Embed Size (px)

Citation preview

This presentation includes forward-looking statements. Actual future conditions (including economic conditions, energy demand, and energy supply) could differ materially due to changes in technology,

the development of new supply sources, political events, demographic changes, and other factors discussed herein (and in Item 1A of ExxonMobil’s latest report on Form 10-K or information set forth

under "factors affecting future results" on the "investors" page of our website at www.exxonmobil.com). This material is not to be reproduced without the permission of Exxon Mobil Corporation.

Crude to Chemicals Technology Solutions

David Ayrapetyan

29 July 2017

6th Petrochemical Conclave, Gandhinagar, Gujarat, India

2

Discussion topics

• Global chemicals growth

• Crude to Chemical complexes

• Enabling technologies

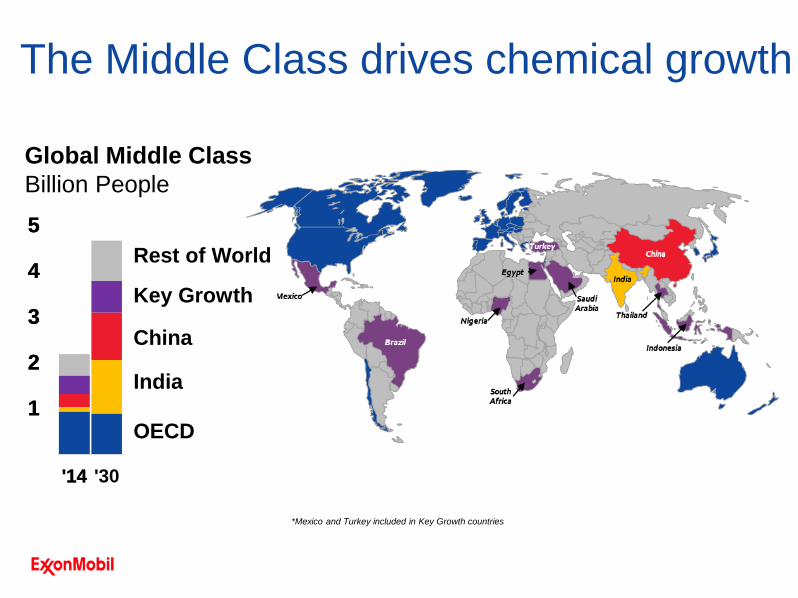

*Mexico and Turkey included in Key Growth countries

Global Middle Class

Billion People

China

India

Key Growth

Rest of World

OECD1

2

3

4

5

'14 '30

The Middle Class drives chemical growth

China

India

Key Growth

Rest of World

OECD1

2

3

4

5

'14 '30

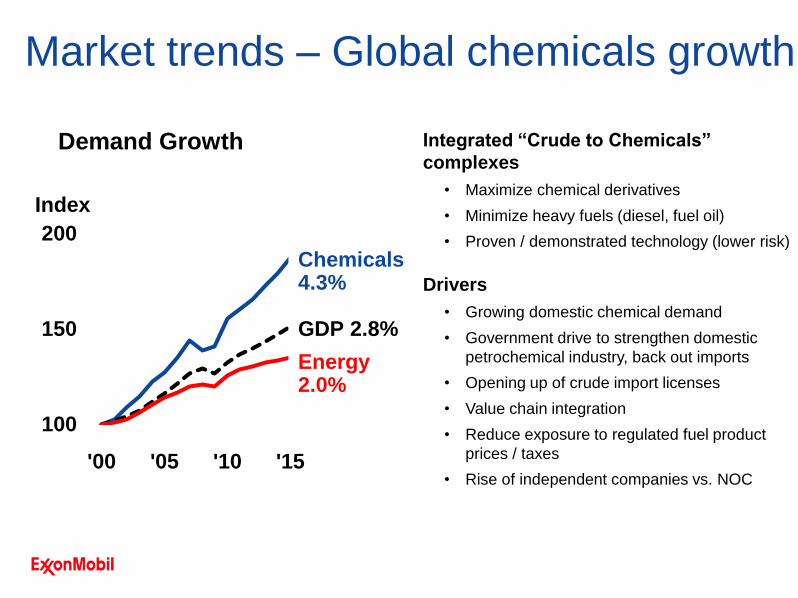

100

150

200

'00 '05 '10 '15

GDP 2.8%

Energy 2.0%

Chemicals 4.3%

Index

NA/EUROW

Asia

Demand Growth

Market trends – Global chemicals growth

Integrated “Crude to Chemicals”

complexes

• Maximize chemical derivatives

• Minimize heavy fuels (diesel, fuel oil)

• Proven / demonstrated technology (lower risk)

