Embed Size (px)

Citation preview

8. Treasury Core Functions

Marco Cangiano

Rome, February 6-8, 2017

Outline

• Theroleofthetreasury

• Budgetexecutionandexpenditurecontrol

• Cashmanagementandlinktodebtmanagement

• TheTreasurySingleAccount

• Conclusions

<<CourseAcronym>>

Theroleandfunctionsofthetreasury

Treasury’sroleinthebudgetcycle

4Source:TheWorldBank,“PublicExpenditureManagementHandbook”,1998

Treasury’sDomain

Traditionalroleoftreasury

• Paymentprocessing- cashandcheques• Revenuecollectionandrecording• Maintainingpublicbankaccount(s)- theTreasurySingleAccountconcept

• Sometreasuriesperformedapre-auditfunction(andstilldoinsomecountries)- Thismayhavebeenassimpleasappropriationcontroloralsoinvolvedreviewofwhetherpaymentsrepresentedtheproperuseofpublicmoney

5

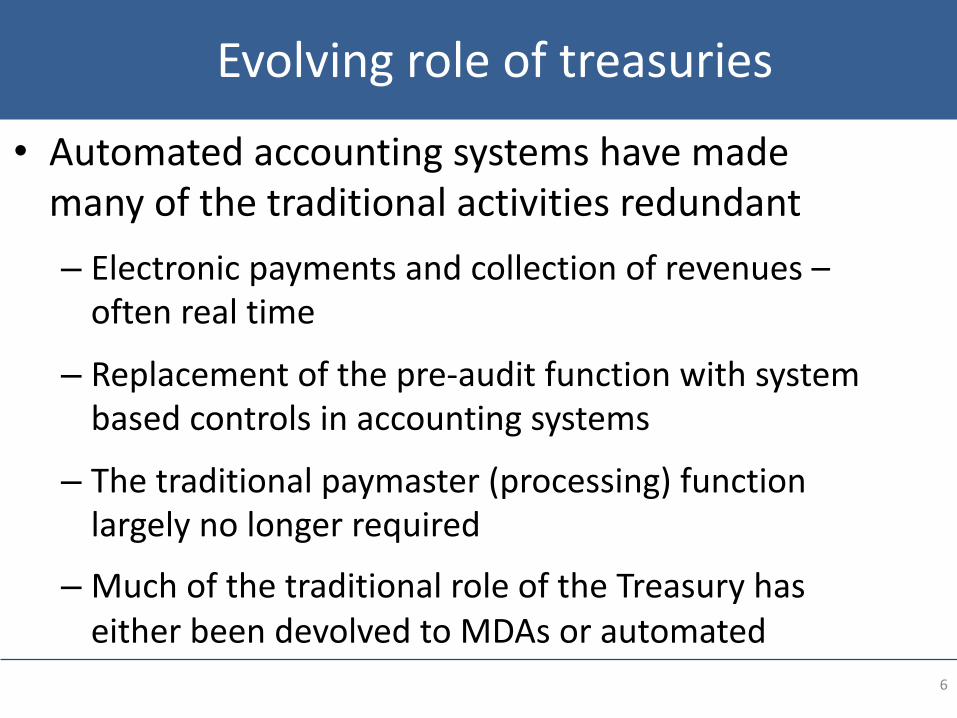

Evolvingroleoftreasuries

• Automatedaccountingsystemshavemademanyofthetraditionalactivitiesredundant– Electronicpaymentsandcollectionofrevenues–oftenrealtime

– Replacementofthepre-auditfunctionwithsystembasedcontrolsinaccountingsystems

– Thetraditionalpaymaster(processing)functionlargelynolongerrequired

– MuchofthetraditionalroleoftheTreasuryhaseitherbeendevolvedtoMDAsorautomated

6

Evolvingroleoftreasuries(2)

• ProvisionofamodernIFMISorcentralaccountingsystem- ThisbringswithittheneedforaneffectiveCoAsupplementedwithclearaccountingpolicies

• Shiftfrompassivetoactivecashmanagement• DecentralisedcontrolsisafeatureofmanymodernTreasury

systems• Anenhancedreportingandaccountingfunction• Greateremphasisoncompliancewithaccountingstandardsand

competentfiscalandstatisticalreporting

7

Coretreasuryfunctions• Processingofpayments• Accountingforgovernmenttransactionsandpreparingconsolidatedfiscalstatements

ofgeneralgovernment• Managinggovernmentpayroll• Applyinginternalcontrolregulations,bothontransactionsandcommitments• CashmanagementandoversightofTSA• Managingthegovernment’se-Treasurysystem

Andinsomecountries:

• Settingaccountingstandards• Undertakinginternalaudit• Conductingdebtmanagementoperations• Managementofexternalgrantsandcounterpartfunds;• Managingpublicprocurement• Monitoringgovernmentguaranteesandothercontingentliabilities• Monitoringoffinancialoperationsofextra-budgetaryfunds,SOEsandsub-national

governments.

8

TreasuryfunctionsPFMFunction Allocationto

MoF Treasury Agency Line Ministries

Macro-fiscal analysisandforecasting x

Budgetpreparation x x

Publicinvestmentplanningandmanagement

x x

Debtmanagementstrategy x x x

Taxpolicy x

RevenueandCustomsAdministration x x

Monitoring ofbudgetexecution x x x

Consolidatedfiscal reporting x x x

Cashforecasting andcashmanagement,TSA

x x

Riskmanagementandguarantees x x

Regulation ofbanksandfinancialinstitutions

x x9

TreasuryfunctionsPFMFunction Allocationto

MoF Treasury Agency Line Ministries

Oversightoffinancialmanagement,ITsystems

x x

Accountingstandardsandpolicies x x x

Paymentprocessing, internalcontrol,commitmentcontrol

x x x

Internalaudit x x x

Public procurementpolicy x x

Management ofpublicassets,liabilitiesandPPPs

x x

Oversight ofstate-ownedenterprises x

International financialrelations x

Inter-governmentalfiscalrelations x

Note:Theentriesinthistablerepresent therangeofpracticesacrossdevelopedandmiddle-incomecountries.Wheremultipleentriesareshowninarowthismayindicatethateither(i)practicesvaryamongcountries,or(ii)responsibilityforthefunctionissharedacrossdifferententities. 10

Treasurymodels• Twomainmodels:

– Centralized – alltreasuryfunctions,includingpaymentandcontrolfunctions,arecentralizedinthefinanceministry(heavilyinFrance,lesssoinSpain).

– Decentralized – operationalfunctions(typicallypaymentprocessingandcontrols)aredecentralizedtolineministriesbutcentralpolicyandoversightfunctionsarelocatedeitherinthefinanceministry(UK)oranarms’-lengthagency(Ireland,Scandinaviancountries).

• Withineachofthesebroadcategories,therearesubstantialvariationswithdifferingcontrolframeworksdependingon:– legalandadministrativeframework;– sizeofthecountryandthatofthegovernment;– degreeofcentralizationofgovernmentdecision-making;– reliabilityoffinancialdataandaccounting/reportingsystems;and– capacityatthecentervs.lineministries.

