Embed Size (px)

Citation preview

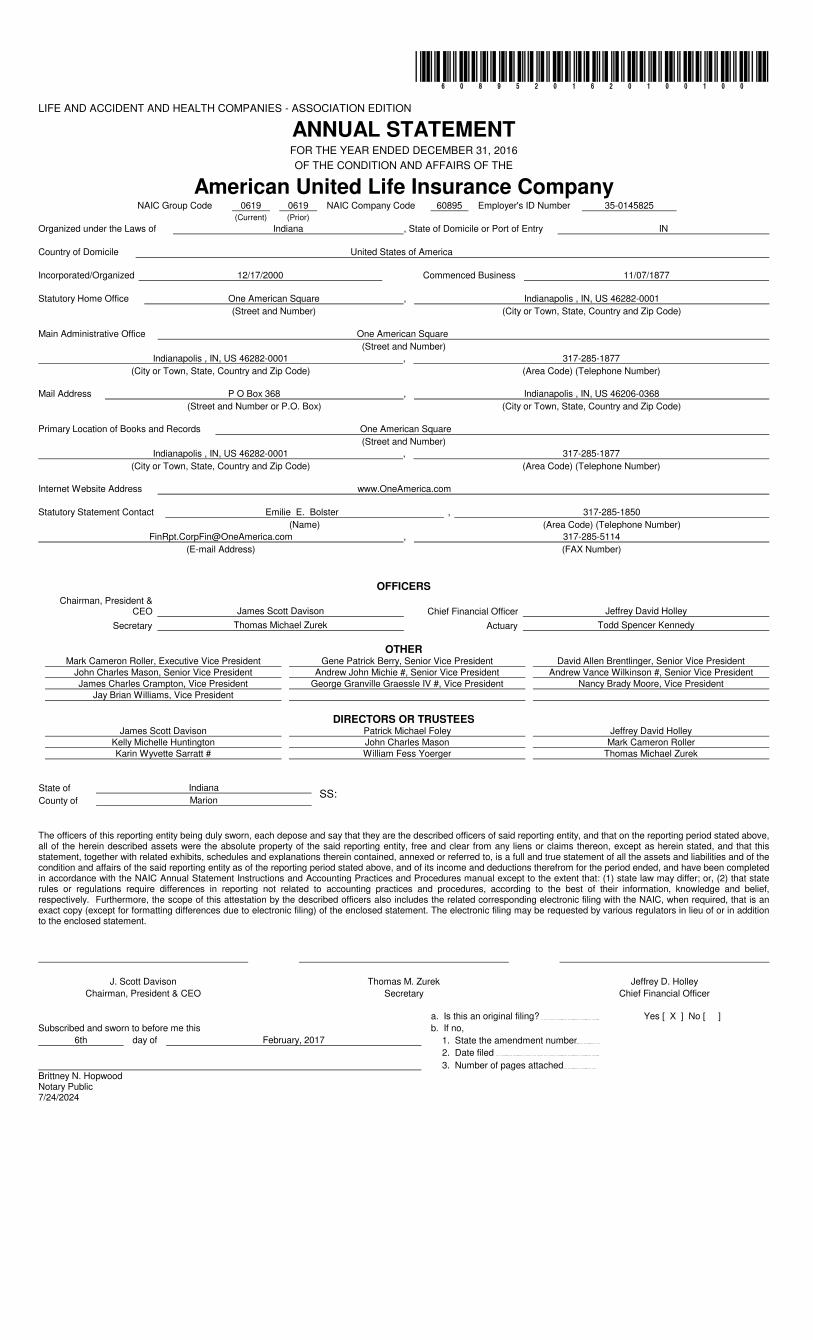

*60895201620100100*LIFE AND ACCIDENT AND HEALTH COMPANIES - ASSOCIATION EDITION

ANNUAL STATEMENTFOR THE YEAR ENDED DECEMBER 31, 2016

OF THE CONDITION AND AFFAIRS OF THE

American United Life Insurance Company NAIC Group Code 0619 0619 NAIC Company Code 60895 Employer's ID Number 35-0145825

(Current) (Prior)

Organized under the Laws of Indiana , State of Domicile or Port of Entry IN

Country of Domicile United States of America

Incorporated/Organized 12/17/2000 Commenced Business 11/07/1877

Statutory Home Office One American Square , Indianapolis , IN, US 46282-0001

(Street and Number) (City or Town, State, Country and Zip Code)

Main Administrative Office One American Square

(Street and Number)

Indianapolis , IN, US 46282-0001 , 317-285-1877

(City or Town, State, Country and Zip Code) (Area Code) (Telephone Number)

Mail Address P O Box 368 , Indianapolis , IN, US 46206-0368

(Street and Number or P.O. Box) (City or Town, State, Country and Zip Code)

Primary Location of Books and Records One American Square

(Street and Number)

Indianapolis , IN, US 46282-0001 , 317-285-1877

(City or Town, State, Country and Zip Code) (Area Code) (Telephone Number)

Internet Website Address www.OneAmerica.com

Statutory Statement Contact Emilie E. Bolster , 317-285-1850

(Name) (Area Code) (Telephone Number)

[email protected] , 317-285-5114

(E-mail Address) (FAX Number)

OFFICERS

Chairman, President & CEO James Scott Davison Chief Financial Officer Jeffrey David Holley

Secretary Thomas Michael Zurek Actuary Todd Spencer Kennedy

OTHERMark Cameron Roller, Executive Vice President Gene Patrick Berry, Senior Vice President David Allen Brentlinger, Senior Vice President

John Charles Mason, Senior Vice President Andrew John Michie #, Senior Vice President Andrew Vance Wilkinson #, Senior Vice President James Charles Crampton, Vice President George Granville Graessle IV #, Vice President Nancy Brady Moore, Vice President

Jay Brian Williams, Vice President

DIRECTORS OR TRUSTEESJames Scott Davison Patrick Michael Foley Jeffrey David Holley

Kelly Michelle Huntington John Charles Mason Mark Cameron Roller Karin Wyvette Sarratt # William Fess Yoerger Thomas Michael Zurek

SS:State of Indiana

County of Marion

The officers of this reporting entity being duly sworn, each depose and say that they are the described officers of said reporting entity, and that on the reporting period stated above, all of the herein described assets were the absolute property of the said reporting entity, free and clear from any liens or claims thereon, except as herein stated, and that this statement, together with related exhibits, schedules and explanations therein contained, annexed or referred to, is a full and true statement of all the assets and liabilities and of the condition and affairs of the said reporting entity as of the reporting period stated above, and of its income and deductions therefrom for the period ended, and have been completed in accordance with the NAIC Annual Statement Instructions and Accounting Practices and Procedures manual except to the extent that: (1) state law may differ; or, (2) that state rules or regulations require differences in reporting not related to accounting practices and procedures, according to the best of their information, knowledge and belief, respectively. Furthermore, the scope of this attestation by the described officers also includes the related corresponding electronic filing with the NAIC, when required, that is an exact copy (except for formatting differences due to electronic filing) of the enclosed statement. The electronic filing may be requested by various regulators in lieu of or in addition to the enclosed statement.

J. Scott Davison Thomas M. Zurek Jeffrey D. Holley

Chairman, President & CEO Secretary Chief Financial Officer

a. Is this an original filing? Yes [ X ] No [ ]

Subscribed and sworn to before me this b. If no,

6th day of February, 2017 1. State the amendment number

2. Date filed

3. Number of pages attached Brittney N. Hopwood Notary Public 7/24/2024

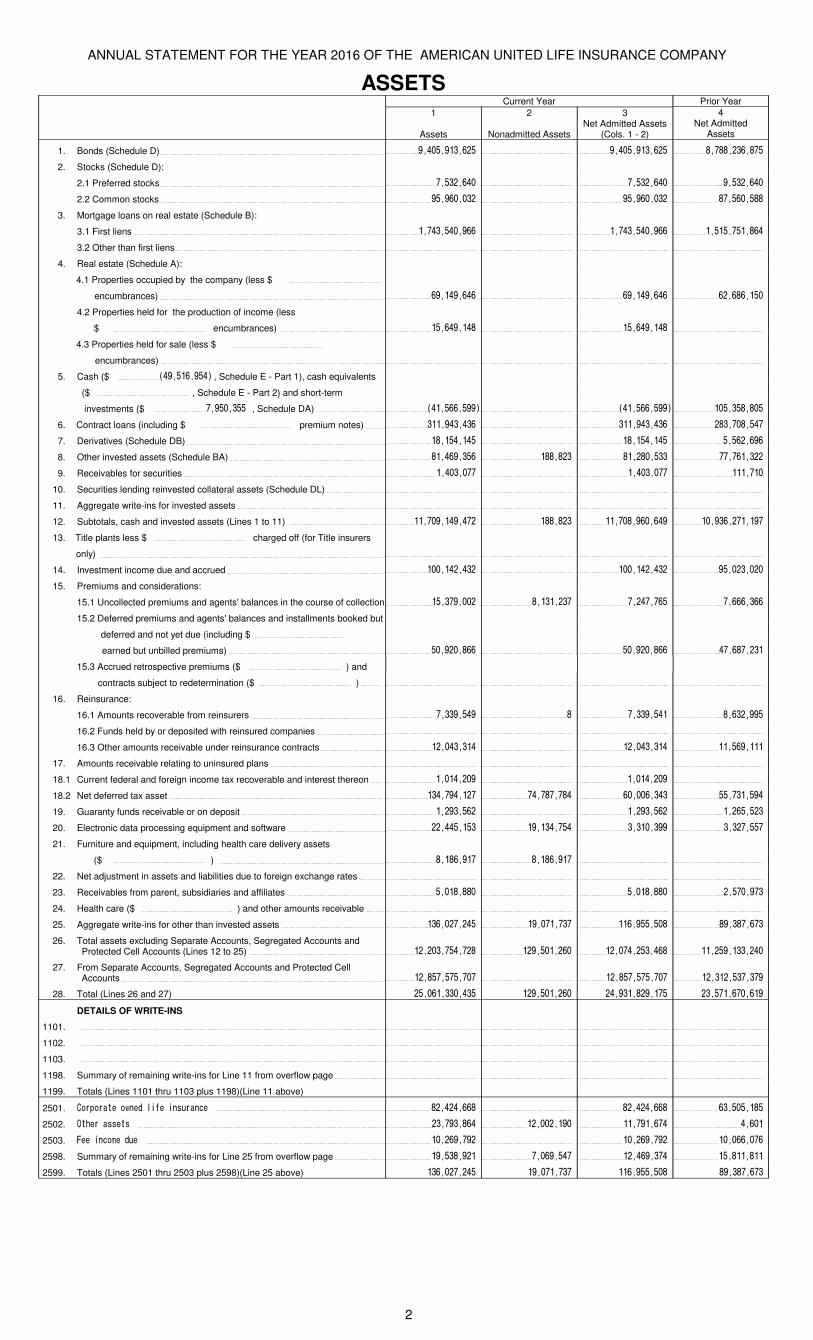

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

ASSETSCurrent Year Prior Year

1

Assets

2

Nonadmitted Assets

3Net Admitted Assets

(Cols. 1 - 2)

4Net Admitted

Assets

1. Bonds (Schedule D) 9,405,913,625 9,405,913,625 8,788,236,875

2. Stocks (Schedule D):

2.1 Preferred stocks 7,532,640 7,532,640 9,532,640

2.2 Common stocks 95,960,032 95,960,032 87,560,588

3. Mortgage loans on real estate (Schedule B):

3.1 First liens 1,743,540,966 1,743,540,966 1,515,751,864

3.2 Other than first liens

4. Real estate (Schedule A):

4.1 Properties occupied by the company (less $

encumbrances) 69,149,646 69,149,646 62,686,150

4.2 Properties held for the production of income (less

$ encumbrances) 15,649,148 15,649,148

4.3 Properties held for sale (less $

encumbrances)

5. Cash ($ (49,516,954) , Schedule E - Part 1), cash equivalents

($ , Schedule E - Part 2) and short-term

investments ($ 7,950,355 , Schedule DA) (41,566,599) (41,566,599) 105,358,805

6. Contract loans (including $ premium notes) 311,943,436 311,943,436 283,708,547

7. Derivatives (Schedule DB) 18,154,145 18,154,145 5,562,696

8. Other invested assets (Schedule BA) 81,469,356 188,823 81,280,533 77,761,322

9. Receivables for securities 1,403,077 1,403,077 111,710

10. Securities lending reinvested collateral assets (Schedule DL)

11. Aggregate write-ins for invested assets

12. Subtotals, cash and invested assets (Lines 1 to 11) 11,709,149,472 188,823 11,708,960,649 10,936,271,197

13. Title plants less $ charged off (for Title insurers

only)

14. Investment income due and accrued 100,142,432 100,142,432 95,023,020

15. Premiums and considerations:

15.1 Uncollected premiums and agents' balances in the course of collection 15,379,002 8,131,237 7,247,765 7,666,366

15.2 Deferred premiums and agents' balances and installments booked but

deferred and not yet due (including $

earned but unbilled premiums) 50,920,866 50,920,866 47,687,231

15.3 Accrued retrospective premiums ($ ) and

contracts subject to redetermination ($ )

16. Reinsurance:

16.1 Amounts recoverable from reinsurers 7,339,549 8 7,339,541 8,632,995

16.2 Funds held by or deposited with reinsured companies

16.3 Other amounts receivable under reinsurance contracts 12,043,314 12,043,314 11,569,111

17. Amounts receivable relating to uninsured plans

18.1 Current federal and foreign income tax recoverable and interest thereon 1,014,209 1,014,209

18.2 Net deferred tax asset 134,794,127 74,787,784 60,006,343 55,731,594

19. Guaranty funds receivable or on deposit 1,293,562 1,293,562 1,265,523

20. Electronic data processing equipment and software 22,445,153 19,134,754 3,310,399 3,327,557

21. Furniture and equipment, including health care delivery assets

($ ) 8,186,917 8,186,917

22. Net adjustment in assets and liabilities due to foreign exchange rates

23. Receivables from parent, subsidiaries and affiliates 5,018,880 5,018,880 2,570,973

24. Health care ($ ) and other amounts receivable

25. Aggregate write-ins for other than invested assets 136,027,245 19,071,737 116,955,508 89,387,673

26. Total assets excluding Separate Accounts, Segregated Accounts and Protected Cell Accounts (Lines 12 to 25) 12,203,754,728 129,501,260 12,074,253,468 11,259,133,240

27. From Separate Accounts, Segregated Accounts and Protected Cell Accounts 12,857,575,707 12,857,575,707 12,312,537,379

28. Total (Lines 26 and 27) 25,061,330,435 129,501,260 24,931,829,175 23,571,670,619

DETAILS OF WRITE-INS

1101.

1102.

1103.

1198. Summary of remaining write-ins for Line 11 from overflow page

1199. Totals (Lines 1101 thru 1103 plus 1198)(Line 11 above)

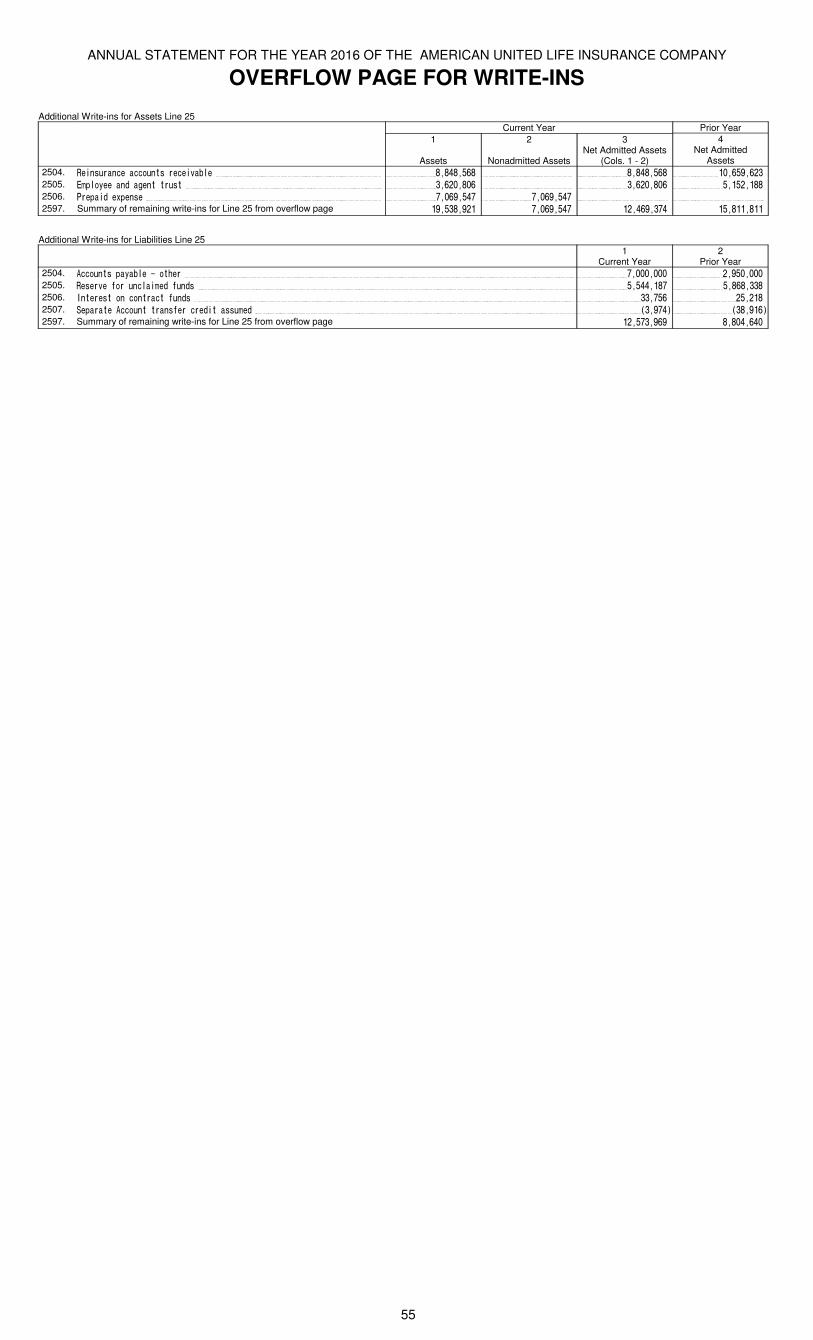

2501. Corporate owned life insurance 82,424,668 82,424,668 63,505,185

2502. Other assets 23,793,864 12,002,190 11,791,674 4,601

2503. Fee income due 10,269,792 10,269,792 10,066,076

2598. Summary of remaining write-ins for Line 25 from overflow page 19,538,921 7,069,547 12,469,374 15,811,811

2599. Totals (Lines 2501 thru 2503 plus 2598)(Line 25 above) 136,027,245 19,071,737 116,955,508 89,387,673

2

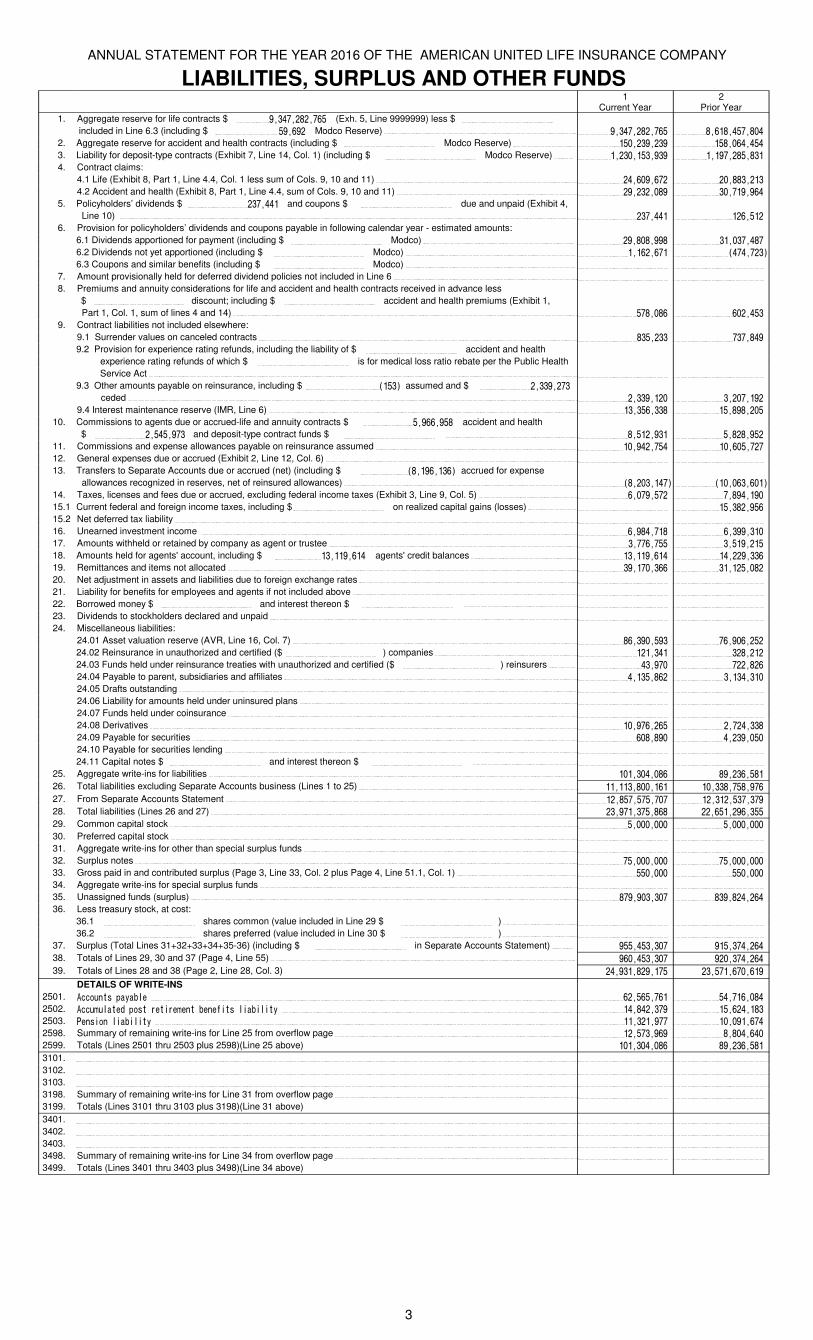

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

LIABILITIES, SURPLUS AND OTHER FUNDS1

Current Year2

Prior Year1. Aggregate reserve for life contracts $ 9,347,282,765 (Exh. 5, Line 9999999) less $

included in Line 6.3 (including $ 59,692 Modco Reserve) 9,347,282,765 8,618,457,804 2. Aggregate reserve for accident and health contracts (including $ Modco Reserve) 150,239,239 158,064,454 3. Liability for deposit-type contracts (Exhibit 7, Line 14, Col. 1) (including $ Modco Reserve) 1,230,153,939 1,197,285,831 4. Contract claims:

