Embed Size (px)

Citation preview

3Q FY2012(Fiscal Year Ending March 31, 2013)

Financial Results Presentation

February 1, 2013

Eisai Co., Ltd.

2

Safe Harbor Statement

• Materials and information provided during this presentation may contain so-called “forward-looking statements.” These statements are based on current expectations, forecasts and assumptions that are subject to risks and uncertainties which could cause actual outcomes and results to differ materially from these statements.

• Risks and uncertainties include general industry and market conditions, and general domestic and international economic conditions such as interest rate and currency exchange fluctuations. Risks and uncertainties particularly apply with respect to product-related forward-looking statements. Product risks and uncertainties include, but are not limited to, technological advances and patents attained by competitors; challenges inherent in new product development, including completion of clinical trials; claims and concerns about product safety and efficacy; regulatory agency’s examination period, obtaining regulatory approvals; domestic and foreign healthcare reforms; trends toward managed care and healthcare cost containment; and governmental laws and regulations affecting domestic and foreign operations.

• Also, for products that are approved, there are manufacturing and marketing risks and uncertainties, which include, but are not limited to, inability to build production capacity to meet demand, unavailability of raw materials, and failure to gain market acceptance.

• The Company disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise.

• This English presentation was translated from the original Japanese version. In the event of any inconsistency between the statements in the two versions, the statements in the Japanese version shall prevail.

3

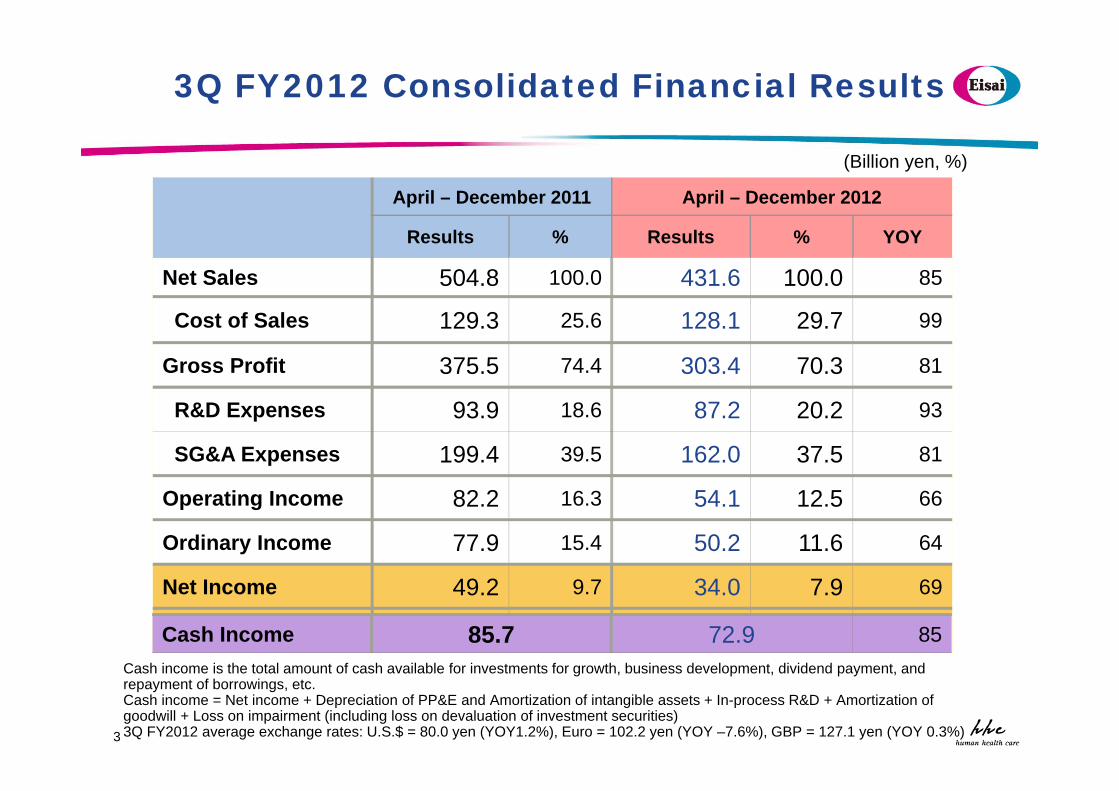

April – December 2011 April – December 2012

Results % Results % YOY

Net Sales 504.8 100.0 431.6 100.0 85

Cost of Sales 129.3 25.6 128.1 29.7 99

Gross Profit 375.5 74.4 303.4 70.3 81

R&D Expenses 93.9 18.6 87.2 20.2 93

SG&A Expenses 199.4 39.5 162.0 37.5 81

Operating Income 82.2 16.3 54.1 12.5 66

Ordinary Income 77.9 15.4 50.2 11.6 64

Net Income 49.2 9.7 34.0 7.9 69

88. ….a

(Billion yen, %)

3Q FY2012 Consolidated Financial Results

Cash income is the total amount of cash available for investments for growth, business development, dividend payment, and repayment of borrowings, etc.Cash income = Net income + Depreciation of PP&E and Amortization of intangible assets + In-process R&D + Amortization of goodwill + Loss on impairment (including loss on devaluation of investment securities)3Q FY2012 average exchange rates: U.S.$ = 80.0 yen (YOY1.2%), Euro = 102.2 yen (YOY –7.6%), GBP = 127.1 yen (YOY 0.3%)

Cash Income 85.7 72.9 85

4

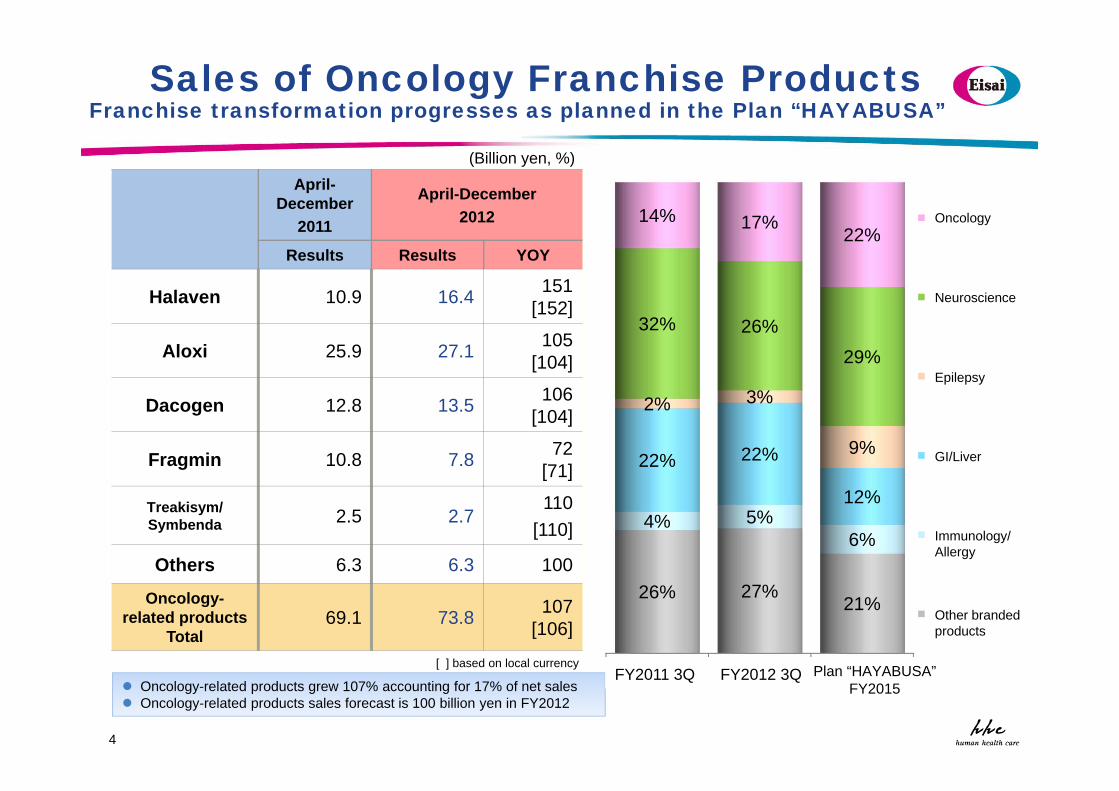

Sales of Oncology Franchise Products Franchise transformation progresses as planned in the Plan “HAYABUSA”

Oncology-related products grew 107% accounting for 17% of net sales Oncology-related products sales forecast is 100 billion yen in FY2012

April-December

2011

April-December2012

Results Results YOY

Halaven 10.9 16.4 151[152]

Aloxi 25.9 27.1 105[104]

Dacogen 12.8 13.5 106[104]

Fragmin 10.8 7.8 72[71]

Treakisym/Symbenda 2.5 2.7

110[110]

Others 6.3 6.3 100

Oncology-related products

Total69.1 73.8 107

[106]

2011年度上期 2012年度上期 計画「はやぶさ」

2015年度

26% 27%21%

4% 5%6%

22% 22%

12%

2% 3%

9%

32% 26%29%

14% 17%22%

がん

脳神経

てんかん

消化器・肝臓

免疫/アレルギー

他ブランド

(Billion yen, %)

[ ] based on local currencyFY2011 3Q Plan “HAYABUSA”

