Embed Size (px)

Citation preview

5–1McQuaig Bille

11College Accounting10th Edition

McQuaig Bille Nobles

© 2011 Cengage Learning

PowerPoint presented by Douglas Cloud Professor Emeritus of Accounting, Pepperdine University

Chapter 5 Closing Entries and the Post-Closing Trial Balance

5–2

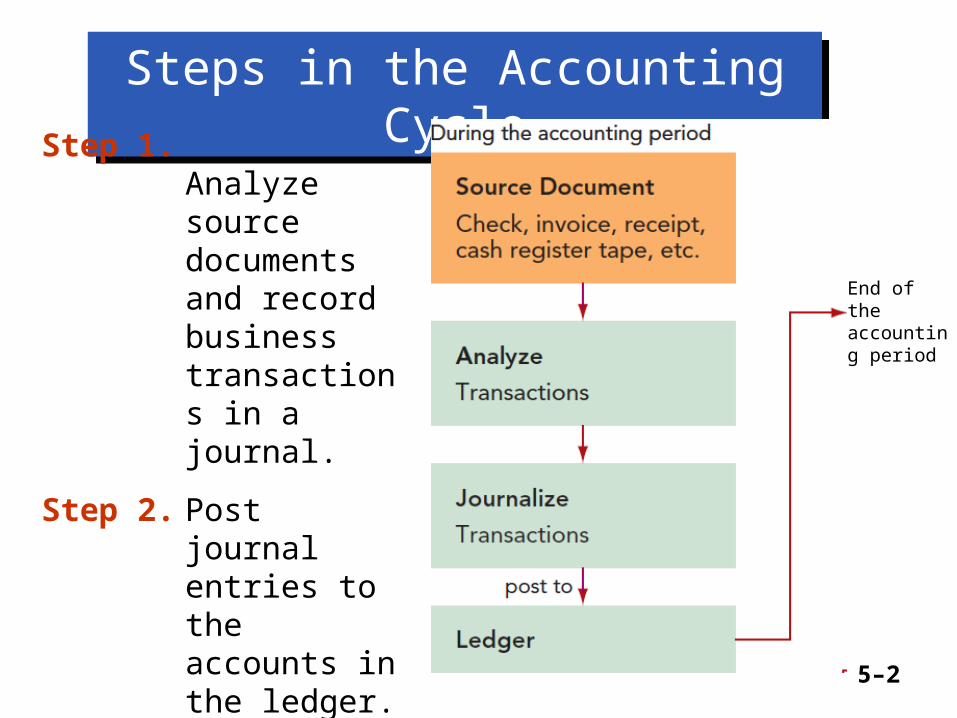

Steps in the Accounting CycleSteps in the Accounting Cycle

Step 1. Analyze source documents and record business transactions in a journal.

Step 2. Post journal entries to the accounts in the ledger.

