Embed Size (px)

Citation preview

Sa les , Use , a nd Wit hholding Ta x For ms a nd Inst ruc tions

Each business must file an Annual Return (Form 165).

Annual Return Filing Deadline: February 28.

78 (Rev. 10-13)

Visit Treasury’s Web site at www.michigan.gov/bustax for assistance with:

• Existing Electronic Funds Transfer (EFT) account questions.• Specificaccountquestions(credits,assessments,penaltywaivers,etc.).• Technicalquestions(taxabilityofitems,lawchanges,etc.).

• Checkingthestatusofyoursales,useandwithholdingtaxtransactions.

Assistanceisalsoavailablebycalling(517)636-6925.Listentoalloptionsontheautomatedphonesystembeforemakingaselection.AssistanceisavailableusingTTYthroughtheMichiganRelayServicebycalling1-800-649-3777or711.Printedmaterialinanalternateformatmayberequestedbycalling(517)636-6925.

NOTE: Flow-ThroughWithholdingmustnowbereportedonaMichigan Flow-Through Withholding Quarterly Return(Form4917)andaMichigan Flow-Through Withholding Reconciliation Return (Form4918).Bothformsareavailableatwww.michigan.gov/taxes.

2

General InformatIonImportant InformationNew Registration Online Services. Beginning in the Springof2014,Treasurywillprovideenhancementstoonlineservicesfor business tax filers. The first of these enhancements willallowonlinemanagement of account profile information suchasbusinessaddresschanges,theabilitytoadd,changeordeleteAuthorizedRepresentativesforyourbusiness,andtheabilitytoupdateCorporateOfficerinformation.Sales, Use and Withholding (SUW) e-filing. New online services for SUW taxfilerswill begin in calendar year 2015.Treasury will offer free electronic filing of SUW returnsthrough its own secure site, whichwill include a simple andsafe electronic payment option. Visit Treasury’sWeb site forupdatesasnewservicesbecomeavailable.Discontinuance of SUW Return Mailings. To promoteefficient,easy,andaccurateprocessing, theSUWreturne-fileoptionwillbeavailableJanuary1,2015.Thisfreee-fileoptionwillbeafastandsecuremethodforsubmittingyourmonthly,quarterly, and/or annual returns and payments. Therefore,beginningwith the January2015 returnperiod,Treasurywillnot mail pre-identified returns. We encourage you to chooseoure-fileoptionwhenavailable;however,aprintableformwillstillbeavailableonTreasury’sWebsite.

Filing by Electronic Funds Transfer (EFT). Using EFT tosubmityoursales,use,andwithholdingtaxpaymentseliminatestherequirement tofilemonthlyorquarterlypaperreturns.Thefiling of the Annual Return for Sales, Use and Withholding Taxes (Form165) isstill required.TheEFT Debit Application (Form2248) orEFT Credit Application (Form2328)must becompleted and signed by an officer giving his or her title andreturned to Treasury. Accelerated Tax Payments. Filers who paid more than$480,000 in withholding tax in the preceding calendar yearmust pay according to their federal schedule and must paywithholding taxes by EFT. Filers who paid more than $720,000 in sales or use tax inthe preceding calendar year must pay their sales and usetaxes on an accelerated schedule. Accelerated tax paymentsmust be remitted by EFT. Additional forms and informationabout EFT and Accelerated Tax payments can be found atwww.michigan.gov/biztaxpayments.Debit transactions will be ineligible for EFT if the account used for the electronic debit is funded or otherwise associated with a foreign financial institution account to the extent thatthepaymenttransactionwouldqualifyasanInternationalACHTransaction(IAT)underNACHARules.Contactyourfinancial

Filing Requirements: You are required to file each return, even if no tax is due. Your filing frequency is determined by the Michigan Department of Treasury (Treasury).

Filing Frequency Due Date Combined return

(Form 160)

Discount Voucher

(Form 161)

EFT: ACH Debit or Credit

(No form required)

annual return

(Form 165)Annual Filer Only: Total tax liability of less than $750 for a calendar year (Jan-Dec).

February 28 (after taxyear end) a

Quarterly Filer: Total tax liability of $750 - $3,600 for a calendar year (Jan-Dec).

20th of the monthfollowing quarter’s end a a

Monthly Filer: Total tax liability greater than $3,600 for a calendar year (Jan-Dec). Seasonal filers: see page 7.

20th of the followingmonth a a a

Electronic Funds Transfer (EFT): Available to all taxpayers - transmissions are required on a monthly basis.

20th of the followingmonth

a aAccelerated Sales and Use Tax EFT: Required if Sales or Use Tax liability was at least $720,000 in the preceding calendar year.

MonthlyTransmissions:

• 1st payment 20th ofthemonth• 2ndpaymentlastdayofthemonth• 3rd payment 20th ofthesubsequentmonth

a a

Accelerated Withholding Tax EFT: Required if Withholding Tax liability averaged $40,000 or more per month in the preceding calendar year.

Paid according tofederal schedule

a a

3

institution for questions about the status of your account. Contact Treasury’s EFT Unit at (517) 636-6925 for alternatepaymentmethods.NOTE: As passed, Public Act 458 of 2012 changed thesales and use tax filing requirements beginning January 1,2014. These changes include a reduction in the number ofprepayments requiredeachmonth,aswellas,achange to theprepaymentcalculation.However,pleasebeadvisedthatHouseBill4920of2013was recently introducedand this legislationwoulddelaythesefilingchangesuntilJanuary1,2015.Atthistime, the Department anticipates the passage of House Bill4920.VisitTreasury’sWebsiteforfilingrequirementupdates.Sales Tax Computation. To determine the tax, retailersmustcompute the tax to the third decimal place and round up to awholecentwhenthethirddecimalplaceisgreaterthanfourordown to awhole centwhen the third decimal place is four orless.Filers Who Pay Once a Year. Filers with no deductions should usethesimplifiedinstructionsonpage8.Changes to an Existing Registration for Michigan Taxes. To makechangestoanexistingTreasuryregistrationfortaxessuchasanaddresschange,addordeletealocation,ornamechange,you must notify Treasury’s Registration Section using theNotice of Change or Discontinuance (Form163)or inwriting.ChangesmadeatthePostOfficeorotherStateagenciesdonotupdate Treasury records. Do not write changes on the annual return.Pre-Identified Returns and Vouchers. The Combined Return for Michigan Taxes (Form160) andDiscount Voucher for Sales and Use Taxes (Form 161) sent to you containspecific information about your account that is processed byelectronically scanning the document. Do not change, copy, or use forms from another business.Ifyouloseyourbookletofmaterials,contactTreasurytohaveanewbookletmailedtoyou. IMPORTANT: To ensure your payment is credited toyour account, use ONLY your pre-identified returns. Use thecorrect pre-identified form for the period for which you arefiling.Magnetic Media/W-2 Reporting. The State only accepts magneticWage and Tax Statements (FormW-2) reporting inthe format published by the Social Security Administration.Filing and format instructions are providedonTransmittal for Magnetic Media Reporting of W-2s, W-2Gs, and 1099s to the State of Michigan (Form447).Retail Sales to Federally Recognized Indian Tribes or Their Qualifying Members. The State has set up special sales and use tax protocols for certain situations involving federallyrecognized Indian tribes and their qualifying members. Foradditional details, visit www.michigan.gov/taxes for NativeAmericaninformation.Sales Tax, Use Tax, and Withholding Tax Reporting Requirements. If a taxpayer inserts a “zero” on (or leavesblank) any line on a form for reporting Sales Tax, Use Tax,or Withholding Tax, the taxpayer is certifying that no tax isowedforthattaxtype.If it isdeterminedthattaxisowed,thetaxpayerwillbeliableforthedeficiencyaswellaspenaltyandinterest.

registering and filing returnsBusinesses that make retail sales or hire employees mustregister their business and file periodic returns to pay thesales,use,andwithholdingtaxesdue.Treasurysetsamonthly,quarterly,orannualfilingfrequencybasedonyourtaxliability.Appropriate forms will be provided to you. Visit www.michigan.gov/businessforadditionalinformation.Your filing frequency may change over time. When it does,Treasurywillnotifyyouandsendyouthenecessarymaterials.Ifyoufileonlyonceannuallyandyouraccumulatedsales,use,andwithholding taxes become$750ormore, youmust notifyTreasury immediately. We will change your filing status andprovideyouwiththeappropriatetaxmaterials.E-Registration for Business Taxes. If you already have aFederal Employer Identification Number (FEIN) and wish toregister for business taxes, you may submit your registrationinformationonline.Bycompletingyourapplicationonline,yourbusiness can:• ReceiveitsSalesTaxLicensewithinsevendays.• Add taxes or licenses to its registration.You cannot use your Social Security number as your FEIN.RegistrationinformationandalinktothejointUnemploymentInsuranceAgency/Treasurye-Registration sitecanbe foundatwww.michigan.gov/business.

