Embed Size (px)

Citation preview

Completion Report

Project Number: 41116-033 Loan Number: 2925 June 2021

India: Jammu and Kashmir Urban Sector Development Investment Program (Project 2)

This document is being disclosed to the public in accordance with ADB’s Access to Information Policy.

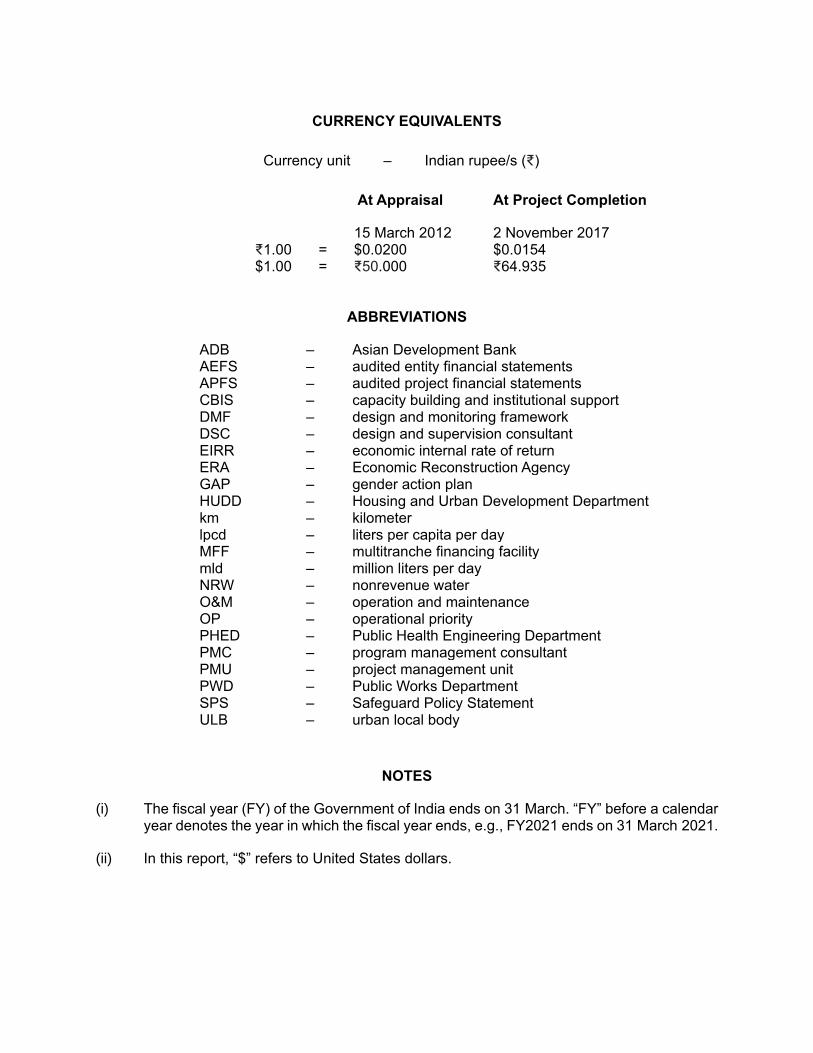

CURRENCY EQUIVALENTS

Currency unit – Indian rupee/s (₹)

At Appraisal At Project Completion

15 March 2012 2 November 2017 ₹1.00 = $0.0200 $0.0154 $1.00 = ₹50.000 ₹64.935

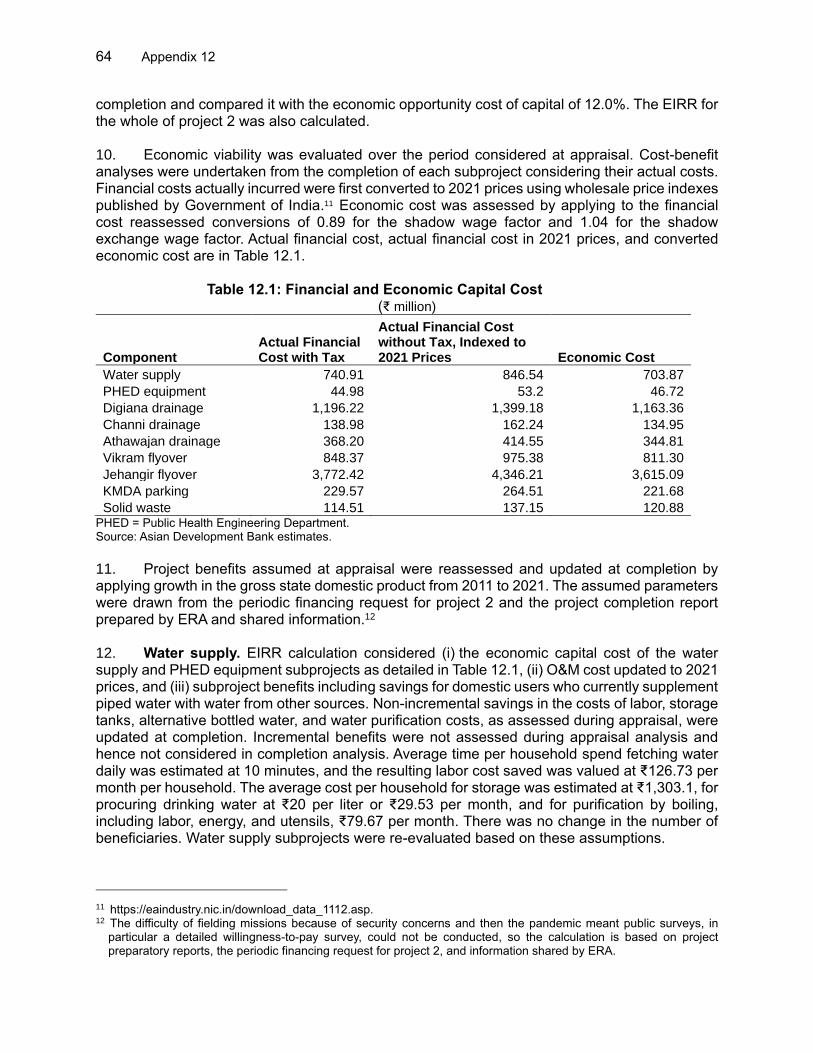

ABBREVIATIONS

ADB – Asian Development Bank AEFS APFS

– –

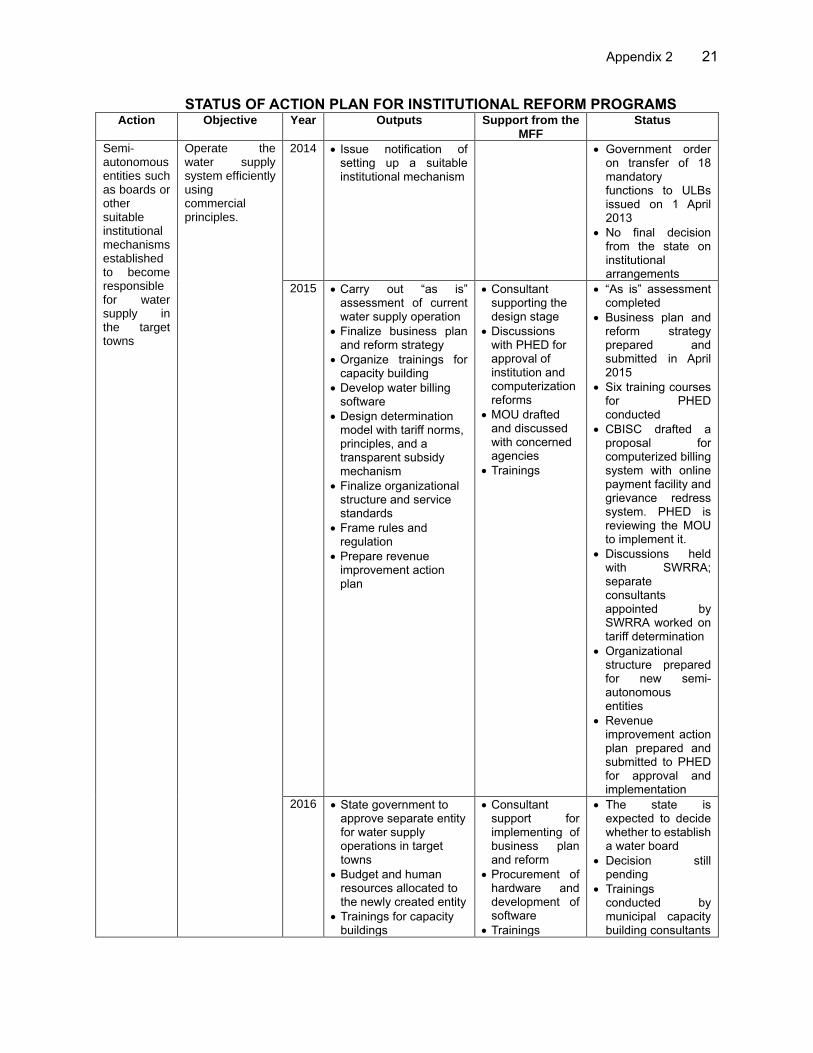

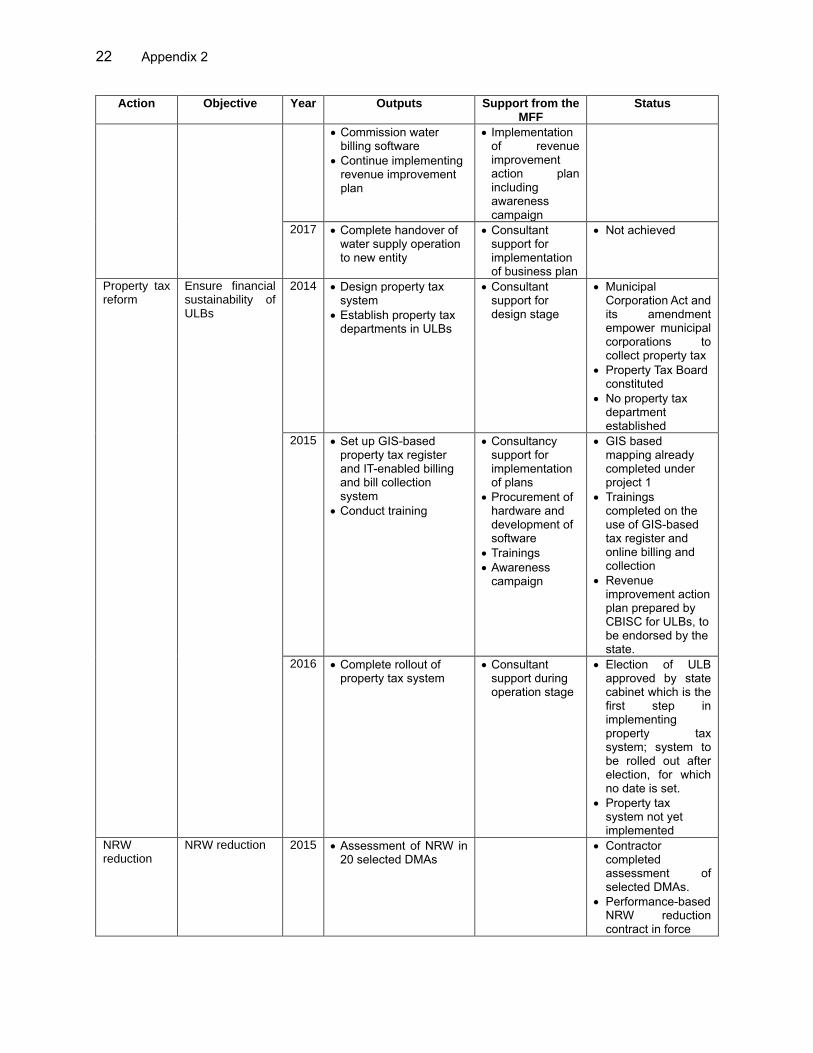

audited entity financial statements audited project financial statements

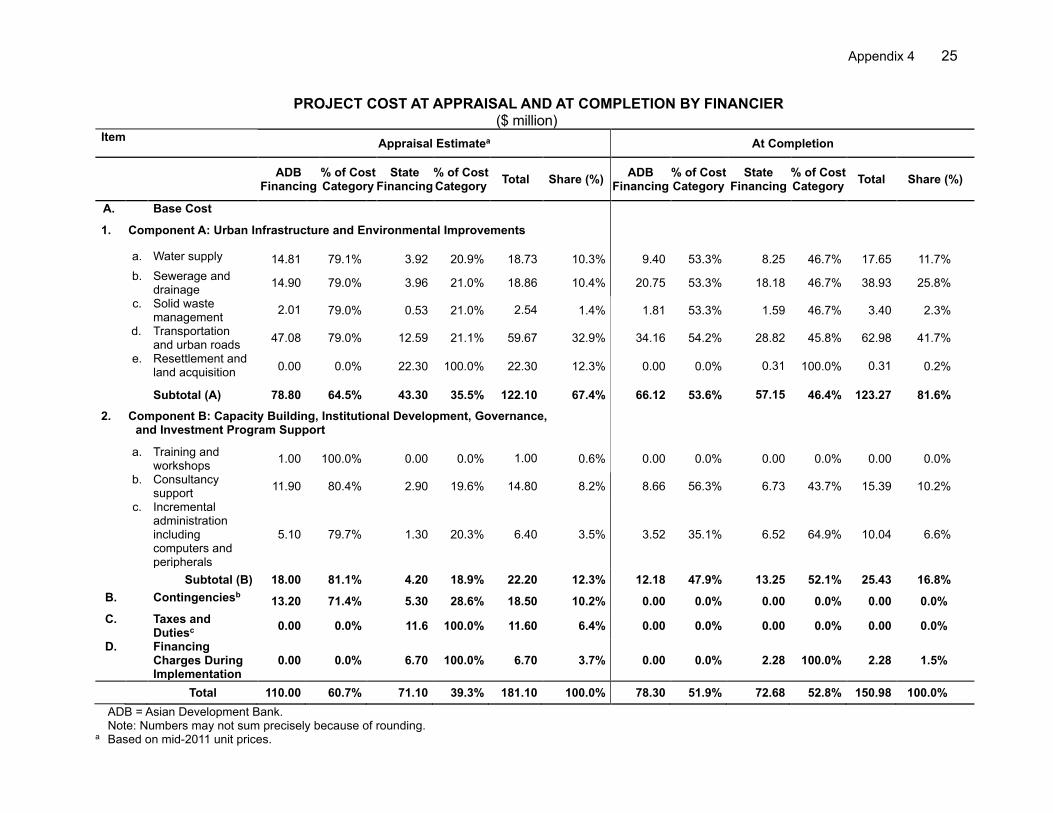

CBIS – capacity building and institutional support DMF – design and monitoring framework DSC – design and supervision consultant EIRR – economic internal rate of return ERA – Economic Reconstruction Agency GAP – gender action plan HUDD – Housing and Urban Development Department km – kilometer lpcd – liters per capita per day MFF – multitranche financing facility mld – million liters per day NRW – nonrevenue water O&M – operation and maintenance OP – operational priority PHED – Public Health Engineering Department PMC – program management consultant PMU – project management unit PWD – Public Works Department SPS – Safeguard Policy Statement ULB – urban local body