• Inpractice,thedistinctionbetween“centralized”and“decentralized”systemsisincreasinglygettingblurredwithmodernIT/TSAsystemswherecontrolsandpaymentfunctionsareautomated. 11

Alternativeorganizationalstructures

• Departments/directoratesofthefinanceministry(e.g.,Australia,France,UK)

• Aseparateministry(e.g.,Brazil,Indonesia,Turkey)• Anarms’-lengthagencyundertheMoF (e.g.,Ireland,Scandinaviancountries)

12

CentralizationandorganizationalCountry Centralized/DecentralizedModel Central

Organization

Centralized Decentralized Hybrid MoFDirect.

Agency

Bulgaria x x

Denmark x x

Estonia x x x

France x x

Finland x x

Hungary x x

Ireland x x

Netherlands x x

Poland x x

Serbia x x

Sweden x x

UnitedKingdom x x x13

Budgetexecutionandexpenditurecontrols

Objectivesofbudgetexecution1. Ensureseconomicandefficientimplementationofbudgetdecisions;

optimizetheuseofavailablebudgetresources

2. Promotesintegrityinmanagingpublicfunds– especiallylegality,financialresponsibility,transparencyandaccountability

3. preventunauthorizedspendingandpaymentarrears;(ii)improvebudgetcredibility;and(iii)promotefinancialintegrity.

4. Assistsintheidentificationofopportunitiesformoreeffectivebudgetinterventionsandimprovedrevenueandexpenditureperformance

5. Encouragesthedevelopmentofmodernandprofessionalfinancialmanagementskills,systemsandproceduresinthepublicsector

Tenstagesinbudgetexecution(1)•

ExpenditureAuthorization:Provideallrevenueandexpendituredepartmentswithappropriateauthoritytocommencebudgetaryoperations(“warrants”)accordingtoagreedspendinglimitsandplans

• Apportionment/allocationofauthorizationforspecificperiodsandspendingunits.Thepurposeofapportionmentistopreventspendingagenciesfromincurringobligationsataratewhichwouldrequiretheauthorizationofadditionalfundsforthefiscalyearinprogress.Thisauthoritytospendisreleasedtothespendingunitsthroughtheissueofwarrants/allotments/décretderépartition.

• Reservation.Oncetheapportionmentofexpenditureauthorizationismadeandthespendingauthorityhasbeenreleased,somecountries’PFMsystemsincludeastageatwhichfundsarereservedforaspecificknownexpensebutforwhichnocontracthasyetbeenissued.

• Commitment:Initiateexpendituredecisions,includingpurchasingandpaymentsoperationsandpayrolldisbursements

• Verification:Establishthatcorrectgoodsandserviceshavebeenreceivedandthattheyhavebeencorrectlyinvoiced

Authorization for Public Expenditure

Limit on amount of expenditure. Government’s expenditure must be within the amounts that the budget appropriations have established, with some flexibility allowed through virements and contingency reserve mechanisms. The nature of those expenditure limits depends on the accounting basis (cash, commitment, or accrual) used in the budget (see Section III). • Limit on time horizon of expenditure. The expenditure must occur within the time limits applicable to the expenditure authorization. Most countries adopt annual budgets authorizing spending for one year; however, some countries authorize multi-year limits for certain types of expenditure (e.g., autorisation d’engagement for multi-year investment projects in France—see Box 3). • Authorized purpose of the expenditure. The authority for expenditure is given for a specific predetermined purpose. The budget classification (which may be organized by programs, sub-programs, projects, economic categories, or line items) usually specifies the purpose for which the expenditure can be made.1 • Administrative unit accountable for expenditure. A unit of government, typically a line ministry, department or agency, is assigned the responsibility to ensure that the appropriated resources are spent as intended within the authorized limits.

10stagesinbudgetexecution(2)• PaymentAuthorization:Initiatepaymentprocessthroughissuanceofappropriate

paymentorder/instructions;Executepayments,includingmanagementofallassociatedtreasuryandbankingarrangementsanddocumentation

• Payment.Onceapaymentorderhasbeenissued,paymentsaremadethroughvariousinstru-ments includingchecks,electronicfundtransfer(EFT),andsometimescash,infavor ofasupplierorotherrecipienttodischargetheliability.

• Accounting:Ensuredetailsofeverytransactionarecorrectlyaccountedfor(manuallyorelectronically);prepareanddistributeperiodicfinancialreportsincludinganalysisonallbudgetexecutionoperations

• FinancialControl/Audit:Operateallpre- andpost-expenditurecontrolsandauditingprocedures

• End-of-YearOperations:Closepaymentoperationsandbudgetaccounts; carryover(unspent)funds,asappropriate,tothenextbudgetyear;meetallstatutoryrequirementsforpresentingafinalreconciliationofbudgetrevenues,expenditures,borrowingandassetchanges(“finalaccounts”).

TABLE 1. TYPES OF CONTROL, THEIR KEY FEATURES AND OBJECTIVES

Type of control Objectives Main features Stage(s) at which applied

Appropriation control Ensures that expenditure is covered in the budget and the proposed amount of expenditure includes all relevant expenses.

Budget cover (against the relevant appropriation) is checked after deducting all expenditures previ- ously approved. The amount should be correctly calculated and there should be no hidden expenses.

Apportionment, reservation, commitment and payment order stages and virements during budget execution.

Aggregate cash control

Minimizes the cost of financing government programs by smoothing the gap between cash inflows and outflows. This control is a key element of the overall cash management system.

Release of spending authority (warrants, notification de crédit, etc.) is controlled against an annual cash plan that is updated on rolling basis. Payments by spending units are coordinated with the cash manager to ensure that sufficient cash is available in the TSA.

Apportionment and payment stages.

Commitment control Ensures that expenditure commit- ments by spending units are fully in line with the expenditure limits and the released spending authority.

Spending units enter into commit- ments only against unencumbered spending authority and the cash plan covers the expected payment profiles of commitments.

Commitment stage.

Control of regularity

Verifies the legal and administrative compliance to ensure that the expenditure operation and related documents/contracts follow the procedure, prescribed in the law and/or financial regulations. /1

Legality of the operation is con- trolled by verifying that the officials approving a transaction have the authority to do so, and that the required supporting documents have been prepared in line with the law/regulations (for audit).

Mainly commitment, verification, payment order and payment stages, but also at other stages.

Accounting control Ensures that transactions are prop- erly recorded and accounted for to produce timely and reliable fiscal reports and financial statements.

Transactions are recognized, clas- sified, and recorded in the books/ general ledger according to a coun- try’s accounting policies/standards and chart of accounts. They are also reconciled with bank statements.

Payment and verification (in case of accrual accounting) stages.

1/ All uses of public funds should be governed by financial regulations. These regulations, among other things, prescribe the establishment of responsibility for financial decisions, the segregation of duties to ensure appropriate checks and balances, and documentation procedures for maintaining a defined audit trail.

Authorization for Expenditure in France Limit on amount of expenditure. Government’sexpendituremustbewithintheamountsthatthebudgetappropriationshaveestablished,withsomeflexibilityallowedthroughvirements andcontingencyreservemechanisms.Thenatureofthoseexpenditurelimitsdependsontheaccountingbasis(cash,commitment,oraccrual)usedinthebudget.

