market value can only be established through the sale of the property or an M.A.I. appraisal of the property within the District. The County has not undertaken to obtain an M.A.I.appraisal of the property within the District.

Proposition 8 Reductions. Proposition 8 provides for the assessment of real property at the lesser of its originally determined (base year) full cash value compounded annually by the inflation factor, or its full cash value as of the lien date, taking into account reductions in value due to damage, destruction, obsolescence or other factors causing a decline in market value. Reductions based on Proposition 8 do not establish new base year values, and the property may be reassessed as of the following lien date up to the lower of the then-current fair market value or the factored base year value.

While the assessed value may be reduced by the County Assessor as a result of Proposition 8, the assessed value has no bearing on the calculation of the Assessments, only on the calculation of ad valorem taxes.

Investors must recognize the uncertainties with respect to the assessed values of the Assessment Parcels, since the Bonds are secured by the Assessment Parcels. See “RISK FACTORS” herein.

12

Assessed Value Appeals. Further, property owners in the District may appeal the County Assessor’s value, and if successful, such appeals may result in a lowering of assessed values in future years. While the assessed value may be reduced by the County Assessor if an appeal is successful, the assessed value has no bearing on the calculation of the Assessments, only on the calculation of ad valorem taxes.

The County has not determined if any assessment appeals are pending for property in the District.

13

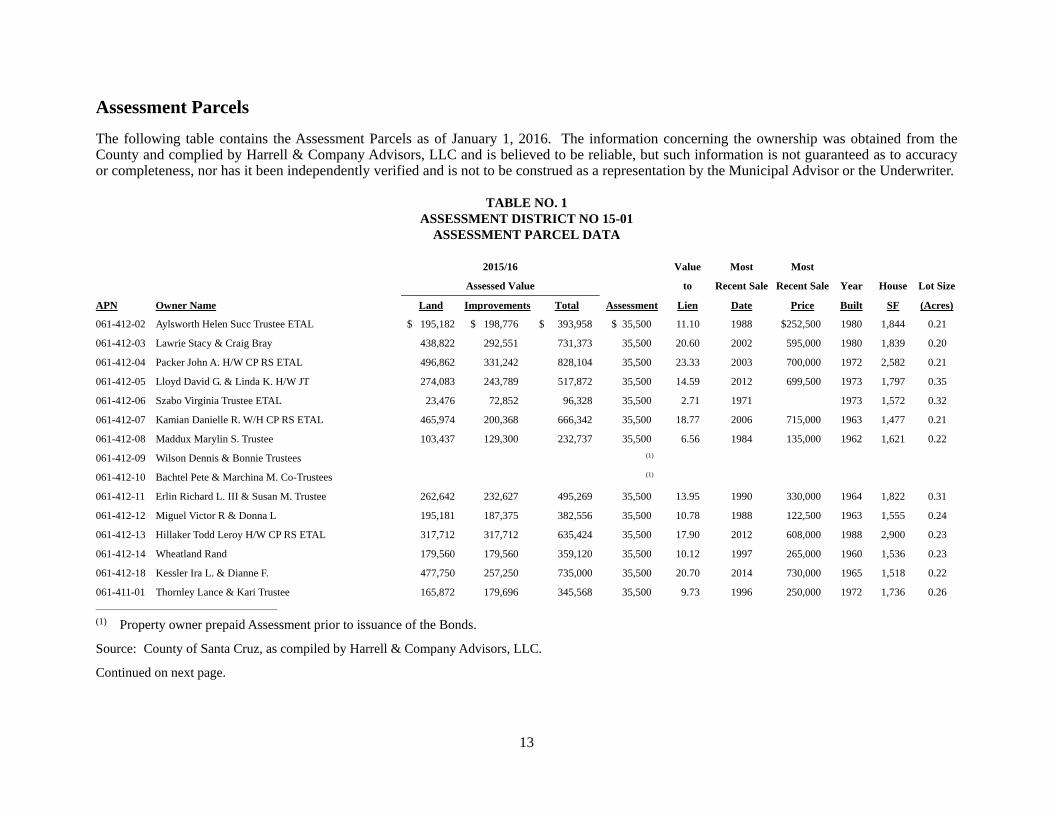

Assessment Parcels

The following table contains the Assessment Parcels as of January 1, 2016. The information concerning the ownership was obtained from the County and complied by Harrell & Company Advisors, LLC and is believed to be reliable, but such information is not guaranteed as to accuracy or completeness, nor has it been independently verified and is not to be construed as a representation by the Municipal Advisor or the Underwriter.

