Embed Size (px)

Citation preview

129

5 : Capital Budgeting Practices in Selected Indian Companies

5.1 Introduction

5.2 Data Analysis and Findings

5.3 Conclusion

130

Chapter 5 : Capital Budgeting Practices in Selected Indian Companies

5.1 Introduction:

This chapter examines the trend in capital budgeting practices of twenty eight companies

operating in different industry. The search for a reliable method of project appraisal dates

back to decades. The issue not only continues to be a matter of concern for academicians and

managers but is also becoming equally significant for shareholders and other investors of the

organization. There are number of tools available to determine the extent of profitability of a

project but some of these methods are not taking care of the continuous changes taking place

in business environment where shareholders value (wealth) maximizing is becoming a very

important decision-making criterion. Further, these methods sometimes fail to address the

basic problems of investment appraisal while some of these methods require complex

decision making processes or it may require too much application of computers. Thus, the

choice of appropriate capital expenditure appraisal method is becoming a difficult task for

project managers, which requires critical analysis of various tools. Finance experts’ propose

various options to address the basic problems of investment management.

My literature review reveals that the traditional discounted cash flow techniques (DCF) are

most commonly used technique (Pay back Period) by many firms. Many organizations are

greatly using modern discounted techniques at the same time some scholars are proposing to

use techniques such as Monte Carlo simulations, real options etc. but all these techniques

have been criticized for its own limitations also. For instance, traditional methods lack

strategic vision. DCF techniques do not help in appraising all types of projects at all the

stages of project implementation which leads to selecting many projects on intuitions,

experience and rule of thumb. Further, techniques like simulation analysis, Monte Carlo, real

options etc are complex and requires too much computational work and information. The

techniques like EVA (economic value added) are criticized for using accounting information

and not cash flow information and also for not addressing to the shareholder value

maximization criterion.

131

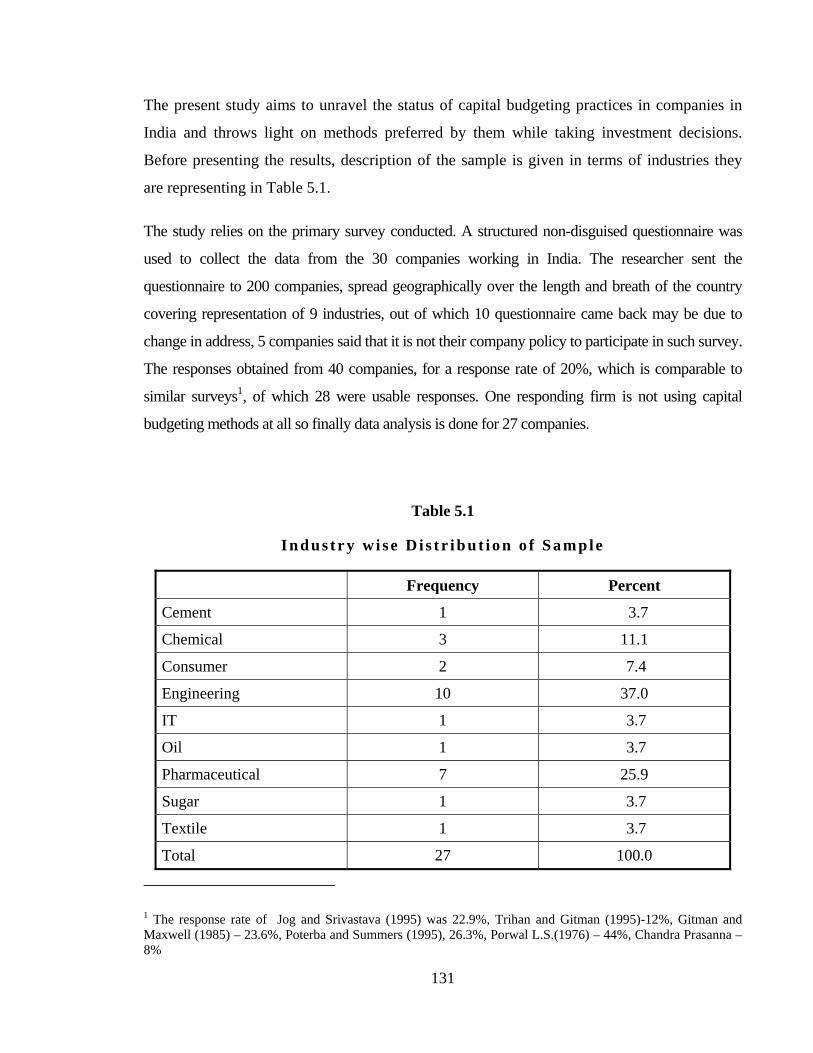

The present study aims to unravel the status of capital budgeting practices in companies in

India and throws light on methods preferred by them while taking investment decisions.

Before presenting the results, description of the sample is given in terms of industries they

are representing in Table 5.1.

The study relies on the primary survey conducted. A structured non-disguised questionnaire was

used to collect the data from the 30 companies working in India. The researcher sent the

questionnaire to 200 companies, spread geographically over the length and breath of the country

covering representation of 9 industries, out of which 10 questionnaire came back may be due to

change in address, 5 companies said that it is not their company policy to participate in such survey.

The responses obtained from 40 companies, for a response rate of 20%, which is comparable to

similar surveys1, of which 28 were usable responses. One responding firm is not using capital

budgeting methods at all so finally data analysis is done for 27 companies.

Table 5.1

I n d u s t r y wi s e D i s t r i b u t i o n o f S a m p l e

Frequency Percent

Cement 1 3.7

Chemical 3 11.1

Consumer 2 7.4

Engineering 10 37.0

IT 1 3.7

Oil 1 3.7

Pharmaceutical 7 25.9

Sugar 1 3.7

Textile 1 3.7

Total 27 100.0

1 The response rate of Jog and Srivastava (1995) was 22.9%, Trihan and Gitman (1995)-12%, Gitman and Maxwell (1985) – 23.6%, Poterba and Summers (1995), 26.3%, Porwal L.S.(1976) – 44%, Chandra Prasanna – 8%

132

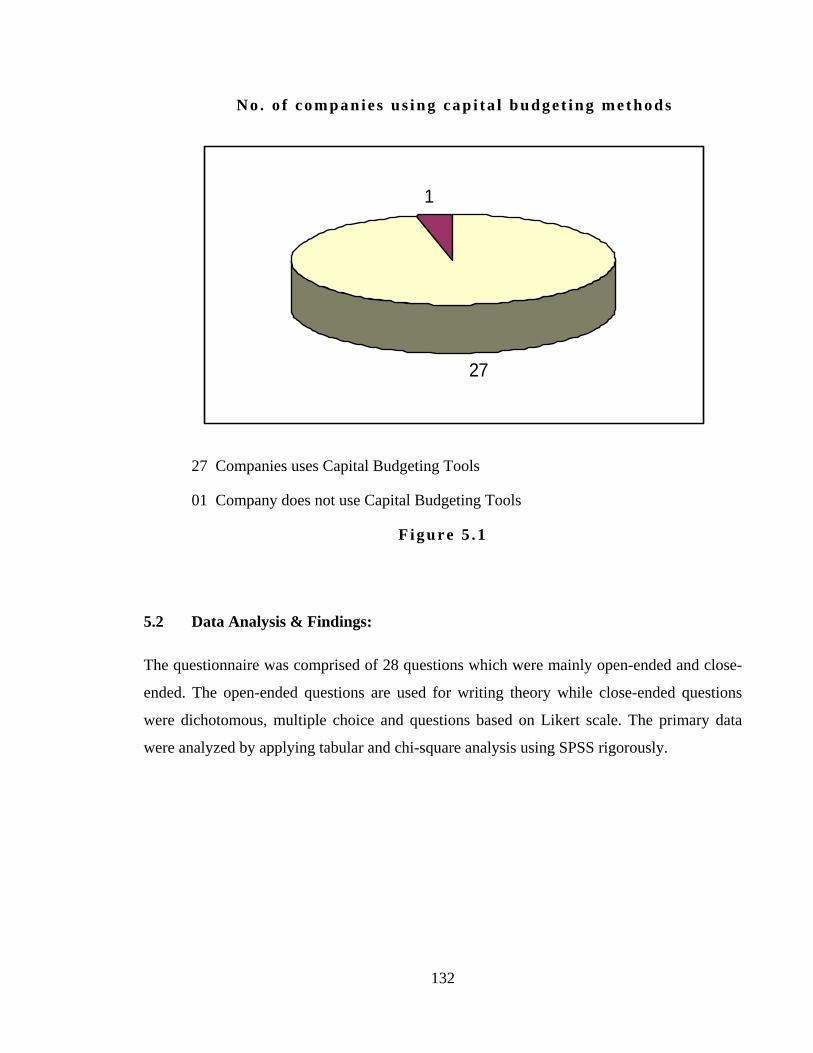

N o . o f c o m p a n i e s u s i n g c a p i t a l b u d g e t i n g m e t h o d s

27

1

27 Companies uses Capital Budgeting Tools

01 Company does not use Capital Budgeting Tools

Figure 5 .1

5.2 Data Analysis & Findings::

The questionnaire was comprised of 28 questions which were mainly open-ended and close-

ended. The open-ended questions are used for writing theory while close-ended questions

were dichotomous, multiple choice and questions based on Likert scale. The primary data

were analyzed by applying tabular and chi-square analysis using SPSS rigorously.

133

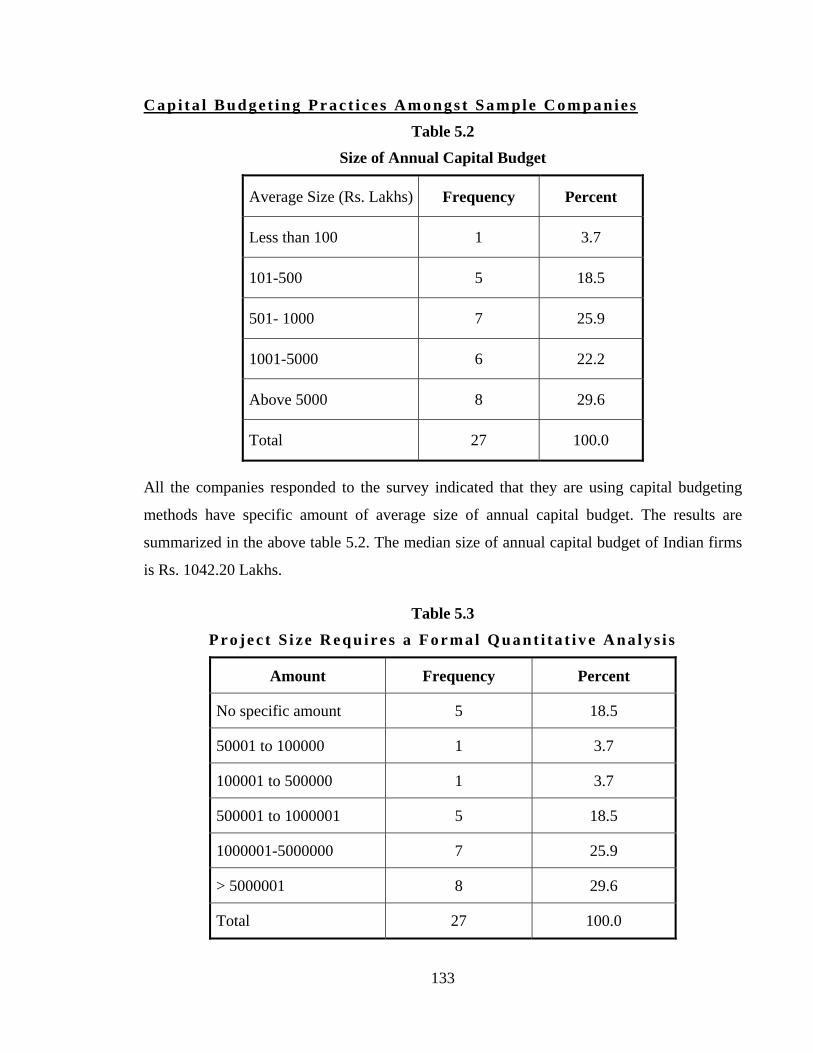

C a p i t a l B u d g e t i n g P r a c t i c e s A m o n g s t S a m pl e C o m p a n i e s

Table 5.2

Size of Annual Capital Budget

Average Size (Rs. Lakhs) Frequency Percent

Less than 100 1 3.7

101-500 5 18.5

501- 1000 7 25.9

1001-5000 6 22.2

Above 5000 8 29.6

Total 27 100.0

All the companies responded to the survey indicated that they are using capital budgeting

methods have specific amount of average size of annual capital budget. The results are

summarized in the above table 5.2. The median size of annual capital budget of Indian firms

is Rs. 1042.20 Lakhs.

Table 5.3

P r o j e c t S i ze R e q u i r e s a F o r m al Quant i ta t i ve Ana lys i s

Amount Frequency Percent

No specific amount 5 18.5

50001 to 100000 1 3.7

100001 to 500000 1 3.7

500001 to 1000001 5 18.5

1000001-5000000 7 25.9

> 5000001 8 29.6

Total 27 100.0

134

The researcher also wanted to know the project size that requires a formal quantitative

analysis in the Indian firms. As one can observe in Table 5.3, all project size requires a

formal quantitative analysis. However, as per the opinion of some respondents, the use of

capital budgeting techniques for evaluating capital expenditure projects depends on the

nature and size of the particular projects. Some respondents said that for replacement

decision or process improvement they may use only PBP. The median size of the project

requiring formal quantitative analysis is Rs. 2200000.5

The table 5.4 given below summarizes the results for time frame for planning capital

expenditures of the organization i.e. how many years in advance usually the capital budgets

are prepared for achieving firm’s objectives.

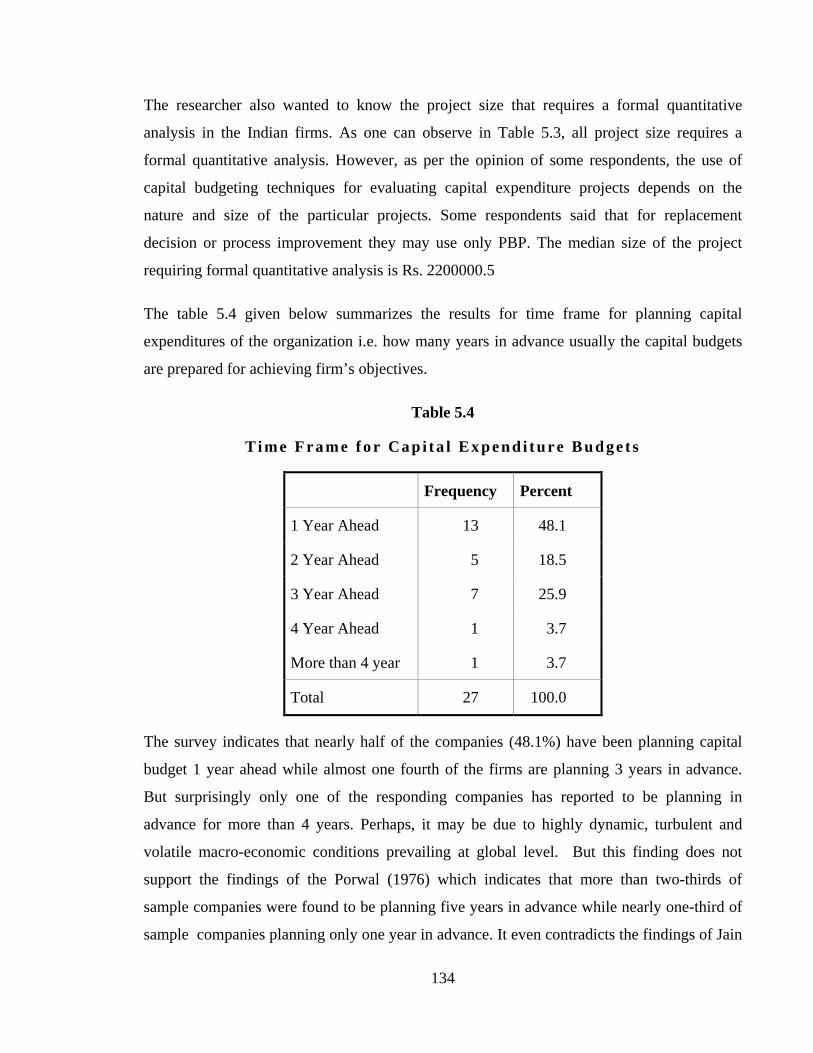

Table 5.4

T i m e F r a m e f o r Cap i t a l E x p e n d i t u r e B u d g e t s

Frequency Percent

1 Year Ahead 13 48.1

2 Year Ahead 5 18.5

3 Year Ahead 7 25.9

4 Year Ahead 1 3.7

More than 4 year 1 3.7

Total 27 100.0

The survey indicates that nearly half of the companies (48.1%) have been planning capital

budget 1 year ahead while almost one fourth of the firms are planning 3 years in advance.

But surprisingly only one of the responding companies has reported to be planning in

advance for more than 4 years. Perhaps, it may be due to highly dynamic, turbulent and

volatile macro-economic conditions prevailing at global level. But this finding does not

support the findings of the Porwal (1976) which indicates that more than two-thirds of

sample companies were found to be planning five years in advance while nearly one-third of

sample companies planning only one year in advance. It even contradicts the findings of Jain

135

P. K., Jain S. K. and Tarde S. M. (1995) which revealed that 45.3% firms have been

planning capital budget five years ahead.

