Embed Size (px)

Citation preview

2014 ACFE European Fraud Conference

5A: Concurrent Session (Accounting) 15.20 (3.20 pm)

Preventing Fraudulent Reporting: A European Perspective

Kurt Ramin, CFE, CPA

Director and Consultant, KPR Associates and Former Partner, PwC, New York and Director, IFRS Foundation, London

Hotel Hilton, Amsterdam, 52’21’04.52 N 4’52’19.69 E March 24, 2014, 15.20 to 16.40

© Kurt Ramin 2014 [email protected]

AGENDA

• Capital Markets versus SMEs

• IFRS – US GAAP - SEC

• XBRL – Oracle-Hyperion/SAP

• ESG = GRI/SASB

• Integrated Reporting as a connector

• Technology and Paradigm Shift needed

• Discussion

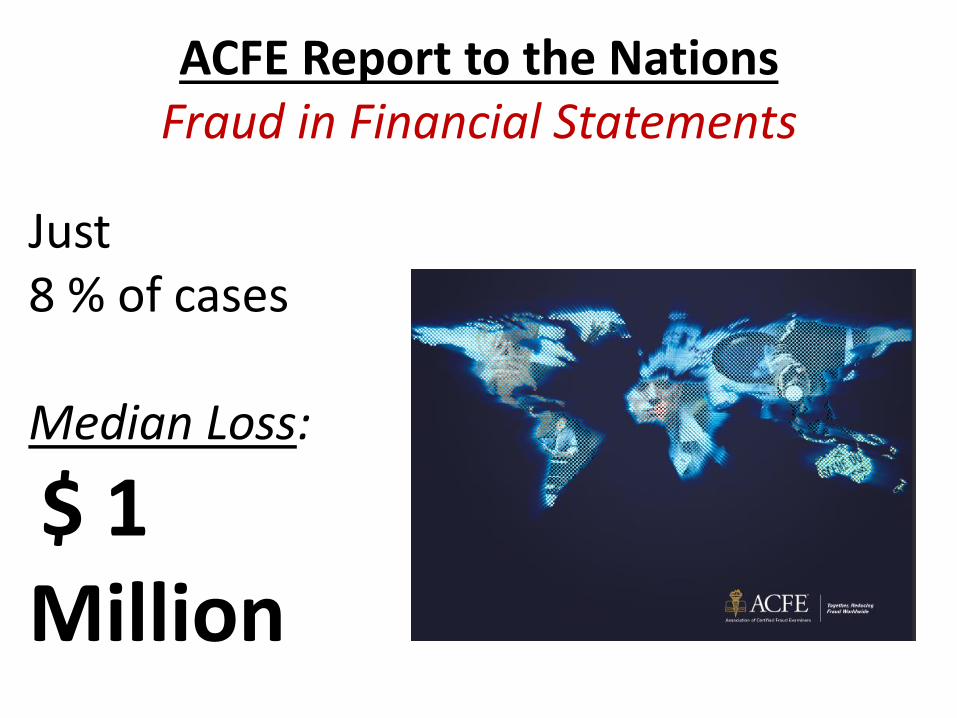

ACFE Report to the Nations Fraud in Financial Statements

Just 8 % of cases Median Loss:

$ 1 Million

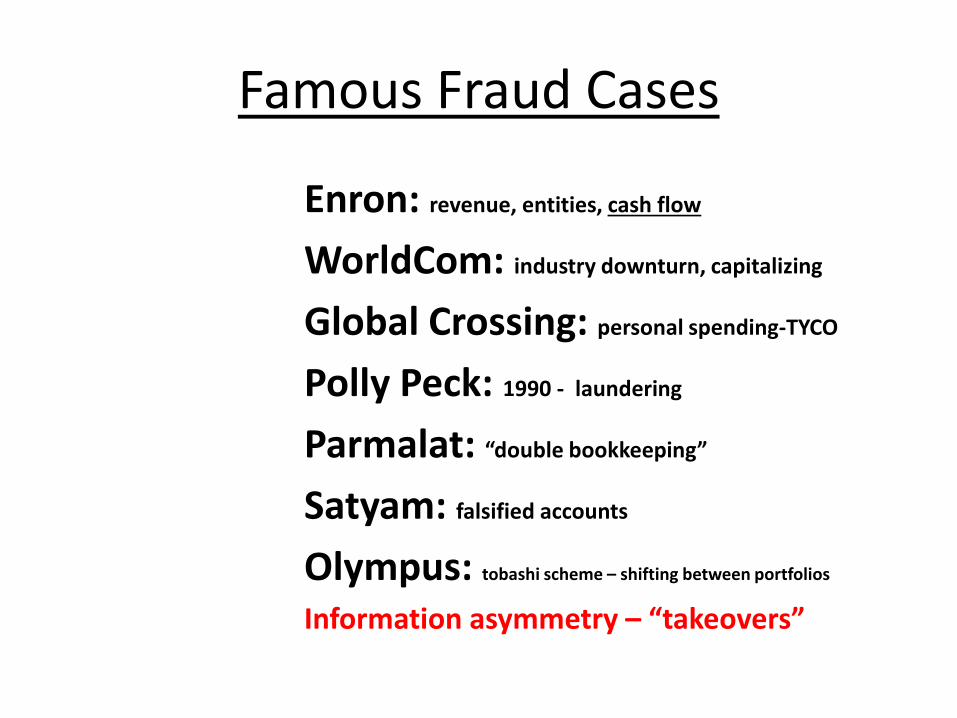

Famous Fraud Cases

Enron: revenue, entities, cash flow

WorldCom: industry downturn, capitalizing

Global Crossing: personal spending-TYCO

Polly Peck: 1990 - laundering

Parmalat: “double bookkeeping”

Satyam: falsified accounts

Olympus: tobashi scheme – shifting between portfolios

Information asymmetry – “takeovers”

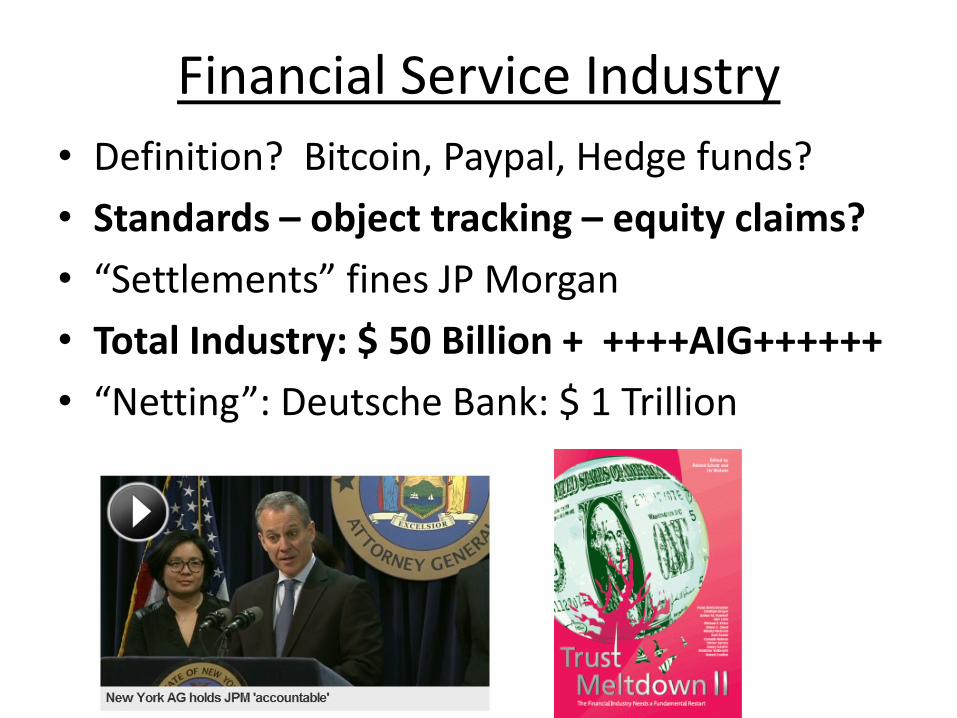

Financial Service Industry

• Definition? Bitcoin, Paypal, Hedge funds?