FY2015FY2012 3Q

Oncology

Neuroscience

GI/Liver

Other brandedproducts

Immunology/Allergy

Epilepsy

5

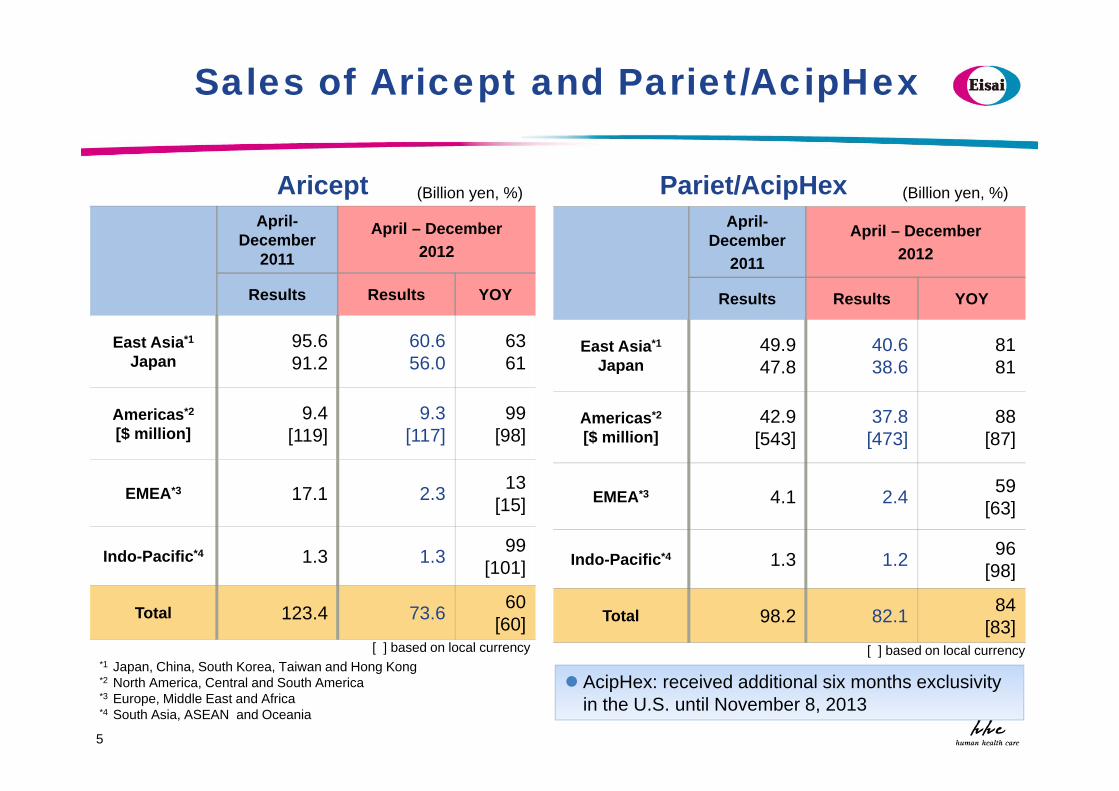

Sales of Aricept and Pariet/AcipHex

April-December

2011

April – December2012

Results Results YOY

East Asia*1

Japan95.691.2

60.656.0

6361

Americas*2

[$ million]9.4

[119] 9.3

[117]99

[98]

EMEA*3 17.1 2.3 13[15]

Indo-Pacific*4 1.3 1.3 99[101]

Total 123.4 73.6 60[60]

April-December

2011

April – December2012

Results Results YOY

East Asia*1

Japan49.947.8

40.638.6

8181

Americas*2

[$ million]42.9

[543]37.8

[473]88

[87]

EMEA*3 4.1 2.4 59[63]

Indo-Pacific*4 1.3 1.2 96[98]

Total 98.2 82.1 84[83]

*1 Japan, China, South Korea, Taiwan and Hong Kong*2 North America, Central and South America *3 Europe, Middle East and Africa*4 South Asia, ASEAN and Oceania

AcipHex: received additional six months exclusivity in the U.S. until November 8, 2013

(Billion yen, %)Aricept Pariet/AcipHex (Billion yen, %)

[ ] based on local currency [ ] based on local currency

April - December2011

April – December2012

Sales % Sales % YOY

East AsiaJapanChina

315.7294.313.0

62.558.3

2.6

274.6250.015.8

63.657.9

3.7

8785

122Americas[$ million]

119.8[1,516] 23.7 114.5

[1,431] 26.5 96[94]

EMEA 34.0 6.7 18.9 4.4 55[59]

Indo-Pacific 5.1 1.0 5.1 1.2 100[102]

Reporting Segment Total 474.6 94.0 413.1 95.7 87

[87]

Others 30.2 6.0 18.5 4.3 61

Consolidated Sales 504.8 100.0 431.6 100.00 85

[86]

6

Sales by Segment Regional transformation progresses as planned in the Plan “HAYABUSA”

Pharmaceuticals Businesses of East Asia, Americas, EMEA and Indo-Pacific. Segment profit from Americas Pharmaceuticals Business in local currency was calculated based on average exchange rate.

(Billion yen, %)

[ ] based on local currency FY2011 3Q Plan “HAYABUSA”FY2015

FY2012 3Q

6% 4% 3%1% 1% 3%

7%4% 7%

24%27% 24%

63% 64% 63%

イースト アジア

アメリカス

EMEA

Indo-Pacific

その他事業

East Asia

EMEA

Others

Americas

Indo-Pacific

7

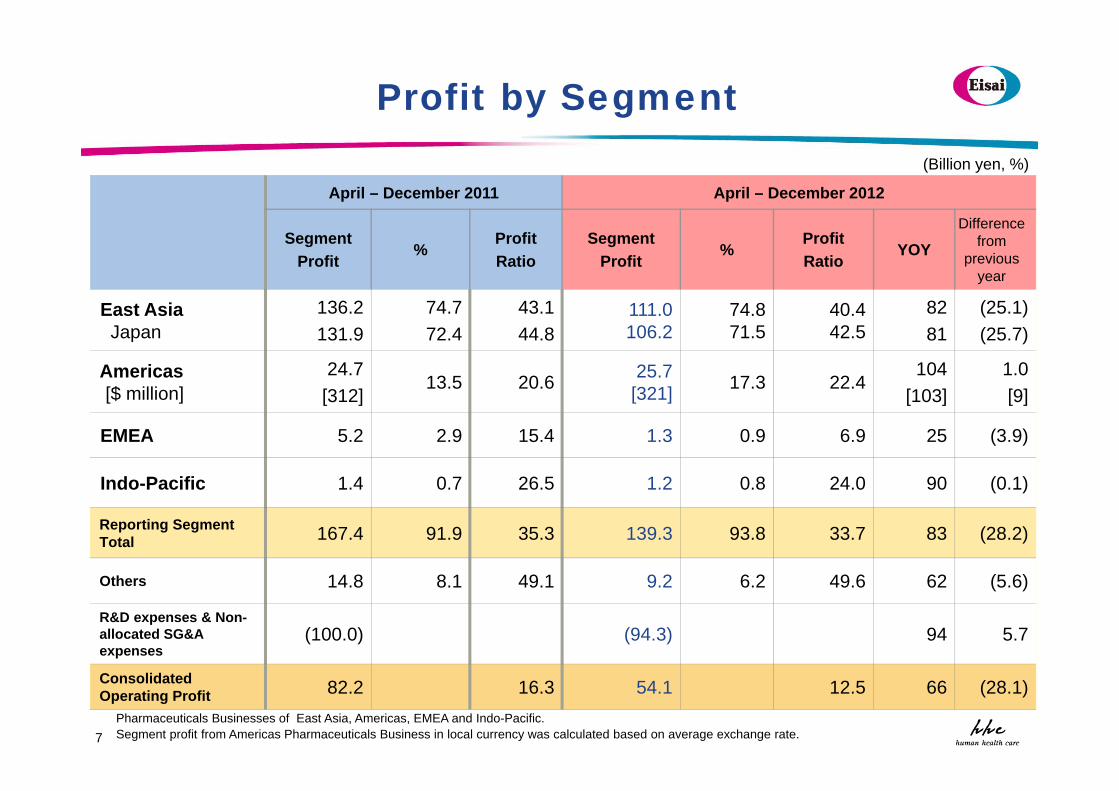

Profit by Segment

April – December 2011 April – December 2012

SegmentProfit

%ProfitRatio

SegmentProfit

%ProfitRatio

YOYDifference

from previous

year

East AsiaJapan

136.2131.9

74.772.4

43.144.8

111.0106.2

74.871.5

40.442.5

8281

(25.1)(25.7)

Americas[$ million]

24.7[312]

13.5 20.6 25.7[321] 17.3 22.4

104[103]

1.0[9]

EMEA 5.2 2.9 15.4 1.3 0.9 6.9 25 (3.9)

Indo-Pacific 1.4 0.7 26.5 1.2 0.8 24.0 90 (0.1)

Reporting Segment Total 167.4 91.9 35.3 139.3 93.8 33.7 83 (28.2)

Others 14.8 8.1 49.1 9.2 6.2 49.6 62 (5.6)

R&D expenses & Non-allocated SG&A expenses

(100.0) (94.3) 94 5.7

Consolidated Operating Profit 82.2 16.3 54.1 12.5 66 (28.1)

Pharmaceuticals Businesses of East Asia, Americas, EMEA and Indo-Pacific.Segment profit from Americas Pharmaceuticals Business in local currency was calculated based on average exchange rate.

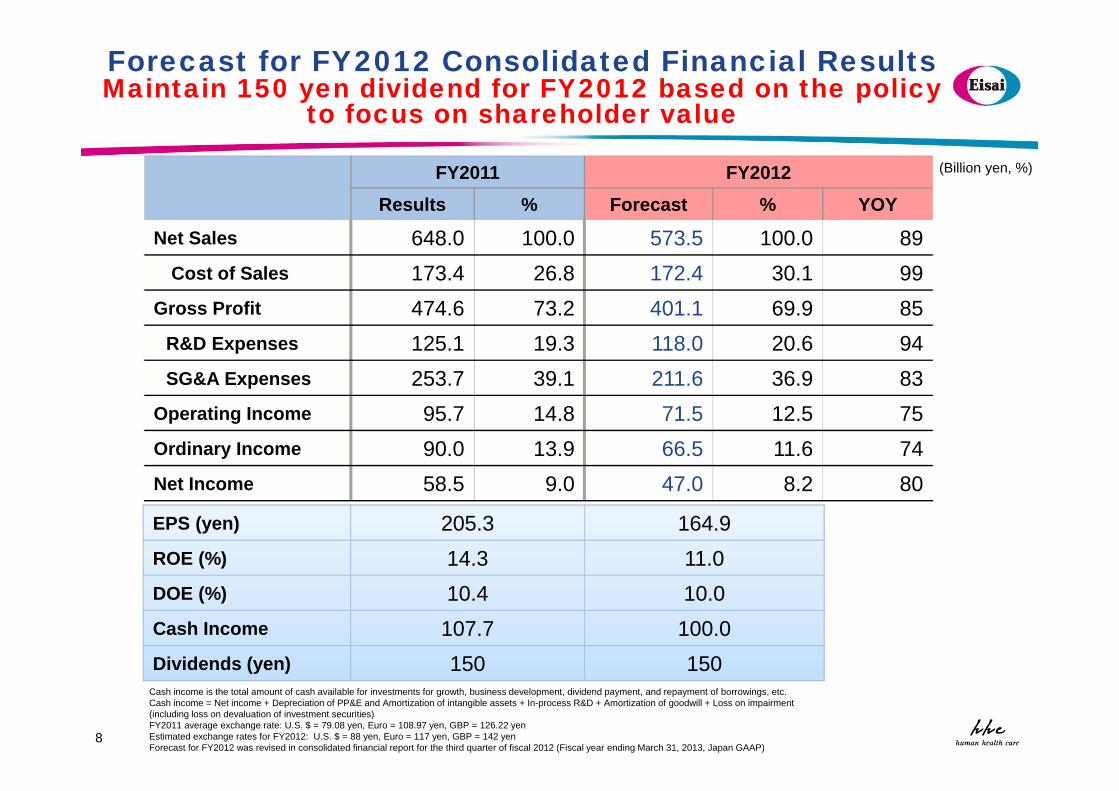

(Billion yen, %)