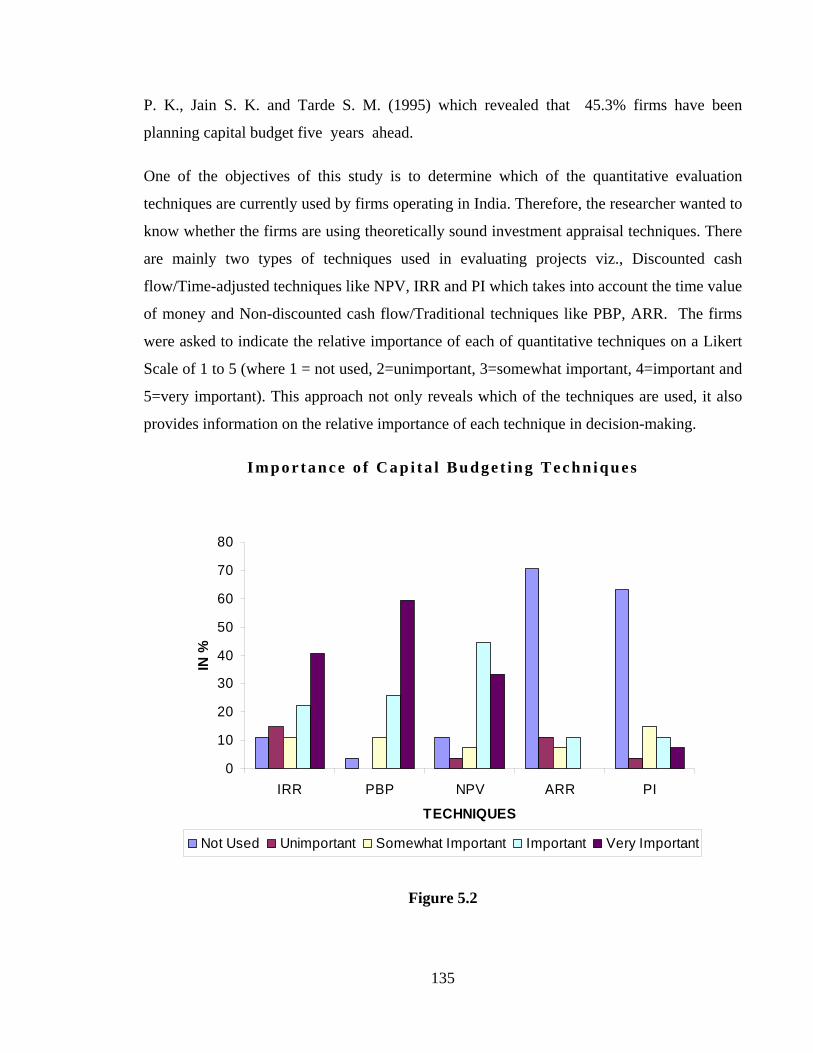

One of the objectives of this study is to determine which of the quantitative evaluation

techniques are currently used by firms operating in India. Therefore, the researcher wanted to

know whether the firms are using theoretically sound investment appraisal techniques. There

are mainly two types of techniques used in evaluating projects viz., Discounted cash

flow/Time-adjusted techniques like NPV, IRR and PI which takes into account the time value

of money and Non-discounted cash flow/Traditional techniques like PBP, ARR. The firms

were asked to indicate the relative importance of each of quantitative techniques on a Likert

Scale of 1 to 5 (where 1 = not used, 2=unimportant, 3=somewhat important, 4=important and

5=very important). This approach not only reveals which of the techniques are used, it also

provides information on the relative importance of each technique in decision-making.

I m p o r t a n c e o f C a p i t a l B u d g e t i n g T e c h n i q u e s

0

10

20

30

40

50

60

70

80

IRR PBP NPV ARR PI

TECHNIQUES

IN %

Not Used Unimportant Somewhat Important Important Very Important

Figure 5.2

136

The results are shown in figure 5.2 ranked according to perceived importance. The responding

firms ranked PBP (59.3%), IRR (40.7%) and NPV (33.3%) as the most important techniques

respectively. Among these techniques PBP is getting highest rating even though it ignores time

value of money and it also ignores cash flow beyond pay back period. It seems as it is easy to

calculate and understand, PBP is still a very popular technique. Although it is not directly

comparable, these results are consistent with the findings of Wong, Farragher and Leung (1987),

who found that payback, IRR and ARR were equally the most popular techniques used in

Singapore. However, IRR is ranked second and NPV is ranked third as the most important but

44.4% consider it as an important technique in this survey. Surprisingly, no respondent consider

ARR as most important technique, in fact 70.4% respondents are not using this technique at all.

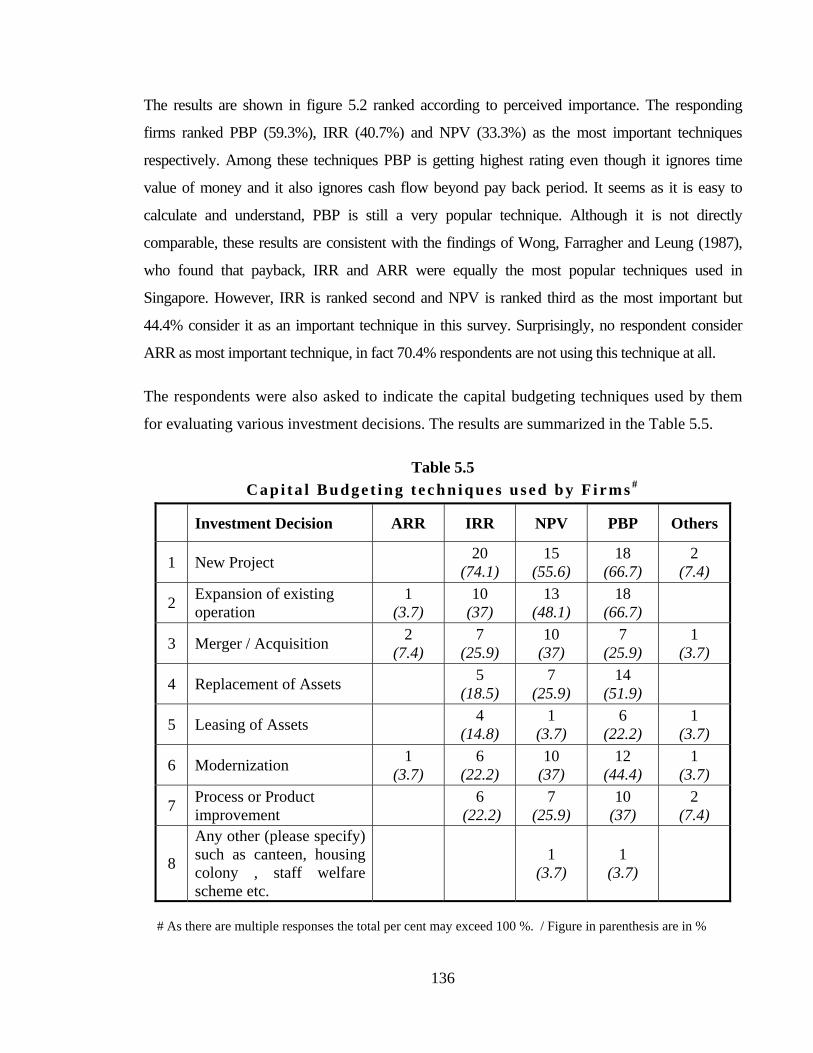

The respondents were also asked to indicate the capital budgeting techniques used by them

for evaluating various investment decisions. The results are summarized in the Table 5.5.

Table 5.5 C a p i t a l B u d g e t i n g t e c h n i q u e s u s e d b y F i r m s #

Investment Decision ARR IRR NPV PBP Others

1 New Project 20 (74.1)

15 (55.6)

18 (66.7)

2 (7.4)

2 Expansion of existing operation

1 (3.7)

10 (37)

13 (48.1)

18 (66.7)

3 Merger / Acquisition 2 (7.4)

7 (25.9)

10 (37)

7 (25.9)

1 (3.7)

4 Replacement of Assets 5 (18.5)

7 (25.9)

14 (51.9)

5 Leasing of Assets 4 (14.8)

1 (3.7)

6 (22.2)

1 (3.7)

6 Modernization 1 (3.7)

6 (22.2)

10 (37)

12 (44.4)

1 (3.7)

7 Process or Product improvement 6

(22.2) 7

(25.9) 10

(37) 2

(7.4)

8

Any other (please specify) such as canteen, housing colony , staff welfare scheme etc.

1 (3.7)

1 (3.7)

# As there are multiple responses the total per cent may exceed 100 %. / Figure in parenthesis are in %

137

One can observe that IRR (74.1%), PBP (66.7%) and NPV(55.6%) respectively are the most

preferred techniques for evaluating new capital budgeting projects. While for expansion,

replacement of assets, modernization and process or product improvement, PBP is preferred

over other techniques. The respondents prefer even NPV (37%) for modernization as well as

mergers and acquisition.

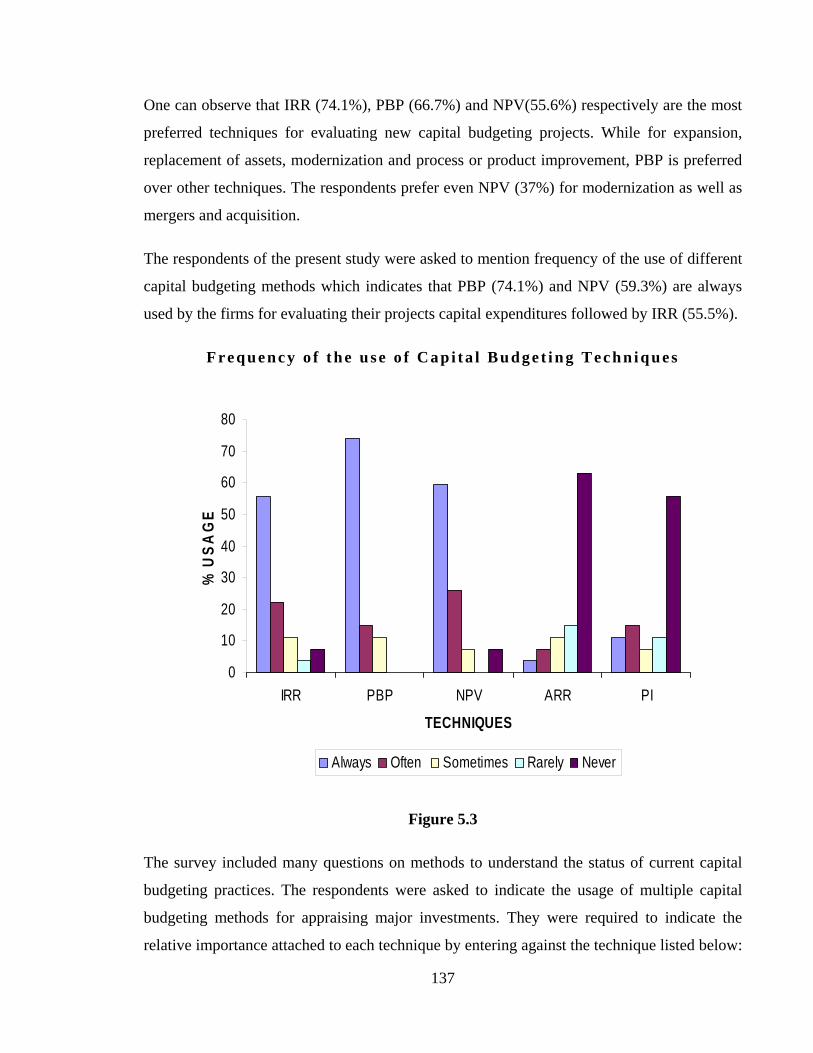

The respondents of the present study were asked to mention frequency of the use of different

capital budgeting methods which indicates that PBP (74.1%) and NPV (59.3%) are always

used by the firms for evaluating their projects capital expenditures followed by IRR (55.5%).

F r e q u e n c y o f t h e u s e o f C a p i t a l B u d g e t i n g T e c h n i q u e s

0

10

20

30

40

50

60

70

80

IRR PBP NPV ARR PI

TECHNIQUES

% U

SAG

E

Always Often Sometimes Rarely Never

Figure 5.3

The survey included many questions on methods to understand the status of current capital

budgeting practices. The respondents were asked to indicate the usage of multiple capital

budgeting methods for appraising major investments. They were required to indicate the

relative importance attached to each technique by entering against the technique listed below:

138

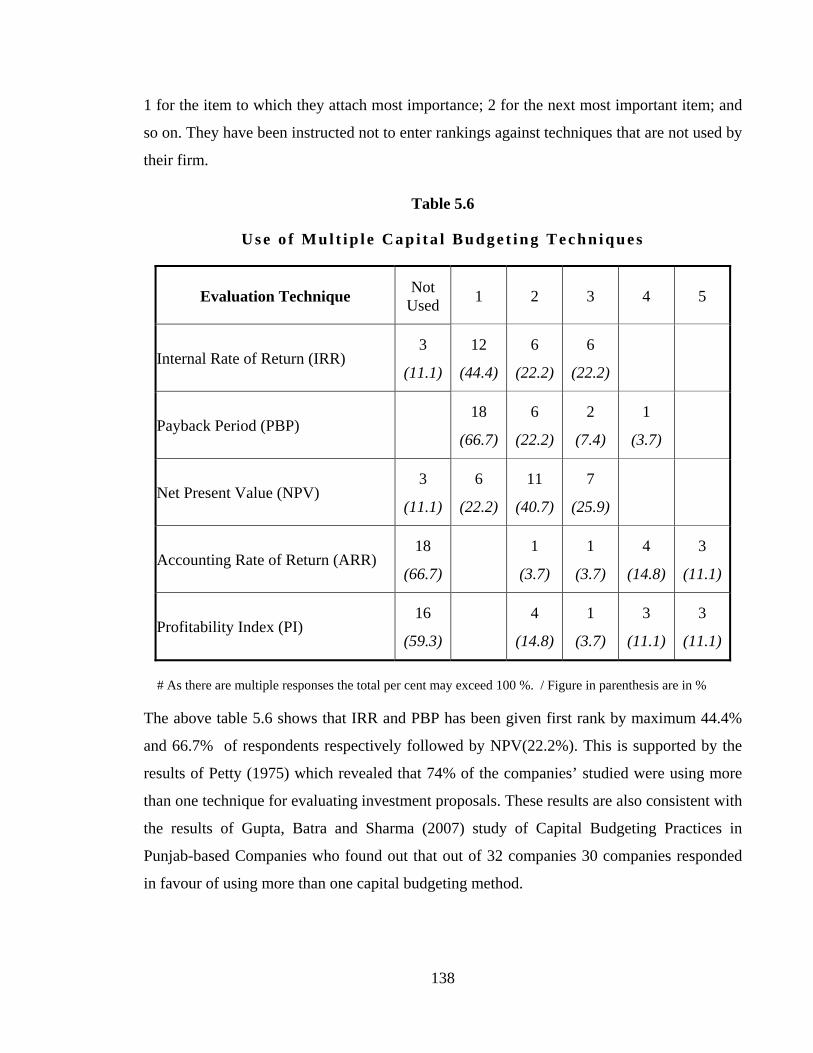

1 for the item to which they attach most importance; 2 for the next most important item; and

so on. They have been instructed not to enter rankings against techniques that are not used by

their firm.

Table 5.6

U s e o f Mul t i p l e Cap i t a l B u d g e t i n g T e c h n i q u e s

Evaluation Technique Not Used 1 2 3 4 5

Internal Rate of Return (IRR) 3

(11.1)

12

(44.4)

6

(22.2)

6

(22.2)

Payback Period (PBP) 18

(66.7)

6

(22.2)

2

(7.4)

1

(3.7)

Net Present Value (NPV) 3

(11.1)

6

(22.2)

11

(40.7)

7

(25.9)

Accounting Rate of Return (ARR) 18

(66.7)

1

(3.7)

1

(3.7)

4

(14.8)

3

(11.1)

Profitability Index (PI) 16

(59.3)

4

(14.8)

1

(3.7)

3

(11.1)

3

(11.1)

# As there are multiple responses the total per cent may exceed 100 %. / Figure in parenthesis are in %

The above table 5.6 shows that IRR and PBP has been given first rank by maximum 44.4%

and 66.7% of respondents respectively followed by NPV(22.2%). This is supported by the

results of Petty (1975) which revealed that 74% of the companies’ studied were using more

than one technique for evaluating investment proposals. These results are also consistent with

the results of Gupta, Batra and Sharma (2007) study of Capital Budgeting Practices in

Punjab-based Companies who found out that out of 32 companies 30 companies responded

in favour of using more than one capital budgeting method.