Sales TaxYoumust register to pay sales tax if youmake retail sales ofgoodsinMichiganeven if the items you sell are not taxable.501(c)(3) or 501(c)(4) Nonprofit Organizations. Ifyoumakesalesat retail,youmust register fora sales tax licenseeven iftheitemsyousellarenottaxable.Ifyourgrosssalesduringtheyeararelessthan$5,000,youdonotneedtocollectorpaysalestax.However,ifyoucollectsalestax,youmustremititevenifyouraggregatesalesfortheyeararelessthan$5,000.For example, if you expect your gross sales to be $6,500 andcollectsales tax,butyouractualgrosssaleswereonly$4,000,you must pay the sales tax collected to Treasury. See theworksheetinstructionsforline5ionpage11.If you don’t collect sales tax on your sales, but your salesare$5,000ormore, you are liable for the taxon all sales.Tocalculate thesales taxdue,divideyourgrosssalesby17.6667and enter the result onyourworksheet, line5j (seeworksheetinstructions, page 11). See Revenue Administrative Bulletin(RAB) 1995-3 on Treasury’s Web site or contact CustomerServiceat(517)636-6925.

Use Tax on Sales and RentalsYoumustregisterandpayusetaxifyou:• Are doing business in Michigan but do not have a retaillocationinMichigan;

• Voluntarilycollectusetaxfromyourcustomers;• Selltelecommunicationsservices;• Renthotelandmotelroomsorotheraccommodations;or• LeasetangiblepersonalpropertytoMichigancustomersfromaMichiganoranout-of-statelocation.

4

Use Tax on PurchasesAlmosteverybusinesshasausetaxliability.Youmustpayusetax on your purchases if you:• Buy goods from out-of-state, unlicensed vendors, unless avalidexemptioncanbeclaimed;

• Buyinventoryexemptfromtaxforresaleonwhichnotaxisdue, then remove items from that inventory for personal orbusinessuse;or

• Use the items you buy for resale as gifts for friends andfamilyorforotherpersonaluses.

Income Tax WithholdingYoumustregisterandpayincometaxwithholdingifyou:• Paywagestoanemployee;or• Withholdincometaxamountsfromotherkindsofpayments

(e.g., lottery winnings, insurance payments, retirementincome,etc.);or

• Paypension,annuity,orotherretirementbenefitsthatwillbesubjecttoincometax.

Ifyouareself-employedandexpectyourannual taxduetobemorethan$500,youmustreportandpayincometaxquarterlyusing Michigan Estimated Individual Income Tax Voucher (MI-1040ES). Otherwise, you may pay your income tax onMichigan Individual Income Tax Return(MI-1040).For complete withholding information, see 2014 Michigan Income Tax Withholding Guide(Form446).

Flow-Through WithholdingAll flow-through withholding tax collected must be reported

and paid using the Michigan Flow-Through Withholding Quarterly Return (Form4917),andannuallyreconciledon theMichigan Annual Flow-Through Withholding Reconciliation Return(Form4918).No flow-through withholding should be reported on, or paid with, Forms 160 & 165. The individual flow-through withholding rate is 4.25 percent.Youmustregisterandpayindividualflow-throughwithholdingif you:• Areaflow-throughentity,S-corporation,partnership,limited

partnership, limited liability partnership, or limited liabilitycorporation with taxable income available for distributionto nonresidentmembers, non-resident shareholders, or non-resident partners. Refer to Treasury’s Web site listed below formoreinformation.

• Are a flow-through entity and one or more of the entity’smembers is a nonresident flow-through entity. The flow-throughentityinMichiganshallwithholdMichiganincometaxfromanysuchnonresidentflow-throughentityonbehalfofallofthenonresidentmembers.

Thecorporateflow-throughwithholding rate is6percent.Youmust register and pay corporate flow-through withholding ifyou:•Areaflow-throughentity,S-corporation,partnership, limitedpartnership, limited liability partnership, or limited liabilitycorporation with greater than $200,000 business incomeavailablefordistributiontoacorporateowneroranotherflow-through entity.

Additional information, form access, and updates on the taxchangesfor2014areavailableatwww.michigan.gov/taxes.

WHAT FoRM To FIlE AND FIlINg INSTRUCTIoNSWiththisbookletyoureceivedthefollowingpre-identifiedformswithyourbusinessnameandaccountnumber:• Annualreturn• Noticeofchangeinyourbusinessstatus• Monthly(orquarterly)returns• Discountvouchers(forsalesandusetaxfilersonly)Someformsmaynotapplytoyou.To prepare your return accurately, complete your worksheetbefore attempting to complete your return. Each item on thereturncorrespondstoalinenumberontheworksheet.Enter your amounts carefully and completely in the boxesprovided. Do not write any messages, credit amounts, orsymbols (+, -, ( ) ) on the returns or vouchers; returns areprocessed by automated equipment. Instead, use Form 163 orwrite to Treasury.UseForm160 if you arepaying all the taxesdue at one timeeither on the 12th or the 20th. If you are paying only part ofyourtax,useForm161.Form161isapaymentformonlyanddoesnotreplacethereturn.Areturnisstillrequiredevenifnotax is due. Complete the form and carefully detach it. Make sure youare sending the form for the correct filing period. Makeyour check payable to the “State of Michigan” and write “SUW” and your account number on your check. Do not fold yourcheckortheform.Mailtheformandchecktotheaddress

printedonthebottomofyourreturnorvoucher.

Combined Return for Michigan Taxes (Form 160)MonthlyandquarterlyfilersnotregisteredtopaybyEFTmustuse this return. (Annual filers and EFT filers do not use thisreturn.)Youarerequiredtofileevenifnotaxisdue.The return and payment are due on or before the 20th of themonth following the taxperiod (monthorquarter). If the20thfallsonaholidayorweekend,theduedateisthefirstbusinessday following the weekend or holiday.Corporate Income Tax (CIT) Estimates. Ifpayingquarterly,CITestimates aredueon the15thof themonth following theend of the quarter. If filing CIT monthly using Form 160 orpayingbyEFT,monthlypaymentsmaybefiledonthe20thdayof themonth. For example, a calendar year taxpayermay filemonthlyCITestimatesusingForm160onFebruary20,March20, and April 20 rather than a single quarterly payment onApril15providedthecombinedestimatesforthosemonthsarecalculatedusingtheinstructionsprovided.Filing InstructionsWhen you file the paper return, complete only one form andwriteasinglecheckfor the totalsales,use,withholding taxes,andCITdueusingthefollowinginstructions:Sales Tax.Enteramountfromworksheetline10B.

5

Sales Tax Discount. Enter amount fromworksheet line 11B.Besuretoincludeanydiscountyoumayhavetakenifyoufiledavoucherbythe12th.Use Tax (sales/rentals). Enter amount from worksheet line10A.Use Tax Discount.Enteramountfromworksheetline11A.Besuretoincludeanydiscountyoumayhavetakenifyoufiledavoucherbythe12th.Use Tax (purchases).Enteramountfromworksheetline14b.Michigan Withholding.Enteramountfromworksheetline16.CIT Estimates.Enteramount fromtheworksheet line19 thatyou are paying with this return.Voucher Payment. Enter amount of tax paid early from thetotalpaymentlineofForm161.Thisisnotacreditorsubtotalline.Onlyenteranamounthereifyoufiledbythe12th.Penalty and Interest.Enteramountfromworksheetline18.Total Payment.Entertheamountofyourcheck.For further instruction on completing and mailing Form 160,seepage5.

Discount Voucher for Sales and Use Taxes (Form 161)Form161isonlyusedbyfilerswhopaypartoftheirtaxearlytoobtainadiscount.Ifyoupayallyourtaxearly,useForm160.IfyouuseForm161tomakeanearlypayment,youmuststillfileForm160,evenifyourbalancedueiszero.DonotuseForm161ifyouareamonthlyfilerwhooweslessthan$1,200forthatfilingperiodinsalesorusetax,aquarterlyfiler,orataxpayerwhofilesonceayear.When the tax rate increased from 4 percent to 6 percent, thelaw required all of the 2 percent increase to go to the SchoolAidfund.Theadditional2percentisnotdiscounted.Therefore,

discounts are calculatedusing2/3 (0.6667)of the sales and/orusetaxcollectedatthe6percenttaxrate.Filing Instructions• Onthefirstline(taxamountyouarepayingearly),enterthe

amountofeachtax(salesoruse)youarepayingearly.• If you are paying all your tax (even by the 12th), use the

monthly/quarterlyreturn(Form160).• Onthesecondline,entertheamountofdiscountforeachtax

typethatyoucomputedusingchart2onpage12.• Onthethirdline,subtractthediscountfromtheamountdue

and enter the result.

Notice of Change or Discontinuance (Form 163)Use Form 163 to notify Treasury of any change(s) in youraccount.Youmustreport:• Changeinmailingaddress.• Change in legal business address.• Changeinaccountnumber.ForFederalID(FEIN)change,

attachIRSverification.• Discontinuance of business.• Sale of all or part of a business.• Sale of a business but operating another business.• Changeofownership(e.g.,addingapartneror

incorporating).• Additionordeletionofataxtype(toaddatax,youmustbe registeredwiththeStateofMichigan).• Changeinseasonallyactivemonths.

