Embed Size (px)

Citation preview

10.0 CLE Hours, Including 2.0 Ethics Hours in Missouri 10.0 CLE Hours, including 2.0 Ethics in Kansas

2300 Main Street, St. 100 ■ KC, MO 64108 ■ phone 816-474-4322 ■ fax 816-474-0103

45th Annual Bench-Bar & Boardroom Conference

Thursday, May 17, 2018

12:50 – 1:40 PM

The Credit Reporting Act:

Not Just About Credit

Michael Rapp, Stecklein & Rapp Chartered

Michael is a licensed attorney in the state of Kansas and Missouri. He is a member of the American Bar Association, Kansas City Metropolitan Bar Association, Wyandotte County Bar Association, as well as the National Association of Consumer Advocates. Since graduating law school, Michael has focused his practice exclusively on Consumer Law with a concentration on Fair Debt Collection Practices (FDCPA), Credit Reporting (FCRA) and Telephone Consumer Protection (TCPA).

Michael regularly gives talks around the Kansas City area to community groups on the topics of Debt and Credit and blogs about FDCPA stories of interest providing short, good-to-know tips for those interested in keeping their finger on the pulse of consumer protection law.

Michael Rapp graduated from UMKC School of Law, where he served as Research Administrator for Friedman on Leases and was awarded the Sanford B. Ladd Award for his exceptional achievement in Real Estate Law. Prior to attending law school, Michael served his country, was decorated, and honorably discharged from the United States Air Force.

5/14/2018

1

UNDERSTANDING

FAIR CREDIT REPORTING ACT VIOLATIONS AND CASES

Stecklein & Rapp Chartered

5/14/2018

2

What We Do: 2

We sue Credit Reporting Agencies

Background Check Companies

Banks

Debt Collectors/Debt Buyers

Employers

Shady Car Lots

5/14/2018

3

Fair Credit Reporting Act

(15 U.S.C. §§1681 et seq.)

Regulates content of consumer reports, especially including the

accuracy of data contained in those reports

full text of statute is available here:

http://www.consumer.ftc.gov/articles/pdf-0111-fair-credit-

reporting-act.pdf

powerful federal consumer statute that often works in

conjunction with other federal consumer statutes (FDCPA, FCBA,

TCPA).

State Counterpart (KSA §50-701)

Summary: The Statute

5/14/2018

4

Summary: The Statute

Like it or not,

every consumer has at least one, if not several, “report cards” that purport to assess the consumer about a variety of qualities such as creditworthiness, or quality as employee or tenant

5/14/2018

5

What is in the FICO Score? 5

35%

30%

15%

10% 10%

On Time Payments

Capacity Used

Length of History

New Credit

Types of Credit

5/14/2018

6

Credit score basics

FICO prepares the credit scores for each credit

bureau

Equifax = Beacon

Experian = Experian-Fair Isaac Risk Model

TransUnion = Empirica

FAKO

Individual lenders may have own internal scoring

process

5/14/2018

7

Credit score basics

Not everyone has a credit score:

Must have at least one account on your credit report

that has been open at least six months

that the creditor has updated at least once during that

six months

5/14/2018

8

Two purposes:

For credit industries (including banking system)

"The banking system is dependent upon fair and accurate credit reporting. Inaccurate credit reports directly impair the efficiency of the banking system, and unfair credit reporting methods undermine the public confidence which is essential to the continued functioning of the banking system.“ §1681(a)(1).

For consumers:

"a need to insure that consumer reporting agencies exercise their grave responsibilities with fairness, impartiality, and a respect for the consumer’s right to privacy." §1681(a)(4).

Summary: The Statute

5/14/2018

9

FCRA Guiding Principles 9

Privacy Limited third party access to consumer reports

Accuracy Responsibilities of consumer reporting

agencies and data furnishers

dispute resolution process

Fairness Adverse action notices to affected consumers

Obsolete information cannot be reported

5/14/2018

10

Intended to protect consumers from the willful and/or negligent inclusion of inaccurate information in their credit reports.

