Embed Size (px)

Citation preview

Financial:

3. Dividend Policy

4. Capital Structure

Operational:

Managerial Remuneration

102

Macroeconomic:

Interest

Strategic:

3. M&A

4. Sharebuyback

7. Factors that impact Shareholder Value Creation

7.1 Introduction

The Shareholder Value Creation is a simple concept where the Shareholders who are

the real owners and risk bearers get a return which is in excess of the cost of capital. If

one considers it from the Investor's point of view then expected return on Equity or if

one looks at it from the operational efficiency point of view then returns in excess of

WACC. The factors that have been considered to analyze in terms of the factors that

impact Shareholder Value Creation are based on the model given below:

7.2 The model of factors affecting SVC

Figure 7.1 SVC model

SVC =

Return - WACC

7.3 Methodology

The research, therefore, make these factors listed below as independent variables and

try and test the how much these factors have the predicting capability of the

shareholder value creation as shown in the model on top using multivariate

regression.

The model given above gives us the relationship of each factor with the input

variables of shareholder value creation and therefore, on the end shareholder value.

The reasoning has been already discussed in the literature review chapter but here the

importance of each of these factors in brief and how are they related to Shareholder

Value is discussed.

7.4 Dividend

Dividend is a major financial decision taken by the firms. It adds to the returns of the

Investors and also shows the outlook of the management.

Walter & Gordon model very clearly emphasize the fact that a company shall

distribute the profits as dividends if the returns from business are less than the

opportunity cost (expected rate of return) of the shareholders and shall reinvest the

profits in business if the returns from business are more than the opportunity cost

(expected rate of return) of the shareholders.

From the research point of view Dividend is a variable while calculating the

Shareholder returns as well as while calculating the WACC.

Table 7.1 below gives the dividends paid by the sample companies for the period

under review.

103

Table 7.1 Dividend paid by sample companies for the period under review

Name 2009-

10 2008-

09 2007-

08 2006-

07 2005-

06 2004-

05 2003-

04 2002-

03 2001-

02 2000-

01

ABB 42.38 42.38 46.62 46.62 42.38 33.91 29.67 25.43 25.43 20.71

ACC 572.63 431.76 375.33 375.02 428.53 124.97 70.88 42.73 51.24 34.14

AMBUJA 397.22 365.59 334.97 532.65 461.24 189.16 142.07 108.71 93.11 73.57

AXIS 486.22 359.01 214.63 126.73 97.54 76.66 57.9 47.71 28.72 19.79

AIRTEL 379.79 379.65 0 0 0 0 0 0 0 0

BHEL 1140.58 832.18 746.52 599.66 354.9 195.81 146.86 97.91 97.91 73.43

BPCL 506.16 253.08 144.62 578.46 90.39 375 525 450 330 225

CAIRN 506.16 253.08 144.62 578.46 90.39 NA NA NA NA NA

CIPLA 1140.58 832.18 746.52 599.66 354.9 195.81 146.86 97.91 97.91 73.43

DLF 339.48 339.44 681.94 340.97 NA NA NA NA NA NA

GAIL 951.36 887.93 845.65 845.65 845.65 676.52 676.52 591.96 380.54 338.26

GRASIM 275.05 275.02 275.02 252.1 183.35 146.68 128.34 91.67 82.5 73.34

HCL 275.05 275.02 275.02 252.1 183.35 146.68 128.34 91.67 82.5 73.34 HDFC BANK 549.29 425.38 301.27 223.57 172.23 140.07 100.05 85.05 70.34 48.72

HDFC 1320.2 1033.6 853.36 710.1 556.61 499.13 423.5 332.93 268.85 304.28 HERO

HONDA 2196.56 399.38 379.41 339.47 399.38 399.38 399.38 359.44 339.49 59.9

HINDALCO 2196.56 399.38 379.41 339.47 399.38 399.38 399.38 359.44 339.49 59.9

HUL 1417.94 1634.51 1976.12 1325.48 1100.62 1100.62 1599.2 1210.69 1100.62 770.21

ICICI 1417.94 1634.51 1976.12 1325.48 1100.62 1100.62 1599.2 1210.69 1100.62 770.21

IDEA 0 0 0 0 0 NA NA NA NA NA

IDFC 195.13 155.54 155.57 112.89 112.49 100 NA NA NA NA

INFOSYS 1434 1345 1902 649 1238 310 862.46 178.81 132.36 66.15

ITC 1434 1345 1902 649 1238 310 862.46 178.81 132.36 66.15

JSPL 116.52 85.33 62.02 55.43 46.19 46.19 30.79 18.29 9.03 6.35

JP ASSOC 183.62 114.25 114.6 78.82 58.04 42.3 26.44 NA NA NA

L&T 752.75 614.97 495.32 368.25 302.25 357.21 199.04 186.8 174.34 161.85

M&M 549.52 278.83 282.61 282.23 243.97 150.81 104.41 63.81 56.21 60.77

MUL 173.3 101.1 144.5 130 101.1 57.8 43.3 42.7 NA NA

NTPC 3133.2 2968.3 2885.9 2638.5 2308.7 1979 1082.3 NA NA NA

ONGC 7058.28 6844.39 6844.39 6630.51 6416.71 5703.74 3422.24 4277.8 1996.31 1568.53

PNB 696.99 693.66 630.61 409.89 315.3 189.18 174.18 106.12 92.86 NA

POWERGRID 631.34 505.08 505.08 368.82 NA NA NA NA NA NA

RANBAAXY 84.21 0 0 317.15 316.89 316.67 316.26 315.63 243.4 115.9 RELIANCE

INFRA 173.86 157.69 147.73 121.12 104.62 87.21 70.49 60.6 59.22 55.09

REL CAP 159.66 159.66 135.1 85.97 71.32 38.19 36.92 36.92 36.92 36.92

RCOM 175.44 165.12 154.8 102.23 0 0 NA NA NA NA

RIL 2384.99 2084.67 1897.05 1631.24 1440.44 1393.51 1045.13 733.1 698.19 663.28

REL POWER 0 0 0 0 NA NA NA NA NA NA

SIEMENS 168.58 168.58 101.15 80.92 64.06 48.05 29.82 24.86 18.23 13.26

SBI 1905 1904.65 1841.15 1357.66 736.82 736.82 657.87 578.93 447.36 315.78

104

SAIL 1363.03 1073.9 1528.25 1280.42 826.08 1363.03 0 0 0 0

STERLITE 315.15 247.97 283.4 223.4 69.84 32.93 21.54 19.76 17.06 30.56

SUN 284.79 284.79 217.47 130.01 102.3 69.57 60.29 46.52 23.39 23.38

SUZLON 284.79 284.79 217.47 130.01 102.3 69.57 NA NA NA NA TATA

MOTOR 859.05 311.61 578.43 578.07 497.94 452.19 282.11 127.91 0 0 TATA

POWER 285.05 255.26 241.38 188.22 168.41 148.6 138.69 128.78 99.06 99.06 TATA STEEL 285.05 255.26 241.38 188.22 168.41 148.6 138.69 128.78 99.06 99.06

TCS 2740.1 3914.43 1370.05 1370.05 1125.39 660.56 552.13 NA NA NA

UNITECH 48.77 20.44 40.58 40.58 16.23 5 3.75 2.5 2.5 2.5

WIPRO 880.9 586 876.5 873.7 712.88 351.79 675 23.26 23.25 11.62

ZEE 194.68 86.8 86.8 65.04 43.47 41.25 41.25 22.69 22.69 22.69

1.The dividend is amount (Rs. Crore);

2. N.A. = Not Available as the companies had not listed on the markets;

3. Source: Capitaline database (Capitaline.com )

7.5 Interest

The interest rate in the economy determines the WACC as it impacts the expected

retums on the Shares and the cost of Debt Capital. The popular finance here is an

inverse relationship between the Interest rates in the economy and the share price. The

economy where the interest rates are high, the share prices tend to be come down as

the expected return on the shares is high (Chandra, 2005).

