Embed Size (px)

Citation preview

67

CHAPTER - 5

COMPARATIVE

ANALYSIS OF

DIVIDEND POLICY

68

CONTENT

5.1 Introduction

5.2 Analysis of selected Companies

5.2.1 Dabur India Ltd.

5.2.2 Nestle India Ltd.

5.2.3 Britannia Industries Ltd.

5.2.4 NTPC Ltd.

5.2.5 PowerGrid Ltd.

5.2.6 Tata Power

5.2.7 Cipla GlobalLtd.

5.2.8 Dr.ReddyLtd.

5.2.9 SunPharma Ltd.

5.2.10 Infosys

5.2.11 TCS Ltd.

5.2.12 Wipro Ltd.

5.2.13 HDFC Bank Ltd.

5.2.14 SBI

5.2.15 Axis Bank

5.2.16 Eicher Motors Ltd.

5.2.17 TVS Ltd.

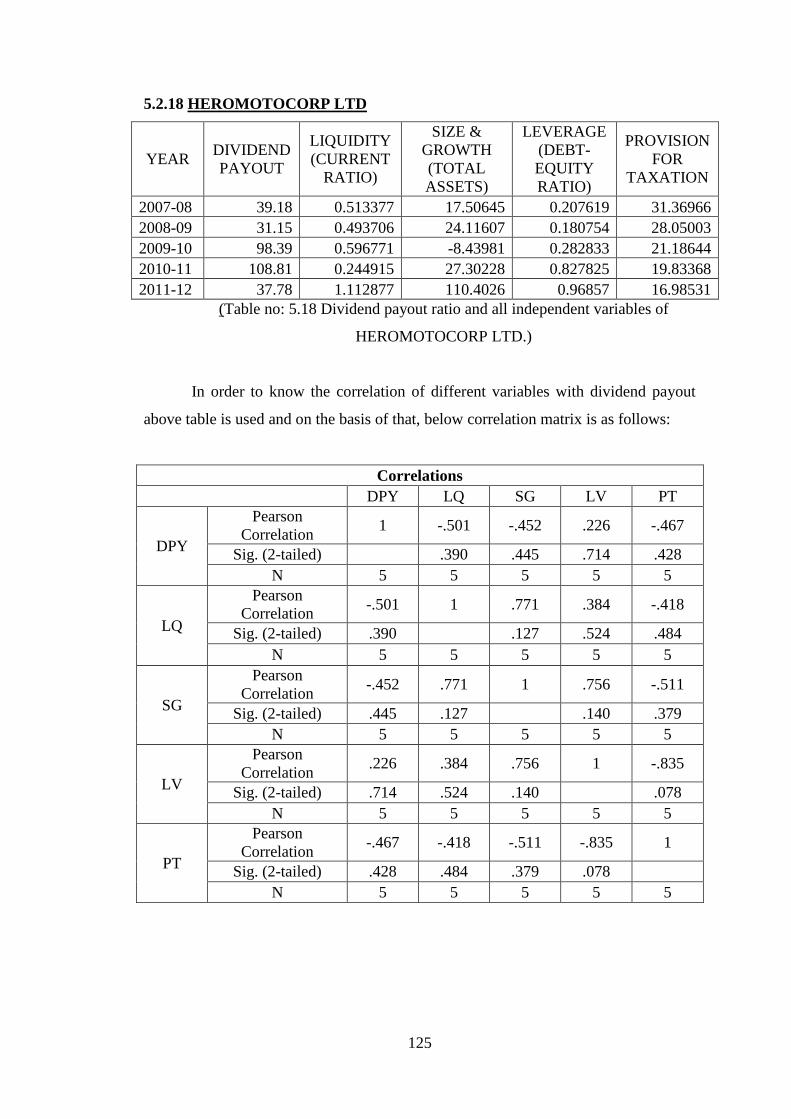

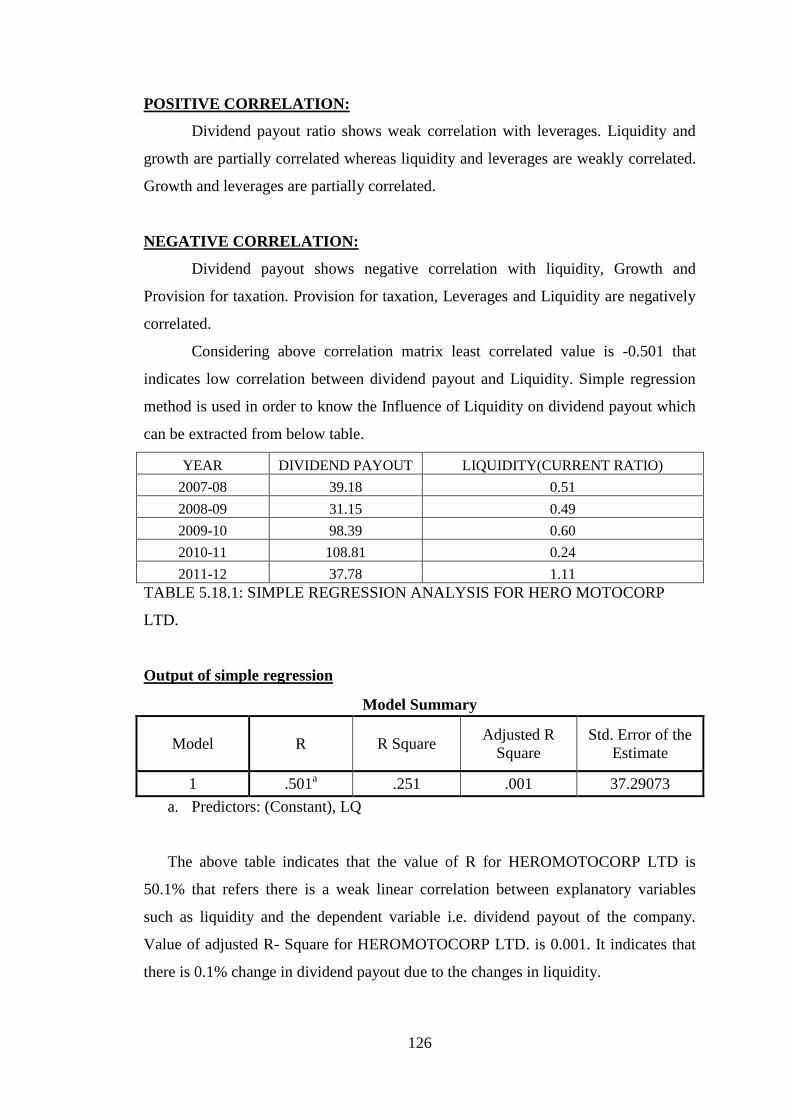

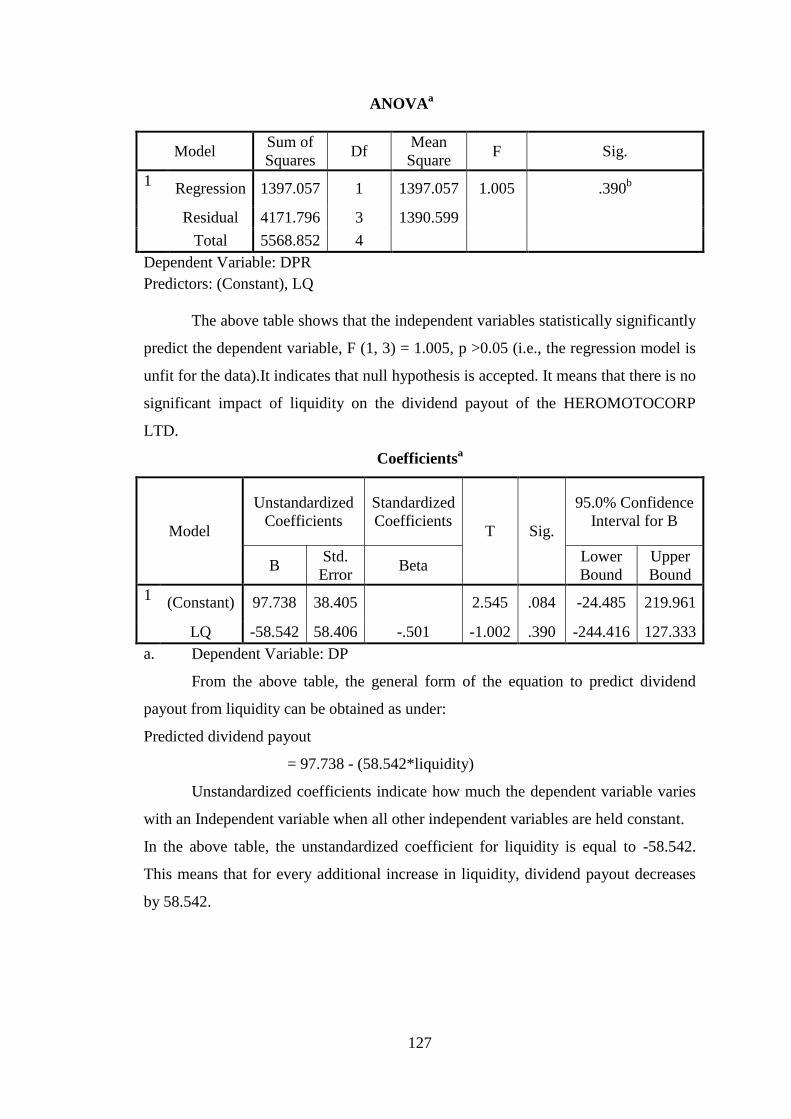

5.2.18 Heromotocorp Ltd

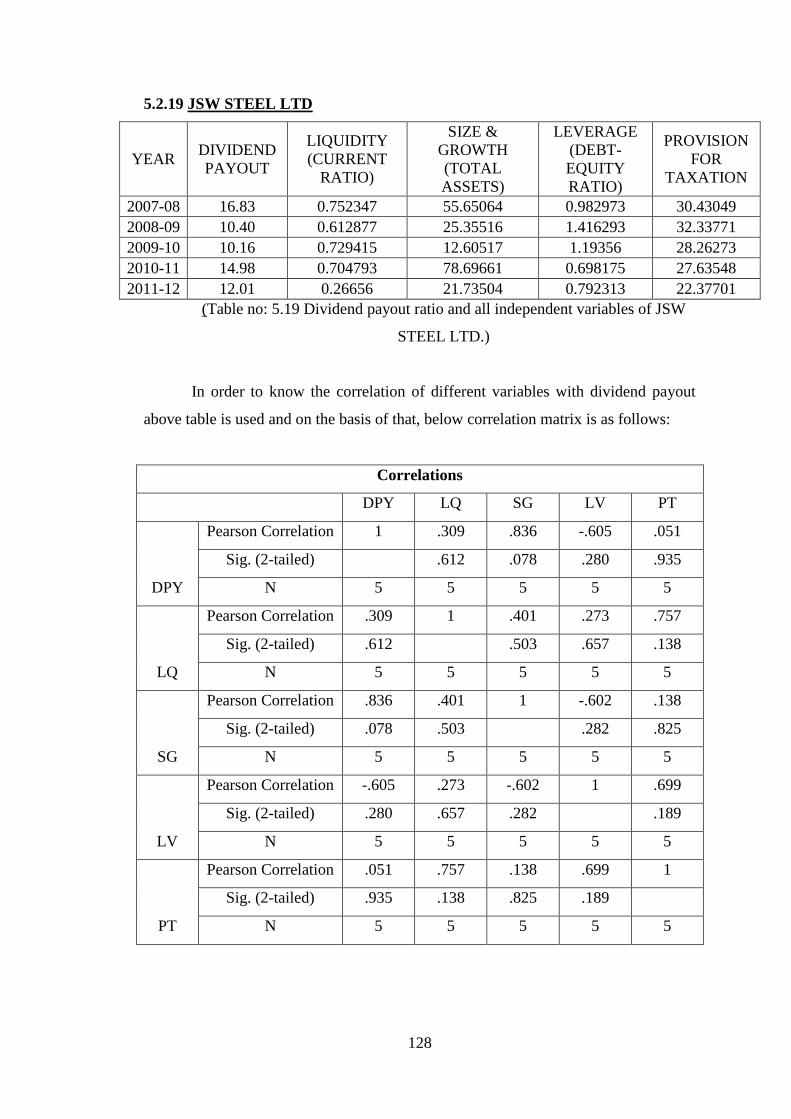

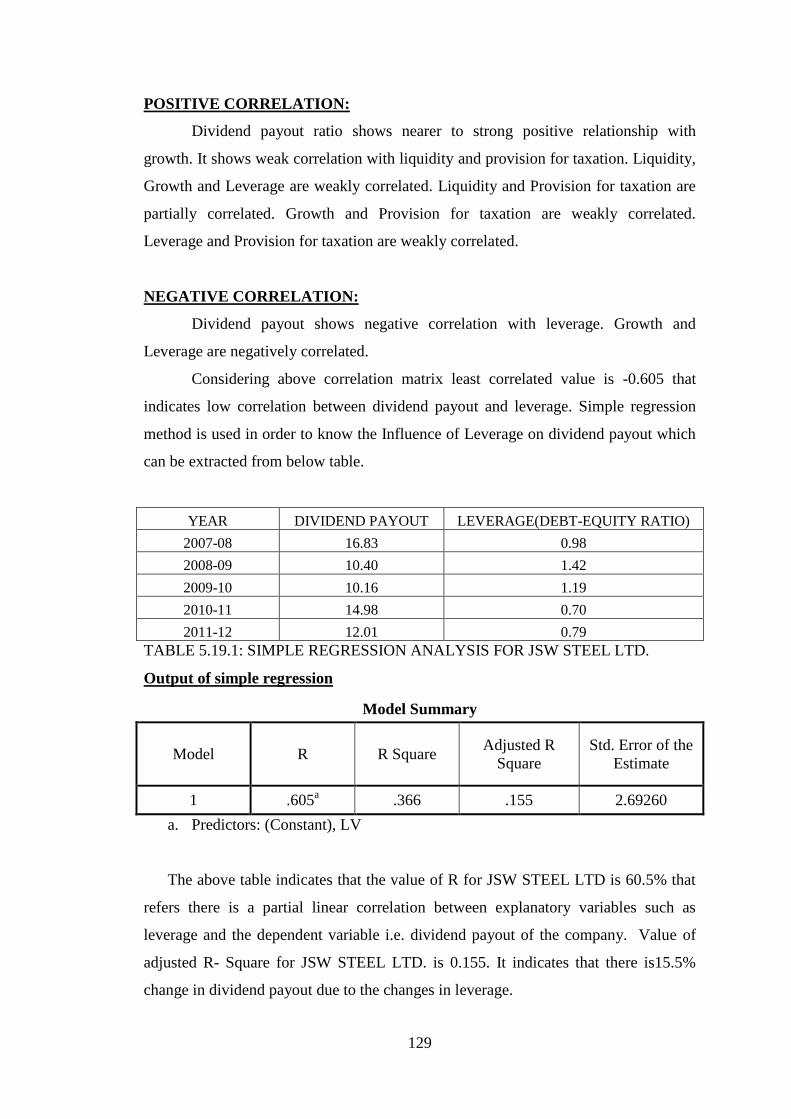

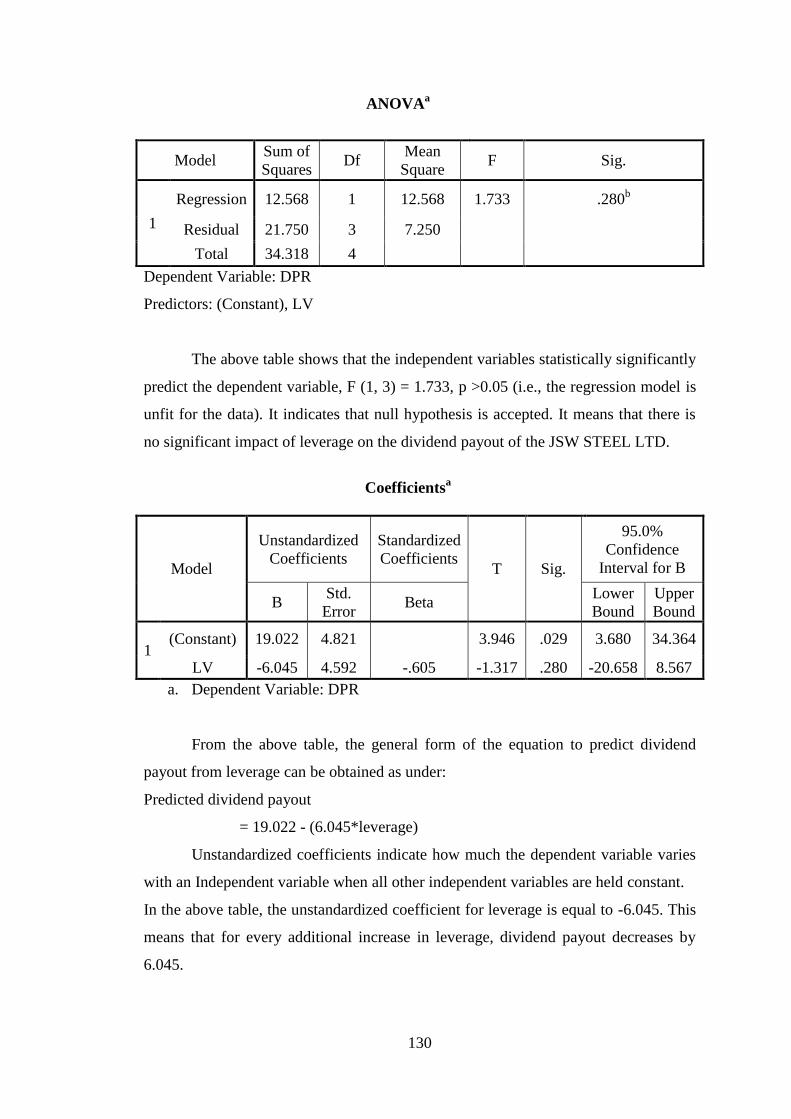

5.2.19 JSW Steel Ltd.

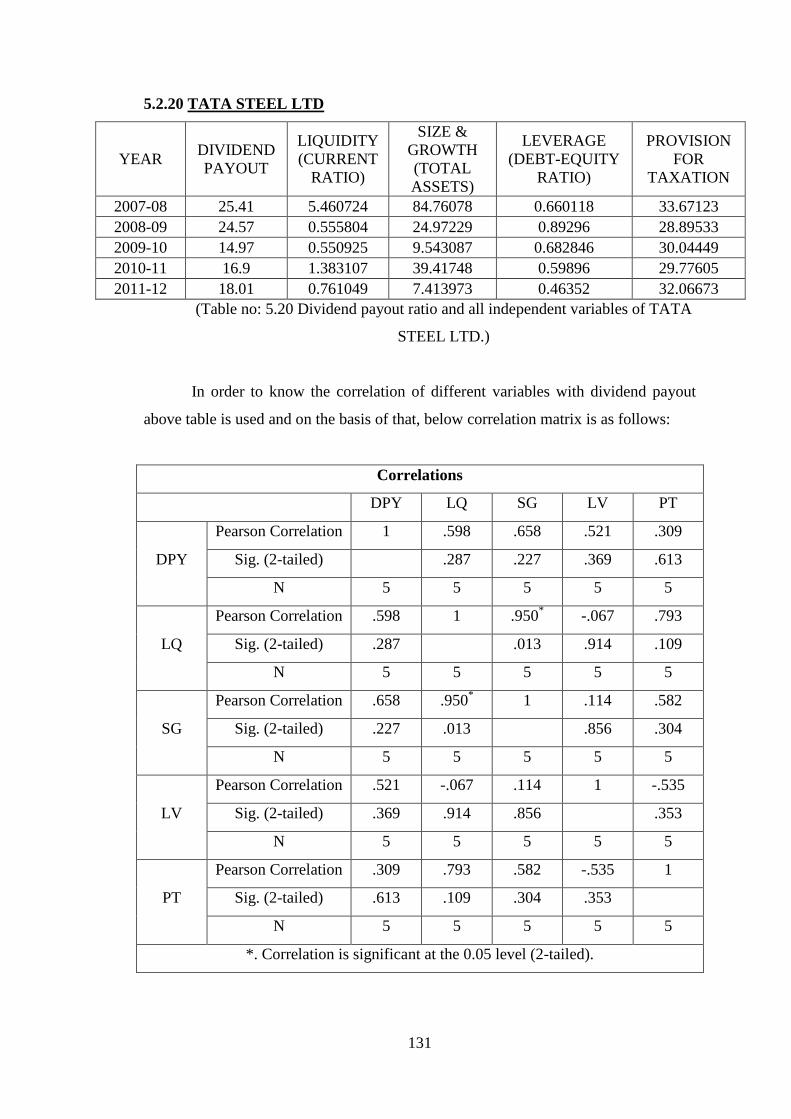

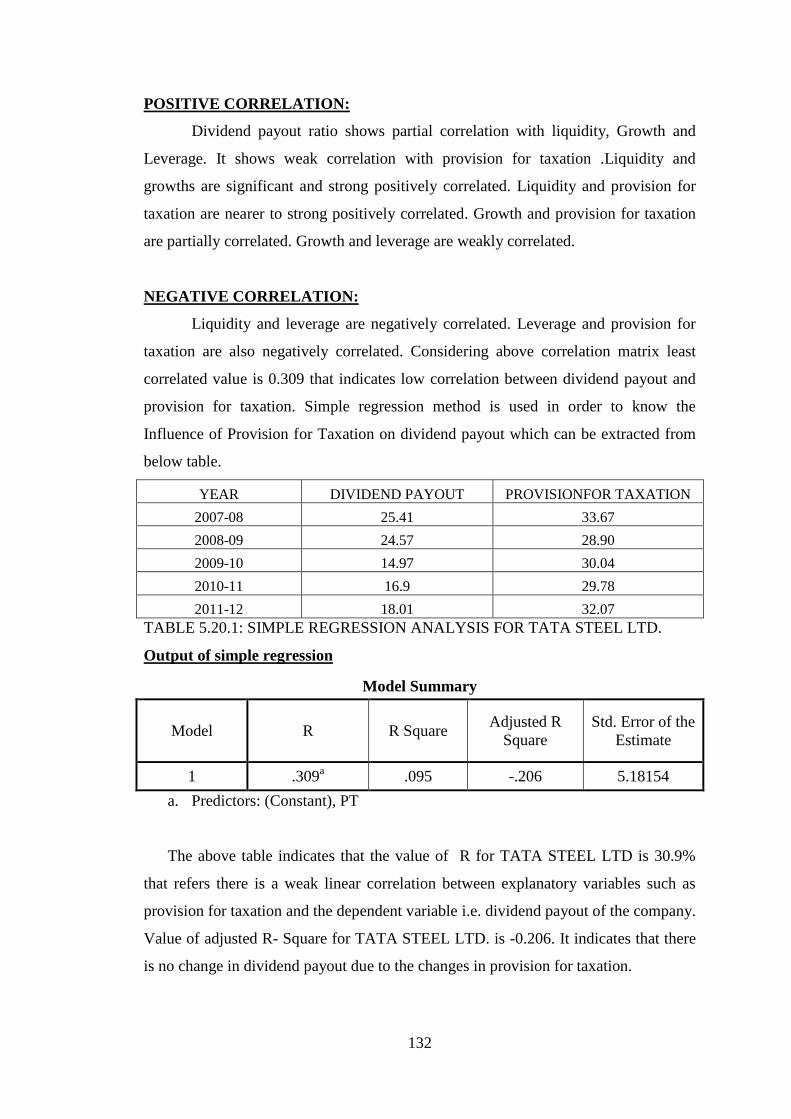

5.2.20 Tata Steel Ltd.

5.2.21 Bhushan Steel

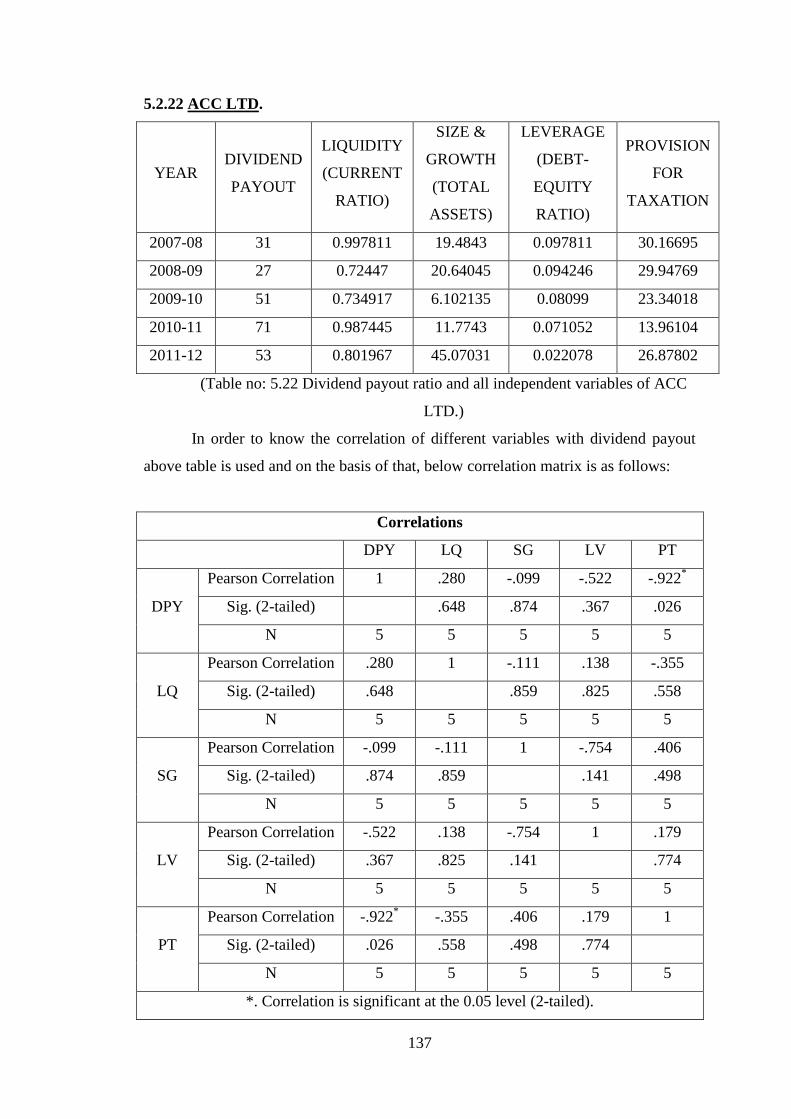

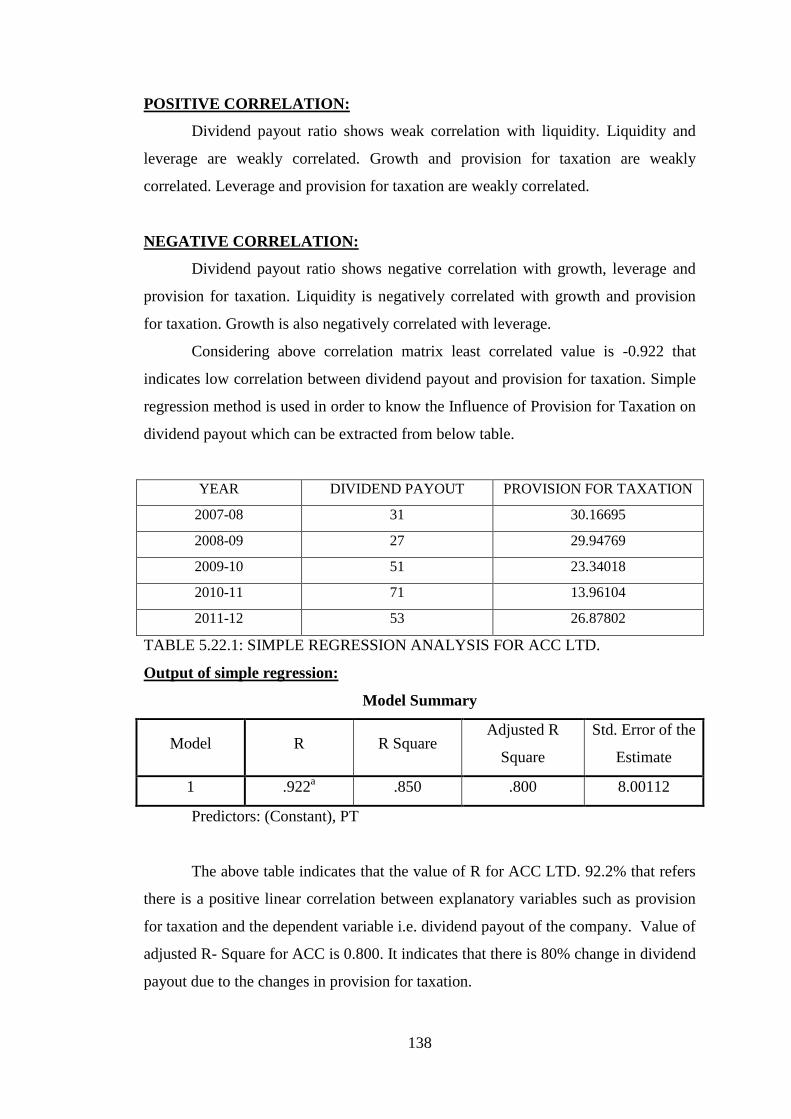

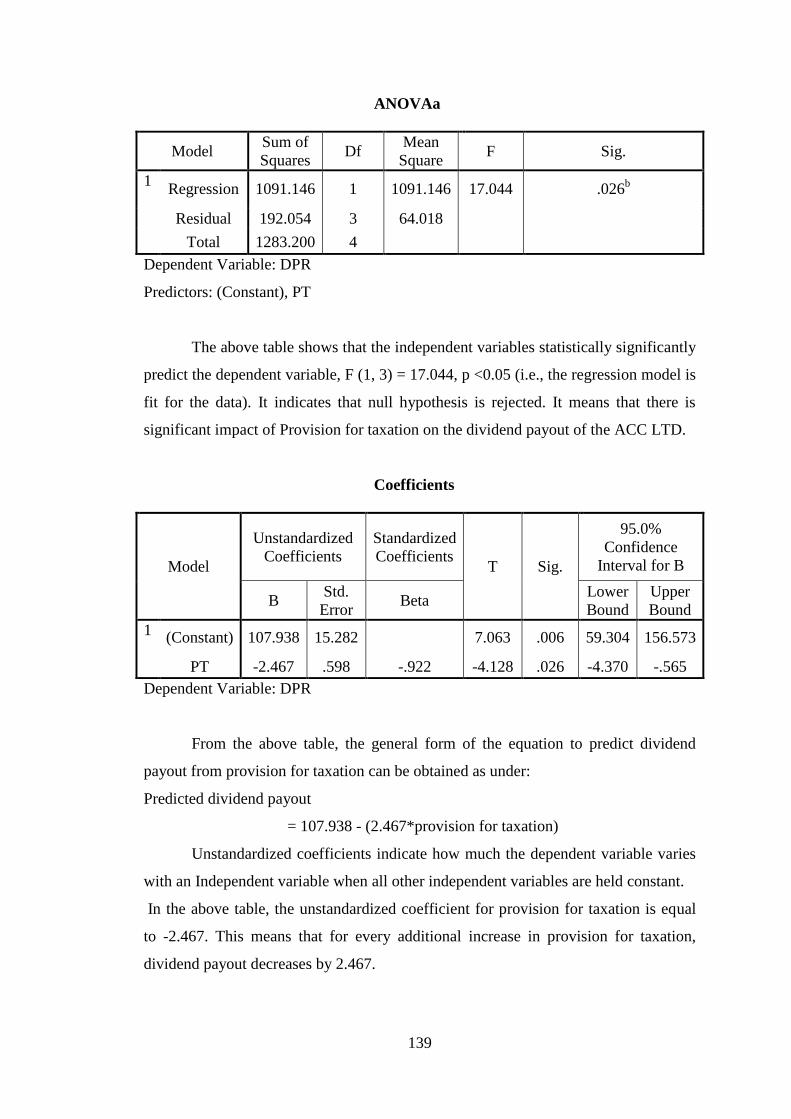

5.2.22 ACC Ltd.

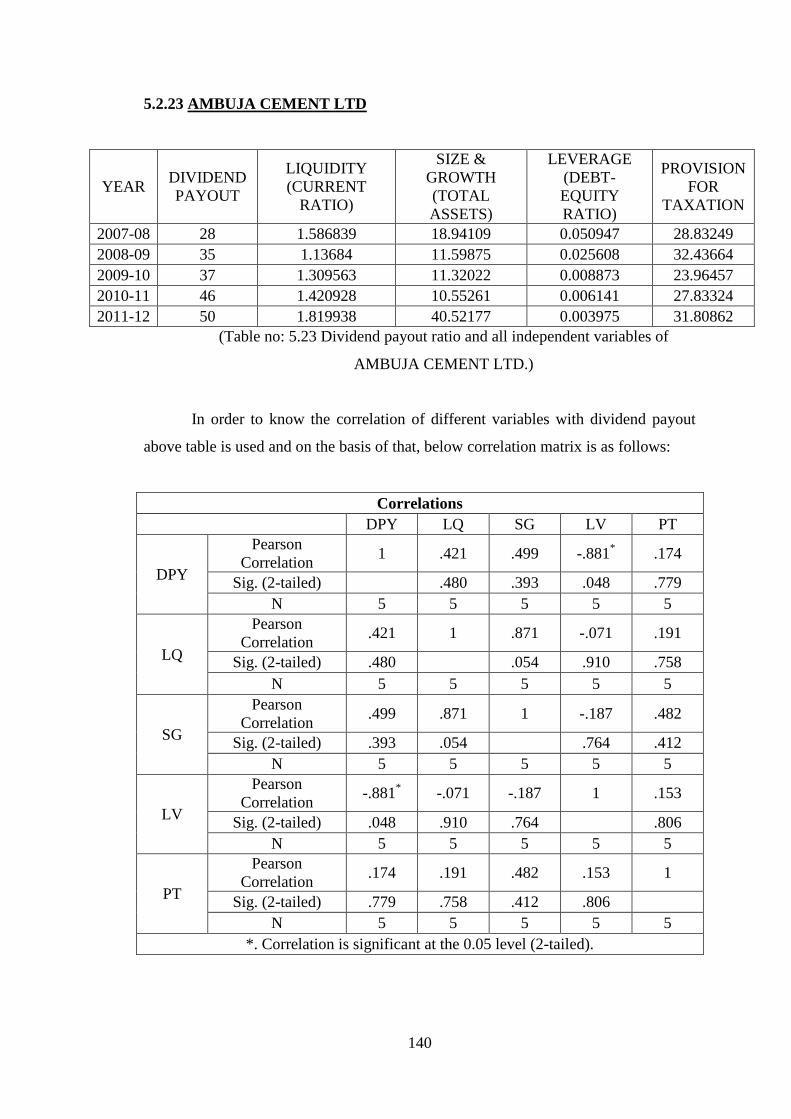

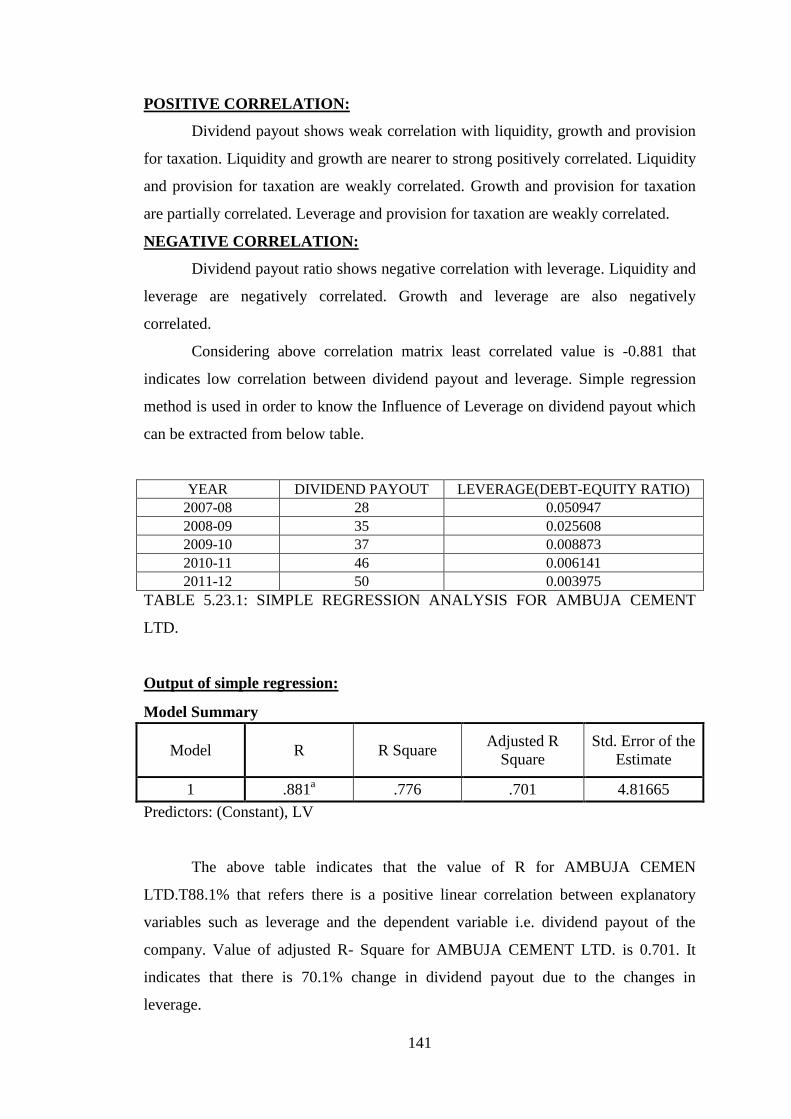

5.2.23 Ambuja Cement Ltd.

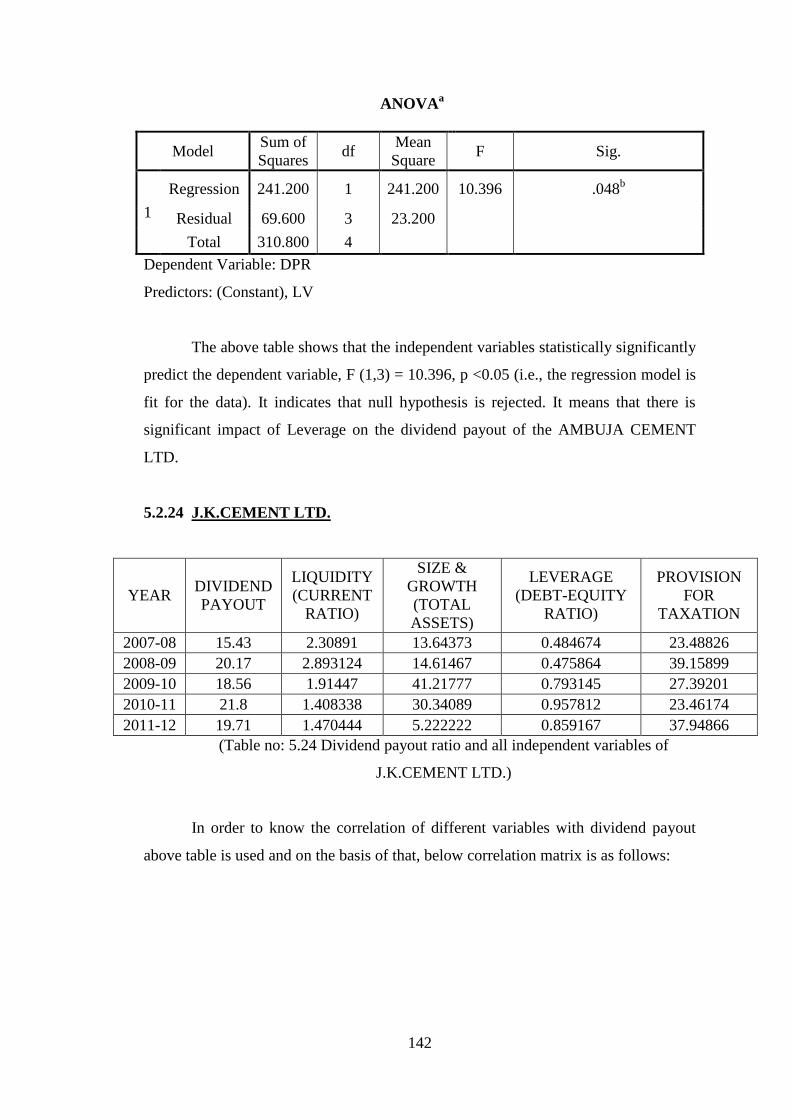

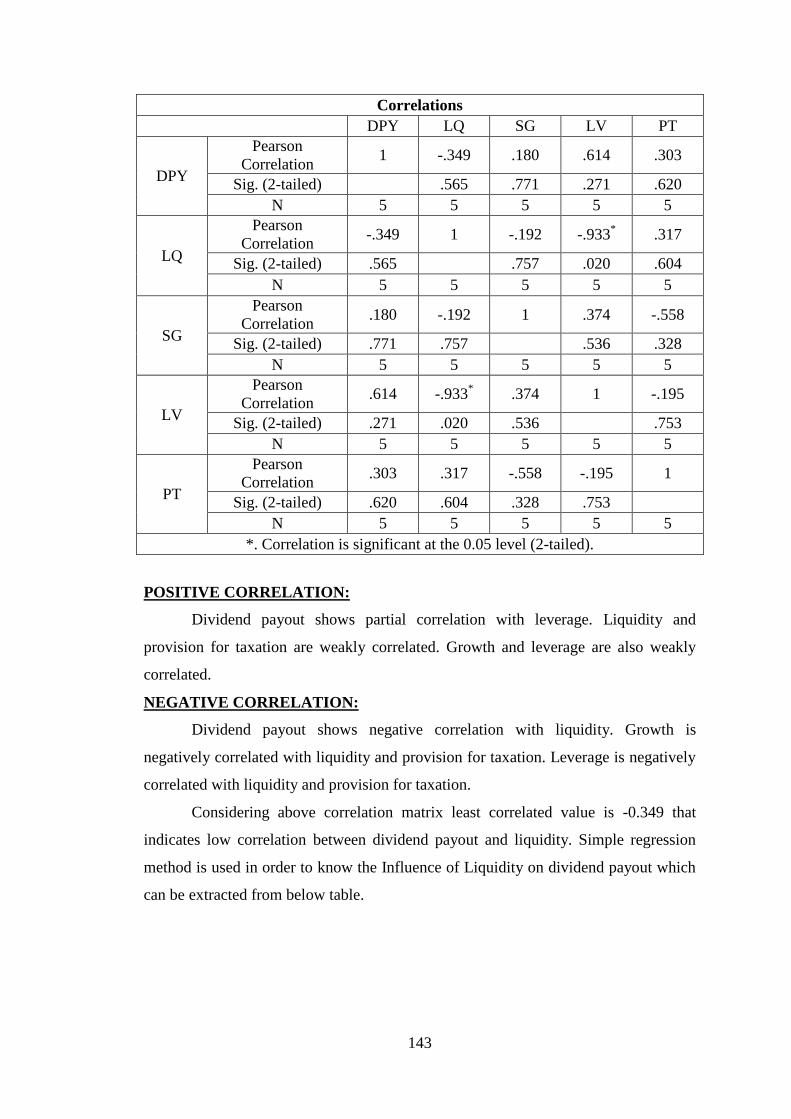

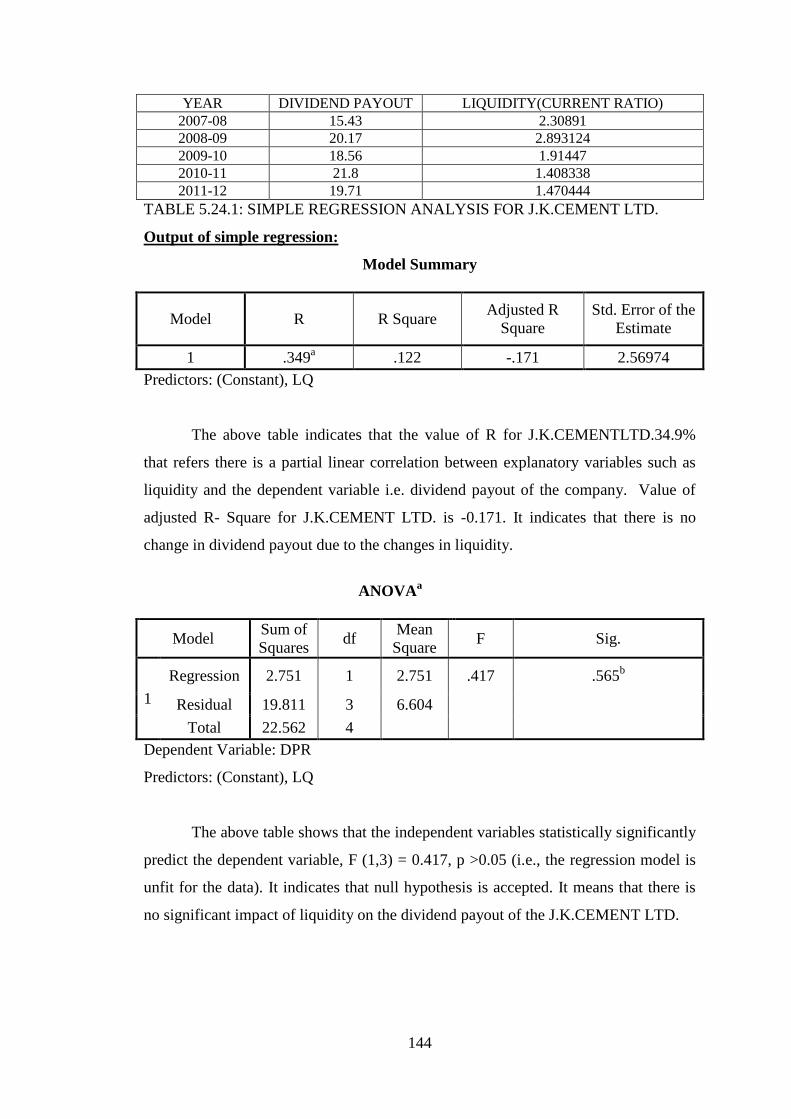

5.2.24 J.K.Cement Ltd.

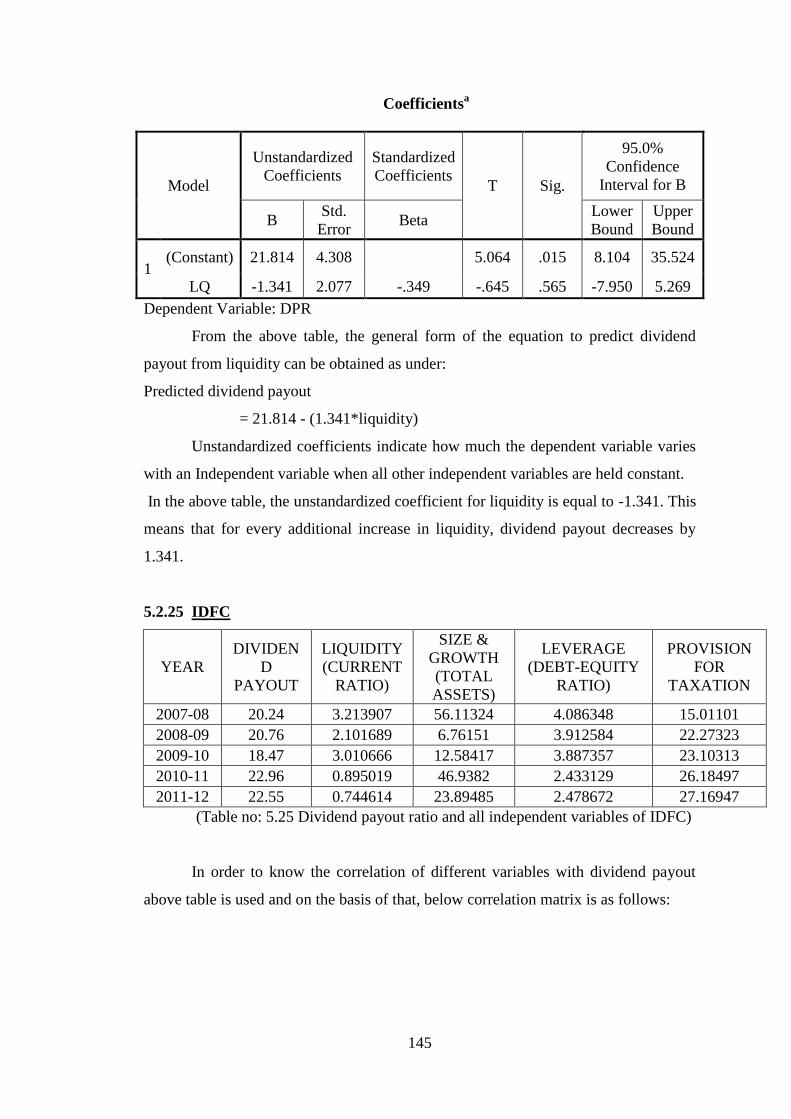

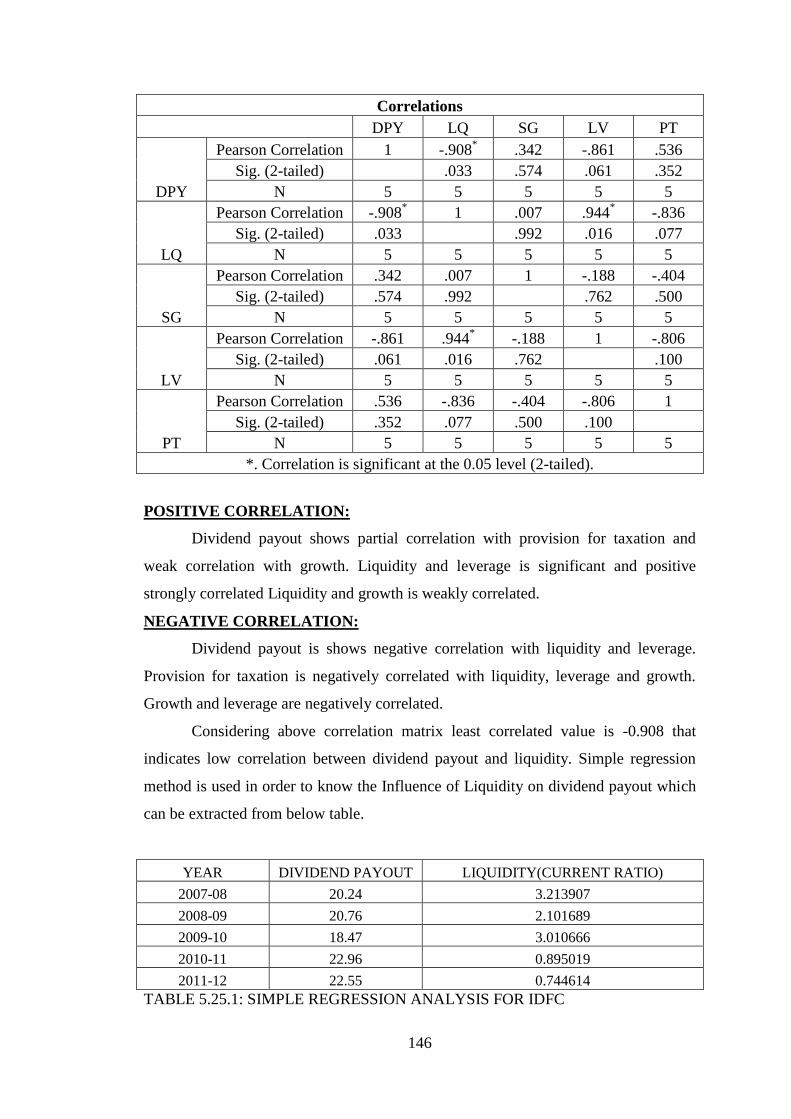

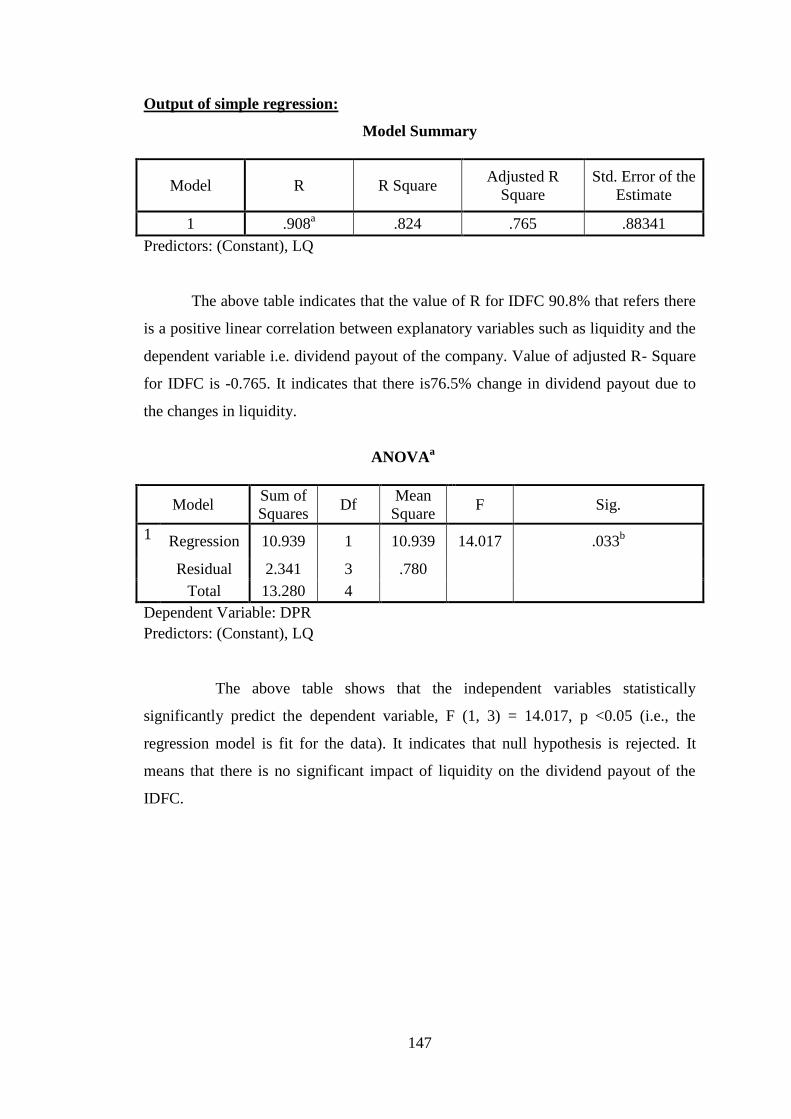

5.2.25 IDFC

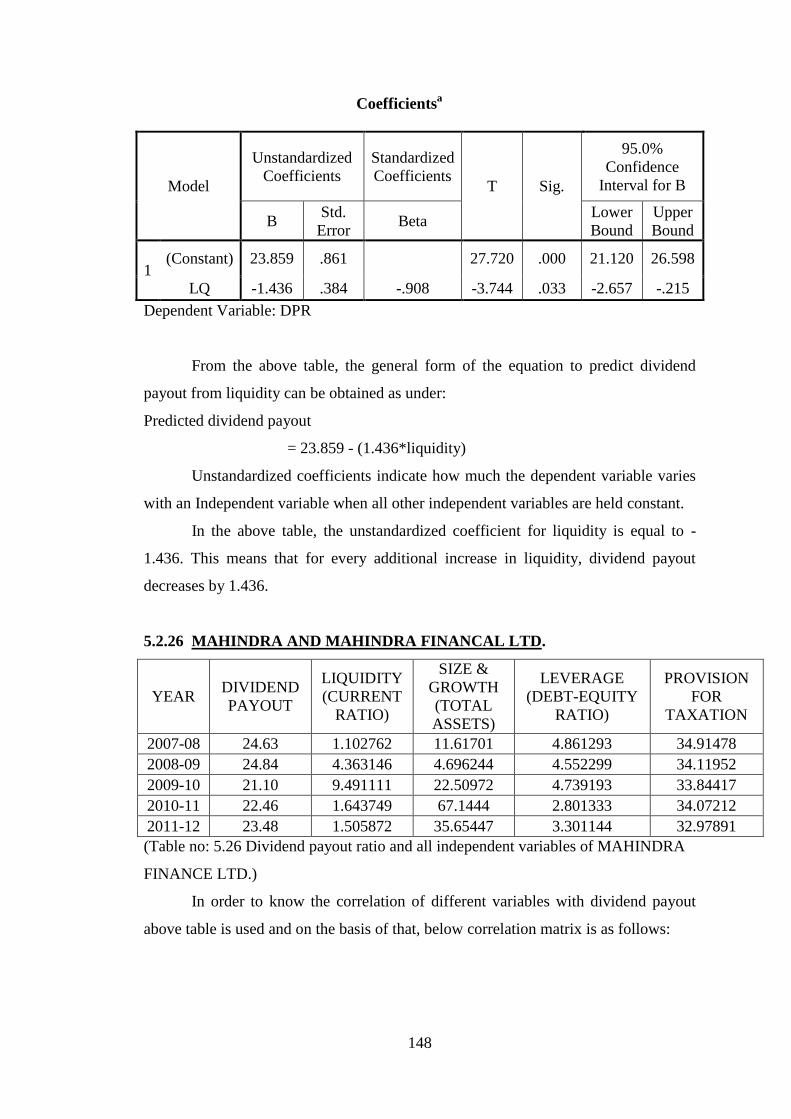

5.2.26 Mahindra and Mahindra Financial Ltd.

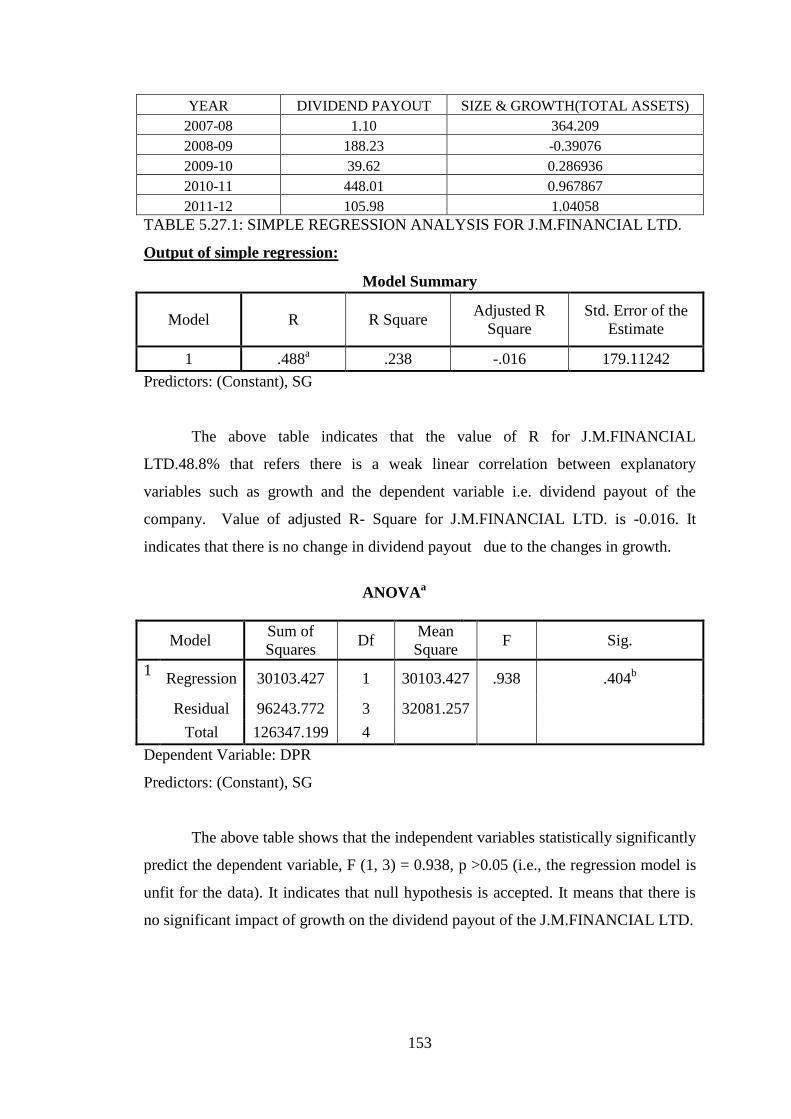

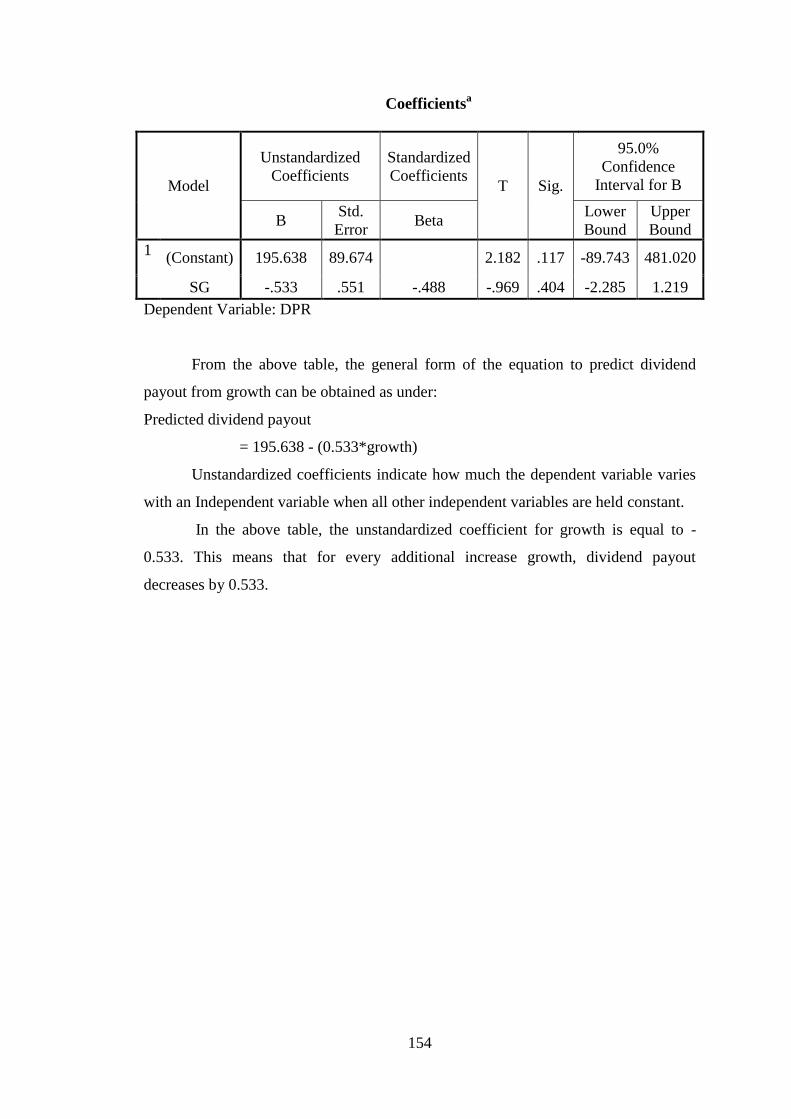

5.2.27 J.M.Financial Ltd.

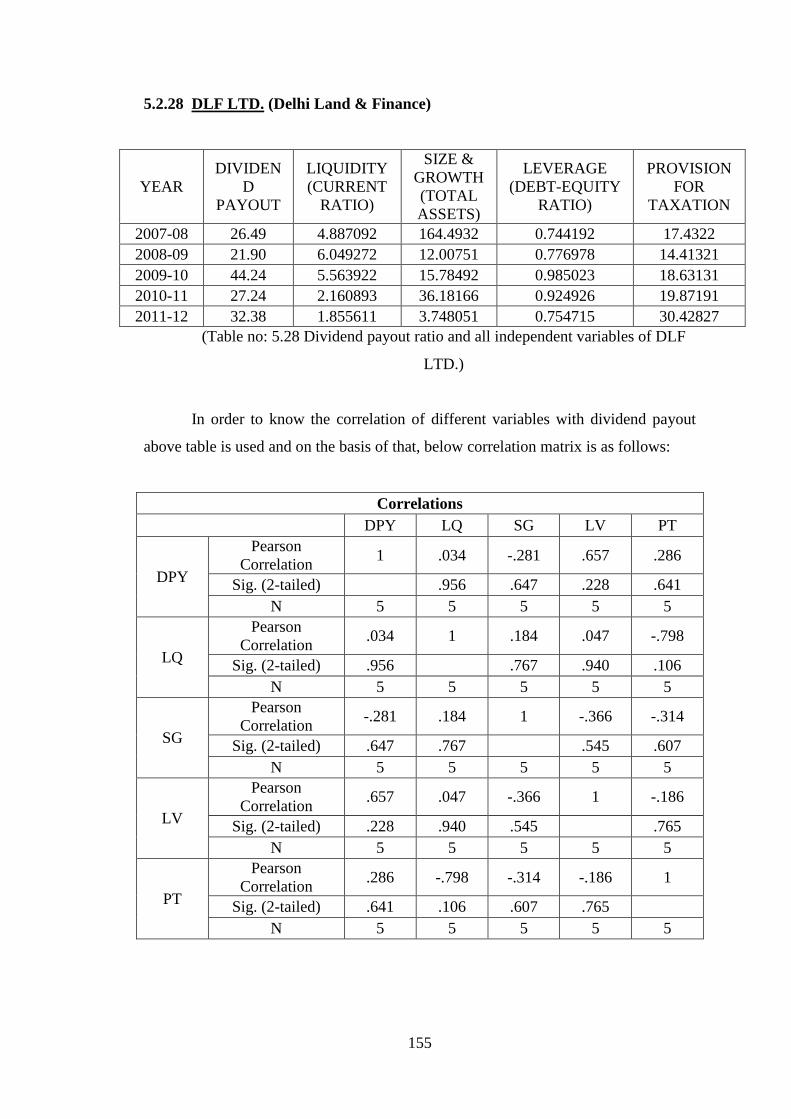

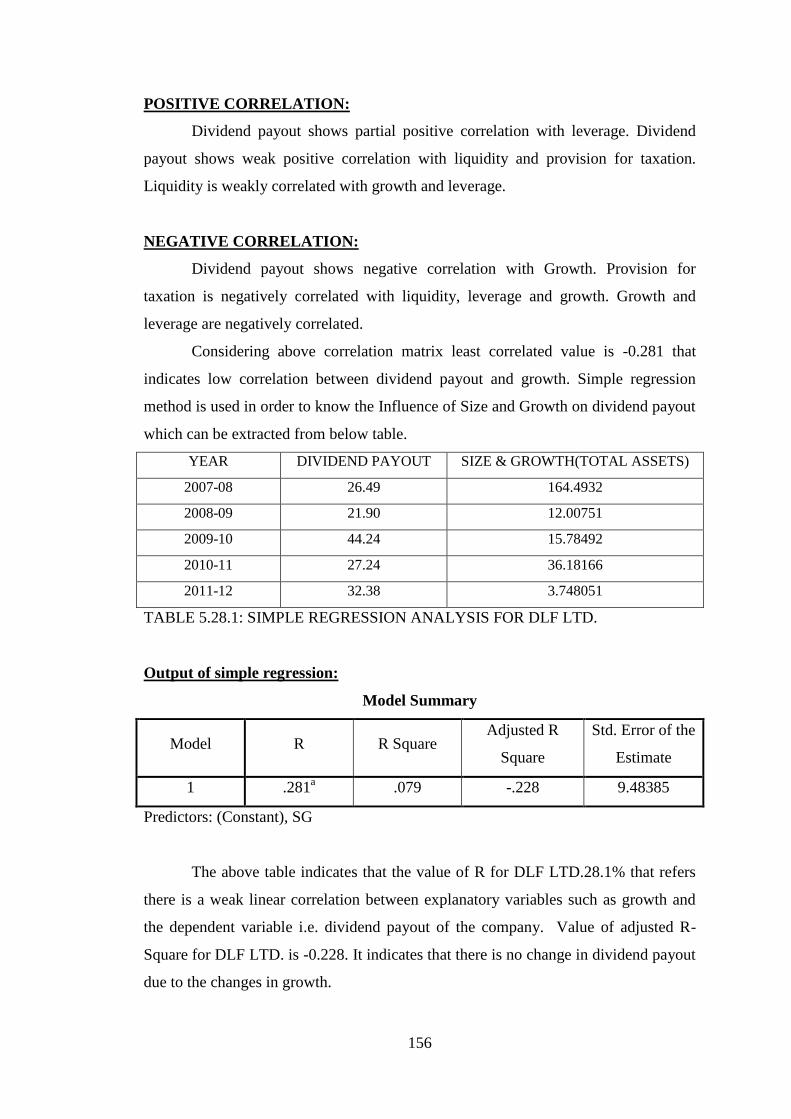

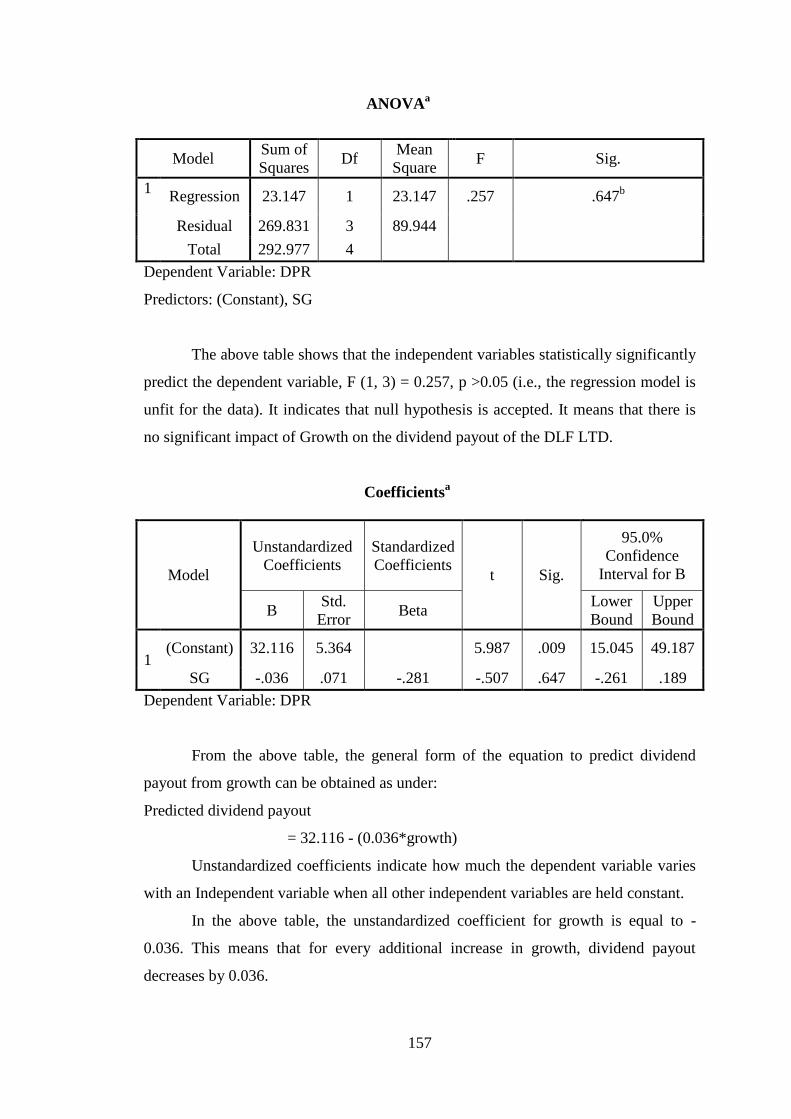

5.2.28 DLF Ltd.

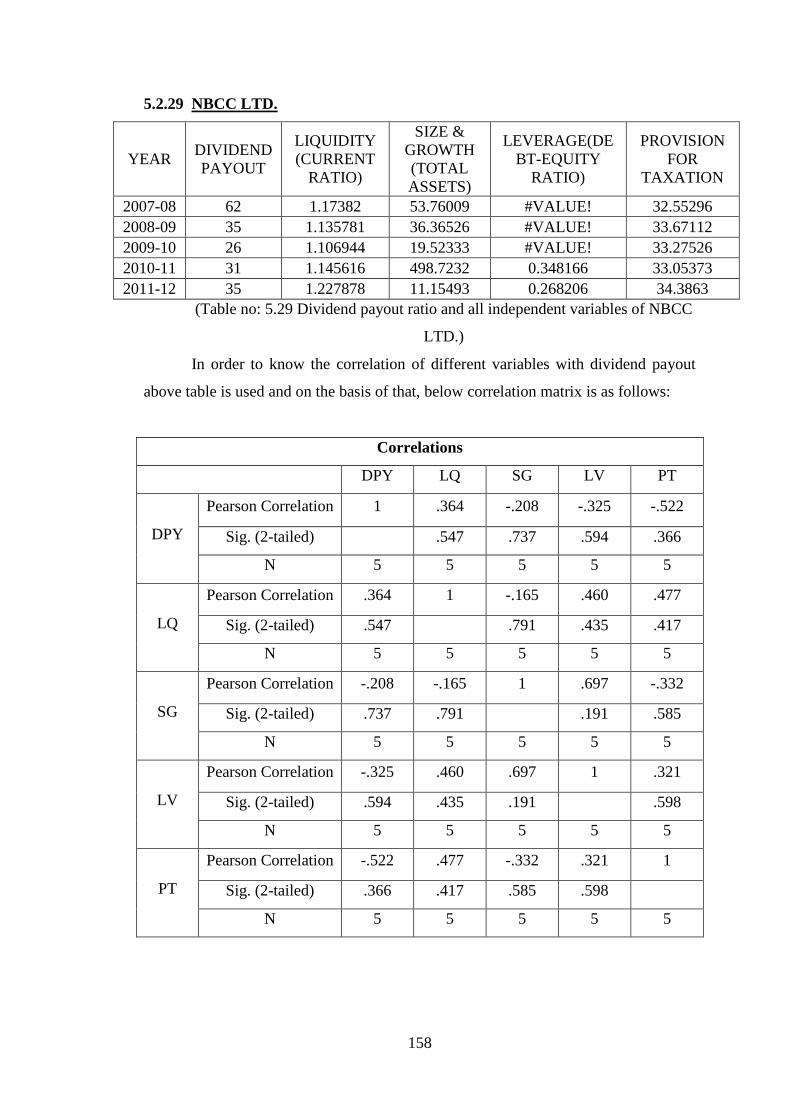

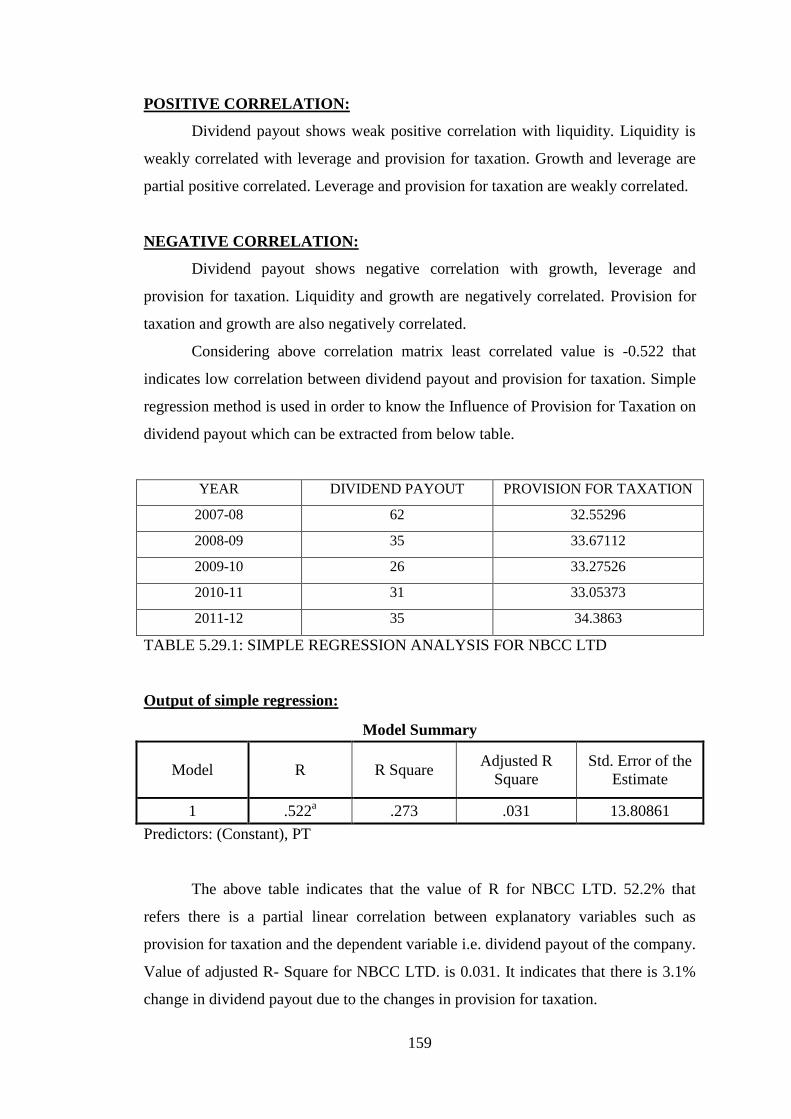

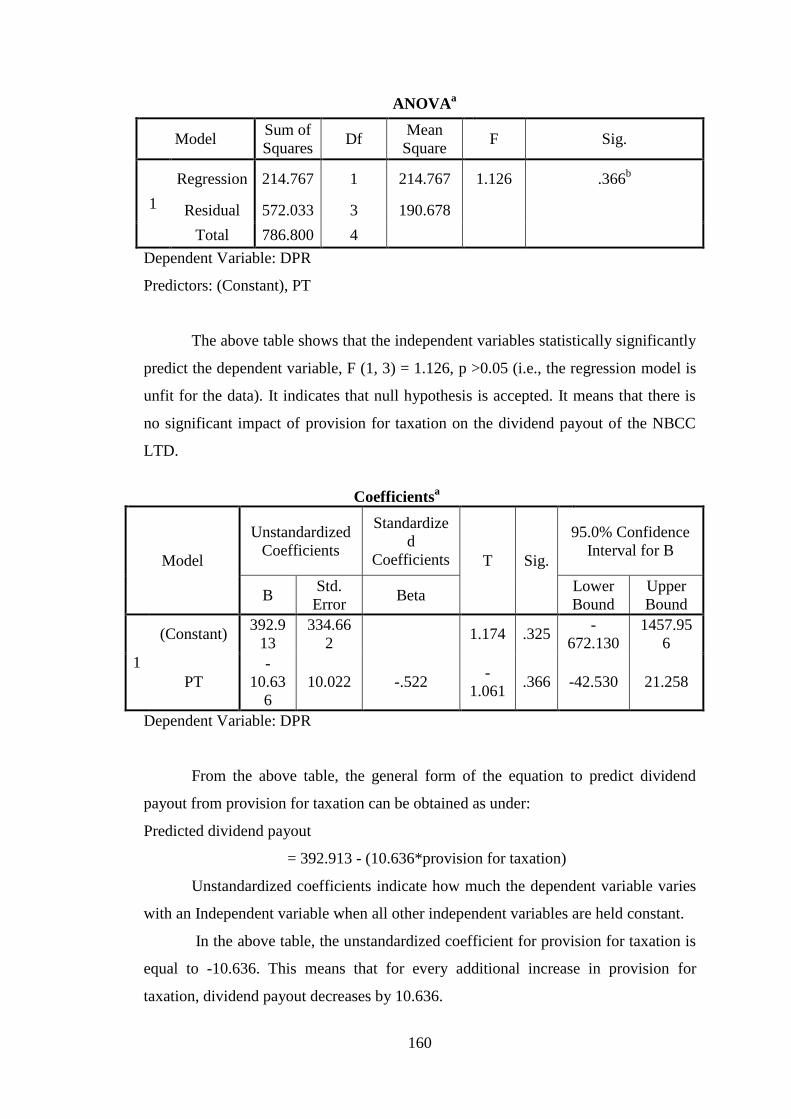

5.2.29 NBCC Ltd.

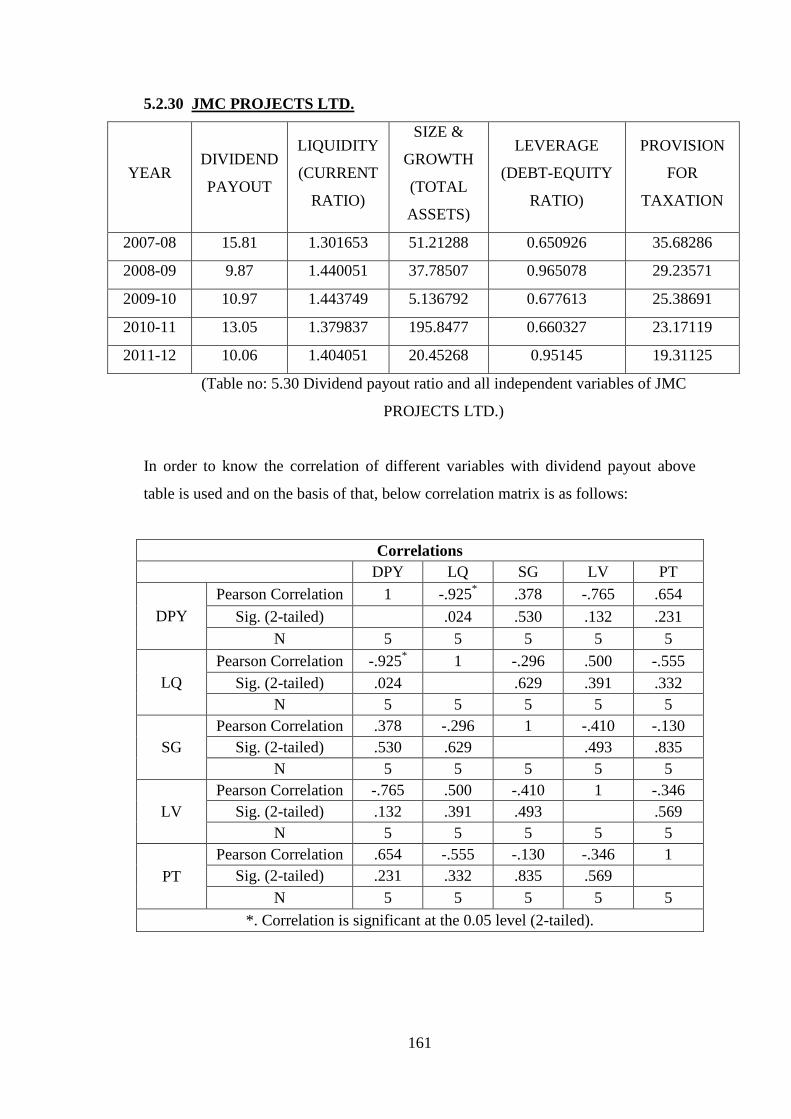

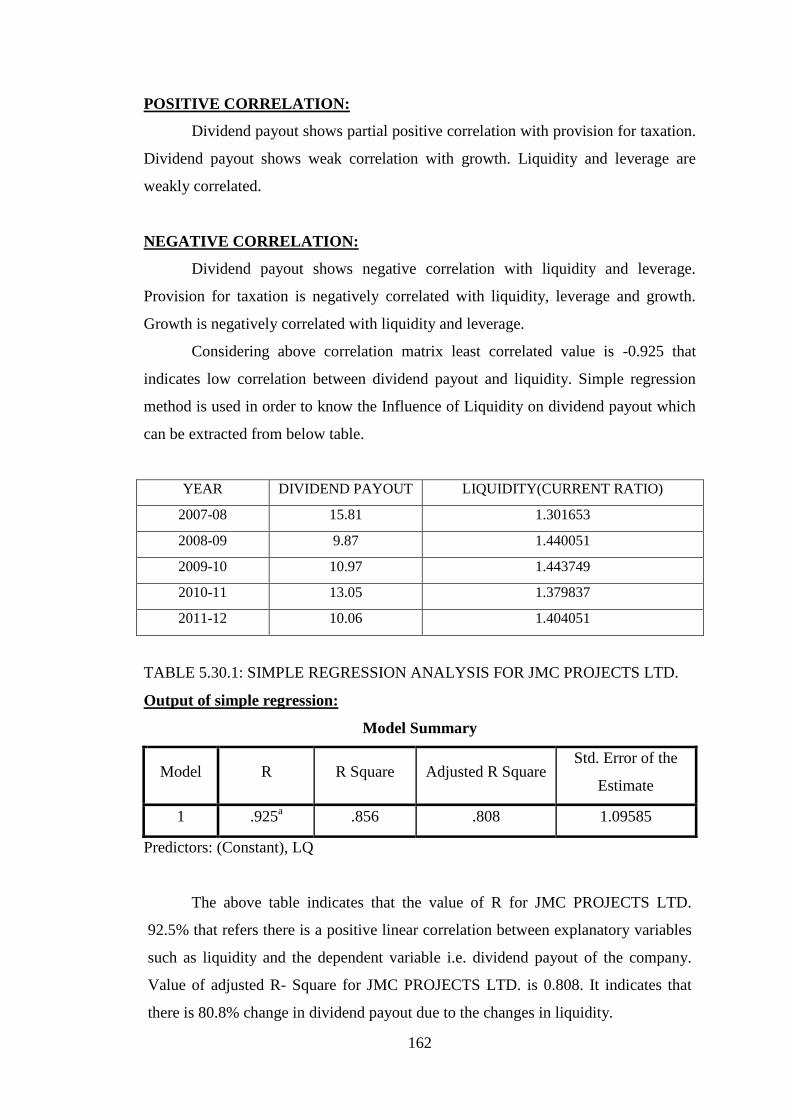

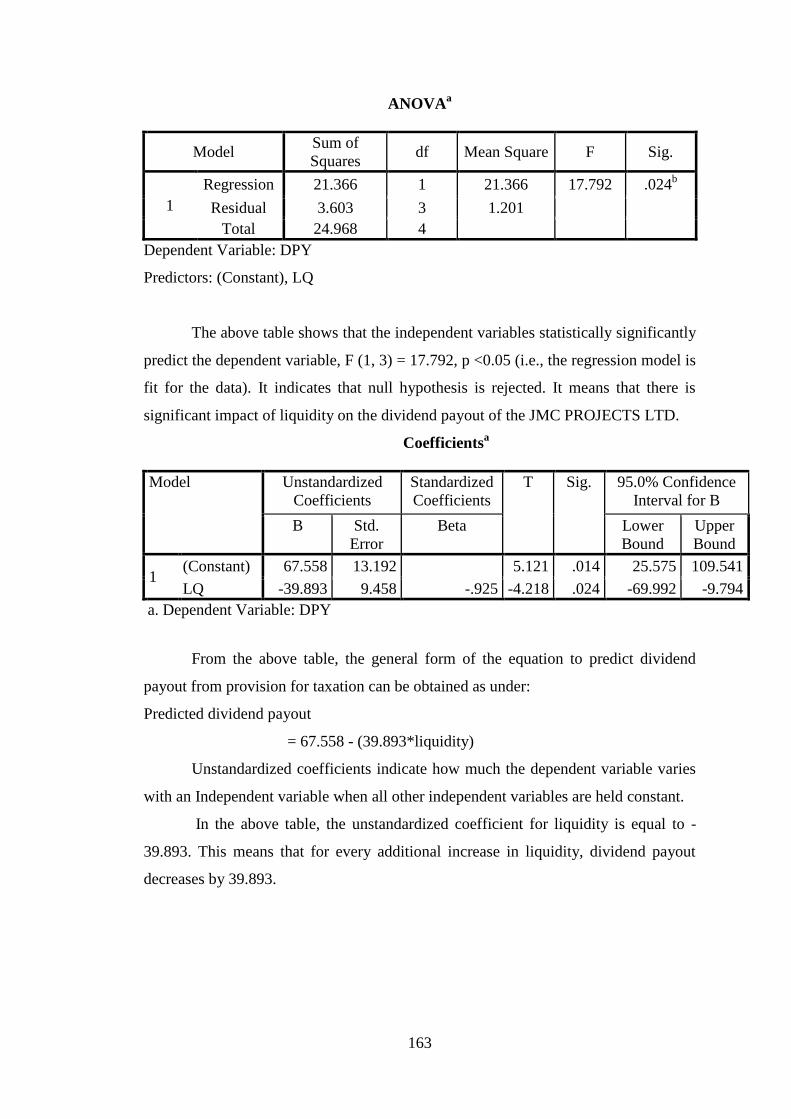

5.2.30 JMC Projects Ltd.

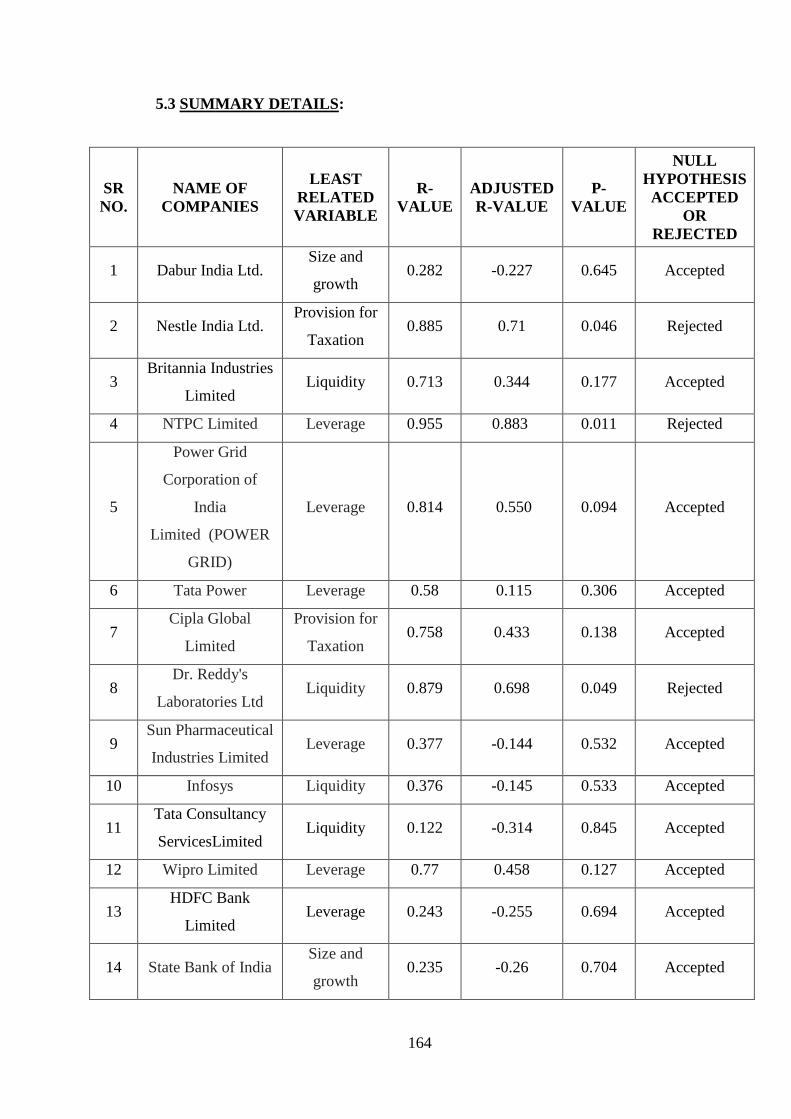

5.3 Summary Details

69

5.1 INTRODUCTION

A number of researchers have advanced theories and provided empirical

evidence regarding determinants of a firm’s dividend policy. The dividend policy

issue, however, is yet unresolved.

There are many factors that could affect a firm’s dividend payout behaviour.

According to partington,198736

these reasons include profitability, stability

of dividend payout and retained earnings, liquidity and cash flows, investment

variables and financial variables. According to Lintner,1956,Rozeff 1992,and

Barclay 1995,investment opportunities, agency costs, financial leverage, last year’s

dividend and firm size influence the dividend policy of a

company.Megginson,195737

states that there are worldwide industrial patterns in

the dividend policy and important factors affecting the dividend payouts are

regulations, industry growth rate, capital investment needs, profitability, earnings

variability and asset characteristics such as the composition of tangible and

intangible assets.

Moreover research in the past also shows that there are significant

influence of growth rate of firm, systematic risk, retained earnings, liquidity,

cash availability, provision for tax and firm size on dividend payout.

In this chapter, issues related to dividend policies have been analysed

within many framework including profitability, growth rate, liquidity, leverage

and provision for taxation etc. The major focus of the research, however is to

find out whether there is dividend policy of all companies ,to know the

relationship between the variables and with dividend payout and the technique of

correlation matrix analysis is used for the purpose, the scope, methodology used

and interpretation of the result of correlation matrix are presented after

discussion and an analysis of the impact of least related variable on the dividend

policy of a firm, that has either been made by merely observing the data of

the selected companies or hereby to go further analysis to know the extent of

impact of least correlated variable on dividend payout simple regression analysis has