TABLE NO. 1 ASSESSMENT DISTRICT NO 15-01

ASSESSMENT PARCEL DATA

2015/16 Value Most Most

Assessed Value to Recent Sale Recent Sale Year House Lot Size

APN Owner Name Land Improvements Total Assessment Lien Date Price Built SF (Acres)

061-412-02 Aylsworth Helen Succ Trustee ETAL $ 195,182 $ 198,776 $ 393,958 $ 35,500 11.10 1988 $252,500 1980 1,844 0.21

061-412-03 Lawrie Stacy & Craig Bray 438,822 292,551 731,373 35,500 20.60 2002 595,000 1980 1,839 0.20

061-412-04 Packer John A. H/W CP RS ETAL 496,862 331,242 828,104 35,500 23.33 2003 700,000 1972 2,582 0.21

061-412-05 Lloyd David G. & Linda K. H/W JT 274,083 243,789 517,872 35,500 14.59 2012 699,500 1973 1,797 0.35

061-412-06 Szabo Virginia Trustee ETAL 23,476 72,852 96,328 35,500 2.71 1971 1973 1,572 0.32

061-412-07 Kamian Danielle R. W/H CP RS ETAL 465,974 200,368 666,342 35,500 18.77 2006 715,000 1963 1,477 0.21

061-412-08 Maddux Marylin S. Trustee 103,437 129,300 232,737 35,500 6.56 1984 135,000 1962 1,621 0.22

061-412-09 Wilson Dennis & Bonnie Trustees (1)

061-412-10 Bachtel Pete & Marchina M. Co-Trustees (1)

061-412-11 Erlin Richard L. III & Susan M. Trustee 262,642 232,627 495,269 35,500 13.95 1990 330,000 1964 1,822 0.31

061-412-12 Miguel Victor R & Donna L 195,181 187,375 382,556 35,500 10.78 1988 122,500 1963 1,555 0.24

061-412-13 Hillaker Todd Leroy H/W CP RS ETAL 317,712 317,712 635,424 35,500 17.90 2012 608,000 1988 2,900 0.23

061-412-14 Wheatland Rand 179,560 179,560 359,120 35,500 10.12 1997 265,000 1960 1,536 0.23

061-412-18 Kessler Ira L. & Dianne F. 477,750 257,250 735,000 35,500 20.70 2014 730,000 1965 1,518 0.22

061-411-01 Thornley Lance & Kari Trustee 165,872 179,696 345,568 35,500 9.73 1996 250,000 1972 1,736 0.26 __________________________________________

(1) Property owner prepaid Assessment prior to issuance of the Bonds.

Source: County of Santa Cruz, as compiled by Harrell & Company Advisors, LLC.

Continued on next page.

14

TABLE NO. 1 ASSESSMENT DISTRICT NO 15-01

ASSESSMENT PARCEL DATA

Continued from prior page.

2015/16 Value Most Most

Assessed Value to Recent Sale Recent Sale Year House Lot Size

APN Owner Name Land Improvements Total Assessment Lien Date Price Built SF (Acres)

061-411-02 Wadsworth William Howard & & Julie Callahan Trustee 441,965 294,645 736,610 35,500 20.75 2010 691,000 1962 1,708 0.23

061-411-03 Rosso Matthew & Sue 210,799 191,277 402,076 35,500 11.33 1989 257,500 1972 1,709 0.23

061-411-04 Fontana Richard Trustee ETAL (1)

061-411-05 Johnston Charles & Madeleine Larronde H/W JT 459,222 302,166 761,388 35,500 21.45 2005 829,000 1966 2,270 0.23

061-411-06 Loiler Brian R. & Shannon Y. H/W JT 522,551 348,368 870,919 35,500 24.53 2012 850,000 1965 2,616 0.41

061-411-07 Masik Donald J. & Nancy M. H/W JT 107,704 248,552 356,256 35,500 10.04 1985 215,000 1965 2,948 0.36

061-411-08 Castellanos Eric Raymond S/M AS JT ETAL 418,652 279,100 697,752 35,500 19.65 2002 579,000 1963 1,946 0.26

061-411-09 Bombardieri Michael J.& Caroline J. 205,067 146,553 351,620 35,500 9.90 1993 249,000 1960 1,724 0.26

061-411-10 Finch Evelyn B. ETAL ALL JT 9,303 - 9,303 35,500 0.26 1974 0.26

060-011-14 Meyer Jonathan J. Trustee (1)

060-011-12 Brody David G. & Megan A. 443,691 295,794 739,485 35,500 20.83 2013 725,000 1960 1,263 0.25

060-011-18 Zing Angela L. M/W SS 371,319 247,546 618,865 35,500 17.43 2012 604,000 2006 2,134 0.25

$6,786,826 $5,177,099 $11,963,925 $816,500 14.65 5.95 __________________________________________

(1) Property owner prepaid Assessment prior to issuance of the Bonds.