4.1 Life (Exhibit 8, Part 1, Line 4.4, Col. 1 less sum of Cols. 9, 10 and 11) 24,609,672 20,883,213 4.2 Accident and health (Exhibit 8, Part 1, Line 4.4, sum of Cols. 9, 10 and 11) 29,232,089 30,719,964

5. Policyholders’ dividends $ 237,441 and coupons $ due and unpaid (Exhibit 4,

Line 10) 237,441 126,512 6. Provision for policyholders’ dividends and coupons payable in following calendar year - estimated amounts:

6.1 Dividends apportioned for payment (including $ Modco) 29,808,998 31,037,487 6.2 Dividends not yet apportioned (including $ Modco) 1,162,671 (474,723)6.3 Coupons and similar benefits (including $ Modco)

7. Amount provisionally held for deferred dividend policies not included in Line 6 8. Premiums and annuity considerations for life and accident and health contracts received in advance less

$ discount; including $ accident and health premiums (Exhibit 1,

Part 1, Col. 1, sum of lines 4 and 14) 578,086 602,453 9. Contract liabilities not included elsewhere:

9.1 Surrender values on canceled contracts 835,233 737,849 9.2 Provision for experience rating refunds, including the liability of $ accident and health

experience rating refunds of which $ is for medical loss ratio rebate per the Public Health

Service Act 9.3 Other amounts payable on reinsurance, including $ (153) assumed and $ 2,339,273

ceded 2,339,120 3,207,192 9.4 Interest maintenance reserve (IMR, Line 6) 13,356,338 15,898,205

10. Commissions to agents due or accrued-life and annuity contracts $ 5,966,958 accident and health

$ 2,545,973 and deposit-type contract funds $ 8,512,931 5,828,952 11. Commissions and expense allowances payable on reinsurance assumed 10,942,754 10,605,727 12. General expenses due or accrued (Exhibit 2, Line 12, Col. 6) 13. Transfers to Separate Accounts due or accrued (net) (including $ (8,196,136) accrued for expense

allowances recognized in reserves, net of reinsured allowances) (8,203,147) (10,063,601)14. Taxes, licenses and fees due or accrued, excluding federal income taxes (Exhibit 3, Line 9, Col. 5) 6,079,572 7,894,190 15.1 Current federal and foreign income taxes, including $ on realized capital gains (losses) 15,382,956 15.2 Net deferred tax liability 16. Unearned investment income 6,984,718 6,399,310 17. Amounts withheld or retained by company as agent or trustee 3,776,755 3,519,215 18. Amounts held for agents' account, including $ 13,119,614 agents' credit balances 13,119,614 14,229,336 19. Remittances and items not allocated 39,170,366 31,125,082 20. Net adjustment in assets and liabilities due to foreign exchange rates 21. Liability for benefits for employees and agents if not included above 22. Borrowed money $ and interest thereon $ 23. Dividends to stockholders declared and unpaid 24. Miscellaneous liabilities:

24.01 Asset valuation reserve (AVR, Line 16, Col. 7) 86,390,593 76,906,252 24.02 Reinsurance in unauthorized and certified ($ ) companies 121,341 328,212 24.03 Funds held under reinsurance treaties with unauthorized and certified ($ ) reinsurers 43,970 722,826 24.04 Payable to parent, subsidiaries and affiliates 4,135,862 3,134,310 24.05 Drafts outstanding 24.06 Liability for amounts held under uninsured plans 24.07 Funds held under coinsurance 24.08 Derivatives 10,976,265 2,724,338 24.09 Payable for securities 608,890 4,239,050 24.10 Payable for securities lending 24.11 Capital notes $ and interest thereon $

25. Aggregate write-ins for liabilities 101,304,086 89,236,581 26. Total liabilities excluding Separate Accounts business (Lines 1 to 25) 11,113,800,161 10,338,758,976 27. From Separate Accounts Statement 12,857,575,707 12,312,537,379 28. Total liabilities (Lines 26 and 27) 23,971,375,868 22,651,296,355 29. Common capital stock 5,000,000 5,000,000 30. Preferred capital stock 31. Aggregate write-ins for other than special surplus funds 32. Surplus notes 75,000,000 75,000,000 33. Gross paid in and contributed surplus (Page 3, Line 33, Col. 2 plus Page 4, Line 51.1, Col. 1) 550,000 550,000 34. Aggregate write-ins for special surplus funds 35. Unassigned funds (surplus) 879,903,307 839,824,264 36. Less treasury stock, at cost:

36.1 shares common (value included in Line 29 $ ) 36.2 shares preferred (value included in Line 30 $ )

37. Surplus (Total Lines 31+32+33+34+35-36) (including $ in Separate Accounts Statement) 955,453,307 915,374,264 38. Totals of Lines 29, 30 and 37 (Page 4, Line 55) 960,453,307 920,374,264 39. Totals of Lines 28 and 38 (Page 2, Line 28, Col. 3) 24,931,829,175 23,571,670,619

DETAILS OF WRITE-INS

2501. Accounts payable 62,565,761 54,716,084 2502. Accumulated post retirement benefits liability 14,842,379 15,624,183 2503. Pension liability 11,321,977 10,091,674 2598. Summary of remaining write-ins for Line 25 from overflow page 12,573,969 8,804,640 2599. Totals (Lines 2501 thru 2503 plus 2598)(Line 25 above) 101,304,086 89,236,581 3101.

3102.

3103.

3198. Summary of remaining write-ins for Line 31 from overflow page 3199. Totals (Lines 3101 thru 3103 plus 3198)(Line 31 above) 3401.

3402.

3403.

3498. Summary of remaining write-ins for Line 34 from overflow page 3499. Totals (Lines 3401 thru 3403 plus 3498)(Line 34 above)

3

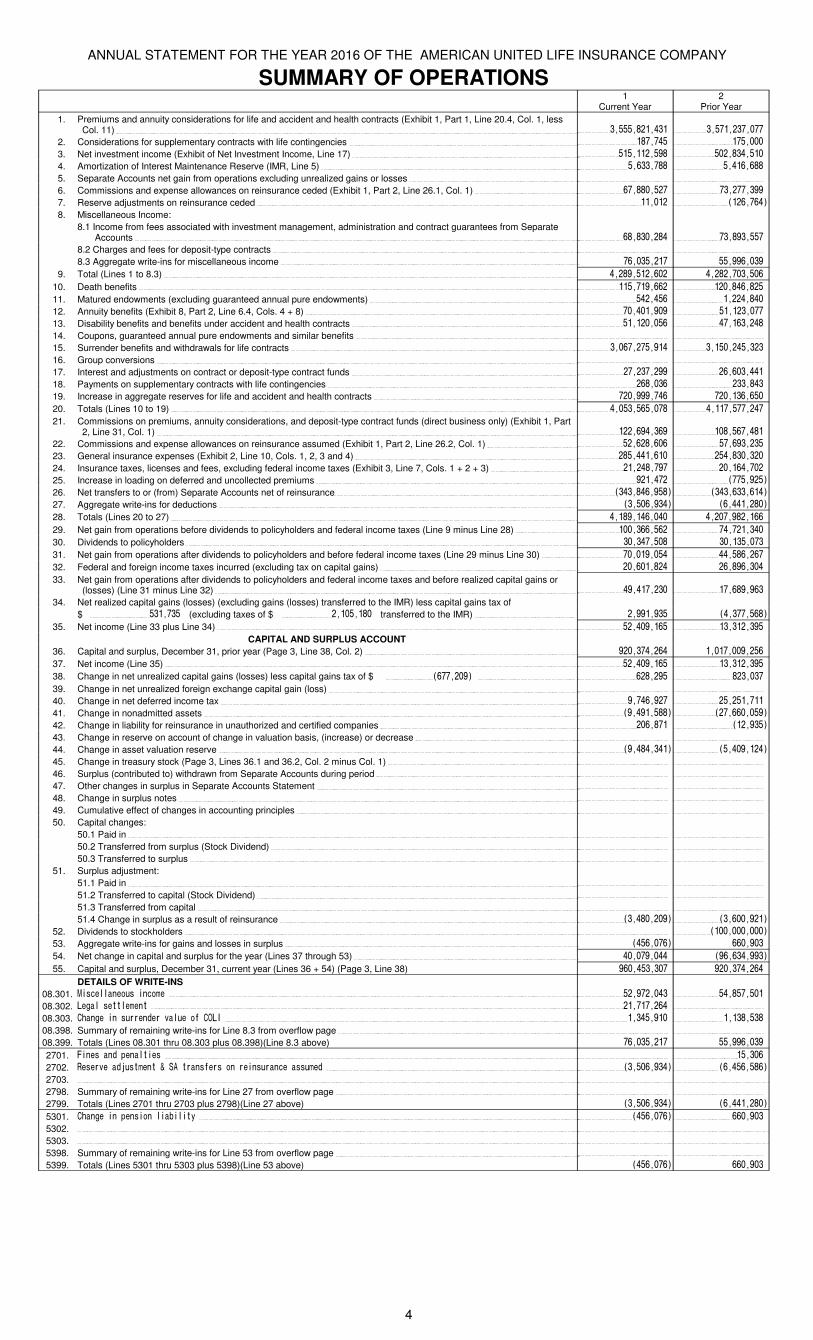

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

SUMMARY OF OPERATIONS1

Current Year2

Prior Year

1. Premiums and annuity considerations for life and accident and health contracts (Exhibit 1, Part 1, Line 20.4, Col. 1, less Col. 11) 3,555,821,431 3,571,237,077

2. Considerations for supplementary contracts with life contingencies 187,745 175,000

3. Net investment income (Exhibit of Net Investment Income, Line 17) 515,112,598 502,834,510

4. Amortization of Interest Maintenance Reserve (IMR, Line 5) 5,633,788 5,416,688

5. Separate Accounts net gain from operations excluding unrealized gains or losses

6. Commissions and expense allowances on reinsurance ceded (Exhibit 1, Part 2, Line 26.1, Col. 1) 67,880,527 73,277,399

7. Reserve adjustments on reinsurance ceded 11,012 (126,764)

8. Miscellaneous Income:

8.1 Income from fees associated with investment management, administration and contract guarantees from Separate Accounts 68,830,284 73,893,557

8.2 Charges and fees for deposit-type contracts

8.3 Aggregate write-ins for miscellaneous income 76,035,217 55,996,039

9. Total (Lines 1 to 8.3) 4,289,512,602 4,282,703,506

10. Death benefits 115,719,662 120,846,825

11. Matured endowments (excluding guaranteed annual pure endowments) 542,456 1,224,840

12. Annuity benefits (Exhibit 8, Part 2, Line 6.4, Cols. 4 + 8) 70,401,909 51,123,077

13. Disability benefits and benefits under accident and health contracts 51,120,056 47,163,248

14. Coupons, guaranteed annual pure endowments and similar benefits

15. Surrender benefits and withdrawals for life contracts 3,067,275,914 3,150,245,323

16. Group conversions

17. Interest and adjustments on contract or deposit-type contract funds 27,237,299 26,603,441

18. Payments on supplementary contracts with life contingencies 268,036 233,843

19. Increase in aggregate reserves for life and accident and health contracts 720,999,746 720,136,650

20. Totals (Lines 10 to 19) 4,053,565,078 4,117,577,247

21. Commissions on premiums, annuity considerations, and deposit-type contract funds (direct business only) (Exhibit 1, Part 2, Line 31, Col. 1) 122,694,369 108,567,481

22. Commissions and expense allowances on reinsurance assumed (Exhibit 1, Part 2, Line 26.2, Col. 1) 52,628,606 57,693,235

23. General insurance expenses (Exhibit 2, Line 10, Cols. 1, 2, 3 and 4) 285,441,610 254,830,320

24. Insurance taxes, licenses and fees, excluding federal income taxes (Exhibit 3, Line 7, Cols. 1 + 2 + 3) 21,248,797 20,164,702

25. Increase in loading on deferred and uncollected premiums 921,472 (775,925)

26. Net transfers to or (from) Separate Accounts net of reinsurance (343,846,958) (343,633,614)

27. Aggregate write-ins for deductions (3,506,934) (6,441,280)

28. Totals (Lines 20 to 27) 4,189,146,040 4,207,982,166

29. Net gain from operations before dividends to policyholders and federal income taxes (Line 9 minus Line 28) 100,366,562 74,721,340

30. Dividends to policyholders 30,347,508 30,135,073

31. Net gain from operations after dividends to policyholders and before federal income taxes (Line 29 minus Line 30) 70,019,054 44,586,267

32. Federal and foreign income taxes incurred (excluding tax on capital gains) 20,601,824 26,896,304

33. Net gain from operations after dividends to policyholders and federal income taxes and before realized capital gains or (losses) (Line 31 minus Line 32) 49,417,230 17,689,963

34. Net realized capital gains (losses) (excluding gains (losses) transferred to the IMR) less capital gains tax of

$ 531,735 (excluding taxes of $ 2,105,180 transferred to the IMR) 2,991,935 (4,377,568)

35. Net income (Line 33 plus Line 34) 52,409,165 13,312,395

CAPITAL AND SURPLUS ACCOUNT

36. Capital and surplus, December 31, prior year (Page 3, Line 38, Col. 2) 920,374,264 1,017,009,256

37. Net income (Line 35) 52,409,165 13,312,395

38. Change in net unrealized capital gains (losses) less capital gains tax of $ (677,209) 628,295 823,037

39. Change in net unrealized foreign exchange capital gain (loss)

40. Change in net deferred income tax 9,746,927 25,251,711

41. Change in nonadmitted assets (9,491,588) (27,660,059)

42. Change in liability for reinsurance in unauthorized and certified companies 206,871 (12,935)

43. Change in reserve on account of change in valuation basis, (increase) or decrease

44. Change in asset valuation reserve (9,484,341) (5,409,124)

45. Change in treasury stock (Page 3, Lines 36.1 and 36.2, Col. 2 minus Col. 1)

46. Surplus (contributed to) withdrawn from Separate Accounts during period

47. Other changes in surplus in Separate Accounts Statement

48. Change in surplus notes

49. Cumulative effect of changes in accounting principles

50. Capital changes:

50.1 Paid in

50.2 Transferred from surplus (Stock Dividend)

50.3 Transferred to surplus

51. Surplus adjustment:

51.1 Paid in

51.2 Transferred to capital (Stock Dividend)

51.3 Transferred from capital

51.4 Change in surplus as a result of reinsurance (3,480,209) (3,600,921)

52. Dividends to stockholders (100,000,000)

53. Aggregate write-ins for gains and losses in surplus (456,076) 660,903

54. Net change in capital and surplus for the year (Lines 37 through 53) 40,079,044 (96,634,993)

55. Capital and surplus, December 31, current year (Lines 36 + 54) (Page 3, Line 38) 960,453,307 920,374,264

DETAILS OF WRITE-INS

08.301. Miscellaneous income 52,972,043 54,857,501

08.302. Legal settlement 21,717,264

08.303. Change in surrender value of COLI 1,345,910 1,138,538

08.398. Summary of remaining write-ins for Line 8.3 from overflow page

08.399. Totals (Lines 08.301 thru 08.303 plus 08.398)(Line 8.3 above) 76,035,217 55,996,039

2701. Fines and penalties 15,306

2702. Reserve adjustment & SA transfers on reinsurance assumed (3,506,934) (6,456,586)

2703.

2798. Summary of remaining write-ins for Line 27 from overflow page

2799. Totals (Lines 2701 thru 2703 plus 2798)(Line 27 above) (3,506,934) (6,441,280)

5301. Change in pension liability (456,076) 660,903

5302.

5303.

5398. Summary of remaining write-ins for Line 53 from overflow page

5399. Totals (Lines 5301 thru 5303 plus 5398)(Line 53 above) (456,076) 660,903

4

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

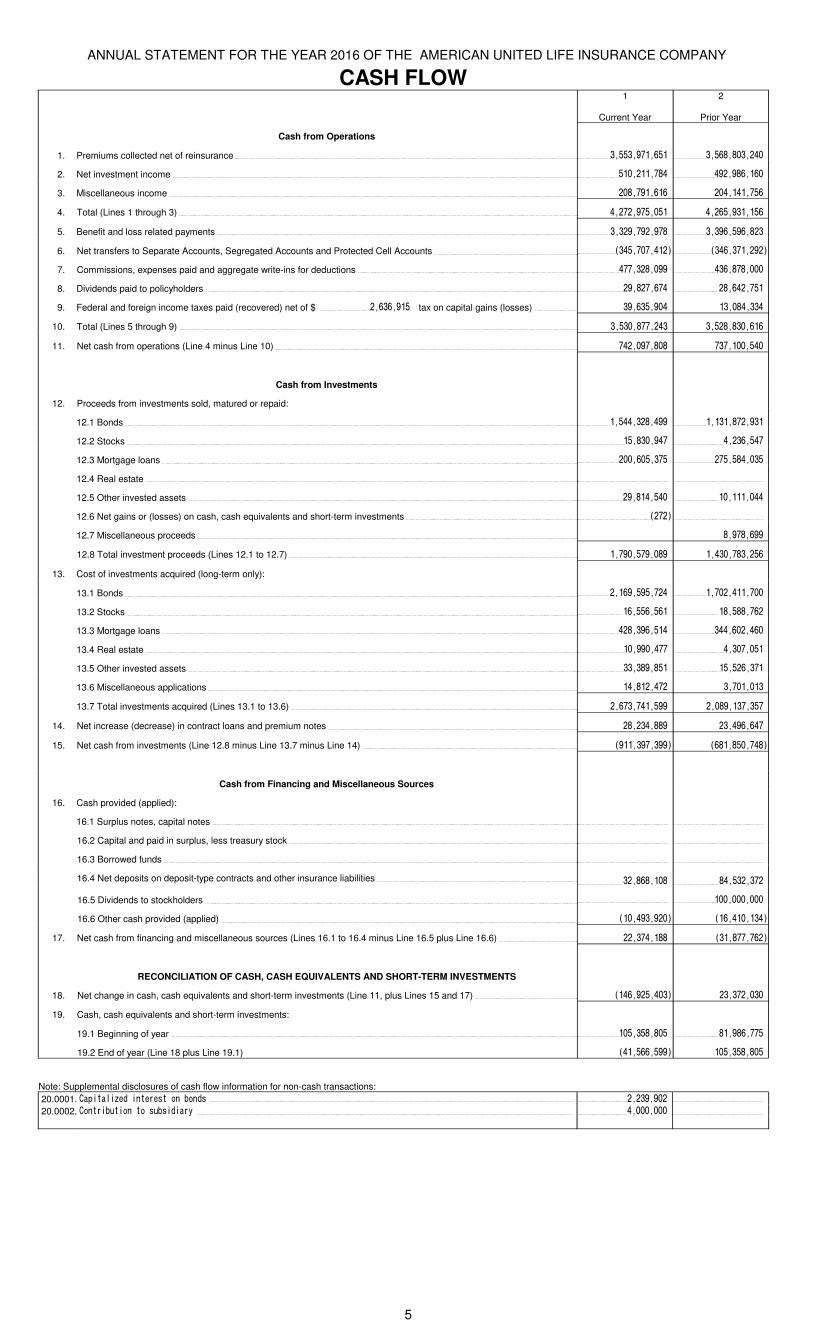

CASH FLOW1

Current Year

2

Prior Year

Cash from Operations

1. Premiums collected net of reinsurance 3,553,971,651 3,568,803,240

2. Net investment income 510,211,784 492,986,160

3. Miscellaneous income 208,791,616 204,141,756

4. Total (Lines 1 through 3) 4,272,975,051 4,265,931,156

5. Benefit and loss related payments 3,329,792,978 3,396,596,823

6. Net transfers to Separate Accounts, Segregated Accounts and Protected Cell Accounts (345,707,412) (346,371,292)

7. Commissions, expenses paid and aggregate write-ins for deductions 477,328,099 436,878,000

8. Dividends paid to policyholders 29,827,674 28,642,751

9. Federal and foreign income taxes paid (recovered) net of $ 2,636,915 tax on capital gains (losses) 39,635,904 13,084,334