139

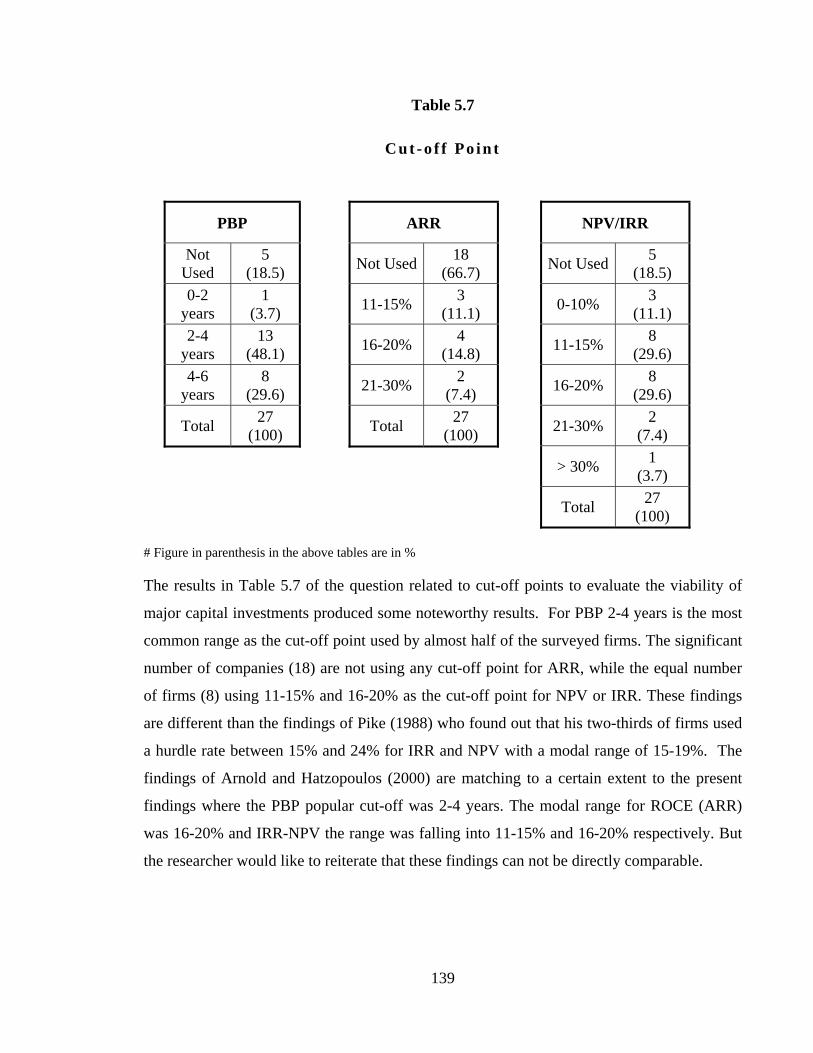

Table 5.7

C u t - o f f Po i n t

PBP

Not Used

5 (18.5)

0-2 years

1 (3.7)

2-4 years

13 (48.1)

4-6 years

8 (29.6)

Total 27 (100)

ARR

Not Used 18 (66.7)

11-15% 3 (11.1)

16-20% 4 (14.8)

21-30% 2 (7.4)

Total 27 (100)

NPV/IRR

Not Used 5 (18.5)

0-10% 3 (11.1)

11-15% 8 (29.6)

16-20% 8 (29.6)

21-30% 2 (7.4)

> 30% 1 (3.7)

Total 27 (100)

# Figure in parenthesis in the above tables are in %

The results in Table 5.7 of the question related to cut-off points to evaluate the viability of

major capital investments produced some noteworthy results. For PBP 2-4 years is the most

common range as the cut-off point used by almost half of the surveyed firms. The significant

number of companies (18) are not using any cut-off point for ARR, while the equal number

of firms (8) using 11-15% and 16-20% as the cut-off point for NPV or IRR. These findings

are different than the findings of Pike (1988) who found out that his two-thirds of firms used

a hurdle rate between 15% and 24% for IRR and NPV with a modal range of 15-19%. The

findings of Arnold and Hatzopoulos (2000) are matching to a certain extent to the present

findings where the PBP popular cut-off was 2-4 years. The modal range for ROCE (ARR)

was 16-20% and IRR-NPV the range was falling into 11-15% and 16-20% respectively. But

the researcher would like to reiterate that these findings can not be directly comparable.

140

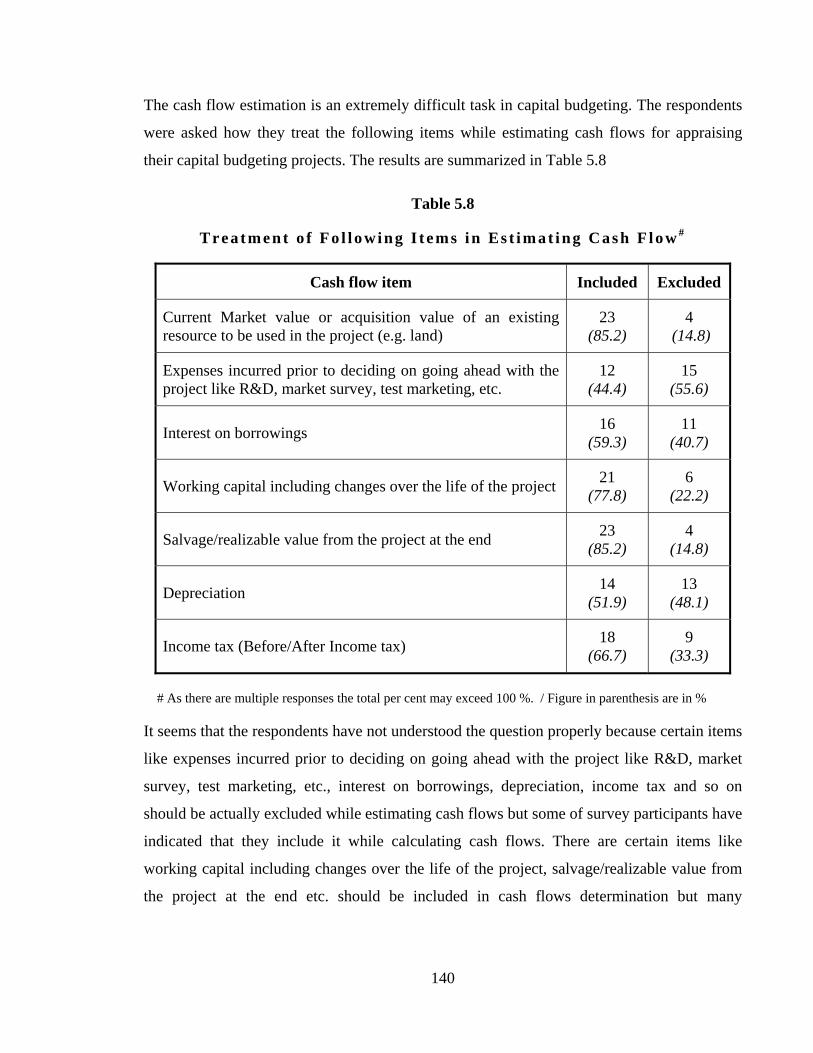

The cash flow estimation is an extremely difficult task in capital budgeting. The respondents

were asked how they treat the following items while estimating cash flows for appraising

their capital budgeting projects. The results are summarized in Table 5.8

Table 5.8

T r e a t m e n t o f F o l l o wi n g I t e m s i n Es t i m a t i ng C a s h F l o w #

Cash flow item Included Excluded

Current Market value or acquisition value of an existing resource to be used in the project (e.g. land)

23 (85.2)

4 (14.8)

Expenses incurred prior to deciding on going ahead with the project like R&D, market survey, test marketing, etc.

12 (44.4)

15 (55.6)

Interest on borrowings 16 (59.3)

11 (40.7)

Working capital including changes over the life of the project 21 (77.8)

6 (22.2)

Salvage/realizable value from the project at the end 23 (85.2)

4 (14.8)

Depreciation 14 (51.9)

13 (48.1)

Income tax (Before/After Income tax) 18 (66.7)

9 (33.3)

# As there are multiple responses the total per cent may exceed 100 %. / Figure in parenthesis are in %

It seems that the respondents have not understood the question properly because certain items

like expenses incurred prior to deciding on going ahead with the project like R&D, market

survey, test marketing, etc., interest on borrowings, depreciation, income tax and so on

should be actually excluded while estimating cash flows but some of survey participants have

indicated that they include it while calculating cash flows. There are certain items like

working capital including changes over the life of the project, salvage/realizable value from

the project at the end etc. should be included in cash flows determination but many

141

participants have shown they exclude it while estimating cash flows. Therefore, the

researcher feels that this question should be ignored for the analysis.

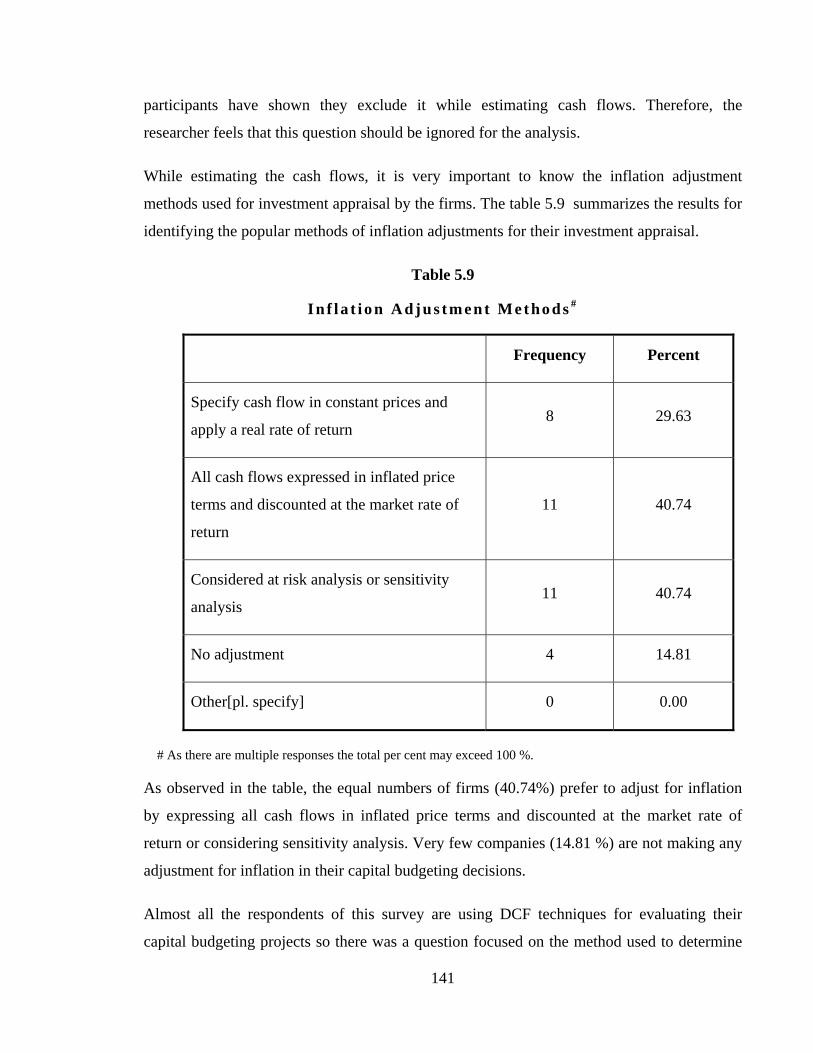

While estimating the cash flows, it is very important to know the inflation adjustment

methods used for investment appraisal by the firms. The table 5.9 summarizes the results for

identifying the popular methods of inflation adjustments for their investment appraisal.

Table 5.9

I n f l a t i o n A d j u s t m e n t M e t ho d s #

Frequency Percent

Specify cash flow in constant prices and

apply a real rate of return 8 29.63

All cash flows expressed in inflated price

terms and discounted at the market rate of

return

11 40.74

Considered at risk analysis or sensitivity

analysis 11 40.74

No adjustment 4 14.81

Other[pl. specify] 0 0.00

# As there are multiple responses the total per cent may exceed 100 %.

As observed in the table, the equal numbers of firms (40.74%) prefer to adjust for inflation

by expressing all cash flows in inflated price terms and discounted at the market rate of

return or considering sensitivity analysis. Very few companies (14.81 %) are not making any

adjustment for inflation in their capital budgeting decisions.

Almost all the respondents of this survey are using DCF techniques for evaluating their

capital budgeting projects so there was a question focused on the method used to determine

142

the minimum acceptable rate of return or the rate of discount to evaluate the proposed capital

expenditure project.

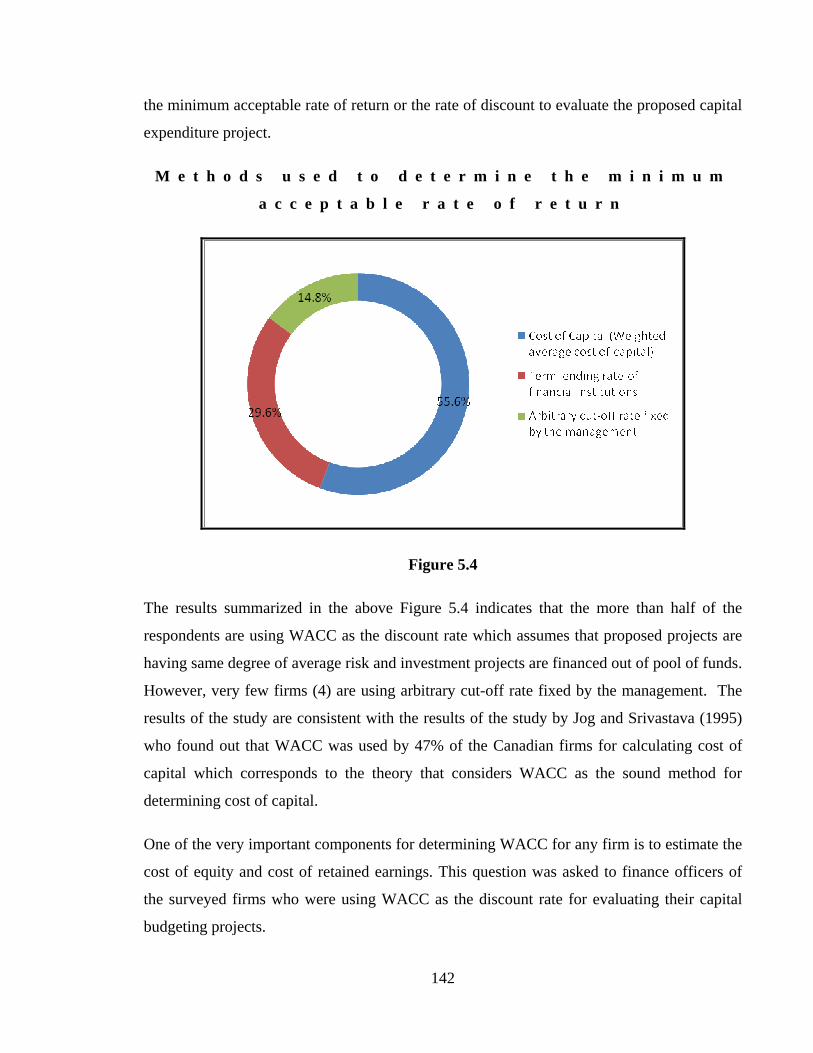

M e t h o d s u s e d t o d e t e r m i n e t h e m i n i m u m

a c c e p t a b l e r a t e o f r e t u r n

Figure 5.4

The results summarized in the above Figure 5.4 indicates that the more than half of the

respondents are using WACC as the discount rate which assumes that proposed projects are

having same degree of average risk and investment projects are financed out of pool of funds.

However, very few firms (4) are using arbitrary cut-off rate fixed by the management. The

results of the study are consistent with the results of the study by Jog and Srivastava (1995)

who found out that WACC was used by 47% of the Canadian firms for calculating cost of

capital which corresponds to the theory that considers WACC as the sound method for

determining cost of capital.

One of the very important components for determining WACC for any firm is to estimate the

cost of equity and cost of retained earnings. This question was asked to finance officers of

the surveyed firms who were using WACC as the discount rate for evaluating their capital

budgeting projects.

143

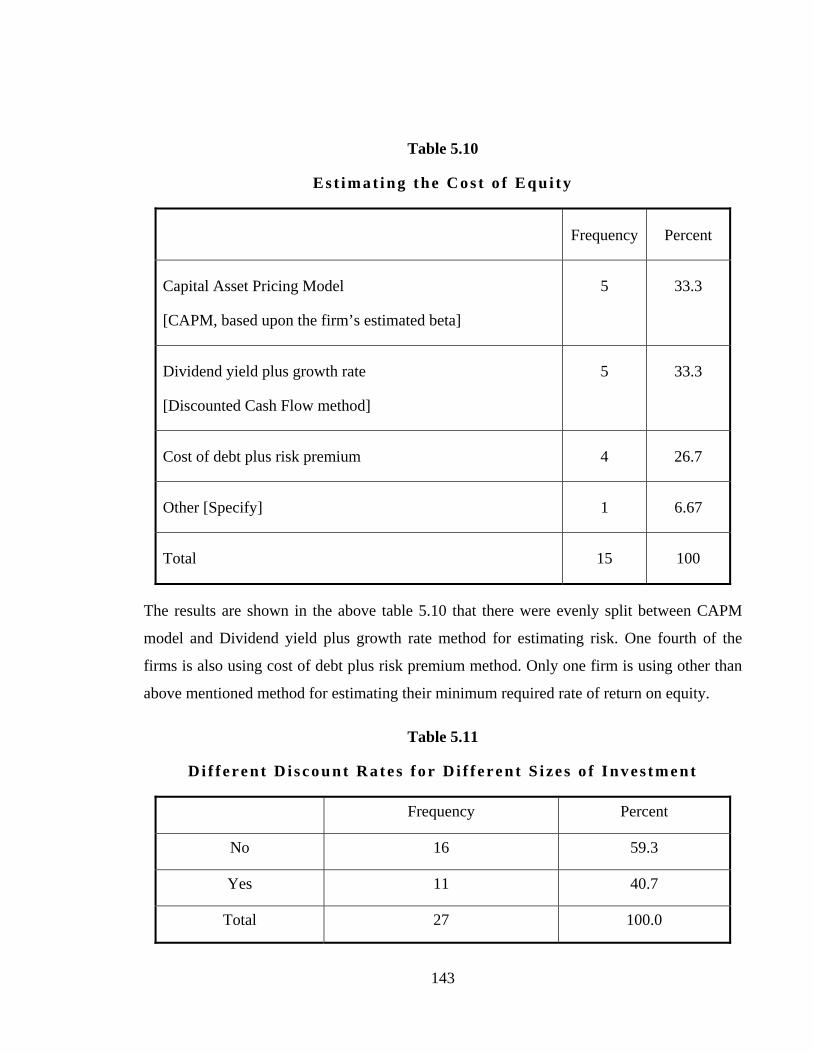

Table 5.10

E s t i m a t i n g t h e C o s t o f E q u i t y

Frequency Percent

Capital Asset Pricing Model

[CAPM, based upon the firm’s estimated beta]

5

33.3

Dividend yield plus growth rate

[Discounted Cash Flow method]

5

33.3

Cost of debt plus risk premium 4 26.7

Other [Specify] 1 6.67

Total 15 100

The results are shown in the above table 5.10 that there were evenly split between CAPM

model and Dividend yield plus growth rate method for estimating risk. One fourth of the

firms is also using cost of debt plus risk premium method. Only one firm is using other than

above mentioned method for estimating their minimum required rate of return on equity.