Annual Return for Sales, Use and Withholding Taxes (Form 165)All sales tax, use tax, and income taxwithholding filersmustfileForm165eachyear,evenifnotaxisdue.Form165istheonly return required frombusinesses thatfileonceayear.Fortaxpayerswho submitmonthly or quarterly returns, Form165balancesthetaxduefortheyearwiththemonthlyorquarterlypaymentsmadeduring theyear.DonotuseForm165 insteadofyourmonthlyorquarterlyreturn.Form165andpaymentaredueFebruary28.No extensionsaregrantedforfilingForm165.SeeAnnualReturnaddressesonpage16.

If You Don’t Have Monthly/Quarterly ReturnsNot having returns does not relieve your obligation topay timely. Pre-identified returns have been mailed foryour account and should be used when available. If a pre-identified return is not available, Form 160 is availableat www.michigan.gov/taxes. Instructions and a mailingaddress will be provided once the form is accessed online. IfInternetaccess isunavailable, sendyourpaymentwitha letterincluding your name, address, telephone number, accountnumber, return period, and amount of each tax and paymentinvolved. See Combined Return addresses on page 16.Ifyoudonothavepre-identifiedreturns,youshould includeawritten request with your mailing, or contact the RegistrationUnitat (517)636-6925forasetofpre-identifiedreturns tobemailedtoyou.

Completing and mailing your Combined Return (Form 160):1. Enter taxduefigureswhencompletingForm160.Gross

salesfiguresarereportedontheannualreturnonly.2. Figures entered on Form 160 must correspond to the

descriptionprovidedforthattaxline.3. SubtotalamountsmustnotbeenteredonForm160.4. Account information changes must not be requested on

Form160.FileForm163torequestaccountchanges.5. A Form 160 must be submitted for each filing period

required according to your filing status. This includesreturnperiodsthathavezerodueornoactivity.

6. Payment for the CIT estimate must be enclosed withForm160ifreportingyourCITestimateonthatform.

7. Alldiscountsmustbecalculatedandreportedcorrectly.8. Appropriate pre-identified return is used for the filing

period indicated on that return.9. Negative/creditfiguresmustnotbeenteredonthereturn.10.Enclosepaymentwithreturnifanamountisdue.11.Youraccountnumbermustbewrittenonyourcheck.12. Do not report or pay your Michigan Flow-Through

WithholdingonForm160.

6

late or Insufficient PaymentReturnsfiled lateorwithoutpaymentof taxduearesubject topenaltyandinterest. Instructionsfor line18onthemonthlyorquarterlyworksheet explainhow tofigurepenalty and intereston those returns. Form 165 instructions for line 26 explainhowtofigurepenaltyandinterest.Additionalpenaltiesmaybechargedforfailingtomeetstatutoryrequirements.Ifyour return isnotfiled,Treasurywill estimateyour taxandbillyou.Also,latefilingofareturnmayresultinanimmediateassessment and legal action may be taken to collect unpaidtaxes,penalty,andinterest.Legal action may include filing liens on real and personalproperty, levying on bank accounts or receivables, seizureand sale of assets, and cancellation of your sales tax license.Businessownersandcorporateofficersmaybeheldpersonallyresponsible for unpaid taxes.Accelerated,monthly, and quarterly taxpayerswho fail to fileForm165aresubjecttoapenaltyof$10perdayfromtheduedateuntilthereturnisfiled.Maximumpenaltyis$400.

Sales Tax licenseSales tax licenses are renewed annually unless discontinued by the taxpayer or by Treasury. The sales tax license is non-transferable.Youmay not use the sales tax license to purchase goods andsuppliesforyourownuse.Seepage3forusetaxinformation.Sales tax licensees who buy goods for resale must furnishtheir supplierswith a completedMichigan Sales and Use Tax Certificate of Exemption(Form3372)containingtheirsalestaxlicensenumberorprovidethesameinformationtothesellerinanotherformat.

Taxpayer’s Account NumberIf you had an FEIN when you registered, your Michigantaxpayer account number is your FEIN. If you did not havean FEIN when you registered, you were assigned a Treasury(TR) number. The TR number is temporary, you must notifyTreasurywhenyougetyourFEIN.Youmay have an FEIN and also have been assigned anMEnumber(s)byTreasury.Keepyouractivetaxaccountsaccuratebyfilingseparatereturnsforeachaccountnumber.

Amended Monthly/Quarterly ReturnsNOTE:Form160isusedtoamendperiodsinthecurrentyear.UseForm165toamendpreviousyears.FillableForms160and165areavailableatwww.michigan.gov/businesstax.If an amendment for the current year results in additional taxdue, complete a blank returnwith the corrected figures, write“amendedreturn”onthetopoftheform,andsendyourreturnandpaymenttotheaddresslistedontheform.Provideawrittenexplanation for the amendment, include your account numberand filing period, and mail to the Treasury Correspondenceaddresslocatedonpage16.If the amendment results in a credit within the current year,do not change the figures on the return for the period beingamended. Carry the credit forward on your worksheet andreduce the tax due on the monthly/quarterly return. Continue

untilyouhaveanamountdueandenterandpaytheamountonthenextmonthly/quarterlyreturnfiled.DonotenteranegativeamountonForm160,as thescanningequipmentreadsallentriesastaxdue.Seemonthlyorquarterlyworksheetinstructionsforline21.Iftheamendmentresultsinacreditcarriedforwardtothenextyear,useForm165.Treasurywillnotifyyouwhenyourcreditisavailable.

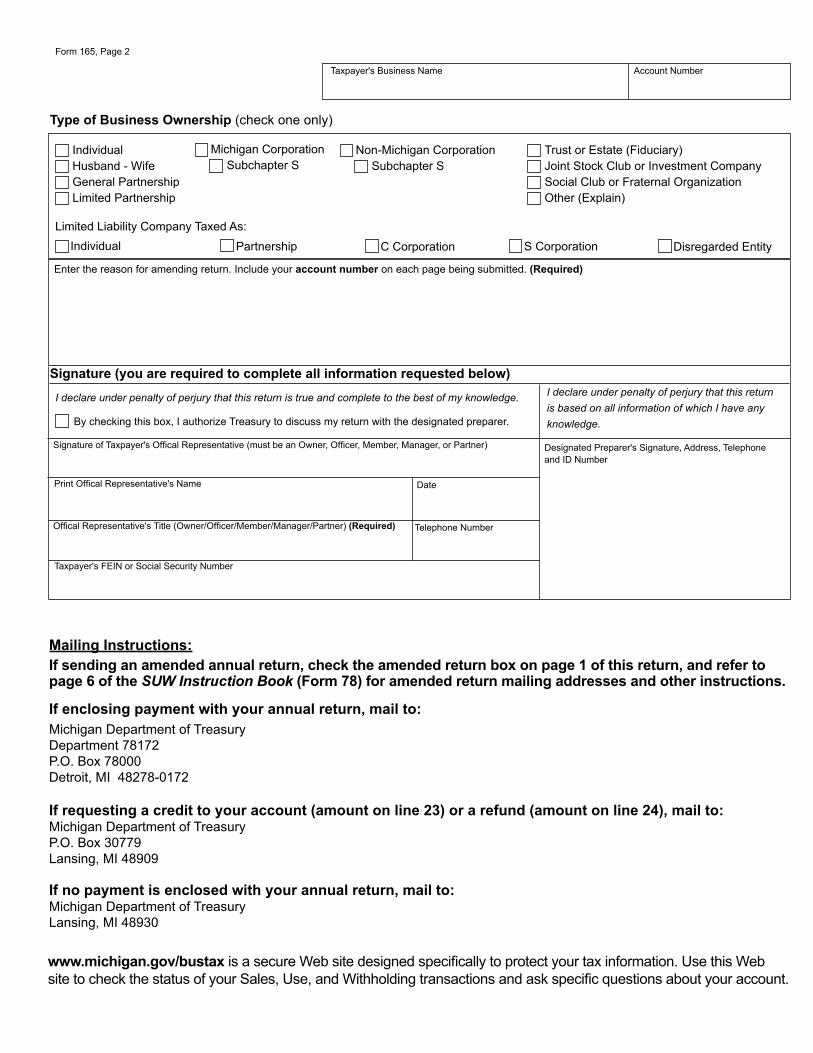

amended annual returnsNOTE: Form 165 is used to amend a previous year’s return.Form160 isused toamendperiods in thecurrentyear.Forms160and165areavailableatwww.michigan.gov/businesstax.To amend Form 165 for a previous year, complete the returnwiththecorrectedfigures.Checkthe“AmendedReturn”boxonpage1andindicatethedateamended.Onpage2ofForm165,writeanexplanationfortheamendment.If the amendment results in additional tax due, send youramendedannualreturnandpaymentto:See Amended Annual Returns on page 16.

Correcting W-2 ErrorsIf theerrorwasformorewithholdingthanwasontheoriginalW-2, issue a correctedW-2 and send a copy to Treasury. Asprovided inRule 206.33(3)(b), the employer can only receivea refund if the originalW-2 is recovered from the employee.When an employee retains the original, erroneous W-2, theemployee, not the employer, must request the refund. Thecorrected form should be clearly marked “Corrected byEmployer.”If the errorwas for lesswithholding thanwas on the originalW-2,donotissueacorrectedW-2.Thistypeofcorrectionmustbehandledinoneofthefollowingways(1979AC,R206.22):

1)Theemployermayrepaytheamountwithheldinerrortothe employee anytimewithin the same calendar year. Theemployershallobtainareceiptfromtheemployeeandkeepin his records. The employer may adjust his records anddeducttheamountrefundedfromthetaxowingonhisnextreturn,oraskforacashrefund.2) If the employer does not repay the employee as notedabove, the employee may claim a credit for the amountwithheld on their individual income tax return (FormMI-1040).