Drivers

• Growing domestic chemical demand

• Government drive to strengthen domestic

petrochemical industry, back out imports

• Opening up of crude import licenses

• Value chain integration

• Reduce exposure to regulated fuel product

prices / taxes

• Rise of independent companies vs. NOC

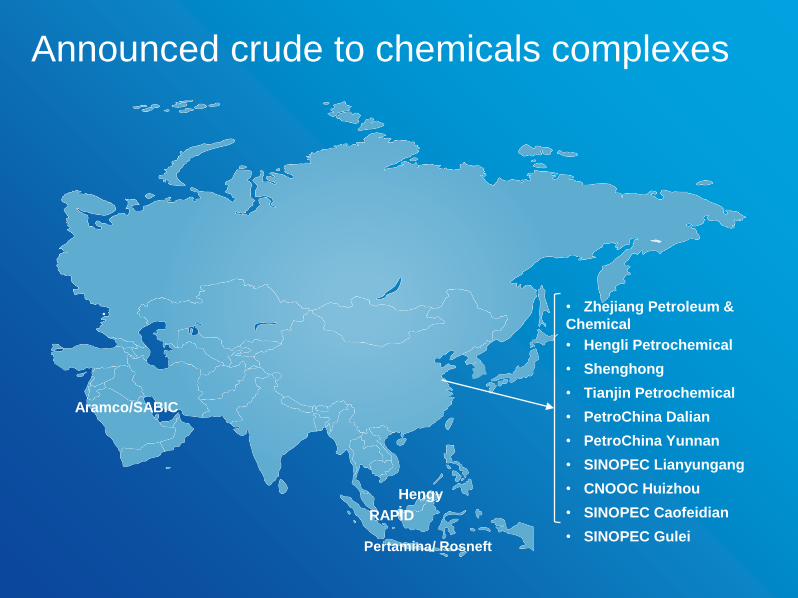

Announced crude to chemicals complexes

Pertamina/ Rosneft

• Zhejiang Petroleum &

Chemical

• Hengli Petrochemical

• Shenghong

• Tianjin Petrochemical

• PetroChina Dalian

• PetroChina Yunnan

• SINOPEC Lianyungang

• CNOOC Huizhou

• SINOPEC Caofeidian

• SINOPEC Gulei

Hengy

i

Aramco/SABIC

RAPID

0

20

40

60

80

100

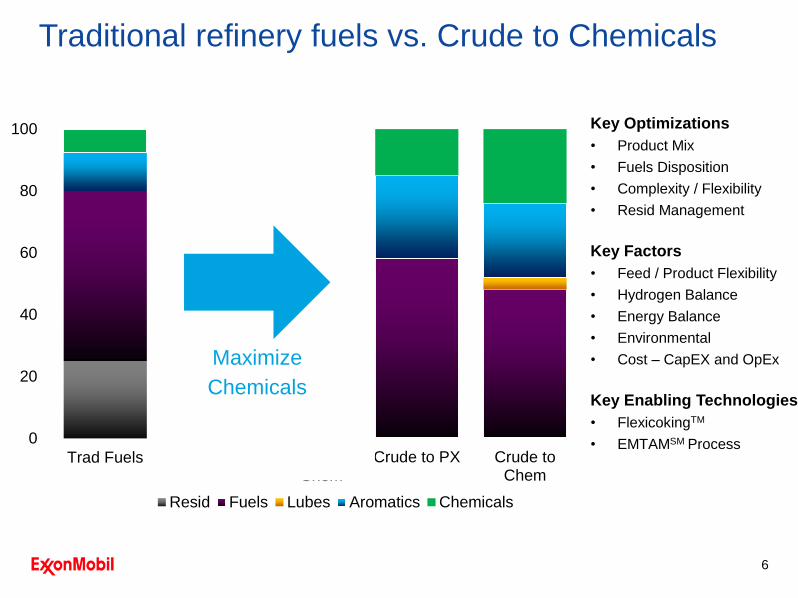

Trad Fuels Crude to PX Crude toChem

Resid Fuels Lubes Aromatics Chemicals

Traditional refinery fuels vs. Crude to Chemicals