Table 5.11

D i f f e re n t D i s c o u n t R a t e s f o r D i f f ere n t S i ze s o f I n v e s t m e n t

Frequency Percent

No 16 59.3

Yes 11 40.7

Total 27 100.0

144

The responding firms were asked to mention whether they use different discount rates for

different sizes of investment or for different types of projects. The results in the Table 5.11

indicate that three-fifth of the firms are not using different discount rates while two-fifth of

the firms are using different discount rates.

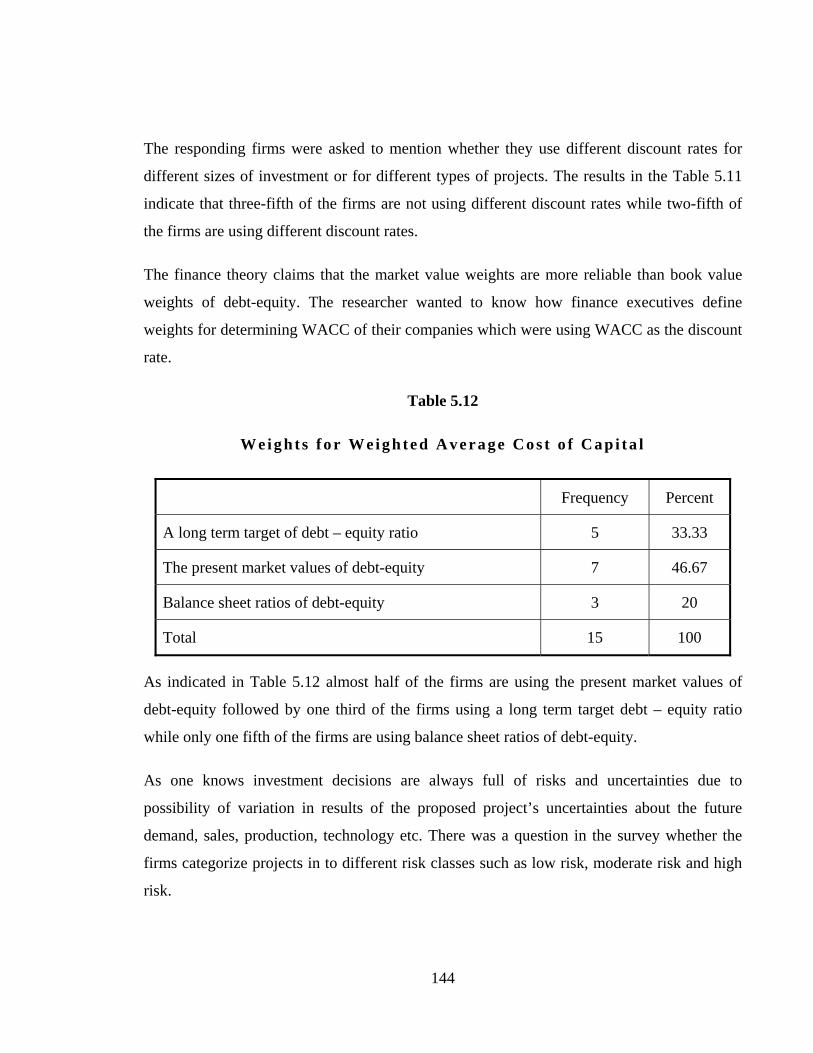

The finance theory claims that the market value weights are more reliable than book value

weights of debt-equity. The researcher wanted to know how finance executives define

weights for determining WACC of their companies which were using WACC as the discount

rate.

Table 5.12

W e i g h t s f o r W e i g h t e d A v e r a g e C o s t o f C a p i t a l

Frequency Percent

A long term target of debt – equity ratio 5 33.33

The present market values of debt-equity 7 46.67

Balance sheet ratios of debt-equity 3 20

Total 15 100

As indicated in Table 5.12 almost half of the firms are using the present market values of

debt-equity followed by one third of the firms using a long term target debt – equity ratio

while only one fifth of the firms are using balance sheet ratios of debt-equity.

As one knows investment decisions are always full of risks and uncertainties due to

possibility of variation in results of the proposed project’s uncertainties about the future

demand, sales, production, technology etc. There was a question in the survey whether the

firms categorize projects in to different risk classes such as low risk, moderate risk and high

risk.

145

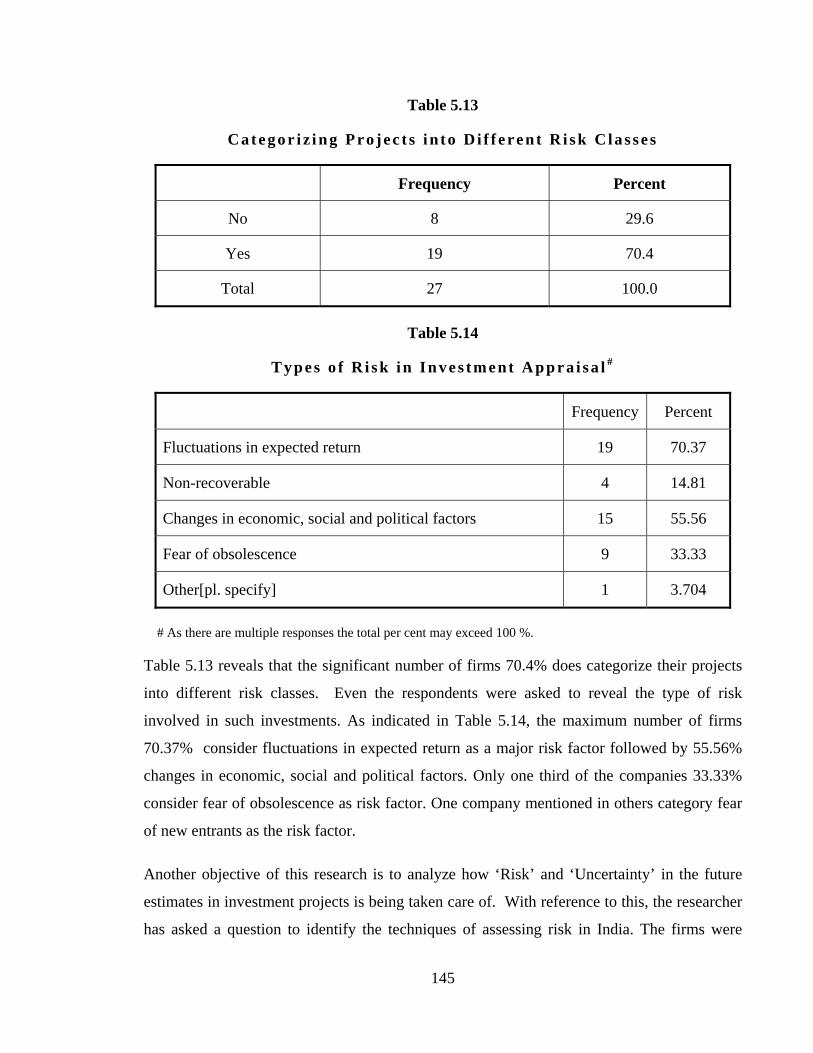

Table 5.13

C a t e g o r i z i ng P r o j e c t s i n t o D i f f eren t R i sk C las se s

Frequency Percent

No 8 29.6

Yes 19 70.4

Total 27 100.0

Table 5.14

T y p e s o f R i s k i n I n v e s t m e nt A p p r a i s a l #

Frequency Percent

Fluctuations in expected return 19 70.37

Non-recoverable 4 14.81

Changes in economic, social and political factors 15 55.56

Fear of obsolescence 9 33.33

Other[pl. specify] 1 3.704

# As there are multiple responses the total per cent may exceed 100 %.

Table 5.13 reveals that the significant number of firms 70.4% does categorize their projects

into different risk classes. Even the respondents were asked to reveal the type of risk

involved in such investments. As indicated in Table 5.14, the maximum number of firms

70.37% consider fluctuations in expected return as a major risk factor followed by 55.56%

changes in economic, social and political factors. Only one third of the companies 33.33%

consider fear of obsolescence as risk factor. One company mentioned in others category fear

of new entrants as the risk factor.

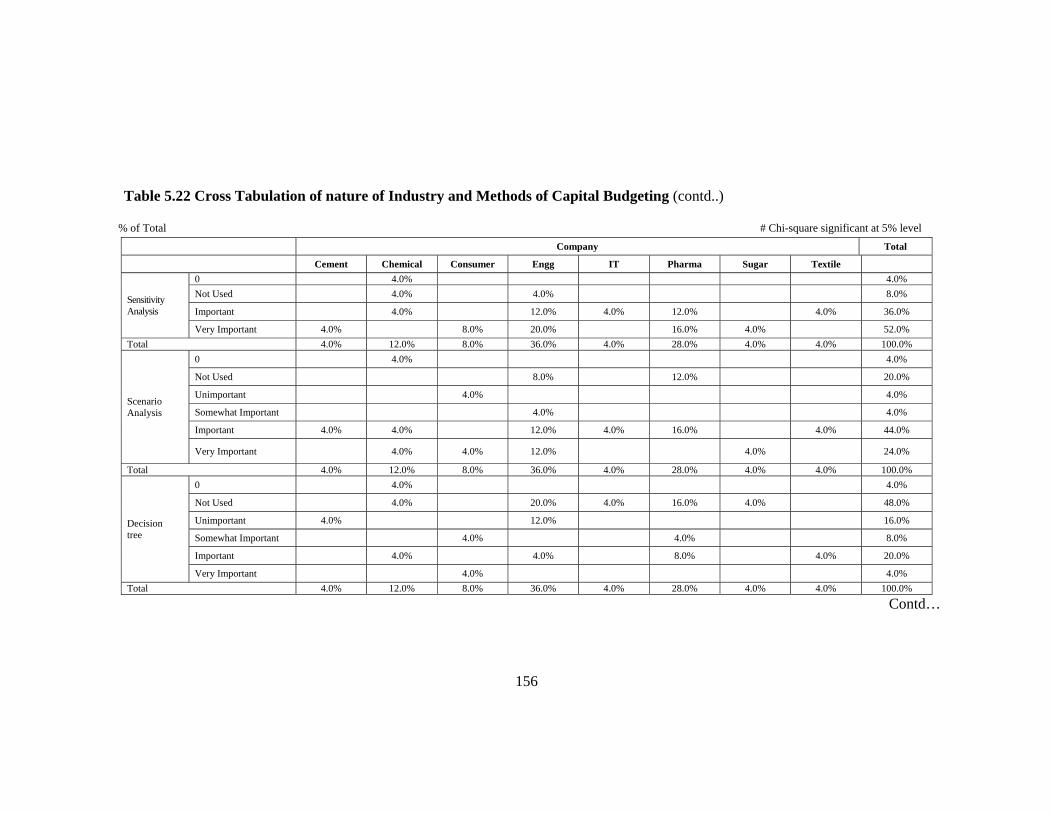

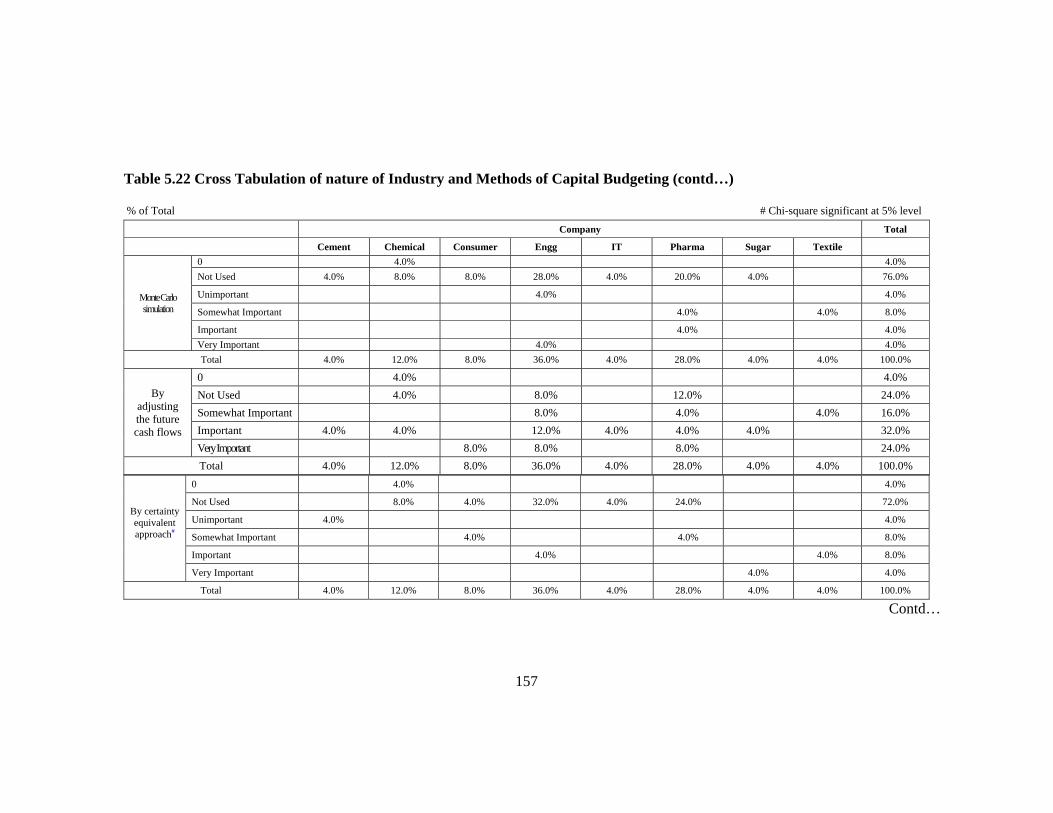

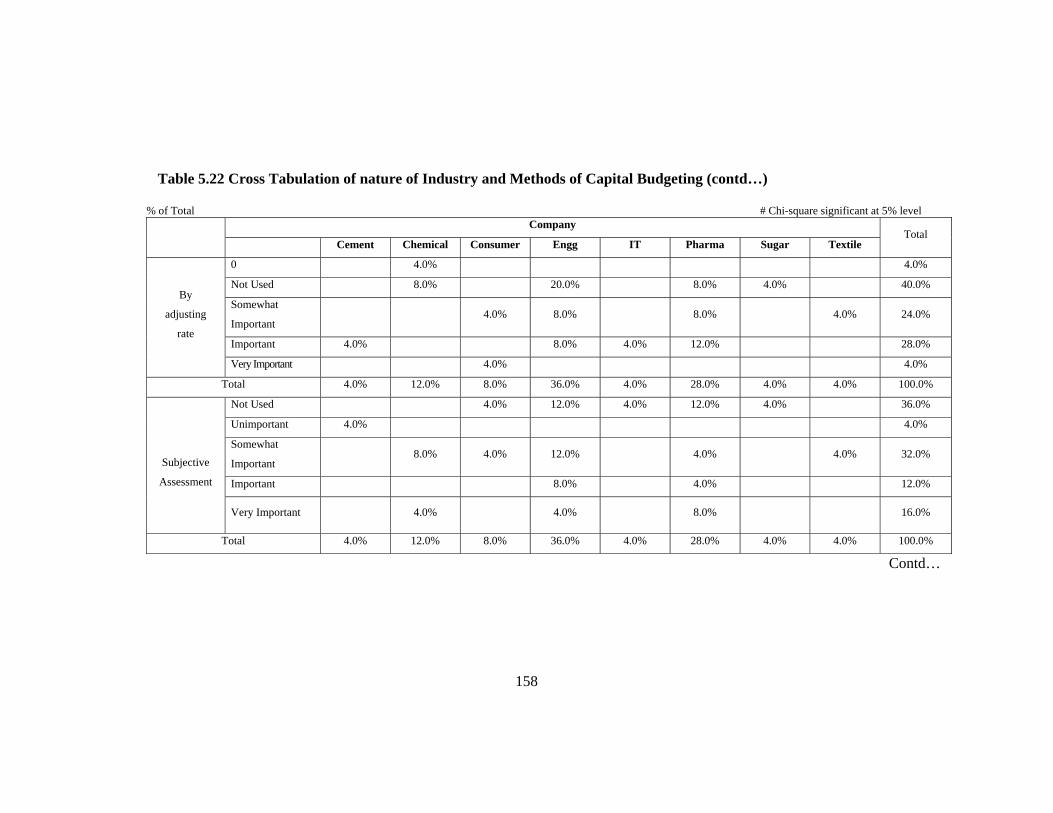

Another objective of this research is to analyze how ‘Risk’ and ‘Uncertainty’ in the future

estimates in investment projects is being taken care of. With reference to this, the researcher

has asked a question to identify the techniques of assessing risk in India. The firms were