To that end, the FCRA regulates the collection, dissemination, and use of consumer information, including consumer credit information

Enforced by the Federal Trade Commission (FTC), the Consumer Financial Protection Bureau (CFPB) and private litigants.

Summary: The Statute

5/14/2018

11

What are consumer reports?

See §1681a(d)(1)

Any written, oral, or other communication of any information by a consumer reporting agency bearing on a consumer’s credit worthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living which is used or expected to be used or collected in whole or in part for the purpose of serving as a factor in establishing the consumer’s eligibility for:

credit or insurance to be used primarily for personal, family, or household purposes;

employment purposes; or

any other purpose authorized under section 604 [§ §1681b].

FCRA and Consumer Reports

5/14/2018

12

Credit reporting players

Consumer: An individual (not an entity).

Credit reporting agency (“CRA”): An entity that

provides consumer reports.

Furnisher: Not defined in Act. Can be anyone who

furnishes consumer information to a CRA.

User: One who accesses the report and views it.

5/14/2018

13

Credit reporting players

Subscriber: Many furnishers are also subscribers.

Subscription to a CRA enables a business to obtain

credit reports about potential customers.

Subscription contract also requires the business to

furnish the CRA with information about existing

customers’ accounts so that the CRA can include

them in its file for that person.

5/14/2018

14

Credit reporting players

Consumer Data Industry Association (CDIA)

Creator of Metro 2, a standard automated data

reporting format used by furnishers to report

information electronically to the CRA’s.

Data is uploaded electronically in an order specified

by the Metro 2 format and using Metro 2 codes.

5/14/2018

15

Credit reporting players

Online Data Exchange (OLDE)

Developed and administers e-OSCAR: Online Solution

for Complete and Accurate Reporting, a web-based

dispute notification system used by the CRA’s and

furnishers when a consumer disputes an account

appearing on a consumer report.

5/14/2018

16

What is a Consumer Reporting Agency?

16

Tenant screeners

Check verifiers

Background checking companies

Credit reporting Agencies

Resellers of all the above

5/14/2018

17

Importance of consumer reports

Three primary areas: assessing credit worthiness, employment background checks, and tenant / housing background checks.

access to credit: two scenarios

prime credit -- ability to borrow at prime rates

access to credit altogether -- outright credit denials

employee screening

negative information on background report can prevent consumer from being employed in large sectors of the economy

tenant screening

similarities to both credit reports and employment background checks

in addition to credit, factors include prior rental payment history, lawsuits involving that tenant and landlord

5/14/2018

18

Standard for Consumer Reports

“Maximum Possible Accuracy”

Accordingly, Congress created

FCRA to implement an especially

high standard of accuracy --

Maximum Possible Accuracy

Accuracy is the Hallmark and

starting place for most claims

under FCRA

5/14/2018

19

A System with Widespread Errors

How Widespread is it? Millions of consumers have substantial

errors on their credit reports. FTC study of the credit reporting industry concluded: One in four (25%) consumers identified

errors on their credit One in 20 (5%) of consumers‘ had

errors serious enough to cause they to pay more for credit.

After Disputes: One in five consumers had an error

that was corrected by a credit reporting agency (CRA) after it was disputed, on at least one of their three credit reports

Slightly more than one in 10 consumers saw a change in their credit score after the CRAs modified errors on their credit report

5/14/2018

20

Why Don't CRAs Just Get it Right?

Overinclusion

no system is perfect –

either underinclusive or overinclusive

CRAs choose overinclusive.

Why?

because their customers are the banks and other potential creditors.

those customers want a better-safe than sorry approach.

How do they accomplish over- inclusiveness?

use loose identifiers

one example: 7 of 9 digits on SSN is a match

5/14/2018

21

Recognizing the FCRA 21

A credit pull was done

A background check was made

Client has a Credit Report

A high interest loan was made

A loan was denied

A job was denied

Simply… anything included in a

consumer’s financial reputation that is untrue!

