Embed Size (px)

Citation preview

3D Systems Corporation: Strategic Analysis and Recommendations

MGMT 3519: Strategic Analysis: Capstone Project

Professor N. MacGregor

March 14, 2015

Submitted by Team Agreement:

Martha Andrews

Monica Argenti

Cathy Le

Victor Phan

Jen Visscher

Brian Zias

Executive Summary

The Additive Manufacturing (AM) industry, more commonly referred to as 3D printing, consists

of firms who market machines, materials, and services that transform raw consumables into real,

physical models of digital design data1. While there are myriad competitors in this moderately-

highly favorable industry, each firm’s business model varies in how it answers fundamental end-

user questions: How do I get the digital model? How do I send it to the printer? What printer is

right for me, if any? How can I enjoy the benefits without owning hardware?

3D Systems Corporation created the AM industry in 1988. Almost three decades later,

they have grown to offer “7 core 3D printing technologies and more than 50 3D printers to

enable everyone to start 3D printing” (3D Systems). More critically, they have expanded beyond

their core hardware businesses and now attempt to serve a variety of end-to-end user value

chains. Fueled by acquisitions, they earned revenues of $653M in 2014.

In order to address the wide spectrum of wants and needs up, down, and across the AM

market, 3D Systems continues a ramped-up acquisition strategy that started in 2009. In the last

six years 3D Systems has acquired over 45 hardware, software, and service firms as a vehicle for

growth and differentiation. 3D Systems’ first mover advantage does not entitle sustainable

competitive advantage in today’s highly competitive and commercialized industry. To both

defend industry leadership and exploit growth opportunities, 3D Systems must:

Combat shrinking net margins by realizing synergies of acquisition portfolio.

Leverage VRIO resources and capabilities to refine and market focused digital threads.

Grow market share and generate new value through alliances and open ecosystems.

Outlined in this paper are five recommendations, which suggest the ability for 3D Systems to

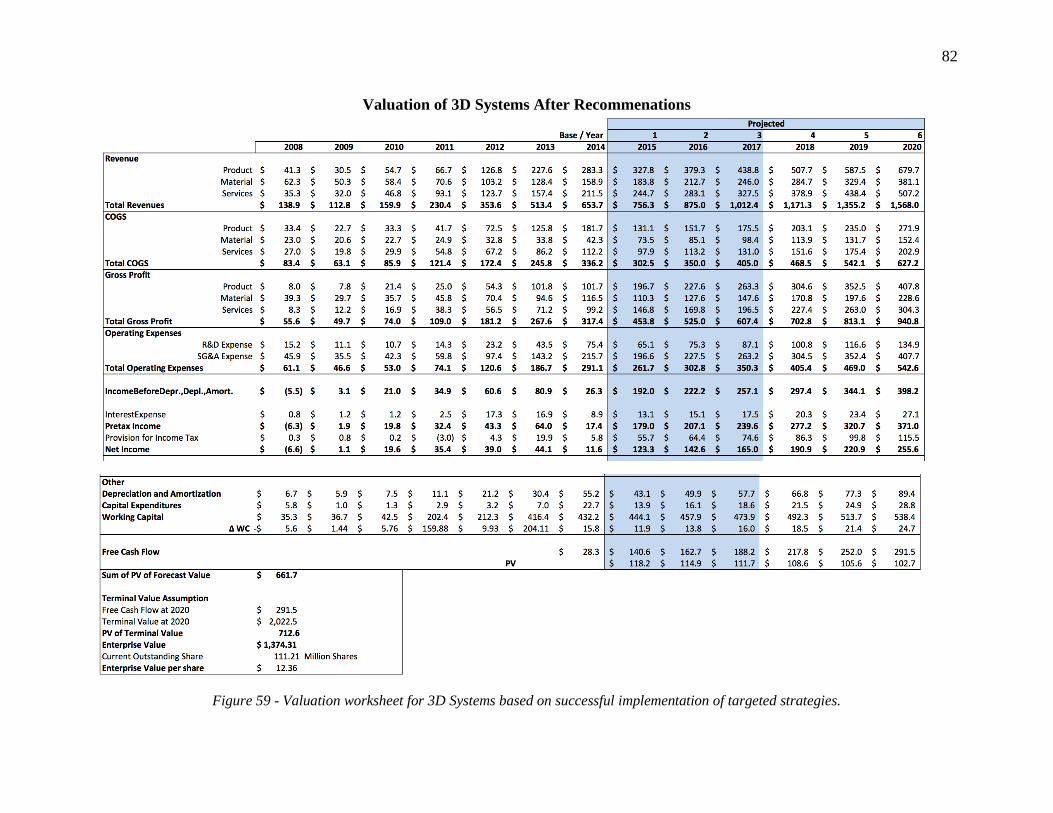

double their 2020 enterprise value from $538.3MM to $1,374.31MM2.

1 Team A’s 2-minute intro video: https://www.youtube.com/watch?v=xofbadeVbuw&feature=youtu.be

2 See 3D Systems valuations 2015-2020 before and after recommendations: Figure 52 and Figure 62

Contents

BACKGROUND .......................................................................................................................................... 1

Additive Manufacturing Technical-Application Summary ...................................................................... 1

Founder, Chuck Hull ................................................................................................................................. 2

3D Systems Corporations ......................................................................................................................... 3

Business Definition and Mission Statement ............................................................................................. 5

EXTERNAL ANALYSIS ............................................................................................................................. 6

General Environment ................................................................................................................................ 6

Industry Definition .................................................................................................................................... 9

Additive Manufacturing User Value Chains ........................................................................................... 12

Market Growth Trends ............................................................................................................................ 13

Industry Life Cycle ................................................................................................................................. 14

Porter’s 6 Forces Analysis ...................................................................................................................... 16

Competitive Landscape ........................................................................................................................... 19

INTERNAL ANALYSIS ............................................................................................................................ 22

Product Portfolio ..................................................................................................................................... 22

Organizational Structure ......................................................................................................................... 24

Strategy Diamond ................................................................................................................................... 25

VRIO Resources and Capabilities........................................................................................................... 27

Financial Performance, 2006-2014 ......................................................................................................... 29

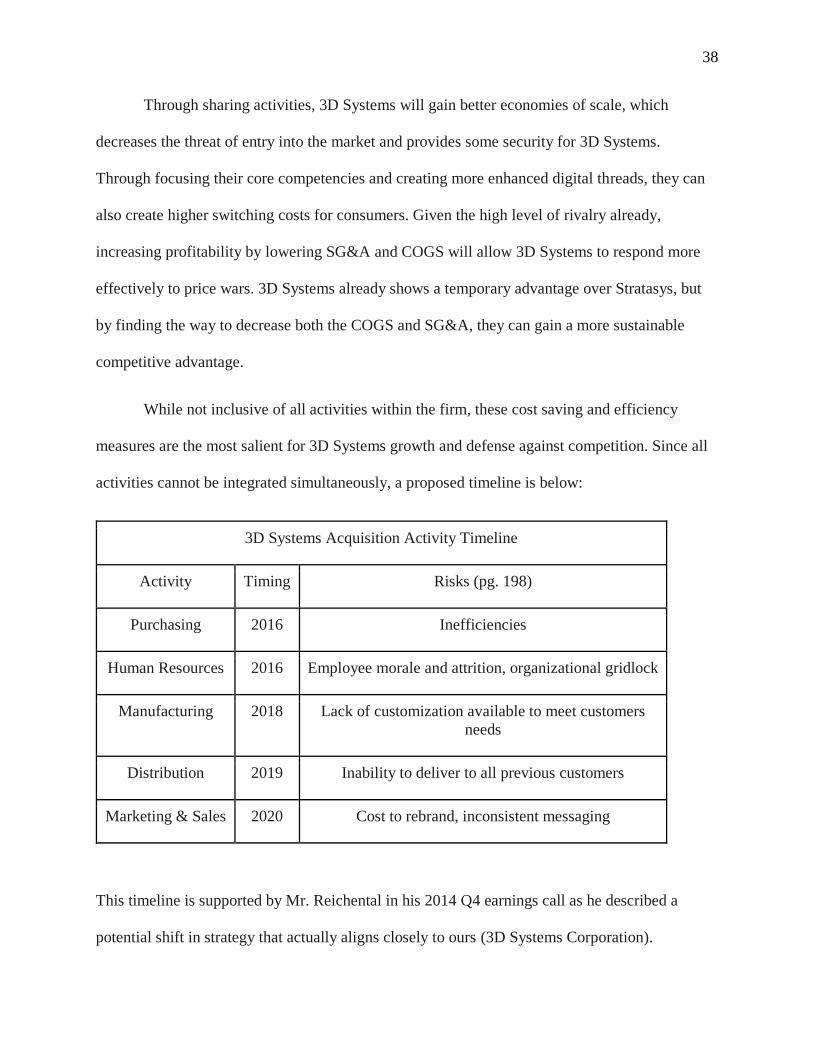

ISSUES AND RECOMMENDATIONS .................................................................................................... 34

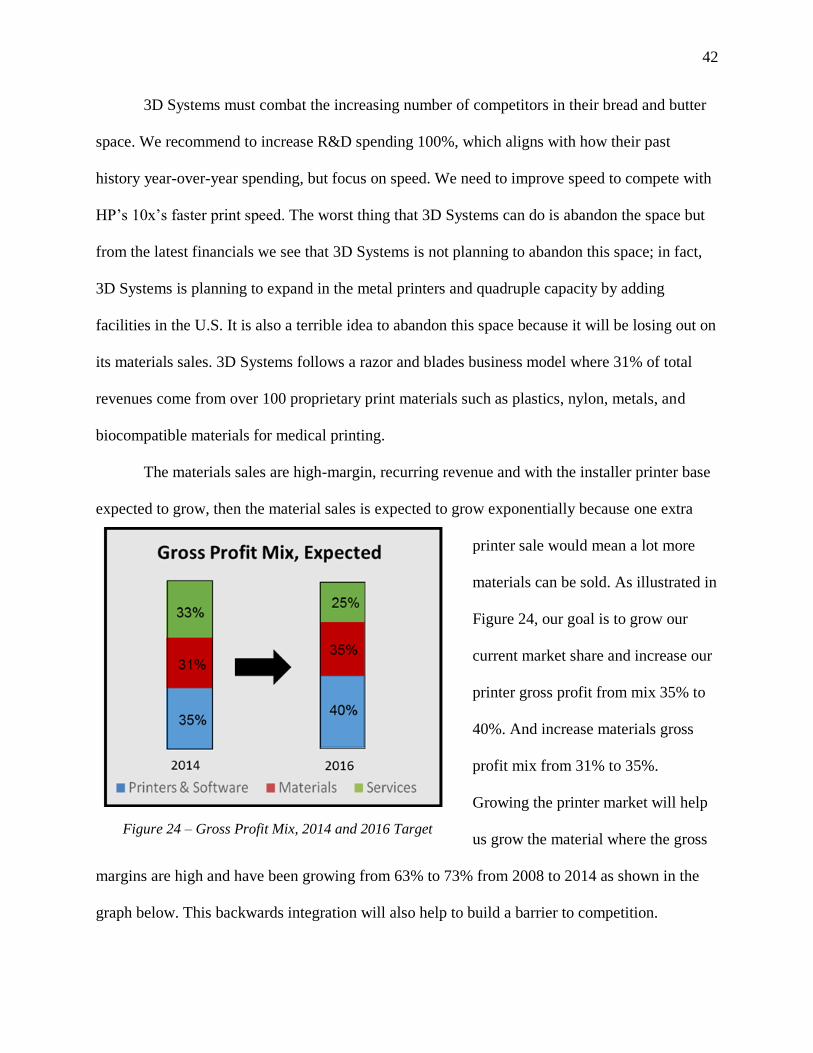

1. Reducing Costs and Growing Revenue by Integration ....................................................................... 34

2. Defending Industrial Market Share ..................................................................................................... 39

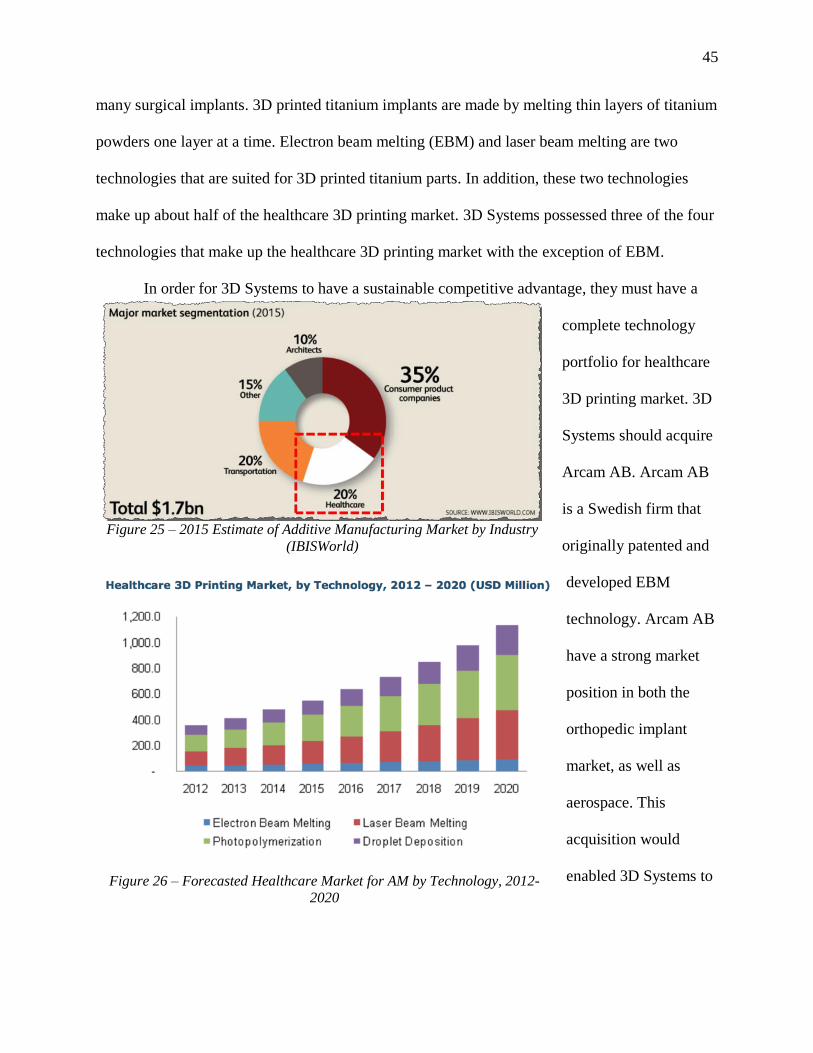

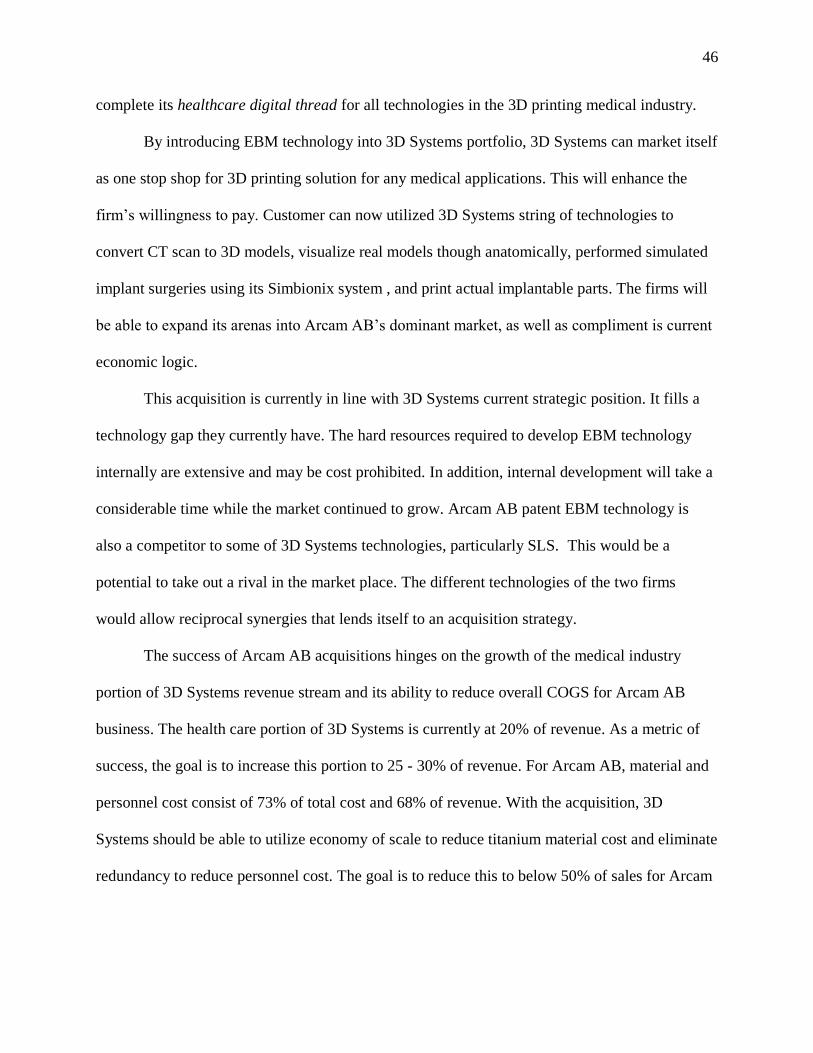

3. Large Growth in Medical Sector ......................................................................................................... 44

4. Stuck-in-the-Middle Professional Software ........................................................................................ 47

5. Stuck-in-the-Middle Consumer Offering ............................................................................................ 53

Implementation Timeline ........................................................................................................................ 57

CONCLUSION ........................................................................................................................................... 58

Appendix A: Additional Figures ................................................................................................................. 60

Appendix B: Financial Analysis ................................................................................................................. 74

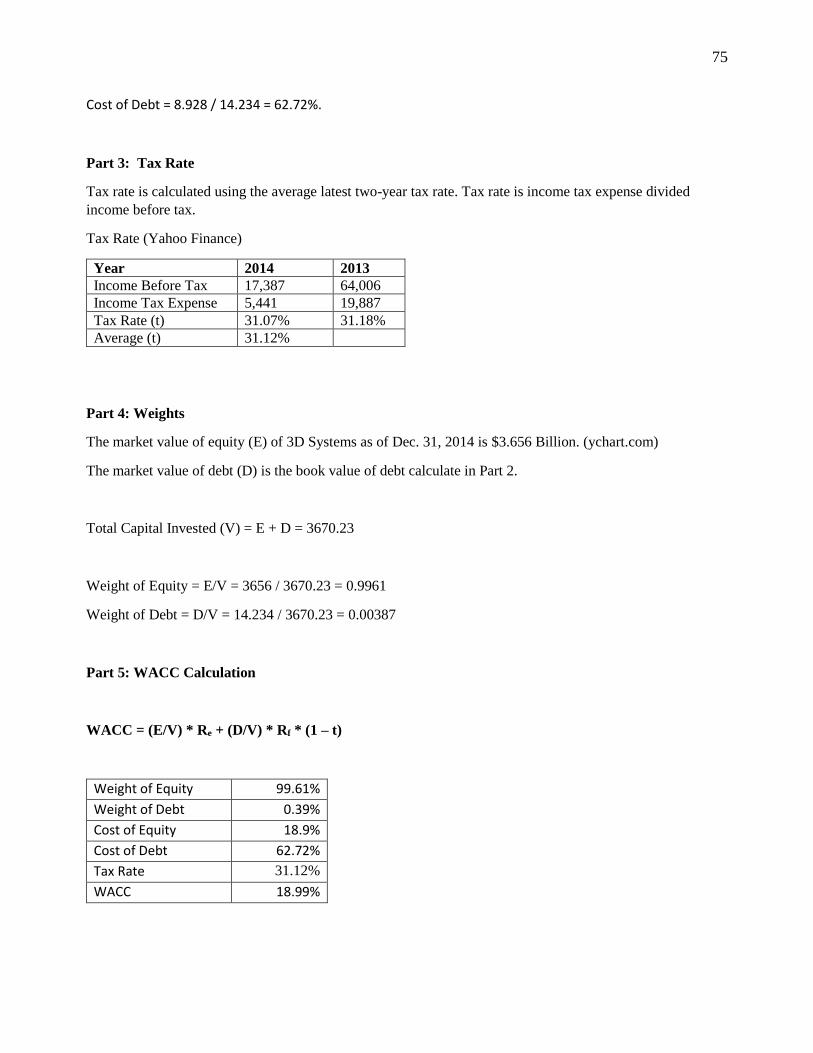

3D Systems WACC Calculation ............................................................................................................. 74

Current Valuation .................................................................................................................................... 76

Valuation of Arcam Acquisition ............................................................................................................. 79

Valuation of 3D Systems After Recommenations .................................................................................. 82