Source: County of Santa Cruz, as compiled by Harrell & Company Advisors, LLC.

15

Assessed Value to Assessment Lien Ratios

Assessed valuation to assessment lien ratios are derived by dividing the 2015/16 Fiscal Year County assessor’s assessed valuation amount of land plus improvements, if any, by the unpaid assessments. For example, a 3:1 ratio means that the assessed value is three times the total assessment lien amount.

According to the County Assessor’s Office, the aggregate assessed valuation of land and improvements of the 23 Assessment Parcels with unpaid assessments is $11,963,925 for Fiscal Year 2015/16. The total lien on the Assessment Parcels is $816,500. The aggregate value-to-lien ratio is 14.7:1 (see “Assessment Parcels” herein). Ratios on individual Assessment Parcels range from 0.26:1 for the 0.26-acre vacant lot to 24.5:1 for a 2,600 square foot single family home on a 0.41-acre lot purchased in 2012. The aggregate value-to-lien ratio including all current overlapping tax and assessment debt of $948,835 is 12.6:1 (see “Direct and Overlapping Debt” below).

Eleven of the parcels were purchased more than 25 years ago, and assessed values may not be representative of market values. Potential purchasers of the Bonds should be aware that if an Assessment Parcel bears an Assessment in excess of its market value, then there may be little incentive for the owner of the Assessment Parcel to pay the assessment on such Assessment Parcel and little likelihood that such property would be purchased in a foreclosure sale. See “RISK FACTORS” describing risks relating to market values of Assessment Parcels.

Table No. 2 categorizes the assessed value to lien ratios for the Assessment Parcels within the District, but excluding any other overlapping debt (see “Effective Tax Rates” and “Direct and Overlapping Debt” below). One parcel is vacant land, and represents 4.3% of the Assessment lien. Table No. 2 categorizes the assessed value to lien ratios for the Assessment Parcels.

TABLE NO. 2 ASSESSMENT DISTRICT NO. 15-01

SUMMARY LIEN TO ASSESSED VALUE RATIO (VALUES AS OF JANUARY 1, 2015)

Assessed No. of % of Value-to Lien Parcels (1) Assessment (1) Total 10:1 and above 18 $639,000 78.3%

5:1 - 9.99:1 3 106,500 13.0%2.71:1 1 35,500 4.3%

0.26:1 (2) 1 35,500 4.3% Total 23 $816,500 100.0%

__________________________________________

(1) Excludes parcels on which Assessment has been prepaid.

(2) Vacant parcel.

Source: County of Santa Cruz.

No property owner in the District owns more than one Assessment Parcel. The property owners in the District will not be personally liable for payments of the Assessments to be applied to pay the principal of and interest on the Bonds. No assurance can be given that any property owner will continue to hold an interest in the Assessment Parcels.

16

Delinquencies

The County intends to include the Assessments which secure the Bonds in the “Teeter Plan,” which is the County’s Alternative Method of Distribution of Tax Levies and Collections and of Tax Sale Proceeds, as provided for in Section 4701 et seq. of the California Revenue and Taxation Code. However, the County reserves the option at any time to discontinue the Teeter Plan as it relates to the Assessments, in which case collections of the Assessments will reflect actual delinquencies. See “RISK FACTORS - Foreclosure and Sale Proceedings” for a further discussion with respect to delinquent assessment payments.

A history of the County-wide delinquency rate in the payment of ordinary ad valorem property taxes is as follows:

Fiscal Year % Delinquent 2006/07 3.47%2007/08 5.15%2008/09 5.61%2009/10 5.29%2010/11 3.98%2011/12 3.90%2012/13 3.64%2013/14 2.90%2014/15 2.72%

All property owners in the District have paid the first installment of property taxes payable for 2015/16, which was due by December 10, 2015. Prior years’ property taxes for all parcels are also current, with the exception of $175 due with respect to parcel number 061-411-06 for 2012/13 supplemental taxes.

The property owners in the District are not personally liable for payments of the Assessments to be applied to pay the principal of and interest on the Bonds. No assurance can be given that any property owner will continue to hold an interest in the Assessment Parcels. See “RISK FACTORS - Payment of the Assessment Not a Personal Obligation.”

Effective Tax Rates

Each home is currently subject to 2015/16 fixed assessments of $152.94 for mosquito abatement, parks and recreation, road repair, lighting and refuse collection. The homes are also subject to septic tank maintenance and management charges of $25.40, which will be eliminated when improvements are complete and the homes are connected to the sewer system. Finally, certain homes are subject to septic tank inspections fees in 2015/16, which will also be eliminated in future years as a result of the issuance of the Bonds.