10. Total (Lines 5 through 9) 3,530,877,243 3,528,830,616

11. Net cash from operations (Line 4 minus Line 10) 742,097,808 737,100,540

Cash from Investments

12. Proceeds from investments sold, matured or repaid:

12.1 Bonds 1,544,328,499 1,131,872,931

12.2 Stocks 15,830,947 4,236,547

12.3 Mortgage loans 200,605,375 275,584,035

12.4 Real estate

12.5 Other invested assets 29,814,540 10,111,044

12.6 Net gains or (losses) on cash, cash equivalents and short-term investments (272)

12.7 Miscellaneous proceeds 8,978,699

12.8 Total investment proceeds (Lines 12.1 to 12.7) 1,790,579,089 1,430,783,256

13. Cost of investments acquired (long-term only):

13.1 Bonds 2,169,595,724 1,702,411,700

13.2 Stocks 16,556,561 18,588,762

13.3 Mortgage loans 428,396,514 344,602,460

13.4 Real estate 10,990,477 4,307,051

13.5 Other invested assets 33,389,851 15,526,371

13.6 Miscellaneous applications 14,812,472 3,701,013

13.7 Total investments acquired (Lines 13.1 to 13.6) 2,673,741,599 2,089,137,357

14. Net increase (decrease) in contract loans and premium notes 28,234,889 23,496,647

15. Net cash from investments (Line 12.8 minus Line 13.7 minus Line 14) (911,397,399) (681,850,748)

Cash from Financing and Miscellaneous Sources

16. Cash provided (applied):

16.1 Surplus notes, capital notes

16.2 Capital and paid in surplus, less treasury stock

16.3 Borrowed funds

16.4 Net deposits on deposit-type contracts and other insurance liabilities 32,868,108 84,532,372

16.5 Dividends to stockholders 100,000,000

16.6 Other cash provided (applied) (10,493,920) (16,410,134)

17. Net cash from financing and miscellaneous sources (Lines 16.1 to 16.4 minus Line 16.5 plus Line 16.6) 22,374,188 (31,877,762)

RECONCILIATION OF CASH, CASH EQUIVALENTS AND SHORT-TERM INVESTMENTS

18. Net change in cash, cash equivalents and short-term investments (Line 11, plus Lines 15 and 17) (146,925,403) 23,372,030

19. Cash, cash equivalents and short-term investments:

19.1 Beginning of year 105,358,805 81,986,775

19.2 End of year (Line 18 plus Line 19.1) (41,566,599) 105,358,805

Note: Supplemental disclosures of cash flow information for non-cash transactions:

20.0001. Capitalized interest on bonds 2,239,902

20.0002. Contribution to subsidiary 4,000,000

5

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

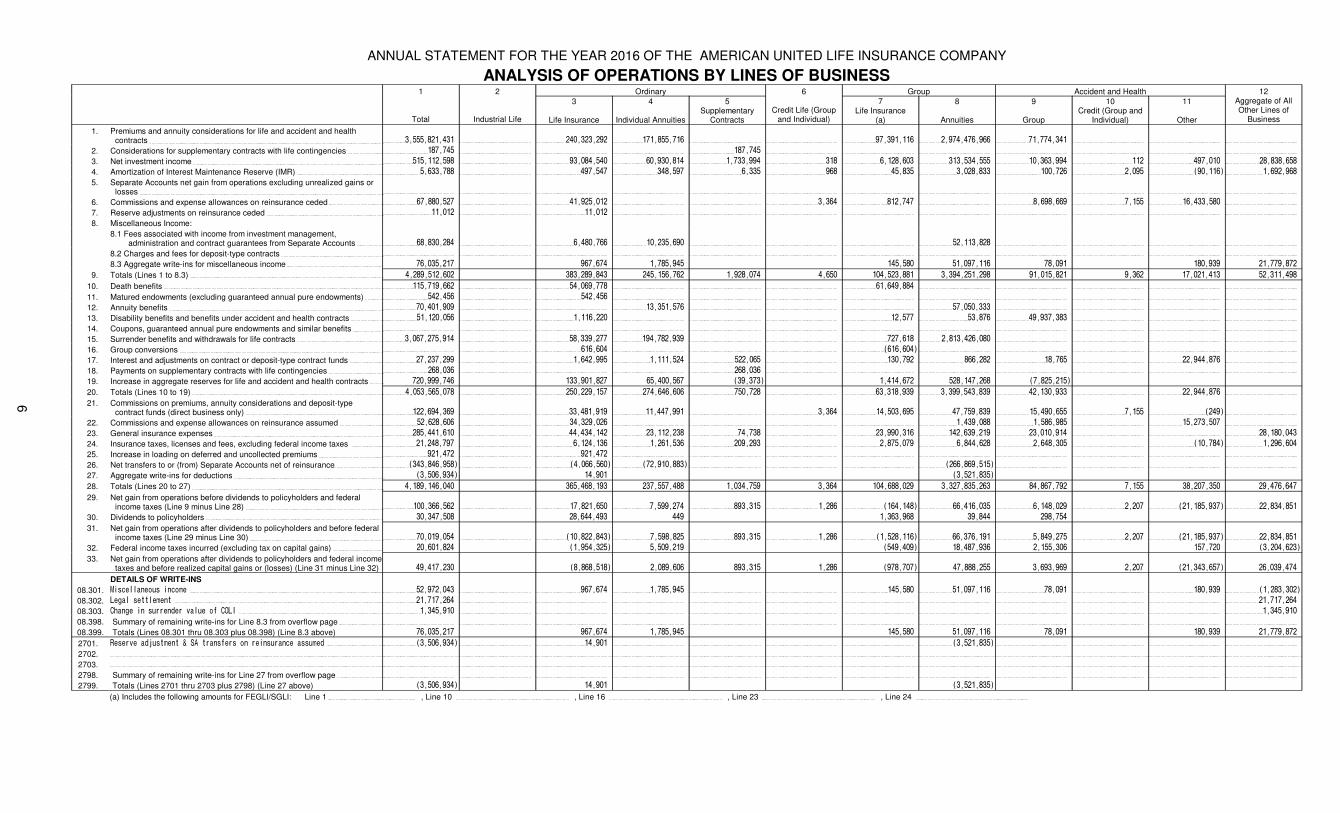

ANALYSIS OF OPERATIONS BY LINES OF BUSINESS1 2 Ordinary 6 Group Accident and Health 12

Total Industrial Life

3

Life Insurance

4

Individual Annuities

5Supplementary

Contracts

Credit Life (Group and Individual)

7Life Insurance

(a)

8

Annuities

9

Group

10Credit (Group and

Individual)

11

Other

Aggregate of All Other Lines of

Business

1. Premiums and annuity considerations for life and accident and health contracts 3,555,821,431 240,323,292 171,855,716 97,391,116 2,974,476,966 71,774,341

2. Considerations for supplementary contracts with life contingencies 187,745 187,745

3. Net investment income 515,112,598 93,084,540 60,930,814 1,733,994 318 6,128,603 313,534,555 10,363,994 112 497,010 28,838,658

4. Amortization of Interest Maintenance Reserve (IMR) 5,633,788 497,547 348,597 6,335 968 45,835 3,028,833 100,726 2,095 (90,116) 1,692,968

5. Separate Accounts net gain from operations excluding unrealized gains or losses

6. Commissions and expense allowances on reinsurance ceded 67,880,527 41,925,012 3,364 812,747 8,698,669 7,155 16,433,580

7. Reserve adjustments on reinsurance ceded 11,012 11,012

8. Miscellaneous Income:

8.1 Fees associated with income from investment management, administration and contract guarantees from Separate Accounts 68,830,284 6,480,766 10,235,690 52,113,828

8.2 Charges and fees for deposit-type contracts

8.3 Aggregate write-ins for miscellaneous income 76,035,217 967,674 1,785,945 145,580 51,097,116 78,091 180,939 21,779,872

9. Totals (Lines 1 to 8.3) 4,289,512,602 383,289,843 245,156,762 1,928,074 4,650 104,523,881 3,394,251,298 91,015,821 9,362 17,021,413 52,311,498

10. Death benefits 115,719,662 54,069,778 61,649,884

11. Matured endowments (excluding guaranteed annual pure endowments) 542,456 542,456

12. Annuity benefits 70,401,909 13,351,576 57,050,333

13. Disability benefits and benefits under accident and health contracts 51,120,056 1,116,220 12,577 53,876 49,937,383

14. Coupons, guaranteed annual pure endowments and similar benefits

15. Surrender benefits and withdrawals for life contracts 3,067,275,914 58,339,277 194,782,939 727,618 2,813,426,080

16. Group conversions 616,604 (616,604)

17. Interest and adjustments on contract or deposit-type contract funds 27,237,299 1,642,995 1,111,524 522,065 130,792 866,282 18,765 22,944,876

18. Payments on supplementary contracts with life contingencies 268,036 268,036

19. Increase in aggregate reserves for life and accident and health contracts 720,999,746 133,901,827 65,400,567 (39,373) 1,414,672 528,147,268 (7,825,215)

20. Totals (Lines 10 to 19) 4,053,565,078 250,229,157 274,646,606 750,728 63,318,939 3,399,543,839 42,130,933 22,944,876

21. Commissions on premiums, annuity considerations and deposit-type contract funds (direct business only) 122,694,369 33,481,919 11,447,991 3,364 14,503,695 47,759,839 15,490,655 7,155 (249)

22. Commissions and expense allowances on reinsurance assumed 52,628,606 34,329,026 1,439,088 1,586,985 15,273,507

23. General insurance expenses 285,441,610 44,434,142 23,112,238 74,738 23,990,316 142,639,219 23,010,914 28,180,043

24. Insurance taxes, licenses and fees, excluding federal income taxes 21,248,797 6,124,136 1,261,536 209,293 2,875,079 6,844,628 2,648,305 (10,784) 1,296,604

25. Increase in loading on deferred and uncollected premiums 921,472 921,472

26. Net transfers to or (from) Separate Accounts net of reinsurance (343,846,958) (4,066,560) (72,910,883) (266,869,515)

27. Aggregate write-ins for deductions (3,506,934) 14,901 (3,521,835)

28. Totals (Lines 20 to 27) 4,189,146,040 365,468,193 237,557,488 1,034,759 3,364 104,688,029 3,327,835,263 84,867,792 7,155 38,207,350 29,476,647

29. Net gain from operations before dividends to policyholders and federal income taxes (Line 9 minus Line 28) 100,366,562 17,821,650 7,599,274 893,315 1,286 (164,148) 66,416,035 6,148,029 2,207 (21,185,937) 22,834,851

30. Dividends to policyholders 30,347,508 28,644,493 449 1,363,968 39,844 298,754

31. Net gain from operations after dividends to policyholders and before federal income taxes (Line 29 minus Line 30) 70,019,054 (10,822,843) 7,598,825 893,315 1,286 (1,528,116) 66,376,191 5,849,275 2,207 (21,185,937) 22,834,851

32. Federal income taxes incurred (excluding tax on capital gains) 20,601,824 (1,954,325) 5,509,219 (549,409) 18,487,936 2,155,306 157,720 (3,204,623)

33. Net gain from operations after dividends to policyholders and federal income taxes and before realized capital gains or (losses) (Line 31 minus Line 32) 49,417,230 (8,868,518) 2,089,606 893,315 1,286 (978,707) 47,888,255 3,693,969 2,207 (21,343,657) 26,039,474

DETAILS OF WRITE-INS

08.301. Miscellaneous income 52,972,043 967,674 1,785,945 145,580 51,097,116 78,091 180,939 (1,283,302)

08.302. Legal settlement 21,717,264 21,717,264

08.303. Change in surrender value of COLI 1,345,910 1,345,910

08.398. Summary of remaining write-ins for Line 8.3 from overflow page

08.399. Totals (Lines 08.301 thru 08.303 plus 08.398) (Line 8.3 above) 76,035,217 967,674 1,785,945 145,580 51,097,116 78,091 180,939 21,779,872

2701. Reserve adjustment & SA transfers on reinsurance assumed (3,506,934) 14,901 (3,521,835)

2702.

2703.

2798. Summary of remaining write-ins for Line 27 from overflow page

2799. Totals (Lines 2701 thru 2703 plus 2798) (Line 27 above) (3,506,934) 14,901 (3,521,835)

(a) Includes the following amounts for FEGLI/SGLI: Line 1 , Line 10 , Line 16 , Line 23 , Line 24

6

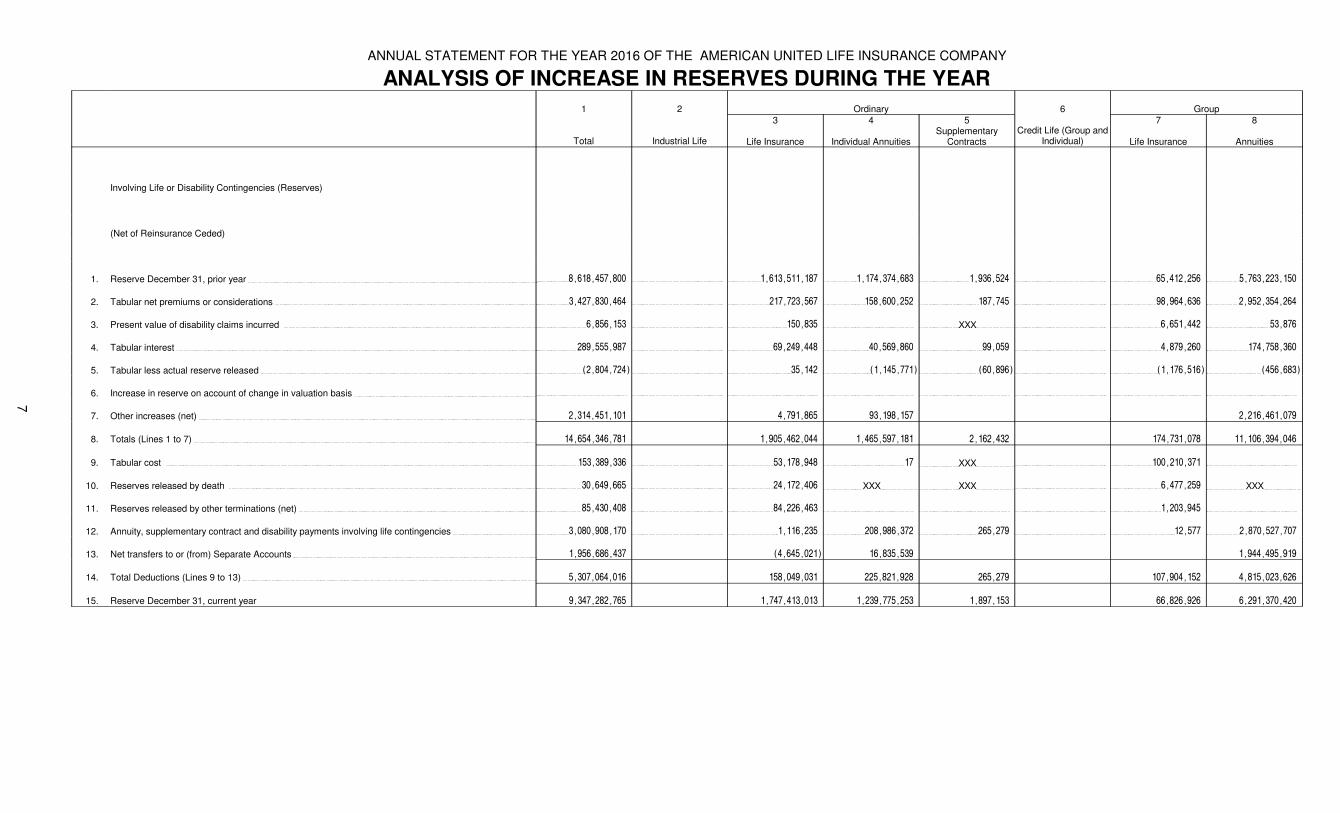

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

ANALYSIS OF INCREASE IN RESERVES DURING THE YEAR

1 2 Ordinary 6 Group

Total Industrial Life

3

Life Insurance

4

Individual Annuities

5Supplementary

ContractsCredit Life (Group and

Individual)

7

Life Insurance

8

Annuities

Involving Life or Disability Contingencies (Reserves)

(Net of Reinsurance Ceded)

1. Reserve December 31, prior year 8,618,457,800 1,613,511,187 1,174,374,683 1,936,524 65,412,256 5,763,223,150

2. Tabular net premiums or considerations 3,427,830,464 217,723,567 158,600,252 187,745 98,964,636 2,952,354,264

3. Present value of disability claims incurred 6,856,153 150,835 XXX 6,651,442 53,876

4. Tabular interest 289,555,987 69,249,448 40,569,860 99,059 4,879,260 174,758,360

5. Tabular less actual reserve released (2,804,724) 35,142 (1,145,771) (60,896) (1,176,516) (456,683)

6. Increase in reserve on account of change in valuation basis

7. Other increases (net) 2,314,451,101 4,791,865 93,198,157 2,216,461,079

8. Totals (Lines 1 to 7) 14,654,346,781 1,905,462,044 1,465,597,181 2,162,432 174,731,078 11,106,394,046

9. Tabular cost 153,389,336 53,178,948 17 XXX 100,210,371

10. Reserves released by death 30,649,665 24,172,406 XXX XXX 6,477,259 XXX

11. Reserves released by other terminations (net) 85,430,408 84,226,463 1,203,945

12. Annuity, supplementary contract and disability payments involving life contingencies 3,080,908,170 1,116,235 208,986,372 265,279 12,577 2,870,527,707

13. Net transfers to or (from) Separate Accounts 1,956,686,437 (4,645,021) 16,835,539 1,944,495,919

14. Total Deductions (Lines 9 to 13) 5,307,064,016 158,049,031 225,821,928 265,279 107,904,152 4,815,023,626

15. Reserve December 31, current year 9,347,282,765 1,747,413,013 1,239,775,253 1,897,153 66,826,926 6,291,370,420

7

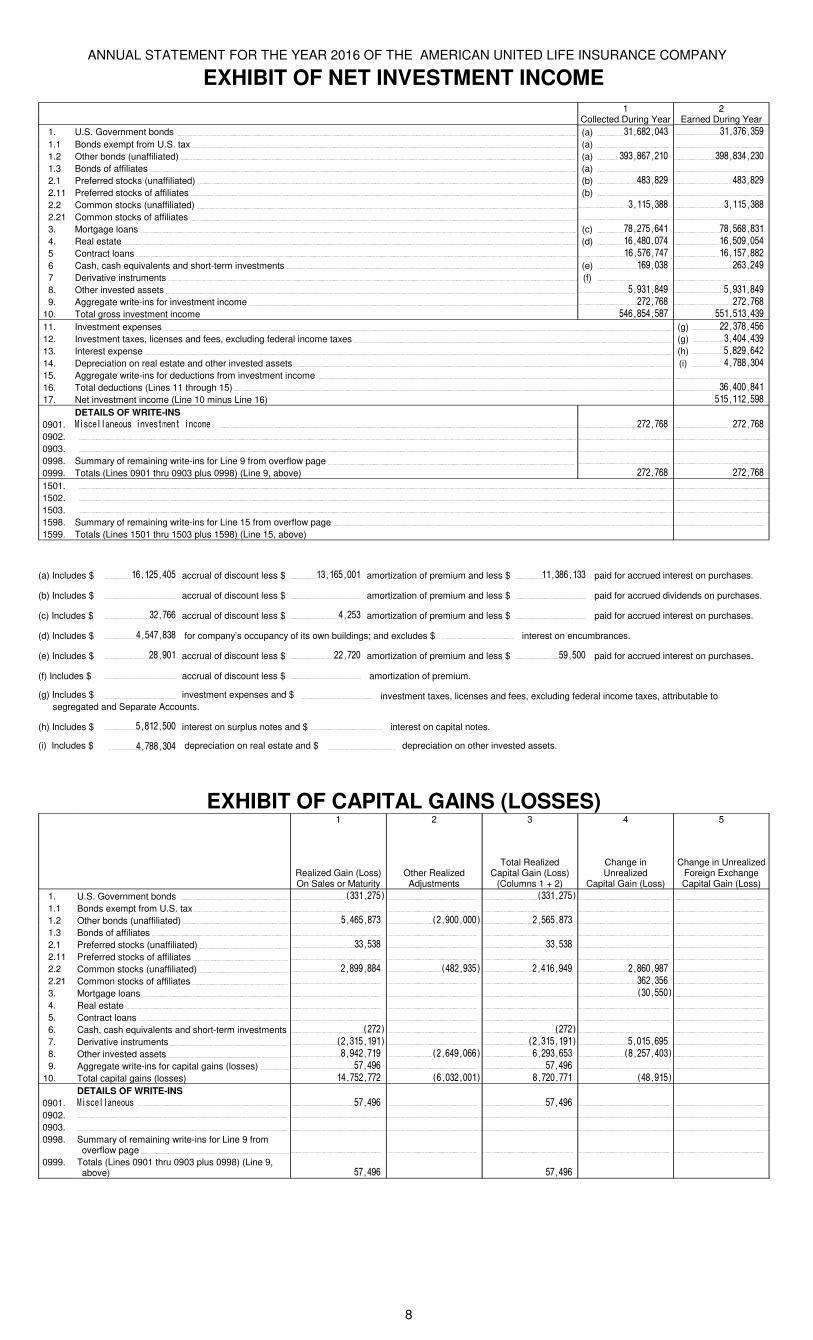

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

EXHIBIT OF NET INVESTMENT INCOME

1 2Collected During Year Earned During Year

1. U.S. Government bonds (a) 31,682,043 31,376,359

1.1 Bonds exempt from U.S. tax (a)

1.2 Other bonds (unaffiliated) (a) 393,867,210 398,834,230

1.3 Bonds of affiliates (a)

2.1 Preferred stocks (unaffiliated) (b) 483,829 483,829

2.11 Preferred stocks of affiliates (b)

2.2 Common stocks (unaffiliated) 3,115,388 3,115,388

2.21 Common stocks of affiliates

3. Mortgage loans (c) 78,275,641 78,568,831

4. Real estate (d) 16,480,074 16,509,054

5 Contract loans 16,576,747 16,157,882

6 Cash, cash equivalents and short-term investments (e) 169,038 263,249

7 Derivative instruments (f)

8. Other invested assets 5,931,849 5,931,849

9. Aggregate write-ins for investment income 272,768 272,768

10. Total gross investment income 546,854,587 551,513,439

11. Investment expenses (g) 22,378,456

12. Investment taxes, licenses and fees, excluding federal income taxes (g) 3,404,439

13. Interest expense (h) 5,829,642

14. Depreciation on real estate and other invested assets (i) 4,788,304

15. Aggregate write-ins for deductions from investment income

16. Total deductions (Lines 11 through 15) 36,400,841

17. Net investment income (Line 10 minus Line 16) 515,112,598

DETAILS OF WRITE-INS

0901. Miscellaneous investment income 272,768 272,768

0902.