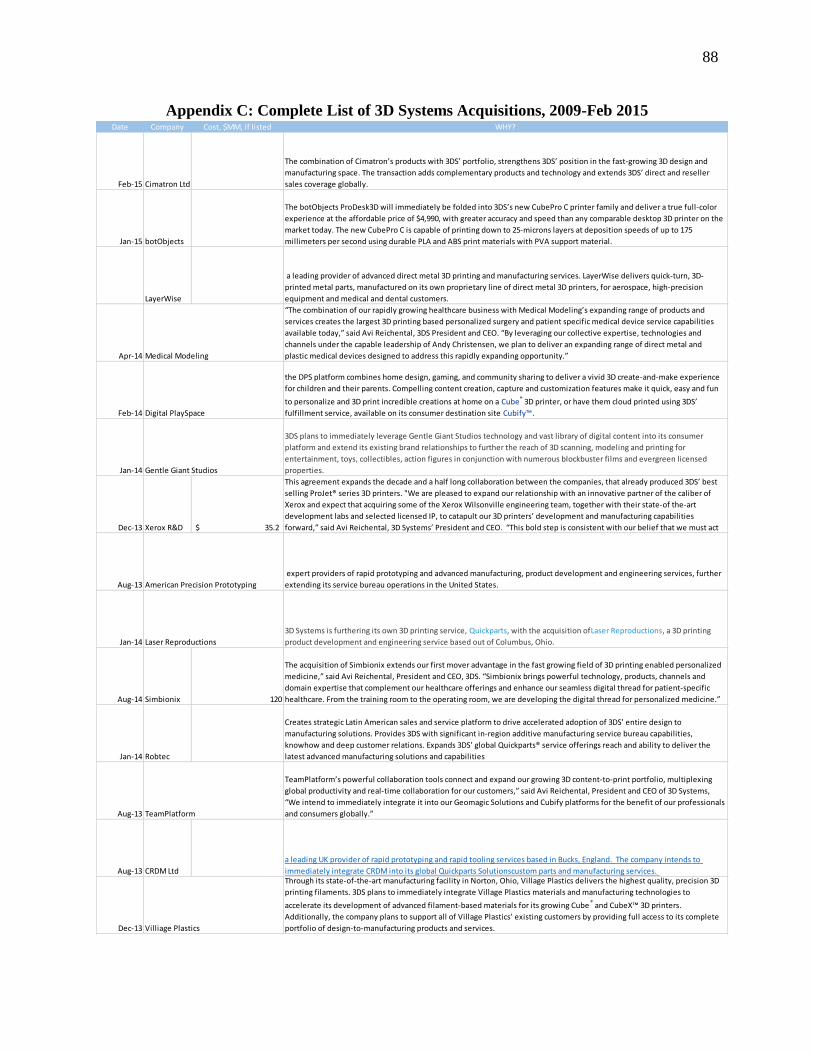

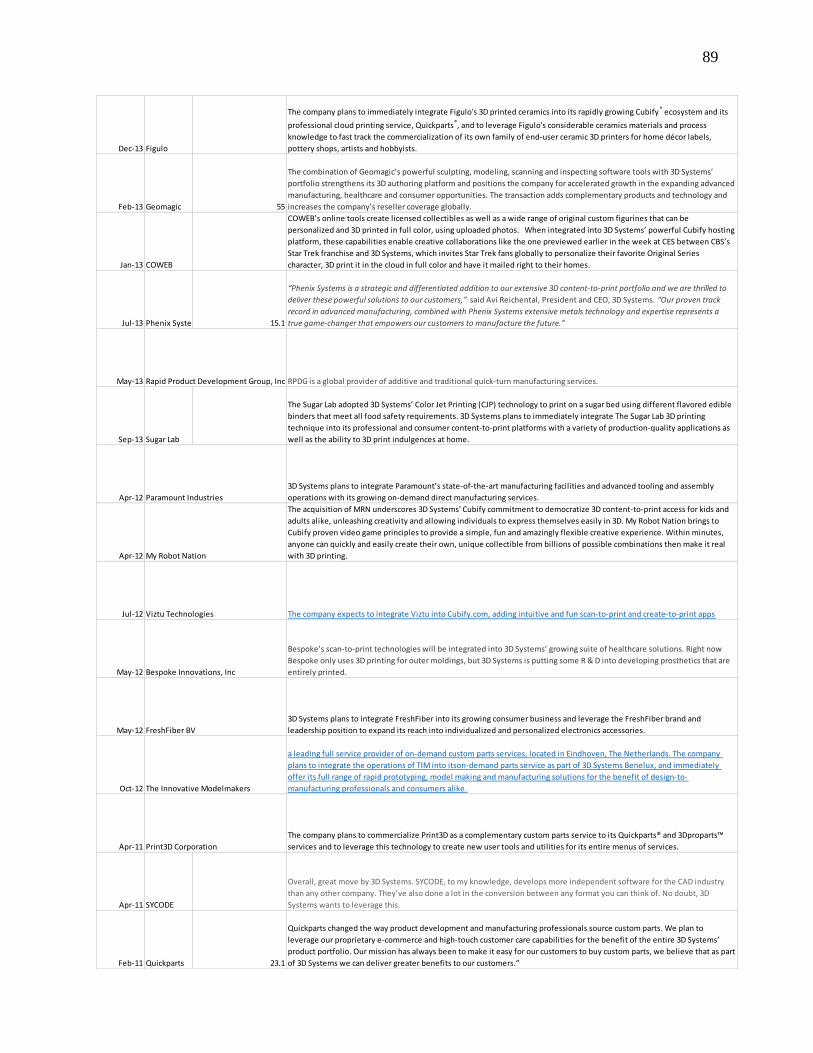

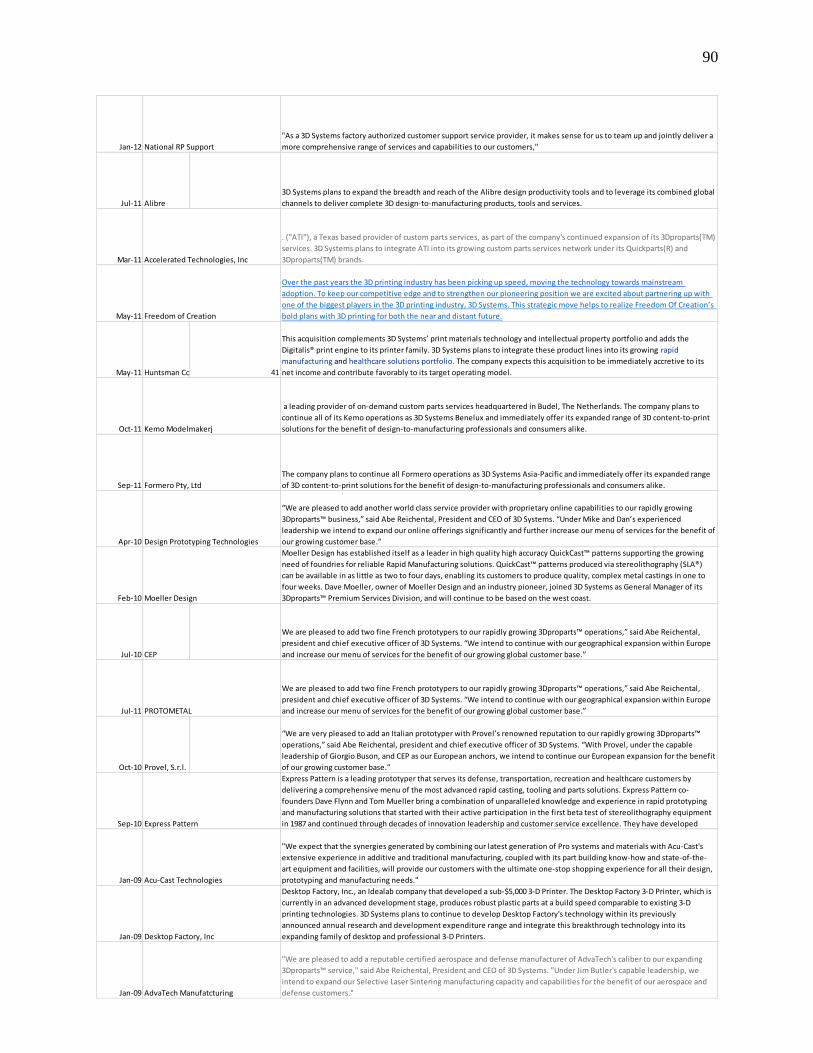

Appendix C: Complete List of 3D Systems Acquisitions, 2009-Feb 2015 ................................................ 88

Works Cited ................................................................................................................................................ 91

List of Figures

Figure 1 – Summary of Additive Manufacturing Technology, Applications, Pricing .................................. 2

Figure 2 – Chuck Hull, Founder ................................................................................................................... 3

Figure 3 – CEO Avi Reichental. ................................................................................................................... 4

Figure 4 – Sampling of 3D Systems Hardware Portfolio ............................................................................. 5

Figure 5 – Private Investment and R&D Expenditure Forecasts .................................................................. 6

Figure 6 – Summary of Primary Segmentation with Examples .................................................................. 10

Figure 7 – Gartner’s Hype Cycle for Additive Manufacturing Applications ............................................. 11

Figure 8 – Additive Manufacturing User Value Chains, Professional (top) and Consumer ....................... 13

Figure 9 – Summary of Analyst Forecasts for Additive Manufacturing Industry ...................................... 13

Figure 10 – Additive Manufacturing’s Industry Life Cycle (IBISWorld) .................................................. 15

Figure 11 – Volatility vs. Growth for Additive Manufacturing .................................................................. 16

Figure 12 – Summary of Porter’s Six Forces Analysis ............................................................................... 17

Figure 13 – Summary of Additive Manufacturing Competitors with 2014 Revenues ............................... 20

Figure 14 – 3D Systems Complete Portfolio of Acquisitions, Through Feb 2015 ..................................... 23

Figure 15 – 3D Systems Current Strategy Diamond ................................................................................... 26

Figure 16 – 3D Systems Current VRIO ...................................................................................................... 27

Figure 17 – 3D Systems Revenue Mix, 2013-2104 .................................................................................... 29

Figure 18 – 3D Systems Income Statement, 2006-2014, $MM .................................................................. 30

Figure 19 – 3D Systems Income Statement, 2006-2014, as % of Revenue ................................................ 31

Figure 20 – 3D Systems Profit Margins and Mix, by Offering, 2008-2014 ............................................... 31

Figure 21 – 3D Systems Cash Balance and Spending on Acquisitions ...................................................... 36

Figure 22 – 3D Systems and Stratasys ROA, 2009-2014 ........................................................................... 37

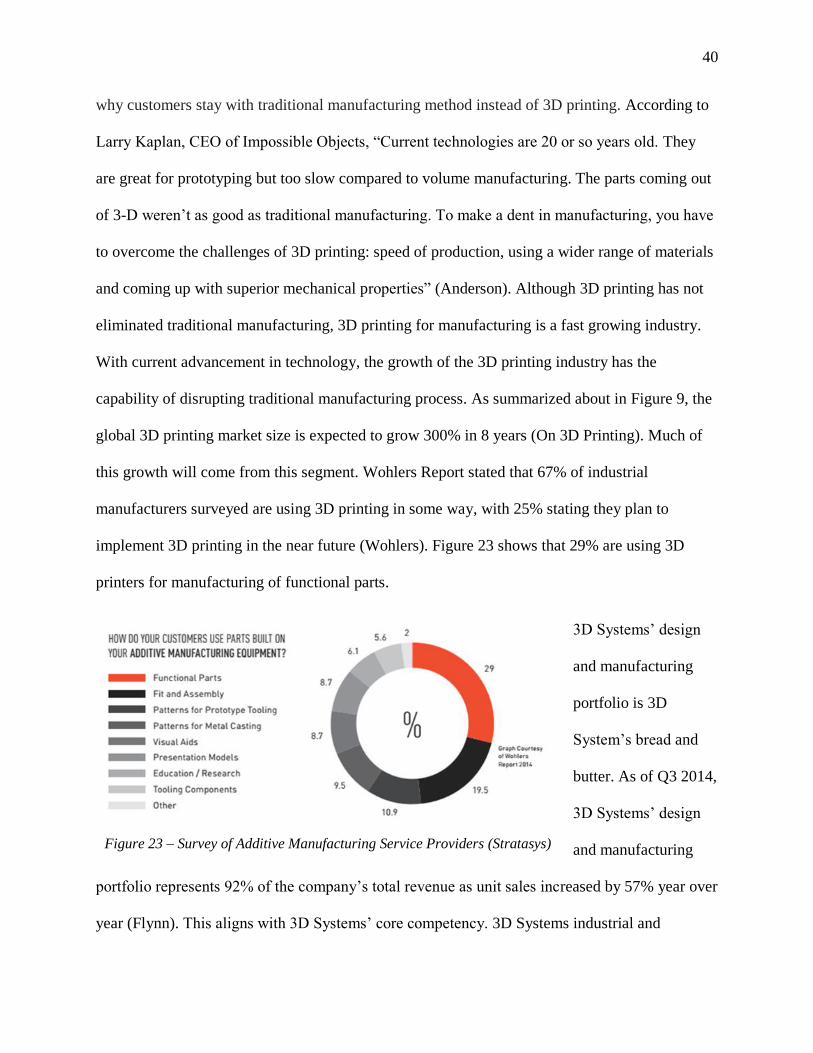

Figure 23 – Survey of Additive Manufacturing Service Providers (Stratasys) ........................................... 40

Figure 24 – Gross Profit Mix, 2014 and 2016 Target ................................................................................. 42

Figure 25 – 2015 Estimate of Additive Manufacturing Market by Industry (IBISWorld) ......................... 45

Figure 26 – Forecasted Healthcare Market for AM by Technology, 2012-2020 ........................................ 45

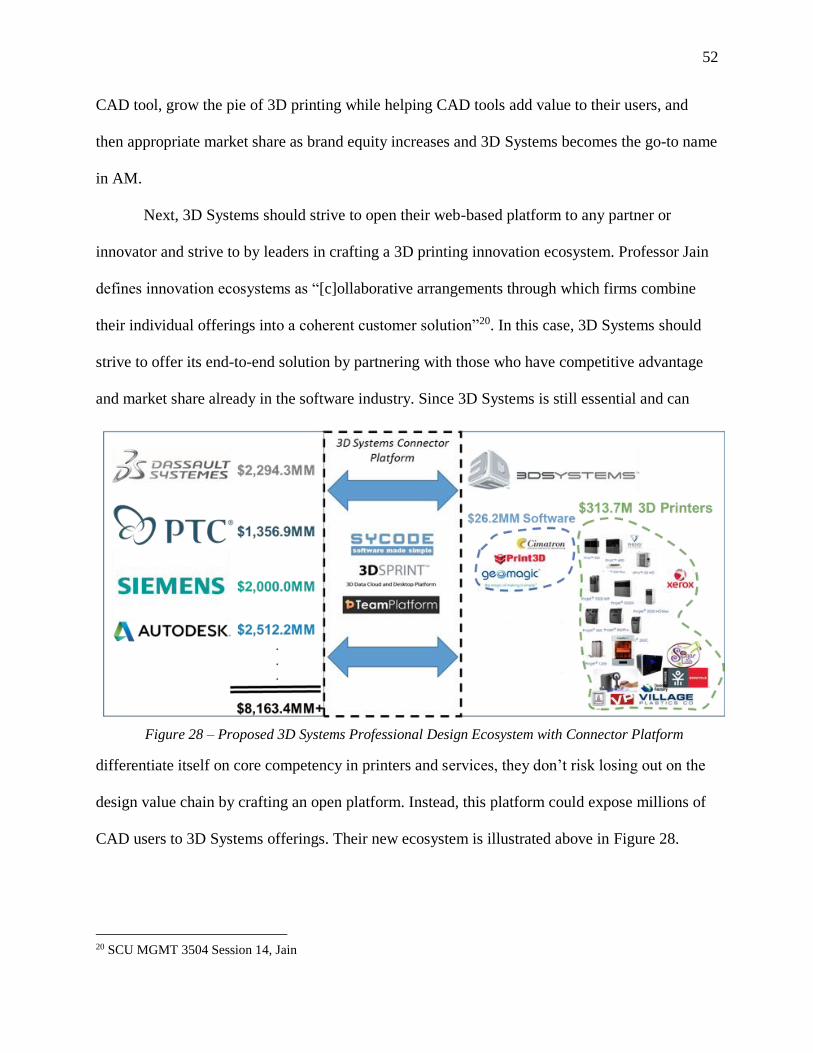

Figure 27 – 3D Systems Current Professional Design Ecosystem ............................................................. 50

Figure 28 – Proposed 3D Systems Professional Design Ecosystem with Connector Platform .................. 52

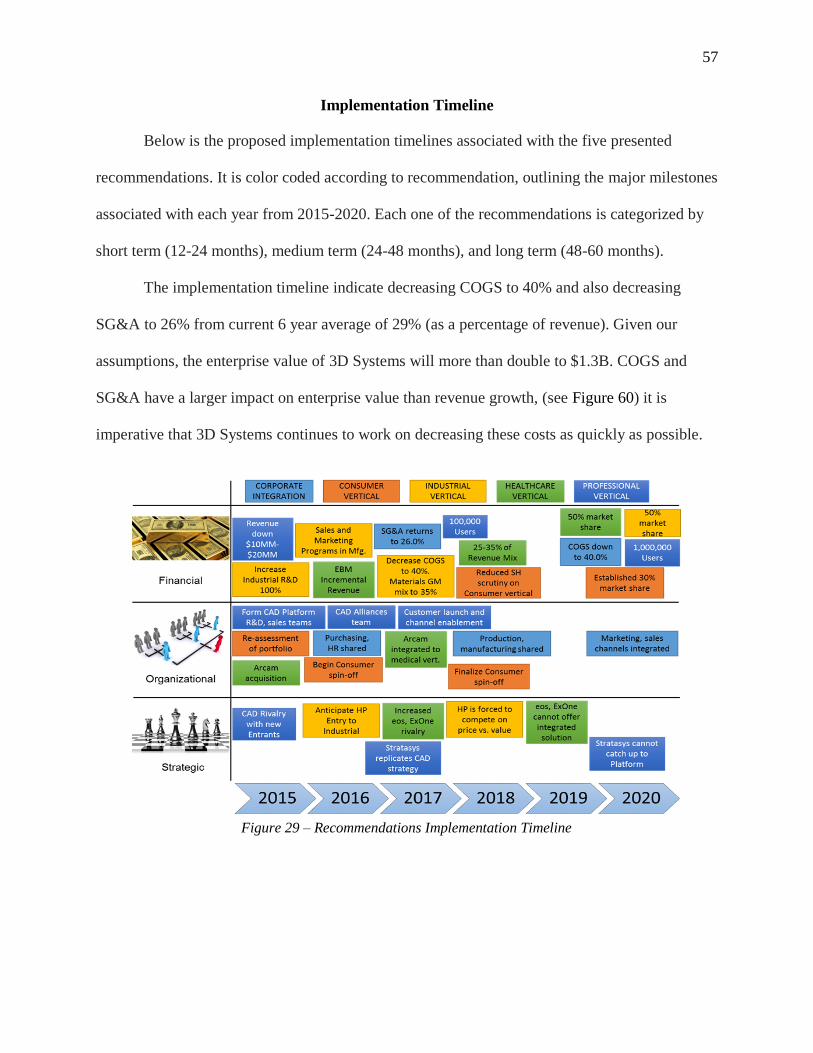

Figure 29 – Recommendations Implementation Timeline .......................................................................... 57

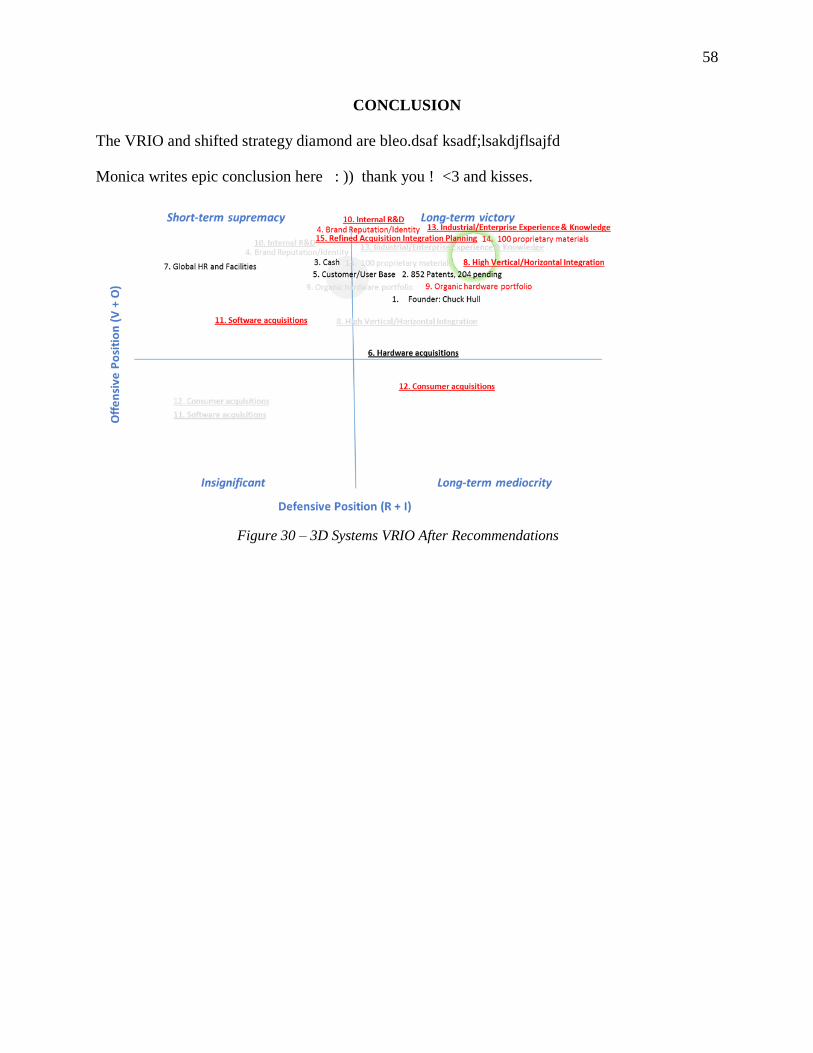

Figure 30 – 3D Systems VRIO After Recommendations ........................................................................... 58

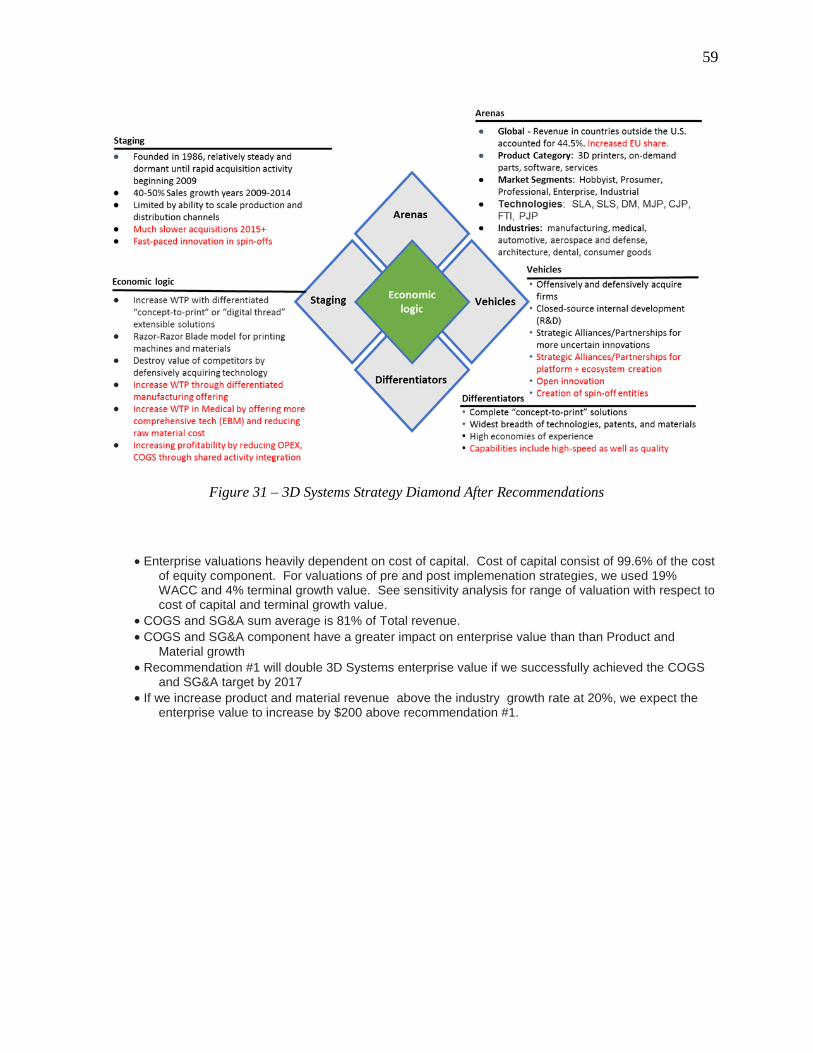

Figure 31 – 3D Systems Strategy Diamond After Recommendations ........................................................ 59

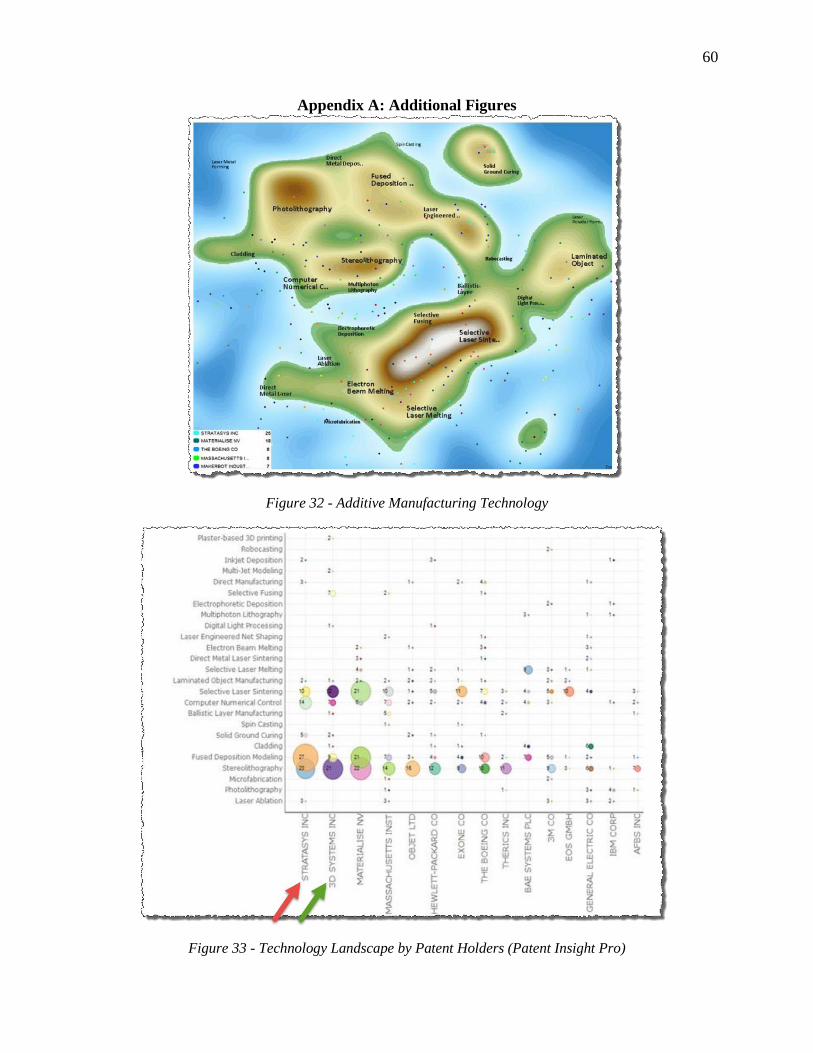

Figure 32 - Additive Manufacturing Technology ....................................................................................... 60

Figure 33 - Technology Landscape by Patent Holders (Patent Insight Pro) ............................................... 60