been run. Based on application of correlation matrix least correlated variable has been

36

Partington, G. H. (1987). Variables influencing dividend policy in Australia:Survey Results.

Journal of Business Finance and Accounting 16, p.165-182. 37

Megginson, W. (1997). In Corporate Finance Theory,Reading,Addison-Wesley ( p.355).

70

found. Least correlated variable refers low value (correlation coefficient). The study

is based on five years data of thirty selected companies of ten industries. The

period concerned is from 2007-2012. For the purpose of simple regression

analysis, dividend payout rate, which is defined as the ratio of dividends per

share for the firms dividend policy is as under:

Dividend Payout Ratio:

It measures the relationship between dividends and earnings.i.g. What

percentage shares of dividend is to be distributed from profit. It is to be calculated,

D/P Ratio = Dividend Per Share *100

Earnings per Share

The factors or explanatory variables are considered for the study purpose

are as under:

1) Liquidity:

Although dividend is related to earnings, the actual payment of dividend is

made from available cash. Thus, liquidity always plays an important role in any cash

payment by a firm. This usually happens in case of high growth firms or firm which

requires more funds for expansion purposes, which have very low liquidity because of

substantial investment like profitability, liquidity etc. Also has positive relationship

with dividend. Hence, greater the cash position and overall liquidity of a company,

greater is the ability to pay dividend.

The Current-Ratio is one of the best-known measures of financial strength and

liquidity. It is calculated as shown below:

Current-Ratio = Total Current-Assets

Total Current-Liabilities

2) Size and Growth:

Jahera, Lioud and Modani (1986) 38

find that size is the major factor that

determines a company’s policy. Big companies are usually in mature industries with

higher credit levels. Therefore, due to the fact that the cost of dividend policy is

relatively large companies have a stable dividend policy and moreover have a higher

payout than small companies. In order to study the influence of size on dividend.

Various measures such as Total Assets, Paid-up Capital, and Net worth etc. have been

38

Jahera, J. L. (1986). Growth,Beta and Agency Costs as Determinants of Dividend. Akron Business

and Economic Review 17, p.55-69.

71

used by researchers to represent size. James Bales said that many arguments may be

advanced against the use of any of the above measures for size. So, no measures are

perfect. Moreover, since all the above mentioned measures are correlated to each

other any measures may be used. Larger firms should be able to pay higher dividends.

Therefore expect to see the positive relationship between size and dividend payment.

Higher Growth companies have lots of investment opportunities and are likely to

pay low dividends because they have profitable uses for the capital. Therefore, high

growth companies prefer to capitalize on their favourable investment prospects and

have clear disincentive’s in paying operating cash flows and profits as

dividends.(Gaver and Gavert,1993)39

this ratio indicates the rate of growth of the total

assets in the business and is expressed in percentage.

3) Leverage:

A firm with large amounts of debts will follow a more conservative dividend

policy. The reason is that if a firm has relatively high financial leverage, its

dependence on external finance is increased. Therefore, such firms’ pay low

dividends to avoid borrowing i.e. a firm with higher leverage will pay a lower

fraction of earnings in order to lower its dependence on external financing leverage

can be calculated by Debt/Equity Ratio. The Debt/Equity or Leverage Ratio indicates

the extent to which the business is reliant on debt financing.

Debt/Equity Ratio =Long-term funds/Shareholder’s fund

4) Provision for Taxation:

In India, dividends were taxed in the hands of investors. Since investor did not

give significance to tax matter individual tax rates were irrelevant while determining

dividend policy in the Indian context. However, shareholders in the high tax bracket