If an issued W-2 is lost or destroyed, give the employee asubstitutecopyclearlymarked“ReissuedbyEmployer.”Note: If thewithholding error occurs before aW-2 is issued,adjust a later paycheck andmake the same adjustment in thenextpaymentduetoTreasury.

gasoline Retailers and WholesalersComplete Form 160 or 161 first; then carry forward yourpayment figure to aFuel Retailer Supplemental Report (Form2189) or toFuel Supplier and Wholesale Distributor Prepaid Sales Tax Report(Form429),andcomplete.Attach your supplemental report to your return. Write yourbusinessnameandaccountnumberonallsupplementalreportsto ensure proper credit for prepaid sales tax on fuel.Thecreditwillreducetheamountoftaxyouwillpaywithyour

7

monthly or quarterly tax returns. If you have a start-up loanfromDecember1983,youmayapplyanycreditaboveyourtaxdueoryoumaycomplete aRefund Request for Prepaid Sales Tax on Gasoline (Form 3891). When preparing Form 165,include the fuel retailer and wholesaler prepayments on line13b.

Seasonal TaxpayersSeasonal businesses must file a Combined Return (Form160)monthly for each of the seasonally activemonths shown on your returns, even if no tax is due. If you have sales or pay wages during the months your business is normally closed, download Form 160 (Combined Return) at michigan.gov/taxes,andsubmititfortheappropriatemonth(s).

Returns Due After Selling or Quitting BusinessAll taxpayersmust submit a finalmonthly or quarterly returnwithin 15 days after the date of selling or quitting business.YourfinalannualreturnisduebyFebruary28.ContacttheTaxClearanceUnitat(517)636-5260toconfirmalldebtshavebeensatisfied.

Instructions and WorksheetsThis booklet includes instructions and worksheets to calculate yourtaxdueandpreparereturnsforsales,use,andwithholdingtaxes.Most taxpayerscollectandpay taxat the6percent rateanddon’tneedaworksheetwitha4percentcolumn.Taxpayerswhostillcollectatthe4percentratewillreceiveadifferentsetofworksheetsandanannualreturnwithboththe4percentand6percentcolumns.Ifyoudon’treceivetheworksheetsandneedthem,contactCustomerServiceat(517)636-6925.Keep the completed worksheets for your records and forpossible audit.Do not file yourworksheet in place of filing amonthly, quarterly, or annual return. Filing the wrong formdelayscreditinginformationandpaymentstoyouraccount.

general Instructions – Annual Return (Form 165) filing requirementsYou must file Form 165 if you are registered for sales tax,use tax, or income tax withholding in the State ofMichigan.MonthlyandquarterlyfilersmustfileForm165onacalendar-yearbasis(notyourfiscalyear).Taxpayers who had multiple active account numbers (TR,

ME, and/or FEIN) in a tax year are required to file separateannual returns for each account number assigned. Identify theregistered tax types foreachaccountnumberand includeonlythose tax figures on the corresponding annual return. If youhave an outside payroll or accounting agency, coordinate thisfilingresponsibilitywiththem.Ifduringtheyearyouraccumulatedsales,use,andwithholdingtaxesbecome$750ormore,youmustnotifyTreasurytochangeyour filing status and provide you with the appropriate taxreturns.Form 165 must be signed and dated by the taxpayer. Thetaxpayermust also include their title.Thismaybe the owner,officer,member,manager,orpartner.Nootherpersonmaysignfor the taxpayer in the taxpayer’s signature box.

W-2 Wage and Tax StatementsYoumustfurnishW-2statementstoyouremployeesbyJanuary31.Refer to“CorrectingW-2Errors”onpage6 foramendingW-2statements.Employers with Michigan employees must report W-2informationtoMichiganonorbeforeFebruary28byenclosingW-2formswithForm165.Payers reportingMichiganwithholdingona1099-Rmustalsoenclose those 1099-R formswith Form 165.See page 16 for Annual Return (Form 165) and W-2 mailing information. Aform1099-MISCmustbefiledformiscellaneousincomeforservices performed in theState ofMichigan, regardless of thestateofresidenceof thepayee,whether therewaswithholdingor not. Taxpayers not registered for withholding should filecorrespondencewiththebusinessaccountnumberandmailto:

MichiganDepartmentofTreasury Lansing,MI48930

Ifyouhave250ormoreMichiganemployees,youmustreportusingmagneticmedia. Ifyouhave fewer than250employees,youmayreportusingmagneticmediaorusingtheStatecopyofthefederalW-2.SeeForm447forinformationaboutmagneticmediareporting.Addressyourmagneticmediato:

MichiganDepartmentofTreasury BusinessTaxesDivision MagneticMediaUnit-SUW Lansing,MI48930

ANNUAl RETURN (FoRM 165): lINE-BY-lINE INSTRUCTIoNSLines not listed are explained on the form.

IMPORTANT: This is a return for Sales Tax, Use Tax,andWithholding Tax. If the taxpayer inserts a “zero” on (orleaves blank) any line for reporting Sales Tax, Use Tax, orWithholding Tax, the taxpayer is certifying that no tax isowedforthattaxtype.If it isdeterminedthattaxisowed,thetaxpayerwillbeliableforthedeficiencyaswellaspenaltyandinterest.NOTE: Ifyoupayonlyincometaxwithholdingorfileannuallyanddonot havedeductions, use the simplified instructions onpage8.

Sales and Use TaxLines 1 through 9: Monthly and quarterly filers, in each

column add the entries from all your worksheets for the yearandenterthetotalsonthecorrespondinglineonForm165.Taxpayerswhofileannually,followtheline-by-lineinstructionsforthemonthlyandquarterlyworksheet,beginningonpage11.Line 11:Monthlyandquarterlyfilers,enterthetotaldiscountsallowedfortheyearineachcolumn.Totaltheamountsfromthemonthlyorquarterlyworksheetline11ineachcolumn.Includediscounts from Form 2189 and Vehicle Dealer Supplemental Report(Form92).Taxpayersfilingannuallyreceiveadiscountifthereturnisfiledtimely. The discount applies only to 2/3 (0.6667) of the salesand/orusetaxcollectedatthe6percenttaxrate.UseChart1onpage8tofigureyourdiscount.

8

If you opened for business late in the year or ended yourbusinessearlyintheyear,the$6permonthdiscountisallowedonly for the months you were in business. No discount isallowedifthereturnisfiledafterFebruary28.Line 13:Enterthetotalamountofeachtaxpaidafterdiscountsduring the report year. Include the amount from your fuelretailer or fuel supplier and wholesale reports. Do not include anypenaltiesor interestpaid.This amount shouldbe the totalof all payments for the year from your monthly/quarterlyworksheet,line12.

Use Tax on Purchases or Inventory WithdrawalLine 14:Enterpurchaseswhichweretaxable.Multiplyby0.06andenterthetaxdueonline14b.Line 15: Enter the use tax on purchases or inventorywithdrawal paid during the year. This amount should be thetotalofallpayments for theyear fromyourmonthly/quarterlyworksheetline14b.

Income Tax WithholdingLine 16:Enter yourgrossMichiganpayroll andother taxablecompensationfortheyear.Line 17: Enter the number of W-2 statements, 1099-MISCs,1099-Rs,plusother1099swithMichiganwithholdingyouaresubmittingfortheyear.Line 18:Enter the totalMichigan incometaxwithheldfor theyearasshownontheW-2and1099-MISCstatements.Line 19: Enter the total Michigan income tax withheld thatwaspaidonyourmonthlyorquarterlyreturns.Thisshouldbethetotalofline16onallyourworksheetsfortheyear.(Donotinclude penalty and interest.)

SummaryLine 22: If line21(taxpaid) isgreater than line20(taxdue),enterthedifference(overpayment)here.Line 23: Enter the amount of the overpayment you wantappliedtoyourmonthlyorquarterlyreturn.Treasurywillnotifyyouwhenyourcreditisavailable.Line 24: Enter the amount of overpayment from line 22 youwantrefundedtoyou.Refundswillnotbemadeinamountsoflessthan$1.Line 25:Ifline21(taxpaid)islessthanline20(taxdue),entertheadditionaltaxdue.Payanyamountof$1ormorewiththisreturn.Line 26:Ifyourreturnislate,computethepenaltyandinterestdue.Ifnotaxisdueonline25,thepenaltyis$10perdaytoamaximumof$400.Ifyouhaveataxdueonline25,thepenaltyisasfollows:• 5 percent of the tax due (line 25) if the late payment isreceivedwithintwomonthsoftheduedate.

• 5percentof the taxdue for each subsequentmonth,orpartthereof,thetaxisnotpaid.

• Maximumpenaltyis25percentoftaxdue.• Interestisdueattherateof1percentabovetheprimeinterestratefromthedaythetaxisdueuntilitispaid.TheprimeratewillbeadjustedJanuary1andJuly1.

• A penalty and interest calculator is available on Treasury’sWeb site at www.michigan.gov/taxes.