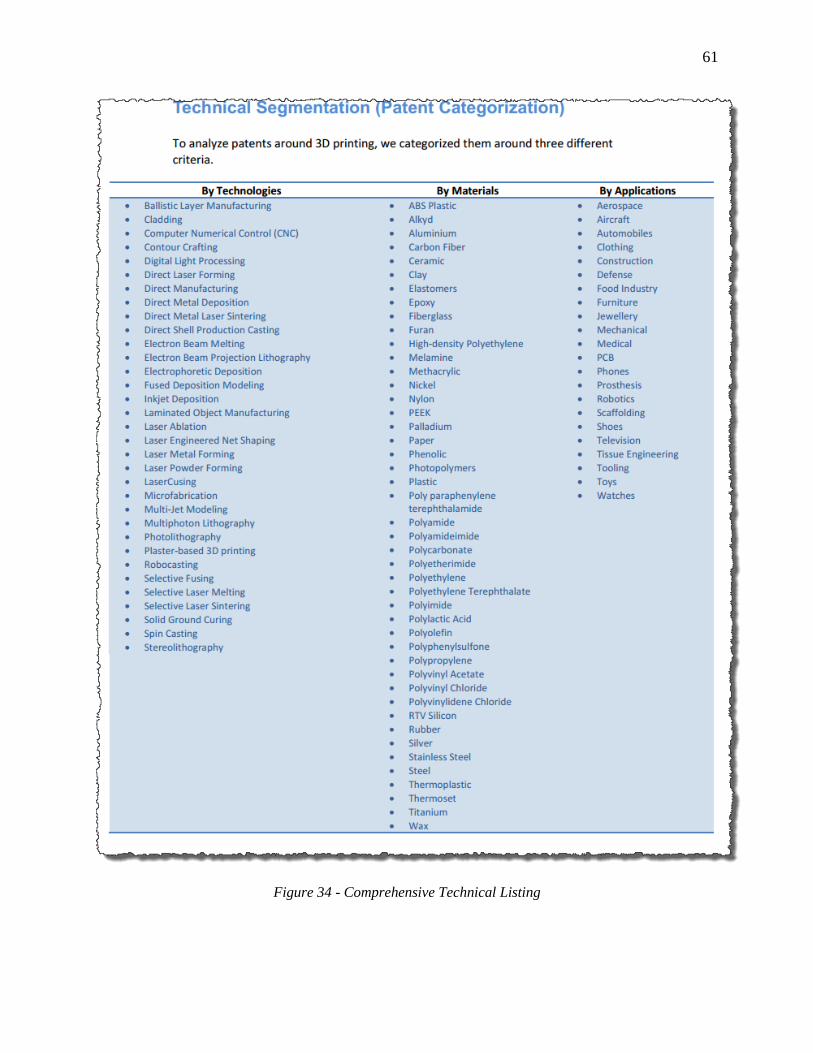

Figure 34 - Comprehensive Technical Listing ............................................................................................ 61

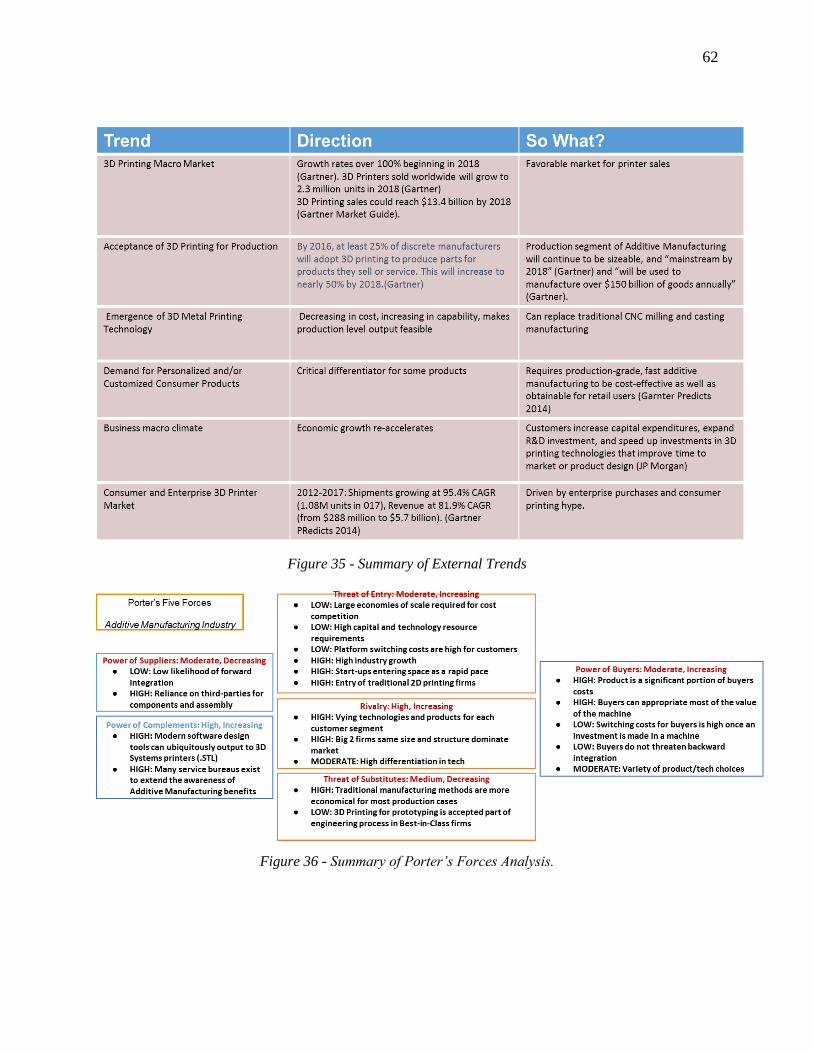

Figure 35 - Summary of External Trends ................................................................................................... 62

Figure 36 - Summary of Porter’s Forces Analysis. ..................................................................................... 62

Figure 37 - Summary of 3D Printing Application Hype (Gartner) ............................................................. 63

Figure 38 – Example of Healthcare “Digital Thread” and Trailing 9 Months Revenue from Vertical ...... 63

Figure 39 - Summary of 3D Sytems SWOT Analysis ................................................................................ 64

Figure 40 - 3D Systems Financials, through 2014 ...................................................................................... 65

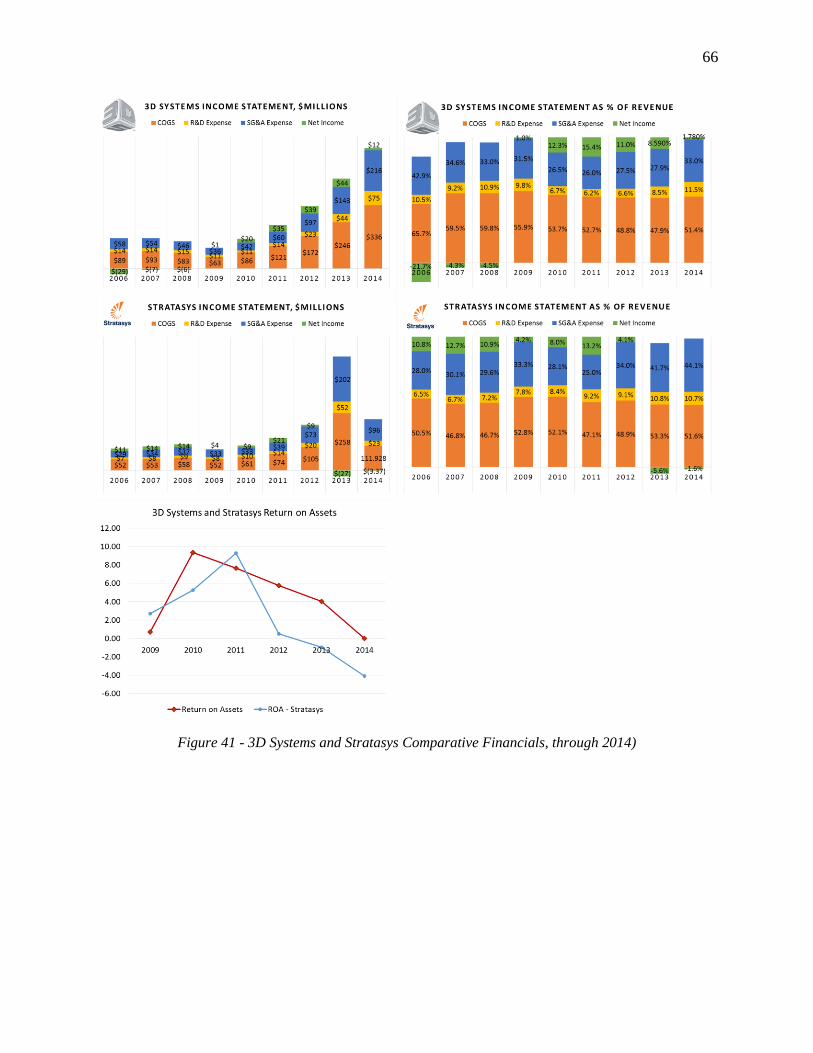

Figure 41 - 3D Systems and Stratasys Comparative Financials, through 2014) ......................................... 66

Figure 42 - Articles Showing New Entrants to Industrial Segment ............................................................ 67

Figure 43 - 3D Systems stock performance vs. Stratasys, S&P 500 Index, Dec 21 2012 through Feb 26

2015 ............................................................................................................................................................ 68

Figure 44 – Summary of 3D Systems Major Issues, Opportunities, and Indicators ................................... 68

Figure 45 - Set of Options Considered for Each Issue and Opportunity..................................................... 69

Figure 46 – Highest User-Rated Industrial Printers, Indicating 3D Systems Products (3D Hubs) ............. 70

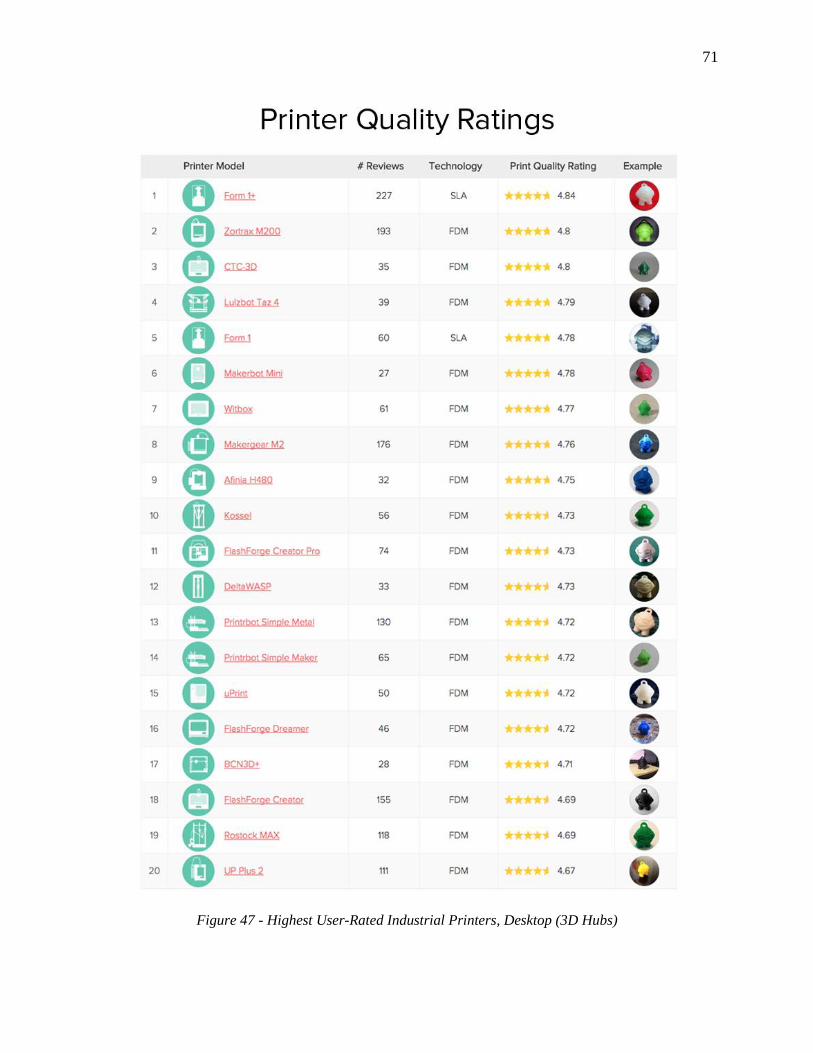

Figure 47 - Highest User-Rated Industrial Printers, Desktop (3D Hubs) ................................................... 71

Figure 48 – Professional CAD User Survey (Market Share) and Competitor Revenues (CIMdata)

(Warfield) .................................................................................................................................................... 72

Figure 49 - Strategic Tests for Strategic Success ........................................................................................ 73

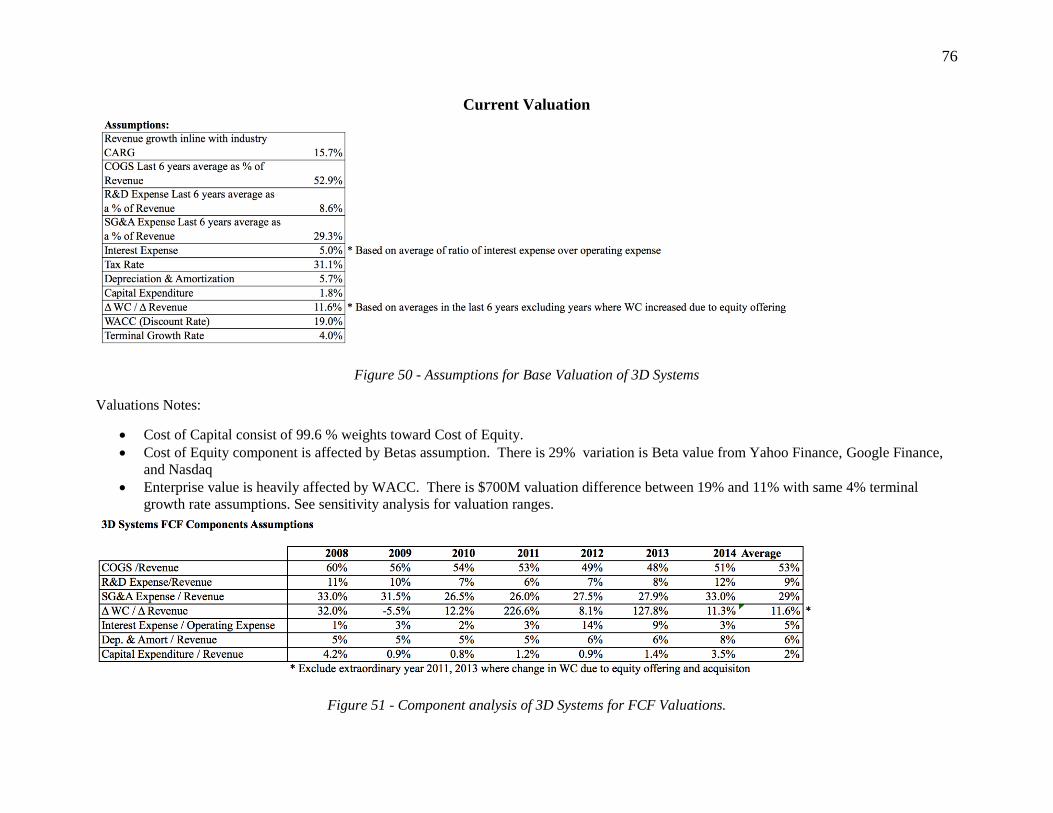

Figure 50 - Assumptions for Base Valuation of 3D Systems ..................................................................... 76

Figure 51 - Component analysis of 3D Systems for FCF Valuations. ........................................................ 76

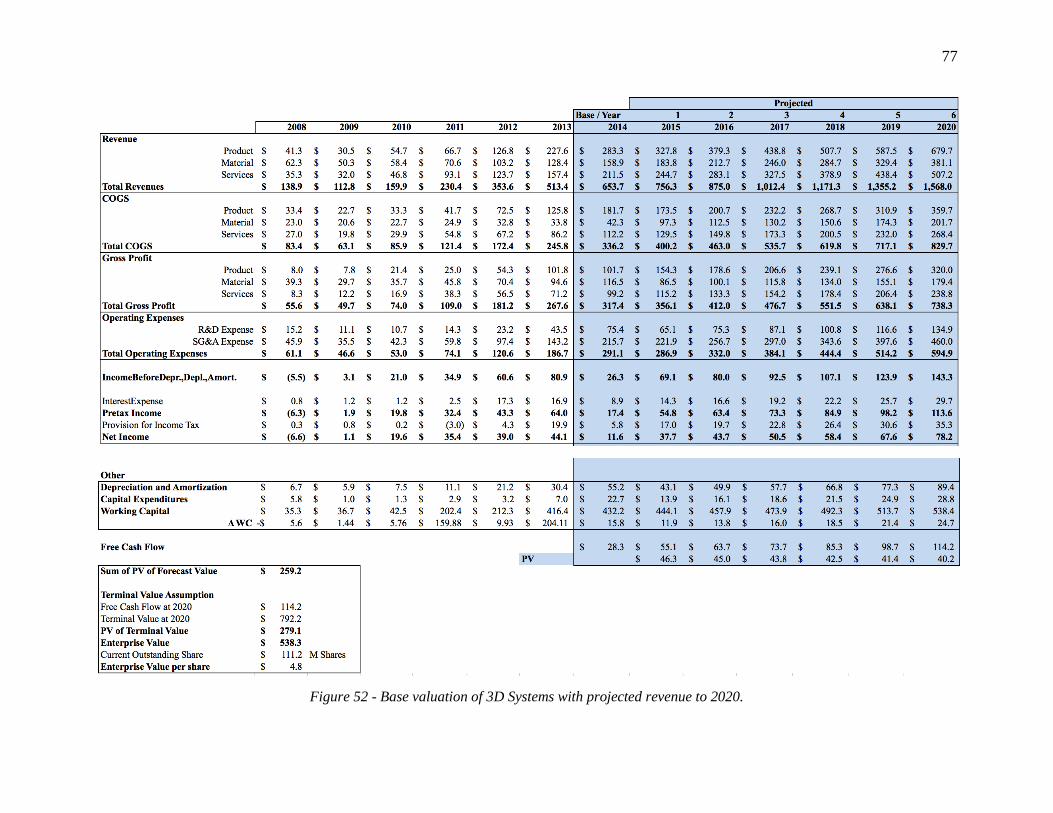

Figure 52 - Base valuation of 3D Systems with projected revenue to 2020. .............................................. 77

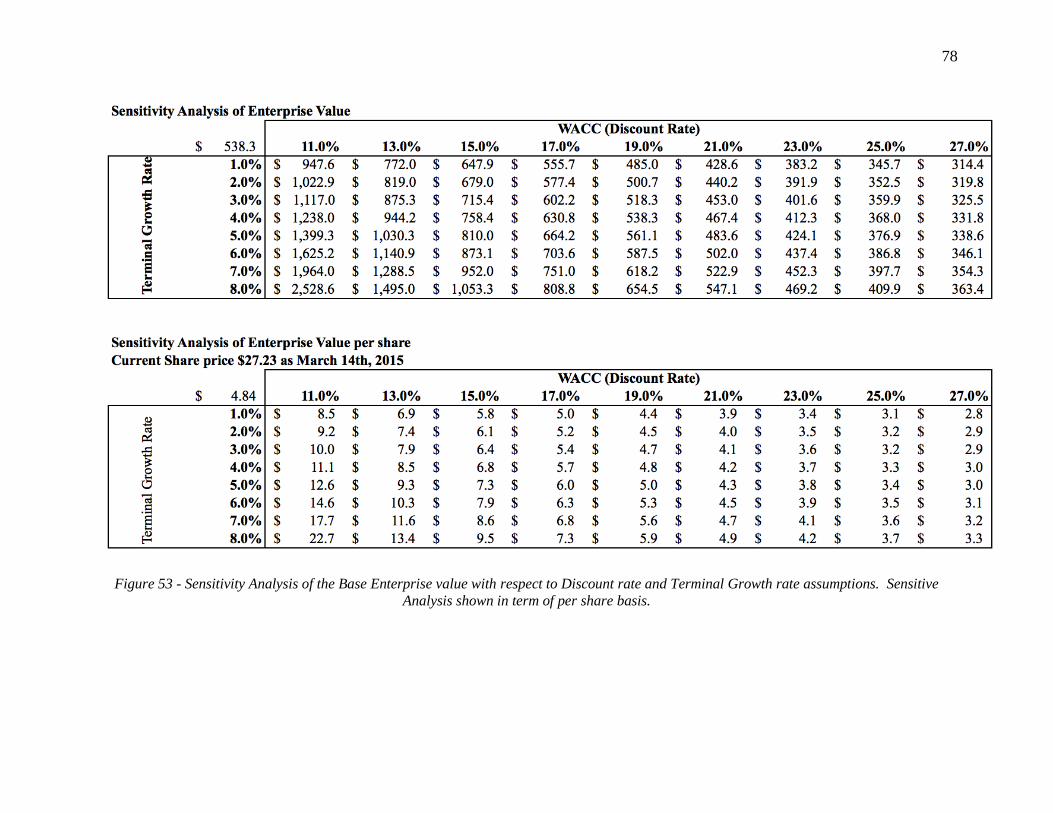

Figure 53 - Sensitivity Analysis of the Base Enterprise value with respect to Discount rate and Terminal

Growth rate assumptions. Sensitive Analysis shown in term of per share basis. ...................................... 78

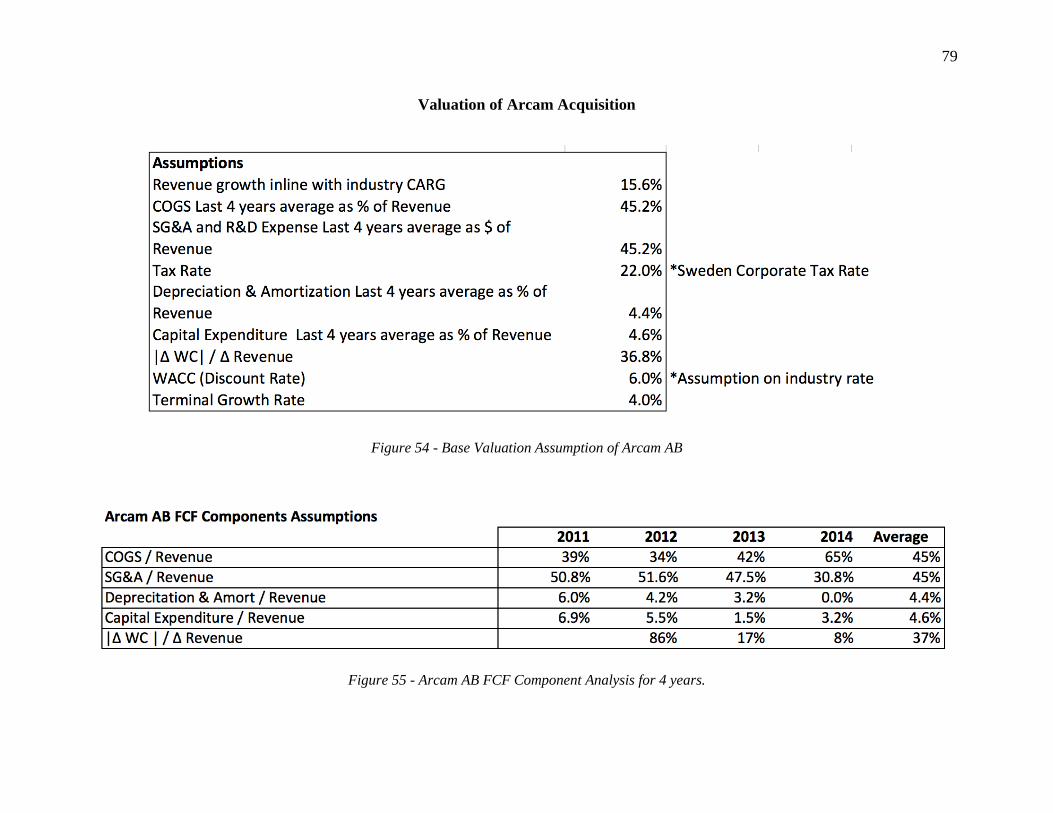

Figure 54 - Base Valuation Assumption of Arcam AB .............................................................................. 79

Figure 55 - Arcam AB FCF Component Analysis for 4 years. ................................................................... 79

Figure 56 - Base valuation of Arcam AB using FCF Analysis .................................................................. 80

Figure 57 - Sensitivity Analysis of Arcam AB Enterprise value with respect to Discount Rate and

Terminal Growth Rate Assumptions ........................................................................................................... 81

Figure 58 - Valuation Assumptions changes based on successful implementation of synergies strategies.