may have preferred dividend income rather than capital gains. This is because, though

dividend income for the individual was free, capital gains are taxable in India.

Under the Finance Act 199740

, no tax was payable on dividends by a company

and consequently there was no withholding tax on dividends paid by a company to its

shareholders. However, a company declaring a dividend was required to pay income-

tax at the rate of 10% on the amount of dividend distributed. If, tax on dividends is

39

Gaver, J. a. (1993). Additional Evidence on the Association between Investment Opportunity Set

and Corporate Financing,Dividend and Compensation plocies . Journal of Accounting and

Economics, p.185-209 40

T.N.Pandey,Budget 1997:New Tax Concept Relating to Dividend Income, Chartered Secretary,

April 1997,p.365-366

72

viewed from point of view of the corporate sector, they have to pay dividend tax and

changes individual tax rates may influence the company’s dividend policy. For

Example, a cut in dividend tax from 20% to 10% on the dividend declared by

companies had been viewed as positive.

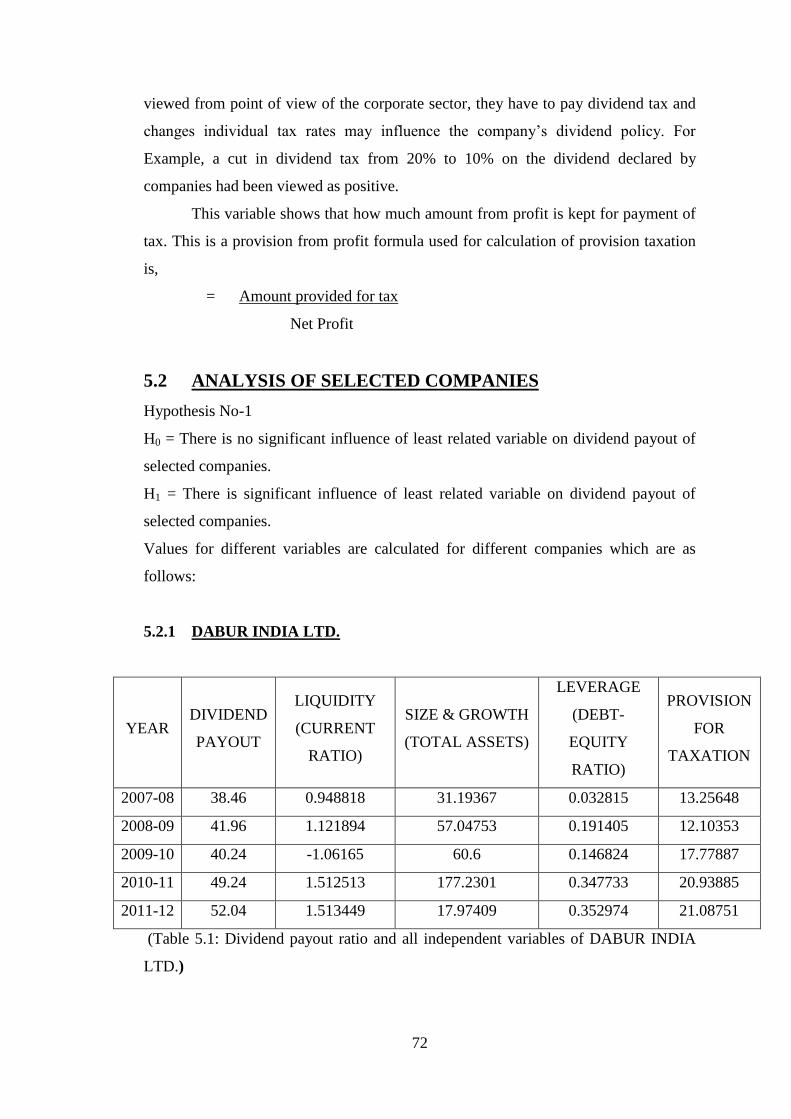

This variable shows that how much amount from profit is kept for payment of

tax. This is a provision from profit formula used for calculation of provision taxation

is,

= Amount provided for tax

Net Profit

5.2 ANALYSIS OF SELECTED COMPANIES

Hypothesis No-1

H0 = There is no significant influence of least related variable on dividend payout of

selected companies.

H1 = There is significant influence of least related variable on dividend payout of

selected companies.

Values for different variables are calculated for different companies which are as

follows:

5.2.1 DABUR INDIA LTD.

YEAR DIVIDEND

PAYOUT

LIQUIDITY

(CURRENT

RATIO)

SIZE & GROWTH

(TOTAL ASSETS)

LEVERAGE

(DEBT-

EQUITY

RATIO)

PROVISION

FOR

TAXATION

2007-08 38.46 0.948818 31.19367 0.032815 13.25648

2008-09 41.96 1.121894 57.04753 0.191405 12.10353

2009-10 40.24 -1.06165 60.6 0.146824 17.77887

2010-11 49.24 1.512513 177.2301 0.347733 20.93885

2011-12 52.04 1.513449 17.97409 0.352974 21.08751

(Table 5.1: Dividend payout ratio and all independent variables of DABUR INDIA

LTD.)

73

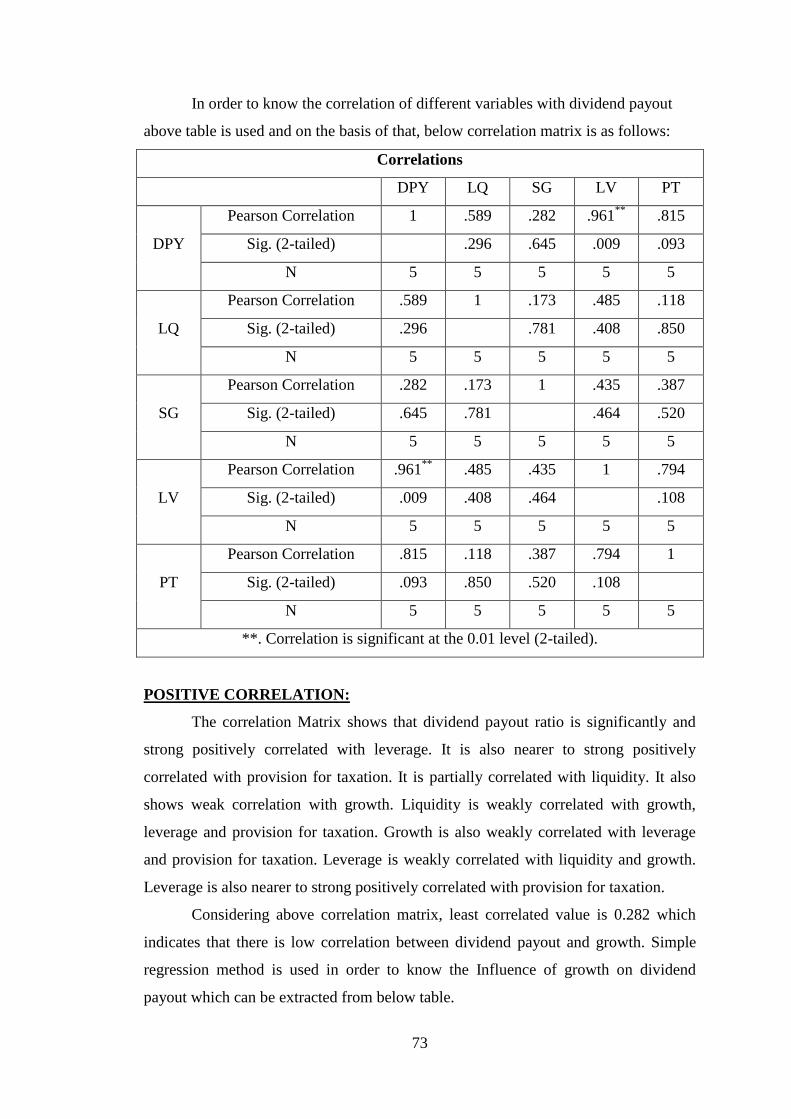

In order to know the correlation of different variables with dividend payout

above table is used and on the basis of that, below correlation matrix is as follows:

Correlations

DPY LQ SG LV PT

DPY

Pearson Correlation 1 .589 .282 .961**

.815

Sig. (2-tailed)

.296 .645 .009 .093

N 5 5 5 5 5

LQ

Pearson Correlation .589 1 .173 .485 .118

Sig. (2-tailed) .296

.781 .408 .850

N 5 5 5 5 5

SG

Pearson Correlation .282 .173 1 .435 .387

Sig. (2-tailed) .645 .781

.464 .520

N 5 5 5 5 5

LV

Pearson Correlation .961**

.485 .435 1 .794

Sig. (2-tailed) .009 .408 .464

.108

N 5 5 5 5 5

PT

Pearson Correlation .815 .118 .387 .794 1

Sig. (2-tailed) .093 .850 .520 .108

N 5 5 5 5 5

**. Correlation is significant at the 0.01 level (2-tailed).

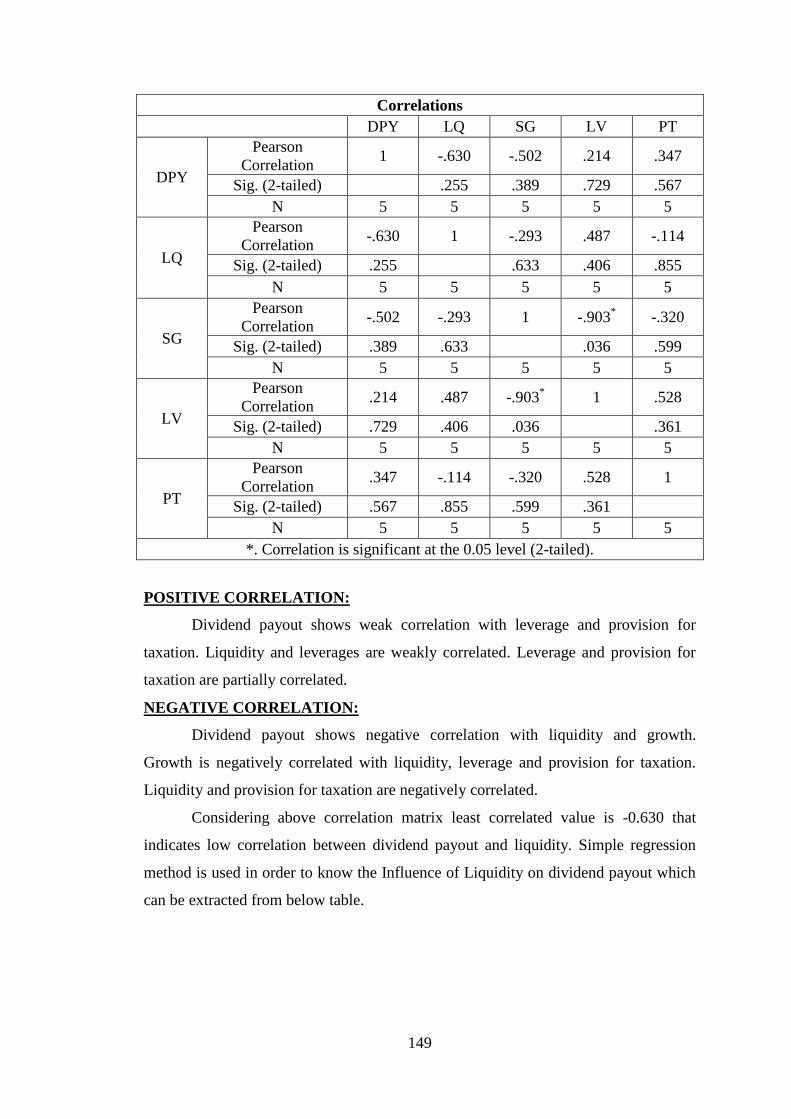

POSITIVE CORRELATION:

The correlation Matrix shows that dividend payout ratio is significantly and

strong positively correlated with leverage. It is also nearer to strong positively

correlated with provision for taxation. It is partially correlated with liquidity. It also

shows weak correlation with growth. Liquidity is weakly correlated with growth,

leverage and provision for taxation. Growth is also weakly correlated with leverage

and provision for taxation. Leverage is weakly correlated with liquidity and growth.

Leverage is also nearer to strong positively correlated with provision for taxation.

Considering above correlation matrix, least correlated value is 0.282 which

indicates that there is low correlation between dividend payout and growth. Simple

regression method is used in order to know the Influence of growth on dividend

payout which can be extracted from below table.

74

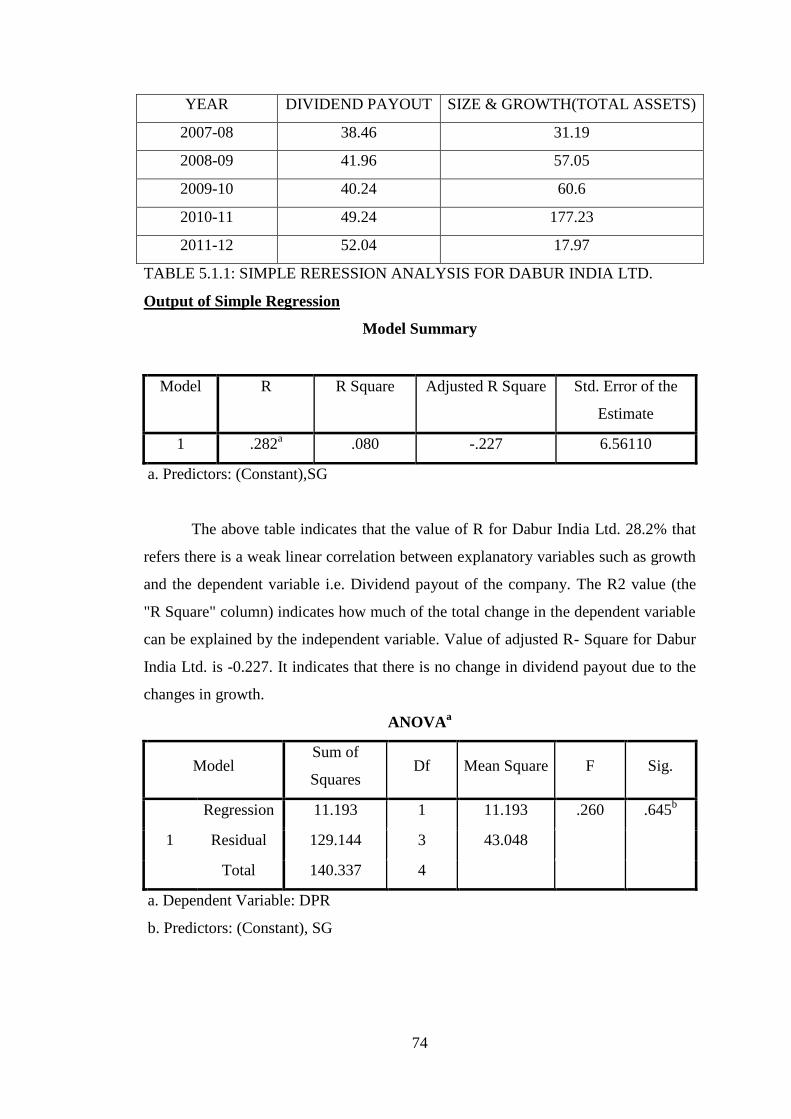

YEAR DIVIDEND PAYOUT SIZE & GROWTH(TOTAL ASSETS)

2007-08 38.46 31.19

2008-09 41.96 57.05

2009-10 40.24 60.6

2010-11 49.24 177.23

2011-12 52.04 17.97

TABLE 5.1.1: SIMPLE RERESSION ANALYSIS FOR DABUR INDIA LTD.