Line 27: Amount due with this return. Add lines 25 and 26.Make check payable to the “State of Michigan.” Write your account number and “SUW” on your check. Do not pay if the amountdueislessthan$1.

ANNUAl RETURN (Form 165) – Simplified Instructions for Annual Filers With No DeductionsIf you file annually (no quarterly or monthly payments) andhave no allowable deductions, use the instructions below tocompleteForm165faster.Ifyouarenotregisteredforsalesorusetax,skiptostep9.Step 1: Completelines1through4.Step 2: Carryamountfromline4toline6.Step 3: Multiply the amount on line 4 by the tax rate (6percent)andentertheresultonline8.Step 4: Enteronline9anyamountyoucollectedinexcessofline 8.For example, if you entered$40on line 8 but actuallycollected$50,enter$10online9.Step 5: Addlines8and9andenteronline10.Step 6: Line11 isyourdiscountamount.YouareeligibleforadiscountifyoupaythetaxduebyFebruary28.Thediscountappliesonlyto2/3(0.6667)ofthesalesand/orusetaxcollectedatthe6percenttaxrate.UseChart1tofigureyourdiscountandenteritonline11.Ifyouwereonlyopenpartoftheyear,multiplythenumberofmonthsyouwereopenby$6.Comparethatagainstthediscountamountyoufigured inChart1.Enter the smallerof these twonumbersonyourworksheet,line11.Step 7: Unlessyoupaidtaxduringtheyear,line13shouldbezero.Step 8: Ifyouboughtanygoodsduringtheyearfromanout-of-statevendoranddidnotpaysalestaxonthemorifyoutookitems from inventory for personal or business use, completelines14and15.Seepage3formoredetailsabouttheusetax.Step 9: Ifyouhaveemployees,completelines16through19.Ifyouhavenoemployees,enterzeroonline19.Step 10:Summary.Completelines20and21.Enterthedifferenceonline25.Ifpayinglate,enteranypenaltyorinterestdueonline26andtotalyouramountdueonline27.Make your check payable to the “State of Michigan.” Write your account number and “SUW”onyourcheck. IfyouarefilingForm165withanyotherremittanceform,sendaseparatecheck for each form. See page 16 for Annual Returnmailinginformation.Retainacopyforyourrecords.

Chart 1 - If your tax due is $108 or more, enter $72 on worksheet, line 11. If your tax due is less than $108, figure your discount below.

Amountoftaxdue ........................... $x0.6667

DiscountAmount= $Enteronworksheet,line11.

Sales and Use Tax

Use Tax on Items Purchased for Business or Personal Use *

Withholding Tax

Summary

Gross sales (including sales by out-of-state vendors subject to use tax) ......Rentals of tangible property and accommodations .......................................Telecommunications services ........................................................................Add lines 1, 2, and 3 .....................................................................................

Resale ...........................................................................................................Industrial processing or agricultural producing ..............................................Interstate commerce ......................................................................................Exempt services ............................................................................................Sales on which tax was paid to Secretary of State........................................Food for human/home consumption ..............................................................Bad debts ......................................................................................................Michigan motor fuel or diesel fuel tax ............................................................Other. Identify: ____________________________ ......................................Tax included in gross sales (line 1)................................................................Total allowable deductions. Add lines 5a - 5j .................................................Taxable balance. Subtract line 5k from line 4 ................................................Tax Rate ........................................................................................................Gross tax due. Multiply line 6 by line 7 ..........................................................Tax collected in excess of line 8 ....................................................................Add lines 8 and 9 ...........................................................................................TOTAL discount allowed (see instructions) ..............................................Total tax due. Subtract line 11 from line 10 ....................................................Tax payments in current year (after discounts)..............................................

Enter your taxable purchases ........................................................Tax payments made in the current year .............................................................................................................

Gross Michigan payroll, pension, and other taxable compensation for the year ................................................Number of W-2, and 1099 forms enclosed .......................................Total Michigan income tax withheld per W-2 and 1099 forms ............................................................................Total Michigan income tax withholding paid during current tax year ..................................................................

Total sales, use and withholding taxes due. Add lines 12A, 12B, 14b and 18 ....................................................Total sales, use and withholding taxes paid. Add lines 13A, 13B, 15 and 19 .....................................................If line 21 is greater than line 20, enter overpayment ........................Amount of line 22 to be credited forward on your account.We will notify you when your credit is verified and available .............Amount of line 22 to be refunded to you............................................If line 21 is less than line 20, enter balance due.................................................................................................If this return is filed late, enter penalty and interest. (See instructions.) .............................................................TOTAL PAYMENT DUE. Add lines 25 and 26. Make check payable to "State of Michigan." ..........................

Michigan Department of Treasury165 (Rev. 07-13)

Taxpayer's Business Name Account Number

Return Year Date Due

1.2.3.4.

5a.b.c.d.e.f.g.h.i.j.

k.6.7.8.9.

10.11.12.13.

1.2.3.4.

5a.b.c.d.e.f.g.h.i.j.

k.6.7.8.9.

10.11.12.13.

A. Use Tax: Sales & Rentals B. Sales Tax

6% 6%

File this return by February 28. Do not use this form to replace a monthly or quarterly return.

Annual Return for Sales, Use and Withholding TaxesIssued under authority of Public Act 167 of 1933.

x .06 =

x .06 x .06

14a..

17.

22.

23.24.

1.2.3.4.

a.b.c.d.e.f.g.h.i.j.

k.6.7.8.9.

10.11.12.13.

14.15.

16.17.18.19.

20.21.22.23.

24.25.26.27.

Amended ReturnAmendment Date

Check box if this is an amended return.

* Use Tax on Items Purchased for Business or Personal Use: Use lines 14 and 15 to report purchases made for use in your business or for items removed from your inventory for personal or business use. Do not repeat the amounts from Column A, lines 1 - 4 here.

5. ALLOWABLE DEDUCTIONS

14b.15.

16.

18.19.

20.21.

25.26.27.

IndividualHusband - WifeGeneral PartnershipLimited Partnership

Type of Business Ownership (check one only)

Non-Michigan CorporationSubchapter S

Trust or Estate (Fiduciary)Joint Stock Club or Investment CompanySocial Club or Fraternal OrganizationOther (Explain)

Mailing Instructions:If sending an amended annual return, check the amended return box on page 1 of this return, and refer to page 6 of the SUW Instruction Book (Form 78) for amended return mailing addresses and other instructions.

If enclosing payment with your annual return, mail to:Michigan Department of Treasury Department 78172P.O. Box 78000Detroit, MI 48278-0172

If requesting a credit to your account (amount on line 23) or a refund (amount on line 24), mail to:Michigan Department of TreasuryP.O. Box 30779Lansing, MI 48909

If no payment is enclosed with your annual return, mail to:Michigan Department of TreasuryLansing, MI 48930

Signature (you are required to complete all information requested below)

Form 165, Page 2

www.michigan.gov/bustax is a secure Web site designed specifically to protect your tax information. Use this Web site to check the status of your Sales, Use, and Withholding transactions and ask specific questions about your account.

I declare under penalty of perjury that this return is true and complete to the best of my knowledge.

Date

By checking this box, I authorize Treasury to discuss my return with the designated preparer.

I declare under penalty of perjury that this return is based on all information of which I have any knowledge.

Signature of Taxpayer's Offical Representative (must be an Owner, Officer, Member, Manager, or Partner)

Taxpayer's FEIN or Social Security Number

Offical Representative's Title (Owner/Officer/Member/Manager/Partner) (Required)

Designated Preparer's Signature, Address, Telephone and ID Number

Telephone Number

Taxpayer's Business Name Account Number

Enter the reason for amending return. Include your account number on each page being submitted. (Required)

Partnership S Corporation

Print Offical Representative's Name

C Corporation Disregarded EntityIndividualLimited Liability Company Taxed As:

Michigan CorporationSubchapter S

11

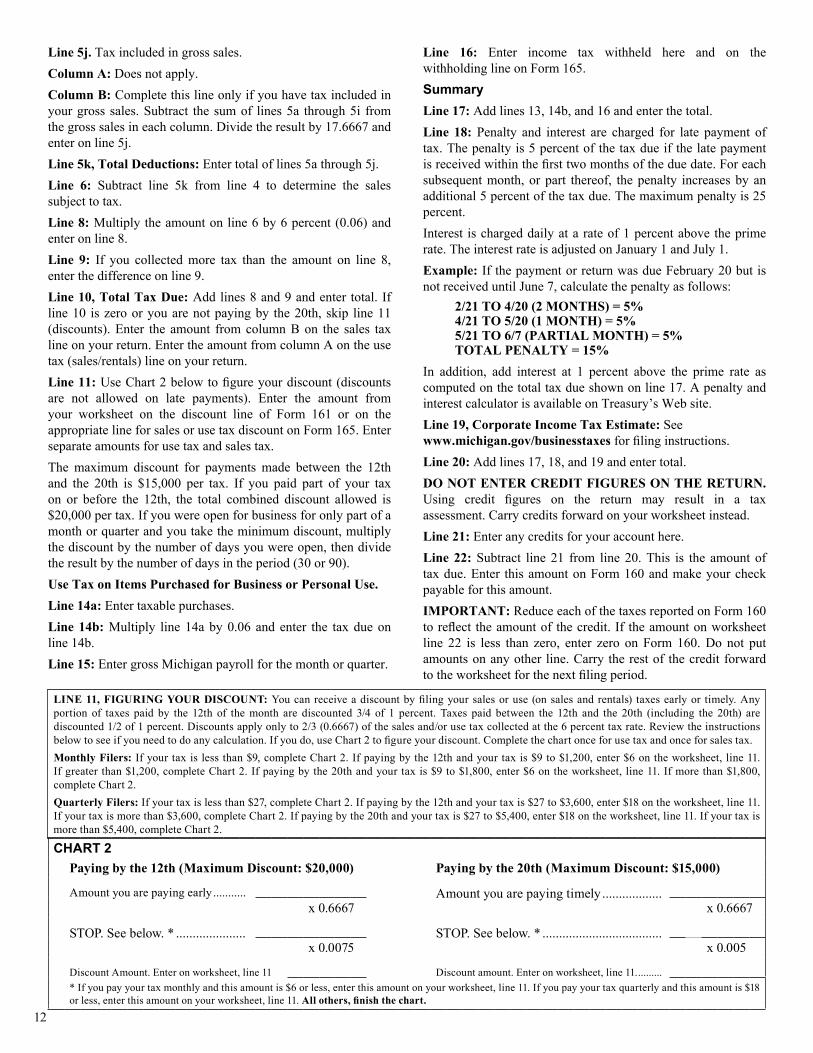

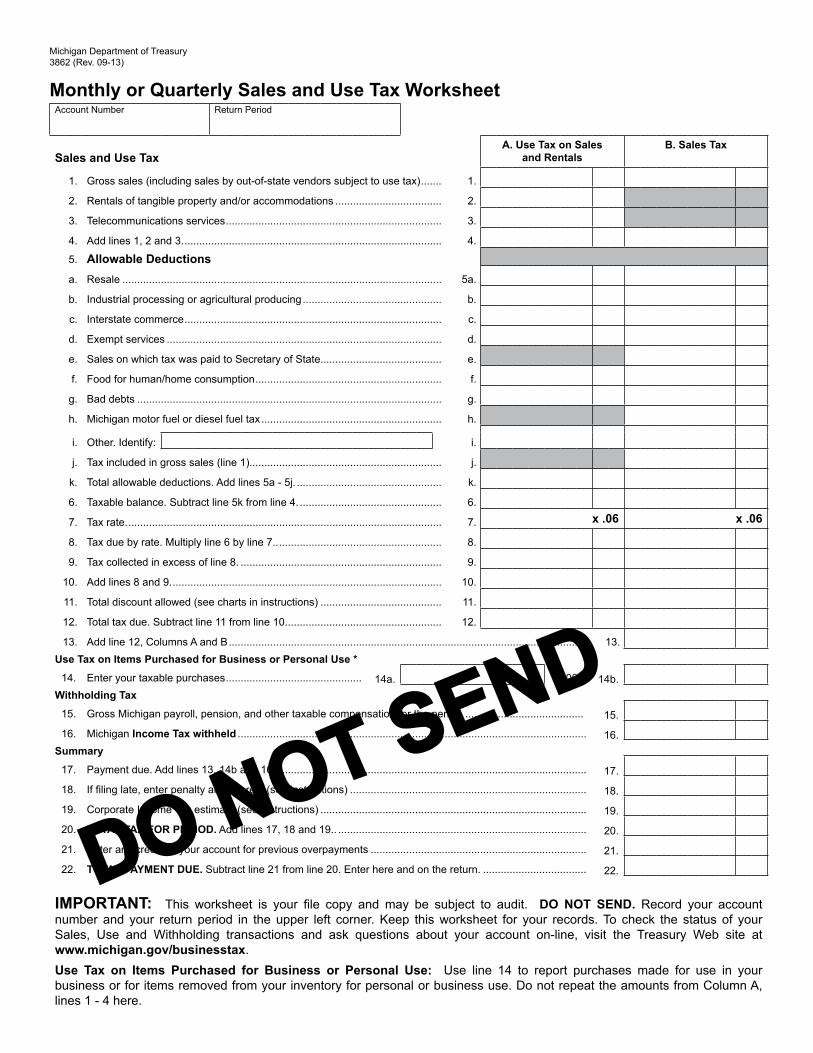

MoNTHlY AND QUARTERlY WoRkSHEETS (FoRM 3862): lINE-BY-lINE INSTRUCTIoNS

Begin on line 15 if filing withholding only. Columns notreferencedonspecificlinesindicatetheyarenotapplicable.Seeinstructionsonpage7ifyoufileannually.Line 1, Gross Sales: Any costs incurred before ownership of the property is transferred to the buyer (including shipping,handling,anddeliverycharges)arenotconsideredservicesandaresubjecttotax.Column A, Use Tax on Sales and Rentals: This line is for out-of-stateretailerswhodonothaveretailstoresinMichigan.Enter total sales of tangible personal property including cash,credit,andinstallmenttransactions.Column B, Sales Tax: Enter total of all sales of tangible personal property including cash, credit, and installmenttransactions.Line 2, Rentals, Column A: Lessors of tangible personalpropertywho pay use tax on rental receiptsmust enter rentalincome.Alsoentertotalhotelandmotelroomrentalsincludingassessments imposed under the Convention and TourismAct, the Convention Facility Development Act, the RegionalTourism Marketing Act, or the Community Conventionor Tourism Marketing Act. See Line 5i for instructions ondeductingtheassessmentsfromrentals.Line 3, Telecommunications Services, Column A: Enter grossincomefromtelecommunicationsservices.Allowable Deductions: Uselines5a-5j todeductnontaxablesales you made from gross sales. Deductions taken for taxexemptsalesmustbesubstantiatedinyourrecords.Forlines5aand5b,aswellasitems3through5underline5iinstructions,youmustobtainacompletedcopyofForm3372,or thesameinformationinanotherformat,fromthepurchaser.Line 5a, Resale: Enter sales which will be resold to others.Line 5b, Industrial Processing/Agricultural Producing: The property sold must be for direct use in producing a productfor eventual sale AT RETAIL OR TO BE AFFIXED TOANDMADE A STRUCTURAL PART OF REAL ESTATELOCATEDINANOTHERSTATE.Line 5c, Interstate Commerce:Entersalesmade in interstatecommerce.Toclaimsuchadeduction, thepropertyor servicemustbedeliveredbyyoutotheout-of-statepurchaser.Propertytransported out of state by the purchaser does not qualify under interstate commerce. You must keep documentation ofshipmentout-of-statetosupportthisdeduction.Line 5d, Exempt Services: Enter charges for nontaxable services billed separately, such as repair or maintenance, ifthese charges were included in gross receipts on line 1. Anycosts incurred before the property is transferred to the buyer (including shipping, handling, and delivery charges) are notconsideredservicesandaresubjecttotax.Line 5e, Tax Paid to the Secretary of State, Column B: Enter salesbylicensedvehicledealers(notincludingtax)ofvehiclesandmobilehomesonwhichyoupaidsalestaxtotheSecretaryof State.

Line 5f, Food for Human/Home Consumption: Enter total of retail sales of grocery-type food, excluding tobacco andalcoholicbeverages.Preparedfoodissubjecttotax.Line 5g, Bad Debts: You may deduct the amount of baddebts from your proceeds if the debts are charged off asuncollectible on your books and records at the time the debtsbecome worthless and you have deducted the debts on yourreturn for a period during which the bad debts are written off as uncollectible.Thedebtmustalsobeeligibletobedeductedforfederal income taxpurposes.EffectiveOctober1,2009, abaddebtdeductionmaybeclaimedbyathird-partylenderprovidedthe retailer who reported the tax and the lender financing thesale executed and maintained a written election designatingwhich party may claim the deduction. Certain additionalconditionsmustbemet.SeeMCL205.54iandMCL205.99a.Line 5h, Michigan Motor Fuel or Diesel Fuel Tax, Column B: MotorfuelretailersmaydeducttheMichiganmotorfueltaxesthatwereincludedingrosssalesonline1andpaid to the State or the distributor.Line 5i, Other Deductions: Identifydeductionsnotcoveredinitems5athrough5honthisline.Examplesofdeductionsare:• Assessments imposed under the Convention and TourismAct,theConventionFacilityDevelopmentAct,theRegionalTourism Marketing Act, or the Community Convention orTourismMarketingAct. Hotels andmotelsmay deduct theassessmentsincludedingrosssalesandrentalsprovidedusetaxontheassessmentswasnotchargedtothecustomers.

• Credits allowed to customers for sales tax originally paidon merchandise voluntarily returned; provided the returnis made within the time period for returns stated in thetaxpayer’s refund policy or 180 days after the initial sale,whichever is earlier. Repossessions are not allowabledeductions.

• Direct sales to the United States Government, State ofMichigan, or its political subdivisions. Direct sales notfor resale to certain nonprofit agencies, churches, schools,hospitals, and homes for the care of children and the aged,providedsuchactivitiesarenonprofitandpaymentisdirectlyfromthefundsoftheexemptorganization.