Target COGS is 40% of Revenue and SG&A is 26% of Revenue. ............................................................ 81

Figure 59 - Valuation worksheet for 3D Systems based on successful implementation of targeted

strategies. .................................................................................................................................................... 82

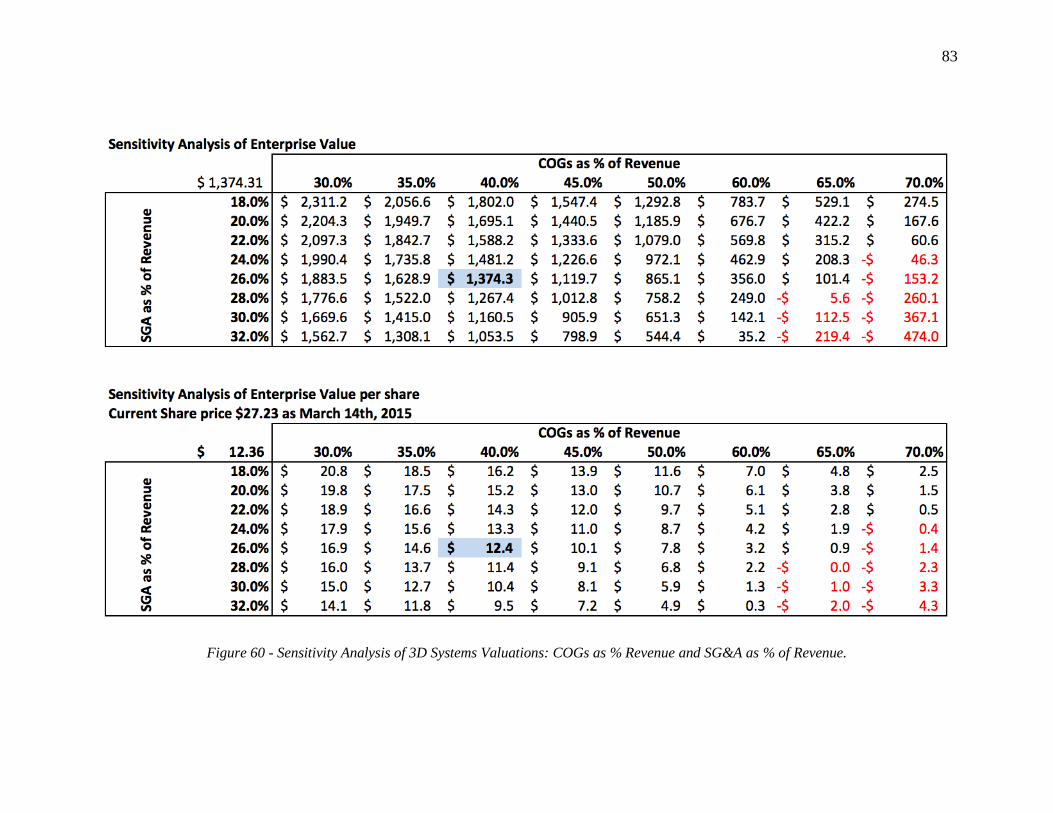

Figure 60 - Sensitivity Analysis of 3D Systems Valuations: COGs as % Revenue and SG&A as % of

Revenue. ..................................................................................................................................................... 83

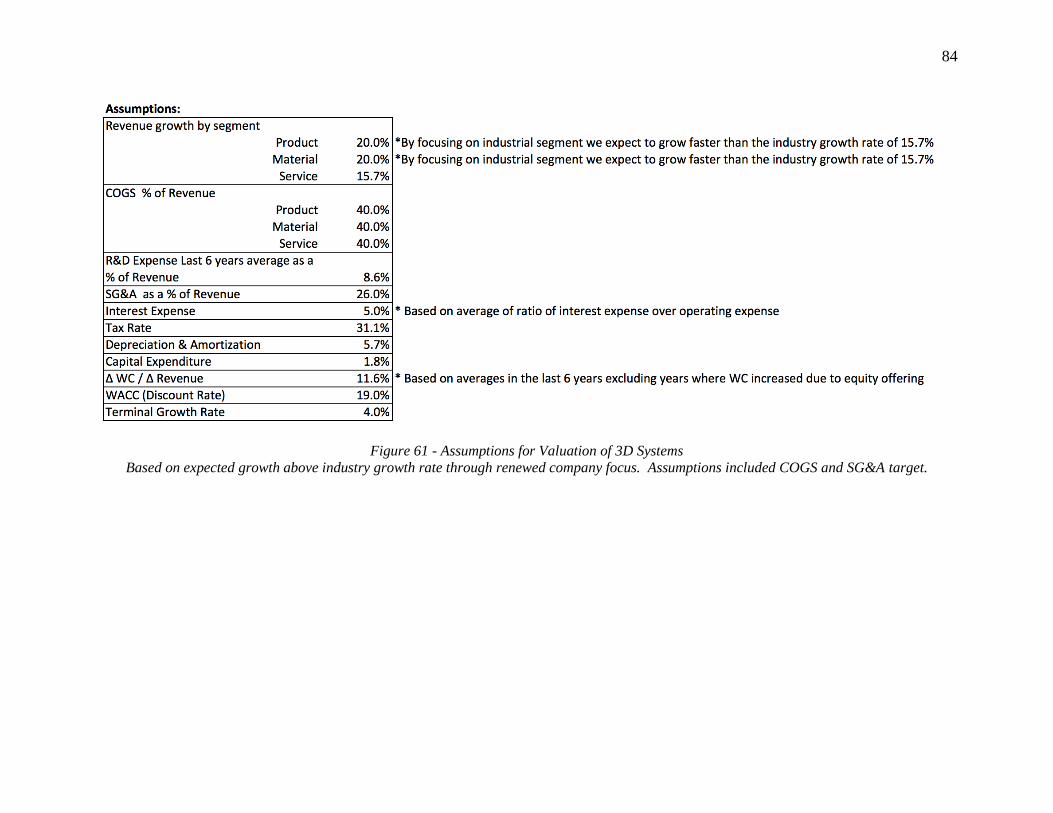

Figure 61 - Assumptions for Valuation of 3D Systems .............................................................................. 84

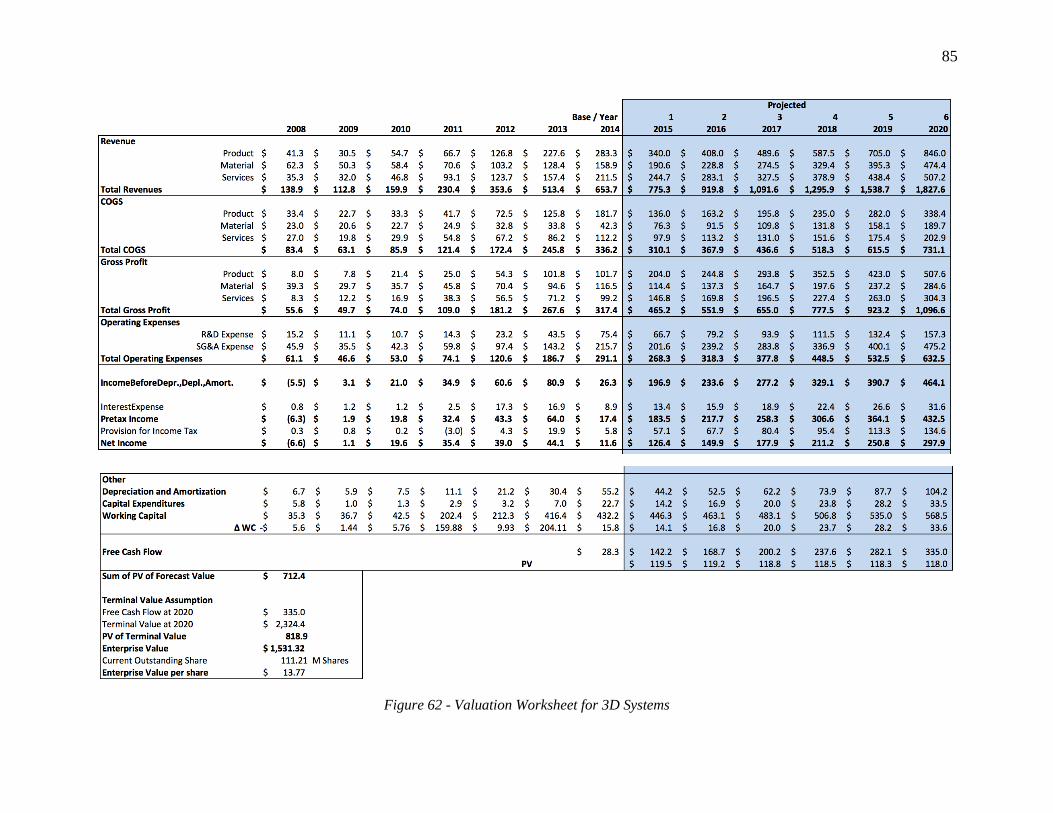

Figure 62 - Valuation Worksheet for 3D Systems ...................................................................................... 85

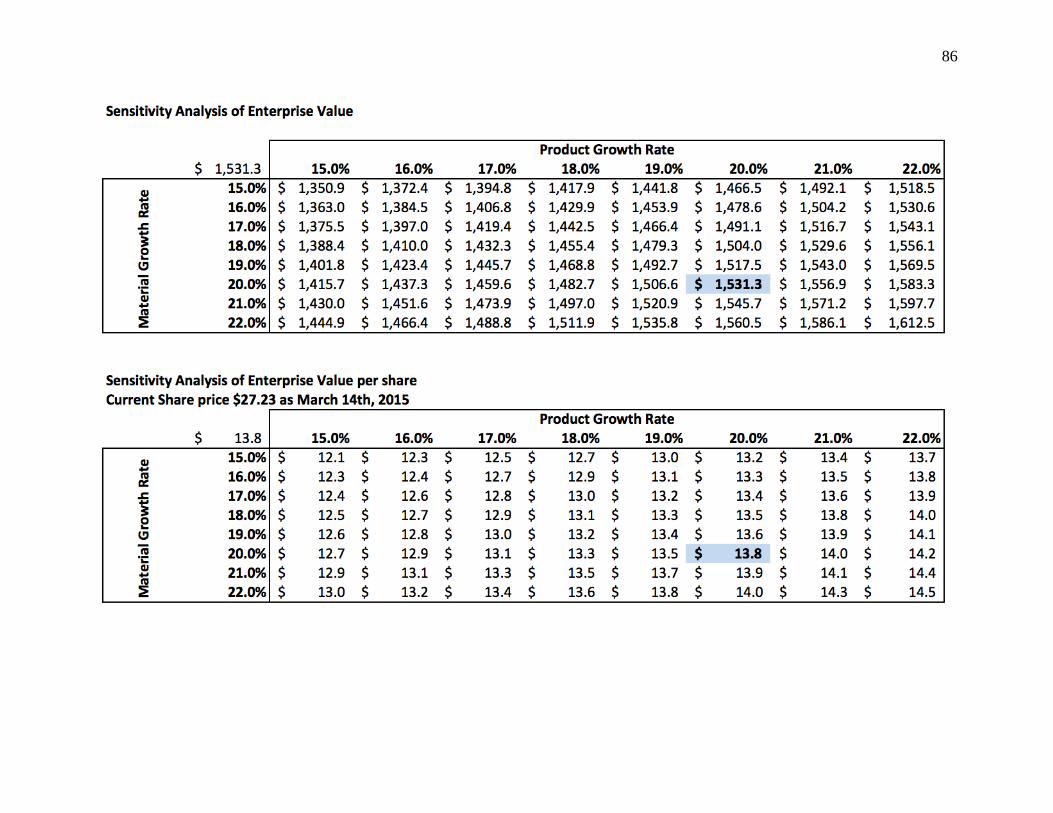

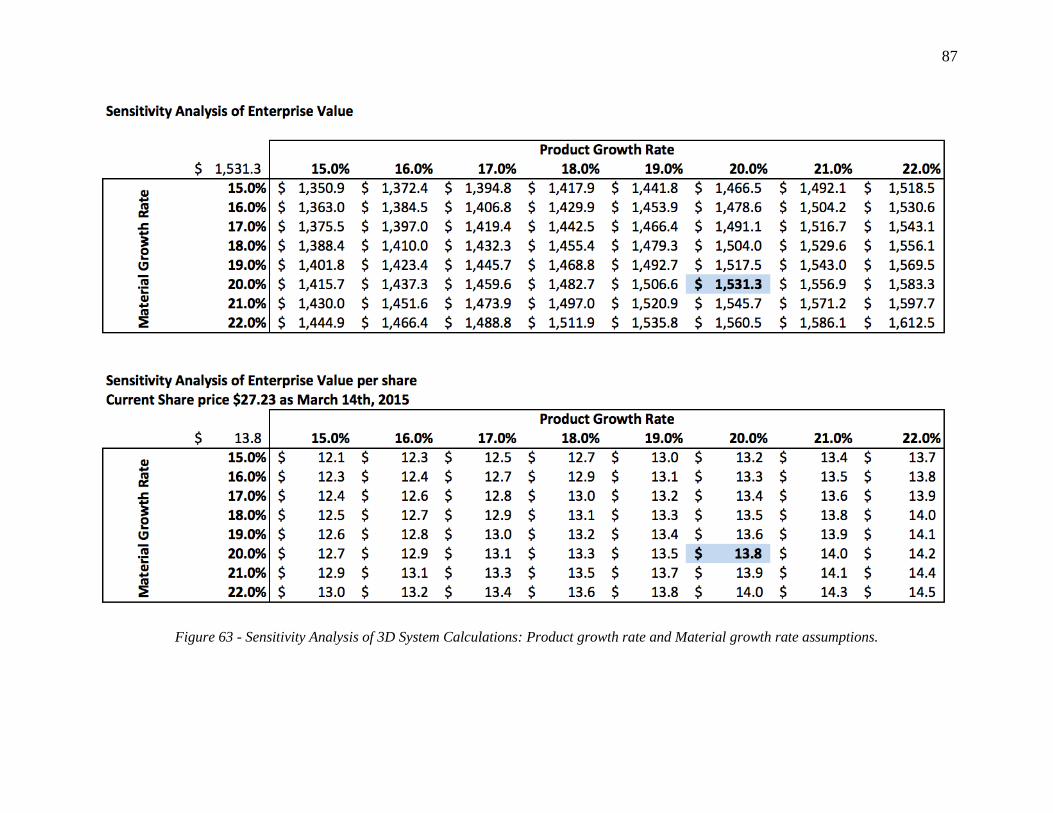

Figure 63 - Sensitivity Analysis of 3D System Calculations: Product growth rate and Material growth rate

assumptions. ................................................................................................................................................ 87

1

BACKGROUND

Additive Manufacturing Technical-Application Summary

Some say the first product ever product printed was a prototype of a small eye-wash cup

in 1984 (3D Printer World), a legacy that remains today as prototyping is still the predominant

additive manufacturing use case by designers and engineers. Early commercialization indicated

viability beyond prototyping: as print speeds increased in the late 1980s, automobile and

aerospace industries took early interest for manufacturing support such as generating complex

wax models for metal casting. For the manufacturing industry, AM increasingly offered a

potential substitution for traditional subtractive and formative manufacturing methods3 due to

ever-increasing variety of materials, including high-strength metals, as well as reductions in cost.

In the last two decades, industry improvements have focused on new technologies as well as

enhancing order-winning features such as precision, speed, and material (Hessman).

Today’s additive manufacturing industry has grown far beyond prototyping and niche

manufacturing to include applications in personalized medicine, mass customized retail goods,

desktop consumer full-service bureaus and packaged software solutions marketed towards a

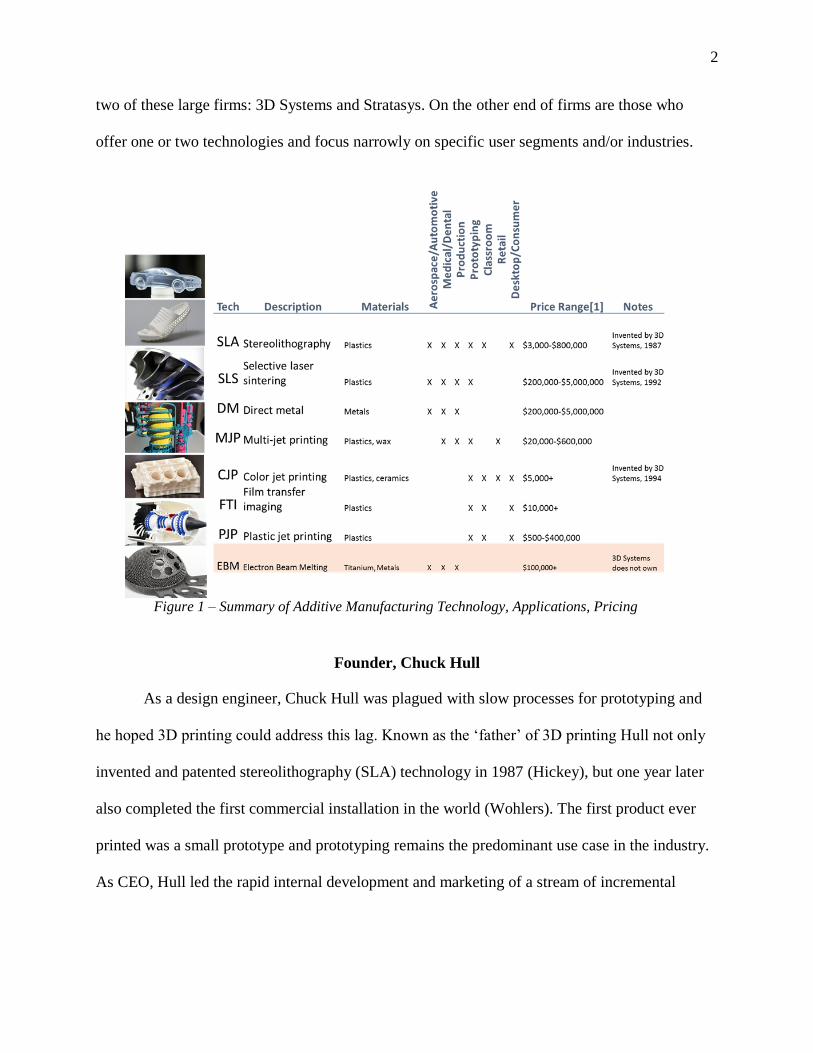

variety of applications in various lifecycle stages. Below in Figure 1 is a snapshot of the most

prolific 3D printing technologies in commercial use as of 20154. The implication of this

spectrum of technology is that it creates a possibility for multiple corporate strategies for

industry players. 3D Systems is on one end of the spectrum: owning technology in 7 of the above

8 architectures allows them to serve a wide variety of customers. At this end of the market, there

are high barriers to entry and high technological requirements, which is why there are really only

3 subtractive is cutting away material from raw stock: machining, milling, turning; formative is conforming raw

material to shape: injection molding, casting, stamping

4 More comprehensive technical background can be found Figure 32 and Figure 33.

2

two of these large firms: 3D Systems and Stratasys. On the other end of firms are those who

offer one or two technologies and focus narrowly on specific user segments and/or industries.

Figure 1 – Summary of Additive Manufacturing Technology, Applications, Pricing

Founder, Chuck Hull

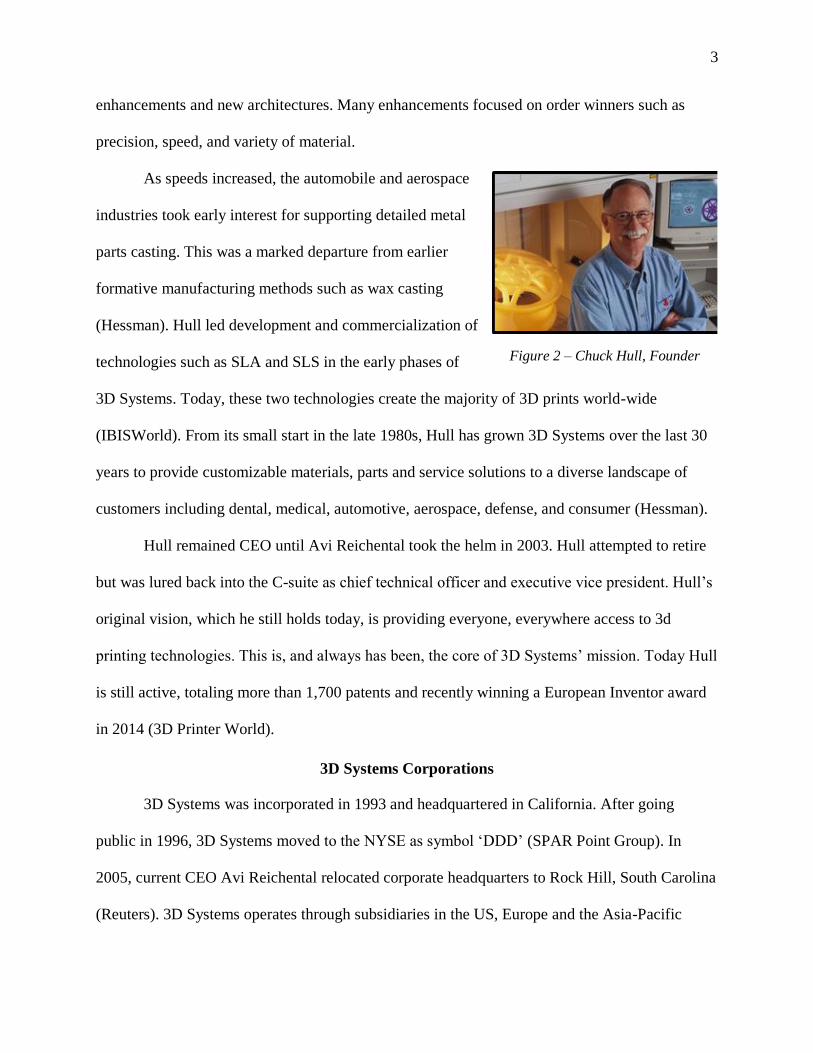

As a design engineer, Chuck Hull was plagued with slow processes for prototyping and

he hoped 3D printing could address this lag. Known as the ‘father’ of 3D printing Hull not only

invented and patented stereolithography (SLA) technology in 1987 (Hickey), but one year later

also completed the first commercial installation in the world (Wohlers). The first product ever

printed was a small prototype and prototyping remains the predominant use case in the industry.

As CEO, Hull led the rapid internal development and marketing of a stream of incremental

3

enhancements and new architectures. Many enhancements focused on order winners such as

precision, speed, and variety of material.

As speeds increased, the automobile and aerospace

industries took early interest for supporting detailed metal

parts casting. This was a marked departure from earlier

formative manufacturing methods such as wax casting

(Hessman). Hull led development and commercialization of

technologies such as SLA and SLS in the early phases of

3D Systems. Today, these two technologies create the majority of 3D prints world-wide

(IBISWorld). From its small start in the late 1980s, Hull has grown 3D Systems over the last 30

years to provide customizable materials, parts and service solutions to a diverse landscape of

customers including dental, medical, automotive, aerospace, defense, and consumer (Hessman).

Hull remained CEO until Avi Reichental took the helm in 2003. Hull attempted to retire

but was lured back into the C-suite as chief technical officer and executive vice president. Hull’s

original vision, which he still holds today, is providing everyone, everywhere access to 3d

printing technologies. This is, and always has been, the core of 3D Systems’ mission. Today Hull

is still active, totaling more than 1,700 patents and recently winning a European Inventor award

in 2014 (3D Printer World).

3D Systems Corporations

3D Systems was incorporated in 1993 and headquartered in California. After going

public in 1996, 3D Systems moved to the NYSE as symbol ‘DDD’ (SPAR Point Group). In

2005, current CEO Avi Reichental relocated corporate headquarters to Rock Hill, South Carolina

(Reuters). 3D Systems operates through subsidiaries in the US, Europe and the Asia-Pacific

Figure 2 – Chuck Hull, Founder

4

regions, selling printers, materials, software, and services (3D Systems). Roughly half of 3D

Systems’ revenue are from global operations and the firm plans to continue to expand facilities

and manufacturing globally (3D Systems).

Although they had begun an acquisition strategy in 2001 with an initial handful of service

bureaus, in 2009 3D Systems initiated their first cycle of rapidly raising and spending cash on

acquisitions. With over 45 acquisitions between 2009 and 2015, their portfolios of hardware,

software, and service bureaus are all extensive. In 2014 alone, 3D Systems spent $354.4 MM in

cash on acquisitions; up by 113% over 2013 (Barney). 3D Systems is pursuing these acquisitions

not only to grow revenue and diversify but also for the potential to increase willingness to pay

with integrated solutions. They have acquired software companies, on-demand parts service

providers, competitors in hardware and the print materials

businesses, scanners, product development and

manufacturing firms, cloud technology solutions, and

medical device designers. This has enabled 3D Systems to

differentiate itself by offering not just hardware and

materials, but complete “concept-to-print” solutions for

specific verticals, which they refer to these as “digital threads” (3D Systems).

3D Systems’ current value proposition is to: “provide the most advanced and

comprehensive 3D design-to-manufacturing solutions, including 3D printers, print materials and

cloud sourced custom parts. Our powerful digital thread, a seamless information exchange across

design and manufacturing, empowers professionals and consumers everywhere to bring their

ideas to life in material choices including plastics, metals, ceramics and edibles.” (3D Systems).

Figure 3 – CEO Avi Reichental.

5

3D Systems describes their mission as broad democratization of AM technology from consumers

to industrial manufacturing5,

Business Definition and Mission Statement

3D Systems provides a “concept-to-print” solution that participates in all steps of the

value chain including design, development, manufacturing and marketing of 3D printers,

materials, parts, and complementary products and services. Though 3D Systems offers nearly 50

unique printers [Figure XX], their core hardware uses stereolithography (SLA) printers, selective

laser sintering (SLS) printers, multi-jet modeling (MJM) printers, film transfer imaging (FTI)

printers, selective laser melting ( SLM) printers, and plastic jet printers (PJP). 3D Systems also

provides content creation using CAD software and digital workflow preparation and

management software tools through content management (GlobalData).

3D Systems uses materials including plastics, metals, ceramics and edibles. In addition to

printing, their “products and services replace and complement traditional methods and reduce the

time and cost of designing new products by printing real parts directly from digital input. These

solutions are used to rapidly design, create, communicate, prototype or produce real parts,

empowering customers to manufacture the future,” (3D Systems).

3D Systems defines itself as a pioneer of 3D design and fabrication--an appropriate

distinction considering the legacy of Chuck Hull. They aim to provide the most advanced and

5http://www.3dsystems.com/es/3d-printers

Figure 4 – Sampling of 3D Systems Hardware Portfolio

6

comprehensive solutions that democratize 3D printing. 3D Systems hopes this more open

process allows users to, “rapidly design, create, communicate, plan, guide, prototype and

produce functional parts, devices and assemblies” (3D Systems). Ultimately, 3D Systems is

betting that their integrated design threads (end-to-end experiences in specific segments) and

user’s ability to enter into any part of the 3D printing process with 3D Systems will eliminate

technical barriers to adoption of 3D Systems tools and platforms.

