Embed Size (px)

Citation preview

The views expressed in these papers and presentations are those of the author(s) only, and the presence of them, or of links to them, on the IMF website does not imply that the IMF, its Executive Board, or its management endorses or shares the views expressed in the papers or presentations.

The US Fiscal Outlook and Treasury Debt IssuancePresentation to 10th OECD Global Bond Market Forum

Stephen M VajsOffice of Debt Management

April 30, 2008

2Office of Debt Management

Topics for today’s discussion

I. Roles of Treasury, Federal Reserve, and Bureau of Public Debt

II. Regular and predictable issuance with a set issuance calendar

III. Role and regulation of primary dealers

IV. Secondary market liquidity and market regulation

3Office of Debt Management

Roles of Treasury, Federal Reserve, and Bureau of Public Debt

Treasury Department• Responsible for Federal government finances, including: receipts, payments, and

financing.• Manages Federal government debt portfolio.

Federal Reserve System• Is the US central bank system. Conducts US monetary policy with dual mandate of:

price stability and full employment.• Acts as the Federal government’s fiscal agent, holds our cash balances and assists

with receipts, payments and auction operations.• Assists with financing of the Federal government through their primary dealers

system.• Regulates the primary dealers.

Bureau of Public Debt (BPD)• Responsible for the financing operations of the federal government – they operate the

auction systems. Whereas Treasury Department officials make financing, issuance and portfolio decisions, BPD carries them out.

4Office of Debt Management

Treasury Issuance Objectives and Constraints

Our Objectives • Long-term: Lowest cost of financing over time• Short-term: Adequate cash balances to cover expenses

Constraints• Uncertainty: Forecast errors, legislation, etc. all create uncertainty in deficit

forecasts, debt limit problems• Size: Treasury is too large to behave opportunistically• Fluctuations in non-marketable debt (Savings Bonds, State and Local

Government Securities (SLGS))

Policy Outcomes• We are regular market participants, not market timers -- “Regular and

Predictable”• We don’t react to interest rate levels• We need flexibility• We strive for transparency

5Office of Debt Management

Size of US Treasury Debt Operations is Hard to Grasp

$4.4 trillion issued in 219 auctions in FY 2007

$238 billion paid in net interest in FY 2007

• represented 8.7% of Government expenditures

More than $1 trillion moved between accounts on NBES daily

More than $500 billion traded daily (primary dealers)