Limit on time horizon of expenditure. Theexpendituremustoccurwithinthetimelimitsapplicabletotheexpenditureauthorization.Mostcountriesadoptannualbudgetsauthorizingspendingforoneyear;however,somecountriesauthorizemulti-yearlimitsforcertaintypesofexpenditure.

Authorized purpose of the expenditure. Theauthorityforexpenditureisgivenforaspecificpre- definedpurpose.Thebudgetclassification(whichmaybeorganizedbyprograms,sub-programs,projects,economiccategories,orlineitems)usuallyspecifiesthepurposeforwhichtheexpenditurecanbemade.

Administrative unit accountable for expenditure. Aunitofgovernment,typicallyalineministry,departmentoragency,isassignedtheresponsibilitytoensurethattheappropriatedresourcesarespentasintendedwithintheauthorizedlimits.

CommitmentandPaymentControlImplementingabudgetlegallyandaccuratelyrequireseffectivecontrolsonexpenditurecommitmentandpayment,includingeffectivesanctionsonunauthorizedactivity:

1. KeyElementsofCommitment Control:

• Statedpurposeandfinanciallimitofapprovedbudgetlines• Clearvirement limitsandprocedures• Commitmentauthorizationproceduresatlineministrylevel• Clearandenforcedprocurementrulesandprocedures

2. KeyElementsofPaymentControl:

• Effectiveproceduresforreceivingandverifyinggoodsandsuppliesasordered,andupdatingrecordsofstocks/inventory

• Clearandenforcedproceduresforissuingofpaymentorders• Effectivesanctionsonincorrectpaymentprocedures/decisions• Educationofregularsuppliersinproceduresandrequirementsofgovernment

purchasing/payment

Nature of expenditure limits • Cash-based budgeting systems primarilyenforcealimitontheaccumulationandliquidationofcashobligationsincurredduringthebudgetyear.Astrictlegalinterpretationofacashappropriationwouldmeanthattheappropriationisutilizedwhenthegovernmentmakesacashpayment.Therefore,enteringintoacommitmentorincurringaliabilityinexcessofthelimitwouldnot,intheabsenceofothercontrols,constituteabreachoflaw.Wherecountrieshavecashappropriationsandaccrualbasedfinancialstatements,thisusuallygivesrisetodifferencesbetweenbudgetexecutionreportsandfinancialstatementsthatrequirereconciliation.

• Commitment-based budgeting systems imposelimitsonbothexpenditurecommitmentsandcashpayments.Commitmentlimitsmaybemulti-yearinnature(usuallyforcapitalprojects)andcarriedoverfromonefinancialyeartothenext,whilecashexpenditurelimitsareusuallysetforthebudgetyear.

• Accrual-based budgeting systems enforcelimitsontheincurrenceofliabilities,expensesorexpenditureevenwhennoimmediatecashtransactionsareinvolved.Inaddition,theymayimposelimitsonaccumulationofcashobligations,multi-yearcommitments,andlong-termobligations(suchaspensions)andcontingentliabilities(suchasguarantees).

• The presence of dual appropriations (either commitment/cash or accrual/cash) can complicate control of budget execution by spending agencies.

• Undercommitment-basedbudgetingsystems,thereisaneedtoseparatelytrackandaccountforbothexpenditurecommitmentsandpayments,liquidatethelatteragainsttheformerduringthecourseofthebudgetyear,andcarryforwardunusedcommitmentappropriationsbetweenyears.

• Underadualaccrualandcashbudgeting/appropriationsframework,thereisaneedforeachagencytomakeprojectionsofbothitsanticipatedcashrequirementsaswellasincurrenceofexpensesandliabilitiesandaccumulation/realizationoflong-termobligationsandcontingentliabilities.

Dualappropriations

• Aspartofthecomprehensivereformofitsbudgetframeworkin2001,Franceintroducedmultiannualcommitmentauthorizationsasameansofcontrollingexpenditureobligationsandassociatedpaymentsforprogramsorprojectsthatspanmorethanoneyear(e.g.,investmentprojects).

• Formultiannualprograms/projects,theapprovedbudgetincludesboththemultiannualcommitmentlimits(autorisations d’engagement or AE)againstwhichitalsosetsannuallimits(crédits de paiement or CP)forcashpaymentsduringtheyear.Assuch,thefocusofexpenditurecontrolatthecommitmentphaseofbudgetexecutionhasmovedfromanannualtoamultiannualbasis,i.e.,thetotalcostofalegalcommitmentintowhichthegovernmentisenteringintoisfullyrecordedagainsttheavailablemultiannualcommitmentauthorizations/AEs.

• Assuch,theAEsareconsumedatthecommitmentstageoftheexpenditureorthelegalactofsigningacontractoftheStatewithathirdparty.

Commitment-basedlimitsinFrance

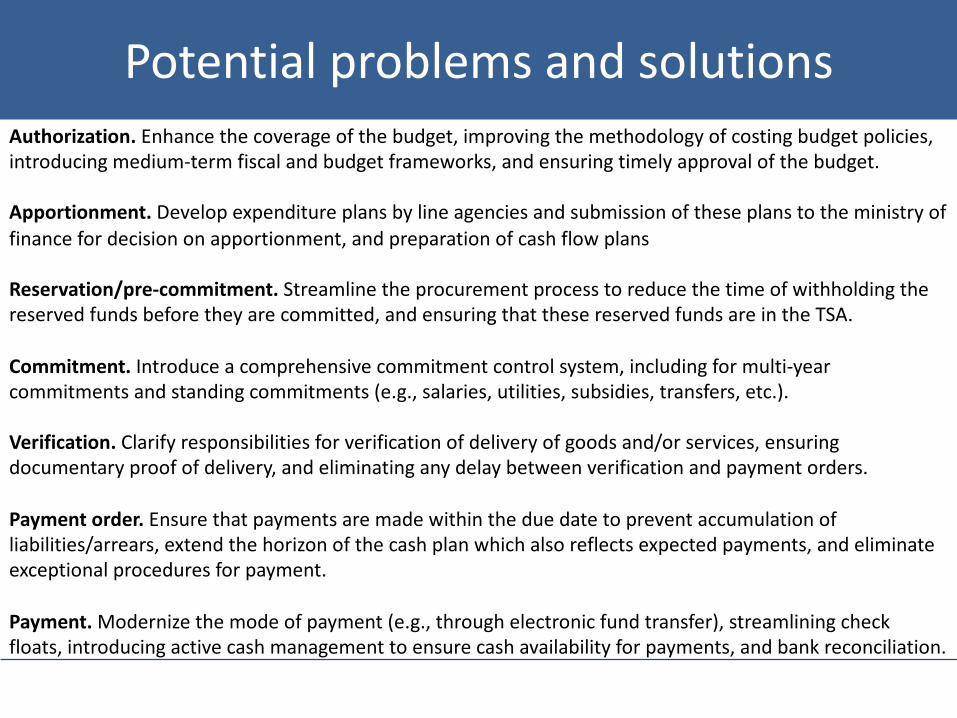

Authorization. Enhancethecoverageofthebudget,improvingthemethodologyofcostingbudgetpolicies,introducingmedium-termfiscalandbudgetframeworks,andensuringtimelyapprovalofthebudget.