The risk free rates of interest prevalent in the economy also determine the cost of

debt, which is an integral part of the modern day companies, especially manufacturing

(Chandra, 2005).

Table 7.2 below gives the weighted average yields of the 364 day T - Bills which is

considered as the benchmark for the Risk free rate of return in the study.

105

Table 7.2 Weighted average yield of 364 day T-Bills

YEAR Rf

2000-01 9.76

2001-02 7.30

2002-03 5.93

2003-04 4.67

2004-05 5.15

2005-06 5.87

2006-07 7.07

2007-08 7.50

2008-09 7.19

2009-10 4.35

Source: Reserve Bank of India official website (http://www.rbi.org.in )

Figure 7.2: 364 day Tbill Wtd. Avg. Yields

12

10

8

6

364 day Tbill Wtd. Avg. Yields

2

0

Q),Q> ,v0%,),Q616.1,63 0z,Q,c3, 1\z,6\,66 6170c5 Q,c5NQ' cP 19 19

If one notices the rate of interest in the Indian economy is seen on a decline in

comparison to 2000-01 to 2009-10 from a monstrous near double digit to a more

acceptable and borrower friendly single digit below 5% mark.

7.6 Debt Equity Ratio

Debt Equity Ratio denotes the Capital Structure of the firm which in turn, influences

the WACC. The research takes a deeper look at whether the Debt Equity Ratio has

any impact on the Shareholder Value Creation as measured by EVA and PFM.

4

106

Table 7.3 Debt Equity Ratio of sample companies for the period under review

Name 2009 -10

2008 -09

2007 -08

2006 -07

2005 -06

2004 -05

2003 -04

2002 -03

2001 -02

2000 -01

ABB 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

ACC 0.1 0.1 0.1 0.2 0.4 0.7 1.0 1.2 1.5 1.5

AMBUJA 0.0 0.0 0.1 0.2 0.4 0.6 0.8 1.1 1.1 0.9

AXIS 71.9 68.9 65.9 59.9 52.8 47.4 43.6 42.8 47.6 56.2

AIRTEL 0.2 0.3 0.4 0.5 0.8 0.6 0.1 0.0 0.0 0.1

BHEL 0.0 0.0 0.0 0.0 0.1 0.1 0.1 0.1 0.2 0.2

BPCL 1.7 1.5 1.2 1.0 0.8 0.5 0.6 0.8 1.0 0.9

CAIRN 0.0 0.0 0.0 0.0 NA NA NA NA NA NA

CIPLA 0.1 0.2 0.1 0.1 0.2 0.1 0.1 0.1 0.0 0.0

DLF 0.9 0.8 1.3 7.5 3.5 1.7 1.0 0.1 0.3 0.9

GAIL 0.1 0.1 0.1 0.2 0.2 0.3 0.3 0.4 0.5 0.5

GRASIM 0.3 0.4 0.4 0.4 0.4 0.5 0.6 0.7 0.7 0.7

HCL 0.2 0.1 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 HDFC BANK 72.4 66.6 65.3 66.1 65.8 64.9 55.9 46.4 39.1 39.8

HDFC 6.5 6.4 6.1 7.2 10.4 10.0 9.0 8.1 7.3 6.7 HERO HONDA 0.0 0.0 0.1 0.1 0.1 0.1 0.2 0.2 0.1 0.1

HINDALCO 0.3 0.4 0.5 0.6 0.5 0.4 0.4 0.3 0.2 0.2

HUL 0.1 0.2 0.0 0.0 0.4 0.8 0.3 0.0 0.0 0.1

ICICI 95.0 95.9 88.7 86.5 89.7 91.7 99.7 125.

0 111.

6 40.7

IDEA 0.6 1.0 1.9 2.1 2.5 2.4 2.0 2.0 3.5 6.0

IDFC 3.9 4.0 4.5 4.5 3.6 2.9 1.9 1.3 1.1 1.0

INFOSYS 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

ITC 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.2 0.2

JSPL 1.1 1.0 1.2 1.5 1.3 1.2 1.3 1.4 1.1 0.8

JP ASSOC 2.1 2.0 2.0 2.1 2.2 2.3 1.9 1.9 1.4 2.5

L&T 0.4 0.5 0.4 0.3 0.4 0.5 0.7 1.0 1.1 1.1

M&M 0.5 0.7 0.5 0.4 0.4 0.5 0.6 0.8 0.7 0.5

MUL 0.1 0.1 0.1 0.1 0.0 0.1 0.1 0.2 0.3 0.3

NTPC 0.6 0.6 0.5 0.5 0.4 0.4 0.4 0.4 0.4 0.4

ONGC 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.1 0.1 0.2

PNB 74.3 72.9 70.6 , 66.0 60.6 56.3 53.4 53.3 51.9 48.9 POWERGRI D 2.0 1.8 1.7 1.6 1.5 1.5 1.5 1.4 1.3 1.3 RANBAAX Y 0.8 0.9 1.2 1.4 0.9 0.2 0.0 0.0 0.0 0.1 RELIANCE INFRA 0.4 0.6 0.6 0.7 0.6 0.6 0.4 0.3 0.3 0.3

REL CAP 1.9 1.8 1.0 0.2 0.3 1.0 1.2 1.6 1.4 1.4

RCOM 0.5 0.7 0.8 0.4 0.0 NA NA NA NA NA

RIL 0.5 0.6 0.6 0.5 0.5 0.5 0.6 0.7 0.7 0.8

107

REL POWER 0.0 0.0 0.0 NA NA NA NA NA NA NA

SIEMENS 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.1

SBI 76.0 75.0 77.5 73.5 62.1 52.6 48.1 45.6 45.7 48.2

SAIL 0.4 0.2 0.2 0.3 0.4 0.9 2.9 5.0 3.8 3.0

STERLITE 0.3 0.3 0.3 0.6 0.6 1.0 1.5 1.1 0.8 0.8

SUN 0.0 0.0 0.2 0.7 1.4 1.1 0.2 0.0 0.0 0.1

SUZLON 1.2 0.8 0.4 0.2 _ 0.2 0.4 0.5 0.3 0.2 0.2 TATA MOTOR 1.1 1.0 0.7 0.6 0.6 0.5 0.4 0.7 0.9 0.9 TATA POWER 0.6 0.5 0.5 0.6 0.5 0.5 0.4 0.6 0.7 0.7 TATA STEEL 0.8 0.8 0.7 0.5 0.3 0.5 1.0 1.4 1.1 1.0

TCS 0.0 0.0 0.0 0.0 0.0 0.2 4.5 0.0 NA NA

UNITECH 1.2 3.2 3.6 3.1 2.6 1.4 0.9 1.0 1.1 1.2

WEPRO 0.4 0.4 0.2 0.0 0.0 0.0 0.0 0.0 0.0 0.0

ME 0.1 0.1 0.1 0.2 0.3 0.2 0.1 0.1 0.1 0.1 1.Source: Capitaline database;

2.N.A. = Not Available

From table 7.3 it can be seen that:

1. Debt Equity ratio of all banking companies is very high. But it must be noted

that the nature of business banks are in and the method of accounting used by

them. All the deposits are a debt and that is large in number. Thus, the

numbers seem extraordinarily high.

2. Most of the software companies are near zero debt.

3. The real estate firms are ones with comparatively high Debt Equity Ratio.

7.7 Mergers & Acquisitions

The companies globally are stressing on increasing the market share, looking

outwardly due to Globalisation. Recent Financial Crisis which caused Global

Recession has also offered attractive valuations. The companies are using the

inorganic way of growth, of Mergers & Acquisitions, rather than the organic method.

