Embed Size (px)

Citation preview

3.3 Working Capital

Topic 3

Working Capital

The capital needed to pay for raw materials, day-to-day running costs and credit offered to customers.

Working Capital=Current Assets – Current Liabilities

Working Capital

Without working capital, a business will not be able to pay its immediate (or short-term) debts.

Liquidity: The ability of a firm to be able to pay its short-term debts.

Liquidation: When a firm ceases trading and its assets are sold for cash.

How much working capital is needed? Too much working capital

• Capital tied up in stock purchases, debtor (accounts receivable), and idle cash

ALL NOT GOOD because the cashcould be used for other investments.

Too little working capital• Not enough cash to pay for wages, stock purchases,

and the paying of debtsALL NOT GOOD because the businessmay need to liquidate to pay its debts even though it is profitable.

Working Capital Cycle

The period of time between spending cash on the production process and receiving cash payments from customers.

The longer the time between buying materials and receiving payment from customer the greater the working capital needs of the customer.

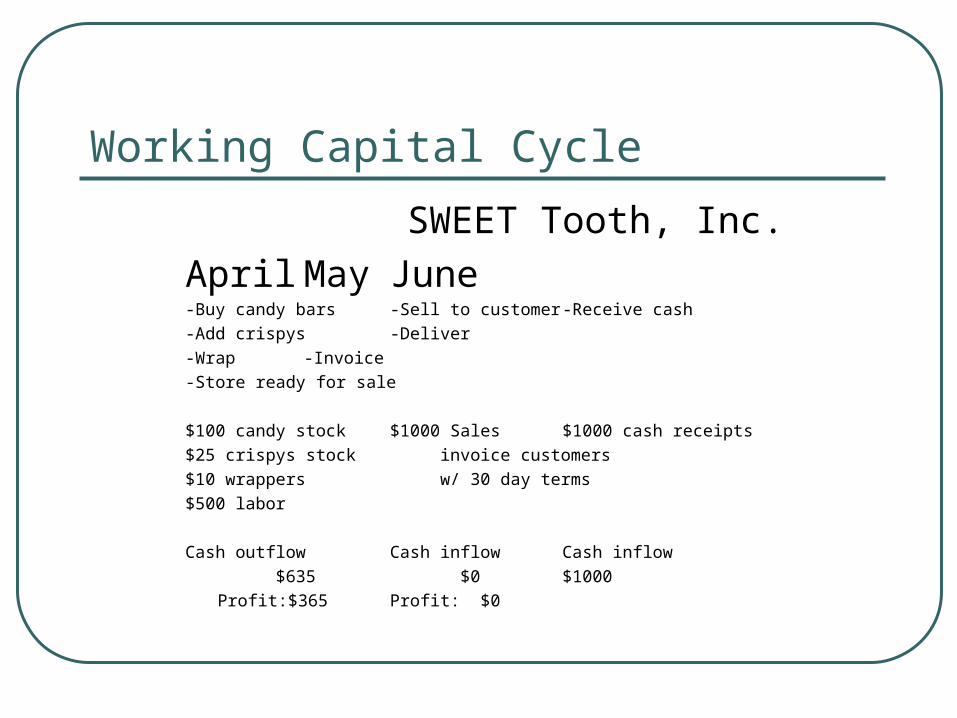

Working Capital Cycle

SWEET Tooth, Inc.

April May June-Buy candy bars -Sell to customer -Receive cash

-Add crispys -Deliver

-Wrap -Invoice

-Store ready for sale

$100 candy stock $1000 Sales $1000 cash receipts

$25 crispys stock invoice customers

$10 wrappers w/ 30 day terms

$500 labor

Cash outflow Cash inflow Cash inflow

$635 $0 $1000

Profit:$365 Profit: $0

Working Capital Cycle

Cash

Materials and

Stock Purchases

Production

Sell on Credit

Credit given to customers by business will lengthen the time before a sale is turned into cash—extending the cycle.

Credit received by the business from suppliers will reduce the length of this cycle.

To give more credit to customers than received from vendors increases the need for working capital.

To receive more credit from vendors than is given to customers reduces the need for working capital.

Cash Flow

The timing of payments to workers and suppliers and receipts from customers.

Businesses must plan this timing in order to meet its financial obligations, fund growth, and STAY in business.

Cash Flow

The sum of cash payments to a business (inflows) less the sum of cash payments made by it (outflows).

Insolvent: When a business cannot meet its short-term debts.

Why is cash flow important?

Business start-ups are offered less time to pay vendors (shorter credit periods)

Banks and lendors may not believe promises to pay because of lack of payment history and may demand payment at agreed upon times without extensions.

Finance is tight for start-ups so there is little flexibility.