146

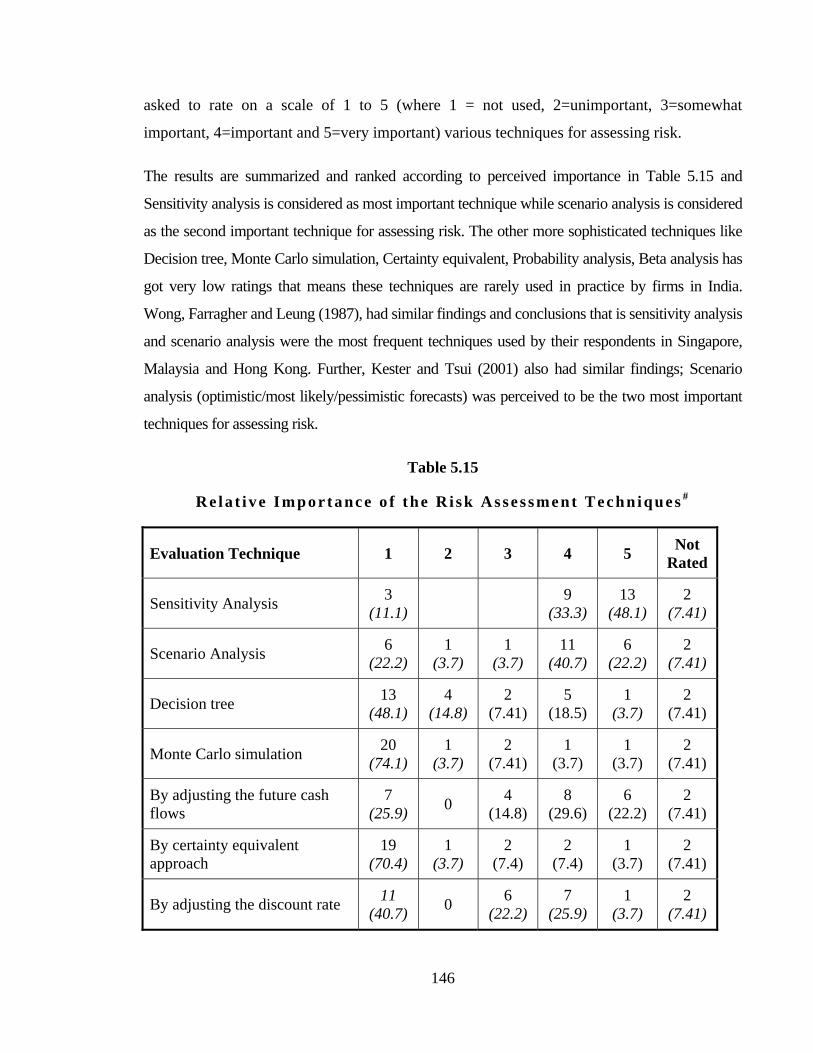

asked to rate on a scale of 1 to 5 (where 1 = not used, 2=unimportant, 3=somewhat

important, 4=important and 5=very important) various techniques for assessing risk.

The results are summarized and ranked according to perceived importance in Table 5.15 and

Sensitivity analysis is considered as most important technique while scenario analysis is considered

as the second important technique for assessing risk. The other more sophisticated techniques like

Decision tree, Monte Carlo simulation, Certainty equivalent, Probability analysis, Beta analysis has

got very low ratings that means these techniques are rarely used in practice by firms in India.

Wong, Farragher and Leung (1987), had similar findings and conclusions that is sensitivity analysis

and scenario analysis were the most frequent techniques used by their respondents in Singapore,

Malaysia and Hong Kong. Further, Kester and Tsui (2001) also had similar findings; Scenario

analysis (optimistic/most likely/pessimistic forecasts) was perceived to be the two most important

techniques for assessing risk.

Table 5.15

R e l a t i v e I m p o r t a nc e o f t h e R i s k A s s e s s m e n t T e c h n i q u e s #

Evaluation Technique 1 2 3 4 5 Not Rated

Sensitivity Analysis 3 (11.1) 9

(33.3) 13

(48.1) 2

(7.41)

Scenario Analysis 6 (22.2)

1 (3.7)

1 (3.7)

11 (40.7)

6 (22.2)

2 (7.41)

Decision tree 13 (48.1)

4 (14.8)

2 (7.41)

5 (18.5)

1 (3.7)

2 (7.41)

Monte Carlo simulation 20 (74.1)

1 (3.7)

2 (7.41)

1 (3.7)

1 (3.7)

2 (7.41)

By adjusting the future cash flows

7 (25.9) 0 4

(14.8) 8

(29.6) 6

(22.2) 2

(7.41)

By certainty equivalent approach

19 (70.4)

1 (3.7)

2 (7.4)

2 (7.4)

1 (3.7)

2 (7.41)

By adjusting the discount rate 11 (40.7) 0 6

(22.2) 7

(25.9) 1

(3.7) 2

(7.41)

147

Evaluation Technique 1 2 3 4 5 Not Rated

Subjective assessment 9 (33.3)

1 (3.7)

8 (29.6)

3 (11.1)

4 (14.8)

2 (7.41)

Probability analysis 15 (55.6)

2 (7.41)

2 (7.41)

4 (14.8)

2 (7.41)

2 (7.41)

Shorten Payback period 12 (44.4) 0 3

(11.1) 7

(25.9) 3

(11.1) 2

(7.41)

Beta analysis 22 (81.5) 0 1

(3.7) 0 2 (7.4)

2 (7.41)

Any other (Please specify) 0 0 0 0 0 0

# As there are multiple responses the total per cent may exceed 100 %. / Figure in parenthesis are in %

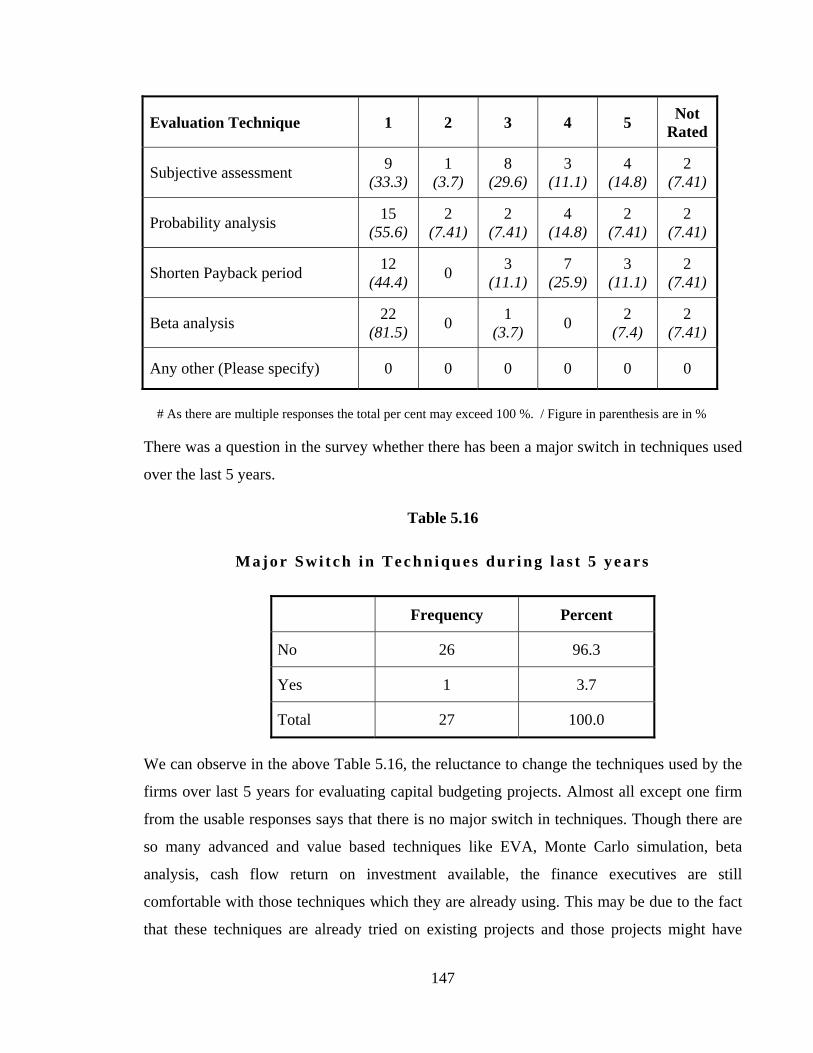

There was a question in the survey whether there has been a major switch in techniques used

over the last 5 years.

Table 5.16

M a j o r Swi t c h i n T e c h n i q u e s d u r i n g l a s t 5 y e a r s

Frequency Percent

No 26 96.3

Yes 1 3.7

Total 27 100.0

We can observe in the above Table 5.16, the reluctance to change the techniques used by the

firms over last 5 years for evaluating capital budgeting projects. Almost all except one firm

from the usable responses says that there is no major switch in techniques. Though there are

so many advanced and value based techniques like EVA, Monte Carlo simulation, beta

analysis, cash flow return on investment available, the finance executives are still

comfortable with those techniques which they are already using. This may be due to the fact

that these techniques are already tried on existing projects and those projects might have

148

given good returns and also it requires less time and computer operations than the new

techniques. This can be cross verified by Q-18, pertaining to the relative importance given to

the various techniques for assessing risk, of this survey where majority of the firms are not

using advanced techniques.

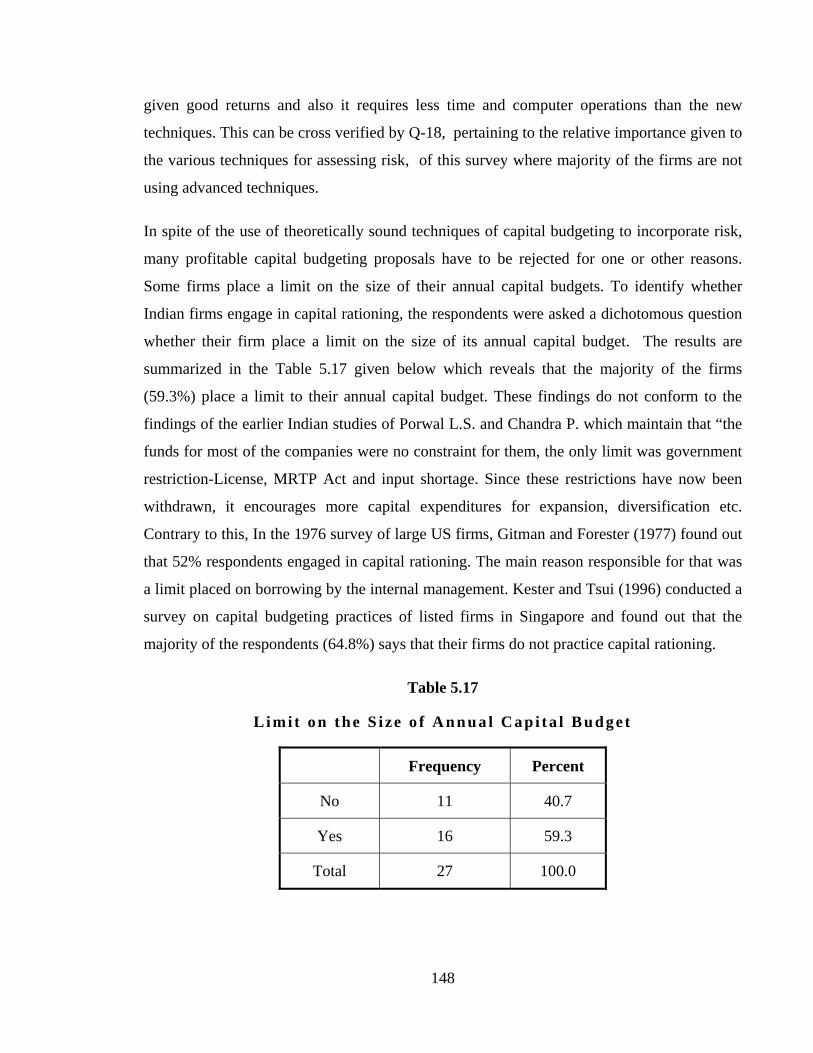

In spite of the use of theoretically sound techniques of capital budgeting to incorporate risk,

many profitable capital budgeting proposals have to be rejected for one or other reasons.

Some firms place a limit on the size of their annual capital budgets. To identify whether

Indian firms engage in capital rationing, the respondents were asked a dichotomous question

whether their firm place a limit on the size of its annual capital budget. The results are

summarized in the Table 5.17 given below which reveals that the majority of the firms

(59.3%) place a limit to their annual capital budget. These findings do not conform to the

findings of the earlier Indian studies of Porwal L.S. and Chandra P. which maintain that “the

funds for most of the companies were no constraint for them, the only limit was government

restriction-License, MRTP Act and input shortage. Since these restrictions have now been

withdrawn, it encourages more capital expenditures for expansion, diversification etc.

Contrary to this, In the 1976 survey of large US firms, Gitman and Forester (1977) found out

that 52% respondents engaged in capital rationing. The main reason responsible for that was

a limit placed on borrowing by the internal management. Kester and Tsui (1996) conducted a

survey on capital budgeting practices of listed firms in Singapore and found out that the

majority of the respondents (64.8%) says that their firms do not practice capital rationing.

Table 5.17

L imi t on the S i ze o f Annua l Cap i ta l Budge t

Frequency Percent

No 11 40.7

Yes 16 59.3

Total 27 100.0

149

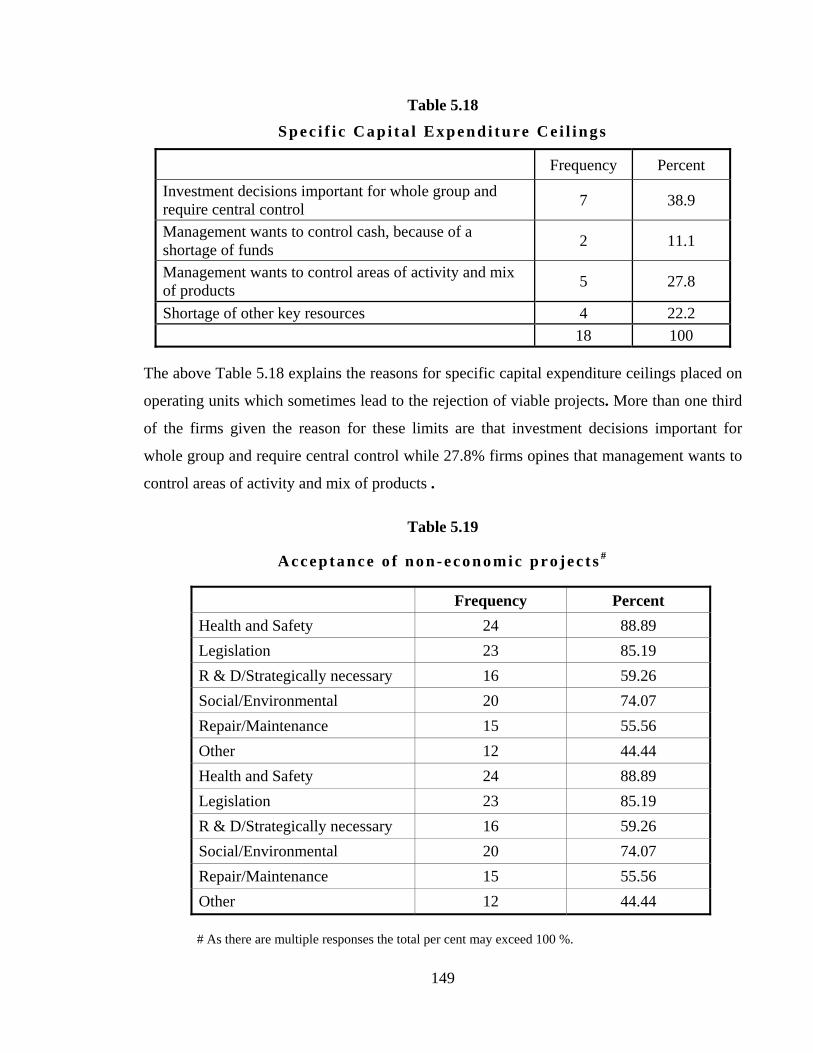

Table 5.18

S p e c i f i c C a p i t a l E x p e n d i t u r e C e i l i n g s

Frequency Percent Investment decisions important for whole group and require central control 7 38.9

Management wants to control cash, because of a shortage of funds 2 11.1

Management wants to control areas of activity and mix of products 5 27.8

Shortage of other key resources 4 22.2 18 100

The above Table 5.18 explains the reasons for specific capital expenditure ceilings placed on

operating units which sometimes lead to the rejection of viable projects. More than one third

of the firms given the reason for these limits are that investment decisions important for

whole group and require central control while 27.8% firms opines that management wants to

control areas of activity and mix of products .

Table 5.19

A c c e p t a n c e o f n o n - e c o n o m i c p r o j e c t s #

Frequency Percent Health and Safety 24 88.89 Legislation 23 85.19 R & D/Strategically necessary 16 59.26 Social/Environmental 20 74.07 Repair/Maintenance 15 55.56 Other 12 44.44 Health and Safety 24 88.89 Legislation 23 85.19 R & D/Strategically necessary 16 59.26 Social/Environmental 20 74.07 Repair/Maintenance 15 55.56 Other 12 44.44

# As there are multiple responses the total per cent may exceed 100 %.

150

The results for the acceptance of non-economic projects have been summarized in Table

5.19. Most of the respondents say that health and safety, legislation and social or

environmental factors are mainly responsible for accepting such projects. Though more than

one half of the survey participants also believe that R&D and repair/maintenance are

sometimes responsible for the acceptance of non-economic projects but in that case we must

accept that these projects will have economic effects also.

