Embed Size (px)

DESCRIPTION

SECURITIZATION PSA

Citation preview

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 1/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 1/

424B5 1 a46806.htm

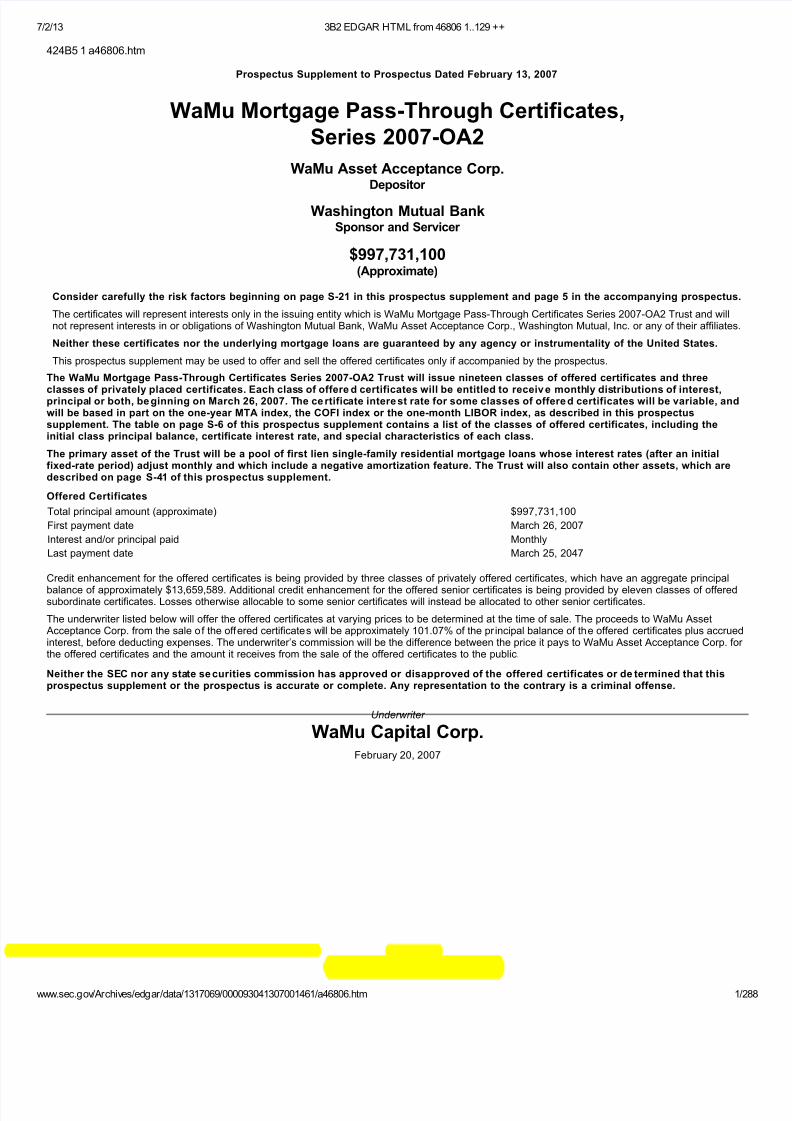

Prospectus Supplement to Prospectus Dated February 13, 2007

WaMu Mortgage Pass-Through Certificates,Series 2007-OA2

WaMu Asset Acceptance Corp.Depositor

Washington Mutual BankSponsor and Servicer

$997,731,100(Approximate)

Consider carefully the risk factors beginning on page S-21 in this prospectus supplement and page 5 in the accompanying prospectus

The certificates will represent interests only in the issuing entity which is WaMu Mortgage Pass-Through Certificates Series 2007-OA2 Trust and willnot represent interests in or obligations of Washington Mutual Bank, WaMu Asset Acceptance Corp., Washington Mutual, Inc. or any of their affiliates.

Neither these certificates nor the underlying mortgage loans are guaranteed by any agency or instrumentality of the United States.

This prospectus supplement may be used to offer and sell the offered certificates only if accompanied by the prospectus.

The WaMu Mortgage Pass-Through Certificates Series 2007-OA2 Trust will issue nineteen classes of offered certificates and three

classes of privately placed certificates. Each class of offere d certificates will be entitled to receiv e monthly distributions of interest,principal or both, be ginning on March 26, 2007. The ce rtificate intere st rate for some classes of offere d certificates will be variable, andwill be based in part on the one-year MTA index, the COFI index or the one-month LIBOR index, as described in this prospectussupplement. The table on page S-6 of this prospectus supplement contains a list of the classes of offered certificates, including theinitial class principal balance, certificate interest rate, and special characteristics of each class.

The primary asset of the Trust will be a pool of first lien single-family residential mortgage loans whose interest rates (after an initialfixed-rate period) adjust monthly and which include a negative amortization feature. The Trust will also contain other assets, which aredescribed on page S-41 of this prospectus supplement.

Offered Certificates

Total principal amount (approximate) $997,731,100

First payment date March 26, 2007

Interest and/or principal paid Monthly

Last payment date March 25, 2047

Credit enhancement for the offered certificates is being provided by three classes of privately offered certificates, which have an aggregate principal

balance of approximately $13,659,589. Additional credit enhancement for the offered senior certificates is being provided by eleven classes of offeredsubordinate certificates. Losses otherwise allocable to some senior certificates will instead be allocated to other senior certificates.

The underwriter listed below will offer the offered certificates at varying prices to be determined at the time of sale. The proceeds to WaMu Asset Acceptance Corp. from the sale of the offered certificates will be approximately 101.07% of the pr incipal balance of the offered certificates plus accruedinterest, before deducting expenses. The underwriter’s commission will be the difference between the price it pays to WaMu Asset Acceptance Corp. forthe offered certificates and the amount it receives from the sale of the offered certificates to the public.

Neither the SEC nor any state se curities commission has approved or disapproved of the offered certificates or de termined that thisprospectus supplement or the prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

Underwriter

WaMu Capital Corp.February 20, 2007

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 2/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 2/

Important Notice About Information Presented in thisProspectus Supplement and the Accompanying Prospectus

We provide information to you about the offered certificates in two separate documents that progressively provide more detail: (a) the accompanyinprospectus, which provides general information, some of which may not apply to your series of certificates, and (b) this prospectus supplement, whichdescribes the specific terms of your series of certificates.

You should be cer tain to re view the information in this prospectus supplement for a description of the specific te rms of your certificates.

We include cross-references in this prospectus supplement and the accompanying prospectus to captions in these materials where you can findfurther related discussions. The following table of contents and the table of contents included in the accompanying prospectus provide the pages onwhich these captions are located.

You can find a listing of the pages where some of the capitalized terms used in this prospectus supplement and the accompanying prospectus are

defined under the caption “Index of Terms” on page S-128 in this prospectus supplement and under the caption “Glossary” beginning on page 138 inthe accompanying prospectus. Capitalized terms used in this prospectus supplement and not otherwise defined in this prospectus supplement have themeanings assigned in the accompanying prospectus.

European Economic Area

In relation to each Member State of the European Economic Area which has implemented the Prospectus Directive (each, a “Relevant Member State”), the underwriter has represented and agreed that with effect from and including the date on which the Prospectus Directive is implemented in thaRelevant Member State (the “Relevant Implementation Date”) it has not made and will not make an offer of certificates to the public in that RelevantMember State prior to the publication of a prospectus in relation to the certificates which has been approved by the competent authority in that RelevantMember State or, where appropriate, approved in another Relevant Member State and notified to the competent authority in that Relevant Member State, all in accordance with the Prospectus Directive, except that it may, with effect from and including the Relevant Implementation Date, make an offeof certificates to the public in that Relevant Member State at any time:

(a)

to legal entities which are authorized or regulated to operate in the financial markets or, if not so authorized or regulated, whose corporatepurpose is solely to invest in securities;

(b)

to any legal entity which has two or more of (1) an average of at least 250 employees during the last financial year; (2) a total balance

sheet of more than €43,000,000 and (3) an annual net turnover of more than €50,000,000, as shown in its last annual or consolidatedaccounts; or

(c)

in any other circumstances which do not require the publication by the issuer of a prospectus pursuant to Article 3 of the ProspectusDirective.

For the purposes of this provision, the expression an “offer of certificates to the public” in relation to any certificates in any Relevant Member Statemeans the communication in any form and by any means of sufficient information on the terms of the offer and the certificates to be offered so as toenable an investor to decide to purchase or subscribe to the certificates, as the same may be varied in that Member State by any measure implementinthe Prospectus Directive in that Member State and the expression “Prospectus Directive” means Directive 2003/71/EC and includes any relevantimplementing measure in each Relevant Member State.

United Kingdom

The underwriter has represented and agreed that:

(a)

it has only communicated or caused to be communicated and will only communicate or cause to be communicated an invitation or inducement to engage in investment activity (within the meaning of Section 21 of the Financial Services and Markets Act) received by it in

connection with the issue or sale of the certificates in circumstances in which Section 21(1) of the Financial Services and Markets Act doesnot apply to the issuer; and

(b)

it has complied and will comply with all applicable provisions of the Financial Services and Markets Act with respect to anything done by it inrelation to the certificates in, from or otherwise involving the United Kingdom.

S-2

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 3/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 3/