FY2011 FY2012Results % Forecast % YOY

Net Sales 648.0 100.0 573.5 100.0 89Cost of Sales 173.4 26.8 172.4 30.1 99

Gross Profit 474.6 73.2 401.1 69.9 85R&D Expenses 125.1 19.3 118.0 20.6 94SG&A Expenses 253.7 39.1 211.6 36.9 83

Operating Income 95.7 14.8 71.5 12.5 75Ordinary Income 90.0 13.9 66.5 11.6 74Net Income 58.5 9.0 47.0 8.2 80

EPS (yen) 205.3 164.9ROE (%) 14.3 11.0DOE (%) 10.4 10.0Cash Income 107.7 100.0Dividends (yen) 150 150

Forecast for FY2012 Consolidated Financial Results Maintain 150 yen dividend for FY2012 based on the policy

to focus on shareholder value

Cash income is the total amount of cash available for investments for growth, business development, dividend payment, and repayment of borrowings, etc.Cash income = Net income + Depreciation of PP&E and Amortization of intangible assets + In-process R&D + Amortization of goodwill + Loss on impairment (including loss on devaluation of investment securities)FY2011 average exchange rate: U.S. $ = 79.08 yen, Euro = 108.97 yen, GBP = 126.22 yen Estimated exchange rates for FY2012: U.S. $ = 88 yen, Euro = 117 yen, GBP = 142 yenForecast for FY2012 was revised in consolidated financial report for the third quarter of fiscal 2012 (Fiscal year ending March 31, 2013, Japan GAAP)

8

(Billion yen, %)

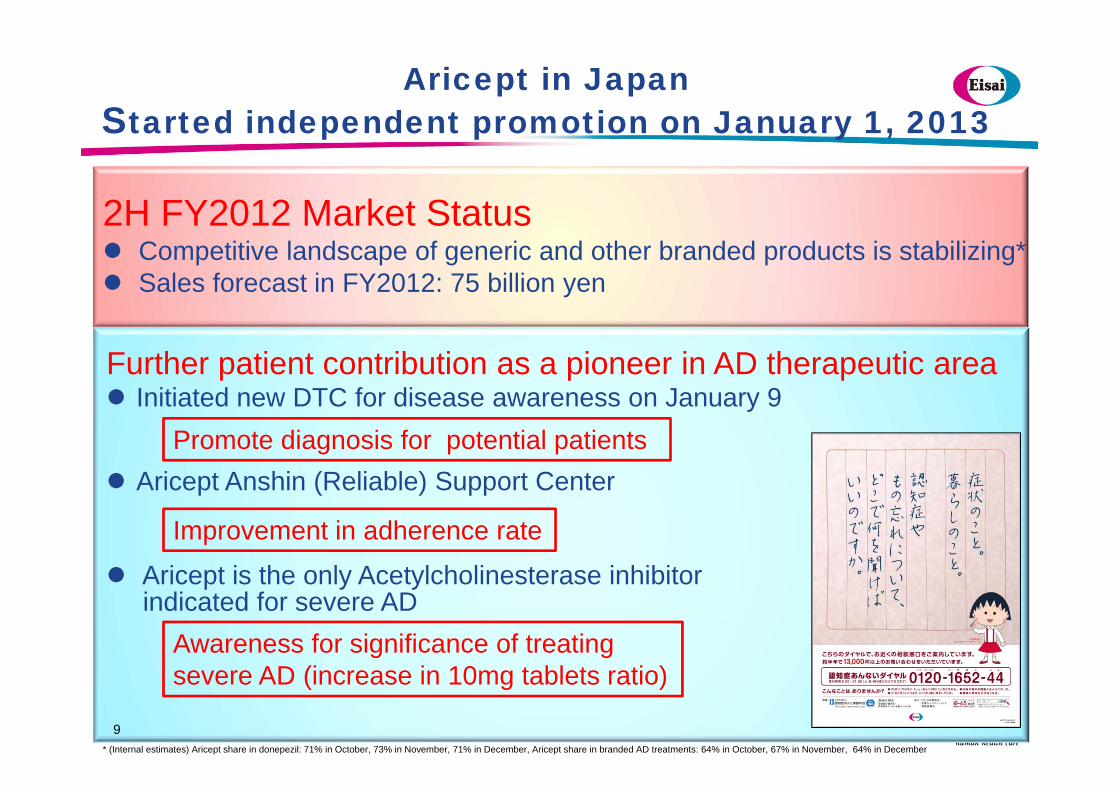

Aricept in JapanStarted independent promotion on January 1, 2013

2H FY2012 Market Status Competitive landscape of generic and other branded products is stabilizing* Sales forecast in FY2012: 75 billion yen

Further patient contribution as a pioneer in AD therapeutic area Initiated new DTC for disease awareness on January 9

Aricept Anshin (Reliable) Support Center

Aricept is the only Acetylcholinesterase inhibitorindicated for severe AD

9

Improvement in adherence rate

Awareness for significance of treating severe AD (increase in 10mg tablets ratio)

Promote diagnosis for potential patients

* (Internal estimates) Aricept share in donepezil: 71% in October, 73% in November, 71% in December, Aricept share in branded AD treatments: 64% in October, 67% in November, 64% in December

10

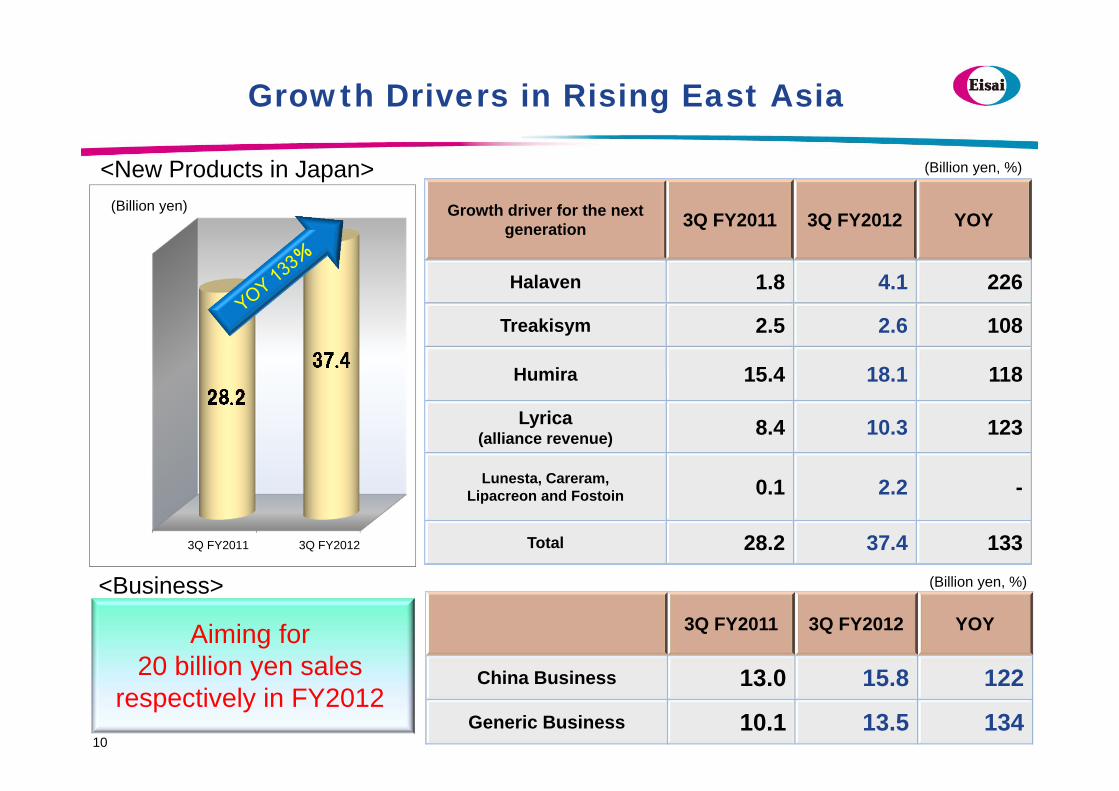

Growth Drivers in Rising East Asia

(Billion yen)

(Billion yen, %)

Growth driver for the next generation 3Q FY2011 3Q FY2012 YOY

Halaven 1.8 4.1 226

Treakisym 2.5 2.6 108

Humira 15.4 18.1 118

Lyrica(alliance revenue) 8.4 10.3 123

Lunesta, Careram,Lipacreon and Fostoin 0.1 2.2 -

Total 28.2 37.4 133

Aiming for20 billion yen sales

respectively in FY2012

3Q FY2011 3Q FY2012 YOY

China Business 13.0 15.8 122

Generic Business 10.1 13.5 134

<Business>

<New Products in Japan>

(Billion yen, %)