• For comparison NYSE trades about $50 billion in equity daily

$4.4 trillion in marketable debt* outstanding end of FY 2007

• represents roughly a quarter of U.S. credit markets

* includes holdings by the Federal Reserve

6Office of Debt Management

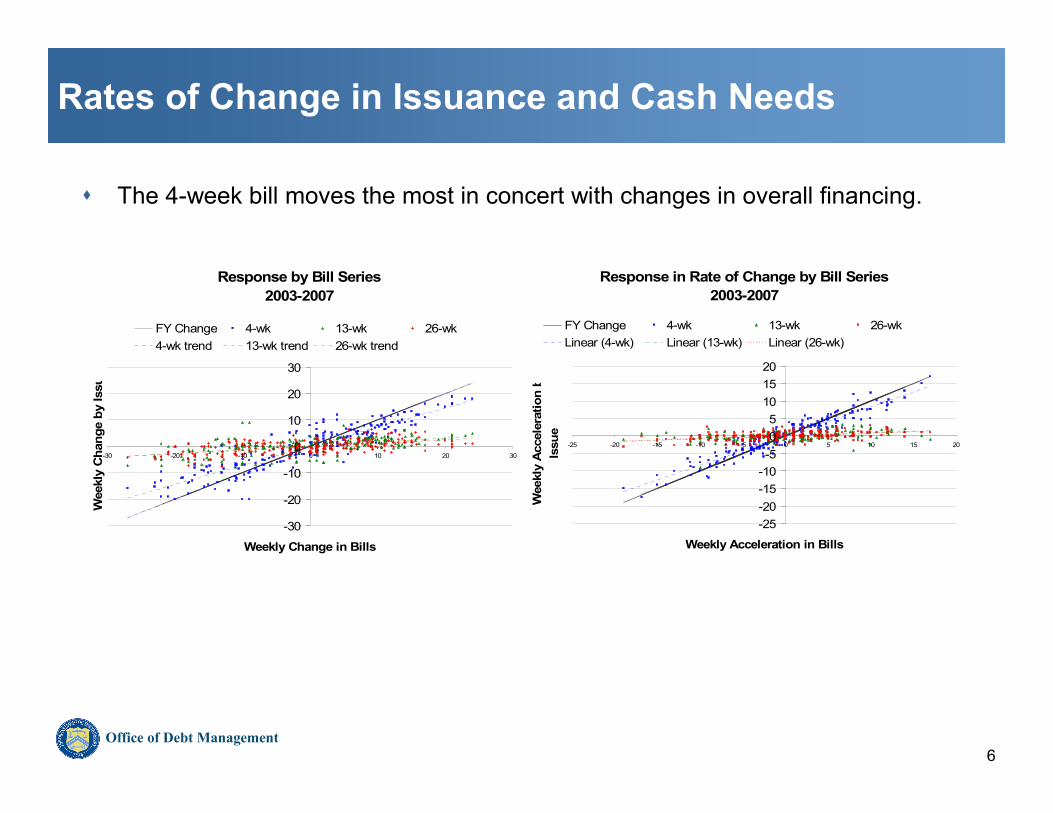

Rates of Change in Issuance and Cash Needs

Response in Rate of Change by Bill Series2003-2007

-25-20-15-10-505

101520

-25 -20 -15 -10 -5 0 5 10 15 20

Weekly Acceleration in BillsW

eekl

y A

ccel

erat

ion

bIs

sue

FY Change 4-wk 13-wk 26-wkLinear (4-wk) Linear (13-wk) Linear (26-wk)

The 4-week bill moves the most in concert with changes in overall financing.

Response by Bill Series2003-2007

-30

-20

-10

0

10

20

30

-30 -20 -10 0 10 20 30

Weekly Change in Bills

Wee

kly

Cha

nge

by Is

su

FY Change 4-wk 13-wk 26-wk4-wk trend 13-wk trend 26-wk trend

7Office of Debt Management

Evaluating the proper number, type and mix of securities in our portfolio is an ongoing effort

Percent of Total Outstanding Treasury Marketable Debt

0%

10%

20%

30%

40%

50%

60%

70%

2001 2002 2003 2004 2005 2006 2007

End of Fiscal Year

0%

5%

10%

15%

Bills (LHS) Nominal Coupons (LHS) TIPS (RHS)

8Office of Debt Management

Regular and predictable debt issuance with a set auction calendar

Universal debt management objective• Lowest cost of financing over time.

Different debt management philosophies• Regular and predictable issuance using a set issuance calendar,

• Opportunistic issuance,

• A hybrid model is probably best suited for most countries.

9Office of Debt Management

Transparency and PredictabilityLeads to Greater Investor Participation over the Long Run

Average Daily Trading Volume of U.S. Treasury Securities (annual)

0

100

200

300

400

500

600

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

*$

Bill

ions

Source: FRB-NY

10Office of Debt Management

Regular and predictable debt issuance with a set auction calendar

• An opportunistic issuance philosophy tries to finance the government by timing the markets, thereby achieving cheap rates.

• Opportunistic issuance appears appealing but can you consistently outsmart the markets over time, should you even try?

• Can you build a thoughtful, balanced, risk mitigating portfolio from opportunistic financing?

• Can you develop a full, domestic yield curve critical to local market development from opportunistic financing?

11Office of Debt Management

Regular and predictable debt issuance with a set auction calendar

What does regular and predictable debt issuance mean? Policy outcomes• Regular market participants, but not market timers,

• Don’t react to interest rate levels,

• Strive for transparency in decision making,

• Provide certainty of supply to the market place,

• Engage in “regular and predictable” auctions, of a set of straight forward securities, on a set issuance schedule.