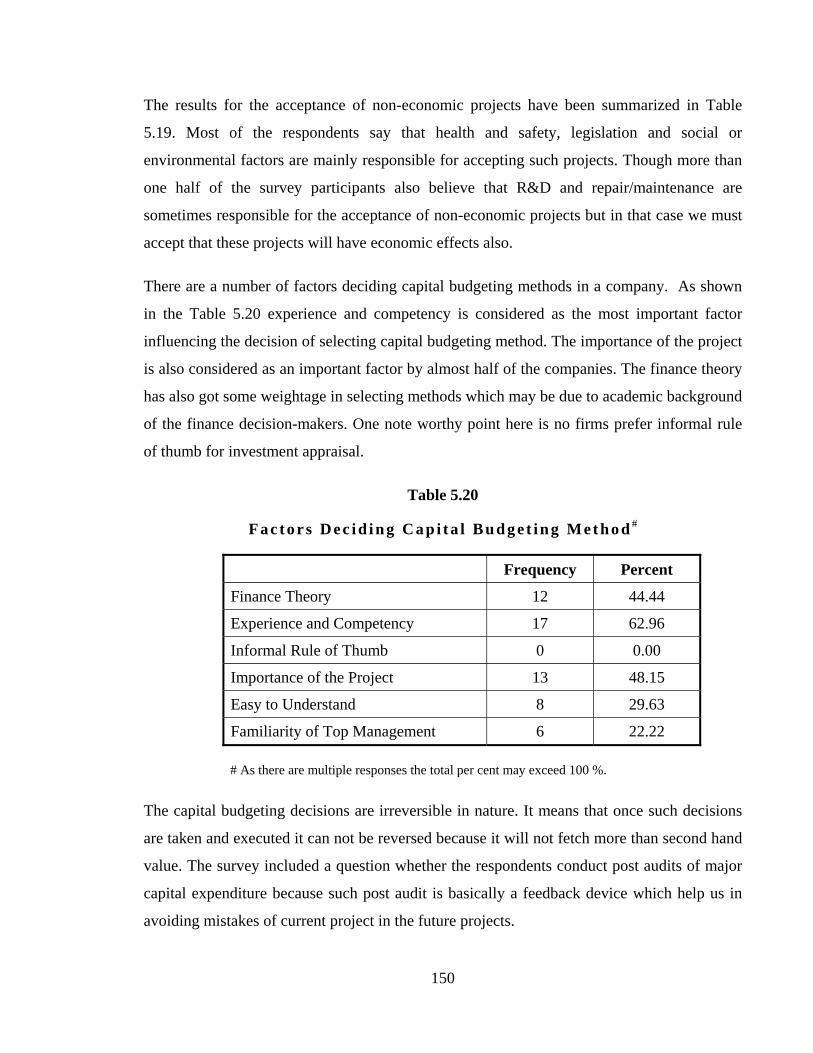

There are a number of factors deciding capital budgeting methods in a company. As shown

in the Table 5.20 experience and competency is considered as the most important factor

influencing the decision of selecting capital budgeting method. The importance of the project

is also considered as an important factor by almost half of the companies. The finance theory

has also got some weightage in selecting methods which may be due to academic background

of the finance decision-makers. One note worthy point here is no firms prefer informal rule

of thumb for investment appraisal.

Table 5.20

F a c t o r s D e c i d i n g C a p i t a l B u d g e t i n g M e t h o d #

Frequency Percent

Finance Theory 12 44.44

Experience and Competency 17 62.96

Informal Rule of Thumb 0 0.00

Importance of the Project 13 48.15

Easy to Understand 8 29.63

Familiarity of Top Management 6 22.22

# As there are multiple responses the total per cent may exceed 100 %.

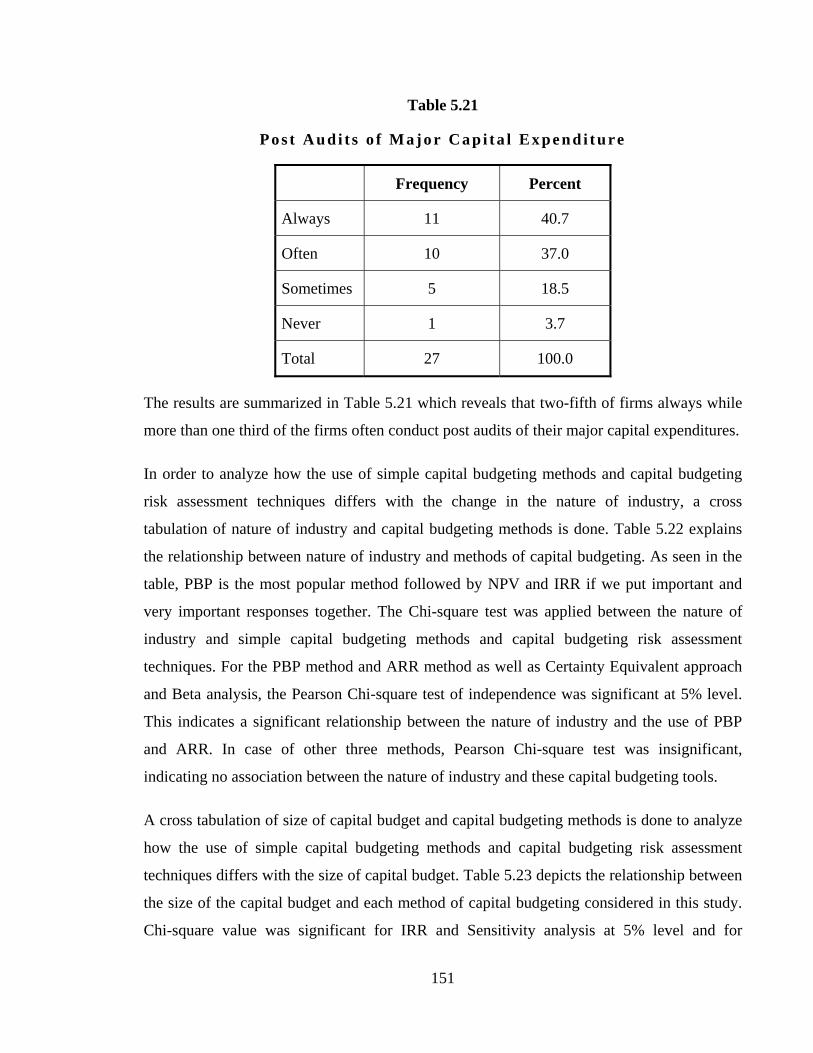

The capital budgeting decisions are irreversible in nature. It means that once such decisions

are taken and executed it can not be reversed because it will not fetch more than second hand

value. The survey included a question whether the respondents conduct post audits of major

capital expenditure because such post audit is basically a feedback device which help us in

avoiding mistakes of current project in the future projects.

151

Table 5.21

Pos t Aud i t s o f Major Cap i ta l Expend i ture

Frequency Percent

Always 11 40.7

Often 10 37.0

Sometimes 5 18.5

Never 1 3.7

Total 27 100.0

The results are summarized in Table 5.21 which reveals that two-fifth of firms always while

more than one third of the firms often conduct post audits of their major capital expenditures.

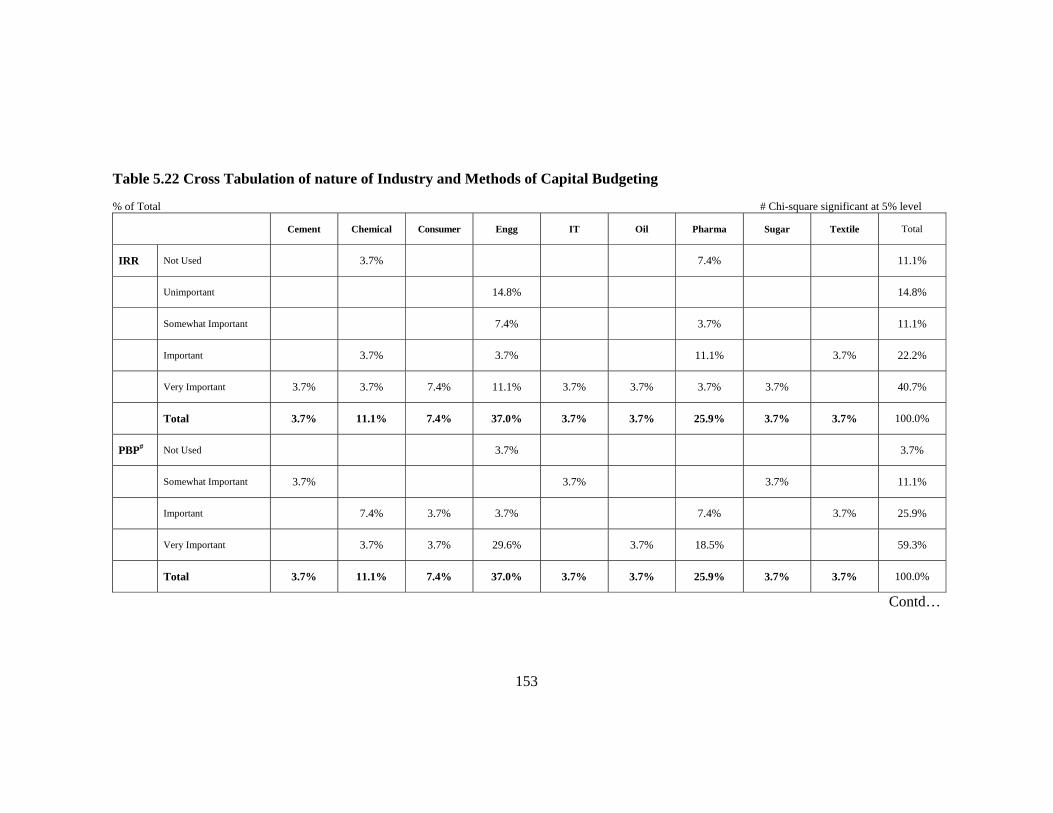

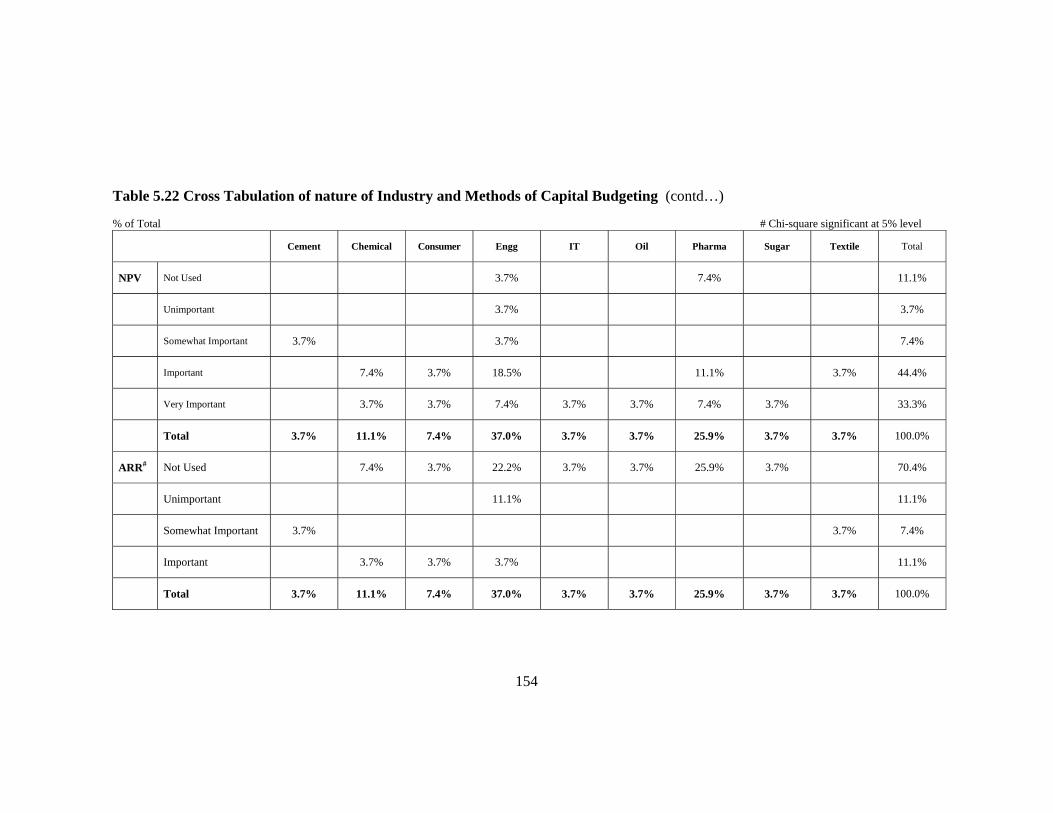

In order to analyze how the use of simple capital budgeting methods and capital budgeting

risk assessment techniques differs with the change in the nature of industry, a cross

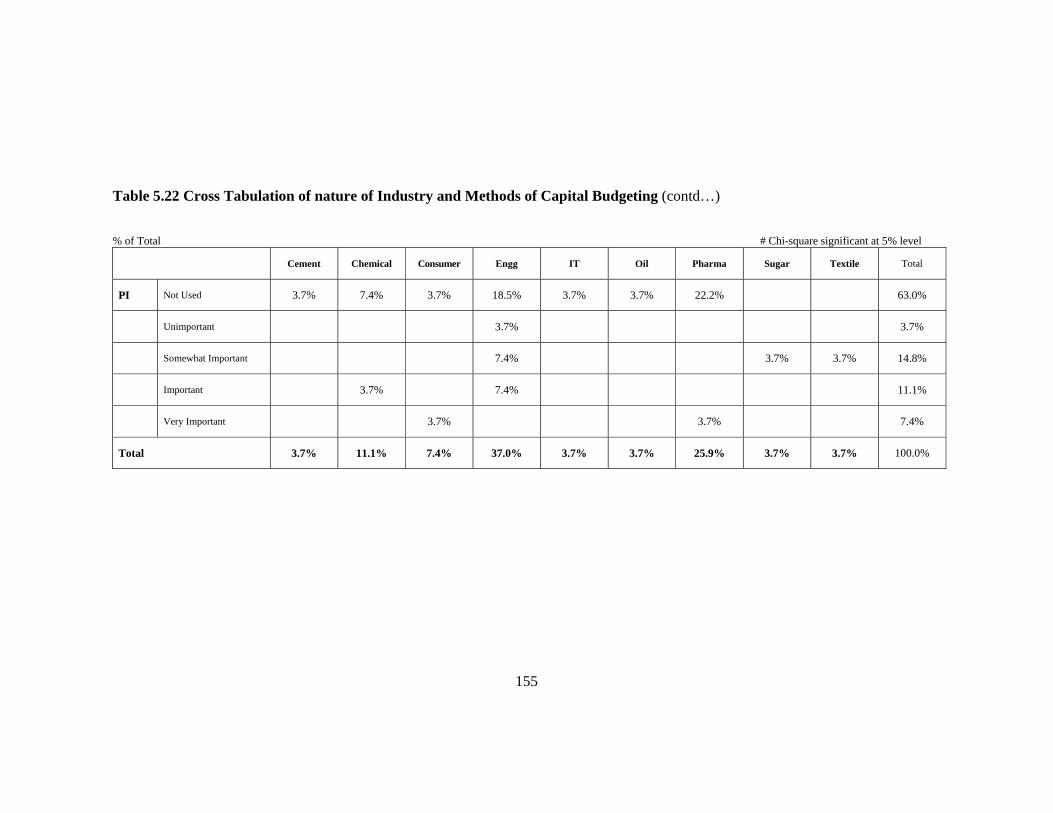

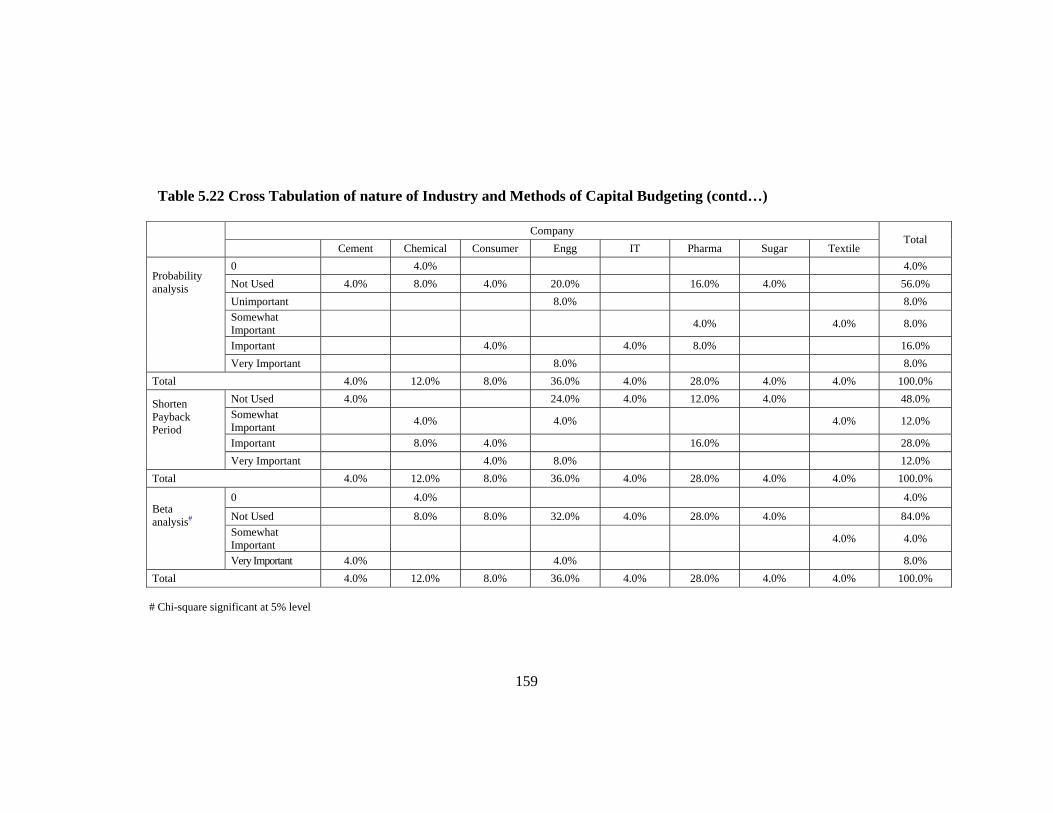

tabulation of nature of industry and capital budgeting methods is done. Table 5.22 explains

the relationship between nature of industry and methods of capital budgeting. As seen in the

table, PBP is the most popular method followed by NPV and IRR if we put important and

very important responses together. The Chi-square test was applied between the nature of

industry and simple capital budgeting methods and capital budgeting risk assessment

techniques. For the PBP method and ARR method as well as Certainty Equivalent approach

and Beta analysis, the Pearson Chi-square test of independence was significant at 5% level.