The reasons, too, are quite obvious. The Greenfield projects have a large gestation

period; especially the capital intensive firms and also the funds required are way too

108

large. For instance Tata Steel would have to spend more than $ 16 bn to set up

facility of Corus with a gestation period of at least 3 years in comparison to the value

of $ 13.2 bn with a ready to use plant by a mere takeover (Director's report in the

Annual Report of Tata Steel, 2008).

Indian companies have started looking at these options since liberalisation of the

economy. Indian companies are looking at M&A in foreign countries as well as in

India.

The Mergers and Acquisition deals in India in 2010 have touched $ 50bn so far three

times the total of 2009 which accounted for $ 16.3 bn and more than 2008 which

clocked deals of the value $ 40 bn.The number of deals have, however, reduced in

comparison to 2009 where India witnessed 453 deals and this year till now we have

411 deals (with 1 month of December to go) (Economic Times Report dated 3rd

November, 2010).

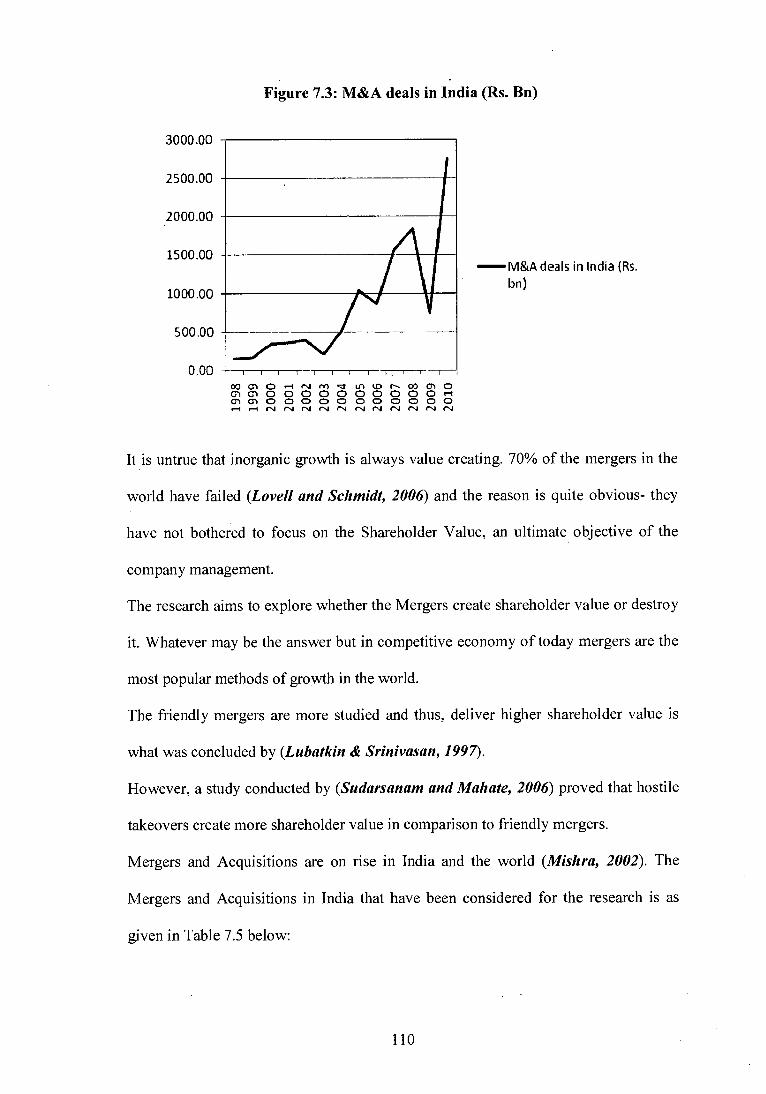

Table 7.4 below lists out the M&A deals in India till December, 2010.

Table-7.4 M&A deals in India

Year M&A deals in India (Rs. bn) 1998 151.00

1999 160.43

2000 336.62

2001 351.71 .

2002 391.62

2003 204.19

2004 513.00

2005 1042.02

2006 865.00

2007 1576.00

2008 1840.00

2009 736.00

2010 2760.00

Source: SEBI official website, http://www.sebi.gov.in accessed on 20-11-2010 at 5.30 PM

109

Figure 7.3: M&A deals in India (Rs. Bn)

3000.00

2500.00

2000.00

1500.00

1000.00

500.00

0.00

—M&A deals in India (Rs. bn)

00 Cl 0 1rs.1 M •,:t N 00 Cl Gl Cl 0 0 0 0 0 0 0 0 0 0 1—( GI CI 0 0 0 0 CD 0 0 CD CD 0 0

rsJ rsl rV ("J N ("J rg rsJ rsJ rsJ rsJ

It is untrue that inorganic growth is always value creating. 70% of the mergers in the

world have failed (Lovell and Schmidt, 2006) and the reason is quite obvious- they

have not bothered to focus on the Shareholder Value, an ultimate objective of the

company management.

The research aims to explore whether the Mergers create shareholder value or destroy

it. Whatever may be the answer but in competitive economy of today mergers are the

most popular methods of growth in the world.

The friendly mergers are more studied and thus, deliver higher shareholder value is

what was concluded by (Lubatkin & Srinivasan, 1997).

However, a study conducted by (Sudarsanam and Mahate, 2006) proved that hostile

takeovers create more shareholder value in comparison to friendly mergers.

Mergers and Acquisitions are on rise in India and the world (Mishra, 2002). The

Mergers and Acquisitions in India that have been considered for the research is as

given in Table 7.5 below:

110

Table 7.5: List of Mergers & Acquisitions for the period under review

Sr. No

Date Company name Acquired by Deal Value

(MN $)

1 21-07-2002 Indo gulf corporation Hindalco industries 438.68

2 20-12-2002 Reliance infrastructure Reliance industries 242.68

3 23-07-2002 Indian aluminium co Hindalco industries 35.83 4 27-05-2002 Customer asset Icici bank 20.53

5 06-01-2003 Transamerica apple distributors Icici bank 15.42

6 15-07-2002 Ambuja cement Rajasthan Ambuja cements 11.05

7 18-07-2002 GE medical systems information Wipro 5.73

8 03-01-2003 Spectra mind eservices pvt. Ltd. Wipro 5.50

9 27-05-2002 Mj pharmaceuticals Sun pharmaceutical Indus 0.25

10 22-12-2003 Bargarh cement Acc 39.97

11 10-03-2004 Bargarh cement Acc 5.94 12 26-10-2004 Kochi refineries Bharat petroleum corp 269.17

13 10-01-2005 Tata finance Tata motors 182.72

14 23-03-2005 Itc hotels Itc 105.22

15 25-11-2004 Siemens vdo automotive Siemens india 82.43

16 31-07-2004 Greenline construction Unitech 49.06

17 21-07-2004 Intelenet global services pv Housing development finance 34.91

18 27-11-2004 Sar transmission pvt Mahindra & mahindra 3.25

19 02-01-2006 Reliance capital ventures It Reliance capital 609.01

20 15-07-2005 Tata infotech Tata consultancy svs 259.30

21 10-10-2005 Wimco Itc 14.78

22 09-08-2005 Vashisti detergents Hindustan unilever 11.35

23 31-03-2006 Pacenet pvt Zee entertainment enterprise 4.00

24 14-12-2005 Tarmac india pvt Acc 2.71

25 10-03-2007 Indian petrochemicals corp Reliance industries 1130.58

26 03-05-2006 Ambuja cement eastern Ambuj a cements 397.26

27 12-03-2007 Punjab tractors Mahindra & mahindra 96.65

28 09-12-2006 Sangli bank Icici bank 67.15

29 30-09-2006 Cardinal drugs Ranbaxy laboratories 2.80

30 12-03-2007 Swaraj engines Mahindra & mahindra 0.03

31 07-09-2006 Harish cement Grasim industries 0.02

32 23-02-2008 Centurion bank of punjab Hdfc bank 2813.25

111

33 06-07-2007 Unza holdings pte Wipro 249.71

34 07-03-2008 Multiple targets Infrastructure dev finance 205.00

35 24-01-2008 Global trade finance State bank of india 131.88

36 28-09-2007 Lodha elevation buildcon pvt Icici bank 20.00

37 10-09-2007 Bharti aquanet Bharti airtel 3.92 38 16-10-2007 Hcl eai services inc Hcl technologies . 3.59