• Sales to contractors of materials which will become partof a finished structure for a qualified exempt nonprofithospital,qualifiedexemptnonprofithousingentityorchurchsanctuary.ThepurchaserwillprovideaMichigan Sales and Use Tax Contractor Eligibility Statement (Form 3520). SeeRAB1999-2.

• Sales to companies that claim direct payment of use tax totheStateofMichigan.Suchcompaniesmusthaveasalestaxlicenseorusetaxregistration,andhavealetterfromTreasuryspecificallygrantingdirectpaymentauthority.

• Qualified nonprofit organizations may take a deduction oftheirsalesiftotalsalesarelessthan$5,000andtheydidnotcollectsalestaxfromtheircustomers.Iftotalsalesare$5,000or more, the entire amount of sales is subject to tax. Forqualifications,seeRAB1995-3.

12

Line 5j. Tax included in gross sales. Column A: Does not apply. Column B:Completethislineonlyifyouhavetaxincludedinyourgross sales.Subtract thesumof lines5a through5i fromthegrosssalesineachcolumn.Dividetheresultby17.6667andenteronline5j.Line 5k, Total Deductions:Entertotaloflines5athrough5j.Line 6: Subtract line 5k from line 4 to determine the salessubjecttotax.Line 8:Multiplytheamountonline6by6percent(0.06)andenteronline8.Line 9: If you collectedmore tax than the amount on line 8,enterthedifferenceonline9.Line 10, Total Tax Due:Addlines8and9andenter total.Ifline10 iszerooryouarenotpayingby the20th, skip line11(discounts).Enter the amount fromcolumnBon the sales taxlineonyourreturn.EntertheamountfromcolumnAontheusetax(sales/rentals)lineonyourreturn.Line 11:UseChart2belowtofigureyourdiscount(discountsare not allowed on late payments). Enter the amount fromyour worksheet on the discount line of Form 161 or on theappropriatelineforsalesorusetaxdiscountonForm165.Enterseparateamountsforusetaxandsalestax.Themaximum discount for paymentsmade between the 12thand the 20th is $15,000 per tax. If you paid part of your taxon or before the 12th, the total combined discount allowed is$20,000pertax.Ifyouwereopenforbusinessforonlypartofamonthorquarterandyoutaketheminimumdiscount,multiplythediscountbythenumberofdaysyouwereopen,thendividetheresultbythenumberofdaysintheperiod(30or90).Use Tax on Items Purchased for Business or Personal Use.Line 14a: Enter taxable purchases.Line 14b: Multiply line14aby0.06 andenter the taxdueonline14b.Line 15:EntergrossMichiganpayrollforthemonthorquarter.

Line 16: Enter income tax withheld here and on thewithholdinglineonForm165.SummaryLine 17:Addlines13,14b,and16andenterthetotal.Line 18: Penalty and interest are charged for late payment oftax.Thepenaltyis5percentofthetaxdueifthelatepaymentisreceivedwithinthefirsttwomonthsoftheduedate.Foreachsubsequentmonth,orpart thereof, thepenalty increasesbyanadditional5percentofthetaxdue.Themaximumpenaltyis25percent. Interest ischargeddailyatarateof1percentabovetheprimerate.TheinterestrateisadjustedonJanuary1andJuly1.Example:IfthepaymentorreturnwasdueFebruary20butisnotreceiveduntilJune7,calculatethepenaltyasfollows:

2/21 TO 4/20 (2 MONTHS) = 5%4/21 TO 5/20 (1 MONTH) = 5%5/21 TO 6/7 (PARTIAL MONTH) = 5%TOTAL PENALTY = 15%

In addition, add interest at 1 percent above the prime rate ascomputedonthetotaltaxdueshownonline17.ApenaltyandinterestcalculatorisavailableonTreasury’sWebsite.Line 19, Corporate Income Tax Estimate: See www.michigan.gov/businesstaxesforfilinginstructions.Line 20:Addlines17,18,and19andentertotal.DO NOT ENTER CREDIT FIGURES ON THE RETURN. Using credit figures on the return may result in a taxassessment.Carrycreditsforwardonyourworksheetinstead.Line 21: Enter any credits for your account here.Line 22: Subtract line21 from line20.This is the amount oftaxdue.Enter thisamountonForm160andmakeyourcheckpayableforthisamount.IMPORTANT:ReduceeachofthetaxesreportedonForm160toreflect theamountof thecredit.If theamountonworksheetline 22 is less than zero, enter zero on Form160.Do not putamountsonanyotherline.Carrytherestof thecreditforwardtotheworksheetforthenextfilingperiod.

LINE 11, FIGURING YOUR DISCOUNT:Youcan receiveadiscountbyfilingyoursalesoruse (onsalesand rentals) taxesearlyor timely.Anyportion of taxes paid by the 12th of themonth are discounted 3/4 of 1 percent. Taxes paid between the 12th and the 20th (including the 20th) arediscounted1/2of1percent.Discountsapplyonlyto2/3(0.6667)ofthesalesand/orusetaxcollectedatthe6percenttaxrate.Reviewtheinstructionsbelowtoseeifyouneedtodoanycalculation.Ifyoudo,useChart2tofigureyourdiscount.Completethechartonceforusetaxandonceforsalestax.Monthly Filers: Ifyourtaxis lessthan$9,completeChart2.Ifpayingbythe12thandyourtaxis$9to$1,200,enter$6ontheworksheet, line11.Ifgreater than$1,200,completeChart2.Ifpayingbythe20thandyourtaxis$9to$1,800,enter$6ontheworksheet, line11.Ifmorethan$1,800,completeChart2.Quarterly Filers:Ifyourtaxislessthan$27,completeChart2.Ifpayingbythe12thandyourtaxis$27to$3,600,enter$18ontheworksheet,line11.Ifyourtaxismorethan$3,600,completeChart2.Ifpayingbythe20thandyourtaxis$27to$5,400,enter$18ontheworksheet,line11.Ifyourtaxismorethan$5,400,completeChart2.

CHART 2Paying by the 12th (Maximum Discount: $20,000) Paying by the 20th (Maximum Discount: $15,000)

Amountyouarepayingearly ........... Amountyouarepayingtimely ..................x0.6667 x0.6667

STOP.Seebelow.* ..................... STOP.Seebelow.* ....................................x0.0075 x0.005

DiscountAmount.Enteronworksheet,line11 Discountamount.Enteronworksheet,line11. .........*Ifyoupayyourtaxmonthlyandthisamountis$6orless,enterthisamountonyourworksheet,line11.Ifyoupayyourtaxquarterlyandthisamountis$18orless,enterthisamountonyourworksheet,line11.All others, finish the chart.

DO NOT SEND

Michigan Department of Treasury3862 (Rev. 09-13)

Monthly or Quarterly Sales and Use Tax WorksheetAccount Number Return Period

Sales and Use TaxA. Use Tax on Sales

and RentalsB. Sales Tax

1. Gross sales (including sales by out-of-state vendors subject to use tax) ....... 1.

2. Rentals of tangible property and/or accommodations .................................... 2.

3. Telecommunications services ......................................................................... 3.

4. Add lines 1, 2 and 3. ....................................................................................... 4.

5. Allowable Deductionsa. Resale ............................................................................................................ 5a.

b. Industrial processing or agricultural producing ............................................... b.

c. Interstate commerce ....................................................................................... c.

d. Exempt services ............................................................................................. d.

e. Sales on which tax was paid to Secretary of State......................................... e.

f. Food for human/home consumption ............................................................... f.

g. Bad debts ....................................................................................................... g.

h. Michigan motor fuel or diesel fuel tax ............................................................. h.

i. Other. Identify: i.

j. Tax included in gross sales (line 1)................................................................. j.

k. Total allowable deductions. Add lines 5a - 5j. ................................................. k.

6. Taxable balance. Subtract line 5k from line 4. ................................................ 6.

7. Tax rate. .......................................................................................................... 7. x .06 x .06

8. Tax due by rate. Multiply line 6 by line 7.. ....................................................... 8.

9. Tax collected in excess of line 8. .................................................................... 9.

10. Add lines 8 and 9. ........................................................................................... 10.

11. Total discount allowed (see charts in instructions) ......................................... 11.

12. Total tax due. Subtract line 11 from line 10. .................................................... 12.

13. Add line 12, Columns A and B ......................................................................................................................... 13.Use Tax on Items Purchased for Business or Personal Use *

14. Enter your taxable purchases .............................................. 14a. x .06 = 14b.Withholding Tax

15. Gross Michigan payroll, pension, and other taxable compensation for the period. ........................................ 15.

16. Michigan Income Tax withheld ...................................................................................................................... 16.Summary

17. Payment due. Add lines 13, 14b and 16 .......................................................................................................... 17.

18. If filing late, enter penalty and interest (see instructions) ................................................................................ 18.

19. Corporate Income Tax estimate (see instructions) .......................................................................................... 19.

20. TOTAL TAX FOR PERIOD. Add lines 17, 18 and 19.. .................................................................................... 20.

21. Enter any credit on your account for previous overpayments ......................................................................... 21.

22. TOTAL PAYMENT DUE. Subtract line 21 from line 20. Enter here and on the return. ................................... 22.