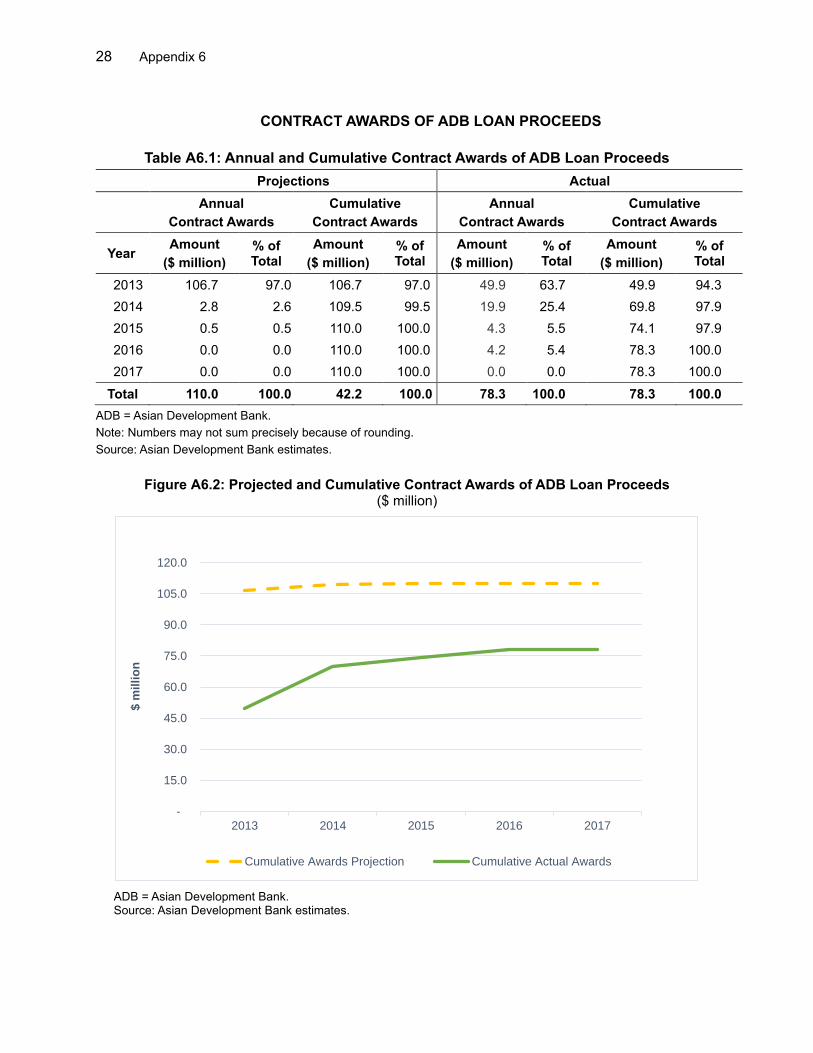

NOTES

(i) The fiscal year (FY) of the Government of India ends on 31 March. “FY” before a calendar year denotes the year in which the fiscal year ends, e.g., FY2021 ends on 31 March 2021.

(ii) In this report, “$” refers to United States dollars.

Vice-President Shixin Chen, Operations 1

Director General Kenichi Yokoyama, South Asia Department (SARD)

Director Norio Saito, Urban Development and Water Division (SAUW), SARD

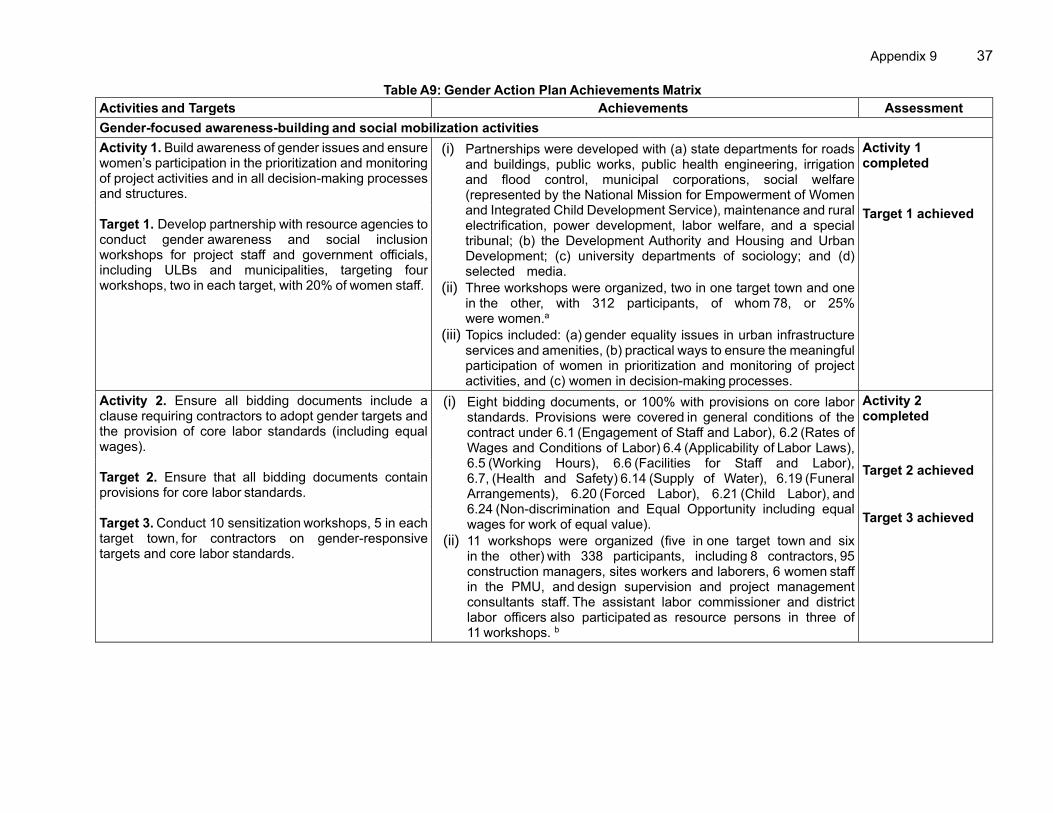

Team leader Momoko Tada, Urban Development Specialist, SAUW, SARD

Team members Saswati Belliappa, Safeguards Specialist, SAUW, SARD Bhawna Kulshreshtha, Executive Assistant, India Resident Mission

(INRM), SARD Girish Mahajan, Senior Environment Officer, INRM, SARD Rodellyn Manalac, Operations Assistant, SAUW, SARD Suhail Mircha, Safeguard Officer, INRM, SARD Pradeep Kumar Pandey, Associate Operations Analyst, INRM, SARD

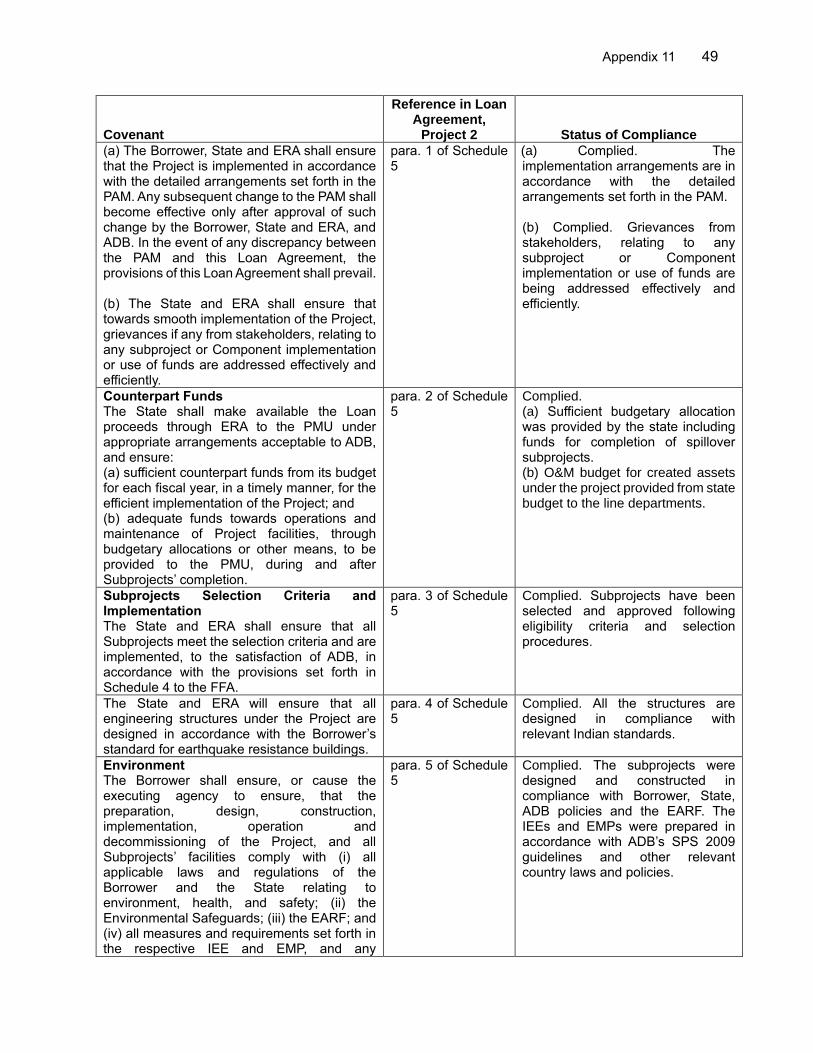

In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area.