Apportionment.Developexpenditureplansbylineagenciesandsubmissionoftheseplanstotheministryoffinancefordecisiononapportionment,andpreparationofcashflowplans

Reservation/pre-commitment.Streamlinetheprocurementprocesstoreducethetimeofwithholdingthereservedfundsbeforetheyarecommitted,andensuringthatthesereservedfundsareintheTSA.

Commitment.Introduceacomprehensivecommitmentcontrolsystem,includingformulti-yearcommitmentsandstandingcommitments(e.g.,salaries,utilities,subsidies,transfers,etc.).

Verification.Clarifyresponsibilitiesforverificationofdeliveryofgoodsand/orservices,ensuringdocumentaryproofofdelivery,andeliminatinganydelaybetweenverificationandpaymentorders.

Paymentorder.Ensurethatpaymentsaremadewithintheduedatetopreventaccumulationofliabilities/arrears,extendthehorizonofthecashplanwhichalsoreflectsexpectedpayments,andeliminateexceptionalproceduresforpayment.

Payment.Modernizethemodeofpayment(e.g.,throughelectronicfundtransfer),streamliningcheckfloats,introducingactivecashmanagementtoensurecashavailabilityforpayments,andbankreconciliation.

Potentialproblemsandsolutions

ManagingPaymentArrears• Paymentarrearsrefertooutstandingfinancialobligationsforwhichpaymentisconsidered

“overdue”.

• Paymentarrearsmayarisefrom:Ø anunrealisticbudget(incl.overestimationofrevenues),Ø poorcashmanagement,Ø poorcontrolofcommitments,andØ individualorsystemiccorruption.

• PaymentsarrearsshouldalwaysbeaprimaryconcernfortheTreasury;theyindicatethatthegovernmentaccountsareundersubstantialfiscalpressureand/orthatbudgetexecutionandcontrolproceduresarefailing

• Accumulationofarrearsdetrimentallyimpactsonthegovernment’scredibilitywithsuppliersandonbudgetexecutionbydistortingspendingand/orborrowingplans

• Removingarrears– andpreventingfurtheraccumulation– requiresasustainedstrategyfromTreasuryandtherelevantdepartments

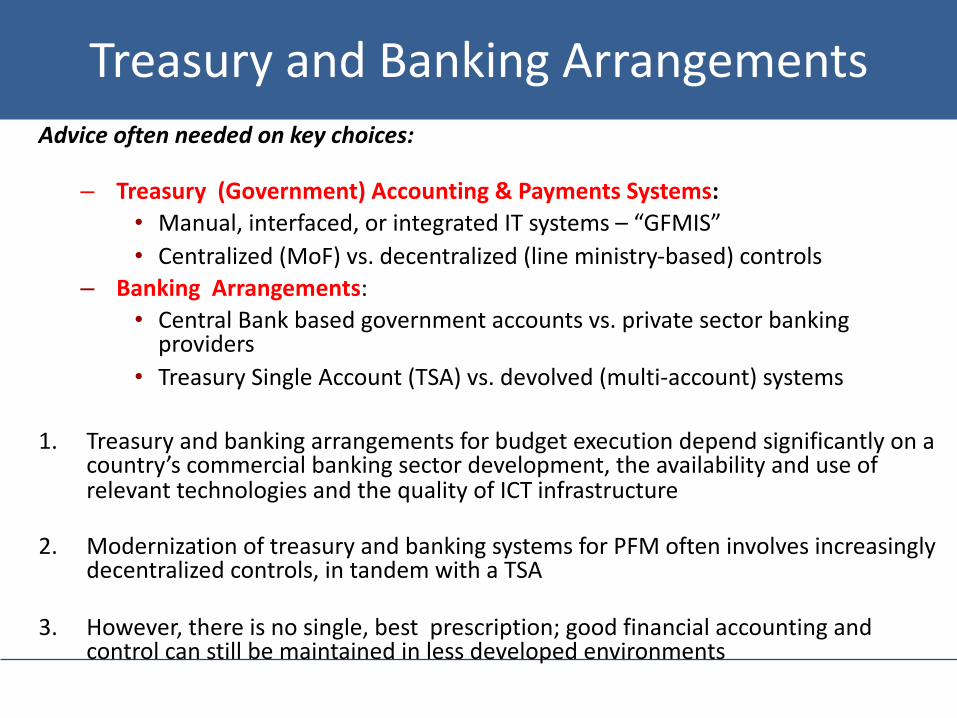

TreasuryandBankingArrangementsAdviceoftenneededonkeychoices:

– Treasury(Government)Accounting&PaymentsSystems:• Manual,interfaced,orintegratedITsystems– “GFMIS”• Centralized(MoF)vs.decentralized(lineministry-based)controls

– BankingArrangements:• CentralBankbasedgovernmentaccountsvs.privatesectorbankingproviders

• TreasurySingleAccount(TSA)vs.devolved(multi-account)systems

1. Treasuryandbankingarrangementsforbudgetexecutiondependsignificantlyonacountry’scommercialbankingsectordevelopment,theavailabilityanduseofrelevanttechnologiesandthequalityofICTinfrastructure

2. ModernizationoftreasuryandbankingsystemsforPFMofteninvolvesincreasinglydecentralizedcontrols,intandemwithaTSA

3. However,thereisnosingle,bestprescription;goodfinancialaccountingandcontrolcanstillbemaintainedinlessdevelopedenvironments

FinancialControlandAudit“Financialcontrol”referstotheregulationsandproceduresthatensuretheintegrityofbudgetoperations.

Therearethreebroadsystems(ormechanisms)offinancialcontrol:

§ Pre-commitmentandpre-paymentcontrols(aparticularemphasisinFrenchPFMadministrativesystems)

§ Post-paymentcheckingandreview- i.e.,“internalaudit”byspecializeddepartmentand/orTreasury-managedagency,focusingonbothtransactionsandsystems

§ FinancialInspectionand/orExternalAudit– thirdparty(independent)authoritynotanswerabletoTreasury/MoF

FinancialReportingandAccounting• The“accountingsystem”providesthefinancialmanagement

“template”forrecording/reportingallbudgetallocations,revenueandexpendituredecisions/actions.

• BudgetClassificationandtheChartofAccounts definehowthisinformationwillberecorded,presented,reportedandanalyzed.