17

Table No. 3 below sets forth Fiscal Year 2015/16 effective tax rates for representative single family residential homes in the District purchased at different points in time, assuming the elimination of the septic tank charges and including the estimated Assessment.

TABLE NO. 3 ASSESSMENT DISTRICT NO. 15-01

FISCAL YEAR 2015/16 EFFECTIVE TAX RATES

APN 061-411-03 060-011-12Year Purchased 1989 2013 2015/16 Assessed Value $402,076.00 $739,485.00 Homeowner’s Exemption (7,000.00) (7,000.00) Net Assessed Value for Ad Valorem Taxes 395,076.00 732,485.00 Ad Valorem Tax Rate (1) 1.111917% 1.111917% Ad Valorem Taxes 4,392.92 8,144.63

Special Assessments: Assessment District No. 15-01 Levy 2,206.00 2,206.00

Other Fixed Assessments (2) 152.94 152.94 Total $ 6,751.86 $ 10,503.57

Effective Tax Rate (based on Gross Assessed Value) 1.68% 1.42% __________________________________________

(1) Comprised of 1% general tax levy, plus debt service levies for Scotts Valley Unified School District(0.0.75224%) and Cabrillo Community College District (0.036693%) General Obligation Bonds.

(2) Includes County Service Area 9C Refuse Collection Charges of $56.92, billed on the tax bill for convenience.

Source: Municipal Advisor.

Direct and Overlapping Debt

Set forth below is the direct and overlapping debt report (the “Debt Report”) prepared by California Municipal Statistics, Inc., as of January 1, 2016. The Debt Report is included for general information purposes only.

The Debt Report generally includes long-term obligations sold in the public credit markets by public agencies whose boundaries overlap the boundaries of the District in whole or in part. Such long-term obligations are not payable from unpaid Assessments nor are they necessarily obligations secured by property within the District. In many cases, long-term obligations issued by a public agency are payable only from the general fund or other revenues of such public agency.

Presently, the Assessment Parcels are subject to $948,835 of direct and overlapping tax and assessment debt and overlapping lease obligation debt, including the outstanding amount of the Bonds. To repay the direct and overlapping tax and assessment debt and overlapping lease obligation debt, the property owners of the land within the District must pay the annual Assessments and the general property tax levy.

In addition, other public agencies whose boundaries overlap those of the District could, without the consent of the County, and in certain cases without the consent of the owners of the land within the District, impose additional taxes or assessment liens on the real property within the District in order to finance public improvements or services to be located or furnished inside of or outside of the District. The lien created on the real property within the District through the levy of such additional taxes or

18

Assessments may be on a parity with the lien of the Assessments. The imposition of additional liens on a parity with the Assessments may reduce the ability or willingness of the property owners to pay the Assessments and increases the possibility that foreclosure proceeds, if any, will not be adequate to pay delinquent Assessments.

TABLE NO. 4 COUNTY OF SANTA CRUZ

ASSESSMENT DISTRICT NO. 15-01 DIRECT AND OVERLAPPING DEBT

2015/16 Assessed Valuation: $11,963,925

DIRECT AND OVERLAPPING TAX AND ASSESSMENT DEBT: % Applicable Debt 1/1/16

Cabrillo Joint Community College District 0.031% $ 38,896

Scotts Valley Unified School District 0.330 93,439

Santa Cruz County Assessment District No. 15-01 100. 816,500 (1)

TOTAL DIRECT AND OVERLAPPING TAX AND ASSESSMENT DEBT $948,835

OVERLAPPING GENERAL FUND DEBT:

Santa Cruz County Certificates of Participation 0.031% $ 23,657

Santa Cruz County Office of Education Certificates of Participation 0.031 3,053

Cabrillo Joint Community College District Certificates of Participation 0.031 286

Scotts Valley Unified School District Certificates of Participation 0.330 11,317

TOTAL OVERLAPPING GENERAL FUND DEBT $ 38,313

COMBINED TOTAL DEBT $987,148 (2)

(1) Excludes issue to be sold.

(2) Excludes tax and revenue anticipation notes, enterprise revenue, mortgage revenue and non-bonded capital leaseobligations.

Ratios to 2015/16 Assessed Valuation:

Direct Debt ($816,500) .................................................................... 6.82%

Total Direct and Overlapping Tax and Assessment Debt .................... 7.93%

Combined Total Debt ......................................................................... 8.25%

__________________________________________

Source: California Municipal Statistics, Inc.