0903.

0998. Summary of remaining write-ins for Line 9 from overflow page

0999. Totals (Lines 0901 thru 0903 plus 0998) (Line 9, above) 272,768 272,768

1501.

1502.

1503.

1598. Summary of remaining write-ins for Line 15 from overflow page

1599. Totals (Lines 1501 thru 1503 plus 1598) (Line 15, above)

(a) Includes $ 16,125,405 accrual of discount less $ 13,165,001 amortization of premium and less $ 11,386,133 paid for accrued interest on purchases.

(b) Includes $ accrual of discount less $ amortization of premium and less $ paid for accrued dividends on purchases.

(c) Includes $ 32,766 accrual of discount less $ 4,253 amortization of premium and less $ paid for accrued interest on purchases.

(d) Includes $ 4,547,838 for company’s occupancy of its own buildings; and excludes $ interest on encumbrances.

(e) Includes $ 28,901 accrual of discount less $ 22,720 amortization of premium and less $ 59,500 paid for accrued interest on purchases.

(f) Includes $ accrual of discount less $ amortization of premium.

(g) Includes $ investment expenses and $ investment taxes, licenses and fees, excluding federal income taxes, attributable tosegregated and Separate Accounts.

(h) Includes $ 5,812,500 interest on surplus notes and $ interest on capital notes.

(i) Includes $ 4,788,304 depreciation on real estate and $ depreciation on other invested assets.

EXHIBIT OF CAPITAL GAINS (LOSSES)1

Realized Gain (Loss) On Sales or Maturity

2

Other Realized Adjustments

3

Total RealizedCapital Gain (Loss)

(Columns 1 + 2)

4

Change inUnrealized

Capital Gain (Loss)

5

Change in Unrealized Foreign Exchange Capital Gain (Loss)

1. U.S. Government bonds (331,275) (331,275)

1.1 Bonds exempt from U.S. tax

1.2 Other bonds (unaffiliated) 5,465,873 (2,900,000) 2,565,873

1.3 Bonds of affiliates

2.1 Preferred stocks (unaffiliated) 33,538 33,538

2.11 Preferred stocks of affiliates

2.2 Common stocks (unaffiliated) 2,899,884 (482,935) 2,416,949 2,860,987

2.21 Common stocks of affiliates 362,356

3. Mortgage loans (30,550)

4. Real estate

5. Contract loans

6. Cash, cash equivalents and short-term investments (272) (272)

7. Derivative instruments (2,315,191) (2,315,191) 5,015,695

8. Other invested assets 8,942,719 (2,649,066) 6,293,653 (8,257,403)

9. Aggregate write-ins for capital gains (losses) 57,496 57,496

10. Total capital gains (losses) 14,752,772 (6,032,001) 8,720,771 (48,915)

DETAILS OF WRITE-INS

0901. Miscellaneous 57,496 57,496

0902.

0903.

0998. Summary of remaining write-ins for Line 9 from overflow page

0999. Totals (Lines 0901 thru 0903 plus 0998) (Line 9, above) 57,496 57,496

8

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

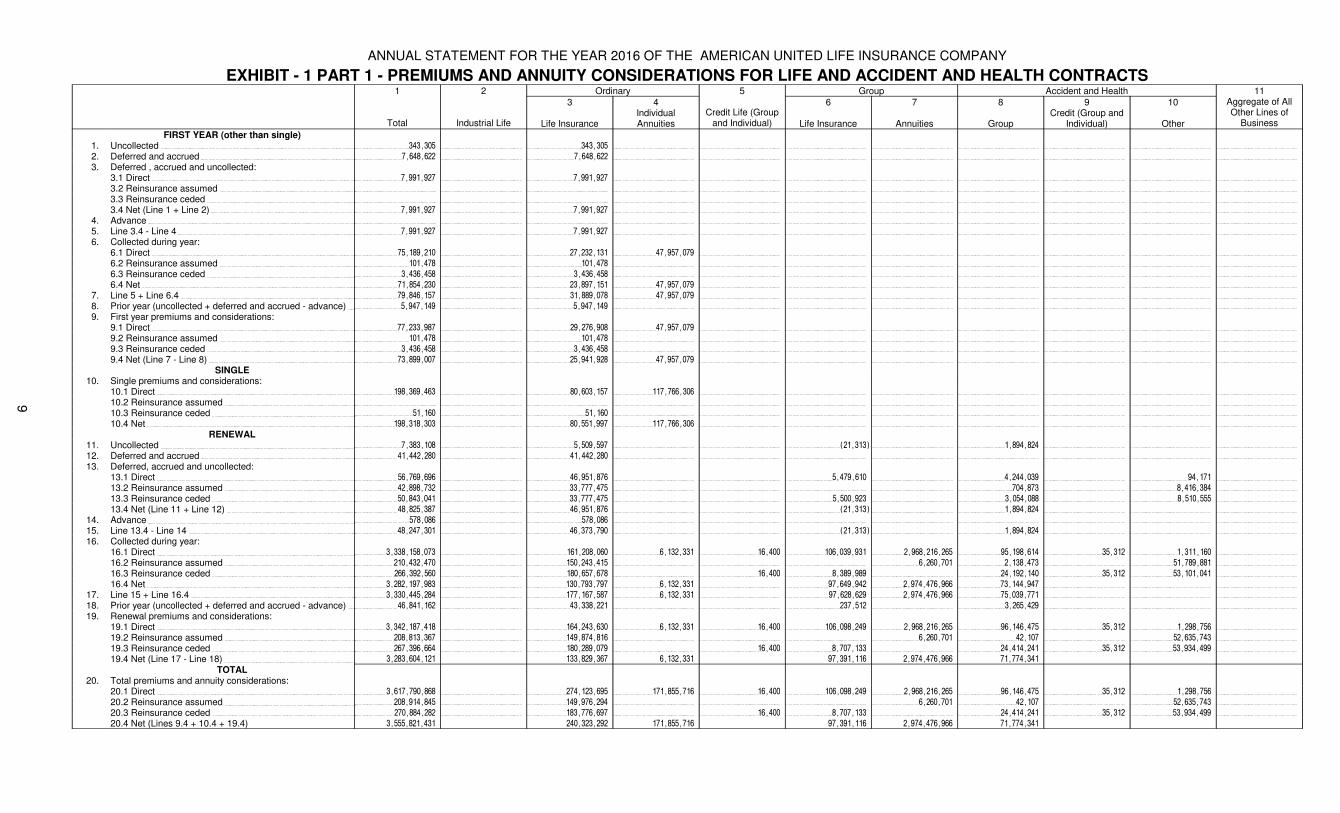

EXHIBIT - 1 PART 1 - PREMIUMS AND ANNUITY CONSIDERATIONS FOR LIFE AND ACCIDENT AND HEALTH CONTRACTS1 2 Ordinary 5 Group Accident and Health 11

Total Industrial Life

3

Life Insurance

4IndividualAnnuities

Credit Life (Group and Individual)

6

Life Insurance

7

Annuities

8

Group

9Credit (Group and

Individual)

10

Other

Aggregate of All Other Lines of

Business

FIRST YEAR (other than single)1. Uncollected 343,305 343,305

2. Deferred and accrued 7,648,622 7,648,622

3. Deferred , accrued and uncollected:3.1 Direct 7,991,927 7,991,927

3.2 Reinsurance assumed

3.3 Reinsurance ceded

3.4 Net (Line 1 + Line 2) 7,991,927 7,991,927

4. Advance

5. Line 3.4 - Line 4 7,991,927 7,991,927

6. Collected during year:6.1 Direct 75,189,210 27,232,131 47,957,079

6.2 Reinsurance assumed 101,478 101,478

6.3 Reinsurance ceded 3,436,458 3,436,458

6.4 Net 71,854,230 23,897,151 47,957,079

7. Line 5 + Line 6.4 79,846,157 31,889,078 47,957,079

8. Prior year (uncollected + deferred and accrued - advance) 5,947,149 5,947,149

9. First year premiums and considerations:9.1 Direct 77,233,987 29,276,908 47,957,079

9.2 Reinsurance assumed 101,478 101,478

9.3 Reinsurance ceded 3,436,458 3,436,458

9.4 Net (Line 7 - Line 8) 73,899,007 25,941,928 47,957,079

SINGLE10. Single premiums and considerations:

10.1 Direct 198,369,463 80,603,157 117,766,306

10.2 Reinsurance assumed

10.3 Reinsurance ceded 51,160 51,160

10.4 Net 198,318,303 80,551,997 117,766,306

RENEWAL11. Uncollected 7,383,108 5,509,597 (21,313) 1,894,824

12. Deferred and accrued 41,442,280 41,442,280

13. Deferred, accrued and uncollected:13.1 Direct 56,769,696 46,951,876 5,479,610 4,244,039 94,171

13.2 Reinsurance assumed 42,898,732 33,777,475 704,873 8,416,384

13.3 Reinsurance ceded 50,843,041 33,777,475 5,500,923 3,054,088 8,510,555

13.4 Net (Line 11 + Line 12) 48,825,387 46,951,876 (21,313) 1,894,824

14. Advance 578,086 578,086

15. Line 13.4 - Line 14 48,247,301 46,373,790 (21,313) 1,894,824

16. Collected during year:16.1 Direct 3,338,158,073 161,208,060 6,132,331 16,400 106,039,931 2,968,216,265 95,198,614 35,312 1,311,160

16.2 Reinsurance assumed 210,432,470 150,243,415 6,260,701 2,138,473 51,789,881

16.3 Reinsurance ceded 266,392,560 180,657,678 16,400 8,389,989 24,192,140 35,312 53,101,041

16.4 Net 3,282,197,983 130,793,797 6,132,331 97,649,942 2,974,476,966 73,144,947

17. Line 15 + Line 16.4 3,330,445,284 177,167,587 6,132,331 97,628,629 2,974,476,966 75,039,771

18. Prior year (uncollected + deferred and accrued - advance) 46,841,162 43,338,221 237,512 3,265,429

19. Renewal premiums and considerations:19.1 Direct 3,342,187,418 164,243,630 6,132,331 16,400 106,098,249 2,968,216,265 96,146,475 35,312 1,298,756

19.2 Reinsurance assumed 208,813,367 149,874,816 6,260,701 42,107 52,635,743

19.3 Reinsurance ceded 267,396,664 180,289,079 16,400 8,707,133 24,414,241 35,312 53,934,499

19.4 Net (Line 17 - Line 18) 3,283,604,121 133,829,367 6,132,331 97,391,116 2,974,476,966 71,774,341

TOTAL20. Total premiums and annuity considerations:

20.1 Direct 3,617,790,868 274,123,695 171,855,716 16,400 106,098,249 2,968,216,265 96,146,475 35,312 1,298,756

20.2 Reinsurance assumed 208,914,845 149,976,294 6,260,701 42,107 52,635,743

20.3 Reinsurance ceded 270,884,282 183,776,697 16,400 8,707,133 24,414,241 35,312 53,934,499

20.4 Net (Lines 9.4 + 10.4 + 19.4) 3,555,821,431 240,323,292 171,855,716 97,391,116 2,974,476,966 71,774,341

9

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

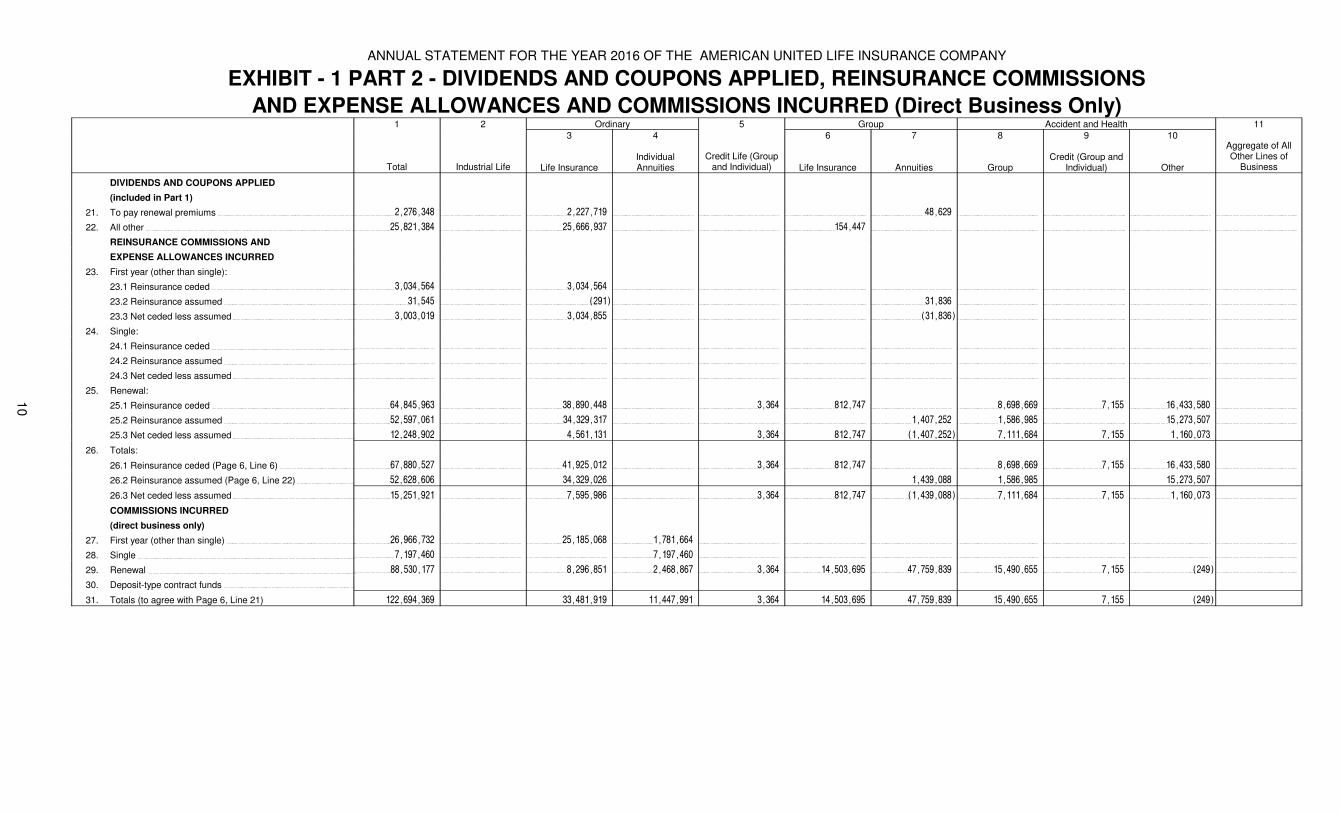

EXHIBIT - 1 PART 2 - DIVIDENDS AND COUPONS APPLIED, REINSURANCE COMMISSIONS

AND EXPENSE ALLOWANCES AND COMMISSIONS INCURRED (Direct Business Only)1 2 Ordinary 5 Group Accident and Health 11

Total Industrial Life

3

Life Insurance

4

IndividualAnnuities

Credit Life (Group and Individual)

6

Life Insurance

7

Annuities

8

Group

9

Credit (Group and Individual)

10

Other

Aggregate of All Other Lines of

Business

DIVIDENDS AND COUPONS APPLIED

(included in Part 1)

21. To pay renewal premiums 2,276,348 2,227,719 48,629

22. All other 25,821,384 25,666,937 154,447

REINSURANCE COMMISSIONS AND

EXPENSE ALLOWANCES INCURRED

23. First year (other than single):

23.1 Reinsurance ceded 3,034,564 3,034,564

23.2 Reinsurance assumed 31,545 (291) 31,836

23.3 Net ceded less assumed 3,003,019 3,034,855 (31,836)

24. Single:

24.1 Reinsurance ceded

24.2 Reinsurance assumed

24.3 Net ceded less assumed

25. Renewal:

25.1 Reinsurance ceded 64,845,963 38,890,448 3,364 812,747 8,698,669 7,155 16,433,580

25.2 Reinsurance assumed 52,597,061 34,329,317 1,407,252 1,586,985 15,273,507

25.3 Net ceded less assumed 12,248,902 4,561,131 3,364 812,747 (1,407,252) 7,111,684 7,155 1,160,073

26. Totals:

26.1 Reinsurance ceded (Page 6, Line 6) 67,880,527 41,925,012 3,364 812,747 8,698,669 7,155 16,433,580

26.2 Reinsurance assumed (Page 6, Line 22) 52,628,606 34,329,026 1,439,088 1,586,985 15,273,507

26.3 Net ceded less assumed 15,251,921 7,595,986 3,364 812,747 (1,439,088) 7,111,684 7,155 1,160,073

COMMISSIONS INCURRED

(direct business only)

27. First year (other than single) 26,966,732 25,185,068 1,781,664

28. Single 7,197,460 7,197,460

29. Renewal 88,530,177 8,296,851 2,468,867 3,364 14,503,695 47,759,839 15,490,655 7,155 (249)

30. Deposit-type contract funds

31. Totals (to agree with Page 6, Line 21) 122,694,369 33,481,919 11,447,991 3,364 14,503,695 47,759,839 15,490,655 7,155 (249)