3Q FY2011 3Q FY2012

11

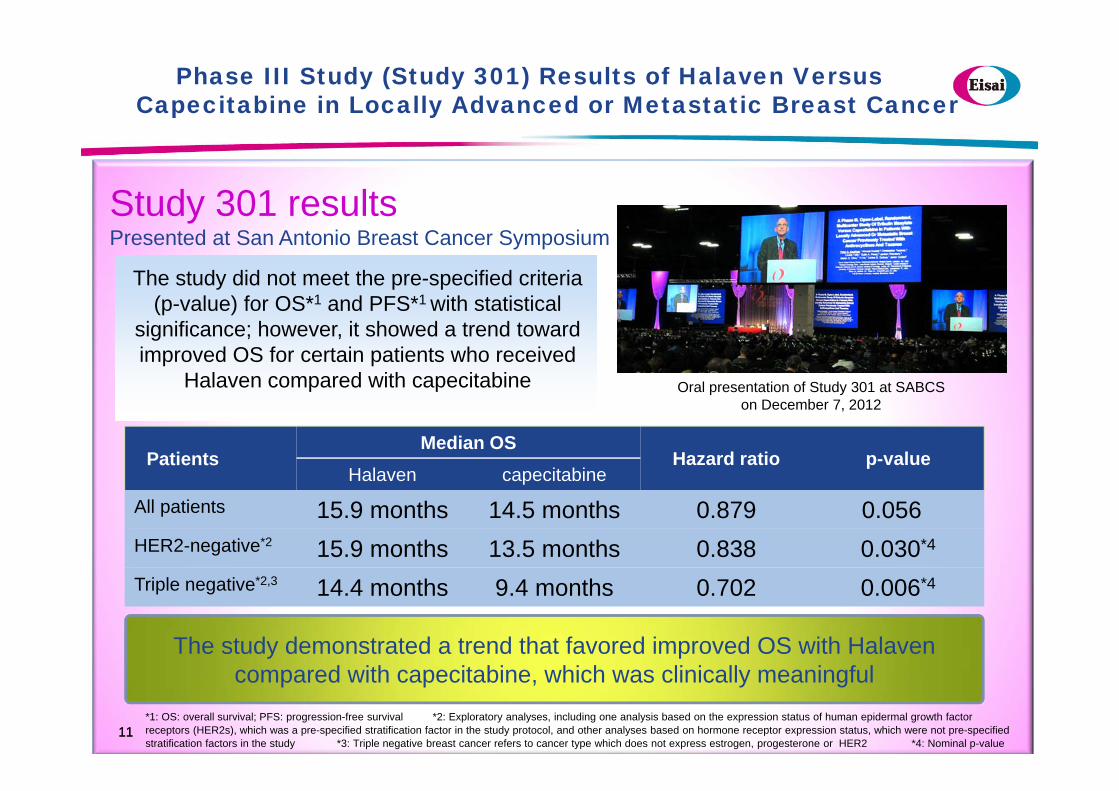

Phase III Study (Study 301) Results of Halaven Versus Capecitabine in Locally Advanced or Metastatic Breast Cancer

11

Study 301 resultsPresented at San Antonio Breast Cancer Symposium

Oral presentation of Study 301 at SABCS on December 7, 2012

The study demonstrated a trend that favored improved OS with Halaven compared with capecitabine, which was clinically meaningful

*1: OS: overall survival; PFS: progression-free survival *2: Exploratory analyses, including one analysis based on the expression status of human epidermal growth factor receptors (HER2s), which was a pre-specified stratification factor in the study protocol, and other analyses based on hormone receptor expression status, which were not pre-specified stratification factors in the study *3: Triple negative breast cancer refers to cancer type which does not express estrogen, progesterone or HER2 *4: Nominal p-value

The study did not meet the pre-specified criteria (p-value) for OS*1 and PFS*1 with statistical

significance; however, it showed a trend toward improved OS for certain patients who received

Halaven compared with capecitabine

PatientsMedian OS

Hazard ratio p-valueHalaven capecitabine

All patients 15.9 months 14.5 months 0.879 0.056HER2-negative*2 15.9 months 13.5 months 0.838 0.030*4

Triple negative*2,3 14.4 months 9.4 months 0.702 0.006*4

12

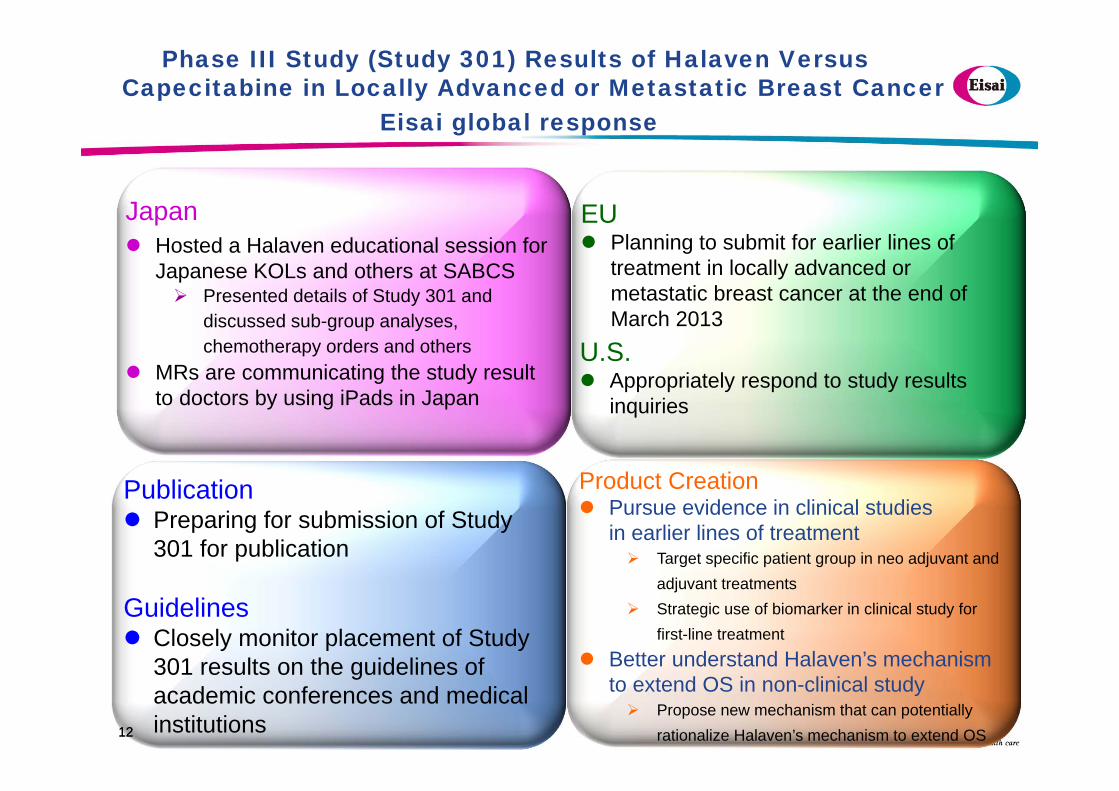

Phase III Study (Study 301) Results of Halaven Versus Capecitabine in Locally Advanced or Metastatic Breast Cancer

Eisai global response

12

Japan Hosted a Halaven educational session for

Japanese KOLs and others at SABCS Presented details of Study 301 and

discussed sub-group analyses, chemotherapy orders and others

MRs are communicating the study result to doctors by using iPads in Japan

EU Planning to submit for earlier lines of

treatment in locally advanced or metastatic breast cancer at the end of March 2013

U.S. Appropriately respond to study results

inquiries

Product Creation Pursue evidence in clinical studies

in earlier lines of treatment Target specific patient group in neo adjuvant and

adjuvant treatments Strategic use of biomarker in clinical study for

first-line treatment

Better understand Halaven’s mechanism to extend OS in non-clinical study Propose new mechanism that can potentially

rationalize Halaven’s mechanism to extend OS

Publication Preparing for submission of Study

301 for publication

Guidelines Closely monitor placement of Study

301 results on the guidelines of academic conferences and medical institutions

13

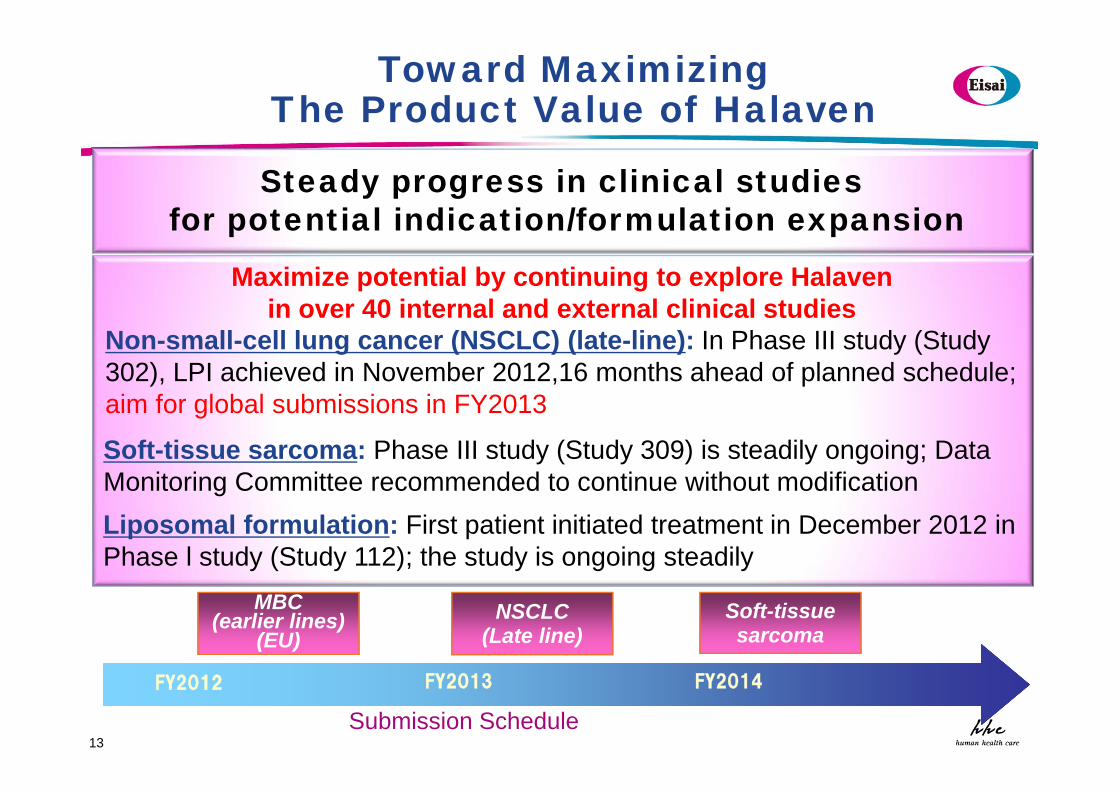

Toward Maximizing The Product Value of Halaven

Non-small-cell lung cancer (NSCLC) (late-line): In Phase III study (Study 302), LPI achieved in November 2012,16 months ahead of planned schedule;aim for global submissions in FY2013

Soft-tissue sarcoma: Phase III study (Study 309) is steadily ongoing; Data Monitoring Committee recommended to continue without modification

Steady progress in clinical studiesfor potential indication/formulation expansion

NSCLC(Late line)

Submission Schedule

Soft-tissuesarcoma

Liposomal formulation: First patient initiated treatment in December 2012 in Phase l study (Study 112); the study is ongoing steadily