End of the accounting period

5–3

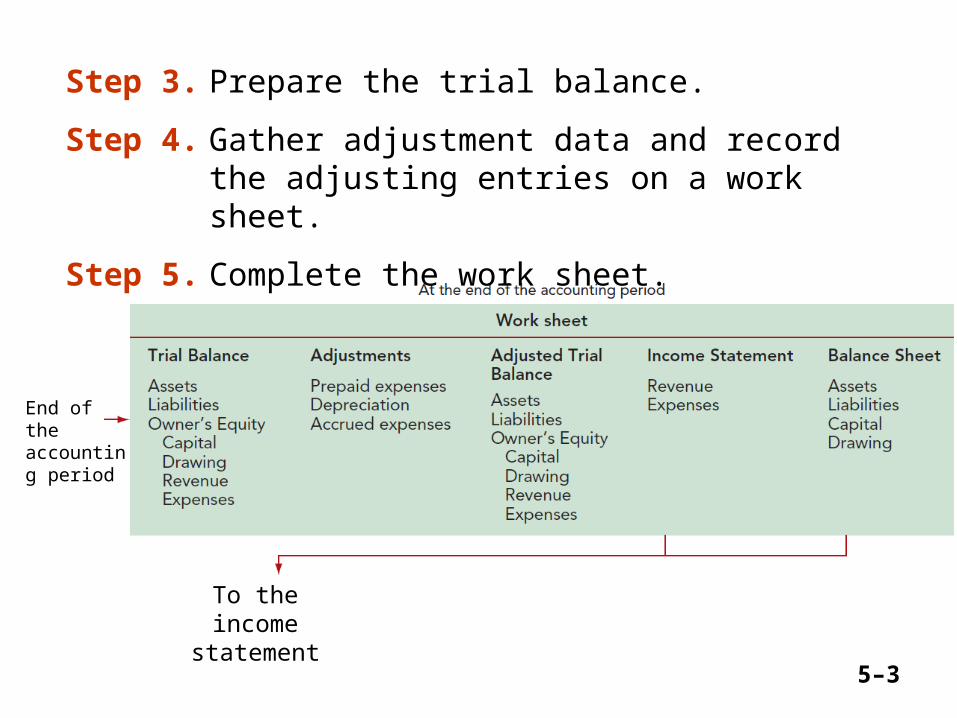

To the income statement

Step 3. Prepare the trial balance.

Step 4. Gather adjustment data and record the adjusting entries on a work sheet.

Step 5. Complete the work sheet.

End of the accounting period

5–4

To journalize adjusting entries

From work sheetStep 6. Prepare financial statements from the data on the work sheet.

5–5

Step 7. Journalize and post the adjusting entries from the data on the work sheet.

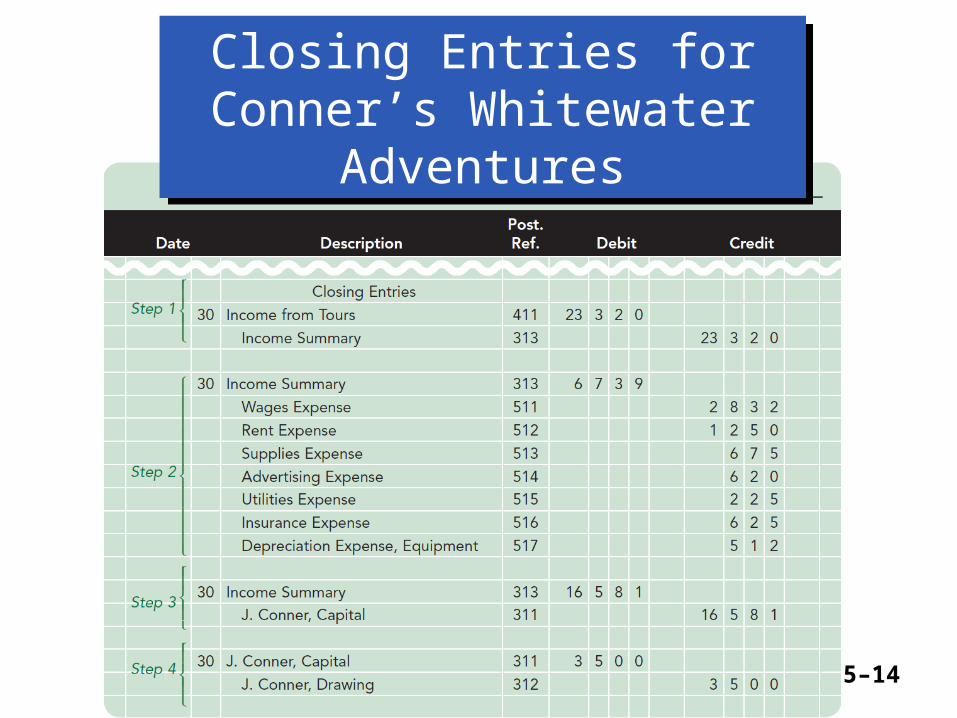

Step 8. Journalize and post the closing entries.

Step 9. Prepare a post-closing trial balance.