• Standards – object tracking – equity claims?

• “Settlements” fines JP Morgan

• Total Industry: $ 50 Billion + ++++AIG++++++

• “Netting”: Deutsche Bank: $ 1 Trillion

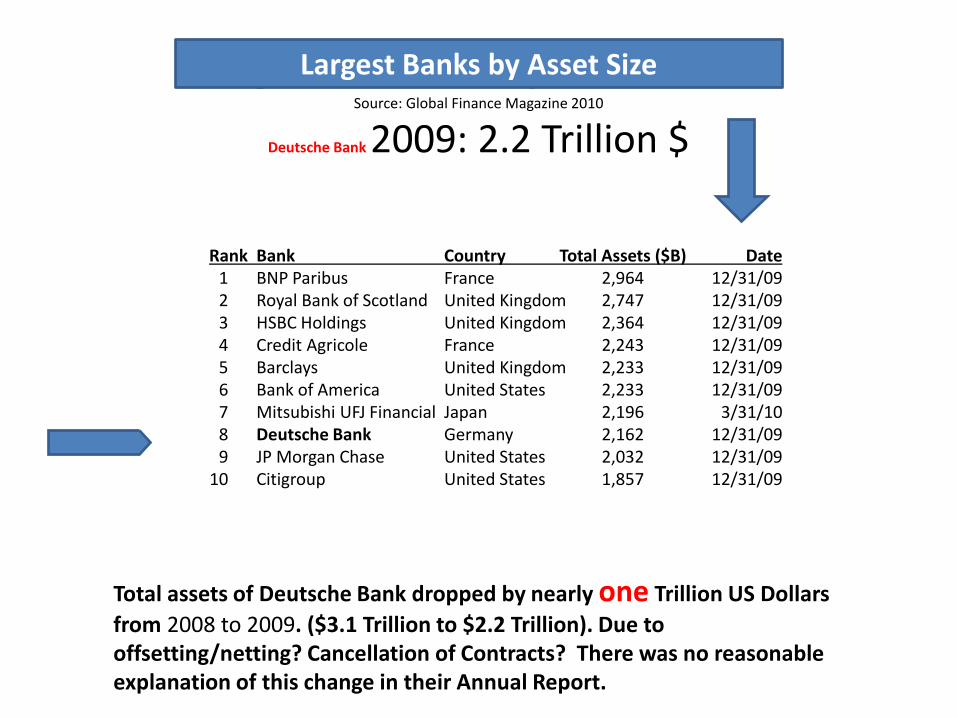

Largest Banks by Asset Size Source: Global Finance Magazine 2010

Deutsche Bank 2009: 2.2 Trillion $

Largest Banks by Asset Size

Rank Bank Country Total Assets ($B) Date 1 BNP Paribus France 2,964 12/31/09 2 Royal Bank of Scotland United Kingdom 2,747 12/31/09 3 HSBC Holdings United Kingdom 2,364 12/31/09 4 Credit Agricole France 2,243 12/31/09 5 Barclays United Kingdom 2,233 12/31/09 6 Bank of America United States 2,233 12/31/09 7 Mitsubishi UFJ Financial Japan 2,196 3/31/10 8 Deutsche Bank Germany 2,162 12/31/09 9 JP Morgan Chase United States 2,032 12/31/09 10 Citigroup United States 1,857 12/31/09

Total assets of Deutsche Bank dropped by nearly one Trillion US Dollars

from 2008 to 2009. ($3.1 Trillion to $2.2 Trillion). Due to offsetting/netting? Cancellation of Contracts? There was no reasonable explanation of this change in their Annual Report.

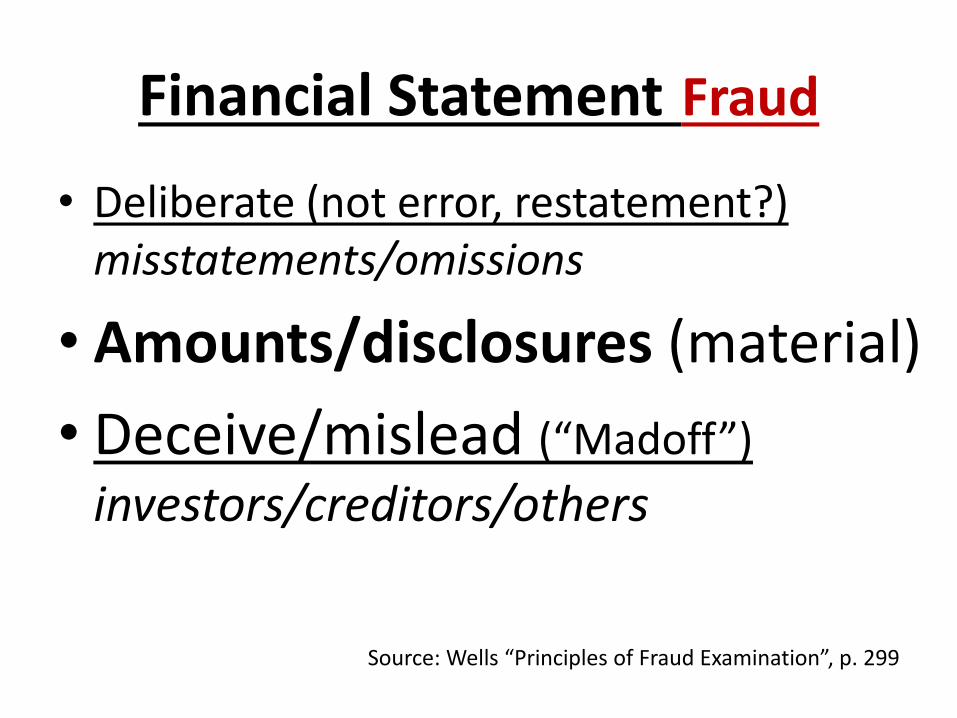

Financial Statement Fraud

• Deliberate (not error, restatement?) misstatements/omissions

• Amounts/disclosures (material)

• Deceive/mislead (“Madoff”)

investors/creditors/others

Source: Wells “Principles of Fraud Examination”, p. 299

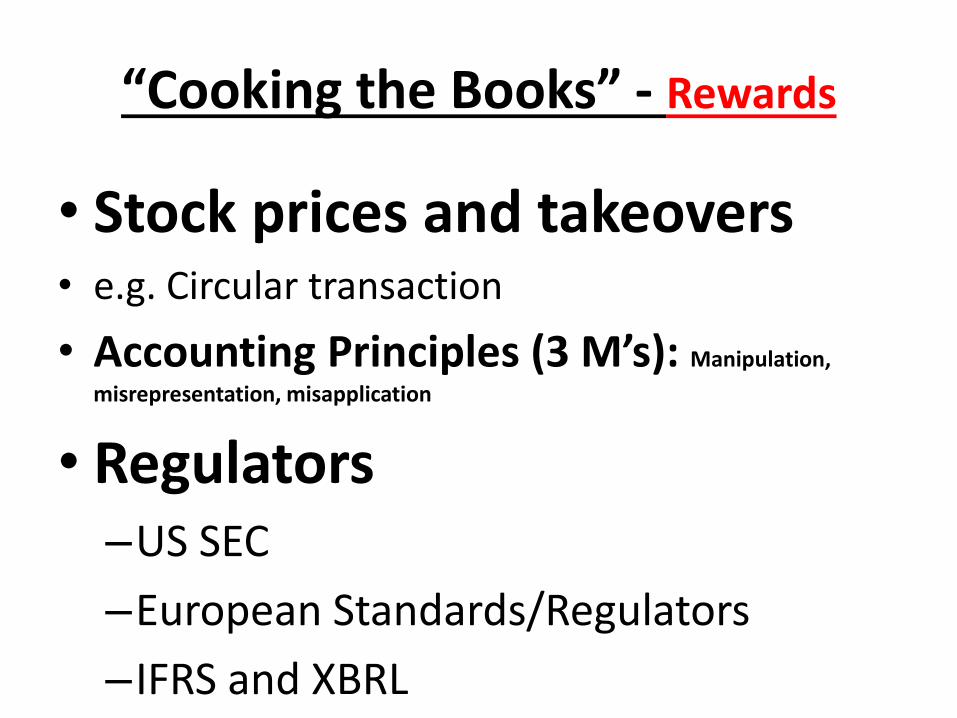

“Cooking the Books” - Rewards

• Stock prices and takeovers • e.g. Circular transaction

• Accounting Principles (3 M’s): Manipulation,

misrepresentation, misapplication

• Regulators –US SEC

–European Standards/Regulators

–IFRS and XBRL

Global Capital Markets www.world-exchanges.org

• Equities: 50.000 listings, $55 tn market cap

• Bonds: $ 30 tn turnover, total Debt $100 tn 55/45 nations

•Other Derivatives

• Currencies – $5 tn daily

• SME’s – Real Estate (store of value boats?)