MBC(earlier lines)

(EU)

Maximize potential by continuing to explore Halavenin over 40 internal and external clinical studies

FY2013 FY2014FY2012

1414

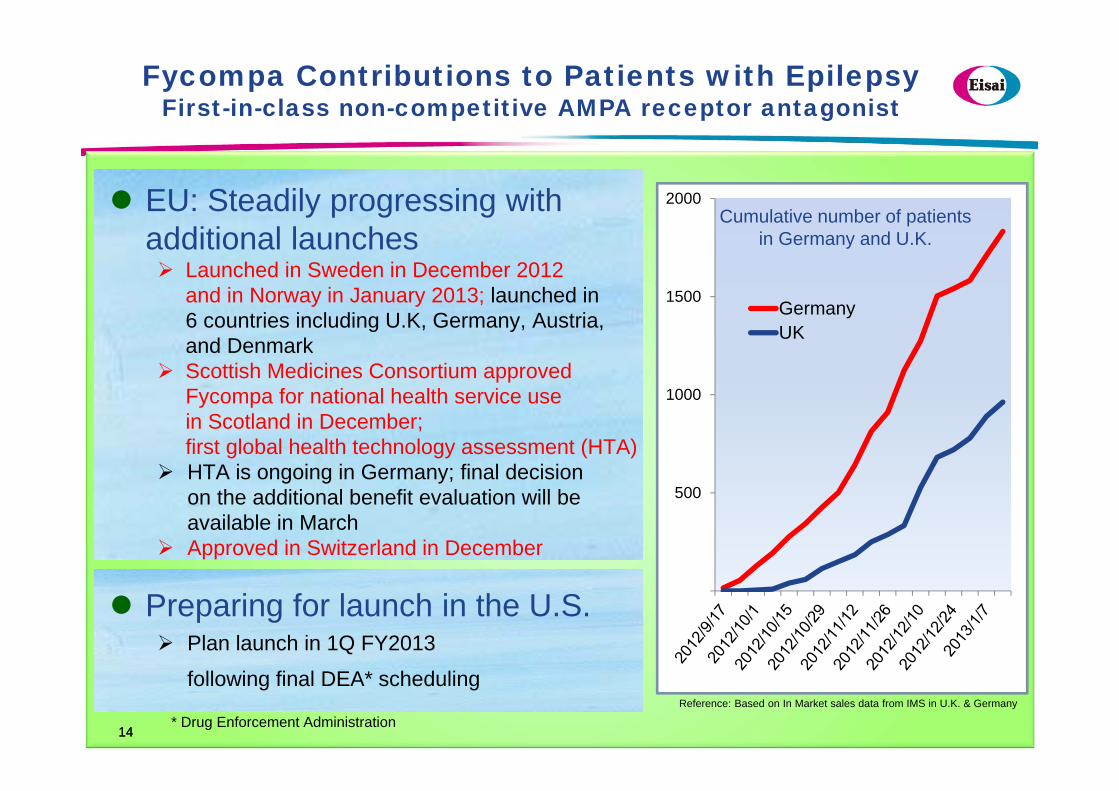

Fycompa Contributions to Patients with EpilepsyFirst-in-class non-competitive AMPA receptor antagonist

EU: Steadily progressing with additional launches Launched in Sweden in December 2012

and in Norway in January 2013; launched in 6 countries including U.K, Germany, Austria, and Denmark

Scottish Medicines Consortium approved Fycompa for national health service usein Scotland in December;first global health technology assessment (HTA)

HTA is ongoing in Germany; final decision on the additional benefit evaluation will be available in March

Approved in Switzerland in December

Preparing for launch in the U.S. Plan launch in 1Q FY2013

following final DEA* scheduling

* Drug Enforcement Administration

500

1000

1500

2000

GermanyUK

Reference: Based on In Market sales data from IMS in U.K. & Germany

Cumulative number of patients in Germany and U.K.

15

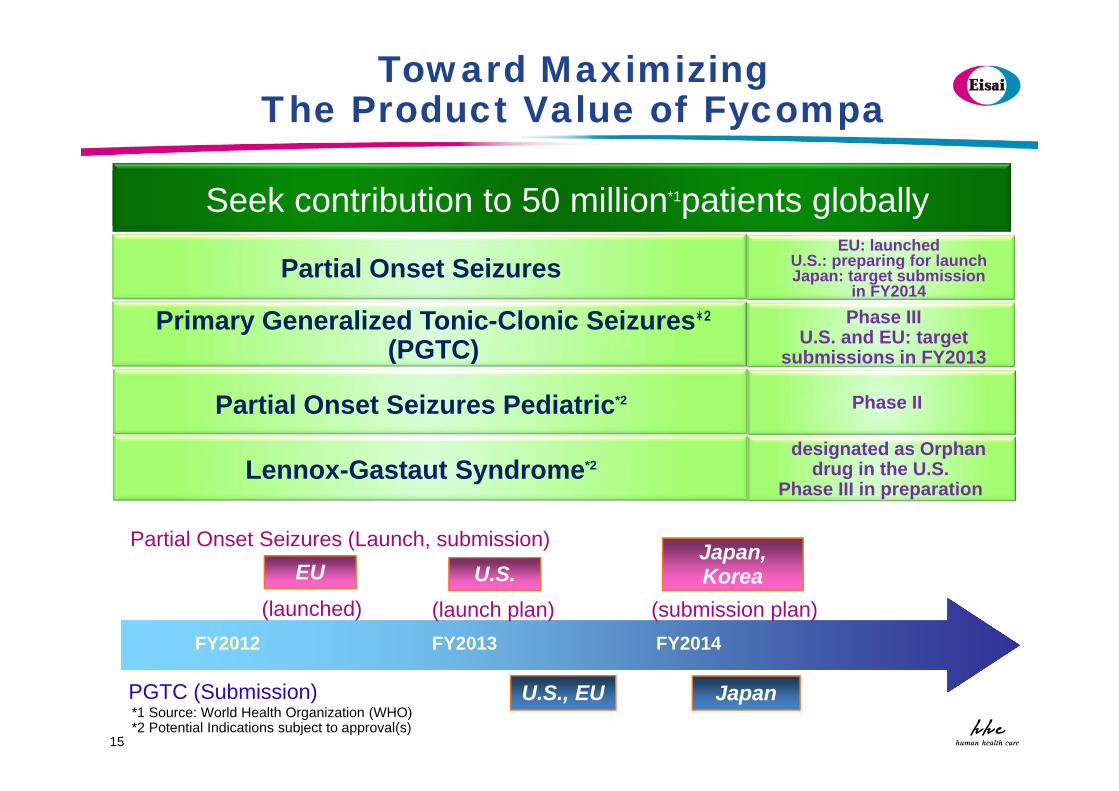

Lennox-Gastaut Syndrome*2designated as Orphan

drug in the U.S.Phase III in preparation

Partial Onset Seizures (Launch, submission)

Toward Maximizing The Product Value of Fycompa

Partial Onset Seizures

Primary Generalized Tonic-Clonic Seizures*2

(PGTC)

Partial Onset Seizures Pediatric*2

EU: launched U.S.: preparing for launchJapan: target submission

in FY2014Phase III

U.S. and EU: target submissions in FY2013

Phase II

*1 Source: World Health Organization (WHO)*2 Potential Indications subject to approval(s)

FY2014FY2012 FY2013

EU

U.S., EU

U.S.

PGTC (Submission)

Japan, Korea

Japan

(launched) (launch plan) (submission plan)

Seek contribution to 50 million*1patients globally

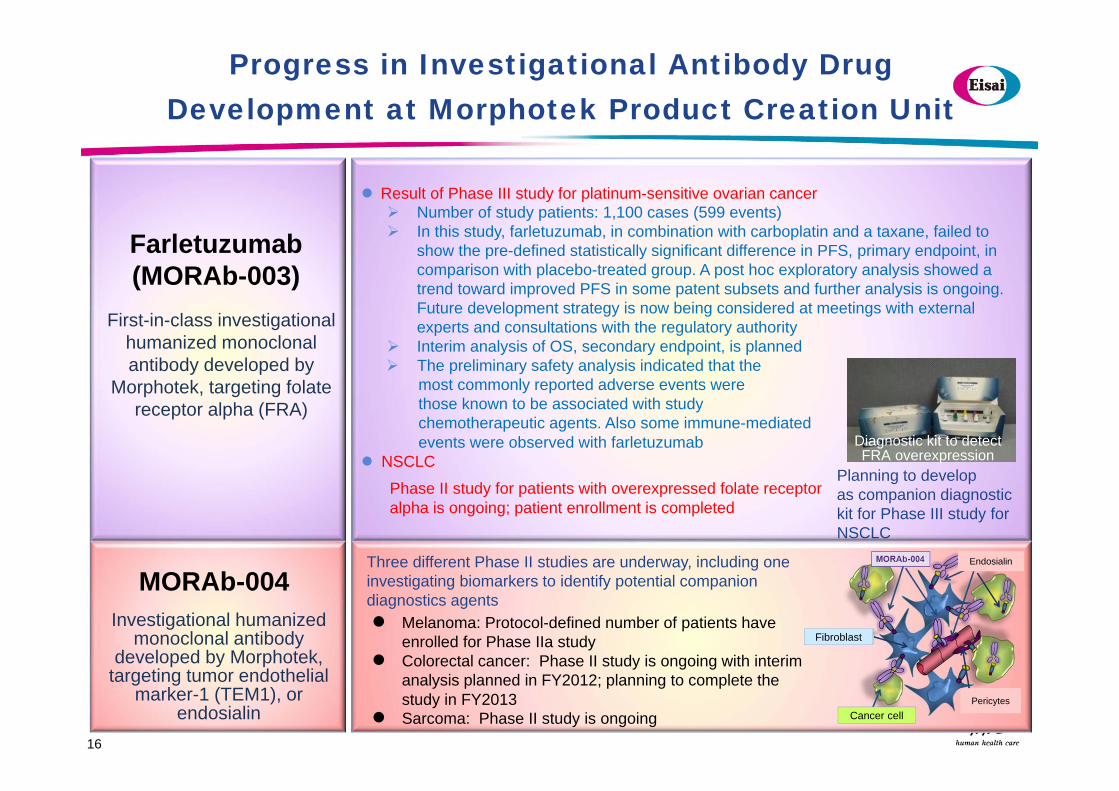

Progress in Investigational Antibody Drug Development at Morphotek Product Creation Unit