EXTERNAL ANALYSIS

General Environment

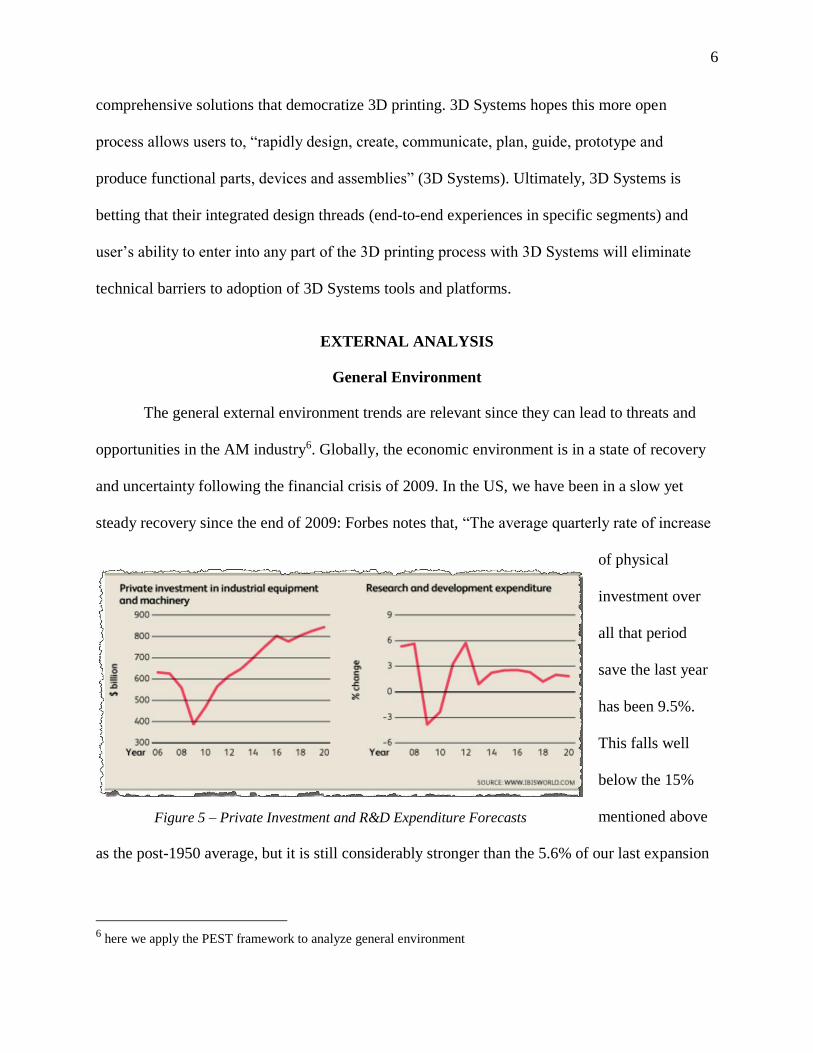

The general external environment trends are relevant since they can lead to threats and

opportunities in the AM industry6. Globally, the economic environment is in a state of recovery

and uncertainty following the financial crisis of 2009. In the US, we have been in a slow yet

steady recovery since the end of 2009: Forbes notes that, “The average quarterly rate of increase

of physical

investment over

all that period

save the last year

has been 9.5%.

This falls well

below the 15%

mentioned above

as the post-1950 average, but it is still considerably stronger than the 5.6% of our last expansion

6 here we apply the PEST framework to analyze general environment

Figure 5 – Private Investment and R&D Expenditure Forecasts

7

(2002-2007)” (Forbes). Ideally, expansion includes enterprise and industrial customers

continuing to spend on capital equipment such as printer. Firms who increase their capital

expenditures and expand R&D investment are target customers for AM. The benefits of AM,

including decreasing time to market and innovating product design, are becoming more

recognized, and adoption of the technology has become standard in manufacturing processes (JP

Morgan). Globally, investment in industrial equipment as well as R&D is projected to grow

steadily through 2020 (IBISWorld). In an expanding economy 3D Systems has a chance to

exploit their strengths in industrial offerings, as well as capture consumers who might be able

and willing to experiment with desktop printing. This growth projection also serves as a fresh

opportunity for new high-capital entrants such as existing 2D printer manufacturers.

Technologically the environment is experiencing several significant trends. First is the

saturation of internet connectivity in developed economies. In countries such as the United

States, UK, Germany, and Japan, internet saturation of the population is quickly nearing 90%

(Internet Live Stats). This means that user needs and wants can be addressed using online tools

and platforms to deliver value, and that most of the population can be reached using the web.

More applicable to the AM industry, the ubiquity of modern desktop computing means that

across segments, everyone should have access to either a PC or a Mac in order to run software

programs or access content services. They also should all be able to connect to printers using

standardized USB or Wifi protocols. There is even an accepted universal file format for 3D

printer data that can be output by nearly every modeling software, the .STL file, which 3D

Systems invented in late 1980s. Today, users can log in to websites and search and download a

wide variety of .STL models.7

7 eg www.grabcad.com, www.thingiverse.com

8

Closely related to the standard .STL file and modern digital connectivity are the political

implications of AM. Two are most important: one is the polarizing political divide between gun

control and the right to bear arms8. In 2013, a university student and self-proclaimed anarchist

designed and printed a 3D printed plastic handgun. Cody Wilson also started a website, Defense

Distributed, and posted the files online, which were downloaded 100,000 times before the U.S.

State Department stepped in and applied enough pressure to force Cody to take them down. With

stronger technologies available during the last two years, it is now feasible to print an entire

lower receiver of an AR-15 rifle. Solid Concepts, now part of Stratasys’ service network, has

also successfully fabricated a .45 caliber semi-automatic pistol out of metal using SLS

technology9. At the federal level, Congress attempted to address this in 2013 when the

Undetectable Firearms Act of 1988 came up for renewal. Fortunate for the AM industry, this

language seemed only to impact manufacturers of 3D-printed guns, not the suppliers of the

manufacturing technology themselves (Peters). Indeed the resulting law extended the act 10

more years and “largely leaves 3D-printed guns untouched by regulation” (Mead). This indicates

low political risk for AM firms, at least for now.

As medical applications are a large emerging trend for additive manufacturing, it is worth

considering the current and future regulatory environments. Currently, 3D-printed medical

devices are treated similar to other products, but in the future there could be more scrutiny: “Two

FDA laboratories are looking into ways 3D printing could affect the way medical devices are

manufactured in the future” (T. Lewis). While actions by regulatory agencies such as the FDA

8 https://www.youtube.com/watch?v=DconsfGsXyA

9 https://www.youtube.com/watch?v=zJyf1IrHtcE

9

may not impact AM firms directly, this should be considered when estimating risks in healthcare

vertical.

Socially, additive manufacturing is met with general optimism and has spurred

conversation around “issues of intellectual property, questions of design methods and processes,

and possible business possibilities and outcomes” (Ratto). AM is also entering the mainstream at

a time where the young adult generation may be poised to exploit it in new ways. Today’s

environment is “one in which the crowdsourcing, sharing, and ‘mash–up’ practices that are

already mainstream around other digital media forms become instantiated in material

artifacts...also disrupted are the professional roles of designers, the relationships between

producers and consumers, and the nature of work itself” (ibid). There are many positive,

emerging applications that are generally viewed as exciting and beneficial by society. As

McKinsey director Katy George puts it, “[e]merging markets’ consumption of manufactured

goods is surging and becoming more sophisticated… Simultaneously, we’re experiencing a

range of technological changes, including advanced robotics, large-scale factory digitization, and

3-D printing,..” (McKinsey & Company). This could apply to the AM industry in several ways,

but might begin with more innovative products coming to market or mass customization of

consumer products.

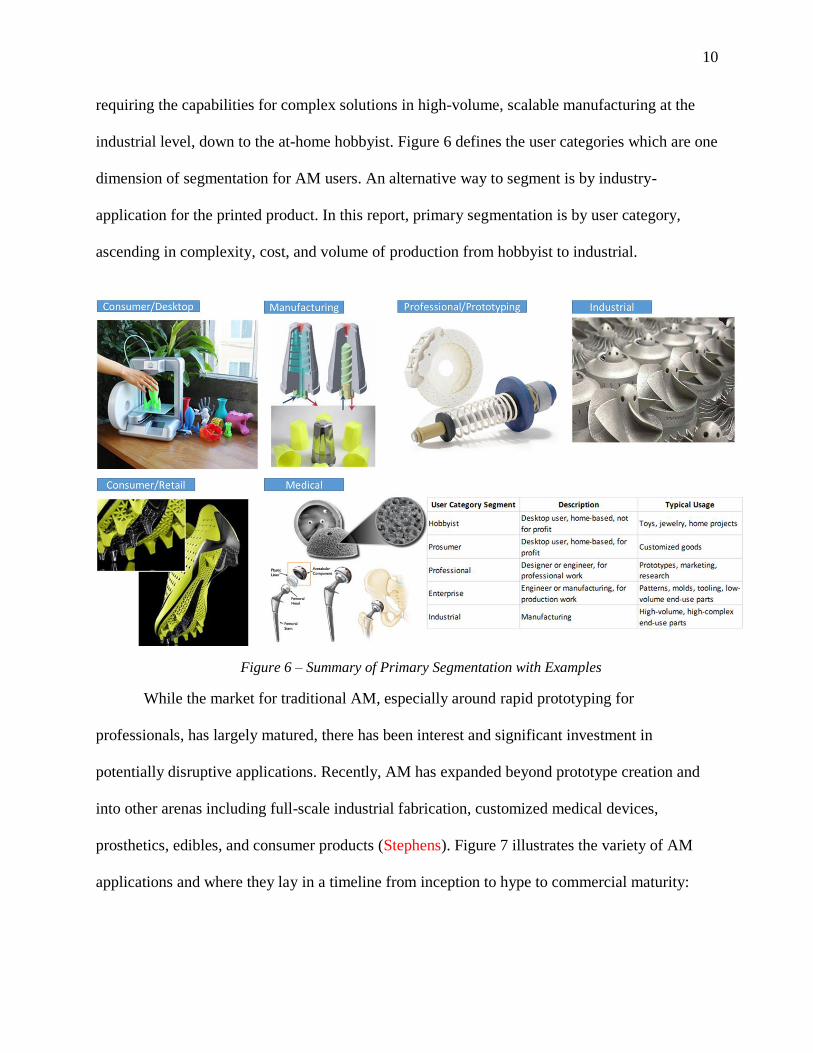

Industry Definition

The additive manufacturing industry was built to support designers and engineers by providing

them with innovative tools for rapid prototyping and low-volume high-complexity component

creation. The industry is worldwide, and consists of hardware (printers), software (modeling),

materials, supplies, and professional services to individual consumers and both large and small

firms. The industry can now be segmented primarily by five user categories ranging from those

10

requiring the capabilities for complex solutions in high-volume, scalable manufacturing at the

industrial level, down to the at-home hobbyist. Figure 6 defines the user categories which are one

dimension of segmentation for AM users. An alternative way to segment is by industry-

application for the printed product. In this report, primary segmentation is by user category,

ascending in complexity, cost, and volume of production from hobbyist to industrial.

Figure 6 – Summary of Primary Segmentation with Examples

While the market for traditional AM, especially around rapid prototyping for

professionals, has largely matured, there has been interest and significant investment in

potentially disruptive applications. Recently, AM has expanded beyond prototype creation and

into other arenas including full-scale industrial fabrication, customized medical devices,

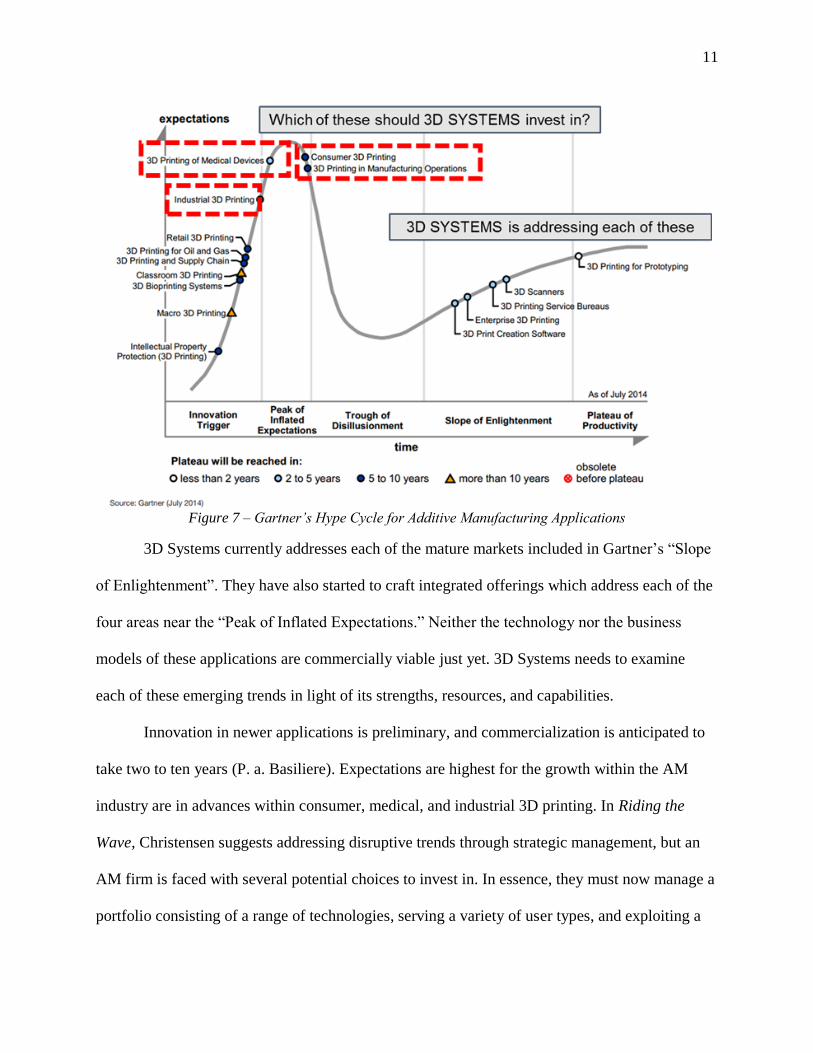

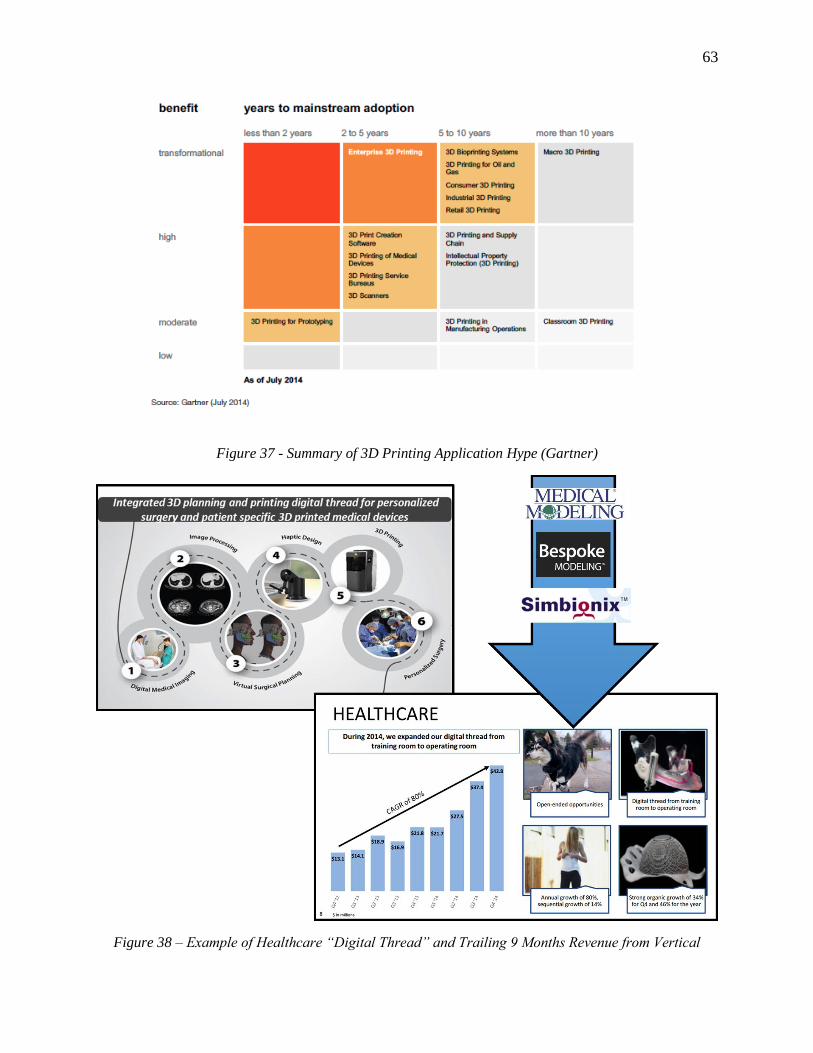

prosthetics, edibles, and consumer products (Stephens). Figure 7 illustrates the variety of AM

applications and where they lay in a timeline from inception to hype to commercial maturity:

11

3D Systems currently addresses each of the mature markets included in Gartner’s “Slope

of Enlightenment”. They have also started to craft integrated offerings which address each of the

four areas near the “Peak of Inflated Expectations.” Neither the technology nor the business

models of these applications are commercially viable just yet. 3D Systems needs to examine

each of these emerging trends in light of its strengths, resources, and capabilities.

Innovation in newer applications is preliminary, and commercialization is anticipated to

take two to ten years (P. a. Basiliere). Expectations are highest for the growth within the AM

industry are in advances within consumer, medical, and industrial 3D printing. In Riding the

Wave, Christensen suggests addressing disruptive trends through strategic management, but an

AM firm is faced with several potential choices to invest in. In essence, they must now manage a

portfolio consisting of a range of technologies, serving a variety of user types, and exploiting a

Figure 7 – Gartner’s Hype Cycle for Additive Manufacturing Applications

12

list of viable and emerging applications. In fact, this is how 3D Systems has approached

constructing their diverse product portfolio.

Offsetting this promising growth is hampered by the technologies speed and economics:

3D printing is not as economical as traditional subtractive and formative manufacturing methods

(eg. milling, injection molding, and casting) for most high-volume fabrication jobs. Replacing

industrial production methods remains at the peak of expectations in 2015 (ibid). However, there

is a trend toward incorporating some 3D technology in traditional manufacturing. A recent

survey of 100 industrial manufacturers showed that 67% of them were using 3D printing in some

way with 25% declaring their plan to implement 3D printing in the near future. This is a

promising projection for 3D Systems and the broader AM industry as a whole. (Stratasys).

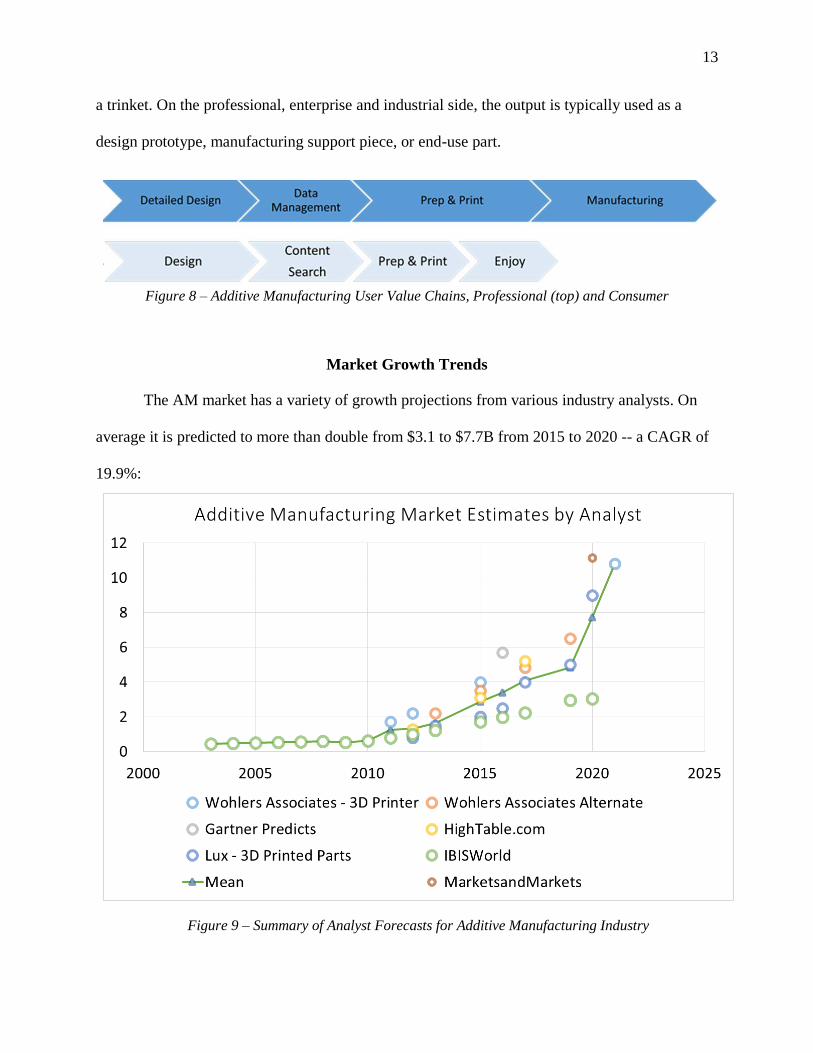

Additive Manufacturing User Value Chains

Within the AM industry, the value chain varies in length depending on the specific segment or

industry. Regardless of segment, all value chains begin with the design and modeling of the

desired 3D shape. The idea is sketched, scanned, or created using consumer or professional

design tools and software. After design, the software will output an .STL digital file that can be

read by a printer pre-processor or a local or web content platform. Content management

platforms enables communication, replication, and shareability of parts and designs either inside

an organization or across the world10. The file may be emailed or uploaded at this point to a

printer or service bureau who will complete the printing. Service bureaus provide complete

services for printing as well as any necessary post-processing and delivery. The actual

“printing,” or physical additive creation of the component uses an installed or desktop 3D printer

with compatible, separately-purchased material. The output for a consumer or prosumer is often

10

eg see Thingiverse: http://www.thingiverse.com/

13

a trinket. On the professional, enterprise and industrial side, the output is typically used as a

design prototype, manufacturing support piece, or end-use part.

Figure 8 – Additive Manufacturing User Value Chains, Professional (top) and Consumer

Market Growth Trends

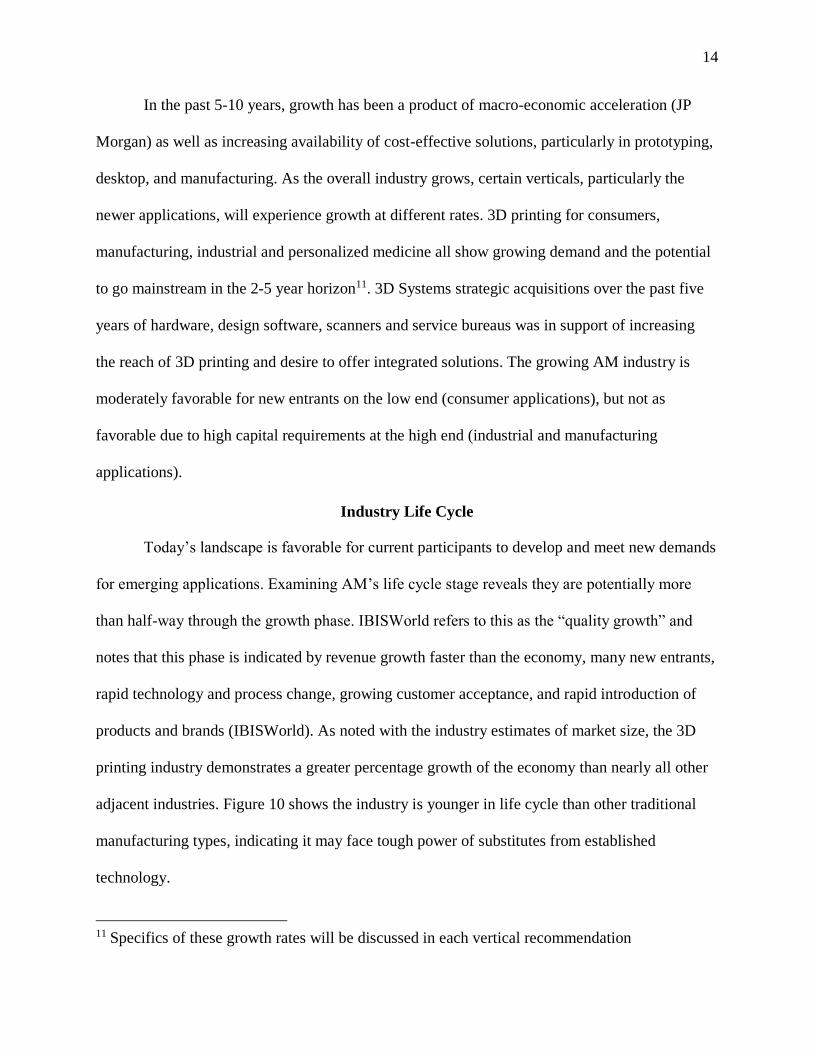

The AM market has a variety of growth projections from various industry analysts. On

average it is predicted to more than double from $3.1 to $7.7B from 2015 to 2020 -- a CAGR of

19.9%:

Figure 9 – Summary of Analyst Forecasts for Additive Manufacturing Industry

14

In the past 5-10 years, growth has been a product of macro-economic acceleration (JP

Morgan) as well as increasing availability of cost-effective solutions, particularly in prototyping,

desktop, and manufacturing. As the overall industry grows, certain verticals, particularly the

newer applications, will experience growth at different rates. 3D printing for consumers,

manufacturing, industrial and personalized medicine all show growing demand and the potential

to go mainstream in the 2-5 year horizon11. 3D Systems strategic acquisitions over the past five

years of hardware, design software, scanners and service bureaus was in support of increasing

the reach of 3D printing and desire to offer integrated solutions. The growing AM industry is

moderately favorable for new entrants on the low end (consumer applications), but not as

favorable due to high capital requirements at the high end (industrial and manufacturing

applications).