Market Capitalization by Region $60 Trillion (24 hours) NYSE -Euronext

10 largest companies: $3 tn

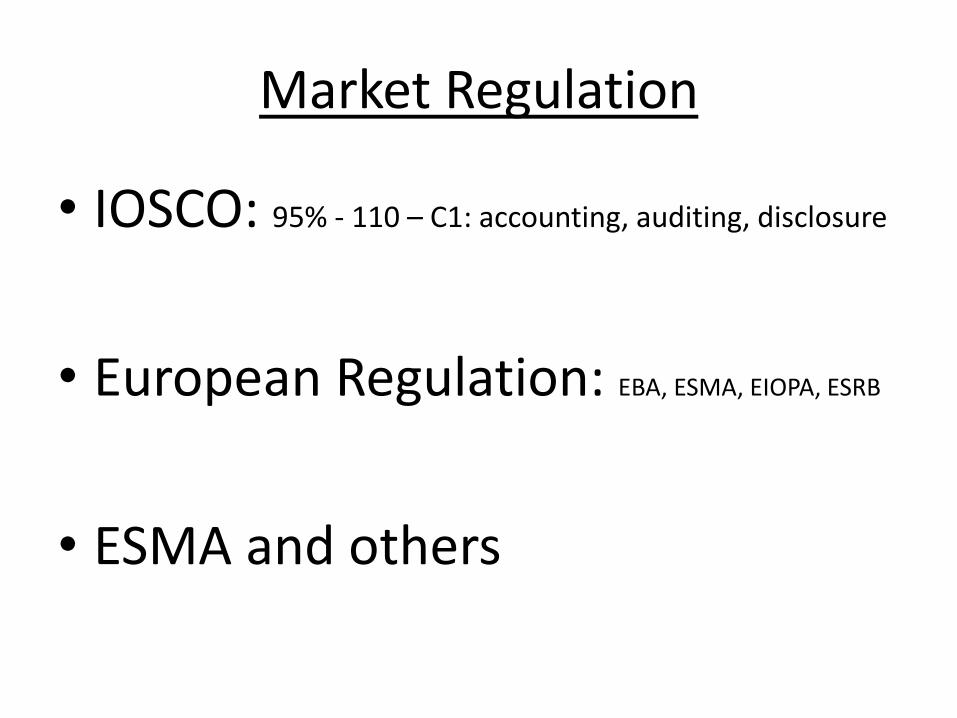

Market Regulation

• IOSCO: 95% - 110 – C1: accounting, auditing, disclosure

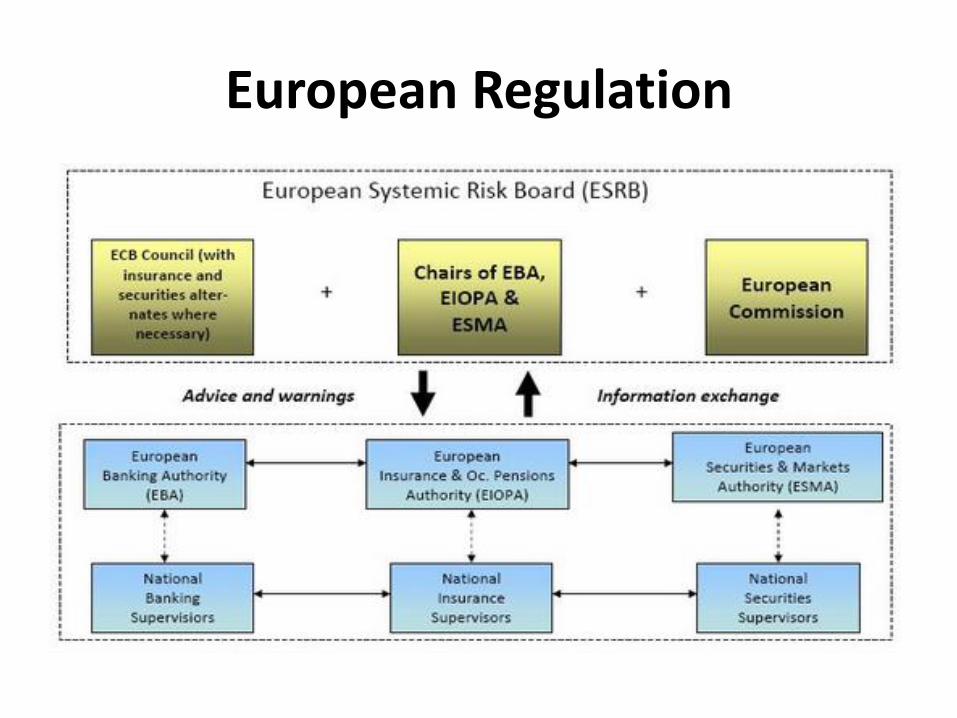

• European Regulation: EBA, ESMA, EIOPA, ESRB

• ESMA and others

http://www.esma.europa.eu/

European Regulation

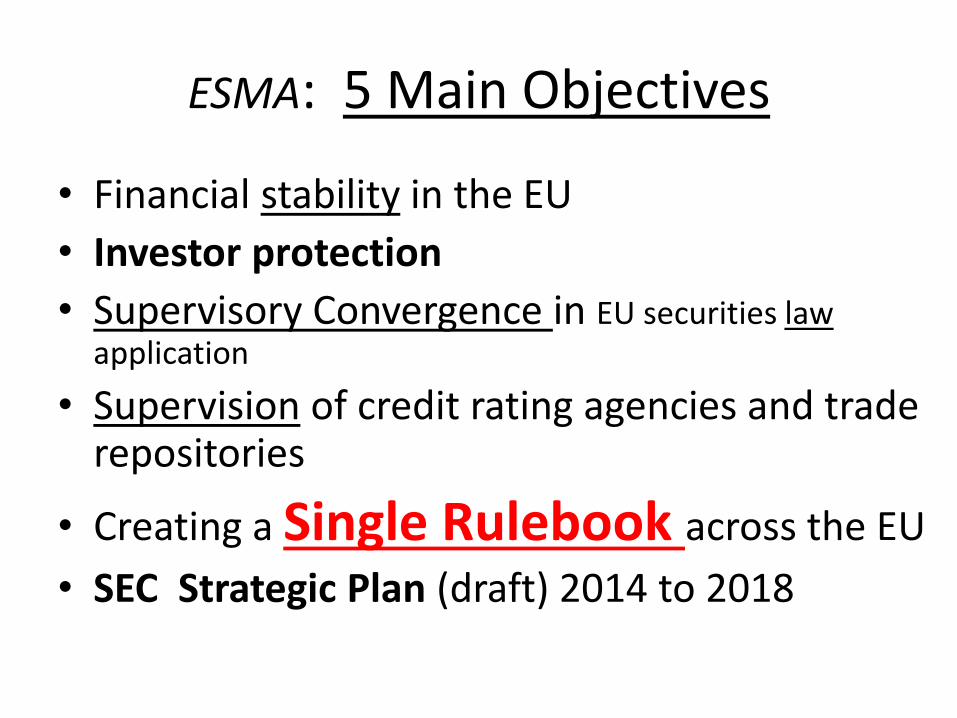

ESMA: 5 Main Objectives

• Financial stability in the EU

• Investor protection

• Supervisory Convergence in EU securities law application

• Supervision of credit rating agencies and trade repositories

• Creating a Single Rulebook across the EU

• SEC Strategic Plan (draft) 2014 to 2018

IFRS: International Financial Reporting Standards

IFRS: International Financial Reporting Standards

• Coverage

• EFRAG

• Endorsement process

• Reconciliations

• International equivalency agreements

• German example – BaFin provides list

– Registry and Enforcement

IFRS Foundation Structure

• History

• Organization

• Trustees

• Board

• Interpretations

• Advisory Committees

20

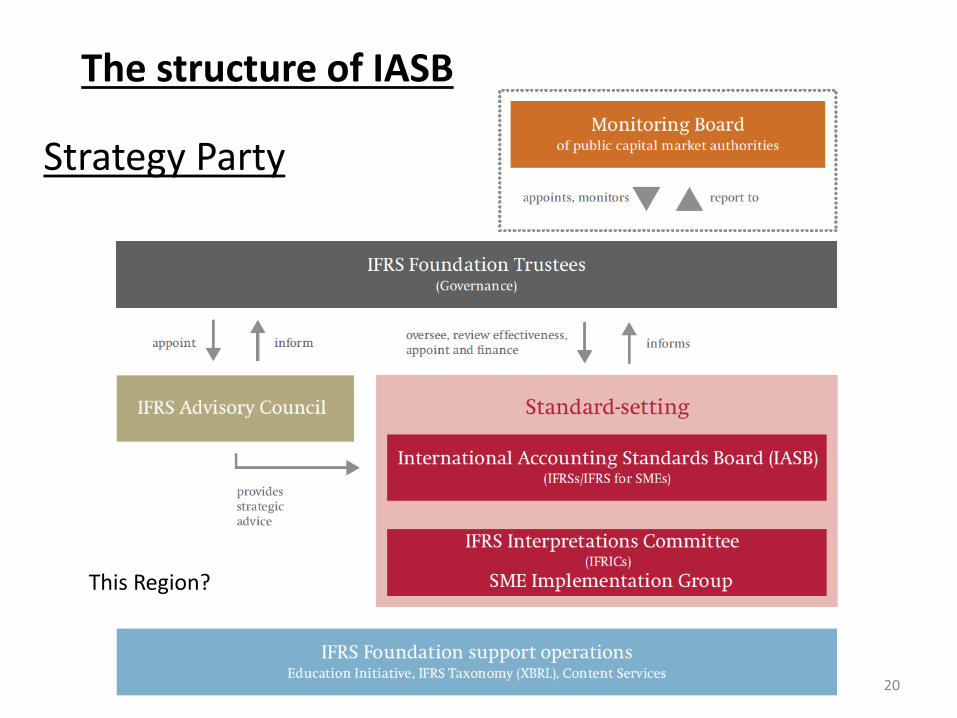

The structure of IASB

Strategy Party

This Region?

Standards: IFRSs and IFRSs for SMEs

• Framework

• Management Commentary

• Typical Standard

• Number of Standards – e.g. Revenue Recognition

– Stock option, Time, Valuation

– Debt or Obligation?

• IPSAS

• Model Financial Statements

Detecting Financial Statement Fraud

• Horizontal & vertical analysis (3-5 years)

• Comparison within industry

• Careful examination of corporate culture/controls/source documents

• Confirmations/Valuation

• Examination of estimates

Keeping up with IFRS

Please refer to Handout: Information and Websites

• www.ifrs.org

• www.fasb.org

• www.iasplus.com

• IFRS Certifications

• Discussion Groups (Linkedin)

• Webcasts

• eIFRSs

http://issuu.com/accountantme/docs/accountant_july-aug_2013_low_res_fo/58 pages 58-61