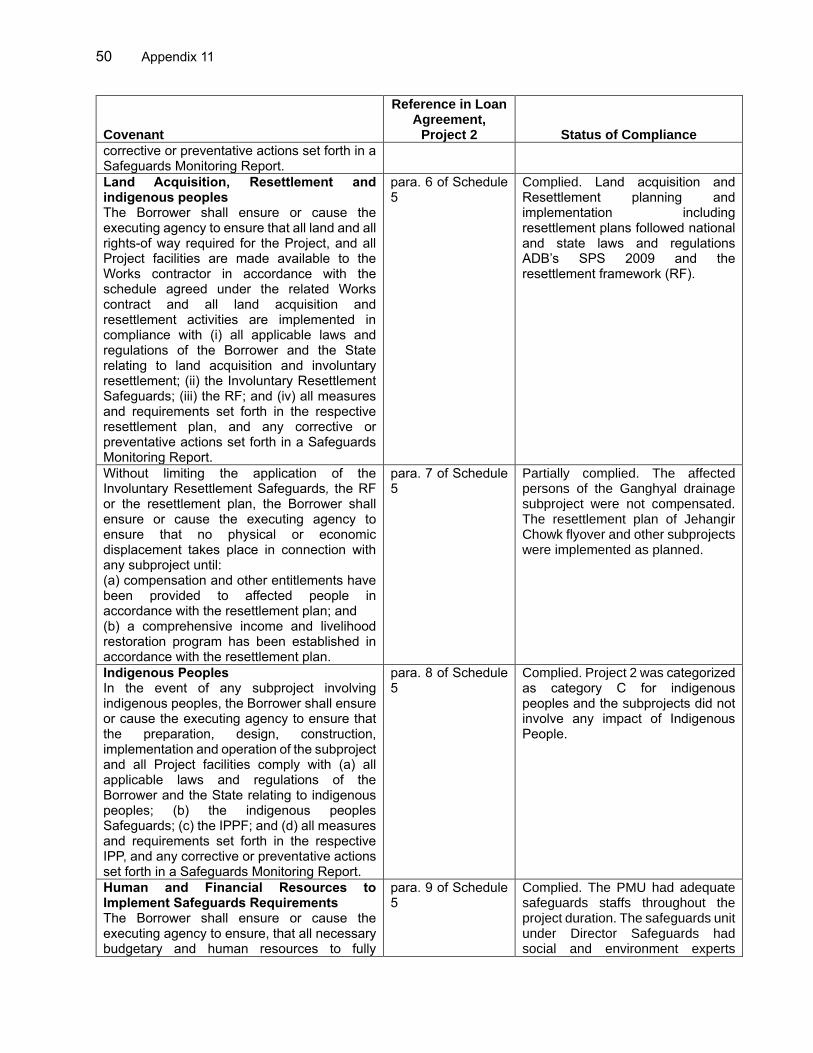

CONTENTS Page

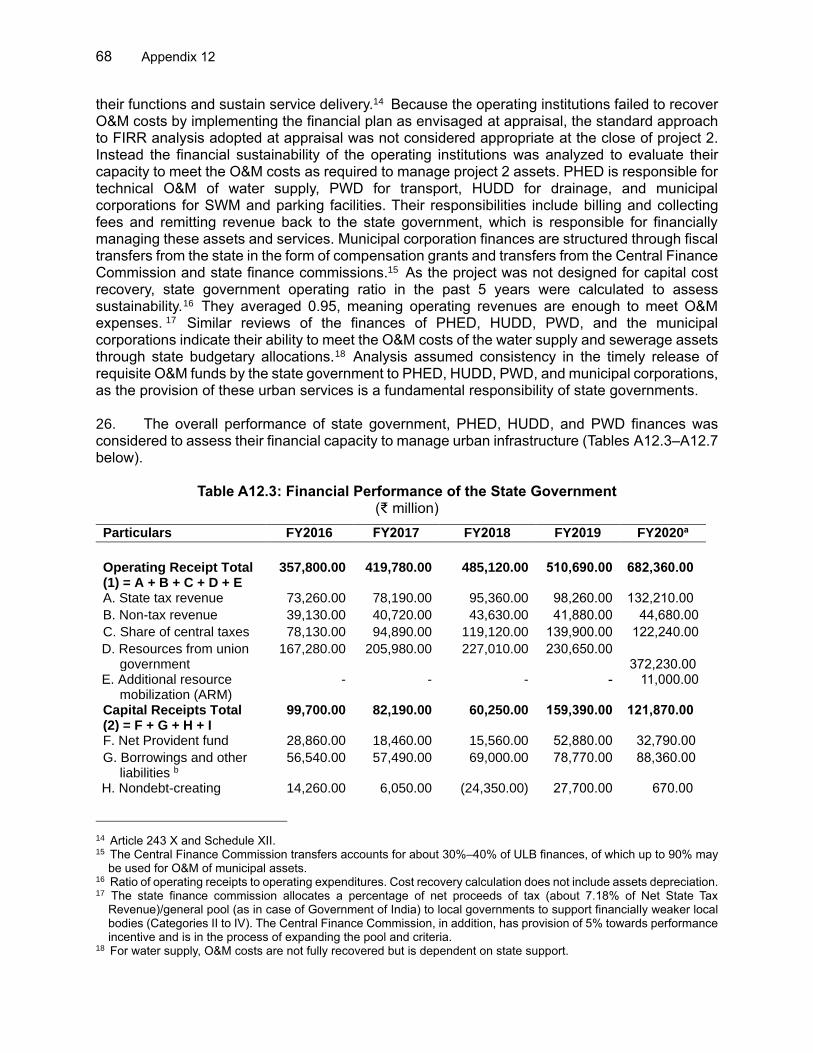

BASIC DATA i

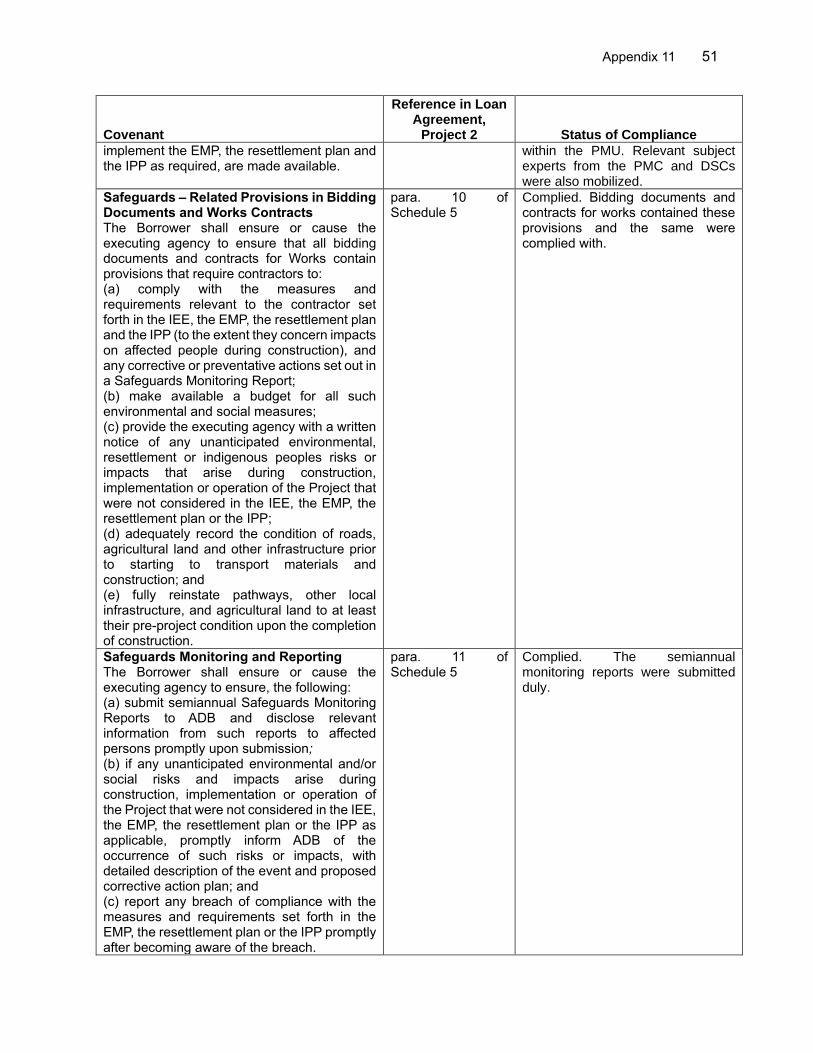

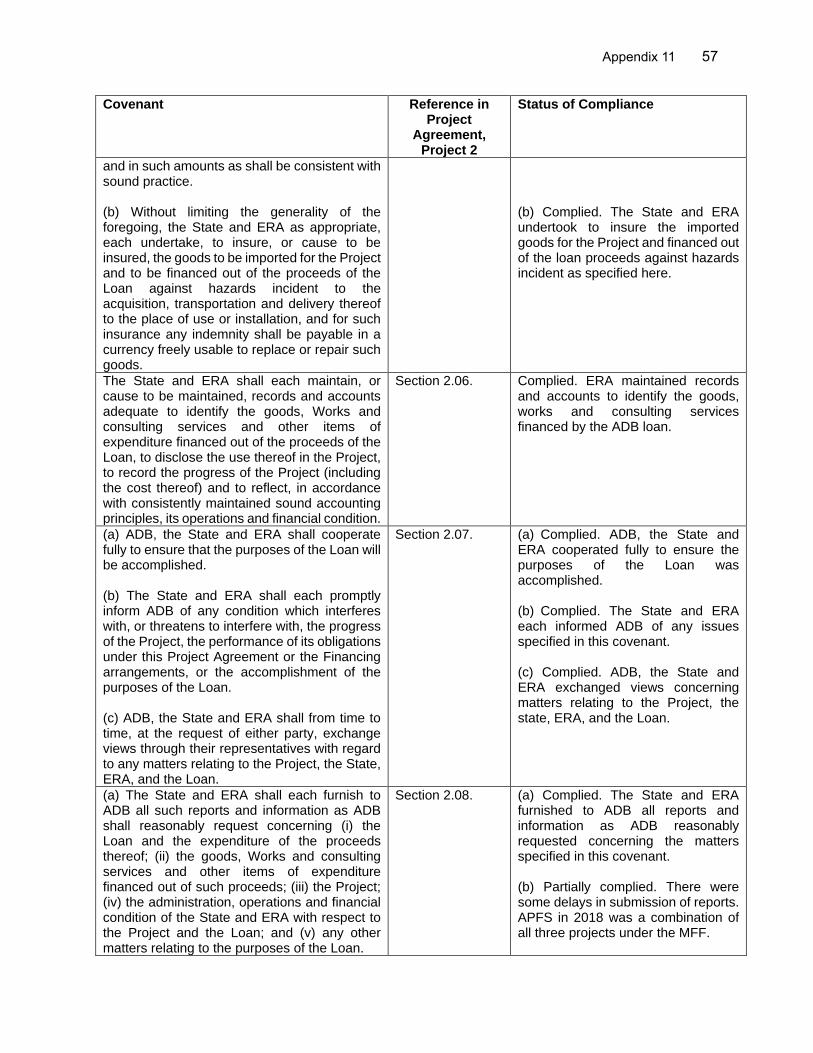

I. PROJECT DESCRIPTION 1

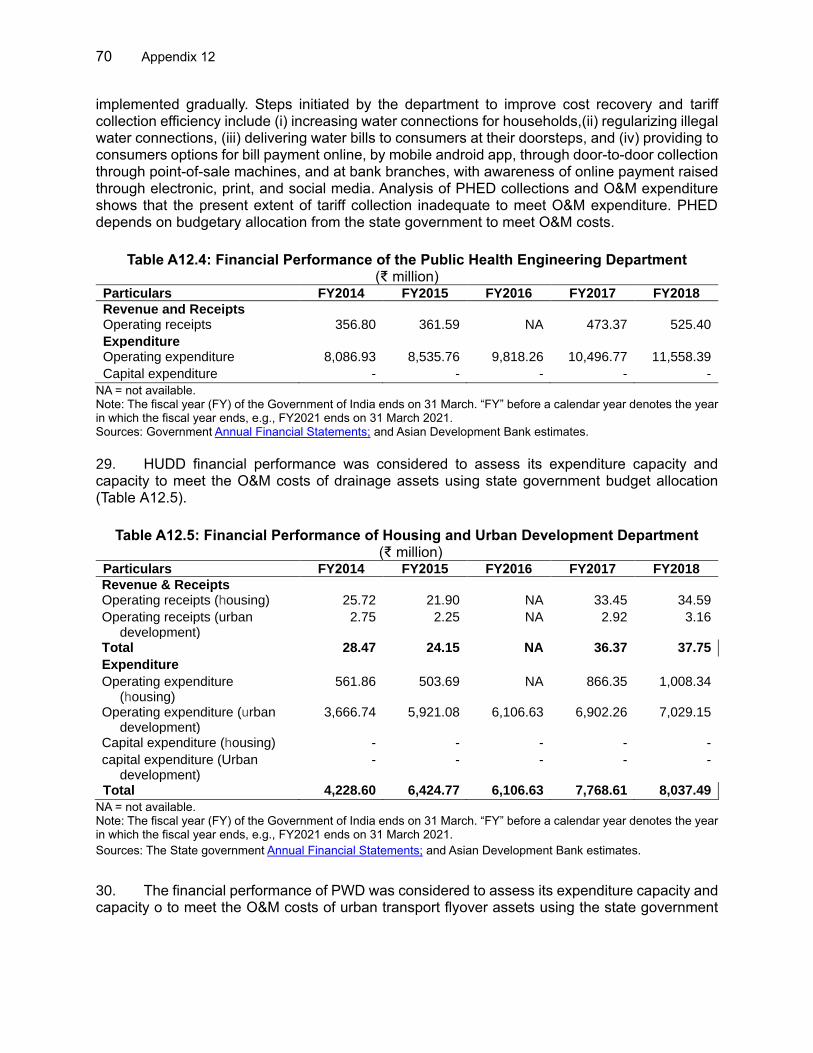

II. DESIGN AND IMPLEMENTATION 1

A. Project Design and Formulation 1

B. Project Outputs 3

C. Project Costs and Financing 5

D. Disbursements 5

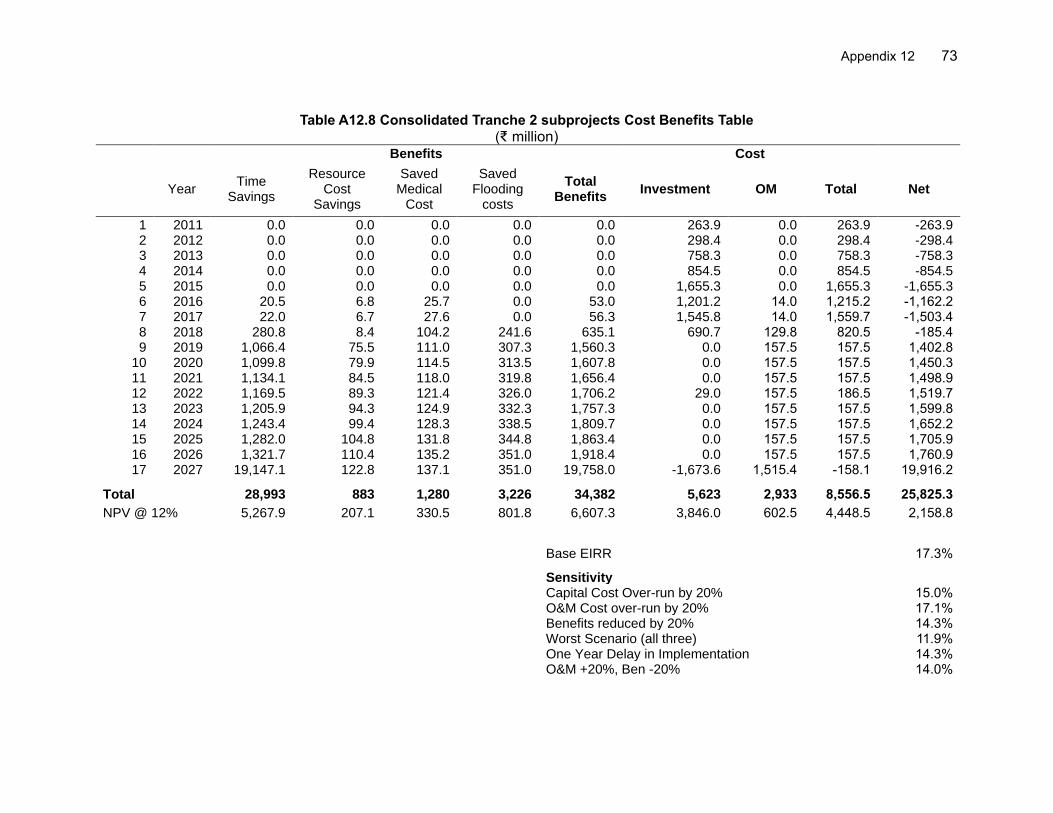

E. Project Schedule 6

F. Implementation Arrangements 6

G. Technical Assistance 6

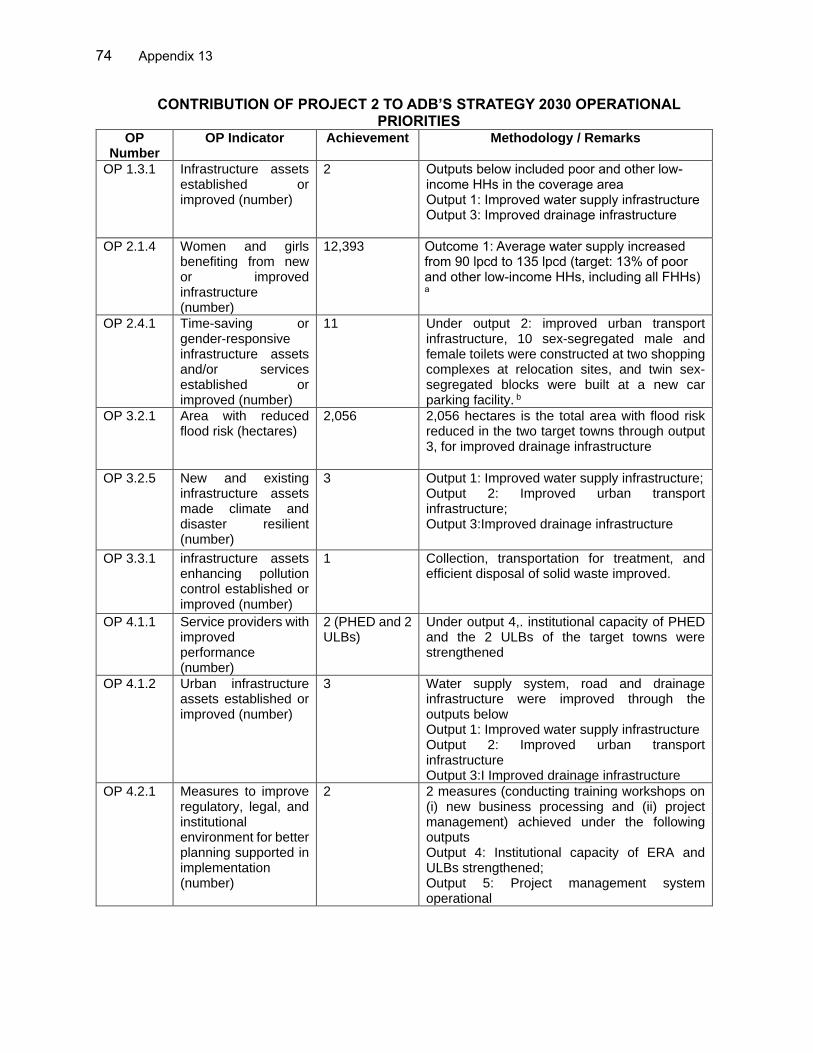

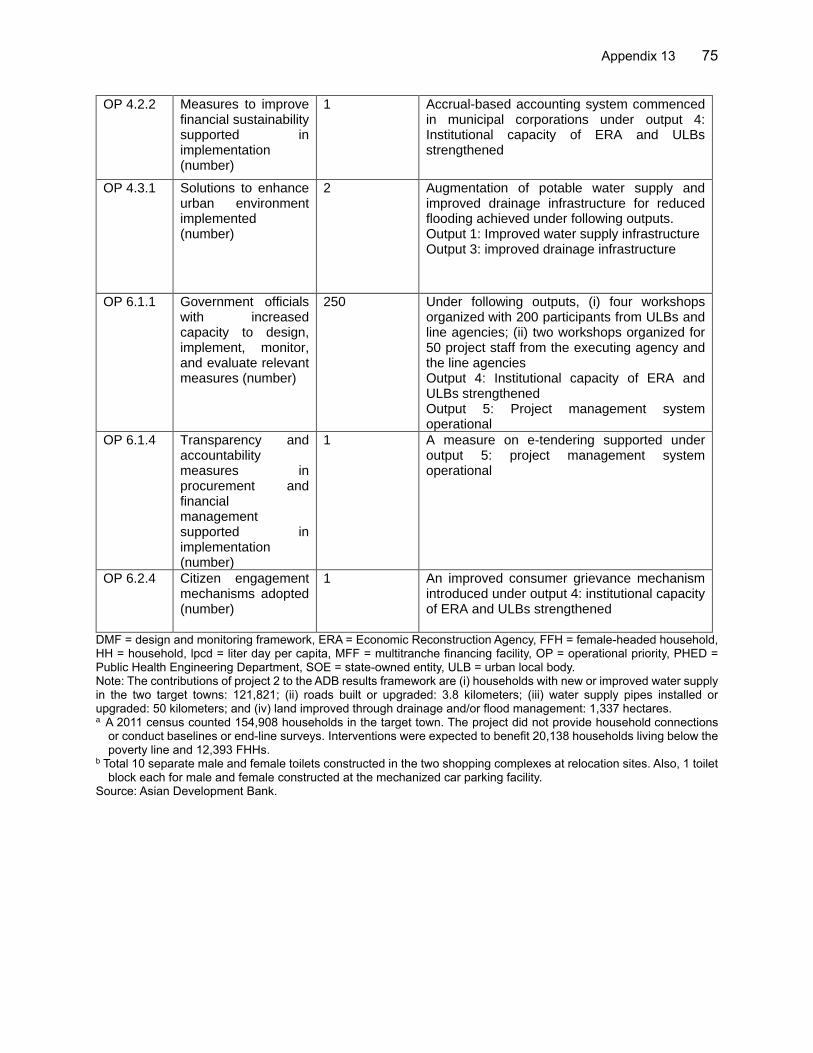

H. Consultant Recruitment and Procurement 7

I. Gender Equity 7

J. Safeguards 8

K. Monitoring and Reporting 9

III. EVALUATION OF PERFORMANCE 10

A. Relevance 10

B. Effectiveness 10

C. Efficiency 11

D. Sustainability 12

E. Development Impact 13

F. Performance of the Borrower and the Executing Agency 13

G. Performance of the Asian Development Bank 14

H. Overall Assessment 14

IV. ISSUES, LESSONS, AND RECOMMENDATIONS 15

A. Issues and Lessons 15

B. Recommendations 15 APPENDIXES

1. Design and Monitoring Framework For Project 2, with Weighting Factors to Determine Effectiveness 16

2. Status of Action Plan for Institutional Reform Programs 21

3. Project Cost at Appraisal and Actual 24

4. Project Cost at Appraisal and at Completion by Financier 25

5. Disbursement of ADB Loan Proceeds 27

6. Contract Awards of ADB Loan Proceeds 28

7. Chronology of Main Events 29

8. Summary of Contract Details 30

9. Implementation of Gender Action Plan and Achievements 33

10. Safeguards Assessments 43

11. Status of Compliance with Loan Covenants 48

12. Economic and Financial Analysis 62

13. Contribution of Project 2 to ADB's Strategy 2030 Operational Priorities 74

BASIC DATA A. Loan Identification 1. Country 2. Loan number and financing source 3. Project title 4. Borrower 5. Executing agency

6. Amount of loan 7. Financing modality

India 2925, ordinary capital resources Jammu and Kashmir Urban Sector Development Investment Program (Project 2) India Economic Reconstruction Agency $110 million Multitranche financing facility

B. Loan Data 1. Appraisal – Date started – Date completed

2. Loan negotiations – Date started – Date completed

3. Date of Board approval

4. Date of loan agreement

5. Date of loan effectiveness – In loan agreement – Actual – Number of extensions

6. Project completion date – Appraisal – Actual

7. Loan closing date – In loan agreement

– Actual – Number of extensions

8. Financial closing date – Actual 9. Terms of loan – Interest rate – Maturity (number of years) – Grace period (number of years)

26 March 2012 13 April 2012

28 September 2012 28 September 2012

26 October 2012

16 May 2013

