Embed Size (px)

Citation preview

Copyright © 2019 IQVIA. All rights reserved.

Drug Delivery & Formulations Summit 2019

Global Pharma Trends & Opportunities for the Packaging

Industry

19 September 2019

Yasemin Karanis, ConsultantThought Leadership, IQVIA

Agenda

1

+ Trends in Global Pharma

+ The shift to specialty & targeted products

+ Opportunities for the packaging industry

2

US42%

EU511%

Japan6%

Pharmerging25%

ROW16%

Global pharma sales forecast 2023

Global pharma to grow at 4-5% CAGR at ex-manufacturer prices and 2-3% at net prices

Notes: *Subject to PPRS rebate; Ex-manufacturer price levels, not including rebates and discounts. Contains Audited + Unaudited data; Growth considered on par if the there is overlap between country and region CAGR rangesSource: IQVIA Thought Leadership Analysis; Market Prognosis March 2019

1,119 1,184 1,233 1,289 1,351 1,419 1,4850.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0

200

400

600

800

1,000

1,200

1,400

1,600

2017 (a) 2018 (a) 2019 (f) 2020 (f) 2021 (f) 2022 (f) 2023 (f)

LC$

Ann

ual G

row

th (%

)

Sale

s (U

S$, b

illio

n)

World Sales - 2019-2023 Current Forecast (Published: March 2019)% Annual Growth - 2017-2023 Current Forecast (Published: March 2019)