Accountant Middle East: 2013 July/August Issue

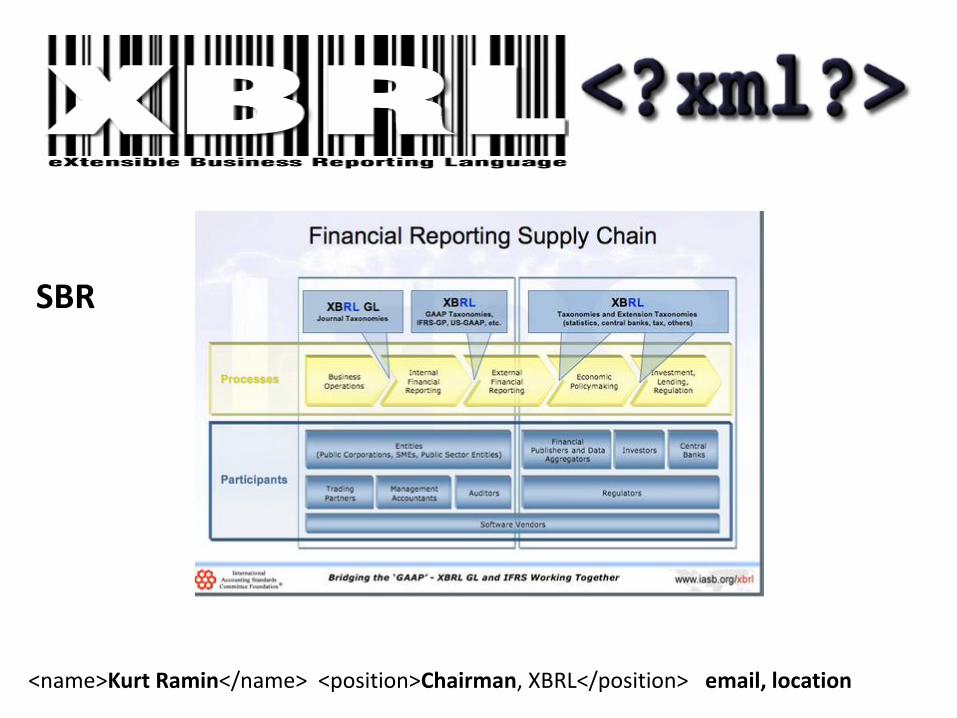

<name>Kurt Ramin</name> <position>Chairman, XBRL</position> email, location

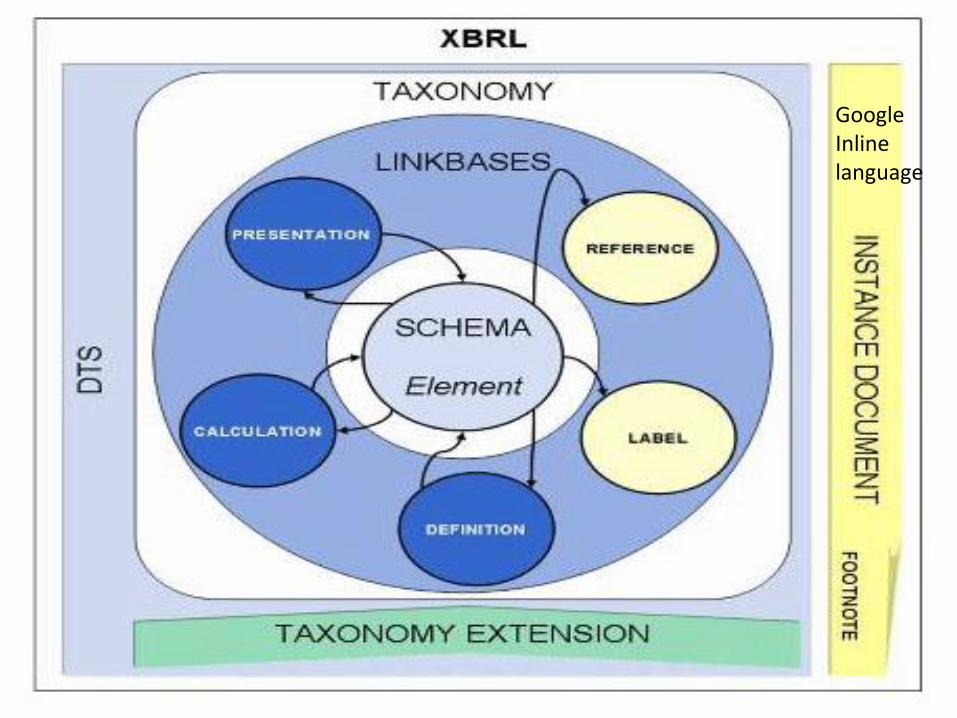

SBR

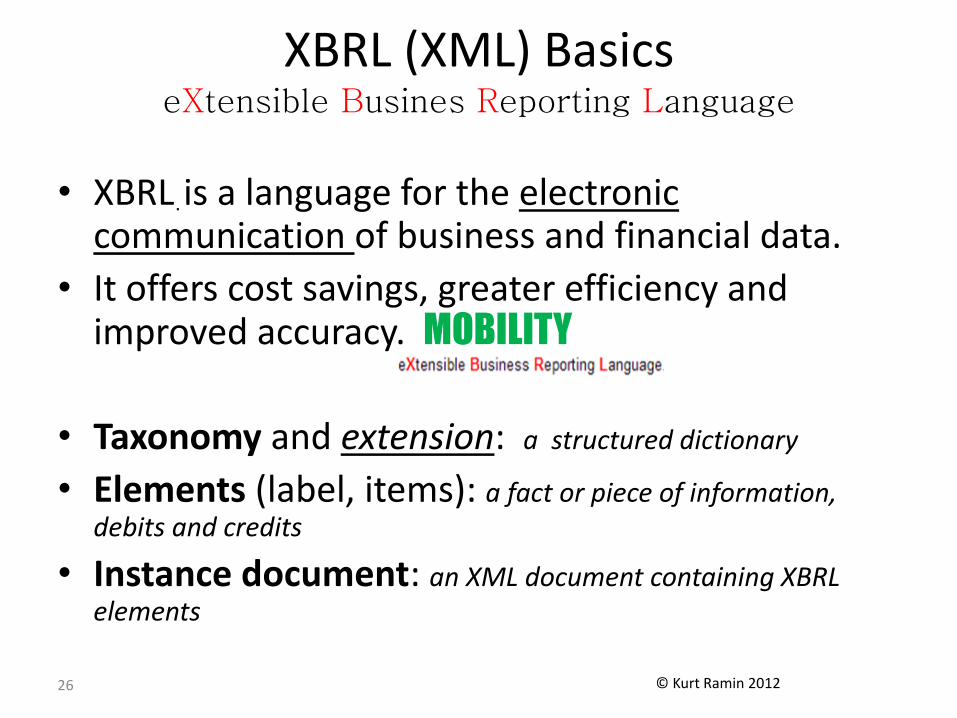

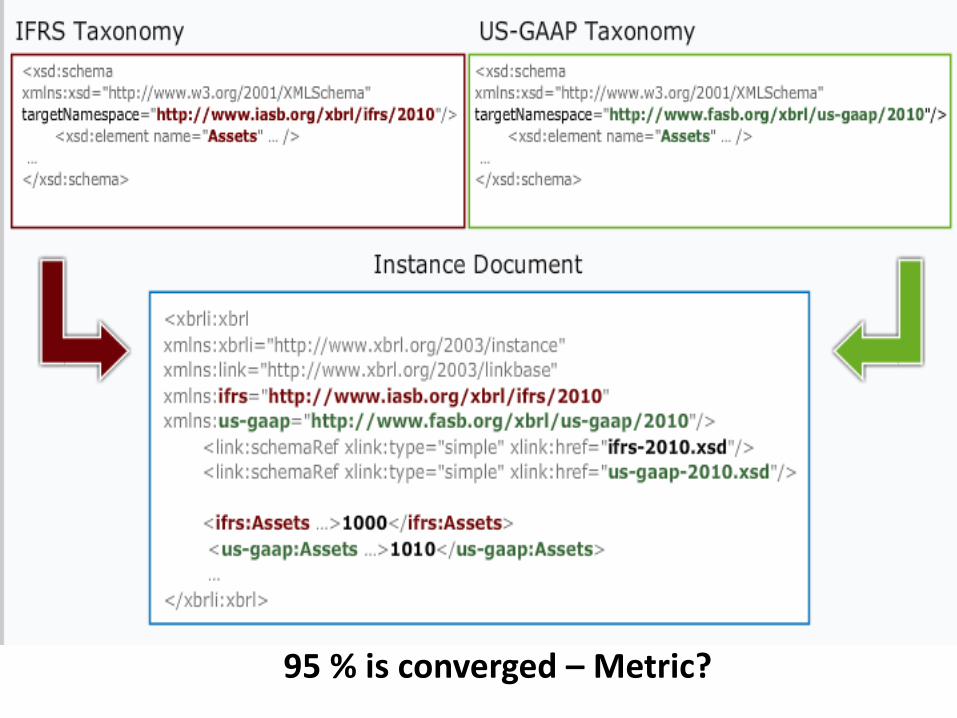

XBRL (XML) Basics eXtensible Busines Reporting Language

26

. • XBRL is a language for the electronic communication of business and financial data.

