Embed Size (px)

Citation preview

vv

$ubrogation: Maximizing Recoveries &

Avoiding Pitfalls

Olivia Martinez PARAGON SUBROGATION SERVICES, INC. 9221 CORBIN AVENUE, SUITE 250 NORTHRIDGE, CALIFORNIA 91324

Telephone: (888) 329-3332 WWW.PARAGONSUBRO.COM

E-Mail: [email protected]

Alan J. Yacoubian JOHNSON, YACOUBIAN & PAYSSÉ

701 POYDRAS STREET, SUITE 4700 NEW ORLEANS, LOUISIANA 70139-7708

Telephone: (504) 528-3001 WWW.JYPLAWFIRM.COM E-Mail: [email protected]

Randall J. Poelma, Jr. DOYEN SEBESTA LLP

450 GEARS ROAD, SUITE 350 HOUSTON, TEXAS 77067 Telephone: (713) 580-8900 WWW.DS-LAWYERS.COM

E-Mail: [email protected]

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

What is $ubrogation?

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

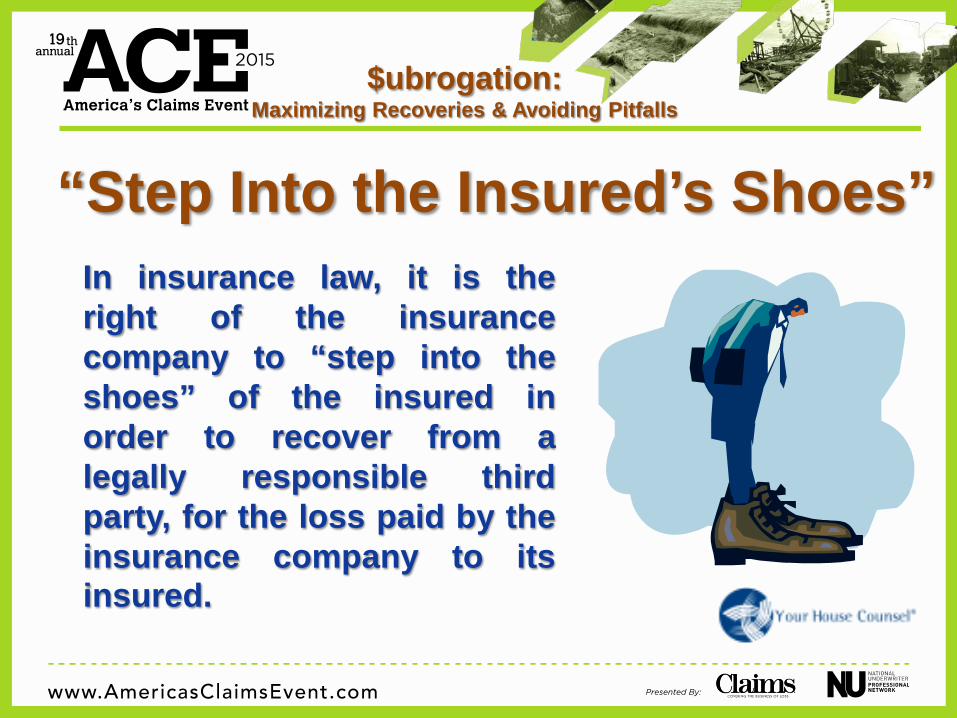

“Step Into the Insured’s Shoes” In insurance law, it is the right of the insurance company to “step into the shoes” of the insured in order to recover from a legally responsible third party, for the loss paid by the insurance company to its insured.

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

Benefits of Subrogation

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

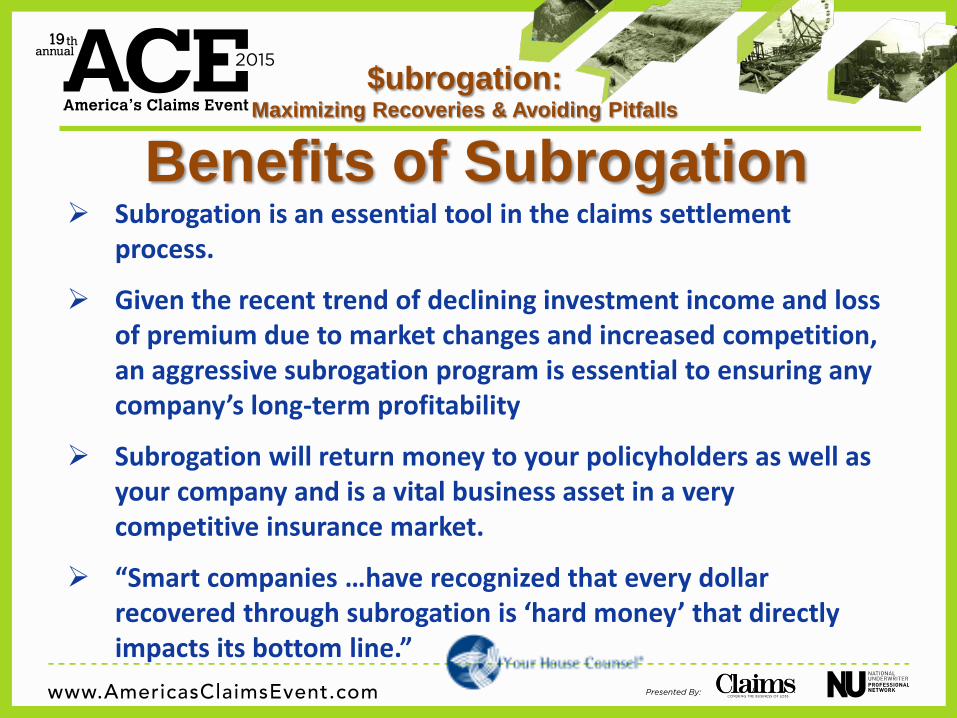

Benefits of Subrogation Subrogation is an essential tool in the claims settlement

process.

Given the recent trend of declining investment income and loss of premium due to market changes and increased competition, an aggressive subrogation program is essential to ensuring any company’s long-term profitability

Subrogation will return money to your policyholders as well as your company and is a vital business asset in a very competitive insurance market.

“Smart companies …have recognized that every dollar recovered through subrogation is ‘hard money’ that directly impacts its bottom line.”

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

Benefits of Subrogation (cont.)

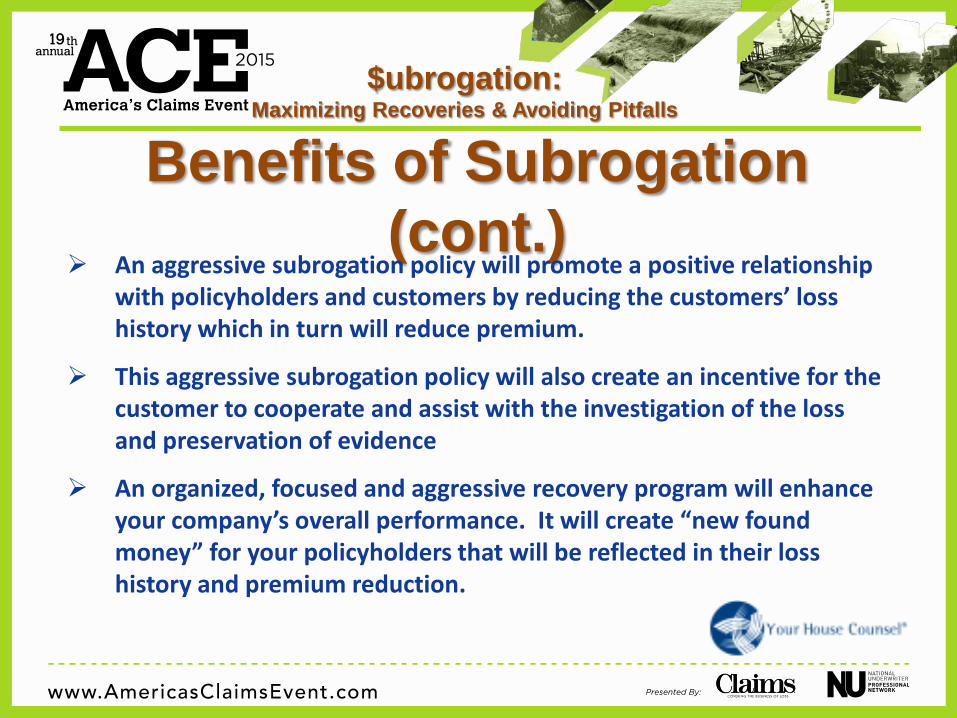

An aggressive subrogation policy will promote a positive relationship

with policyholders and customers by reducing the customers’ loss history which in turn will reduce premium.

This aggressive subrogation policy will also create an incentive for the customer to cooperate and assist with the investigation of the loss and preservation of evidence

An organized, focused and aggressive recovery program will enhance your company’s overall performance. It will create “new found money” for your policyholders that will be reflected in their loss history and premium reduction.

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

Maximizing $ubrogation Recoveries

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

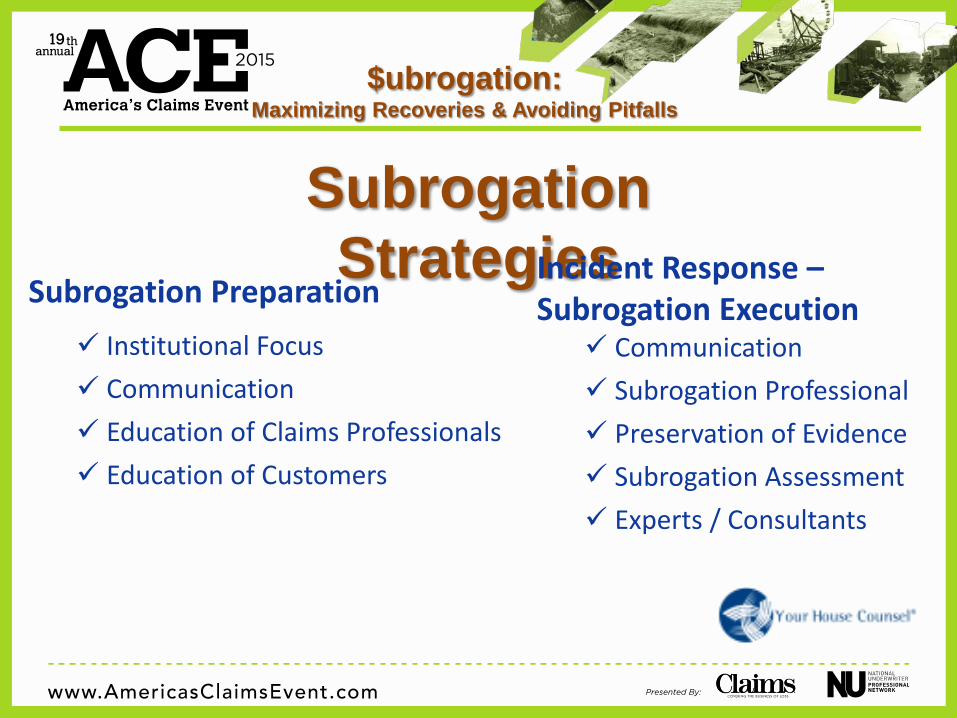

Subrogation Preparation Institutional Focus Communication Education of Claims Professionals Education of Customers

Subrogation Strategies Incident Response –

Subrogation Execution Communication Subrogation Professional Preservation of Evidence Subrogation Assessment Experts / Consultants

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

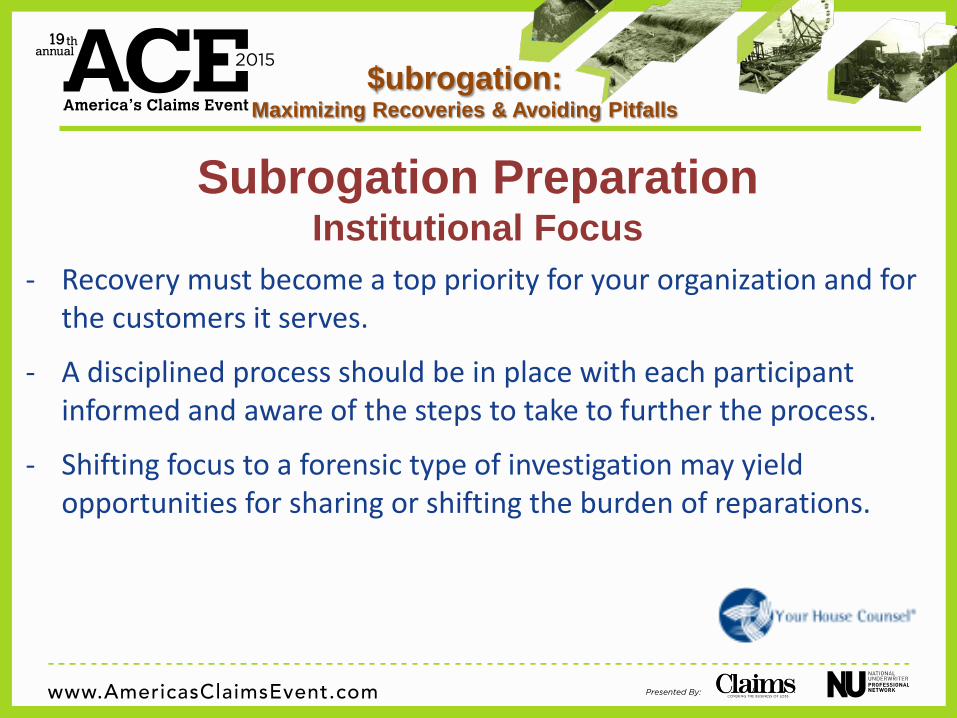

- Recovery must become a top priority for your organization and for the customers it serves.

- A disciplined process should be in place with each participant informed and aware of the steps to take to further the process.

- Shifting focus to a forensic type of investigation may yield opportunities for sharing or shifting the burden of reparations.

Subrogation Preparation Institutional Focus

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

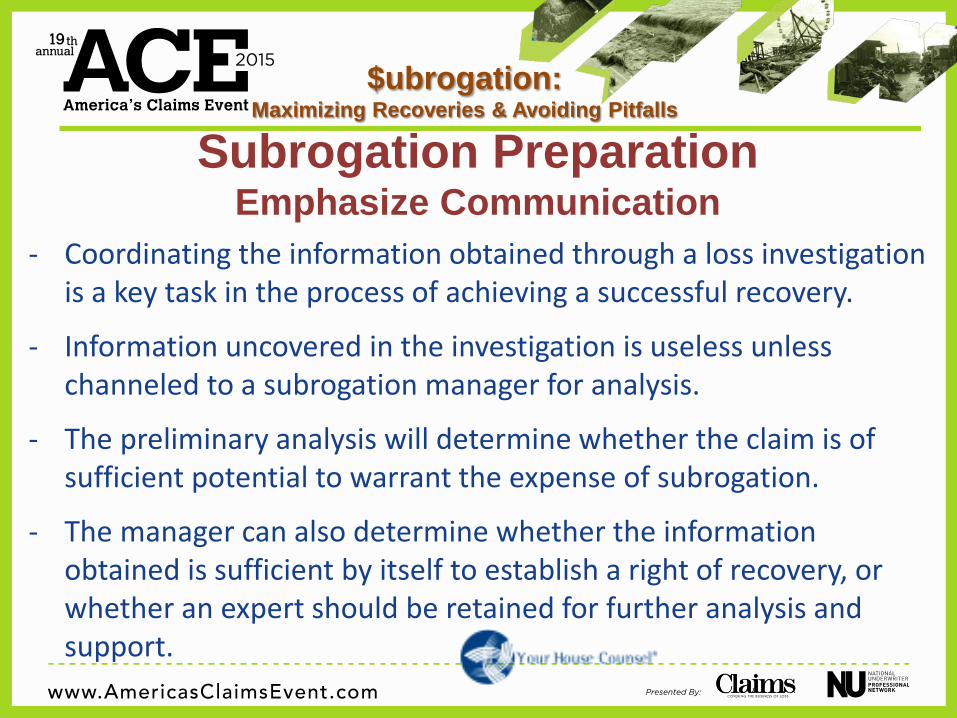

- Coordinating the information obtained through a loss investigation is a key task in the process of achieving a successful recovery.

- Information uncovered in the investigation is useless unless channeled to a subrogation manager for analysis.

- The preliminary analysis will determine whether the claim is of sufficient potential to warrant the expense of subrogation.

- The manager can also determine whether the information obtained is sufficient by itself to establish a right of recovery, or whether an expert should be retained for further analysis and support.

Subrogation Preparation Emphasize Communication

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

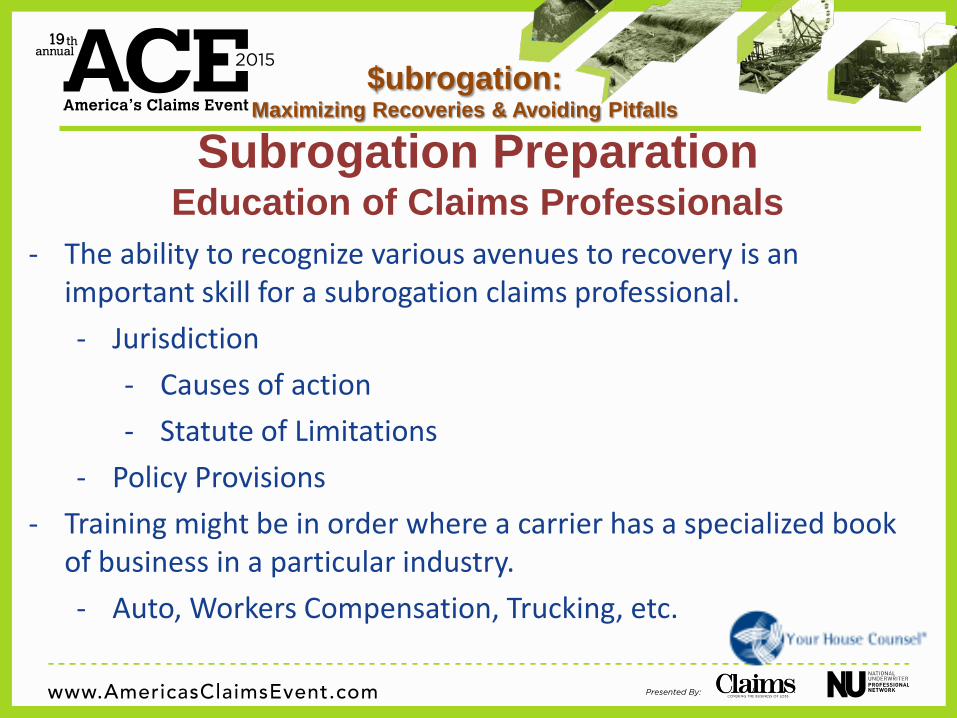

- The ability to recognize various avenues to recovery is an important skill for a subrogation claims professional. - Jurisdiction

- Causes of action - Statute of Limitations

- Policy Provisions - Training might be in order where a carrier has a specialized book

of business in a particular industry. - Auto, Workers Compensation, Trucking, etc.

Subrogation Preparation Education of Claims Professionals

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

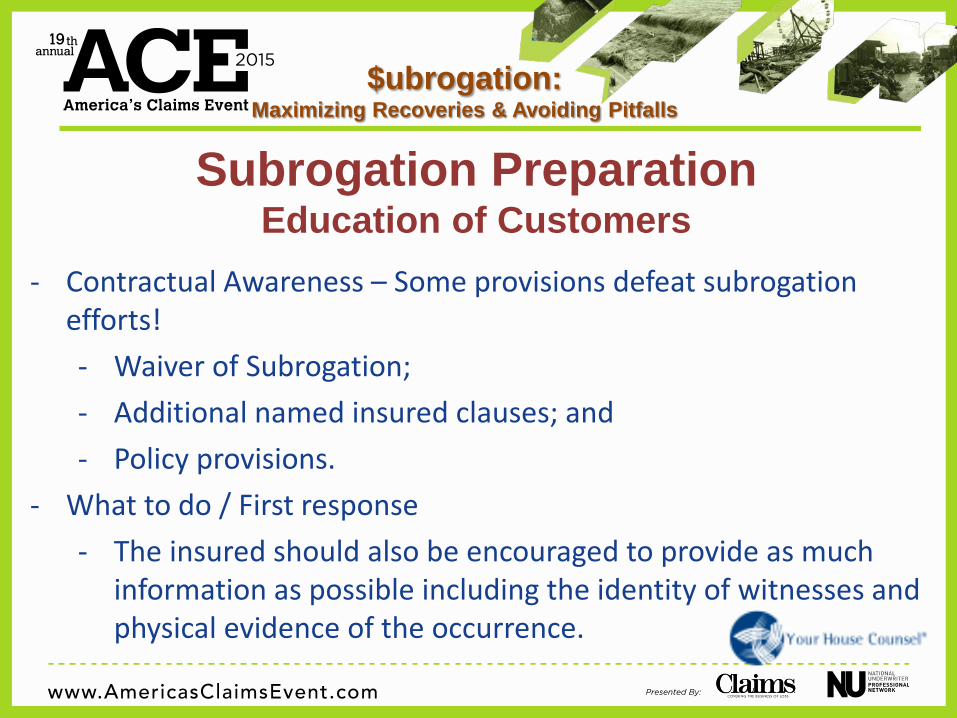

- Contractual Awareness – Some provisions defeat subrogation efforts! - Waiver of Subrogation; - Additional named insured clauses; and - Policy provisions.

- What to do / First response - The insured should also be encouraged to provide as much

information as possible including the identity of witnesses and physical evidence of the occurrence.

Subrogation Preparation Education of Customers

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

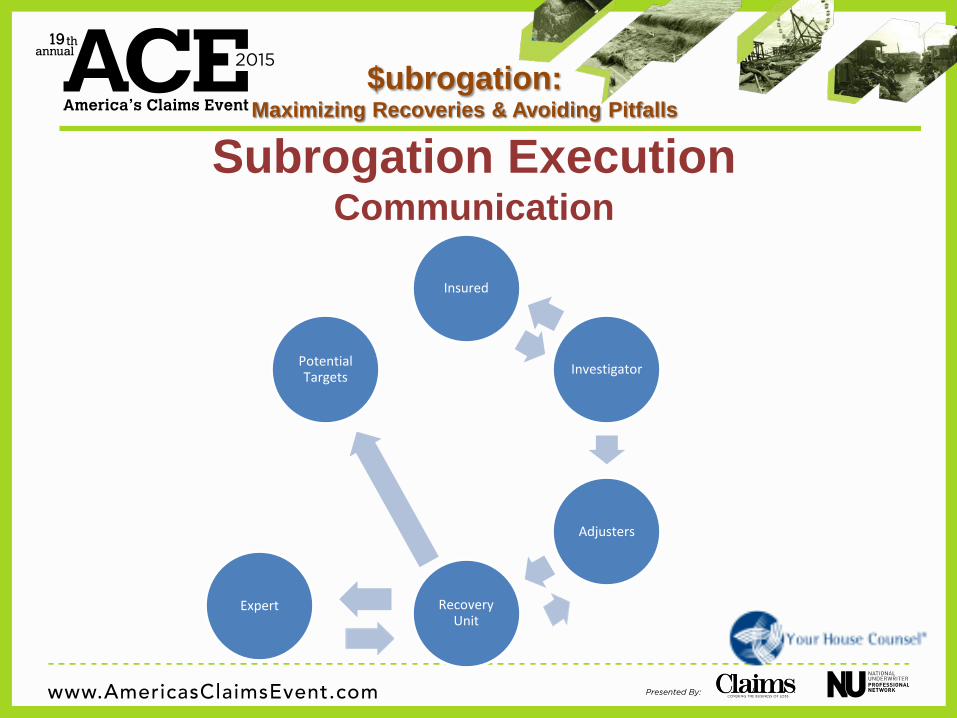

Insured

Investigator

Adjusters

Recovery Unit

Expert

Potential Targets

Subrogation Execution Communication

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

- Effective management of the loss scene is critical. - First and foremost, physical control of the loss scene, such as

effective containment and response, is vital to prevent additional damages.

- Once the evidence is secured, potentially responsible third parties should then be notified so that they have an opportunity to conduct their own inspection of the evidence and cannot later claim spoliation.

- Example – Utility provider of natural gas uses “curb cock”

Subrogation Execution Evidence: Collection &

Preservation

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

Dependent on insurance product

• Workers Compensation • Auto / Hull / Property • Liability (Commercial,

Personal, E&O, D&O, etc.)

• Health Insurance

Subrogation Execution Subrogation Assessment

Potential Theories • Breach of Contract / Breach of Warranty (Implied/Express) • Products Liability • Design / Construction Defect (including weather events) • Spread or Exacerbation of Damages

• Be creative under the circumstances

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

- Experts are an expensive proposition in any case, but when the size and complexity of a loss is significant they are well worth the investment.

- Have an expert on “standby.” - Having an expert who is willing to rush to the scene of an

accident to conduct a forensic investigation is invaluable. - Conducting interviews after a loss may lead to the loss of

valuable evidence. - Prepare and Think Subrogation!

Subrogation Execution Experts Consultants

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

Pitfalls to Avoid in Handling Subrogation Claims

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

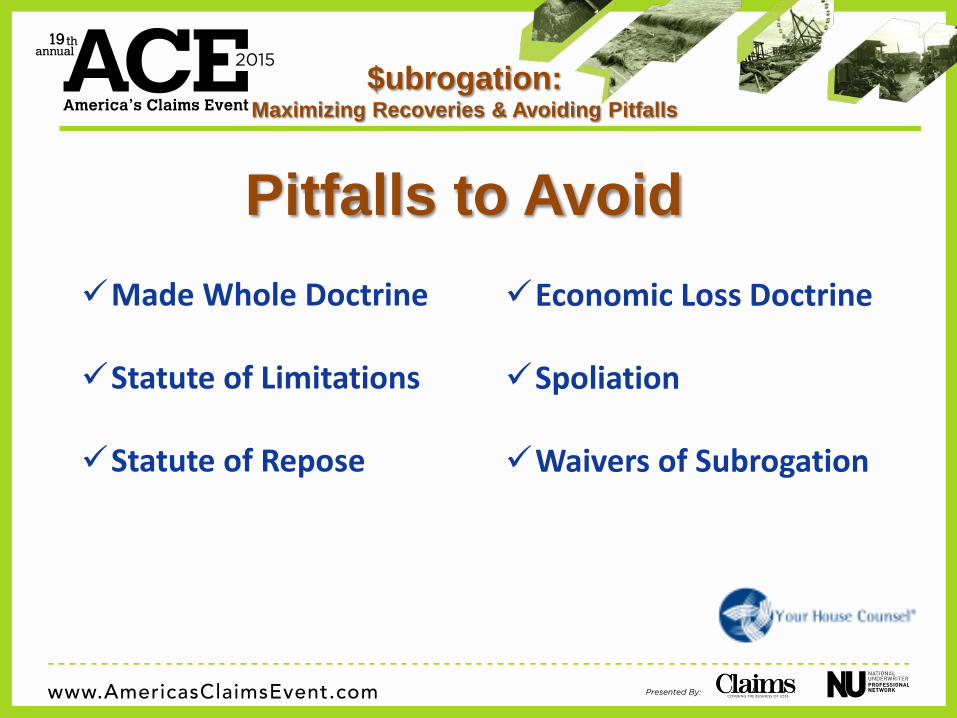

Pitfalls to Avoid Made Whole Doctrine

Statute of Limitations

Statute of Repose

Economic Loss Doctrine Spoliation

Waivers of Subrogation

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

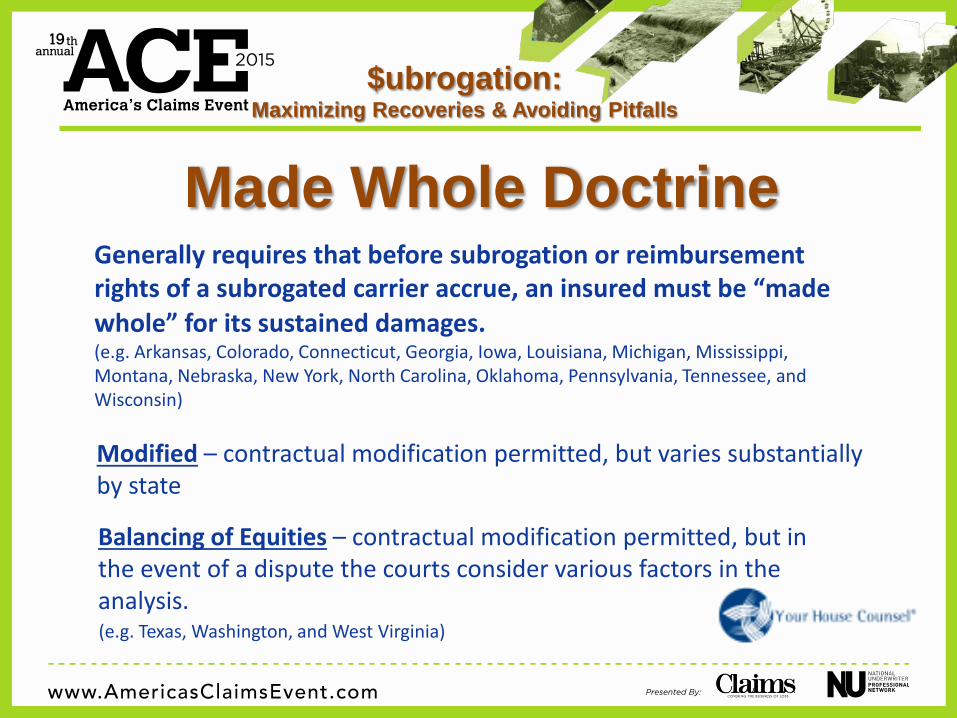

Made Whole Doctrine Generally requires that before subrogation or reimbursement rights of a subrogated carrier accrue, an insured must be “made whole” for its sustained damages. (e.g. Arkansas, Colorado, Connecticut, Georgia, Iowa, Louisiana, Michigan, Mississippi, Montana, Nebraska, New York, North Carolina, Oklahoma, Pennsylvania, Tennessee, and Wisconsin)

Modified – contractual modification permitted, but varies substantially by state

Balancing of Equities – contractual modification permitted, but in the event of a dispute the courts consider various factors in the analysis. (e.g. Texas, Washington, and West Virginia)

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

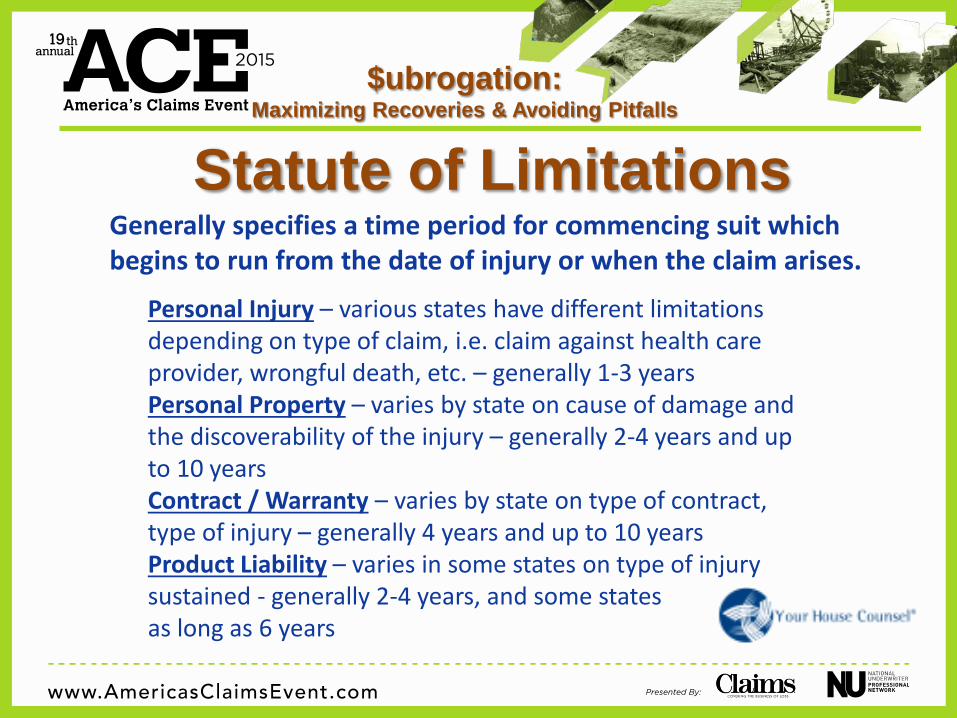

Statute of Limitations Generally specifies a time period for commencing suit which begins to run from the date of injury or when the claim arises. Personal Injury – various states have different limitations

depending on type of claim, i.e. claim against health care provider, wrongful death, etc. – generally 1-3 years Personal Property – varies by state on cause of damage and the discoverability of the injury – generally 2-4 years and up to 10 years Contract / Warranty – varies by state on type of contract, type of injury – generally 4 years and up to 10 years Product Liability – varies in some states on type of injury sustained - generally 2-4 years, and some states as long as 6 years

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

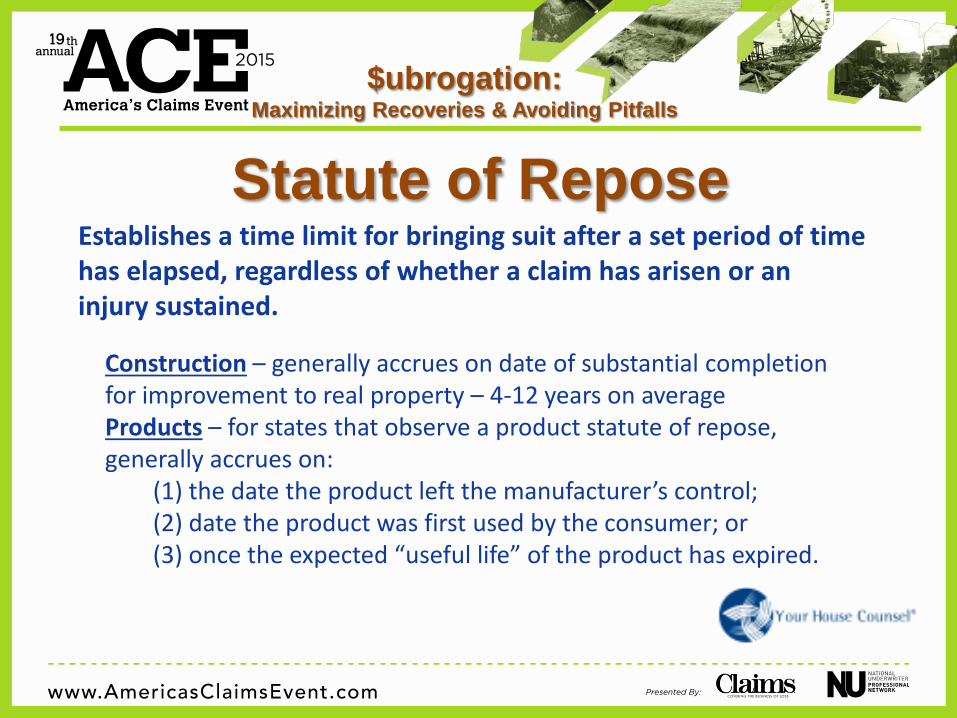

Statute of Repose Establishes a time limit for bringing suit after a set period of time has elapsed, regardless of whether a claim has arisen or an injury sustained.

Construction – generally accrues on date of substantial completion for improvement to real property – 4-12 years on average Products – for states that observe a product statute of repose, generally accrues on: (1) the date the product left the manufacturer’s control; (2) date the product was first used by the consumer; or (3) once the expected “useful life” of the product has expired.

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

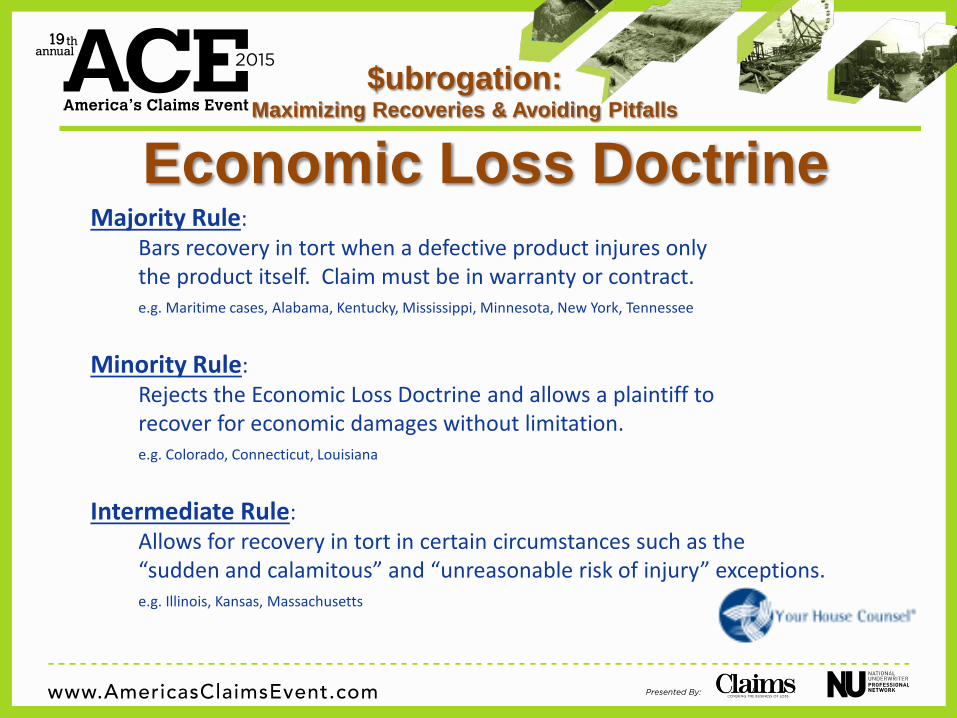

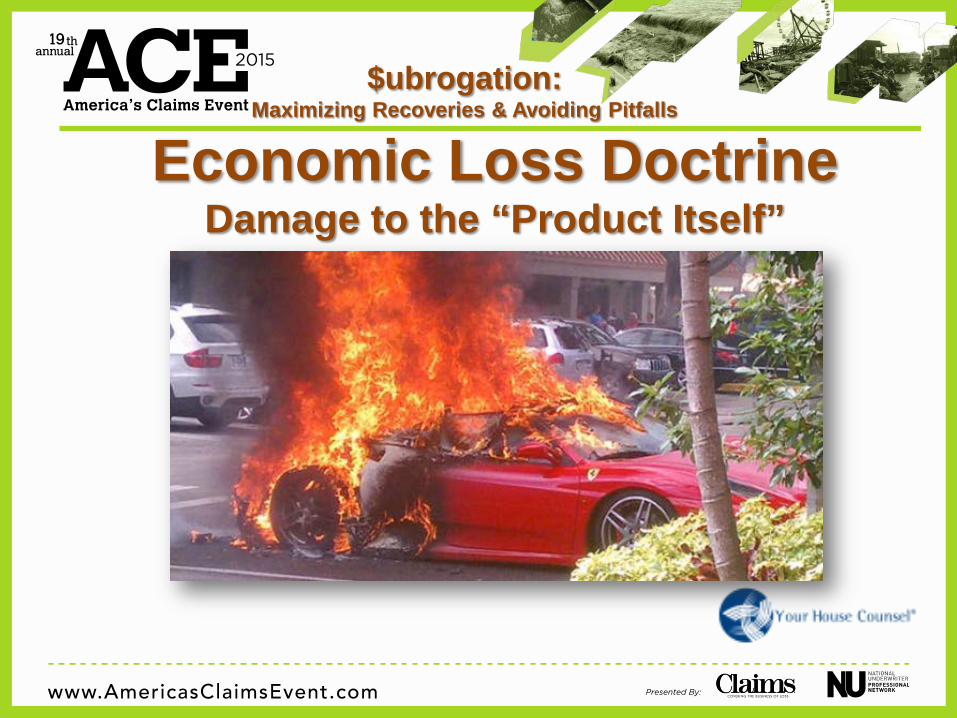

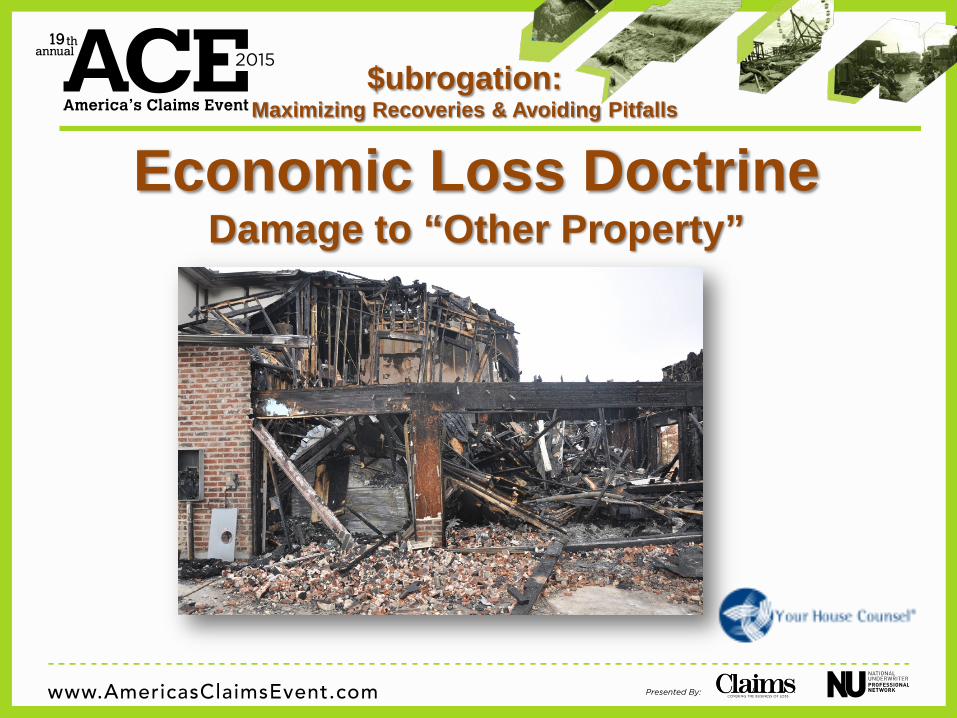

Economic Loss Doctrine Majority Rule: Bars recovery in tort when a defective product injures only the product itself. Claim must be in warranty or contract. e.g. Maritime cases, Alabama, Kentucky, Mississippi, Minnesota, New York, Tennessee

Minority Rule: Rejects the Economic Loss Doctrine and allows a plaintiff to recover for economic damages without limitation. e.g. Colorado, Connecticut, Louisiana

Intermediate Rule: Allows for recovery in tort in certain circumstances such as the “sudden and calamitous” and “unreasonable risk of injury” exceptions. e.g. Illinois, Kansas, Massachusetts

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

Economic Loss Doctrine Damage to the “Product Itself”

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

Economic Loss Doctrine Damage to “Other Property”

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

Spoliation

Spoliation of evidence refers to the loss, destruction, or material alteration of an object or document that is evidence or potential evidence in a legal proceeding by

one who has the responsibility for its preservation.

NFPA 921 – Guide for Fire & Explosion Investigations - 2014 Edition

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

The majority of states address spoliation through the imposition of sanctions or adverse inference instructions to juries. Currently, only 10 states recognize an independent tort General consideration by all states is “fairness”

Spoliation

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

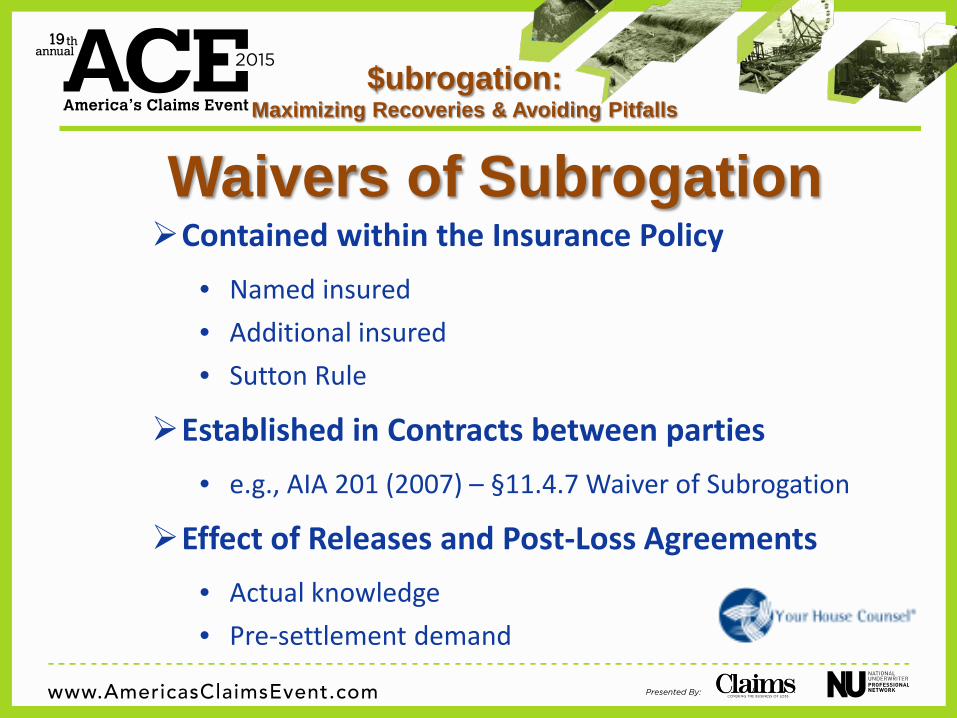

Waivers of Subrogation Contained within the Insurance Policy

• Named insured • Additional insured • Sutton Rule

Established in Contracts between parties • e.g., AIA 201 (2007) – §11.4.7 Waiver of Subrogation

Effect of Releases and Post-Loss Agreements • Actual knowledge • Pre-settlement demand

$ubrogation: Maximizing Recoveries & Avoiding Pitfalls

Pitfalls to Avoid Made Whole Doctrine

Statute of Limitations

Statute of Repose

Economic Loss Doctrine

Spoliation

Waivers of Subrogation

Uniform Preferred Rates and Portfolio Fee Arrangements. Our Member Firms offer Uniform Preferred Rates as well as

Portfolio Fee Arrangements that work to your advantage.

Why Each of Your House Counsel Member Firms Is The One To Turn To

®

Uniform Preferred Rates and Portfolio Fee Arrangements. Our Member Firms offer Uniform Preferred Rates as well as

Portfolio Fee Arrangements that work to your advantage.

We conduct extensive due diligence coupled with a very stringent vetting process.

This assures you that our Members are highly qualified.

Why Each of Your House Counsel Member Firms Is The One To Turn To

®

Uniform Preferred Rates and Portfolio Fee Arrangements. Our Member Firms offer Uniform Preferred Rates as well as

Portfolio Fee Arrangements that work to your advantage.

We conduct extensive due diligence coupled with a very stringent vetting process.

This assures you that our Members are highly qualified.

You’ll be represented by a neighbor, not a stranger. Our local representation means our Members

know the nuances of their jurisdictions.

Why Each of Your House Counsel Member Firms Is The One To Turn To

®

Uniform Preferred Rates and Portfolio Fee Arrangements. Our Member Firms offer Uniform Preferred Rates as well as

Portfolio Fee Arrangements that work to your advantage.

We conduct extensive due diligence coupled with a very stringent vetting process.

This assures you that our Members are highly qualified.

You’ll be represented by a neighbor, not a stranger. Our local representation means our Members

know the nuances of their jurisdictions.

Finding a local law firm with proven experience will take minutes, not days or weeks.

YourHouseCounsel.com makes the search for a qualified firm fast, easy and private.

Why Each of Your House Counsel Member Firms Is The One To Turn To

®

Uniform Preferred Rates and Portfolio Fee Arrangements. Our Member Firms offer Uniform Preferred Rates as well as

Portfolio Fee Arrangements that work to your advantage.

We conduct extensive due diligence coupled with a very stringent vetting process.

This assures you that our Members are highly qualified.

You’ll be represented by a neighbor, not a stranger. Our local representation means our Members

know the nuances of their jurisdictions.

Finding a local law firm with proven experience will take minutes, not days or weeks.

YourHouseCounsel.com makes the search for a qualified firm fast, easy and private.

We’re right where you need us. That’s because we are adding highly qualified Members

in jurisdictions throughout the country.

Why Each of Your House Counsel Member Firms Is The One To Turn To

®

CONCLUSION