Farletuzumab(MORAb-003)

MORAb-004Three different Phase II studies are underway, including one investigating biomarkers to identify potential companion diagnostics agents

Investigational humanized monoclonal antibody

developed by Morphotek, targeting tumor endothelial

marker-1 (TEM1), or endosialin

Result of Phase III study for platinum-sensitive ovarian cancer Number of study patients: 1,100 cases (599 events) In this study, farletuzumab, in combination with carboplatin and a taxane, failed to

show the pre-defined statistically significant difference in PFS, primary endpoint, in comparison with placebo-treated group. A post hoc exploratory analysis showed a trend toward improved PFS in some patent subsets and further analysis is ongoing. Future development strategy is now being considered at meetings with external experts and consultations with the regulatory authority

Interim analysis of OS, secondary endpoint, is planned The preliminary safety analysis indicated that the

most commonly reported adverse events were those known to be associated with study chemotherapeutic agents. Also some immune-mediatedevents were observed with farletuzumab

NSCLC

Phase II study for patients with overexpressed folate receptoralpha is ongoing; patient enrollment is completed

First-in-class investigational humanized monoclonal antibody developed by

Morphotek, targeting folate receptor alpha (FRA)

Diagnostic kit to detectFRA overexpression

Planning to developas companion diagnostic kit for Phase III study for NSCLC

Melanoma: Protocol-defined number of patients have enrolled for Phase IIa study

Colorectal cancer: Phase II study is ongoing with interim analysis planned in FY2012; planning to complete the study in FY2013

Sarcoma: Phase II study is ongoing16

Fibroblast

Endosialin

Cancer cellPericytes

17

Lenvatinib (E7080)

Steady Progress of Investigational Lenvatinib

In-house developed, oral, molecular-targeting agent with a unique inhibitory profile of receptor tyrosine kinases, mechanism of action may occur from both inhibition of angiogenesis and tumor proliferation

<Target indications>Thyroid cancer, HCC,

RCC, NSCLC, endometrial cancer, melanoma, glioma,

etc.

Differentiated thyroid cancer: Planning submission in FY2013Global Phase III study enrollment is completed and trial is ongoing

HCCGlobal Phase III study started

NSCLC Phase II study started in the U.S., Europe, Japan and Asia with patients with RET chromosomal translocation

Clinical studies for endometrial cancer (Phase II), melanoma (Phase II), glioma (Phase II), RCC (Phase Ib/II), and solid cancer in combination with Golvatinib (Phase I/II) are progressing steadily

Chart: Created based on Nature Biotechnology 2005;23(3)

• Detect chromosomal translocation using deep sequencing technology

• Initiated investigation to develop companion diagnostics agents

18

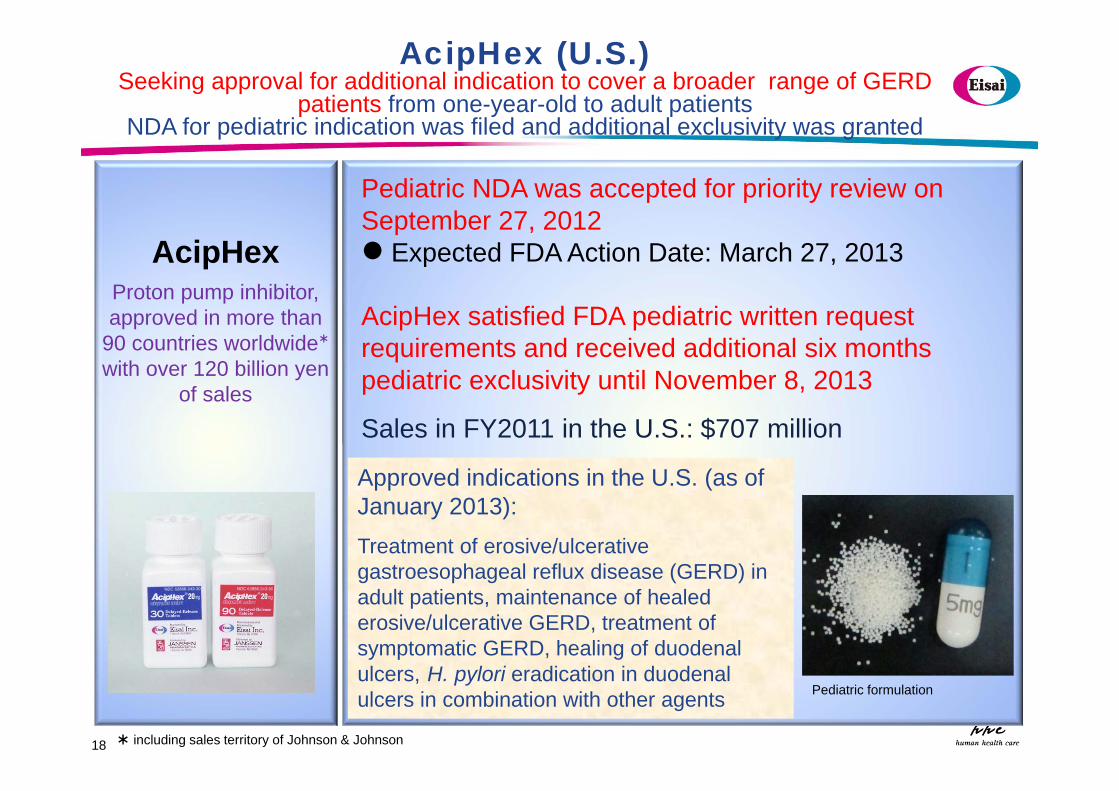

AcipHexProton pump inhibitor, approved in more than

90 countries worldwide*

with over 120 billion yen of sales

AcipHex (U.S.) Seeking approval for additional indication to cover a broader range of GERD

patients from one-year-old to adult patients NDA for pediatric indication was filed and additional exclusivity was granted

Pediatric NDA was accepted for priority review on September 27, 2012 Expected FDA Action Date: March 27, 2013

AcipHex satisfied FDA pediatric written request requirements and received additional six months pediatric exclusivity until November 8, 2013

Sales in FY2011 in the U.S.: $707 million

Approved indications in the U.S. (as of January 2013):Treatment of erosive/ulcerative gastroesophageal reflux disease (GERD) in adult patients, maintenance of healed erosive/ulcerative GERD, treatment of symptomatic GERD, healing of duodenal ulcers, H. pylori eradication in duodenal ulcers in combination with other agents

* including sales territory of Johnson & Johnson

Pediatric formulation

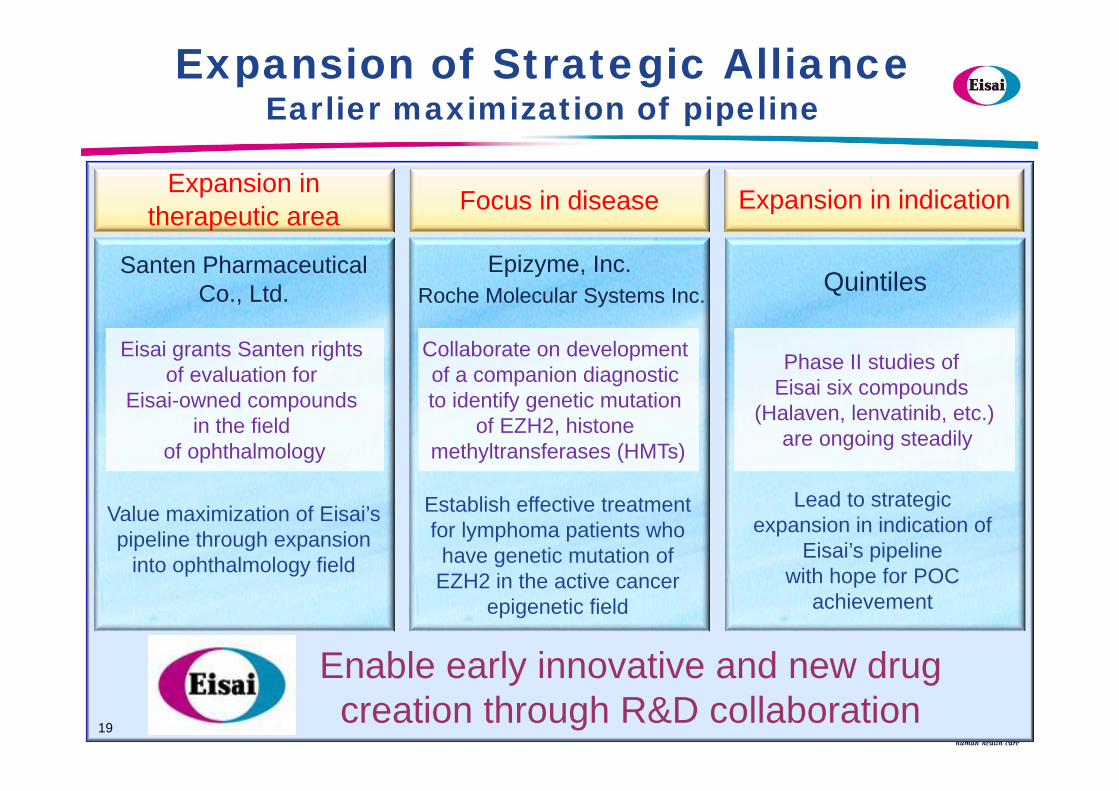

Expansion of Strategic AllianceEarlier maximization of pipeline

にすと

Enable early innovative and new drug creation through R&D collaboration

19

Lead to strategic expansion in indication of

Eisai’s pipelinewith hope for POC

achievement

Establish effective treatment for lymphoma patients who have genetic mutation of EZH2 in the active cancer

epigenetic field

Santen Pharmaceutical Co., Ltd.