• It offers cost savings, greater efficiency and improved accuracy. MOBILITY

• Taxonomy and extension: a structured dictionary

• Elements (label, items): a fact or piece of information, debits and credits

• Instance document: an XML document containing XBRL elements

© Kurt Ramin 2012

Google Inline language

28

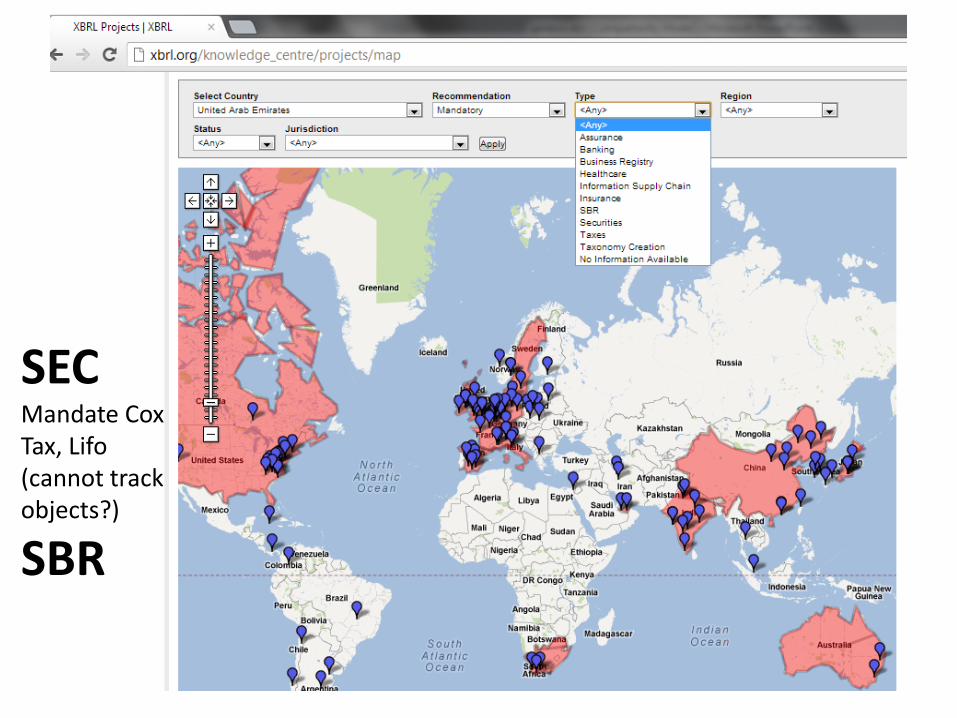

SEC Mandate Cox Tax, Lifo (cannot track objects?)