5/14/2018

22

Time Out to Review

At this point, let's pause and review what we have considered so far:

Consumer reports affect almost every consumer, usually in multiple arenas

FCRA holds those reports to a very high level accuracy

Inaccuracies, that cause credit scores to appear lower than they are, are rampant

Creditors make more money from consumers with a negative credit rating,

especially if that negative rating does not reflect an actually higher lending risk.

Putting that all together:

There is a need in the community. These cases are all around you.

5/14/2018

23

Litigating Inaccuracies

No Strict Liability for Accuracy

in other words, mere fact that there is an inaccuracy does not equal liability

the issue always is reasonableness of procedures to ensure used to ensure accuracy

Reasonableness of Procedures arises in two instances:

1. reasonable procedures to ensure maximum possible accuracy was not reported (CRA only)

2. after a consumer disputes an error, reasonableness of investigation of that dispute (both CRA and Furnisher)

More about disputes and accuracy later . . .

5/14/2018

24

Players in the Consumer Reporting Game

Creditor #1

Pot. Creditor #2

Consumer CRA

Potential creditor requests report from CRA

5/14/2018

25

Players in the Consumer Reporting Game

Consumer Reporting Agencies (CRAs)

Consumer Reporting Agency

any person which, for monetary fees, dues, or on a

cooperative nonprofit basis, regularly engages in whole or in

part in the practice of assembling or evaluating consumer

credit information or other information on consumers for the

purpose of furnishing consumer reports to third parties, and

which uses any means or facility of interstate commerce for

the purpose of preparing or furnishing consumer reports.

§1681a(f).

3 national CRAs: Equifax, Experian, and TransUnion

sometimes referred to as:

credit bureaus

credit reporting agency

a consumer reporting agency that regularly engages in the

practice of assembling or evaluating, and maintaining, for

the purpose of furnishing consumer reports to third parties

bearing on a consumer’s credit worthiness, credit standing, or

credit capacity, each of the following regarding consumers

residing nationwide. §1681a(p).

5/14/2018

26

National Speciality CRAs “nationwide specialty consumer reporting agency” means

a consumer reporting agency that compiles and maintains files on consumers on a nationwide basis relating to-- (1) medical records or payments;

(2) residential or tenant history;

(3) check writing history;

(4) employment history; or

(5) insurance claims. §1681a(x).

For more information:

List of Speciality CRAs:

http://files.consumerfinance.gov/f/201501_cfpb_list_consumer-reporting-agencies.pdf

Account Screening CRAs:

http://cfefund.org/sites/default/files/Account%20Screening%20CRA%20Agencies%20Banking%20Access% 20report.pdf

Players in the Consumer Reporting Game

5/14/2018

27

Players in the Consumer Reporting Game

Furnishers of Information: Who reports

"furnishers" are

Original creditors (Creditor #1 in graph

above)

Third party debt collectors

Resellers of public record information (like

Lexis Nexis)

Past landlords

Why report?

low cost collection tool

subscriber agreement may obligate

5/14/2018

28

Users of Consumer Reports:

Who buys reports and why?

potential creditors, employers, banks, and landlords (Creditor #2 in graph above)

permissible purposes for a CRA to furnish a consumer report to a user

– §1681b(a)

when a user "pulls" a report without a permissible purpose, there may be a claim for an "impermissible pull"

hard "pulls" for credit -- usually when consumer authorizes it in conjunction with an application for credit

these lower credit scores because it shows that the person is in need of credit and lacks sufficient resources at the time

soft "pulls" for credit do not lower credit scores one example: credit card bank inquires about a

consumer's credit score to assess whether to offer a pre-approved credit card

5/14/2018

29

Private Causes of Action Pursuant to FCRA

Liability:

Determine the Source of the Problem to Assess Appropriate Statutory Provision for Liability

Refresher:

Hallmark of an FCRA claim is inaccurate information

That inaccurate information may originate either with a CRA or a Furnisher

5/14/2018

30

Private Causes of Action Pursuant to FCRA

Inaccurate Information Originating with the CRA

Accuracy of report. Whenever a

consumer reporting agency prepares a consumer report it shall follow reasonable procedures to assure maximum possible accuracy of the information concerning the individual about whom the report relates.