19

SOURCES OF PAYMENT FOR THE BONDS

Repayment of the Bonds

The Bonds are issued upon and are secured by a first lien on and security interest in all of the Assessments (including prepayment thereof), and any other amounts held in the Redemption Fund and the Reserve Fund created under the Fiscal Agent Agreement (including the Capitalized Interest Account and the Prepayment Account therein). Principal of and interest on the Bonds are payable exclusively out of the Redemption Fund. The Assessments and all moneys deposited into those funds are dedicated under the Fiscal Agent Agreement to the payment of the principal of, and interest and any premium on, the Bonds as provided therein and in the Act and the Bond Law until all of the Bonds have been paid and retired or until moneys or Federal Securities have been set aside irrevocably for that purpose in accordance with the Fiscal Agent Agreement.

Although the unpaid Assessments constitute fixed liens on the Assessment Parcels, they are not personal indebtedness of the owners of the Assessment Parcels. Furthermore, there can be no assurance as to the willingness or ability of the property owners to pay the unpaid Assessments.

Collection of Assessments. The unpaid Assessments levied annually on the Assessment Parcels will be collected, together with interest on the declining balances, on the tax roll of the County on which general taxes on real property are collected, and the unpaid Assessments are payable and become delinquent at the same time and in the same proportionate amounts and bear the same proportionate penalties and interest after delinquency as do general taxes, and the Assessment Parcels are subject to the same provisions for sale and redemption as are properties for nonpayment of general taxes. The annual Assessment installments together with interest are to be paid into the Redemption Fund which will be used to pay the principal of and interest on the Bonds as they become due.

Limited Obligations. The obligations of the County under the Fiscal Agent Agreement and the Bonds are not general obligations of the County, but are special obligations, payable solely from the Assessments and other assets pledged therefor under the Fiscal Agent Agreement. Neither the faith and credit nor the taxing power of the County (except to the limited extent described herein), or the State of California, or any political subdivision thereof is pledged to the payment of the Bonds.

The Bonds are “Limited Obligation Improvement Bonds” and under Section 9603 of the Act, are payable solely from and secured solely by the Assessments and the amounts in the Redemption Fund and the Reserve Fund created under the Fiscal Agent Agreement. The County is not obligated to advance available surplus funds from its treasury to cure any deficiency in the Redemption Fund.

Teeter Plan. The County has adopted a Teeter Plan as provided for in Section 4701 et seq. of the California Revenue and Taxation Code, under which a tax distribution procedure is implemented and secured roll taxes are distributed to taxing agencies within the County on the basis of the tax levy, rather than on the basis of actual tax collections. The County intends to include the Assessments of the District in its Teeter program. However, the County reserves the option at any time to discontinue the Teeter Plan as it relates to the Assessments, in which case collections of the Assessments will reflect actual delinquencies.

Foreclosure Covenant. In the Fiscal Agent Agreement, the County will covenant with and for the benefit of the owners of the Bonds that it will order, and cause to be commenced, and thereafter diligently prosecute an action in the superior court to foreclose the lien of any Assessment or installment thereof which has been billed, but has not been paid, pursuant to and as provided in Sections 8830 and 8835, inclusive of the Bond Law and the conditions specified in the Fiscal Agent Agreement as further described below.

20

The County’s Auditor-Controller-Treasurer-Tax Collector will determine if any of the conditions described below exist and will notify the County Counsel of any such delinquencies. The County Counsel will commence, or cause to be commenced, such foreclosure proceedings, including collection actions preparatory to the filing of any complaint. The County Counsel is authorized to employ outside counsel to conduct any such foreclosure proceedings.

Within 60 days of either of the following determinations, which will be made not later than October 1 each year, the County will take the following actions:

(A) If the Auditor-Controller-Treasurer-Tax Collector determines that any single parcel is, or anyparcels under common ownership are, delinquent in the payment of two or more semi-annualinstallments of Assessment payments, the County shall cause the commencement of foreclosureagainst each such delinquent parcel.

(B) If the Auditor-Controller-Treasurer-Tax Collector determines that the total amount of delinquentAssessments for the prior Fiscal Year for the entire Assessment District exceeds 5% of the totalAssessments due and payable for the prior Fiscal Year, the County shall cause the commencementof foreclosure against each parcel of land within the District with any amount of delinquency forthe prior Fiscal Year.

However, notwithstanding the foregoing, the County may elect to defer foreclosure proceedings on any parcel if the County has received funds equal to the delinquent Assessments from any other source, and those funds are available to contribute toward the payment of the principal of (including Sinking Fund Payments) and interest on the Bonds when due (including without limitation funds from the sale of the receivables associated with delinquent Assessments).

So long as the Assessments are included in the County’s Teeter Plan (see “Repayment of the Bonds - Teeter Plan” above), the County may initiate foreclosure proceedings under their customary practice for delinquent property taxes (5 years) rather than by October 1 each year.