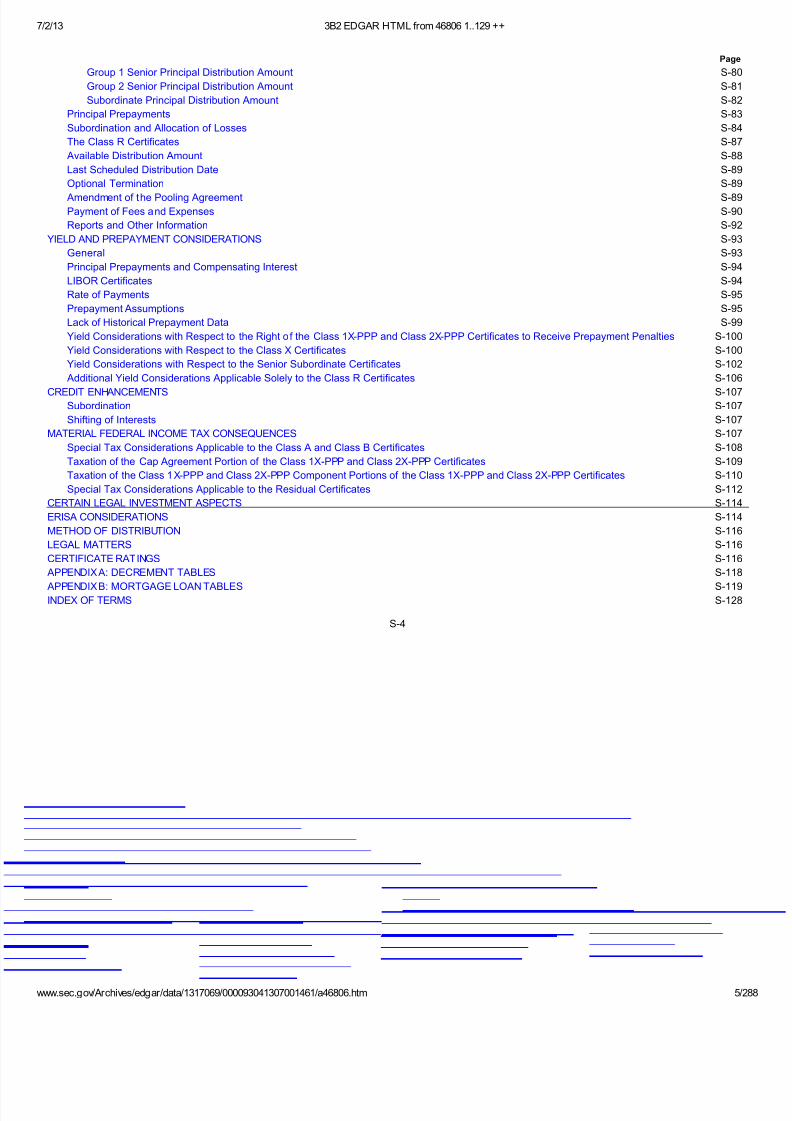

TABLE OF CONTENTS

Page

SUMMARY INFORMATION S-5

Transaction Participants S-5

What You Own S-5

Information About the Mortgage Pool S-5

The Certificates S-6

The Offered Certificates S-6

The Non-Offered Certificates S-12

Relationship Between Loan Groups and the Offered Certificates S-12

Initial Principal Balance of the Certificates S-13

Last Scheduled Distribution Date S-13Distributions on the Certificates S-13

Monthly Distributions S-13

Distributions of Interest S-13

Compensating Interest and Interest Shortfalls S-16

Distributions of Principal S-16

Cross-Collateralization S-17

The Class R Certificates S-17

Credit Enhancements S-17

Allocation of Losses S-18

Optional Termination S-18

Yield Considerations S-18

Book-Entry Registration S-19

Denominations S-19

Legal Investment S-19ERISA Considerations S-19

Federal Income Tax Consequences S-19

Ratings S-20

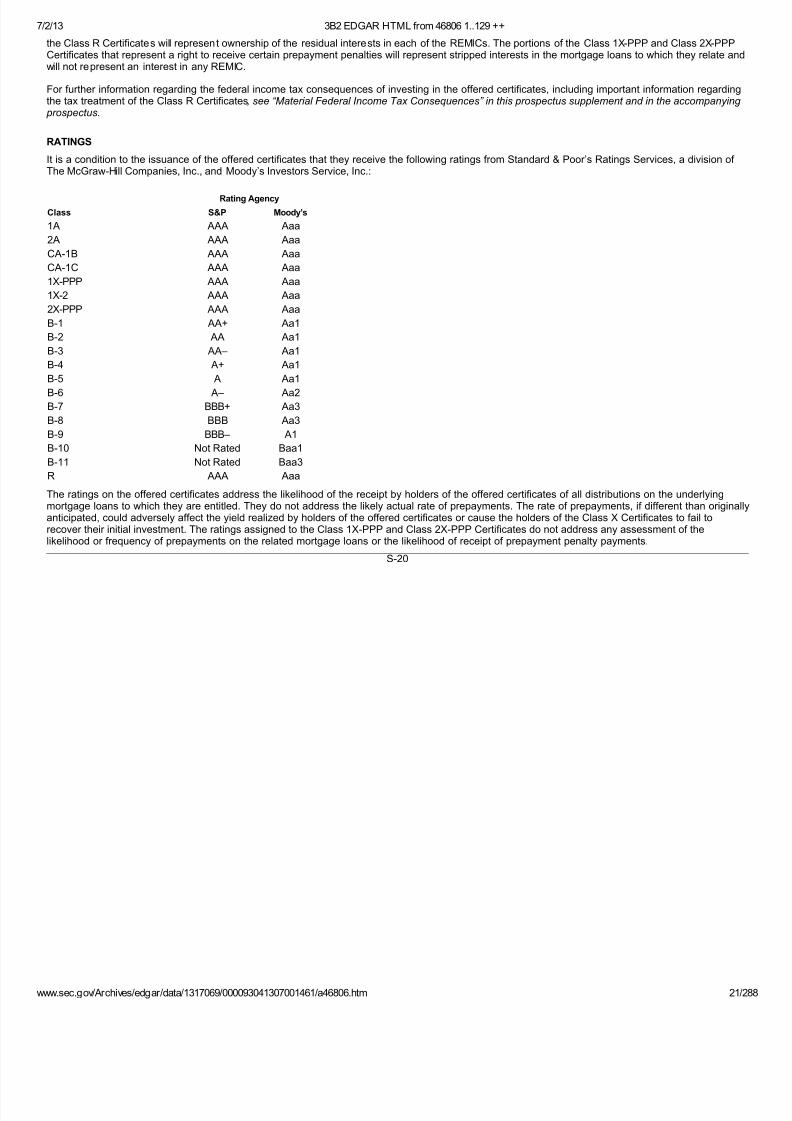

RISK FACTORS S-21

THE SPONSOR S-37

General S-37

The Sponsor’s Origination Channels S-37

STATIC POOL INFORMATION S-38

UNDERWRITING OF THE MORTGAGE LOANS S-38

General S-38

Evaluation of the Borrower’s Credit Standing S-38

Evaluation of the Borrower’s Repayment Ability S-39

Evaluation of the Adequacy of the Collateral S-39

Documentation Programs S-39Exceptions to Program Parameters S-40

Automated Underwriting System S-40

Quality Control Review S-40

THE DEPOSITOR S-41

THE TRUST S-41

General S-41

Assignment of the Mortgage Loans and Other Assets to the Trust S-41

Restrictions on Activities of the Trust S-42

Discretionary Activities With Respect to the Trust S-42

THE TRUSTEES S-43

The Trustee S-43

General S-43

Material Duties of the Trustee S-43

Events of Default Under the Pooling Agreement S-43

The Delaware Trustee S-44

Limitations on the Trustees’ Liability S-44

Resignation and Removal of the Trustees S-44

THE SERVICERS S-44

General S-44

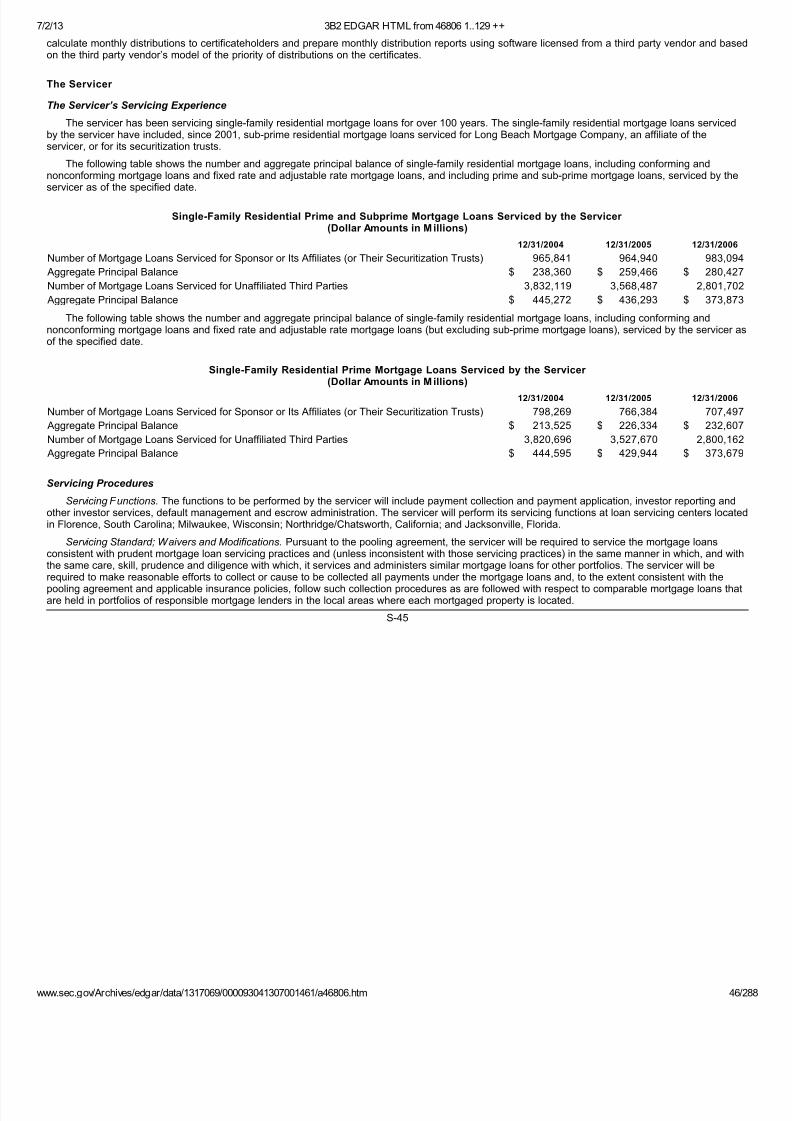

The Servicer S-45

The Servicer’s Servicing Experience S-45

Servicing Procedures S-45

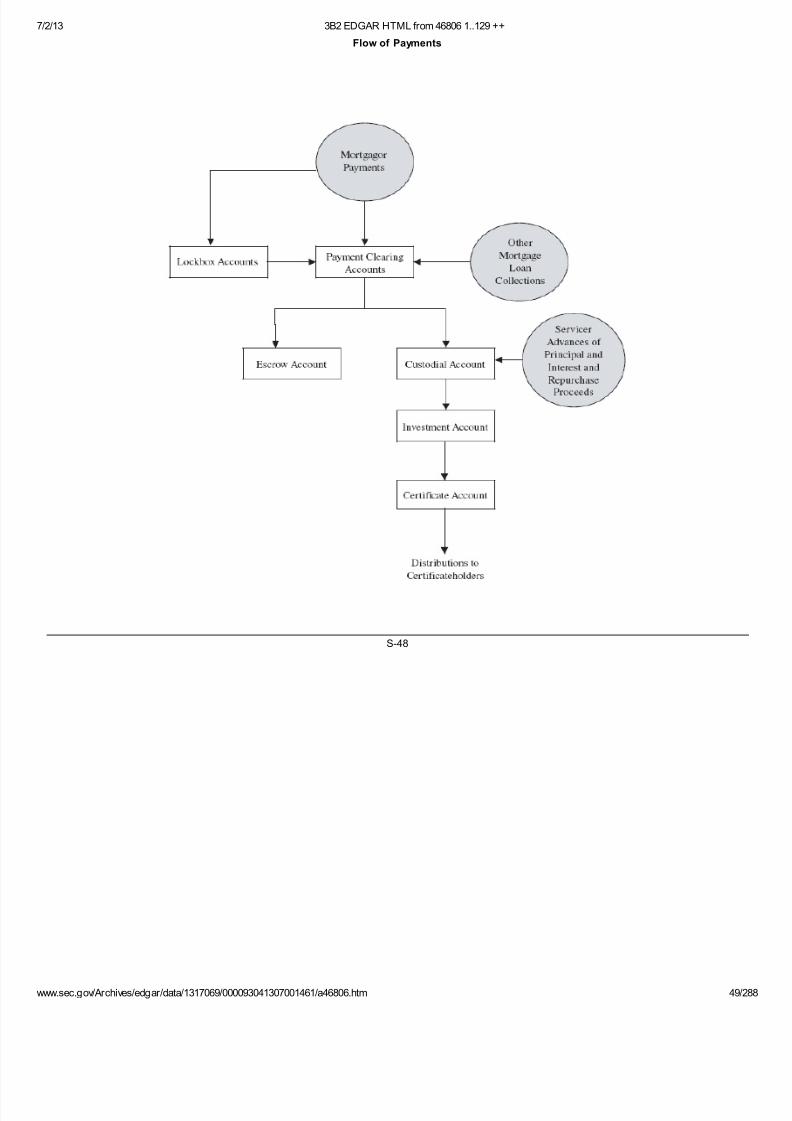

Flow of Payments S-48

The Servicer’s Quality Control Procedures S-50

The Administrative Agent S-51

The Administrative Agent’s Servicing Experience S-51

Services Performed by the Administrative Agent S-51

The Administrative Agent’s Quality Control Procedures S-52

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 4/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 4/

The Custodian S-52

Special Servicing Agreements S-53

AFFILIATIONS AND RELATED TRANSACTIONS S-53

DESCRIPTION OF THE MORTGAGE POOL S-54

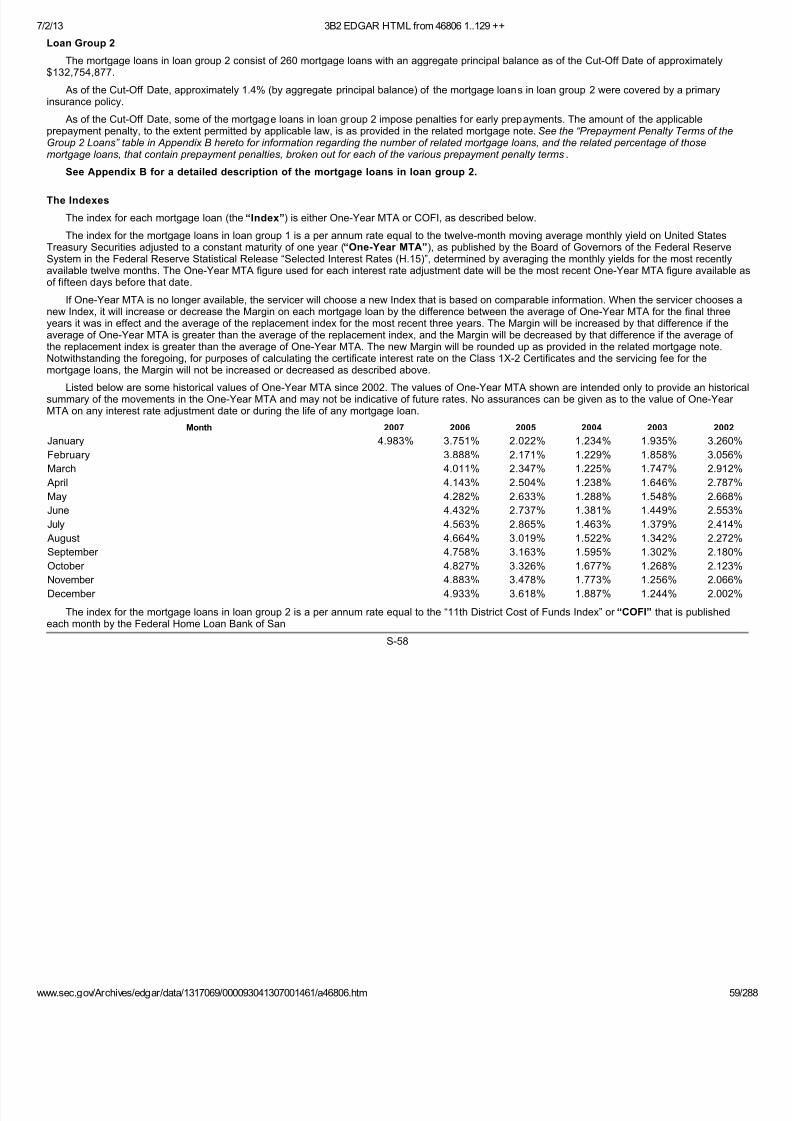

The Indexes S-58

Additional Information S-59

Representations and Warranties Regarding the Mortgage Loans S-60

Criteria for Selection of Mortgage Loans S-61

DESCRIPTION OF THE CERTIFICATES S-62

General S-62

Book-Entry Registration S-64Definitive Certificates S-64

Priority of Distributions S-64

Distributions to the Class 1X-PPP and Class 2X-PPP Certificates S-68

Distributions of Interest S-69

Calculation of LIBOR S-76

Calculation of Indexes for MTA and COFI Certificates S-78

Cross-Collateralization S-78

Distributions of Principal S-79

General S-79

S-3

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 5/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 5/

Page

Group 1 Senior Principal Distribution Amount S-80

Group 2 Senior Principal Distribution Amount S-81

Subordinate Principal Distribution Amount S-82

Principal Prepayments S-83

Subordination and Allocation of Losses S-84

The Class R Certificates S-87

Available Distribution Amount S-88

Last Scheduled Distribution Date S-89

Optional Termination S-89

Amendment of the Pooling Agreement S-89Payment of Fees and Expenses S-90

Reports and Other Information S-92

YIELD AND PREPAYMENT CONSIDERATIONS S-93

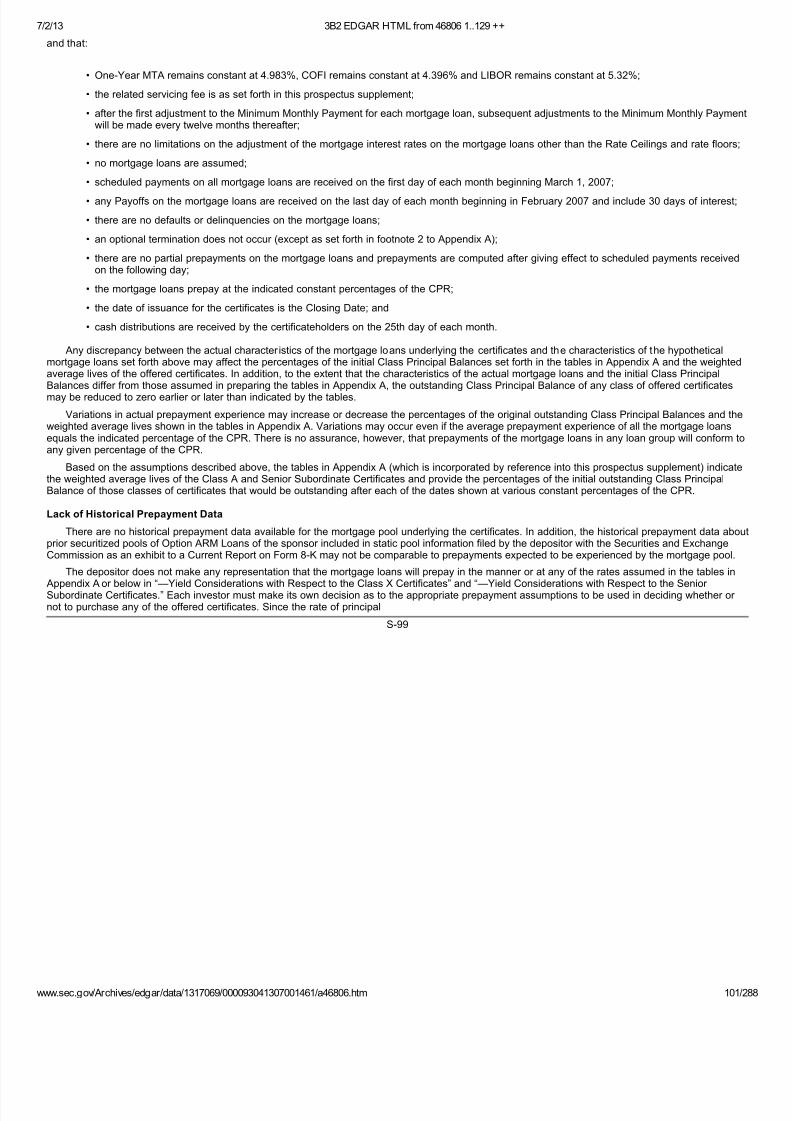

General S-93

Principal Prepayments and Compensating Interest S-94

LIBOR Certificates S-94

Rate of Payments S-95

Prepayment Assumptions S-95

Lack of Historical Prepayment Data S-99

Yield Considerations with Respect to the Right of the Class 1X-PPP and Class 2X-PPP Certificates to Receive Prepayment Penalties S-100