14 August 2013 19 August 2013 0

31 March 2017 30 May 2017 31 March 2017 30 May 2017 1

8 February 2018 London interbank offered rate (LIBOR)-based (floating) + 0.60% 25 years 5 years

a Unfinished works were completed with government funding in March 2020. March 2020 is the starting point for an 18-month period by the end of which this project completion report must be circulated.

ii

10. Disbursements

a. Dates

Initial Disbursement

26 September 2013

Final Disbursement

25 October 2017

Time Interval

50 months

Effective Date

19 August 2013

Actual Closing Date

30 May 2017

Time Interval

45 months

b. Amount ($ million)

Category Original Allocation

1a

Increased during

Implemen- tation

2

Canceled during

Implemen- tation

3

Last

Revised Allocation (4=1+2–3)

Amount Disbursed

5

Net Undisbursed Balance (6=4-5)

I Base Cost

Component A: Urban Infrastructure and Environmental Improvements

Water supply 14.81 0.00 0.00 14.81 9.40 5.41

Sewerage, drainage, and sanitation

14.90 0.00 0.00 14.90 20.75 (5.85)

Solid waste management

2.01 0.00 0.00 2.01 1.81 0.20

Transportation and urban roads

47.08 1.07 0.00 48.15 34.16 13.99

Resettlement and land acquisition

0 0.00 0.00 0.00 0.00 0.00

Subtotal (A) 78.80 1.07 0.00 79.87 66.12 13.75

Component B: Capacity Building, Institutional Development, Governance, and Investment Program Support

Training and workshops

1.00 (1.00) 0.00 0.00 0.00 0.00

Consultancy support

11.90 (3.41) 0.00 8.49 8.66 (0.17)

Incremental administration, including computers, and peripherals

5.10 (0.04) (2.00) 3.06 3.52 (0.46)

Subtotal (B) 18.00 (4.45) (2.00) 11.55 12.18 (0.63)

II Contingencies 13.20 3.38 (13.00) 3.58 0.00 3.58

III Taxes and duties 0.00 0.00 0.00 0.00 0.00 0.00

IV Financing charges during implementation

0.00 0.00 0.00 0.00 0.00 0.00

Total 110.00 0.00 (15.00) 95.00 78.30 16.70 a From periodic financing request and loan agreement. b The undisbursed balance of $16.70 million was canceled at project completion.

iii

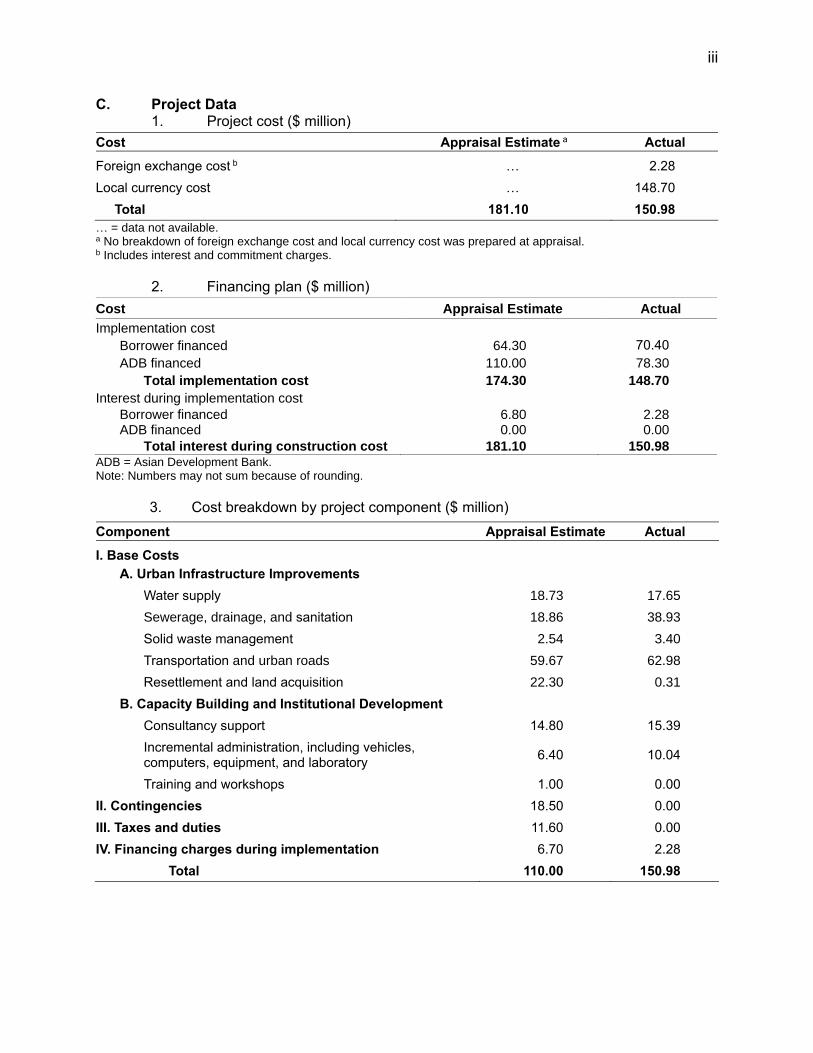

C. Project Data 1. Project cost ($ million)

Cost Appraisal Estimate a Actual

Foreign exchange cost b … 2.28

Local currency cost … 148.70

Total 181.10 150.98

… = data not available. a No breakdown of foreign exchange cost and local currency cost was prepared at appraisal. b Includes interest and commitment charges.

2. Financing plan ($ million)

Cost Appraisal Estimate Actual

Implementation cost

Borrower financed 64.30 70.40

ADB financed 110.00 78.30

Total implementation cost 174.30 148.70

Interest during implementation cost

Borrower financed ADB financed

6.80 0.00

2.28 0.00

Total interest during construction cost 181.10 150.98 ADB = Asian Development Bank. Note: Numbers may not sum because of rounding.