Upon the redemption or sale of the real property responsible for such delinquencies, the County will apply the net proceeds thereof as follows: (i) pay defaulted interest or principal on the Bonds, (ii) deposit to the Reserve Fund the amount of any delinquency advanced therefrom, (iii) reimburse the County for the amount of any previously unreimbursed fees, costs and expenses incurred by the County in connection with such delinquency, (iv) deposit to the Reserve Fund an amount sufficient to cause the amount therein to be equal to the Reserve Requirement, and (v) the balance, if any, will be disbursed as set forth in the judgment of foreclosure or as required by law.

Possibility of Foreclosure Delays. No assurances can be given that any real property subject to a judicial foreclosure sale will be sold or, if sold, that the proceeds of sale will be sufficient to pay any delinquent Assessment installment. If court foreclosure proceedings are necessary, there may be a delay in payments to the owner of the Bonds pending prosecution of the foreclosure proceedings and receipt by the County of the proceeds of the foreclosure sale. It is also possible that no bid for the purchase of the applicable property would be received at the foreclosure sale. See “RISK FACTORS - Foreclosure and Sale Proceedings.”

Priority of Lien. Each Assessment (and any Assessment thereof) and each installment thereof, and any interest and penalties on each Assessment, constitute a lien against the Assessment Parcel on which it was imposed until it is paid. The lien is subordinate to all fixed special assessment liens imposed upon the same property prior to the date that the Assessments became a lien on the property assessed, but has priority over all private liens and over all fixed special assessment liens which may thereafter be created against the property. The lien is co-equal to and independent of the lien for general taxes. The direct and overlapping debt of property within the District as of January 1, 2016 is shown under the heading “THE DISTRICT - Direct and Overlapping Debt.”

21

Sales of Tax-Defaulted Property Generally. If foreclosure is deemed necessary, property securing delinquent Assessment installments which is not sold pursuant to the judicial foreclosure proceedings described above may be sold, subject to redemption by the property owner, in the same manner and to the same extent as real property sold for nonpayment of general County property taxes. On or before June 30 of the year in which such delinquency occurs, the property becomes tax-defaulted. This initiates a five-year period during which the property owner may redeem the property. At the end of the five-year period the property becomes subject to sale by the County Auditor-Controller-Treasurer-Tax Collector. Except in certain circumstances, as provided in the Bond Law, the purchaser at any such sale takes such property subject to all unpaid assessments, interest and penalties, costs, fees and other charges which are not satisfied by application of the sales proceeds and subject to all public improvement assessments which may have priority.

Delinquency Resulting in Ultimate or Temporary Loss on Bonds. If amounts in the Redemption Fund are temporarily insufficient to pay Bonds that have matured or past due interest, or the principal and interest on Bonds coming due during the current tax year, but it does not appear to the Auditor-Controller-Treasurer-Tax Collector that there will be an ultimate loss to the owner of the Bonds, the Auditor-Controller-Treasurer-Tax Collector will, pursuant to the Bond Law, pay the principal of Bonds which have matured as presented and make interest payments on the Bonds when due as long as there are available funds in the Redemption Fund, in the following order of priority: All matured interest payments will be made before the principal of any other Bond is paid.

When funds become available for the payment of any Bond which was not paid upon presentment, the Auditor-Controller-Treasurer-Tax Collector will notify the registered owner of such Bond by registered mail to present the Bond for payment. If the Bond is not presented for payment within ten days after the mailing of the notice, interest will cease to accrue on the Bond.

If it appears to the Auditor-Controller-Treasurer-Tax Collector that there is a danger of an ultimate loss accruing to the Bond Owner for any reason, he or she is required pursuant to the Act to withhold payment on all matured Bonds and interest on all Bonds and report the facts to the Board of Supervisors so that the Board of Supervisors may take proper action to equitably protect the Bond Owner.

Upon the receipt of such notification from the Auditor-Controller-Treasurer-Tax Collector, the Board of Supervisors is required to fix a date for a hearing upon such notice. At the hearing the Board of Supervisors will determine whether in its judgment there will ultimately be insufficient money in the Redemption Fund to pay the principal of the unpaid Bonds and interest thereon.

If the Board of Supervisors determines that in its judgment there will ultimately be a shortage in the Redemption Fund to pay the principal of the unpaid Bonds and interest thereon (an “Ultimate Default”), the Board of Supervisors will direct the Auditor-Controller-Treasurer-Tax Collector to pay to the owner of all outstanding and unpaid Bonds such proportion thereof as the amount of funds on hand in the Redemption Fund bears to the total amount of the unpaid principal of the Bonds and interest which has accrued or will accrue thereon. Similar proportionate payments will thereafter be made periodically as moneys come into the Redemption Fund.