6

0

20

40

60

80

100

Trad Fuels Crude to PX Crude toChem

Maximize

Chemicals

Key Optimizations

• Product Mix

• Fuels Disposition

• Complexity / Flexibility

• Resid Management

Key Factors

• Feed / Product Flexibility

• Hydrogen Balance

• Energy Balance

• Environmental

• Cost – CapEX and OpEx

Key Enabling Technologies

• FlexicokingTM

• EMTAMSM Process

FlexicokingTM

7

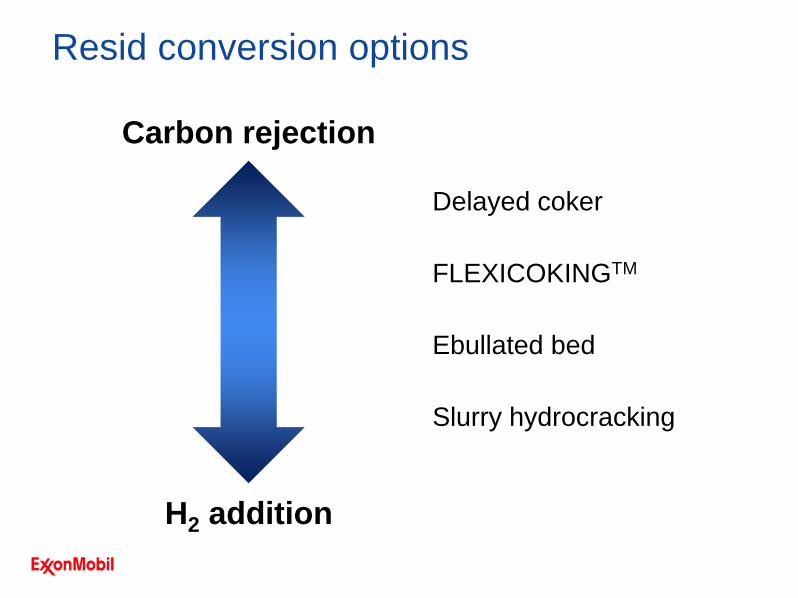

Resid conversion options

Delayed coker

FLEXICOKINGTM

Ebullated bed

Slurry hydrocracking

Carbon rejection

H2 addition

9

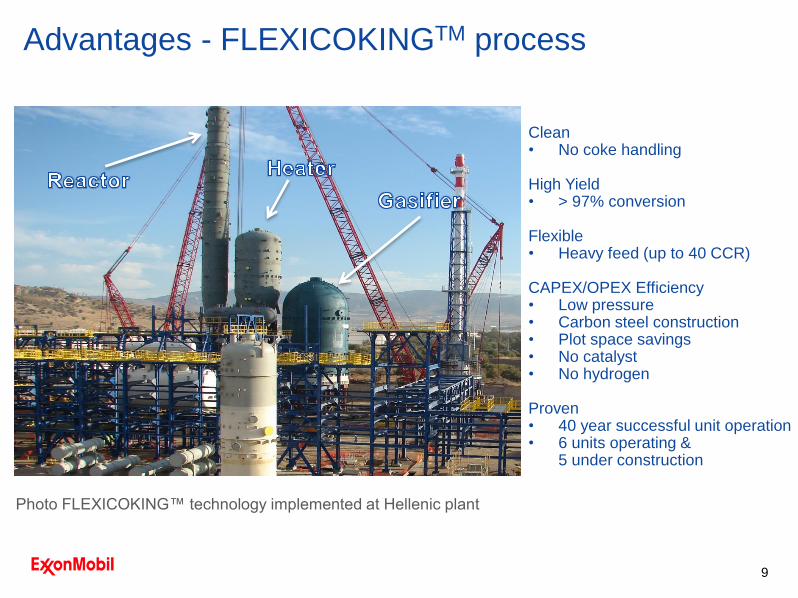

Clean• No coke handling

High Yield• > 97% conversion

Flexible• Heavy feed (up to 40 CCR)

CAPEX/OPEX Efficiency• Low pressure• Carbon steel construction• Plot space savings• No catalyst• No hydrogen