Output of Simple Regression

Model Summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .282a .080 -.227 6.56110

a. Predictors: (Constant),SG

The above table indicates that the value of R for Dabur India Ltd. 28.2% that

refers there is a weak linear correlation between explanatory variables such as growth

and the dependent variable i.e. Dividend payout of the company. The R2 value (the

"R Square" column) indicates how much of the total change in the dependent variable

can be explained by the independent variable. Value of adjusted R- Square for Dabur

India Ltd. is -0.227. It indicates that there is no change in dividend payout due to the

changes in growth.

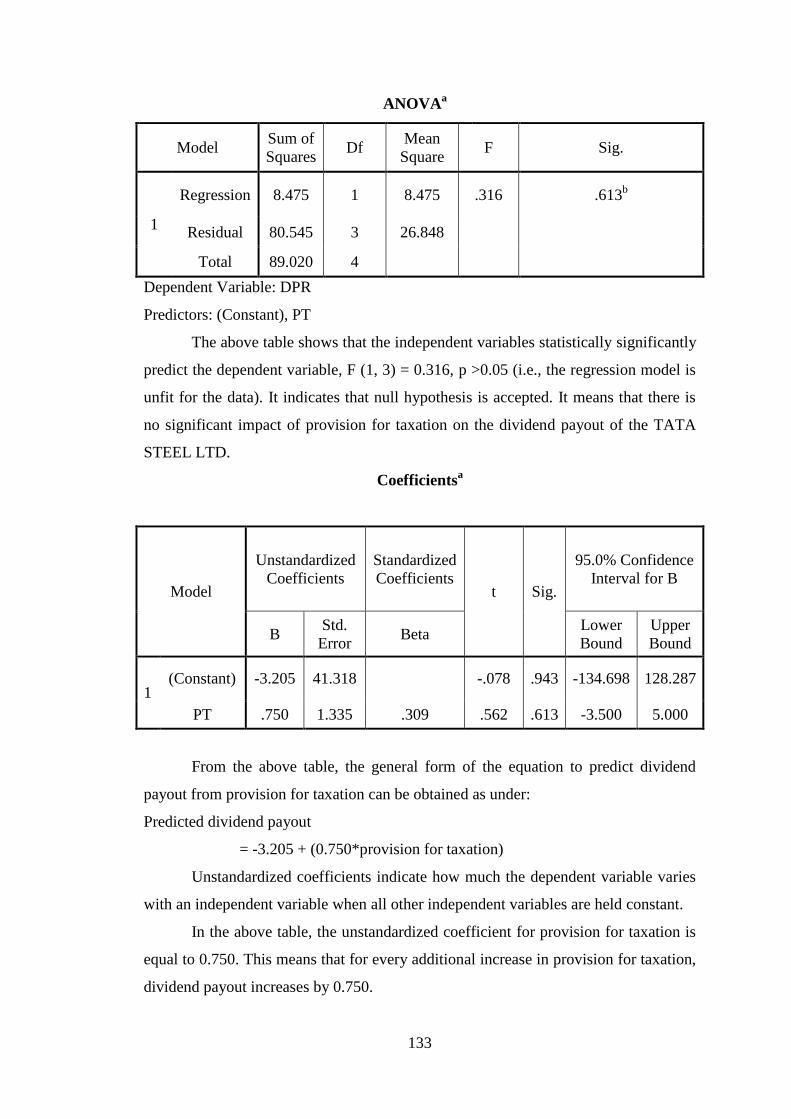

ANOVAa

Model Sum of

Squares Df Mean Square F Sig.

1

Regression 11.193 1 11.193 .260 .645b

Residual 129.144 3 43.048

Total 140.337 4

a. Dependent Variable: DPR

b. Predictors: (Constant), SG

75

The F-ratio in the ANOVA table tests whether the overall regression model is

a good fit for the data. The above table shows that the independent variables

statistically significantly predict the dependent variable, F (1, 3) = 0.260, p >0.05 (i.e.,

the regression model is unfit for the data). It indicates that null hypothesis is accepted.

It means that there is no significant impact of size and growth on the dividend payout

for Dabur Company.

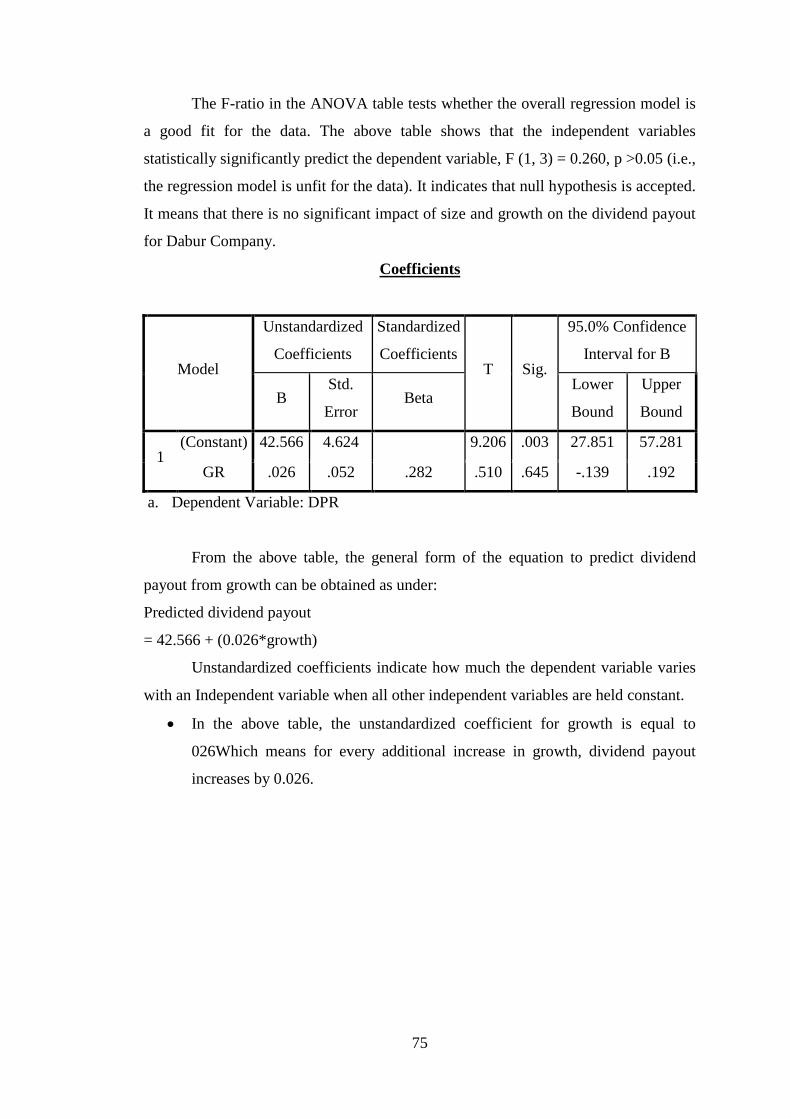

Coefficients

Model

Unstandardized

Coefficients

Standardized

Coefficients T Sig.

95.0% Confidence

Interval for B

B Std.

Error Beta

Lower

Bound

Upper

Bound

1 (Constant) 42.566 4.624 9.206 .003 27.851 57.281

GR .026 .052 .282 .510 .645 -.139 .192

a. Dependent Variable: DPR

From the above table, the general form of the equation to predict dividend

payout from growth can be obtained as under:

Predicted dividend payout

= 42.566 + (0.026*growth)

Unstandardized coefficients indicate how much the dependent variable varies

with an Independent variable when all other independent variables are held constant.

In the above table, the unstandardized coefficient for growth is equal to

026Which means for every additional increase in growth, dividend payout

increases by 0.026.

76

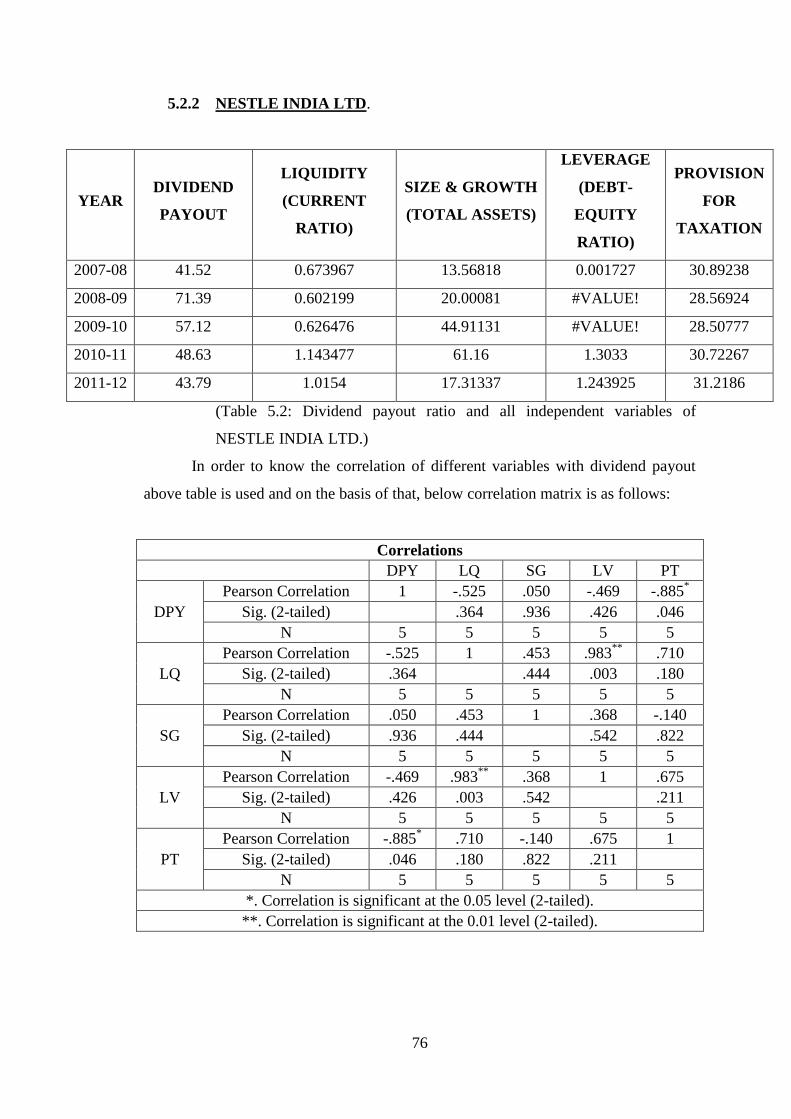

5.2.2 NESTLE INDIA LTD.

YEAR DIVIDEND

PAYOUT

LIQUIDITY

(CURRENT

RATIO)

SIZE & GROWTH

(TOTAL ASSETS)

LEVERAGE

(DEBT-

EQUITY

RATIO)

PROVISION

FOR

TAXATION

2007-08 41.52 0.673967 13.56818 0.001727 30.89238

2008-09 71.39 0.602199 20.00081 #VALUE! 28.56924

2009-10 57.12 0.626476 44.91131 #VALUE! 28.50777

2010-11 48.63 1.143477 61.16 1.3033 30.72267

2011-12 43.79 1.0154 17.31337 1.243925 31.2186

(Table 5.2: Dividend payout ratio and all independent variables of

NESTLE INDIA LTD.)

In order to know the correlation of different variables with dividend payout

above table is used and on the basis of that, below correlation matrix is as follows:

Correlations

DPY LQ SG LV PT

DPY

Pearson Correlation 1 -.525 .050 -.469 -.885*

Sig. (2-tailed)

.364 .936 .426 .046

N 5 5 5 5 5

LQ

Pearson Correlation -.525 1 .453 .983**

.710

Sig. (2-tailed) .364

.444 .003 .180

N 5 5 5 5 5

SG

Pearson Correlation .050 .453 1 .368 -.140

Sig. (2-tailed) .936 .444

.542 .822

N 5 5 5 5 5

LV

Pearson Correlation -.469 .983**

.368 1 .675

Sig. (2-tailed) .426 .003 .542

.211

N 5 5 5 5 5

PT

Pearson Correlation -.885* .710 -.140 .675 1

Sig. (2-tailed) .046 .180 .822 .211

N 5 5 5 5 5

*. Correlation is significant at the 0.05 level (2-tailed).

**. Correlation is significant at the 0.01 level (2-tailed).

77

POSITIVE CORRELATION:

Dividend payout shows weak positive correlation with Growth ratio. Liquidity

and leverage are significant and strongly positively correlated. Liquidity is also partial

positive correlated with growth and provision for taxation. Growth and leverage are

also partially correlated. Leverage is also partially correlated with provision for

taxation.

NEGATIVE CORRELATION:

Dividend payout shows negative correlation with liquidity, leverage and provision for

taxation. Growth and provision for taxation are negatively correlated.

Considering above correlation matrix least correlated value is -0.885 that

indicates low correlation between dividend payout and provision for taxation. Simple

regression method is used in order to know the Influence of provision for taxation on

dividend payout which can be extracted from below table.

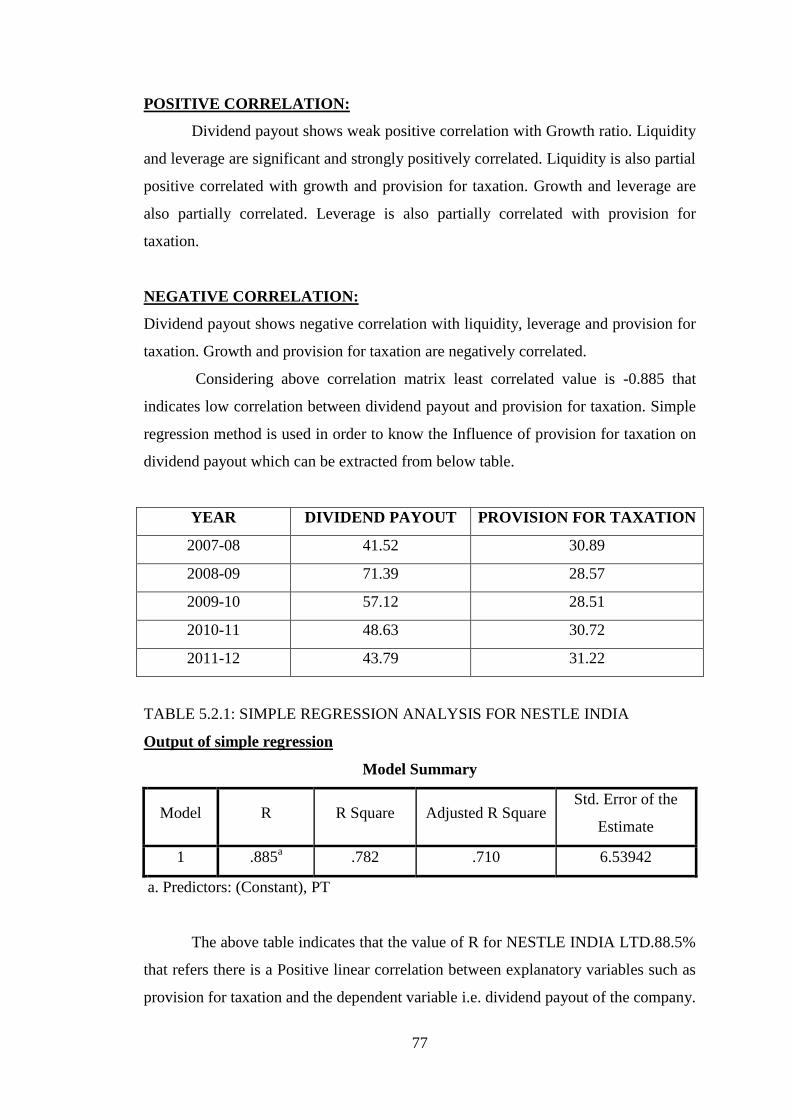

YEAR DIVIDEND PAYOUT PROVISION FOR TAXATION

2007-08 41.52 30.89

2008-09 71.39 28.57

2009-10 57.12 28.51

2010-11 48.63 30.72

2011-12 43.79 31.22

TABLE 5.2.1: SIMPLE REGRESSION ANALYSIS FOR NESTLE INDIA

Output of simple regression

Model Summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .885a .782 .710 6.53942

a. Predictors: (Constant), PT

The above table indicates that the value of R for NESTLE INDIA LTD.88.5%

that refers there is a Positive linear correlation between explanatory variables such as

provision for taxation and the dependent variable i.e. dividend payout of the company.

78

Value of adjusted R- Square for Nestle India Ltd. is 0.710. It indicates that there is

71% change in dividend payout due to the changes in Provision for taxation.

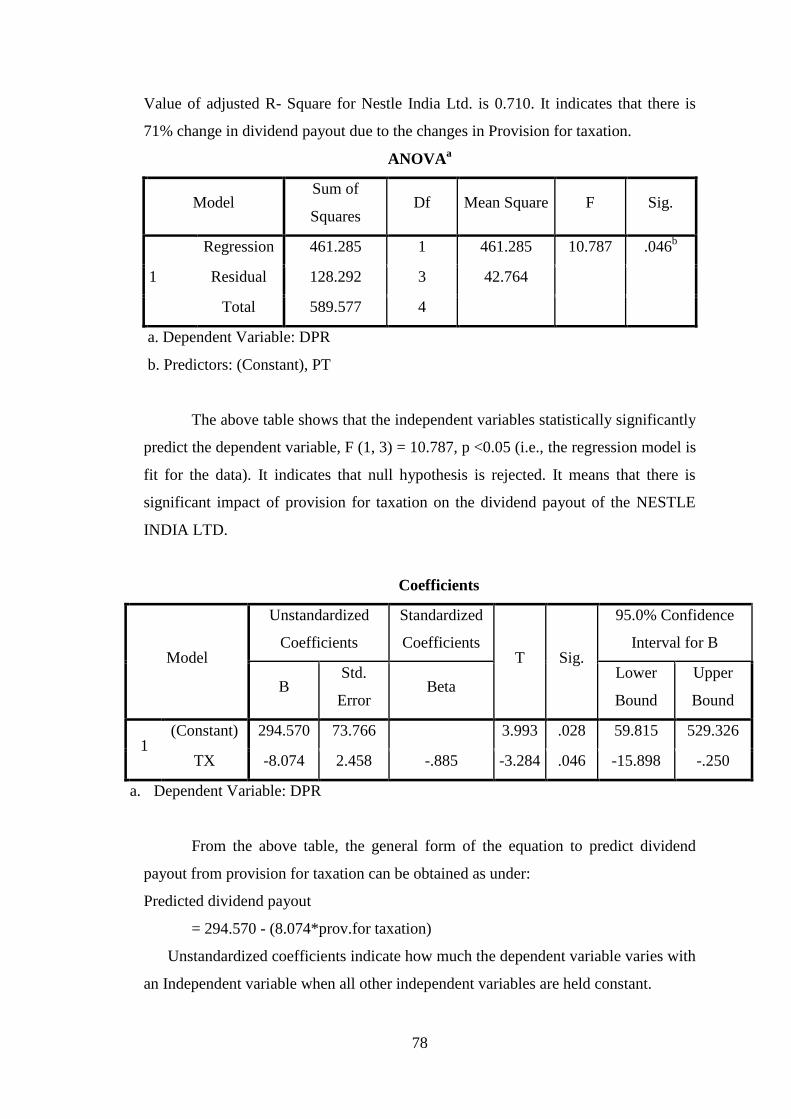

ANOVAa

Model Sum of

Squares Df Mean Square F Sig.

1

Regression 461.285 1 461.285 10.787 .046b

Residual 128.292 3 42.764

Total 589.577 4

a. Dependent Variable: DPR

b. Predictors: (Constant), PT

The above table shows that the independent variables statistically significantly

predict the dependent variable, F (1, 3) = 10.787, p <0.05 (i.e., the regression model is

fit for the data). It indicates that null hypothesis is rejected. It means that there is

significant impact of provision for taxation on the dividend payout of the NESTLE

INDIA LTD.

Coefficients

Model

Unstandardized

Coefficients

Standardized

Coefficients T Sig.

95.0% Confidence

Interval for B

B Std.

Error Beta

Lower

Bound

Upper

Bound

1 (Constant) 294.570 73.766 3.993 .028 59.815 529.326

TX -8.074 2.458 -.885 -3.284 .046 -15.898 -.250

a. Dependent Variable: DPR

From the above table, the general form of the equation to predict dividend

payout from provision for taxation can be obtained as under:

Predicted dividend payout

= 294.570 - (8.074*prov.for taxation)

Unstandardized coefficients indicate how much the dependent variable varies with

an Independent variable when all other independent variables are held constant.

79

In the above table, the unstandardized coefficient for provision for taxation is

equal to-8.074. This means that for every additional in increase provision for

taxation, dividend payout decreases by 8.074.

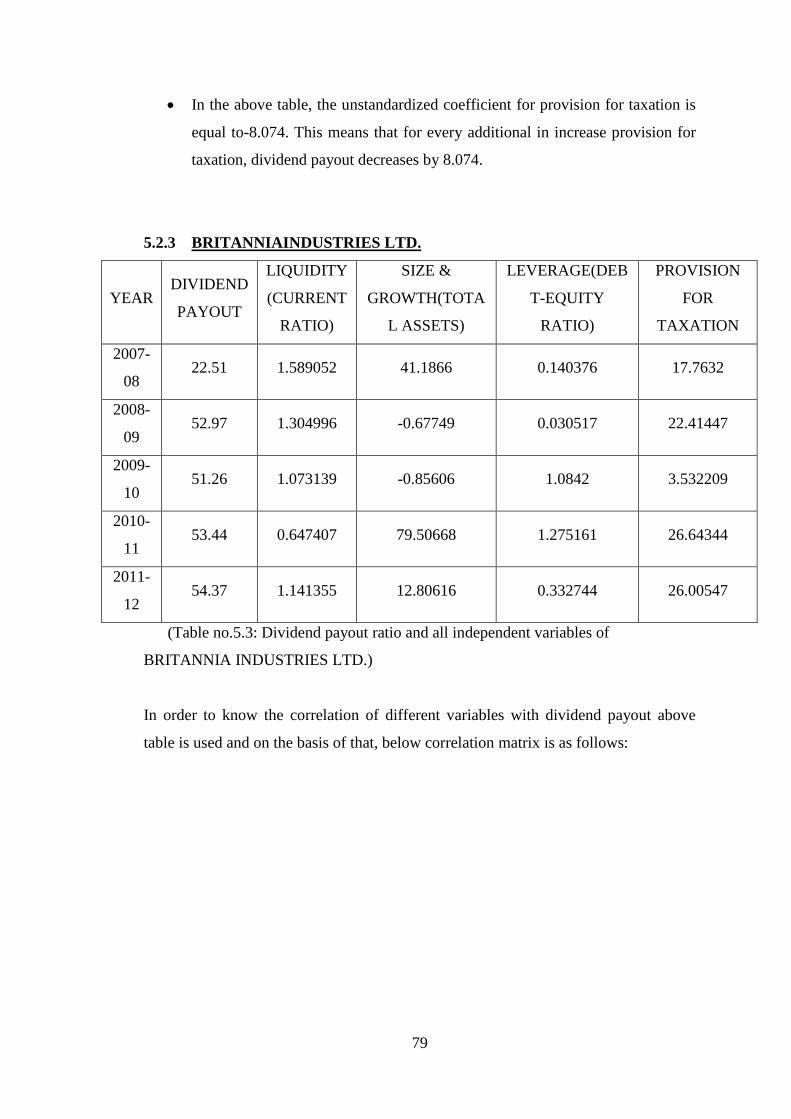

5.2.3 BRITANNIAINDUSTRIES LTD.

YEAR DIVIDEND

PAYOUT

LIQUIDITY

(CURRENT

RATIO)

SIZE &

GROWTH(TOTA

L ASSETS)

LEVERAGE(DEB

T-EQUITY

RATIO)

PROVISION

FOR

TAXATION

2007-

08 22.51 1.589052 41.1866 0.140376 17.7632

2008-

09 52.97 1.304996 -0.67749 0.030517 22.41447

2009-

10 51.26 1.073139 -0.85606 1.0842 3.532209

2010-

11 53.44 0.647407 79.50668 1.275161 26.64344

2011-

12 54.37 1.141355 12.80616 0.332744 26.00547

(Table no.5.3: Dividend payout ratio and all independent variables of

BRITANNIA INDUSTRIES LTD.)

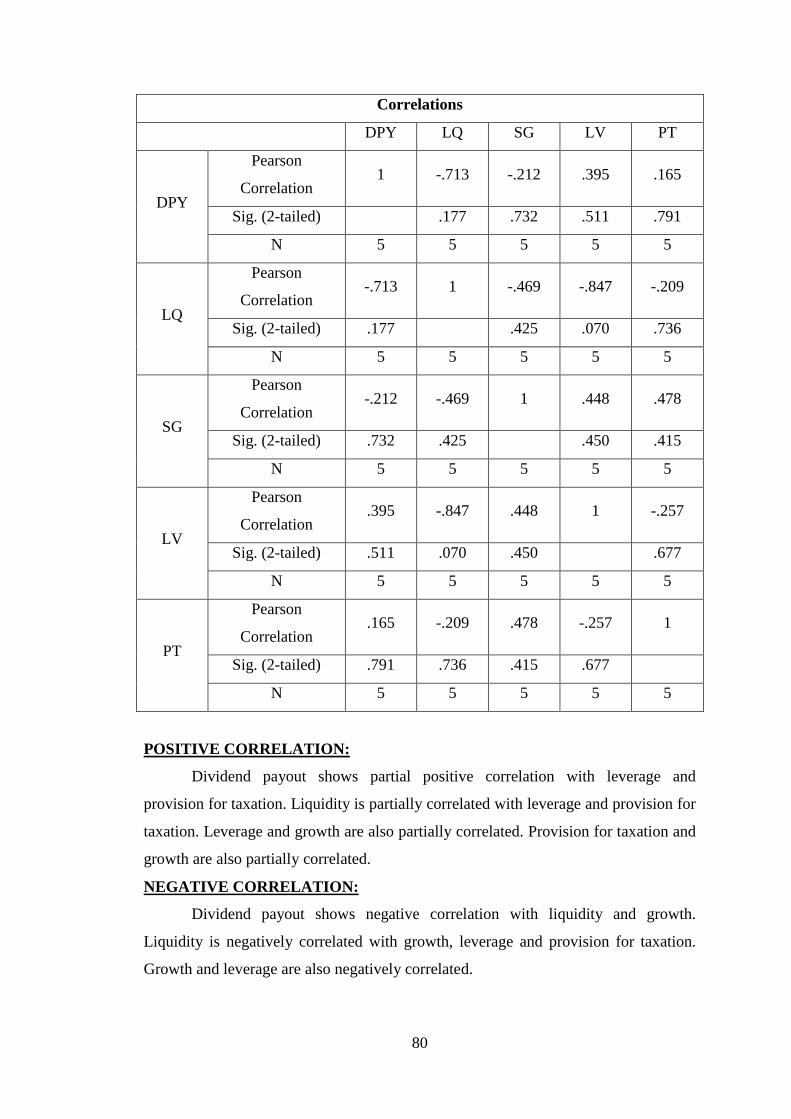

In order to know the correlation of different variables with dividend payout above

table is used and on the basis of that, below correlation matrix is as follows:

80

Correlations

DPY LQ SG LV PT

DPY

Pearson

Correlation 1 -.713 -.212 .395 .165

Sig. (2-tailed)

.177 .732 .511 .791

N 5 5 5 5 5

LQ

Pearson

Correlation -.713 1 -.469 -.847 -.209

Sig. (2-tailed) .177

.425 .070 .736

N 5 5 5 5 5

SG

Pearson

Correlation -.212 -.469 1 .448 .478

Sig. (2-tailed) .732 .425

.450 .415

N 5 5 5 5 5

LV

Pearson

Correlation .395 -.847 .448 1 -.257

Sig. (2-tailed) .511 .070 .450

.677

N 5 5 5 5 5

PT

Pearson

Correlation .165 -.209 .478 -.257 1

Sig. (2-tailed) .791 .736 .415 .677

N 5 5 5 5 5

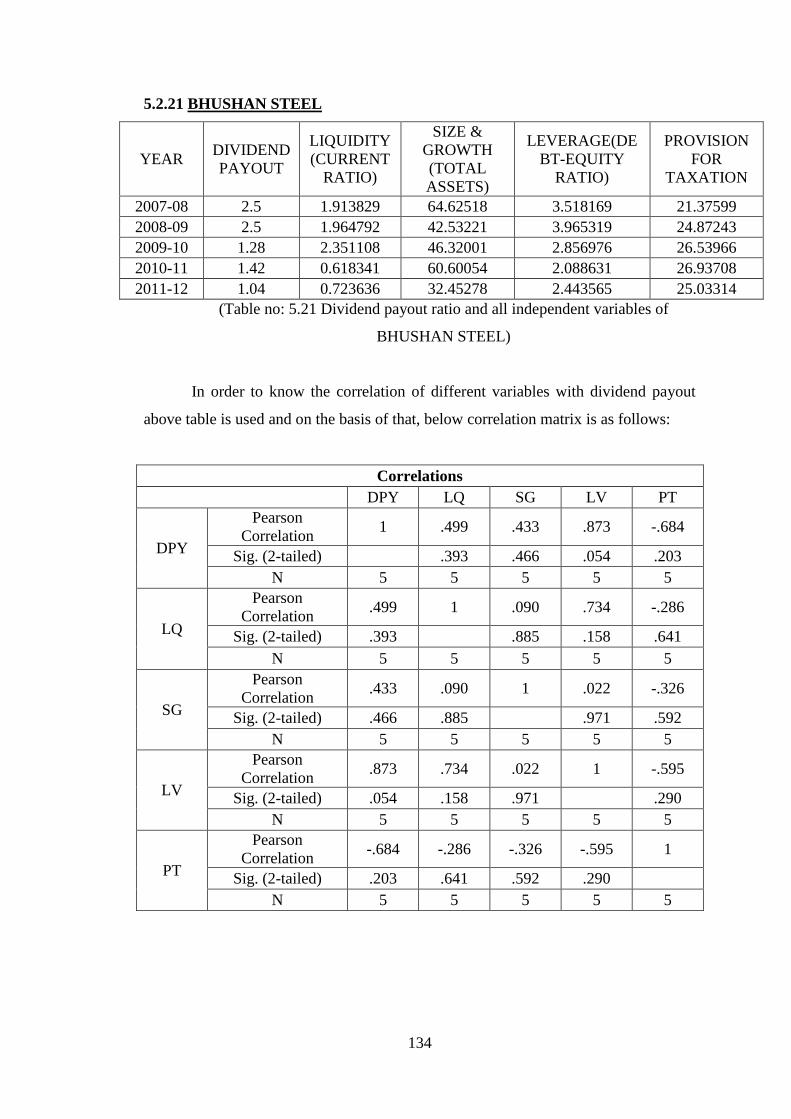

POSITIVE CORRELATION:

Dividend payout shows partial positive correlation with leverage and

provision for taxation. Liquidity is partially correlated with leverage and provision for

taxation. Leverage and growth are also partially correlated. Provision for taxation and

growth are also partially correlated.

NEGATIVE CORRELATION:

Dividend payout shows negative correlation with liquidity and growth.

Liquidity is negatively correlated with growth, leverage and provision for taxation.

Growth and leverage are also negatively correlated.

81

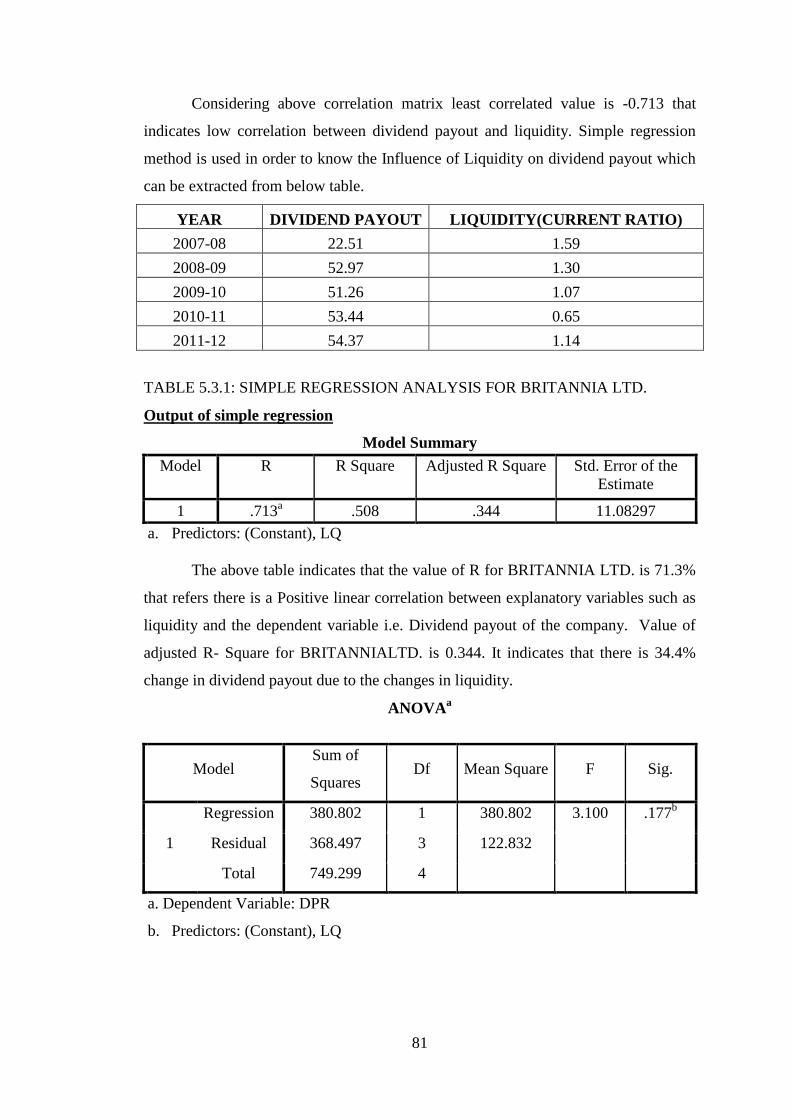

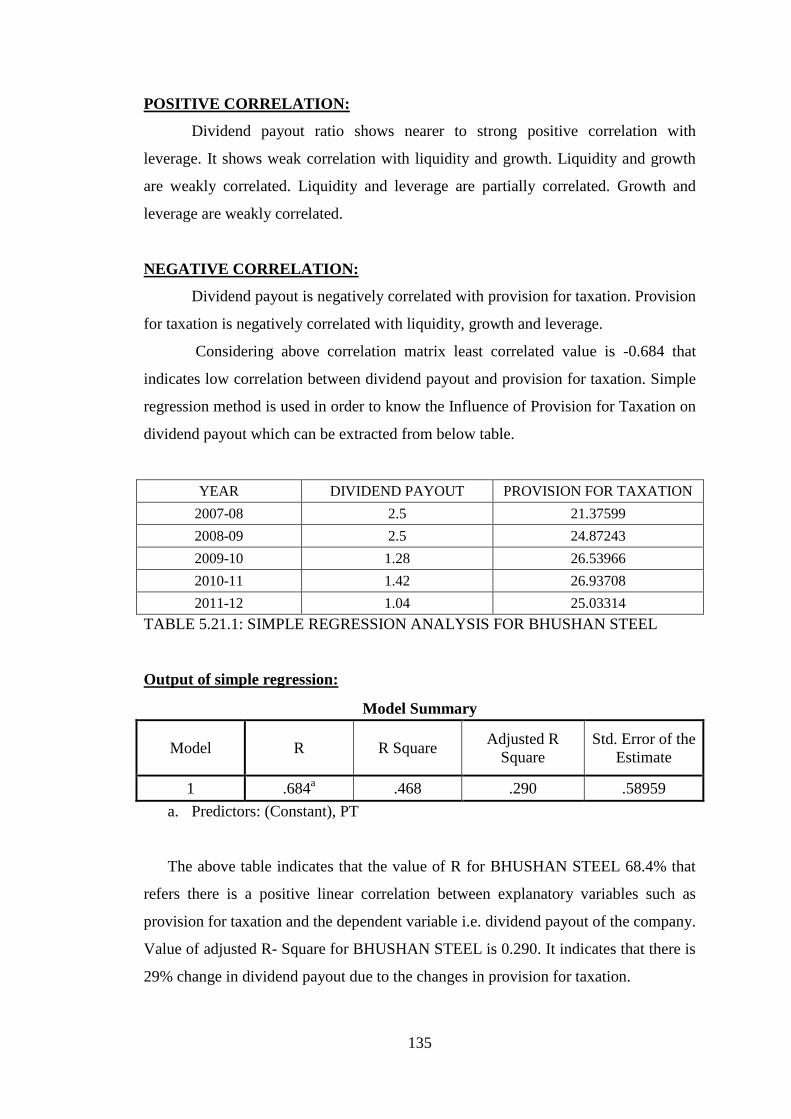

Considering above correlation matrix least correlated value is -0.713 that

indicates low correlation between dividend payout and liquidity. Simple regression

method is used in order to know the Influence of Liquidity on dividend payout which

can be extracted from below table.