2023 Market Share (US$) based on March 2019 Forecast

World Sales (actual) Published: March 2019

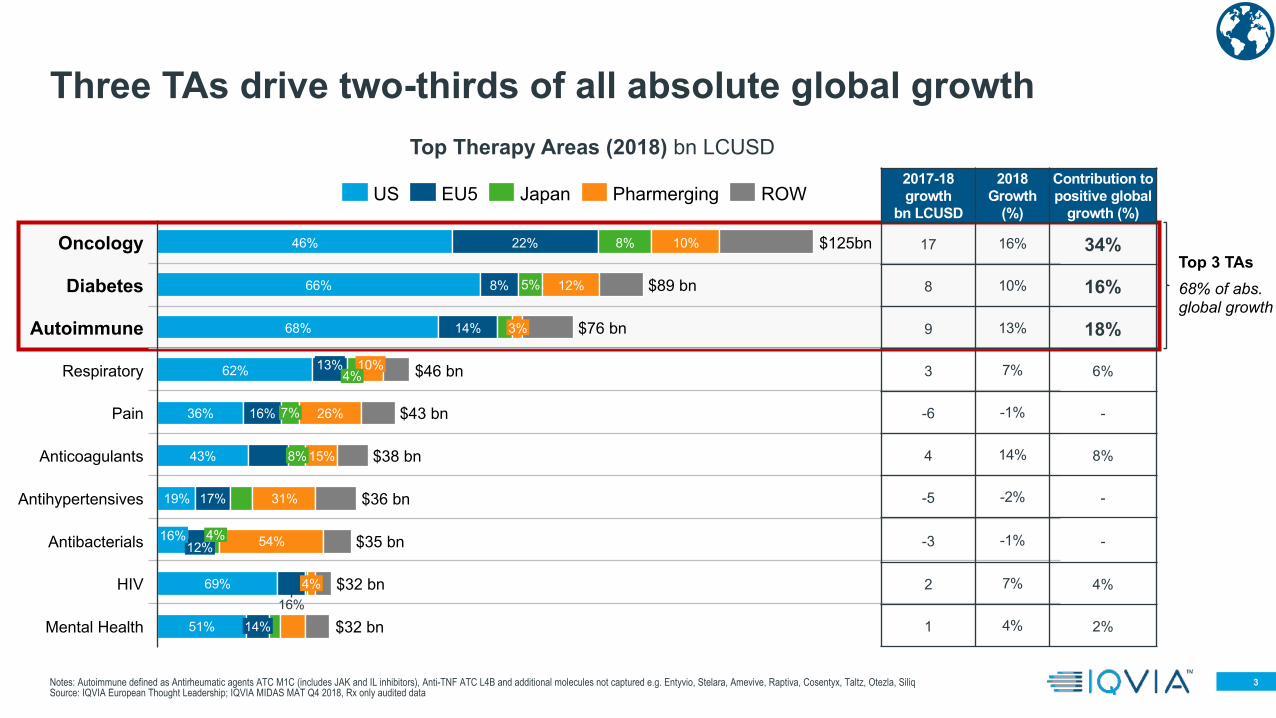

3

2017-18growth

bn LCUSD

2018Growth

(%)

Contribution to positive global

growth (%)

17 16% 34%

8 10% 16%

9 13% 18%

3 7% 6%

-6 -1% -

4 14% 8%

-5 -2% -

-3 -1% -

2 7% 4%

1 4% 2%

Three TAs drive two-thirds of all absolute global growth

Notes: Autoimmune defined as Antirheumatic agents ATC M1C (includes JAK and IL inhibitors), Anti-TNF ATC L4B and additional molecules not captured e.g. Entyvio, Stelara, Amevive, Raptiva, Cosentyx, Taltz, Otezla, SiliqSource: IQVIA European Thought Leadership; IQVIA MIDAS MAT Q4 2018, Rx only audited data

22%

4%

7%

Mental Health

5%

12%

Anticoagulants

12%

Oncology

Antihypertensives

10%

Pain

8%

3%

46%

8%66%Diabetes

14%68%Autoimmune

19%

Respiratory 10%13%4%

69%

17%

62%

26%16%

$32 bn

$38 bn

36%

15%8%

16%

43%

$36 bn

14%

4% 54%

$76 bn

HIV

16%Antibacterials

31%

51%

$89 bn

$125bn

$46 bn

$43 bn

$35 bn

$32 bn

US EU5 ROWJapan Pharmerging

Top Therapy Areas (2018) bn LCUSD

Top 3 TAs68% of abs. global growth

4

0%

10%

20%

30%

40%

50%

60%

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Specialty ~90% of abs. growth in US, Europe

The unstoppable rise of Specialty: set to become dominant segment in the developed markets by 2023

Source: IQVIA Market Prognosis, Sep 2018; IQVIA Institute, Dec 2018

USGermanyU.K.France

ItalySpain

EU5 Japan PharmergingChinaRussiaOther Pharmerging

BrazilIndia

Forecast2019–2023

Forecast2019–2023

Forecast2019–2023

Forecast2019–2023

Spec

ialit

y sp

endi

ng a

s a

prop

ortio

n of

tota

l spe

nd (%

)

5

Global volume growth is moderate, delivery form growth comes from oral solids

Source: IQVIA European Thought Leadership, Excludes Hospital Solutions, Imaging and traditional Chinese medicines, MIDAS MAT Q1 2014 – MAT Q1 2019. Standard Units

Regional Market Share 2019 (SU) Global Rx Volume (SU Bn)