Upon the determination by the Board of Supervisors that an Ultimate Default will occur, the Auditor-Controller-Treasurer-Tax Collector will notify the Bond Owner to surrender its Bonds to the Auditor-Controller-Treasurer-Tax Collector for cancellation. Upon cancellation of the Bonds, the Bond Owner will be credited with the principal amount of the Bond so canceled. The Auditor-Controller-Treasurer-Tax Collector will then pay by warrant the proportionate amount of principal and accrued interest due on the Bonds of the Bond Owner as may be available from time to time out of the money in the Redemption Fund. Interest will cease to accrue on principal payments made from the date of such payment, but interest will continue to accrue on the unpaid principal at the rate specified on the Bonds until payment thereof is made. No premiums will be paid on payments of principal on Bonds made in advance of the maturity date thereon.

22

If Bonds are not surrendered for registration and payment, the Auditor-Controller-Treasurer-Tax Collector will give notice to the Bond Owner by registered mail, at the Bond Owner’s last address as shown on the registration books maintained by the Registrar, of the amount available for payment. Interest on such amount will cease to accrue as of ten days after the date of mailing of such notice.

If the Board of Supervisors determines that in its judgment there will not be an Ultimate Default, it will direct the Auditor-Controller-Treasurer-Tax Collector to pay matured Bonds and interest as long as there is available money in the Redemption Fund.

Reserve Fund

The Fiscal Agent will establish the Reserve Fund on the closing date with a portion of the proceeds of the Bonds equal to the “Reserve Requirement,” which is defined as Maximum Annual Debt Service (as defined in the Fiscal Agent Agreement). The Reserve Requirement as of the Closing Date is $45,752.50. See “THE FINANCING PLAN - Estimated Uses of Funds” and “APPENDIX B - SUMMARY OF THE FISCAL AGENT AGREEMENT.”

The County will cause the Reserve Fund to be administered in accordance with Part 16 of the Act; provided, however, that proceeds from redemption or sale of properties, if and to the extent that payment of delinquent Assessments and interest thereon was made from the Reserve Fund, will be credited to the Reserve Fund.

If amounts in the Redemption Fund are insufficient to pay the principal, if any, of and interest on the Bonds, at any time, the Fiscal Agent will withdraw from the Reserve Fund, to the extent of any funds therein, the amount of such insufficiency, and will transfer any amounts so withdrawn to the Redemption Fund.

For a further description of disbursements from the Reserve Fund, see “APPENDIX B - SUMMARY OF THE FISCAL AGENT AGREEMENT - Reserve Fund.”

23

RISK FACTORS

General

BEFORE PURCHASING ANY OF THE BONDS, ALL PROSPECTIVE INVESTORS AND THEIR PROFESSIONAL ADVISORS SHOULD CAREFULLY CONSIDER, AMONG OTHER THINGS, THE FOLLOWING RISK FACTORS, WHICH ARE NOT MEANT TO BE AN EXHAUSTIVE LISTING OF ALL RISKS ASSOCIATED WITH THE PURCHASE OF THE BONDS. MOREOVER, THE ORDER OF PRESENTATION OF THE RISK FACTORS DOES NOT NECESSARILY REFLECT THE ORDER OF THEIR IMPORTANCE.

The purchase of the Bonds involves investment risk. If a risk factor materializes to a sufficient degree, it could delay or prevent payment of principal of and/or interest on the Bonds. Such risk factors include, but are not limited to, the following matters.

Debt service on the Bonds is payable from installment payments of principal and interest on unpaid Assessments on the Assessment Parcels. The principal of the Assessments is the aggregate of the amounts of the individual Assessments levied against the Assessment Parcels. The individual Assessment on a parcel will be paid in annual installments, together with interest on the unpaid balance, unless the unpaid balance is subsequently prepaid. The annual installments of principal and interest with respect to an Assessment Parcel will be collected on the County tax roll at the same time and in the same manner as general real property taxes are collected. The annual installments of principal and interest with the respect to all Assessment Parcels were, at the time of initial levy of the Assessments, equal in the aggregate to the annual debt service on the Bonds.

Payment of the Assessment Not a Personal Obligation

The owners of Assessment Parcels are not personally liable for the payment of the Assessment or the Assessment installments. Rather, an assessment is a lien only on an Assessment Parcel. Accordingly, if the value of an Assessment Parcel is not sufficient to fully secure the assessment on it, the County has no recourse against the owner.

No County Obligation to Pay Debt Service

IF ASSESSMENT INSTALLMENT COLLECTIONS ARE INSUFFICIENT, THE ONLY AMOUNTS AVAILABLE TO PAY DEBT SERVICE ON THE BONDS WILL BE THE AMOUNT ON DEPOSIT FROM TIME TO TIME IN THE RESERVE FUND, AND IF SO ADVANCED WILL REDUCE THE RESERVE FUND BY THE AMOUNT OF THE FUNDS ADVANCED.