Yield Considerations with Respect to the Class X Certificates S-100

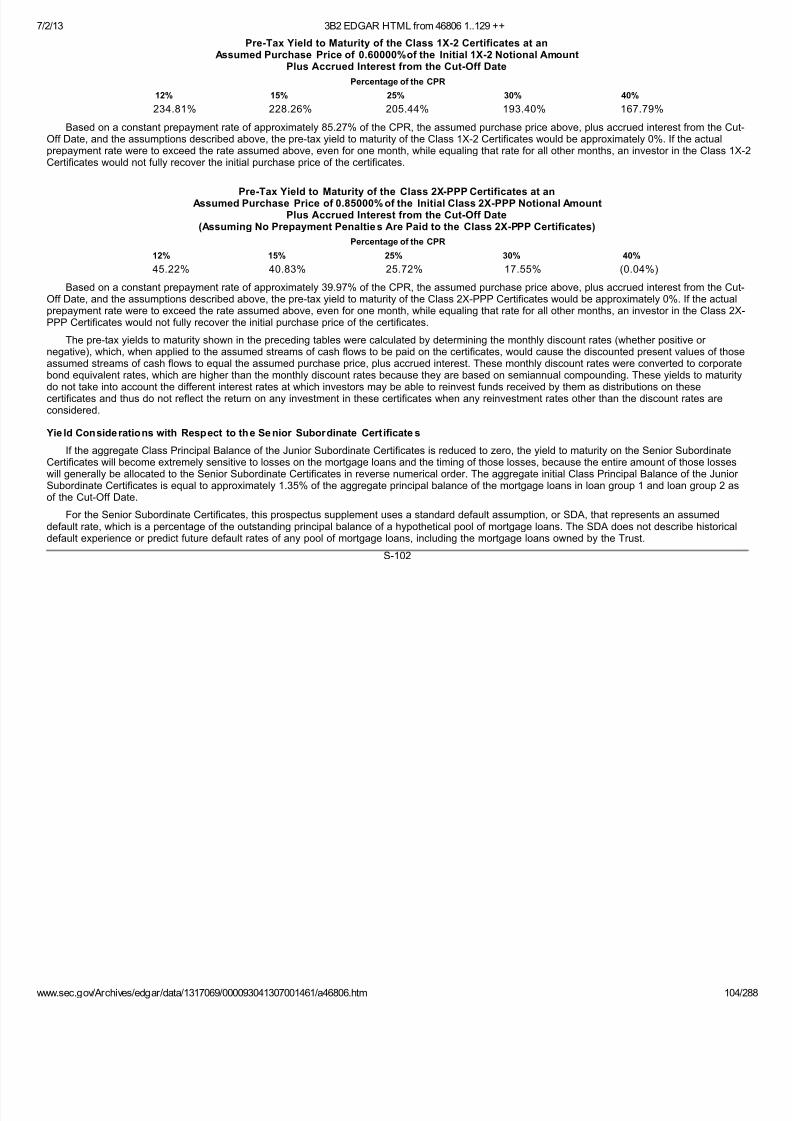

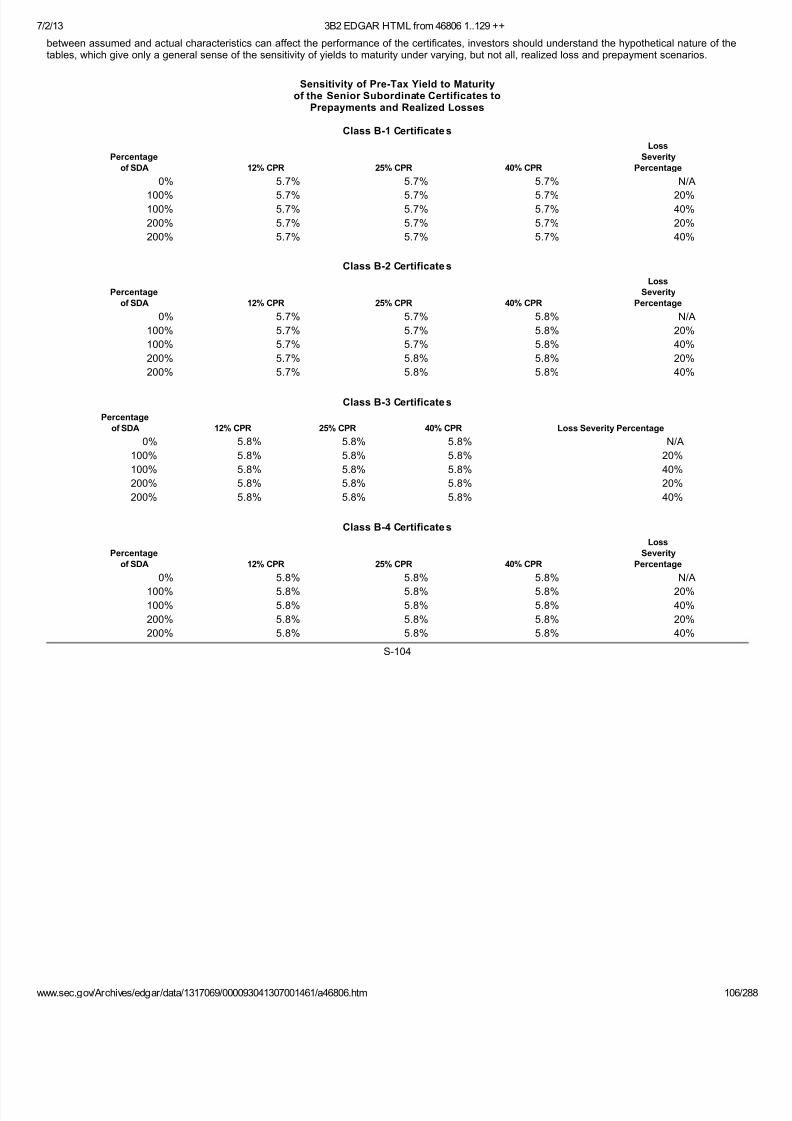

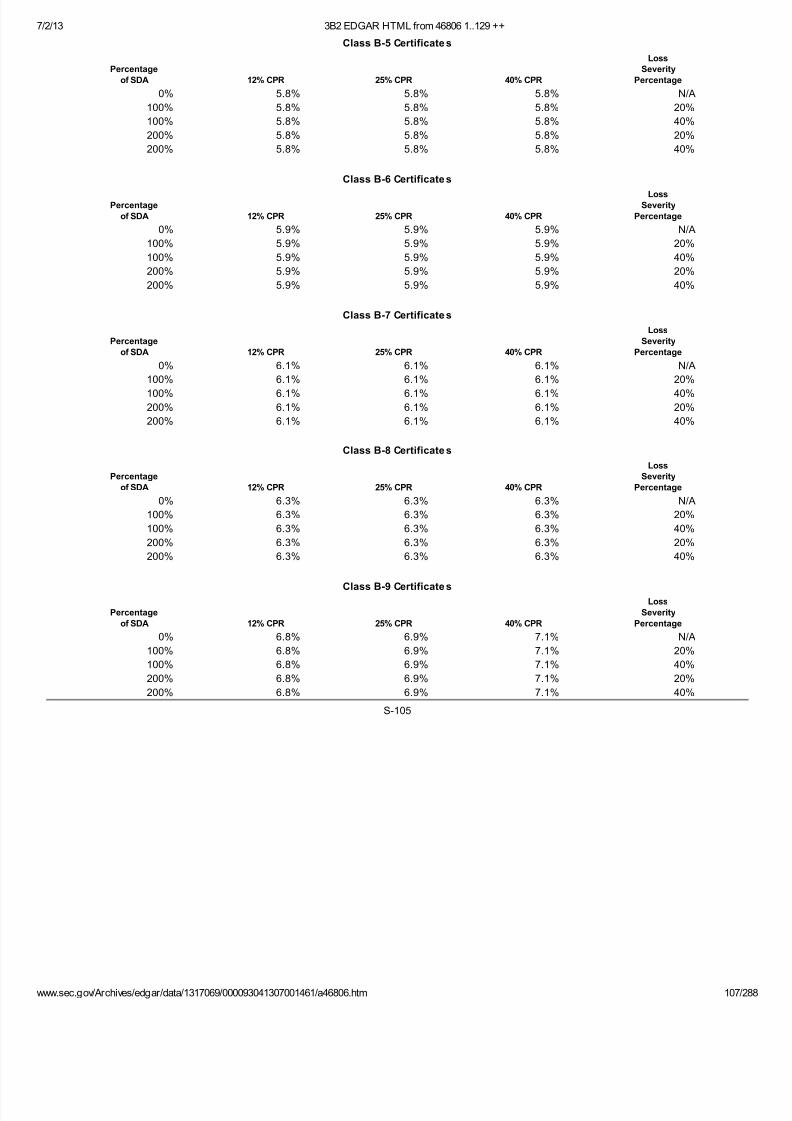

Yield Considerations with Respect to the Senior Subordinate Certificates S-102

Additional Yield Considerations Applicable Solely to the Class R Certificates S-106

CREDIT ENHANCEMENTS S-107Subordination S-107

Shifting of Interests S-107

MATERIAL FEDERAL INCOME TAX CONSEQUENCES S-107

Special Tax Considerations Applicable to the Class A and Class B Certificates S-108

Taxation of the Cap Agreement Portion of the Class 1X-PPP and Class 2X-PPP Certificates S-109

Taxation of the Class 1X-PPP and Class 2X-PPP Component Portions of the Class 1X-PPP and Class 2X-PPP Certificates S-110

Special Tax Considerations Applicable to the Residual Certificates S-112

CERTAIN LEGAL INVESTMENT ASPECTS S-114

ERISA CONSIDERATIONS S-114

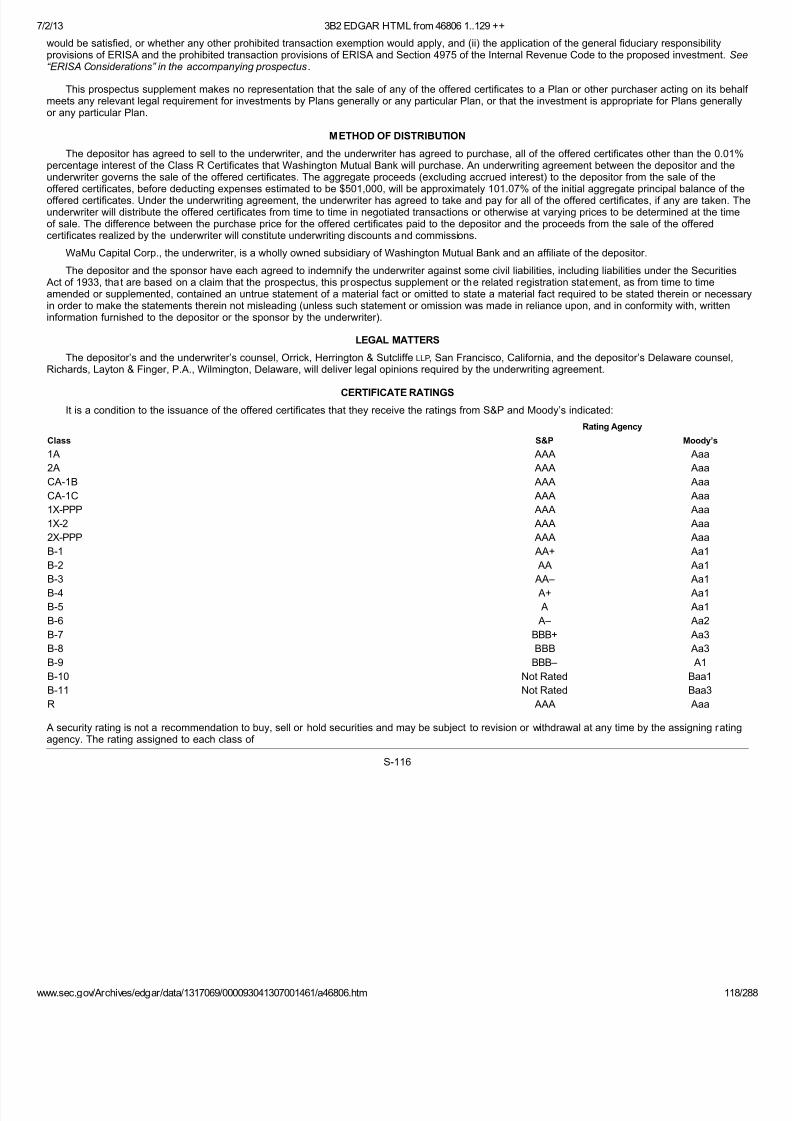

METHOD OF DISTRIBUTION S-116

LEGAL MATTERS S-116

CERTIFICATE RATINGS S-116

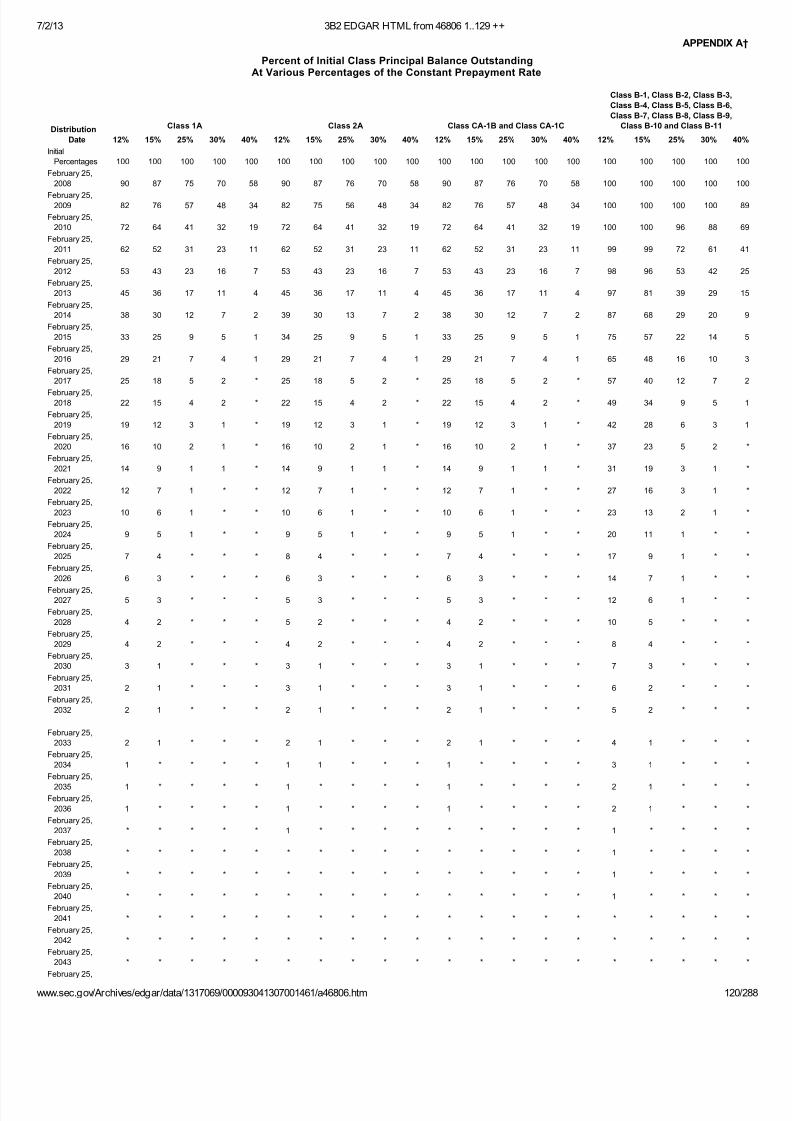

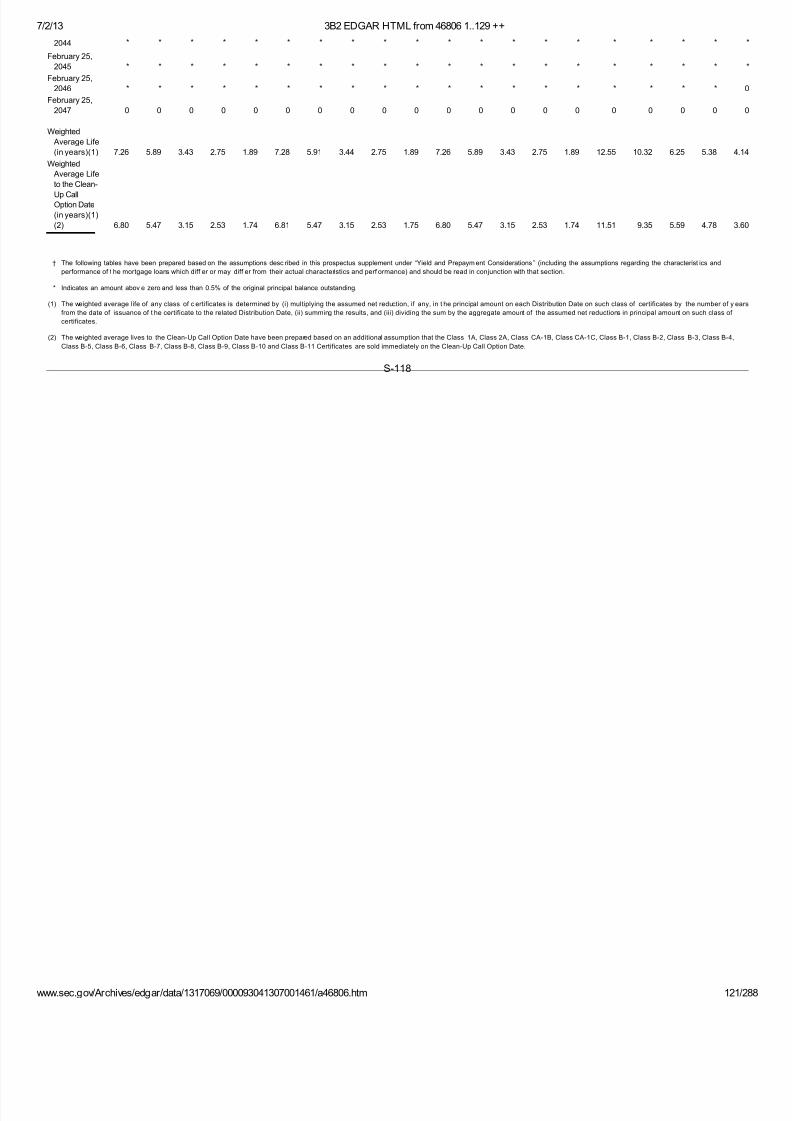

APPENDIX A: DECREMENT TABLES S-118

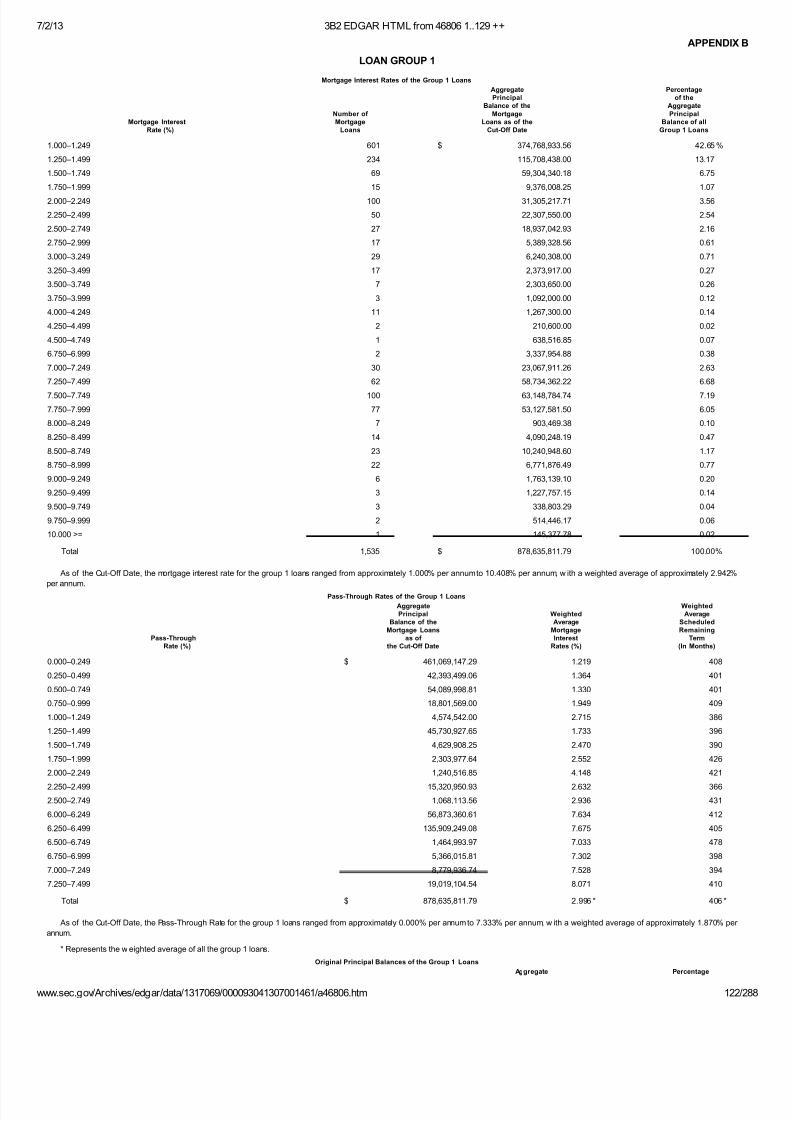

APPENDIX B: MORTGAGE LOAN TABLES S-119INDEX OF TERMS S-128

S-4

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 6/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 6/

SUMMARY INFORMATION

The following summary highlights selected information from this prospectus supplement. It does not contain all of the information that youneed to consider in making your investment decision. To understand the terms of the offered certificates, read carefully this entire prospectusupplement and the accompanying prospectus.