3. Cost breakdown by project component ($ million)

Component Appraisal Estimate Actual

I. Base Costs

A. Urban Infrastructure Improvements

Water supply 18.73 17.65

Sewerage, drainage, and sanitation 18.86 38.93

Solid waste management 2.54 3.40

Transportation and urban roads 59.67 62.98

Resettlement and land acquisition 22.30 0.31

B. Capacity Building and Institutional Development

Consultancy support 14.80 15.39

Incremental administration, including vehicles, computers, equipment, and laboratory

6.40 10.04

Training and workshops 1.00 0.00

II. Contingencies 18.50 0.00

III. Taxes and duties 11.60 0.00

IV. Financing charges during implementation 6.70 2.28

Total 110.00 150.98

iv

4. Project 2 Schedule

Item Appraisal Estimate Actual

Date of contract with consultants

Project management consultants Q1 2013 Q2 2013

Design and supervision consultants Q1 2013 Q1 2013

Capacity building and institutional support consultants Q3 2014 Q3 2014

Nonrevenue water reduction consultants Q1 2014 Q1 2014

Civil works contract

Date of contract award Q1 2013 Q3 2013

Completion of work Q4 2016 Q4 2019

Equipment and supplies

First procurement Q1 2013 Q1 2014

Last procurement Q3 2013 Q3 2014

Completion of equipment installation Q3 2015 Q3 2017

Start of operations

Completion of tests and commissioning Q3 2016 Q1 2020

Beginning of start up Q3 2016 Q1 2020a

Q = quarter.

a Works under water supply, transport, and drainage subprojects were not completed before financial closure, but the unfinished works were eventually completed in March 2020 with state government funding.

5. Project Performance Report Ratings

Implementation Period Single Project Rating

From 1 August to 31 December 2013 Potential Problem From 1 January to 31 December 2014 On track From 1 January to 31 December 2015 On track From 1 January to 31 December 2016 On track From 1 January to 31 December 2017 On track From 1 January to 31 March 2018 On track

D. Data on Asian Development Bank Missions

Name of Mission Date No. of

Persons No. of

Person-Days Specialization of

Members

Contact 14–17 Jul 2010 2 8 a, e

Contact 24 Apr–7 May 2011 6 84 d, c, a, g, j, k

Loan review 3 23–28 Jan 2012 2 12 d, f

Loan review 4/fact-finding 26 Mar–16 Apr 2012 7 154 d, r, g, a, d, s, t

Midterm review 1 22–26 Apr 2013 2 10 d, l

Special project administration

1–10 Jun 2013 3 30 d, a, l

Loan review 5 11–14 Jun 2013 2 8 e, u

Special loan administration 22–26 Oct 2013 2 10 a, l

Special loan administration 19–22 Nov, Apr 2013 2 8 l, g

Midterm review 2 10–17 Feb 2014 3 24 a, l, f

Loan review 6 21–25 Jul 2014 2 10 a, l

Loan review 7 17–24 Nov 2014 4 32 a, d, l, s

Special loan administration 15–17 Apr 2015 2 6 a, l

v

Name of Mission Date No. of

Persons No. of

Person-Days Specialization of

Members

Loan review 8 7–9 Sep 2015 2 6 a, l

Midterm review 3

Loan review 9

Loan review 10

Loan review 11

16–21 Nov 2015

4–11 Apr 2016

21–22 Nov 2016

27 Feb–1 Mar 2017

7

5

3

3

42

40

6

9

d, b, a, l, t, j, f

d, l, s, t, s

d, a, c

d, a, s

Loan review 12 18–22 Jun 2018 2 10 d, v

Loan review 13 26–30 Nov 2018 4 20 d, s, w, x

a = project implementation officer, India Resident Mission, b = financial/administrative analyst, c = resettlement specialist, d = urban development specialist, South Asia Urban Development Division, e = urban economist, South Asia Urban Development Division, f = project analyst, India Resident Mission, g = safeguard specialist, j = environmental specialist, l = associate project analyst, r = project counsel, s = consultant project specialist, t = gender consultant, u = transport specialist, v = country director, India Resident Mission, w = principal portfolio management specialist, x = urban specialist, India Resident Mission. Source: Asian Development Bank.

I. PROJECT DESCRIPTION 1. The Jammu and Kashmir Urban Sector Development Investment Program was designed to expand and upgrade urban services in the major urban areas of the state to Indian national and state standards. The focus was on providing an improved living environment to the population including the poor and other low-income segments. The program aimed to enhance public access to water supply, sanitation, drainage, and road facilities for more than 2.4 million people living in the state’s two main cities and other selected towns. It also aimed to modernize and streamline the planning, operation and maintenance (O&M), and administrative functions of the responsible city departments.1 2. The Asian Development Bank (ADB) approved the program as a multitranche financing facility (MFF) on 31 May 2007 at an estimated cost of $485 million. 2 The ADB loan was $300 million, and the Government of India/state government contributed $185 million. The second loan under the MFF (Loan 2925-IND, project 2) was approved on 26 October 2012, signed on 16 May 2013, and declared effective on 19 August 2013. 3 The estimated project cost was $181.1 million, covered by an ADB loan of $110.0 million, and a government contribution of $71.1 million. 3. The expected impact of project 2 was an improved living environment in Jammu and Srinagar (the target towns). The anticipated outcome was improved urban services in the target towns. The planned outputs were (i) water supply infrastructure improved, (ii) urban transport infrastructure improved, (iii) drainage infrastructure improved, (iv) project management system operational, and (v) institutional capacity of Economic Reconstruction Agency (ERA) and urban local bodies (ULBs) strengthened.

II. DESIGN AND IMPLEMENTATION A. Project Design and Formulation 4. Project 2 was designed in accordance with government and ADB sector strategies at appraisal. The project was closely aligned with India’s Eleventh Five-Year Plan (2007–2012), emphasizing improvement and augmentation of economic and social infrastructure and improved municipal services in urban areas.4 It was also consistent with the state government’s strategies in the country’s Eleventh Five-Year Plan to achieve national service standards for critical indicators of quality of life, by narrowing poverty and regional disparities and providing basic

1 Because urban local bodies (ULBs) such as municipal corporations had limited technical and operational experience,

the responsibility for basic urban services was shared as follows: capital works financed by external funding sources, including the Asian Development Bank (ADB), were planned, designed, and implemented by the state’s Economic Reconstruction Agency (ERA) on behalf of ULBs. O&M responsibility lies with the state’s: (i) Public Health Engineering Department (PHED) for water supply systems, (ii) Housing and Urban Development Department (HUDD) for sewerage systems; and (iii) ULBs for solid waste facilities and transportation. Each entity is also responsible for billing and fee collection, but the revenues are passed on to the state.

2 ADB. 2007. Report and Recommendation of the President to the Board of Directors for the Proposed Multitranche Financing Facility to India for the Jammu and Kashmir Urban Sector Development Investment Project. Manila.

3 The first loan (Loan 2331-IND, project 1) under the MFF was approved on 4 June 2007; the third loan (Loan 3132-IND, project 3) on 18 June 2014.

4 Government of India, Planning Commission. 2007. Eleventh Five-Year Plan, 2007–2012. New Delhi.

2

services.5 Project 2 also aligned with ADB’s country partnership strategy for India, 2009–2012 which highlighted the need to tackle interregional disparities; Urban Sector Strategy, 1999; and Strategy 2020 and its focus on poverty reduction and institutional strengthening.6 The project still aligns with Strategy 2030 and its operational priorities (OPs) by making cities more livable (OP4) with better access to urban basic services such as safe drinking water in national-standard quantity; strengthening governance and institutional capacity (OP6); addressing remaining poverty and reducing inequalities (OP1); accelerating progress in gender equality (OP2); and tackling climate change, building climate and disaster resilience, and enhancing environmental sustainability (OP3).7 5. The program’s design reflected ADB’s learning from urban projects in India and from an earlier urban sector loan to the state, which covered only a part of the large medium-term requirements for urban development by the state.8 The MFF aimed to meet the remaining priority needs. Project 2 ($181.1 million of a total program cost of $485.0 million) continued to address the infrastructure gaps and the capacity constraints at the respective agencies. ADB’s experience in India’s urban sector had shown that project sustainability hinged on three main imperatives:9 (i) selection of subprojects through extensive consultation with a wide range of stakeholders and a demand-driven approach; (ii) institutional development to ensure that adequate O&M funds are mobilized from internal resources and gradually transferred from the state to the responsible entities; and (iii) capacity building in service-delivery institutions with a view to adopting corporatized or commercially oriented operations that include user fees. These imperatives guided the selection of subprojects and ensured wide public input and suggestions from stakeholders. The subprojects implemented were the same as those identified at appraisal. 6. The modality of projects under an MFF was appropriate and effective in facilitating a long-term relationship between ERA and ADB.10 It suited the complex works in urban areas, which required flexibility in scope and longer implementation periods to coordinate multiple stakeholders. Further, it allowed flexible ADB support that factored in a climate with severe winters and frequent monsoon flooding. At appraisal, the design and monitoring framework (DMF) was prepared with adequate quality, defining the outcomes and outputs with sound results chain.11 The reform targets, however, were rather ambitious considering the state’s capacity and the local context (para. 13). Achievements are detailed in Appendix 1. 7. During implementation, some changes in project scope took place. Number of overhead water supply tanks to be built were reduced from 10 to 8 because of poor contractor performance. Similarly, the length of drainage to be rehabilitated was reduced from 28.3 km to 26.6 km because

5 State government, Planning and Development Department. 2007. Eleventh Five-Year Plan (2007–2012). New Delhi.

Project 2 was also consistent with the sector road map developed by the state in conjunction with the Jawaharlal Nehru National Urban Renewal Mission, through which the Government of India fast-tracks reform-driven development planning to modernize 63 major towns of India.

6 ADB. 2009. Country Strategy and Program: India, 2009–2012. Manila, ADB. 1999. Urban Sector Strategy. Manila, ADB. 2008. Strategy 2020: The Long-Term Strategic Framework of the Asian Development Bank, 2008–2020. Manila.

7 ADB. 2018. Strategy 2030: Achieving a Prosperous, Inclusive, Resilient, and Sustainable Asia and the Pacific. Manila. 8 ADB. 2004. Report and Recommendation of the President on a Proposed Loan to India for the Multisector Project

for Infrastructure Rehabilitation in Jammu and Kashmir. Manila (Loan 2151-IND, for $250 million, approved on 22 December 2004). That loan covered such urgent investment needs as rehabilitating water supply systems, and project 1 expanded these investments.

9 Summarized in ADB. 2006. Special Evaluation Study on Urban Sector Strategy and Operations. Manila. 10 ADB recognized the benefits of longer-term relationships through its earlier long-term support to urban sectors in

Karnataka and Rajasthan. 11 Impact indicators for project 2 were set to match the outcome indicators of MFF, to follow the guideline at appraisal.

3

of encroachment issues.12 The loan savings from these changes were partly reallocated in 2016 to the much-needed rehabilitation of 23 drainage pumping stations and 3.2 km of drainage (not a part of the project 2 at appraisal) damaged during the 2014 floods (para. 11).13 Also in 2016, as a result of currency depreciation, $15.0 million was canceled from the ADB loan.14 The skills training under the transport subproject was not implemented because of lack of interest from the affected households.15 While other due diligence was properly implemented, the design could have considered incorporating more comprehensive solutions, such as 24x7 water supply with O&M arrangements, into construction contracts. Also, the assessment at appraisal of the state’s capacity to implement the reform was rather optimistic, leading to delays in achieving some targets (para. 13).16 With these exceptions, the design was still relevant at completion since the development needs for basic urban services had not changed. No overlaps with interventions of other development partners emerged.17 B. Project Outputs 8. Of the 18 indicators for the 5 planned outputs of project 2, 14 were achieved, 2 were partially achieved, and 2 were not achieved.

1. Urban Infrastructure Improvements 9. Water supply. All four target outputs under this subproject were achieved or exceeded. Although only 50 km of distribution pipeline were rehabilitated by project completion, the remaining 17 km were completed with government funding in March 2020.18 The target of augmenting 23.5 million liters per day (MLD) potable water supply was substantially achieved—i.e., by 20.0 MLD—with the installation of 19 tube wells. The detailed design conducted during project implementation found that augmenting full 23.5 MLD was technically not feasible. The target of replacing 112 pumps and other electro-mechanical equipment was exceeded—project 2 replaced 148 pumps and other electro-mechanical equipment.19 The installation of 14 mobile water tankers and maintenance equipment was achieved as planned,20 and boosted the average water supply from 90 liters per capita per day (lpcd) to 135 lpcd (national standard).21 Also, an additional 10,200-people, against the target of additional 3,800 people, in low-income or poor households benefited from an increase in water supply from 20 lpcd to 70 lpcd (the national standard in areas without sewerage). Overall, project 2 gave 0.54 million people access to municipal water supply, albeit with delays.

12 As memo to approve these changes were not processed, the achievements are assessed against the original target. 13 Savings were also used to cover administration costs and to prepare subsequent projects under the facility. 14 Approved memo dated 15 February 2016. 15 The planned training (an output indicator) was to consist of workshops on artisanal and handicrafts work for 39

women members of shopkeeper households that had to be relocated during the flyover construction. The training needs assessment resulted in only four women expressing interest in livelihood training. The cost benefit analysis by ERA concluded that the training was not feasible to be conducted. Since no memo for this change of scope was prepared, this report assesses the achievement against the original indicator.

16 The state government’s capacity was gradually improved with capacity building throughout the MFF’s duration. 17 Project 2 was consistent with the sector road map developed by the state in conjunction with the Jawaharlal Nehru

National Urban Renewal Mission. 18 The works were not finished by the project’s completion despite the engagement of more subcontractors to expedite

the works due to inadequate contractor performance (para. 20). 19 While 7 additional pumps were also supplied, the replacement was not finished by project completion. 20 In addition, 2 pick-up or delivery vans, 1 suction-cum-jetting machine, and 1 backhoe loader were procured. One

package for 2 mobile water tankers and O&M equipment was terminated because of the supplier’s inability to execute the contract.