5–6

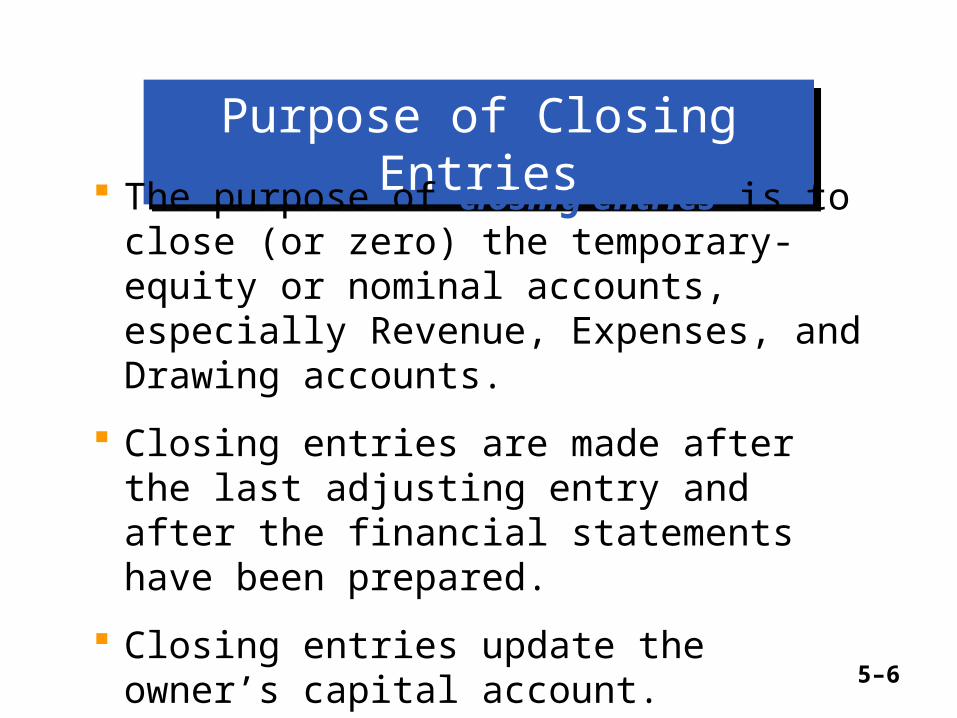

Purpose of Closing EntriesPurpose of Closing Entries

The purpose of closing entries is to close (or zero) the temporary-equity or nominal accounts, especially Revenue, Expenses, and Drawing accounts.

Closing entries are made after the last adjusting entry and after the financial statements have been prepared.

Closing entries update the owner’s capital account.

5–7

Procedure for ClosingProcedure for Closing

The procedure for closing is simply to balance off the account; in other words, to make the balance equal to zero.

5–8

Steps in the Closing ProcedureSteps in the Closing Procedure

Step 1. Close the revenue account(s) into Income Summary.

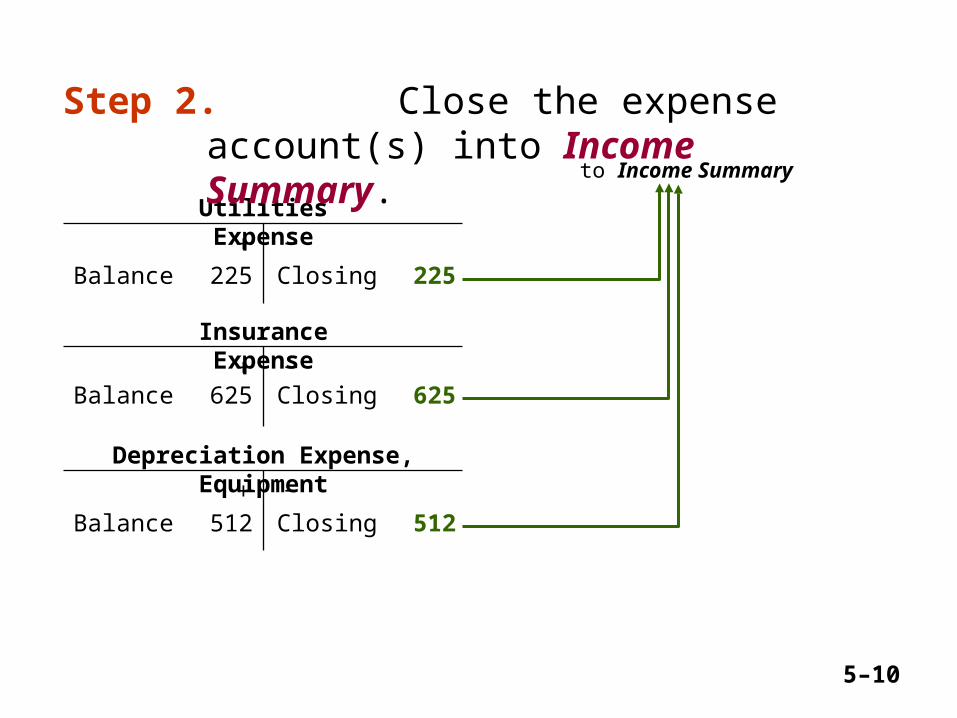

Step 2. Close the expense accounts into Income Summary.