10

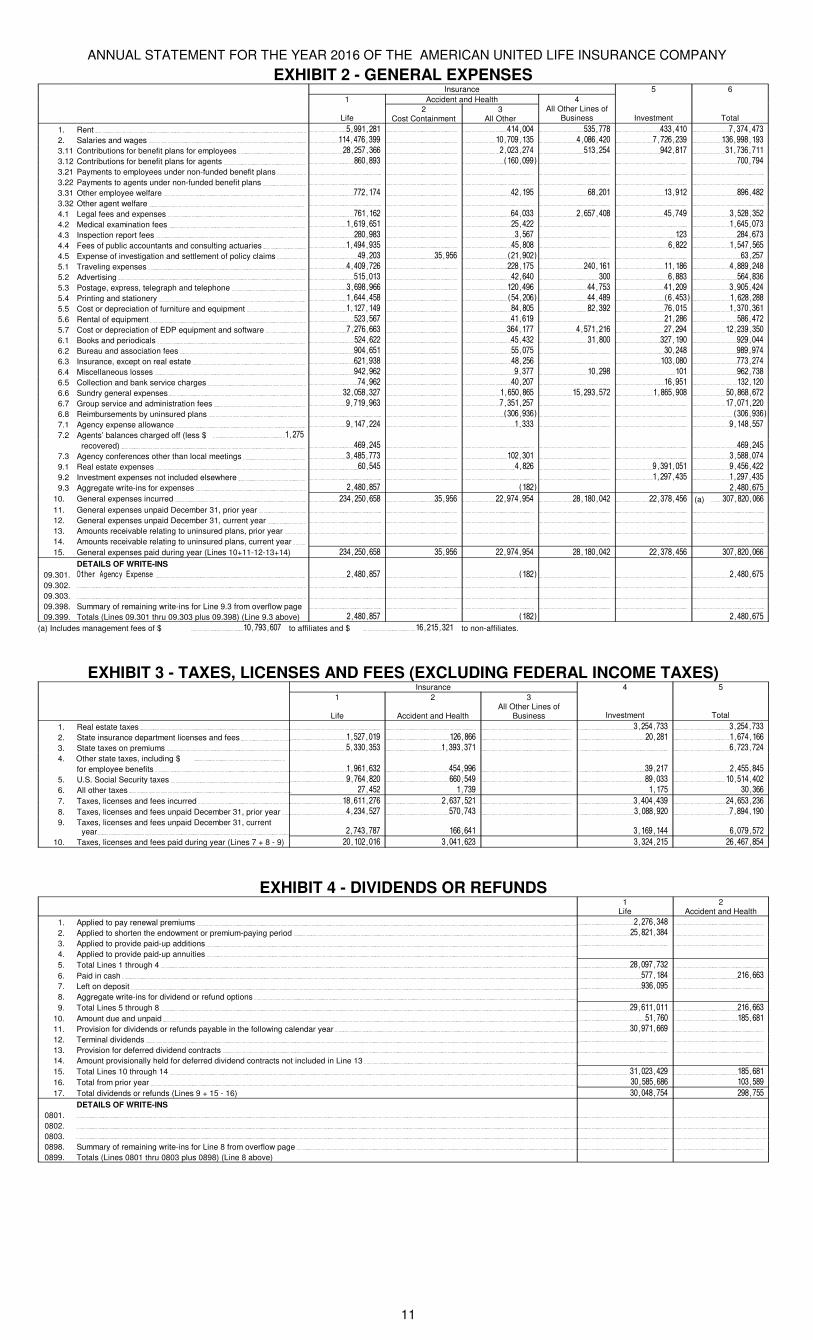

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

EXHIBIT 2 - GENERAL EXPENSESInsurance 5 6

1 Accident and Health 4

Life2

Cost Containment3

All Other

All Other Lines of Business Investment Total

1. Rent 5,991,281 414,004 535,778 433,410 7,374,473

2. Salaries and wages 114,476,399 10,709,135 4,086,420 7,726,239 136,998,193

3.11 Contributions for benefit plans for employees 28,257,366 2,023,274 513,254 942,817 31,736,711

3.12 Contributions for benefit plans for agents 860,893 (160,099) 700,794

3.21 Payments to employees under non-funded benefit plans

3.22 Payments to agents under non-funded benefit plans

3.31 Other employee welfare 772,174 42,195 68,201 13,912 896,482

3.32 Other agent welfare

4.1 Legal fees and expenses 761,162 64,033 2,657,408 45,749 3,528,352

4.2 Medical examination fees 1,619,651 25,422 1,645,073

4.3 Inspection report fees 280,983 3,567 123 284,673

4.4 Fees of public accountants and consulting actuaries 1,494,935 45,808 6,822 1,547,565

4.5 Expense of investigation and settlement of policy claims 49,203 35,956 (21,902) 63,257

5.1 Traveling expenses 4,409,726 228,175 240,161 11,186 4,889,248

5.2 Advertising 515,013 42,640 300 6,883 564,836

5.3 Postage, express, telegraph and telephone 3,698,966 120,496 44,753 41,209 3,905,424

5.4 Printing and stationery 1,644,458 (54,206) 44,489 (6,453) 1,628,288

5.5 Cost or depreciation of furniture and equipment 1,127,149 84,805 82,392 76,015 1,370,361

5.6 Rental of equipment 523,567 41,619 21,286 586,472

5.7 Cost or depreciation of EDP equipment and software 7,276,663 364,177 4,571,216 27,294 12,239,350

6.1 Books and periodicals 524,622 45,432 31,800 327,190 929,044

6.2 Bureau and association fees 904,651 55,075 30,248 989,974

6.3 Insurance, except on real estate 621,938 48,256 103,080 773,274

6.4 Miscellaneous losses 942,962 9,377 10,298 101 962,738

6.5 Collection and bank service charges 74,962 40,207 16,951 132,120

6.6 Sundry general expenses 32,058,327 1,650,865 15,293,572 1,865,908 50,868,672

6.7 Group service and administration fees 9,719,963 7,351,257 17,071,220

6.8 Reimbursements by uninsured plans (306,936) (306,936)

7.1 Agency expense allowance 9,147,224 1,333 9,148,557

7.2 Agents’ balances charged off (less $ 1,275

recovered) 469,245 469,245

7.3 Agency conferences other than local meetings 3,485,773 102,301 3,588,074

9.1 Real estate expenses 60,545 4,826 9,391,051 9,456,422

9.2 Investment expenses not included elsewhere 1,297,435 1,297,435

9.3 Aggregate write-ins for expenses 2,480,857 (182) 2,480,675

10. General expenses incurred 234,250,658 35,956 22,974,954 28,180,042 22,378,456 (a) 307,820,066

11. General expenses unpaid December 31, prior year

12. General expenses unpaid December 31, current year

13. Amounts receivable relating to uninsured plans, prior year

14. Amounts receivable relating to uninsured plans, current year

15. General expenses paid during year (Lines 10+11-12-13+14) 234,250,658 35,956 22,974,954 28,180,042 22,378,456 307,820,066

DETAILS OF WRITE-INS

09.301. Other Agency Expense 2,480,857 (182) 2,480,675

09.302.

09.303.

09.398. Summary of remaining write-ins for Line 9.3 from overflow page

09.399. Totals (Lines 09.301 thru 09.303 plus 09.398) (Line 9.3 above) 2,480,857 (182) 2,480,675

(a) Includes management fees of $ 10,793,607 to affiliates and $ 16,215,321 to non-affiliates.

EXHIBIT 3 - TAXES, LICENSES AND FEES (EXCLUDING FEDERAL INCOME TAXES)Insurance 4 5

1

Life

2

Accident and Health

3All Other Lines of

Business Investment Total

1. Real estate taxes 3,254,733 3,254,733

2. State insurance department licenses and fees 1,527,019 126,866 20,281 1,674,166

3. State taxes on premiums 5,330,353 1,393,371 6,723,724

4. Other state taxes, including $

for employee benefits 1,961,632 454,996 39,217 2,455,845

5. U.S. Social Security taxes 9,764,820 660,549 89,033 10,514,402

6. All other taxes 27,452 1,739 1,175 30,366

7. Taxes, licenses and fees incurred 18,611,276 2,637,521 3,404,439 24,653,236

8. Taxes, licenses and fees unpaid December 31, prior year 4,234,527 570,743 3,088,920 7,894,190

9. Taxes, licenses and fees unpaid December 31, current year 2,743,787 166,641 3,169,144 6,079,572

10. Taxes, licenses and fees paid during year (Lines 7 + 8 - 9) 20,102,016 3,041,623 3,324,215 26,467,854

EXHIBIT 4 - DIVIDENDS OR REFUNDS1

Life2

Accident and Health

1. Applied to pay renewal premiums 2,276,348

2. Applied to shorten the endowment or premium-paying period 25,821,384

3. Applied to provide paid-up additions

4. Applied to provide paid-up annuities

5. Total Lines 1 through 4 28,097,732

6. Paid in cash 577,184 216,663

7. Left on deposit 936,095

8. Aggregate write-ins for dividend or refund options

9. Total Lines 5 through 8 29,611,011 216,663

10. Amount due and unpaid 51,760 185,681

11. Provision for dividends or refunds payable in the following calendar year 30,971,669

12. Terminal dividends

13. Provision for deferred dividend contracts

14. Amount provisionally held for deferred dividend contracts not included in Line 13

15. Total Lines 10 through 14 31,023,429 185,681

16. Total from prior year 30,585,686 103,589

17. Total dividends or refunds (Lines 9 + 15 - 16) 30,048,754 298,755

DETAILS OF WRITE-INS

0801.

0802.

0803.

0898. Summary of remaining write-ins for Line 8 from overflow page

0899. Totals (Lines 0801 thru 0803 plus 0898) (Line 8 above)

11

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

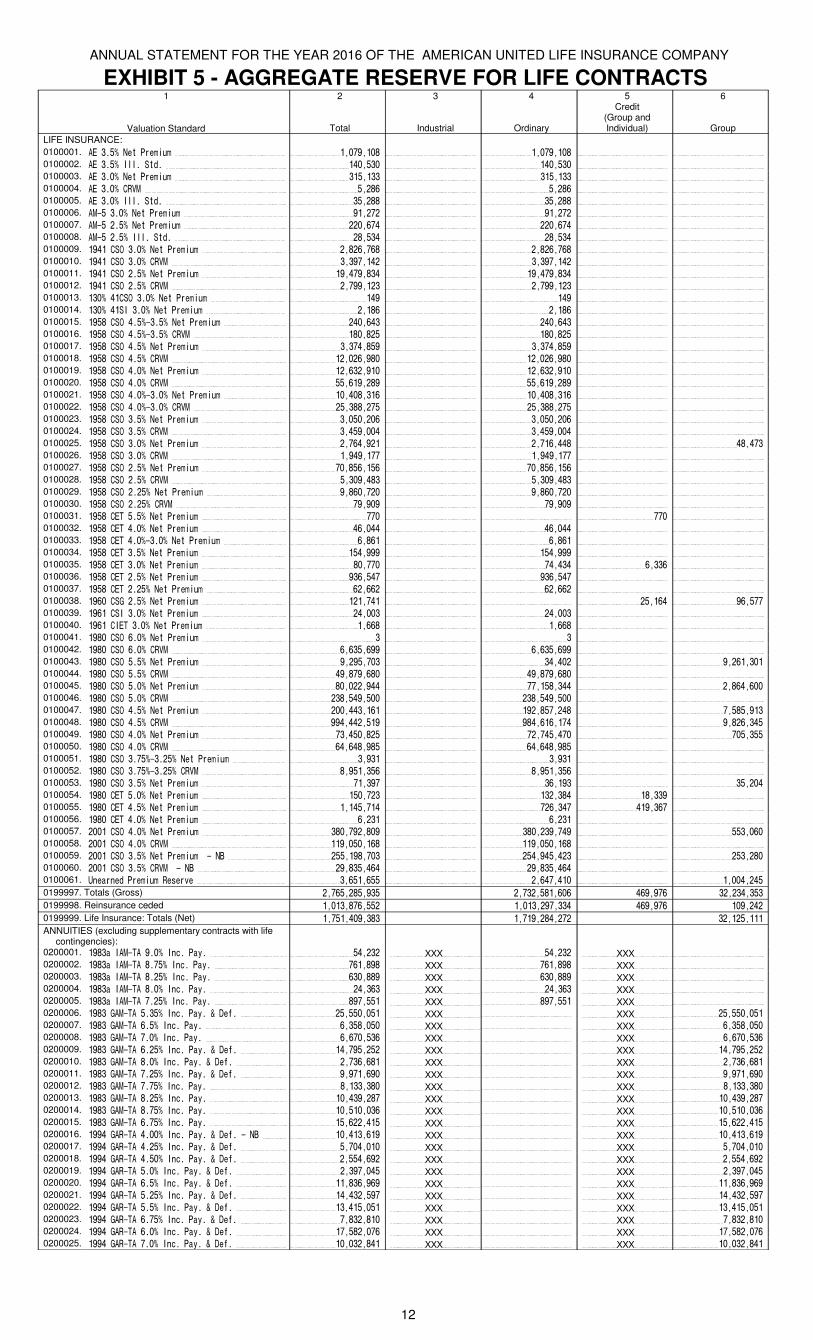

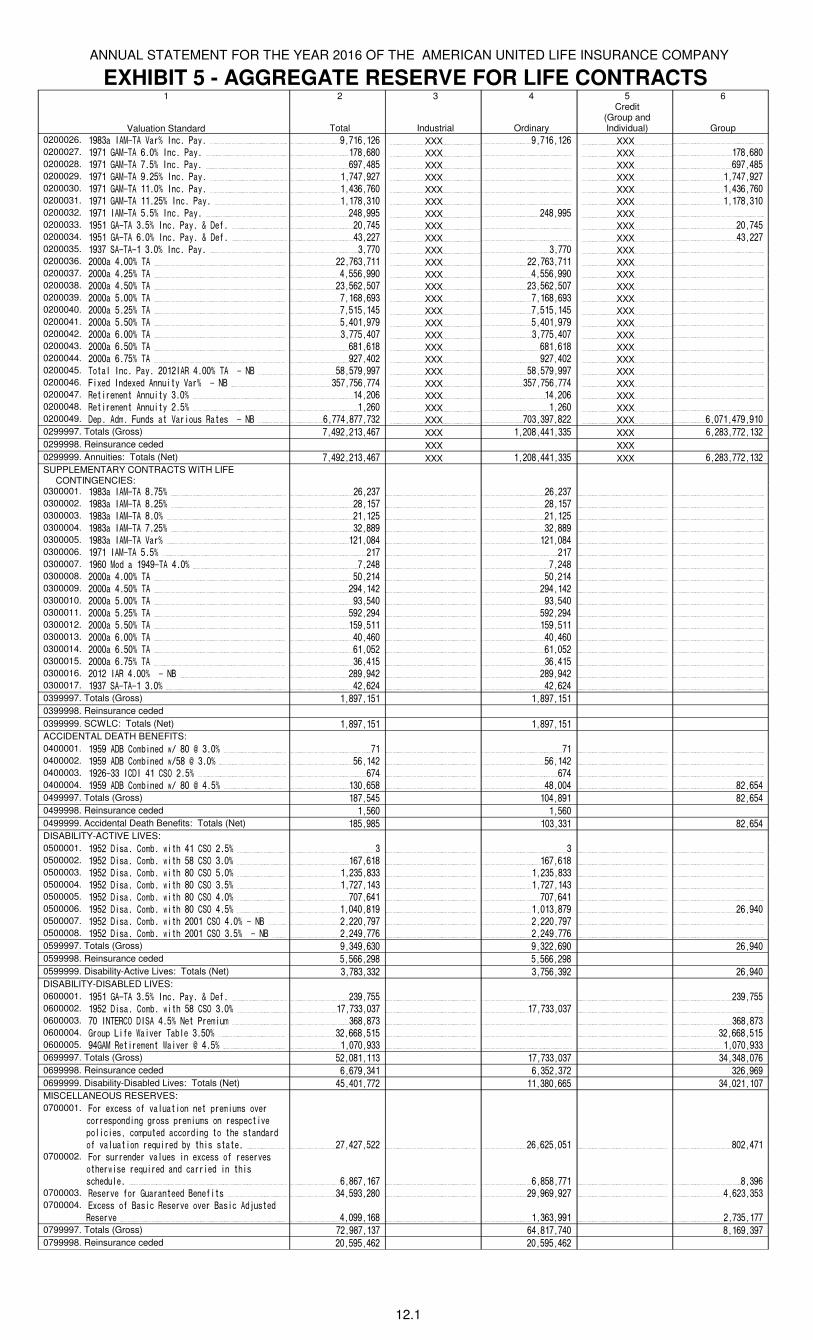

EXHIBIT 5 - AGGREGATE RESERVE FOR LIFE CONTRACTS1

Valuation Standard

2

Total

3

Industrial

4

Ordinary

5Credit

(Group and Individual)

6

Group

LIFE INSURANCE:

0100001. AE 3.5% Net Premium 1,079,108 1,079,108 0100002. AE 3.5% Ill. Std. 140,530 140,530 0100003. AE 3.0% Net Premium 315,133 315,133 0100004. AE 3.0% CRVM 5,286 5,286 0100005. AE 3.0% Ill. Std. 35,288 35,288 0100006. AM-5 3.0% Net Premium 91,272 91,272 0100007. AM-5 2.5% Net Premium 220,674 220,674 0100008. AM-5 2.5% Ill. Std. 28,534 28,534 0100009. 1941 CSO 3.0% Net Premium 2,826,768 2,826,768 0100010. 1941 CSO 3.0% CRVM 3,397,142 3,397,142 0100011. 1941 CSO 2.5% Net Premium 19,479,834 19,479,834 0100012. 1941 CSO 2.5% CRVM 2,799,123 2,799,123 0100013. 130% 41CSO 3.0% Net Premium 149 149 0100014. 130% 41SI 3.0% Net Premium 2,186 2,186 0100015. 1958 CSO 4.5%-3.5% Net Premium 240,643 240,643 0100016. 1958 CSO 4.5%-3.5% CRVM 180,825 180,825 0100017. 1958 CSO 4.5% Net Premium 3,374,859 3,374,859 0100018. 1958 CSO 4.5% CRVM 12,026,980 12,026,980 0100019. 1958 CSO 4.0% Net Premium 12,632,910 12,632,910 0100020. 1958 CSO 4.0% CRVM 55,619,289 55,619,289 0100021. 1958 CSO 4.0%-3.0% Net Premium 10,408,316 10,408,316 0100022. 1958 CSO 4.0%-3.0% CRVM 25,388,275 25,388,275 0100023. 1958 CSO 3.5% Net Premium 3,050,206 3,050,206 0100024. 1958 CSO 3.5% CRVM 3,459,004 3,459,004 0100025. 1958 CSO 3.0% Net Premium 2,764,921 2,716,448 48,473 0100026. 1958 CSO 3.0% CRVM 1,949,177 1,949,177 0100027. 1958 CSO 2.5% Net Premium 70,856,156 70,856,156 0100028. 1958 CSO 2.5% CRVM 5,309,483 5,309,483 0100029. 1958 CSO 2.25% Net Premium 9,860,720 9,860,720 0100030. 1958 CSO 2.25% CRVM 79,909 79,909 0100031. 1958 CET 5.5% Net Premium 770 770 0100032. 1958 CET 4.0% Net Premium 46,044 46,044 0100033. 1958 CET 4.0%-3.0% Net Premium 6,861 6,861 0100034. 1958 CET 3.5% Net Premium 154,999 154,999 0100035. 1958 CET 3.0% Net Premium 80,770 74,434 6,336 0100036. 1958 CET 2.5% Net Premium 936,547 936,547 0100037. 1958 CET 2.25% Net Premium 62,662 62,662 0100038. 1960 CSG 2.5% Net Premium 121,741 25,164 96,577 0100039. 1961 CSI 3.0% Net Premium 24,003 24,003 0100040. 1961 CIET 3.0% Net Premium 1,668 1,668 0100041. 1980 CSO 6.0% Net Premium 3 3 0100042. 1980 CSO 6.0% CRVM 6,635,699 6,635,699 0100043. 1980 CSO 5.5% Net Premium 9,295,703 34,402 9,261,301 0100044. 1980 CSO 5.5% CRVM 49,879,680 49,879,680 0100045. 1980 CSO 5.0% Net Premium 80,022,944 77,158,344 2,864,600 0100046. 1980 CSO 5.0% CRVM 238,549,500 238,549,500 0100047. 1980 CSO 4.5% Net Premium 200,443,161 192,857,248 7,585,913 0100048. 1980 CSO 4.5% CRVM 994,442,519 984,616,174 9,826,345 0100049. 1980 CSO 4.0% Net Premium 73,450,825 72,745,470 705,355 0100050. 1980 CSO 4.0% CRVM 64,648,985 64,648,985 0100051. 1980 CSO 3.75%-3.25% Net Premium 3,931 3,931 0100052. 1980 CSO 3.75%-3.25% CRVM 8,951,356 8,951,356 0100053. 1980 CSO 3.5% Net Premium 71,397 36,193 35,204 0100054. 1980 CET 5.0% Net Premium 150,723 132,384 18,339 0100055. 1980 CET 4.5% Net Premium 1,145,714 726,347 419,367 0100056. 1980 CET 4.0% Net Premium 6,231 6,231 0100057. 2001 CSO 4.0% Net Premium 380,792,809 380,239,749 553,060 0100058. 2001 CSO 4.0% CRVM 119,050,168 119,050,168 0100059. 2001 CSO 3.5% Net Premium - NB 255,198,703 254,945,423 253,280 0100060. 2001 CSO 3.5% CRVM - NB 29,835,464 29,835,464 0100061. Unearned Premium Reserve 3,651,655 2,647,410 1,004,245 0199997. Totals (Gross) 2,765,285,935 2,732,581,606 469,976 32,234,353 0199998. Reinsurance ceded 1,013,876,552 1,013,297,334 469,976 109,242 0199999. Life Insurance: Totals (Net) 1,751,409,383 1,719,284,272 32,125,111 ANNUITIES (excluding supplementary contracts with life

contingencies): 0200001. 1983a IAM-TA 9.0% Inc. Pay. 54,232 XXX 54,232 XXX 0200002. 1983a IAM-TA 8.75% Inc. Pay. 761,898 XXX 761,898 XXX 0200003. 1983a IAM-TA 8.25% Inc. Pay. 630,889 XXX 630,889 XXX 0200004. 1983a IAM-TA 8.0% Inc. Pay. 24,363 XXX 24,363 XXX 0200005. 1983a IAM-TA 7.25% Inc. Pay. 897,551 XXX 897,551 XXX 0200006. 1983 GAM-TA 5.35% Inc. Pay. & Def. 25,550,051 XXX XXX 25,550,051 0200007. 1983 GAM-TA 6.5% Inc. Pay. 6,358,050 XXX XXX 6,358,050 0200008. 1983 GAM-TA 7.0% Inc. Pay. 6,670,536 XXX XXX 6,670,536 0200009. 1983 GAM-TA 6.25% Inc. Pay. & Def. 14,795,252 XXX XXX 14,795,252 0200010. 1983 GAM-TA 8.0% Inc. Pay. & Def. 2,736,681 XXX XXX 2,736,681 0200011. 1983 GAM-TA 7.25% Inc. Pay. & Def. 9,971,690 XXX XXX 9,971,690 0200012. 1983 GAM-TA 7.75% Inc. Pay. 8,133,380 XXX XXX 8,133,380 0200013. 1983 GAM-TA 8.25% Inc. Pay. 10,439,287 XXX XXX 10,439,287 0200014. 1983 GAM-TA 8.75% Inc. Pay. 10,510,036 XXX XXX 10,510,036 0200015. 1983 GAM-TA 6.75% Inc. Pay. 15,622,415 XXX XXX 15,622,415 0200016. 1994 GAR-TA 4.00% Inc. Pay. & Def. - NB 10,413,619 XXX XXX 10,413,619 0200017. 1994 GAR-TA 4.25% Inc. Pay. & Def. 5,704,010 XXX XXX 5,704,010 0200018. 1994 GAR-TA 4.50% Inc. Pay. & Def. 2,554,692 XXX XXX 2,554,692 0200019. 1994 GAR-TA 5.0% Inc. Pay. & Def. 2,397,045 XXX XXX 2,397,045 0200020. 1994 GAR-TA 6.5% Inc. Pay. & Def. 11,836,969 XXX XXX 11,836,969 0200021. 1994 GAR-TA 5.25% Inc. Pay. & Def. 14,432,597 XXX XXX 14,432,597 0200022. 1994 GAR-TA 5.5% Inc. Pay. & Def. 13,415,051 XXX XXX 13,415,051 0200023. 1994 GAR-TA 6.75% Inc. Pay. & Def. 7,832,810 XXX XXX 7,832,810 0200024. 1994 GAR-TA 6.0% Inc. Pay. & Def. 17,582,076 XXX XXX 17,582,076 0200025. 1994 GAR-TA 7.0% Inc. Pay. & Def. 10,032,841 XXX XXX 10,032,841

