Embed Size (px)

Citation preview

80%

70%

60%

50%

40%

30%

20%

10%

0%

-

10%

-

20%

1980’s

Under 14 15-24 25-34 35-44 45-54 55-64 65+Source: U.S. Census

Change in Population GrowthChange in Population Growth

4%

16%

47%

11%

-3%

22%

-13%

80%

70%

60%

50%

40%

30%

20%

10%

0%

-

10%

-

20%

1990’s

Source: U.S. Census

Under 14 15-24 25-34 35-44 45-54 55-64 65+

Change in Population GrowthChange in Population Growth

12%

7%

-8%

20%

49%

12%15%

80%

70%

60%

50%

40%

30%

20%

10%

0%

-

10%

-

20%

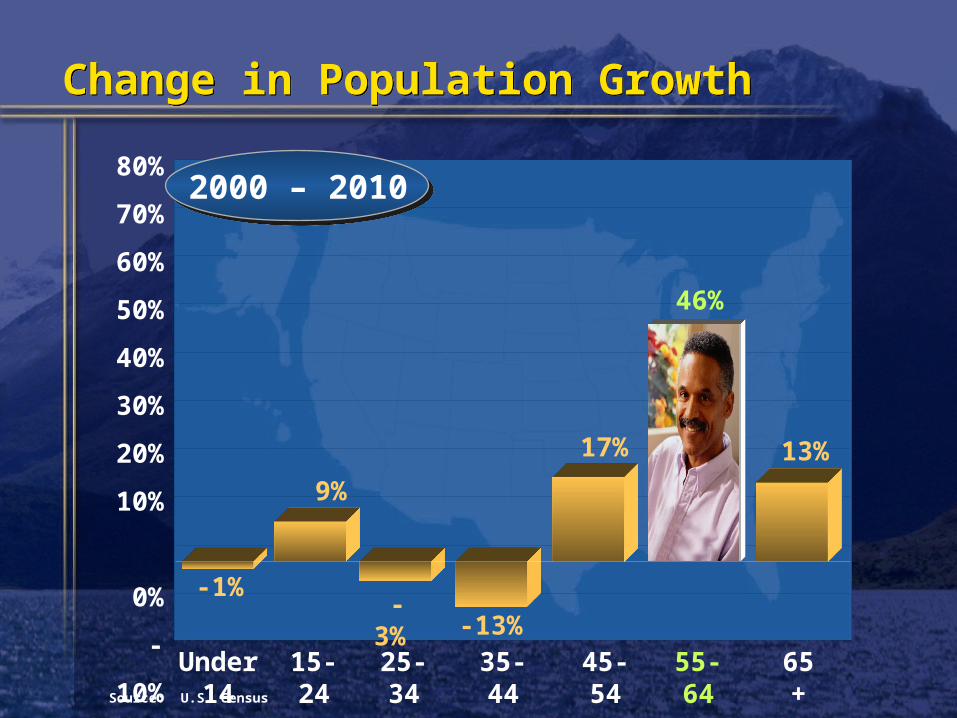

2000 – 2010

Source: U.S. Census

Under 14 15-24 25-34 35-44 45-54 55-64 65+

Change in Population GrowthChange in Population Growth

-1% -3%

-13%

17% 13%

46%

9%

80%

70%

60%

50%

40%

30%

20%

10%

0%

-

10%

-

20%

2010 – 2020

Source: U.S. Census

Under 14 15-24 25-34 35-44 45-54 55-64 65+

Change in Population GrowthChange in Population Growth

7% 7%

-10%

3% 8%

73%

54%

Where is The Rollover Money Coming From?Where is The Rollover Money Coming From?

$2.2 Trillion$2.2 TrillionCurrent total U.S. IRA assetsCurrent total U.S. IRA assets

Amount of assetsby 2007

The IRA Opportunity is HugeThe IRA Opportunity is Huge

What is an Automated 401(k) Program?What is an Automated 401(k) Program?

• Automatic Enrollment• Automatic Enrollment

• Automatic Increase• Automatic Increase

• Default Investment• Default Investment

The Shift to Automated 401(k)sThe Shift to Automated 401(k)s

• Employees are not saving enough for retirement

• Employees are not saving enough for retirement

The Shift to Automated 401(k)sThe Shift to Automated 401(k)s

*AARP, 2007

out of employees do not participate in their company’s 401(k) programs*

out of employees do not participate in their company’s 401(k) programs*

33 1010

• Employees are not saving enough for retirement

• Employees are not saving enough for retirement

The Media is Driving ExpectationsThe Media is Driving Expectations

GOLDEN RULE FOR THE GOLDEN YEARS: GET A PLANGOLDEN RULE FOR THE GOLDEN YEARS: GET A PLANInvestmentNews Daily, November 26, 2007InvestmentNews Daily, November 26, 2007

Aging US Boomer Population May Find Financial Stress in RetirementAging US Boomer Population May Find Financial Stress in Retirement

MatureMarket News, April 11, 2007MatureMarket News, April 11, 2007

InvestmentNews Daily, January 7, 2008InvestmentNews Daily, January 7, 2008

The Media is Driving ExpectationsThe Media is Driving Expectations

A Way to Convert Savings to Retirement IncomeA Way to Convert Savings to Retirement IncomeThe Wall Street Journal, April 23, 2006The Wall Street Journal, April 23, 2006

IBM TO PROVIDE FINANCIAL ADVICE FOR WORKERSIBM TO PROVIDE FINANCIAL ADVICE FOR WORKERSThe Wall Street Journal, August 8, 2007The Wall Street Journal, August 8, 2007

To Save Beyond 401(k)s, Understand Your BudgetTo Save Beyond 401(k)s, Understand Your BudgetThe Wall Street Journal, March 6, 2007The Wall Street Journal, March 6, 2007

Financial Advisor team and RPM present onsite to Dealer

Relationship Management supports all aspects of the plan

Client Market Center Sales Process

Client Dealer contacts Retirement Group via 1-800 line

Retirement Group generates Proposal and sends to Retirement Plan Manager

RPM works with Financial Advisor team to schedule meeting with Dealer

Quarterly Statements

®

Participant Statement

![[Free- ]_saint-saens-camille-dance-macabre-5455.pdf](https://img.pdfslide.us/doc/110x75/55cf883e55034664618ed70e/free-scorescomsaint-saens-camille-dance-macabre-5455pdf.jpg)