• Financialregulationsdefineandcontrolallaccountingandreportingoperations;ensureaccuracy,transparency,consistencyandlegitimacy

• Accountingandreporting practicesvarywidely;increasingconvergencetointernationalmethodsandstandards (e.g.IPSASandGFSM)

• Accountingsystemsarenotstatic;constantdevelopmentandimprovementintheconcepts,methods,standardsandtechnologies

Cashmanagement

TheObjectivesofCashManagementOverridingobjective:

Ensuringcashisavailabletomeetcommitmentsjustintime

Ø Economisingoncashwithingovernment• Savingcosts• Reducingrisk

Ø Managingefficientlythegovernment’saggregateshort-termcashflow• Bothcashdeficitsandcashsurpluses

Ø Insuchawayasalsotobenefit• Debtmanagement• Monetarypolicy• Financialmarkets(marketliquidityandinfrastructure) 31

Approachestocashmanagement

• Traditional(Passive)Approach

• Essentiallypassive• Monitoringcashbalances,

maintainingcashbuffertohandlebothvolatilityandunanticipatedoutflows

• Ifnecessaryrestraining/slowingexpendituresordelayingbillpayments- cash“rationing”notcashmanagement

• Modern(Active)Approach

• Managingcashmoreactively• Tryingtosmoothweeklyordailycash

flowbymoreactiveborrowingandlendinginmoneymarket

• Allowsloweraveragecashbuffer–withbenefitstootherpolicies

• Givestoolstoprotectexpenditureplansfromcashflowvolatility

32

OECDandmanymiddle-incomecountries(especiallyinEuropeandLatin-America)movingtowardmoreactiveapproach

FiscalObjective

v Ensurecashisavailabletolineministries andspendingagenciestomeetbudget obligationsandcommitments,whendue

v Managebalancesingovernmentbankaccounts effectivelyby:

(i)borrowingtocoverexpectedcashshortfalls,andavoid“idle”balances(ii)investingduringperiodsofsurplus,and(iii)minimizingborrowingcosts

MonetaryObjective

v Neutralizetheimpactonthedomesticbankingsectorofthegovernment’scashflows,ensuringthat:

(i)therearenolargeandunexpectedchangesinliquidityinthebankingsystem

(ii) overallmonetarypolicy(incl.monetarygrowthandinflationtargetsetc.)isnotundermined

KeyPolicyObjectives

Cashflowforecasting

Ø EfficientcashmanagementrequiresabilitytoforecastdailycashflowsacrosstheTSA• Tofacilitateorderlyachievementofbudgettargets;andto

ensurethatbudgetedexpenditureissmoothlyfinanced• Todevisethestrategiesforsmoothingthecashflowprofile

Ø Asmoothercashflowmeans:• Loweraveragecashbalances• Reducedborrowingcosts• Interestoncashbalancesalwayslessthaninterestonmarginalborrowing

• Lesspressureoncentralbanks’monetarypolicyoperations

34

Cashflowforecasting:theaim

Ø ObjectiveistoanticipatecashneedsofgovernmentØ Forecastsneededoftotalnetcashflow(hencealsocashbalance)

• Receiptsandpayments(abovetheline);and• Financingtransactions(belowtheline)- debtredemptions,new

borrowing,assetssales• Focusisdomesticcurrency

Ø MayneedtoidentifyFXflowsseparately(dependsonTSAstructure)

Ø Forecastinformationisneededforsomeperiodahead§ Timingoffuturepeaksandtroughsmustbeidentifiedtomake

decisionsaboutthematurityofrequiredborrowingorlendingØ Ideally

• Daily(ifnecessaryweekly)some3monthsahead• Rolledforwardregularly(weekly)

35

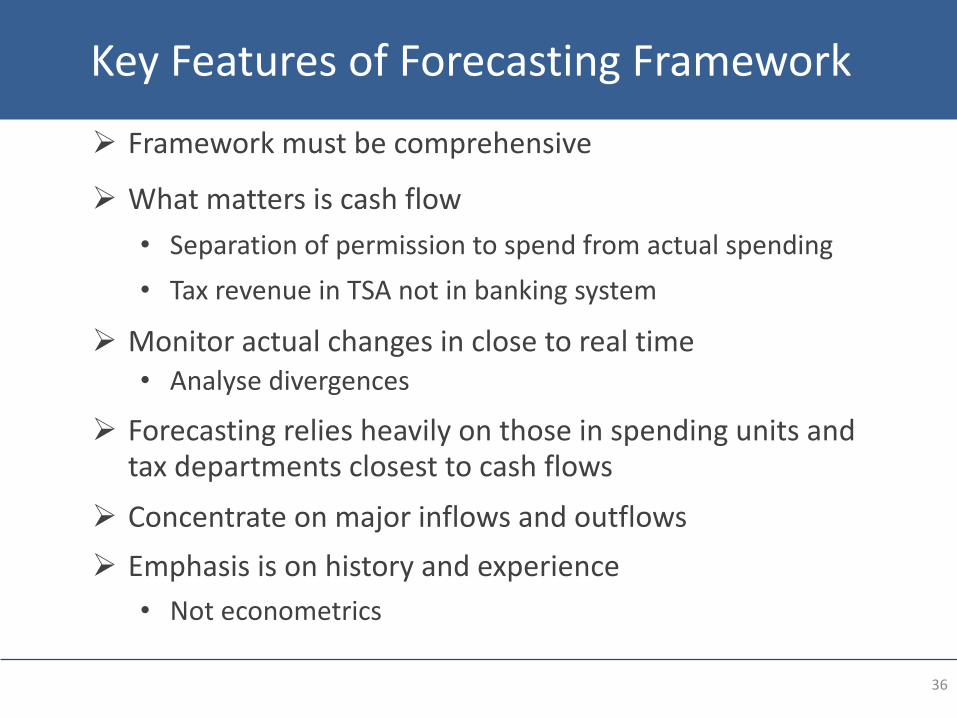

KeyFeaturesofForecastingFramework

Ø Frameworkmustbecomprehensive

Ø Whatmattersiscashflow• Separationofpermissiontospendfromactualspending• TaxrevenueinTSAnotinbankingsystem

Ø Monitoractualchangesinclosetorealtime• Analysedivergences

Ø Forecastingreliesheavilyonthoseinspendingunitsandtaxdepartmentsclosesttocashflows

Ø ConcentrateonmajorinflowsandoutflowsØ Emphasisisonhistoryandexperience

• Noteconometrics

36

ToolandTechniques- 1Ø Atstartofyear,forecastsconsistentwithannualbudget

• Butneedunbiasedestimates– whatisgoingtohappen,notwhat“should”happen;donotconstrainbudgetasyearprogresses

• Mayhelptoseparateforecastingfrombudgetexecutionprocesses

Ø Revenueforecastsfromthetaxdepartments• Monthlytotalsoftaxreceipts,bytaxforxxmonthsahead• Daily[weekly]taxreceiptsfornextmonth,1-3monthsifpossible• Taxusuallymorevariableandmoreunpredictable

Ø Expenditureforecastsfromspendingagenciesorunits• Expectedexpenditure(cashnotcommitments)byday/weekforxxmonthsahead• Focusonlargestspendingunits[80/20rule]• Requirepre-notificationofmajorexpenditures• Manycountrieshaveanend-yearsurgeinexpenditure– avoidrulespreventing

end-yearcarryoverofunusedappropriations

37

ToolandTechniques- 2Ø Identifyseasonality

• Monthlysalarypayments;regularsocialwelfareorpensionpayments• Someotherexpenditures– e.g.agriculturalsupport– maybeseasonal• Taxpaymentdays(geartaxpaymentdaystodaysofexpenditureoutflow)