21 Government of India. 1999. Manual on Water Supply and Treatment. Delhi.

4

10. Urban transport. The five target outputs under this subproject were mostly achieved, although with delays. The construction of one flyover, including the upgrade of 2.5 km of roads was achieved only in part (62%) by project completion because of poor contractor performance and local unrest during implementation; the remainder was finished with government funding in July 2019. The construction of another flyover, including the upgrade of 1.3 km of road, were also achieved, although 7% was completed with government contribution after project completion. The delay was due to poor contractor performance. The targets achieved within the project duration were the construction of one mechanized car parking facility, and separate male and female toilet blocks at the facility and in the two relocation complexes. Notwithstanding the delays, it is assessed that the flyover corridors contributed to substantial savings in vehicle hours per day and benefited about 1.4 million people (para. 31). 11. Drainage. The three target outputs under this subproject were achieved, although with delays. First, the target to rehabilitate 28.3 km of drains were substantially achieved with 26.6 km (para. 7). Similarly, the target of building 10 km of new drainage was substantially achieved with 8.5 km with delay in September 2018 using the government funds. The balance was not implemented because of slow works progress.22 All targeted awareness generation campaigns on health, hygiene, sanitation, and the management of drainage systems were conducted. In addition, 23 drainage pumping stations, and 3.2 km of drainage damaged by the 2014 floods were rehabilitated (with loan savings resulting from the delays in the water supply and drainage subprojects) and completed in May 2017. Despite the delays, the achievements helped reduce water logging incidences and benefited about 1.4 million people. 12. Solid waste management. While no output targets were set for solid waste management (SWM), project 2 included a relatively small waste management component, i.e., the procurement of 34 modern waste collectors and 10 dumpers, among other equipment.23 These were procured as planned and being used. Together with the land fill sites developed under project 1, project 2 contributed to improved solid waste management with increases capacity.

2. Project Management and Institutional Capacity Strengthening 13. The achievements varied when it comes to the outputs of the project management and institutional capacity development component. Of the 6 output targets, 3 were achieved, 2 were partly achieved, and 1 was not achieved. Regarding project management, the target of timely project completion was not achieved because the water supply, drainage, and transport subprojects were not finished by project completion.24 The target of providing training workshops for at least 50 project staff at ERA and line agencies, with 20% female participation, was achieved as planned. As regards institutional capacity building, the target of training 100 ULB representatives; ward members; and 100 municipal, ERA, and line agency staff with (with 20% of them women) on new business processes was achieved.25 The partly achieved targets were the

22 Part of the work was subcontracted, with ADB concurrence, to overcome the slow progress. The subcontractor was

also a main contractor in another package with relatively good performance. 23 Other goods packages were: 4 rear-end loader compactors with 300 bins; 2 hook loaders and 10 containers; and

1,000 hand carts and 300 cycle rickshaws. 24 The capacity building consumed 28% of the total consultancy support recruited to implement the institutional reform

programs that were a part of the loan covenants and to prepare the subsequent project. The support was required because the state had limited resources for capacity building and institutional reforms. The positions of project management consultant (PMC) and design and supervision consultant (DSC) were filled with engineers and other design staff members to better meet the transport sector needs, consuming 72% of the consultancy cost.

25 This target was exceeded by 4 training units with 200 participants, including PHED and ULB staff, and 25% female participation. Ward members did not participate because no municipal election took place during project 2.

5

(i) adoption of accrual-based system by the municipalities, and published balance sheets from fiscal year (FY) 2015;26 and (ii) preparation and adoption of organizational development plans for semi-autonomous water supply entities by June 2013—achieved with delays in April 2015.27 The target of more efficient billing and collection by 2015 was achieved (although late) when the PHED introduced a computerized water billing system in 2019. 28 However, the target of procuring laboratory equipment for air and water quality monitoring by the State Pollution Control Board was not implemented as another source funded the equipment. Overall, it became evident that the reform targets were rather ambitious considering the state’s limited capacity and the local context, including frequent local unrest, which required a longer implementation period. Details of the institutional reform action plan are in Appendix 2. C. Project Costs and Financing 14. The estimated project cost at appraisal was $181.1 million, to be covered by an ADB loan of $110.0 million and a government contribution of $71.1 million. The cost of the water supply subproject at loan closure proved to be 37% ($5.4 million) less than the appraisal estimate, mainly because of slow works progress. The loan savings were partially reallocated to the drainage subproject to repair damages from the 2014 floods (para. 7), so the subproject required 39% or $5.8 million more funds than the estimated. The cost of the transportation subproject at loan closure proved to be 27% or $12.9 million less than the appraisal estimate because of unfinished works. Owing to currency depreciation, $15.0 million was canceled from the ADB loan; $16.7 million was committed but not utilized. This translated to a project cost of $150.98 million at completion, or an ADB loan of $78.3 million and a government contribution of $72.68 million. The main reason for the lower ADB loan amount was the depreciation of the rupee between the time of appraisal and the actual disbursement, with no contingency disbursement required. Estimate and actual project costs are shown in Appendix 3 and summarized by financier in Appendix 4. D. Disbursements 15. In the early stage of implementation, disbursement was slowed by the delays in procurement and works progress. The first disbursement was in August 2013 and by yearend, $4.7 million had been disbursed. In 2014, severe floods in the state limited the disbursement to $7.1 million against a projected $59.5 million at appraisal. Disbursement picked up to $16.3 million in 2015, rose to $21.8 million in 2016, and reached $28.4 million in 2017. On 8 February 2018 (financial closure), disbursement totaled $78.3 million or 82% of the revised loan amount of $95.0 million (71% of the original loan amount of $110.0 million). In December 2016, a reallocation of loan proceeds was approved to help ERA optimize the use of the loan amounts and to reduce the state’s anticipated financial burden from spillover works.29 At the financial closure in February 2018, the unutilized loan amount of $16.7 million was canceled. While the disbursement projection at appraisal was optimistic for the project start up (para. 16), the delay caused by the floods was unforeseeable.30 ADB received all withdrawal applications through the Controller of Aid Accounts and Audit of the Ministry of Finance, Government of India. The disbursement mechanism required

26 A double-entry accounting system was adopted and launched in the two ULBs. They prepared financial statements

until FY2017 but the practice did not continue after the consultant support ended at project’s completion in 2017. 27 While the state government issued an order in 2013 to transfer urban functions such as water supply and sewerage

to ULBs, a decision to create a semi-autonomous water board is still pending to date at the state legislature. 28 Other relevant improvements in the state’s efforts include the installation of bulk water metering and a supervisory

control and data acquisition (SCADA) system, computerized accounting at the PHED, approval of a new water tariff in 2020, and the formulation (with consultant support) of a revenue improvement action plan.

29 Approved memo dated 20 December 2016. 30 To mitigate the slow disbursement, the construction team took a sectional approach to the flyover works.

6

statements of expenditure and documented claims.31 All disbursement-related qualifications by the auditors were duly addressed. Projected and actual loan disbursements are in Appendix 5. E. Project Schedule 16. The original project completion date of March 2017 was extended once to May 2017—the maximum loan availability of the MFF.32 Major reasons of delay were (i) late procurement caused by contractor’s limited interest in working in an unstable local context and in severe winter, and limited state capacity; (ii) the persistently slow progress of civil works, which delayed disbursement; (iii) occasional public unrest; and (iv) 100-year floods in 2014. Local unrest has continually affected implementation. There were also issues with (i) ERA and state staff being overloaded with work on multiple large projects; (ii) delay in implementing the resettlement plan because of the slow construction of the state-funded relocation complexes, which also delayed flyover construction;33 (iii) delay in obtaining permission for the relocation of structures; and (iv) an overlap period of project 2 with then-ongoing project 1 and concurrent appraisals of project 3.34 The original loan closing date of 31 March 2017 was extended once, and the loan was eventually closed on 8 February 2018. The extension was required to optimize loan utilization, enable the completion of ongoing works to maximize project outcomes, and reduce the state’s financial burden from spillover works. The full completion of outputs with government contribution was in March 2020. A chronology of main events is in Appendix 7. F. Implementation Arrangements 17. The project implementation arrangements were as specified at appraisal. They were generally adequate to achieve the envisaged outputs, although later than planned. The executing agency was ERA, guided by state-level inter-ministerial support, city committees and a works finalization committee chaired by the division commissioner. ERA established a project management unit (PMU) for project 2 and implementation units in the target towns. While the PMU and implementation units were assisted by a project management consultant (PMC) and two design and supervision consultants (DSCs), the PMU in particular was overloaded with tasks for other projects (para. 16). The DSCs supported the preparation of detailed designs and bidding documents, the bidding process, and construction supervision. Also in place was capacity building and institutional support (CBIS) for the PHED and ULBs, as well as consulting services for a plan to reduce nonrevenue water (NRW). Safeguard consultants were mobilized for environmental and social aspects, including an external monitor for resettlement.35 G. Technical Assistance 18. The preceding ADB-funded project (footnote 8) was accompanied by a $0.5 million project preparatory technical assistance (TA) grant to prepare a comprehensive investment

31 The project benefited from a simplified statement of expenditure process that did not require the submission of

supporting documents for individual payments up to $100,000. 32 Approved memo dated 26 January 2017. 33 Project 2 should have started before 2013, but the slow construction of state-funded rehabilitation complexes meant

that ERA did not proceed until after the loan signing. 34 These issues of work overload were partially mitigated by staff increases in the project implementation units, and by

strengthening interagency coordination and project monitoring (para. 39). 35 A social safeguards unit at the PMU headed by the director of safeguards was responsible for the preparation and

implementation of resettlement plans, with support from the PMC and DSCs. ERA used a collector’s office for the preparation of land acquisition documents and payment of compensation to the affected persons. The Divisional Level Committee was responsible for determining the value of land during private negotiations with titleholders, or for compulsory acquisition where private negotiations failed.

7

plan.36 The TA supported the preparation of the MFF and of sector plans and policies to promote cost recovery through tariff reform. To further support ERA in implementing the MFF, ADB approved a $0.4 million TA in December 2006.37 The advisory TA helped ERA, especially in the early stages of the MFF, to (i) improve ERA’s functionality, (ii) build its project management and implementation capacity, (iii) expedite contract award and execution by providing guidance to ERA on procurement-related issues, and (iv) assist in setting and achieving yearly targets for contract award and disbursement. H. Consultant Recruitment and Procurement 19. Consultants were recruited in accordance with ADB Guidelines on the Use of Consultants (2010, as amended from time to time). ERA followed the quality- and cost-based selection procedure to select the PMC and one DSC, and the CBIS and NRW consultants. The contract of the first PMC recruited under project 1 was not extended at its completion in December 2011 because of weak performance. The recruitment of a new PMC took 17 months until May 2013 because the government process delayed the startup of project 2.38 Similarly, the contract of one DSC finished in December 2013, but a new DSC was recruited only in July 2014.39 Local engineering firms qualified for the large consulting contracts for flyover and drainage works. The overall performance of consultants is rated generally satisfactory. The newly recruited PMC and DSC performed substantially better than their predecessors. However, the delivery of their services was hampered by site constraints, design changes, and a delay in finalizing the drawings. The performance of the CBIS and NRW consultants was generally satisfactory. 20. Procurement followed ADB Procurement Guidelines (2010, as amended from time to time) and was generally carried out as planned, although with delays because of limited contractor interest and state capacity. The civil works packages for the two flyovers and the rehabilitation of drainage were procured through international competitive bidding. Remaining works packages were estimated to cost $10 million or less, and were procured through national competitive bidding. All works contracts were bills of quantity based on item rates. The preparation of standard bidding documents, bids evaluation reports, and contract agreements was in line with ADB guidelines. ADB’s prior review of all stages of bidding was conducted in accordance with the Procurement Guidelines. The contractors’ performance was unsatisfactory in the works for water supply, flyover, and drainage, which had to be completed with government contribution (paras. 9–11). The works for water supply distribution network and drainage did not improve even when subcontracting was allowed to overcome the slow progress. Although the PMU and implementation units held regular meetings with contractors to resolve hindrances, the three contracts proceeded slowly with persistent low workers deployment. The contractors’ performance in all other six work packages was satisfactory. I. Gender Equity 21. Project 2 was categorized effective gender mainstreaming. Broadly, the gender action plan (GAP) covered the: (i) provision of urban services to poor households headed by women; (ii) creation of income opportunities for unemployed family members, especially women, who had to

36 ADB. 2004. Technical Assistance for Preparation of the Jammu and Kashmir Urban Infrastructure Development

Project. Manila (TA 4515-IND, for $0.5 million, approved on 21 December 2004). 37 ADB. 2006. Technical Assistance to India for Strengthening Urban Project Management in Jammu and Kashmir.

Manila (TA 4888-IND, for $0.4 million, approved on 2 December 2006). 38 The gap between the two PMC contracts was covered by the DSCs. The original projections for the contract award

could have been more realistic in factoring in the risks of delay. 39 The performance of the other DSC was generally satisfactory, so the contract was retained until project completion.

8

be relocated during flyover construction and expanded civil works; (iii) development of women-friendly civil amenities to promote the safety of women and girls in the public transport system, (iv) promotion of health and hygiene-related practices; and (iv) promotion of community-led water conservation initiatives and women’s leadership in water supply management. 22. The GAP and the gender-related targets of the DMF were supported by a dedicated consulting firm. A gender specialist led the team of consultants at the firm that supported the consultation and participation plan; gender-focused awareness-raising, behavior change communications, and training programs; and community-based solid waste management activities. Social and resettlement experts, supported by the social and resettlement specialist of the PMC firm, provided supervisory support. They also assisted municipalities and other line departments implementing awareness-raising, community-mobilizing, and capacity-building activities. The project team collected sex-disaggregated data and regularly submitted the reports on GAP progress. Overall, progress and results were monitored and reported adequately. 23. The project completed 9 of the 10 GAP activities (90%), and achieved 13 of 14 (93%) combined quantitative targets of the GAP and DMF. This successful implementation and the gender-equality features contributed to significant practical and strategic gender benefits. They helped reduce the time poverty of women and alleviated the safety risks of faraway water collection by women and girls. The benefit of the water pipeline improvements positively impacted 13% of low-income households and 8% households headed by women in the target area. Of about 90,000 people covered by this subproject, 48% are estimated to be women and girls. The rehabilitation and construction of drains as per DMF outputs helped reducing water logging and flood risk for the population in the coverage area, including women and girls. The sex-segregated toilets at the relocation complexes and the parking facility contributed to the safety of women and girls. The awareness generation events with 50% women participants increased people’s knowledge of risks and hazards, and how to manage household water and sanitation. The project provided employment opportunities to women and ensured wage parity between men and women in construction and maintenance work. The provision in the project for stringent compliance with the law on wage parity was seen as a silver line for women workers. The women residents acknowledged that the pre-project consultations had given them confidence to raise their voice. This led to the construction of the drains factoring in their problems and concerns. J. Safeguards

24. Project 2 was classified category B for environment, category A for involuntary resettlement and category C for indigenous peoples, as per ADB’s Safeguard Policy Statement 2009 (SPS). The safeguard categorization was unchanged during implementation. An environmental assessment and review framework, resettlement framework, and indigenous peoples planning framework were prepared for the MFF but revised during loan processing to be consistent with the SPS.40 Initial environmental examinations were prepared for the subprojects under project 2 (Appendix 10) in accordance with the SPS, and government requirements. No significant environmental impacts were observed. The examinations showed that the impacts during operation are generally beneficial, while the construction impacts were reversible in nature (including traffic, noise, and dust) and could be adequately mitigated through good construction management. The examination findings and the environmental management plans formed an integral part of the bidding and contract documents, and included a grievance redress and

40 The SPS applies to tranches under the MFF for which ADB approved periodic financing requests after 20 January

2010. The subprojects under project 2 required compliance with the SPS, whereas project 1 was implemented under the former ADB safeguard policies for environment, resettlement, and indigenous people.