Epizyme, Inc.Roche Molecular Systems Inc. Quintiles

Phase II studies of Eisai six compounds

(Halaven, lenvatinib, etc.)are ongoing steadily

Value maximization of Eisai’s pipeline through expansion

into ophthalmology field

Collaborate on development of a companion diagnostic to identify genetic mutation

of EZH2, histone methyltransferases (HMTs)

Eisai grants Santen rights of evaluation for

Eisai-owned compounds in the field

of ophthalmology

Expansion in therapeutic area Focus in disease Expansion in indication

Abundant Growth Drivers in Product PortfolioGlobal launches in succession increase corporate value

20

New products already launched Halaven Approved in 44 countries and launched in the U.S., EU, Japan, and others

Submission for earlier lines of treatment in locally advanced or metastatic breastcancer is planned in EU by the end of FY2012

Lunesta Insomnia treatment that improves difficulty with falling asleep and staying asleepLaunched in Japan in April 2012; restriction on administration period to be lifted in May 2013

Fycompa Approved in 31 countries, and launched in EU in September 2012 Careram A novel disease-modifying anti-rheumatic drug that inhibits production of

inflammatory cytokine and immunoglobulin; launched in September 2012Gliadel World’s only implant in the brain, sustained release formulation for brain tumor

(malignant glioma); launched in Japan in January 2013

New products soon-to-be launchedBELVIQ Approved in the U.S. in June 2012; expected to be launched in 4Q FY2012

Fycompa Expected to be launched in the U.S. in 1Q FY2013

Actonel Once-monthly formulation for the treatment of osteoporosis Approved in Japan in December 2012; expected to be launched in February 2013

21

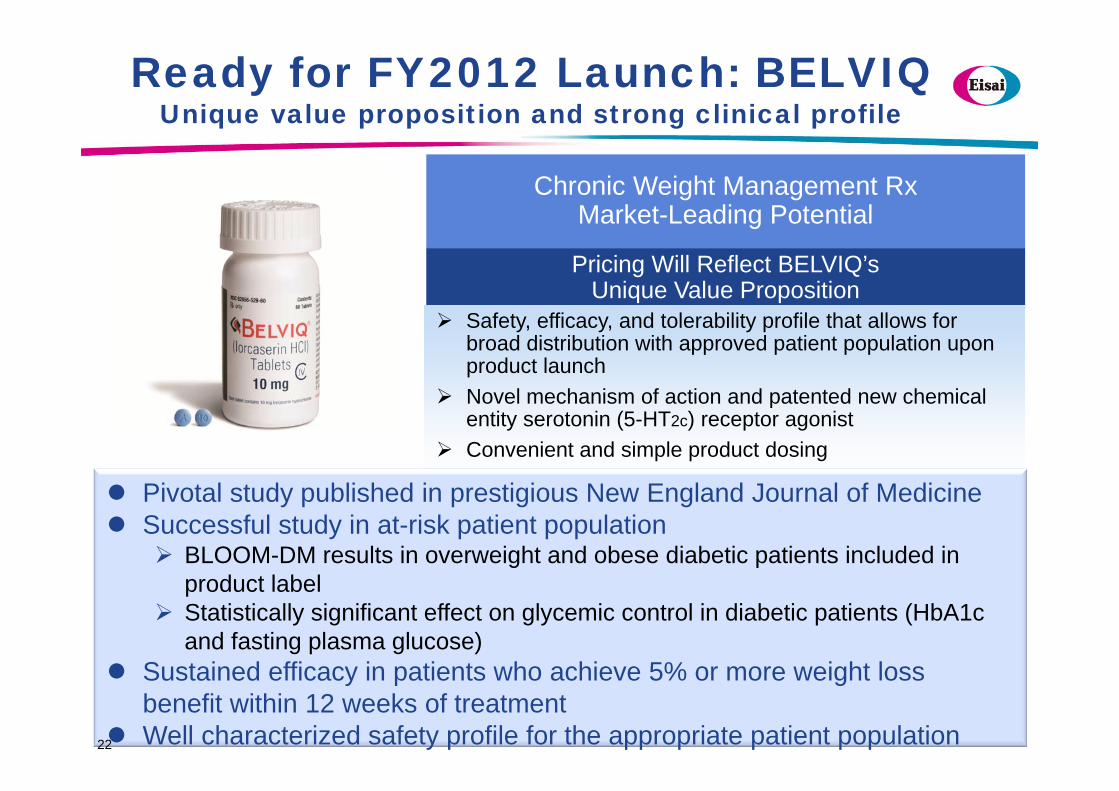

Launch Readiness ofBELVIQ

21

Pricing Will Reflect BELVIQ’s Unique Value Proposition

Safety, efficacy, and tolerability profile that allows for broad distribution with approved patient population upon product launch

Novel mechanism of action and patented new chemical entity serotonin (5-HT2c) receptor agonist

Convenient and simple product dosing

Ready for FY2012 Launch: BELVIQUnique value proposition and strong clinical profile

Chronic Weight Management Rx Market-Leading Potential

Pivotal study published in prestigious New England Journal of Medicine Successful study in at-risk patient population

BLOOM-DM results in overweight and obese diabetic patients included in product label

Statistically significant effect on glycemic control in diabetic patients (HbA1c and fasting plasma glucose)

Sustained efficacy in patients who achieve 5% or more weight loss benefit within 12 weeks of treatment

Well characterized safety profile for the appropriate patient population22

23

Prior experience in GERD market positions Eisai for effective execution in the chronic weight management market

Substantial patient and physician overlap for obesity and GERD

Prior contracting experience with payors on broad market productAcipHex experience provides us with unique capabilities that directly relate to

chronic weight management market

a

Experience in establishing underserved prescription markets

Seeking 40% coverage of commercial lives*1 within first

year of launchSeeking >50% coverage of

commercial lives

Launch year 3 and beyondSeeking 70% coverage of

commercial lives plus access to public lives*2 through removal of

government restrictions

Launch year 1 Launch year 2

Leveraging Commercial Experience

*1: Commercial lives includes individuals who privately purchase medical insurance or receive it through workplace benefits*2: Public lives includes individuals who receive medical insurance coverage through government-sponsored programs

24

Reference Data

24

2525

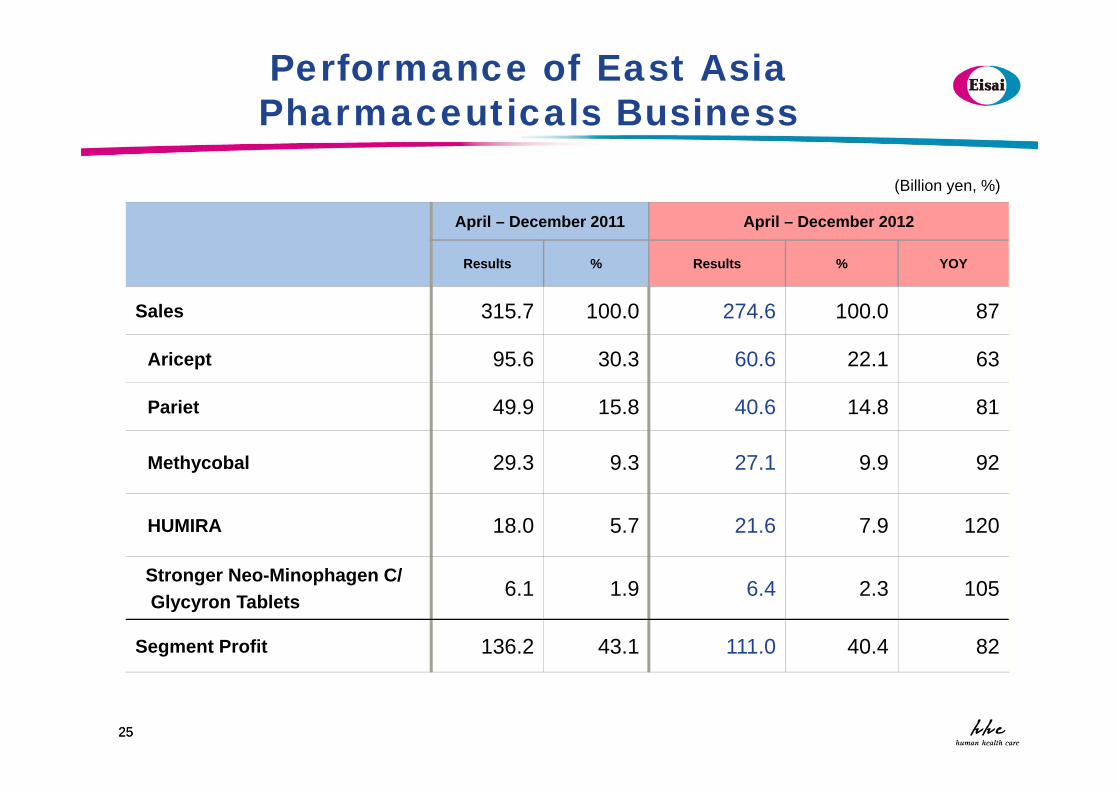

Performance of East Asia Pharmaceuticals Business

April – December 2011 April – December 2012

Results % Results % YOY

Sales 315.7 100.0 274.6 100.0 87

Aricept 95.6 30.3 60.6 22.1 63

Pariet 49.9 15.8 40.6 14.8 81

Methycobal 29.3 9.3 27.1 9.9 92

HUMIRA 18.0 5.7 21.6 7.9 120

Stronger Neo-Minophagen C/ Glycyron Tablets 6.1 1.9 6.4 2.3 105

Segment Profit 136.2 43.1 111.0 40.4 82

(Billion yen, %)

26

Performance of East Asia Pharmaceuticals Business

April – December 2011 April – December 2012Results % Results % YOY

Sales 1,055 100.0 1,247 100.0 118Methycobal 465 44.1 534 42.8 115Stronger Neo-Minophagen C/ Glycyron Tablets

226 21.4 271 21.7 120

Aricept 106 10.0 127 10.2 121Pariet 67 6.4 82 6.6 121

April – December 2011 April – December 2012Results % Results % YOY

Sales 294.3 100.0 250.0 100.0 85Prescription 263.9 89.7 216.4 86.6 82Aricept 91.2 31.0 56.0 22.4 61Pariet 47.8 16.2 38.6 15.4 81Methycobal 23.4 8.0 20.1 8.0 86HUMIRA 15.4 5.2 18.1 7.2 118Actonel 8.8 3.0 6.9 2.8 79OTC 15.9 5.4 15.8 6.3 99Generics 10.1 3.4 13.5 5.4 134Diagnostics 4.4 1.5 4.3 1.7 97Segment Profit 131.9 44.8 106.2 42.5 81

<Japan>

<China>

(Billion yen, %)

(MM RMB, %)