12

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

EXHIBIT 5 - AGGREGATE RESERVE FOR LIFE CONTRACTS1

Valuation Standard

2

Total

3

Industrial

4

Ordinary

5Credit

(Group and Individual)

6

Group

0200026. 1983a IAM-TA Var% Inc. Pay. 9,716,126 XXX 9,716,126 XXX 0200027. 1971 GAM-TA 6.0% Inc. Pay. 178,680 XXX XXX 178,680 0200028. 1971 GAM-TA 7.5% Inc. Pay. 697,485 XXX XXX 697,485 0200029. 1971 GAM-TA 9.25% Inc. Pay. 1,747,927 XXX XXX 1,747,927 0200030. 1971 GAM-TA 11.0% Inc. Pay. 1,436,760 XXX XXX 1,436,760 0200031. 1971 GAM-TA 11.25% Inc. Pay. 1,178,310 XXX XXX 1,178,310 0200032. 1971 IAM-TA 5.5% Inc. Pay. 248,995 XXX 248,995 XXX 0200033. 1951 GA-TA 3.5% Inc. Pay. & Def. 20,745 XXX XXX 20,745 0200034. 1951 GA-TA 6.0% Inc. Pay. & Def. 43,227 XXX XXX 43,227 0200035. 1937 SA-TA-1 3.0% Inc. Pay. 3,770 XXX 3,770 XXX 0200036. 2000a 4.00% TA 22,763,711 XXX 22,763,711 XXX 0200037. 2000a 4.25% TA 4,556,990 XXX 4,556,990 XXX 0200038. 2000a 4.50% TA 23,562,507 XXX 23,562,507 XXX 0200039. 2000a 5.00% TA 7,168,693 XXX 7,168,693 XXX 0200040. 2000a 5.25% TA 7,515,145 XXX 7,515,145 XXX 0200041. 2000a 5.50% TA 5,401,979 XXX 5,401,979 XXX 0200042. 2000a 6.00% TA 3,775,407 XXX 3,775,407 XXX 0200043. 2000a 6.50% TA 681,618 XXX 681,618 XXX 0200044. 2000a 6.75% TA 927,402 XXX 927,402 XXX 0200045. Total Inc. Pay. 2012IAR 4.00% TA - NB 58,579,997 XXX 58,579,997 XXX 0200046. Fixed Indexed Annuity Var% - NB 357,756,774 XXX 357,756,774 XXX 0200047. Retirement Annuity 3.0% 14,206 XXX 14,206 XXX 0200048. Retirement Annuity 2.5% 1,260 XXX 1,260 XXX 0200049. Dep. Adm. Funds at Various Rates - NB 6,774,877,732 XXX 703,397,822 XXX 6,071,479,910 0299997. Totals (Gross) 7,492,213,467 XXX 1,208,441,335 XXX 6,283,772,132 0299998. Reinsurance ceded XXX XXX 0299999. Annuities: Totals (Net) 7,492,213,467 XXX 1,208,441,335 XXX 6,283,772,132 SUPPLEMENTARY CONTRACTS WITH LIFE

CONTINGENCIES: 0300001. 1983a IAM-TA 8.75% 26,237 26,237 0300002. 1983a IAM-TA 8.25% 28,157 28,157 0300003. 1983a IAM-TA 8.0% 21,125 21,125 0300004. 1983a IAM-TA 7.25% 32,889 32,889 0300005. 1983a IAM-TA Var% 121,084 121,084 0300006. 1971 IAM-TA 5.5% 217 217 0300007. 1960 Mod a 1949-TA 4.0% 7,248 7,248 0300008. 2000a 4.00% TA 50,214 50,214 0300009. 2000a 4.50% TA 294,142 294,142 0300010. 2000a 5.00% TA 93,540 93,540 0300011. 2000a 5.25% TA 592,294 592,294 0300012. 2000a 5.50% TA 159,511 159,511 0300013. 2000a 6.00% TA 40,460 40,460 0300014. 2000a 6.50% TA 61,052 61,052 0300015. 2000a 6.75% TA 36,415 36,415 0300016. 2012 IAR 4.00% - NB 289,942 289,942 0300017. 1937 SA-TA-1 3.0% 42,624 42,624 0399997. Totals (Gross) 1,897,151 1,897,151 0399998. Reinsurance ceded 0399999. SCWLC: Totals (Net) 1,897,151 1,897,151 ACCIDENTAL DEATH BENEFITS:

0400001. 1959 ADB Combined w/ 80 @ 3.0% 71 71 0400002. 1959 ADB Combined w/58 @ 3.0% 56,142 56,142 0400003. 1926-33 ICDI 41 CSO 2.5% 674 674 0400004. 1959 ADB Combined w/ 80 @ 4.5% 130,658 48,004 82,654 0499997. Totals (Gross) 187,545 104,891 82,654 0499998. Reinsurance ceded 1,560 1,560 0499999. Accidental Death Benefits: Totals (Net) 185,985 103,331 82,654 DISABILITY-ACTIVE LIVES:

0500001. 1952 Disa. Comb. with 41 CSO 2.5% 3 3 0500002. 1952 Disa. Comb. with 58 CSO 3.0% 167,618 167,618 0500003. 1952 Disa. Comb. with 80 CSO 5.0% 1,235,833 1,235,833 0500004. 1952 Disa. Comb. with 80 CSO 3.5% 1,727,143 1,727,143 0500005. 1952 Disa. Comb. with 80 CSO 4.0% 707,641 707,641 0500006. 1952 Disa. Comb. with 80 CSO 4.5% 1,040,819 1,013,879 26,940 0500007. 1952 Disa. Comb. with 2001 CSO 4.0% - NB 2,220,797 2,220,797 0500008. 1952 Disa. Comb. with 2001 CSO 3.5% - NB 2,249,776 2,249,776 0599997. Totals (Gross) 9,349,630 9,322,690 26,940 0599998. Reinsurance ceded 5,566,298 5,566,298 0599999. Disability-Active Lives: Totals (Net) 3,783,332 3,756,392 26,940 DISABILITY-DISABLED LIVES:

0600001. 1951 GA-TA 3.5% Inc. Pay. & Def. 239,755 239,755 0600002. 1952 Disa. Comb. with 58 CSO 3.0% 17,733,037 17,733,037 0600003. 70 INTERCO DISA 4.5% Net Premium 368,873 368,873 0600004. Group Life Waiver Table 3.50% 32,668,515 32,668,515 0600005. 94GAM Retirement Waiver @ 4.5% 1,070,933 1,070,933 0699997. Totals (Gross) 52,081,113 17,733,037 34,348,076 0699998. Reinsurance ceded 6,679,341 6,352,372 326,969 0699999. Disability-Disabled Lives: Totals (Net) 45,401,772 11,380,665 34,021,107 MISCELLANEOUS RESERVES:

0700001. For excess of valuation net premiums over

corresponding gross premiums on respective

policies, computed according to the standard

of valuation required by this state. 27,427,522 26,625,051 802,471 0700002. For surrender values in excess of reserves

otherwise required and carried in this

schedule. 6,867,167 6,858,771 8,396 0700003. Reserve for Guaranteed Benefits 34,593,280 29,969,927 4,623,353 0700004. Excess of Basic Reserve over Basic Adjusted

Reserve 4,099,168 1,363,991 2,735,177 0799997. Totals (Gross) 72,987,137 64,817,740 8,169,397 0799998. Reinsurance ceded 20,595,462 20,595,462

12.1

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

EXHIBIT 5 - AGGREGATE RESERVE FOR LIFE CONTRACTS1

Valuation Standard

2

Total

3

Industrial

4

Ordinary

5Credit

(Group and Individual)

6

Group

0799999. Miscellaneous Reserves: Totals (Net) 52,391,675 44,222,278 8,169,397

9999999. Totals (Net) - Page 3, Line 1 9,347,282,765 2,989,085,424 6,358,197,341

12.2

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

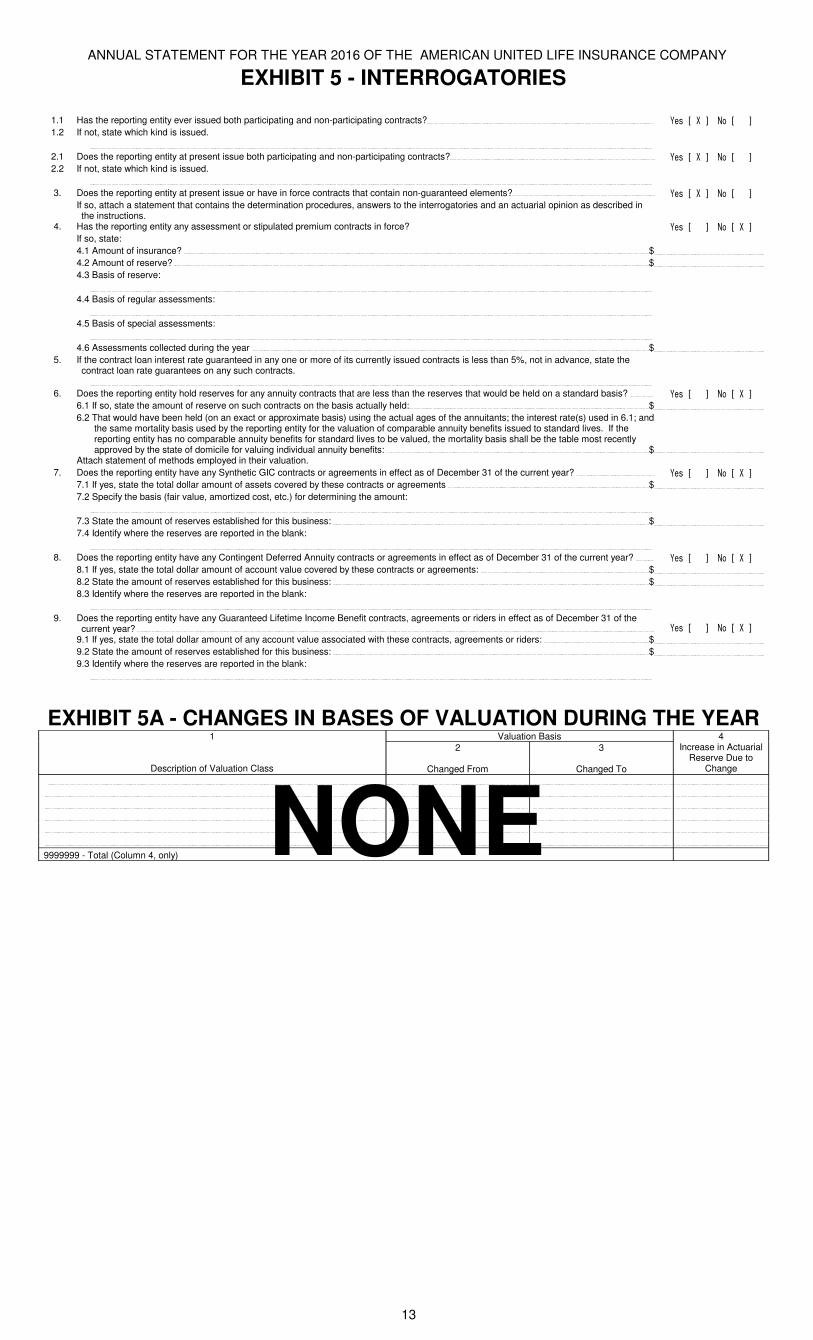

EXHIBIT 5 - INTERROGATORIES

1.1 Has the reporting entity ever issued both participating and non-participating contracts? Yes [ X ] No [ ]

1.2 If not, state which kind is issued.

2.1 Does the reporting entity at present issue both participating and non-participating contracts? Yes [ X ] No [ ]

2.2 If not, state which kind is issued.

3. Does the reporting entity at present issue or have in force contracts that contain non-guaranteed elements? Yes [ X ] No [ ]

If so, attach a statement that contains the determination procedures, answers to the interrogatories and an actuarial opinion as described in the instructions.

4. Has the reporting entity any assessment or stipulated premium contracts in force? Yes [ ] No [ X ]

If so, state:

4.1 Amount of insurance? $

4.2 Amount of reserve? $

4.3 Basis of reserve:

4.4 Basis of regular assessments:

4.5 Basis of special assessments:

4.6 Assessments collected during the year $

5. If the contract loan interest rate guaranteed in any one or more of its currently issued contracts is less than 5%, not in advance, state the contract loan rate guarantees on any such contracts.

6. Does the reporting entity hold reserves for any annuity contracts that are less than the reserves that would be held on a standard basis? Yes [ ] No [ X ]

6.1 If so, state the amount of reserve on such contracts on the basis actually held: $

6.2 That would have been held (on an exact or approximate basis) using the actual ages of the annuitants; the interest rate(s) used in 6.1; and the same mortality basis used by the reporting entity for the valuation of comparable annuity benefits issued to standard lives. If the reporting entity has no comparable annuity benefits for standard lives to be valued, the mortality basis shall be the table most recently approved by the state of domicile for valuing individual annuity benefits: $

Attach statement of methods employed in their valuation.

7. Does the reporting entity have any Synthetic GIC contracts or agreements in effect as of December 31 of the current year? Yes [ ] No [ X ]

7.1 If yes, state the total dollar amount of assets covered by these contracts or agreements $

7.2 Specify the basis (fair value, amortized cost, etc.) for determining the amount:

7.3 State the amount of reserves established for this business: $

7.4 Identify where the reserves are reported in the blank:

8. Does the reporting entity have any Contingent Deferred Annuity contracts or agreements in effect as of December 31 of the current year? Yes [ ] No [ X ]

8.1 If yes, state the total dollar amount of account value covered by these contracts or agreements: $

8.2 State the amount of reserves established for this business: $

8.3 Identify where the reserves are reported in the blank:

9. Does the reporting entity have any Guaranteed Lifetime Income Benefit contracts, agreements or riders in effect as of December 31 of the current year? Yes [ ] No [ X ]

9.1 If yes, state the total dollar amount of any account value associated with these contracts, agreements or riders: $

9.2 State the amount of reserves established for this business: $

9.3 Identify where the reserves are reported in the blank:

EXHIBIT 5A - CHANGES IN BASES OF VALUATION DURING THE YEAR1 Valuation Basis 4

Description of Valuation Class

2

Changed From

3

Changed To

Increase in Actuarial Reserve Due to

Change

9999999 - Total (Column 4, only) NONE

13

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

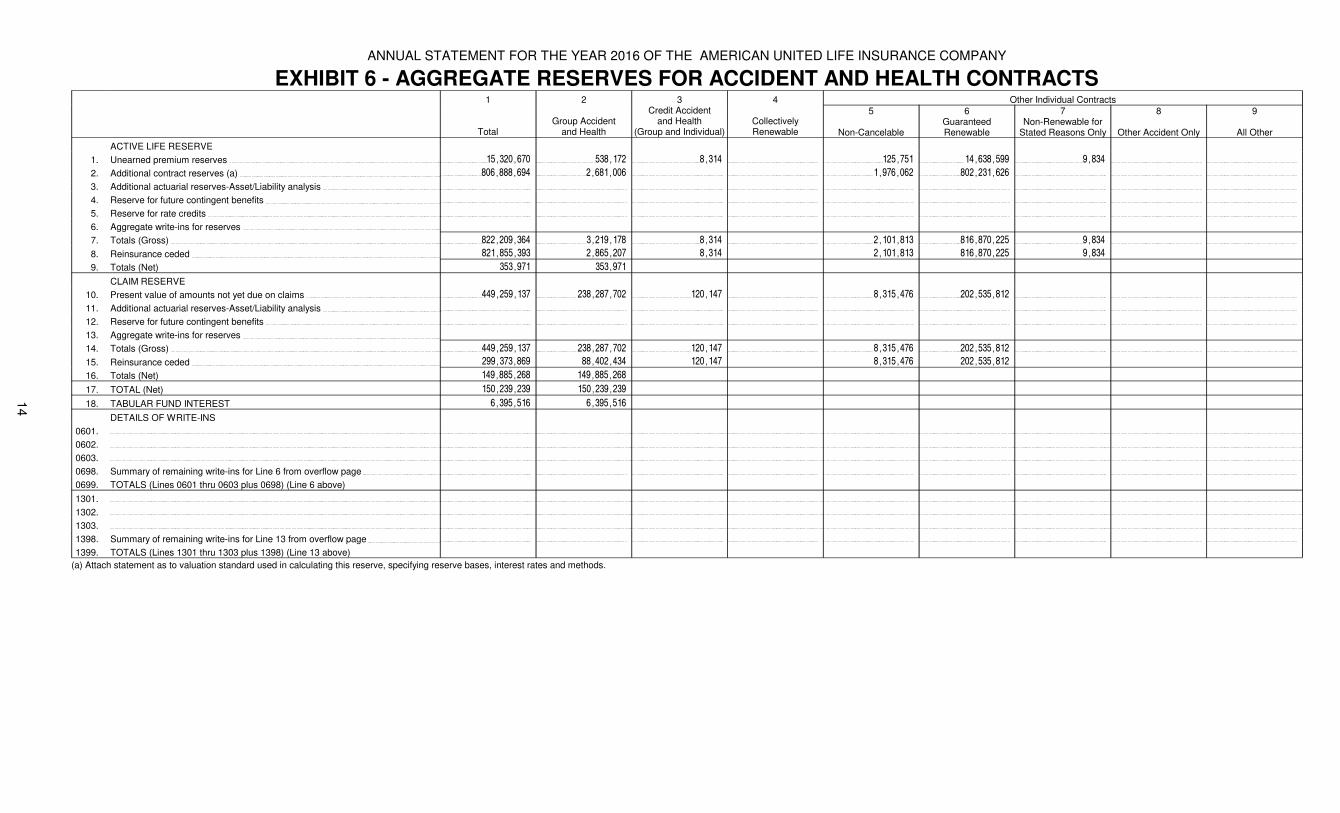

EXHIBIT 6 - AGGREGATE RESERVES FOR ACCIDENT AND HEALTH CONTRACTS1 2 3 4 Other Individual Contracts

TotalGroup Accident

and Health

Credit Accidentand Health

(Group and Individual)CollectivelyRenewable

5

Non-Cancelable

6Guaranteed Renewable

7Non-Renewable for

Stated Reasons Only

8

Other Accident Only

9

All Other

ACTIVE LIFE RESERVE

1. Unearned premium reserves 15,320,670 538,172 8,314 125,751 14,638,599 9,834

2. Additional contract reserves (a) 806,888,694 2,681,006 1,976,062 802,231,626

3. Additional actuarial reserves-Asset/Liability analysis

4. Reserve for future contingent benefits

5. Reserve for rate credits

6. Aggregate write-ins for reserves

7. Totals (Gross) 822,209,364 3,219,178 8,314 2,101,813 816,870,225 9,834

8. Reinsurance ceded 821,855,393 2,865,207 8,314 2,101,813 816,870,225 9,834

9. Totals (Net) 353,971 353,971

CLAIM RESERVE

10. Present value of amounts not yet due on claims 449,259,137 238,287,702 120,147 8,315,476 202,535,812

11. Additional actuarial reserves-Asset/Liability analysis

12. Reserve for future contingent benefits

13. Aggregate write-ins for reserves

14. Totals (Gross) 449,259,137 238,287,702 120,147 8,315,476 202,535,812

15. Reinsurance ceded 299,373,869 88,402,434 120,147 8,315,476 202,535,812

16. Totals (Net) 149,885,268 149,885,268

17. TOTAL (Net) 150,239,239 150,239,239

18. TABULAR FUND INTEREST 6,395,516 6,395,516

DETAILS OF WRITE-INS

0601.

0602.

0603.

0698. Summary of remaining write-ins for Line 6 from overflow page

0699. TOTALS (Lines 0601 thru 0603 plus 0698) (Line 6 above)

1301.

1302.

1303.

1398. Summary of remaining write-ins for Line 13 from overflow page

1399. TOTALS (Lines 1301 thru 1303 plus 1398) (Line 13 above)

(a) Attach statement as to valuation standard used in calculating this reserve, specifying reserve bases, interest rates and methods.