YEAR DIVIDEND PAYOUT LIQUIDITY(CURRENT RATIO)

2007-08 22.51 1.59

2008-09 52.97 1.30

2009-10 51.26 1.07

2010-11 53.44 0.65

2011-12 54.37 1.14

TABLE 5.3.1: SIMPLE REGRESSION ANALYSIS FOR BRITANNIA LTD.

Output of simple regression

Model Summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .713a .508 .344 11.08297

a. Predictors: (Constant), LQ

The above table indicates that the value of R for BRITANNIA LTD. is 71.3%

that refers there is a Positive linear correlation between explanatory variables such as

liquidity and the dependent variable i.e. Dividend payout of the company. Value of

adjusted R- Square for BRITANNIALTD. is 0.344. It indicates that there is 34.4%

change in dividend payout due to the changes in liquidity.

ANOVAa

Model Sum of

Squares Df Mean Square F Sig.

1

Regression 380.802 1 380.802 3.100 .177b

Residual 368.497 3 122.832

Total 749.299 4

a. Dependent Variable: DPR

b. Predictors: (Constant), LQ

82

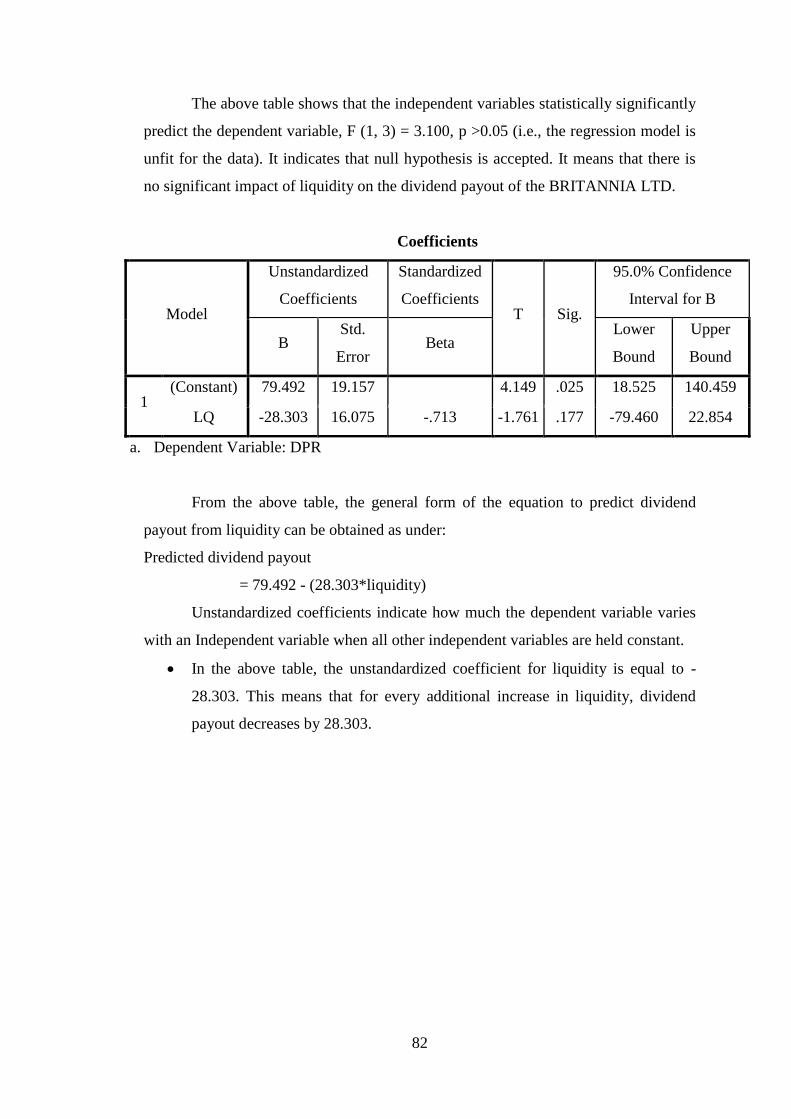

The above table shows that the independent variables statistically significantly

predict the dependent variable, F (1, 3) = 3.100, p >0.05 (i.e., the regression model is

unfit for the data). It indicates that null hypothesis is accepted. It means that there is

no significant impact of liquidity on the dividend payout of the BRITANNIA LTD.

Coefficients

Model

Unstandardized

Coefficients

Standardized

Coefficients T Sig.

95.0% Confidence

Interval for B

B Std.

Error Beta

Lower

Bound

Upper

Bound

1 (Constant) 79.492 19.157 4.149 .025 18.525 140.459

LQ -28.303 16.075 -.713 -1.761 .177 -79.460 22.854

a. Dependent Variable: DPR

From the above table, the general form of the equation to predict dividend

payout from liquidity can be obtained as under:

Predicted dividend payout

= 79.492 - (28.303*liquidity)

Unstandardized coefficients indicate how much the dependent variable varies

with an Independent variable when all other independent variables are held constant.

In the above table, the unstandardized coefficient for liquidity is equal to -

28.303. This means that for every additional increase in liquidity, dividend

payout decreases by 28.303.

83

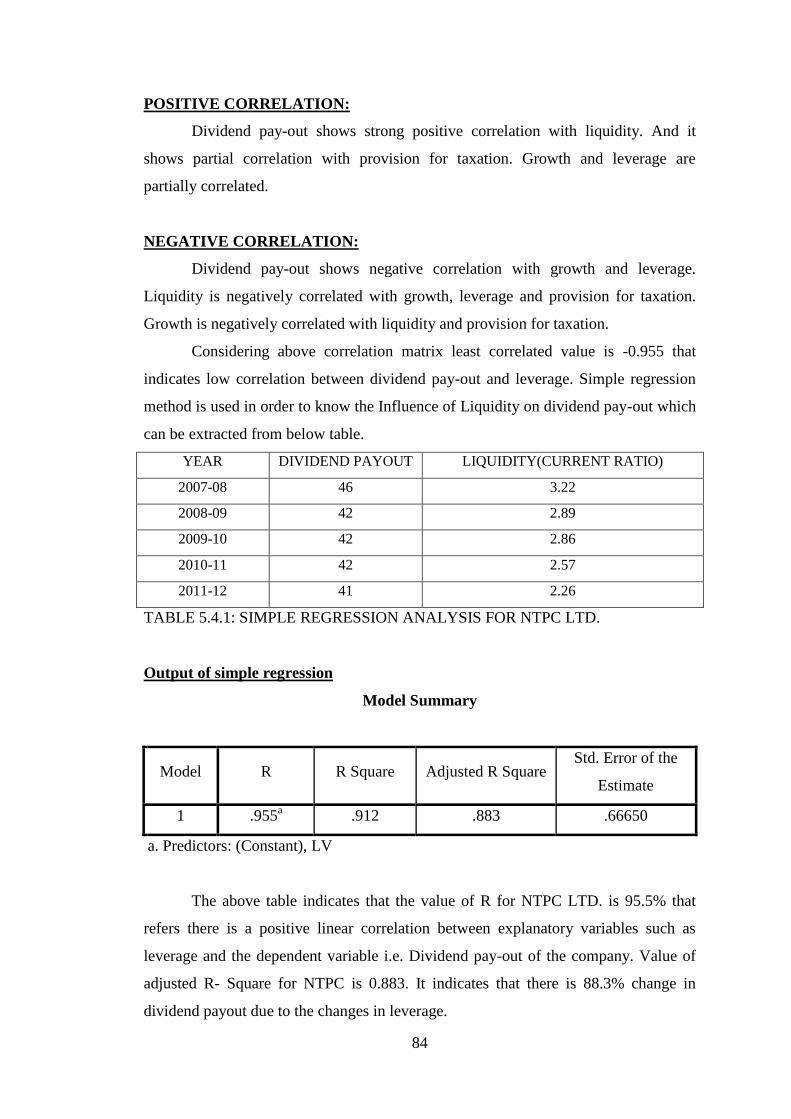

5.2.4 NTPC LTD

YEAR DIVIDEND

PAYOUT

LIQUIDITY

(CURRENT

RATIO)

SIZE &

GROWTH

(TOTAL

ASSETS)

LEVERAGE(DEB

T-EQUITY

RATIO)

PROVISION

FOR

TAXATION

2007-08 46 3.221831 10.47 0.516558 27.69505

2008-09 42 2.893298 16.055 0.602541 6.745018

2009-10 42 2.864418 8.017458 0.605362 24.65849

2010-11 42 2.572039 23.13398 0.632637 24.45643

2011-12 41 2.257266 12.00821 0.666903 25.16632

(Table no: 5.4 Dividend payout ratio and all independent variables of NTPC LTD.)

In order to know the correlation of different variables with dividend payout

above table is used and on the basis of that, below correlation matrix is as follows:

Correlations

DPY LQ SG LV PT

DPY

Pearson Correlation 1 .826 -.259 -.955* .308

Sig. (2-tailed)

.085 .674 .011 .614

N 5 5 5 5 5

LQ

Pearson Correlation .826 1 -.313 -.954* -.095

Sig. (2-tailed) .085

.608 .012 .879

N 5 5 5 5 5

SG

Pearson Correlation -.259 -.313 1 .329 -.256

Sig. (2-tailed) .674 .608

.588 .678

N 5 5 5 5 5

LV

Pearson Correlation -.955* -.954

* .329 1 -.107

Sig. (2-tailed) .011 .012 .588

.865

N 5 5 5 5 5

PT

Pearson Correlation .308 -.095 -.256 -.107 1

Sig. (2-tailed) .614 .879 .678 .865

N 5 5 5 5 5

*. Correlation is significant at the 0.05 level (2-tailed).

84

POSITIVE CORRELATION:

Dividend pay-out shows strong positive correlation with liquidity. And it

shows partial correlation with provision for taxation. Growth and leverage are

partially correlated.

NEGATIVE CORRELATION:

Dividend pay-out shows negative correlation with growth and leverage.

Liquidity is negatively correlated with growth, leverage and provision for taxation.

Growth is negatively correlated with liquidity and provision for taxation.

Considering above correlation matrix least correlated value is -0.955 that

indicates low correlation between dividend pay-out and leverage. Simple regression

method is used in order to know the Influence of Liquidity on dividend pay-out which

can be extracted from below table.

YEAR DIVIDEND PAYOUT LIQUIDITY(CURRENT RATIO)

2007-08 46 3.22

2008-09 42 2.89

2009-10 42 2.86

2010-11 42 2.57

2011-12 41 2.26

TABLE 5.4.1: SIMPLE REGRESSION ANALYSIS FOR NTPC LTD.

Output of simple regression

Model Summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .955a .912 .883 .66650

a. Predictors: (Constant), LV

The above table indicates that the value of R for NTPC LTD. is 95.5% that

refers there is a positive linear correlation between explanatory variables such as

leverage and the dependent variable i.e. Dividend pay-out of the company. Value of

adjusted R- Square for NTPC is 0.883. It indicates that there is 88.3% change in

dividend payout due to the changes in leverage.

85

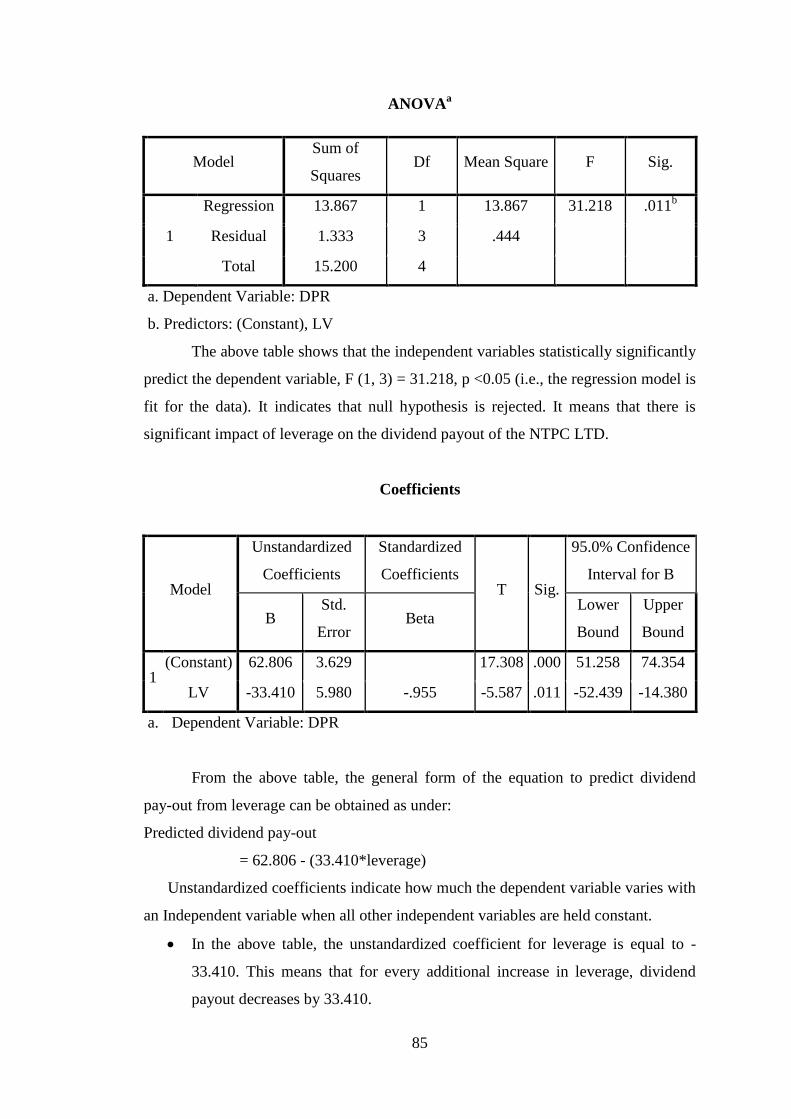

ANOVAa

Model Sum of

Squares Df Mean Square F Sig.

1

Regression 13.867 1 13.867 31.218 .011b

Residual 1.333 3 .444

Total 15.200 4

a. Dependent Variable: DPR

b. Predictors: (Constant), LV

The above table shows that the independent variables statistically significantly

predict the dependent variable, F (1, 3) = 31.218, p <0.05 (i.e., the regression model is

fit for the data). It indicates that null hypothesis is rejected. It means that there is

significant impact of leverage on the dividend payout of the NTPC LTD.

Coefficients

Model

Unstandardized

Coefficients

Standardized

Coefficients T Sig.

95.0% Confidence

Interval for B

B Std.

Error Beta

Lower

Bound

Upper

Bound

1 (Constant) 62.806 3.629 17.308 .000 51.258 74.354

LV -33.410 5.980 -.955 -5.587 .011 -52.439 -14.380

a. Dependent Variable: DPR

From the above table, the general form of the equation to predict dividend

pay-out from leverage can be obtained as under:

Predicted dividend pay-out

= 62.806 - (33.410*leverage)

Unstandardized coefficients indicate how much the dependent variable varies with

an Independent variable when all other independent variables are held constant.

In the above table, the unstandardized coefficient for leverage is equal to -

33.410. This means that for every additional increase in leverage, dividend

payout decreases by 33.410.

86

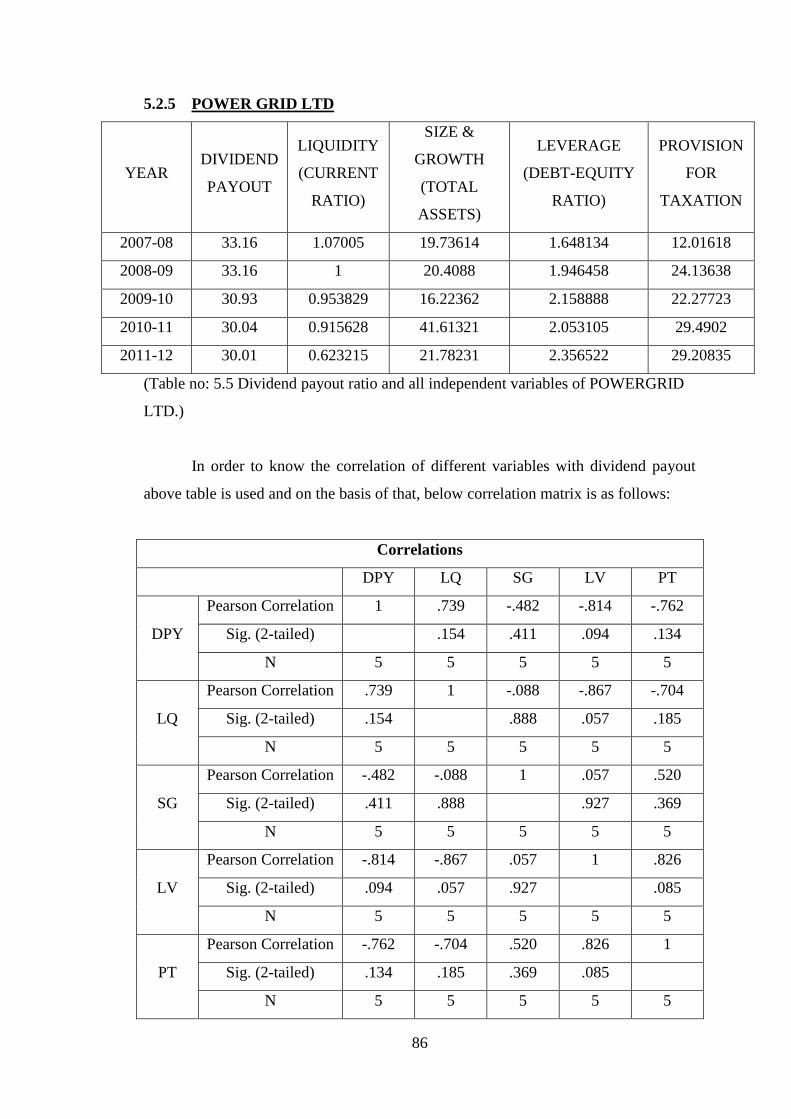

5.2.5 POWER GRID LTD

YEAR DIVIDEND

PAYOUT

LIQUIDITY

(CURRENT

RATIO)

SIZE &

GROWTH

(TOTAL

ASSETS)

LEVERAGE

(DEBT-EQUITY

RATIO)

PROVISION

FOR

TAXATION

2007-08 33.16 1.07005 19.73614 1.648134 12.01618

2008-09 33.16 1 20.4088 1.946458 24.13638

2009-10 30.93 0.953829 16.22362 2.158888 22.27723

2010-11 30.04 0.915628 41.61321 2.053105 29.4902

2011-12 30.01 0.623215 21.78231 2.356522 29.20835

(Table no: 5.5 Dividend payout ratio and all independent variables of POWERGRID

LTD.)

In order to know the correlation of different variables with dividend payout

above table is used and on the basis of that, below correlation matrix is as follows:

Correlations

DPY LQ SG LV PT

DPY

Pearson Correlation 1 .739 -.482 -.814 -.762

Sig. (2-tailed)

.154 .411 .094 .134

N 5 5 5 5 5

LQ

Pearson Correlation .739 1 -.088 -.867 -.704

Sig. (2-tailed) .154

.888 .057 .185

N 5 5 5 5 5

SG

Pearson Correlation -.482 -.088 1 .057 .520

Sig. (2-tailed) .411 .888

.927 .369

N 5 5 5 5 5

LV

Pearson Correlation -.814 -.867 .057 1 .826

Sig. (2-tailed) .094 .057 .927

.085

N 5 5 5 5 5

PT

Pearson Correlation -.762 -.704 .520 .826 1

Sig. (2-tailed) .134 .185 .369 .085

N 5 5 5 5 5

87

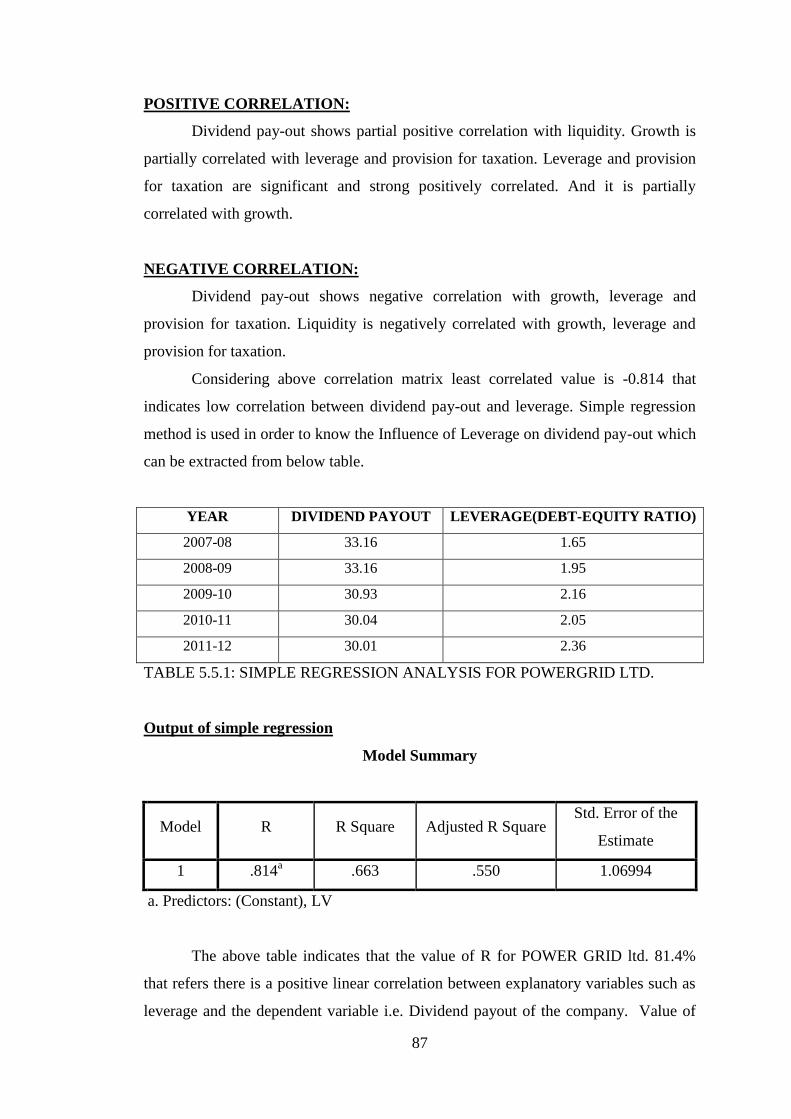

POSITIVE CORRELATION:

Dividend pay-out shows partial positive correlation with liquidity. Growth is

partially correlated with leverage and provision for taxation. Leverage and provision

for taxation are significant and strong positively correlated. And it is partially

correlated with growth.

NEGATIVE CORRELATION:

Dividend pay-out shows negative correlation with growth, leverage and

provision for taxation. Liquidity is negatively correlated with growth, leverage and

provision for taxation.

Considering above correlation matrix least correlated value is -0.814 that

indicates low correlation between dividend pay-out and leverage. Simple regression

method is used in order to know the Influence of Leverage on dividend pay-out which

can be extracted from below table.

YEAR DIVIDEND PAYOUT LEVERAGE(DEBT-EQUITY RATIO)

2007-08 33.16 1.65

2008-09 33.16 1.95

2009-10 30.93 2.16

2010-11 30.04 2.05

2011-12 30.01 2.36

TABLE 5.5.1: SIMPLE REGRESSION ANALYSIS FOR POWERGRID LTD.

Output of simple regression

Model Summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .814a .663 .550 1.06994

a. Predictors: (Constant), LV

The above table indicates that the value of R for POWER GRID ltd. 81.4%

that refers there is a positive linear correlation between explanatory variables such as

leverage and the dependent variable i.e. Dividend payout of the company. Value of

88

adjusted R- Square for POWER GRID LTD. is 0.550. It indicates that there is 55%

change in dividend payout due to the changes in leverage.

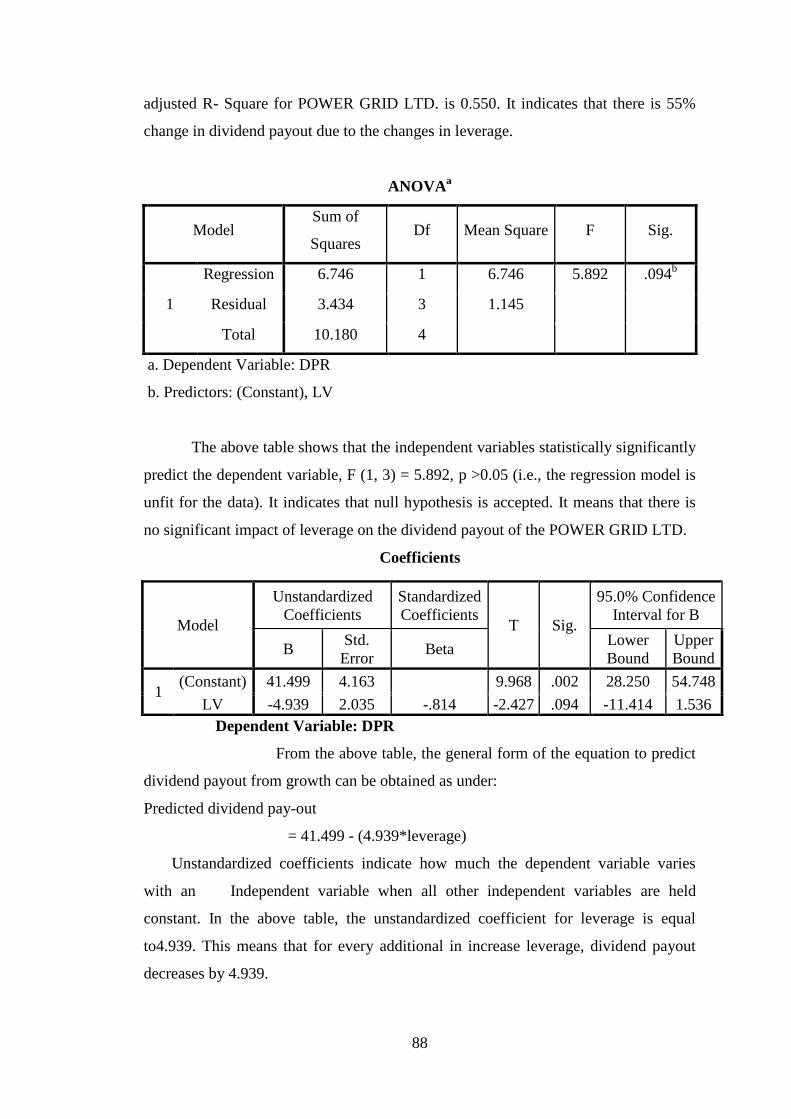

ANOVAa

Model Sum of

Squares Df Mean Square F Sig.

1

Regression 6.746 1 6.746 5.892 .094b

Residual 3.434 3 1.145

Total 10.180 4

a. Dependent Variable: DPR

b. Predictors: (Constant), LV

The above table shows that the independent variables statistically significantly

predict the dependent variable, F (1, 3) = 5.892, p >0.05 (i.e., the regression model is

unfit for the data). It indicates that null hypothesis is accepted. It means that there is

no significant impact of leverage on the dividend payout of the POWER GRID LTD.

Coefficients

Dependent Variable: DPR

From the above table, the general form of the equation to predict

dividend payout from growth can be obtained as under:

Predicted dividend pay-out

= 41.499 - (4.939*leverage)

Unstandardized coefficients indicate how much the dependent variable varies

with an Independent variable when all other independent variables are held

constant. In the above table, the unstandardized coefficient for leverage is equal

to4.939. This means that for every additional in increase leverage, dividend payout

decreases by 4.939.

Model

Unstandardized

Coefficients

Standardized

Coefficients T Sig.

95.0% Confidence

Interval for B

B Std.

Error Beta

Lower

Bound

Upper

Bound

1 (Constant) 41.499 4.163 9.968 .002 28.250 54.748

LV -4.939 2.035 -.814 -2.427 .094 -11.414 1.536

89

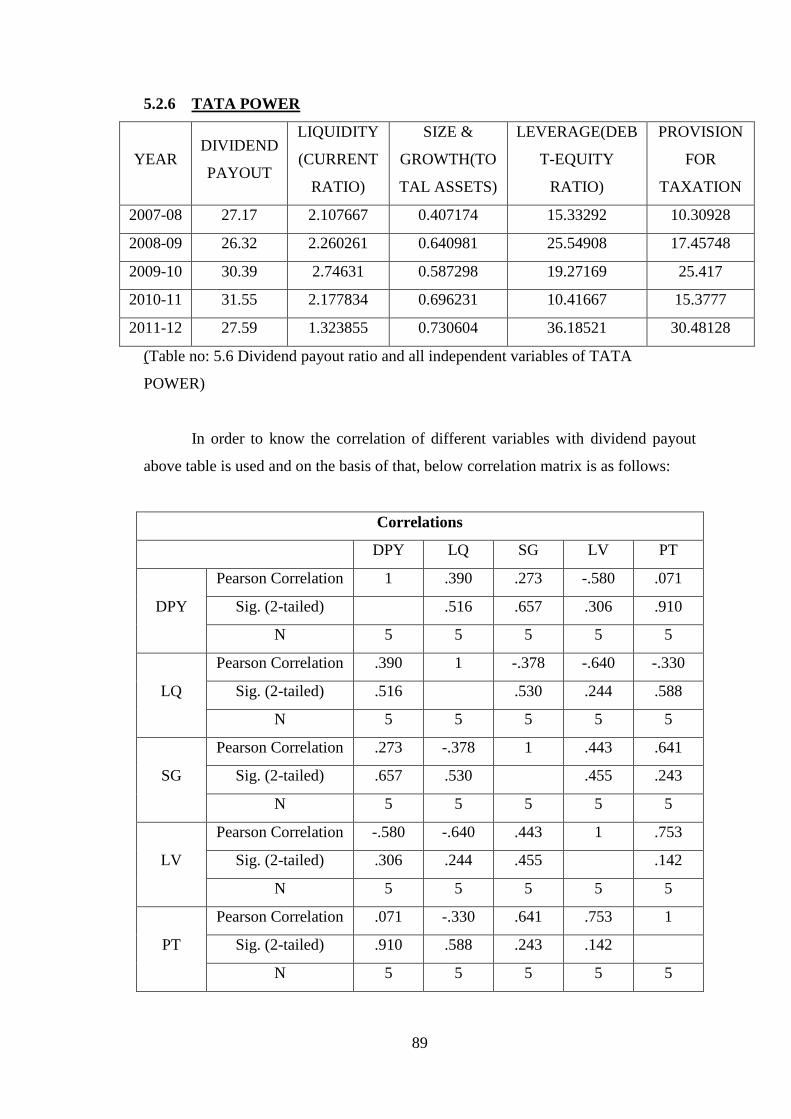

5.2.6 TATA POWER

YEAR DIVIDEND

PAYOUT

LIQUIDITY

(CURRENT

RATIO)

SIZE &

GROWTH(TO

TAL ASSETS)

LEVERAGE(DEB

T-EQUITY

RATIO)

PROVISION

FOR

TAXATION

2007-08 27.17 2.107667 0.407174 15.33292 10.30928

2008-09 26.32 2.260261 0.640981 25.54908 17.45748

2009-10 30.39 2.74631 0.587298 19.27169 25.417

2010-11 31.55 2.177834 0.696231 10.41667 15.3777

2011-12 27.59 1.323855 0.730604 36.18521 30.48128

(Table no: 5.6 Dividend payout ratio and all independent variables of TATA

POWER)

In order to know the correlation of different variables with dividend payout

above table is used and on the basis of that, below correlation matrix is as follows:

Correlations

DPY LQ SG LV PT

DPY

Pearson Correlation 1 .390 .273 -.580 .071

Sig. (2-tailed)

.516 .657 .306 .910

N 5 5 5 5 5

LQ

Pearson Correlation .390 1 -.378 -.640 -.330

Sig. (2-tailed) .516

.530 .244 .588

N 5 5 5 5 5

SG

Pearson Correlation .273 -.378 1 .443 .641

Sig. (2-tailed) .657 .530

.455 .243

N 5 5 5 5 5

LV

Pearson Correlation -.580 -.640 .443 1 .753

Sig. (2-tailed) .306 .244 .455

.142

N 5 5 5 5 5

PT

Pearson Correlation .071 -.330 .641 .753 1

Sig. (2-tailed) .910 .588 .243 .142

N 5 5 5 5 5

90

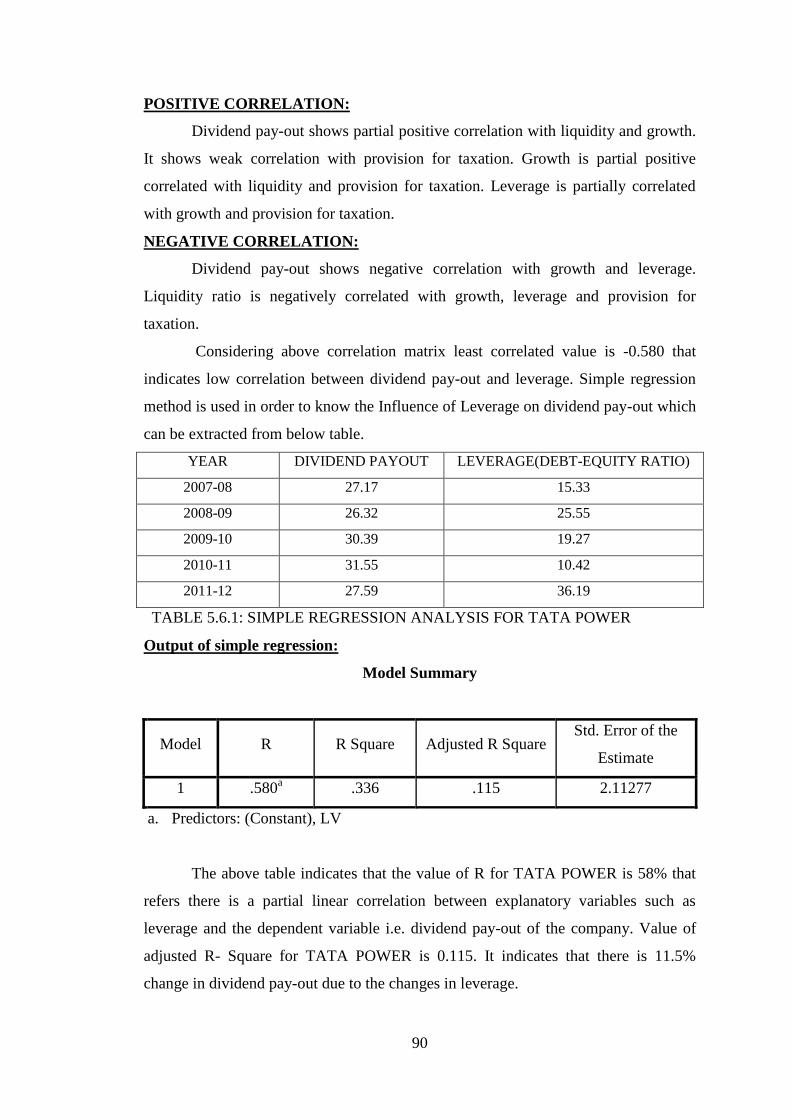

POSITIVE CORRELATION:

Dividend pay-out shows partial positive correlation with liquidity and growth.

It shows weak correlation with provision for taxation. Growth is partial positive

correlated with liquidity and provision for taxation. Leverage is partially correlated

with growth and provision for taxation.

NEGATIVE CORRELATION:

Dividend pay-out shows negative correlation with growth and leverage.

Liquidity ratio is negatively correlated with growth, leverage and provision for

taxation.

Considering above correlation matrix least correlated value is -0.580 that

indicates low correlation between dividend pay-out and leverage. Simple regression

method is used in order to know the Influence of Leverage on dividend pay-out which

can be extracted from below table.

YEAR DIVIDEND PAYOUT LEVERAGE(DEBT-EQUITY RATIO)

2007-08 27.17 15.33

2008-09 26.32 25.55

2009-10 30.39 19.27

2010-11 31.55 10.42

2011-12 27.59 36.19

TABLE 5.6.1: SIMPLE REGRESSION ANALYSIS FOR TATA POWER

Output of simple regression:

Model Summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .580a .336 .115 2.11277

a. Predictors: (Constant), LV

The above table indicates that the value of R for TATA POWER is 58% that

refers there is a partial linear correlation between explanatory variables such as

leverage and the dependent variable i.e. dividend pay-out of the company. Value of

adjusted R- Square for TATA POWER is 0.115. It indicates that there is 11.5%

change in dividend pay-out due to the changes in leverage.