§1681e(b). Nothing here about a dispute. §1681e(b) obligation on CRAs exists

without regard to any dispute.

5/14/2018

31

Typical Problems Entity to Sue & Statute Violated

Mixed File

one consumer has info on

his report belonging to

another

Merged File

took consumers with separate

files and merged them onto

one single file.

Frank and John are now one

entity

Multiple Files

consumer has multiple files

CRA

15 U.S.C. §§1681e(b)

failure to follow

reasonable procedures to

assure maximum possible

accuracy

Private Causes of Action Pursuant to FCRA

5/14/2018

32

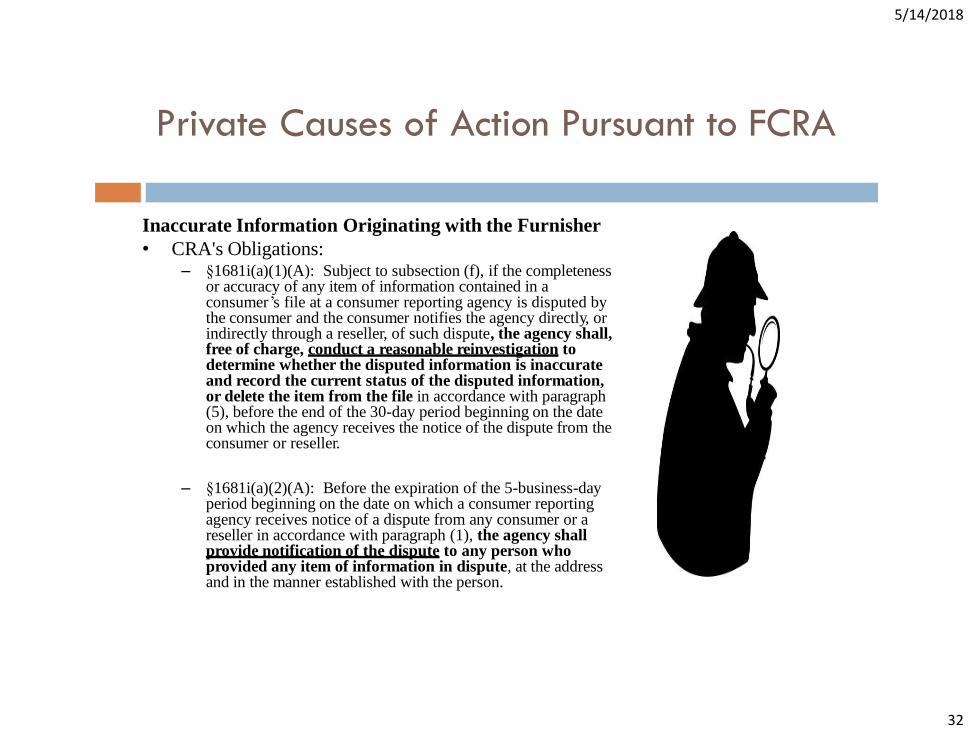

Inaccurate Information Originating with the Furnisher

• CRA's Obligations: – §1681i(a)(1)(A): Subject to subsection (f), if the completeness

or accuracy of any item of information contained in a consumer’s file at a consumer reporting agency is disputed by the consumer and the consumer notifies the agency directly, or indirectly through a reseller, of such dispute, the agency shall, free of charge, conduct a reasonable reinvestigation to determine whether the disputed information is inaccurate and record the current status of the disputed information, or delete the item from the file in accordance with paragraph (5), before the end of the 30-day period beginning on the date on which the agency receives the notice of the dispute from the consumer or reseller.

– §1681i(a)(2)(A): Before the expiration of the 5-business-day

period beginning on the date on which a consumer reporting agency receives notice of a dispute from any consumer or a reseller in accordance with paragraph (1), the agency shall provide notification of the dispute to any person who provided any item of information in dispute, at the address and in the manner established with the person.