SBR

Other technologies

• Translation

• Legal (legaltech)

• ERP

• Big data

• Social Networks

• Travel and Expense

• Payroll

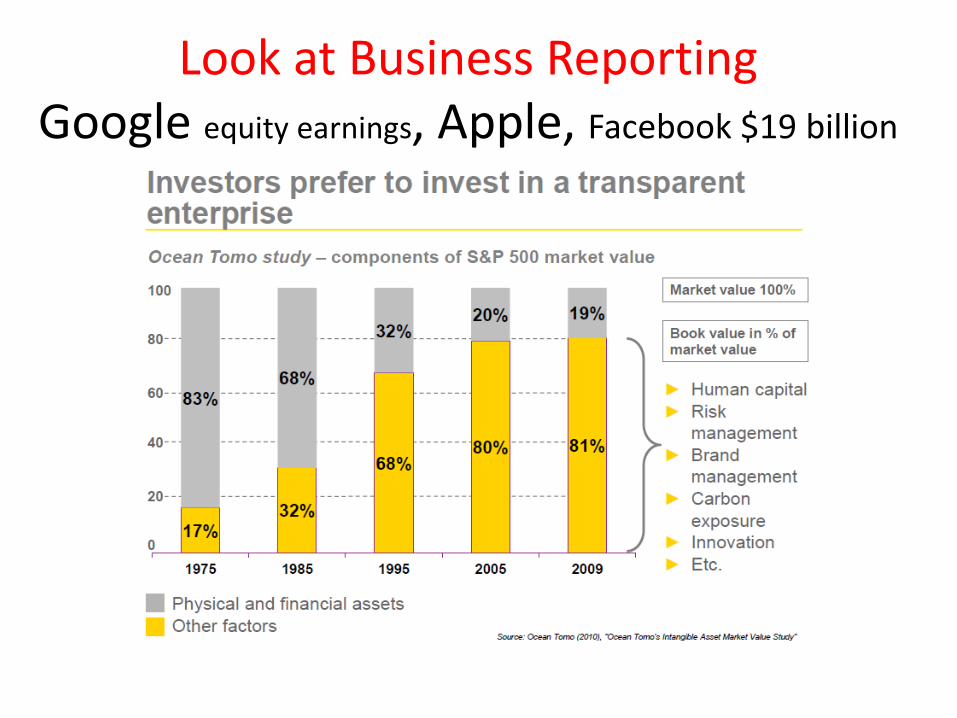

Look at Business Reporting Google equity earnings, Apple, Facebook $19 billion

95 % is converged – Metric?

Financial Reporting and other Data

• Sustainability Reports

• Integrated Reports

• Valuation Reports

• Other Economic Segments (Public Sector/Tax)

• Global Financial Flows (electronic)

• Supply Chain

• Object Tracking

http://www.financialexecutives.org/KenticoCMS/FEI_Blogs/Financial-Reporting-Blog/February-2014/The-State-of-Sustainability-Reporting-Among-SEC-Re.aspx#axzz2sbTLJMFx

• Organizational Impact of Integrated Reporting is Significant p. 19

• Ramin noted, “Without technology and tracking objects, nothing is going to happen – especially on the forecasting. Human capital can’t be valued, so you need to be able to at least forecast what it’s going to cost you for the next couple of years.

• Without the data you’re not going to be able to report. For some industries, the data collection is already in the supply chain, so that’s good. I think certain industries are well equipped to do more and move ahead. In the supply chain, in some companies where it’s pretty much automated, they don’t look at value; they look at the tracking of people and products. It’s already there. The smart companies have one system worldwide. Without technology we can’t do much to improve sustainability and business reporting.”[15]

• 15 http://www.theiirc.org/wp-content/uploads/2013/08/103_Kurt-Ramin-and-Stephen-Lew.pdf • INTERVIEWEES (AMONG OTHERS): • Dr. Robert Eccles, Professor of Management Practice, Harvard Business School

• Mark Miller, Director of External Reporting, Medtronic, Inc.

• Linda Qian, CSR Communications Manager, Corporate Responsibility Office, Intel

• Francis Quinn, Director of CSR Technologies, WebFilings

• Kurt Ramin, MBA, CFE, CPA, CEBS, Consultant, Member of FEI’s Committee on Governance, Risk and Compliance, Former Partner at PwC and Former Director of the IFRS Foundation at the IASB, London.

•

Just Released

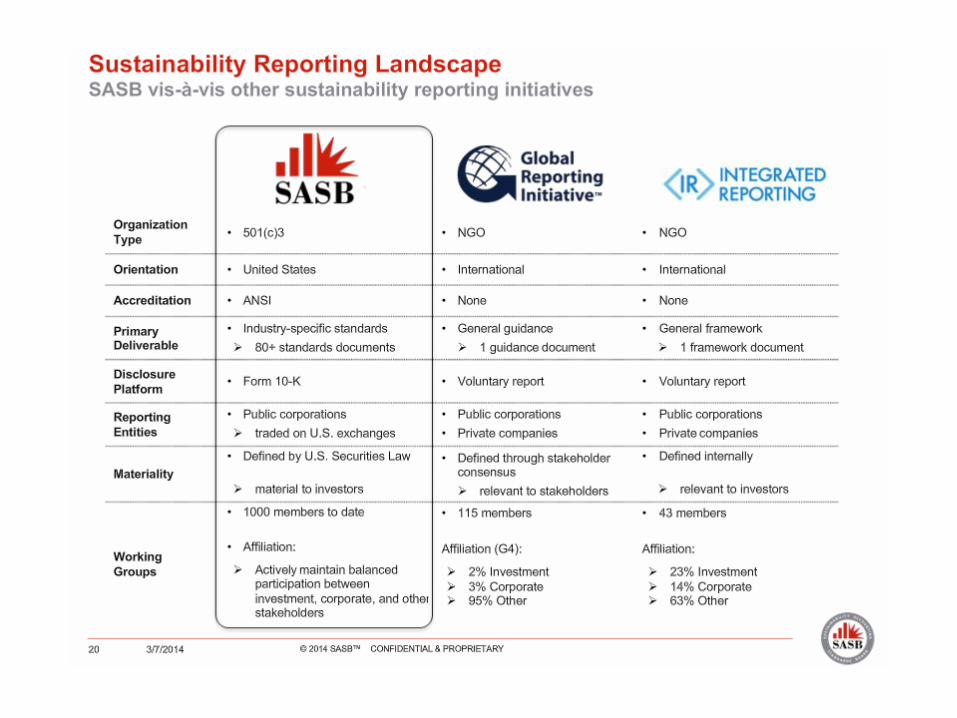

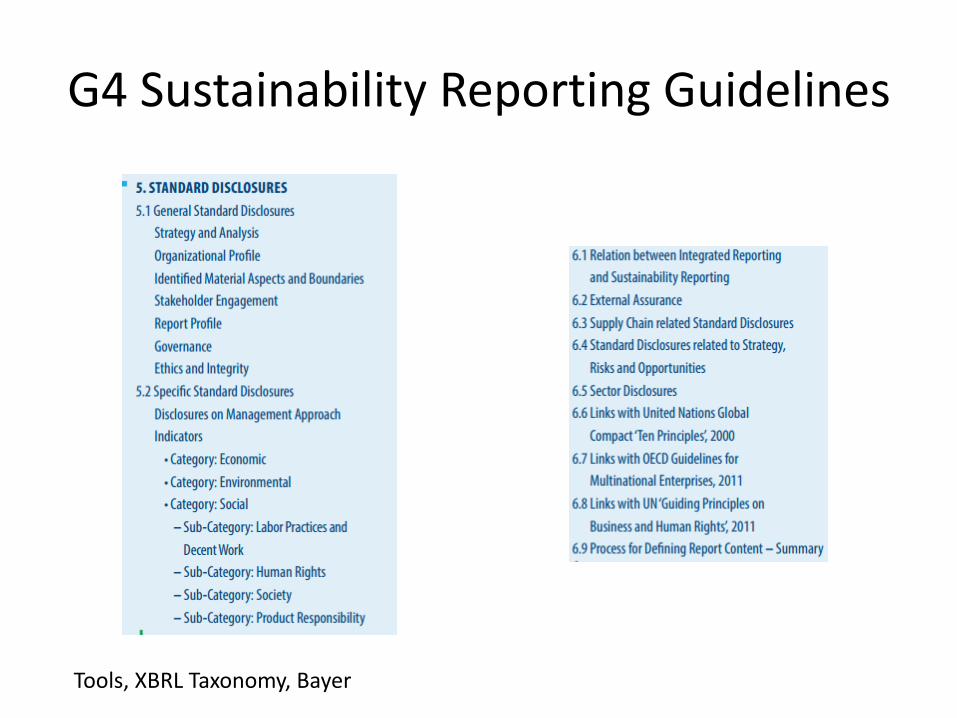

Global Reporting Initiative (GRI)