91

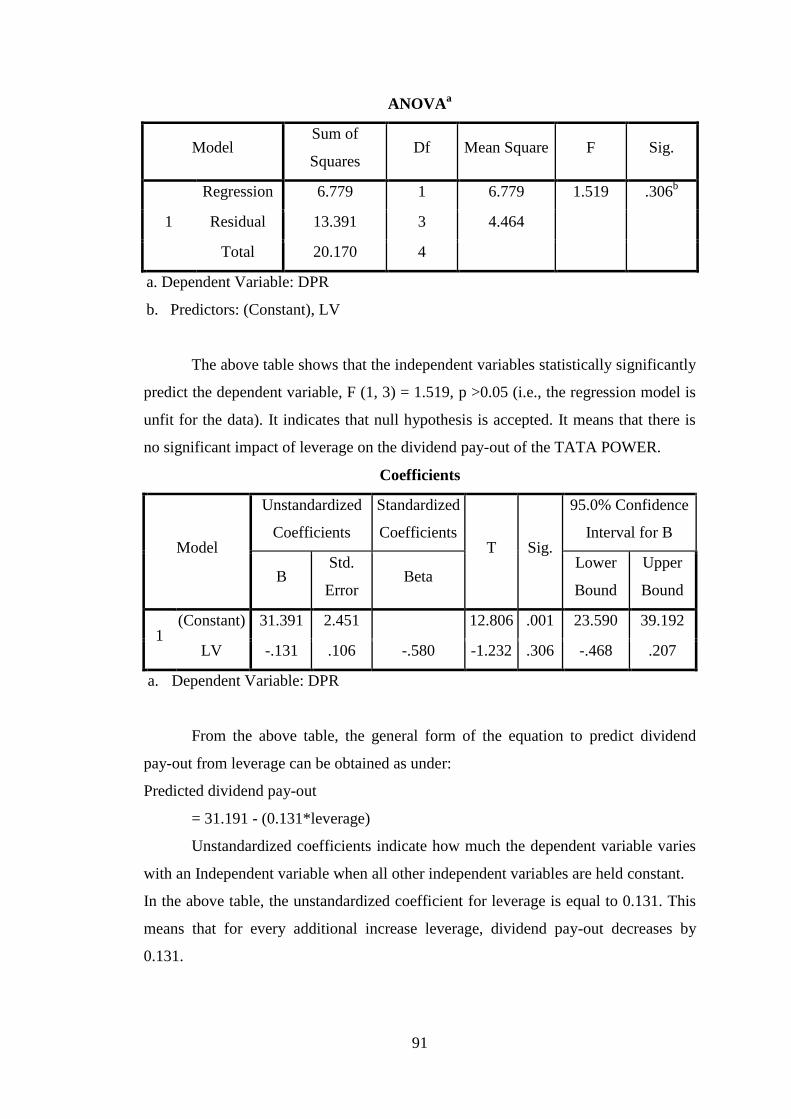

ANOVAa

Model Sum of

Squares Df Mean Square F Sig.

1

Regression 6.779 1 6.779 1.519 .306b

Residual 13.391 3 4.464

Total 20.170 4

a. Dependent Variable: DPR

b. Predictors: (Constant), LV

The above table shows that the independent variables statistically significantly

predict the dependent variable, F (1, 3) = 1.519, p >0.05 (i.e., the regression model is

unfit for the data). It indicates that null hypothesis is accepted. It means that there is

no significant impact of leverage on the dividend pay-out of the TATA POWER.

Coefficients

Model

Unstandardized

Coefficients

Standardized

Coefficients T Sig.

95.0% Confidence

Interval for B

B Std.

Error Beta

Lower

Bound

Upper

Bound

1 (Constant) 31.391 2.451 12.806 .001 23.590 39.192

LV -.131 .106 -.580 -1.232 .306 -.468 .207

a. Dependent Variable: DPR

From the above table, the general form of the equation to predict dividend

pay-out from leverage can be obtained as under:

Predicted dividend pay-out

= 31.191 - (0.131*leverage)

Unstandardized coefficients indicate how much the dependent variable varies

with an Independent variable when all other independent variables are held constant.

In the above table, the unstandardized coefficient for leverage is equal to 0.131. This

means that for every additional increase leverage, dividend pay-out decreases by

0.131.

92

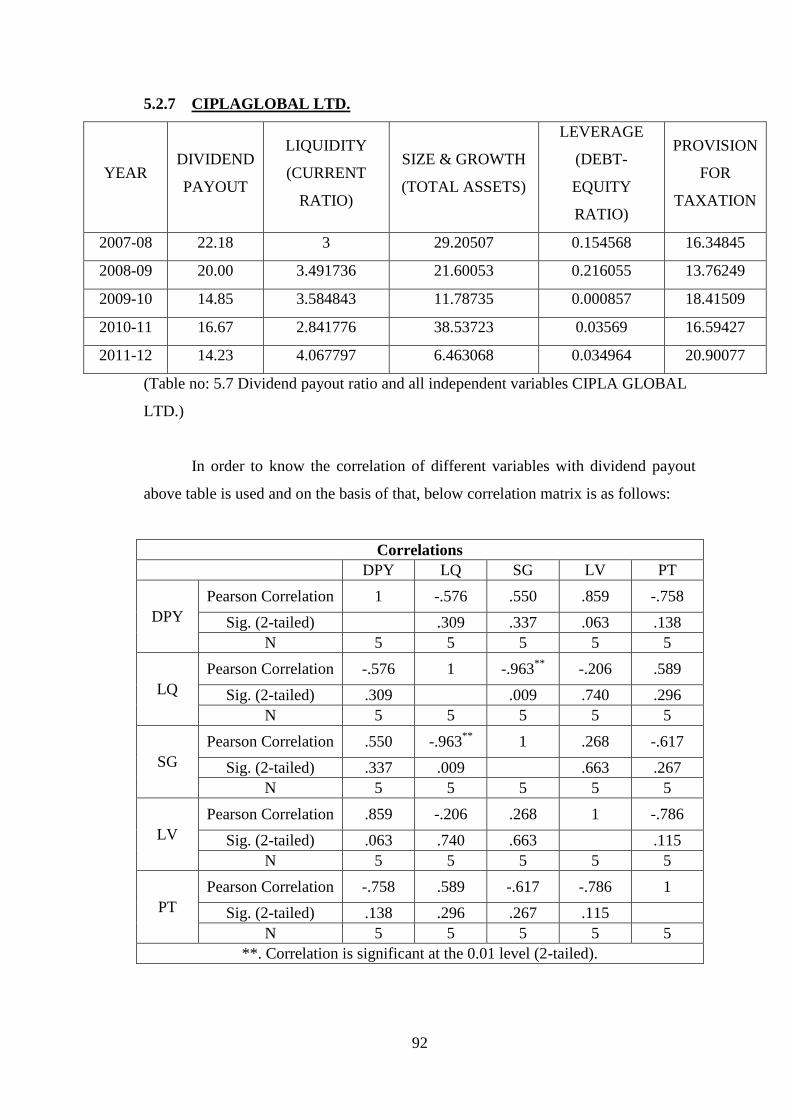

5.2.7 CIPLAGLOBAL LTD.

YEAR DIVIDEND

PAYOUT

LIQUIDITY

(CURRENT

RATIO)

SIZE & GROWTH

(TOTAL ASSETS)

LEVERAGE

(DEBT-

EQUITY

RATIO)

PROVISION

FOR

TAXATION

2007-08 22.18 3 29.20507 0.154568 16.34845

2008-09 20.00 3.491736 21.60053 0.216055 13.76249

2009-10 14.85 3.584843 11.78735 0.000857 18.41509

2010-11 16.67 2.841776 38.53723 0.03569 16.59427

2011-12 14.23 4.067797 6.463068 0.034964 20.90077

(Table no: 5.7 Dividend payout ratio and all independent variables CIPLA GLOBAL

LTD.)

In order to know the correlation of different variables with dividend payout

above table is used and on the basis of that, below correlation matrix is as follows:

Correlations

DPY LQ SG LV PT

DPY

Pearson Correlation 1 -.576 .550 .859 -.758

Sig. (2-tailed)

.309 .337 .063 .138

N 5 5 5 5 5

LQ

Pearson Correlation -.576 1 -.963**

-.206 .589

Sig. (2-tailed) .309

.009 .740 .296

N 5 5 5 5 5

SG

Pearson Correlation .550 -.963**

1 .268 -.617

Sig. (2-tailed) .337 .009

.663 .267

N 5 5 5 5 5

LV

Pearson Correlation .859 -.206 .268 1 -.786

Sig. (2-tailed) .063 .740 .663

.115

N 5 5 5 5 5

PT

Pearson Correlation -.758 .589 -.617 -.786 1

Sig. (2-tailed) .138 .296 .267 .115

N 5 5 5 5 5

**. Correlation is significant at the 0.01 level (2-tailed).

93

POSITIVE CORRELATION:

Dividend pay-out shows strong positive correlation with leverage. It shows

partial positive correlation with growth. Liquidity and provision for taxation are

partially correlated. Growth and leverage are partially correlated with leverage.

NEGATIVE CORRELATION:

Dividend pay-out shows negative correlations with liquidity and provision for

taxation. Liquidity is negatively correlated with growth and leverage. Growth and

provision for taxation are negatively correlated. Leverage and provisions for taxation

are also negatively correlated.

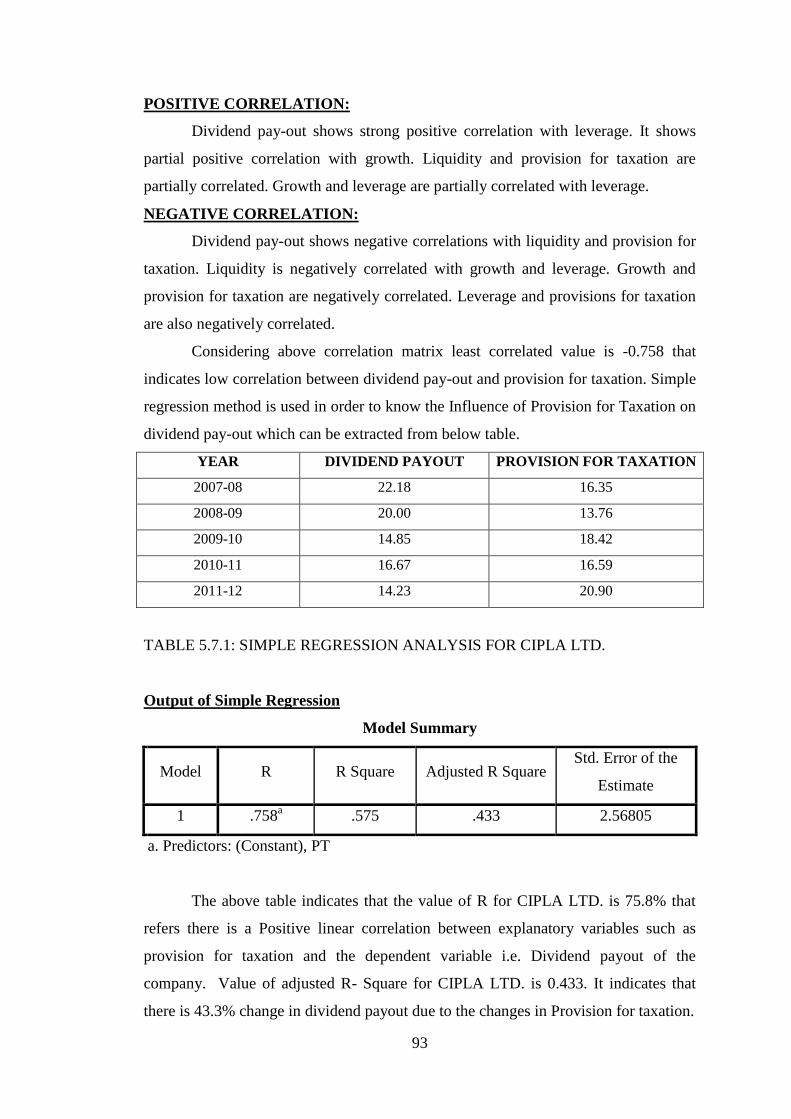

Considering above correlation matrix least correlated value is -0.758 that

indicates low correlation between dividend pay-out and provision for taxation. Simple

regression method is used in order to know the Influence of Provision for Taxation on

dividend pay-out which can be extracted from below table.

YEAR DIVIDEND PAYOUT PROVISION FOR TAXATION

2007-08 22.18 16.35

2008-09 20.00 13.76

2009-10 14.85 18.42

2010-11 16.67 16.59

2011-12 14.23 20.90

TABLE 5.7.1: SIMPLE REGRESSION ANALYSIS FOR CIPLA LTD.

Output of Simple Regression

Model Summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .758a .575 .433 2.56805

a. Predictors: (Constant), PT

The above table indicates that the value of R for CIPLA LTD. is 75.8% that

refers there is a Positive linear correlation between explanatory variables such as

provision for taxation and the dependent variable i.e. Dividend payout of the

company. Value of adjusted R- Square for CIPLA LTD. is 0.433. It indicates that

there is 43.3% change in dividend payout due to the changes in Provision for taxation.

94

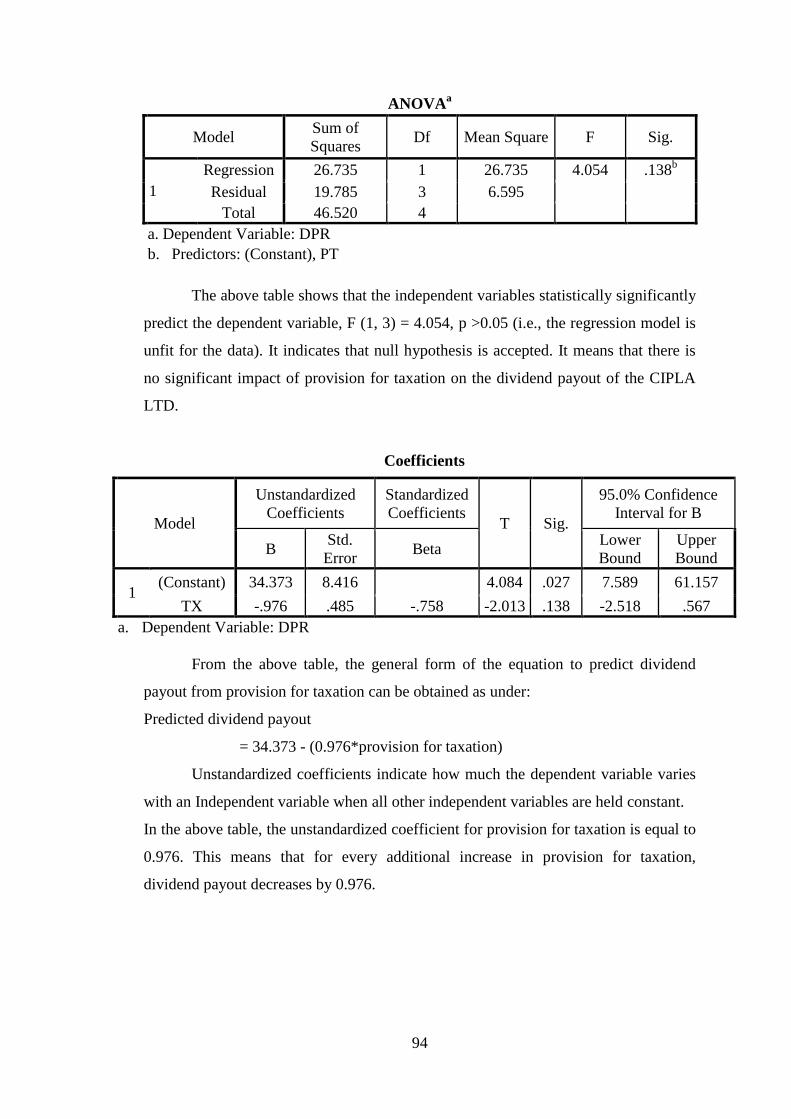

ANOVAa

Model Sum of

Squares Df Mean Square F Sig.

1

Regression 26.735 1 26.735 4.054 .138b

Residual 19.785 3 6.595

Total 46.520 4

a. Dependent Variable: DPR

b. Predictors: (Constant), PT

The above table shows that the independent variables statistically significantly

predict the dependent variable, F (1, 3) = 4.054, p >0.05 (i.e., the regression model is

unfit for the data). It indicates that null hypothesis is accepted. It means that there is

no significant impact of provision for taxation on the dividend payout of the CIPLA

LTD.

Coefficients

Model

Unstandardized

Coefficients

Standardized

Coefficients T Sig.

95.0% Confidence

Interval for B

B Std.

Error Beta

Lower

Bound

Upper

Bound

1 (Constant) 34.373 8.416 4.084 .027 7.589 61.157

TX -.976 .485 -.758 -2.013 .138 -2.518 .567

a. Dependent Variable: DPR

From the above table, the general form of the equation to predict dividend

payout from provision for taxation can be obtained as under:

Predicted dividend payout

= 34.373 - (0.976*provision for taxation)

Unstandardized coefficients indicate how much the dependent variable varies

with an Independent variable when all other independent variables are held constant.

In the above table, the unstandardized coefficient for provision for taxation is equal to

0.976. This means that for every additional increase in provision for taxation,

dividend payout decreases by 0.976.

95

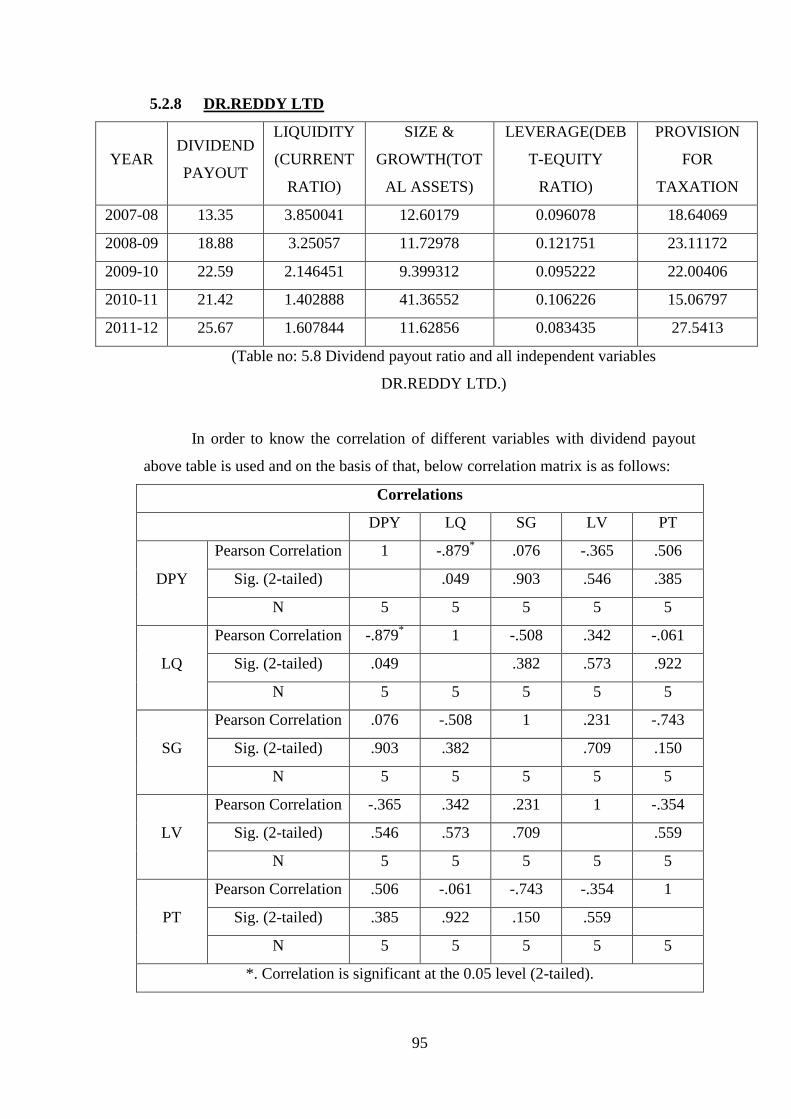

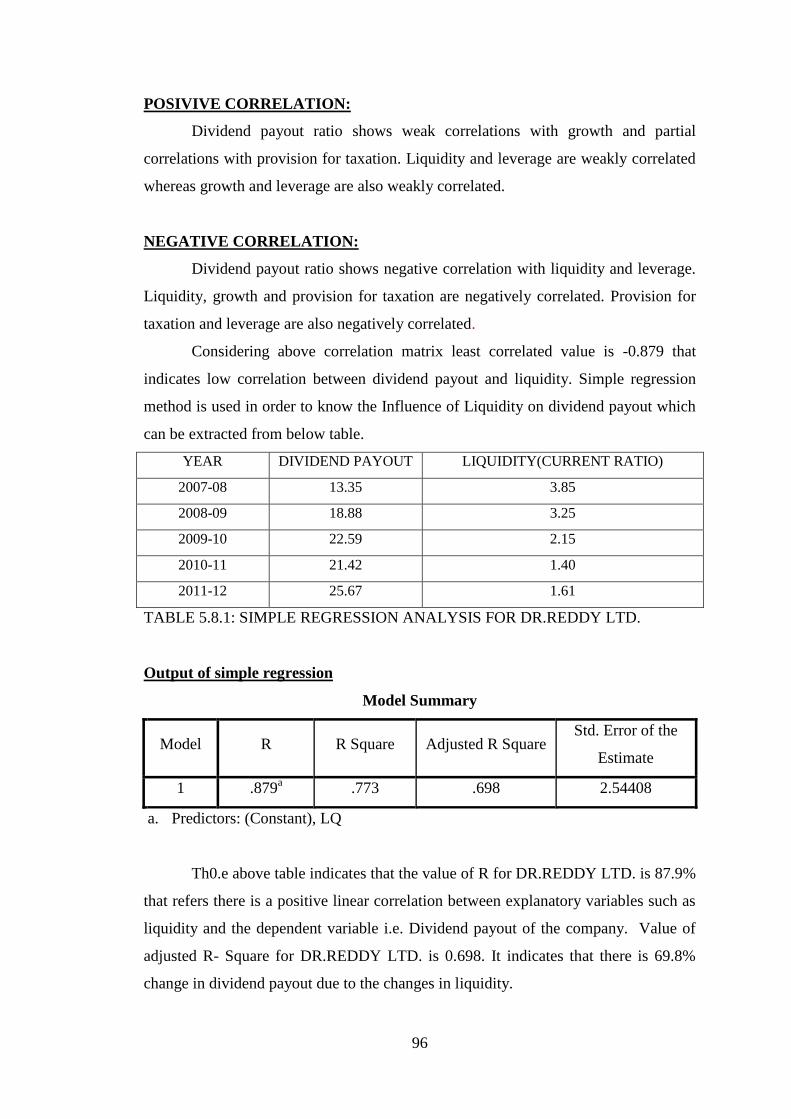

5.2.8 DR.REDDY LTD

YEAR DIVIDEND

PAYOUT

LIQUIDITY

(CURRENT

RATIO)

SIZE &

GROWTH(TOT

AL ASSETS)

LEVERAGE(DEB

T-EQUITY

RATIO)

PROVISION

FOR

TAXATION

2007-08 13.35 3.850041 12.60179 0.096078 18.64069

2008-09 18.88 3.25057 11.72978 0.121751 23.11172

2009-10 22.59 2.146451 9.399312 0.095222 22.00406

2010-11 21.42 1.402888 41.36552 0.106226 15.06797

2011-12 25.67 1.607844 11.62856 0.083435 27.5413

(Table no: 5.8 Dividend payout ratio and all independent variables

DR.REDDY LTD.)

In order to know the correlation of different variables with dividend payout

above table is used and on the basis of that, below correlation matrix is as follows:

Correlations

DPY LQ SG LV PT

DPY

Pearson Correlation 1 -.879* .076 -.365 .506

Sig. (2-tailed)

.049 .903 .546 .385

N 5 5 5 5 5

LQ

Pearson Correlation -.879* 1 -.508 .342 -.061

Sig. (2-tailed) .049

.382 .573 .922

N 5 5 5 5 5

SG

Pearson Correlation .076 -.508 1 .231 -.743

Sig. (2-tailed) .903 .382

.709 .150

N 5 5 5 5 5

LV

Pearson Correlation -.365 .342 .231 1 -.354

Sig. (2-tailed) .546 .573 .709

.559

N 5 5 5 5 5

PT

Pearson Correlation .506 -.061 -.743 -.354 1

Sig. (2-tailed) .385 .922 .150 .559

N 5 5 5 5 5

*. Correlation is significant at the 0.05 level (2-tailed).

96

POSIVIVE CORRELATION:

Dividend payout ratio shows weak correlations with growth and partial

correlations with provision for taxation. Liquidity and leverage are weakly correlated

whereas growth and leverage are also weakly correlated.

NEGATIVE CORRELATION:

Dividend payout ratio shows negative correlation with liquidity and leverage.

Liquidity, growth and provision for taxation are negatively correlated. Provision for

taxation and leverage are also negatively correlated.

Considering above correlation matrix least correlated value is -0.879 that

indicates low correlation between dividend payout and liquidity. Simple regression

method is used in order to know the Influence of Liquidity on dividend payout which

can be extracted from below table.

YEAR DIVIDEND PAYOUT LIQUIDITY(CURRENT RATIO)

2007-08 13.35 3.85

2008-09 18.88 3.25

2009-10 22.59 2.15

2010-11 21.42 1.40

2011-12 25.67 1.61

TABLE 5.8.1: SIMPLE REGRESSION ANALYSIS FOR DR.REDDY LTD.

Output of simple regression

Model Summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .879a .773 .698 2.54408

a. Predictors: (Constant), LQ

Th0.e above table indicates that the value of R for DR.REDDY LTD. is 87.9%

that refers there is a positive linear correlation between explanatory variables such as

liquidity and the dependent variable i.e. Dividend payout of the company. Value of

adjusted R- Square for DR.REDDY LTD. is 0.698. It indicates that there is 69.8%

change in dividend payout due to the changes in liquidity.

97

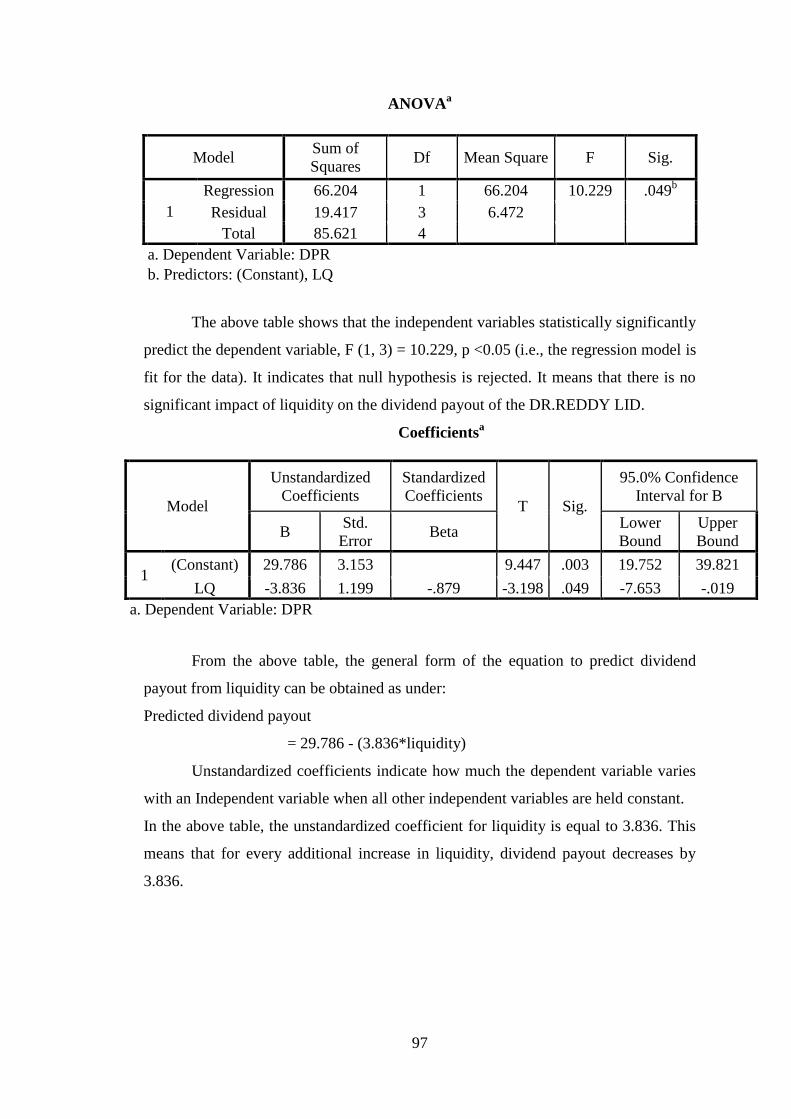

ANOVAa

Model Sum of

Squares Df Mean Square F Sig.

1

Regression 66.204 1 66.204 10.229 .049b

Residual 19.417 3 6.472

Total 85.621 4

a. Dependent Variable: DPR

b. Predictors: (Constant), LQ

The above table shows that the independent variables statistically significantly

predict the dependent variable, F (1, 3) = 10.229, p <0.05 (i.e., the regression model is

fit for the data). It indicates that null hypothesis is rejected. It means that there is no

significant impact of liquidity on the dividend payout of the DR.REDDY LID.

Coefficientsa

Model

Unstandardized

Coefficients

Standardized

Coefficients T Sig.

95.0% Confidence

Interval for B

B Std.

Error Beta

Lower

Bound

Upper

Bound

1 (Constant) 29.786 3.153 9.447 .003 19.752 39.821

LQ -3.836 1.199 -.879 -3.198 .049 -7.653 -.019

a. Dependent Variable: DPR

From the above table, the general form of the equation to predict dividend

payout from liquidity can be obtained as under:

Predicted dividend payout

= 29.786 - (3.836*liquidity)

Unstandardized coefficients indicate how much the dependent variable varies

with an Independent variable when all other independent variables are held constant.

In the above table, the unstandardized coefficient for liquidity is equal to 3.836. This

means that for every additional increase in liquidity, dividend payout decreases by

3.836.

98

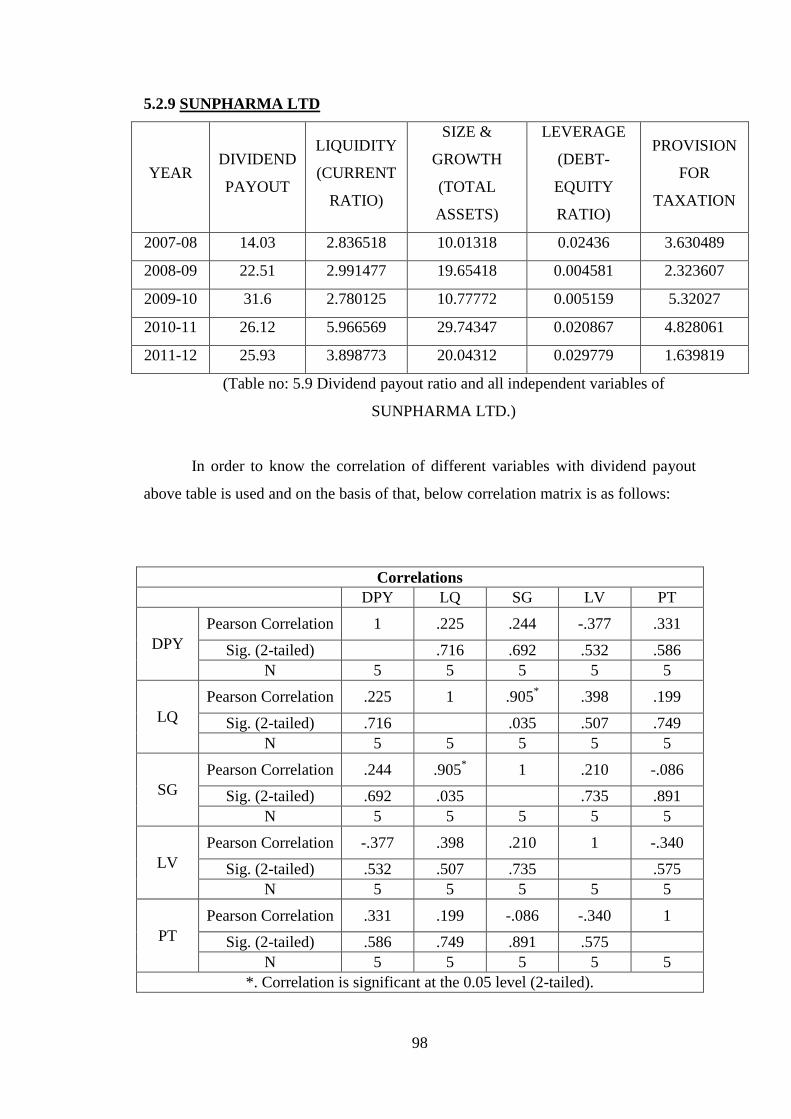

5.2.9 SUNPHARMA LTD

YEAR DIVIDEND

PAYOUT

LIQUIDITY

(CURRENT

RATIO)

SIZE &

GROWTH

(TOTAL

ASSETS)

LEVERAGE

(DEBT-

EQUITY

RATIO)

PROVISION

FOR

TAXATION

2007-08 14.03 2.836518 10.01318 0.02436 3.630489

2008-09 22.51 2.991477 19.65418 0.004581 2.323607

2009-10 31.6 2.780125 10.77772 0.005159 5.32027

2010-11 26.12 5.966569 29.74347 0.020867 4.828061

2011-12 25.93 3.898773 20.04312 0.029779 1.639819

(Table no: 5.9 Dividend payout ratio and all independent variables of

SUNPHARMA LTD.)

In order to know the correlation of different variables with dividend payout

above table is used and on the basis of that, below correlation matrix is as follows:

Correlations

DPY LQ SG LV PT

DPY

Pearson Correlation 1 .225 .244 -.377 .331

Sig. (2-tailed)

.716 .692 .532 .586

N 5 5 5 5 5

LQ

Pearson Correlation .225 1 .905* .398 .199

Sig. (2-tailed) .716

.035 .507 .749

N 5 5 5 5 5

SG

Pearson Correlation .244 .905* 1 .210 -.086

Sig. (2-tailed) .692 .035

.735 .891

N 5 5 5 5 5

LV

Pearson Correlation -.377 .398 .210 1 -.340

Sig. (2-tailed) .532 .507 .735

.575

N 5 5 5 5 5

PT

Pearson Correlation .331 .199 -.086 -.340 1

Sig. (2-tailed) .586 .749 .891 .575

N 5 5 5 5 5

*. Correlation is significant at the 0.05 level (2-tailed).

99

POSITIVE CORRELATION:

Dividend payout shows weak correlation with liquidity; growth and provision

for taxation. Liquidity and growth are significant and strong positively correlated.

Whereas liquidity, leverage and provision for taxation are weakly correlated. Growth

and leverage also weakly correlated.

NEGATIVE CORRELATION:

Dividend payout shows negative correlation with leverage. Provision for

taxation, growth and leverage are negatively correlated.

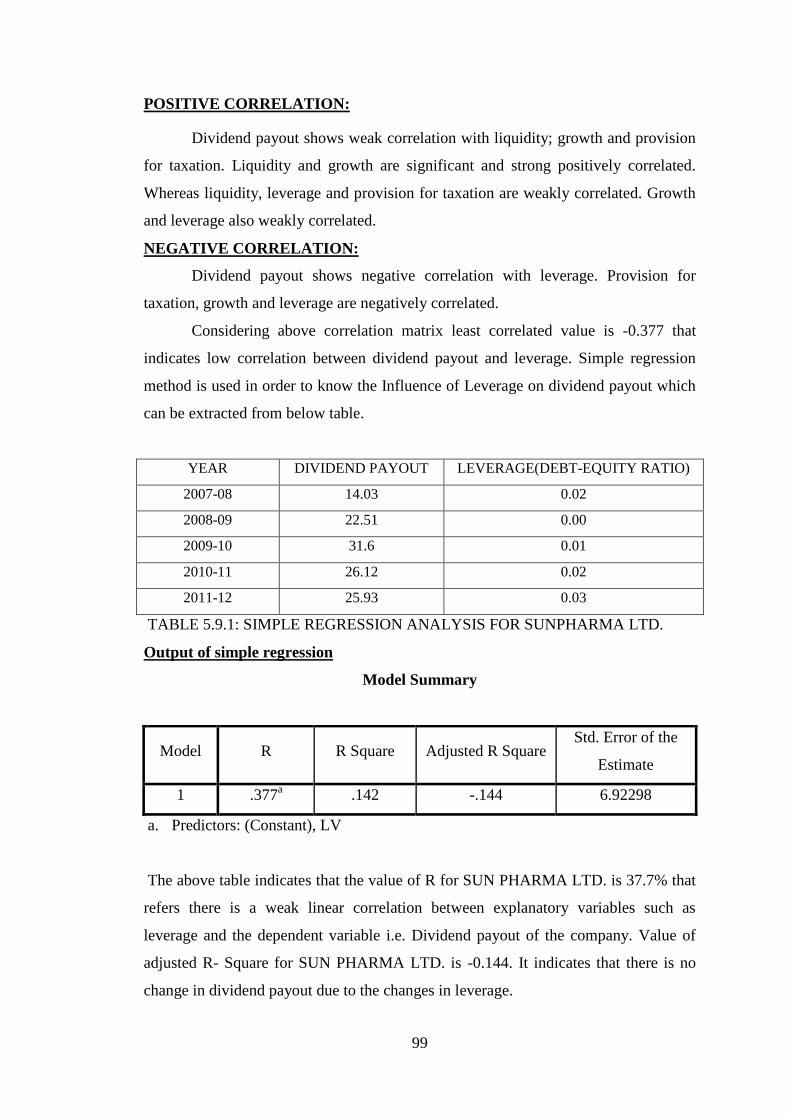

Considering above correlation matrix least correlated value is -0.377 that

indicates low correlation between dividend payout and leverage. Simple regression

method is used in order to know the Influence of Leverage on dividend payout which

can be extracted from below table.