IMPORTANT: This worksheet is your file copy and may be subject to audit. DO NOT SEND. Record your account number and your return period in the upper left corner. Keep this worksheet for your records. To check the status of your Sales, Use and Withholding transactions and ask questions about your account on-line, visit the Treasury Web site at www.michigan.gov/businesstax.Use Tax on Items Purchased for Business or Personal Use: Use line 14 to report purchases made for use in your business or for items removed from your inventory for personal or business use. Do not repeat the amounts from Column A, lines 1 - 4 here.

DO NOT SEND

Michigan Department of Treasury3862 (Rev. 09-13)

Monthly or Quarterly Sales and Use Tax WorksheetAccount Number Return Period

Sales and Use TaxA. Use Tax on Sales

and RentalsB. Sales Tax

1. Gross sales (including sales by out-of-state vendors subject to use tax) ....... 1.

2. Rentals of tangible property and/or accommodations .................................... 2.

3. Telecommunications services ......................................................................... 3.

4. Add lines 1, 2 and 3. ....................................................................................... 4.

5. Allowable Deductionsa. Resale ............................................................................................................ 5a.

b. Industrial processing or agricultural producing ............................................... b.

c. Interstate commerce ....................................................................................... c.

d. Exempt services ............................................................................................. d.

e. Sales on which tax was paid to Secretary of State......................................... e.

f. Food for human/home consumption ............................................................... f.

g. Bad debts ....................................................................................................... g.

h. Michigan motor fuel or diesel fuel tax ............................................................. h.

i. Other. Identify: i.

j. Tax included in gross sales (line 1)................................................................. j.

k. Total allowable deductions. Add lines 5a - 5j. ................................................. k.

6. Taxable balance. Subtract line 5k from line 4. ................................................ 6.

7. Tax rate. .......................................................................................................... 7. x .06 x .06

8. Tax due by rate. Multiply line 6 by line 7.. ....................................................... 8.

9. Tax collected in excess of line 8. .................................................................... 9.

10. Add lines 8 and 9. ........................................................................................... 10.

11. Total discount allowed (see charts in instructions) ......................................... 11.

12. Total tax due. Subtract line 11 from line 10. .................................................... 12.

13. Add line 12, Columns A and B ......................................................................................................................... 13.Use Tax on Items Purchased for Business or Personal Use *

14. Enter your taxable purchases .............................................. 14a. x .06 = 14b.Withholding Tax

15. Gross Michigan payroll, pension, and other taxable compensation for the period. ........................................ 15.

16. Michigan Income Tax withheld ...................................................................................................................... 16.Summary

17. Payment due. Add lines 13, 14b and 16 .......................................................................................................... 17.

18. If filing late, enter penalty and interest (see instructions) ................................................................................ 18.

19. Corporate Income Tax estimate (see instructions) .......................................................................................... 19.

20. TOTAL TAX FOR PERIOD. Add lines 17, 18 and 19.. .................................................................................... 20.

21. Enter any credit on your account for previous overpayments ......................................................................... 21.

22. TOTAL PAYMENT DUE. Subtract line 21 from line 20. Enter here and on the return. ................................... 22.

IMPORTANT: This worksheet is your file copy and may be subject to audit. DO NOT SEND. Record your account number and your return period in the upper left corner. Keep this worksheet for your records. To check the status of your Sales, Use and Withholding transactions and ask questions about your account on-line, visit the Treasury Web site at www.michigan.gov/businesstax.Use Tax on Items Purchased for Business or Personal Use: Use line 14 to report purchases made for use in your business or for items removed from your inventory for personal or business use. Do not repeat the amounts from Column A, lines 1 - 4 here.

15

oTHER HElPFUl INFoRMATIoNCorporate Income Tax EstimatesOn January 1, 2012 legislation for the Corporate Income Tax(CIT)wasenacted.Visitwww.michigan.gov/businesstaxes for additionalinformation,forms,andfilingrequirements.

Successor liabilityIfyousellyourbusiness,your successormustholdenoughofthe purchase money to satisfy the amount of sales, use, andwithholdingtaxthatmaybedueuntilyouproduceareceiptforpaymentofthetaxfromTreasuryoracertificatefromTreasurystatingnotaxisdue.Ifthesuccessorfailstowithholdsufficientfunds,heorshemaybeheldliableforunpaidtaxes.

officer liabilityOfficers, members, managers, or partners of a corporation,limited liability company, limited liability partnership,partnership, or limited partnership who have responsibilityforfiling returnsormakingpayments arepersonally liable forfailure to file or for unpaid taxes, penalty, and interest underPublicAct169of1982.

Revenue Administrative Bulletins (RAB)An RAB is a directive issued by Treasury. Its purpose isto promote uniform application of tax laws throughout theState and provide information and guidance to taxpayers. AnRAB states the official position of Treasury, has the status ofprecedent in the disposition of cases unless and until revokedor modified, and may be relied on by taxpayers in situationswhere the facts, circumstances, and issues presented aresubstantiallysimilar to thoseset forth in theRAB.A taxpayermustconsidertheeffectsofsubsequentlegislation,regulations,courtdecisions,andRABswhenrelyingonanRAB.SeeRAB1989-34formoreinformation.ToaccessacopyofaparticularRAB,gotowww.michigan.gov/treasury.

Unclaimed Property Reporting for Businesses and government EntitiesMichigan’sUniformUnclaimedPropertyAct,PublicAct29of1995,asamended,requiresbusinessesandgovernmententitiesto report and remit to the Michigan Department of Treasuryabandonedandunclaimedpropertybelongingtoownerswhoselastknownaddress is inMichigan. Inaddition,everybusinessor government entity that is incorporated in Michigan mustreport to the Treasury abandoned property belonging to owners where there is no known address.Mostbusinesseshaveunclaimedpropertyresultingfromnormaloperations. Any asset, tangible or intangible, belonging to athird party that remains unclaimed for a specified period oftime isconsideredunclaimedproperty.Forexample,uncashedpayrollchecksmustbeturnedover to theStateafteroneyear;mostotherpropertytypes,suchasvendorchecksandaccountsreceivables credit balances, must be turned over after threeyears.Government entitiesmust turn over unclaimedpropertyafter one year.Due Date. The due date for the unclaimed property annualreportisJuly1,2014forpropertyreachingitsdormancyperiodasofMarch31,2014.

Dormancy Period. The dormancy period for most propertytypes is three years. A detailed listing of property types along withthecorrespondingdormancyperiodscanbefoundatwww.michigan.gov/unclaimedproperty.Report Unclaimed Property to Avoid Penalties.Reviewyourrecords to determine if you are holding unclaimed property.Property remitted voluntarily will not be subject to the 25percent penalty outlined in the law; however, interest will becharged. If you are selected for an audit, you will be subjectto the penalty and interest charges outlined in the law. State-initiatedauditswillcoverthelasttenyears,asauthorizedintheUniformUnclaimedPropertyAct.Noncompliance With Unclaimed Property Reporting Requirements. Section 31(2) of the Uniform UnclaimedPropertyActgivestheStateTreasurertheauthoritytoconductunclaimed property examinations (audits) if there is reasontobelieve thatanentity isaholder thathas failed to reportorhasunderreportedunclaimedproperty.Asaresultoftheaudit,penaltyandinterestmaybeassessedasfollows:Interest at one percentage point above the adjusted prime rateperannumpermonthon thepropertyorvalueof thepropertyfromthedatethepropertyshouldhavebeenpaidordelivered,and/orPenalty at 25 percent of the value of the property that shouldhavebeenpaidordelivered,and/orPenaltyat$100foreachdaythereportiswithheldorthedutyisnotperformedbutnotmorethan$5,000.Reporting Manual and Free Software. The Manualfor Reporting Unclaimed Property, including formsand instructions, is available at www.michigan.gov/unclaimedproperty.Also availableonTreasury’sWeb site isthe Holder Reporting System (HRS), a free software packageforcreatingunclaimedpropertyreports inanelectronicformatforsubmissiontoTreasury.

16

maIlInG InformatIonAnnual Return (Form 165) & W2If enclosing payment with your Annual Return, mail to:

MichiganDepartmentofTreasury Department78172 P.O.Box78000 Detroit,MI48278-0172If requesting a Credit to your account (amount on line 23) or a Refund (amount on line 24), mail to:

MichiganDepartmentofTreasury P.O.Box30779 Lansing,MI48909All other Annual Returns without payment, mail to:

MichiganDepartmentofTreasury Lansing,MI48930

amended annual returnsIf the amendment results in additional tax due, send youramendedannualreturnandpaymentto: MichiganDepartmentofTreasury Department78172 P.O.Box78000 Detroit,MI48278-0172Ifnopaymentisincludedwiththeamendedannualreturn,sendthe return to: MichiganDepartmentofTreasury BusinessTaxesDivision P.O.Box30427 Lansing,MI48909

Combined Returns (Form 160)If you are including payment, mail to: MichiganDepartmentofTreasury Department77003 Detroit,MI48277-0003If you are not including payment, mail to: MichiganDepartmentofTreasury Lansing,MI48930

CorrespondenceSend correspondence to:

MichiganDepartmentofTreasury BusinessTaxesDivision P.O.Box30427 Lansing,Michigan48909Writeyouraccountnumberonallchecksandcorrespondence.Returns should be sent to the address on the return.