9

monitoring mechanism, as well as provisions for occupational and community health and safety. 25. Significant resettlement impacts were noted as part of one flyover subproject, for which a resettlement plan was prepared in consultation with stakeholders, reviewed, cleared, and disclosed by ADB and ERA on their websites and to affected persons. The resettlement plan envisaged an impact on 285 shops (257 shops operated by tenant and 28 owner operated shops). During the plan’s implementation, the impact on 25 shops was avoided by changing the alignment and/or engineering design. In all, 260 shops were rehabilitated. Of these, 99 shops rehabilitated by the municipality, and 161 were allotted to the shop operators in the two relocation complexes.41 Divisional Level Committee took two key decisions during the implementation:42 (i) affected persons were paid ₹1 million for the loss of residence (apart from all other entitled compensation); and (ii) the owners of the commercial establishment whose shops were operated by the tenants were given an additional compensation of ₹0.25 million. The tenants of affected shops were provided with new shops to continue their business and trade as before. Thus, all titleholders and non-titleholders were compensated in line with the provision of the resettlement framework and resettlement plan, and with the SPS.43 26. For the storm water drainage subproject, at Digiana, Gangyal areas, 35 affected persons and 1 temple trust (common property resource owner) were identified to face the loss of strips of land and minor structures such as boundary walls. Land ownership could not be established and is under investigation by the District Authority. A complaint was received by ADB from one affected person regarding non-receipt of compensation. ERA agreed to implement a corrective action plan by July 2021 to ensure compensation payments to all affected persons under the subproject. For all other subprojects in the targeted cities, the resettlement plan was implemented as proposed,44 and no indigenous peoples were affected. The safeguard compliance management—including institutional arrangements, information disclosure, consultations, grievance redressal, capacity building of project staff, and regular submission of semiannual safeguard monitoring reports—was rated generally satisfactory.45

K. Monitoring and Reporting

27. Of the 62 loan covenants of project 2, 52 were complied with, 7 were partially complied with, and 3 were not complied with. The partially complied covenants concern (i) the compensation payment to affected persons in the drainage subproject, (ii) unfinished works and institutional reforms by the project completion, and (iii) ERA’s pending submission of the project financial statement for FY2018 for disclosure by ADB. The covenants not complied with concern (i) the setup of semi-autonomous water supply entities, where the state government’s decision is still pending; and (ii) financial reporting (para. 28). Notable achievements of reform-related covenants include the empowerment of municipalities to collect property tax. The geographic information system developed under project 1 is used for the collection, while the complete rollout is yet to be achieved. Bi-annual environmental and social safeguard monitoring reports, including

41 91 shops were relocated to the Jehangir Chowk shopping complex and 70 shops were relocated to the Rambagh

shopping complex. 42 The state government constituted the Divisional Level Committee in May 2011 to fast-track the implementation of

the resettlement plan/s for subprojects being executed by ERA under project 2. 43 ADB’s aide-mémoire dated 26–30 June 2017 directed ERA to pay all pending compensation to shopkeepers affected

by the flyover construction. ERA confirmed that all payments due as per the final resettlement plan were paid except for 1 payment to an affected person who could not be traced, which was deposited in an escrow account.

44 ADB. 2020. Social Monitoring Report (March–August 2019): Jammu and Kashmir Urban Sector Development Investment Program – Tranche 2. Manila.

45 ERA, supported by the PMC and DSC, ensured adequate safeguard monitoring and management.

10

external monitoring reports on social safeguards, were submitted to ADB on time and duly disclosed. 28. The financial management arrangements of the borrower and executing agency were robust and counterpart funding was timely. Separate project financial accounts were maintained and audited by statutory auditors. Except for FY2018, audited project financial statements (APFS) were received, albeit with delays up to 3.6 months from the due dates but within the grace period of 6 months.46 The APFS for FY2018 were rejected because they included a combined audit report for all three projects despite the requirement for separate reports and opinions. Also, audited entity financial statements (AEFS) for fiscal yearend 2017 and prior years were combined with the APFS, all of which constituted noncompliance. Appendix 11 details the status of compliance with loan covenants.

III. EVALUATION OF PERFORMANCE A. Relevance 29. The project is relevant to government development objectives and ADB country and sector strategies, both at appraisal and completion (para. 4).47 Although the project predated ADB’s Strategy 2030, it is relevant to the strategy’s operational priorities (para. 4). At completion, the project remains aligned with the ADB policy focus for India on inclusive growth, infrastructure, and environmental sustainability. The project aligns with the government’s 5-year plans, the NITI Aayog’s 3-year action agenda (FY2018–FY2020), and the state’s Eleventh and Twelfth Five-Year Plans (FY2007–FY2018), which prioritized water supply in urban areas, wastewater management, and urban poverty alleviation.48 No development partner initiatives related to the project took place. 30. The MFF modality was appropriate considering the flexibility of moving outputs to other tranches without affecting the facility outcome, and the advantage of a longer engagement with the stakeholders. The DMF was ambitious in achieving reforms that were partly dependent on legislative engagement and capacity. The project results chain was nevertheless sound, and the indicators and the subprojects developed were generally appropriate to achieve the intended outcomes. While the project experienced delays in completion (para. 16), the state finished all the remaining works with its own funds49. The loan savings were utilized to respond to emerging needs such as the rehabilitation of the drainage pumping stations damaged by the historic floods of 2014, yielding enhanced outcomes. ADB loan proceeds were reallocated to maximize the outcome. B. Effectiveness

31. Project 2 is rated effective in achieving the outcome and output targets. Of the five outcome targets, four were achieved although with delay (para. 16) and one was not achieved. Weighing the indicators against the actual cost of each component, the degree of overall achievement of outcome targets was assessed at 87% (Table A1.2). The target towns benefitted

46 Late by 0.8 months for FY2014, 3.6 months for FY2015, 2.2 months for FY2016, and 2.9 months for FY2017. 47 Government of India, National Institution for Transforming India (NITI) Aayog. 2012. Twelfth Five-Year Plan, 2012–

2017. Delhi; and ADB. 2013. India: Country Partnership Strategy (2013–2017). Manila. 48 NITI Aayog is a policy think tank of the Government of India that provides directional and policy inputs. Government

of India, NITI Aayog. 2017. India Three-Year Action Agenda, 2017–2018 to 2019–2020. Delhi; and State government, Planning Department. 2012. Eleventh and Twelfth Five-Year Plans, 2007–2018. Delhi.

49 There was also weakness in project design (para. 7) that led to delays in achieving outputs.

11

from the project with the increased (i) average water supply from 90 lpcd to 135 lpcd (national standard) as expected at appraisal; and (ii) access to potable water supply of 70 lpcd (national standard for areas without sewerage) for an additional 10,200 people against the target of 3,800 people. These contributed to the 14% weighted achievement of water supply outcome. (iii) Project 2 was also planned to increase volume of solid waste collected and disposed to 375 tons per day. While all the collection equipment were procured as planned and are being used, there is absence of data to verify the achievement, resulting to 0% weighted achievement. (iv) While not assessed quantitatively, it is assumed that the target towns also benefitted from reduced water logging. As per ERA’s validation, there was no reported incidence of inundation in the target areas.50 This contributed to 31% weighted achievement of drainage outcome. (v) The project was also expected to reduce travel time with average vehicle-hours saved per day by 8,600 and 4,326 in the flyover corridor of the two target towns. This was substantially achieved as communities confirmed that the travel time was reduced by around half and contributed to weighted achievement of transport outcome of 41%.51 These outcome achievements in all the urban infrastructure improvements were directly attributable to the subprojects’ achieved outputs. 32. As for the outputs, the weighted achievement of targets based on costs was 90% (Table A1.2).52 The weighted achievements per urban infrastructure subprojects are 13% for water

supply, 39% for transport, 25% for drainage, and 2% for solid waste management (paras. 9–12).53 These output achievements in all the urban infrastructure improvements directly contributed to the subprojects’ achieved outcome. Out of the 6 output targets for institutional capacity development and project management, 2 were achieved, 3 were partly achieved and 1 was not achieved (para. 13), resulting in the 10% weighted achievement. Safeguards were implemented effectively, and no adverse effect from the project was observed. Environmental safeguards mitigation measures were implemented effectively, and no adverse effect from the project was

observed (para. 24). Resettlement plans were prepared and implemented as planned (paras. 24–26). Gender action plans were satisfactorily implemented, and targets were substantially achieved

(paras. 22–23). C. Efficiency 33. Project 2 is rated efficient. The overall economic internal rate of return (EIRR) is above ADB’s threshold. The large implementation delays and associated cancellation of ADB loan are considered in the EIRR calculation. The EIRRs at completion of the major subproject components were recalculated against their appraisal estimate. The EIRRs at completion for the two water supply components were assessed at 12.2% for water supply system and 8.5% for PHED’s equipment for water supply, compared with the appraisal estimates of 13.3% and 13.0%.54 For the three drainage components, the EIRRs at completion were assessed as 14.1%, 22.1%, and

50 Constraints posed by the coronavirus disease (COVID-19) limited the gathering of data for this completion report. 51 A traffic volume survey was not conducted at the project completion given the challenges posed by COVID-19.

Alternatively, the contribution of flyovers to reduce travel time was confirmed by the communities through selected interviews.

52 Of 18 outputs in the DMF, 14 were achieved, 2 were partly achieved, and 2 were not achieved. 53 Captured in the weighted achievements of outputs are the goods provided to collect solid waste, such as waste

collectors and dumpers, which were not included in the DMF. 54 Field missions and discussions with households to update the willingness-to-pay survey were not possible because

of local unrest and travel restrictions imposed during the COVID-19 pandemic. In both subprojects, the intended benefits were realized, but the EIRR at completion is lower than at appraisal because of cost and time overruns.

12

9.8%, compared with the appraisal estimate of 22.0%, 13.6%, and 15.4%.55 For the two flyover components, the EIRRs at completion were assessed at 15.6% and 14.1%, compared with the appraisal estimates of 13.9% and 14.9%.56 For solid waste management subproject, the EIRR at completion was assessed as 24.7%, higher than the appraisal estimate of 17.8%. For the parking facility, the EIRR at completion was assessed at 13.4%, slightly above the appraisal estimate of 13.1%. Except for one drainage component and the PHED’s equipment for water supply, all other re-evaluated subprojects have EIRRs near or above the benchmark of 12% at completion, justifying the investments. The EIRRs of the drainage and PHED equipment components fell below the threshold for economic viability at appraisal because of cost overruns and implementation delays. Several indirect and direct benefits, such as an improved environment and better quality of life, could not be quantified and were not captured in the analysis. However, the qualitative assessments demonstrate the direct or indirect contribution to an improved urban environment and better quality of life. The overall EIRR for project 2 at completion was assessed at 17.3%, although it was not assessed at appraisal. The economic net present value of all the completed subprojects was positive, except for one drainage and one water supply component, when applying the 12% discount rate. The undisbursed ADB loan amount was $16.7 million at project completion. The institutional efficiencies and the grievance redress mechanisms developed by ERA reduced transaction costs and improved transparency and governance accountability while significantly augmenting ERA’s administrative capacity. The project experienced delays due mostly to uncontrollable factors as severe weather conditions and public unrest. There was only one extension (March 2017 to May 2017) to optimize loan utilization to complete ongoing works, thus reducing state’s burden from spillover works. These factors are considered in the economic analysis. Details are given in Appendix 12. D. Sustainability 34. Project 2 is rated likely sustainable. The Constitution of India mandates the states to allocate the funds required to maintain their functions and sustain service delivery.57 Since the operating entities are not recovering the operation and maintenance (O&M) costs as planned, the standard approach to computing the financial internal rate of return adopted at appraisal, was not considered appropriate at project completion. Instead, a financial sustainability analysis of the operating entities was carried out to evaluate their capacity to meet the O&M costs required to manage the project 2 assets. The responsibility for the O&M of infrastructure assets lies with the PHED (water supply), Public Works Department (PWD, transport), Housing and Urban Development Department (HUDD, drainage), and ULBs (solid waste management and parking). Their responsibilities include billing and fee collection, and remitting the revenues back to the state, which is responsible for financially managing these assets and services. For ULBs, finances are structured through fiscal transfers from the state as grants and transfers from the central finance commissions and state finance commissions.58 Since the project was not designed for capital cost recovery, the operating ratio of the state government in the past 5 years was calculated to assess the project sustainability.59 The ratio averaged 0.95, meaning that the

55 For all three components, the intended benefits were realized. For one component, the EIRR at completion is higher

than at appraisal thanks to cost reductions. In two other components, it is lower than at appraisal because of cost and time overruns. In one component, 1.3 km of new drains were built even though this was not in the original scope.