YEAR DIVIDEND PAYOUT LEVERAGE(DEBT-EQUITY RATIO)

2007-08 14.03 0.02

2008-09 22.51 0.00

2009-10 31.6 0.01

2010-11 26.12 0.02

2011-12 25.93 0.03

TABLE 5.9.1: SIMPLE REGRESSION ANALYSIS FOR SUNPHARMA LTD.

Output of simple regression

Model Summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .377a .142 -.144 6.92298

a. Predictors: (Constant), LV

The above table indicates that the value of R for SUN PHARMA LTD. is 37.7% that

refers there is a weak linear correlation between explanatory variables such as

leverage and the dependent variable i.e. Dividend payout of the company. Value of

adjusted R- Square for SUN PHARMA LTD. is -0.144. It indicates that there is no

change in dividend payout due to the changes in leverage.

100

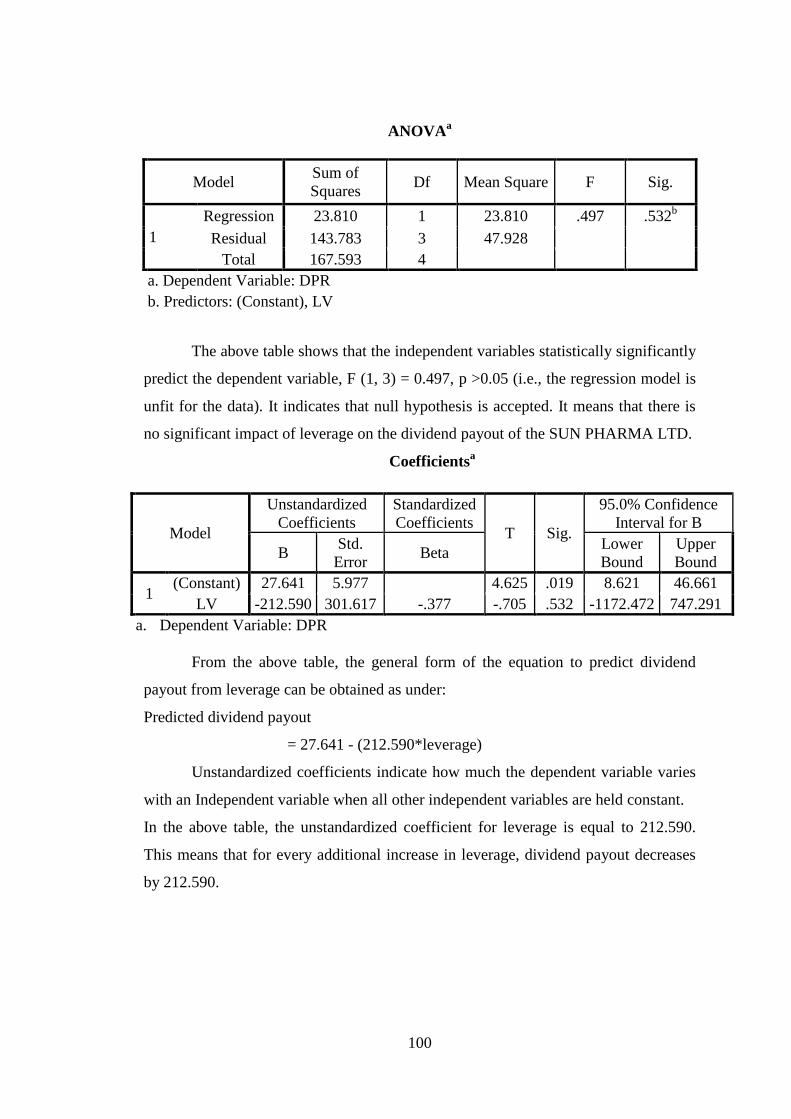

ANOVAa

Model Sum of

Squares Df Mean Square F Sig.

1

Regression 23.810 1 23.810 .497 .532b

Residual 143.783 3 47.928

Total 167.593 4

a. Dependent Variable: DPR

b. Predictors: (Constant), LV

The above table shows that the independent variables statistically significantly

predict the dependent variable, F (1, 3) = 0.497, p >0.05 (i.e., the regression model is

unfit for the data). It indicates that null hypothesis is accepted. It means that there is

no significant impact of leverage on the dividend payout of the SUN PHARMA LTD.

Coefficientsa

Model

Unstandardized

Coefficients

Standardized

Coefficients T Sig.

95.0% Confidence

Interval for B

B Std.

Error Beta

Lower

Bound

Upper

Bound

1 (Constant) 27.641 5.977 4.625 .019 8.621 46.661

LV -212.590 301.617 -.377 -.705 .532 -1172.472 747.291

a. Dependent Variable: DPR

From the above table, the general form of the equation to predict dividend

payout from leverage can be obtained as under:

Predicted dividend payout

= 27.641 - (212.590*leverage)

Unstandardized coefficients indicate how much the dependent variable varies

with an Independent variable when all other independent variables are held constant.

In the above table, the unstandardized coefficient for leverage is equal to 212.590.

This means that for every additional increase in leverage, dividend payout decreases

by 212.590.

101

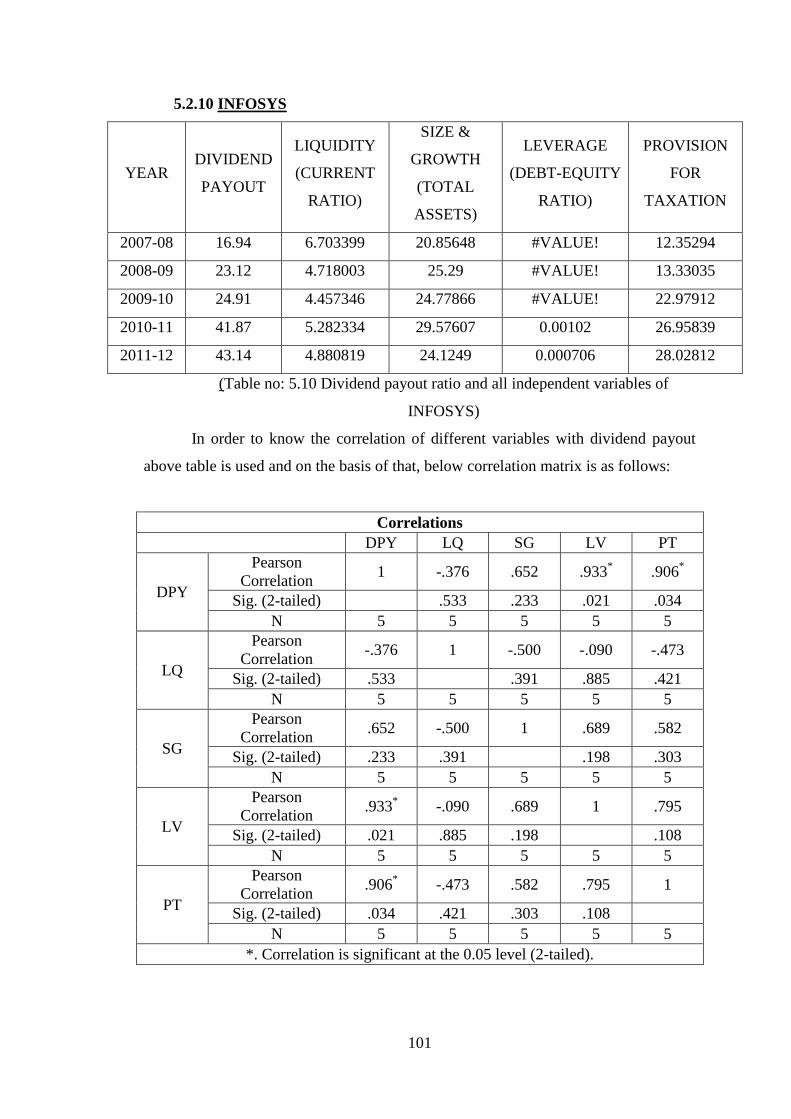

5.2.10 INFOSYS

YEAR DIVIDEND

PAYOUT

LIQUIDITY

(CURRENT

RATIO)

SIZE &

GROWTH

(TOTAL

ASSETS)

LEVERAGE

(DEBT-EQUITY

RATIO)

PROVISION

FOR

TAXATION

2007-08 16.94 6.703399 20.85648 #VALUE! 12.35294

2008-09 23.12 4.718003 25.29 #VALUE! 13.33035

2009-10 24.91 4.457346 24.77866 #VALUE! 22.97912

2010-11 41.87 5.282334 29.57607 0.00102 26.95839

2011-12 43.14 4.880819 24.1249 0.000706 28.02812

(Table no: 5.10 Dividend payout ratio and all independent variables of

INFOSYS)

In order to know the correlation of different variables with dividend payout

above table is used and on the basis of that, below correlation matrix is as follows:

Correlations

DPY LQ SG LV PT

DPY

Pearson

Correlation 1 -.376 .652 .933

* .906

*

Sig. (2-tailed)

.533 .233 .021 .034

N 5 5 5 5 5

LQ

Pearson

Correlation -.376 1 -.500 -.090 -.473

Sig. (2-tailed) .533

.391 .885 .421

N 5 5 5 5 5

SG

Pearson

Correlation .652 -.500 1 .689 .582

Sig. (2-tailed) .233 .391

.198 .303

N 5 5 5 5 5

LV

Pearson

Correlation .933

* -.090 .689 1 .795

Sig. (2-tailed) .021 .885 .198

.108

N 5 5 5 5 5

PT

Pearson

Correlation .906

* -.473 .582 .795 1

Sig. (2-tailed) .034 .421 .303 .108

N 5 5 5 5 5

*. Correlation is significant at the 0.05 level (2-tailed).

102

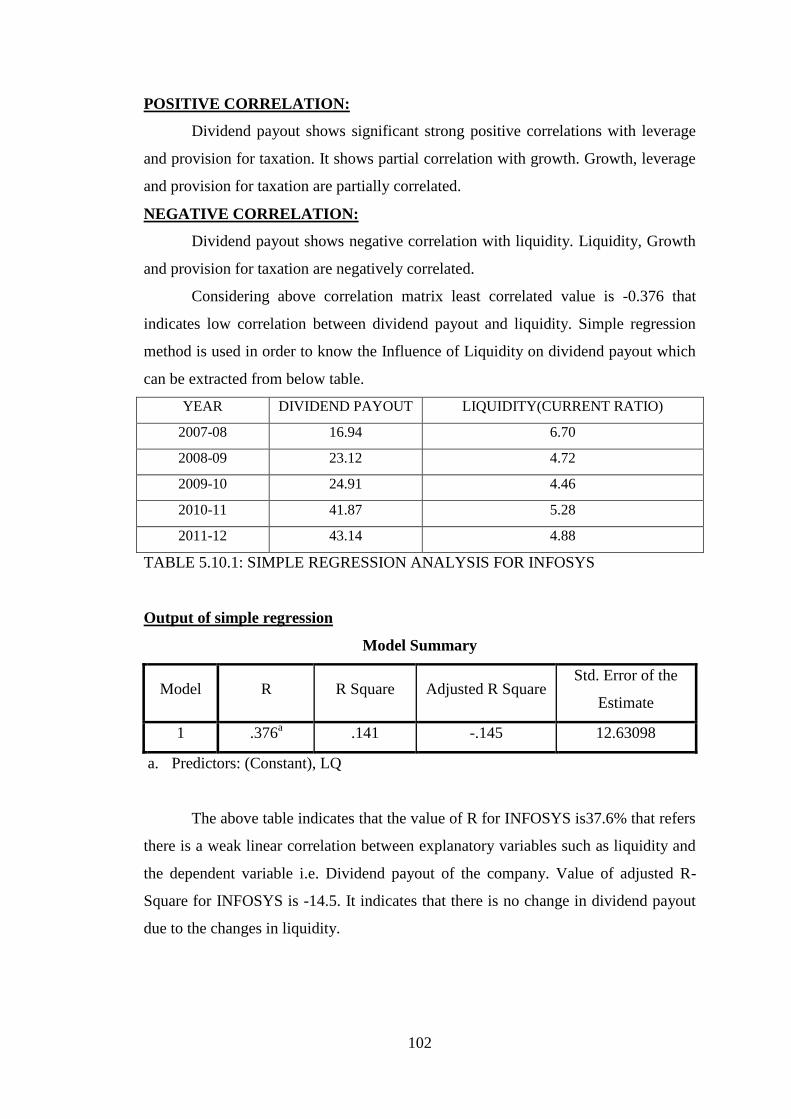

POSITIVE CORRELATION:

Dividend payout shows significant strong positive correlations with leverage

and provision for taxation. It shows partial correlation with growth. Growth, leverage

and provision for taxation are partially correlated.

NEGATIVE CORRELATION:

Dividend payout shows negative correlation with liquidity. Liquidity, Growth

and provision for taxation are negatively correlated.

Considering above correlation matrix least correlated value is -0.376 that

indicates low correlation between dividend payout and liquidity. Simple regression

method is used in order to know the Influence of Liquidity on dividend payout which

can be extracted from below table.

YEAR DIVIDEND PAYOUT LIQUIDITY(CURRENT RATIO)

2007-08 16.94 6.70

2008-09 23.12 4.72

2009-10 24.91 4.46

2010-11 41.87 5.28

2011-12 43.14 4.88

TABLE 5.10.1: SIMPLE REGRESSION ANALYSIS FOR INFOSYS

Output of simple regression

Model Summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .376a .141 -.145 12.63098

a. Predictors: (Constant), LQ

The above table indicates that the value of R for INFOSYS is37.6% that refers

there is a weak linear correlation between explanatory variables such as liquidity and

the dependent variable i.e. Dividend payout of the company. Value of adjusted R-

Square for INFOSYS is -14.5. It indicates that there is no change in dividend payout

due to the changes in liquidity.

103

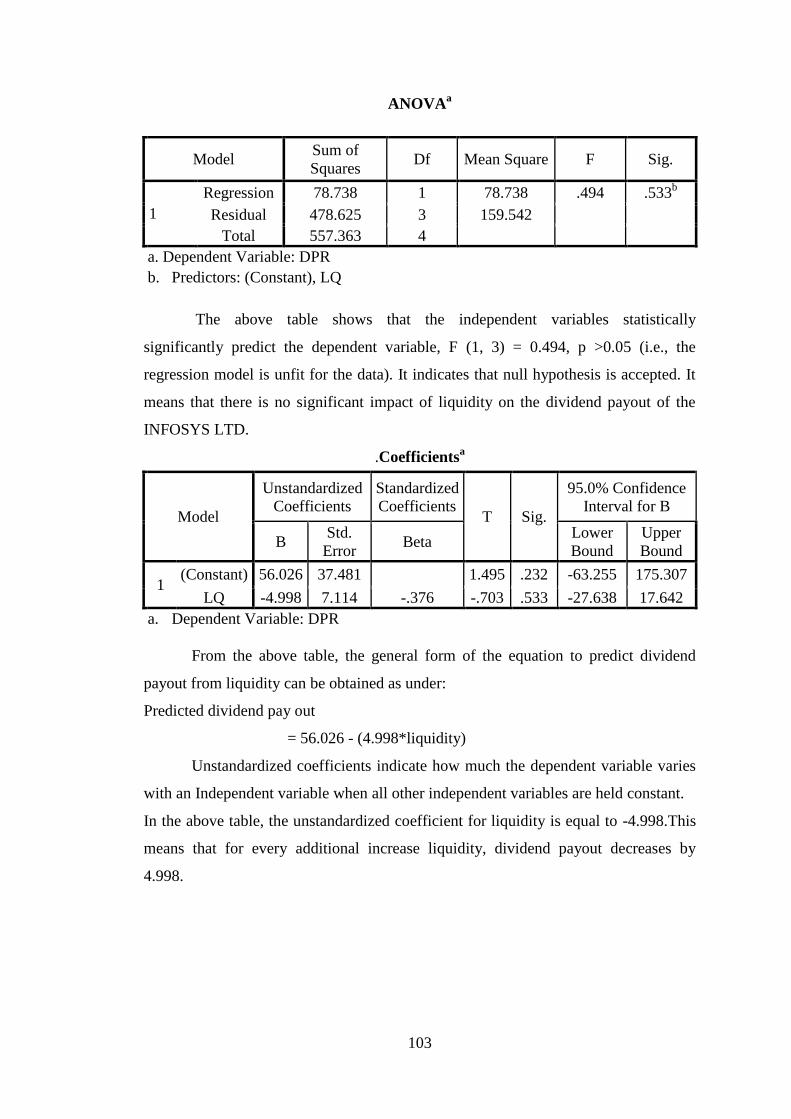

ANOVAa

Model Sum of

Squares Df Mean Square F Sig.

1

Regression 78.738 1 78.738 .494 .533b

Residual 478.625 3 159.542

Total 557.363 4

a. Dependent Variable: DPR

b. Predictors: (Constant), LQ

The above table shows that the independent variables statistically

significantly predict the dependent variable, F (1, 3) = 0.494, p >0.05 (i.e., the

regression model is unfit for the data). It indicates that null hypothesis is accepted. It

means that there is no significant impact of liquidity on the dividend payout of the

INFOSYS LTD.

.Coefficientsa

Model

Unstandardized

Coefficients

Standardized

Coefficients T Sig.

95.0% Confidence

Interval for B

B Std.

Error Beta

Lower

Bound

Upper

Bound

1 (Constant) 56.026 37.481 1.495 .232 -63.255 175.307

LQ -4.998 7.114 -.376 -.703 .533 -27.638 17.642

a. Dependent Variable: DPR

From the above table, the general form of the equation to predict dividend

payout from liquidity can be obtained as under:

Predicted dividend pay out

= 56.026 - (4.998*liquidity)

Unstandardized coefficients indicate how much the dependent variable varies

with an Independent variable when all other independent variables are held constant.

In the above table, the unstandardized coefficient for liquidity is equal to -4.998.This

means that for every additional increase liquidity, dividend payout decreases by

4.998.

104

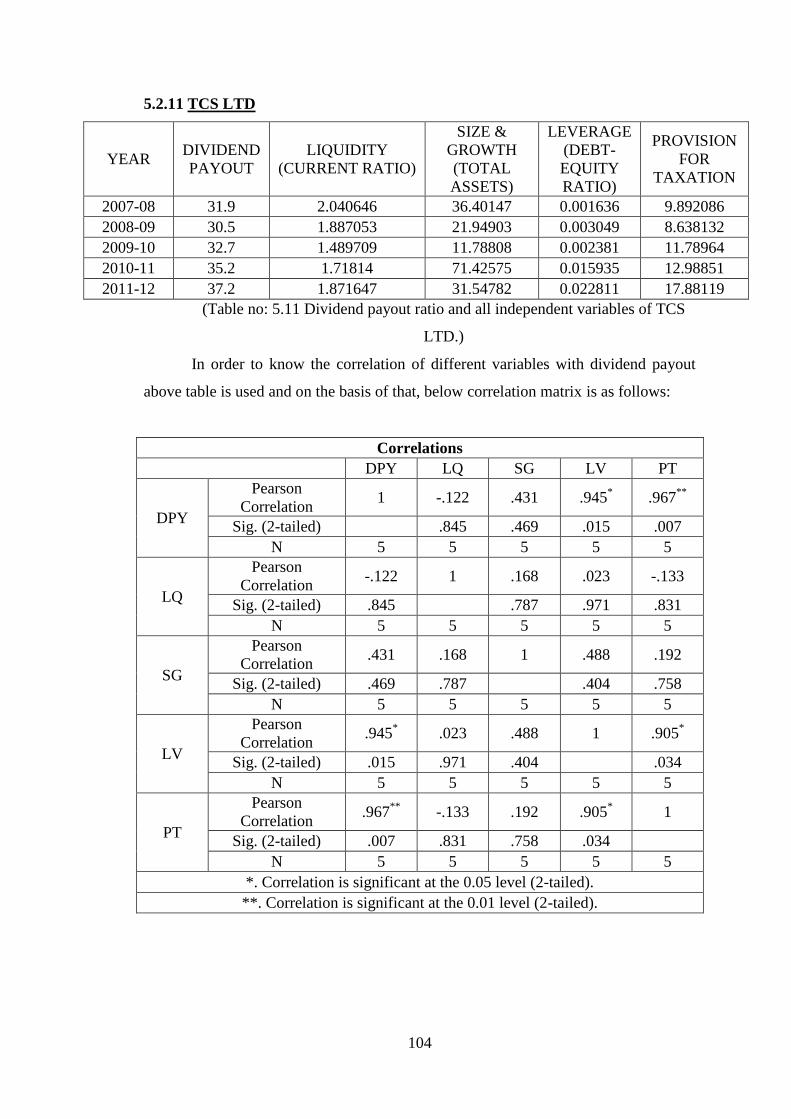

5.2.11 TCS LTD

YEAR DIVIDEND

PAYOUT

LIQUIDITY

(CURRENT RATIO)

SIZE &

GROWTH

(TOTAL

ASSETS)

LEVERAGE

(DEBT-

EQUITY

RATIO)

PROVISION

FOR

TAXATION

2007-08 31.9 2.040646 36.40147 0.001636 9.892086

2008-09 30.5 1.887053 21.94903 0.003049 8.638132

2009-10 32.7 1.489709 11.78808 0.002381 11.78964

2010-11 35.2 1.71814 71.42575 0.015935 12.98851

2011-12 37.2 1.871647 31.54782 0.022811 17.88119

(Table no: 5.11 Dividend payout ratio and all independent variables of TCS

LTD.)

In order to know the correlation of different variables with dividend payout

above table is used and on the basis of that, below correlation matrix is as follows:

Correlations

DPY LQ SG LV PT

DPY

Pearson

Correlation 1 -.122 .431 .945

* .967

**

Sig. (2-tailed)

.845 .469 .015 .007

N 5 5 5 5 5

LQ

Pearson

Correlation -.122 1 .168 .023 -.133

Sig. (2-tailed) .845

.787 .971 .831

N 5 5 5 5 5

SG

Pearson

Correlation .431 .168 1 .488 .192

Sig. (2-tailed) .469 .787

.404 .758

N 5 5 5 5 5

LV

Pearson

Correlation .945

* .023 .488 1 .905

*

Sig. (2-tailed) .015 .971 .404

.034

N 5 5 5 5 5

PT

Pearson

Correlation .967

** -.133 .192 .905

* 1

Sig. (2-tailed) .007 .831 .758 .034

N 5 5 5 5 5

*. Correlation is significant at the 0.05 level (2-tailed).

**. Correlation is significant at the 0.01 level (2-tailed).

105

POSITIVE CORRELATION:

Dividend payout is significant and strong positively correlated with leverage

and provision for taxation. Dividend payout is weakly correlated with growth.

Liquidity, growth and leverage are weakly correlated. Growth, leverage and provision

for taxation are also weakly correlated. Leverage shows significant and strong

positive relationship with provision for taxation.

NEGATIVE CORRELATION:

Dividend payout shows negative correlation with liquidity. Provision for

taxation and liquidity are negatively correlated.

Considering above correlation matrix least correlated value is -0.122 that

indicates low correlation between dividend payout and liquidity. Simple regression

method is used in order to know the Influence of Liquidity on dividend payout which

can be extracted from below table.

YEAR DIVIDEND PAYOUT LIQUIDITY(CURRENT RATIO)

2007-08 31.9 2.04

2008-09 30.5 1.89

2009-10 32.7 1.49

2010-11 35.2 1.72

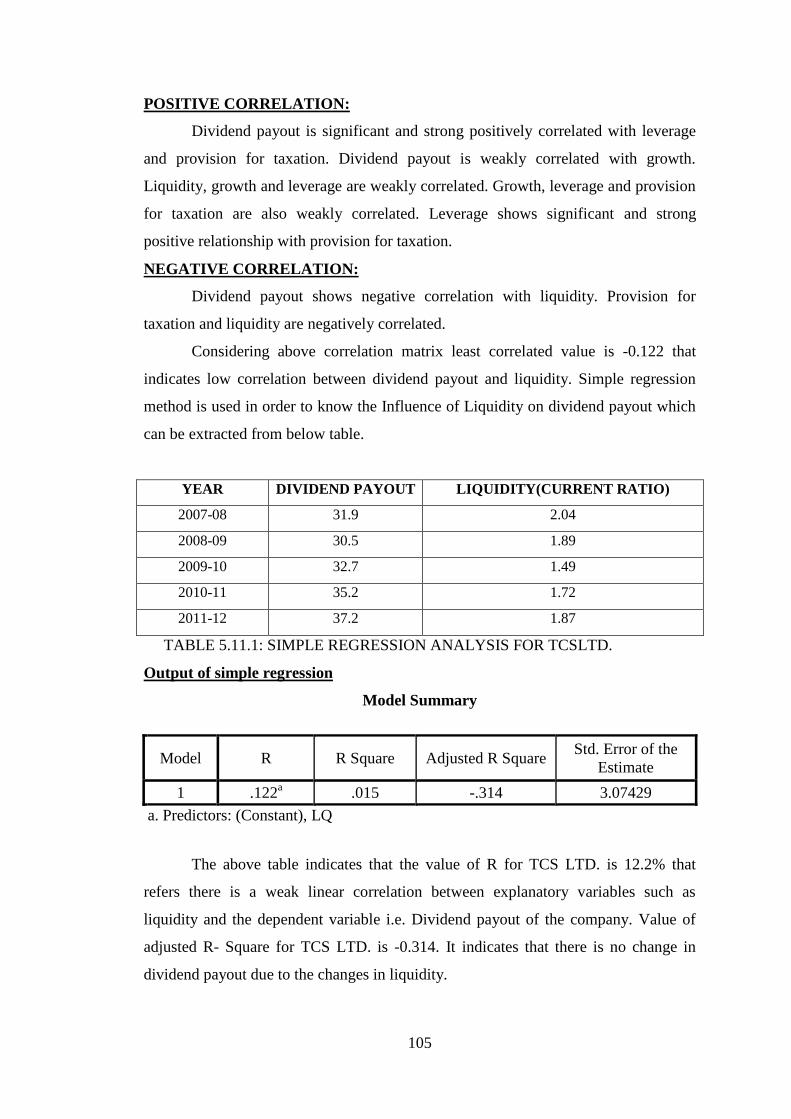

2011-12 37.2 1.87

TABLE 5.11.1: SIMPLE REGRESSION ANALYSIS FOR TCSLTD.

Output of simple regression

Model Summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .122a .015 -.314 3.07429

a. Predictors: (Constant), LQ

The above table indicates that the value of R for TCS LTD. is 12.2% that

refers there is a weak linear correlation between explanatory variables such as

liquidity and the dependent variable i.e. Dividend payout of the company. Value of

adjusted R- Square for TCS LTD. is -0.314. It indicates that there is no change in

dividend payout due to the changes in liquidity.

106

ANOVAa

Model Sum of

Squares Df Mean Square F Sig.

1

Regression .426 1 .426 .045 .845b

Residual 28.354 3 9.451

Total 28.780 4

a. Dependent Variable: DPR

b. Predictors: (Constant), LQ

The above table shows that the independent variables statistically significantly

predict the dependent variable, F (1, 3) = 0.045, p >0.05 (i.e., the regression model is

unfit for the data). It indicates that null hypothesis is accepted. It means that there is

no significant impact of liquidity on the dividend payout of TCS.

Coefficientsa

Model

Unstandardized

Coefficients

Standardized

Coefficients T Sig.

95.0% Confidence

Interval for B

B Std.

Error Beta

Lower

Bound

Upper

Bound

1 (Constant) 36.323 13.363 2.718 .073 -6.205 78.850

LQ -1.567 7.379 -.122 -.212 .845 -25.049 21.915

a. Dependent Variable: DPR

From the above table, the general form of the equation to predict dividend

payout from liquidity can be obtained as under:

Predicted dividend payout

= 36.323 - (1.567*liquidity)

Unstandardized coefficients indicate how much the dependent variable varies

with an Independent variable when all other independent variables are held constant.

In the above table, the unstandardized coefficient for liquidity is equal to -1.567. This

means that for every additional increase in liquidity, dividend payout Decreases by

1.567.

107

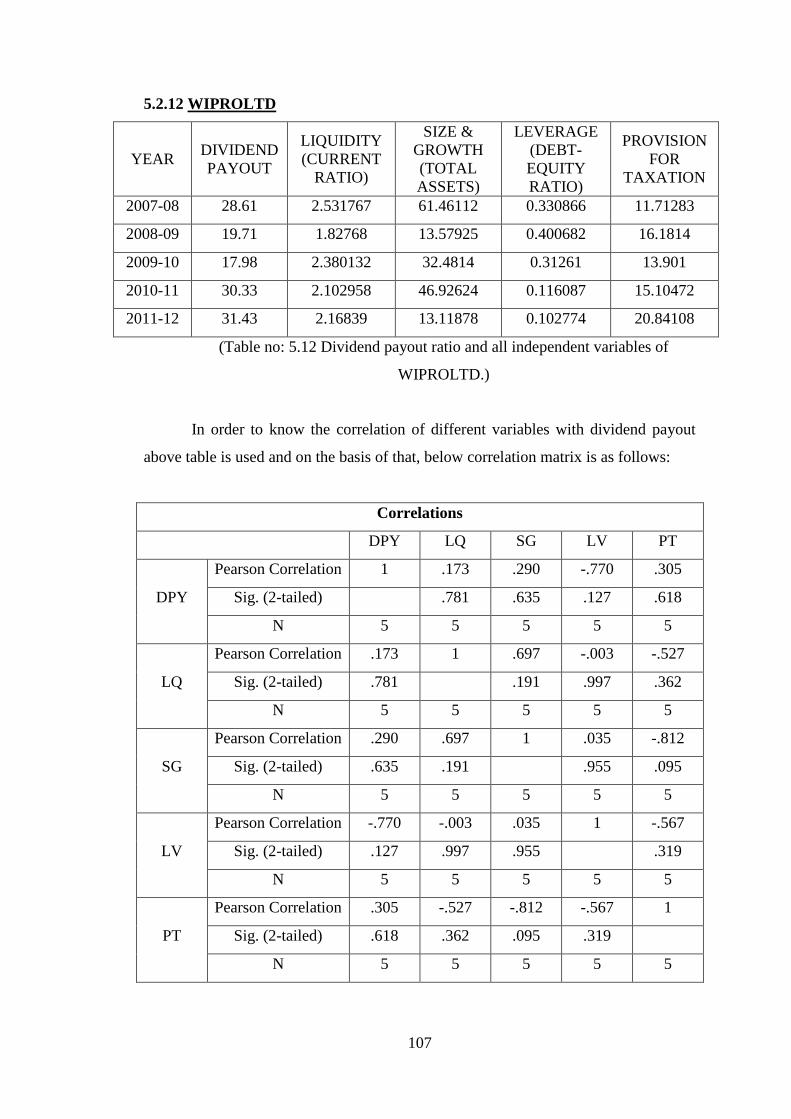

5.2.12 WIPROLTD

YEAR DIVIDEND

PAYOUT

LIQUIDITY

(CURRENT

RATIO)

SIZE &

GROWTH

(TOTAL

ASSETS)

LEVERAGE

(DEBT-

EQUITY

RATIO)

PROVISION

FOR

TAXATION

2007-08 28.61 2.531767 61.46112 0.330866 11.71283

2008-09 19.71 1.82768 13.57925 0.400682 16.1814

2009-10 17.98 2.380132 32.4814 0.31261 13.901

2010-11 30.33 2.102958 46.92624 0.116087 15.10472

2011-12 31.43 2.16839 13.11878 0.102774 20.84108

(Table no: 5.12 Dividend payout ratio and all independent variables of

WIPROLTD.)

In order to know the correlation of different variables with dividend payout

above table is used and on the basis of that, below correlation matrix is as follows:

Correlations

DPY LQ SG LV PT

DPY

Pearson Correlation 1 .173 .290 -.770 .305

Sig. (2-tailed)

.781 .635 .127 .618

N 5 5 5 5 5

LQ

Pearson Correlation .173 1 .697 -.003 -.527

Sig. (2-tailed) .781

.191 .997 .362

N 5 5 5 5 5

SG

Pearson Correlation .290 .697 1 .035 -.812

Sig. (2-tailed) .635 .191

.955 .095

N 5 5 5 5 5

LV

Pearson Correlation -.770 -.003 .035 1 -.567

Sig. (2-tailed) .127 .997 .955

.319

N 5 5 5 5 5

PT

Pearson Correlation .305 -.527 -.812 -.567 1

Sig. (2-tailed) .618 .362 .095 .319

N 5 5 5 5 5

108

POSITIVE CORRELATION:

Dividend payout shows weak correlation with liquidity, growth and provision

for taxation. Liquidity and growth are partially correlated. Growth and leverage are

weakly correlated.

NEGATIVE CORRELATION:

Dividend payout shows negative correlation with leverage. Provision for

taxation, liquidity, leverage and growth are negatively correlated.

Considering above correlation matrix least correlated value is -0.770 that

indicates low correlation between dividend payout and leverage. Simple regression

method is used in order to know the Influence of Leverage on dividend payout which

can be extracted from below table.

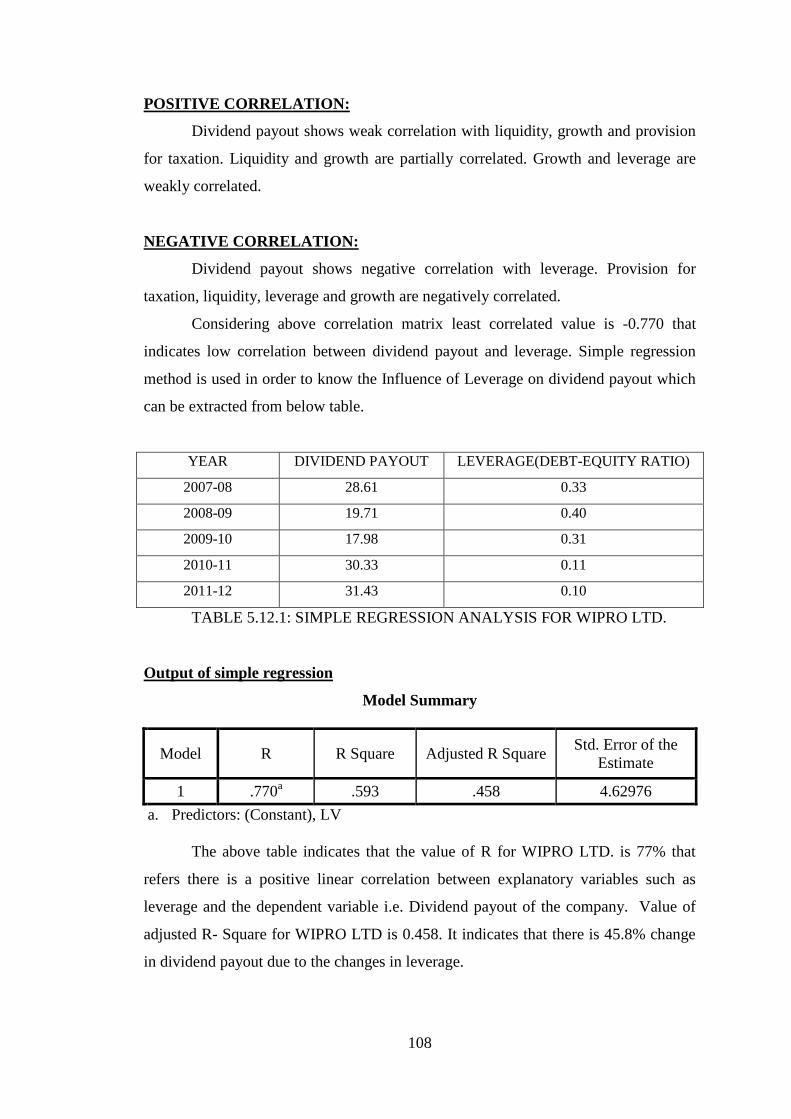

YEAR DIVIDEND PAYOUT LEVERAGE(DEBT-EQUITY RATIO)

2007-08 28.61 0.33

2008-09 19.71 0.40

2009-10 17.98 0.31

2010-11 30.33 0.11

2011-12 31.43 0.10

TABLE 5.12.1: SIMPLE REGRESSION ANALYSIS FOR WIPRO LTD.

Output of simple regression

Model Summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .770a .593 .458 4.62976

a. Predictors: (Constant), LV

The above table indicates that the value of R for WIPRO LTD. is 77% that

refers there is a positive linear correlation between explanatory variables such as

leverage and the dependent variable i.e. Dividend payout of the company. Value of

adjusted R- Square for WIPRO LTD is 0.458. It indicates that there is 45.8% change

in dividend payout due to the changes in leverage.