Industry Life Cycle

Today’s landscape is favorable for current participants to develop and meet new demands

for emerging applications. Examining AM’s life cycle stage reveals they are potentially more

than half-way through the growth phase. IBISWorld refers to this as the “quality growth” and

notes that this phase is indicated by revenue growth faster than the economy, many new entrants,

rapid technology and process change, growing customer acceptance, and rapid introduction of

products and brands (IBISWorld). As noted with the industry estimates of market size, the 3D

printing industry demonstrates a greater percentage growth of the economy than nearly all other

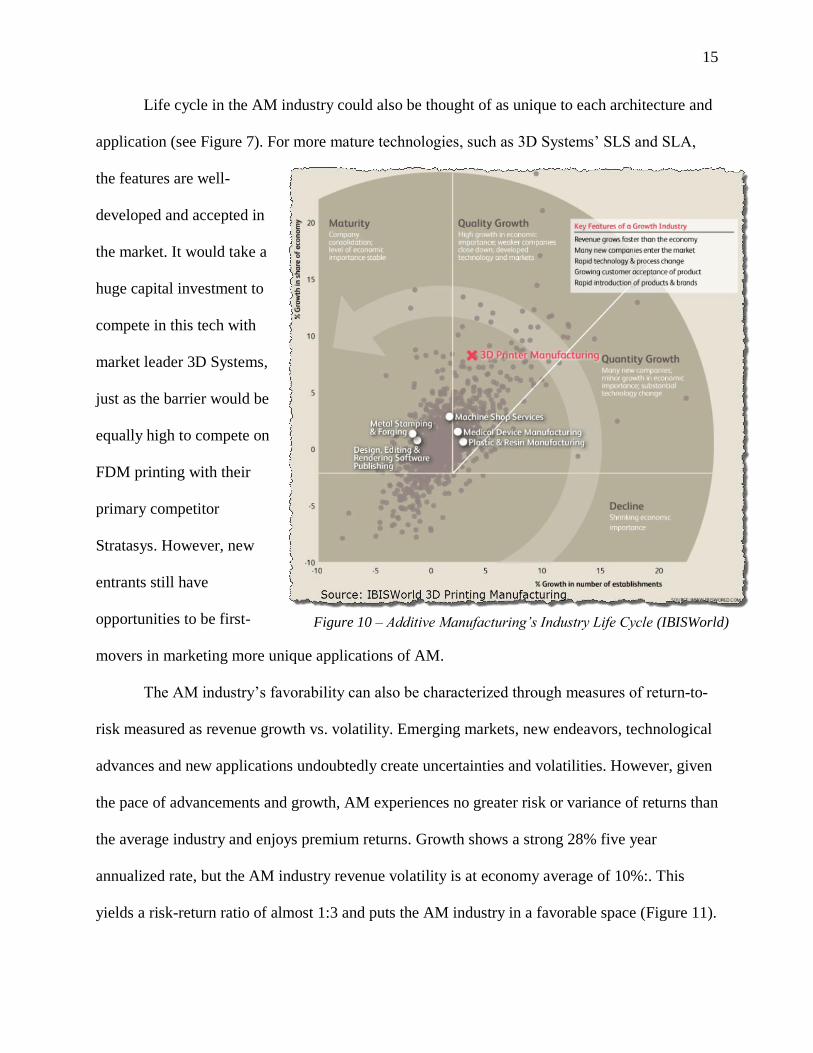

adjacent industries. Figure 10 shows the industry is younger in life cycle than other traditional

manufacturing types, indicating it may face tough power of substitutes from established

technology.

11

Specifics of these growth rates will be discussed in each vertical recommendation

15

Life cycle in the AM industry could also be thought of as unique to each architecture and

application (see Figure 7). For more mature technologies, such as 3D Systems’ SLS and SLA,

the features are well-

developed and accepted in

the market. It would take a

huge capital investment to

compete in this tech with

market leader 3D Systems,

just as the barrier would be

equally high to compete on

FDM printing with their

primary competitor

Stratasys. However, new

entrants still have

opportunities to be first-

movers in marketing more unique applications of AM.

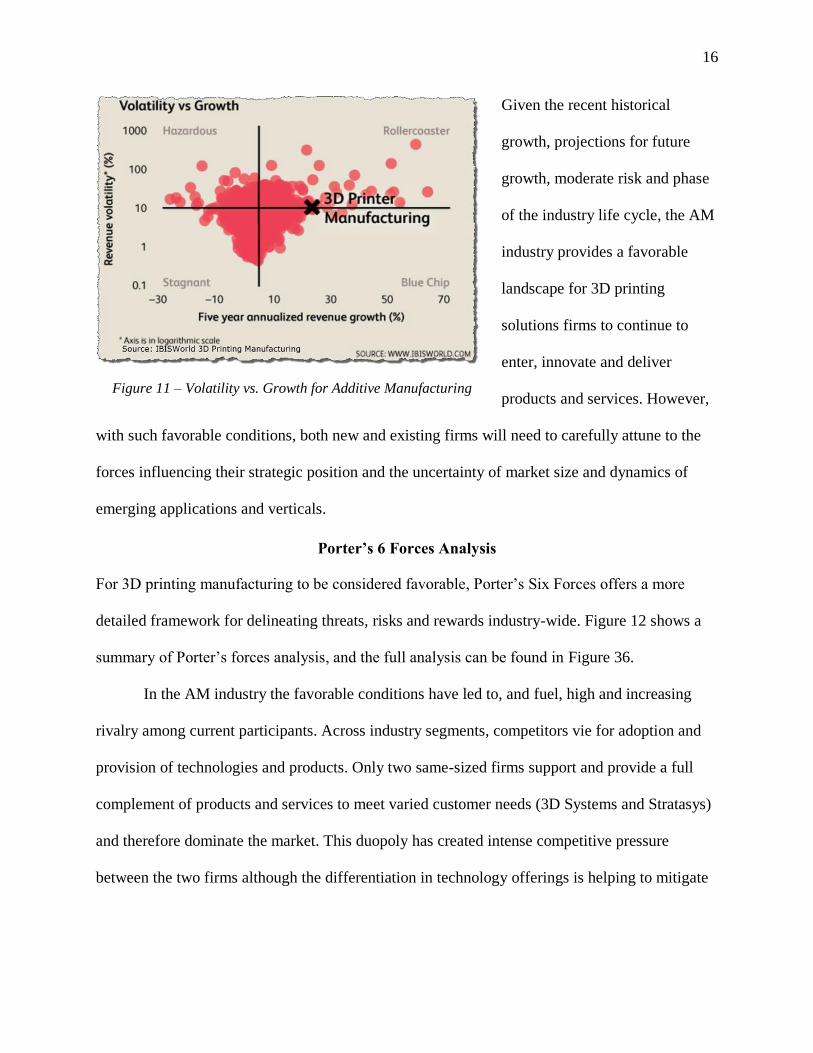

The AM industry’s favorability can also be characterized through measures of return-to-

risk measured as revenue growth vs. volatility. Emerging markets, new endeavors, technological

advances and new applications undoubtedly create uncertainties and volatilities. However, given

the pace of advancements and growth, AM experiences no greater risk or variance of returns than

the average industry and enjoys premium returns. Growth shows a strong 28% five year

annualized rate, but the AM industry revenue volatility is at economy average of 10%:. This

yields a risk-return ratio of almost 1:3 and puts the AM industry in a favorable space (Figure 11).

Figure 10 – Additive Manufacturing’s Industry Life Cycle (IBISWorld)

16

Given the recent historical

growth, projections for future

growth, moderate risk and phase

of the industry life cycle, the AM

industry provides a favorable

landscape for 3D printing

solutions firms to continue to

enter, innovate and deliver

products and services. However,

with such favorable conditions, both new and existing firms will need to carefully attune to the

forces influencing their strategic position and the uncertainty of market size and dynamics of

emerging applications and verticals.

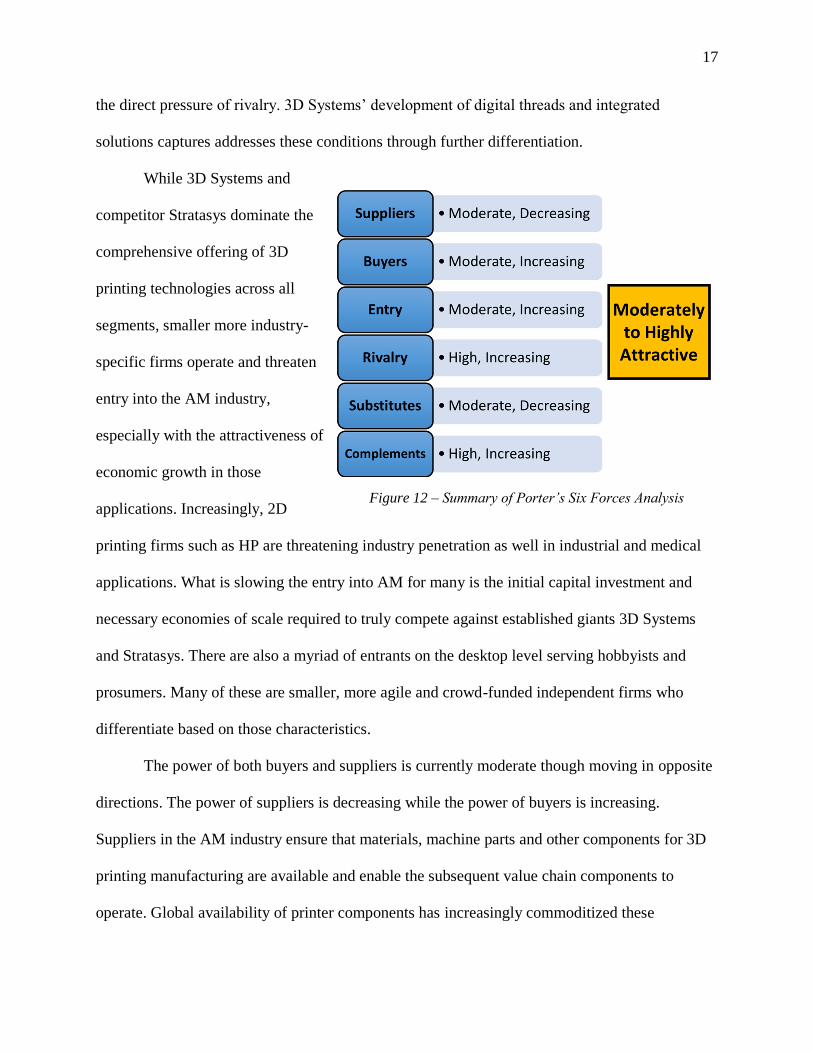

Porter’s 6 Forces Analysis

For 3D printing manufacturing to be considered favorable, Porter’s Six Forces offers a more

detailed framework for delineating threats, risks and rewards industry-wide. Figure 12 shows a

summary of Porter’s forces analysis, and the full analysis can be found in Figure 36.

In the AM industry the favorable conditions have led to, and fuel, high and increasing

rivalry among current participants. Across industry segments, competitors vie for adoption and

provision of technologies and products. Only two same-sized firms support and provide a full

complement of products and services to meet varied customer needs (3D Systems and Stratasys)

and therefore dominate the market. This duopoly has created intense competitive pressure

between the two firms although the differentiation in technology offerings is helping to mitigate

Figure 11 – Volatility vs. Growth for Additive Manufacturing

17

the direct pressure of rivalry. 3D Systems’ development of digital threads and integrated

solutions captures addresses these conditions through further differentiation.

While 3D Systems and

competitor Stratasys dominate the

comprehensive offering of 3D

printing technologies across all

segments, smaller more industry-

specific firms operate and threaten

entry into the AM industry,

especially with the attractiveness of

economic growth in those

applications. Increasingly, 2D

printing firms such as HP are threatening industry penetration as well in industrial and medical

applications. What is slowing the entry into AM for many is the initial capital investment and

necessary economies of scale required to truly compete against established giants 3D Systems

and Stratasys. There are also a myriad of entrants on the desktop level serving hobbyists and

prosumers. Many of these are smaller, more agile and crowd-funded independent firms who

differentiate based on those characteristics.

The power of both buyers and suppliers is currently moderate though moving in opposite

directions. The power of suppliers is decreasing while the power of buyers is increasing.

Suppliers in the AM industry ensure that materials, machine parts and other components for 3D

printing manufacturing are available and enable the subsequent value chain components to

operate. Global availability of printer components has increasingly commoditized these

Figure 12 – Summary of Porter’s Six Forces Analysis

18

components and nearly erased switching costs for purchasers. It is highly unlikely that materials

providers would forward integrate to build whole printer or service systems. Simultaneously

firms in the industry are increasingly acquiring their own supply chains (backward integrating)

slowly relying less on 3rd parties for components and assembly.

Converse to suppliers’ trajectory, buyer power is increasing. Most buyers of 3D printing

machines and services do not immediately threaten backward integration into production or

supply nor do buyers easily switch due to high purchase costs. Despite these pressures that

suggest low buyer power, the majority of the value in 3D printing manufacturing is captured by

the buyer once they have the printed part. As firms in the industry make strategy considerations,

attentiveness to buyers’ preferences and demands (and therefore value) will be especially

important. If demands are not well attended to, the moderate threat of substitutes could pose a

risk for the present players and potential entrants. While there are more traditional modes of

modeling and production, 3D printing is becoming the norm for prototyping, and modeling and

producing are being incorporated into the digital threads of more comprehensive 3D printing

solutions. Concurrently, traditional manufacturing methods are getting more economical for

production and until 3D printing technology can offer the speed and low cost of traditional

methods, the threat of substitutes on the enterprise and industrial levels will remain.

Porter’s final and often overlooked ‘sixth force’ relates to complements. As the

popularity of 3D printing--especially for prototyping--increases, file types for all kinds of 3D

printer work has been standardized. The standard file type (.STL) can be created, stored,

communicated by complements before the printing stage. The power of complements is similarly

high and increasing in the production phase as service bureaus reach more and more customers.

19

Porter’s forces demonstrate what Wohlers, Gartner, IBISWorld and other industry

analysts have identified: the AM industry has moderate to medium to high favorability. Though

the threat of entry challenges current industry firms to make defensive decisions, the

opportunities for deeper penetration into the industrial and medical segments and delivery of

solutions to the consumer and prosumer are also present. Though 3D Systems is constrained by

the same forces as the rest of the AM industry their focus on building comprehensive and well-

integrated solutions address these very forces both offensively and defensively.

Competitive Landscape

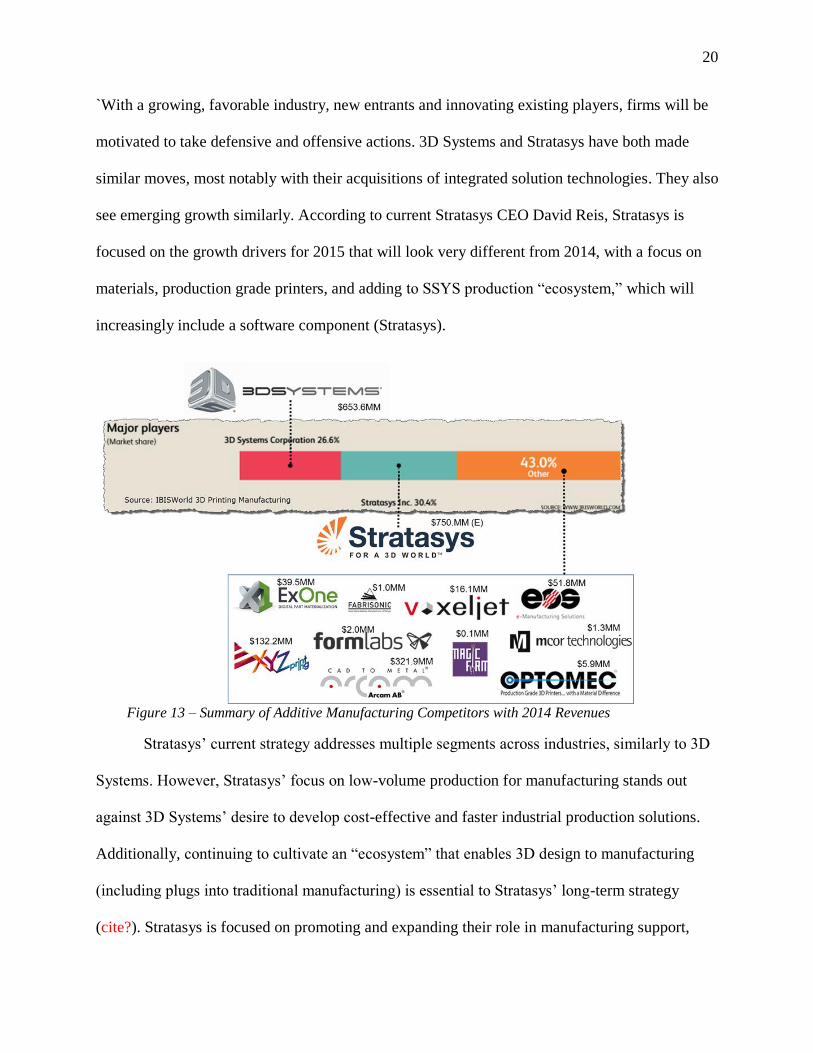

Porter’s Five Forces highlighted the growing threat of new entrants into the AM industry

as well as increasing rivalry. Currently, 3D Systems (26.6% market share) and Stratasys (30.4%

market share) are the largest players, each with a comprehensive offering of 3D printing

manufacturing solutions across almost all segments and industries. Stratasys and 3D Systems

have diversified portfolios of products and offerings and each has a market capitalization of over

$3 billion, with the nearest competitor (ExOne) at $212 million. The remaining 43% of the AM

industry is made up of a growing number of more industry- or segment-specific offerings

including ExOne, HP, Arcam, formlabs, Lulzbot, Zortrax and others with the largest number of

firms operating in the consumer sector. See Figure 13 for a summary of significant competitors.

Though 3D Systems and Stratasys are the major players in the AM industry, more

industry-specific players such as Arcam, EOS and ExOne are introducing new technologies and

potential threats to the current operators. Their participation in the medical and aerospace

industries (which is incorporated into both the enterprise and industrial segments of the AM

industry) is specifically of interest to 3D Systems. This is because of 3D Systems’ hope to scale

further in these segments and ride the growing trend in medical and healthcare revenues.

20

`With a growing, favorable industry, new entrants and innovating existing players, firms will be

motivated to take defensive and offensive actions. 3D Systems and Stratasys have both made

similar moves, most notably with their acquisitions of integrated solution technologies. They also

see emerging growth similarly. According to current Stratasys CEO David Reis, Stratasys is

focused on the growth drivers for 2015 that will look very different from 2014, with a focus on

materials, production grade printers, and adding to SSYS production “ecosystem,” which will

increasingly include a software component (Stratasys).

Stratasys’ current strategy addresses multiple segments across industries, similarly to 3D

Systems. However, Stratasys’ focus on low-volume production for manufacturing stands out

against 3D Systems’ desire to develop cost-effective and faster industrial production solutions.

Additionally, continuing to cultivate an “ecosystem” that enables 3D design to manufacturing

(including plugs into traditional manufacturing) is essential to Stratasys’ long-term strategy

(cite?). Stratasys is focused on promoting and expanding their role in manufacturing support,

Figure 13 – Summary of Additive Manufacturing Competitors with 2014 Revenues

21

from jigs and fixtures (which aid in traditional manufacturing processes), to casts and molds

(which assist in the same), to tools for plastic injection molding and sheet metal fabrication

(Baruah).

One differentiator between 3D Systems and Stratasys has been the level of forward

integration of the user value chain. Since 2001, 3D Systems has acquired 21 service bureaus

across the world, giving them a global network of service locations consolidated under their

Quickparts brand (J.P.Morgan). Stratasys, on the other hand, initially encouraged its distribution

reseller channel to offer services as part of a sales strategy, but very recently has started to

acquire major service bureaus such as Solid Concepts. 3D Systems has first-mover advantage in

forward integration. This helps them capture profits from using the machines to create finished

outputs for customers who have not yet, or may not ever, purchase a printer. Given Stratasys’

new direction into production printing and materials, and increasing acquisitions of service

bureaus, this will create more direct competition between these two firms, therefore increasing

rivalry between 3D Systems and Stratasys. This will be further compounded by the news of a

new entrant into the industrial market.

In late 2014, HP announced its Multi Jet Fusion Technology with an intended launch in

2016 (Reuters). This technology lays down a thin layer of powdered plastic and then uses its

thermal inkjet technology to print a chemical agent on top. While this is similar to 3D System’s

Z Corp (ZPrinters are now the Projet x60 series) or voxeljet’s plastic printers, it appears that the

differences are threefold. First, HP dispenses not just a binder or “fusing agent,” but also a

“detailing agent” that makes edges smoother and could simplify post-processing. Second, HP

uses “fusing energy” on each pass, which could increase the strength of the part as well as

increase the speed of the printer. HP did not specify what type of technology was used for this.

22

Lastly, HP implied that its inkjet printheads are superior to competitors, leading to finer details

and greater speed. The technologies that would allow specific comparison to current printheads

were not named.

HP’s shift from 2D printing to 3D printing threatens to disrupt the current 3D printing

process by introducing a significantly faster process for printing stronger parts with finer details .

However, quite a bit of uncertainty remains regarding the precision of HP’s technology and their

ability to rise to or surpass the current industry standards. In the long run, HP’s success will be

measured by its ability to capture market share away from the established firms and provide a 3D

printed solution that is faster, more cost effective, and more precise than today’s solutions.

In total, 70% of 3D Systems’ product line is exposed to new entrants, but little impact is

expected over the next two years (Jefferies). As most rising segments of the AM industry are

anticipated to develop within 2-5 years, there is no immediate threat to 3D Systems. However,

with anxious new and developing enterprises working in the wings to capture more of the AM

industry, 3D Systems strategy moving forward will need to obstruct the progress of these

segments or capture the value away from their competitors.

INTERNAL ANALYSIS

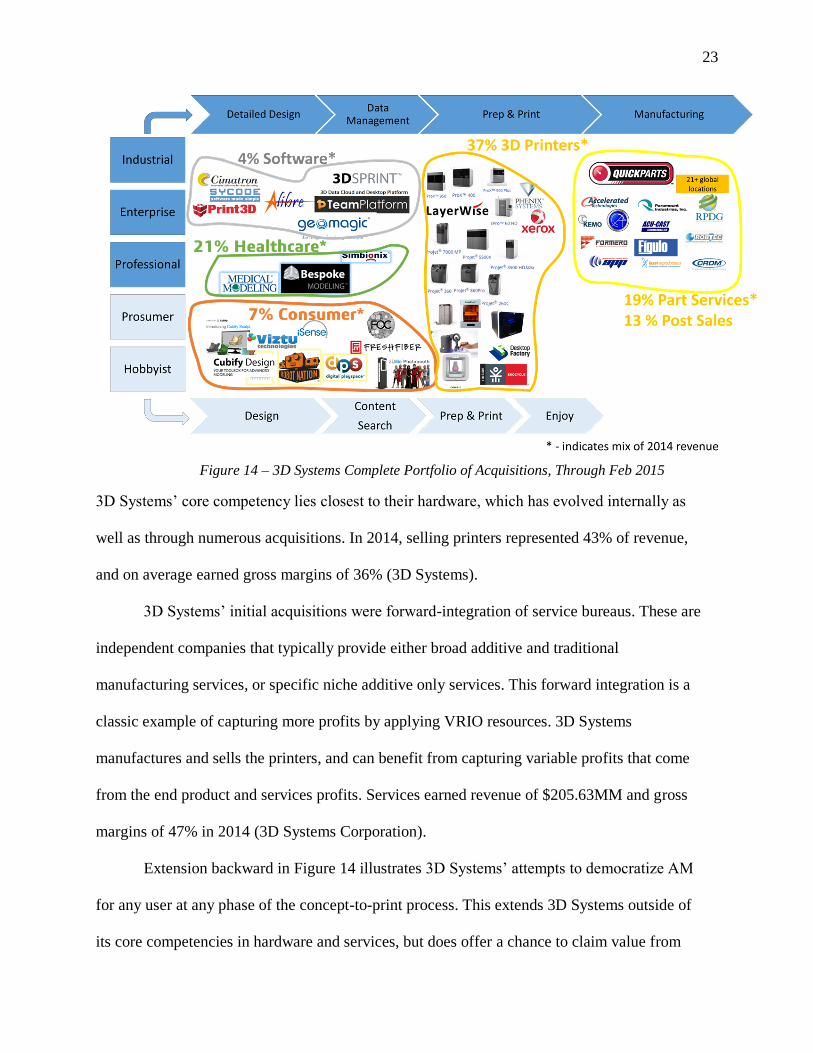

Product Portfolio

3D Systems has both developed and acquired a highly diversified portfolio of hardware and

software offerings that serve a range of user segments and industries. Recalling the end-user

value chain above, Figure 14 illustrates how 3D Systems has expanded both forward and

backward from their initial core competencies in printer hardware and materials:

23

Figure 14 – 3D Systems Complete Portfolio of Acquisitions, Through Feb 2015

3D Systems’ core competency lies closest to their hardware, which has evolved internally as

well as through numerous acquisitions. In 2014, selling printers represented 43% of revenue,

and on average earned gross margins of 36% (3D Systems).