Ø Identifymajorindividualflows– manyarepreciseandpredictable• Debtissuanceandredemption;interestongovernmentdebt(avoidredemptions

ondaysofheavyexpenditure)• Transferstolowerlevelsofgovernment• Receiptsfrommajorassetsales• Lesspredictablebutimportanttoidentify:

- Paymentsonmajorpublicprojects- Taxpaymentsbythelargestcompanies

Ø Particularproblemswithdonorgrantsanddisbursements• Highlyuncertain,difficulttoforecast,dependsonprojectprogress• Maybepossibletoassumethatprojectspendingandproject-relatedfundingnet

tozero– butdoesnotcopewithlumpyflows• InflowsmayalsogotoseparateaccountsnotTSA

38

MakingforecastingworkinpracticeØ Importantthatspendingunitsandtaxdepartmentscooperate

• Insistonprofilesandforecasts,andreportsonwhyvariationstoforecastsoccurred• Goodadministrativepracticeshouldbeenough;butifnecessarylegislate

Ø CarrotsandSticks• Rewardgoodforecasting:greaterdelegatedauthority,easiervirement,roll-over

unusedappropriations(financialpenaltiesforpoorforecasting)• Ensurethereisnoincentivetohoardcash

Ø Dailymonitoring• MonitoractualtransactionsacrossTSA• Outturnforthedaymustbeknownnolaterthanfollowingmorning• Analyseexperience:e.g.doforecasterrorsimplytimingchangeswithinthemonth

orchangesinthelevelofactivity?

Ø Personalcontacts• Avoidrequests/informationgoinguphierarchy,acrossanddown• Cashforecastersintreasurymusthavedirectcontactwithoppositenumbersin

majorspendingunitsandtaxdepartments39

ManagingforecastdataØ Cashflowforecastingusuallyrequiresdevelopmentofasinglecentral

databaseindependentoftheIFMIS.Reflectsdifferentpurposes:• Cashflowdataareneededtosupportimmediateoperationaldecisions• Theydonothavetobeof“accounting”qualityorprecision

• NotallaccountingchangesrepresentcashflowsØ Cashmanagersneedadatabasethatis:

• Flexibleandundertheircontrol• Allowspreparationofscenarios,what-ifsetc• Abletoholdoutturninformationforanalyticalpurposes

Ø ManycountriesuseExcel,atleastinitially

40

WhodoesWhat?Ø Variousnationalmodels– no“right”approach– butemergingbestpracticeØ Spendingunitsandtaxdepartments– provideabovethelinedataØ InMoF/Treasury/DebtManagementOfficedistinguishbetween:

• Whoaggregates‘abovetheline’forecasts;andtakesresponsibilityfortheprojectionofthetotal

• Whoadds‘belowtheline’transactions– willoftenbedebtmanagers• Whoisresponsiblefortakingdecisionsaboutinvestmentofsurplusesorissuanceof

T-BillstomanagecashflowØ Centralbank– providesbankingservicesandinformationflows

• MayprovidedetailsofactualflowsordisbursementsØ Goodpracticeguidance

• Identifywhoisresponsibleforwhat– othersshouldnotsecondguess• Singlefocusforfinalcompilationanddecisionmaking– onecashmanager• Regular[weekly]meetingsofthoseresponsibleinMoFtoreviewforecastupdates,

decideoninvestment/issuancepolicies,establishriskparameters

41

PuttingtheforecasttoworkØSmoothingthenetcash- Distinguishbetween:

• “Roughtuning”– issuingTreasurybills(orothershort-terminstruments)toapatterndesignedtooffsettheimpactonbankingsectorofnetcashflowsinandoutofgovernment,ietosmoothsomewhatthechangesintheTSA

• “Finetuning”– moreactivepolicies,awiderrangeofinstruments,tosmooththetreasury’sbalancemorefully– technicallymoredemanding

Ø IdentifyresponsibilitywithinMoF/Treasury/DMO• IncreasinglygiventoDMOorsimilar,inconsultationwithothers,

becauseofthebenefitsofintegrationbetweendebtandcashmanagement

• Butdifferentinternationalmodels

42

RoughTuning:Example

43

-25000

-20000

-15000

-10000

-5000

0

5000

1 5 9 13 17 21 25 29 33 37 41 45 49 53 57 61 65 69 73 77 81 85 89 93 97 101 105

Cumulative Daily Cash Flow

-25000

-20000

-15000

-10000

-5000

0

5000

10000

1 5 9 13 17 21 25 29 33 37 41 45 49 53 57 61 65 69 73 77 81 85 89 93 97 101 105

Cumulative Daily Cash Flow

Cum Daily Cash Flow after Bill Issuance

RoughTuningwithweeklyissueofTreasuryBillsonly

Convertsthis profiletothis profile[Finetuningmakesitflat]

Puttingtheforecasttowork

ManagementofCashBalancesØ Separatelyidentify

• Managementofdaytodaycash,includingthecashbuffer• Managementofastructuralsurplus(netofanydebtrepayment)

Ø Structuralsurplus:distinguishbetween• Cashthatmightbeneededoneday

[egin6months]– usuallymanagedbycashmanagersalongsidethecashbuffer

• Longer-termfundso Sovereignwealthfunds,fundsfor

futuregenerations,fiscalstabilisationfunds,pensionliabilityfundsetc

o Managedseparately– incontextofgovernment’swholebalancesheet

Ø Governmentsneedaccesstoliquidity• Impliessomecashbalances• Howdoyoudecidetheminimum? 44

0

2

4

6

8

10

12

14

16

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70 73 76 79 82 85 88 91 94 97 100103106

WorkingDays

bn

Ringfencedbalances(donor funds,stabilisationfundetc) =2billion

CashBuffer =6billion

Target:keepcashflowsinrangeof+/- 3billion,i.e.TSAinrange8-14billion

WhatDeterminestheCashBuffer?1.Thevolatilityofdailycashflows2.Theabilitytoforecastthosecashflows

– Thestandarddeviationoferrorsintheforecastwill[should]bemuchlessthanstandarddeviationofoutturn

– Keyareaforpolicyfocus– treasurershavelessleverageoverotherdeterminants

3.Thescopetomanageunanticipatedfluctuationsandthetimescaleoverwhichtheycanbemanaged– HowsooncanadditionalT-Billsbeissued?