OWNERS OF BONDS MAY NOT RELY UPON THE COUNTY TO ADVANCE FUNDS TO PAY DEBT SERVICE ON THE BONDS FOLLOWING DEPLETION OF THE RESERVE FUND EVEN IF THE COUNTY MAY HAVE PREVIOUSLY DONE SO OR MAY DO SO CONTEMPORANEOUSLY WITH RESPECT TO OTHER BONDS OR OBLIGATIONS.

Risks of Real Estate Secured Investments Generally

The Bond Owners will be subject to the risks generally incident to an investment secured by real estate, including, without limitation, (i) adverse changes in local market conditions (including as a result of an economic downturn similar to that experienced in 2007 to about 2011), such as changes in the market value of real property in the vicinity of the District, the supply of or demand for competitive properties in such area, and the market value of residential property in the event of sale or foreclosure; (ii) changes in real estate tax rate and other operating expenses, governmental rules (including, without limitation, laws

24

relating to hazardous materials) and fiscal policies; and (iii) natural disasters (including, without limitation, earthquakes, fires and floods), which may result in uninsured losses.

No assurance can be given that the individual homeowners will pay the Assessments in the future or that they will be able to pay such Assessments on a timely basis. See “Bankruptcy” below, for a discussion of certain limitations on the County’s ability to pursue judicial proceedings with respect to delinquent parcels

Risks Related to Declines in Home Values

Homes within the District were likely affected by the decline in market value along with the rest of the State during the recent economic crisis. Future declines in home values could result in property owner unwillingness or inability to pay mortgage payments, as well as ad valorem property taxes and Assessments, when due. Under such circumstances, bankruptcies could occur. Bankruptcy by homeowners with delinquent Assessments would delay the commencement and completion of foreclosure proceedings to collect delinquent Assessments. See “Bankruptcy.”

Valuation of Property in the District

The value of the land within the District is a critical factor in determining the investment quality of the Bonds. If there is a default in the payment of the Assessments, the County’s only remedy is to commence foreclosure proceedings on the delinquent property in an attempt to obtain funds to pay the delinquent Assessment. Further, reductions in assessed value indicating a decline in market value (as described below) may affect the willingness or ability of taxpayers to pay their Assessments prior to delinquency.

Assessed Value. The County has relied on the assessed valuations of the 2015/16 County Assessor’s rolls for the valuations for all of the property within the District presented in this Official Statement.

Article XIIIA. Pursuant to the California voter initiative process, on June 6, 1978, California voters approved Proposition 13 which added Article XIIIA to the California Constitution. This amendment imposed certain limitations on taxes that may be levied against real property to 1% of the full cash value of the property, adjusted annually for inflation at a rate not exceeding 2% annually. Full cash value is determined as of the 1975/76 assessment year, upon change in ownership (acquisition) or when newly constructed. Article XIIIA has subsequently been amended to permit reduction of the “full cash value” base in the event of declining property values caused by substantial damage, destruction or other factors, and to provide that there would be no increase in the “full cash value” base in the event of reconstruction of property damaged or destroyed in a disaster and in other special circumstances.

Reduction in Inflationary Rate. The annual inflationary adjustment, while limited to 2%, is determined annually and may not exceed the percentage change in the California Consumer Price Index (CCPI).

Because the Revenue and Taxation Code does not distinguish between positive and negative changes in the CCPI used for purposes of the inflation factor, there was a decrease of 0.237% in 2009/10 – applied to the 2010/11 tax roll – reflecting the actual change in the CCPI, as reported by the State Department of Finance. For each fiscal year since Article XIIIA has become effective (the 1978/79 fiscal year), the annual increase for inflation has been at least 2% except in nine fiscal years (including for the upcoming Fiscal Year 2015/16) as shown below:

25

Tax Roll Percentage 1981/82 1.000%1995/96 1.1901996/97 1.1101998/99 1.8532004/05 1.8672010/11 (0.237)2011/12 0.7532014/15 0.4542015/16 1.998

Proposition 8 Adjustments. Proposition 8, approved in 1978, provides for the assessment of real property at the lesser of its originally determined (base year) full cash value compounded annually by the inflation factor, or its full cash value as of the lien date, taking into account reductions in value due to damage, destruction, obsolescence or other factors causing a decline in market value. Reductions based on Proposition 8 do not establish new base year values, and the property may be reassessed as of the following lien date up to the lower of the then-current fair market value or the factored base year value. While the assessed value may be reduced by the County Assessor as a result of Proposition 8, the assessed value has no bearing on the calculation of the Assessments, only on the calculation of ad valorem taxes.

The County cannot guarantee that reductions in assessed value will not occur in future years.