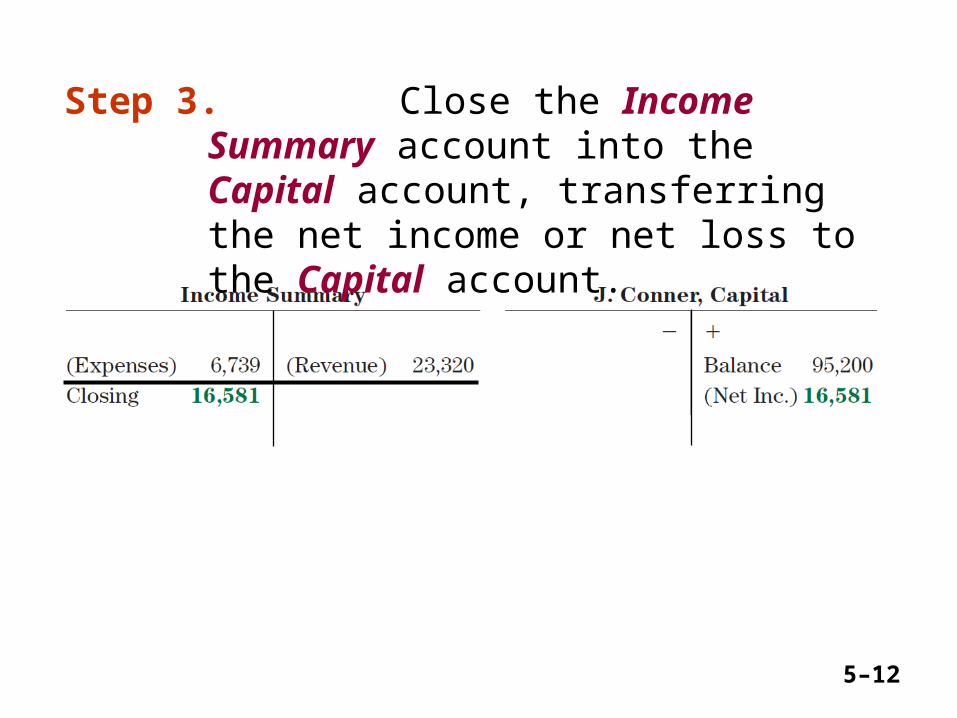

Step 3. Close the Income Summary account into the Capital account, transferring the net income or net loss to the Capital account.

Step 4. Close the Drawing account into the Capital account.

5–9

Closing the Accounts for Conner’s Whitewater Adventure

Closing the Accounts for Conner’s Whitewater Adventure

Step 1. Close the revenue account(s) into Income Summary.