39 03-10-2007 Zenotech laboratories Ranbaxy laboratories 2.56 40 08-10-2008 Citigroup global services lt Tata consultancy svs 512.00

41 08-10-2008 Citigroup global services It Tata consultancy svs 512.00 42 25-06-2008 Spice communications Idea cellular 327.87 43 23-12-2008 Citi technology services Wipro 127.00 44 30-07-2008 Punjab tractors Mahindra & mahindra 87.58

(Source: http://ww w.etintelli gence.com/eti g/researchchannels/mergersacqui sition/i ndianIn di an . j sp)

It is, thus, researched whether the Mergers and Acquisitions listed above created or

destroyed shareholder value.

7.8 Earnings Per Share

Earnings per Share is used as a proxy for Sharebuybacks. Sharebuybacks is done by

the companies in order to improve on the EPS. The research tends to analyse the

impact of EPS on the shareholder value creation as measured by EVA and PFM.

Sharebuybacks - History

Among the countries which allow share buyback by companies, the U.S. has the

longest history. Share buybacks had appeared in the U.S. in the late 1960s, and had

become very popular by mid-1980s. The buyback system was not subject to any

special federal regulation till 1982 although the U.S. SEC had been contemplating it

for a long time (Cook, Krigman and Leach J., 2003).

As in Europe, share buybacks began to be permitted in the late 1990s in Asian

countries. Buybacks were permitted in Japan in 1995 followed by Malaysia (1997),

Singapore and Hong Kong in 1998 and Taiwan in 2000 (Gupta, 2003).

Share buybacks in India

112

India recognized the usefulness of the share buyback system in late 1998. Till then,

the Companies Act in India had strictly prohibited companies from buying back own

shares.

Shares are bought back by the companies usually to have a positive impact on the

Earnings per Share (Gupta, 2003).

There have been a good number companies that filed for Sharebuybacks in India but

at ground level not all the companies exercised their permission to buy back the

shares and not the entire quantity that was applied for. Reliance Industries for

example had announced to buy back as much as 10% of its equity shares from the

open market at the rate of Rs. 570/- per share but in reality bought back shares worth

only Rs. 2.87 Cr which was a miniscule fraction of what was filed.

Table 7.6 gives the list companies that bought back shares from 2000-01 to 200-10.

Table 7.6 Table showing the names of the companies who filed for Sharebuyback

in the period under review

Sr. No Year Name of the co 1 2003-04 ADF Foods Ltd 2 2003-04 Indian Motor Parts and Accessories Limited 3 2003-04 International Conveyors Ltd 4 2003-04 Solitaire Machine Tools Limited 5 2004-05 Aegis Logistics Ltd 6 2004-05 Avery India Ltd 7 2004-05 Britannia Industries Ltd 8 2004-05 Fine Line Circuits Limited 9 2004-05 Glaxosmithkline Consumer Healthcare Ltd 10 2004-05 Mastek Ltd 11 2004-05 Public Announcement 12 2004-05 Reliance Energy Ltd 13 2004-05 Reliance Industries Limited 14 2004-05 Sun Pharmaceutical Industries Ltd — PDF 15 2005-06 Apollo Finvest (I) Ltd 16 2005-06 Berger Paints India Limited

113

17 2005-06 DIL Ltd 18 2005-06 ETC Networks Ltd 19 2005-06 India Bulls Financial Services Ltd 20 2005-06 India Forge Drop Stamping Ltd 21 2005-06 Polaris Software Lab Limited 22 2005-06 Polaris Software Lab Ltd 23 2005-06 Prime Securiteis Ltd 24 2005-06 SRF Polymers Ltd 25 2006-07 Abbott India Limited 26 2006-07 Carol Info Services Limited 27 2006-07 Natco Pharma Limited 28 2006-07 Revathy Equipment Limited 29 2007-08 Gujarat Ambuja Exports Ltd 30 2007-08 Ace Software Limited 31 2007-08 Apollo Finvest (India) Limited 32 2007-08 Assam Carbon Products Limited 33 2007-08 GTL Limited 34 2007-08 Hindustan Unilever Limited 35 2007-08 Madras Cements Ltd 36 2008-09 Rain Commodities Ltd 37 2008-09 Surana Telecom and Power Ltd 38 2008-09 Abbott India Limited 39 2008-09 Alembic Ltd 40 2008-09 Amrutanjan Health Care Ltd. 41 2008-09 ANG Auto Ltd 42 2008-09 Binani Metals Limited 43 2008-09 Bosch Ltd. 44 2008-09 DLF Ltd 45 2008-09 E.I.D. Parry (India) Ltd. 46 2008-09 Eicher Motors Ltd. 47 2008-09 FDC Limited 48 2008-09 Gateway Distriparks Ltd. 49 2008-09 Godawari Power & Ispat Limited 50 2008-09 Godrej Consumer Products Ltd. 51 2008-09 Goldiam International Ltd 52 2008-09 Great Offshore Ltd 53 2008-09 Gujarat Fluorochemicals Limited 54 2008-09 HEG Ltd 55 2008-09 Hydro S&S Industries Ltd 56 2008-09 India Infoline Ltd. 57 2008-09 IPCA Laboratories Ltd. 58 2008-09 Jindal Poly Films Ltd. 59 2008-09 Kilburn Engineering Ltd. 60 2008-09 LKP Finance Ltd

114

61 2008-09 Maestros Mediline Systems Ltd. 62 2008-09 Monnet Ispat & Energy Ltd. 63 2008-09 MRO-TEK Ltd 64 2008-09 Patni Computer Systems Limited 65 2008-09 R Systems International Ltd. 66 2008-09 Rain Commodities Ltd 67 2008-09 Reliance Infrastructure Ltd. 68- 2008-09 Sasken Communication Technologies Ltd. 69 2008-09 Supreme Petrochem Limited 70 2008-09 Surana Telecom and Power Ltd. 71 2008-09 T V Today Network Ltd 72 2008-09 The Supreme Industries Ltd. 73 2008-09 TTK Healthcare Ltd. 74 2008-09 Valiant Communications Ltd 75 2008-09 Zen Technologies Ltd 76 2009-10 Aegis Logistics Limited 77 2009-10 Apcotex Industries Limited 78 2009-10 Apollo Tyres Ltd. 79 2009-10 Aro Granite Industries Ltd. 80 2009-10 Austin Engineering Company Ltd. 81 2009-10 Avantel Ltd. 82 2009-10 Bhagyanagar India Limited 83 2009-10 Bright Brothers Limited 84 2009-10 Dai-Ichi Karkaria Ltd. 85 2009-10 Deccan Chronicle Holdings Limited 86 2009-10 Gee Cee Ventures Limited 87 2009=10 Gitanjali Gems Ltd. 88 2009-10 Godrej Industries Ltd. 89 2009-10 GSS America Infotech Ltd. 90 2009-10 Gujarat Petrosynthese Limited 91 2009-10 HOV Services Ltd. 92 2009-10 ICI India Ltd 93 2009-10 Indiabulls Securities Ltd. 94 2009-10 M/s. Aegis Logistics Limited 95 2009-10 M/s. Goldiam International Ltd 96 2009-10 Mangalam Cement Ltd. 97 2009-10 Merck Ltd 98 2009-10 Nava Bharat Ventures Ltd. 99 2009-10 Pennar Industries Ltd 100 2009-10 Poddar Pigments Limited 101 2009-10 Provogue India Ltd 102 2009-10 Selan Exploration Technology Ltd. 103 2009-10 SoftSol India Limited - Corrigendum to PA 104 2009-10 SRF Ltd.

115

2009-10 2009-10 2009- 10 2009- 10

The Sandesh Ltd. TIPS Industries Limited TV Today Network Limited Zensar Technologies Limited

105 106 107 108

Source: http://www.sebi.gov.in

Though the number of companies that filed for buybacks were 109. In reality a very

few of them actually undertook the real buyback. Whichever companies that

undertook the buyback did not do it to the levels that were desired.

The companies on an average bought back only 5% of what was desired (Gupta,

2003).

All the studies that were undertaken (to the best of the information of the researcher)

were undertaken to find out the impact of share buyback announcement on the share

price of the security of the acquirer company and acquire company but none of the

studies focussed on the fact whether the company management in reality considered

the impact of a strategic decision such as Share buyback on the Shareholder Value

Creation.

7.9 Managerial Remuneration

This is the remuneration paid to the Directors for managing the company and being

trustees of the end risk bearers of the company, the equity shareholders. The directors

are supposed to take the decisions for the wealth maximisation of the Shareholders.

The research takes an in-depth look at, if the Managerial Remuneration in reality has

any relation to the Shareholder Value created by them.

There is no study (to the best of information of the researcher) to evaluate whether the

managers (to be understood as board level managers) are compensated for the quality

of the decisions and whether the compensation paid to the managers is also based on

whether their decisions have created or destroyed shareholder value.

116

Table 7.7 given below gives the details of managerial remuneration paid to managers

(as defined above) for the sample companies for the period under review.

Table 7.7 Managerial Remuneration paid during the period under review

Sr. No Name\Year 09-10 08-09 07-08 06-07 05-06 04-05 03-04 02-03 01-02 00-01

1 ABB 1.81 2.48 2.55 2.53 2.89 1.52 1.03 0.84 0.75 0.55

2 ACC 5.23 3.96 3.33 3.59 2.99 1.42 1.81 1.91 1.82 1.97

3 AIRTEL 29.89 29.1 27.61 24.32 20.47 13.64 8.55 0.86 0.4 0.28

4 AMBUJA 5.65 7.67 10.28 14.72 21.76 12.71 9.99 11.7 6.32 3.85

5 AXIS 0.58 0.51 0.72 0.7 0.59 0.5 0.54 0.32 0.24 0.17

6 BHEL 2 0.85 1.44 0.88 0.69 0.55 0.79 0.48 0.41 0.74

7 BPCL 1.49 1.31 1.04 0.83 0.51 0.56 0.48 0.45 0.45 0.34

8 CAIRN 0.12 0.13 0.71 0.22 NA NA NA NA NA NA

9 CIPLA 29.59 28.57 27.63 22.64 22.58 16.13 12.04 9.89 8.42 0.03

10 DLF 27.61 18.34 31.55 19.51 12.28 10.47 5.64 4.42 4.13 3.41

11 GAIL 3.35 1.15 1.09 1.1 0.78 0.73 0.72 0.63 0.32 0.8

12 GRASIM 21.8 19.11 19.04 13.73 7.21 4.34 2.88 2.71 2.13 0.72

13 HCL 10.58 10.38 4.26 2.22 3.54 3.33 1.66 0.46 0 0

14 HDFC 13.21 16.07 11.39 9.61 7.29 6.11 5.18 4.71 3.83 3.12

15 HDFC BANK 0.47 0.44 0.42 0.39 0.46 0.19 0.15 0.12 0.04 0.05

16 • HERO HONDA 122.49 77.94 62.29 54.78 61.14 52.68 45.57 37.66 0.3 16.4

17 HINDALCO 27.2 18.65 9.88 14.99 7.33 4.12 3.19 1.03 0.02 0.71

18 HUL 15.93 13.42 9.79 10.08 5.81 6.52 7.78 7.26 6.15 7.6

19 ICICI 0.46 0.42 0.36 0.42 0.38 0.32 0.39 0.37 0.13 0.15

20 IDEA 6.19 5.05 4.15 1.61 0 0.47 0.42 0 0 0

21 IDFC 14.42 4.13 4.67 1.82 1.17 0.75 0.36 0.56 0.58 0.44

22 INFOSYS 16 16 15 4 6 5 6 4.71 7.24 4.27

23 ITC 17.16 13.94 16.8 16.49 10.27 7.09 6 4.35 3.87 3.08

24 JPSPL 76.35 35.09 19.72 13.26 12 2.42 1.72 1.44 0.71 0.33

25 JP ASSOC 7.83 8.16 5.37 2.9 1.88 1.35 2.15 2 0.41 0

26 L&T 68.83 56.68 38.2 27.46 17.44 16.17 7.48 6.14 3.41 2.87

27 M&M 8.19 6.29 6.54 6.15 6.89 6.94 5.93 4.35 3.02 2.01

28 MUL 7.6 7.6 9.4 6.71 5.25 4.54 3.74 3.38 1.65 1.08

29 NTPC 0.3 0.2 1.2 0.7 1 0 0.8 0.8 0.49 0.68

30 ONGC 3.81 2.15 1.66 1.01 0.96 0.86 0.82 0.58 0.62 0.58

31 PNB 1.46 1.42 1.35 0.94 0.82 0.73 0.7 0.35 0.28 0.31

32 POWERGRID 1.83 0.59 0.4 0.71 0.45 0.54 0.54 0.52 0.18 0

33 Ranbaxy 11.84 26.59 27.73 31.24 13.31 7.95 11.63 11.21 9.85 4.4

34 RCOM 1.51 1.45 35.53 44.68 0 0 NA NA NA NA

35 REL POWER 0.72 0.64 0.23 0 0 0 0 0 0 0

117

36 REL CAP 0.53 0.44 0.37 0.29 0.2 0.15 0.13 0.01 0.01 0.01

37 REL INFRA 5.01 5.97 14.06 5.33 5.08 4.62 2.55 1.16 1.1 0.74

38 RIL 42.56 42.84 40.3 69.61 48.56 46.69 55.41 41.04 35.37 35.58

39 SAIL 0.19 0.25 1.79 1.13 0.8 0.06 0.64 0.63 0.76 0.61

40 SBI 0.74 0.61 1 1.23 1.08 1.23 0.99 0.74 0.63 0.72

41 SIEMENS 1.38 1.29 1.54 9.59 5.46 5.74 2.95 2.23 2.1 2.15

42 STERLITE 12.29 10.55 15.23 14.92 14.89 6.65 3.92 4.45 3.67 3.05

43 SUN PHARMA 3.95 3.45 3.06 2.7 2.28 1.4 1.33 1.28 0.85 0.93

44 SUZLON 2.13 1.23 1.59 1.61 1.79 1.64 0 0 0 0

45 TATA MOTOR 13.22 12.13 10.16 6.89 5.69 5.59 7.56 0 1.39 0.56

46 TATA POWER 13.21 12.25 6.99 4.77 1.8 2 2.22 2.5 2.07 1.77

47 TATA STEEL 7.4 10.4 12.08 7.97 6.89 6.27 4.71 2.33 2.55 2.85

48 TCS 0 0 12.8 11.08 5.41 4.09 1.97 0 0 NA

49 UNITECH 9.88 8.47 9.16 6.25 1.71 0.89 0.6 0.48 0.4 0.41

50 WIPRO 27 16.3 7.6 0 0 7.5 10.69 7.57 8.31 7.9

51 ZEE 4.41 3.8 1.22 1.5 1.65 0.27 0.5 4.26 3.6 2.26 Source : Capitaline Database

N. A. = Not Available

7.10 Study

The objectives of study, therefore, are:

3. To study the factors that impact Shareholder Value Creation as measured by

EVA and PFM.

a. To study the impact of Dividend on the Shareholder Value Creation as

measured by EVA and PFM;

b. To study the impact of Capital Structure on the Shareholder Value

Creation as measured by EVA and PFM;

c. To study the impact of Mergers & Acquisitions on Shareholder Value

Creation as measured by EVA and PFM;

d. To study the impact of Sharebuybacks on the Shareholder Value

Creation as measured by EVA and PFM;

e. To study the impact of Interest Rates on the Shareholder Value

Creation as measured by EVA and PFM;

118

f. To study if the Managerial Remuneration is paid based on the

Shareholder Value Creation as measured by EVA and PFM.

4. To study the direction of association of these factors with Shareholder value as

measured by EVA and PFM.

To study these objectives the hypothesis tested shall be:

3 & 41: To study the impact of Dividend on SVC

110=There is no significant impact of Dividend on the shareholder value creation

as measured by EVA and PFM

Alternative hypothesis

111=There is significant impact of Dividend on the shareholder value creation as

measured by EVA and PFM

3&42 : To Study the impact of Capital Structure on the SVC

110=There is no significant impact of Capital Structure on shareholder value

creation as measured by EVA and PFM

Alternative hypothesis

Hi=There is significant impact of Capital Structure on shareholder value

creation as measured by EVA and PFM

3&43: To Study the impact of Managerial Remuneration on the SVC

110=There is no significant impact of MR on the shareholder value creation as

measured by EVA and PFM

Alternative hypothesis

Hi=There is significant impact of MR on shareholder value creation as measured

by EVA and PFM

3&44: To study the impact of Mergers and Acquisitions on the SVC

119

110=There is no significant impact of M&A on the shareholder value creation as

measured by EVA and PFM

Alternative hypothesis

Hi=There is significant impact of M&A on the shareholder value creation as

measured by EVA and PFM

3&45: To study the impact of Sharebuyback on the SVC

110=There is no significant impact of Sharebuyback on the shareholder value

creation as measured by EVA and PFM

Alternative hypothesis

Hi=There is significant impact of Sharebuyback on the shareholder value

creation as measured by EVA and PFM

3&46: To study the impact of Interest Rates on the SVC

110=There is no significant impact of Interest Rates on the shareholder value

creation as measured by EVA and PFM

Alternative hypothesis

Hi=There is significant impact of Interest Rates on the shareholder value

creation as measured by EVA and PFM

7.11 Factors affecting EVA

Table 7.8 given below gives coefficients of various independent variables such as

Managerial Remuneration, Dividend, Interest Rate, Debt Equity Ratio, Earnings per

Share

120

Table 7.8: Coefficients' of Independent Variables with EVA

Model

Unstandardized Coefficients

Standardized Coefficients t Sig.

B Std. Error Beta

(Constant) 7404.78 1506.18 4.916 .000

Managerial Remuneration -.306 27.81 -.001 -.011 .991

Earnings Per Share -1.80 9.96 -.009 -.181 .857

Dividend .69 .37 .088 1.847 .065

Interest -1076.15 221.53 -.229 -4.858 .000

Capital. Structure (DE -36.714 16.22 -.106 -2.264 .024 Ratio)

a. Dependent Variable: EVA

Table 7.9: Model Summary of all independent variables with EVA

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .259a .067 .056 7202.21742

a. Predictors: (Constant), DE, INTEREST EPS, MR, DIV b. Dependent Variable: EVA

Table 7.9 gives the model's details with respect to what is the explaining power of the

independent variables about the Shareholder Value Creation as measured by EVA.

Table 7.10 gives the ANOVA test results for the model in terms of the statistical

significance of the R2 value meaning thereby the explanatory capability of the

independent variable of the dependent variable.

121

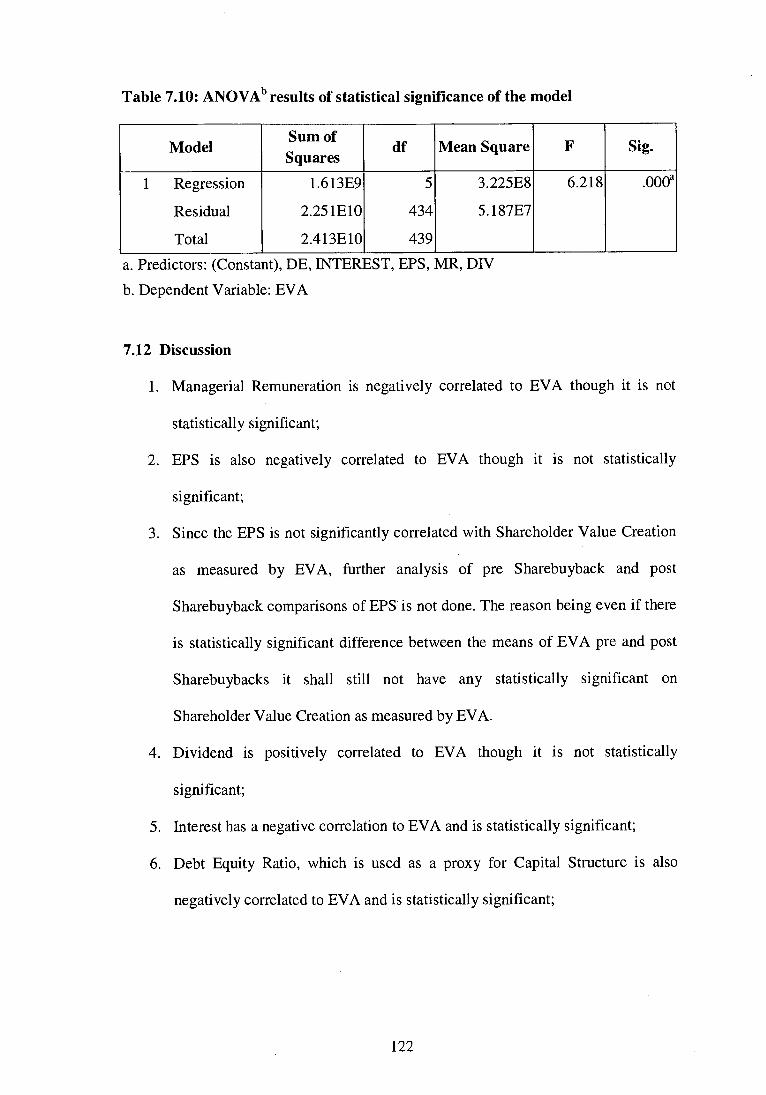

Table 7.10: ANOVAb results of statistical significance of the model

Model Sum of Squares

df Mean Square F Sig.

1 Regression

Residual

Total

1.613E9

2.251E10

2.413E10

5

434

439

3.225E8

5.187E7

6.218 .000a

a. Predictors: (Constant), DE, INTEREST, EPS, MR, DIV

b. Dependent Variable: EVA

7.12 Discussion

1. Managerial Remuneration is negatively correlated to EVA though it is not

statistically significant;

2. EPS is also negatively correlated to EVA though it is not statistically

significant;

3. Since the EPS is not significantly correlated with Shareholder Value Creation

as measured by EVA, further analysis of pre Sharebuyback and post

Sharebuyback comparisons of EPS is not done. The reason being even if there

is statistically significant difference between the means of EVA pre and post

Sharebuybacks it shall still not have any statistically significant on

Shareholder Value Creation as measured by EVA.