Proven• 40 year successful unit operation• 6 units operating &

5 under construction

Advantages - FLEXICOKINGTM process

Photo FLEXICOKING™ technology implemented at Hellenic plant

10

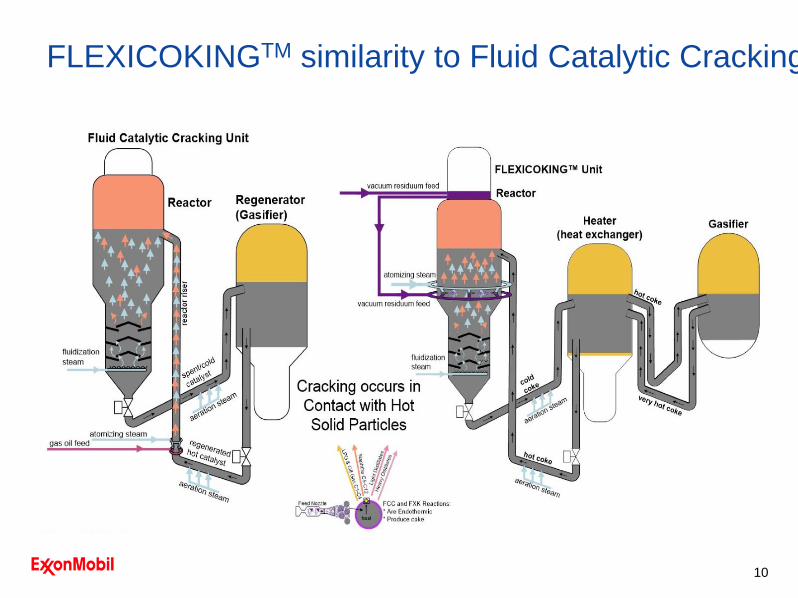

FLEXICOKINGTM similarity to Fluid Catalytic Cracking

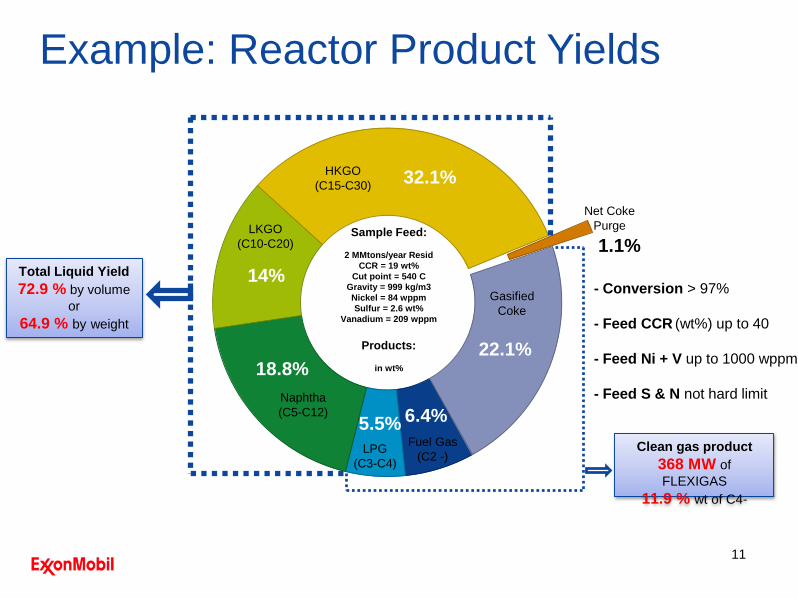

6.4%5.5%

18.8%

14%

32.1%

1.1%

22.1%

Example: Reactor Product Yields

Sample Feed:

2 MMtons/year Resid

CCR = 19 wt%

Cut point = 540 C

Gravity = 999 kg/m3

Nickel = 84 wppm

Sulfur = 2.6 wt%

Vanadium = 209 wppm

Products:

in wt%

11

Gasified

Coke

HKGO

(C15-C30)

LKGO

(C10-C20)

Naphtha

(C5-C12)

LPG

(C3-C4)

Fuel Gas

(C2 -)