14

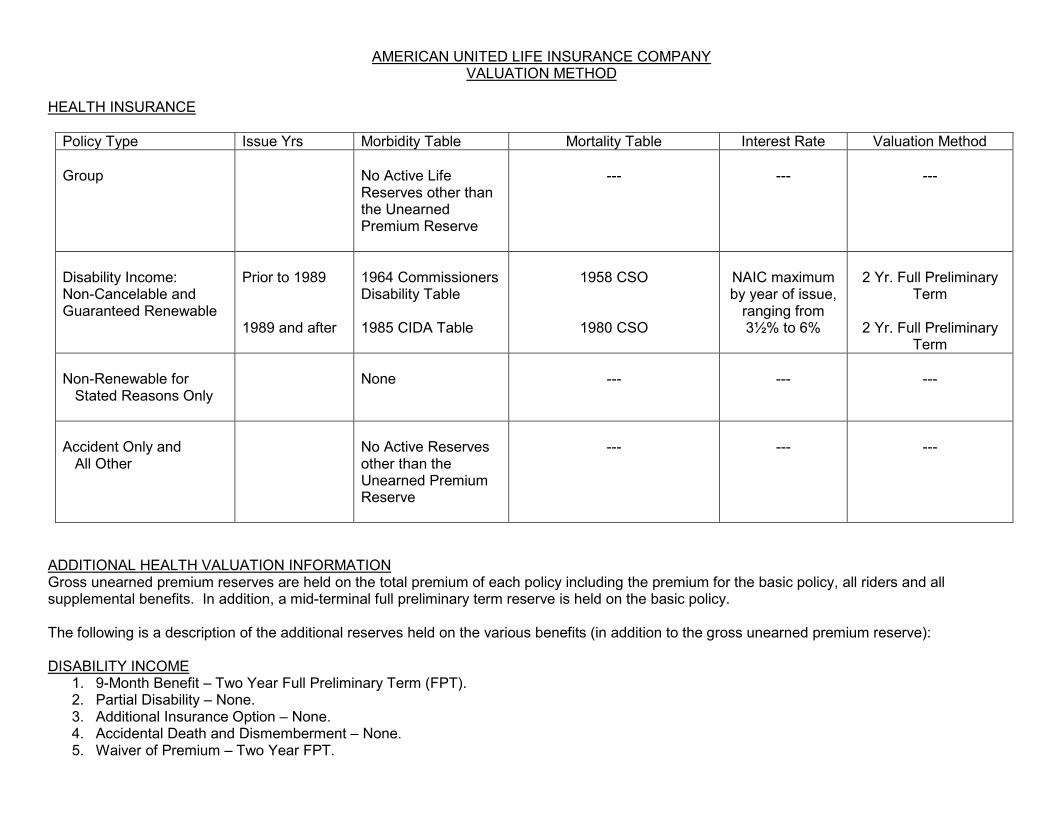

AMERICAN UNITED LIFE INSURANCE COMPANY VALUATION METHOD

HEALTH INSURANCE

Policy Type Issue Yrs Morbidity Table Mortality Table Interest Rate Valuation Method

Group

No Active Life Reserves other than the Unearned Premium Reserve

---

---

---

Disability Income: Non-Cancelable and Guaranteed Renewable

Prior to 1989 1989 and after

1964 Commissioners Disability Table 1985 CIDA Table

1958 CSO

1980 CSO

NAIC maximum by year of issue,

ranging from 3½% to 6%

2 Yr. Full Preliminary

Term

2 Yr. Full Preliminary Term

Non-Renewable for Stated Reasons Only

None

---

---

---

Accident Only and All Other

No Active Reserves other than the Unearned Premium Reserve

---

---

---

ADDITIONAL HEALTH VALUATION INFORMATION Gross unearned premium reserves are held on the total premium of each policy including the premium for the basic policy, all riders and all supplemental benefits. In addition, a mid-terminal full preliminary term reserve is held on the basic policy. The following is a description of the additional reserves held on the various benefits (in addition to the gross unearned premium reserve): DISABILITY INCOME

1. 9-Month Benefit – Two Year Full Preliminary Term (FPT). 2. Partial Disability – None. 3. Additional Insurance Option – None. 4. Accidental Death and Dismemberment – None. 5. Waiver of Premium – Two Year FPT.

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

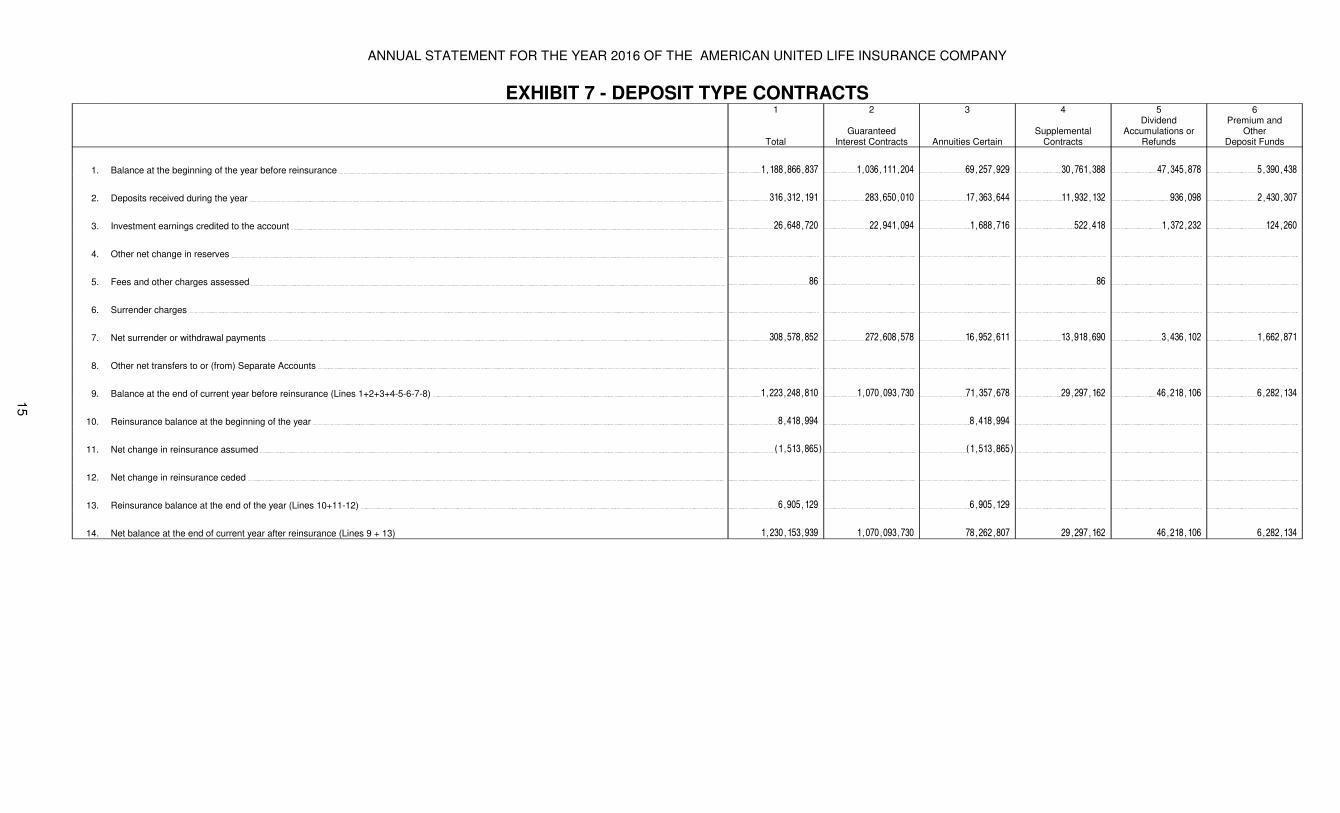

EXHIBIT 7 - DEPOSIT TYPE CONTRACTS1

Total

2

GuaranteedInterest Contracts

3

Annuities Certain

4

Supplemental Contracts

5Dividend

Accumulations or Refunds

6Premium and

OtherDeposit Funds

1. Balance at the beginning of the year before reinsurance 1,188,866,837 1,036,111,204 69,257,929 30,761,388 47,345,878 5,390,438

2. Deposits received during the year 316,312,191 283,650,010 17,363,644 11,932,132 936,098 2,430,307

3. Investment earnings credited to the account 26,648,720 22,941,094 1,688,716 522,418 1,372,232 124,260

4. Other net change in reserves

5. Fees and other charges assessed 86 86

6. Surrender charges

7. Net surrender or withdrawal payments 308,578,852 272,608,578 16,952,611 13,918,690 3,436,102 1,662,871

8. Other net transfers to or (from) Separate Accounts

9. Balance at the end of current year before reinsurance (Lines 1+2+3+4-5-6-7-8) 1,223,248,810 1,070,093,730 71,357,678 29,297,162 46,218,106 6,282,134

10. Reinsurance balance at the beginning of the year 8,418,994 8,418,994

11. Net change in reinsurance assumed (1,513,865) (1,513,865)

12. Net change in reinsurance ceded

13. Reinsurance balance at the end of the year (Lines 10+11-12) 6,905,129 6,905,129

14. Net balance at the end of current year after reinsurance (Lines 9 + 13) 1,230,153,939 1,070,093,730 78,262,807 29,297,162 46,218,106 6,282,134

15

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

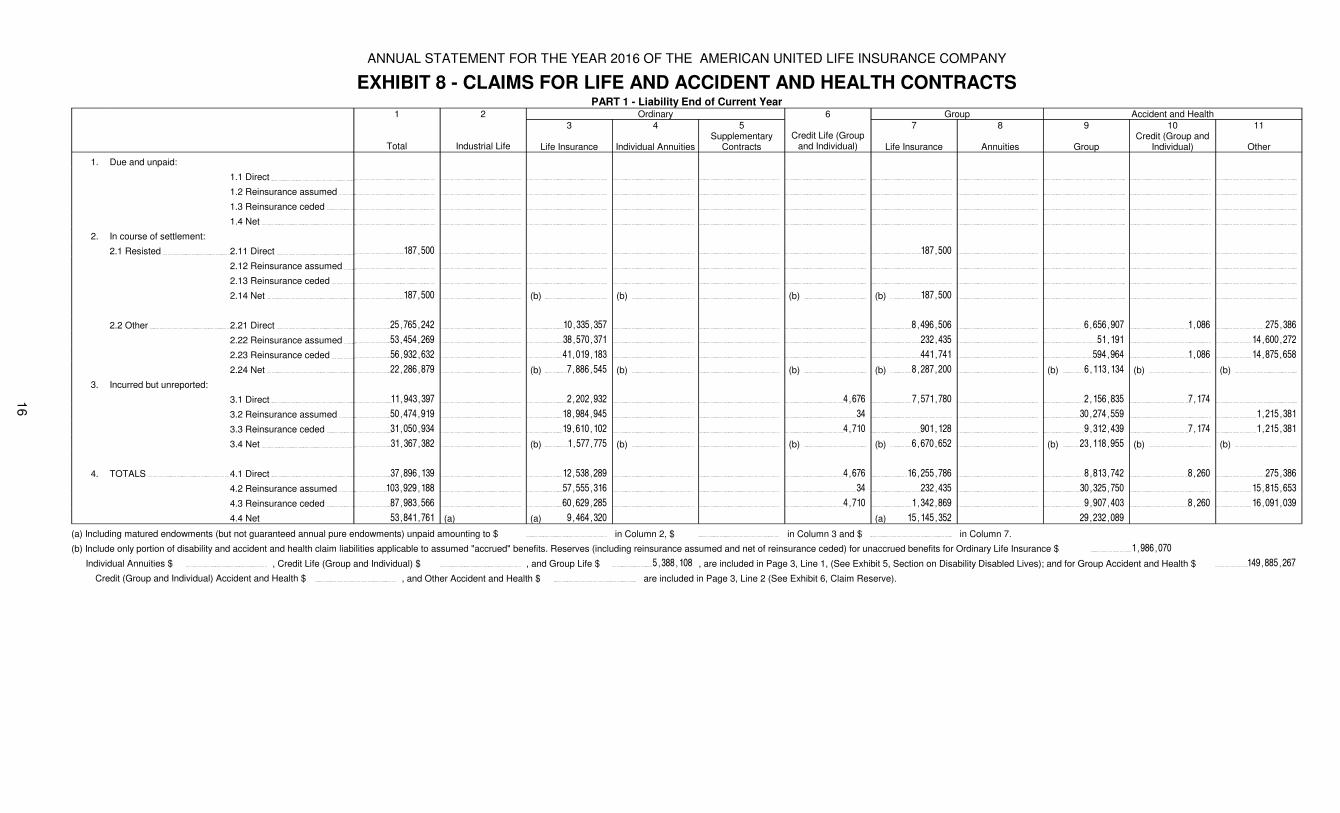

EXHIBIT 8 - CLAIMS FOR LIFE AND ACCIDENT AND HEALTH CONTRACTSPART 1 - Liability End of Current Year

1 2 Ordinary 6 Group Accident and Health

Total Industrial Life

3

Life Insurance

4

Individual Annuities

5Supplementary

ContractsCredit Life (Group

and Individual)

7

Life Insurance

8

Annuities

9

Group

10Credit (Group and

Individual)

11

Other

1. Due and unpaid:

1.1 Direct

1.2 Reinsurance assumed

1.3 Reinsurance ceded

1.4 Net

2. In course of settlement:

2.1 Resisted 2.11 Direct 187,500 187,500

2.12 Reinsurance assumed

2.13 Reinsurance ceded

2.14 Net 187,500 (b) (b) (b) (b) 187,500

2.2 Other 2.21 Direct 25,765,242 10,335,357 8,496,506 6,656,907 1,086 275,386

2.22 Reinsurance assumed 53,454,269 38,570,371 232,435 51,191 14,600,272

2.23 Reinsurance ceded 56,932,632 41,019,183 441,741 594,964 1,086 14,875,658

2.24 Net 22,286,879 (b) 7,886,545 (b) (b) (b) 8,287,200 (b) 6,113,134 (b) (b)

3. Incurred but unreported:

3.1 Direct 11,943,397 2,202,932 4,676 7,571,780 2,156,835 7,174

3.2 Reinsurance assumed 50,474,919 18,984,945 34 30,274,559 1,215,381

3.3 Reinsurance ceded 31,050,934 19,610,102 4,710 901,128 9,312,439 7,174 1,215,381

3.4 Net 31,367,382 (b) 1,577,775 (b) (b) (b) 6,670,652 (b) 23,118,955 (b) (b)

4. TOTALS 4.1 Direct 37,896,139 12,538,289 4,676 16,255,786 8,813,742 8,260 275,386

4.2 Reinsurance assumed 103,929,188 57,555,316 34 232,435 30,325,750 15,815,653

4.3 Reinsurance ceded 87,983,566 60,629,285 4,710 1,342,869 9,907,403 8,260 16,091,039

4.4 Net 53,841,761 (a) (a) 9,464,320 (a) 15,145,352 29,232,089

(a) Including matured endowments (but not guaranteed annual pure endowments) unpaid amounting to $ in Column 2, $ in Column 3 and $ in Column 7.

(b) Include only portion of disability and accident and health claim liabilities applicable to assumed "accrued" benefits. Reserves (including reinsurance assumed and net of reinsurance ceded) for unaccrued benefits for Ordinary Life Insurance $ 1,986,070

Individual Annuities $ , Credit Life (Group and Individual) $ , and Group Life $ 5,388,108 , are included in Page 3, Line 1, (See Exhibit 5, Section on Disability Disabled Lives); and for Group Accident and Health $ 149,885,267

Credit (Group and Individual) Accident and Health $ , and Other Accident and Health $ are included in Page 3, Line 2 (See Exhibit 6, Claim Reserve).

16

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

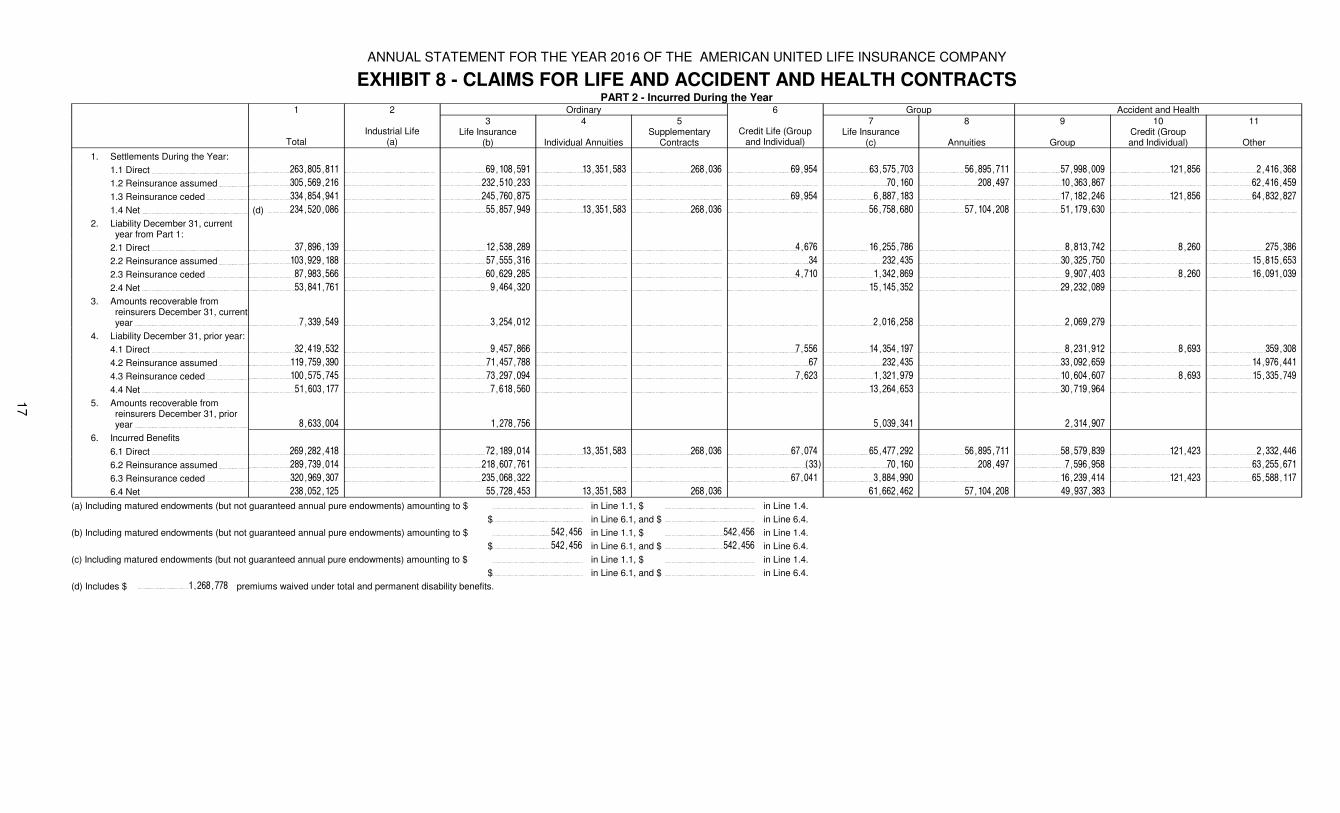

EXHIBIT 8 - CLAIMS FOR LIFE AND ACCIDENT AND HEALTH CONTRACTSPART 2 - Incurred During the Year

1 2 Ordinary 6 Group Accident and Health

TotalIndustrial Life

(a)

3Life Insurance

(b)

4

Individual Annuities

5Supplementary

ContractsCredit Life (Group

and Individual)

7Life Insurance

(c)

8

Annuities

9

Group

10Credit (Groupand Individual)

11

Other

1. Settlements During the Year:

1.1 Direct 263,805,811 69,108,591 13,351,583 268,036 69,954 63,575,703 56,895,711 57,998,009 121,856 2,416,368

1.2 Reinsurance assumed 305,569,216 232,510,233 70,160 208,497 10,363,867 62,416,459

1.3 Reinsurance ceded 334,854,941 245,760,875 69,954 6,887,183 17,182,246 121,856 64,832,827

1.4 Net (d) 234,520,086 55,857,949 13,351,583 268,036 56,758,680 57,104,208 51,179,630

2. Liability December 31, current year from Part 1:

2.1 Direct 37,896,139 12,538,289 4,676 16,255,786 8,813,742 8,260 275,386

2.2 Reinsurance assumed 103,929,188 57,555,316 34 232,435 30,325,750 15,815,653

2.3 Reinsurance ceded 87,983,566 60,629,285 4,710 1,342,869 9,907,403 8,260 16,091,039

2.4 Net 53,841,761 9,464,320 15,145,352 29,232,089

3. Amounts recoverable from reinsurers December 31, current year 7,339,549 3,254,012 2,016,258 2,069,279

4. Liability December 31, prior year:

4.1 Direct 32,419,532 9,457,866 7,556 14,354,197 8,231,912 8,693 359,308

4.2 Reinsurance assumed 119,759,390 71,457,788 67 232,435 33,092,659 14,976,441

4.3 Reinsurance ceded 100,575,745 73,297,094 7,623 1,321,979 10,604,607 8,693 15,335,749

4.4 Net 51,603,177 7,618,560 13,264,653 30,719,964

5. Amounts recoverable from reinsurers December 31, prior year 8,633,004 1,278,756 5,039,341 2,314,907

6. Incurred Benefits

6.1 Direct 269,282,418 72,189,014 13,351,583 268,036 67,074 65,477,292 56,895,711 58,579,839 121,423 2,332,446

6.2 Reinsurance assumed 289,739,014 218,607,761 (33) 70,160 208,497 7,596,958 63,255,671

6.3 Reinsurance ceded 320,969,307 235,068,322 67,041 3,884,990 16,239,414 121,423 65,588,117

6.4 Net 238,052,125 55,728,453 13,351,583 268,036 61,662,462 57,104,208 49,937,383

(a) Including matured endowments (but not guaranteed annual pure endowments) amounting to $ in Line 1.1, $ in Line 1.4.

$ in Line 6.1, and $ in Line 6.4.

(b) Including matured endowments (but not guaranteed annual pure endowments) amounting to $ 542,456 in Line 1.1, $ 542,456 in Line 1.4.

$ 542,456 in Line 6.1, and $ 542,456 in Line 6.4.

(c) Including matured endowments (but not guaranteed annual pure endowments) amounting to $ in Line 1.1, $ in Line 1.4.

$ in Line 6.1, and $ in Line 6.4.

(d) Includes $ 1,268,778 premiums waived under total and permanent disability benefits.