3659

519

21110861

2.859

632

715

2014

40 6275 140244

645

759

777

2019

2.446

+3%CAGR 2014-19

46%

11%

10%

8%

8%

18% Most volume still in oral solid - ~58% volume comes

from tablets and capsules

primarily used in mass markets to

treat symptoms as thyroid

insufficiency, hypertension or

pain

Powders

Other

Gels, Creams

Tablets

Coated Tabs

Aerosol

Injectables

Capsules

Liquids

ChinaPharmerging JapanEU5

USRoW

6

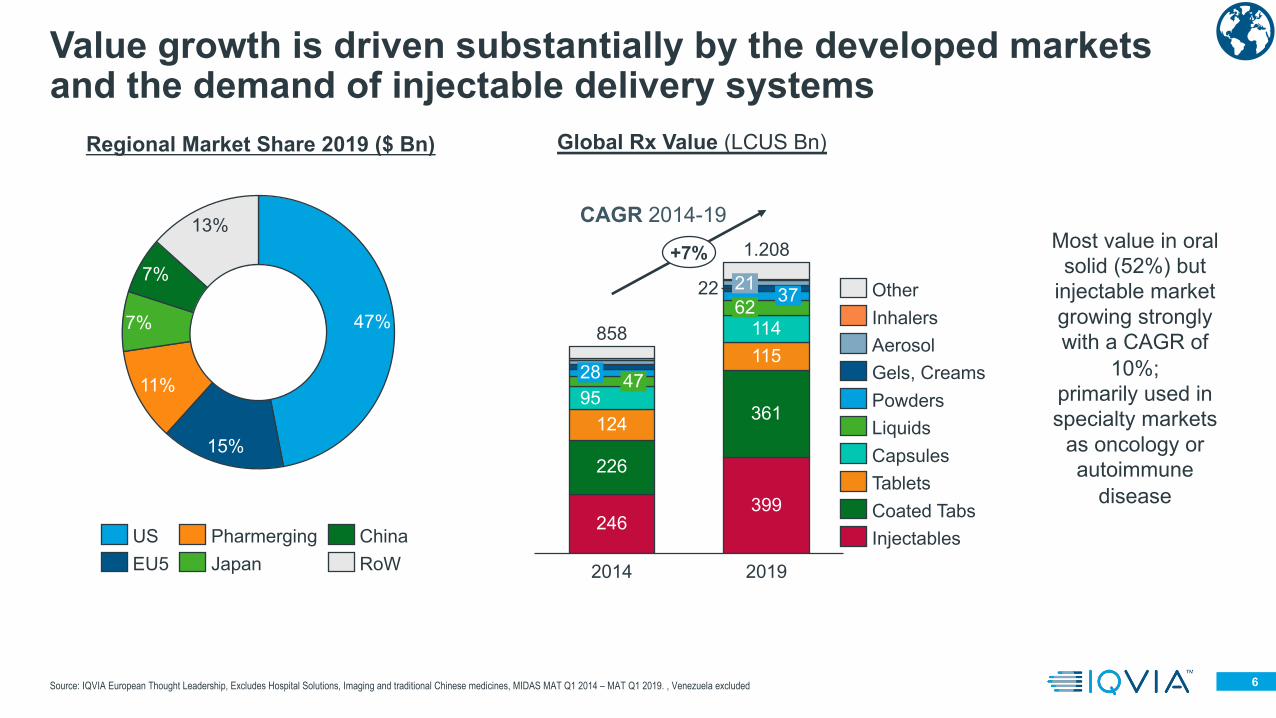

Value growth is driven substantially by the developed markets and the demand of injectable delivery systems

Source: IQVIA European Thought Leadership, Excludes Hospital Solutions, Imaging and traditional Chinese medicines, MIDAS MAT Q1 2014 – MAT Q1 2019. , Venezuela excluded

Regional Market Share 2019 ($ Bn) Global Rx Value (LCUS Bn)

47

115

95

114

226

28

124

62

2014

212237

361

2019

858

1.208

246

399

+7%

CAGR 2014-19

47%

15%

11%

7%

7%

13%

Aerosol

Other

Capsules

Powders

Inhalers

Gels, Creams

Liquids

Tablets

Coated Tabs

InjectablesChinaUS

JapanEU5

Pharmerging

RoW

Most value in oral

solid (52%) but

injectable market

growing strongly

with a CAGR of

10%;

primarily used in

specialty markets

as oncology or

autoimmune

disease

Agenda

7

+ Trends in Global Pharma

+ The shift to specialty & targeted products

+ Opportunities for the packaging industry

8

Biologics account for a high proportion of the future pipeline which should sustain strong growth

Source: IQVIA NSP Dataset (January 2018 – December 2018); IQVIA Analysis; IQVIA Pipeline Intelligence (April 2019)

Preclinical

Phase-I

Phase-II

Phase-III

Pre-reg / registration

1455

Biologic Small molecule

780

861

316

114

1328

888

932

372

150

Biologic sales are 32% of total market but pipeline is 45% biologics

Biologics and small molecules(Q2 2009-19) US$ Bn

Global Pharmaceutical Pipeline (2019)