Cash VS Profit

Profit: Revenue – Expenses or what is “left over”

Cash: The working capital of the business.

• Goods are purchased for resale before the sale.

• Cash is not always received at the time of sale.

• Cash “timing” does not match profit “timing”

Forecasting Cash Inflows

Capital injection into the business by owner – easy to forecast

Bank loans – easy to forecast

Customer cash purchases – difficult to forecast; depends on sales

Debtor’s payments (Accounts Receivable) – difficult to forecast; depends on sales; depends on repayment by customer

Debtor: Customers who have bought products on credit and will pay cash at an agreed upon date in the future.

Forecasting Cash Outflows

Lease/Rent payments – easy to forecast

Utilities – difficult to forecast; the vary due to external factors

Labor costs – forecast dependent on sales demand estimates

Variable costs – costs vary; usually consistent with sales demand

Structure of Cash-Flow Forecast

Section 1: Cash Inflow• Cash sales, payments for credit sales, capital

injections

Section 2: Cash Outflow• Wages, materials, rent, and other costs

Section 3: Net monthly cash flow withopening and closing

• Cash flow for period with start and ending cash balances. If a closing balance is negative, a bank overdraft will be needed (credit line access).

Vocabulary

Cash-Flow Forecast• Estimate of a firm’s future cash inflows and outflows.

Net Monthly Cash Flow• Estimated difference between monthly cash inflows

and outflows. Opening Cash Balance

• Cash held by the business at the start of the month. Closing Cash Balance

• Cash held at the end of the month becomes the next month’s opening balance.

Example

Jan Feb Mar

Cash Inflow Owner’s Capital 6000 0 0

Cash Sales 3000 4500 6500

Payments by Debtors 0 2000 2000

Total Cash In 9000 6500 8500

Cash Outflows

Rent/Lease 9000 1000 1000

Materials 500 1000 3000

Labor 1000 2000 3000

Other Costs 500 1000 500

Total Cash Out 11000 5000 7500

Net Cash Flow Net Monthly Cash Flow (2000) 1500 1000

Opening Balance 0 (2000) (500)

Closing Balance (2000) (500) 500

Benefits of Cash Flow Forecasts

Negative periods of cash flow can be planned for handling with financing with bank or cash injections from owners.

Negative cash flows can be reduced by eliminating purchases or by reducing sales on credit.

Cash flow statements are required for new businesses by investors and bankers – with reasoning for the projections.

Causes of Cash Flow Problems

Poor Credit Control• Businesses must manage their collection from

debt extended to customers (Accounts Receivable).

Allowing Customers too much Credit• In order to be competitive, extending

generous payment terms to customers reduces short-term cash flows.

Causes of Cash Flow Problems

Expanding Too Rapidly• Expansion requires additional labor and

materials which can cause cash shortages even though the company is profitable.

Unexpected Events• Unforeseen costs, equipment repairs, dip in

sales, competitors lower prices can negatively impact cash flow.

How to Improve Cash Flow

Increase Cash Flow Reduce Cash Outflows

CAREFULDo not harm Sales or Profits

How to Increase Cash FlowMethod How it Works Evaluation

Overdraft (Credit Line)

Flexible loans in which businesses can draw at any time.

Interest rates can be highCan be rescinded by the bank

Short-Term Loan A fixed amount can be borrowed at any time.

Interest must be paidThe loan must be repaid

Sale of Assets Cash can be raised by selling redundant assets.

Selling assets quickly can result in a low sales priceThe assets might be needed laterThe assets could be used as collateral for future loans

Sale and Leaseback Assets can be sold and leased back at a reduced price.

Leasing costs add to overheadCould be loss of profit on sale of assetThe asses could be used as collateral for future loans

Reduce Credit terms to customers

Cash flow can be brought forward from reducing terms from 60 days to 30 days.

Customers may change to different firm for their purchases

Debt Factoring Sell Accounts Receivable to raise cash.

The debt purchases company will not pay full value for the A/RCustomer may perceive the company is in financial trouble

How to Reduce Cash Flow

Method How it Works Evaluation

Delay payments to suppliers (creditors)

Cash outlays will fall in short term if bills are paid in 2 months instead of 1 month

Suppliers may reduce discounts offeredSuppliers may demand cash on delivery or refuse to supply if they feel the risk of not being paid is too high

Delay spending on capital equipment

By not buying equipment cash will not have to be paid

Business may become inefficient if outdated equipment is not replacedExpansion becomes difficult

Use leasing not outright purchase of equipment

No large cash outlay is required

The asset is not owned by the businessLeasing charges are added to overhead

Cut overhead spending that does not affect output – like advertising

Costs will not reduce production capacity or sales but cash payments will be reduced

Future demand may be reduced by failing to promote your product effectively.