17

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

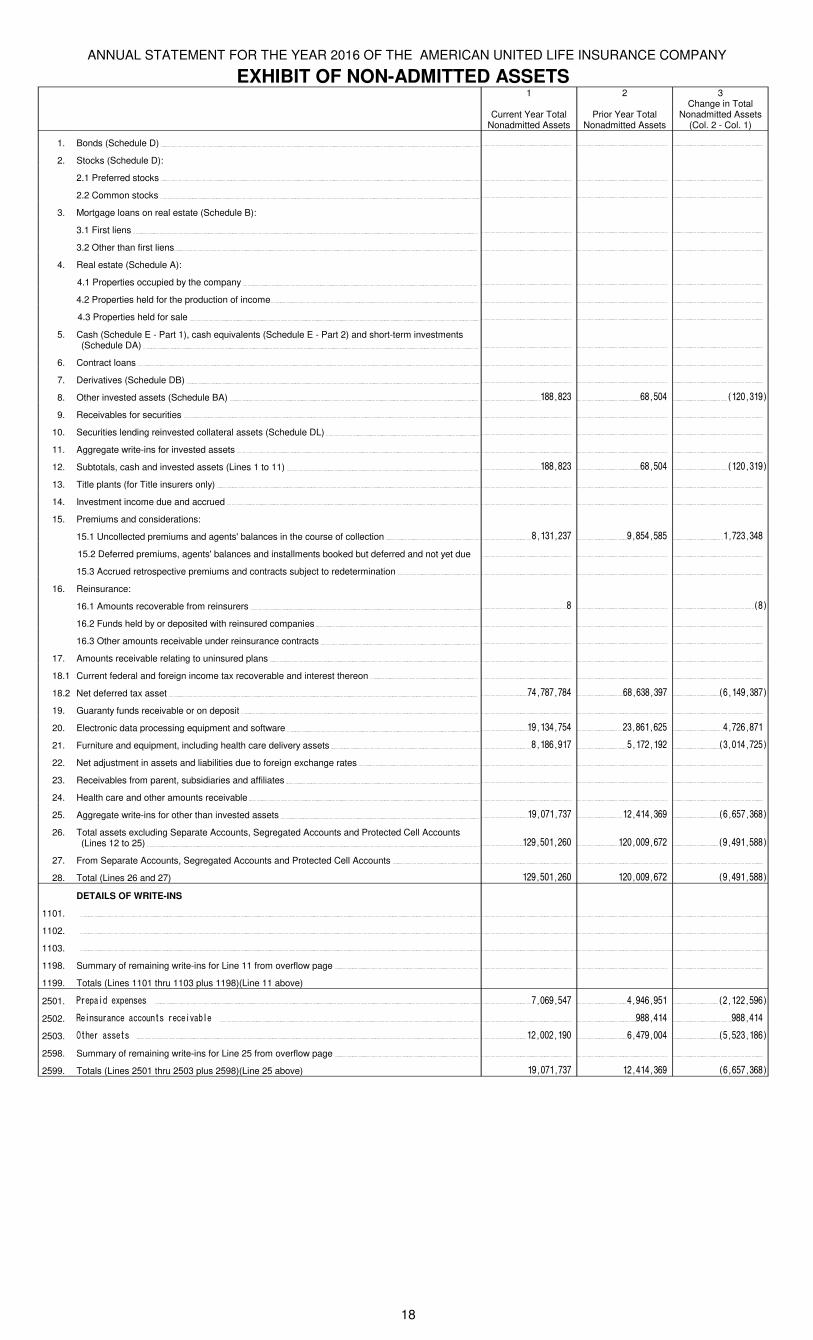

EXHIBIT OF NON-ADMITTED ASSETS1

Current Year Total Nonadmitted Assets

2

Prior Year Total Nonadmitted Assets

3Change in Total

Nonadmitted Assets (Col. 2 - Col. 1)

1. Bonds (Schedule D)

2. Stocks (Schedule D):

2.1 Preferred stocks

2.2 Common stocks

3. Mortgage loans on real estate (Schedule B):

3.1 First liens

3.2 Other than first liens

4. Real estate (Schedule A):

4.1 Properties occupied by the company

4.2 Properties held for the production of income

4.3 Properties held for sale

5. Cash (Schedule E - Part 1), cash equivalents (Schedule E - Part 2) and short-term investments (Schedule DA)

6. Contract loans

7. Derivatives (Schedule DB)

8. Other invested assets (Schedule BA) 188,823 68,504 (120,319)

9. Receivables for securities

10. Securities lending reinvested collateral assets (Schedule DL)

11. Aggregate write-ins for invested assets

12. Subtotals, cash and invested assets (Lines 1 to 11) 188,823 68,504 (120,319)

13. Title plants (for Title insurers only)

14. Investment income due and accrued

15. Premiums and considerations:

15.1 Uncollected premiums and agents' balances in the course of collection 8,131,237 9,854,585 1,723,348

15.2 Deferred premiums, agents' balances and installments booked but deferred and not yet due

15.3 Accrued retrospective premiums and contracts subject to redetermination

16. Reinsurance:

16.1 Amounts recoverable from reinsurers 8 (8)

16.2 Funds held by or deposited with reinsured companies

16.3 Other amounts receivable under reinsurance contracts

17. Amounts receivable relating to uninsured plans

18.1 Current federal and foreign income tax recoverable and interest thereon

18.2 Net deferred tax asset 74,787,784 68,638,397 (6,149,387)

19. Guaranty funds receivable or on deposit

20. Electronic data processing equipment and software 19,134,754 23,861,625 4,726,871

21. Furniture and equipment, including health care delivery assets 8,186,917 5,172,192 (3,014,725)

22. Net adjustment in assets and liabilities due to foreign exchange rates

23. Receivables from parent, subsidiaries and affiliates

24. Health care and other amounts receivable

25. Aggregate write-ins for other than invested assets 19,071,737 12,414,369 (6,657,368)

26. Total assets excluding Separate Accounts, Segregated Accounts and Protected Cell Accounts (Lines 12 to 25) 129,501,260 120,009,672 (9,491,588)

27. From Separate Accounts, Segregated Accounts and Protected Cell Accounts

28. Total (Lines 26 and 27) 129,501,260 120,009,672 (9,491,588)

DETAILS OF WRITE-INS

1101.

1102.

1103.

1198. Summary of remaining write-ins for Line 11 from overflow page

1199. Totals (Lines 1101 thru 1103 plus 1198)(Line 11 above)

2501. Prepaid expenses 7,069,547 4,946,951 (2,122,596)

2502. Reinsurance accounts receivable 988,414 988,414

2503. Other assets 12,002,190 6,479,004 (5,523,186)

2598. Summary of remaining write-ins for Line 25 from overflow page

2599. Totals (Lines 2501 thru 2503 plus 2598)(Line 25 above) 19,071,737 12,414,369 (6,657,368)

18

ANNUAL STATEMENT FOR THE YEAR 2016 OF THE AMERICAN UNITED LIFE INSURANCE COMPANY

19

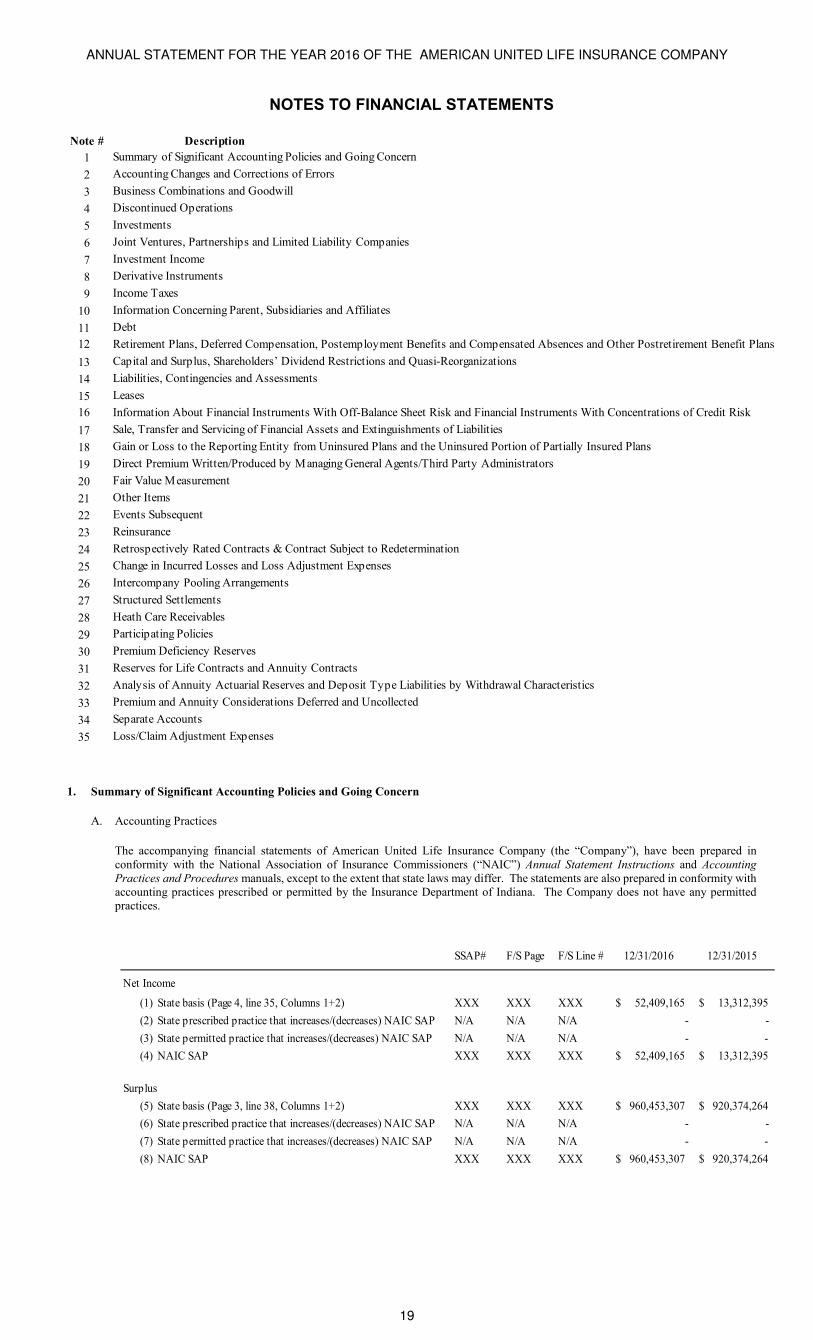

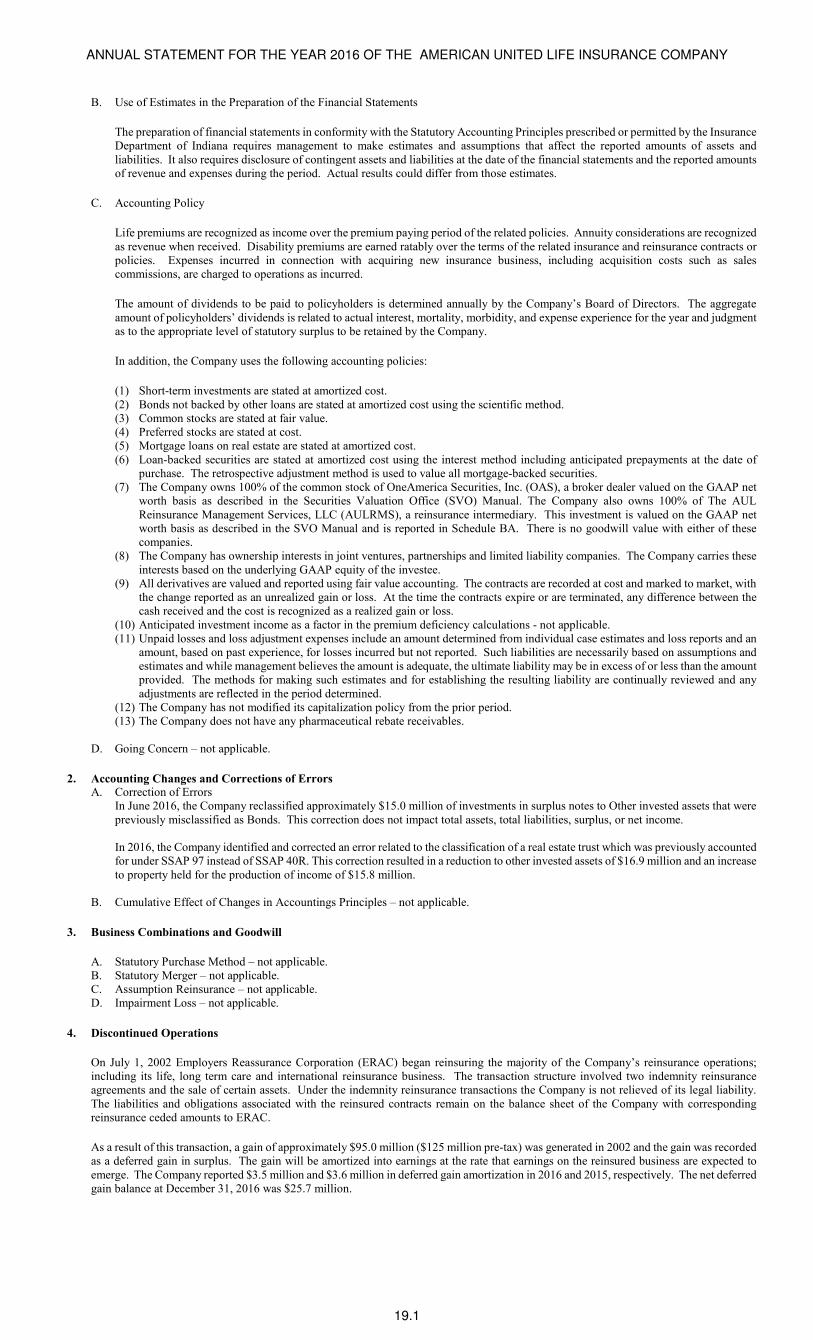

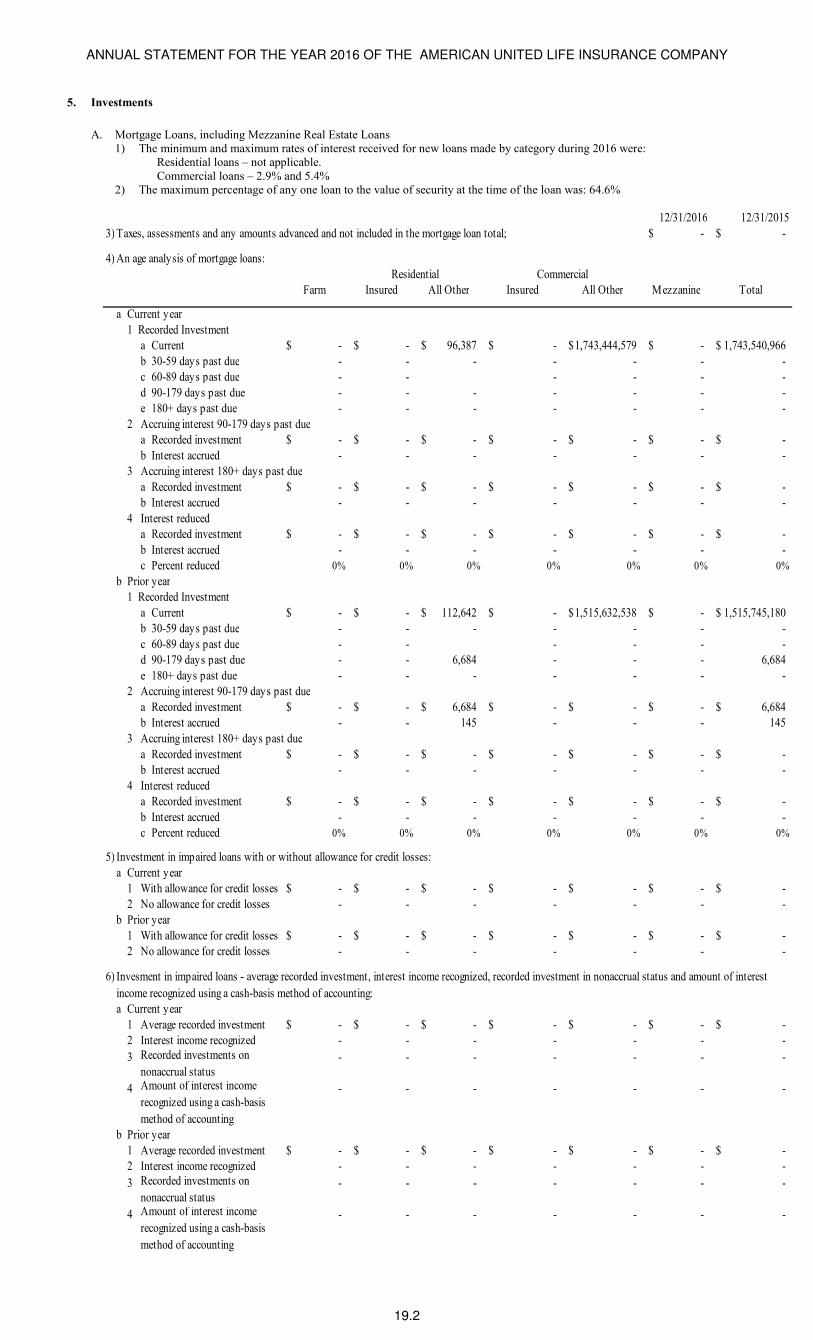

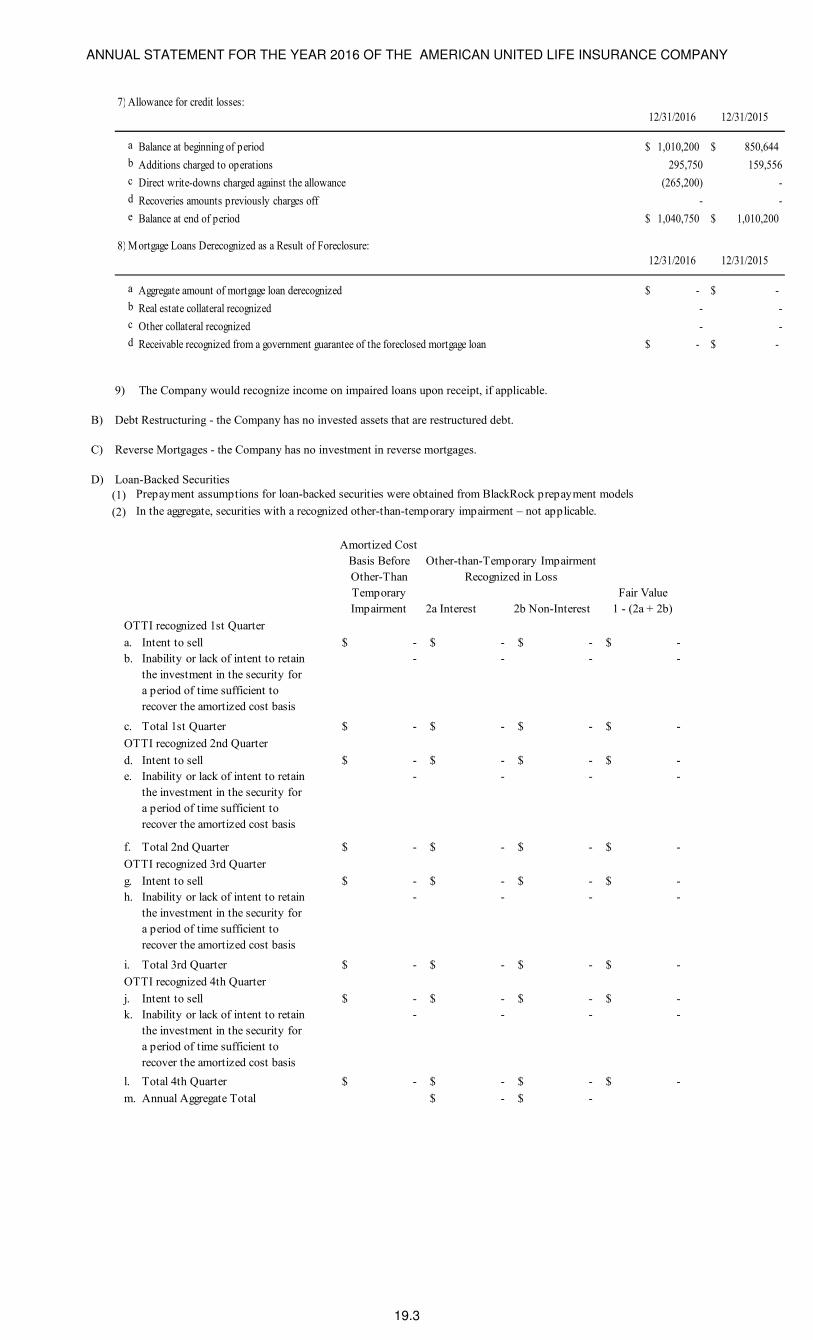

NOTES TO FINANCIAL STATEMENTS

Note # Description

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

Information About Financial Instruments With Off-Balance Sheet Risk and Financial Instruments With Concentrations of Credit Risk

Debt

Capital and Surplus, Shareholders’ Dividend Restrictions and Quasi-Reorganizations

Liabilities, Contingencies and Assessments

Summary of Significant Accounting Policies and Going Concern

Accounting Changes and Corrections of Errors

Business Combinations and Goodwill

Discontinued Operations

Investments

Joint Ventures, Partnerships and Limited Liability Companies

Leases

Investment Income

Derivative Instruments

Income Taxes

Information Concerning Parent, Subsidiaries and Affiliates

Retirement Plans, Deferred Compensation, Postemployment Benefits and Compensated Absences and Other Postretirement Benefit Plans

Intercompany Pooling Arrangements

Structured Settlements

Heath Care Receivables

Sale, Transfer and Servicing of Financial Assets and Extinguishments of Liabilities