This indicates a significant relationship between the nature of industry and the use of PBP

and ARR. In case of other three methods, Pearson Chi-square test was insignificant,

indicating no association between the nature of industry and these capital budgeting tools.

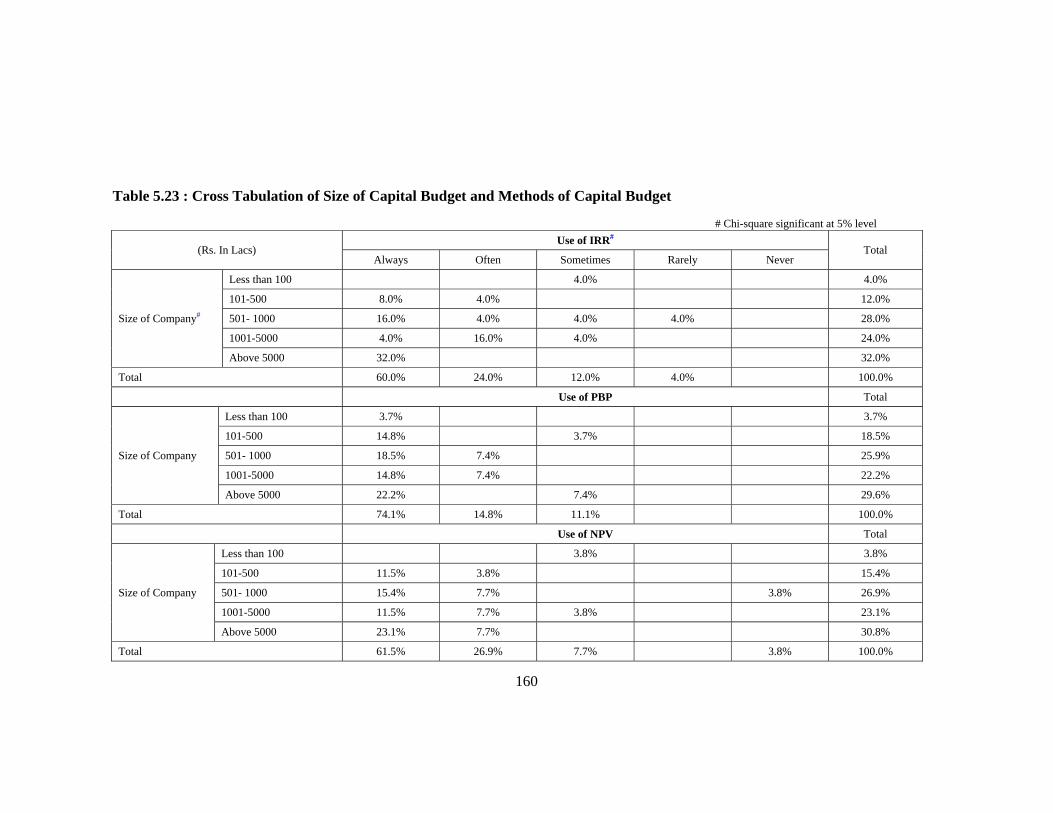

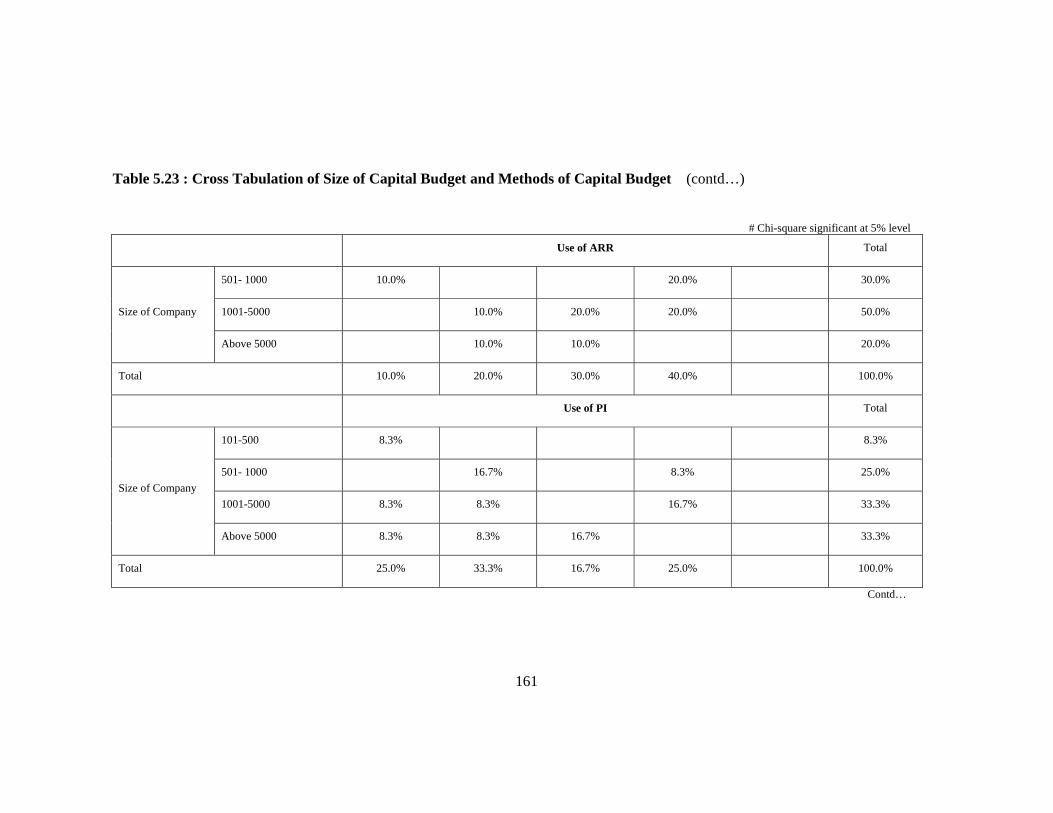

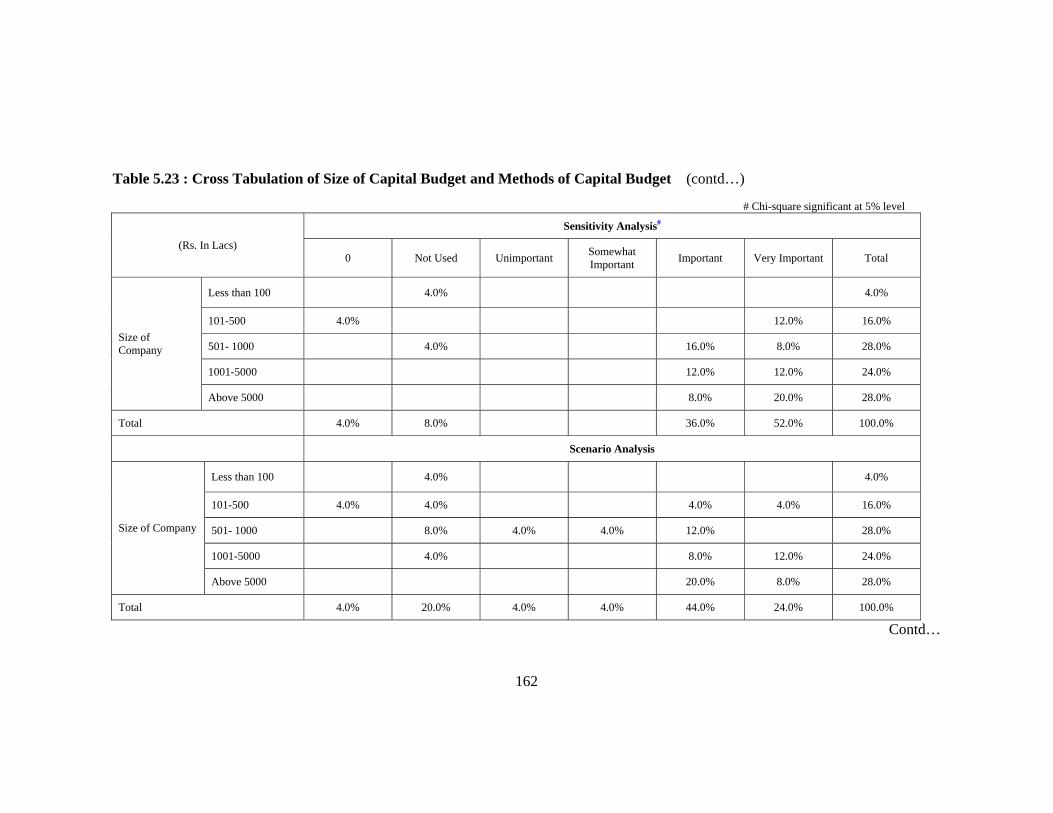

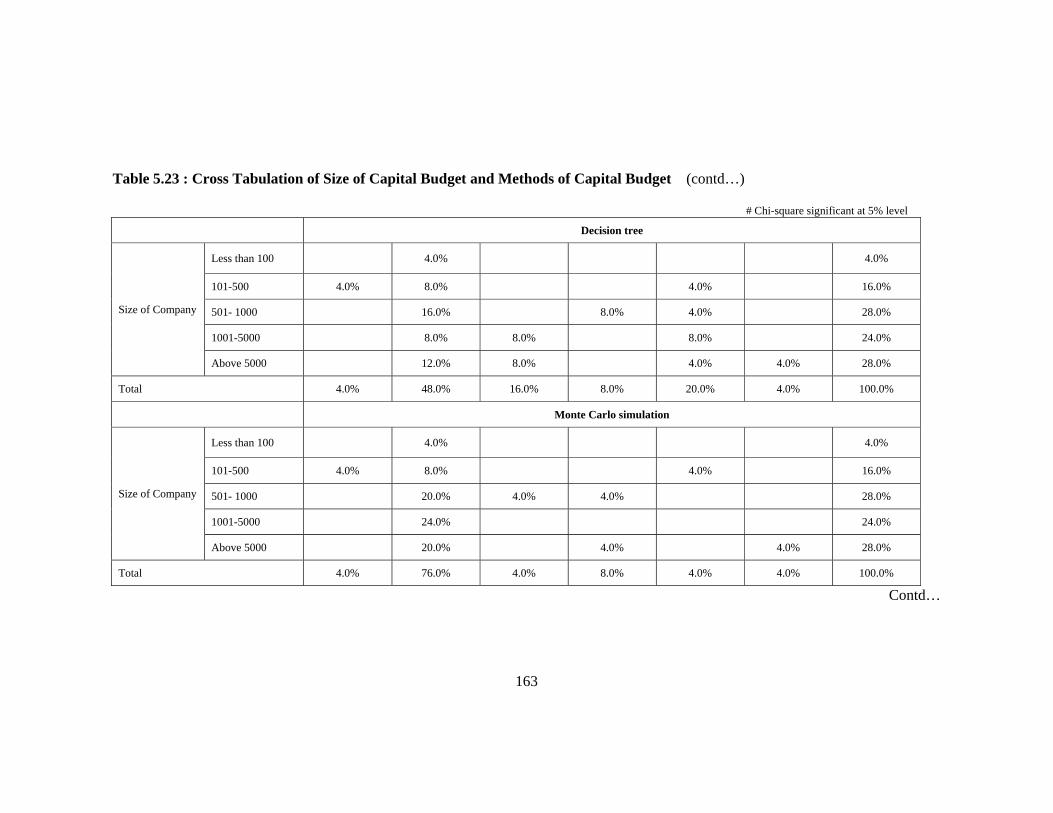

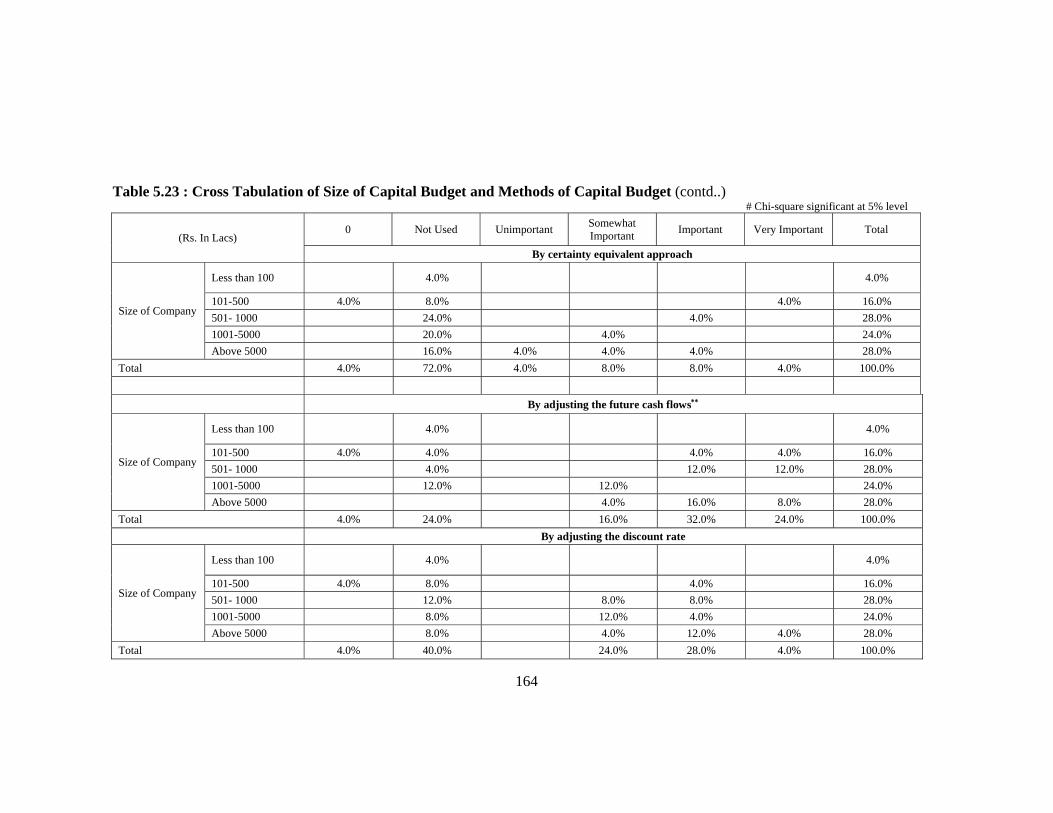

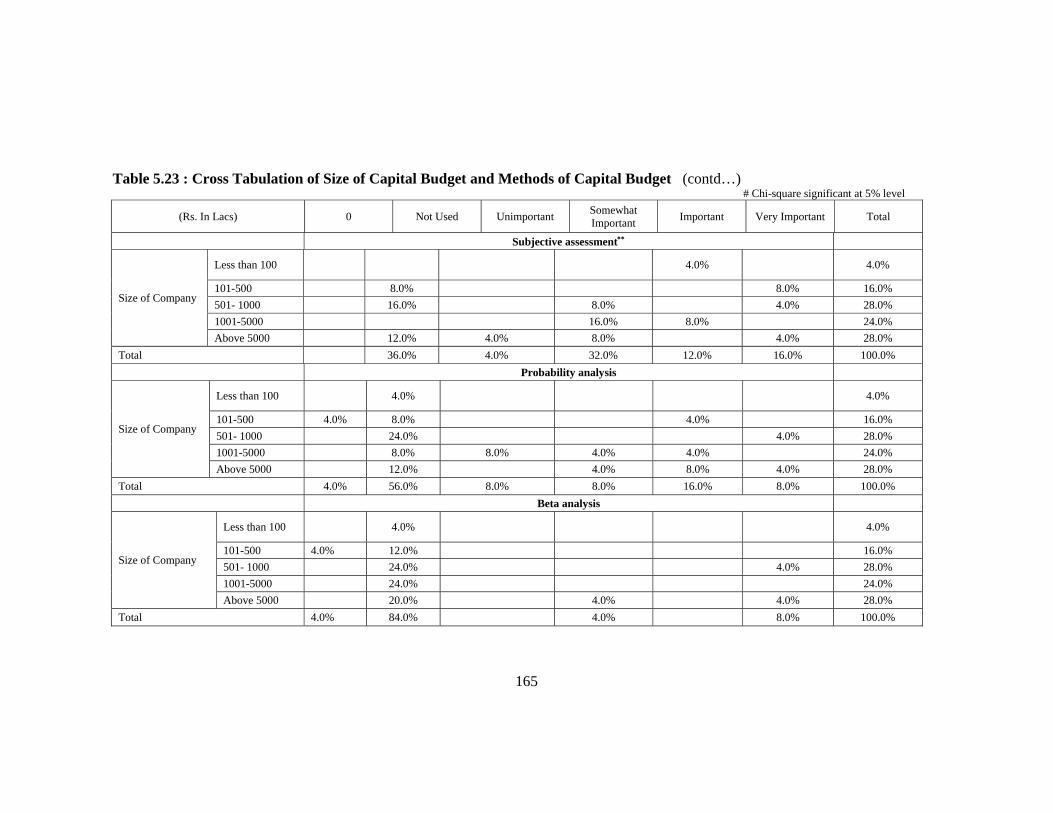

A cross tabulation of size of capital budget and capital budgeting methods is done to analyze

how the use of simple capital budgeting methods and capital budgeting risk assessment

techniques differs with the size of capital budget. Table 5.23 depicts the relationship between

the size of the capital budget and each method of capital budgeting considered in this study.