109

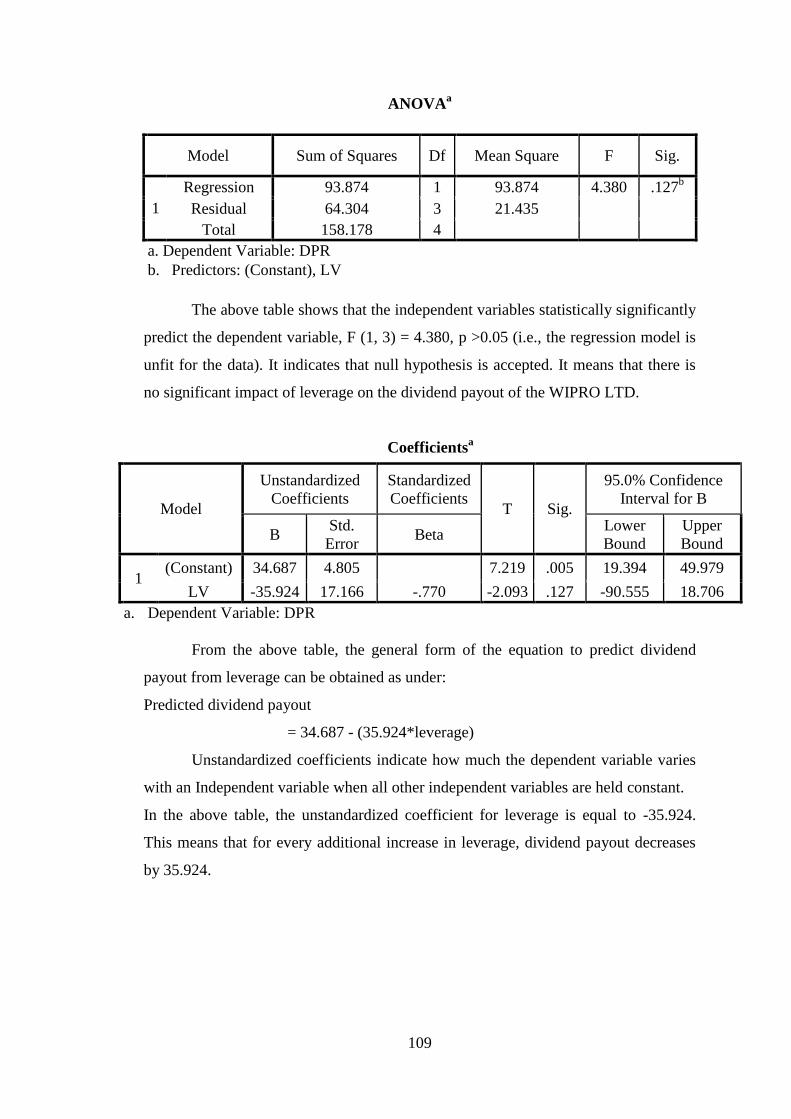

ANOVAa

Model Sum of Squares Df Mean Square F Sig.

1

Regression 93.874 1 93.874 4.380 .127b

Residual 64.304 3 21.435

Total 158.178 4

a. Dependent Variable: DPR

b. Predictors: (Constant), LV

The above table shows that the independent variables statistically significantly

predict the dependent variable, F (1, 3) = 4.380, p >0.05 (i.e., the regression model is

unfit for the data). It indicates that null hypothesis is accepted. It means that there is

no significant impact of leverage on the dividend payout of the WIPRO LTD.

Coefficientsa

Model

Unstandardized

Coefficients

Standardized

Coefficients T Sig.

95.0% Confidence

Interval for B

B Std.

Error Beta

Lower

Bound

Upper

Bound

1 (Constant) 34.687 4.805 7.219 .005 19.394 49.979

LV -35.924 17.166 -.770 -2.093 .127 -90.555 18.706

a. Dependent Variable: DPR

From the above table, the general form of the equation to predict dividend

payout from leverage can be obtained as under:

Predicted dividend payout

= 34.687 - (35.924*leverage)

Unstandardized coefficients indicate how much the dependent variable varies

with an Independent variable when all other independent variables are held constant.

In the above table, the unstandardized coefficient for leverage is equal to -35.924.

This means that for every additional increase in leverage, dividend payout decreases

by 35.924.

110

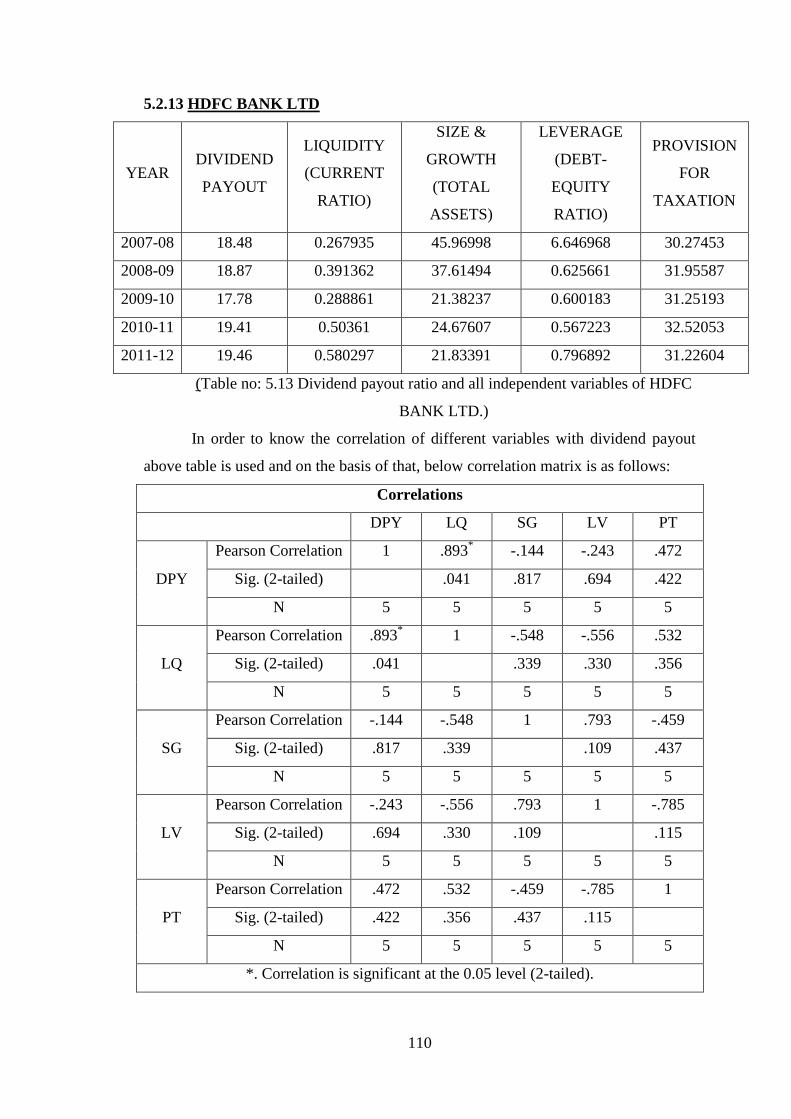

5.2.13 HDFC BANK LTD

YEAR DIVIDEND

PAYOUT

LIQUIDITY

(CURRENT

RATIO)

SIZE &

GROWTH

(TOTAL

ASSETS)

LEVERAGE

(DEBT-

EQUITY

RATIO)

PROVISION

FOR

TAXATION

2007-08 18.48 0.267935 45.96998 6.646968 30.27453

2008-09 18.87 0.391362 37.61494 0.625661 31.95587

2009-10 17.78 0.288861 21.38237 0.600183 31.25193

2010-11 19.41 0.50361 24.67607 0.567223 32.52053

2011-12 19.46 0.580297 21.83391 0.796892 31.22604

(Table no: 5.13 Dividend payout ratio and all independent variables of HDFC

BANK LTD.)

In order to know the correlation of different variables with dividend payout

above table is used and on the basis of that, below correlation matrix is as follows:

Correlations

DPY LQ SG LV PT

DPY

Pearson Correlation 1 .893* -.144 -.243 .472

Sig. (2-tailed)

.041 .817 .694 .422

N 5 5 5 5 5

LQ

Pearson Correlation .893* 1 -.548 -.556 .532

Sig. (2-tailed) .041

.339 .330 .356

N 5 5 5 5 5

SG

Pearson Correlation -.144 -.548 1 .793 -.459

Sig. (2-tailed) .817 .339

.109 .437

N 5 5 5 5 5

LV

Pearson Correlation -.243 -.556 .793 1 -.785

Sig. (2-tailed) .694 .330 .109

.115

N 5 5 5 5 5

PT

Pearson Correlation .472 .532 -.459 -.785 1

Sig. (2-tailed) .422 .356 .437 .115

N 5 5 5 5 5

*. Correlation is significant at the 0.05 level (2-tailed).

111

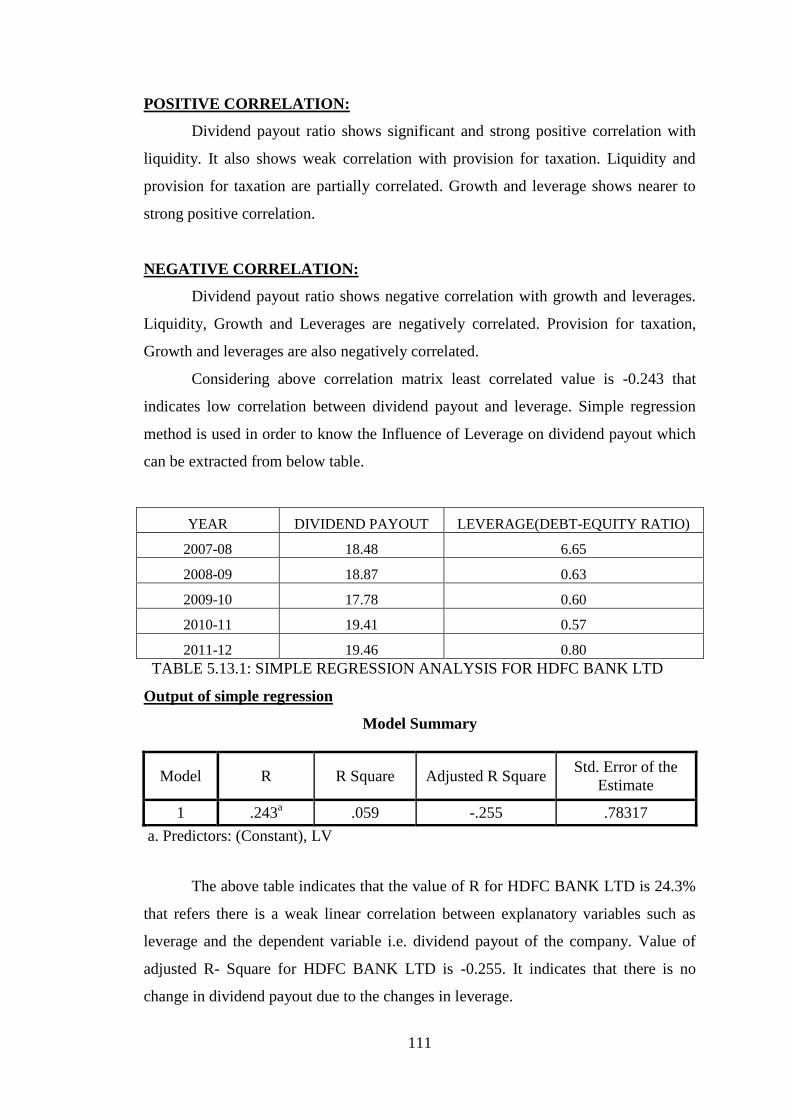

POSITIVE CORRELATION:

Dividend payout ratio shows significant and strong positive correlation with

liquidity. It also shows weak correlation with provision for taxation. Liquidity and

provision for taxation are partially correlated. Growth and leverage shows nearer to

strong positive correlation.

NEGATIVE CORRELATION:

Dividend payout ratio shows negative correlation with growth and leverages.

Liquidity, Growth and Leverages are negatively correlated. Provision for taxation,

Growth and leverages are also negatively correlated.

Considering above correlation matrix least correlated value is -0.243 that

indicates low correlation between dividend payout and leverage. Simple regression

method is used in order to know the Influence of Leverage on dividend payout which

can be extracted from below table.

YEAR DIVIDEND PAYOUT LEVERAGE(DEBT-EQUITY RATIO)

2007-08 18.48 6.65

2008-09 18.87 0.63

2009-10 17.78 0.60

2010-11 19.41 0.57

2011-12 19.46 0.80

TABLE 5.13.1: SIMPLE REGRESSION ANALYSIS FOR HDFC BANK LTD

Output of simple regression

Model Summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .243a .059 -.255 .78317

a. Predictors: (Constant), LV

The above table indicates that the value of R for HDFC BANK LTD is 24.3%

that refers there is a weak linear correlation between explanatory variables such as

leverage and the dependent variable i.e. dividend payout of the company. Value of

adjusted R- Square for HDFC BANK LTD is -0.255. It indicates that there is no

change in dividend payout due to the changes in leverage.

112

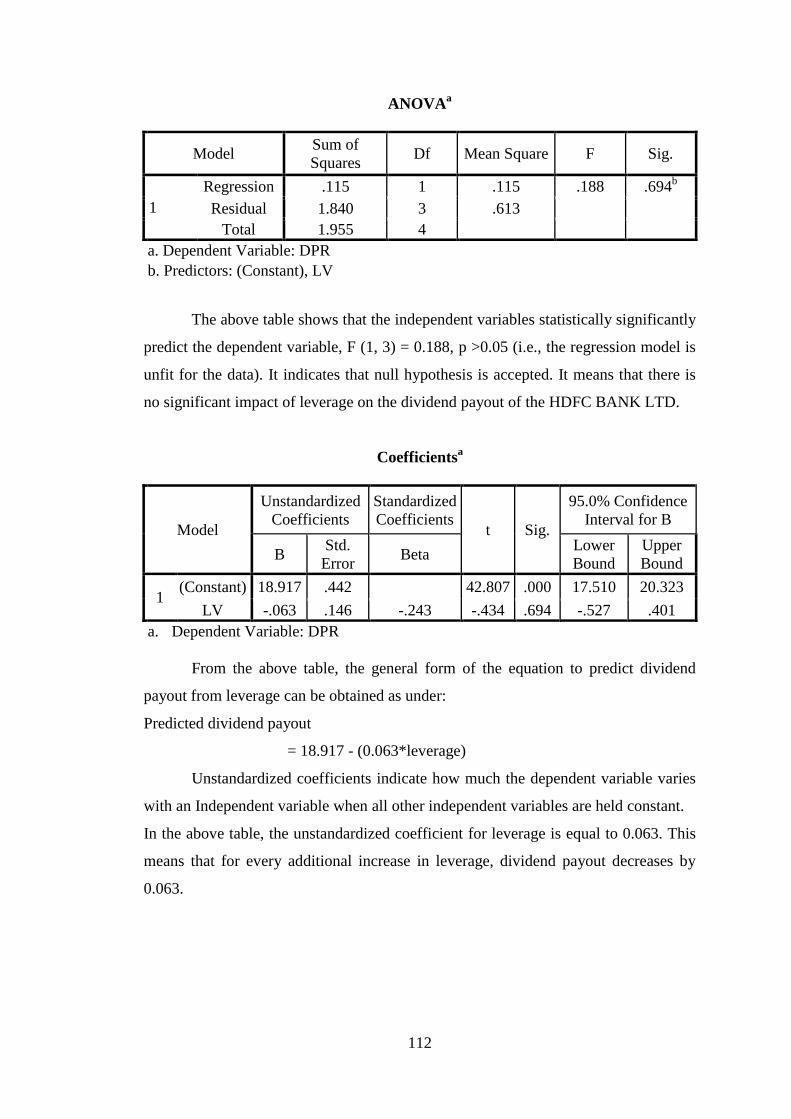

ANOVAa

Model Sum of

Squares Df Mean Square F Sig.

1

Regression .115 1 .115 .188 .694b

Residual 1.840 3 .613

Total 1.955 4

a. Dependent Variable: DPR

b. Predictors: (Constant), LV

The above table shows that the independent variables statistically significantly

predict the dependent variable, F (1, 3) = 0.188, p >0.05 (i.e., the regression model is

unfit for the data). It indicates that null hypothesis is accepted. It means that there is

no significant impact of leverage on the dividend payout of the HDFC BANK LTD.

Coefficientsa

Model

Unstandardized

Coefficients

Standardized

Coefficients t Sig.

95.0% Confidence

Interval for B

B Std.

Error Beta

Lower

Bound

Upper

Bound

1 (Constant) 18.917 .442 42.807 .000 17.510 20.323

LV -.063 .146 -.243 -.434 .694 -.527 .401

a. Dependent Variable: DPR

From the above table, the general form of the equation to predict dividend

payout from leverage can be obtained as under:

Predicted dividend payout

= 18.917 - (0.063*leverage)

Unstandardized coefficients indicate how much the dependent variable varies

with an Independent variable when all other independent variables are held constant.

In the above table, the unstandardized coefficient for leverage is equal to 0.063. This

means that for every additional increase in leverage, dividend payout decreases by

0.063.

113

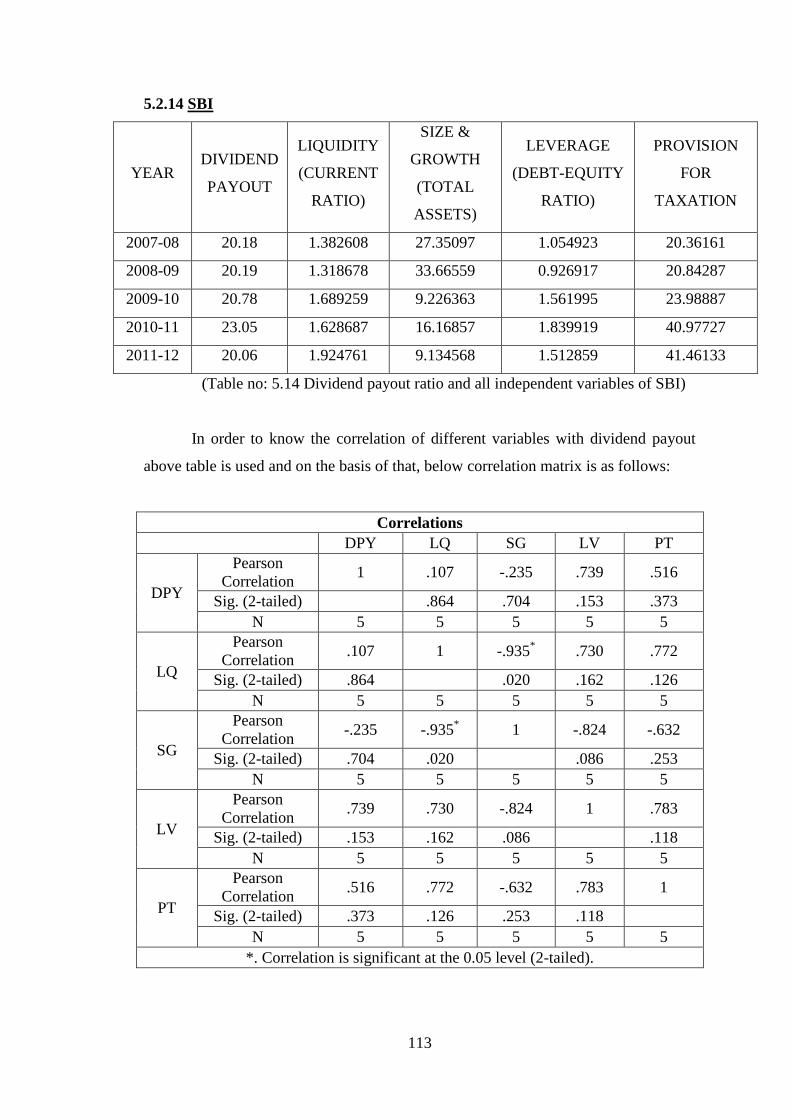

5.2.14 SBI

YEAR DIVIDEND

PAYOUT

LIQUIDITY

(CURRENT

RATIO)

SIZE &

GROWTH

(TOTAL

ASSETS)

LEVERAGE

(DEBT-EQUITY

RATIO)

PROVISION

FOR

TAXATION

2007-08 20.18 1.382608 27.35097 1.054923 20.36161

2008-09 20.19 1.318678 33.66559 0.926917 20.84287

2009-10 20.78 1.689259 9.226363 1.561995 23.98887

2010-11 23.05 1.628687 16.16857 1.839919 40.97727

2011-12 20.06 1.924761 9.134568 1.512859 41.46133

(Table no: 5.14 Dividend payout ratio and all independent variables of SBI)

In order to know the correlation of different variables with dividend payout

above table is used and on the basis of that, below correlation matrix is as follows:

Correlations

DPY LQ SG LV PT

DPY

Pearson

Correlation 1 .107 -.235 .739 .516

Sig. (2-tailed)

.864 .704 .153 .373

N 5 5 5 5 5

LQ

Pearson

Correlation .107 1 -.935

* .730 .772

Sig. (2-tailed) .864

.020 .162 .126

N 5 5 5 5 5

SG

Pearson

Correlation -.235 -.935

* 1 -.824 -.632

Sig. (2-tailed) .704 .020

.086 .253

N 5 5 5 5 5

LV

Pearson

Correlation .739 .730 -.824 1 .783

Sig. (2-tailed) .153 .162 .086

.118

N 5 5 5 5 5

PT

Pearson

Correlation .516 .772 -.632 .783 1

Sig. (2-tailed) .373 .126 .253 .118

N 5 5 5 5 5

*. Correlation is significant at the 0.05 level (2-tailed).

114

POSITIVE CORRELATION:

Dividend payout ratio shows partial correlation with leverage and provision

for taxation. Dividend payout ratio shows weak correlation with Liquidity. Liquidity,

Leverage and provision for taxation are partially correlated.

NEGATIVE CORRELATION:

Dividend payout shows negative correlation with growth. Growth, Liquidity,

Leverage and provision for taxation are negatively correlated.

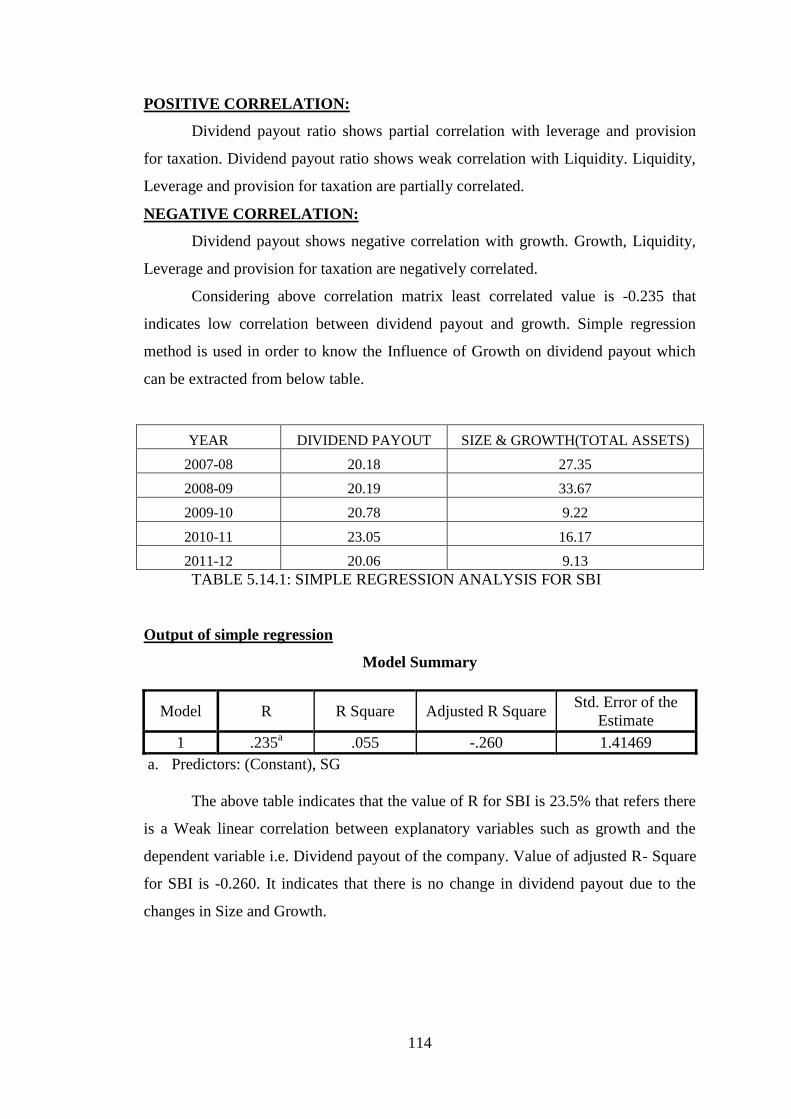

Considering above correlation matrix least correlated value is -0.235 that

indicates low correlation between dividend payout and growth. Simple regression

method is used in order to know the Influence of Growth on dividend payout which

can be extracted from below table.

YEAR DIVIDEND PAYOUT SIZE & GROWTH(TOTAL ASSETS)

2007-08 20.18 27.35

2008-09 20.19 33.67

2009-10 20.78 9.22

2010-11 23.05 16.17

2011-12 20.06 9.13

TABLE 5.14.1: SIMPLE REGRESSION ANALYSIS FOR SBI

Output of simple regression

Model Summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .235a .055 -.260 1.41469

a. Predictors: (Constant), SG

The above table indicates that the value of R for SBI is 23.5% that refers there

is a Weak linear correlation between explanatory variables such as growth and the

dependent variable i.e. Dividend payout of the company. Value of adjusted R- Square

for SBI is -0.260. It indicates that there is no change in dividend payout due to the

changes in Size and Growth.

115

ANOVAa

Model Sum of

Squares Df Mean Square F Sig.

1

Regression .349 1 .349 .175 .704b

Residual 6.004 3 2.001

Total 6.353 4

a. Dependent Variable: DPR

b. Predictors: (Constant), SG

The above table shows that the independent variables statistically significantly

predict the dependent variable, F (1, 3) = 0.175, p >0.05 (i.e., the regression model is

unfit for the data). It indicates that null hypothesis is accepted. It means that there is

no significant impact of growth on the dividend payout of the SBI.

Coefficientsa

Model

Unstandardized

Coefficients

Standardized

Coefficients t Sig.

95.0% Confidence

Interval for B

B Std.

Error Beta

Lower

Bound

Upper

Bound

1 (Constant) 21.365 1.380 15.478 .001 16.972 25.757

GR -.027 .064 -.235 -.418 .704 -.231 .177

a. Dependent Variable: DPR

From the above table, the general form of the equation to predict dividend

payout from growth can be obtained as under:

Predicted dividend payout

= 21.365 - (0.027*growth)

Unstandardized coefficients indicate how much the dependent variable varies

with an Independent variable when all other independent variables are held constant.

In the above table, the unstandardized coefficient for growth is equal to 0.027. This

means that for every additional increase in growth, dividend payout decreases by

0.027.

116

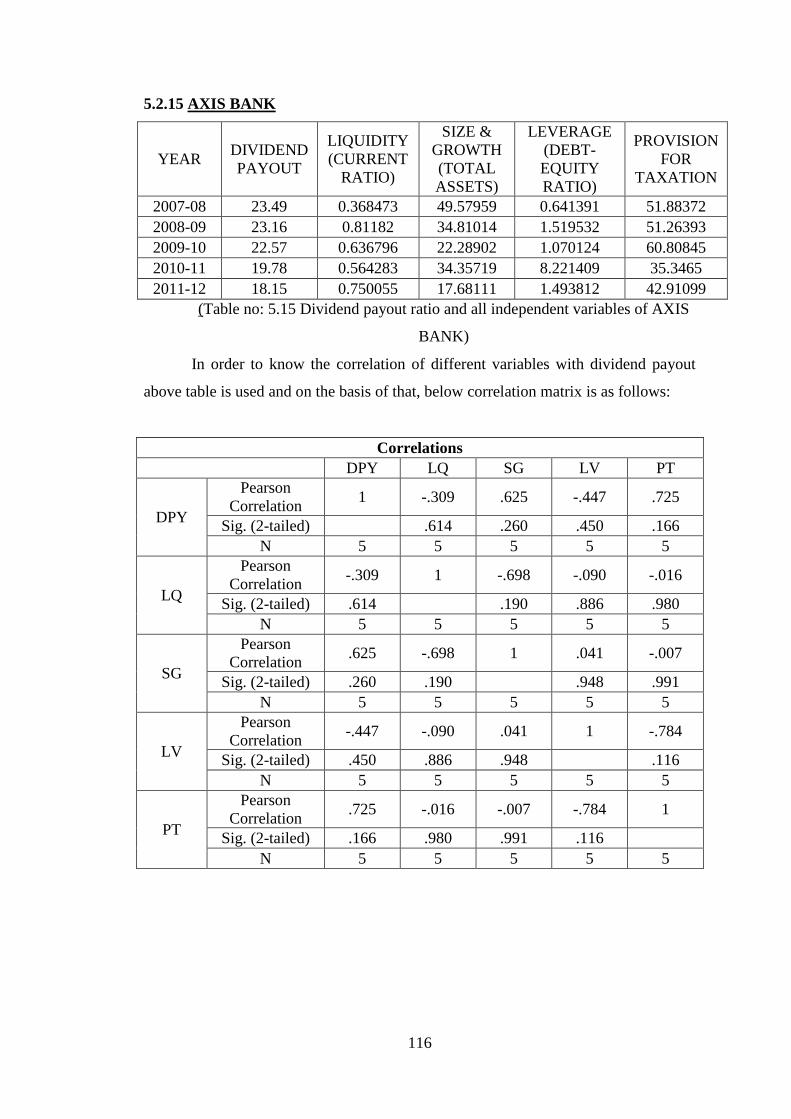

5.2.15 AXIS BANK

YEAR DIVIDEND

PAYOUT

LIQUIDITY

(CURRENT

RATIO)

SIZE &

GROWTH

(TOTAL

ASSETS)

LEVERAGE

(DEBT-

EQUITY

RATIO)

PROVISION

FOR

TAXATION

2007-08 23.49 0.368473 49.57959 0.641391 51.88372

2008-09 23.16 0.81182 34.81014 1.519532 51.26393

2009-10 22.57 0.636796 22.28902 1.070124 60.80845

2010-11 19.78 0.564283 34.35719 8.221409 35.3465

2011-12 18.15 0.750055 17.68111 1.493812 42.91099

(Table no: 5.15 Dividend payout ratio and all independent variables of AXIS

BANK)

In order to know the correlation of different variables with dividend payout

above table is used and on the basis of that, below correlation matrix is as follows:

Correlations

DPY LQ SG LV PT

DPY

Pearson

Correlation 1 -.309 .625 -.447 .725

Sig. (2-tailed)

.614 .260 .450 .166

N 5 5 5 5 5

LQ

Pearson

Correlation -.309 1 -.698 -.090 -.016

Sig. (2-tailed) .614

.190 .886 .980

N 5 5 5 5 5

SG

Pearson

Correlation .625 -.698 1 .041 -.007

Sig. (2-tailed) .260 .190

.948 .991

N 5 5 5 5 5

LV

Pearson

Correlation -.447 -.090 .041 1 -.784

Sig. (2-tailed) .450 .886 .948

.116

N 5 5 5 5 5

PT

Pearson

Correlation .725 -.016 -.007 -.784 1

Sig. (2-tailed) .166 .980 .991 .116

N 5 5 5 5 5

117

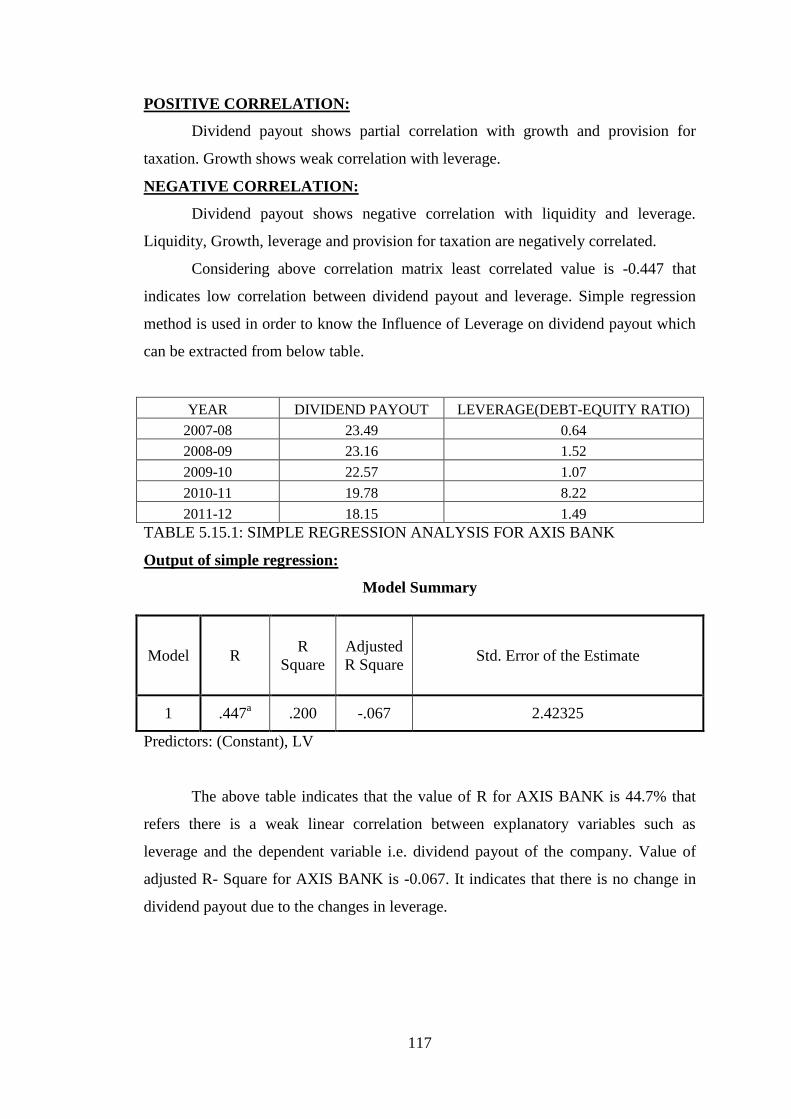

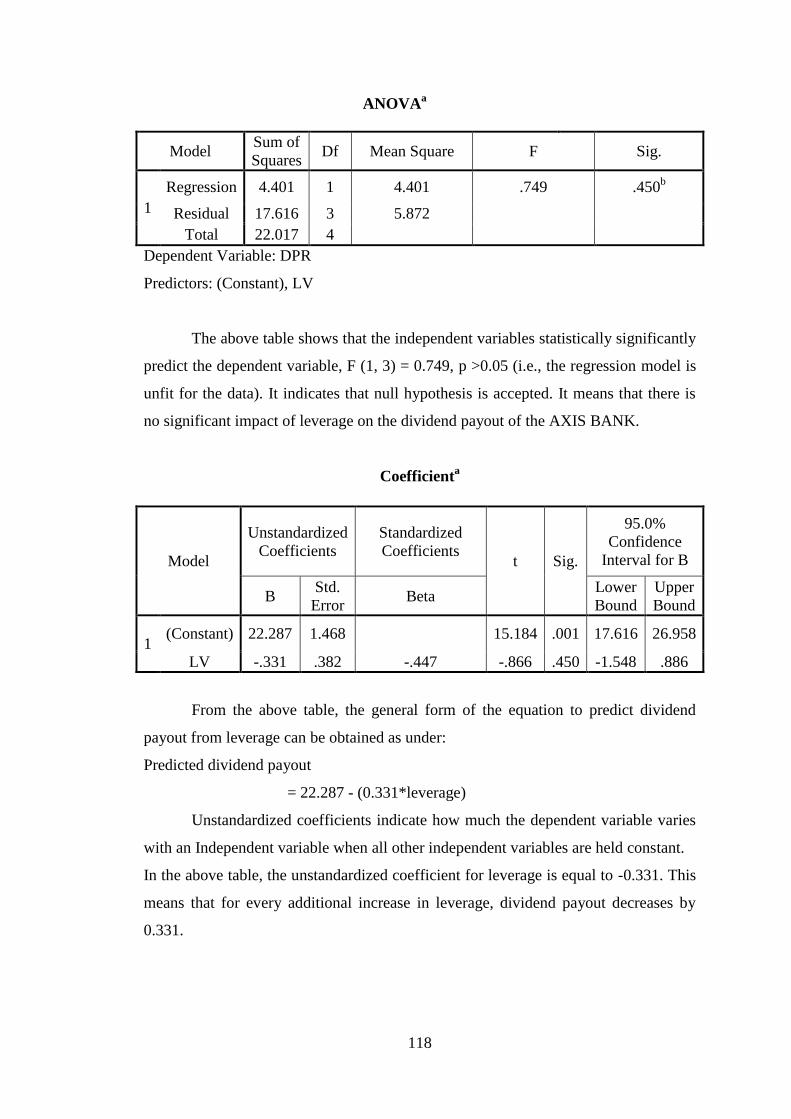

POSITIVE CORRELATION:

Dividend payout shows partial correlation with growth and provision for

taxation. Growth shows weak correlation with leverage.

NEGATIVE CORRELATION: