Embed Size (px)

Citation preview

14/30/2015

FUNDING PUBLIC EDUCATION

Bucks County Schools Intermediate Unit #22

Thursday, April 30th, 2015

Dave Matyas

Business Administrator

Central Bucks School District

24/30/2015

Typical Role of the Business Administrator

• Depending on District Size, Oversight of Most Non Academic Areas:– Building and Grounds– Transportation– Food Service– Warehousing– Community School– Business Office Administration

• Financial Reporting/Accounting/Audits• Budgeting• Taxes (Real Estate, Earned Income, Real Estate Transfer, etc)• Payroll• Accounts Payable• Investment Management• Child Accounting• Purchasing• Insurance

34/30/2015

Develop the Annual Budget• Fiscal/Budget Year is from July 1 to June 30.• Funds of a School District

– General Fund– Food Service Fund– Capital

• Construction Fund• Technology Fund• Transportation

– Fund Balance (limited to 8-12% of the budget)• Governor Wolf has been discussing lowering this amount to 4%

for all school districts

4

• Act 1 is a law limiting real estate tax increases to an inflation formula

• Developed by averaging the State Average Weekly Wage (SAWW) and Employment Cost Index (ECI) to approximate the base rate of inflation over the past 18 months

• Act 1 also allows exceptions to Act 1 to allow for greater inflation growth due to factors outside the control of a school board

• The Act 1 index is published in September

4/30/2015

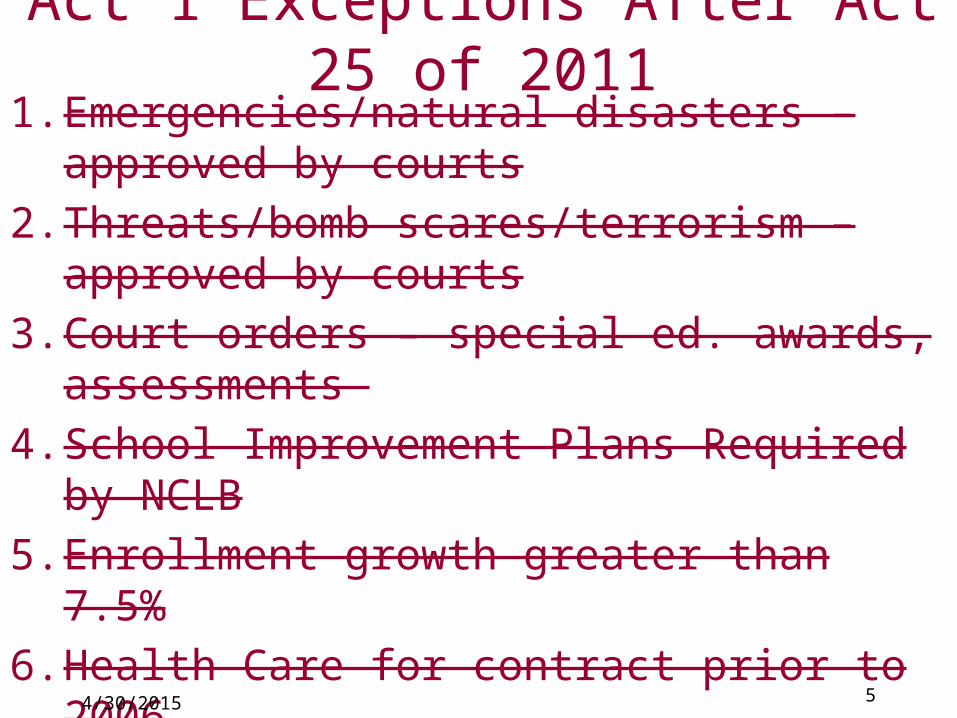

Act 1 of 2006

5

1. Emergencies/natural disasters – approved by courts

2. Threats/bomb scares/terrorism –approved by courts

3. Court orders – special ed. awards, assessments

4. School Improvement Plans Required by NCLB

5. Enrollment growth greater than 7.5%

6. Health Care for contract prior to 2006

7. State/local revenue growth below the base index

8. Construction debt prior to 2006

9. Special Education

10.Contribution to PSERS greater than base index4/30/2015

Act 1 Exceptions After Act 25 of 2011

6

2006

-07

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

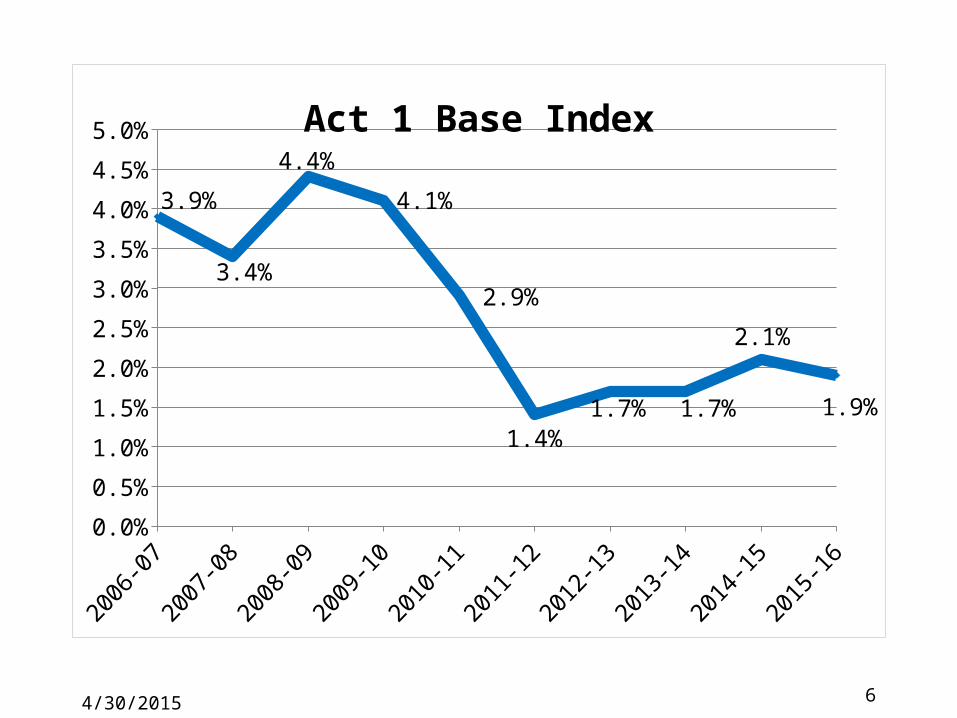

3.9%

3.4%

4.4%

4.1%

2.9%

1.4%1.7% 1.7%

2.1%

1.9%

Act 1 Base Index

4/30/2015

7

54-5

556

-57

58-5

960

-61

62-6

364

-65

66-6

768

-69

70-7

172

-73

74-7

576

-77

78-7

980

-81

82-8

384

-85

86-8

788

-89

90-9

192

-93

94-9

596

-97

98-9

900

-01

02-0

304

-05

06-0

708

-09

10-1

112

-13

14-1

516

-17

18-1

920

-21

22-2

324

-25

26-2

728

-29

30-3

132

-33

34-3

536

-37

38-3

940

-41

42-4

344

-45

46-4

70%

5%

10%

15%

20%

25%

30%

35%

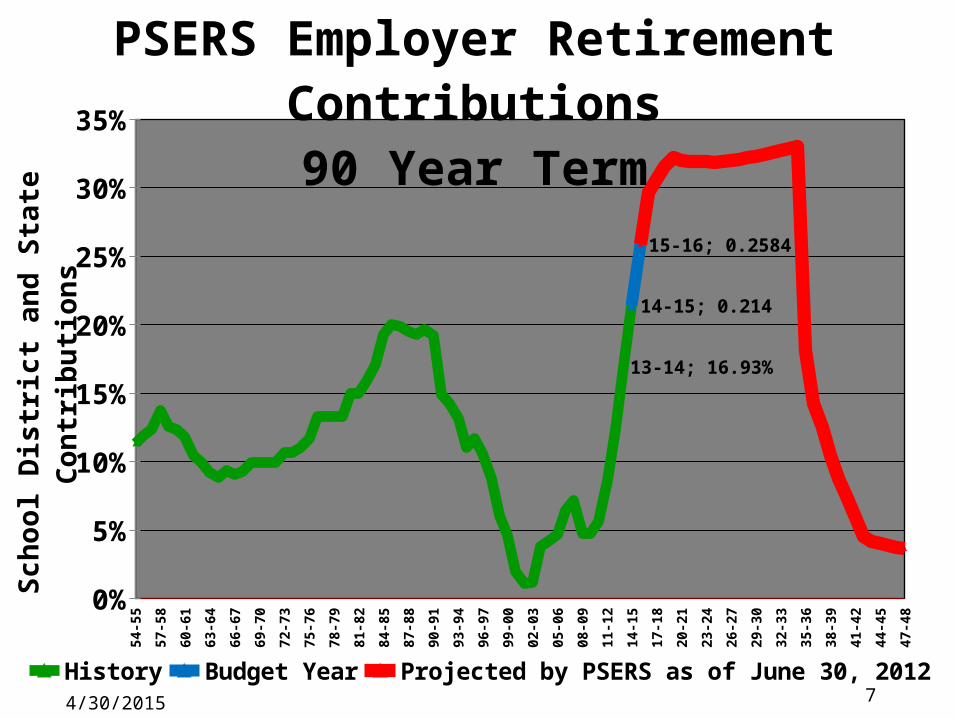

13-14; 16.93%

14-15; 0.214

15-16; 0.2584

History Budget Year Projected by PSERS as of June 30, 2012

Sch

ool D

istr

ict

and

Sta

te C

ontr

ibu

tion

sPSERS Employer Retirement Contributions

90 Year Term

4/30/2015

84/30/2015

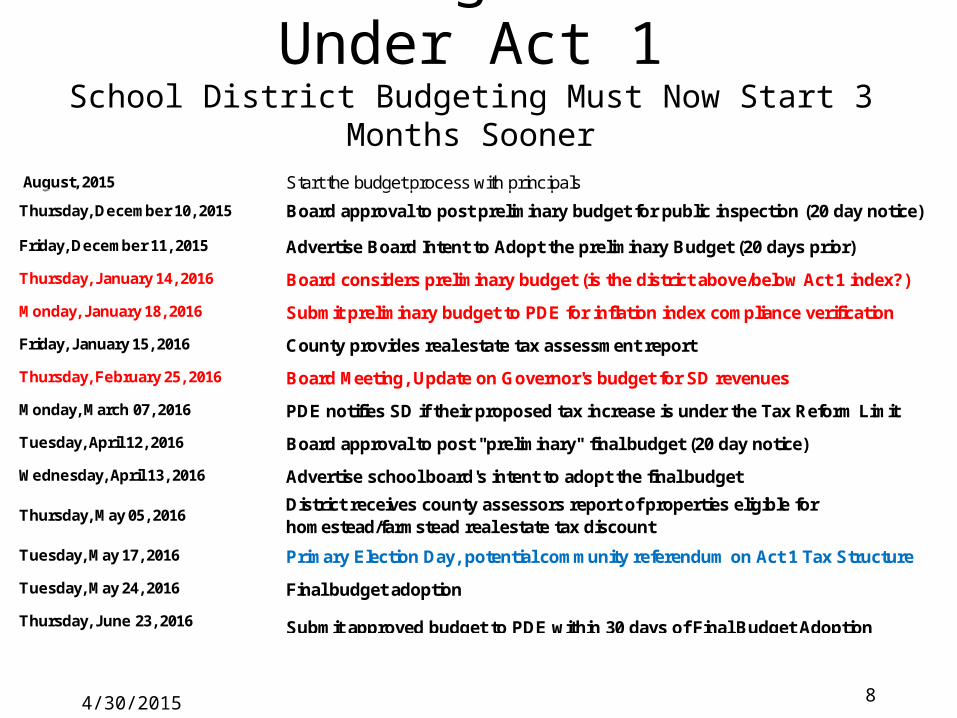

2015-16 Budget Timeline Under Act 1School District Budgeting Must Now Start 3 Months Sooner

August, 2015 Start the budget process with principals

Thursday, December 10, 2015

Friday, December 11, 2015 Advertise Board Intent to Adopt the preliminary Budget (20 days prior)

Thursday, January 14, 2016 Board considers preliminary budget (is the district above/below Act 1 index?)

Monday, January 18, 2016 Submit preliminary budget to PDE for inflation index compliance verification

Friday, January 15, 2016 County provides real estate tax assessment report

Thursday, February 25, 2016 Board Meeting, Update on Governor's budget for SD revenues

Monday, March 07, 2016 PDE notifies SD if their proposed tax increase is under the Tax Reform Limit

Tuesday, April 12, 2016 Board approval to post "preliminary" final budget (20 day notice)

Wednesday, April 13, 2016 Advertise school board's intent to adopt the final budget

Thursday, May 05, 2016

Tuesday, May 17, 2016 Primary Election Day, potential community referendum on Act 1 Tax Structure

Tuesday, May 24, 2016 Final budget adoption

Thursday, June 23, 2016 Submit approved budget to PDE within 30 days of Final Budget Adoption

District receives county assessors report of properties eligible for homestead/farmstead real estate tax discount

Board approval to post preliminary budget for public inspection (20 day notice)

94/30/2015

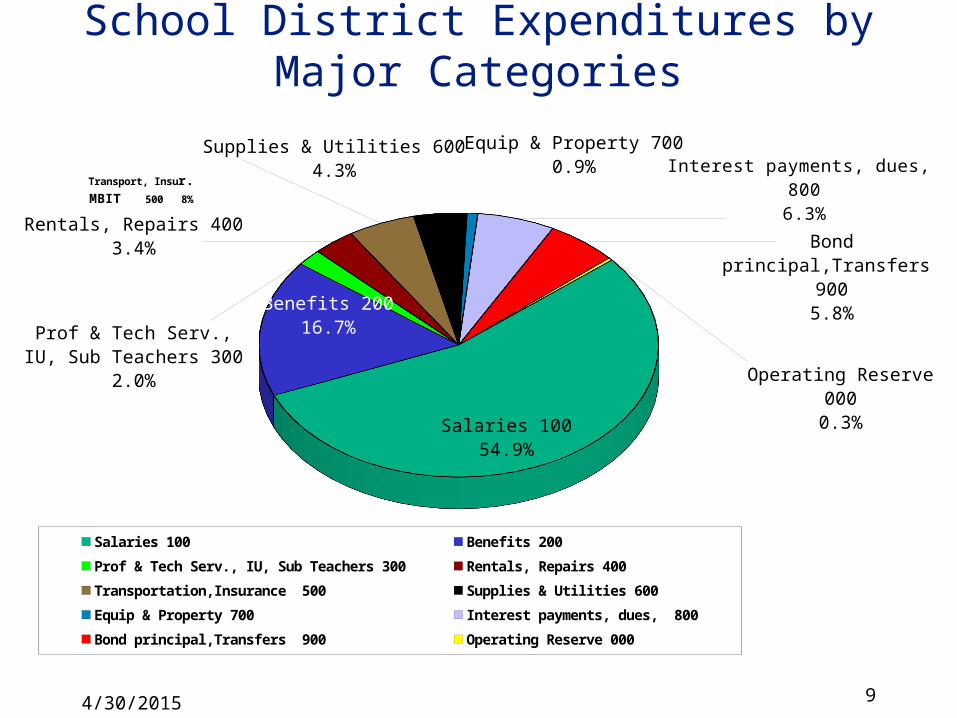

School District Expenditures by Major Categories

Salaries 10054.9%

Benefits 20016.7%

Prof & Tech Serv., IU, Sub Teachers 300

2.0%

Rentals, Repairs 4003.4%

Transport, Insur.MBIT 500 8%

Supplies & Utilities 6004.3%

Equip & Property 7000.9%

Interest payments, dues, 8006.3%

Bond principal,Transfers 900

5.8%

Operating Reserve 0000.3%

Salaries 100 Benefits 200 Prof & Tech Serv., IU, Sub Teachers 300

Rentals, Repairs 400 Transportation,Insurance 500 Supplies & Utilities 600

Equip & Property 700 Interest payments, dues, 800 Bond principal,Transfers 900

Operating Reserve 000

104/30/2015

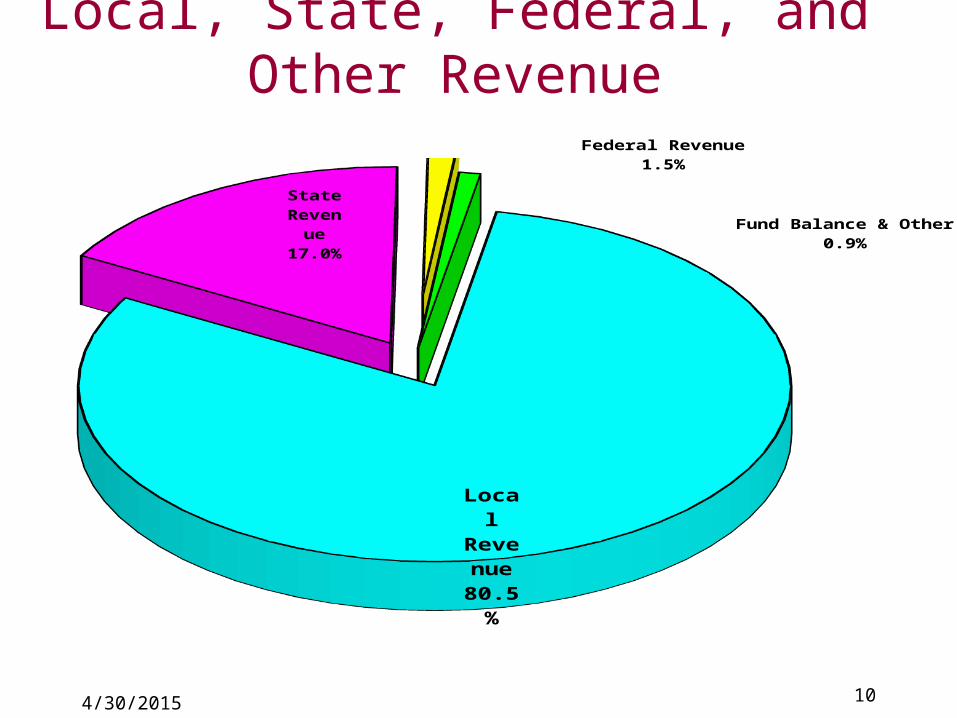

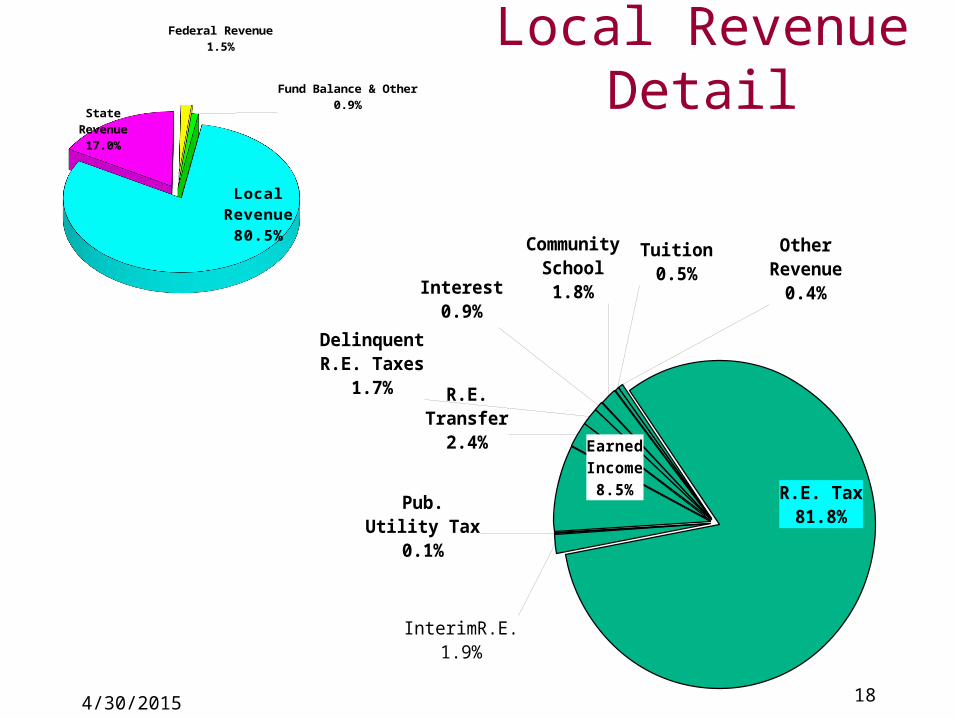

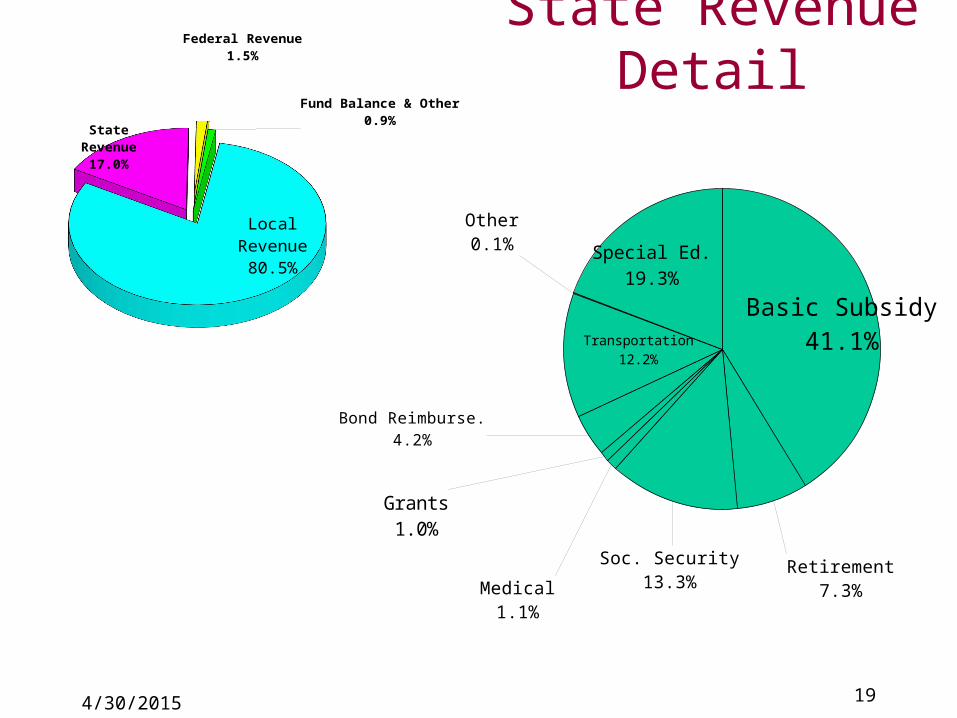

Local, State, Federal, and Other Revenue

Lo-cal Revenu

e80.5

%

State Rev-enue17.0

%

Federal Revenue1.5%

Fund Balance & Other0.9%

114/30/2015

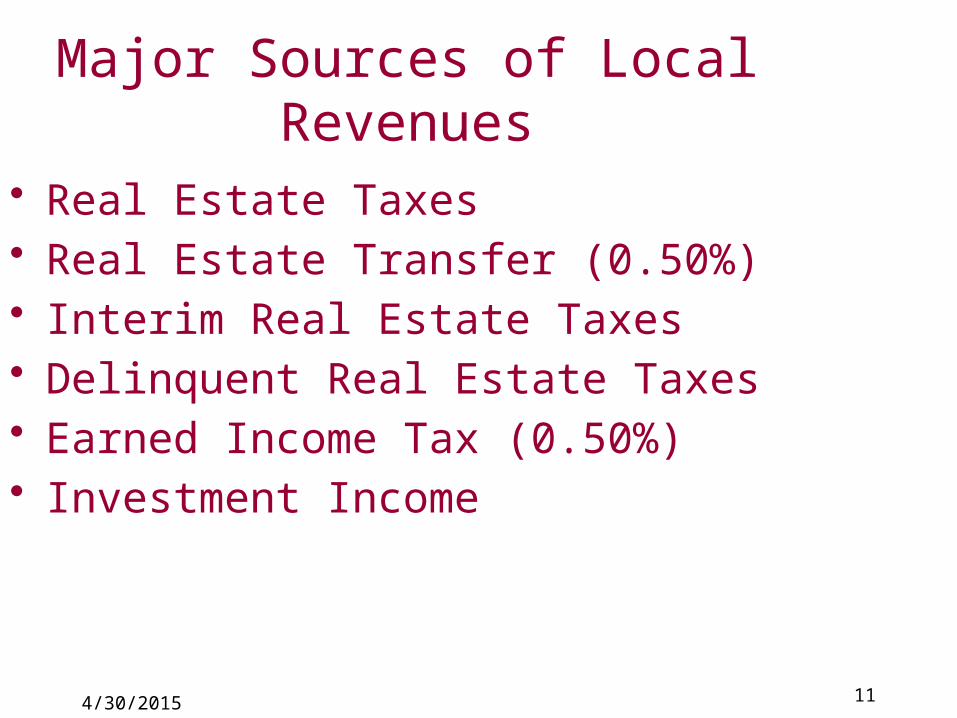

Major Sources of Local Revenues

• Real Estate Taxes• Real Estate Transfer (0.50%)• Interim Real Estate Taxes• Delinquent Real Estate Taxes• Earned Income Tax (0.50%)• Investment Income

124/30/2015

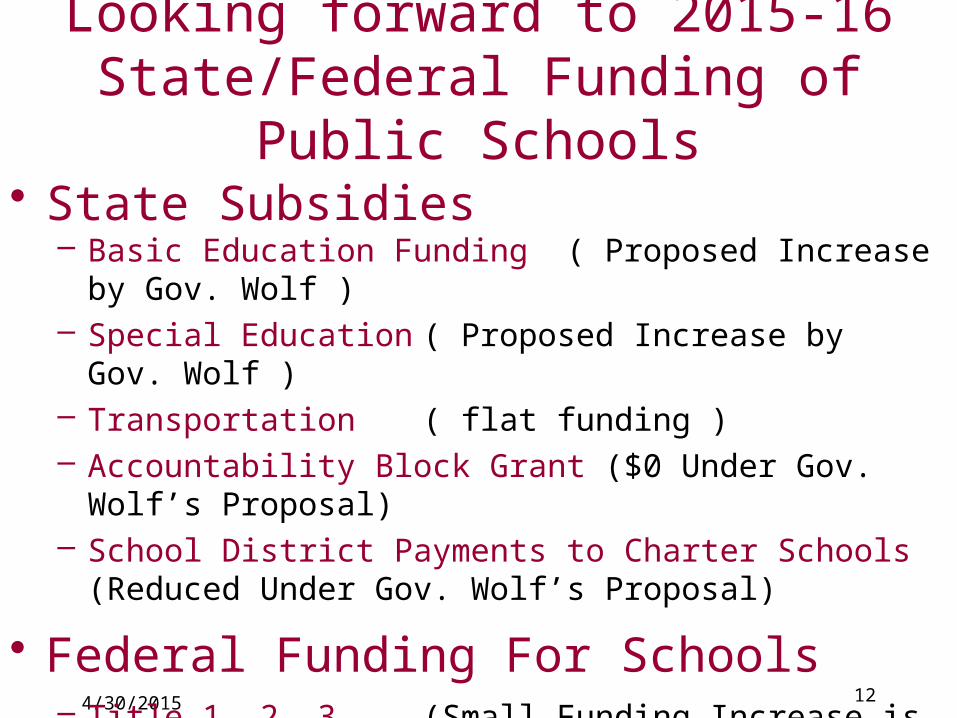

Looking forward to 2015-16State/Federal Funding of Public Schools

• State Subsidies– Basic Education Funding ( Proposed Increase by Gov. Wolf )– Special Education ( Proposed Increase by Gov. Wolf )– Transportation ( flat funding )– Accountability Block Grant ($0 Under Gov. Wolf’s Proposal)– School District Payments to Charter Schools (Reduced Under

Gov. Wolf’s Proposal)

• Federal Funding For Schools– Title 1, 2, 3 (Small Funding Increase is Expected)

134/30/2015

Spending From the State-Wide View Point

Spending From the State-Wide View Point

• Lets Take a Look at What has Been Happening to Public School Funding Over The Years

• Lets Take a Look at What has Been Happening to Public School Funding Over The Years

14

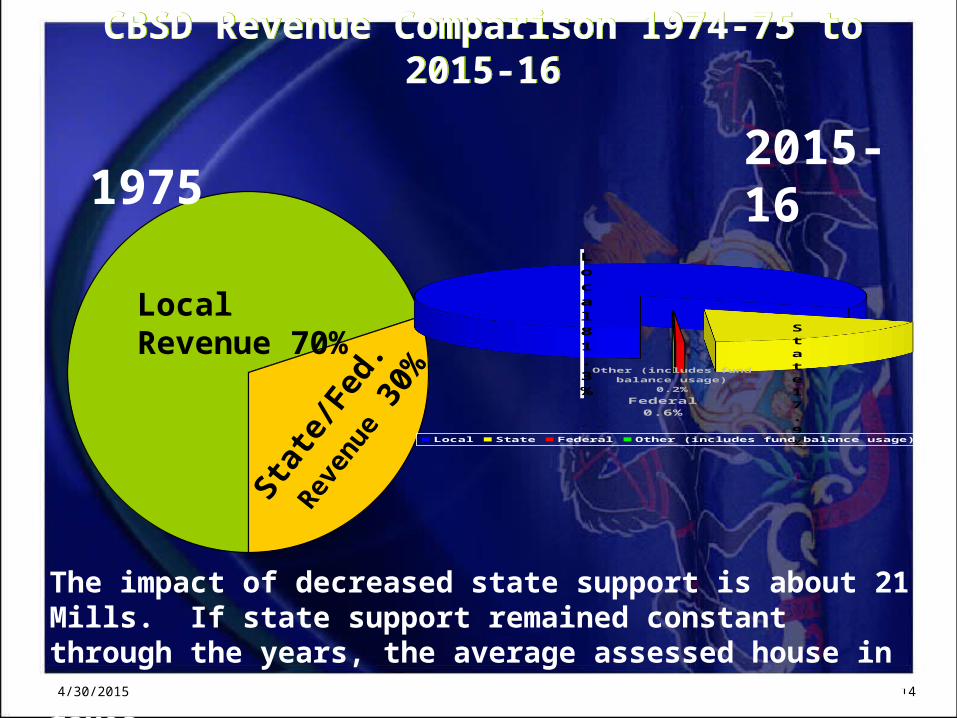

CBSD Revenue Comparison 1974-75 to 2015-16CBSD Revenue Comparison 1974-75 to 2015-16

Local Revenue 70%

Stat

e/Fed

.

Rev

enue

30%

1975Local81.3%

State17.9%

Federal0.6%

Other (includes fund balance usage)

0.2%

Local State Federal Other (includes fund balance usage)

2015-16

The impact of decreased state support is about 21 Mills. If state support remained constant through the years, the average assessed house in CB would be paying about $ 840 dollars less in RE taxes.

4/30/2015

15

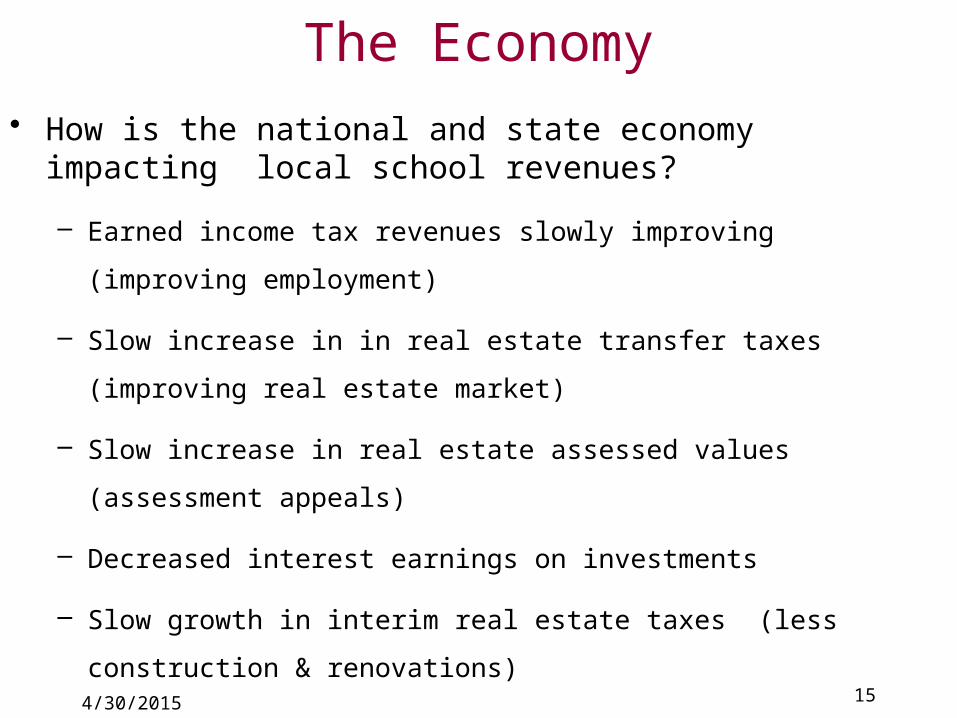

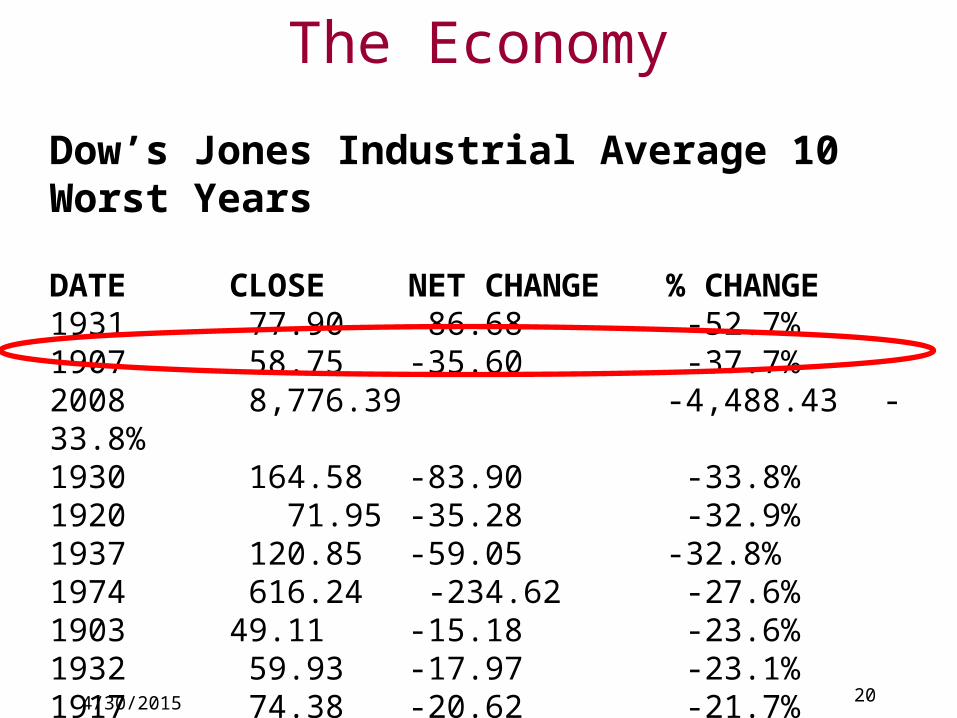

The Economy

4/30/2015

• How is the national and state economy impacting local school revenues?

– Earned income tax revenues slowly improving (improving employment)

– Slow increase in in real estate transfer taxes (improving real estate market)

– Slow increase in real estate assessed values (assessment appeals)

– Decreased interest earnings on investments

– Slow growth in interim real estate taxes (less construction & renovations)

– More families applying for free/reduced price lunches - starting to decline

164/30/2015

FUNDING PUBLIC EDUCATION

Questions?

174/30/2015

184/30/2015

Local Revenue Detail

R.E. Tax81.8%

InterimR.E.1.9%

Pub. Utility Tax0.1%

Earned Income8.5%

R.E. Transfer2.4%

Delinquent R.E. Taxes

1.7%

Interest0.9%

Community School1.8%

Tuition0.5%

Other Revenue

0.4%

Local Revenue

80.5%

State Revenue

17.0%

Federal Revenue1.5%

Fund Balance & Other0.9%

194/30/2015

State Revenue Detail

Basic Subsidy41.1%

Retirement7.3%

Soc. Security13.3%Medical

1.1%

Grants1.0%

Bond Reimburse.4.2%

Transportation12.2%

Other0.1%

Special Ed.19.3%

Local Revenue80.5%

State Revenue17.0%

Federal Revenue1.5%

Fund Balance & Other0.9%

20

The Economy

4/30/2015

Dow’s Jones Industrial Average 10 Worst Years

DATE CLOSE NET CHANGE % CHANGE 1931 77.90 -86.68 -52.7% 1907 58.75 -35.60 -37.7% 2008 8,776.39 -4,488.43 -33.8% 1930 164.58 -83.90 -33.8% 1920 71.95 -35.28 -32.9% 1937 120.85 -59.05 -32.8% 1974 616.24 -234.62 -27.6% 1903 49.11 -15.18 -23.6% 1932 59.93 -17.97 -23.1%1917 74.38 -20.62 -21.7%

21

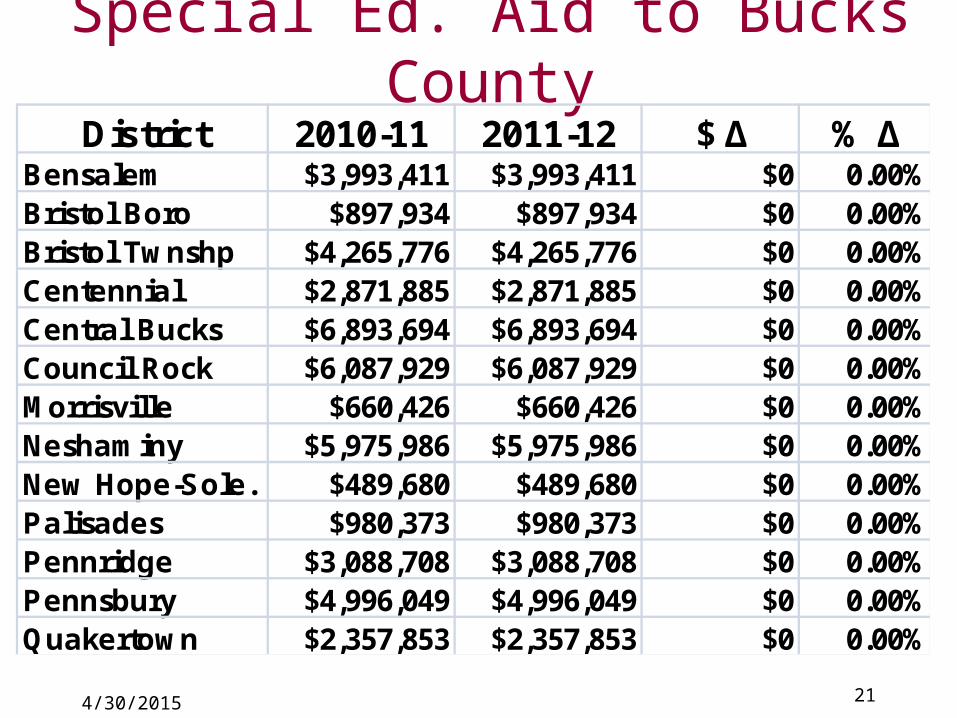

Special Ed. Aid to Bucks CountyDistrict 2010-11 2011-12 $ ∆ % ∆

Bensalem $3,993,411 $3,993,411 $0 0.00%Bristol Boro $897,934 $897,934 $0 0.00%Bristol Twnshp $4,265,776 $4,265,776 $0 0.00%Centennial $2,871,885 $2,871,885 $0 0.00%Central Bucks $6,893,694 $6,893,694 $0 0.00%Council Rock $6,087,929 $6,087,929 $0 0.00%Morrisville $660,426 $660,426 $0 0.00%Neshaminy $5,975,986 $5,975,986 $0 0.00%New Hope-Sole. $489,680 $489,680 $0 0.00%Palisades $980,373 $980,373 $0 0.00%Pennridge $3,088,708 $3,088,708 $0 0.00%Pennsbury $4,996,049 $4,996,049 $0 0.00%Quakertown $2,357,853 $2,357,853 $0 0.00%

4/30/2015

22

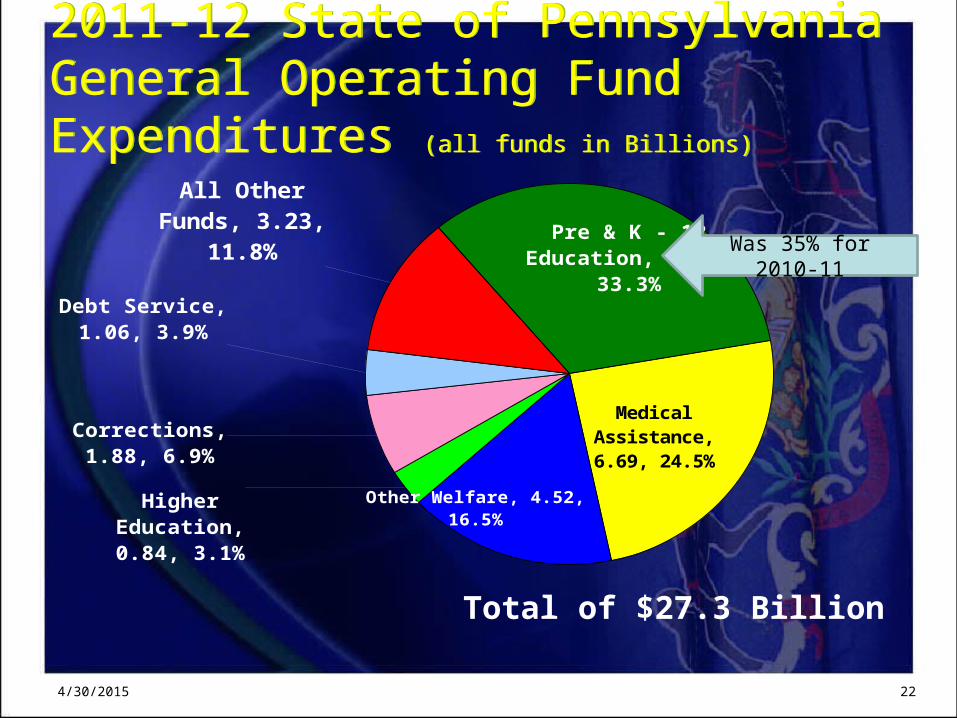

2011-12 State of Pennsylvania General Operating Fund Expenditures (all funds in Billions)

2011-12 State of Pennsylvania General Operating Fund Expenditures (all funds in Billions)

Pre & K - 12 Education, 9.11, 33.3%

Medical Assistance, 6.69, 24.5%

Other Welfare, 4.52, 16.5%Higher Education, 0.84, 3.1%

Corrections, 1.88, 6.9%

Debt Service, 1.06, 3.9%

All Other Funds, 3.23,

11.8%

Total of $27.3 Billion

4/30/2015

Was 35% for 2010-11

23

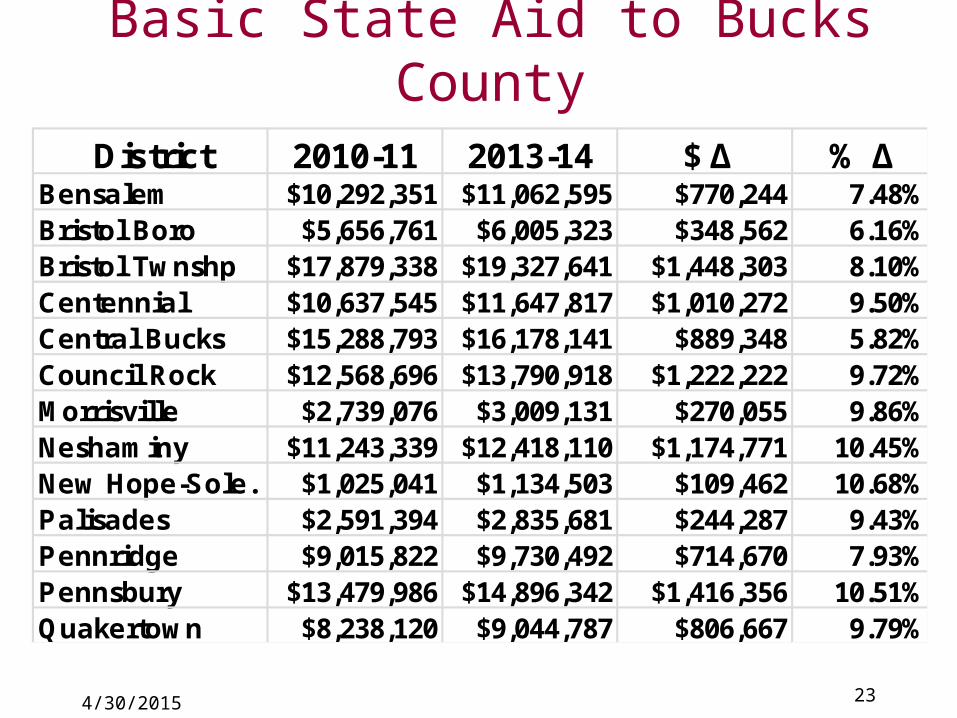

Basic State Aid to Bucks County

District 2010-11 2013-14 $ ∆ % ∆Bensalem $10,292,351 $11,062,595 $770,244 7.48%Bristol Boro $5,656,761 $6,005,323 $348,562 6.16%Bristol Twnshp $17,879,338 $19,327,641 $1,448,303 8.10%Centennial $10,637,545 $11,647,817 $1,010,272 9.50%Central Bucks $15,288,793 $16,178,141 $889,348 5.82%Council Rock $12,568,696 $13,790,918 $1,222,222 9.72%Morrisville $2,739,076 $3,009,131 $270,055 9.86%Neshaminy $11,243,339 $12,418,110 $1,174,771 10.45%New Hope-Sole. $1,025,041 $1,134,503 $109,462 10.68%Palisades $2,591,394 $2,835,681 $244,287 9.43%Pennridge $9,015,822 $9,730,492 $714,670 7.93%Pennsbury $13,479,986 $14,896,342 $1,416,356 10.51%Quakertown $8,238,120 $9,044,787 $806,667 9.79%

4/30/2015

24

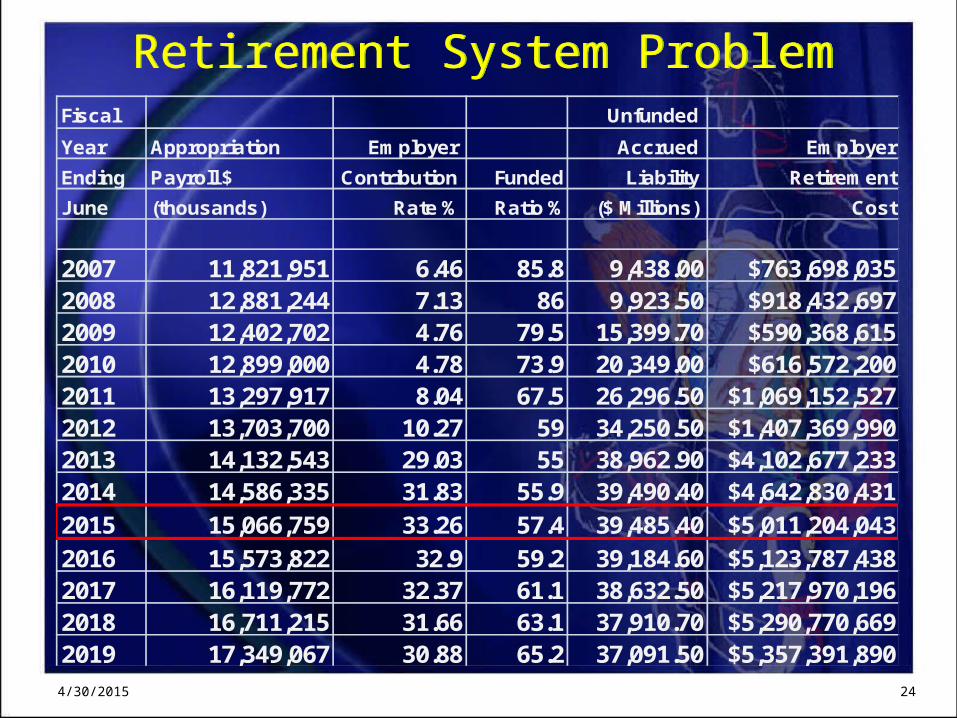

Retirement System ProblemRetirement System Problem

4/30/2015

Fiscal Unfunded

Year Appropriation Employer Accrued Employer

Ending Payroll $ Contribution Funded Liability Retirement

June (thousands) Rate % Ratio % ($ Millions) Cost

2007 11,821,951 6.46 85.8 9,438.00 $763,698,0352008 12,881,244 7.13 86 9,923.50 $918,432,6972009 12,402,702 4.76 79.5 15,399.70 $590,368,6152010 12,899,000 4.78 73.9 20,349.00 $616,572,2002011 13,297,917 8.04 67.5 26,296.50 $1,069,152,5272012 13,703,700 10.27 59 34,250.50 $1,407,369,9902013 14,132,543 29.03 55 38,962.90 $4,102,677,2332014 14,586,335 31.83 55.9 39,490.40 $4,642,830,431

2015 15,066,759 33.26 57.4 39,485.40 $5,011,204,043

2016 15,573,822 32.9 59.2 39,184.60 $5,123,787,4382017 16,119,772 32.37 61.1 38,632.50 $5,217,970,1962018 16,711,215 31.66 63.1 37,910.70 $5,290,770,6692019 17,349,067 30.88 65.2 37,091.50 $5,357,391,890

25

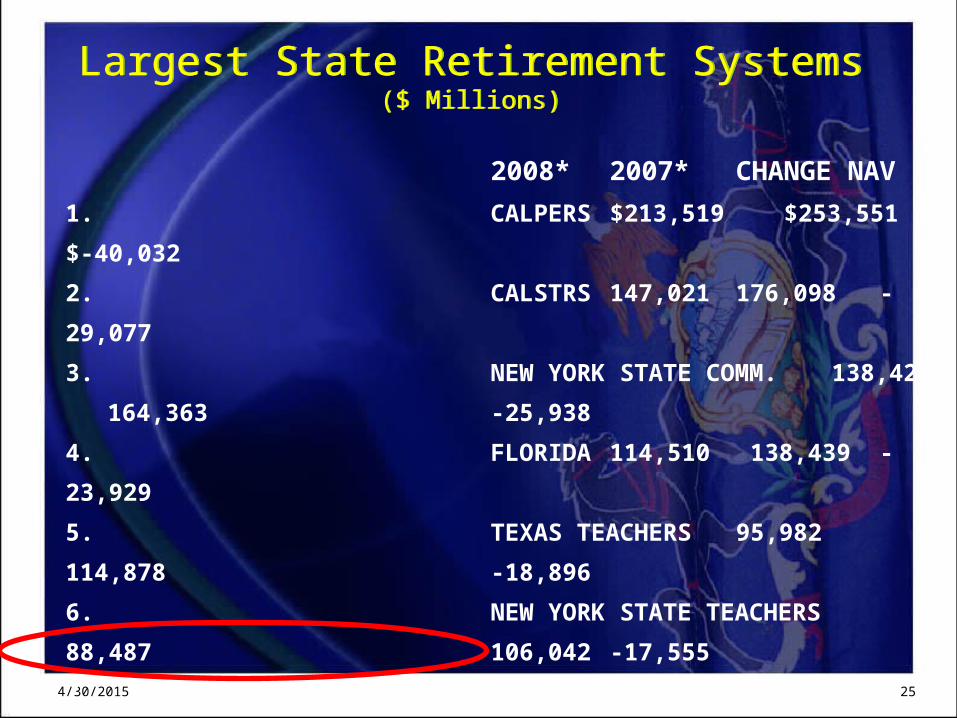

Largest State Retirement Systems($ Millions)

Largest State Retirement Systems($ Millions)

4/30/2015

2008* 2007* CHANGE NAV

1. CALPERS $213,519 $253,551 $-40,032

2. CALSTRS 147,021 176,098 -29,077

3. NEW YORK STATE COMM. 138,425 164,363 -25,938

4. FLORIDA 114,510 138,439 -23,929

5. TEXAS TEACHERS 95,982 114,878 -18,896

6. NEW YORK STATE TEACHERS 88,487 106,042 -17,555

7. WISCONSIN INVESTMENT BD. 72,493 89,328 -16,835

8. NEW JERSEY 70,826, 82,780, -11,954,

9. NORTH CAROLINA 65,924 77,384 -11,460

10. OHIO STATE TEACHERS 62,611 78,311 -15,700

11. OHIO PUBLIC EMPLOYEES 57,940 84,123 -26,183

12. Pennsylvania School Employees 54,666 68,678 -14,012

264/30/2015

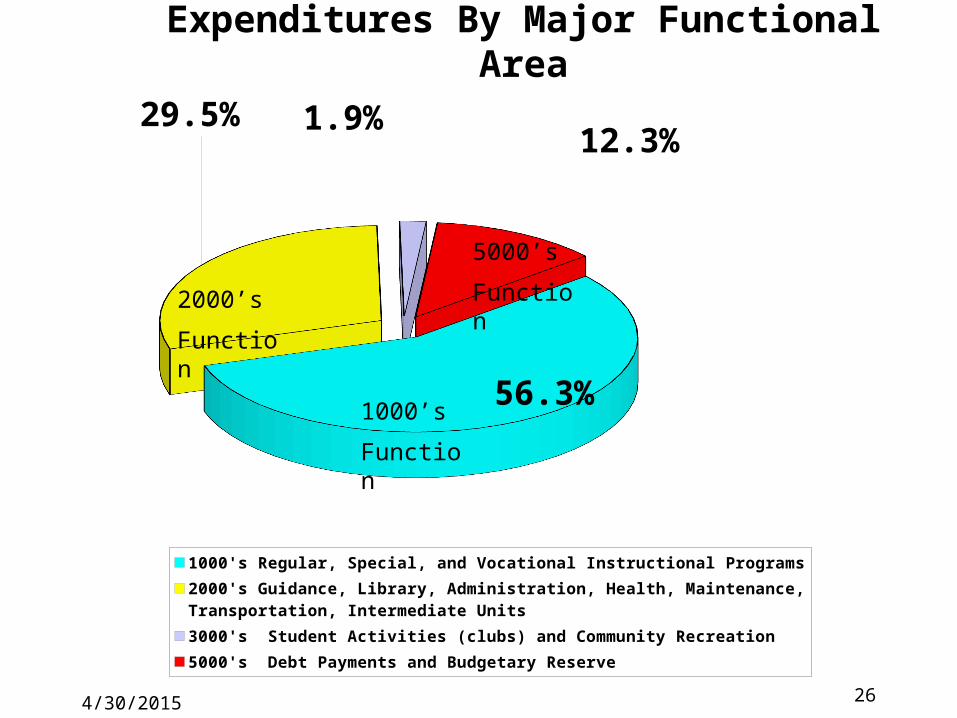

56.3%

29.5% 1.9%12.3%

1000's Regular, Special, and Vocational Instructional Programs2000's Guidance, Library, Administration, Health, Maintenance, Transportation, Intermediate Units 3000's Student Activities (clubs) and Community Recreation5000's Debt Payments and Budgetary Reserve

Expenditures By Major Functional Area

1000’s

Function

2000’s

Function

5000’s

Function

4/30/2015 36

May 5, 2007Bucks County IU#22

Act 1 Overview

Higher Income Taxes and Slot Machine Proceeds Reduce Residential

Real Estate Taxes

374/30/2015

Act 1 - Overview

Act 1 provides a vehicle for the community within a school district to opt into real estate tax reform by shifting some taxes from real estate to an income tax.

The tax shift from real estate to an income based tax can be accomplished through raising the Earned Income Tax (EIT) or implementing an Equivalent Personal Income Tax (PIT).

384/30/2015

What is EIT

The Earned income tax (EIT) is a tax on gross wages paid to the municipality and school district where you live – not where you work.

The current earned income tax is 1% of gross wages. A half of 1% goes to CBSD and a half of 1% goes to the township or borough where you live.

Pensions and social security are not taxable.

394/30/2015

How Tax Reform Works

Only primary residential properties and Farms are eligible for a real estate tax credit.– Apartments, vacation homes, and commercial

properties are not eligible for real estate tax credits. Why?

• Apartments are considered to be commercial properties. And, commercial properties should not benefit from a tax reduction since the properties will not pay any additional wage taxes to help fund the real estate tax credits.

The county Assessors Office determines what properties are eligible for a real estate tax credit (not the school district).

404/30/2015

Tax Reform in Four Easy Steps

414/30/2015

Step 1

In Central Bucks, the Median Assessed Value of a home for real estate taxing purposes is $36,800.

Then …

– The tax study commission can recommend an assessment reduction ranging from 25% to 50%

424/30/2015

Step 2

The tax study commission recommended a 25% discount for the median assessed valued home….– On a home with an assessed value of $36,800, a 25%

reduction is $9,200 of assessed value (taxable value).– $9,200 x the district millage rate = the $ discount that

people will see on their tax bill.• $9,200 x 102 mills (.102) = $970. (after Act 1 formula rounding)

This is the discount everyone would see on their tax bill even if their house has an assessed value of more than $36,800

434/30/2015

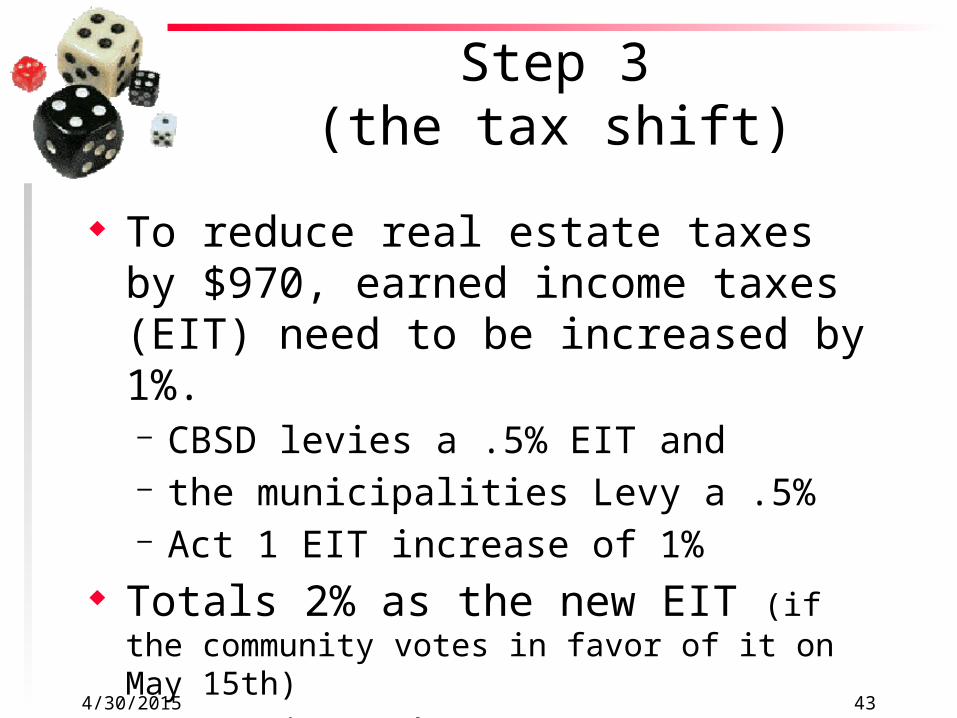

Step 3(the tax shift)

To reduce real estate taxes by $970, earned income taxes (EIT) need to be increased by 1%.– CBSD levies a .5% EIT and – the municipalities Levy a .5%– Act 1 EIT increase of 1%

Totals 2% as the new EIT (if the community votes in favor of it on May 15th)– But, it’s the new 1% tax we are interested in…

444/30/2015

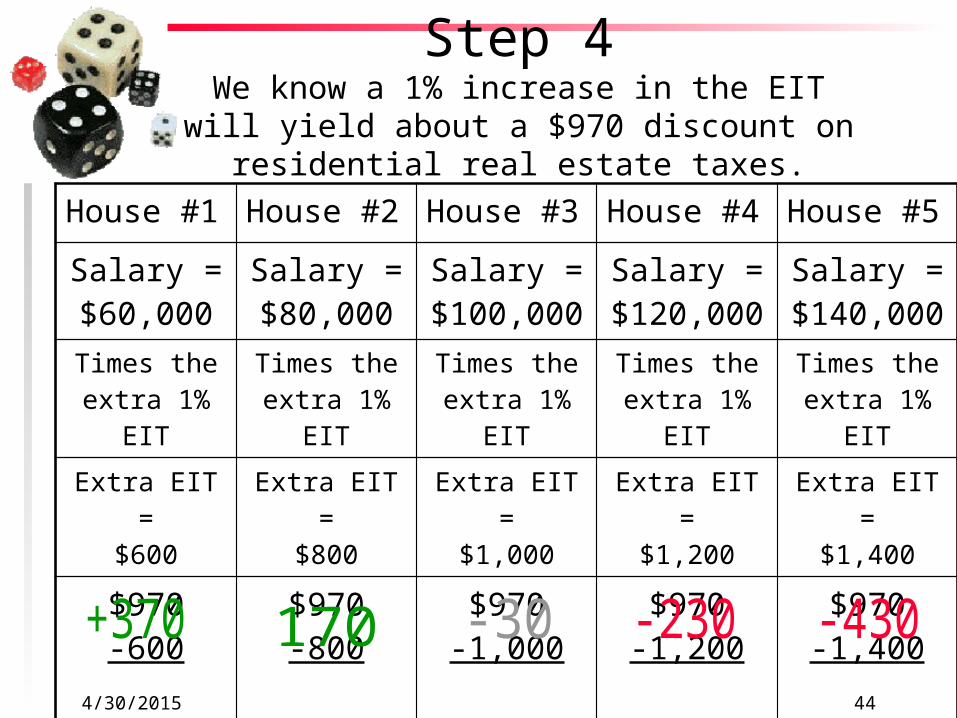

Step 4We know a 1% increase in the EIT will yield about a

$970 discount on residential real estate taxes.

House #1 House #2 House #3 House #4 House #5

Salary = $60,000

Salary = $80,000

Salary = $100,000

Salary = $120,000

Salary = $140,000

Times the extra 1% EIT

Times the extra 1% EIT

Times the extra 1% EIT

Times the extra 1% EIT

Times the extra 1% EIT

Extra EIT =$600

Extra EIT =$800

Extra EIT =$1,000

Extra EIT =$1,200

Extra EIT =$1,400

$970-600

$970-800

$970-1,000

$970-1,200

$970-1,400

454/30/2015

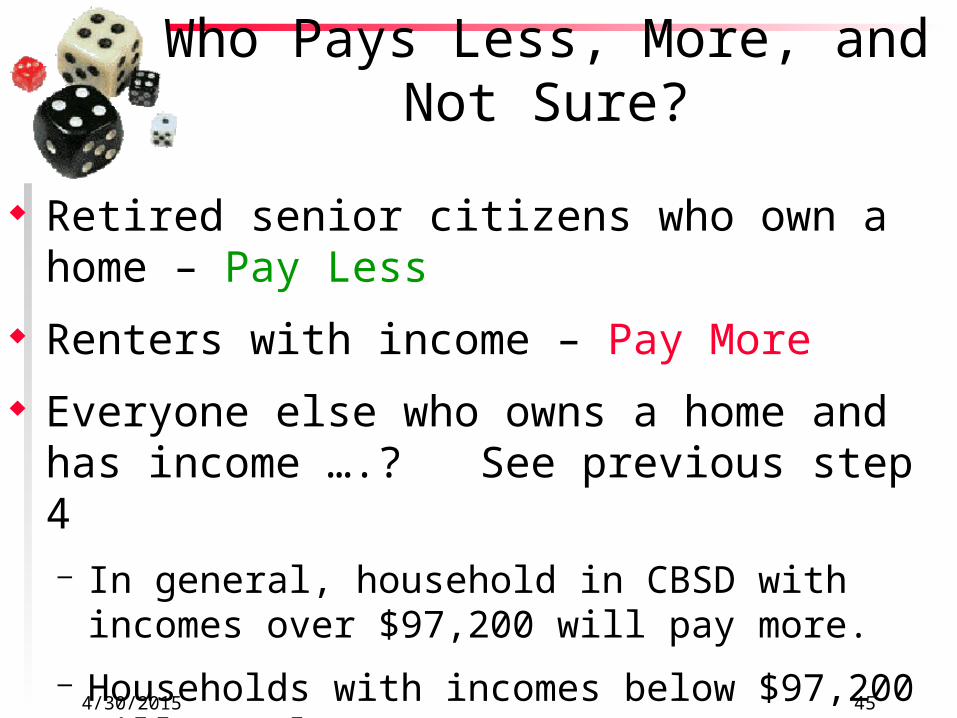

Who Pays Less, More, and Not Sure?

Retired senior citizens who own a home – Pay Less

Renters with income – Pay More

Everyone else who owns a home and has income ….? See previous step 4 – In general, household in CBSD with incomes over

$97,200 will pay more.

– Households with incomes below $97,200 will pay less.

46

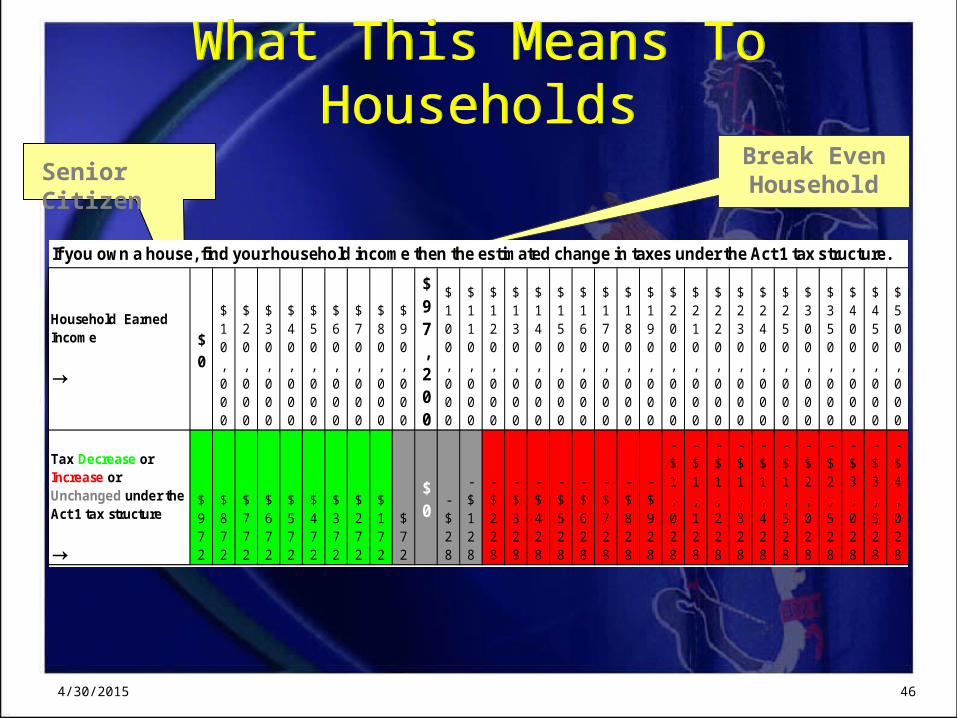

What This Means To HouseholdsWhat This Means To Households

If you own a house, find your household income then the estimated change in taxes under the Act 1 tax structure.

Household Earned Income

→$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$97,200

$100,000

$110,000

$120,000

$130,000

$140,000

$150,000

$160,000

$170,000

$180,000

$190,000

$200,000

$210,000

$220,000

$230,000

$240,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

Tax Decrease or Increase or Unchanged under the Act 1 tax structure

→

$972

$872

$772

$672

$572

$472

$372

$272

$172

$72

$0

-$28

-$128

-$228

-$328

-$428

-$528

-$628

-$728

-$828

-$928

-$1,028

-$1,128

-$1,228

-$1,328

-$1,428

-$1,528

-$2,028

-$2,528

-$3,028

-$3,528

-$4,028

4/30/2015

Senior CitizenBreak Even Household

47

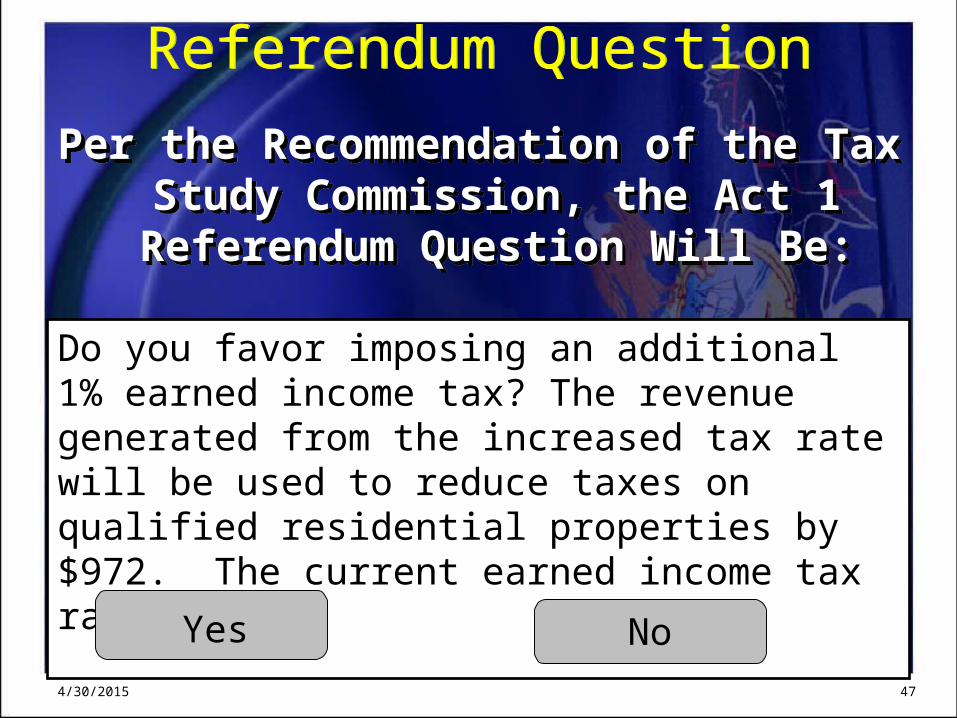

Referendum QuestionReferendum Question

Per the Recommendation of the Tax Study Commission, the Act 1 Referendum

Question Will Be:

Per the Recommendation of the Tax Study Commission, the Act 1 Referendum

Question Will Be:

4/30/2015

Do you favor imposing an additional 1% earned income tax? The revenue generated from the increased tax rate will be used to reduce taxes on qualified residential properties by $972. The current earned income tax rate is .5%.

Yes No

484/30/2015

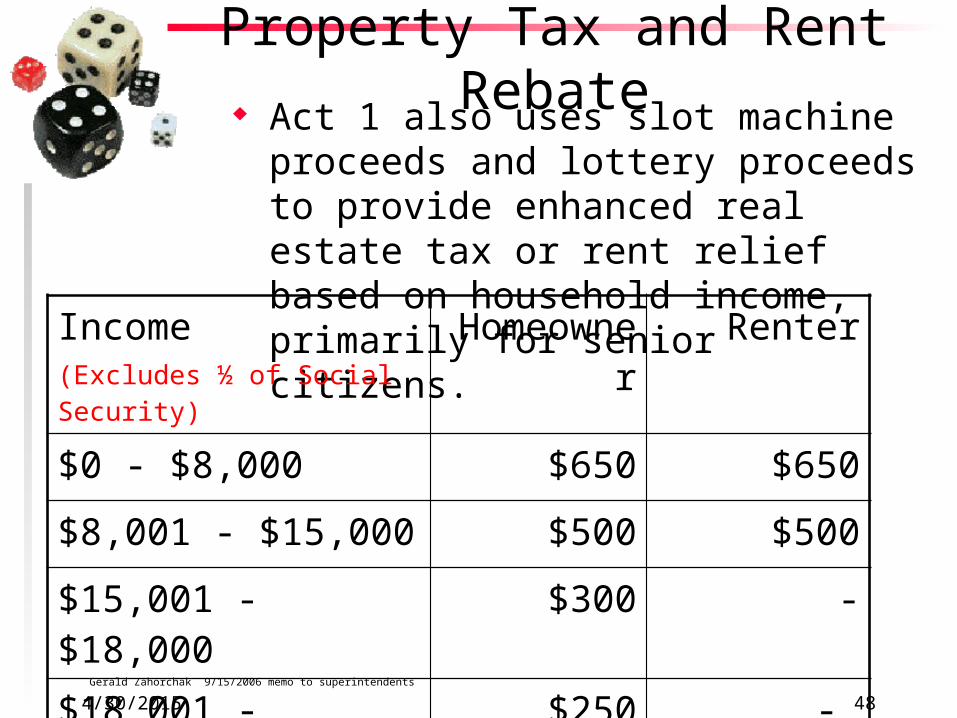

Property Tax and Rent Rebate Act 1 also uses slot machine proceeds and

lottery proceeds to provide enhanced real estate tax or rent relief based on household income, primarily for senior citizens.

Income (Excludes ½ of Social Security)

Homeowner Renter

$0 - $8,000 $650 $650

$8,001 - $15,000 $500 $500

$15,001 - $18,000 $300 -

$18,001 - $35,000 $250 -

Gerald Zahorchak 9/15/2006 memo to superintendents

494/30/2015

FUNDING PUBLIC EDUCATION

Questions?