G4 Sustainability Reporting Guidelines

Tools, XBRL Taxonomy, Bayer

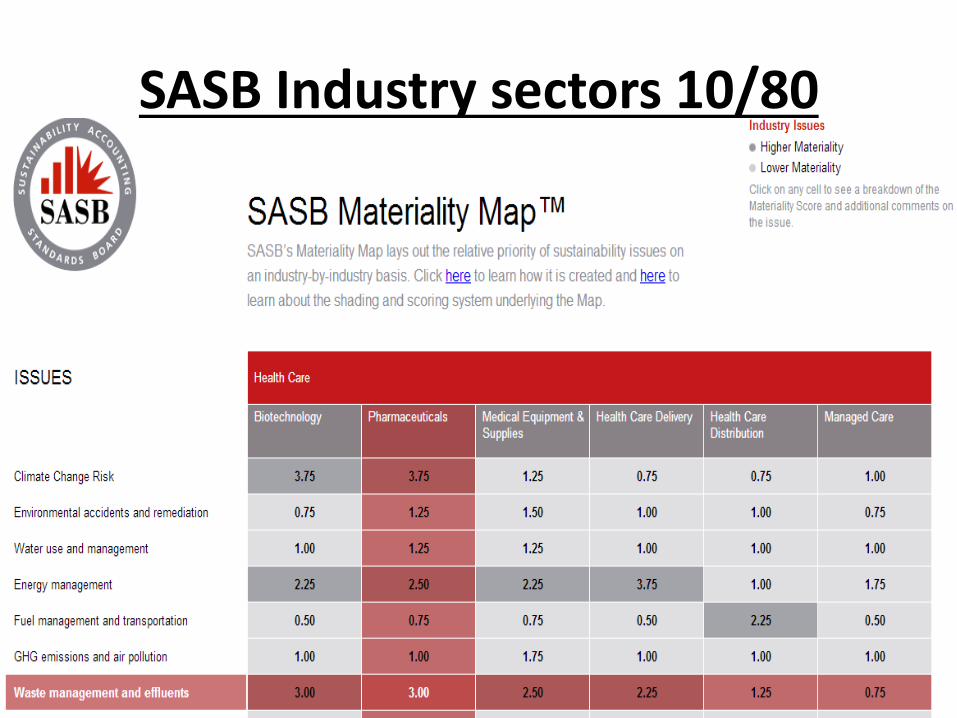

Sustainability Accounting Standards Board (SASB)

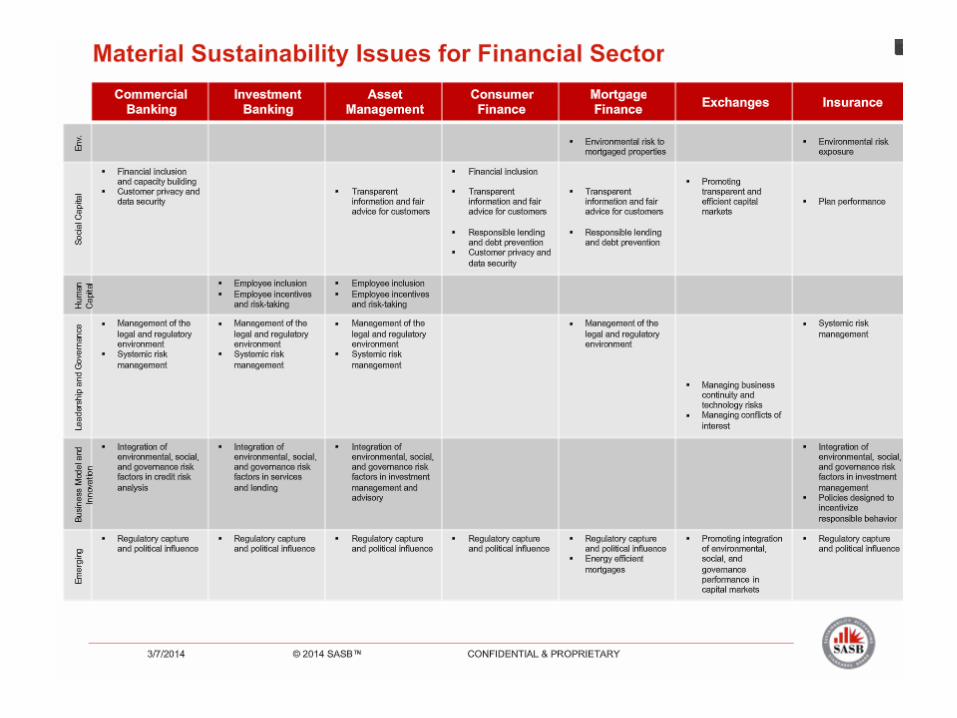

SASB Industry sectors 10/80

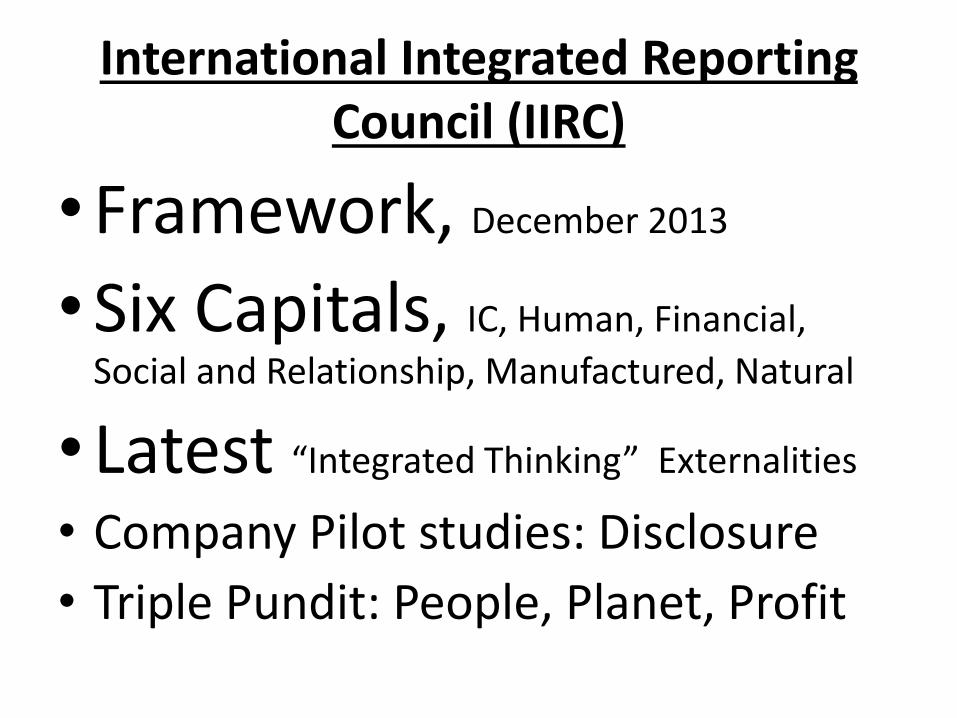

International Integrated Reporting Council (IIRC)

International Integrated Reporting Council (IIRC)