Private Causes of Action Pursuant to FCRA

5/14/2018

33

Private Causes of Action Pursuant to FCRA

Furnisher's Obligation:

1681s-2(b) Duties of Furnishers of Information upon Notice of Dispute (1). After receiving notice pursuant to section 611(a)(2) [§ 1681i] of a dispute

with regard to the completeness or accuracy of any information provided by a person to a consumer reporting agency, the person shall

(A) conduct an investigation with respect to the disputed information; (B) review all relevant information provided by the consumer reporting agency

pursuant to section 611(a)(2) [§ 1681i]; (C) report the results of the investigation to the consumer reporting agency; (D) if the investigation finds that the information is incomplete or inaccurate, report

those results to all other consumer reporting agencies to which the person furnished the information and that compile and maintain files on consumers on a nationwide basis; and

(E) if an item of information disputed by a consumer is found to be inaccurate or incomplete or cannot be verified after any reinvestigation under paragraph (1), for purposes of reporting to a consumer reporting agency only, as appropriate, based on the results of the reinvestigation promptly– (i) modify that item of information; (ii) delete that item of information; or (iii) permanently block the reporting of that item of information

5/14/2018

34

Typical Problems (here, possibilities are endless) Entity to Sue and Statute Violated

•reporting of non-existent debt altogether

debt never incurred

debt incurred by another person (family)

•inaccurate date of first delinquency

•inaccurate amount of debt owed

•failure to mark as paid

failure to mark as disputed *

•incomplete information

technically accurate but misleading because

incomplete (such as reporting that sent to collections

but failing to report that has been paid in full)

•bankruptcy -- continuing to report details about the

discharged debt rather than simply reporting

"discharged in bankruptcy"

•medical information -- may not report facts that

disclose private medical information

•Identity theft

Dispute process requires:

reasonable reinvestigation

parroting or automated verification not

sufficient

o must conduct “searching inquiry”

Once dispute made with CRA:

CRA [15 U.S.C. §§1681i]

CRA’s list of duties during reinvestigation process

Furnisher [15 U.S.C. §§1681s-2(b)] Furnisher’s list of

duties during reinvestigation process

Problems Originating with Furnisher

5/14/2018

35

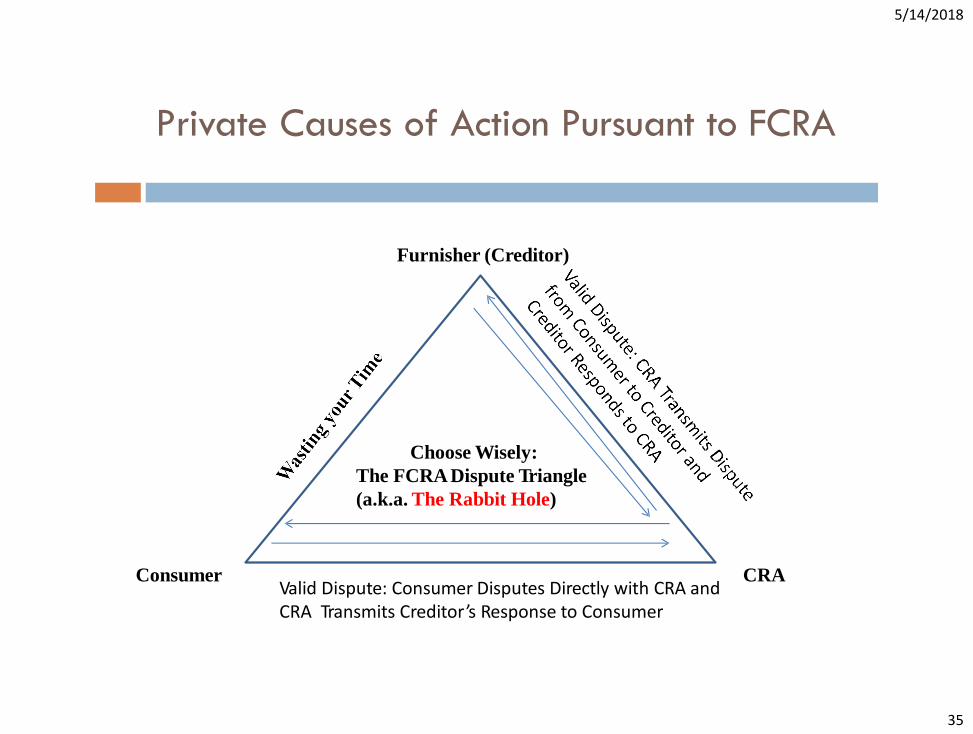

Choose Wisely:

The FCRA Dispute Triangle

(a.k.a. The Rabbit Hole)

Furnisher (Creditor)

Consumer CRA Valid Dispute: Consumer Disputes Directly with CRA and CRA Transmits Creditor ’s Response to Consumer

Private Causes of Action Pursuant to FCRA

5/14/2018

36

Private Causes of Action Pursuant to FCRA

CRITICAL POINT:

There is NO private cause of action against a furnisher unless and until 30 days after a dispute is filed with a credit bureau

What Actually Happens in a Dispute?

CRA reduces dispute to a code according to the METRO 2 guidelines

That code is transmitted to furnisher via E-OSCAR system

Furnisher typically does a cursory review to confirm that the information being reported is the same as what furnisher intended to report

essentially parroting back the information to CRA

case after case has held that this is not a reasonable reinvestigation

5/14/2018

37

Damages

Actual Damages pecuniary damages

examples: paying more for mortgage

losing job offer and resulting lost wages

non-pecuniary damages emotional distress

need not corroborate with medical evidence

consumer's family/friends may testify

causation remains a requirement the error must be shown to have caused the

damage

thus, causation may not exist where consumer has accurate negative information Defendant will argue that, even if it violated statute,

consumer's credit score was already damaged and consumer would have suffered credit denials regardless

5/14/2018

38

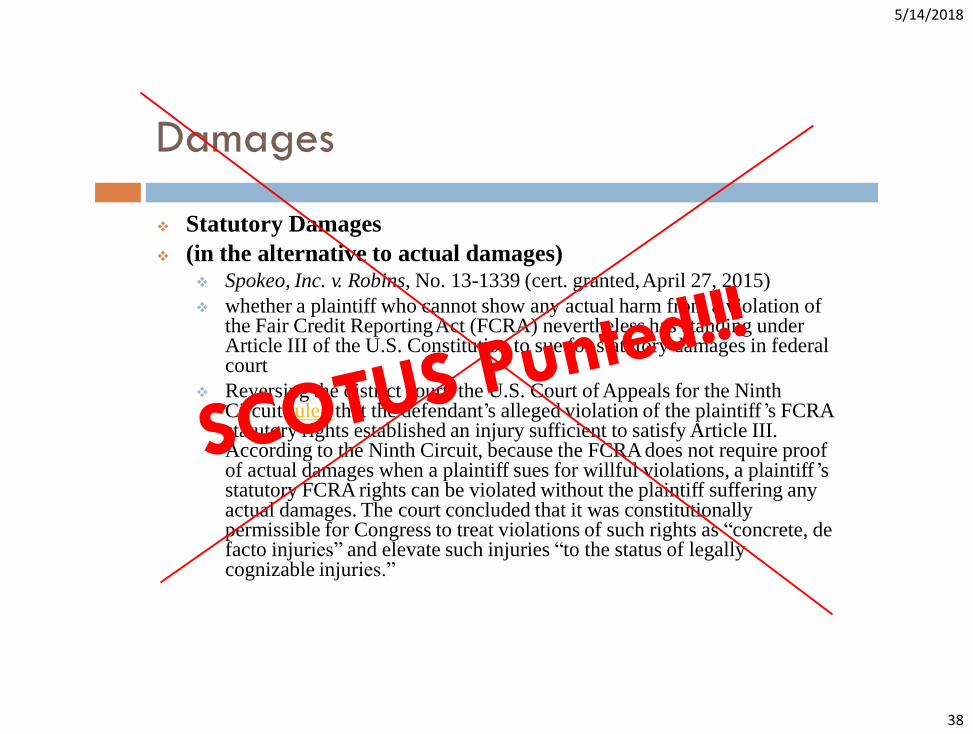

Damages

Statutory Damages

(in the alternative to actual damages) Spokeo, Inc. v. Robins, No. 13-1339 (cert. granted, April 27, 2015)

whether a plaintiff who cannot show any actual harm from a violation of the Fair Credit Reporting Act (FCRA) nevertheless has standing under Article III of the U.S. Constitution to sue for statutory damages in federal court