4.Safetynets– Emergencycreditfacilitiesorcashreserves– Endofdayborrowingfromcommercialbanks– [Short-termborrowingfromcentralbank]

45

CashBuffersinPracticeØ SeveralnorthernEuropeancountriesoperatewithcashbalancesinthecentralbank<0.1%

annualcentralgovernmentexpenditure

• Buttheyhaveliquidmoneymarkets,sophisticatedactivecashmanagement.Someplantobelongofcashandon-lendonlywhenpositionissecure

• Dryingupofliquidityledsometobemorecautious

Ø Someotherapproaches– theimportanceofsignallingprudence:

• Targetbalancecalculatedasasafetyreserveineventofadversemarketconditions–dependsonexpectedtimetoreturntonormality

• Maintainingbalancesasleastasgreatasthedebtredemptionsdueinthefollowingmonth,implicitlyallowingforafailedauction

• Toguaranteebudgetexecutionordebtservicefor[X]months

Ø Recommendedbufferinabsenceofdevelopedcashmanagement:

• Cumulativeforecasterrorsoverpolicyreactionperiodcoupledwithacautionarybalanceformarketdisruptionorauctionfailure

• Butthebufferhasanopportunitycost– thereisatrade-offwithcaution

46

CashFlowBuffer:Illustration

-6000

-4000

-2000

0

2000

4000

6000

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49

CumulativeForecastCumulativeActualCumulativeError

Mns

Days

Deterioration 4.9 bn over 4 days

Deterioration 5.8 bn over 6 days

Buffer=Cumulativeforecasterroroverreactionperiod,plus

precautionarybalance

Thefinancialcrisis:somelessons?Ø TheCashManagementReformProgram

• Morefocusonliquidityrisks=>highercashbuffer!• Importanceofimprovedcashflowforecasting

Ø Strongcaseforclosecoordination(orintegration)ofcashanddebtmanagement• Moneymarketisanadditionalshort-noticesourceoffunds– huge

increaseinT-Billissuanceinmanycountries• Bothdebtmanagersandcashmanagersneedaliquidmoneymarket

Ø Developmechanismstocooperatewithcentralbank• Essentialwhenbankingsectorunderstress• Mutualinterestinmoneymarketdevelopment– developrepomarket• Cooperationdoesnotjeopardisepolicyindependence

Ø Developa“financingcontinuityplan”• Greatercautioninrespectofcash,somefront-endloadingofauctions;

proceduresforshort-noticeissuance/[tapping]ofT-Bills,TBonds• Developcashmanagementsafetynets– alongsidethecashbuffer 48

WhatisReducingtheEffectivenessofTreasuryandCashManagement?

Ø PoorCoADesignØ ToomanybankaccountsØ LackofconsolidationofbudgetexecutionprocessesØ Cashadvances/cashfloatsØ PrepaymentsØ Paymentsbychequeinlieuofbanktransfers

49

WhatisReducingtheEffectivenessofTreasuryandCashManagement?

ØNocommitmentcontrolovercapitalandrecurrentspending

ØCapitalcashflowsnotprovidedØRevenuesnotbroughttoaccounteachdayØSpendingdecisionsneedtobeanchoredintheoriginalbudget

ØNewspendingrequests- Remember,approvalofsomethingnewmaymeanyoucannotpayexistingcommitments– medicines,salaries,etc.

50

Conclusions

Ø Growinginternationalappreciationoftheimportanceofactivecashmanagement• Reducesdebtinterestcosts• Contributestootherpolicies

Ø Underpinnedbycashflowforecasts• Anticipatecashflowneedsofgovernment• Dependentoncentralisinginformationfrommanysources

Ø UseofT-Bills,collateraliseddepositsandothershortterminstruments(repoandreverserepo)totunecashflows• Identifykeyresponsibilities• Focusonmoneymarketdevelopment

Ø Identifytargetcashbalances– butincludeabuffer51

TreasurySingleAccount(TSA)

DefinitionsandJustification

ATreasurySingleAccount(TSA)isa

“Unifiedstructureofgovernmentbankaccounts” that…..involvesatop(or“parent”)account,usuallyatthecentralbank,throughwhichthegovernmenttransactsallitsreceiptsandpaymentsandgetsaconsolidatedviewofitscashpositionattheendofeachday.”

Source:PattanayakandFainboim,2011,IMFTechnicalNotesandManuals

TypicalBankingArrangement

MultiplicityofBankAccounts(NoCashConsolidation)

SpendingMinistry

Bank

Accounts

SU

SU

SU

SU

SU

SU

SU

SU

Ministryof

Finance

SpendingMinistry

SpendingMinistry

SU = Spending Units

SU

CommonProblemsinBankingArrangements

1. Multiplebankaccounts:partialornocashconsolidation

2. Idlecashonbankaccountsnotremuneratedwhileaccountsindeficitattractinterest(additionalborrowingcosts)

3. Lowcollectionefficiency– floats rangefromafewdaystomonths

4. Noformalspecificationofserviceexpectations

5. Difficulttoestablish“fullcashposition”ofthegovernment,hence:

§ impossibletoprioritizeandcontrolexpendituredisbursements.§ bankreconciliationresponsibilitiesdispersedandoftenneglected.§ relianceonbankingratherthanaccountingsystemsforbudgetperformance

information.

6. AcomplexstructureofTreasurybankaccountsinthecentralbankandcommercialbanks:differentaccountsfordifferenttypesofexpendituresandrevenues,fewautomatedlinkages

TSA:SummaryofBenefits1. Ensurescomplete,real-timeinformationongovernmentcash

resources(withsupportofaGFMIS)§ enablesefficientcashmanagement§ helpspreparationofaccurateandreliablecashflowforecasts§ optimizesthecostofgovernmentoperations:includes

minimizingthevolumeandcostofgovernmentborrowingandloweringliquidityreserveneeds

§ increasesthereturnonexcesscash

2. Facilitatesefficientcollectionandpaymentmechanisms

3. Improvesoperationalandappropriationcontrolduringbudgetexecution

4. Enhancesefficiencyandtimelinessofbankreconciliation

5. Facilitatestimelyandmorecompleteaccountingstatements/reports,including sourcesandusesofcash

GuidingPrinciples1. Unifiedstructure

§ “Completefungibility”ofallcashresources(inrealtime,ifelectronicbankingisinplace)

2. OversightbytheTreasury

§ Noothergovernmentagencyoperatesbankaccountsoutsidetreasurycontrol/supervision

§ CashbalanceintheTSAismaintainedatalevelsufficienttomeetdailyoperationalrequirements(linkagestodebtmanagement)

3. Comprehensivecoverage

§ Fullconsolidationofcashbalancesofallgovernmententities(budgetaryandextra-budgetary)

BankingArrangementsunderaTSA

58

Debt repayments/interest payments

Subsidies

Transfers (e.g. to local governments)

Payments to suppliers

Payment of wages and salaries

ØØ

ØØ

ØÚ

ÚØ

Ø

Daily settlement with TSA

Bank account(s) of the treasury

Transit / zero-balance bank accounts of the

treasury

Tax payersGovernment Borrowings

TSAStrategy:FocusonCashConsolidation

1. DefinethescopeoftheTSAinapolicydocument2. Developastrategywithprioritizedactions:

§ firstfocusonpotentiallyriskyaccountswithsignificantbalances§ potentiallytargetcommercialbankaccountsofspendingagencies,

extra-budgetaryfunds,anddonorprojectsinthatorder3. Distinguishbetweentheauthoritytospendandphysicallocationofcash:

§ developanaccountingsystemthatclearlyandaccuratelyidentifiescashbalancesofeachentity;

§ developafunctionalityinGFMIStomaintainledgersub-accountswithcorrespondingcreditlimits;

§ establishlegalauthoritytopoolcash(couldinfringeonfiscalautonomyofsub-nationalgovernments)