Net Coke

Purge

Total Liquid Yield

72.9 % by volume

or

64.9 % by weight

Clean gas product

368 MW of

FLEXIGAS

11.9 % wt of C4-

- Conversion > 97%

- Feed CCR (wt%) up to 40

- Feed Ni + V up to 1000 wppm

- Feed S & N not hard limit

FLEXIGAS –fired in plant furnaces and boilers

FLEXIGAS firing

FLEXICOKINGTM

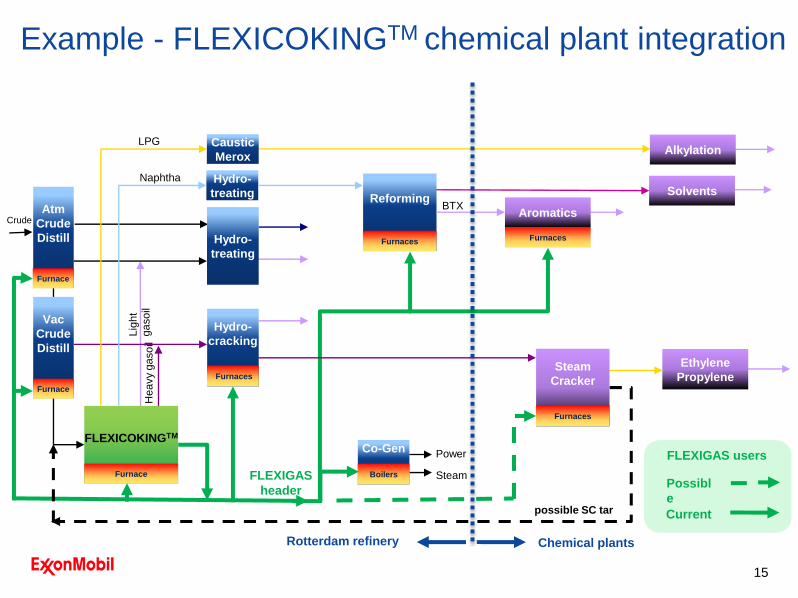

chemical plant integration in existing operating plant

Example - FLEXICOKINGTM chemical plant integration

15

Hydro-

treating

Atm

Crude

Distill

Vac

Crude

Distill

Hydro-

cracking

Furnaces

Co-GenFLEXICOKINGTM

FLEXIGAS

header

Power

Steam

Furnace

Furnace

BoilersFurnace

Hydro-

treating

Caustic

MeroxAlkylation

Reforming

Furnaces

Aromatics

Solvents

Steam

Cracker

Furnaces

Ethylene

Propylene

Furnaces

Crude

Naphtha

LPGLig

ht

ga

soil

Hea

vy g

asoil

BTX

FLEXIGAS users

Current

Possibl

e

Chemical plantsRotterdam refinery

possible SC tar

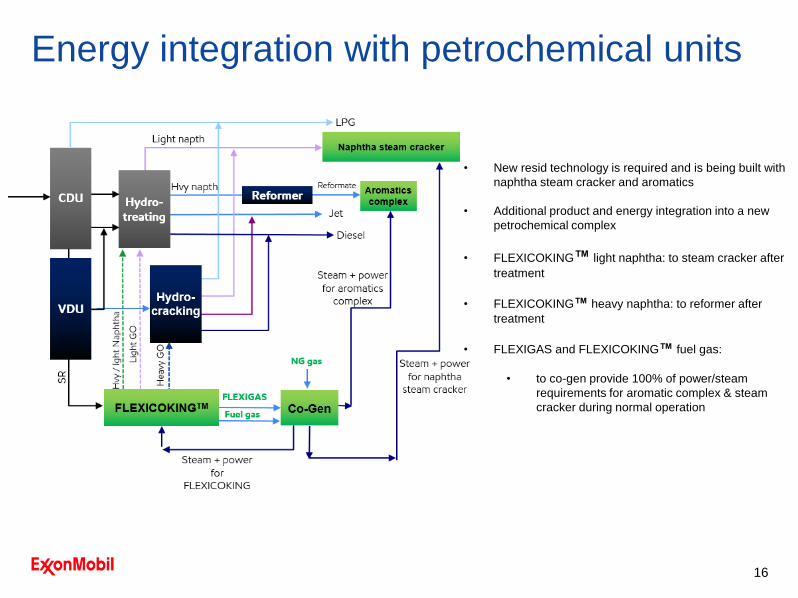

Energy integration with petrochemical units

16

• New resid technology is required and is being built with

naphtha steam cracker and aromatics

• Additional product and energy integration into a new

petrochemical complex

• FLEXICOKING™ light naphtha: to steam cracker after

treatment

• FLEXICOKING™ heavy naphtha: to reformer after

treatment

• FLEXIGAS and FLEXICOKING™ fuel gas:

• to co-gen provide 100% of power/steam

requirements for aromatic complex & steam

cracker during normal operation

©2016 ExxonMobil. ExxonMobil, the ExxonMobil logo, the interlocking “X” device and other product or service names used herein are trademarks of

ExxonMobil, unless indicated otherwise. This document may not be distributed, displayed, copied or altered without ExxonMobil's prior written