3D Systems’ initial acquisitions were forward-integration of service bureaus. These are

independent companies that typically provide either broad additive and traditional

manufacturing services, or specific niche additive only services. This forward integration is a

classic example of capturing more profits by applying VRIO resources. 3D Systems

manufactures and sells the printers, and can benefit from capturing variable profits that come

from the end product and services profits. Services earned revenue of $205.63MM and gross

margins of 47% in 2014 (3D Systems Corporation).

Extension backward in Figure 14 illustrates 3D Systems’ attempts to democratize AM

for any user at any phase of the concept-to-print process. This extends 3D Systems outside of

its core competencies in hardware and services, but does offer a chance to claim value from

24

the beginning of the process. .The portfolio and “digital thread” strategy is key to 3D Systems’

economic logic of increasing willingness-to-pay and seeding users by offering integrated

solutions.

Organizational Structure

Organizationally, the firm is led by President and CEO Abraham (Avi) Reichental and

the independent Chairman of the Board of Directors Walter Loeenbaum II who joined in 1999.

Reichental is supported by C-level reports in distinct functional areas including technology

(Chuck Hull, CTO and founder), Finance (Ted Hull, CFO, EVP of Finance), Operations (Mark

Wright, COO, EVP), Marketing (Cathy Lewis, CMO), Legal (Andrew Johnson, CLO),

Accounting (David Robert Styka, CAO, VP) (Google).

In 2014 two long-serving members of the executive team were repositioned into

functional areas to better manage 3D Systems current strategy. Damon Gregorie, former CFO

became the new Vice President of Mergers and Acquisitions and former COO Dr. Kevin McAlea

became the COO of Healthcare. The movement of key executives into the new roles signaled a

renewed focus on integrating the company’s recent M&A activities and its increasing interest in

the lucrative medical device industry and healthcare market.

Beyond the leadership in the firm, 3D System had 2,136 full time employees on its

payroll at the end of 2014, representing an increase of more than 50% from 2013, and an

increase of 540% from 2008. This growth is both organic and fueled by acquisitions. This is a

large factor in increasing the company’s costs and has contributed to their shrinking operating

margins. Manufacturing and assembly of their 3D printers are managed in three eastern US

locations and Israel. Material manufacturing and distribution is also mainly handled from three

plants in the US and one in Switzerland, with some partnerships around specialized materials.

Because of 3D System’s aggressive acquisition cycle they have the added challenge of

25

integrations. Integrating and realizing synergies of a single merger or acquisition is difficult

(Christofferson). Taking these steps almost monthly (45 over 5 years) has been costly for 3D

Systems. Realizing synergies around technologies and services has been slow, evidenced by

rising SG&A and falling ROA. Some of these acquisitions have also been defensive, and finding

a place for the technology and people involved can be difficult. Difficulties are exacerbated by

geographic proximity (or lack of), and incorporating the different cultures of the acquired

companies, many of which are smaller startups and move at a very different pace than 3D

Systems. There is also the difficulty of making sure high level managers in acquired companies

stay with the company by giving them an appropriate amount of resources and responsibility.

All of these challenges often put acquiring companies in the position of taking on costs,

without yet realizing synergies. 3D Systems is currently struggling to realize all the available

synergies available through these 45 acquisitions.

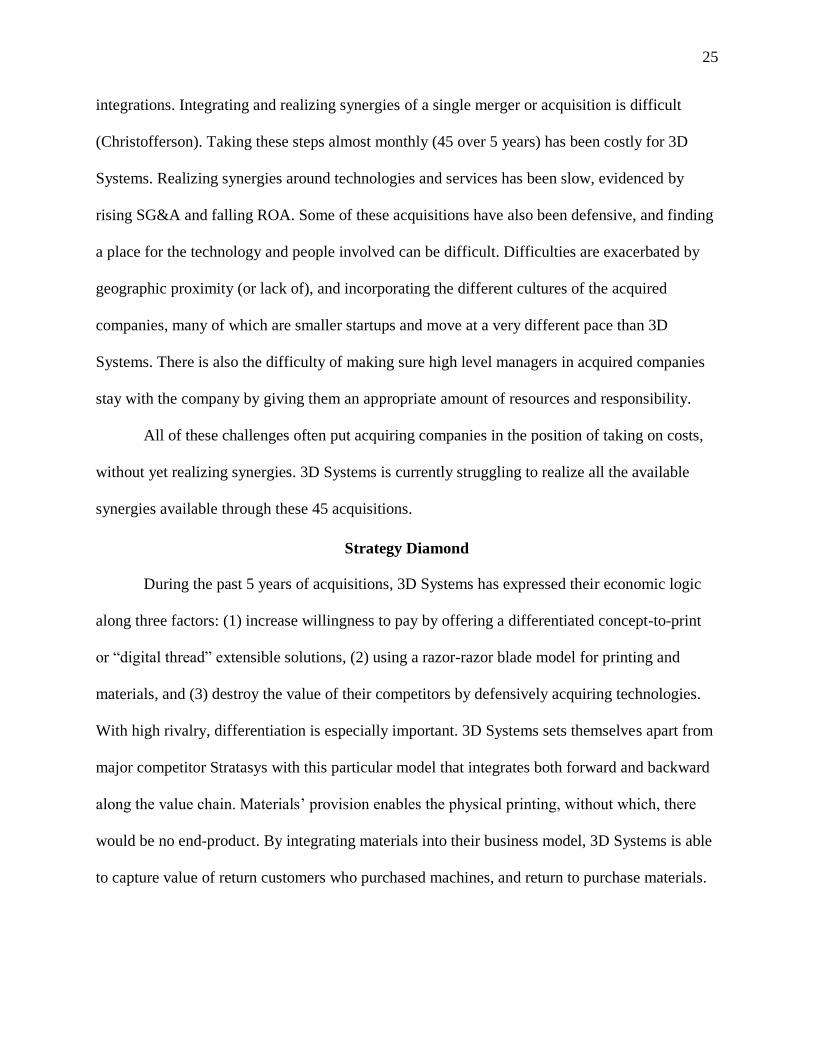

Strategy Diamond

During the past 5 years of acquisitions, 3D Systems has expressed their economic logic

along three factors: (1) increase willingness to pay by offering a differentiated concept-to-print

or “digital thread” extensible solutions, (2) using a razor-razor blade model for printing and

materials, and (3) destroy the value of their competitors by defensively acquiring technologies.

With high rivalry, differentiation is especially important. 3D Systems sets themselves apart from

major competitor Stratasys with this particular model that integrates both forward and backward

along the value chain. Materials’ provision enables the physical printing, without which, there

would be no end-product. By integrating materials into their business model, 3D Systems is able

to capture value of return customers who purchased machines, and return to purchase materials.

26

This razor-razor blade model of selling the machines and the materials was key to the economic

mix for 3D Systems in the past, with materials making up 68% of the gross profit mix in 2008.

There has been a year-over-year decline in the materials segment and today materials make up

only one third of 3D

Systems’ revenue mix.

Forward and backward

integration is also

represented in the

creation of “digital

threads.” 3D Systems

has acquired a number

of companies, both

defensively and offensively. They integrate these companies along these threads to produce an

end-to-end solution. In this way, 3D Systems makes their own solutions more robust, and they

are able to keep some technologies from their competitors. Their main economic logic is made

possible by a clear set of differentiators led by the digital thread solution. To create digital

threads and meet the diverse needs of the market, 3D Systems provides the widest breadth of

technologies, patents and materials. With experience on their side from decades in the industry,

3D Systems has created high economies of experience that can only be matched over time.

As a corporation, 3D Systems operational arenas could be described along four

dimensions: industry vertical, usage category, technology, and geography12. They are certainly

12

To simplify, this analysis deals predominantly with the first three dimensions, i.e. not an international analysis

Figure 15 – 3D Systems Current Strategy Diamond

27

global with 44.5% of their revenue coming from sources outside the U.S. Technologically, 3D

Systems focuses primarily on seven core technologies that they leverage for 3D printers, on-

demand parts, software and services. They serve consumer and hobbyists, prosumers,

professional, enterprise and industrial segments of the manufacturing, medical, automotive,

aerospace and defense, architectural, dental and consumer industries. Between its inception in

1986 and 2009, 3D Systems grew steadily, but slowly. Rapid growth started in 2009 leading to

40-50% sales growth in 5 years. This seemingly accelerated pace of staging is aimed at future

success. However, their success has been limited by the ability to scale the distribution channels

on either side of the core business of making printers. This limitation has shaped its economic

logic. Moving forward, strategic moves for 3D Systems may continue to include offensive and

defensive acquisitions, investment in closed-source (internal) R&D, and seeking alliances. With

the wide breadth of offerings across these corporate dimensions, 3D Systems will need to focus

intensely on its core capabilities, available resources and leverage their key differentiators to be

successful and continue to grow in their target technologies and industries.

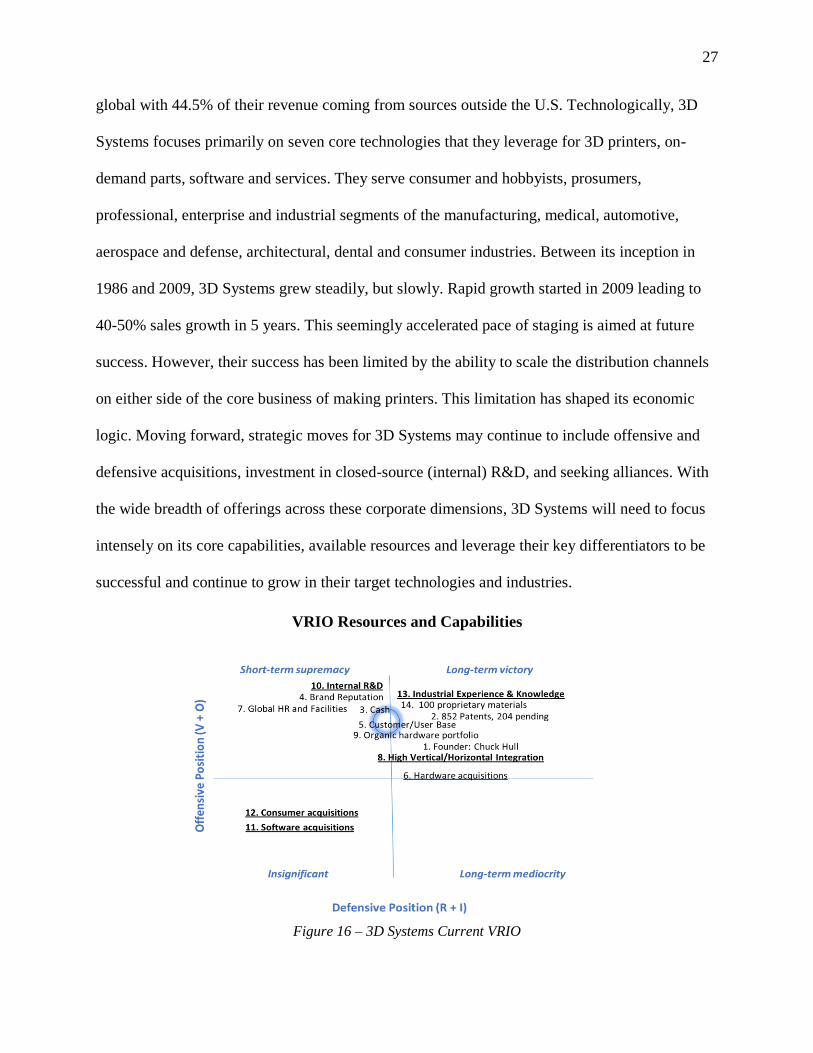

VRIO Resources and Capabilities

Figure 16 – 3D Systems Current VRIO

28

3D Systems VRIO captures a comprehensive list of resources and capabilities. Figure 16

identifies 13 resource and capabilities deemed most critical to strategic analysis. In the long term

victory quadrant, 3D Systems’ Chuck Hull, patents, proprietary materials, and industrial and

enterprise experience and knowledge are valuable, rare, difficult to imitate, and the organization

fully exploits these resource and capabilities. Other resource and capabilities that are valuable,

rare, and the organization exploits these resource and capabilities but these items have medium

to low level of difficulty to imitate means they only have a temporary competitive advantage

consist of cash, customer/user base, organic hardware portfolio, internal R&D, brand

reputation/identity, and global HR and facility.

Based on the current assessment of 3D Systems capabilities and resources, they are

experiencing short-term supremacy and are on the cusp of long-term victory. The focus of this

paper is on five key resources and capabilities, indicated by underline in Figure 16 that are most

important to position the company for long term victory. To make the shift into true sustained

competitive advantage 3D Systems needs to position itself more defensively against new entrants

and current rivals by bettering their resources and reducing imitability while offensively

developing innovative solutions that are more valuable and better utilized by the organization.

Currently consumer acquisitions and software acquisitions are under-exploited due to

lack of realized synergies, add little value to 3D Systems due to lack of full integration into the

digital threads and are neither rare nor inimitable, evidenced by competitor Stratasys’ ability to

make similar acquisitions but on a smaller scale.

Currently internal R&D is exploited by 3D Systems and highly valuable but not

particularly rare or inimitable. According to 3D Hubs Trends, 3D Systems industrial printers are

preferred to competitors due to their superior print quality (3D Hubs). However, with the

29

increasing threat of entrants such as HP, to actualize the benefits of the R&D for sustained

competitive advantage 3D Systems will need to develop faster and more cost effective

technologies that are unique.

Finally, the industrial and enterprise experience and knowledge is a key resource and

capability for 3D Systems. Decades of experience, development, investment, acquisition, trial,

error and re-discovery has garnered a clear advantage in the industry with the most valuable and

time-tested experience.

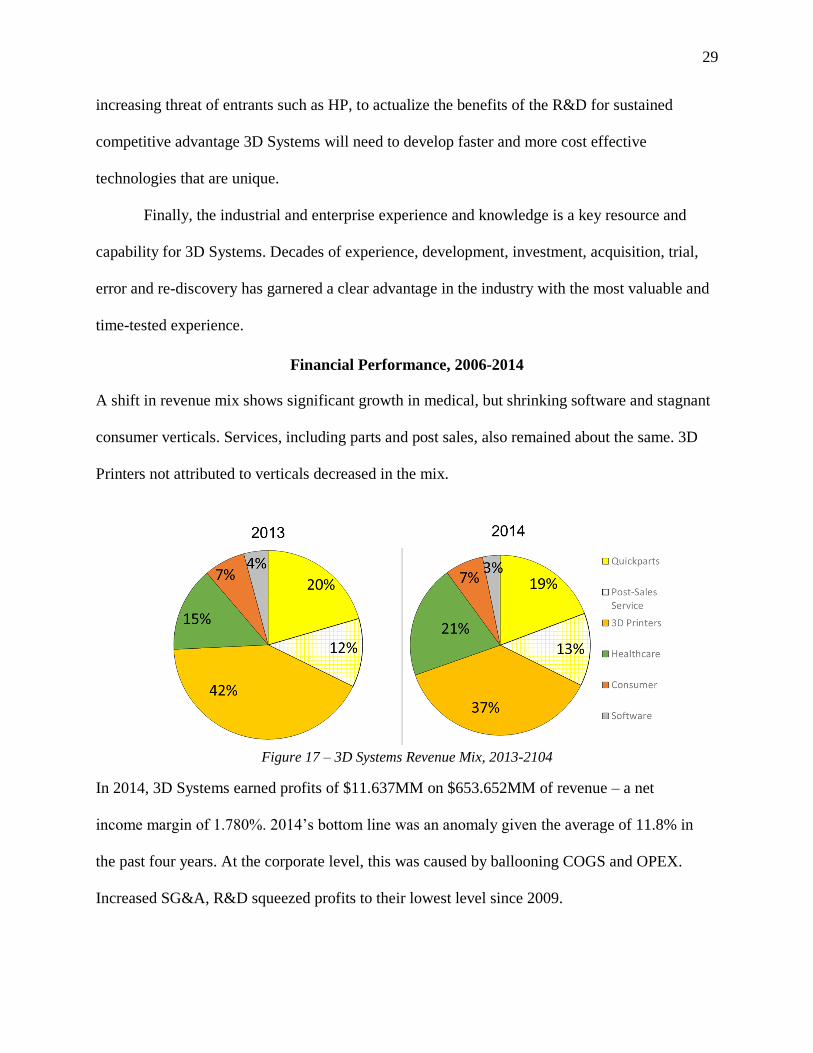

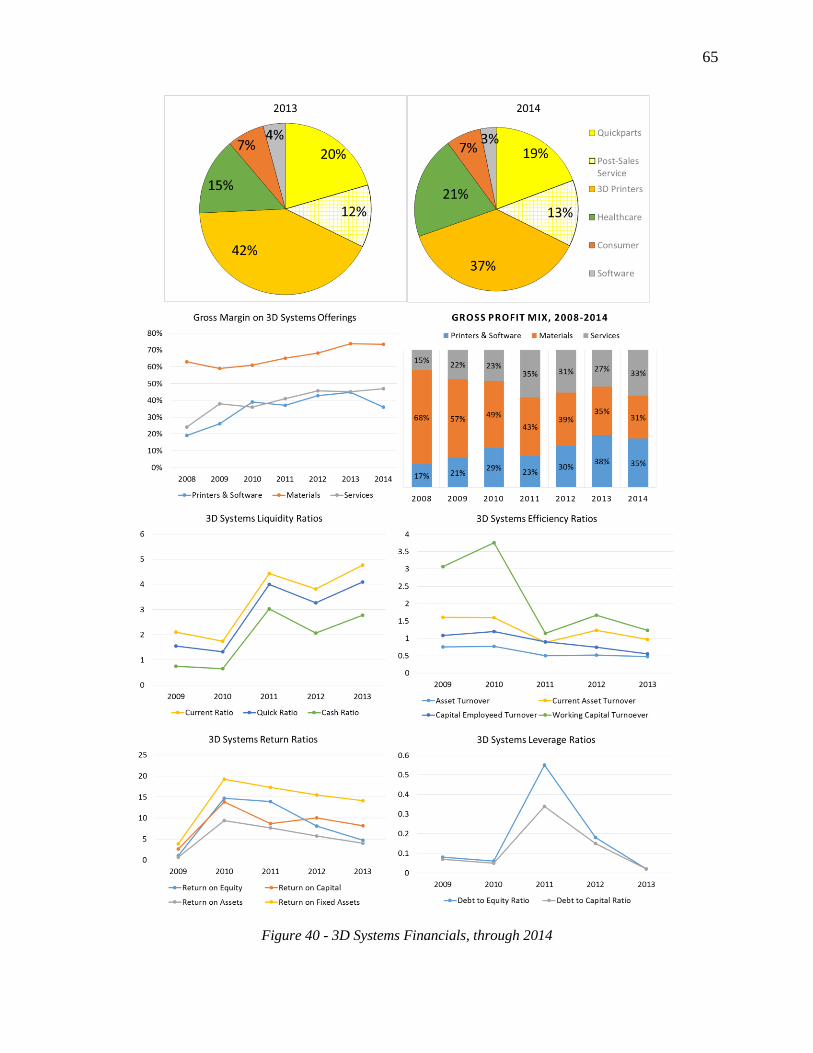

Financial Performance, 2006-2014

A shift in revenue mix shows significant growth in medical, but shrinking software and stagnant

consumer verticals. Services, including parts and post sales, also remained about the same. 3D

Printers not attributed to verticals decreased in the mix.

Figure 17 – 3D Systems Revenue Mix, 2013-2104

In 2014, 3D Systems earned profits of $11.637MM on $653.652MM of revenue – a net

income margin of 1.780%. 2014’s bottom line was an anomaly given the average of 11.8% in

the past four years. At the corporate level, this was caused by ballooning COGS and OPEX.

Increased SG&A, R&D squeezed profits to their lowest level since 2009.

30

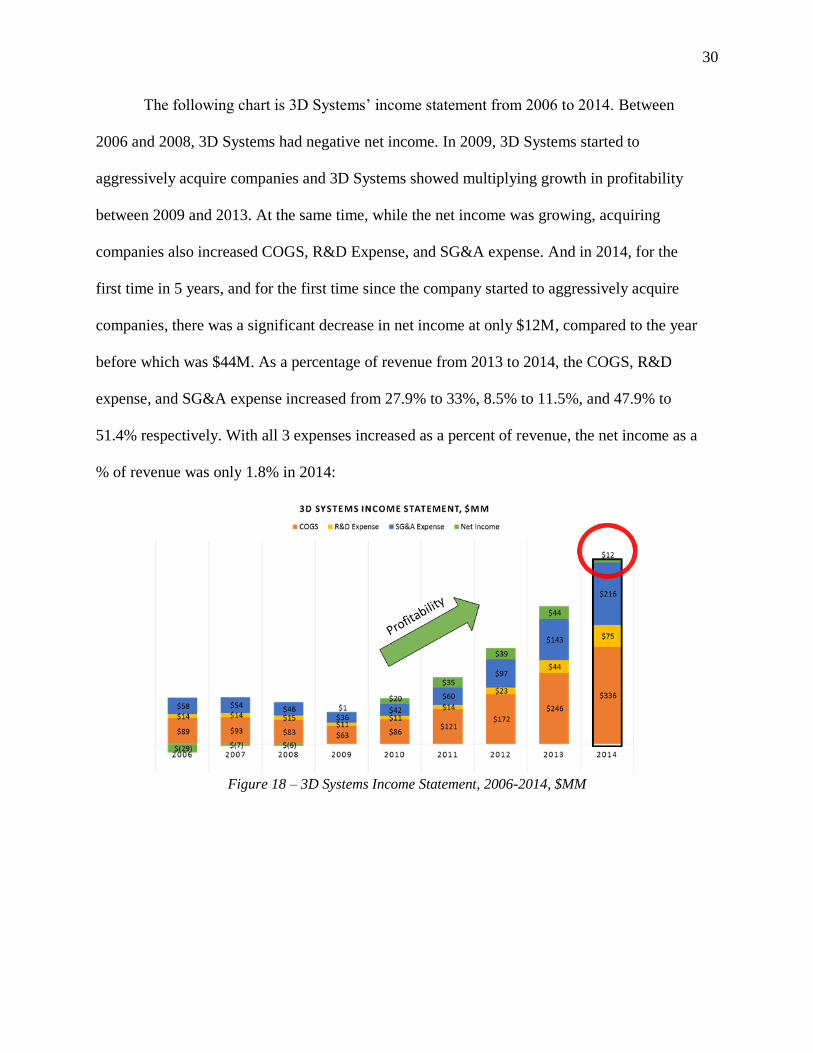

The following chart is 3D Systems’ income statement from 2006 to 2014. Between

2006 and 2008, 3D Systems had negative net income. In 2009, 3D Systems started to

aggressively acquire companies and 3D Systems showed multiplying growth in profitability

between 2009 and 2013. At the same time, while the net income was growing, acquiring

companies also increased COGS, R&D Expense, and SG&A expense. And in 2014, for the

first time in 5 years, and for the first time since the company started to aggressively acquire

companies, there was a significant decrease in net income at only $12M, compared to the year

before which was $44M. As a percentage of revenue from 2013 to 2014, the COGS, R&D

expense, and SG&A expense increased from 27.9% to 33%, 8.5% to 11.5%, and 47.9% to

51.4% respectively. With all 3 expenses increased as a percent of revenue, the net income as a

% of revenue was only 1.8% in 2014:

Figure 18 – 3D Systems Income Statement, 2006-2014, $MM

31

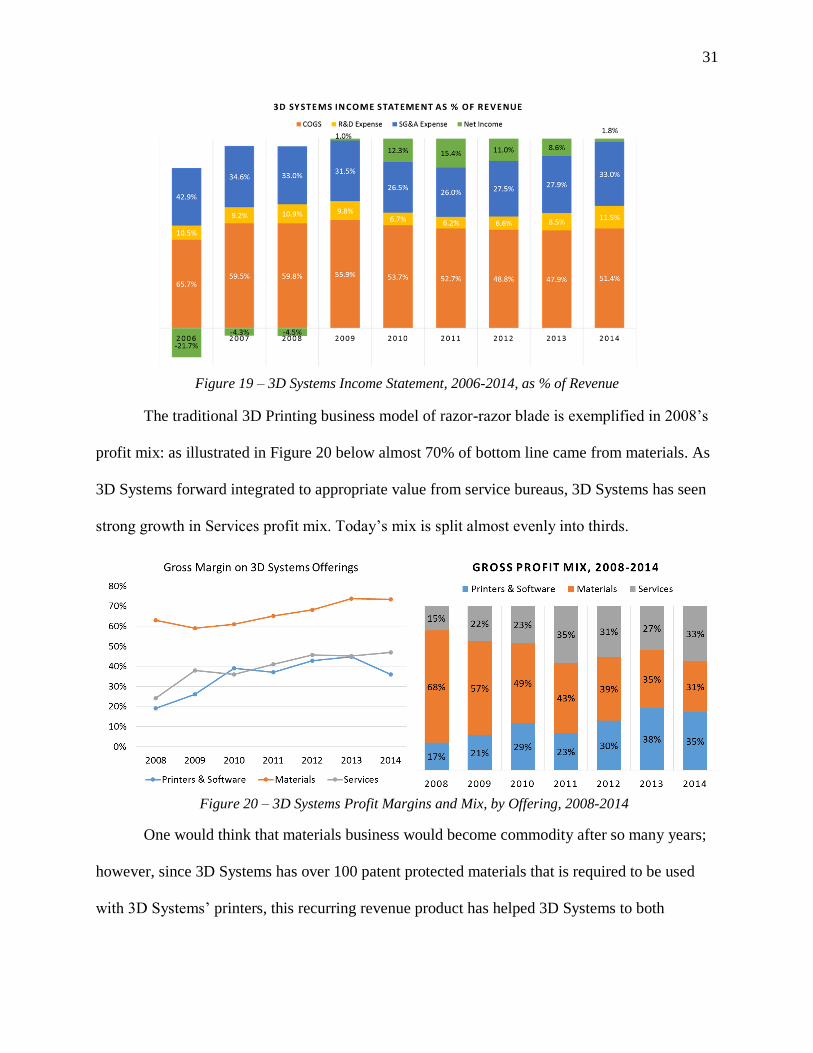

Figure 19 – 3D Systems Income Statement, 2006-2014, as % of Revenue

The traditional 3D Printing business model of razor-razor blade is exemplified in 2008’s

profit mix: as illustrated in Figure 20 below almost 70% of bottom line came from materials. As

3D Systems forward integrated to appropriate value from service bureaus, 3D Systems has seen

strong growth in Services profit mix. Today’s mix is split almost evenly into thirds.