5–10

Utilities Expense

Balance 225 Closing 225+ ‒

Insurance Expense

Balance 625 Closing 625+ ‒

Depreciation Expense, Equipment

Balance 512 Closing 512+ ‒

to Income Summary

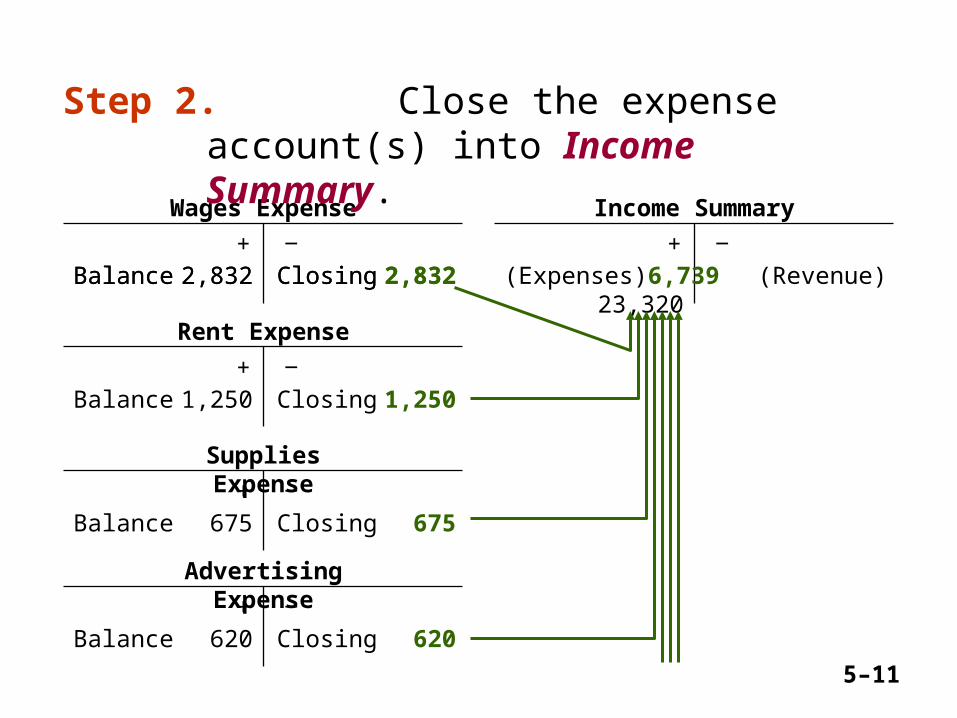

Step 2. Close the expense account(s) into Income Summary.

5–11

Wages Expense

Balance 2,832 Closing 2,832+ ‒

Income Summary

(Expenses) 6,739 (Revenue) 23,320+ ‒

Rent Expense

Balance 1,250 Closing 1,250+ ‒

Supplies Expense

Balance 675 Closing 675+ ‒

Advertising Expense

Balance 620 Closing 620+ ‒

Balance 2,832 Closing 2,832

Step 2. Close the expense account(s) into Income Summary.

5–12

Step 3. Close the Income Summary account into the Capital account, transferring the net income or net loss to the Capital account.

5–13

Balance 3,500

Step 4. Close the Drawing account into the Capital account.

5–14

Closing Entries for Conner’s Whitewater Adventures

Closing Entries for Conner’s Whitewater Adventures

5–15

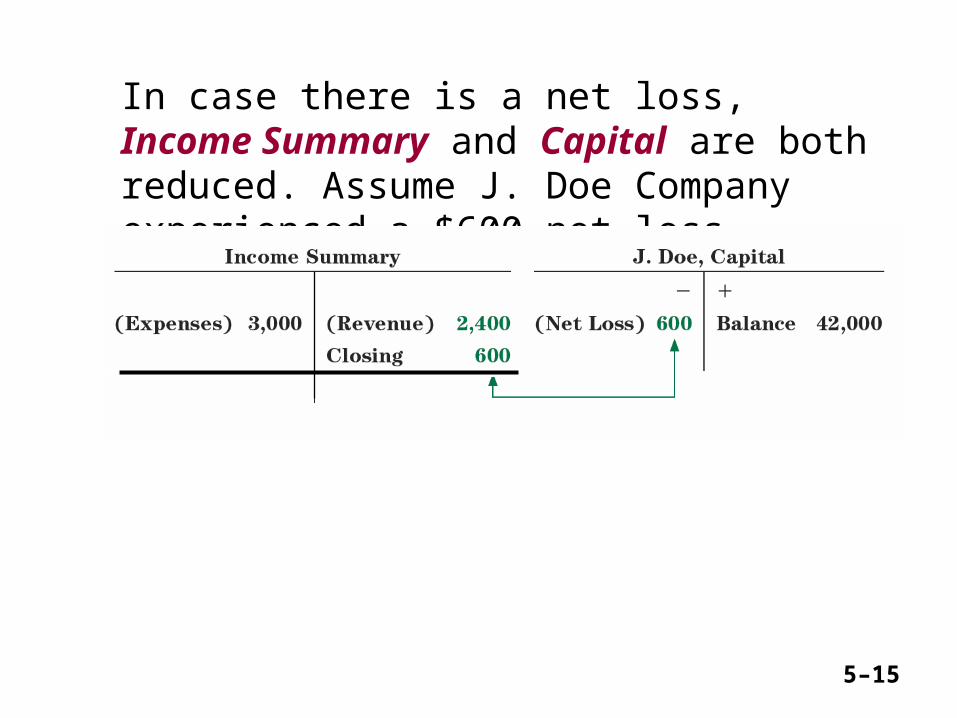

In case there is a net loss, Income Summary and Capital are both reduced. Assume J. Doe Company experienced a $600 net loss.