19%

68%

32%

81%

2009 2019

661

1,035

Non-BiologicBiologic

9

Injectables fastest growing due to shift to specialised medicines

Source: IQVIA European Thought Leadership Analysis; IQVIA MIDAS MAT Q1 2019; Rx only

Combinations (2019) Volume (SU) Forms of Administration (2019)

53%

35%

5%

Oral

Parenteral

Ophthalmic

LungTopical

2%

2%

Other

2%

80%

20%Combination

Plain

Admin route, Global (2019) LCUSD

Injectables 5y CAGR 10%

Form Sales LCUSD(MAT Q1 2019)

5y CAGR%(2014-19)

Coated Tabs 361 10%

Infusion 128 12%

Prefilled Syringes 127 14%

Tablets 115 -1%

Capsules 114 4%

Vials 100 5%

Liquids 62 6%

Powders 37 6%

Pens & Cartridges 25 14%

Other 138 5%

10

Pre-Filled Syringes are the fastest growing injectables segment

Notes: Notes: Injectables defined as NFC2: Ampoules, Infusions, Pens & Cartridges, Prefilled Syringes and Vials;Source: IQVIA European Thought Leadership; IQVIA MIDAS MAT Q1 2019; Rx only, Venezuela excluded.

Global Injectables split, LCUSD 5y Injectables Positive Contribution to growth (2014-19), LCUSD

47%

17%

12%

12%

6%6%

China

PharmergingJapan

EU5

RoW

US

5%

27%

6%5%

25%

6%

32%

30%

2014

32%

32%

2019

$246 bn

$399 bn+10%

Vials

Ampoules Prefilled SyringesPens & Cartridges Infusion

CAGR %

5%14%

5%

14%

12%

11

Only 22% of products in late-stage pipeline belong to large pharma

Innovation in oncology will continue with a diverse range of companies driving it

Source: IQVIA, ARK R&D Intelligence; IQVIA Institute; IQVIA Thought Leadership Analysis Q1 2019

• 506 smaller companies, with just 1 product in clinical development

Total:711 companies

0

10

20

30

40

50

60

70

60300 5 2510 15 20 35 40 45 9550 10055 65 70 75 80 85 90

Pfizer

GSK / Tesaro

Celgene

Oncology % of late stage pipeline

Onc

olog

y in

dica

tions

in la

te-s

tage

pip

elin

e

AstraZeneca

Lilly

Merck & Co

Novartis

Roche

Top-10 oncology companiesOther large pharma companies (<$10bn) Academic Institutions

Smaller companies with an oncology pipeline

BMS

12Notes: Bubble size represents 2018 sales in US$; Products without 5-years sales excluded from CAGR average. Definitions hormonal therapies: ATC LO2: AA, AB, AE, AX, BA, BB, BG, BX; Checkpoint inhibitors include PD-1/L1 and CTLA-4 targeted therapies: nivolumab, pembrolizumab, atezolizumab, avelumab, durvalumab and ipilimumab. Source: IQVIA MIDAS MAT Q4 2018 (Rx only)

0 44186

50

42

400

-8 36 404 10 12-50

14 16 20 24 26 28

200

30 328 38

0

250

300

350

34

450

500

550

600

2

650

22

Long term growth (2013-18) CAGR (%)

mAbs

Shor

t ter

m g

row

th (2

017-

18)

Checkpoint inhibitors

Cytotoxics

Haematological

mAbs(solid tumors)

Targeted small molecules

Targeted small molecules (solid tumours)

Hormonal

Targeted therapies in oncology, biologic or small molecule, dominate the high value growth areas

Oncology PPG = 15.9%

Onc

olog

y 5y

r CA

GR

= 1

3.8%

3-year Oncology growth dynamicsInjectablesMixOrals

Agenda

13

+ Trends in Global Pharma

+ The shift to specialty & targeted products

+ Opportunities for the packaging industry

14

The importance of focusing on the patient is increasingly recognised by companies