4. Dividend is positively correlated to EVA though it is not statistically

significant;

5. Interest has a negative correlation to EVA and is statistically significant;

6. Debt Equity Ratio, which is used as a proxy for Capital Structure is also

negatively correlated to EVA and is statistically significant;

122

7. ANOVA shows the model to be statistically significant but is more due to

large sample as the R 2 of .067 is very small and does not explain any variance

in the dependent variable.

7.13 Study of factors affecting PFM

The variables are then regressed with the other shareholder value creation measure

namely PFM. Table 7.11 to 7.13 give the details of the results factors affecting

shareholder value creation as measured by PFM. Table 7.11 shows the significance of

the coefficients of the independent variables with the dependent variable PFM, Table

7.12 shows the predicting power of the independent variables of PFM and Table 7.13

shows the statistical significance of the model.

Table 7.11: Coefficients' of Independent Variables with PFM

Model

Unstandardized Coefficients

Standardized Coefficients T Sig.

B Std. Error Beta

(Constant) -26720.00 12615.77 -2.118 .035

Managerial Remuneration -132.09 232.97 -.03 -.567 .571

Earnings Per Share 238.86 83.42 .14 2.863 .004

Dividend -4.09 3.11 -.06 -1.313 .190

Interest 3351.93 1855.57 .09 1.806 .072

Capital Structure (Debt Equity 447.55 135.83 .16 3.295 .001

Ratio)

a. Dependent Variable: PFM

Table 7.12:Model Summary of the independent variables with PFM

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .229a .053 .042 60325.98

123

Table 7.13: ANOVAb of the model

Model Sum of Squares

df Mean Square F Sig.

1 Regression

Residual

Total

8.752E10

1.579E12

1.667E12

5

434

439

1.750E10

3.639E9

4.810 .000a

a. Predictors: (Constant), DE, INTEREST, EPS, MR, DTV

b. Dependent Variable: PFM

7.14 Discussion

1. Managerial Remuneration is negatively correlated to PFM though it is not

statistically significant just like EVA;

2. EPS is positively correlated to PFM unlike EVA and it is statistically

significant;

3. Since the EPS is statistically significantly correlated with PFM, a further

investigation is needed with respect to the impact of Sharebuyback decisions

on shareholder value creation as measured by PFM.

4. Dividend is negatively correlated to PFM though it is not statistically

significant unlike EVA where Dividend has positive correlation;

5. Interest is positively correlated to PFM and is statistically significant at 95%

level of confidence;

6. Debt Equity Ratio, which is used as a proxy for Capital Structure is also

positively correlated to PFM and is statistically significant;

7. ANOVA shows the model to be statistically significant but is more due to

large sample as the R2 of .053 is very small and does not explain any variance

in the dependent variable.

124

The ANOVA tests show the model to have statistical significance in spite of low R 2

due to large sample size.

7.15 Pre & Post PFM of Sharebuybacks

The shareholder value creation as measured by PFM of the sample companies that did

buyback its shares or showed intent to buy back its shares was further evaluated using

"t- test". Table 7.14 shows the average PFM of companies' pre and post

Sharebuybacks.

Table 7.14: Average PFM pre and post Sharebuyback

Average PFM (Rs. Cr.) Pre Buyback

Post Buyback -585.71 -1219.11

Figure 7.4 Average PFM pre and post Sharebuyback

13 Average PFM (Rs. Cr.) Pre

Buyback

1:1 Average PFM (Rs. Cr.) Post Buyback

125

Table 7.15: Paired Samples Test (Share buyback)

Paired Differences

t df Sig. (2- tailed) Mean

Std. Deviation

Error Mean

95% Confidence Interval of the

Difference

Lower Upper

Pair PREPFM - POSTPFM

1029.27 87101.29 5134.21 -8231.67 10641.17 .17 21 .79

Table 7.16: Paired Samples Correlations (Share buyback)

N Correlation Sig.

Pair 1 PREPFM & POSTPFM 223 .021 .713

According to Gupta (2003) major reasons behind Sharebuybacks in India are:

i. Returning to shareholders the surplus cash not required in the foreseeable

future.

ii. Enhancing the earning per share.

iii. Conveying to investors the management's view that the market is currently

undervaluing the company's share in relation to its intrinsic value and that

the proposed buyback will facilitate recognition of the true value.

iv. Stabilising the market price of the company's share.

v. Providing an exit route to shareholders in case of illiquid shares.

vi. Raising the promoters' voting power.

ii. Off-setting the equity dilution caused by allotment of shares against

employee stock option plans.

i. Warding off a takeover threat.

ii. Raising the debt-equity ratio of the company.

126

From Table 7.15 and 7.16 we infer that there is no statistically significant difference

in the mean Shareholder Value Creation as measured by PFM pre and post share

buyback. This only means that the managers do not take the shareholder value

creation in to consideration while considering share buybacks.

One major reason for this could also be the fact that there has been a difference in the

intent of buy back and actual buy back of shares by the companies. The companies

did not end buying back the quantum that they had set out the intent to buy.

Therefore, a lot of companies lost their market price.

Table 7.17 below gives the names of some of the big names from NIFTY companies

who did not match the market expectations in terms of the actual buy back.

Table 7.17 showing the NIFTY company's buy back record

Sr. No Name of the company Year Amount of buyback (Rs. Cr.)

r-4 N

CI") 71- In

■.c) t- ---

oo

S terlite 2000-01 27.95 Hindalco 2001-02 0.01 Siernen 2001-02 2.36 Hindalco 2002-03 0.75 Sterlite 2002-03 10.04 Sun Pharma 2002-03 0.18 Sun Pharma 2003-04 0.24 RIL 2004-05 2.87

Source: http://www.capitaline.com

7.16 Do the Mergers & Acquisitions create Shareholder Value?

A detailed list of Mergers and Acquisitions in India since 1999-2000 till 2010 is given

in Appendix 4. The method of choosing 44 companies is enlisted in the research

methodology.

127

Table 7.18: Paired Samples Test PFM (M&A)

Paired Differences

t df Sig. (2- tailed) Mean

Std.. Deviation

ESrtrdo'r

Mean

95% Confidence Interval of the

Difference

Lower Upper

Pair PREPFM - POSTPFM

829.95 67108.47 5072.92 -9182.44 10842.33 .16 17 .87

Table 7.19: Paired Samples Correlations PFM (M&A)

N Correlation Sig.

Pair 1 PREPFM & POSTPFM 175 .037 .622

Table 7.20: Paired Samples Test EVA (M&A)

Paired Differences

t df Sig. (2- tailed) Mean

Std. Deviation

Std * Error Mean

95% Confidence Interval of the

Difference

Lower Upper

Pair 1

PREEVA - POSTEVA

398.43 17729.38 1982.21 -3547.05 4343.91 .20 79 .841

Table 7.21: Paired Samples Correlations EVA (M&A)

N Correlation Sig.

Pair 1 PREEVA & POSTEVA 80 .033 .774

The research is trying to study the impact of Mergers and Acquisitions on the

shareholder value creation as measured by EVA and PFM. The Mergers and

Acquisitions is a topic of strategic importance and therefore, it can be argued that the

results disseminate over longer time duration. Thus, the research considers a long

term time duration to evaluate the impact of Mergers and Acquisitions on the

128

Pre Merger Post Merger

EVA

■ PFM Pre Merger

■ PFM Post Merger

■ EVA Pre Merger

■ EVA Post Merger

600.00

400.00

200.00

0.00

-200.00

-400.00

-600.00

-800.00

-1000.00

-1200.00

-1400.00

shareholder value creation measures. Appendix 5 shows the pre and post merger EVA

and PFM values of the deals considered above. Table 7.22 shows the average pre

merger and post merger EVA and PFM values for the said sample over the period

under review.