5–16

The resulting journal entry:

5–17

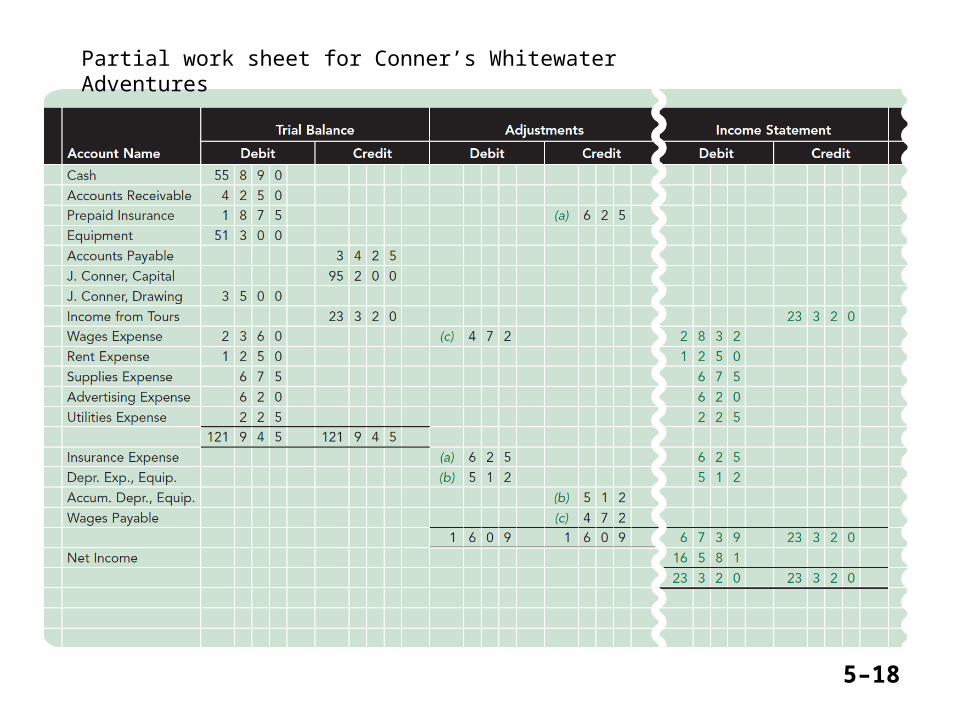

Closing Entries Taken Directly from the Work Sheet

Closing Entries Taken Directly from the Work Sheet

You can gather information for the closing entries either directly from the ledger accounts or from the work sheet (figures for three of the four entries can be taken from the last four columns) .

You may plan the closing entries by balancing off all the figures that appear in the Income Statement columns.

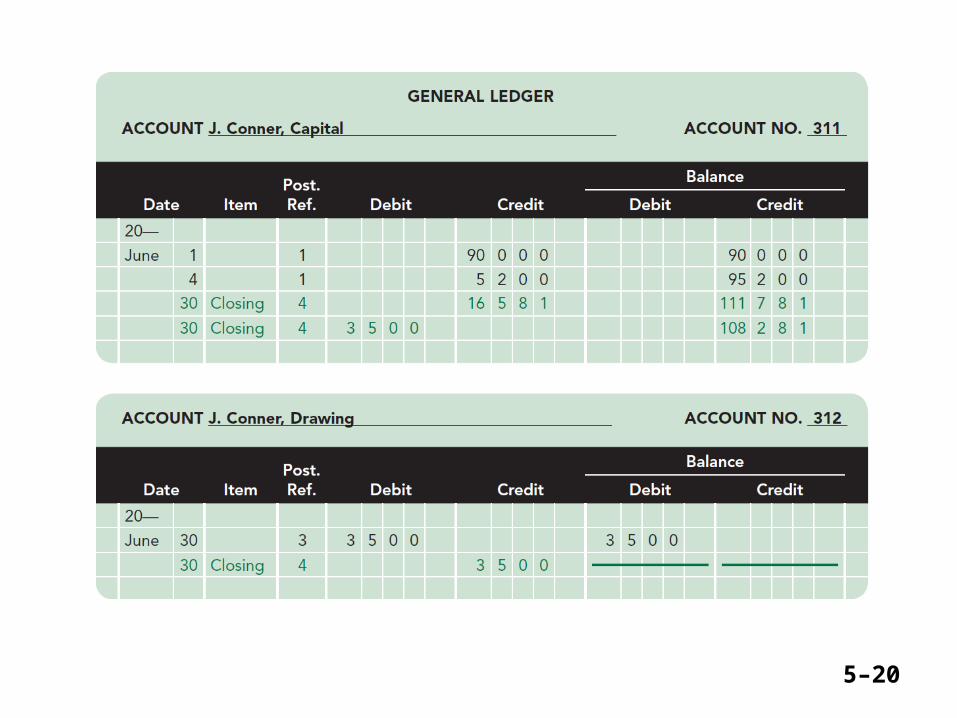

In the Item column of the ledger account, we write the word “Closing.”