Reversing the district court, the U.S. Court of Appeals for the Ninth Circuit ruled that the defendant’s alleged violation of the plaintiff’s FCRA statutory rights established an injury sufficient to satisfy Article III. According to the Ninth Circuit, because the FCRA does not require proof of actual damages when a plaintiff sues for willful violations, a plaintiff’s statutory FCRA rights can be violated without the plaintiff suffering any actual damages. The court concluded that it was constitutionally permissible for Congress to treat violations of such rights as “concrete, de facto injuries” and elevate such injuries “to the status of legally cognizable injuries.”

5/14/2018

39

Damages

Attorney's Fees

wrongdoer pays Plaintiff's fees

lodestar method

Attorney’s fees can and sometimes do exceed the consumer ’s recovery

This allows “small” violations to be vigorously prosecuted

5/14/2018

40

Punitive Damages

willful misconduct

even reckless misconduct.

See Safeco Insurance Co. of America v. Burr, 551 U.S. 47 (2007)

Damages

5/14/2018

41

Employment Background checks

Just like credit reports,

inaccuracy is also the

hallmark of employment

background checks claims

Common examples:

wrong criminal history

(same or similar name)

misdemeanor vs. felony

expungements

5/14/2018

42

Employment Background checks

Proper Procedure

Purpose

obtain written consent by job applicant

§1681b(b)(2): Disclosure to Consumer

Must provide "a clear and conspicuous disclosure has been made in writing to the consumer at any time before the report is procured or caused to be procured, in a document that consists solely of the disclosure, that a consumer report may be obtained for employment purposes"; and

ensure applicant has an opportunity to dispute any erroneous information in report before employer takes adverse action based upon that report

§1681b(b): Conditions for Furnishing and Using Consumer Reports for Employment

§1681b(b)(3): Pre-Adverse Action Notice

in using a consumer report for employment purposes, before taking any adverse action based in whole or in part on the report, the person intending to take such adverse action shall provide to the consumer to whom the report relates – (i) a copy of the report; and (ii) a description in writing of the rights of the consumer under this title

class action potential

5/14/2018

43

What to worry about: 43

Attorney Fees

Levine v. JPMorgan Chase & Co., No. 13-C-498, 2014

WL 4410682 (E.D. Wis. Sept. 5, 2014)

Your client’s relatives

Anthony v. Equifax Info. Servs., LLC, No. 2:13-CV-

01424-TLN, 2015 WL 502857 (E.D. Cal. Feb. 5, 2015)

Credit Repair Organizations Act

Prohibiting taking money for a promise to fix credit.

15 U.S. Code § 1679b(b)

5/14/2018

44

Consumer Repair Companies 44

What they do:

File numerous disputes with the CRAs

Spam Disputes (Filing numerous disputes back to back)

Take advantage of the 30 day rule

Often get items deleted

The downside:

Often temporary

Tradelines often reinserted from other CRAs

Can get consumer banned from making disputes

5/14/2018

45

Why isn’t the FCRA used? 45

Wrongfully sued

focusing on the suing party

Identity theft

focusing on the thief

Declined employment

focusing on wrongful behavior of the employer

Declined loan

focusing on the party that has reported the wrong information

Debt collection

focusing on the creditor who is trying to collect money from your client

5/14/2018

46

Thank You and

Contact Me with Questions.

Michael Rapp

Stecklein & Rapp Chartered

748 Ann Ave

Kansas City, KS 66101

T: 913.371.0727

L: www.linkedin.com/in/aj-stecklein-562751137

L: www.linkedin.com/in/michael-rapp-8627452