•Framework, December 2013

•Six Capitals, IC, Human, Financial,

Social and Relationship, Manufactured, Natural

• Latest “Integrated Thinking” Externalities

• Company Pilot studies: Disclosure

• Triple Pundit: People, Planet, Profit

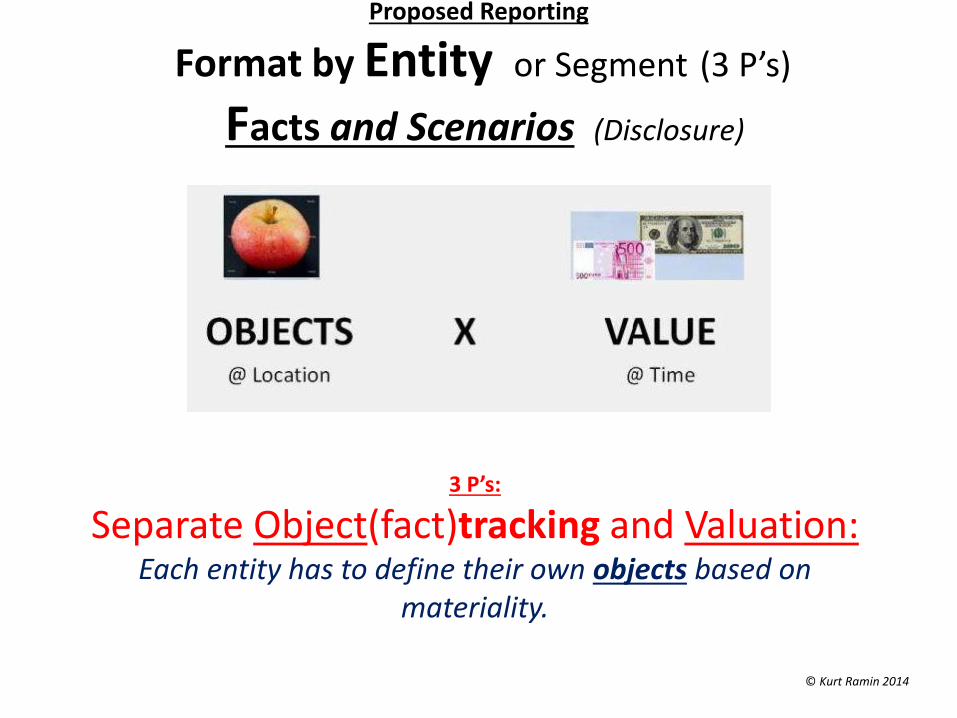

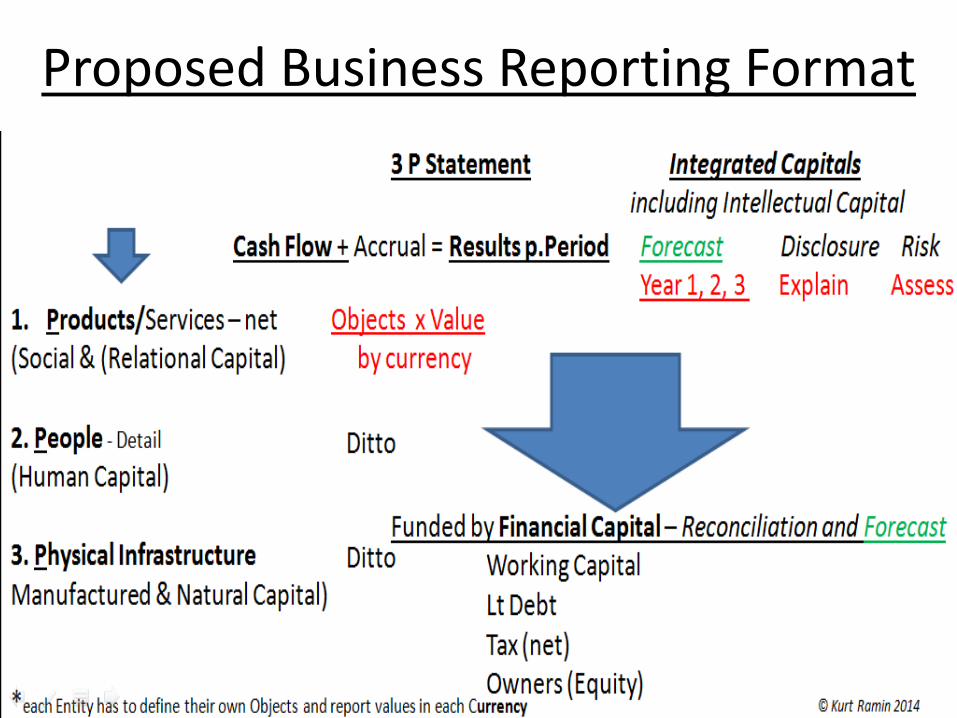

Proposed Reporting

Format by Entity or Segment (3 P’s)

Facts and Scenarios (Disclosure)

3 P’s:

Separate Object(fact)tracking and Valuation: Each entity has to define their own objects based on

materiality.

© Kurt Ramin 2014

Proposed Business Reporting Format

How many ‘Capitals’ do we need?

“Keeping up with IFRS”

January 2014

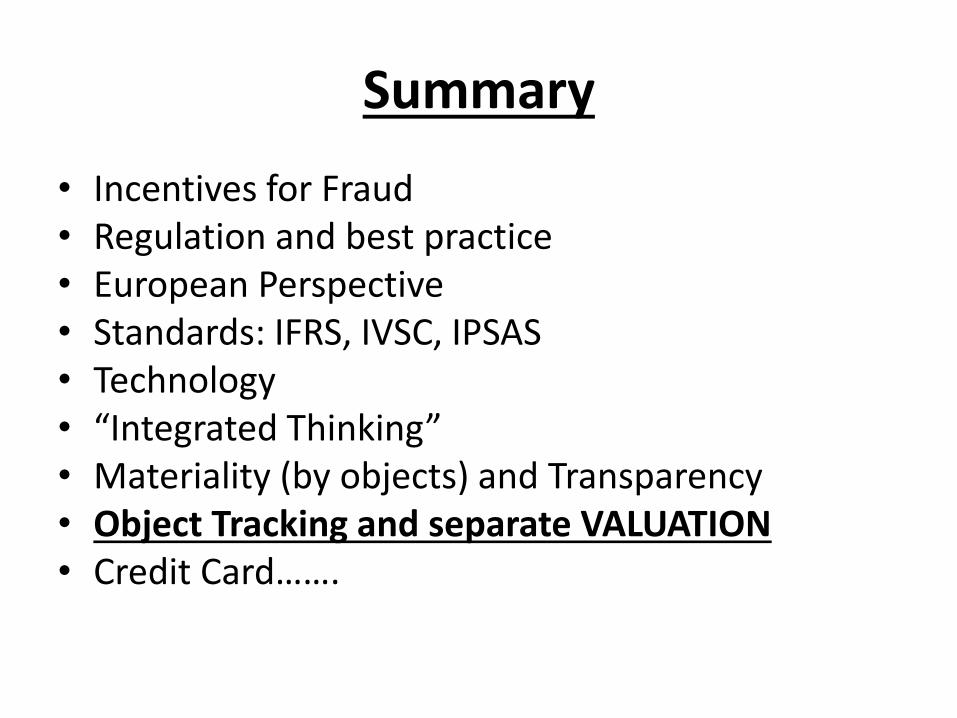

Summary

• Incentives for Fraud • Regulation and best practice • European Perspective • Standards: IFRS, IVSC, IPSAS • Technology • “Integrated Thinking” • Materiality (by objects) and Transparency • Object Tracking and separate VALUATION • Credit Card…….

![WELCOME [ec.europa.eu]ec.europa.eu/regional_policy/sources/conferences/etc2016/3_project... · 15.15 – 15.20 Welcome – col. Wim Van Zele . 15.20 – 15.40 Presentation MIRG EU](https://img.pdfslide.us/doc/110x75/602196beb088e57d5a22563b/welcome-ec-ec-1515-a-1520-welcome-a-col-wim-van-zele-1520-a-1540.jpg)