5–18

Partial work sheet for Conner’s Whitewater Adventures

5–19

Posting the Closing EntriesPosting the Closing Entries

Accountants call the accounts that are to be closed (such as revenue, expenses, Income Summary, and Drawing) nominal (temporary-equity) accounts.

Accountants call the accounts that remain open from one fiscal period to the next real (permanent) accounts.

5–20

5–21

5–22

The Post-Closing Trial BalanceThe Post-Closing Trial Balance

The Post-Closing Trial Balance

To verify the balances of the accounts that remain open, a post-closing trial balance is prepared using the final balance figures from the ledger accounts.

Note that the accounts listed in the post-closing trial balance are the real or permanent accounts.

5–23

Tracking Down an ErrorTracking Down an Error

If the totals of the post-closing trial balance are not equal, here’s the recommended procedures for tracking down the error.1. Re-add the trial balance columns.

2. Check to see that the figures were correctly transferred from the ledger accounts to the post-closing trial balance.

3. Verify the posting of the adjusting entries and the recording of the new balances.

4. Make sure that the closing entries have been posted and that all revenues, expense, Income Summary, and Drawing accounts have zero balances.

5–24

Cash and Accrual AccountingCash and Accrual Accounting

Under the cash basis of accounting, revenue is recorded when it is received in cash, and generally expenses are recorded when they are paid in cash.

Under the accrual basis of accounting, revenue is recorded when it is earned, and expenses are recorded when they are incurred.

5–25

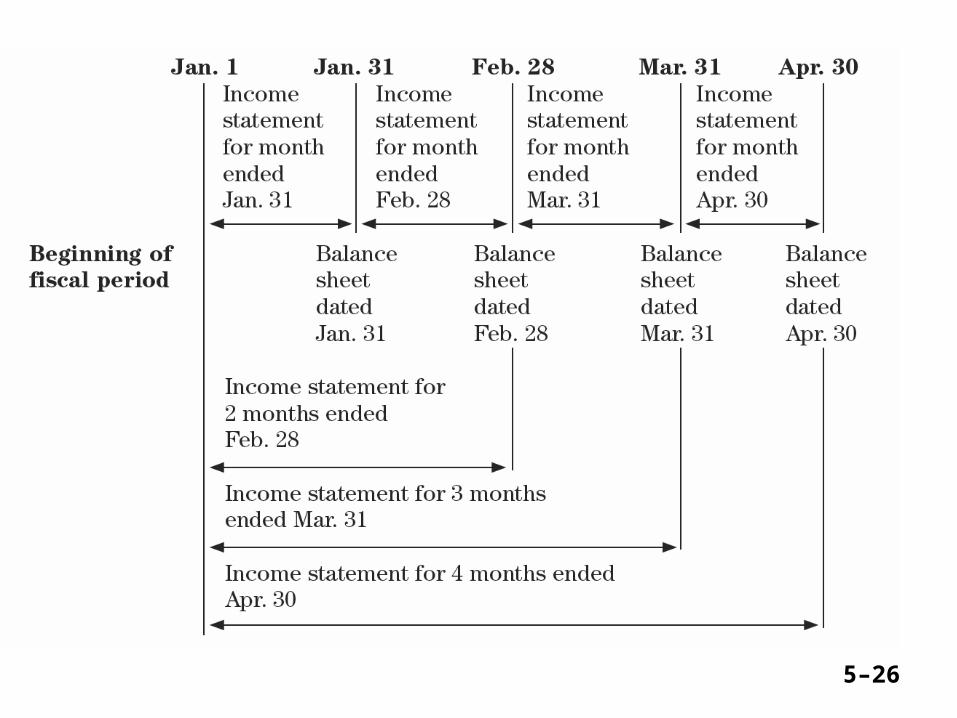

Interim StatementsInterim Statements

Financial statements prepared during the fiscal year, for periods of less than twelve months, are called interim statements.

A business may prepare the financial statements monthly to provide up-to-date information about the results of operations.

5–26