4. Assurespendingagenciesthatcashwillbeavailablewhenneeded:§ developsuperiorcashforecastingandmanagementcapabilitiesto

meetcashneedsofallentities

TSAStructure:Options1. Acentralized bank account structure:

§ typicallyasinglebankaccount (possibly with sub-accounts)generallymaintained atthe centralbank

§ usuallymanagedwithinwelldevelopedaccountingsystemandaGFMIS§ typicallyRTGS-basedpayments(oftenwithtreasuryasadirectparticipant)

2. Adistributed bank account structure:§ severalindependentbankaccounts(generallyZBAsopenedwithcommercial

banks)operatedbylineagencies/spendingunitsfortheirowntransactions,withpositiveandnegativebalancesintheseaccountsnettedintotheTSAmainaccount

3. Acombination ofcentralizedanddistributedfeatures4. Atthecentralbank:

§ safehavenforgovernmentcashdeposits,minimizescreditriskexposure§ facilitatesthecentralbank’smonetarypolicyoperations§ canfacilitatecost-effectivebankingarrangementsandspeedysettlements§ oftenalegalrequirement

5. Atcommercialbanks – muchlesscommon(Peru,Argentina)

BudgetAuthority/TransactionsProcessing

1. Thedecisionastowhether– andtowhatextent-budgetauthorityshouldbedelegatedtolineministriesisindependentoftheTSAstructure.

2. ATSAcanoperatewithbothcentralizedanddecentralizedtransactionprocessingandaccountingcontrolsystems.

TSAstructureTransactionProcessingSystemCentralized Decentralized

Centralized FranceBrazil

India

Distributed UnitedKingdom Sweden

AdvancedOrganizationalFeatures1. Aninterbanksettlement/clearingsystem

2. Arealtimegrosssettlementsystem(RTGS)atthecentralbankforhighvaluetransactions

3. MajorcommercialbanksandTreasuryconnectedtoRTGS

4. Developmentofasmallpaymentsclearingsystem

5. Electronictransactionprocessingandpaymentsystem(e.g.,GFMIS)withinterface/connectivitytothebanks

6. ATreasurygeneralledgersystemtokeeptrackofcashflowsthroughtheTSA

7. FrameworkagreementsbetweenTreasury(MoF)andbanks

§ Standardizedservicesandtransparentfees§ Penaltiesfordelaysandunder-performance§ Monitoringaccounts/balances

8. AnMoUbetweentheMoF/TreasuryandtheCentralBank 6262

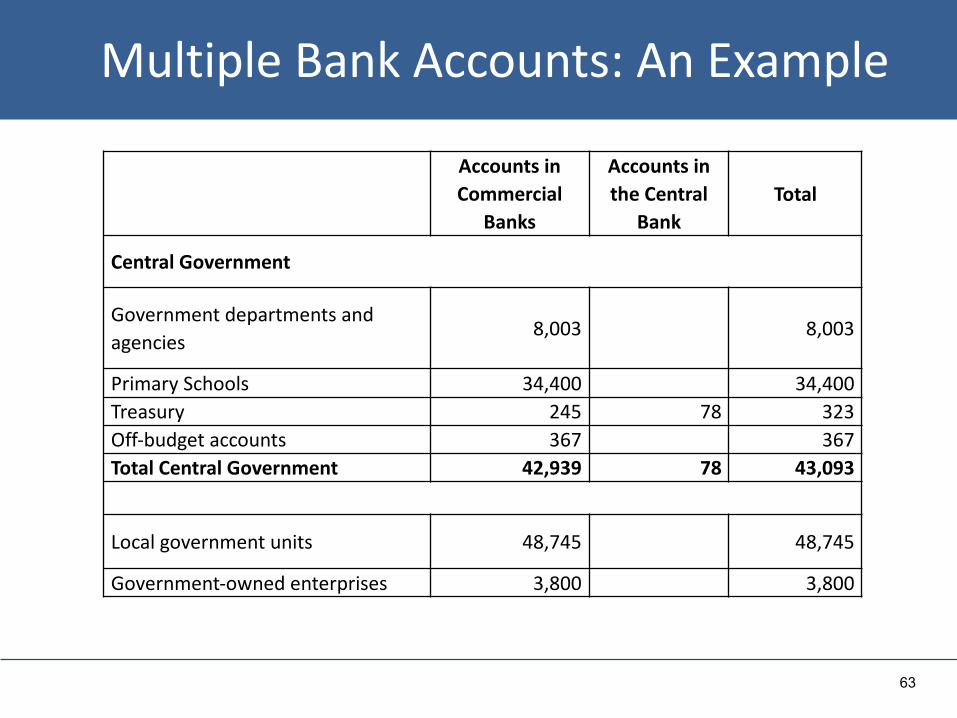

MultipleBankAccounts:AnExample

AccountsinCommercial

Banks

AccountsintheCentral

BankTotal

CentralGovernment

Governmentdepartmentsandagencies

8,003 8,003

PrimarySchools 34,400 34,400Treasury 245 78 323Off-budgetaccounts 367 367TotalCentral Government 42,939 78 43,093

Localgovernmentunits 48,745 48,745

Government-ownedenterprises 3,800 3,800

63

MultipleBankAccounts– IdleCash…

64

TSACoverage

• Budgetarycentralgovernment– Oftendonorfundedprojectsgetexcluded

• Centralgovernment,including:– Autonomousgovernmententities– Extra-budgetaryfunds– Social-securityfundsandothertrustfunds(Brazil)

• Distinguishbetweentransferprogramsandpensionfunds

• Centralandsub-nationalgovernments– EitherunderasingleTSA(France)orseparateTSAs(China)

• Publiccorporations(generallynotincluded)– Shouldincludethoseactingasgovernmentagencies.

6565

InstitutionalChallengesforTreasuryReforms(thesevenCs)

• Consistency withinternationalstandards• Compliance byspendingagenciesandunits• Coverageofthebudgetandreportingframework• Consolidation ofcash• Complexity – ensurethebasicsareinplacebeforemovingtoimplementmorecomplexreforms

• Cost – beforeembarkingonanyreformacost/benefitanalysisshouldbeundertaken

• Capacity – developingcapacitytoimplementthenewreformsiscritical

Selected references

67

• Pattanyak,S.,ExpenditureControl:KeyFeatures,Stages,andActors,IMFTechnicalNotesandManuals, May2016,availableat:http://blog-pfm.imf.org

• Pattanyak,S.andI.Fainboim,TreasurySingleAccount:AnEssentialToolforGovernment,IMFTechnicalNotesandManuals, August2011,availableat:www.imf.org/external/pubs/ft/wp/2010/wp10143.pdf

• Saxena,Sandeep,andSamiYläoutinen,ManagingBudgetaryVirements,IMFTechnicalNotesandManuals, May2016,availableat:http://blog-pfm.imf.org

• WilliamsM.,on“TheTreasuryFunctionandtheTreasurySingleAccount”inAllenR.,HemmingR.,andB.Potter,InternationalHandbookonExpenditureManagement,Chapter16,Macmillan.2013.