56 The intended benefits of both flyovers were realized. In one case, EIRR at completion is higher than at appraisal because of lower costs. In the other case, it is lower than at appraisal because of cost and time overruns.

57 Constitution of India. Article 243 Schedule X and XII. 58 The Central Finance Commission transfers for 30%–40% of ULB finances, of which up to 90% may be used for the

O&M of municipal assets. 59 Ratio of operating receipts to operating expenditures. The cost recovery calculation does not include the depreciation

of assets.

13

operating revenues are sufficient to meet the O&M expenses.60 A similar review of the overall finances of the PHED, HUDD, PWD, and the ULBs indicates their ability to meet the O&M cost through state budgetary allocations.61 The analysis assumed the timely release by the state of the requisite O&M funds since the provision of these services is a fundamental duty of the state government. The details of the financial re-evaluation are in Appendix 12. 35. Institutional capacities, including on social and gender dimensions, were strengthened by the ongoing reforms and implemented under the MFF, such as door-to-door collection of municipal solid waste, O&M of (i) the parking facility by a ULB;62 (ii) new water treatment system by the PHED; (iii) flyovers by the PWD; and (iv) drainage improvements by HUDD. Billing and collection of water supply were also improved through online payment system. While the PHED, PWD, and HUDD have sufficient human resources and technical institutional capacities for O&M, the ULBs of the target towns require continuous strengthening of human resources and institutional capacities for better asset management and governance. E. Development Impact 36. The development impact of project 2 is rated satisfactory. It benefited 0.54 million people with access to municipal water supply services, contributing to the MFF’s target of 2.2 million people.63 The functional drainage system benefited 1.4 million people and contributed to the facility’s target of 2.0 million people. Access to better road infrastructure benefited 1.4 million people and contributed to the facility’s target of 2.4 million people. The sanitation component for a sewage treatment plant was not pursued, and therefore did not contribute to the facility’s planned target of 1.0 million people.64 The implementation of the GAP resulted in some strategic gender benefits in the core area of gender equality in human capital development. The project contributed to stronger financial management by the ULBs and the PHED. Contributions to ADB’s Strategy 2030 are listed in Appendix 13. The project’s environmental and involuntary resettlement impacts are as assessed in paras. 24–26 and Appendix 10.

F. Performance of the Borrower and the Executing Agency 37. The performance of the borrower and the executing agency is rated satisfactory. The borrower, represented by the Indian Department of Economic Affairs, provided timely guidance and decisions to the state government and undertook regular tripartite review meetings with ADB, the state government, and ERA. This helped identify bottlenecks, resolve issues, and monitor progress. The state government gave ERA strong support, including timely counterpart funding, not least to complete the unfinished works after the project’s completion. 38. The PMU continued its overall project management and implementation structure from project 1. To mitigate the work overload (para. 17), project implementation staff was increased during project 2. Interagency coordination, monitoring, and progress reporting from the field was also strengthened. These efforts partially improved the disbursement (para. 15). The floods in 2014 hampered project implementation, but ERA worked efficiently to restore the ongoing works.

60 The state allocates a percentage of net tax proceeds to local governments to support financially weaker local bodies. 61 ERA confirmed that the state has been allocating necessary O&M budget in a timely manner in the past. 62 For the parking facility, the operating agency is collecting the car parking charges at ₹20 per hour or ₹1,000 per

month. This contributes to the recovery of O&M costs. 63 In the target towns, population benefited from potable water supply reached 2.4 million in 2017, while this is due to

the MFF as well as other government projects. The state government. 2020. Digest of Statistics, 2017–18. Jammu. 64 The sewerage treatment plant was nor pursued under project 2 as it was not part of the master plan for larger

wastewater issue in the town and lacked a viable O&M plan.

14

The PMU handled safeguard compliance and monitoring requirements well and submitted timely monitoring reports to ADB. Other than the pending compensation payment to land and asset owners under the drainage subproject, no major issues arose through the complaint mechanisms. Minor concerns related to construction were handled in a timely manner. The PMU successfully constructed two relocation complexes and relocated 161 shops (para. 25). The APFS for FY2018 were rejected for having a combined audit report for all three projects. This was noncompliant with loan covenants and indicates that ERA financial management was less than satisfactory. With two exceptions (incomplete institutional reforms and incomplete compensation payment), all other loan covenants were complied with (Appendix 11). G. Performance of the Asian Development Bank 39. ADB’s performance is rated satisfactory. ADB missions for regular review, midterm review, and special project administration were undertaken to assess progress, provide advice for resolving outstanding issues, and facilitate minor changes in scope, optimizing the utilization of project 2 loan amount through reallocation of loan proceeds. ADB monitoring, capacity building, and guidance through 20 missions and 12 tripartite reviews throughout the project cycle helped define processes, address issues through time-bound actions and targets, and expedite project implementation. ADB provided training on procurement guidelines, disbursement, and safeguards. On the other hand, the project implementation schedule during appraisal and processing proved to be overly ambitious and should have more realistically considered the time required to implement ADB financed projects especially given the lessons from the previous ADB loans in the state. ADB’s financial management was less than satisfactory in that ADB could have followed up with ERA on compliance with APFS and AEFS requirements. H. Overall Assessment 40. Project 2 is rated successful. It was relevant to government development objectives and ADB policies at appraisal, and was still relevant upon completion. Changes to components were timely and appropriate. The project is assessed effective because weighted achievement of the overall outcome targets was assessed at 87%. The project is rated efficient with an overall EIRR assessed at 17.3%. The project is rated likely sustainable, because O&M costs for project assets are met through statutory transfers from state and central finance commissions, municipal taxes, and user charges.

Table 1: Overall Ratings

Criteria Rating

Relevance Relevant

Effectiveness Effective

Efficiency Efficient

Sustainability Likely sustainable

Overall assessment Successful

Development impact Satisfactory

Performance of the borrower and executing agency

Satisfactory

Performance of the Asian Development Bank

Satisfactory

Source: Asian Development Bank estimates.

15

IV. ISSUES, LESSONS, AND RECOMMENDATIONS A. Issues and Lessons 41. The following important lessons emerged from the project. First, enhancing readiness at loan approval by having detailed designs, would help deliver projects in a timelier manner.65 Second, the establishment of a land acquisition collector’s office within the PMU proved extremely beneficial in coordinating involuntary resettlements. Third, MFFs impose a burden on executing and implementing agencies in the initial years as they prepare for subsequent tranches while also being responsible for implementing the ongoing project, which requires sufficient implementation support. Fourth, the ambitious reform agenda required more time given the local context and the state’s capacity. Fifth, continued budget transfer from the state to the line departments for the O&M cost is necessary for sustainability until the line departments can recover the O&M cost through its operation. Sixth, the project schedule should be realistic in terms of consultant recruitment, detailed design development, and contract periods. Seventh, the subprojects' scope should be more outcome-oriented, including end-to-end solutions, such as 24x7 water supply or 5–10 years O&M arrangement in construction contracts, subject to the capacity of the asset operator. Finally, ADB should monitor compliance with APFS and AEFS submission requirements.

B. Recommendations

42. Specific recommendations for project implementation are as follows. First, the PMU should be supported by consultants specialized in reforms and policy formation to push the agenda. Second, a robust assessment of circumstances is needed at appraisal—how achievable are the planned institutional reforms and how much time needs to be allotted in light of government capacity and local context (para. 16). Third, ADB interact closely with executing and implementing agencies to ensure that robust financial management systems are maintained throughout project implementation (para. 28).66 The inclusion of an ADB financial management staff member in the team that monitors and supports the executing and implementing agencies—even with missions where necessary—is key to improving financial management performance and ensuring that funds are used for the purposes intended. Fourth, to sustain the good practices in promoting gender inclusive in urban development, ERA should take forward the similar practices in the design and implementation of their projects. 43. General recommendations for MFF and project preparation are: (i) the project scope and implementation period should be realistic in projects with multiple stakeholders and extreme weather conditions; (ii) initiatives to strengthen the financial management capacity of the executing and implementing agencies and systems should be defined clearly to ensure the agencies’ ability to use, monitor, account, and report ADB’s funds; and (iii) social and gender targets on beneficiaries based on empirical baseline surveys should be included, and mid-course adjustments on the targets should be carried out, in the face of the changes on the ground.

65 Land was identified for construction of the two rehabilitation complexes prior to loan approval. ADB funding for the

construction may have been explored for better monitoring and faster completion of the facilities. 66 While letters or official communications from ADB to the executing agency were forthcoming for every financial report

received (annually), it is important for the project team to closely monitor and follow up the executing agency’s response to the recommendations and comments, to confirm that these were understood by the appropriate units preparing the reports, including the auditors, and that they will be acted upon or applied to their subsequent reports.

16 Appendix 1

DESIGN AND MONITORING FRAMEWORK FOR PROJECT 2, WITH WEIGHTING FACTORS TO DETERMINE EFFECTIVENESS

Table A1.1: Design and Monitoring Framework for Project 2

Design Summary

Performance Targets and Indicators

with Baselines Project Achievements of Project 2a

Impact Improved living environment in Jammu and Srinagar

By 2020: Increased population coverage of infrastructure and services;b 2.2 million people with access to municipal water supply scheme

By 2020: A total of 2.4 million people had access to municipal water supply scheme through the MFF intervention; of which 540,000 directly benefited from project 2.

1.0 million people with access to proper sanitation

The sanitation component (online sewerage treatment plant) was not pursued under project 2.c

2.0 million people served by a functional drainage system

1.4 million people are served by functional drainage system.

2.4 million people with access to better road facilities

1.4 million people had access to better road facilities.

Outcome Improved urban services in Jammu and Srinagar

By the end of investment program: Average water supply increased to 135 lpcd from 90 lpcd (target: 13% of low-income/poor HHs [incl. all FHHs]) (Baseline= 90 lpcd for 120,000 households in 2011)

By the end of the investment program: Achieved. Average water supply increased to 135 lpcd from 90 lpcd for 120,000 households, or 13% of poor and other low-income HHs including all FHHs.

Additional 3,800 people in Srinagar (target: 13% of low-income/poor HHs [incl. all FHHs]) have access from potable water supply of 70 lpcd. (Baseline = 20 lpcd supply in 2011 for project area)

Exceeded. 10,200 people in the target town (13% of low-income/poor HHs [incl. all FHHs]) benefitted from having access to potable water supply of 70 lpcd.

Increased volume of solid waste collected and disposed to 375 metric tons/day (Baseline= 250 MT in 2011)

Not achieved. All the goods were procured and being used as planned. However, in the absence of data of the volume of solid waste collected, the achievement is assessed as not achieved,

Water logging reduced to 0.5 hours for 2 days/year in the project area of Jammu and 0.3 hours for 1 day/year in the project area of Srinagar (Baseline = In Jammu-2.5 hours for 10 days in a year, and in Srinagar – 2 hours for 30 days in a year).

Achieved. Per confirmation from ERA, there was no incidence of inundation since project completion.d

Appendix 1 17

Design Summary

Performance Targets and Indicators

with Baselines Project Achievements of Project 2a

Vehicle-hours saved per day to average 8,600 with the Srinagar flyover corridors and 4,326 with the Jammu flyover corridor (Baseline:13,656 vehicle-hours per day in Srinagar and 7,843 in Jammu in 2011)

Substantially achieved. With the construction of flyovers, the vehicle-hours (travel time) for users were reduced by half.d

Outputs 1. Improved water

supply infrastructure

By December 2016: 1. 67 km water pipelines rehabilitated

(coverage area includes 13% low-income/poor HHs [incl. all FHHs])

1. Achieved with delay in March 2020. 67 km

of water pipelines were rehabilitated, of which 50 km were completed under ADB financing and the rest were rehabilitated using state funds. Coverage area included 13% of low-income HHs, including all FHHs.

2. 23.5 MLD potable water supply augmented

2. Substantially achieved. Augmentation by 20 million liters per day was achieved by developing 19 tube wells, replacing 148 pumps and other electro-mechanical equipment, and providing 14 mobile water tankers.

3. 112 pumps and other electro-mechanical equipment replaced

3. Exceeded. 148 pumps were replaced, as was other electro-mechanical equipment. 7 additional pumps were supplied, not fully before the project closure.

4. 14 mobile water tankers and maintenance equipment installed

4. Achieved. 14 mobile water tankers were supplied as planned, as was other maintenance equipment.

2. Improved urban transport infrastructure

By December 2016: 1. 1 elevated expressway /flyover

constructed and 2.5km roads upgraded in Srinagar

1. Achieved with delay in July 2019, with 38%

being completed by the state fund after loan closure.

2. 1 elevated expressway /flyover constructed and 1.3km roads upgraded in Jammu

2. Achieved with delay in May 2018, with 7% completed using state funds after loan closure.

3. 1 off-street mechanized car parking facility constructed in Srinagar

3. Achieved. 1 off-street mechanized parking was developed that can accommodate 288 light motor vehicles at a time.

4. At least 1 separate male and female toilet blocks in every shopping complex at relocation sites and mechanized car parking facility

4. Exceeded. 10 male and female segregated toilets were constructed in the two shopping complexes at relocation sites. Also, 1 toilet block each for males and females was constructed at the mechanized car parking facility.

18 Appendix 1

Design Summary

Performance Targets and Indicators

with Baselines Project Achievements of Project 2a

5. Conduct 5 skills training workshops on artisanal and handicrafts work for women family members of shopkeepers relocated due to flyover construction at Jehangir chowk (target: 39 women from 39 families)

5. Not achieved. Efforts were made but the trainings could not be conducted as not many women family members relocated by flyover construction showed interest in receiving it.

3. Improved drainage infrastructure

By December 2016: 1. 28.3 km of drains rehabilitated

(coverage area includes 13% low income/poor HHs)

1. Substantially achieved. 26.6 km of drains

was rehabilitated in a coverage area that includes 13% of poor and other low-income HHs. Balance 1.7 km was not implemented due to encroachment.

2. 10 km of new drains/drainage channel constructed.

2. Substantially achieved with delay in September 2018. 8.5 km of new drains and a drainage channel constructed including around 3.3 km completed by the state fund.