authorization. To the extent ExxonMobil authorizes distributing, displaying and/or copying of this document, the user may do so only if the document is

unaltered and complete, including all of its headers, footers, disclaimers and other information. You may not copy this document to or reproduce it in

whole or in part on a website. ExxonMobil does not guarantee the typical (or other) values. Any data included herein is based upon analysis of

representative samples and not the actual product shipped. The information in this document relates only to the named product or materials when not in

combination with any other product or materials. We based the information on data believed to be reliable on the date compiled, but we do not represent,

warrant, or otherwise guarantee, expressly or impliedly, the merchantability, fitness for a particular purpose, freedom from patent infringement, suitability,

accuracy, reliability, or completeness of this information or the products, materials or processes described. The user is solely responsible for all

determinations regarding any use of material or product and any process in its territories of interest. We expressly disclaim liability for any loss, damage

or injury directly or indirectly suffered or incurred as a result of or related to anyone using or relying on any of the information in this document. This

document is not an endorsement of any non-ExxonMobil product or process, and we expressly disclaim any contrary implication. The terms “we,” “our,”

"ExxonMobil Chemical" and "ExxonMobil" are each used for convenience, and may include any one or more of ExxonMobil Chemical Company, Exxon

Mobil Corporation, or any affiliate either directly or indirectly stewarded.