12Office of Debt Management

Regular and predictable debt issuance with a set auction calendar

US Treasury issuance schedule – Pattern of financing

Nominal Securities Frequency Max Increments• 4-week bills (52x) Weekly $7 billion • 13-& 26-week bills (52x) Weekly $2 billion• 2-year notes (12x) Monthly $2 billion• 5-year notes (12x) Monthly $1 billion• 10-year notes (8x) Quarterly, with reopening $1 billion• 30-year bonds (4x) Quarterly $1 billion

Treasury Inflation Protected Securities (TIPS, our inflation linked product)• 5-year TIP (2x) Semi-annual $2 billion• 10-year TIP (4x) Quarterly $2 billion• 20-year TIP (2x) Semi-annual $2 billion

13Office of Debt Management

Quarterly Debt Issuance Patterns

Two & Three Years

-40-20

020406080

100

I-02

III I-03

III I-04

III I-05

III I-06

III I-07

III

Bills

-200-150-100-50

050

100150

I-02

III I-03

III I-04

III I-05

III I-06

III I-07

III

Five to Ten Years

-100

-50

0

50

100

I-02

III I-03

III I-04

III I-05

III I-06

III I-07

III

Five to Ten Year TIPS

-15-10-505

10152025

I-02

III I-03

III I-04

III I-05

III I-06

III I-07

III

Over Ten Years TIPS

02468

101214

I-02

III I-03

III I-04

III I-05

III I-06

III I-07

III

Over Ten Years

-15-10-505

1015

I-02

III I-03

III I-04

III I-05

III I-06

III I-07

III

Buybacks

-10

-8

-6-4

-2

0

I-02

III I-03

III I-04

III I-05

III I-06

III I-07

III

Net Marketable Borrowing

-200-150-100-50

050

100150200

I-02

III I-03

III I-04

III I-05

III I-06

III I-07

III

14Office of Debt Management

Regular and predictable debt issuance with a set auction calendar

How do you achieve lowest cost financing through regular and predictable issuance?

• By providing certainty of supply, through a set auction schedule and transparent decision making, as an issuer you promote investor participation and are rewarded with a liquidity premium,

• Instead of timing the market, you achieve lower borrowing costs through consistent investor demand for your liquid securities.

15Office of Debt Management

Regular and predictable debt issuance with a set auction calendar

Advantages of regular and predictable issuance allows you to prudently spreaddebt across maturities to

• Capture a liquidity premium and lower borrowing costs,• Facilitate local market development by building a full yield curve,• Reduce risk: spreading out issuance reduces rollover risk, mitigating interest

cost fluctuations,• Diversify the investor base, and fill maturities preferences,• Improve cash management, issue regularly to dynamically meet fluctuating

cash needs.

16Office of Debt Management

Regular and predictable debt issuance with a set auction calendar

Regular and predictable debt management policy tools• Auction Sizes: within certain established increments,• Auction Frequency,• Security Offering Menu,• Auction Regulations,• Market monitoring, consultation, and surveillance.

17Office of Debt Management

Role and regulation of primary dealers

Primary dealers are banks and securities firms who may trade directly with theFederal Reserve System, they are required to

• To make bids and offers with the Federal Reserve when they conduct open market operations - monetary policy,

• To actively participate in all U.S. Treasury auctions,• Provide information about the financial markets to the Federal Reserve and

Treasury Department,• Consult with the Treasury about financing the federal government.

Primary dealer facts• Currently there are 21 primary dealers, at one time there were over 40,• Firms represent a wide geographic distribution, 11 are non-US based firms,• They are: BNP, Bank of America, Barclays, Bear Stearns, Cantor Fitzgerald,

Citigroup, Countrywide, Credit Suisse, Daiwa, Deutsche Bank, Dresdner, RBS Greenwich, Goldman Sachs, HSBC, JP Morgan, Lehman Brothers, Merrill Lynch, Mizuho, Morgan Stanley, Nomura, and UBS.

18Office of Debt Management

Role and regulation of primary dealers

Advantages of being a primary dealer• Access to trading with the Federal Reserve and the information flows that

accompany that,• Because dealers purchase a vast majority of Treasury securities this allows

dealers to be an intermediary between Treasury and ultimate investors,• Opportunity to consult frequently with monetary and fiscal policy authorities.

The Federal Reserve regulates the primary dealers, not the Treasury Department• Federal Reserve periodically meets with the leadership of the primary dealers and

grades their performance in open market operations and in Treasury auctions,• The Federal Reserve uses moral suasion with the dealers to ensure their active

performance participation and performance,• Although Treasury does not regulate the primary dealers, Treasury does meet with

them twice a year to gather their views on: the financial markets, federal government budget financing, and their auction performance.

19Office of Debt Management

Secondary market liquidity and market regulation

Promote market transparency• Make transparent, predictable issuance decisions,• Regular issuance provides a structured framework for investor participation,• Issuers must be available to customers for feedback and guidance, listen and be

credible.

Ensure proper regulation and market integrity• Broadly speaking you must protect investors to attract participants,• Establish consistent, fair practices across markets, level playing field for participants,• Instills investor confidence in markets.

But don’t over regulate• Don’t interfere with price discovery,• Don’t interfere with occasionally volatile markets, let participants work through issues

– don’t over react,• Let participants develop trading practices,• Encourage innovation through market based, private working groups.

20Office of Debt Management

Secondary market liquidity and market regulation

Cornerstones of liquid secondary market• Concentration of issuance in critical tenors: 1-month, 3-month, 6-month, 2-

year, 5-year, 10-year, 30-year, 5- 10- and 20-year TIPS,

• Repo markets and ability to short issues,

• Futures market,

• When issued trading: after announcement, pre-settlement. Facilitates investor demand and price discovery.

• STRIPS market

21Office of Debt Management

Secondary market liquidity and market regulation

Share of non-resident participation in G-7 government bond markets

0%

10%

20%

30%

40%

50%

60%

70%

Canada UK U.S. France Germany Japan Italy

Mar 2005

Q3 2005

Dec 2005

end-2004

end-2004

Q4 2005

Sep 2004

22Office of Debt Management

Secondary market liquidity and market regulation

Foreign Holdings of US Treasury Securities (Bil.$)

0

50

100

150

200

250

300

350

400

450

500

550

600

650

700

750

Oct

-01

Oct

-02

Oct

-03

Oct

-04

Oct

-05

Oct

-06

Japan: Holdings of US Treasury Securities (Bil.$) China: Holdings of US Treasury Securities (Bil.$)

United Kingdom: Holdings of US Treasury Securities (Bil.$) OPEC: Holdings of US Treasury Securities (Bil.$)

Caribbean Banking Centers: Holdings of US Treasury Securities (Bil.$) Korea: Holdings of US Treasury Securities (Bil.$)

Taiw an: Holdings of US Treasury Securities (Bil.$)

Japan

China

UK

23Office of Debt Management

The Top 3 Emerging Buyers of Treasuries have Increased Their Rate of Accumulation. Brazil, for example, is now the 5th Largest Holder of U.S. Treasuries.

Top 3 Em erging Buyers of U.S. TreasuriesExponential Increase in Holdings

0

20

40

60

80

100

120

140

Jun-00 Jun-01 Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07

$ Billions

-10

40

90

140

190

240$Billions

OPECUKBrazil

Note: Flows through the U.K. include Middle-Eastern, Asian, and Hedge Fund flows.

24Office of Debt Management

Treasury Monitors and is Supportive of Private-Sector Initiatives for Ensuring the Integrity of the Marketplace for Treasury Securities

Recent introduction of a principles-based framework a private sector called the Treasury Market Practices Group (TMPG).

Evaluate and enhance their current activities in the secondary markets and to fulfill their responsibilities as stakeholders in the Treasury market.

Signs of success and improved liquidity.

Suggested sites for more information on this important initiative:• http://www.newyorkfed.org/tmpg/• http://www.newyorkfed.org/newsevents/news/markets/2007/an070209.html