Figure 20 – 3D Systems Profit Margins and Mix, by Offering, 2008-2014

One would think that materials business would become commodity after so many years;

however, since 3D Systems has over 100 patent protected materials that is required to be used

with 3D Systems’ printers, this recurring revenue product has helped 3D Systems to both

32

decreased costs and increased willingness-to-pay; this is illustrated by the increasing gross

margin on materials.

Examining 3D Systems’ balance sheet with Ratio analysis demonstrates three important

trends between 2009 and 201313. First, is that three equity issuances14 in the last five years have

raised over $620MM and buoyed liquidity drastically. Similarly, the second salient trend is the

reduction of debt reflected in the leverage ratios. These both indicate that 3D Systems has the

flexibility to make strategic moves and can continue to amass returns if it can keep its cost

structure from ballooning further. Working to inflate the cost balloon and squeezing the bottom

line are higher OPEX and COGS resulting from the vast number of 3D Systems subsidiaries.

This appears in the trend of decreasing returns on assets, equity, and capital.

In summary, 3D Systems is ostensibly a healthy firm from a financial perspective.

However, recent volatility in stock prices for both them and Stratasys indicate there is high

uncertainty ahead as the AM industry addresses growth opportunities and competitive threats. As

the Wall Street Journal summarized in an October 2014 article, “3D Systems is investing heavily

in an attempt to capitalize on rising demand for 3D printing technology, …but the company has

been having trouble reaching its sales goals as well: It lowered its 2014 revenue forecast by

about 7%... the stock is now off about 60% for the year to date…” (Wall Street Journal). As of

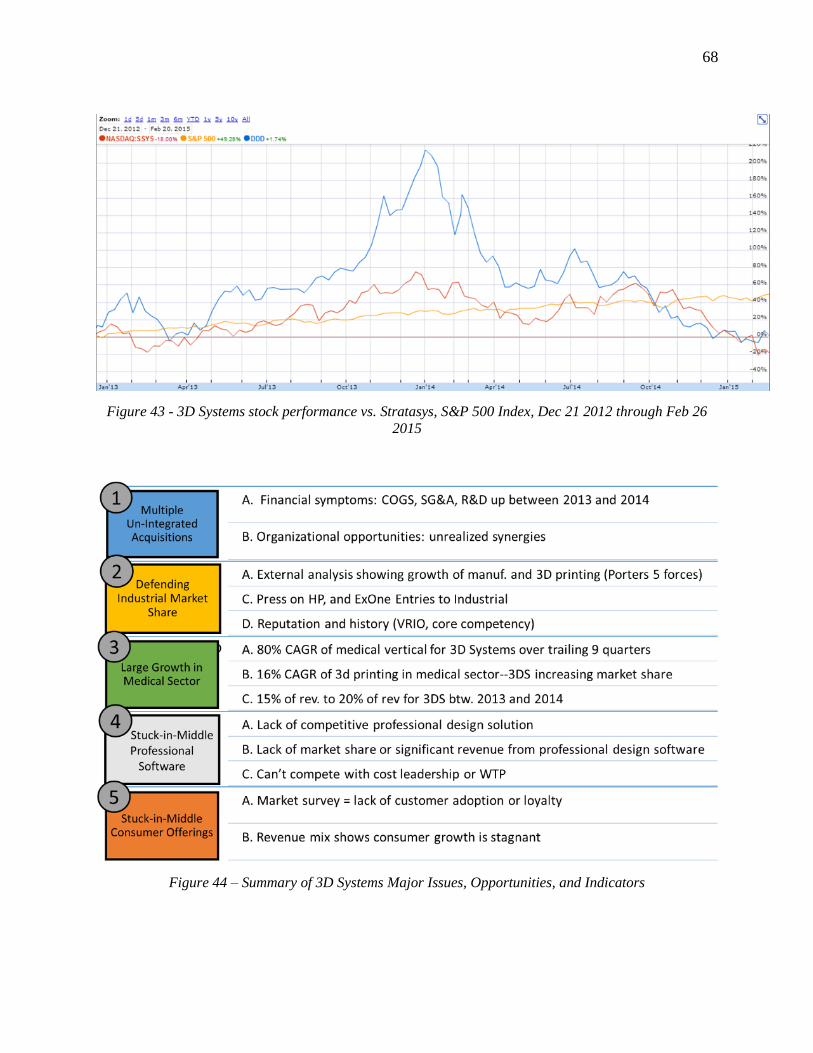

March, 2015, 3D Systems stock is still down over 70% in the past 13 months (see Figure 43).

Beyond experiencing the ups and downs of investor behavior, 3D Systems has grown well with

current vehicles in light of high levels of threat. However, they face several threats from new

entrants, shrinking margins, and higher rivalry.

13 See Figure 40 for full Financial Analysis 14

March 2011, $54MM. May 2013, $250MM. May 2014, $317MM.

33

3D Systems has been able to leverage their strengths to exploit the value chain in additive

manufacturing by forward integrating into service bureaus and capturing their profits. They have

also built an array of acquisitions and begin to formulate cohesive digital thread solutions. This

may uniquely place them to address emerging applications. However, they first must bring down

cost structure by integrating more effectively and sharing activities. They must not stray too far

from VRIO capabilities as they expand solutions. They must take advantage of innovative

business models – such as platforms and spin-offs – to reach and address the widest array of

customers and achieve their mission of truly democratizing 3D printing. This must all be

accomplished in an environment poised for growth and characterized by high levels of rivalry

and threat of entrants15. To further compel new entrants, 3D Systems will see the expiration this

year of several key patents around their SLS technology. Start-up entrants are defining the lower-

end of the desktop market as well-funded firms enter on the top end. As each disruptive

application of additive manufacturing reaches commercial viability, additional rivalry will

follow. 3D Systems faces decisions of how, where, and when to compete in each segment,

industry, and application.

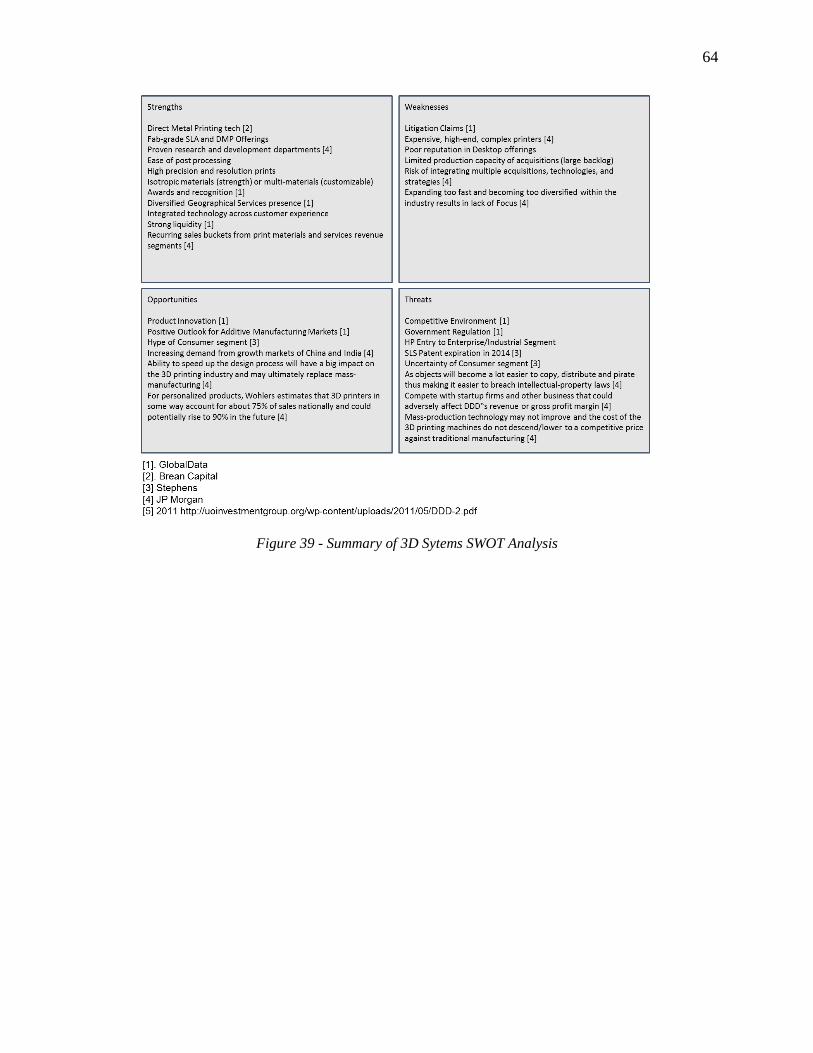

15 See Figure 39 for a summary of 3D Systems SWOT analysis

34

ISSUES AND RECOMMENDATIONS

As 3D Systems’ VRIO indicated, they are sitting in between the short-term supremacy and long

term victory. Helping them move from a temporary to sustainable competitive advantage will be

important as the market continues to grow and new entrants threaten 3D Systems market share.

There are many opportunities for improvement, growth, and innovation as evidenced by the

symptoms (see Figure 44) that are resulting from issues that were uncovered. While many

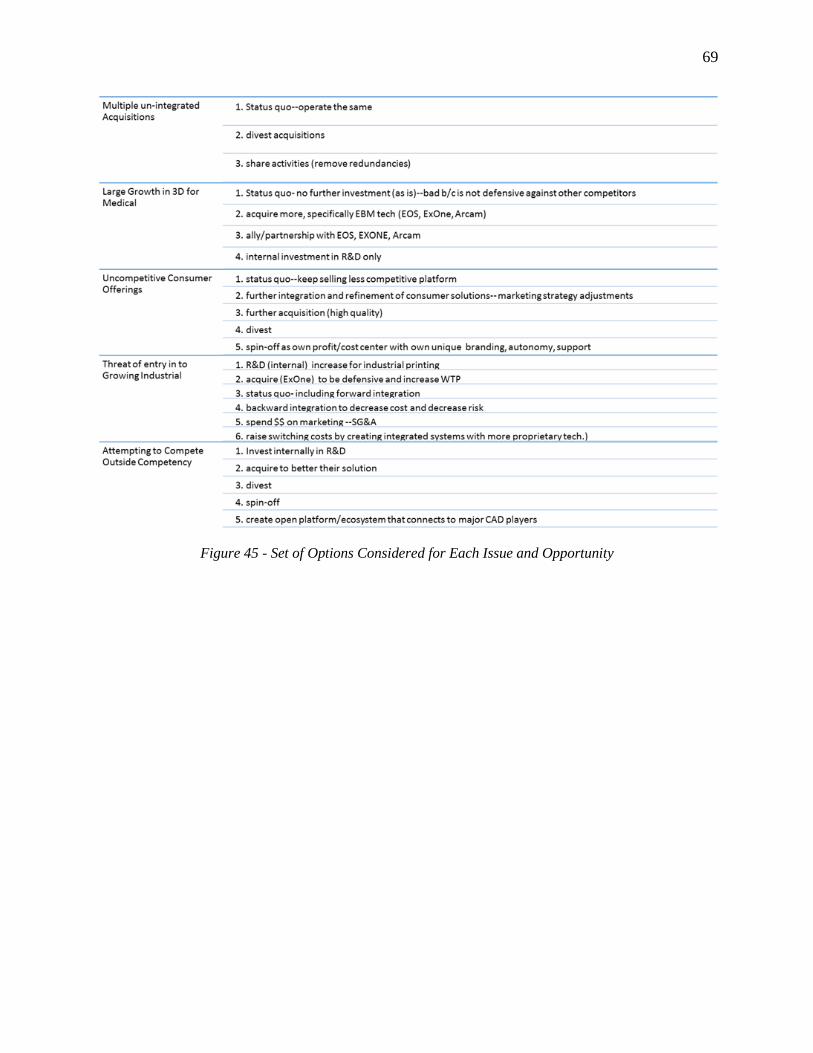

options were considered (see Figure 45) there are five critical components that will be crucial to

success:

1. Combat shrinking margins by realizing synergies of acquisition portfolio.

2. Defend industrial market share through increased research and development and sales

and marketing expenditures.

3. Acquire a leader in EBM technology to fill a gap in 3D Systems medical portfolio.

4. Create an open platform that connects professional design tools to the 3D Systems

ecosystem.

5. Spin off and rebrand the consumer solutions side of 3D Systems to focus on technology

improvement and recapture market share.

1. Reducing Costs and Growing Revenue by Integration

As mentioned above, to remain competitive in the AM industry, 3D Systems’

acquisitions have aligned with specific digital threads that can help them gain market power in

these digital threads (Barney). These integrated solutions will increase switching costs for

customers, and make it harder for rivals and potential competitors to capture 3D Systems’ market

share. Though these acquisitions have the potential to move 3D Systems into a more competitive

position, they also increased their operating expenditures, which were 44.5% of revenue in 2014,

35

up from 36.4% of revenue in 2013 (3D Systems). Most recently, COGS for 3D Systems made a

notable increase in 2014 after steady decline between 2009 and 2013. This has increased

pressure on their net income, which from 2010-2013 was 10x what it was in 201416.

With the pace of acquisitions over the past six years, 3D Systems must carefully direct

their resources and capabilities into developing or steering these subsidiaries towards their larger

strategic goals. If 3D Systems maintains status quo they will continue to make acquisitions

without full integration and realization of synergies, resulting in further profit pressures. As

illustrated in their 2014 financials, merely acting as a holding company leads to climbing

operating expenses and eroding profitability. Alternatively, 3D Systems could divest the various

acquisitions to more narrowly focus their business. This retraction; however, from segments or

industries risks suggesting poor financial health and will negatively affect their share price. With

significant sunk costs and the associated goodwill that would be lost in the divestment, short

term profitability would be damaged. The option that holds the most future value is for 3D

Systems to more fully realize cost and revenue-enhancing synergies between the core business

and their various acquisitions through aggressive integration and sharing of activities.

To continue to build a sustainable competitive advantage through increased willingness

to pay, 3D Systems must decrease their operating expenditures and cost of goods sold,

particularly in relation to their main competitor, Stratasys. Currently, their operating

expenditures as a percentage of revenue are lower than those of Stratasys, but this only creates a

temporary competitive advantage. Decreasing operating expenses by eliminating redundancies

such as human resources, legal, finance, accounting etc., 3D Systems would build upon their

economic logic by lowering their costs through scale and creating efficiencies. This would also

16 Refer to Figure 40

36

allow 3D Systems to focus their energy and resources on the core competencies of the businesses

they have acquired.

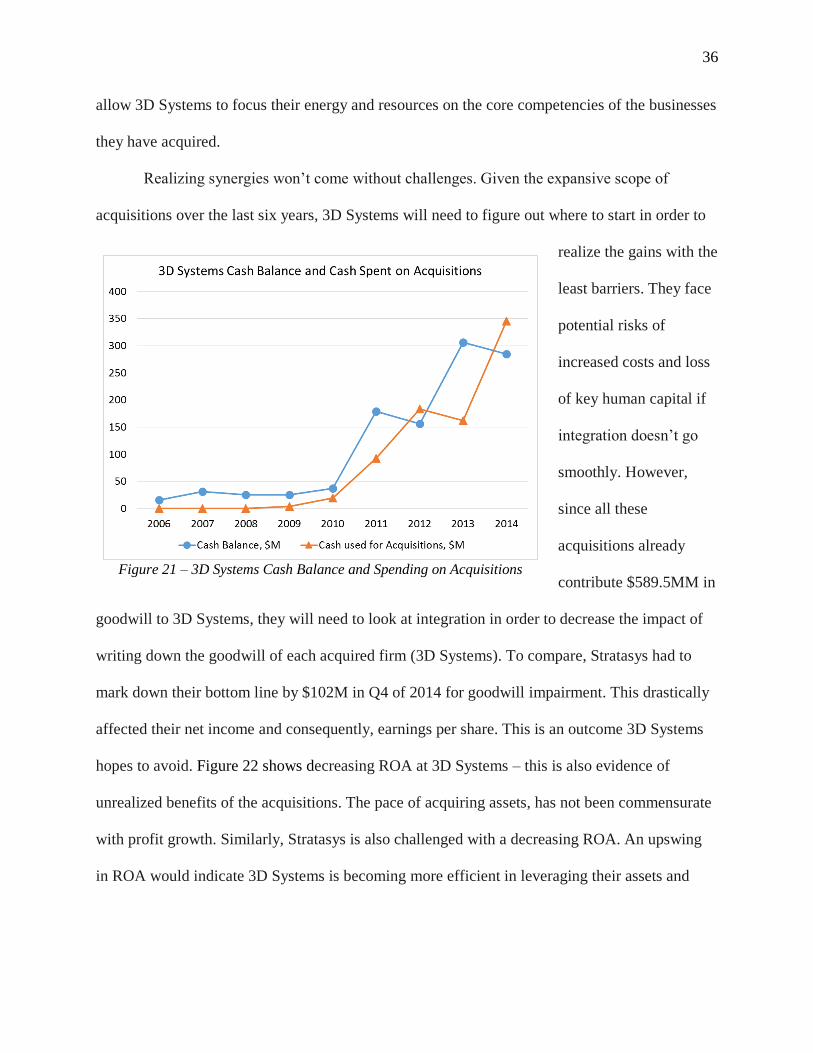

Realizing synergies won’t come without challenges. Given the expansive scope of

acquisitions over the last six years, 3D Systems will need to figure out where to start in order to

realize the gains with the

least barriers. They face

potential risks of

increased costs and loss

of key human capital if

integration doesn’t go

smoothly. However,

since all these

acquisitions already

contribute $589.5MM in

goodwill to 3D Systems, they will need to look at integration in order to decrease the impact of

writing down the goodwill of each acquired firm (3D Systems). To compare, Stratasys had to

mark down their bottom line by $102M in Q4 of 2014 for goodwill impairment. This drastically

affected their net income and consequently, earnings per share. This is an outcome 3D Systems

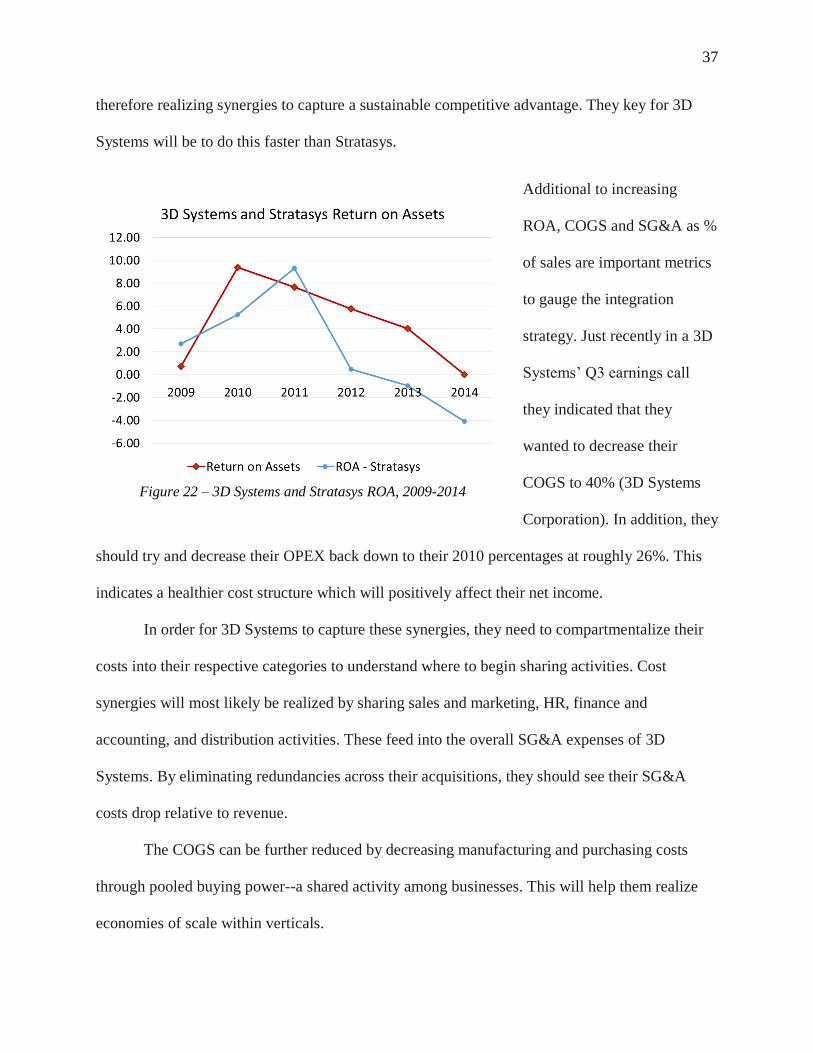

hopes to avoid. Figure 22 shows decreasing ROA at 3D Systems – this is also evidence of

unrealized benefits of the acquisitions. The pace of acquiring assets, has not been commensurate

with profit growth. Similarly, Stratasys is also challenged with a decreasing ROA. An upswing

in ROA would indicate 3D Systems is becoming more efficient in leveraging their assets and

Figure 21 – 3D Systems Cash Balance and Spending on Acquisitions

37

therefore realizing synergies to capture a sustainable competitive advantage. They key for 3D

Systems will be to do this faster than Stratasys.

Additional to increasing

ROA, COGS and SG&A as %

of sales are important metrics

to gauge the integration

strategy. Just recently in a 3D

Systems’ Q3 earnings call

they indicated that they

wanted to decrease their

COGS to 40% (3D Systems

Corporation). In addition, they

should try and decrease their OPEX back down to their 2010 percentages at roughly 26%. This

indicates a healthier cost structure which will positively affect their net income.

In order for 3D Systems to capture these synergies, they need to compartmentalize their

costs into their respective categories to understand where to begin sharing activities. Cost

synergies will most likely be realized by sharing sales and marketing, HR, finance and

accounting, and distribution activities. These feed into the overall SG&A expenses of 3D

Systems. By eliminating redundancies across their acquisitions, they should see their SG&A

costs drop relative to revenue.

The COGS can be further reduced by decreasing manufacturing and purchasing costs

through pooled buying power--a shared activity among businesses. This will help them realize

economies of scale within verticals.

Figure 22 – 3D Systems and Stratasys ROA, 2009-2014

38

Through sharing activities, 3D Systems will gain better economies of scale, which

decreases the threat of entry into the market and provides some security for 3D Systems.

Through focusing their core competencies and creating more enhanced digital threads, they can

also create higher switching costs for consumers. Given the high level of rivalry already,

increasing profitability by lowering SG&A and COGS will allow 3D Systems to respond more

effectively to price wars. 3D Systems already shows a temporary advantage over Stratasys, but