Chi-square value was significant for IRR and Sensitivity analysis at 5% level and for

152

adjusting the future cash flows and subjective assessment at 10% level. In case of other

methods, Pearson Chi-square test was insignificant, indicating no association between the

size of capital budget and these capital budgeting tools.

Conclusion:

The results of the present survey is reassuring that pay back period as a capital budgeting

method is widely used even today but now it is not the only method used for investment

appraisal. The firms use multiple criteria in selecting capital budgeting projects. The firms

prefer to use now DCF techniques like IRR and NPV also. All the respondent in this survey

are using PBP as well as IRR or NPV while evaluating investment projects. The firms

surveyed find risk to be an important consideration in their capital budgeting decisions. The

sensitivity analysis and scenario analysis are the most widely used techniques for project risk

analysis. Most of the firms are using WACC as the discount rate for using DCF techniques

and they prefer to use present market values of debt-equity for assigning weights.

153

Table 5.22 Cross Tabulation of nature of Industry and Methods of Capital Budgeting % of Total # Chi-square significant at 5% level

Cement Chemical Consumer Engg IT Oil Pharma Sugar Textile Total

IRR Not Used 3.7% 7.4% 11.1%

Unimportant 14.8% 14.8%

Somewhat Important 7.4% 3.7% 11.1%

Important 3.7% 3.7% 11.1% 3.7% 22.2%

Very Important 3.7% 3.7% 7.4% 11.1% 3.7% 3.7% 3.7% 3.7% 40.7%

Total 3.7% 11.1% 7.4% 37.0% 3.7% 3.7% 25.9% 3.7% 3.7% 100.0%

PBP# Not Used 3.7% 3.7%

Somewhat Important 3.7% 3.7% 3.7% 11.1%

Important 7.4% 3.7% 3.7% 7.4% 3.7% 25.9%

Very Important 3.7% 3.7% 29.6% 3.7% 18.5% 59.3%

Total 3.7% 11.1% 7.4% 37.0% 3.7% 3.7% 25.9% 3.7% 3.7% 100.0%

Contd…

154

Table 5.22 Cross Tabulation of nature of Industry and Methods of Capital Budgeting (contd…) % of Total # Chi-square significant at 5% level

Cement Chemical Consumer Engg IT Oil Pharma Sugar Textile Total

NPV Not Used 3.7% 7.4% 11.1%

Unimportant 3.7% 3.7%

Somewhat Important 3.7% 3.7% 7.4%

Important 7.4% 3.7% 18.5% 11.1% 3.7% 44.4%

Very Important 3.7% 3.7% 7.4% 3.7% 3.7% 7.4% 3.7% 33.3%

Total 3.7% 11.1% 7.4% 37.0% 3.7% 3.7% 25.9% 3.7% 3.7% 100.0%

ARR# Not Used 7.4% 3.7% 22.2% 3.7% 3.7% 25.9% 3.7% 70.4%

Unimportant 11.1% 11.1%

Somewhat Important 3.7% 3.7% 7.4%

Important 3.7% 3.7% 3.7% 11.1%

Total 3.7% 11.1% 7.4% 37.0% 3.7% 3.7% 25.9% 3.7% 3.7% 100.0%

155

Table 5.22 Cross Tabulation of nature of Industry and Methods of Capital Budgeting (contd…) % of Total # Chi-square significant at 5% level

Cement Chemical Consumer Engg IT Oil Pharma Sugar Textile Total

PI Not Used 3.7% 7.4% 3.7% 18.5% 3.7% 3.7% 22.2% 63.0%

Unimportant 3.7% 3.7%

Somewhat Important 7.4% 3.7% 3.7% 14.8%

Important 3.7% 7.4% 11.1%

Very Important 3.7% 3.7% 7.4%

Total 3.7% 11.1% 7.4% 37.0% 3.7% 3.7% 25.9% 3.7% 3.7% 100.0%

156

Table 5.22 Cross Tabulation of nature of Industry and Methods of Capital Budgeting (contd..) % of Total # Chi-square significant at 5% level

Contd…

Company Total

Cement Chemical Consumer Engg IT Pharma Sugar Textile

Sensitivity Analysis

0 4.0% 4.0% Not Used 4.0% 4.0% 8.0%

Important 4.0% 12.0% 4.0% 12.0% 4.0% 36.0%

Very Important 4.0% 8.0% 20.0% 16.0% 4.0% 52.0% Total 4.0% 12.0% 8.0% 36.0% 4.0% 28.0% 4.0% 4.0% 100.0%

Scenario Analysis

0 4.0% 4.0%

Not Used 8.0% 12.0% 20.0%

Unimportant 4.0% 4.0%

Somewhat Important 4.0% 4.0%

Important 4.0% 4.0% 12.0% 4.0% 16.0% 4.0% 44.0%

Very Important 4.0% 4.0% 12.0% 4.0% 24.0%

Total 4.0% 12.0% 8.0% 36.0% 4.0% 28.0% 4.0% 4.0% 100.0%

Decision tree

0 4.0% 4.0%

Not Used 4.0% 20.0% 4.0% 16.0% 4.0% 48.0%

Unimportant 4.0% 12.0% 16.0%

Somewhat Important 4.0% 4.0% 8.0%

Important 4.0% 4.0% 8.0% 4.0% 20.0%

Very Important 4.0% 4.0% Total 4.0% 12.0% 8.0% 36.0% 4.0% 28.0% 4.0% 4.0% 100.0%

157

Table 5.22 Cross Tabulation of nature of Industry and Methods of Capital Budgeting (contd…) % of Total # Chi-square significant at 5% level

By certainty

equivalent approach#

0 4.0% 4.0%

Not Used 8.0% 4.0% 32.0% 4.0% 24.0% 72.0%

Unimportant 4.0% 4.0%

Somewhat Important 4.0% 4.0% 8.0%

Important 4.0% 4.0% 8.0%

Very Important 4.0% 4.0%

Total 4.0% 12.0% 8.0% 36.0% 4.0% 28.0% 4.0% 4.0% 100.0%

Contd…

Company Total

Cement Chemical Consumer Engg IT Pharma Sugar Textile

Monte Carlo simulation

0 4.0% 4.0% Not Used 4.0% 8.0% 8.0% 28.0% 4.0% 20.0% 4.0% 76.0%

Unimportant 4.0% 4.0%

Somewhat Important 4.0% 4.0% 8.0%

Important 4.0% 4.0% Very Important 4.0% 4.0% Total 4.0% 12.0% 8.0% 36.0% 4.0% 28.0% 4.0% 4.0% 100.0%

By adjusting the future cash flows

0 4.0% 4.0% Not Used 4.0% 8.0% 12.0% 24.0% Somewhat Important 8.0% 4.0% 4.0% 16.0% Important 4.0% 4.0% 12.0% 4.0% 4.0% 4.0% 32.0% Very Important 8.0% 8.0% 8.0% 24.0% Total 4.0% 12.0% 8.0% 36.0% 4.0% 28.0% 4.0% 4.0% 100.0%

158

Table 5.22 Cross Tabulation of nature of Industry and Methods of Capital Budgeting (contd…) % of Total # Chi-square significant at 5% level

Company

Total Cement Chemical Consumer Engg IT Pharma Sugar Textile

By

adjusting

rate

0 4.0% 4.0%

Not Used 8.0% 20.0% 8.0% 4.0% 40.0%

Somewhat

Important 4.0% 8.0% 8.0% 4.0% 24.0%

Important 4.0% 8.0% 4.0% 12.0% 28.0%

Very Important 4.0% 4.0%

Total 4.0% 12.0% 8.0% 36.0% 4.0% 28.0% 4.0% 4.0% 100.0%

Subjective

Assessment

Not Used 4.0% 12.0% 4.0% 12.0% 4.0% 36.0%

Unimportant 4.0% 4.0%

Somewhat

Important 8.0% 4.0% 12.0% 4.0% 4.0% 32.0%

Important 8.0% 4.0% 12.0%

Very Important 4.0% 4.0% 8.0% 16.0%

Total 4.0% 12.0% 8.0% 36.0% 4.0% 28.0% 4.0% 4.0% 100.0%

Contd…

159

Table 5.22 Cross Tabulation of nature of Industry and Methods of Capital Budgeting (contd…)

Company

Total Cement Chemical Consumer Engg IT Pharma Sugar Textile

Probability analysis

0 4.0% 4.0% Not Used 4.0% 8.0% 4.0% 20.0% 16.0% 4.0% 56.0% Unimportant 8.0% 8.0% Somewhat Important 4.0% 4.0% 8.0%

Important 4.0% 4.0% 8.0% 16.0% Very Important 8.0% 8.0%

Total 4.0% 12.0% 8.0% 36.0% 4.0% 28.0% 4.0% 4.0% 100.0%

Shorten Payback Period

Not Used 4.0% 24.0% 4.0% 12.0% 4.0% 48.0% Somewhat Important 4.0% 4.0% 4.0% 12.0%

Important 8.0% 4.0% 16.0% 28.0% Very Important 4.0% 8.0% 12.0%

Total 4.0% 12.0% 8.0% 36.0% 4.0% 28.0% 4.0% 4.0% 100.0%

Beta analysis#

0 4.0% 4.0%

Not Used 8.0% 8.0% 32.0% 4.0% 28.0% 4.0% 84.0% Somewhat Important 4.0% 4.0%

Very Important 4.0% 4.0% 8.0% Total 4.0% 12.0% 8.0% 36.0% 4.0% 28.0% 4.0% 4.0% 100.0%

# Chi-square significant at 5% level

160

Table 5.23 : Cross Tabulation of Size of Capital Budget and Methods of Capital Budget # Chi-square significant at 5% level

(Rs. In Lacs) Use of IRR#

Total Always Often Sometimes Rarely Never

Size of Company#

Less than 100 4.0% 4.0%

101-500 8.0% 4.0% 12.0%

501- 1000 16.0% 4.0% 4.0% 4.0% 28.0%

1001-5000 4.0% 16.0% 4.0% 24.0%

Above 5000 32.0% 32.0%

Total 60.0% 24.0% 12.0% 4.0% 100.0%

Use of PBP Total

Size of Company

Less than 100 3.7% 3.7%

101-500 14.8% 3.7% 18.5%

501- 1000 18.5% 7.4% 25.9%

1001-5000 14.8% 7.4% 22.2%

Above 5000 22.2% 7.4% 29.6%

Total 74.1% 14.8% 11.1% 100.0%

Use of NPV Total

Size of Company

Less than 100 3.8% 3.8%

101-500 11.5% 3.8% 15.4%

501- 1000 15.4% 7.7% 3.8% 26.9%

1001-5000 11.5% 7.7% 3.8% 23.1%

Above 5000 23.1% 7.7% 30.8%

Total 61.5% 26.9% 7.7% 3.8% 100.0%

161

Table 5.23 : Cross Tabulation of Size of Capital Budget and Methods of Capital Budget (contd…) # Chi-square significant at 5% level

Use of ARR Total

Size of Company

501- 1000 10.0% 20.0% 30.0%

1001-5000 10.0% 20.0% 20.0% 50.0%

Above 5000 10.0% 10.0% 20.0%

Total 10.0% 20.0% 30.0% 40.0% 100.0%

Use of PI Total

Size of Company

101-500 8.3% 8.3%

501- 1000 16.7% 8.3% 25.0%

1001-5000 8.3% 8.3% 16.7% 33.3%

Above 5000 8.3% 8.3% 16.7% 33.3%

Total 25.0% 33.3% 16.7% 25.0% 100.0%

Contd…

162

Table 5.23 : Cross Tabulation of Size of Capital Budget and Methods of Capital Budget (contd…) # Chi-square significant at 5% level

(Rs. In Lacs)

Sensitivity Analysis#

0 Not Used Unimportant Somewhat Important Important Very Important Total

Size of Company

Less than 100 4.0% 4.0%

101-500 4.0% 12.0% 16.0%

501- 1000 4.0% 16.0% 8.0% 28.0%

1001-5000 12.0% 12.0% 24.0%

Above 5000 8.0% 20.0% 28.0%

Total 4.0% 8.0% 36.0% 52.0% 100.0%

Scenario Analysis

Size of Company

Less than 100 4.0% 4.0%

101-500 4.0% 4.0% 4.0% 4.0% 16.0%

501- 1000 8.0% 4.0% 4.0% 12.0% 28.0%

1001-5000 4.0% 8.0% 12.0% 24.0%

Above 5000 20.0% 8.0% 28.0%

Total 4.0% 20.0% 4.0% 4.0% 44.0% 24.0% 100.0%

Contd…

163

Table 5.23 : Cross Tabulation of Size of Capital Budget and Methods of Capital Budget (contd…) # Chi-square significant at 5% level

Decision tree

Size of Company

Less than 100 4.0% 4.0%

101-500 4.0% 8.0% 4.0% 16.0%

501- 1000 16.0% 8.0% 4.0% 28.0%

1001-5000 8.0% 8.0% 8.0% 24.0%

Above 5000 12.0% 8.0% 4.0% 4.0% 28.0%

Total 4.0% 48.0% 16.0% 8.0% 20.0% 4.0% 100.0%

Monte Carlo simulation

Size of Company

Less than 100 4.0% 4.0%

101-500 4.0% 8.0% 4.0% 16.0%

501- 1000 20.0% 4.0% 4.0% 28.0%

1001-5000 24.0% 24.0%

Above 5000 20.0% 4.0% 4.0% 28.0%

Total 4.0% 76.0% 4.0% 8.0% 4.0% 4.0% 100.0%

Contd…

164

Table 5.23 : Cross Tabulation of Size of Capital Budget and Methods of Capital Budget (contd..) # Chi-square significant at 5% level

(Rs. In Lacs) 0 Not Used Unimportant Somewhat

Important Important Very Important Total

By certainty equivalent approach

Size of Company

Less than 100 4.0% 4.0%

101-500 4.0% 8.0% 4.0% 16.0% 501- 1000 24.0% 4.0% 28.0% 1001-5000 20.0% 4.0% 24.0% Above 5000 16.0% 4.0% 4.0% 4.0% 28.0%

Total 4.0% 72.0% 4.0% 8.0% 8.0% 4.0% 100.0% By adjusting the future cash flows∗∗

Size of Company

Less than 100 4.0% 4.0%

101-500 4.0% 4.0% 4.0% 4.0% 16.0% 501- 1000 4.0% 12.0% 12.0% 28.0% 1001-5000 12.0% 12.0% 24.0% Above 5000 4.0% 16.0% 8.0% 28.0%

Total 4.0% 24.0% 16.0% 32.0% 24.0% 100.0% By adjusting the discount rate

Size of Company

Less than 100 4.0% 4.0%

101-500 4.0% 8.0% 4.0% 16.0% 501- 1000 12.0% 8.0% 8.0% 28.0% 1001-5000 8.0% 12.0% 4.0% 24.0% Above 5000 8.0% 4.0% 12.0% 4.0% 28.0%

Total 4.0% 40.0% 24.0% 28.0% 4.0% 100.0%

165

Table 5.23 : Cross Tabulation of Size of Capital Budget and Methods of Capital Budget (contd…) # Chi-square significant at 5% level

(Rs. In Lacs) 0 Not Used Unimportant Somewhat Important Important Very Important Total

Subjective assessment∗∗

Size of Company

Less than 100 4.0% 4.0%

101-500 8.0% 8.0% 16.0% 501- 1000 16.0% 8.0% 4.0% 28.0% 1001-5000 16.0% 8.0% 24.0% Above 5000 12.0% 4.0% 8.0% 4.0% 28.0%

Total 36.0% 4.0% 32.0% 12.0% 16.0% 100.0% Probability analysis

Size of Company

Less than 100 4.0% 4.0%

101-500 4.0% 8.0% 4.0% 16.0% 501- 1000 24.0% 4.0% 28.0% 1001-5000 8.0% 8.0% 4.0% 4.0% 24.0% Above 5000 12.0% 4.0% 8.0% 4.0% 28.0%

Total 4.0% 56.0% 8.0% 8.0% 16.0% 8.0% 100.0% Beta analysis

Size of Company

Less than 100 4.0% 4.0%

101-500 4.0% 12.0% 16.0% 501- 1000 24.0% 4.0% 28.0% 1001-5000 24.0% 24.0% Above 5000 20.0% 4.0% 4.0% 28.0%

Total 4.0% 84.0% 4.0% 8.0% 100.0%