Source: IQVIA Patient centricity: measuring impact; *incl. external HC system stakeholders, joint ventures and non-traditional / innovative co-development

The 2000s

Multi-stakeholder go-to-market approach

• Coordinated many-to-many approach

• Multiple in-field roles engaging with a large variety of stakeholders

Evolving Model

Patient-centric go-to-market approach

• Patient at the centre of the engagement

• Value-based partnerships* with other stakeholders to create patient benefit

The 1990s

Traditional go-to-market approach

• One-to-one relationship between sales rep and physician

• Push strategy

Reps Patient relationsMSLs

Market Access Regulatory KAMs

15

Compliance is undoubtedly the biggest source of inefficiency

• Adherence decreases with the frequency of the regimen:

Source: IQVIA European Thought Leadership; IQVIA Institute 2012 “Responsible use of Medicine; https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3711878/; http://annals.org/aim/fullarticle/1357338

57%Non-adherence

9%

Delayed evidence-basedtreatment practise 13%

11%Antibiotic misuse

Medication errors

62

6%Suboptimal generic use

269

4%Mismanaged polypharmacyin the elderly

42

100%Total avoidable costs

18

54

30

475

USA Estimated avoidable costs (2012) bn USD

72%1x

69%2x

65%3x

51%4xDaily dosing

Adherence rate

• Packaging is important: A study on using calendar packaging in 7 trials showed 6 showed positive results

• Therapy areas matter:- Adherence is greatest in patients with HIV, arthritis,

gastro or cancer.- Lowest in pulmonary, diabetes or sleep disorders.

16Key findings from IQVIA project on case studies for value added medicines

Innovation in drug delivery & formulations can provide a range of benefits to patients and healthcare systems e.g. VAMs

Reduced opioid induced constipation

Improved inhaler

Simplified and safer administration

Superior Efficacy Reduced Side Effects Improved Patient Experience

Value Added Medicine Benefit

Additional Therapeutic Option

Improved progression free

survival

Non-stimulant treatment optionMetex PEN

Not exhaustive

17

Value Added Medicines products fall on a spectrum of innovation

Source: IQVIA European Thought Leadership

Lower level innovation• Combination• Formulation• Dermal patches

Incremental innovation• Inhalers• Auto-injectors

Novel delivery tech• Nanoparticles• Microchips• Minipumps

Continuous innovation• Lower barrier to entry

• Broader patient reach

• Established solutionsBreakthrough innovation

• Higher barrier to entry

• Narrower patient reach

• Higher differentiation

Innovation at many levels

Network effects

Broader patient reach

Higher differentiationDigital

Digital pill• Novel tech• Holy grail of

adherence• Not yet perfect

Digital therapeutics• Gamification• Telehealth

Integration with smart devices• Large userbase• Established platforms

18

Strong forces are driving changes in healthcare

Global pharma seeing

decelerating growth and

squeezed budgets

Specialty set to become

dominant segment by

value

Innovation in delivery and

formulations key in creating product

differentiation

Pharma companies increasingly

require patient centric delivery

solutions

19

Prescription launch offering types have multiplied since 2010- a changing landscape

Synthetic small molecule therapeutics since 1899 (Aspirin)

Recombinant biologics since 1982 (Humulin)

Prescription digital therapeutics since 2010 (BlueStar)**

*Gendicine was approved in China in 2003, but Glybera was first gene therapy approved by EMA and FDA**First standalone prescription digital therapeutic (re-Set) approved by FDA November 2018

Cell Therapy since 2011 (Provenge)

Controlled substances for psychiatric disorders 2019

(Spravato) Until 2010 there were only two types of innovative prescription medicine to launch: small molecule of biologic, into systems designed to approve, provide and pay for them

Now an accelerating number of new types of prescription therapeutic are being approved –systems need to catch up

Gene Therapy since 2012 (Glybera)*

Thank you

Yasemin Karanis

Consultant, European Thought LeadershipIQVIA