Table 7.22: Average Pre Merger and Post Merger shareholder value creation

values

PFM (Rs. Cr.) EVA (Rs. Cr.) Pre Merger Post Merger Pre Merger Post Merger

-271.82 -1139.23 427.10 170.48

Figure 7.5: Impact of Merger & Acquisition on Shareholder Value Creation as

measured by EVA and PFM

7.17 Discussion

The research tries to answer the question whether the decision taken for a Merger and

Acquisition in reality has any significant impact on the shareholder value creation as

measured by EVA and PFM.

129

1. It is already seen in the discussion on top that not only is there any impact of

managerial remuneration on the shareholder value creation but in fact is

negatively correlated with both measures of value creation studied in this

research. This point is made because a strategic decision such as Mergers and

Acquisition is made by board of directors for which they get remunerated.

2. The research proves that the quality of Mergers and Acquisitions reviewed

have not been value creating. If table 7.22 and figure 1 above are noticed we

see it very clearly that the Shareholder Value destruction has resulted from a

Merger and Acquisition decisions.

3. Pre Merger EVA for the sample was 427.10 crore which declined to 170.48

crore post merger, where as pre merger PFM of the sample was -271.82 crore

and it worsened to -1139.23 crore post merger.

4. The "t — test" as shown in table 7.20 shows there is no statistically significant

difference in average EVA pre and post merger but in absolute terms, as

stated above, show a subtle decline in EVA.

5. The "t — test" as shown in table 7.18 shows there is no statistically significant

difference in average PFM pre and post merger but in absolute terms, as

stated above, show a subtle decline in PFM.

6. The decision to merge should create shareholder value for the acquiring

company as the amount involved in the deal is very high. The managers,

therefore, should keep in mind the impact of their decisions on the shareholder

value irrespective of the measure they use i.e. EVA or PFM.

7. It may be argued the PFM is market based measure and thus, the unrelated

market movements may have impact on the share price and it may not be

completely attributable only to Merger and Acquisition but even EVA, which

130

is based on historical accounting method also projects a decline in value

creation.

7.18 Conclusion

From the discussion given above, we infer following:

1. A very interesting finding is that Managerial Remuneration is negatively

correlated to Shareholder Value Creation as measured by EVA and PFM;

2. Earnings per Share do not significantly impact EVA but has a significant

statistical bearing on PFM. This could be due to the fact that EPS has a direct

impact on Market Price (Pandye, 2010), which is a major input to calculate

PFM. This also shows that strategic decisions like Sharebuybacks do not have

a significant impact on the shareholder value creation in Indian markets;

3. There is no major and statistically significant impact of share buyback on the

average PFM pre and post buyback. Which means that the quantum of buy

back as promised and as actually undertaken is not the same or the managers

do not take in to account impact of Share buyback on the shareholder value.

There is no empirical evidence to prove the later but there is enough data, as

given in Table 7.17 to prove the former point.

4. Capital Structure of a company has statistically significant relationship with

shareholder value creation as measured by EVA and PFM though it is

negatively correlated with EVA and positively correlated with PFM;

5. Interest very strangely is positively correlated with PFM and as is proven by

various researchers in finance is negatively correlated to EVA for Indian

Markets as well. This is because interest directly impacts the WACC where as

it indirectly affects the expected return on equity through CAPM model where

risk free rate of return and beta are inputs. In this equation as well increase in

131

risk free rate of return tends to reduce beta as the markets and stocks find

similar reaction. Also the interest rate movements (unless very high), do not

show to have sizeable impact on the investor's market perceptions in India

(Sriniwasan, 2006);

6. Capital structure as represented by Debt Equity Ratio has statistically

significant relationship with shareholder value creation as measured by EVA

and PFM. Strangely, however, the study proves that capital structure is

negatively correlated to EVA and has positive correlation with PFM. This is

because the capital structure directly impacts the WACC which is a major

input for EVA, whereas, the equity shareholders are happy with a levered

capital structure as it has a positive impact on the EPS which in turn has a

positive impact on the market price, and therefore, the shareholder value

creation as measured by PFM.

7. Managerial Remuneration has a negative correlation (though not statistically

significant) is a very interesting finding. It goes against the basic finance

literature that says "The job of the Board of Directors is to take decisions in

such a manner that maximises Shareholder Value" (Pandye, 2010). It shows

that the managers in NIFTY companies considered to be the best companies

in terms of management practices, stability of returns, market capitalisation,

turnover in the markets, market leadership, etc are the ones where the

managers do not keep in mind the shareholder interest whether considered in

terms of Investment efficiency (PFM) or from operational efficiency (EVA)

view point.

8. With respect to the hypothesis of impact of Dividend on Shareholder Value

Creation, we accept the "null hypothesis" "There is no significant impact of

132

Dividend on the shareholder value creation as measured by EVA and

PFM" and reject the alternative hypothesis "There is significant impact of

Dividend on the shareholder value creation as measured by EVA and

PFM". Also the dividend is negatively correlated to PFM and positively

correlated to EVA, though both correlations are not statistically significant.

9. With respect to hypothesis of impact of Capital Structure on the Shareholder

Value Creation we reject the null hypothesis "There is no significant impact

of Capital Structure on shareholder value creation as measured by EVA

and PFM" and accept the alternative hypothesis "There is significant impact

of Capital Structure on shareholder value creation as measured by EVA

and PFM". Capital structure has a positive correlation with PFM and

negative correlation with EVA and both the correlations are statistically

significant.

10.With respect to hypothesis of relation of Managerial Remuneration with

shareholder value creation, we accept the null hypothesis "There is no

significant impact of MR on the shareholder value creation as measured by

EVA and PFM" and reject the alternative hypothesis "There is significant

impact of MR on shareholder value creation as measured by EVA and

PFM". What is also very interesting to note is Managerial Remuneration is

negatively correlated to shareholder value creation as measured by EVA and

PFM both.

11.With respect to the hypothesis about the impact of Interest Rates on the

Shareholder value creation we accept the null hypothesis that "There is no

significant impact of Interest Rates on the shareholder value creation as

measured by PFM" but we reject the null hypothesis "There is no significant

133

impact of Interest Rates on the shareholder value creation as measured by

EVA" and thus, reject the alternative hypothesis "There is significant impact

of Interest Rates on the shareholder value creation as measured by PFM"

accept the alternative hypothesis "There is significant impact of Interest

Rates on the shareholder value creation as measured by EVA". Interest rate

is significantly negatively correlated to EVA and has positive correlation with

PFM which is not statistically significant.

12. With respect to hypothesis on Earnings per share, which is used as proxy for

Sharebuyback we accept the null hypothesis vis-a-vis EVA "There is no

significant impact of Sharebuyback on the shareholder value creation as

measured by EVA" and therefore, reject the alternative hypothesis that

"There is significant impact of Sharebuyback on the shareholder value

creation as measured by EVA".

For PFM, however we reject the null hypothesis "There is no significant

impact of Sharebuyback on the shareholder value creation as measured by

PFM" and accept the alternative hypothesis "There is no significant impact

of Sharebuyback on the shareholder value creation as measured by PFM".

13. The "t-test" for pre and post merger is statistically insignificant towards

shareholder value creation as measured by both PFM and EVA. We, therefore,

accept the null hypothesis "There is no significant impact of M&A on the

shareholder value creation as measured by EVA and PFM" and reject the

alternative hypothesis "There is significant impact of M&A on the

shareholder value creation as measured by EVA and PFM"

134

WACC

Return

SVC = Return - WACC

14. The model that we started with in the section above is redone on the basis of

the results that the research has thrown open with respect to the Shareholder

Value Creation as measured by EVA and PFM

Figure 7.6 Model showing factors affecting EVA

Macroeconomic:

Interest

Financial:

Capital Structure

Figure 7.7 Model showing factors affecting PFM

Strategic:

Sharebuyback

Financial:

Capital Structure

SVC =

Return - WACC

135