27

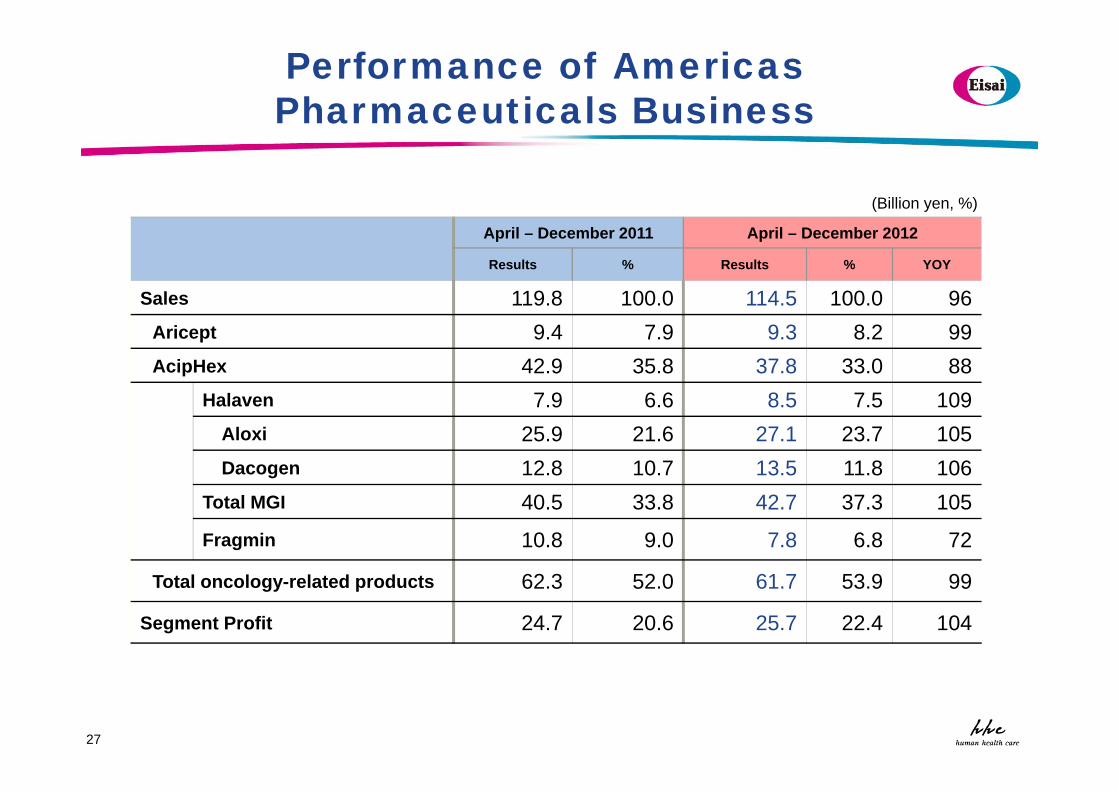

Performance of Americas Pharmaceuticals Business

April – December 2011 April – December 2012

Results % Results % YOY

Sales 119.8 100.0 114.5 100.0 96Aricept 9.4 7.9 9.3 8.2 99AcipHex 42.9 35.8 37.8 33.0 88

Halaven 7.9 6.6 8.5 7.5 109Aloxi 25.9 21.6 27.1 23.7 105Dacogen 12.8 10.7 13.5 11.8 106

Total MGI 40.5 33.8 42.7 37.3 105

Fragmin 10.8 9.0 7.8 6.8 72

Total oncology-related products 62.3 52.0 61.7 53.9 99

Segment Profit 24.7 20.6 25.7 22.4 104

(Billion yen, %)

2828

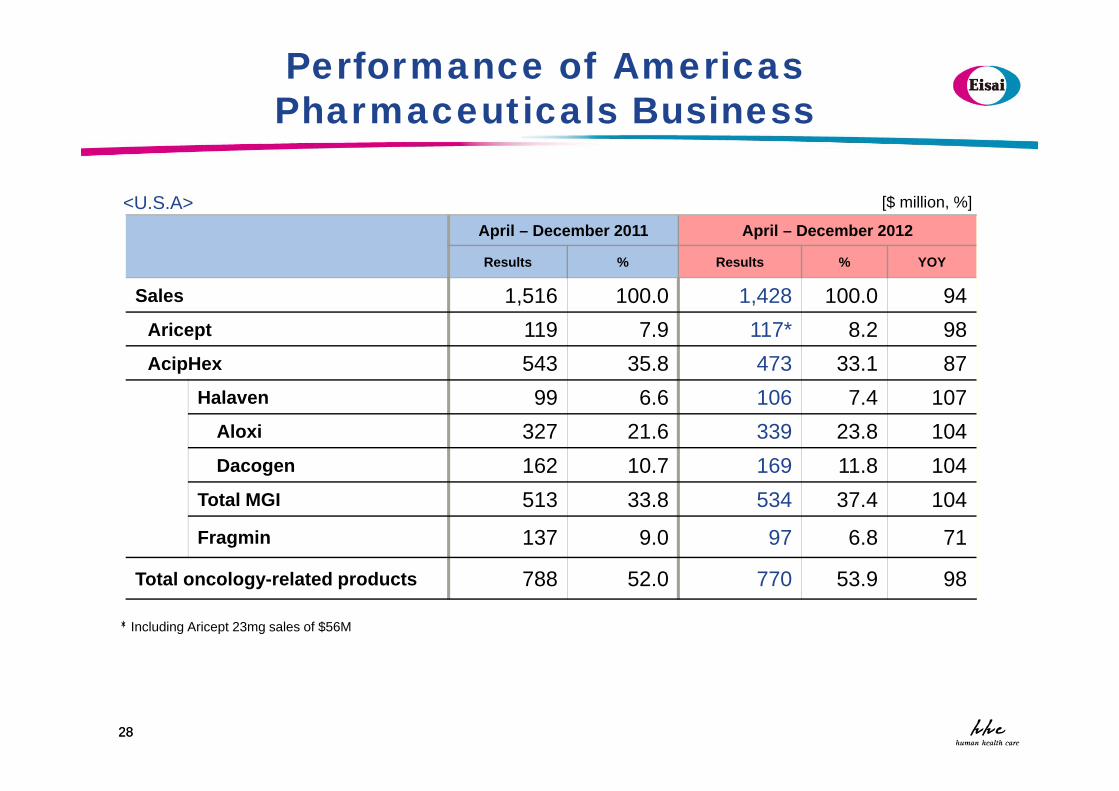

Performance of Americas Pharmaceuticals Business

April – December 2011 April – December 2012

Results % Results % YOY

Sales 1,516 100.0 1,428 100.0 94Aricept 119 7.9 117* 8.2 98AcipHex 543 35.8 473 33.1 87

Halaven 99 6.6 106 7.4 107Aloxi 327 21.6 339 23.8 104Dacogen 162 10.7 169 11.8 104

Total MGI 513 33.8 534 37.4 104

Fragmin 137 9.0 97 6.8 71

Total oncology-related products 788 52.0 770 53.9 98

* Including Aricept 23mg sales of $56M

<U.S.A> [$ million, %]

29

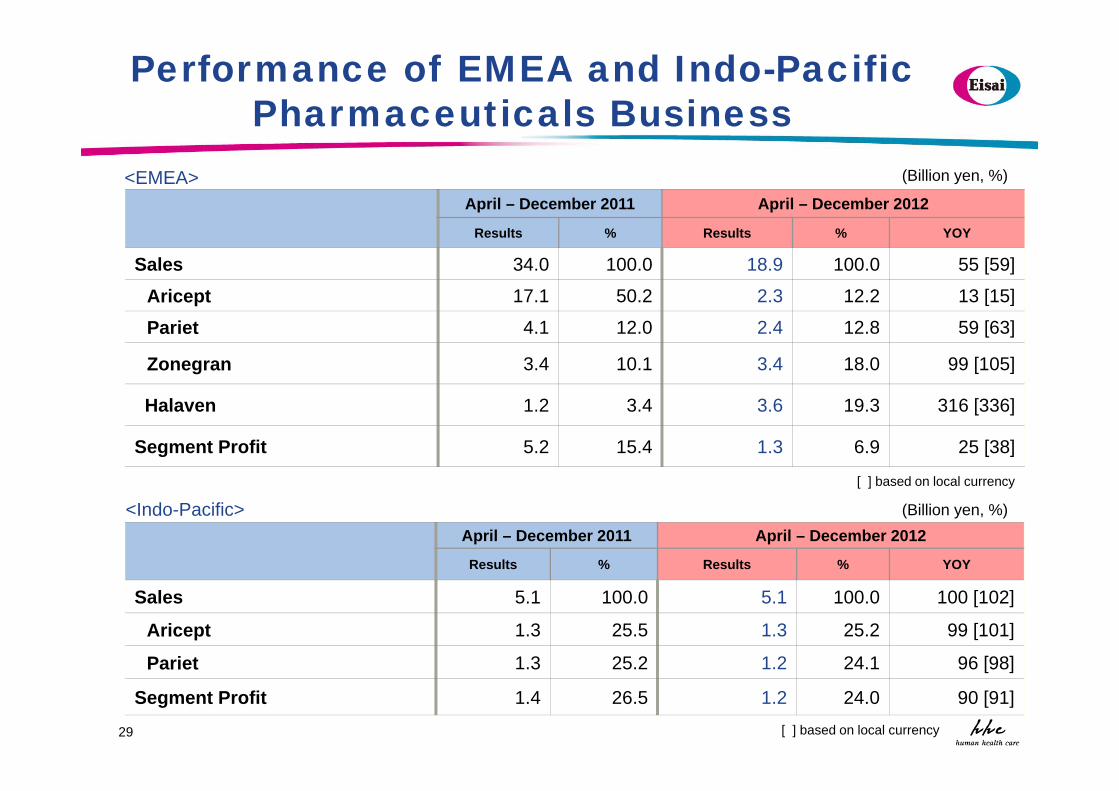

Performance of EMEA and Indo-Pacific Pharmaceuticals Business

April – December 2011 April – December 2012

Results % Results % YOY

Sales 34.0 100.0 18.9 100.0 55 [59]

Aricept 17.1 50.2 2.3 12.2 13 [15]

Pariet 4.1 12.0 2.4 12.8 59 [63]

Zonegran 3.4 10.1 3.4 18.0 99 [105]

Halaven 1.2 3.4 3.6 19.3 316 [336]

Segment Profit 5.2 15.4 1.3 6.9 25 [38]

April – December 2011 April – December 2012

Results % Results % YOY

Sales 5.1 100.0 5.1 100.0 100 [102]

Aricept 1.3 25.5 1.3 25.2 99 [101]

Pariet 1.3 25.2 1.2 24.1 96 [98]

Segment Profit 1.4 26.5 1.2 24.0 90 [91]

<Indo-Pacific>

<EMEA>

[ ] based on local currency

(Billion yen, %)

(Billion yen, %)

[ ] based on local currency