This summary provides an overview of certain calculations, cash flows and other information to aid your understanding. This summary isqualified by the full description of these calculations, cash flows and other information in this prospectus supplement and the accompanying

prospectus.

TRANSACTION PARTICIPANTS

On February 22, 2007, which is the closing date, the mortgage loans that support the certificates will be sold by Washington Mutual Bank, the sponsor othe securitization transaction, to WaMu Asset Acceptance Corp., the depositor. On the closing date, the depositor will sell the mortgage loans and

related assets to the WaMu Mortgage Pass-Through Certificates Series 2007-OA2 Trust. In exchange for the mortgage loans and related assets, theTrust will issue the certificates pursuant to the order of the depositor.

The mortgage loans will be serviced by Washington Mutual Bank, as servicer. Some servicing functions will be performed by Washington MutualMortgage Securities Corp., as administrative agent of the servicer. Some servicing functions will be outsourced to third party vendors.

The trustee of the Trust will be LaSalle Bank National Association, and the Delaware trustee will be Christiana Bank & Trust Company. WashingtonMutual Bank fsb will have possession of and will review the mortgage notes, mortgages and other legal documents related to the mortgage loans ascustodian for the Trust.

WHAT YOU OWN

Your ce rtificates re pre sent inte rests only in the assets of the issuing entity. All payments to you will come only from the amountsreceive d in connection with those assets.

The Trust owns a pool of mortgage loans and other assets, as described under “The Trust” in this prospectus supplement.

There are no outstanding series or classes of securities that are backed by the assets of the issuing entity or otherwise have claims on the assets of theissuing entity, other than the certificates. The depositor does not expect that any securities representing additional interests in or claims on the assets o

the issuing entity will be issued in the future.

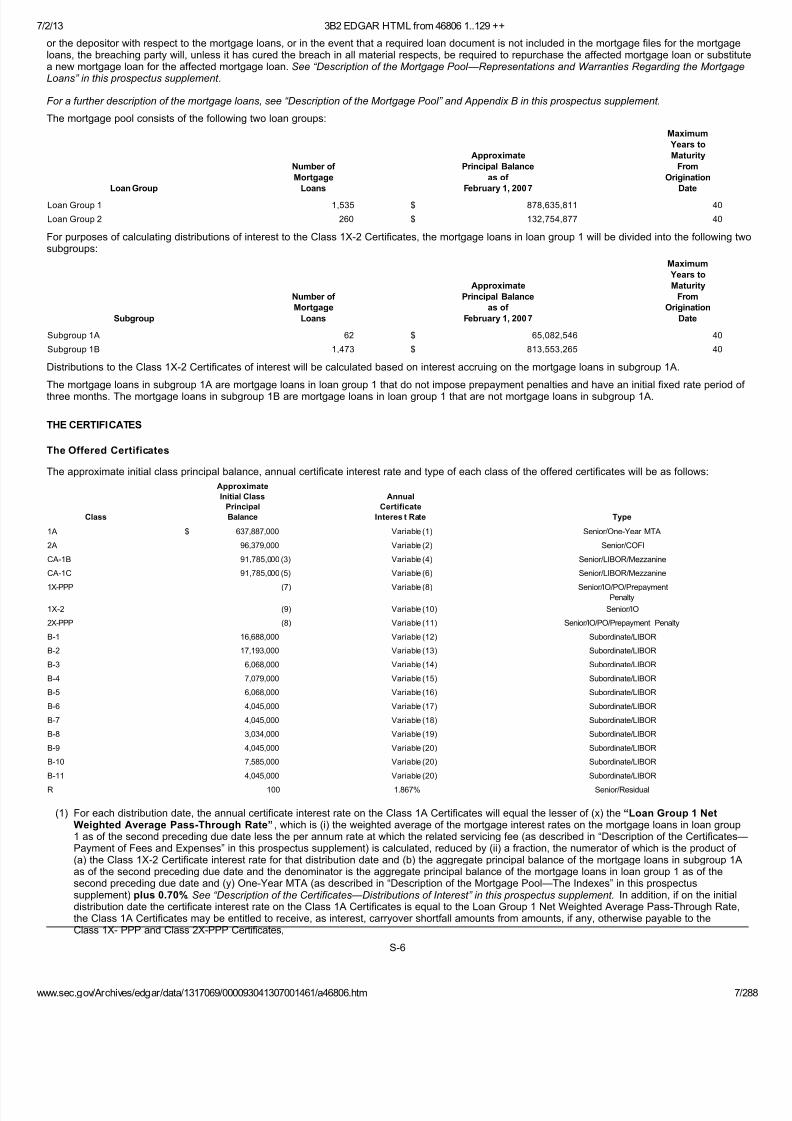

Information About the Mortgage Pool

The mortgage pool consists of 1,795 mortgage loans with an aggregate principal balance as of February 1, 2007 of approximately $1,011,390,689. All the mortgage loans are secured by residential properties (or shares of cooperative apartments) and each has an original term to maturity of not morethan 40 years.

After an initial fixed-rate period of one or three months, the interest rate on each mortgage loan will adjust monthly to equal the sum of an index and amargin. As of February 1, 2007, approximately 67.0% of the mortgage loans (by aggregate principal balance) were still in their initial fixed-rate period.The interest rates on the mortgage loans are subject to overall maximum and minimum interest rate limits.

The index for the mortgage loans in loan group 1 will be One-Year MTA, the 12-month moving average yield on United States Treasury Securitiesadjusted to a constant maturity of one year. The index for the mortgage loans in loan group 2 will be COFI, the 11th District Monthly Weighted AverageCost of Funds Index published by the Federal Home Loan Bank of San Francisco.

While the interest rate on each mortgage loan will adjust monthly (after the initial fixed-rate period), the minimum monthly payment on each mortgageloan generally will adjust only annually. On each annual payment adjustment date, the minimum monthly payment generally will not increase or decrease

by more than 7.5%. As a result, the interest due with respect to a mortgage loan for any given month may, under certain circumstances, exceed themonthly payment for that month. In that case, payment of the excess of interest due over the monthly payment will be deferred and that excess will beadded to the principal balance of that mortgage loan in the form of “negative amortization.” See “Description of the Mortgage Pool” in this prospectussupplement.

In the event of a material breach of the representations and warranties made by the sponsor

S-5

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 7/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 7/

or the depositor with respect to the mortgage loans, or in the event that a required loan document is not included in the mortgage files for the mortgageloans, the breaching party will, unless it has cured the breach in all material respects, be required to repurchase the affected mortgage loan or substitua new mortgage loan for the affected mortgage loan. See “Description of the Mortgage Pool —Representations and Warranties Regarding the MortgagLoans” in this prospectus supplement .

For a further description of the mortgage loans, see “Description of the Mortgage Pool” and Appendix B in this prospectus supplement.

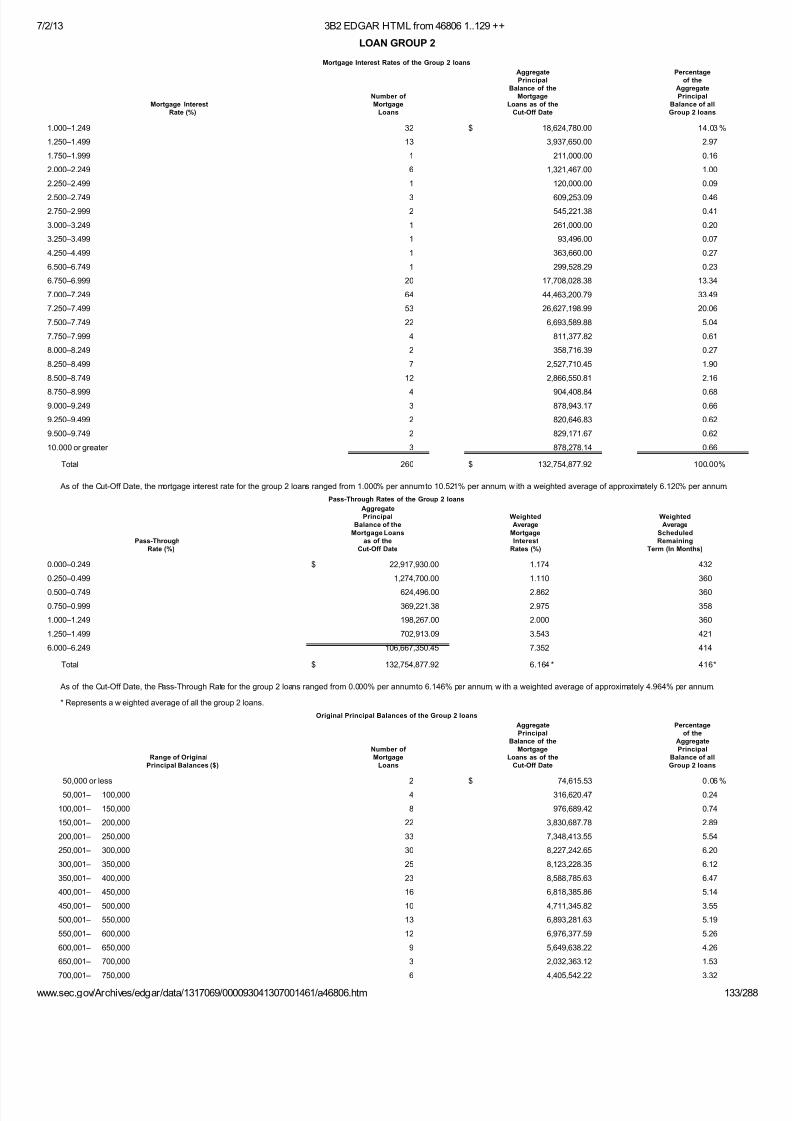

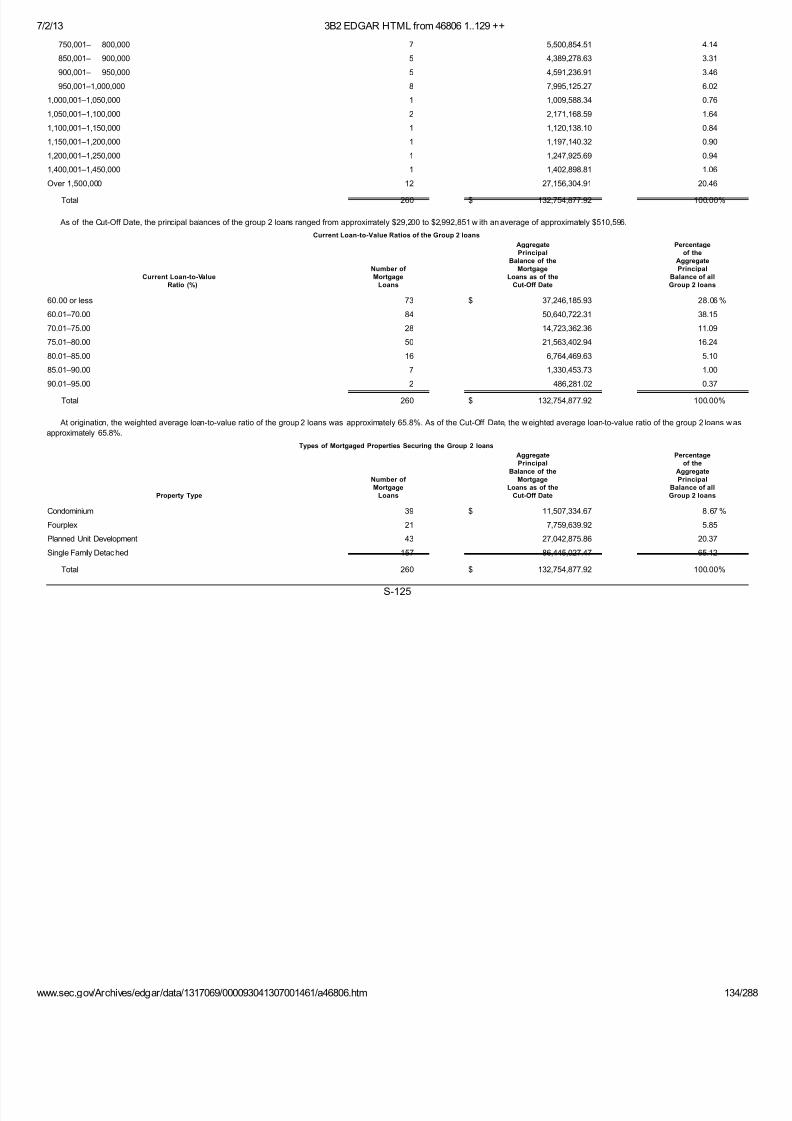

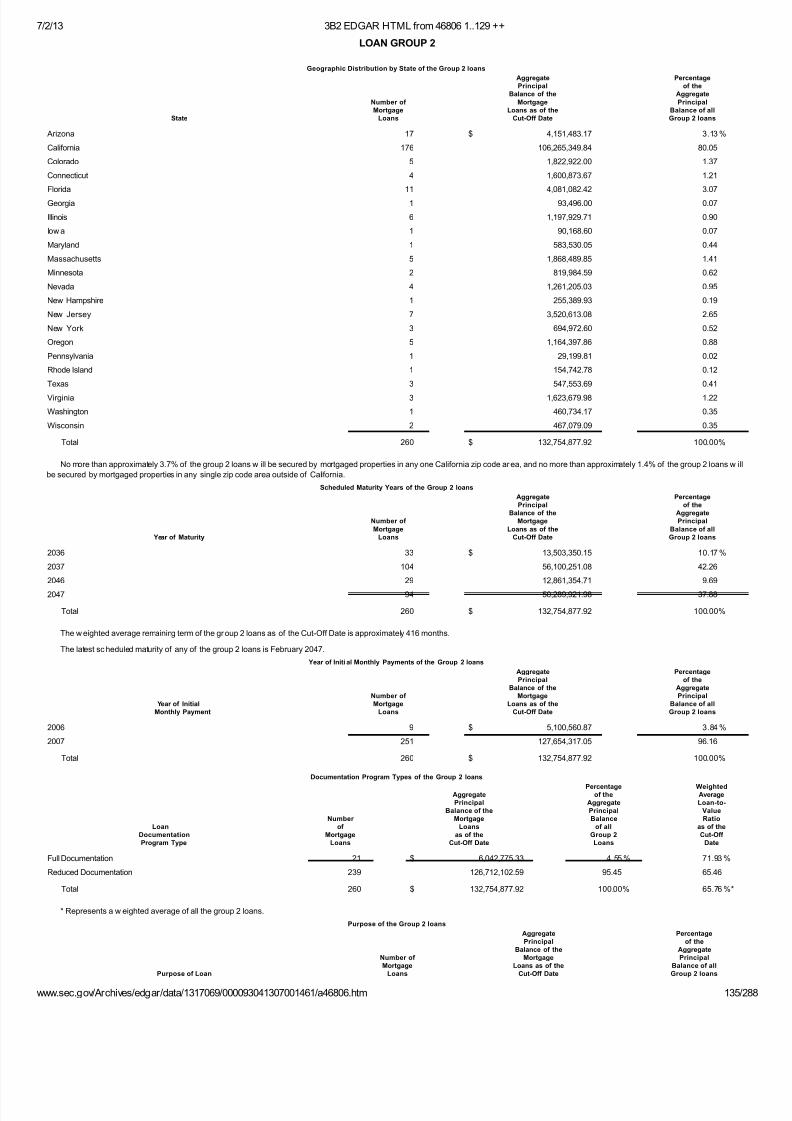

The mortgage pool consists of the following two loan groups:

Loan Group

Number of

MortgageLoans

Approximate

Principal Balance

as of February 1, 2007

Maximum

Years to

Maturity

From

OriginationDate

Loan Group 1 1,535 $

878,635,811 40 Loan Group 2 260 $

132,754,877 40

For purposes of calculating distributions of interest to the Class 1X-2 Certificates, the mortgage loans in loan group 1 will be divided into the following twsubgroups:

Subgroup

Number of Mortgage

Loans

Approximate

Principal Balanceas of

February 1, 2007

Maximum

Years to

Maturity

FromOrigination

Date

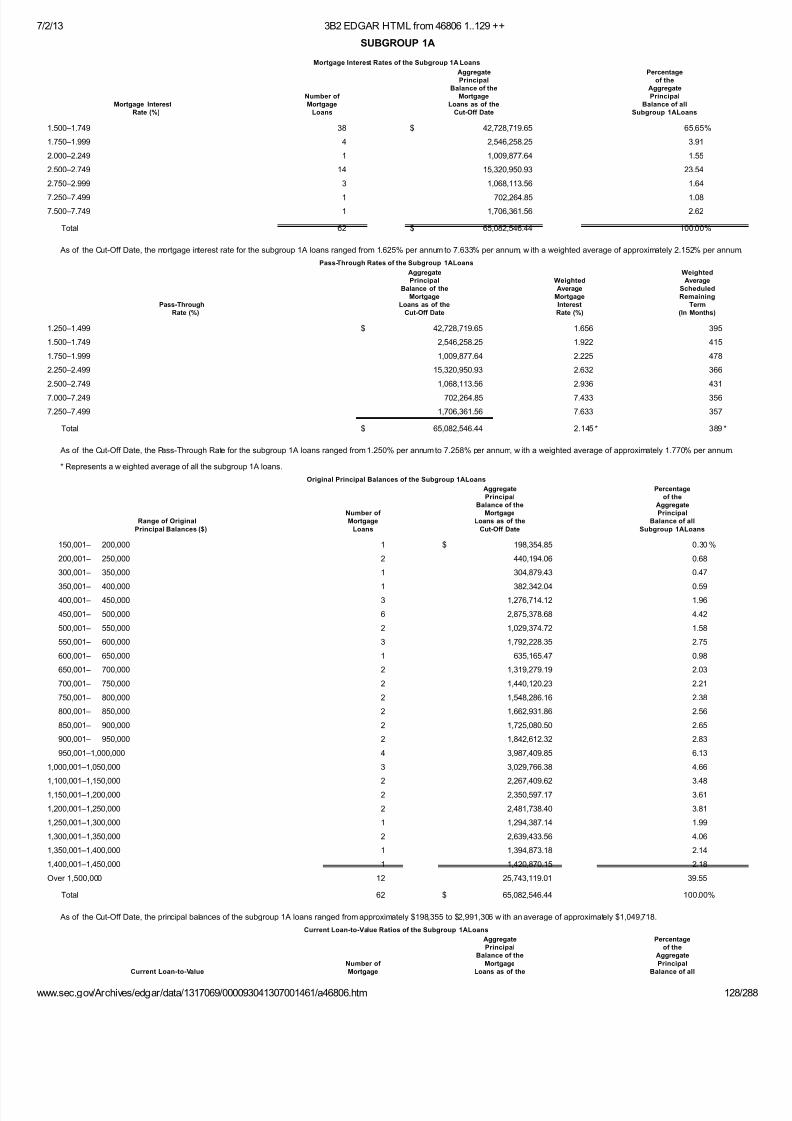

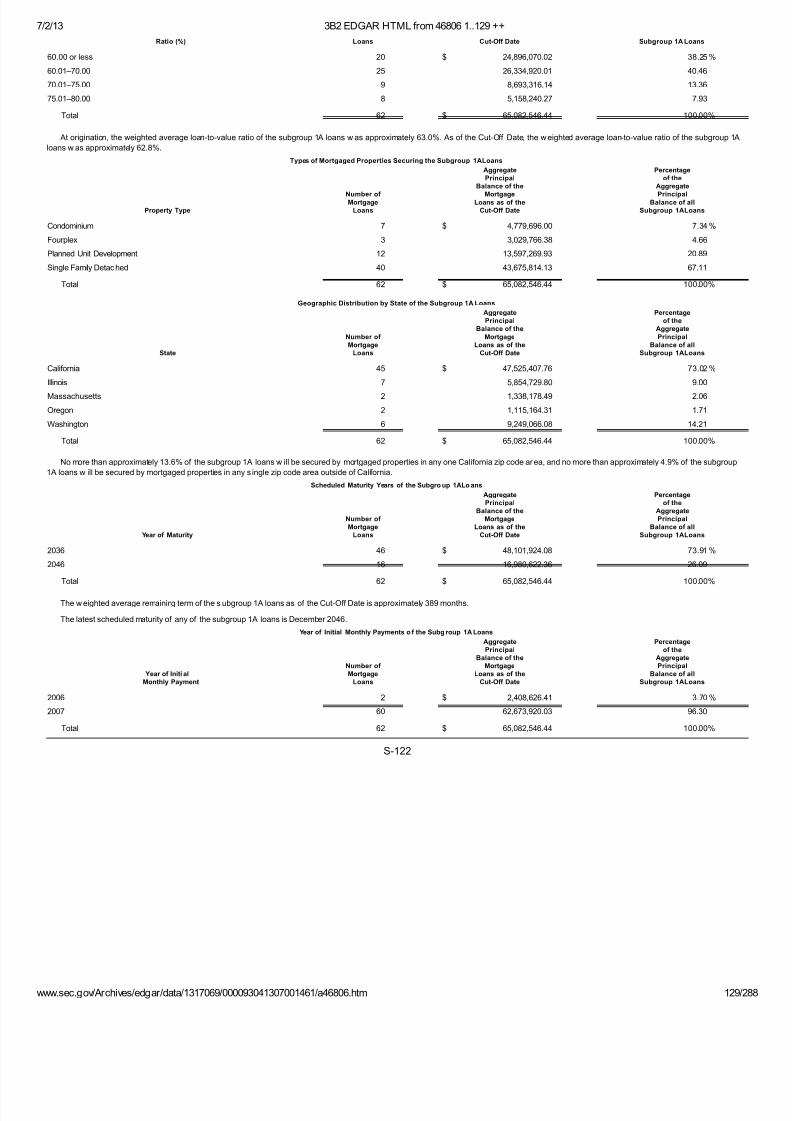

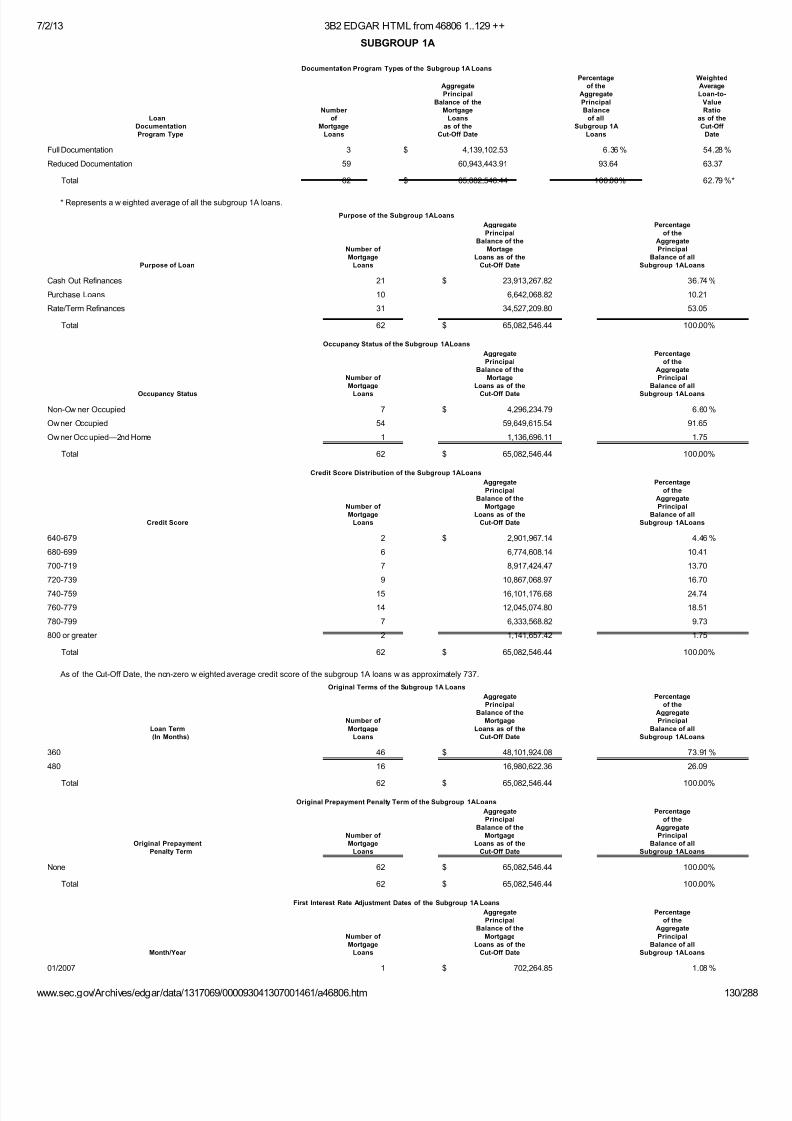

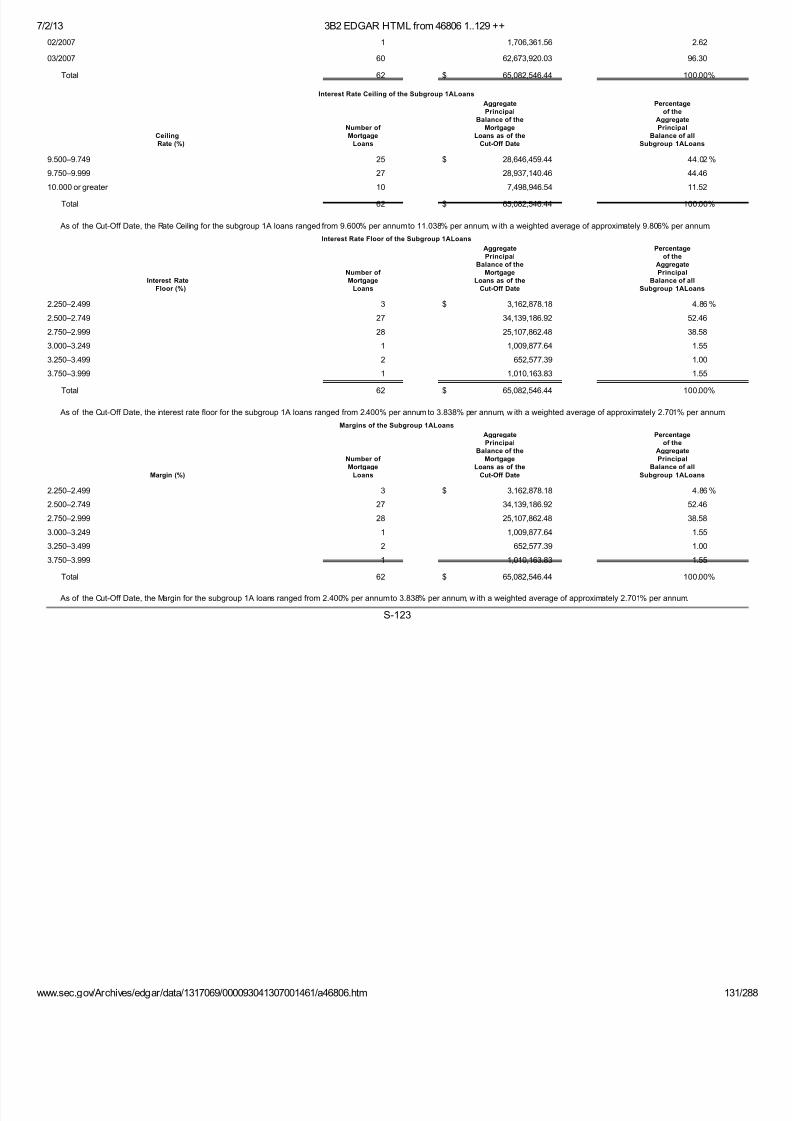

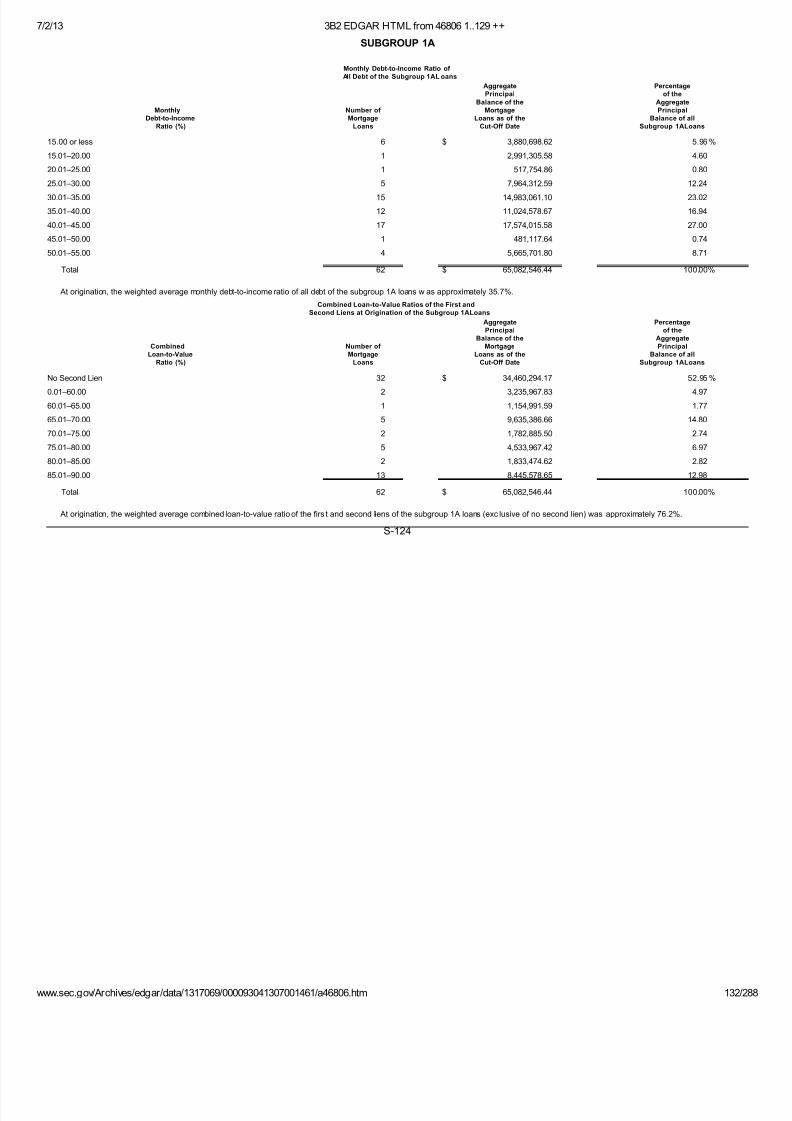

Subgroup 1A 62 $

65,082,546 40

Subgroup 1B 1,473 $

813,553,265 40

Distributions to the Class 1X-2 Certificates of interest will be calculated based on interest accruing on the mortgage loans in subgroup 1A.

The mortgage loans in subgroup 1A are mortgage loans in loan group 1 that do not impose prepayment penalties and have an initial fixed rate period ofthree months. The mortgage loans in subgroup 1B are mortgage loans in loan group 1 that are not mortgage loans in subgroup 1A.

THE CERTIFICATES

The Offered Certificates

The approximate initial class principal balance, annual certificate interest rate and type of each class of the offered certificates will be as follows:

Class

Approximate

Initial Class

Principal

Balance

Annual

Certificate

Interes t Rate Type

1A $

637,887,000 Variable (1)

Senior/One-Year MTA

2A 96,379,000 Variable (2)

Senior/COFI

CA-1B 91,785,000 (3)

Variable (4)

Senior/LIBOR/Mezzanine

CA-1C 91,785,000 (5)

Variable (6)

Senior/LIBOR/Mezzanine

1X-PPP (7)

Variable (8)

Senior/IO/PO/PrepaymentPenalty

1X-2 (9)

Variable (10)

Senior/IO

2X-PPP (8)

Variable (11)

Senior/IO/PO/Prepayment Penalty

B-1 16,688,000 Variable (12)

Subordinate/LIBOR

B-2 17,193,000 Variable (13)

Subordinate/LIBOR

B-3 6,068,000 Variable (14)

Subordinate/LIBOR

B-4 7,079,000 Variable (15)

Subordinate/LIBOR

B-5 6,068,000 Variable (16)

Subordinate/LIBOR

B-6 4,045,000 Variable (17)

Subordinate/LIBOR

B-7 4,045,000 Variable (18)

Subordinate/LIBOR

B-8 3,034,000 Variable (19)

Subordinate/LIBOR

B-9 4,045,000 Variable (20)

Subordinate/LIBOR

B-10 7,585,000 Variable (20)

Subordinate/LIBOR

B-11 4,045,000 Variable (20)

Subordinate/LIBOR

R 100 1.867% Senior/Residual

(1)

For each distribution date, the annual certificate interest rate on the Class 1A Certificates will equal the lesser of (x) the “Loan Group 1 NetWeighted Average Pass-Through Rate”, which is (i) the weighted average of the mortgage interest rates on the mortgage loans in loan group1 as of the second preceding due date less the per annum rate at which the related servicing fee (as described in “Description of the Certificates—Payment of Fees and Expenses” in this prospectus supplement) is calculated, reduced by (ii) a fraction, the numerator of which is the product of (a) the Class 1X-2 Certificate interest rate for that distribution date and (b) the aggregate principal balance of the mortgage loans in subgroup 1Aas of the second preceding due date and the denominator is the aggregate principal balance of the mortgage loans in loan group 1 as of thesecond preceding due date and (y) One-Year MTA (as described in “Description of the Mortgage Pool—The Indexes” in this prospectussupplement) plus 0.70%. See “Description of the Certificates—Distributions of Interest” in this prospectus supplement. In addition, if on the initialdistribution date the certificate interest rate on the Class 1A Certificates is equal to the Loan Group 1 Net Weighted Average Pass-Through Rate,the Class 1A Certificates may be entitled to receive, as interest, carryover shortfall amounts from amounts, if any, otherwise payable to theClass 1X- PPP and Class 2X-PPP Certificates,

S-6

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 8/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 8/

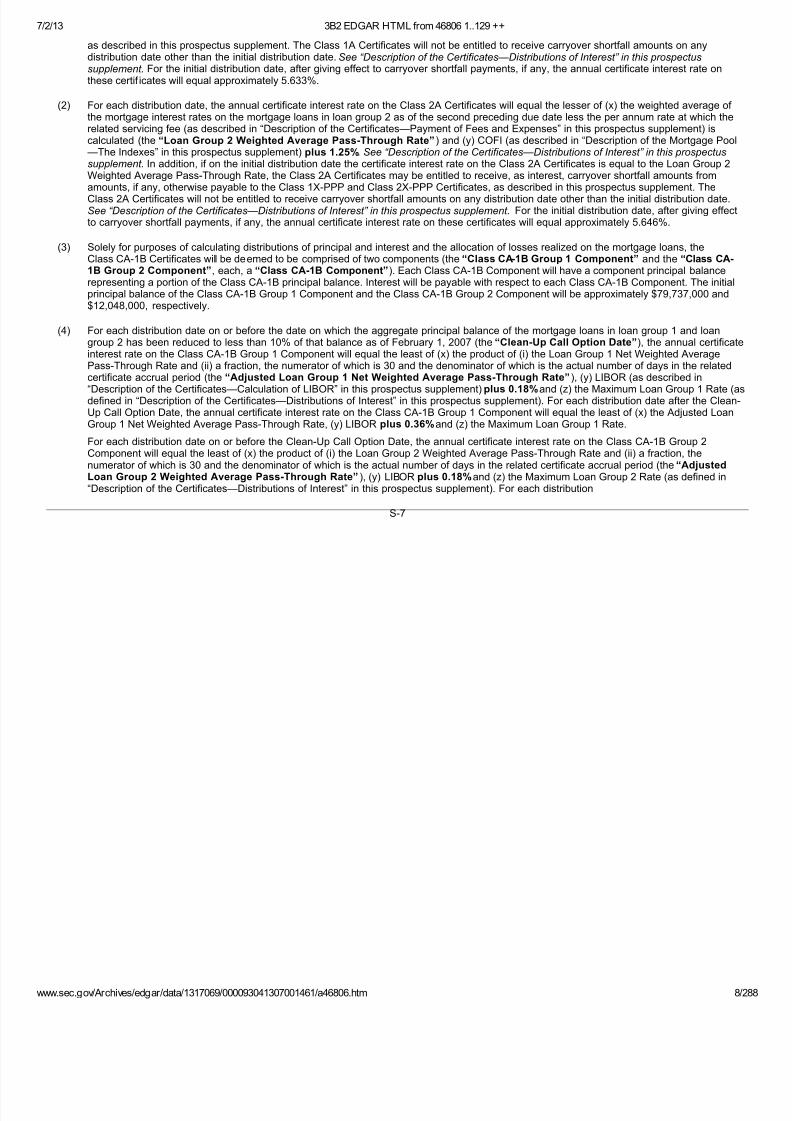

as described in this prospectus supplement. The Class 1A Certificates will not be entitled to receive carryover shortfall amounts on anydistribution date other than the initial distribution date. See “Description of the Certificates—Distributions of Interest” in this prospectussupplement. For the initial distribution date, after giving effect to carryover shortfall payments, if any, the annual certificate interest rate onthese certif icates will equal approximately 5.633%.

(2)

For each distribution date, the annual certificate interest rate on the Class 2A Certificates will equal the lesser of (x) the weighted average of the mortgage interest rates on the mortgage loans in loan group 2 as of the second preceding due date less the per annum rate at which therelated servicing fee (as described in “Description of the Certificates—Payment of Fees and Expenses” in this prospectus supplement) iscalculated (the “Loan Group 2 Weighted Average Pass-Through Rate”) and (y) COFI (as described in “Description of the Mortgage Pool—The Indexes” in this prospectus supplement) plus 1.25%. See “Description of the Certificates—Distributions of Interest” in this prospectussupplement. In addition, if on the initial distribution date the certificate interest rate on the Class 2A Certificates is equal to the Loan Group 2Weighted Average Pass-Through Rate, the Class 2A Certificates may be entitled to receive, as interest, carryover shortfall amounts fromamounts, if any, otherwise payable to the Class 1X-PPP and Class 2X-PPP Certificates, as described in this prospectus supplement. The

Class 2A Certificates will not be entitled to receive carryover shortfall amounts on any distribution date other than the initial distribution date.See “Description of the Certificates—Distributions of Interest” in this prospectus supplement. For the initial distribution date, after giving effectto carryover shortfall payments, if any, the annual certificate interest rate on these certificates will equal approximately 5.646%.

(3)

Solely for purposes of calculating distributions of principal and interest and the allocation of losses realized on the mortgage loans, theClass CA-1B Certificates will be deemed to be comprised of two components (the “Class CA-1B Group 1 Component” and the “Class CA-1B Group 2 Component”, each, a “Class CA-1B Component”). Each Class CA-1B Component will have a component principal balancerepresenting a portion of the Class CA-1B principal balance. Interest will be payable with respect to each Class CA-1B Component. The initialprincipal balance of the Class CA-1B Group 1 Component and the Class CA-1B Group 2 Component will be approximately $79,737,000 and$12,048,000, respectively.

(4)

For each distribution date on or before the date on which the aggregate principal balance of the mortgage loans in loan group 1 and loangroup 2 has been reduced to less than 10% of that balance as of February 1, 2007 (the “Clean-Up Call Option Date”), the annual certificateinterest rate on the Class CA-1B Group 1 Component will equal the least of (x) the product of (i) the Loan Group 1 Net Weighted AveragePass-Through Rate and (ii) a fraction, the numerator of which is 30 and the denominator of which is the actual number of days in the relatedcertificate accrual period (the “Adjusted Loan Group 1 Net Weighted Average Pass-Through Rate”), (y) LIBOR (as described in

“Description of the Certificates—Calculation of LIBOR” in this prospectus supplement) plus 0.18%and (z) the Maximum Loan Group 1 Rate (adefined in “Description of the Certificates—Distributions of Interest” in this prospectus supplement). For each distribution date after the Clean-Up Call Option Date, the annual certificate interest rate on the Class CA-1B Group 1 Component will equal the least of (x) the Adjusted LoanGroup 1 Net Weighted Average Pass-Through Rate, (y) LIBOR plus 0.36%and (z) the Maximum Loan Group 1 Rate.

For each distribution date on or before the Clean-Up Call Option Date, the annual certificate interest rate on the Class CA-1B Group 2Component will equal the least of (x) the product of (i) the Loan Group 2 Weighted Average Pass-Through Rate and (ii) a fraction, thenumerator of which is 30 and the denominator of which is the actual number of days in the related certificate accrual period (the “AdjustedLoan Group 2 Weighted Average Pass-Through Rate”), (y) LIBOR plus 0.18%and (z) the Maximum Loan Group 2 Rate (as defined in“Description of the Certificates—Distributions of Interest” in this prospectus supplement). For each distribution

S-7

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 9/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 9/

date after the Clean-Up Call Option Date, the annual certificate interest rate on the Class CA-1B Group 2 Component will equal the least of (x)the Adjusted Loan Group 2 Weighted Average Pass-Through Rate, (y) LIBOR plus 0.36%and (z) the Maximum Loan Group 2 Rate.

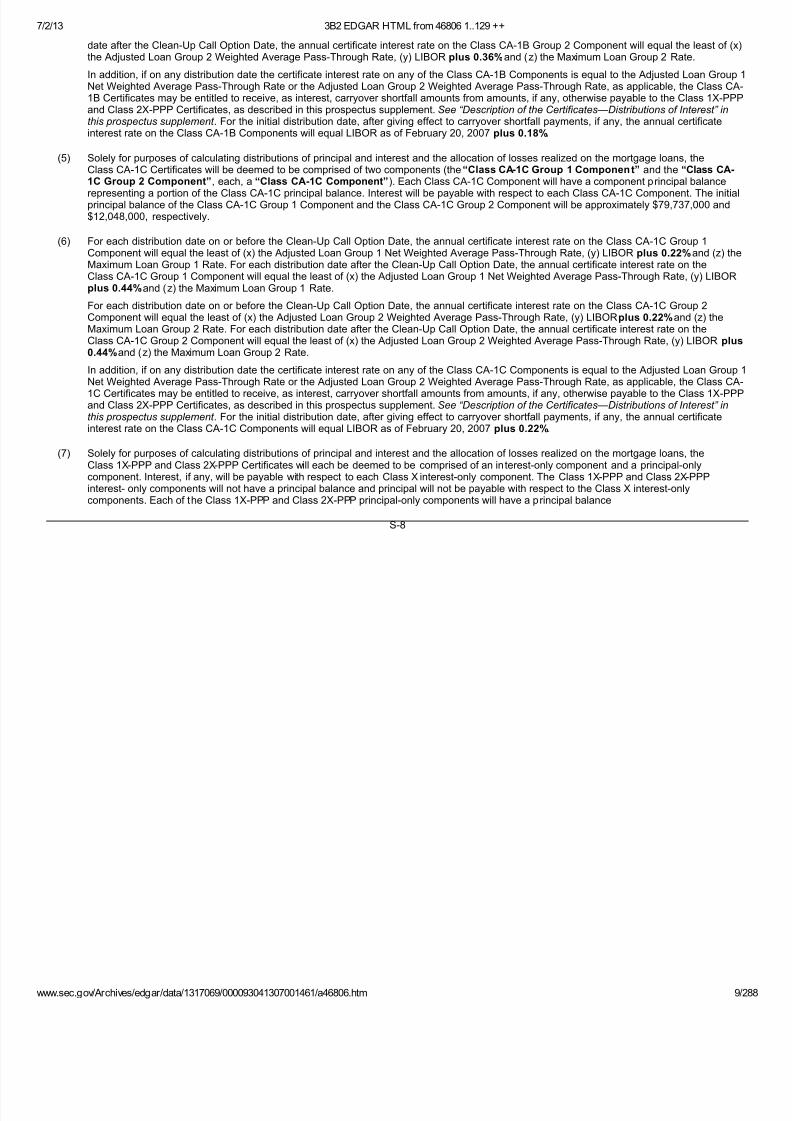

In addition, if on any distribution date the certificate interest rate on any of the Class CA-1B Components is equal to the Adjusted Loan Group 1Net Weighted Average Pass-Through Rate or the Adjusted Loan Group 2 Weighted Average Pass-Through Rate, as applicable, the Class CA-1B Certificates may be entitled to receive, as interest, carryover shortfall amounts from amounts, if any, otherwise payable to the Class 1X-PPPand Class 2X-PPP Certificates, as described in this prospectus supplement. See “Description of the Certificates—Distributions of Interest” inthis prospectus supplement . For the initial distribution date, after giving effect to carryover shortfall payments, if any, the annual certificateinterest rate on the Class CA-1B Components will equal LIBOR as of February 20, 2007 plus 0.18%.

(5)

Solely for purposes of calculating distributions of principal and interest and the allocation of losses realized on the mortgage loans, theClass CA-1C Certificates will be deemed to be comprised of two components (the “Class CA-1C Group 1 Component” and the “Class CA-1C Group 2 Component”, each, a “Class CA-1C Component”). Each Class CA-1C Component will have a component principal balance

representing a portion of the Class CA-1C principal balance. Interest will be payable with respect to each Class CA-1C Component. The initialprincipal balance of the Class CA-1C Group 1 Component and the Class CA-1C Group 2 Component will be approximately $79,737,000 and$12,048,000, respectively.

(6)

For each distribution date on or before the Clean-Up Call Option Date, the annual certificate interest rate on the Class CA-1C Group 1Component will equal the least of (x) the Adjusted Loan Group 1 Net Weighted Average Pass-Through Rate, (y) LIBOR plus 0.22%and (z) theMaximum Loan Group 1 Rate. For each distribution date after the Clean-Up Call Option Date, the annual certificate interest rate on theClass CA-1C Group 1 Component will equal the least of (x) the Adjusted Loan Group 1 Net Weighted Average Pass-Through Rate, (y) LIBORplus 0.44%and (z) the Maximum Loan Group 1 Rate.

For each distribution date on or before the Clean-Up Call Option Date, the annual certificate interest rate on the Class CA-1C Group 2Component will equal the least of (x) the Adjusted Loan Group 2 Weighted Average Pass-Through Rate, (y) LIBOR plus 0.22%and (z) theMaximum Loan Group 2 Rate. For each distribution date after the Clean-Up Call Option Date, the annual certificate interest rate on theClass CA-1C Group 2 Component will equal the least of (x) the Adjusted Loan Group 2 Weighted Average Pass-Through Rate, (y) LIBOR plus0.44%and (z) the Maximum Loan Group 2 Rate.

In addition, if on any distribution date the certificate interest rate on any of the Class CA-1C Components is equal to the Adjusted Loan Group 1Net Weighted Average Pass-Through Rate or the Adjusted Loan Group 2 Weighted Average Pass-Through Rate, as applicable, the Class CA-

1C Certificates may be entitled to receive, as interest, carryover shortfall amounts from amounts, if any, otherwise payable to the Class 1X-PPPand Class 2X-PPP Certificates, as described in this prospectus supplement. See “Description of the Certificates—Distributions of Interest” inthis prospectus supplement . For the initial distribution date, after giving effect to carryover shortfall payments, if any, the annual certificateinterest rate on the Class CA-1C Components will equal LIBOR as of February 20, 2007 plus 0.22%.

(7)

Solely for purposes of calculating distributions of principal and interest and the allocation of losses realized on the mortgage loans, theClass 1X-PPP and Class 2X-PPP Certificates will each be deemed to be comprised of an interest-only component and a principal-onlycomponent. Interest, if any, will be payable with respect to each Class X interest-only component. The Class 1X-PPP and Class 2X-PPPinterest- only components will not have a principal balance and principal will not be payable with respect to the Class X interest-onlycomponents. Each of the Class 1X-PPP and Class 2X-PPP principal-only components will have a principal balance

S-8

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 10/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 10/

which initially will equal zero. Interest will not accrue on any Class X principal-only component. In the event that interest otherwise payable withrespect to the Class 1X-PPP or Class 2X-PPP interest-only component is reduced as a result of the allocation of net negative amortization (asdescribed in “Description of the Certificates—Distributions of Interest” in this prospectus supplement), the amount of such reduction will beadded as principal to the related Class X principal balance.

In addition, the Class 1X-PPP Certificates will be entitled to receive prepayment penalties paid by borrowers upon voluntary full prepayment of certain mortgage loans in loan group 1 if such mortgage loans are prepaid during certain periods, and the Class 2X-PPP Certificates will beentitled to receive prepayment penalties paid by borrowers upon voluntary full prepayment of certain mortgage loans in loan group 2 if suchmortgage loans are prepaid during certain periods. See “Description of the Mortgage Pool” and “Description of the Certificates—Distributionsto the Class 1X-PPP and Class 2X-PPP Certificates” herein and the “Prepayment Penalty Terms of the Group 1 Loans” and “Prepayment Penalty Terms of the Group 2 Loans” tables in Appendix B hereto for more information regarding the Class 1X-PPP and Class 2X-PPP Certificates and prepayment penalties.

(8)

The amount of interest available for distribution to the Class 1X-PPP Certificates on any distribution date (before giving effect to the allocationof any shortfall in interest collections and payment of carryover shortfall amounts) will equal the Class 1X-PPP Accrued Interest (as defined inthis prospectus supplement). Notwithstanding the foregoing, interest otherwise available for distribution to the Class 1X-PPP Certificates on andistribution date may instead be distributed as carryover shortfall amounts. See “Description of the Certificates—Distributions of Interest” in thi

prospectus supplement.

(9)

For each distribution date, the Class 1X-2 Certificates will not receive any distributions of principal, but will accrue interest on the Class 1X-2notional amount, which will equal the aggregate principal balance of the mortgage loans in subgroup 1A as of the second preceding due date.The initial Class 1X-2 notional amount will be approximately $65,082,546. See “Description of the Certificates—Distributions of Interest” in this

prospectus supplement .

(10)

For each distribution date, the certificate interest rate for the Class 1X-2 Certificates will be equal to the weighted average of an amount oneach mortgage loan in subgroup 1A which is calculated as follows: (a) for each mortgage loan in subgroup 1A that was in its initial three monthfixed rate period in the calendar month immediately preceding such distribution date, 0.00% and (b) for each mortgage loan in subgroup 1Athat was not in its initial three month fixed rate period in the calendar month immediately preceding such distribution date, the excess, if any, ofthe initial Margin (as defined in “Description of the Mortgage Pool” in this prospectus supplement) for such mortgage loan over 1.475%.

(11)

The amount of interest available for distribution to the Class 2X-PPP Certificates on any distribution date (before giving effect to the allocationof any shortfall in interest collections and payment of carryover shortfall amounts) will equal the Class 2X-PPP Accrued Interest (as defined inthis prospectus supplement). Notwithstanding the foregoing, interest otherwise available for distribution to the Class 2X-PPP Certificates on andistribution date may instead be distributed as carryover shortfall amounts. See “Description of the Certificates—Distributions of Interest” in thi

prospectus supplement.

(12)

For each distribution date on or before the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-1 Certificates willequal the least of (x) the Class B Net Weighted Average Pass- Through Rate (as defined in “Description of the Certificates—Distributions of Interest” in this prospectus supplement), (y) LIBOR plus 0.34%and (z) the Maximum Class B Rate (as defined in “Description of the Certificate—Distributions of Interest” in this prospectus supplement). For each distribution date after the Clean-Up Call Option Date, the annual certificateinterest rate on the Class B-1 Certificates will equal the least of (x) the Class B Net Weighted Average Pass-Through Rate, (y) LIBOR plus0.51%and (z) the Maximum Class B Rate. In addition, if on any distribution date the certificate interest rate on

S-9

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 11/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 11/

the Class B-1 Certificates is equal to the Class B Net Weighted Average Pass-Through Rate, the Class B-1 Certificates may be entitled toreceive, as interest, carryover shortfall amounts from amounts, if any, otherwise payable to the Class 1X-PPP and Class 2X-PPP Certificates,as described in this prospectus supplement. See “Description of the Certificates—Distributions of Interest” in this prospectus supplement . For the initial distribution date, after giving effect to carryover shortfall payments, if any, the annual certificate interest rate on these certificates willequal LIBOR as of February 20, 2007 plus 0.34%.

(13)

For each distribution date on or before the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-2 Certificates willequal the least of (x) the Class B Net Weighted Average Pass- Through Rate, (y) LIBOR plus 0.35%and (z) the Maximum Class B Rate. For each distribution date after the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-2 Certificates will equal the leastof (x) the Class B Net Weighted Average Pass-Through Rate, (y) LIBOR plus 0.525%and (z) the Maximum Class B Rate. In addition, if on anydistribution date the certificate interest rate on the Class B-2 Certificates is equal to the Class B Net Weighted Average Pass-Through Rate, theClass B-2 Certificates may be entitled to receive, as interest, carryover shortfall amounts from amounts, if any, otherwise payable to theClass 1X-PPP and Class 2X-PPP Certificates, as described in this prospectus supplement. See “Description of the Certificates—Distributions oInterest” in this prospectus supplement . For the initial distribution date, after giving effect to carryover shortfall payments, if any, the annualcertificate interest rate on these certificates will equal LIBOR as of February 20, 2007 plus 0.35%.

(14)

For each distribution date on or before the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-3 Certificates willequal the least of (x) the Class B Net Weighted Average Pass- Through Rate, (y) LIBOR plus 0.36%and (z) the Maximum Class B Rate. For each distribution date after the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-3 Certificates will equal the leastof (x) the Class B Net Weighted Average Pass-Through Rate, (y) LIBOR plus 0.54%and (z) the Maximum Class B Rate. In addition, if on anydistribution date the certificate interest rate on the Class B-3 Certificates is equal to the Class B Net Weighted Average Pass-Through Rate, theClass B-3 Certificates may be entitled to receive, as interest, carryover shortfall amounts from amounts, if any, otherwise payable to theClass 1X-PPP and Class 2X-PPP Certificates, as described in this prospectus supplement. See “Description of the Certificates—Distributions oInterest” in this prospectus supplement . For the initial distribution date, after giving effect to carryover shortfall payments, if any, the annualcertificate interest rate on these certificates will equal LIBOR as of February 20, 2007 plus 0.36%.

(15)

For each distribution date on or before the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-4 Certificates willequal the least of (x) the Class B Net Weighted Average Pass- Through Rate, (y) LIBOR plus 0.39%and (z) the Maximum Class B Rate. For each distribution date after the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-4 Certificates will equal the least

of (x) the Class B Net Weighted Average Pass-Through Rate, (y) LIBOR plus 0.585%and (z) the Maximum Class B Rate. In addition, if on anydistribution date the certificate interest rate on the Class B-4 Certificates is equal to the Class B Net Weighted Average Pass-Through Rate, theClass B-4 Certificates may be entitled to receive, as interest, carryover shortfall amounts from amounts, if any, otherwise payable to theClass 1X-PPP and Class 2X-PPP Certificates, as described in this prospectus supplement. See “Description of the Certificates—Distributions oInterest” in this prospectus supplement . For the initial distribution date, after giving effect to carryover shortfall payments, if any, the annualcertificate interest rate on these certificates will equal LIBOR as of February 20, 2007 plus 0.39%.

(16)

For each distribution date on or before the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-5 Certificates willequal the least of (x) the

S-10

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 12/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 12/

Class B Net Weighted Average Pass-Through Rate, (y) LIBOR plus 0.41%and (z) the Maximum Class B Rate. For each distribution date after the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-5 Certificates will equal the least of (x) the Class B NetWeighted Average Pass-Through Rate, (y) LIBOR plus 0.615%and (z) the Maximum Class B Rate. In addition, if on any distribution date thecertificate interest rate on the Class B-5 Certificates is equal to the Class B Net Weighted Average Pass-Through Rate, the Class B-5Certificates may be entitled to receive, as interest, carryover shortfall amounts from amounts, if any, otherwise payable to the Class 1X-PPPand Class 2X-PPP Certificates, as described in this prospectus supplement. See “Description of the Certificates—Distributions of Interest” inthis prospectus supplement . For the initial distribution date, after giving effect to carryover shortfall payments, if any, the annual certificateinterest rate on these certificates will equal LIBOR as of February 20, 2007 plus 0.41%.

(17)

For each distribution date on or before the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-6 Certificates willequal the least of (x) the Class B Net Weighted Average Pass- Through Rate, (y) LIBOR plus 0.46%and (z) the Maximum Class B Rate. For each distribution date after the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-6 Certificates will equal the leastof (x) the Class B Net Weighted Average Pass-Through Rate, (y) LIBOR plus 0.69%and (z) the Maximum Class B Rate. In addition, if on any

distribution date the certificate interest rate on the Class B-6 Certificates is equal to the Class B Net Weighted Average Pass-Through Rate, theClass B-6 Certificates may be entitled to receive, as interest, carryover shortfall amounts from amounts, if any, otherwise payable to theClass 1X-PPP and Class 2X-PPP Certificates, as described in this prospectus supplement. See “Description of the Certificates—Distributions oInterest” in this prospectus supplement . For the initial distribution date, after giving effect to carryover shortfall payments, if any, the annualcertificate interest rate on these certificates will equal LIBOR as of February 20, 2007 plus 0.46%.

(18)

For each distribution date on or before the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-7 Certificates willequal the least of (x) the Class B Net Weighted Average Pass- Through Rate, (y) LIBOR plus 0.70%and (z) the Maximum Class B Rate. For each distribution date after the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-7 Certificates will equal the leastof (x) the Class B Net Weighted Average Pass-Through Rate, (y) LIBOR plus 1.050%and (z) the Maximum Class B Rate. In addition, if on anydistribution date the certificate interest rate on the Class B-7 Certificates is equal to the Class B Net Weighted Average Pass-Through Rate, theClass B-7 Certificates may be entitled to receive, as interest, carryover shortfall amounts from amounts, if any, otherwise payable to theClass 1X-PPP and Class 2X-PPP Certificates, as described in this prospectus supplement. See “Description of the Certificates—Distributions oInterest” in this prospectus supplement . For the initial distribution date, after giving effect to carryover shortfall payments, if any, the annualcertificate interest rate on these certificates will equal LIBOR as of February 20, 2007 plus 0.70%.

(19)

For each distribution date on or before the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-8 Certificates willequal the least of (x) the Class B Net Weighted Average Pass- Through Rate, (y) LIBOR plus 0.90%and (z) the Maximum Class B Rate. For each distribution date after the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-8 Certificates will equal the leastof (x) the Class B Net Weighted Average Pass-Through Rate, (y) LIBOR plus 1.35%and (z) the Maximum Class B Rate. In addition, if on anydistribution date the certificate interest rate on the Class B-8 Certificates is equal to the Class B Net Weighted Average Pass-Through Rate, theClass B-8 Certificates may be entitled to receive, as interest, carryover shortfall amounts from amounts, if any, otherwise payable to theClass 1X-PPP and Class 2X-PPP Certificates, as described in this prospectus supplement. See “Description of the Certificates—Distributions oInterest” in this prospectus supplement . For the initial distribution date, after giving effect to

S-11

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 13/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 13/

carryover shortfall payments, if any, the annual certificate interest rate on these certificates will equal LIBOR as of February 20, 2007 plus0.90%.

(20)

For each distribution date on or before the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-9, Class B-10 andClass B-11 Certificates will equal the least of (x) the Class B Net Weighted Average Pass-Through Rate, (y) LIBOR plus 1.20%and (z) theMaximum Class B Rate. For each distribution date after the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-9,Class B-10 and Class B-11 Certificates will equal the least of (x) the Class B Net Weighted Average Pass-Through Rate, (y) LIBOR plus 1.80%and (z) the Maximum Class B Rate. In addition, if on any distribution date the certificate interest rate on the Class B-9, Class B-10 and Class B-11 Certificates is equal to the Class B Net Weighted Average Pass-Through Rate, the Class B-9, Class B-10 and Class B-11 Certificates maybe entitled to receive, as interest, carryover shortfall amounts from amounts, if any, otherwise payable to the Class 1X-PPP and Class 2X-PPPCertificates, as described in this prospectus supplement. See “Description of the Certificates—Distributions of Interest” in this prospectussupplement . For the initial distribution date, after giving effect to carryover shortfall payments, if any, the annual certificate interest rate onthese certificates will equal LIBOR as of February 20, 2007 plus 1.20%.

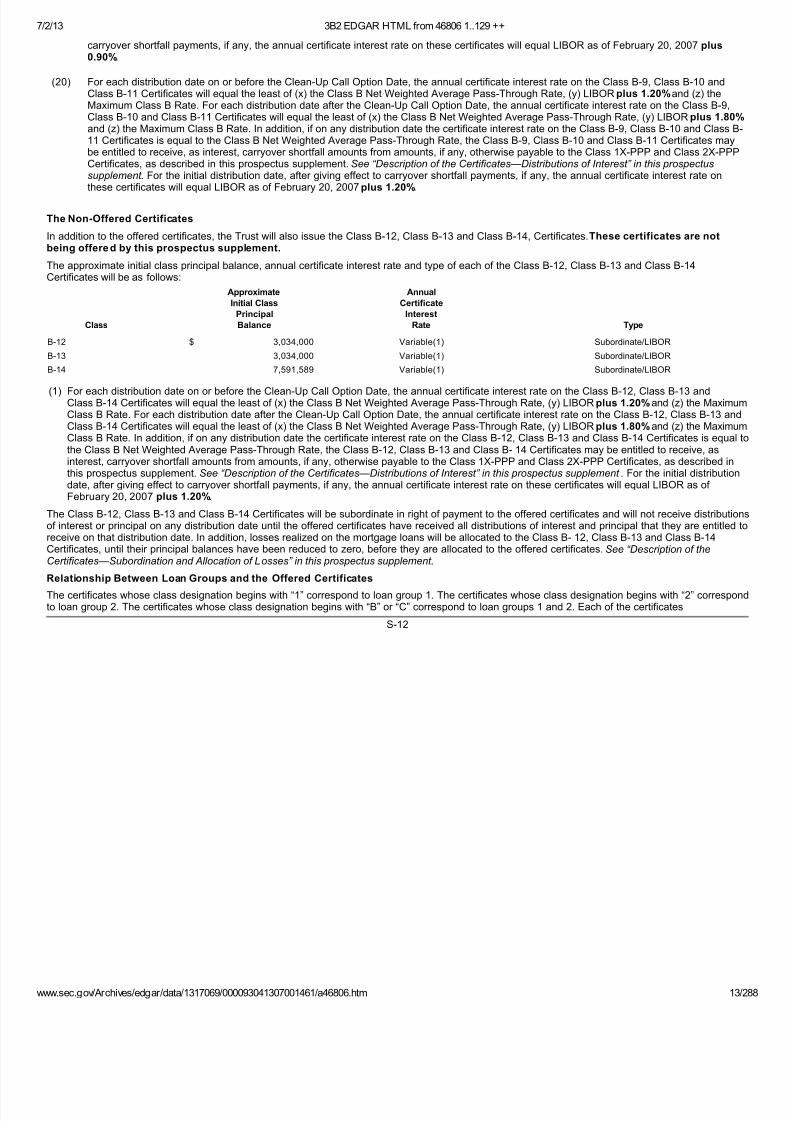

The Non-Offered Certificates

In addition to the offered certificates, the Trust will also issue the Class B-12, Class B-13 and Class B-14, Certificates. These certificates are notbeing offere d by this prospectus supplement.

The approximate initial class principal balance, annual certificate interest rate and type of each of the Class B-12, Class B-13 and Class B-14Certificates will be as follows:

Class

Approximate

Initial Class

Principal

Balance

Annual

Certificate

Interest

Rate Type

B-12 $

3,034,000 Variable(1) Subordinate/LIBOR

B-13 3,034,000 Variable(1) Subordinate/LIBOR

B-14 7,591,589 Variable(1) Subordinate/LIBOR

(1)

For each distribution date on or before the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-12, Class B-13 andClass B-14 Certificates will equal the least of (x) the Class B Net Weighted Average Pass-Through Rate, (y) LIBOR plus 1.20%and (z) the MaximumClass B Rate. For each distribution date after the Clean-Up Call Option Date, the annual certificate interest rate on the Class B-12, Class B-13 andClass B-14 Certificates will equal the least of (x) the Class B Net Weighted Average Pass-Through Rate, (y) LIBOR plus 1.80%and (z) the MaximumClass B Rate. In addition, if on any distribution date the certificate interest rate on the Class B-12, Class B-13 and Class B-14 Certificates is equal tthe Class B Net Weighted Average Pass-Through Rate, the Class B-12, Class B-13 and Class B- 14 Certificates may be entitled to receive, asinterest, carryover shortfall amounts from amounts, if any, otherwise payable to the Class 1X-PPP and Class 2X-PPP Certificates, as described inthis prospectus supplement. See “Description of the Certificates—Distributions of Interest” in this prospectus supplement . For the initial distributiondate, after giving effect to carryover shortfall payments, if any, the annual certificate interest rate on these certificates will equal LIBOR as of February 20, 2007 plus 1.20%.

The Class B-12, Class B-13 and Class B-14 Certificates will be subordinate in right of payment to the offered certificates and will not receive distributionof interest or principal on any distribution date until the offered certificates have received all distributions of interest and principal that they are entitled toreceive on that distribution date. In addition, losses realized on the mortgage loans will be allocated to the Class B- 12, Class B-13 and Class B-14Certificates, until their principal balances have been reduced to zero, before they are allocated to the offered certificates. See “Description of theCertificates—Subordination and Allocation of Losses” in this prospectus supplement.

Relationship Between Loan Groups and the Offered Certificates

The certificates whose class designation begins with “1” correspond to loan group 1. The certificates whose class designation begins with “2” corresponto loan group 2. The certificates whose class designation begins with “B” or “C” correspond to loan groups 1 and 2. Each of the certificates

S-12

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 14/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 14/

generally receives distributions based on principal and interest collected from mortgage loans in its corresponding loan group or loan groups.

Initial Principal Balance of the Certificates

The initial aggregate principal balance of the certificates issued by the Trust is approximately $1,011,390,689, subject to an upward or downwardvariance of no more than 5%.

The initial aggregate principal balance of the certificates has the following composition:

•

the senior certificates related to loan group 1 and loan group 2 comprise approximately 90.75% of the principal balance of the applicable loan group;

•

the Class B-1, Class B-2, Class B-3, Class B-4, Class B-5, Class B-6, Class B-7, Class B-8, Class B-9, Class B-10 and Class B-11 Certificatescomprise approximately 7.90% of the aggregate principal balance of loan groups 1 and 2; and

•

the privately offered Class B-12, Class B-13 and Class B-14 Certificates comprise approximately 1.35% of the aggregate principal balance of loangroups 1 and 2.

Last Scheduled Distribution Date

The last scheduled distribution date for each class of certificates is the distribution date in the month after the scheduled maturity date for the latestmaturing mortgage loan in the related loan group or loan groups.

The actual rate of principal payments on the certificates will depend on the rate of principal payments (including principal prepayments) on the relatedmortgage loans. No assurance can be given as to the actual payment experience on the mortgage loans.

See “Description of the Certificates—Last Scheduled Distribution Date” in this prospectus supplement.

DISTRIBUTIONS ON THE CERTIFICATES

Monthly Distributions

Each month, the trustee, LaSalle Bank National Association, will make distributions of interest and/or principal to the holders of the certificates.Distributions will be made on the 25th day of each month, or if the 25th day is not a business day, on the next business day. The first distribution date w

be March 26, 2007.

Source of Payments. The mortgagors pay their interest and principal during the month to the servicer. Each month, the servicer subtracts its servicingfee and sends the remainder to the trustee. On the distribution date for that month, the trustee distributes that remaining amount by loan group to theholders of the certificates related to that loan group in the order described in “Description of the Certificates—Priority of Distributions” in this prospectussupplement (in accordance with the monthly distribution report). The servicing fee will be calculated as a per annum percentage for each mortgage loanThe following table describes the servicing fee for each type of mortgage loan:

Type of Mortgage Loan Servicing Fee

subgroup 1A loan 0.375%

subgroup 1B loan that does not impos e a penal ty for voluntary full prepayments the greater of (i) 0.375% and (ii) the excess, if any, of the initial Margin on thatmortgage loan over 1.10%

subgroup 1B loan that imposes a penalty for voluntary full prepayments and has a

prepayment penalty term of 12 m onths from origin ation the greater of (i) 0.375% and (ii) the excess, if any, of the initial Margin on that

mortgage loan over 1.40%

subgroup 1B loan that imposes a penalty for voluntary full prepayments and has a

prepayment penalty term of 30 months o r 36 months from origination the greater of (i) 0.375% and (ii) the excess, if any, of the initial Margin on that

mortgage loan over 2.40%

group 2 loan the greater of (i) 0.375% and (ii) the excess, if any, of the initial Margin on that

mortgage loan over 1.75%

Advances. For any month, if the servicer receives a payment on a mortgage loan that is less than the minimum monthly payment due or if no payment ireceived at all, the servicer will advance its own funds or funds collected by the servicer on the mortgage loans but not required to be distributed to thecertificateholders on the current distribution date, to cover the difference between the minimum monthly payment due and the amount actually receivedby the servicer. However, the servicer will not be required to make advances if it determines that those advances will not be recoverable from futurepayments or collections on that mortgage loan. See “The Servicers—The Servicer—Servicing Procedures—Advances” in this prospectus supplement.

Distributions of Interest

Each class of offered certificates will accrue interest. On each distribution date interest will be distributed to these classes in the order described in“Description of the Certificates—Priority of Distributions” in this prospectus supplement.

Solely for purposes of calculating distributions of principal and interest and the allocation of losses

S-13

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 15/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 15/

realized on the mortgage loans, each of the Class 1X-PPP and Class 2X-PPP Certificates will be deemed to be comprised of an interest-only componenand a principal-only component. Interest, if any, will be payable with respect to each Class 1X-PPP and Class 2X-PPP interest-only component. TheClass 1X-PPP and Class 2X-PPP interest-only components will not have a principal balance and principal will not be payable with respect to the interestonly components. Each of the Class 1X-PPP and Class 2X-PPP principal-only components will have a principal balance, which initially will equal zero.Interest will not accrue on any Class 1X-PPP or Class 2X-PPP principal-only component.

The Class 1X-2 Certificates will accrue interest on the Class 1X-2 Notional Amount. The Class 1X-2 Certificates will not have a pr incipal component andwill not receive distributions of principal.

Solely for purposes of calculating distributions of principal and interest and the allocation of losses realized on the mortgage loans, the Class CA-1BCertificates will be deemed to be comprised of the Class CA-1B Group 1 Component and the Class CA-1B Group 2 Component. Each Class CA-1BComponent will have a component principal balance representing the portion of the related class principal balance. Interest will be payable with respectto each Class CA-1B Component.

Solely for purposes of calculating distributions of principal and interest and the allocation of losses realized on the mortgage loans, the Class CA-1CCertificates will be deemed to be comprised of the Class CA-1C Group 1 Component and the Class CA-1C Group 2 Component. Each Class CA-1CComponent will have a component principal balance representing the portion of the related class principal balance. Interest will be payable with respectto each Class CA-1C Component.

Interest to be distributed on the certificates (or added to the principal balance of the certificates in the form of Net Negative Amortization, as definedbelow) on any distribution date will consist of accrued and unpaid interest as of previous distribution dates and interest accrued during the periodbeginning on the 25th day of the preceding calendar month (or, in the case of the first distribution date, February 22, 2007) and ending on the 24th dayof the month of that distribution date, except for the Class 1A, Class 2A, Class 1X-PPP, Class 1X-2 and Class 2X-PPP Certificates, which accrue interesduring the preceding calendar month. Interest on the Class CA-1B, Class CA-1C and Class B Certificates (as defined in “Description of the Certificates—General” in this prospectus supplement) will be calculated based on the actual number of days in the certificate accrual period and assuming a 360 dayyear. Interest on the Class 1A, Class 2A, Class 1X-PPP, Class 1X-2 and Class 2X-PPP Certificates will be calculated based on a year consisting of twelvthirty- day months.

In the event that an increase in the applicable index causes interest to accrue on a mortgage loan for a given month in excess of the monthly paymentfor that mortgage loan, the excess interest will be added to the outstanding principal balance of that mortgage loan in the form of “negative amortizationFor any distribution date, the excess, if any, of (i) the aggregate amount of negative amortization with respect to all mortgage loans in a loan group for the calendar month prior to that distribution date, over (ii) the aggregate amount of prepayments in full and partial prepayments received with respect to

all mortgage loans in that loan group during the related prepayment period (the “Net Negative Amortization”), will be deducted from interest payableto the related certificates as described in “Description of the Certificates—Distributions of Interest” in this prospectus supplement. The amount deductedfrom the interest payable to each class of certificates will be added to the principal balance of that class.

It is possible that, on any given distribution date, there will be insufficient payments from the mortgage loans to make the interest distributions (net of anNet Negative Amortization deducted from interest payable) described in this prospectus supplement. If the servicer does not advance its own funds,because it determines that the advance would be nonrecoverable, some certificates, most likely the subordinate certificates, may not receive the fullamount of accrued interest to which they are entitled. If this happens, those certificates will be entitled to receive any shortfall in interest distributions onfuture distribution dates in the same priority as their distribution of current interest. However, there will be no extra interest paid on that shortfall.

The amount of interest each Class CA-1B or Class CA-1C Component and each class of Class B Certificates accrues during each certificate accrualperiod will equal a ratio, the numerator of which is the actual number of days in that accrual period and the denominator of which is 360, multiplied by th

S-14

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 16/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 16/

annual certificate interest rate in effect for that accrual period for that class or component and multiplied by the related class principal balance or component principal balance. The amount of interest the Class 1A, Class 2A and Class 1X-2 Certificates accrue during each certificate accrual periodwill equal 1/12th of the annual certificate interest rate in effect for that accrual period for that class multiplied by their respective class principal balanceor class notional amount, as applicable. The principal balance used for this calculation for the Class A Certificates (as defined in “Description of theCertificates—General” in this prospectus supplement) and Class B Certificates on the first distribution date will be the applicable principal balance as of February 22, 2007, which is the closing date. The principal balance used for this calculation on each distribution date thereafter will be the applicableprincipal balance immediately after the preceding distribution date. For a description of how the interest distributions to the Class 1X-2, Class 1X-PPPand Class 2X- PPP Certificates are determined, see “Description of the Certificates—Distributions of Interest” in this prospectus supplement. The annuacertificate interest rate for each class of offered certificates is described on pages S-6 to S-12 of this prospectus supplement.

No interest will accrue on the Class 1X-PPP or Class 2X-PPP principal-only components.

One-Year MTA Certificates. The certificate interest rate for the Class 1A Certificates adjusts monthly based on an index (currently One-Year MTA, asdescribed in “Description of the Mortgage Pool—The Indexes” in this prospectus supplement). The formula for the calculation of the certificate interestrate for the Class 1A Certificates appears in the notes to the table on page S-6 of this prospectus supplement. However, the certificate interest rate for these certificates is subject to a cap described in the notes to the table on page S-6 of this prospectus supplement. For more information, see “Risk Factors—If an Index is Replaced, the Mortgage Loan Margins and the Certificate Margin on the MTA and COFI Certificates May be Adjusted”, “—TheClass 1A Certificates May Receive Interest at a Certificate Interest Rate Lower than the One-Year MTA Index Plus the Related Margin”, “Description of the Mortgage Pool—The Indexes” and “Description of the Certificates—Distributions of Interest” in this prospectus supplement.

For the initial distribution date only, the Class 1A Certificates may receive as interest, in addition to interest accrued at their certificate interest rate,carryover shortfall amounts, as described in “Description of the Certificates—Distributions of Interest—Carryover Shortfall Amount ” in this prospectussupplement. The Class 1A Certificates will not receive any carryover shortfall payments on any other distribution date .

COFI Certificates. The certificate interest rate for the Class 2A Certificates adjusts monthly based on an index (currently COFI, as described in“Description of the Mortgage Pool—The Indexes” in this prospectus supplement). The formula for the calculation of the certificate interest rate for theClass 2A Certificates appears in the notes to the table on page S-6 of this prospectus supplement. However, the certificate interest rate for thesecertificates is subject to a cap described in the notes to the table on page S-6 of this prospectus supplement. For more information, see “Risk Factors—If an Index is Replaced, the Mortgage Loan Margins and the Certificate Margin on the MTA and COFI Certificates May be Adjusted”, “—The Class 2ACertificates May Receive Interest at a Certificate Interest Rate Lower than the COFI Index Plus the Related Margin”, “Description of the Mortgage Pool—The Indexes” and “Description of the Certificates—Distributions of Interest” in this prospectus supplement.

For the initial distribution date only, the Class 2A Certificates may receive as interest, in addition to interest accrued at their certificate interest rate,carryover shortfall amounts, as described in “Description of the Certificates—Distributions of Interest—Carryover Shortfall Amount ” in this prospectussupplement. The Class 2A Certificates will not receive any carryover shortfall payments on any other distribution date .

LIBOR Certificates. The certificate interest rates for the Class CA-1B, Class CA-1C and Class B Certificates (or components thereof) adjust monthlybased on the average of quotations of the London Interbank Offered Rate for one-month U.S. dollar deposits, or LIBOR, as described in “Description of the Certificates—Calculation of LIBOR” in this prospectus supplement. The formulas for the calculation of the certificate interest rates for these classesof certificates (or the components thereof) appear in the notes to the table on page S-6 of this prospectus supplement. However, the certificate interestrates for these classes (or the components thereof) are subject to caps described in the notes to the table on page S-6 of this prospectus supplement.

On each distribution date, the Class CA-1B, Class CA-1C and Class B Certificates may receive

S-15

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 17/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 17/

as interest, in addition to interest accrued at their certificate interest rates, carryover shortfall amounts, as described in “Description of the Certificates—Distributions of Interest—Carryover Shortfall Amount ” in this prospectus supplement.

Subject to the limitations described under “Description of the Certificates—Distributions of Interest—Carryover Shortfall Amounts” in this prospectussupplement, interest otherwise available for distribution to the Class 1X-PPP and Class 2X-PPP Certificates on any distribution date may be reduced bycarryover shortfall amounts payable to the Class A and Class B Certificates, as described in “Description of the Certificates—Distributions of Interest—Carryover Shortfall Amounts” in this prospectus supplement.

Compensating Interest and Interest Shortfalls

Prepayments in Full. When mortgagors make prepayments in full, they need not pay a full month’s interest. Instead, they are required to pay interestonly to the date of their prepayment. To compensate certificateholders for the shortfall in interest this causes, the servicer may pay compensatinginterest to the certificateholders out of the servicing fee it collects, as well as from certain other sources. For a description of how compensating interest

is allocated among the certificates as well as important limitations on the amount of compensating interest that will be allocated among the certificates,see “Description of the Certificates—Distributions of Interest—Compensating Interest” and “Yield and Prepayment Considerations” in this prospectussupplement.

Partial Prepayments. When mortgagors make partial prepayments, they do not pay interest on the amount of that prepayment. Certificateholders willreceive no compensating interest to compensate them for the shortfall in interest this causes.

Distributions of Principal

General. As the mortgagors pay principal on the mortgage loans in each loan group, that principal is passed on to the holders of the certificates relatedto that loan group.

The Class A Certificates and (in the event Net Negative Amortization has been allocated to the Class 1X-PPP or Class 2X-PPP Certificates) the Class 1XPPP and Class 2X-PPP Certificates, in the aggregate, generally will receive their pro rata share of scheduled principal payments received on themortgage loans in the related loan group on each distribution date. In addition, unless credit enhancement to the Class A, Class 1X-PPP and Class 2X-PPP Certificates has reached a specified level and the delinquencies and losses on the mortgage loans in the related loan group do not exceedspecified limits, the Class A, Class 1X-PPP and Class 2X-PPP Certificates, in the aggregate, generally will receive 100% of all principal prepaymentsreceived on the mortgage loans in the related loan group, net of any portion thereof applied to reduce negative amortization, until the tenth anniversary

of the first distribution date, after which they will receive a disproportionately large, but decreasing, share of principal prepayments.Certificates Related to Loan Group 1. On each distribution date, a portion of the principal received or advanced on the mortgage loans in loan group 1will be distributed to the Class 1A and Class 1X-PPP Certificates and the Class CA-1B Group 1 and Class CA-1C Group 1 Components in the order of priority described in “Description of the Certificates—Distributions of Principal—Group 1 Senior Principal Distribution Amount ” in this prospectussupplement. However, not all of these certificates may receive principal on each distribution date. See Appendix A for a table showing, foeach class of these certificates (other than the Class 1X-PPP Certificates), the rate of return of principal that would result from differentrates of prepayments on the mortgage loans in loan group 1. However, if the Class B Certificates are no longer outstanding, then the Class 1Aand Class 1X-PPP Certificates and the Class CA-1B Group 1 and Class CA-1C Group 1 Components will not receive principal in the order of prioritydescribed in “Description of the Certificates—Distributions of Principal—Group 1 Senior Principal Distribution Amount ” in this prospectus supplement.Instead, each of these classes of certificates will generally receive principal pro rata according to its class principal balance or related componentprincipal balance, as applicable.

Certificates Related to Loan Group 2 . On each distribution date, a portion of the principal received or advanced on the mortgage loans in loan group 2will be distributed to the Class 2A and Class 2X-PPP Certificates and the Class CA-1B Group 2 and Class CA-1C Group 2 Components in the order of priority described in “Description of the Certificates—Distributions of Principal—Group 2 Senior Principal Distribution Amount ” in this prospectussupplement. However, not all of these ce rtificates may receiv e principal on each

S-16

7/15/2019 424B5 FILING WAMU 2007-OA2 Prospectus and Supplemental Prospectus 288 PAGES

http://slidepdf.com/reader/full/424b5-filing-wamu-2007-oa2-prospectus-and-supplemental-prospectus-288-pages 18/288

7/2/13 3B2 EDGAR HTML from 46806 1..129 ++

www.sec.gov/Archives/edgar/data/1317069/000093041307001461/a46806.htm 18/

distribution date. See Appendix A for a table showing, for each class of these certificates (other than the Class 2X-PPP Certificates), therate of return of principal that would result from different rates of prepayments on the mortgage loans in loan group 2. However, if theClass B Certificates are no longer outstanding, then the Class 2A and Class 2X-PPP Certificates and the Class CA-1B Group 2 and Class CA-1C Group2 Components will not receive principal in the order of priority described in “Description of the Certificates—Distributions of Principal—Group 2 Senior Principal Distribution Amount ” in this prospectus supplement. Instead, each of these classes of certificates will generally receive principal pro rataaccording to its class principal balance or related component principal balance, as applicable.

Class B Certificates. On each distribution date, the Class B-1, Class B-2, Class B-3, Class B-4, Class B-5, Class B-6, Class B-7, Class B-8, Class B-9,Class B-10, Class B-11, Class B-12, Class B-13 and Class B-14 Certificates will be entitled to receive a portion of the scheduled principal received or advanced on the mortgage loans, pro rata, according to their respective class principal balances. Unless credit enhancement to the senior certificateshas reached a specified level and the delinquencies and losses on the mortgage loans do not exceed specified limits, the Class B Certificates generallywill receive a portion of the principal prepayments on the mortgage loans only on and after the tenth anniversary of the first distribution date. However,under certain conditions described in this prospectus supplement under “Description of the Certificates—Priority of Distributions,” the amount of princip

prepayments otherwise distributable to some classes of Class B Certificates (as defined in “Description of the Certificates—General” in this prospectussupplement) will instead be paid to other classes of these certificates with a higher priority.

Priority of Principal Distributions. Each class of certificates entitled to principal receives its principal entitlements in the order described in “Description ofthe Certificates—Priority of Distributions” in this prospectus supplement. It is possible that, on any given distribution date, there will be insufficientpayments from the mortgage loans to make the principal distributions described in this prospectus supplement. As a result, some certificates, most likelthe subordinate certificates, may not receive the full amount of principal distributions to which they are entitled.

The Class 1X-PPP and Class 2X-PPP Certificates will not receive any distributions of principal in respect of their interest-only components.

The Class 1X-2 Certificates will not receive any distributions of principal.

For a more detailed description of how distributions of principal will be allocated among the various classes of certificates, see “Description of theCertificates—Distributions of Principal” in this prospectus supplement.

Cross-Collateralization